Abstract

A central concern of media scholars has been the discursive and economic power of a small number of transnational media corporations (TNMCs). In this paper, we advance research on TNMC power through a novel empirical analysis of their global-spatial organization, reflected in their corporate global office networks. Our findings reveal both global and regional corporate strategies and, further, demonstrate how US new media firms are expanding into Chinese global media cities to penetrate this emerging media market. Our analyses provide a crucial macro-level overview of the structural power of TNMCs to consolidate control over the global network of media.

Keywords

Introduction

Over a period of some four decades, one of the central concerns of media and communication scholars has been to uncover the diverse ways in which media corporations exercise power within their respective domains. Indeed, the need to pay constant attention to power relations has come to be considered as ‘one of the seemingly commonplace assumptions of critical media studies’ (Birkinbine et al., 2017: 477). One longstanding area of concern has been how communications technologies and media corporations have been integral to the expansion of economic and political power, bringing with it uneven geographies of cultural and economic imperialism. Research focussed specifically on the spatialization of media has addressed the geographical and institutional extension of media organizations, specifically with regard to the ‘institutional extension of corporate power in the communication industry’ (Mosco, 2009: 158). This line of research can be traced back to the work of Schiller (1969, 1976, 1989) on the penetration and expansion of transnational corporate products and practices across the world. In Communication and Cultural Domination (Schiller, 1976: 7), Schiller (1989) describes how ‘these aggressive business empires organize the world market as best they can, subject of course, to the uneven and partial constraints of national regulation, often minimal and differential levels of economic development in the areas they are active’. Just over a decade later, in Culture Inc., Schiller (1989) described how ‘the power and influence of giant, private corporations, directed towards obtaining information capabilities at the lowest possible costs’ (p. 114) had entered and weakened national communication systems and as such was creating ‘a near-total corporate informational cultural environment’ (p. 123). More recently, Thussu’s (2006, 2007) work on the global flow and contra-flow of media has sought to map media flows focussing both on the ‘dominant flows’ of mainstream commercial commodities largely emanating from the corporations of the Global North, and also the contra-flows arising from the peripheries of global media industries. With regard to the former, Thussu (2007) notes how the ‘shift from a state-centric and national view of media to one defined by consumer interest and transnational markets has been a key factor in the expansion and acceleration of media flows’ (p. 11), with US-led Western media developing global reach and influence. Media flows, Thussu notes, have a close relationship with economic power, with US media products continuing to define ‘the global’. Yet, Thussu suggests that we may also begin to see a shift towards ‘a new cartography’ of global communication as the media and communication industries in countries such as China and India become increasingly integrated into the global market. Similarly concerned with media flows and corporate power, in Communication Power (2009), Castells (2009) argues that globalization, digitization, networking and deregulation have radically altered media operations such that they have ‘removed most of the limits to corporate media expansion, allowing for the consolidation of oligopolistic control by a few companies over much of the core of the global network of media’ (p. 72). Mosco (2009: 161) argues that transnational media firms ‘are increasingly able to use the genuine multinational dimensions of their product, marketing, labor, and financing to transcend the legal, regulatory, cultural, and financial constraints of their home base’.

In this paper, we seek to make our own original contribution to the literature concerned with the spatialization of media and the nexus of transnational media corporation (TNMC) power, space and territory, flows and networks, as represented by the work of Schiller, Thussu, Castells and others, through an empirical analysis of the global-spatial organization of TNMCs across a select set of ‘global media cities’ (Krätke, 2003; Krätke and Taylor, 2004; Hoyler and Watson, 2013). As Mosco (2009) notes, much of the research on corporate power in the media industries has focussed on how corporate concentration, in both its horizontal and vertical forms, has increased the structural power of a small set of oligopolistic corporations, where power is understood as the ability to ‘exert the greatest degree of ownership and control over the means of producing, distributing, marketing and exhibiting media products’ (Mirrlees, 2013: 87). Yet, as Mosco argues, corporate restructuring also changes the spatial patterning of business activity, producing a ‘remapping of corporate space’ in such a way as to create another form of business concentration, centred on agglomerations of business activity in leading urban centres. As such, the geographical extent of a corporation’s operations represents another facet of structural power (Mirrlees, 2013). In this regard, one way in which firms seek to extend their corporate power across space is through a transnationalization strategy and the development of a transnational office network. Such networks are necessary for managing and enabling the ‘material coordination of flows of information, communication and culture’ (Birkinbine et al., 2017: 478), or put another way, a corporation’s office network forms a crucial part of its ‘structural capacity’ (Fitzgerald, 2012) to exert ownership and control over the means of producing, distributing, marketing and exhibiting media products worldwide (Mirrlees, 2013).

Beginning from the above premise, in this paper, we provide an empirical analysis of the office networks and transnational locational strategies of leading media corporations and their integration into the world city network. This allows us to understand the ‘backbone’ (Castells, 2009: 73) of the global media network, as constructed through the locational strategies of leading TNMCs, through which they both exert corporate power over the means of producing, distributing, marketing and exhibiting media products worldwide and at the same time connect local and national media firms across the globe into global media networks. Uncovering the networks that allow for the coordination of flows of information and communication across space, our results provide a crucial ‘top-level’ overview of the structural capacity of the largest TNMCs to exert their substantial economic power across geographical space (Derudder and Taylor, 2020).

Media power and the transnational geographies of media corporations

The story of media corporations over the last few decades has been one of mergers, acquisitions and strategic partnerships, giving rise to a small number of very large media corporations with oligopolistic control over much of the world’s media (Castells, 2009; Held et al., 1999; Noam, 2016; Warf, 2007). The economic power of these media corporations, and the tendency towards concentration of media ownership (Flew, 2018), has allowed them to take on a hegemonic role in the production, circulation and consumption of media content globally. Mirrlees (2013: 76) argues that the ‘end game’ of market competition in the global media industries is ‘control of audiences, intellectual property, and the means of media production, distribution, and exhibition by a few firms’. Indeed, we recently witnessed a wave of mergers and acquisitions that has made the largest firms even larger: for example, the AT&T acquisition of Time Warner in June 2018, the merger of Walt Disney and 21st Century Fox in July 2018, and the acquisition of Sky by Comcast in October 2018 (Birkinbine and Gómez, 2020). As Gershon (2020) notes, what distinguishes transnational media corporations (TNMCs) from other types of transnational corporations is that the principal commodity being sold is information and entertainment, with the TNMC being the most powerful economic force for global media activity. Globalization, deregulation and digitization have removed many of the limits to corporate media expansion, leading to the rapid growth of the global commercial media market (Castells, 2009; Warf, 2007). At the same time, concerns have arisen that corporate size limits the availability of media products and ideas, whilst also promoting particular corporate agendas (McChesney, 2008).

The convergence of media and the digitalization of content has led to horizontal expansion of interests across a variety of media, information and telecommunications sectors (Flew, 2018), while at the same time leading to vertical integration within corporations to enhance the ability to produce and distribute cultural products widely across a variety of platforms (Arsenault and Castells, 2008; Mirrlees, 2013). Moreover, the rapid emergence of digital media technology has fundamentally changed the media industries. Gershon (2020) points to three business and technology shifts in particular. First, internet and broadband delivery has resulted in new business models that maximize the potential for instantaneous and on-demand communication to a global customer base. Second, digital media has allowed for entirely new forms of creativity and communication expression. Third, and most importantly in the context of this article, is the change in the TNMC players themselves. New media firms from the United States such as Apple, Alphabet (Google, YouTube), Amazon, Facebook and Netflix, which blend technology and media, have become not only some of the world’s largest TNMCs, but are now some of the largest corporations globally (Apple, Alphabet and Amazon rank 11, 13 and 37 by total revenue in the Fortune Global 500 in 2019, https://fortune.com/global500/). In recent years, these have been joined by the Chinese internet technology companies Baidu, Alibaba and Tencent (the latter two rank 182 and 237 in the Fortune Global 500). These ‘platform corporations’ are integrated into transnational networks of finance and capital (Negus, 2019) and ‘aim to move across conventional industry boundaries, having a promiscuous relationship to the traditional content providers and distribution channels’ (Flew, 2018: 23).

Accompanying the growth and concentration of TNMCs and their oligopolistic control over the global commercial media market have been longstanding concerns regarding the power of these corporations. While the notion of media power is recognized as being complex and multifaceted, it has been predominantly conceptualized in two distinct ways: structural power and relational power (Castells, 2009; Corner, 2011; Freedman, 2014; Flew, 2018; Mirrlees, 2013). First, structural power, or ‘power to’, is generally understood to relate to the positions of the organizations which control most of the resources that are the basis for them to exercise power. Applied to media corporations, for Mirrlees (2013: 87), a structural approach to power recognizes that the most ‘powerful’ TNMCs are ‘those that own or control the majority of the material and symbolic resources required to produce, distribute, market and exhibit media products in many countries around the world’. Mirrlees suggests that these resources include material resources, such as capitalization and revenue, production and distribution subsidiaries, intellectual property library, and, importantly for this paper, the geographical extent of its operations; and symbolic resources, including the public perception of the business and its products, brand prestige in various markets and the knowledge and skills of its workforce. Second, relational power, or ‘power over’, is conceptualized as existing in the relationships between two or more entities, where relational capacity enables one social actor to influence asymmetrically the decision of other social actors, to favour the empowered actor’s interests (Castells, 2009). In terms of global media corporations, such a perspective recognizes that structural power exists, but adds the dimension of ‘power relations between a media corporation and other actors, the goals of a media corporation and the strategies it employs to achieve them’ (Mirrlees, 2013: 89). These two forms of power are not mutually exclusive, but rather a media corporation’s control of material and symbolic resources—that is its structural power—shapes its capacity to coerce and persuade others—that is its relational power (Mirrlees, 2013). Thus, while academic concern regarding media power has focussed predominantly on the discursive and cultural components of media power from a relational or ‘power over’ perspective (e.g. the relations between media, politics, democracy and civil society), media power must be understood as both a cultural and an economic phenomenon (Couldry, 2000). For Freedman (2014: 146), media power refers to ‘more than the cultural processes by which established patterns of media power come to be accepted’, but also ‘the material relations that underlie this inequality and which then structure the complex operations of media as power holders in their own right’. Put more succinctly, media power is ‘also about owning, censoring, regulating, controlling, decision making and profiting’ (Freedman, 2014: 15). As Flew (2018) argues, TNMCs are not only institutional sites through which cultural or symbolic power may be exerted, but also major corporations that invest in resources, employ people and produce goods and services, and therefore exert significant economic power. Thus, a structural perspective on power offers important insights into the capacity of TNMCs in this regard.

As Mirrlees (2013) emphasises, ultimately, the goal of all media corporations is profit maximization, and in order to generate profits, corporations ‘bring money, technology, media and hundreds (if not thousands) of people together in productive social relations’ (p. 60). While TNMCs operate under one single corporate identity, the realities of contemporary media production are highly complex, involving production companies, financiers, distributors, marketers and exhibitors (Mirrlees, 2013: 60), some of whom will be internal to the corporation, and others external, but which nevertheless require managing and coordinating. Furthermore, increasingly, productions are cross-border in nature as media producers look to meet specific creative, technical and market-specific objectives; take advantage of expert skills; access locally embedded resources; tap into existing local inter-organizational networks; and manage resource interdependencies across project partners (Morawetz et al., 2007; Sydow et al., 2010; Hoyler and Watson, 2019). The resulting labour structure of these cross-border productions has been termed the ‘New International Division of Cultural Labour’ (NICL; Miller et al., 2001), which Artz (2016) describes as acting to structurally consolidate and creatively coordinate local and global media production. Within this NICL, TNMCs take on a coordinating and financing role such that they become ‘financial flagships, coordinating and controlling organizationally and territorially decentralized entertainment production networks’ (Mirrlees, 2013: 150). Accordingly, as Castells (2009) argues, the major organizational transformation we are witnessing in global media is ‘the formation of global networks of interlocked businesses organized around strategic partnerships’ in which the dominance of the small number of oligopolistic media corporations is ‘predicated on their ability to leverage and connect to locally and nationally focussed media organizations everywhere’ (p. 72). For Castells, the terrain on which power relationships operate has become primarily organized around networks and is constructed between the local and the global.

Given the above, the geographical extent of a corporation’s operations represents an important facet of structural power. The geographical reach of a media corporation may be seen as developing in several stages. Gershon (2020) suggests that as a company’s exports steadily increase, offices in foreign territories are set up to handle the sales and services of its products, usually as flexible and reasonably independent entities. Subsequently, the office may become involved in other facets of international business such as media production and licencing abroad, with managerial, financial and technical expertise subsequently transferred to these offices. Finally, as pressures arise from the various international operations, there arises the need for a comprehensive global strategy (Gershon, 2020). International operations need significant coordination, and in this regard, we see the development of a transnational corporate office network as a crucial part of the structural power, or ‘structural capacity’ (Fitzgerald, 2012), of the corporation to control and coordinate production, distribution, marketing and exhibition of their media products across multiple territorial media markets, and as being necessary for managing and coordinating the ‘material coordination of flows of information, communication and culture’ (Birkinbine et al., 2017: 478) across the various functions and locations of the corporation. As Mosco (2009: 161) notes, ‘rapid and efficient communication systems are essential for a company to manage the multiplicity of exchanges that flow within an integrated, multidivisional corporation whose success depends on timely assessments of relative performance’.

This corporate restructuring and resulting remapping of corporate space is significantly changing the spatial patterning of business activity in the media industries (Mosco, 2009). But further, it is doing so in such a way as to create another form of business concentration, centred on agglomerations of business activity in leading urban centres (Mosco, 2009). A noted geographical feature of the media industries has been the heavy concentration of production activities within a limited number of large creative media clusters (Davis et al., 2009; Karlsson and Picard, 2011). Curtin (2003, 2009, 2010) has described these agglomerations as ‘media capitals’, referring both to the production capacity of a location and to broader networks of financing, distribution, exhibition and advertising. Corporate expansion via offices in these cities can be related to broader capitalist logics of accumulation (Harvey, 2001). First and perhaps foremost is the ‘extension of markets’, involving entering a foreign market and serving it from that location. For Karlsson and Picard (2011), the strategies pursued by TNMCs focussing upon opening up new markets necessitates a presence in the large cities that are global media centres, allowing them to access the latest trends and developments in the general culture industry as well as the latest technological developments. Second, there is the matter of the efficiencies gained though the ‘concentration of productive resources’. These clusters are both the location of reservoirs of specialized labour, and many media firms and associated services, providing a milieu of potential local specialist collaborators for firms as part of flexible project production forms, acting to make production of entertainment and content more efficient (Karlsson and Picard, 2011). Furthermore, as Curtin (2009) notes, most subcontracted tasks will go to local firms because it is easier to oversee their work.

Importantly in relation to this paper, media capital is also a term which seeks to recognize the ways in which they now serve less as centres for national media production, and more as ‘central nodes in the transnational flow of culture, talent, and resources’ (Curtin, 2009: 111). These multiple networks stretch beyond individual clusters to ‘link media cities to other cities across the globe in a complex pattern of connections and flows’ (Hoyler and Watson, 2013: 106). External linkages of firms are not restricted to the local milieu; due to competition becoming more global and the need to serve global markets, many of the largest media firms have extended the geographical scale of their external connections (Karlsson and Picard, 2011; Nachum and Keeble, 2003), linking together media production centres across the world through their corporate networks. Thus, Krätke (2003; Krätke and Taylor, 2004) has described these media centres as ‘global media cities’, noting how transnational media corporations form ‘a global network of branch offices and subsidiary firms, by means of which the urban centres of cultural production are linked with each other world-wide’ (Krätke, 2003: 624). As large media corporations have increasingly expanded their operations across a wide range of geographical locations, in recent years, centres of media production have become more dispersed (Flew, 2018), and previously peripheral cities have developed media production capacity (see, e.g. Keane, 2006, on East Asia), resulting in both greater connectivity between centres of production and rise in the number of production centres.

Given the above discussion, the premise that we develop in this paper is that a firm’s global locational strategy, and subsequently the development of an international office network spanning key global media cities, is a key expression of a firm’s ability to exert power through the ownership and control over the means of production, distribution and exhibition of media products across multiple territories (Mirrlees, 2013). As Sassen (1991) argues, ‘centralised control and management over a geographically dispersed array of plants, offices, and service outlets cannot be taken for granted or seen as an inevitable outcome of a “world system.” The possibility of such centralized control needs to be produced’ (p. 325). Thus, if as Curtin (2003: 205) describes, ‘media capitals are places where things come together and, consequently, where the generation and circulation of new mass culture forms become possible’, then we would argue that it is through the global networks of the TNMCs, anchored in global media cities across the globe, that we see the realization of this generation and circulation.

Methodology

As Birkinbine et al. (2017: 4) state, researchers have relied on a variety of methods to try to ‘get a sense of how media companies are structured and how they behave’. Yet, they also argue that researchers are yet to provide ‘a systematic global overview of the most powerful media corporations’ (Birkinbine et al., 2017: 5). Along similar lines, Freedman (2014) suggests there is an argument to emphasize macro-level analysis in order to get to grips with the underlying dynamics of media power. It is such a systematic macro-level global overview that we seek to provide in this article, focussed specifically on the global office networks of TNMCs and their specific locational strategies. To do so, we build methodologically and conceptually on two decades of world city research undertaken by the Globalization and World Cities (GaWC) research network, an international group of scholars concerned with the role of cities in economic globalization. The central tenet of GaWC research is that the office networks of global service providers, and other transnational firms with worldwide reach such as TNMCs, can serve as a proxy for the physical and virtual links between city economies across space (Taylor and Derudder, 2016) necessary for centralized control and management over a geographically dispersed array of assets.

This premise provides the underlying basis for two methodological approaches that respectively allow us to examine the ‘material coordination of flows of information, communication and culture’ (Birkinbine et al., 2017: 478) across transnational office networks of TNMCs, and the shared and contrasting locational strategies in terms of the location of offices between various types of TNMCs. The first methodology we employ is the use of the interlocking network model (ILNM) for world cities, developed to measure intercity relations from data on intra-firm office locations (Taylor, 2001). As with all network models, the ILNM consists of nodes (in this case, cities) and the links between them, or ‘edges’ (in this case, the assumed flow of knowledge, goods and people between these cities). However, the ILNM for world cities is unusual in that it also has an additional sub-nodal level, which is comprised of the firms located within the cities/nodes, in our case TNMCs, and it is the working flows between the offices of these firms – of information and people – that constitute the ‘world city network’ (Taylor and Derudder, 2016). As such, the main measure of importance in the ILNM is ‘network connectivity’, which quantifies the extent and intensity of links between corporate offices, and by proxy between the cities in which they are based. The results of this modelling, that is a measure of how connected cities are to other cities through the transnational office networks of TNMCs, allow us to determine which cities are the central locations from which TNMCs are controlling and managing their transnational corporate networks across geographical space. These cities represent the key locations through which the structural power of TNMCs is being realized, that is to say the key locations in which ownership and control over the production, distribution, marketing and exhibition of media products is being concentrated.

Furthermore, through comparison with a similar analysis undertaken in 2011, we can make a longitudinal assessment of network connectivity. The second approach we employ is a principal component analysis (PCA), a method of data reduction which converts large data matrices (in our case, containing information on the office locations of selected TNMCs) into smaller matrices by combining similar variables. This allows us not only to identify the locational strategies of individual TNMCs, but also to identify common patterns with regard to the way in which TNMCs use particular cities. With the geographical extent of a corporation’s operations representing a facet of structural power (Mirrlees, 2013), the results of the PCA allow us to explore the transnational geographies of TNCMs. Further information on these methods is provided in subsequent sections.

Data collection

The data on the office networks of TNMCs used in this study were collected in the summer of 2018, as part of the latest round of a larger longitudinal data collection exercise focussing on locational strategies of advanced producer services (APS) and TNMCs. This has been undertaken regularly since 2000 by GaWC researchers providing the only longitudinal dataset of its kind. Here, we define a TNMC as ‘a nationally headquartered company that has a diverse range of business operations (assets, sales, employment and affiliates) in many different countries’ (Mirrlees, 2013: 91), and as one that ‘maintains facilities in more than one country and plans its operations and investments in a multi-country perspective’ (Herman and McChesney, 1997: 13). The starting point for the selection of firms was a list of the top 50 international media corporations (based on revenues) produced and updated by the Institute of Media and Communication Policy (https://www.mediadb.eu/en.html, consulted 25 October 2018 1 ). The research team sought to collect locational information on their global office networks via corporate websites. For reasons of consistency across sectors in the overall data gathering, the number of TNMCs for which this data was sought was restricted to 25. There is a strong US representation within these firms, with a total of 16 of the 25 being headquartered in the US. Four were European, two Canadian, two Chinese and one Japanese. For each firm, information was gathered on the location and importance of headquarters and branch offices in 709 cities worldwide. Cities were selected based on a number of overlapping criteria, including size (population), political status (capital cities), presence of (regional) headquarter functions in APS firms and TNMCs and previous research. Our overall approach has been to be as inclusive as possible, ensuring that there were no potential omissions as we recorded information. Firm locations in the wider functional area of a city were allocated to the core city. The available information for each firm’s office location was standardized to categorize its importance in a firm’s organizational network. This ‘media value’, mvij, gauges the importance of the presence of firm j located in city i and was coded from 0 (no office in the city) to 5 (headquarters), with a ‘typical’ office of a firm scoring 2 (1 for a minor office, 3 for a particularly large office, 4 for significant additional functions like a regional headquarters). This gives heaviest weighting to the corporate headquarters, which forms the focal management and strategic centre of the firm at the global level (Adler and Florida, 2020), next to those offices performing these functions at the regional level, and so on. The result is a matrix of 25 firms × 709 cities with 17,725 media values. This media value matrix was used as the input for a three-fold analysis, consisting of: (1) an analysis of connectivity between global media cities in 2018; (2) an analysis of the change in this connectivity between 2011 and 2018 by comparing results with those of earlier research along similar lines; and (3) a principal component analysis (PCA) to uncover the spatial configuration of global media networks in 2018. These are detailed in the following section.

Calculating global network connectivity

To calculate measures of network connectivity, the 25 firms × 709 cities matrix first needs to be transformed into a 709 cities × 709 cities matrix. In network analysis, this transformation is called a bipartite projection (Liu and Derudder, 2012): a transformation that allows devising measures of connectivity based on a set of assumptions about how the so-called ‘co-behaviour’ of agents (in this case the presence of a media firm in multiple cities through its offices) is reflected in ‘flows’ between those agents (in this case flows between offices located in different cities). Different bipartite projections have been devised and applied in the world city network literature (Neal, 2014), but here we draw on the model that has been most commonly applied: the interlocking network model (ILNM), first specified in Taylor (2001). The numerical specification of the ILNM is based on the calculation of city-dyad connectivity, CDCa-b,j, between a pair of cities a and b for media firm j:

The value of CDCa-b,j is not an actual measure of intercity connectivity, but a proxy for the potential level of flows based on the assumption that (1) a shared presence of a media firm in a pair of cities a and b opens up the potential for intercity interaction (electronic messages, telephone conferences, face-to-face meeting through business travel), while (2) the level of potential interaction depends on the importance, size and operational capabilities associated with the media firm’s presence in those cities. For example, the CDCa-b,j between a city with a global headquarters (5) and a city with a regional headquarters (4) equals 20; the CDCa-b,j between a city with a large office (3) and a city with a minor office (1) equals 3; the CDCa-b,j between a city with a typical office (2) and a city with no office (0) equals 0. Aggregating a city’s city-dyad connectivities CDCa-b,j with all other 708 cities for each of the 25 firms then produces a measure of its overall network connectivity NCa:

To make NCa independent of the number of firms and cities in the data, these measures are commonly reported as a percentage of the most connected city (in our case, New York).

Calculating changes in connectivity, 2011–2018

To put the interpretation of our NC results in a broader longitudinal context, we compare them with results of an earlier analysis of 2011 data using the same methodological approach (Hoyler and Watson, 2013). This time frame allows us to gain insights into the unfolding of transnational media networks after the global financial crisis of 2007–2008 and before the impact of the COVID-19 pandemic. Rather than exploring shifting ranks or absolute changes in NC, we marshal a methodology – first put forward in (Derudder and Taylor, 2016) – that standardizes connectivity change. This has a number of distinct interpretative advantages, for example it also allows exploring how the most connected city, in both years, New York, fares when compared to the rest of the cities.

To this end, we first compute standardized network connectivities NC for both 2011 and 2018 as z-scores. For both cross-sections, this produces an open number sequence pivoting on zero (average connectivity) with individual cities’ connectivities expressed as standard deviations from the average. Cities’ connectivity change is then calculated by subtracting the 2011 value from the 2018 value, after which the obtained values are again standardized into z-scores. This produces readily interpretable, standardized measures of connectivity change in that the distribution conforms to a standard normal distribution: its average is 0, its standard deviation equals 1, while statistical testing shows that this distribution can indeed be considered to be a normal distribution. The advantage here is that this measure of change can be interpreted as a z-score: cities with an absolute value of ⩾2 have witnessed exceptional connectivity change, and cities with a value close to 0 have seen a connectivity change in line with the change in the distribution at large. In addition, it also allows assessing how New York has fared compared to all other cities.

Principal component analysis

In addition to calculating network connectivities, we apply PCA to uncover common patterns of variation in the data. PCA reduces large data matrices by combining similar variables (in our case, the location strategies of 25 individual firms) into smaller interpretable components. In order to maximize all variances accounted for in the data, results were rotated using varimax rotation. This technique maximizes the sum of the variances of the squared loadings, simplifying the interpretation of the findings by associating each variable to at most one factor. Following the exploratory approach to world city network analysis employed by Taylor et al. (2002), a number of different principal component analyses were performed on the data, each with a differing number of components in the solution. The importance of each individual analysis to understanding the data was considered, with reference both to the composition of the components and to the amount of variability accounted for by each component. The results reveal common patterns in how TNMCs use cities, or put another way, show groups of firms with similar locational strategies with regard to their transnational office networks. This solution accounts for 46 per cent of the original variation of the data in the matrix: 20.7 per cent, 17.4 per cent and 7.9 per cent for the three components, respectively. Adding more components to the solution resulted in diminishing returns in the amount of variance accounted for and gave geographically narrow components relating to the spatial strategies of individual firms.

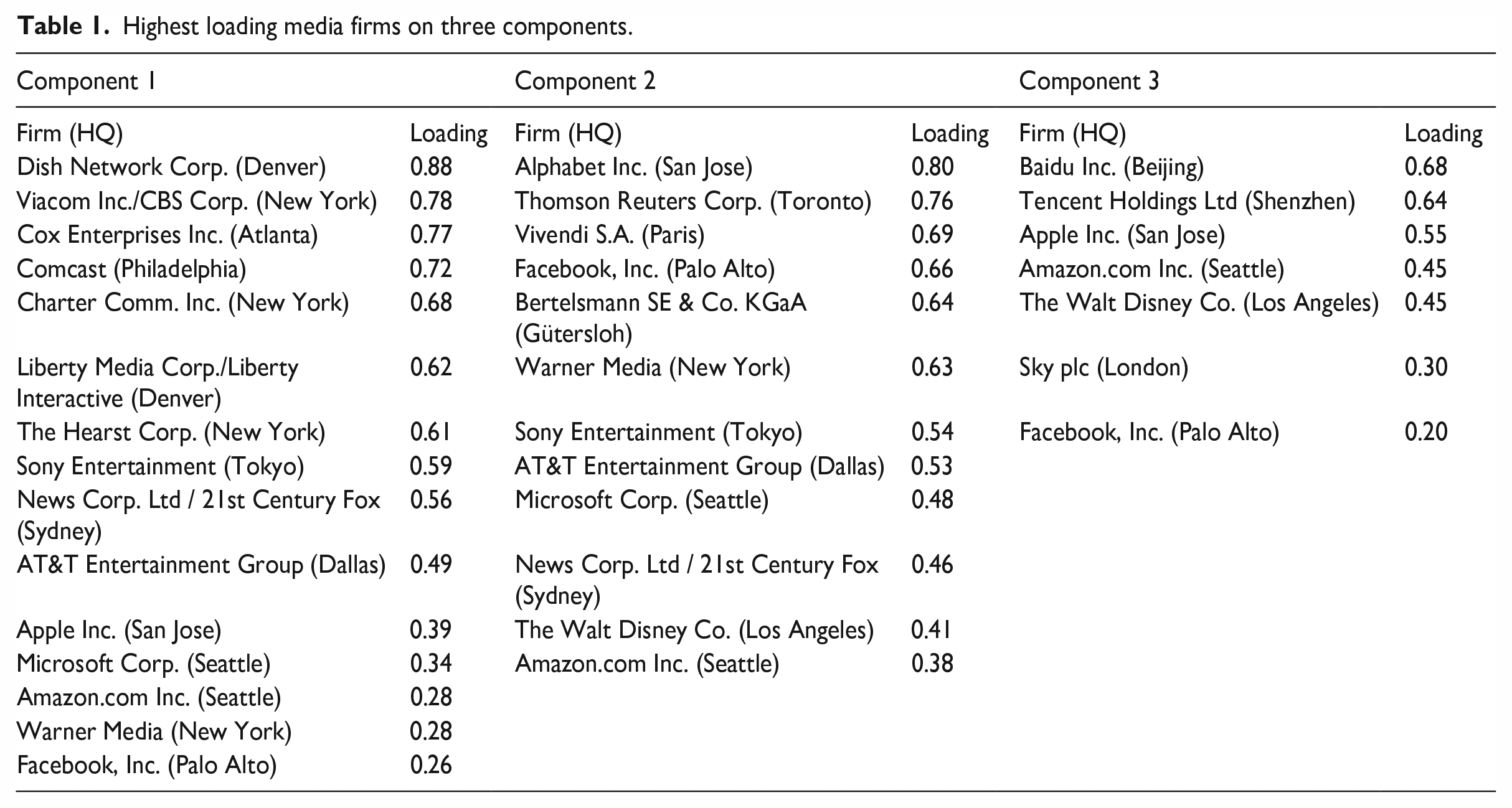

The analysis provides us with two specific results. The first are the component loadings for the media firms. With each component representing a shared spatial strategy amongst the firms in that component, these scores allow us to determine which types of firms are engaging in which types of spatial strategies, and how significantly. Table 1 shows the highest loadings for the media firms on each of the three components in the solution. Firms with larger loadings (higher correlations) are those with a more important role in producing the patterns reported in the analysis. The second result are component scores for the cities in the matrix. It is these scores that allow us to gain insight into the spatial configuration of the networks created between global media cities by TNMCs. Scores for a given city indicate that city’s significance with regard to articulating media services across the world. For ease of interpretation, we have allocated cities to a series of categories based on their component scores. Super-articulator cities represent those cities that achieve very high component scores above 5.0. Articulator cities represent cities with high component scores between 4.0 and 4.9. Primary field cities are cities scoring between 3.0 and 3.9, while sub-primary field cities score between 2.0 and 2.9. Cities scoring between 1.0 and 1.9 are allocated to the category of secondary field cities. In the subsequent discussion, the names given to components reflect the dominant geographical patterns that emerge from the component scores.

Highest loading media firms on three components.

Findings

Global media cities and their shifting network connectivities

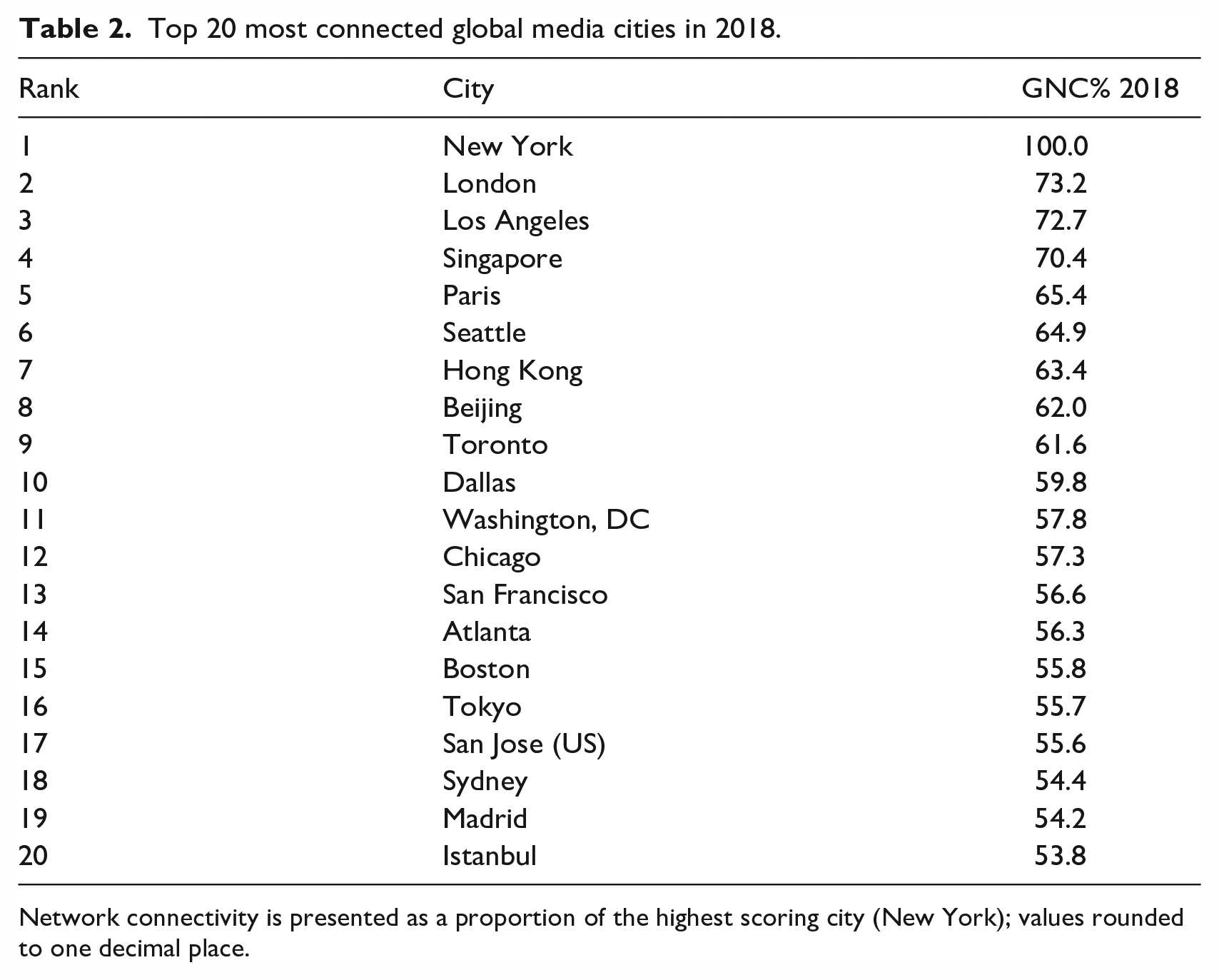

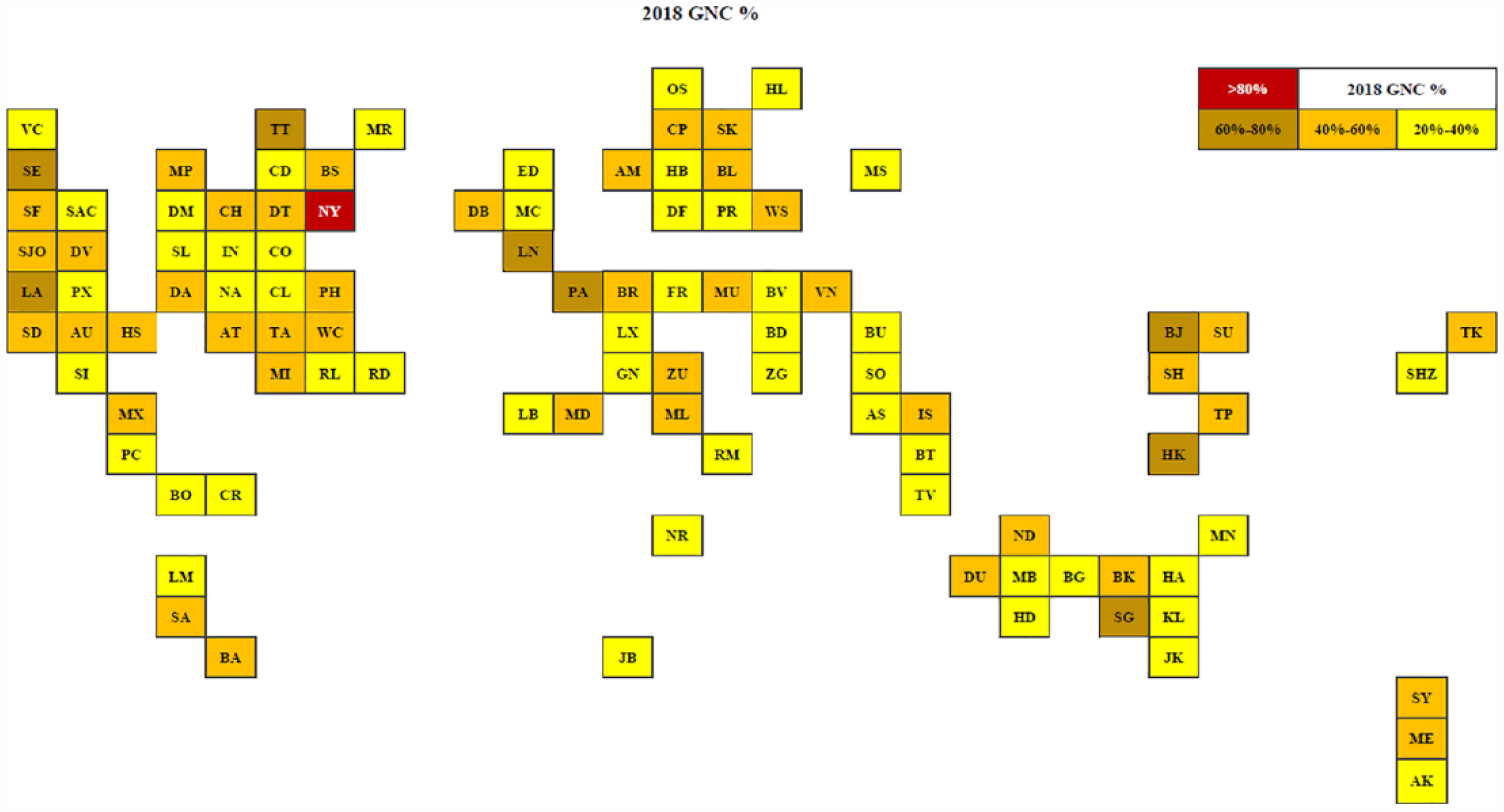

Table 2 ranks the top 20 most connected global media cities in 2018. New York is shown to be the most connected city: it is the most important node in the flows within the cumulative office networks of the TNMCs in our sample. The second ranked city, London, has only 73 per cent of New York’s connectivity, closely followed by Los Angeles and then Singapore. Paris is fifth with 65 per cent of New York’s connectivity. Figure 1 displays the location of the top 100 most connected global media cities in cartographic form. This allows for a visual appraisal of the networked urban geographies of the leading global media corporations. The most connected ‘global media cities’ – those cities forming important nodes within the networks of multiple global media firms – are shown to be located within North America, Europe and Asia. The cartogram is however marked as much by the lack of major media cities in the Global South as it is by the concentration of media cities in the Global North.

Top 20 most connected global media cities in 2018.

Network connectivity is presented as a proportion of the highest scoring city (New York); values rounded to one decimal place.

Top 100 most connected global media cities.

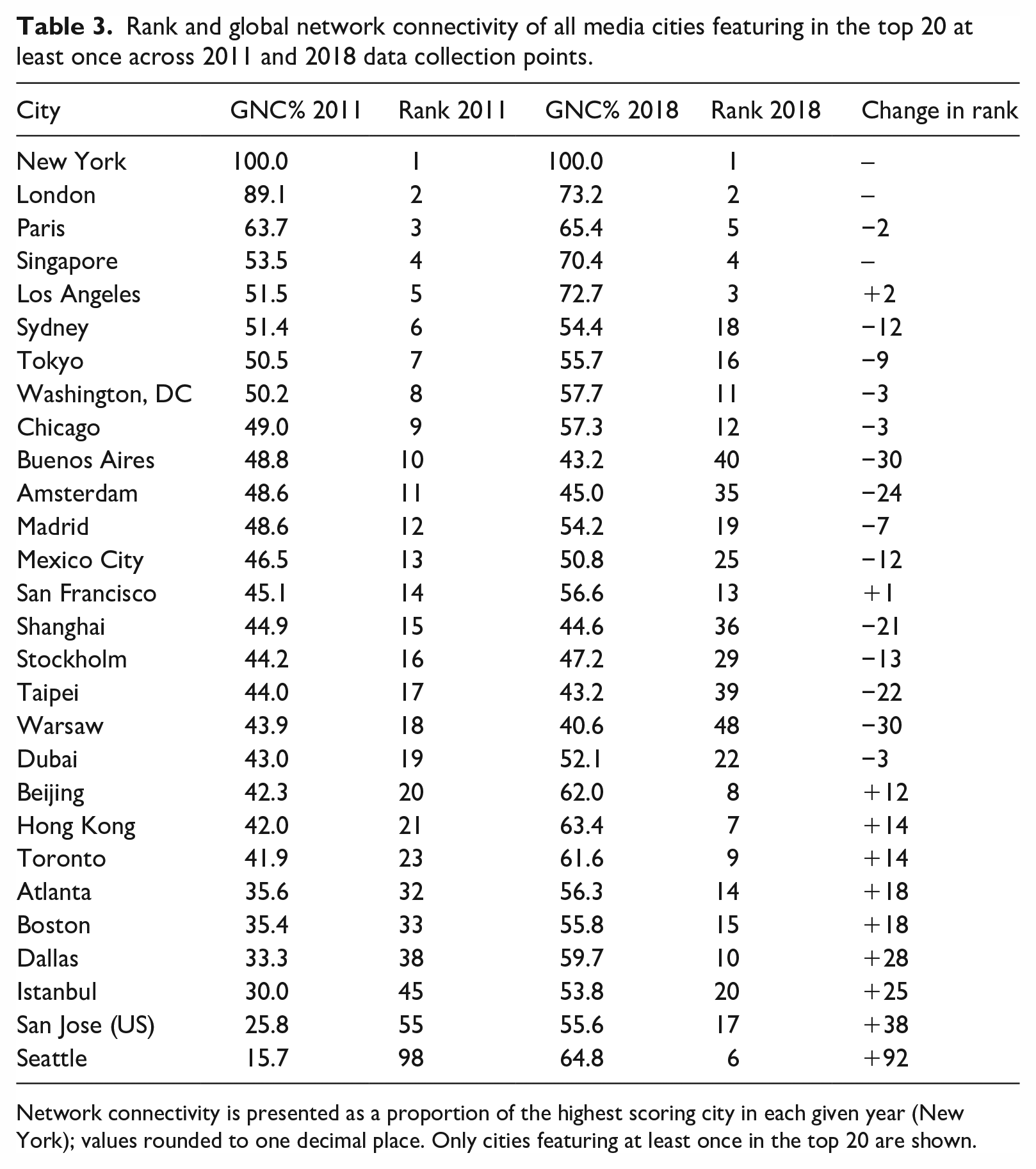

By drawing comparisons between the 2018 findings, and those from an earlier data collection point in 2011, we are able to evaluate change in global media city connectivity over time. Table 3 presents the rank and global network connectivity of all cities that feature in the top 20 at least once across the two data collection points. Notably, there is consistency in the position of the world’s two primary global media cities – New York and London – ranked first and second, respectively, in both 2011 and 2018. There is also consistency in the cities that make up the remainder of the top 5 – Los Angeles, Singapore and Paris – although there is some movement between the ranking of Los Angeles and Paris. More interesting, however, are six cities showing significant rises in their ranking between 2011 and 2018 to enter the top ten most connected cities in 2018. Three North American cities – Seattle (6th), Toronto (9th) and Dallas (10th) – move significantly up the rankings between 2011 and 2018, as do two Asian cities – Hong Kong (7th) and Beijing (8th).

Rank and global network connectivity of all media cities featuring in the top 20 at least once across 2011 and 2018 data collection points.

Network connectivity is presented as a proportion of the highest scoring city in each given year (New York); values rounded to one decimal place. Only cities featuring at least once in the top 20 are shown.

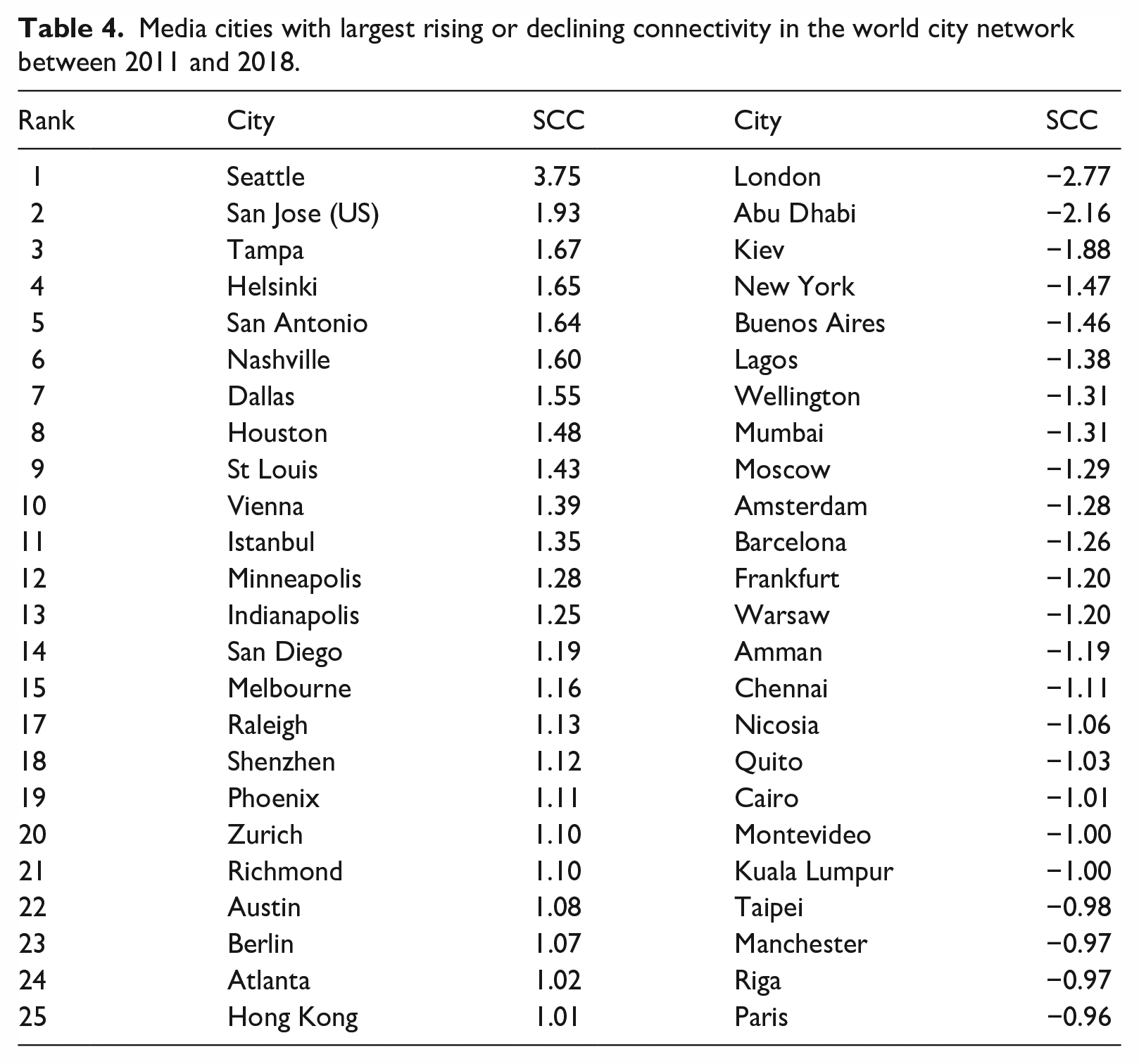

We can examine these changes in rankings in more detail by considering standardized connectivity changes. Table 4 displays those media cities with largest rising or declining standardized connectivity in the world city network between 2011 and 2018. A number of cities are notable due to their respective large gains or losses in connectivity. Seattle, the headquarters location of both Microsoft and Amazon, as well as an important regional headquarters for Chinese internet firm Baidu, displays a significant increase in connectivity, demonstrating the emergence of these ‘new media’ firms into the group of largest media corporations. Similarly, San Jose in California, which houses the headquarters of new media firms Alphabet (the parent company of Google) and Apple, sees a significant rise in connectivity. A detailed analysis of corporate headquarter locations in the US by Adler and Florida (2020) reveals that the number of Fortune 500 corporate headquarters has grown in both these cities over the last 20 years, driven primarily by the tech sector. While New York and London remain the two most connected global media cities, both significantly lose connectivity.

Media cities with largest rising or declining connectivity in the world city network between 2011 and 2018.

Figure 2 plots the 50 cities with the largest gains in standardized connectivity and the 50 cities with the largest falls. The geography of these changes in connectivity proves to be particularly interesting. US cities generally show an increase in connectivity, while cities across most of the rest of the world tend to lose connectivity. In the case of Europe and China, there is a more complex pattern of gains and losses in connectivity across major cities.

Global media cities with largest gains and falls in standardised connectivity.

Global media fields

The rankings and shifting connectivities for global media cities offer useful insight into how the international office networks of media corporations preferentially form networks between particular cities. However, the use of principal component analysis (PCA) allows us to uncover more detail about the spatial configuration of these networks. The findings from a three-component solution from the PCA analysis identify one global strategy as well as two regional strategies, these latter two focussing on the United States and China, respectively. Each component will be discussed in turn, following the rank order in terms of incorporated data variance.

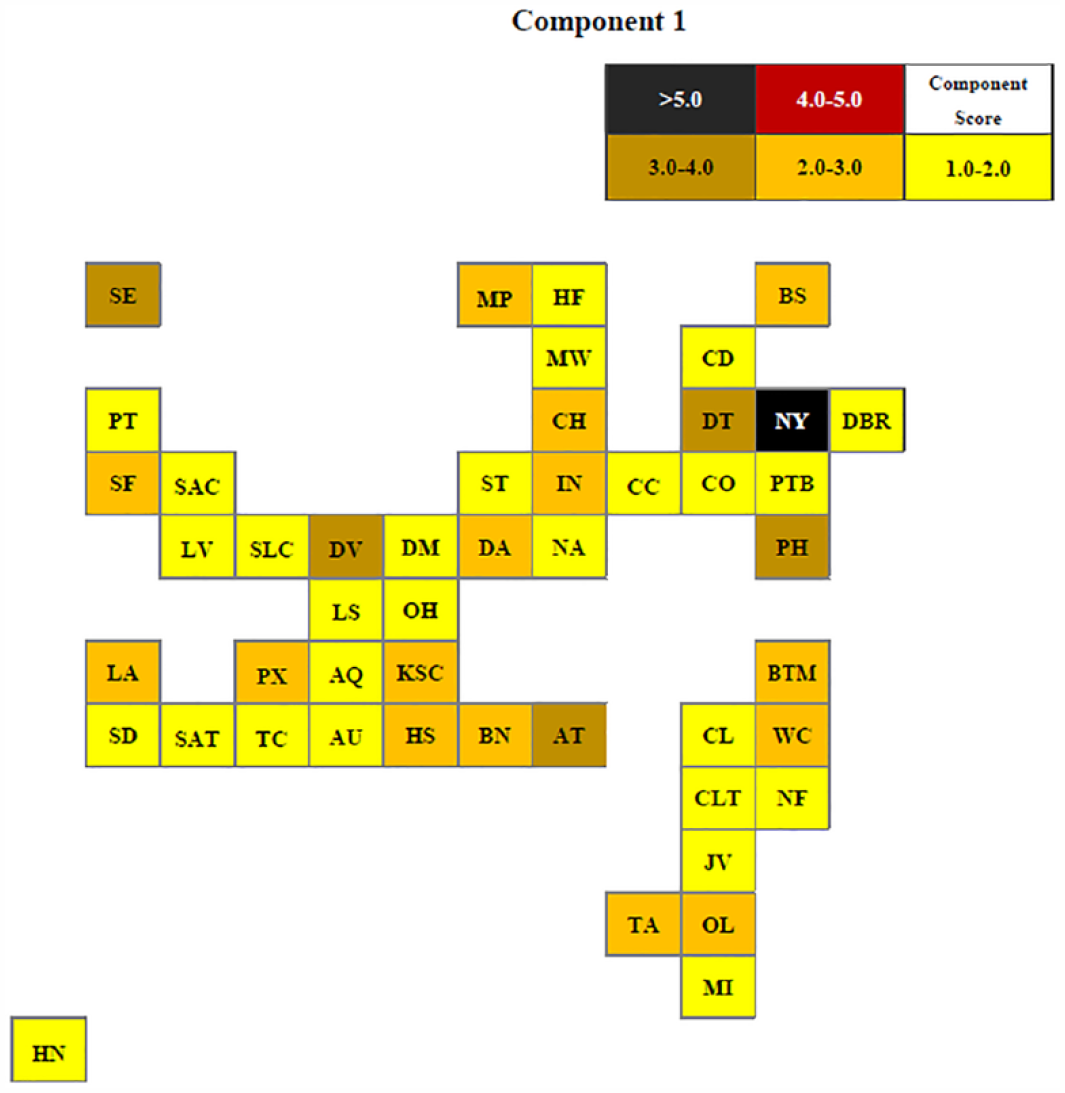

Component 1: US media strategy

Component 1, displayed in Figure 3, accounts for 20.7 per cent of the total variance. It reveals a media field based upon an almost exclusively-US locational strategy. The field contains 15 major media firms with loadings above 0.2 (Table 1), only two of which (Sony, Tokyo and News Corp., Sydney) are headquartered outside the US. The highest loadings are attached to firms in television, including the DISH Network Corporation (Denver) and Viacom (New York), and to communications firms, including Cox Enterprises (Atlanta) and Comcast (Philadelphia).

US media strategy.

The importance of these firms to this strategy is reflected in the field’s geography: New York is the articulator in this field (5.46), with a city score significantly larger than a secondary pair of cities that consists of Denver (3.80) and Atlanta (3.63). These are followed by a very ‘long-tail’ of US cities with slowly diminishing scores, led by Seattle (3.20), Philadelphia (3.11) and Detroit (3.03). All of the top 20 cities in this component are located within the US. The first non-US city in the field (London) is the 59th city in rank order by city score. This finding corresponds with those of both Krätke and Taylor (2004) and Hoyler and Watson (2013), who in their respective earlier analyses also identify US media fields, with New York acting as an articulator city. However, Los Angeles is shown to play a less important role in our 2018 analysis. Further, unlike the study of Krätke and Taylor (2004), which contains a number of cities in the Pacific Rim, the strategy identified here has an almost exclusively US focus, with only two cities outside the US featuring with a minor role. These results suggest that US television and communication corporations tend not to follow transnational expansion strategies, but rather underline the enduring importance of the US home base market, which effectively ensures that these corporations do not ‘stray too far from their home culture’ (Chan, 2005: 26).

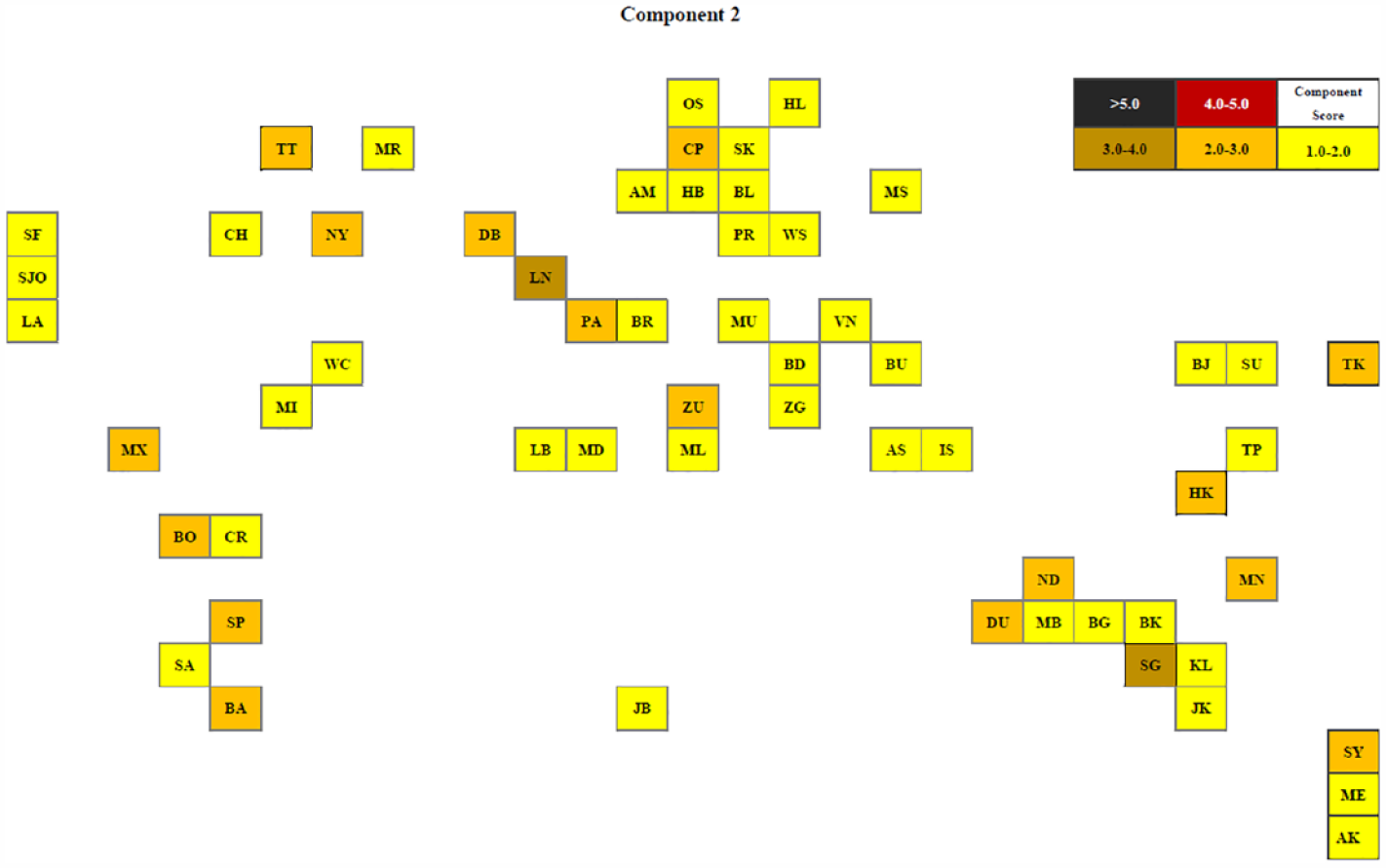

Component 2: Global media strategy

Component 2 shows a very different geography from that of Component 1. Accounting for 17.4 per cent of the total variance, the component reveals a global locational strategy. The field, displayed in Figure 4, contains 12 major media firms with loadings above 0.2 (Table 1). Of these, seven are from the US: these consist of a mixture of ‘new media’ and technology firms (Alphabet, Facebook, Microsoft, Amazon and AT&T Entertainment Group) and ‘traditional’ large media firms (Warner Media and Walt Disney). Two are from Europe (Vivendi, headquartered in Paris, France, and Bertelsmann, headquartered in Gütersloh, Germany), along with one from Canada (Thomson Reuters), one from Japan (Sony Entertainment) and one from Australia (News Corp).

Global media strategy.

These are firms that share a primarily international locational strategy rather than a domestic one. While there are no stand-out cities in terms of articulators, there is high geographical diversity within this component. Top ranking cities cover Asia, Europe, the US, South America and Australasia. Singapore (3.38) and London (3.26) are the highest scoring cities, with Paris (3.00), New York (2.99) and New Delhi (2.94) closely behind. Scores then decrease steadily and incrementally. These results demonstrate the globality of this media field; it is one consisting of a more globalized set of US firms with a number of European and other firms which share this globalized strategy. This is an interesting finding when compared to previous analyses of media corporations. Krätke and Taylor (2004), for example, identified global strategies, but connections with the US tended to be relatively weak and these were typically articulated through European cities and predominantly included European media firms. Conversely, among two global strategies, Hoyler and Watson (2013) identified a US-led global media strategy which suggested that the US printing and publishing corporations that primarily underpinned the component tended to be more transnational than US television and broadcasting firms with regard to their locational strategies. Our own findings are that, alongside a select group of large traditional media firms from across the world, US new media firms are pioneering new internationalization strategies that are acting to connect media cities across the world into media production and distribution networks.

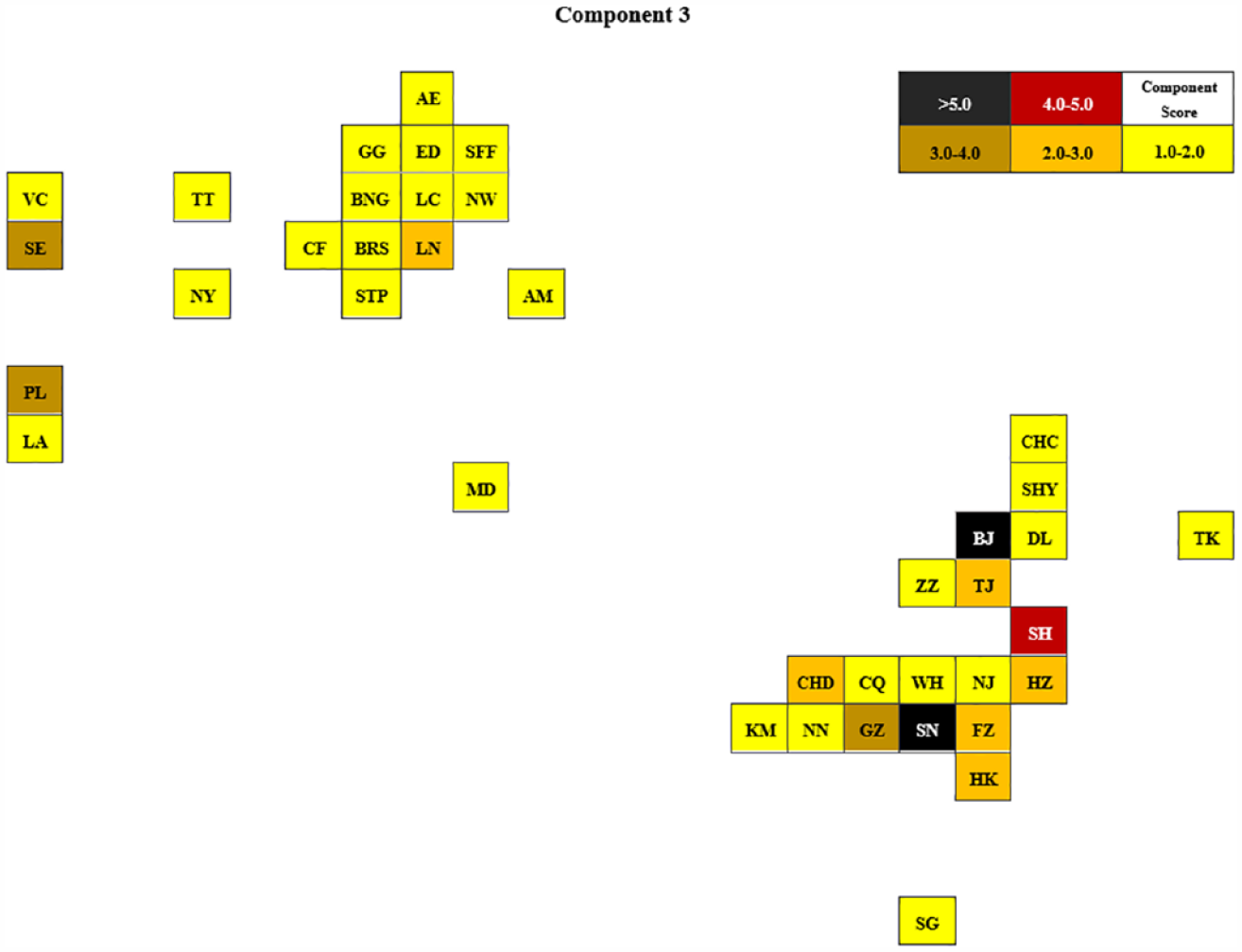

Component 3: Chinese media strategy

Component 3, displayed in Figure 5, accounts for just 7.9 per cent of total variance, but once again has its own unique geography, revealing a media field based upon a predominantly China-focussed media strategy. However, this component is also uniquely constituted in terms of firms. The field contains seven major media firms with loadings above 0.4 (Table 1), including five ‘new media giants’ (Flew, 2018). The emergence of these new media giants into the top grossing media firms is the most significant development in global media in the past decade, but further, our analysis suggests that they have a locational strategy rather different to that of the traditional US and European media giants. In the component, two Chinese-headquartered new media firms have a significantly higher loading than other firms. The first is Baidu Inc. (0.68). Headquartered in Beijing, Baidu is a Chinese multinational technology company specializing in internet-related services and products and artificial intelligence, and has grown quickly to become one of the largest AI and internet companies in the world. The second is Tencent Holdings (0.64). Headquartered in Shenzhen, Tencent is a Chinese multinational conglomerate holding company whose subsidiaries specialize in various internet-related services and products, entertainment, artificial intelligence and technology. The company has a near monopoly on messaging applications, with their WeChat platform having 500 million users in 2015, making it the largest messaging platform in the world (Hong, 2017). However, this distinct China-focussed strategy is not limited to Chinese new media firms. The component also features three of the US new media giants – Apple (0.55), Amazon (0.45) and Facebook (0.20), as well as a ‘traditional’ US media giant in The Walt Disney Company (0.45).

Chinese media strategy.

This component consists of two major Chinese media firms with a focus on their large domestic market, and firms from elsewhere which similarly have a significant focus on the Chinese media market. Chinese cities are notable in this media field as articulators; Beijing (6.24) is the super-articulator of the field, but Shenzhen (5.13) and Shanghai (4.52) also have scores that are significantly higher than the others. Of the 12 cities with scores higher than 2.0, 9 are Chinese (in addition to the above, Guangzhou, Fuzhou, Hangzhou, the SAR of Hong Kong, Tianjin and Chengdu). Two are US cities: Palo Alto, the location of Facebook’s headquarters, and Seattle, the location of Amazon’s headquarters, and it is notable that both Tencent and Baidu also have offices in these two cities. The broadcasting corporation Sky plc is the outlier of this component, with its own specific UK-focussed geography.

Closing discussion

Accompanying the growth and concentration of TNMCs and their oligopolistic control over the global commercial media market have been longstanding concerns regarding the power of these corporations (Castells, 2009; Corner, 2011; Freedman, 2014; Flew, 2018; Mirrlees, 2013). In this paper, we have developed the premise that a TNMC’s global office network, as determined by its transnational locational strategy, is an expression of the structural power of that firm. Here, structural power – or ‘power to’ – is understood as the ability of a firm to ‘exert the greatest degree of ownership and control over the means of producing, distributing, marketing and exhibiting media products’ (Mirrlees, 2013: 87). We have sought to contribute to research on the spatialization of TNMC power through a novel empirical analysis of the global-spatial organization of TNMCs, as reflected in their corporate global office networks, centred in global media cities. Through uncovering the structural networks that allow for the control and management of communicative resources across space, our results provide a crucial macro-level overview of the structural power of TNMCs to consolidate ownership and control over media at a transnational scale.

At the macro-level, two opposing trends appear from our results. On the one hand, our findings suggest a strong tendency amongst some US television and communications corporations to remain territorially anchored in their home market, with locational strategies focussed on exerting control over the production and distribution of content primarily for US television consumers. Yet, on the other hand, there is more evidence of media corporations pursuing internationalization strategies to expand their networks of ownership and control across the world. Our findings reveal a group of firms from across Europe, North America, Asia and Australasia, including both traditional and new media firms, that share similar strategies for global expansion. This not only provides clear evidence of the transnationalization of media corporations, but also indicates how the structural power of these corporations now reaches across geographical space.

The transnational office networks being developed by these corporations are a means for them to exert ownership and control over the means of producing, distributing, marketing and exhibiting media products well beyond their home territories. For example, our findings support the premise that over the course of the last few decades, US and European TNMCs have worked to expand their corporate networks into Asia in an attempt to share in the profitability of the continent’s large potential media audiences (Sussman and Lent, 1999). The emergence from our analysis of a media strategy centred on China can be considered the latest iteration of this, as transnational media corporations seek to enter what could potentially become the world’s largest market for media content. This is further reflected in the ‘media capitals’ (Curtin, 2003, 2009, 2010) or ‘global media cities’ (Krätke and Taylor, 2004; Hoyler and Watson, 2013) in which these office networks are ‘anchored’, with the map of highly connected media cities reaching out beyond US cities and the old colonial centres of Europe, into Asia. Of the top 10 most connected global media cities, 5 are in North America, 3 are in Asia and 2 in Europe.

It is notable that this Asian locational strategy is newly emerging when compared to previous analyses of the locational strategies of TNMCs (Krätke and Taylor, 2004; Hoyler and Watson, 2013). In some senses, perhaps, it is not as new as it might seem. In the second component of our principal components analysis, we reveal a global media strategy in which primarily US and European TNMCs are reaching out to exert ownership and control into Asian media production centres, as well as to some extent across Central and South America. One might view this as simply the continuation of a longstanding US and European media imperialism. Yet, our results must also be set in the context of the development of new media, with internet and social media corporations recently emerging to become some of the largest TNMCs. Findings from the third component of our principal components analysis suggest that the opening of the Chinese media market to Western media is being pioneered by new media firms from the US, chiming with recent discourse regarding the appearance of a platform imperialism being driven by US-based platforms (see Jin, 2020). Yet, crucially, our results also demonstrate the rise of Chinese new media firms that, while focussed predominantly on serving the domestic market, are also reaching out into the US with their global office networks. These firms, Hong (2017: 342) argues, represent a ‘parallel universe’ of profitable conglomerates that rival US firms thanks to China’s huge userbase. But as Yeo (2016) describes it, the extent to which US capital has been invested in China’s internet sector has led to interwoven economic interests between the two. Thus, we are witnessing a concurrent expansion of the power of new media across the two continents that cannot simply be defined in terms of a uni-directional imperialism. As researchers such as Thussu (2007) and Teer-Tomaselli et al. (2019) have recognized, flows of information, communication and culture are not one-directional from the West outwards; rather, there also exists a ‘contraflow’ of information, media content, consumer goods and capital from other parts of the world into more developed markets. In this regard, this paper provides an important over-arching conceptual and empirical framework for more locally specific analyses of media production networks that seek to understand the embeddedness of domestic media markets within the global media economy.

Footnotes

Acknowledgements

The authors are very grateful to the two anonymous referees whose feedback helped to improve the clarity of the arguments presented in this paper.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.