Abstract

Over the past decade, open government has promised increased government accessibility, responsiveness, and accountability. However, the diverse frames that societal actors hold on open government are often overlooked, even though understanding these frames is crucial, as open government principles may not always align with the practical expectations of its stakeholders. This gap is particularly evident in executive government agencies, where the tension between different frames plays out in daily operations. Against this background, this article identifies and analyses four distinct societal frames of open government within the context of the Dutch Tax Administration.

Through a qualitative document analysis of over two hundred written documents, we identify four frames of open Tax Administration: service-oriented, controlling, transformative, and cautious. We plot different societal actors in an arena, to illustrate their overlapping and diverging interests, expectations, and perceived risks. Amongst the actors, the service-oriented frame is the most predominant, emphasizing transparency and accountability for public service delivery. Understanding and addressing the diverse societal frames on open government is crucial for effective policymaking and ensuring compliance. The results illustrate that opening government is a collaborative process that requires a mutual understanding between government and its target audiences.

Key Points for Practitioners

In executive agencies, the practice of open government often diverges from strategic definitions, and this gap needs attention

Open government is a socially produced concept, with different societal actors adhering to distinct frames

Opening government is a complex, collaborative process that requires consideration of the varying societal frames when developing open government initiatives

Introduction

Democracy is always a work in progress. Academics, policymakers, politicians, and engaged citizens across the globe argue that the notion of open government contributes to democratic ideals by making governments more accessible, responsive, and accountable (Open Government Partnership, 2024; Wirtz & Birkmeyer, 2015). Interest in open government has surged over the last decade and has become a focal point for research as well as national and international government initiatives (Cucciniello et al., 2017; Kempeneer & Wolswinkel, 2023; Meijer, 2015; OECD, 2016; Tai, 2021). Open government is critical for fostering public trust, improving policy effectiveness, and encouraging innovation through open data (Kassen, 2021; Kim & Lee, 2012).

By the commonly-used OECD definition, open government (OG) involves practices of transparency, accountability, and participation (OECD, 2016). These elements are intertwined, shaping the practice of open government at both the policy and executive levels. Wirtz and Birkmeyer's (2015) describe OG as ‘a multilateral, political and social process, which includes in particular transparent, collaborative and participatory action by government and administration’ (p. 392). Despite a consensus on the broad principles of OG, its interpretation and implementation differ significantly across contexts (Gonzalez-Zapata & Heeks, 2015). Even though OG ‘plays a crucial role as the mediator between government and private actors’ (Valli Buttow & Weerts, 2022; p. 231), actors often have varied expectations and understandings of the principles of transparency, accountability, and participation. This diversity of the phenomenon and divergence in understanding can be attributed to the different “frames” through which actors perceive open government (Criado et al., 2018). Currently, understanding of the societal frames of OG remains limited, with exemptions such as research by Ham et al. (2019) which explores ‘strategic formation paths’ of open government data.

This article addresses this gap by adopting a framing perspective on OG. We view OG as a co-productive process where engaged actors frame their actions, beliefs, and roles (Visser et al., 2021). By analysing how societal actors frame OG, this study provides insight into how openness is understood and enacted within executive agencies. This co-production is the essence of our view on processes of open government and government agencies. The main purpose of this article is to construct the societal arena of frames on open government to understand how these frames co-produce the concept. The central research question of this paper is: How do different societal actors frame open government in the context of executive agencies? To answer this, we conducted a qualitative document analysis focusing on the Dutch Tax Administration, a key case given its recent societal scrutiny concerning openness and transparency following the recent child benefit scandal (Peeters & Widlak, 2023).

While previous OG research has focused on institutional approaches (Safarov, 2019) or technological aspects like open data (Ruijer et al., 2023; Zhenbin et al., 2020), few studies have explored the social processes and frames that shape OG in practice. This paper builds on the work of Ruijer et al. (2020) who highlight the lack of a shared cognitive framework for understanding open government, and Bovaird & Loeffler (2012), who emphasise the co-production of public services. These studies underscore the need to explore OG as a socially constructed process that evolves through the engagement of diverse stakeholders.

The concept of framing provides a valuable lens through which to study open government (Schön & Rein, 1994; Van Hulst & Yanow, 2016). Framing can be used as a conceptual tool “to understand and analyze processes of meaning-making and to capture differences between actors in how they construct meaning of and in policy processes” (Van Hulst et al., 2024; p. 6). Recent research has underscored the importance of examining how public officers’ perceptions and public definitions of OG—closely related to framing—affect the concept (Gil-Garcia et al., 2020; Moon, 2020; Wolswinkel, 2023). Better understanding of these frames can provide insight into the challenges and opportunities associated with implementing OG.

This gap is especially pronounced in executive agencies like tax administrations. Executive agencies differ from other public organizations due to their unique combination of managerial autonomy and their operational focus on service delivery, often separated from direct political oversight (Verschuere & Bach, 2012). Unlike other public organizations more directly involved in policymaking, executive agencies often have a dual role in policy execution while maintaining a functional distance from policy formulation (Chen et al., 2019; Dom et al., 2022; Neuroni et al., 2013). Recently, Dutch executive agencies have been scrutinised for being inaccessible, and reversely employees of the Dutch Tax Administration have spoken out about their dissatisfaction with unfiltered information distribution by the media (Ministry of Finance, 2021). As a result, despite the potential benefits of OG for service delivery, many public agencies do not proactively participate in OG initiatives (Zhenbin et al., 2020).

Through the analysis of over two hundred documents and an outside-in perspective on societal actors, amongst which are taxpayers, employees of the tax administration, and the media, we offer a nuanced picture of the varied expectations, concerns, and aspirations surrounding open government in practice (Wirtz et al., 2023). By identifying and analysing the different frames through which actors perceive open government, we shed light on the unique challenges and opportunities that arise in the implementation of these principles. As executive agencies navigate the complex balance between openness and operational stability, our study fills a critical gap in the literature by contextualising the core components of open government—transparency, accountability, and participation—within this underexplored institutional setting (Harrison & Sayogo, 2014; Neuroni et al., 2013). Ultimately, this research contributes to both the conceptual development of open government and its real-world application, particularly in the evolving context of public service delivery.

Theoretical Framework

Starting from the aim to unravel the societal frames on OG, the theoretical exploration is focussed on two elements: which definitions of OG are helpful to analyse the frames, and which preliminary frames already exist in literature.

Defining Open Government

Open government (OG) is a complex concept with no clear consensus on its definition despite extensive academic attention (Cucciniello et al., 2017; Wirtz & Birkmeyer, 2015). This inherent opaqueness has to do with its dialogical nature, as Criado et al. (2018; p.72–73) describe; ‘it is a paradigm with the purpose of maintaining a permanent dialogue with citizens, where the government system revolves around active citizenship to generate synergies with government institutions in a collaborative and transparent manner’. However, as we argue in this paper, the citizens’ (and other soctietal actor's) perspectives often remain underexamined.

Tai (2021) categorises OG definitions into two main groups. The first, proposed by Meijer et al. (2012), emphasises openness in information (vision) and interaction (voice) through public access to information and participatory activities. The second, based on the Open Government Directive (Obama, 2009) and formalised by Wirtz & Birkmeyer (2015), defines OG as a multilateral process focusing on transparency, participation, and collaboration. In practice, organisations like the Open Government Partnership (OGP) include transparency, participation, and accountability as essential pillars fostering democracy and inclusive growth (OECD, 2016; Open Government Partnership, 2024) (OGP, 2024). In this study, we will start from the OECD approach to OG (2016) and focus on transparency, accountability and participation in our theoretical and empirical analysis. This practice-oriented approach was chosen, because we are analysing a practical case study in which the subject (Dutch Tax Administration) pursues OG in concordance with the principles advocated by the OGP. We do however emphasise the inclusion of a qualification of the social process of OG in this research: a multilateral, political and social process where various actors co-produce the concept through their interactions, beliefs, and roles. By concentrating on the OECD definition, we aim to capture these underlying interpretive frameworks that guide OG practices.

The first component of OG is transparency, which has received the most academic attention (Tai, 2021). According to the OECD (2016, p. 25), transparency involves making relevant government information available and accessible to the public (OECD, 2016). This corresponds to what the literature calls nominal and effective transparency, the idea that information should both be visible and inferable (Hood & Heald, 2006; Michener & Bersch, 2013). Nominal transparency being simply the making public of government data, and effective transparency being the quality of the information and whether it can be easily found, used and understood by the public. More nominal transparency does not immediately imply more effective transparency, as Renteria's research about information provision in Mexican municipal governments (2024) points out; there are still many ways in which public officers can generate opacity whilst fulfilling nominal transparency needs.

In the context of executive agencies, transparency means that the Tax Administration should make information on its procedures and functioning public, comprehensible, and useful. Some literature focuses on fiscal transparency, meaning the disclosure of information about the expenses of government/executive agencies, which are funded by the money the Tax Administration collects. Increased fiscal transparency has been found to lead to better financial management and governance (Benito & Bastida, 2009; Bisogno & Cuadrado-Ballesteros, 2022). Moreover, fiscal transparency increases tax compliance of citizens (one of the Tax Administration's main objectives) (Capasso et al., 2021).

The second component of OG as defined by the OECD (2016) is accountability. In their conceptualisation of the interdependencies between transparency, participation and accountability, Harrison & Sayogo (2014) define accountability as ‘the obligation of government to answer to its citizens usually by reporting information about the use of public resources in ways that enable citizens to assess its performance’ (p. 515–516). Transparency is a necessary condition for accountability, and together they form interdependent cornerstones of open and democratic government (Harrison & Sayogo, 2014).

Many scholars agree on the possible advantages of accountability for executive agencies. These advantages include improved perceptions of legitimacy and performance goals, increased fiscal responsibility and, ultimately, a strengthening of societal trust in government agencies (Grimmelikhuijsen, 2012; Halachmi & Holzer, 2010; Harrison & Sayogo, 2014). However, unrestrained demands for accountability may lead to an audit culture characterized by dwindling trust (Tough, 2011). Furthermore, in their piece fittingly titled ‘The New Ambiguity of “Open Government”’, Yu & Robinson (2011) argue that while governments may increasingly deliver open data, increased data accessibility does not necessarily result in more accountable governments, reinforcing the transparency-accountability gap discussed by Park and Gil-Garcia (2022).

The final element of OG is participation, which is about processes in which stakeholders have an active role in and share control over decisions (Luyet et al., 2012; Reed, 2008). Participation in this sense is about the collaborative interactions between government and citizens, which construct a more responsive and inclusive governance system.

Participation is not limited to decisions about legislation and policy, but could also be organised around the implementation of policy and thus also about the work of a tax authority. For instance, citizens might be invited to participate in a new tax-paying procedure or to join a panel to test new tax software. There are even forms of participation in which citizens could take over specific public services, known as coproduction or citizen initiatives (Bovaird, 2007). Although there are no specific examples of co-production in tax services, related practices such as participatory budgeting and collaborative tax monitoring exist (Enachescu et al., 2019; Huiskers-Stoop & Gribnau, 2019)

Framing Open Government

It is alongside these three dimensions (transparency, accountability, and participation) that we will perform the framing analysis of OG by the relevant actors. Although framing analysis is a widely used established tool in the study of public policies (Van Hulst & Yanow, 2016), it has to our knowledge not yet been used to study actors’ expectations and understandings of OG. Most OG studies focus on specific components such as transparency, accountability, or participation without integrating them into comprehensive frames that capture the multi-faceted nature of the concept. Moreover, societal perspectives are often neglected. This while these societal perspectives would be helpful to add to our understanding of OG as ‘previous research has particularly focused on the provider perspective of OG, widely neglecting the equally important perspective of citizens and other external stakeholders’ (Wirtz et al., 2023: p. 803). Therefore, in this section of our theoretical framework, we provide some preliminary frames which we have drawn up from OG literature.

Some research has been done on how OG (more specifically open government data) can have different benefits and goals for different stakeholders, that can be interpreted as preliminary frames. Gonzalez-Zapata & Heeks (2015) identify two groups of stakeholders: those that are responsible for delivering open government data (e.g., politicians) and those that are interested in utilising it (e.g., civil society activities). Both groups have different reasons for having an interest in open government data. Gonzalez-Zapata & Heeks (2015) translated these reasons into four different perspectives which stakeholders can have on open government data: bureaucratic, technological, political and economic. The proposed conceptual dimensions of OG by Gil-Garcia et al. (2020) combine main elements from the OECD definition with information technology and information availability. Valli Buttow & Weerts (2022) perform a critical discourse analysis (CDA) of OECD documents and, therefore, come closest to our framing analysis. They use the CDA to show how open government data came to be and how the expectations of open government data have changed over the years. They describe open government data as a Swiss army knife: always useful, but without a single and clearly defined purpose. From their study three main purposes of open government data can be identified. Firstly, open government data increases transparency, which improves democracy by increasing trust in the government. Secondly, to boost economic development by using the economic potential of data. Thirdly, open government data leads to the public being able to create innovations and provide solutions enhancing the efficiency of public services.

Janssen et al. (2012) further emphasise the technological perspective by exploring the role of digital platforms in enhancing transparency and enabling new forms of citizen engagement. This perspective aligns with what we describe as the digital engagement frame, where technology-driven interactions enhance governmental accountability and responsiveness (Linders, 2012). Some authors express criticism of the techno-optimism surrounding open government. They warn of the risks of exclusion and call for a more critical reflection on the power dynamics associated with technology (Hansson et al., 2015; Peeters & Widlak, 2023). Ham et al. (2019) analyse open government data by looking at the level of data provision and data usage in different countries. Here they make the distinction between the goals of the government providing the data and the goals of the market (private organisations) using the data. Other works, such as research by Harrison & Sayogo (2014), also highlights roles and responsibilities in OG. From these insights we have identified what can be termed a public accountability frame focused on oversight and a service delivery frame centered on improving government responsiveness and effectiveness in meeting public needs.

Moon (2020) describes the transition from old OG to new OG by analysing a case study of South-Korea, where he describes different goals of OG and where citizens are mentioned as one of the stakeholders. He mentions how the role of citizens is changing from being passively informed and the receivers of services, to being active co-producers of public services and users of open data. He identifies that the main values of OG are shifting from merely increasing transparency and accountability to also collaborating with stakeholders on improving the delivery of public services. Meanwhile, Valli Buttow & Weerts (2022) also propose that open government data is part of a deeper transformation of the administrative structure and organizational culture of governments altogether. The idea is to create government data ecosystems that go across different levels of government and national borders, and include a variety of institutions and societal actors. Together these authors construct what can be seen as a collaborative, multi-purpose transformation frame on open government. Lastly, an economic growth frame can be identified based on research by Gonzalez-Zapata & Heeks, 2015; Zuiderwijk & Janssen (2014). By making information publicly available, OG is described as an economic tool to generate economic value. With open government data, businesses and entrepreneurs can create new products, jobs, profits and room for investments. This frame is also seen in more practice-oriented publications and an integral part of the OECD's definition of open government which focuses on inclusive growth.

Although the literature has investigated other stakeholders and different goals of OG, a comprehensive understanding of the interplay between the expectations and interpretations of OG for the relevant stakeholders is missing. The preliminary frames presented here served as a basis for our empirical analysis and eventually inspired our results and the final frames (see Methods for further elaboration on this process).

Methods

Framing Analysis

The study of documents provides critical insights into the social construction of modern phenomena, such as open government. By examining these documents, we can better understand key policy issues, debates, emerging concepts, policy-making options, and the positions of various stakeholders (Karppinen & Moe, 2019). An effective method for interpreting documents from multiple perspectives is framing analysis. Framing analysis goes beyond identifying different interests and opinions around a policy issue; it explores the underlying perceptions and beliefs that shape those interests. These perceptions, known as frames, are described by Schön and Rein (1994) as the “underlying structures of belief, perception, and appreciation” (p. 23). Unlike more surface-level factors such as specific interests or themes, frames represent deeper and more stable cognitive structures. The purpose of framing analysis is to systematically identify and examine these frames, providing a more comprehensive understanding of how actors construct and perceive policy issues—in this case, the openness of tax administration.

Van Hulst & Yanow (2016) expanded upon the concept by emphasising that framing is not merely a static entity but a dynamic social process. They argue for an approach that not only identifies frames, but also considers the processes of sense-making that shape these frames. This shift in focus, from frame analysis to framing analysis, highlights the evolving nature of how policy issues are constructed in discourse. In this paper, we adopt this framing analysis approach to investigate how various actors frame the openness of the tax administration through written documents. Although these documents only capture fragments of the broader social processes that influence framing, we integrate these diverse elements into our analysis to provide a richer understanding of the issue.

Research Strategy and Process

To understand the actor's frames on open government and open tax administration, we analysed the different voices in the contemporary debate on openness concerning the Dutch Tax Administration. This analysis was done in three steps: (1) selection of documents, (2) coding the documents, and (3) analysis.

Firstly, we selected documents. For the selection, the research team constructed several target audiences for whom openness might be relevant in the context of the Tax Administration. Thereafter, for each target audience the kind of documents were determined in which the construction of frames could be retraced. For instance, political debates about the Tax Administration and the reports of these debates contain indications of politicians’ perceptions and beliefs. The media formulate their frames in commentaries in media as well as in publications of NGOs for journalists, so these sources were used for this target audience. For finding relevant sources, keywords were used, and these were selected in congruence with the OECD definition. The final selection of documents was supplemented by internal reports, messages, and blogs from the civil servant Intranet, provided by a contact (author 4) at the Tax Administration. Through this process of purposeful criterion sampling (Patton, 1990), the final collection of documents consisted of 207 newspaper articles, internal and external research reports, accounts of political debates and commission meetings and more. An overview of the documents and search strategy for each target audience is found in Appendix 1.

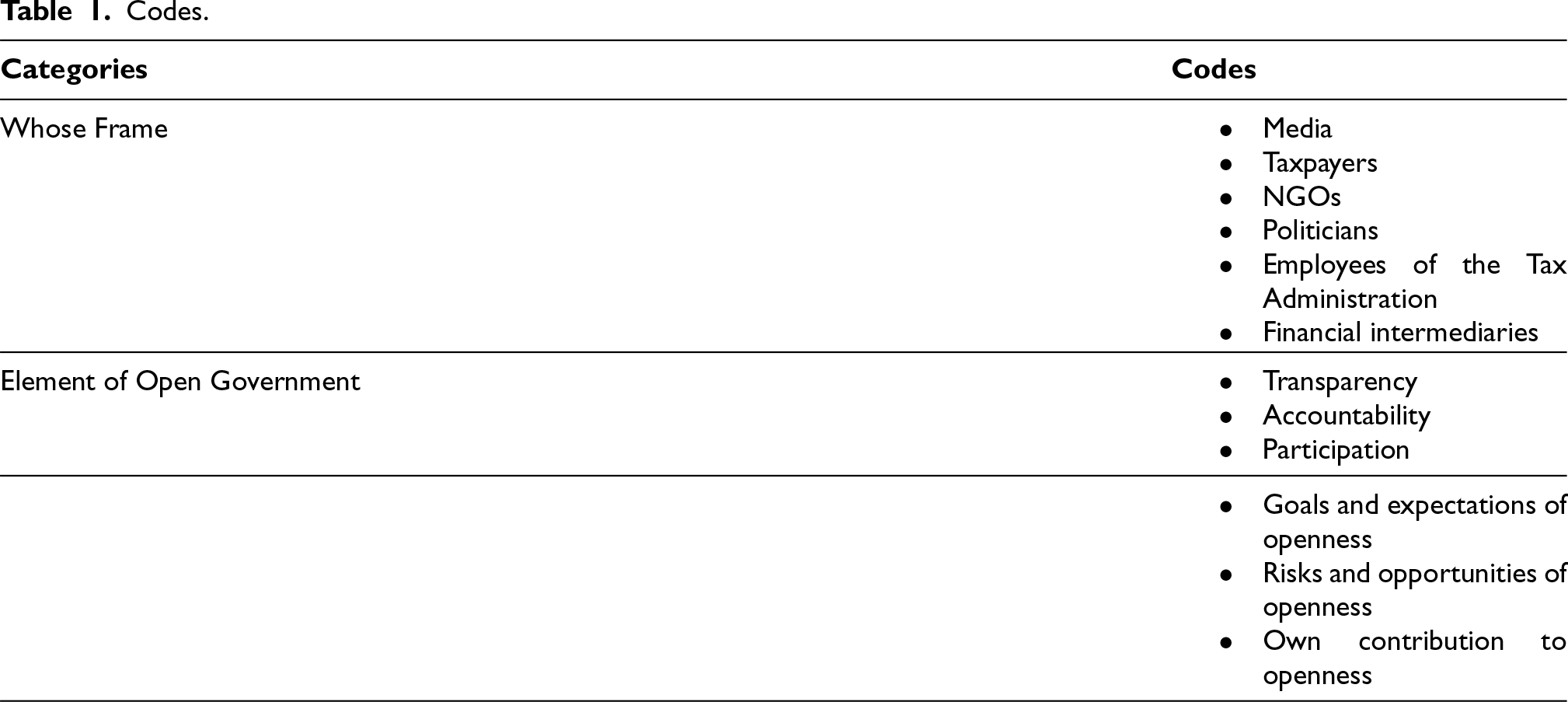

The second step was coding the documents. The 207 selected documents were uploaded to the data analysis software Atlas.ti and coded by the first and second author of this article. A code tree was developed beforehand (see Table 1). This code tree was based on the different target audiences around an open Tax Administration, and on the different elements of openness as distinguished by the OECD (transparency, accountability, participation). Moreover, in the literature on frame analysis, authors advise to have attention to the diagnosis of the phenomenon or problem, as well as the goals, solutions, and (proposed) actions (Lindekilde, 2014; Schön & Rein, 1994). Therefore, we added to the code tree the codes risks and opportunities of openness; goals and expectations of openness; and the actor's own contribution to openness. The code tree is summarized in Table 1 and in Appendix 2. On several moments during the coding process, we organised discussions between the authors about the conceptualisation and goodness-of-fit of the codes to ensure inter-coder reliability (Braun & Clarke, 2006).

Codes.

Codes.

The third step of the research involved applying framing analysis to the coded documents, guided by theories that describe frames as “interpretative packages” (Gamson & Modigliani, 1989; Lindekilde, 2014). We systematically coded the documents, focusing on how key elements—such as themes, metaphors, and recurring words and/or sentences—were linked to form coherent frames around the issue of OG. We mapped connections between different actors’ statements, revisited documents to validate whether patterns held across sources, and tested different configurations of the frames through team discussions. Through this iterative coding process, patterns emerged across different actors, showing distinct clusters of elements that went beyond the OECD's dimension of open government. As such, frames were identified by analysing recurring patterns in the data, particularly how actors made sense of the concept of openness in the tax administration. To ensure validity, the identified frames were compared with the literature on open government and framing theory, ensuring they aligned with existing concepts while also reflecting the specific context of our study. The research team discussed and verified these frames to ensure consistency and theoretical grounding.

The object of this study is the Dutch Tax Administration. The Netherlands, being member of the Open Government Partnership, takes part in the worldwide transition towards open governance by implementing open government principles on all levels and sectors of administration (Meijer, 2015; Safarov, 2019). These include for instance principles of open democracy through digital democracy and transparent elections, open information through the Government Information Act and open technology through open-source practices and open data communities (Ministry of the Interior and Kingdom Relations, 2020). Although some of these principles have been thoroughly developed on a strategy-level, to policy makers and politicians it remains somewhat of a puzzle how these principles of open government should translate in practice, especially in the context of executive governmental agencies, such as the tax administrations (Harrison & Sayogo, 2014).

In this national context, the Dutch Tax Administration lends itself as a suitable case for analysis for a threefold of reasons. Firstly, under the name of ‘Action Plan Open Government 2020–2022’ and ‘Desiring Openness’, the Dutch government and Tax Administration specifically have been working on exploring and implementing open government. Secondly, the Dutch Tax Administration has been under heavy scrutiny when it comes to transparency and accountability, due to the recent child benefit scandal where thousands of parents were wrongly accused of fraud and forced to pay back their child benefits in full (Peeters & Widlak, 2023; van Dam et al., 2020). Thirdly, since 1 May 2022 the Open Government Act legally obliges public agencies to actively, instead of passively, disclose.

Results

The analysis of the documents resulted in four distinct frames societal actors employ regarding an open Dutch Tax Administration. After comparing the four frames, we present an arena of open Dutch Tax Administration, positioning carious actors based on their framing of open government.

Service-Oriented: Transparency to Improve Service Delivery

The first frame focuses on openness as a means to improve public service delivery by the Dutch Tax Administration. The actors frame transparency and open government as necessary for compliance, responsiveness and fostering trust in the reciprocal relationship between the taxpayer and the executive organisation. All actors repeatedly make use of words such as “trust”, “access”, “tailoring” and the documents stress the reciprocal relationship between the actors and the Tax Administration. This aligns with previous research highlighting the role of openness as fundamental to fostering compliance and trust in public institutions (Zhenbin et al., 2020). This service-oriented frame is common across most societal actors, particularly taxpayers, employees, and financial intermediaries, all of whom benefit from a more transparent and responsive Tax Administration. Taxpayers, for instance, have this frame because they interact directly with the Tax Administration to resolve personal tax issues and expect efficient, accessible services.

Within this frame, transparency is seen as crucial, encompassing both the passive availability of information for public access (nominal transparency) and the active sharing of clear, useful information to help address taxpayers’ individual fiscal issues (Hood & Heald, 2006; Michener & Bersch, 2013). Across all actors, however, there is dissatisfaction with the current level of effective transparency. Taxpayers, media and financial intermediaries often address that while information is technically available, it is often difficult to find, use, or comprehend, particularly due to overly technical language, lack of personal points of contact, and the complexity of navigating online resources. Employees, too, encounter problems with effective transparency: ‘On the one hand, we want to serve the taxpayer as best as we can and provide tailor-made services where necessary. On the other hand, we must also ensure that everyone is treated equally and that the rules apply to everyone in the same way.’ (Internal report about transparency at the Dutch Tax Administration, 2019, translated)

Controlling: Accountability and Transparency for Oversight and Control

The controlling frame views openness as essential for ensuring accountability and overseeing the Dutch Tax Administration. In this frame, the need to monitor and scrutinise the actions of the Tax Administration is emphasized. This frame has gained importance due to the Dutch childcare benefits scandal, where a lack of information and suspected purposeful obscuring were noted. Where transparency as a component of OG was more prevalent in the service-oriented frame, here the emphasis is laid on accountability (Harrison & Sayogo, 2014; OECD, 2016).

This frame is predominantly advocated by politicians and the media, with some influence from NGOs and employees. All actors emphasise the need to monitor and scrutinise the actions of the Tax Administration to uphold democratic values and safeguard the public from potential abuses of power. Politicians and media align with this frame because they are responsible for holding public institutions accountable. NGOs adopt this frame to ensure that the tax Administration takes citizens’ rights into account, as regular taxpayers do not usually speak up about this themselves. By positioning themselves as protectors of the public interest, these actors frame transparency as necessary for ensuring that the Tax Administration is held accountable for its decisions and actions. For examples, journalists assert: ‘Our democracy is also protected by journalism. Controlling the power of the state is one of the most important tasks of journalism: checking whether authorities and organisations honour the agreements and take their societal responsibility.’ (letter of the ‘Association for Investigative Journalism’, 24 April 2021, translated). ‘Which Secretary of State and which part of the department is responsible for communication? Which is responsible for the rule of law? Which for ICT? Which for changing culture? […] I’m afraid that three parts of the department and two ministers will argue every day about their responsibilities’

Cautious: Balancing the Limits and Opportunities of Open Government

The cautious frame presents a strategic and thoughtful approach to openness, emphasising the need to balance the benefits of transparency with the potential risks it may entail. Rather than simply limiting openness, actors in this frame advocate for purposeful and measured transparency, where the focus is on ensuring that transparency serves a clear function and enhances public trust without leading to unintended consequences. Excessive transparency might lead to information misuse or overload, damaging trust in the Tax Administration (Yu and Robinson, 2011). Actors from this frame try to put a limit on the mindless increase of open government practice when it does not serve a purpose.

This frame was found predominantly among the employees, politicians NGOs and financial intermediaries. Politicians, in particular, are wary of nominal transparency, where the pressure to disclose information may lead to external scrutiny that is not productive or beneficial. A politician voiced these concerns during a debate on the childcare benefits scandal: ‘The solution is being found in transparency. Everything, literally everything, needs to be made public. Understandable and fair when it comes to this specific case, but I ask myself where it will end and will it even contribute to the restoration of trust. Personally, I think not.’ (Den Haan, 21 April 2021, translated)

The cautious frame also contributes to the broader open government debate by ensuring that transparency practices are sustainable and aligned with long-term goals. NGOs, for example, advocate for transparency regarding data use and decision-making processes but also express concern about the risks of exposing sensitive information, particularly when it comes to personal data protection (Harrison et al., 2012). Taxpayers share these concerns: ‘The Tax Administration sits on heaps of data from citizens and companies and generously shares that data with other agencies. Taxpayers find it much more difficult to access information that concerns them. The confidentiality obligation of the tax authorities has an uneven outcome and needs a refresh to better protect privacy’ (Financial Daily Paper, 2021, translated)

Transformative: Openness and Participation as Drivers for Systemic Change

The transformative frame sees openness not simply as a tool to improve specific government functions, but as a catalyst for fundamental systemic change in governance structures, public engagement, and decision-making processes. One might argue that the developments in open government (OG) are inherently transformative, making the inclusion of a ‘transformative’ frame seem redundant. However, we chose to include the transformative frame because it represents a distinct and radical vision of how openness fundamentally reshapes governance structures, extending far beyond the immediate goals of service delivery and accountability. The documents, actors, and quotations reflecting this frame diverged significantly in tone and scope from the other frames, reinforcing its necessity as a separate, unique perspective.

The transformation envisioned here involves more than just making information available—it is about creating a governance system that allows citizens to play an active role in shaping policies, decision-making, and government accountability. This transformative frame is radical in its goals, advocating for a shift from traditional, hierarchical governance to a collaborative, open, and digital governance model that adapts to the complexities of modern society. Unlike the service-oriented and controlling frames, which view openness in terms of specific goals (service delivery and accountability, respectively), the transformative frame envisions openness as the foundation of a new governance model—one that is participatory, decentralised, and driven by digital innovation. Digitalisation is an essential part of this process, as the Open State Foundation writes: ‘The good news is: it is all possible because of technology. Digitalisation offers unimaginable opportunities for sharing information and co-creation. These will lead to more trust, effective control and better policy. What is more, open government data will lead to an increase in economic value for society’ (Open State Foundation, 19 april 2021)

Comparison of the Four Frames on Open Tax Administration

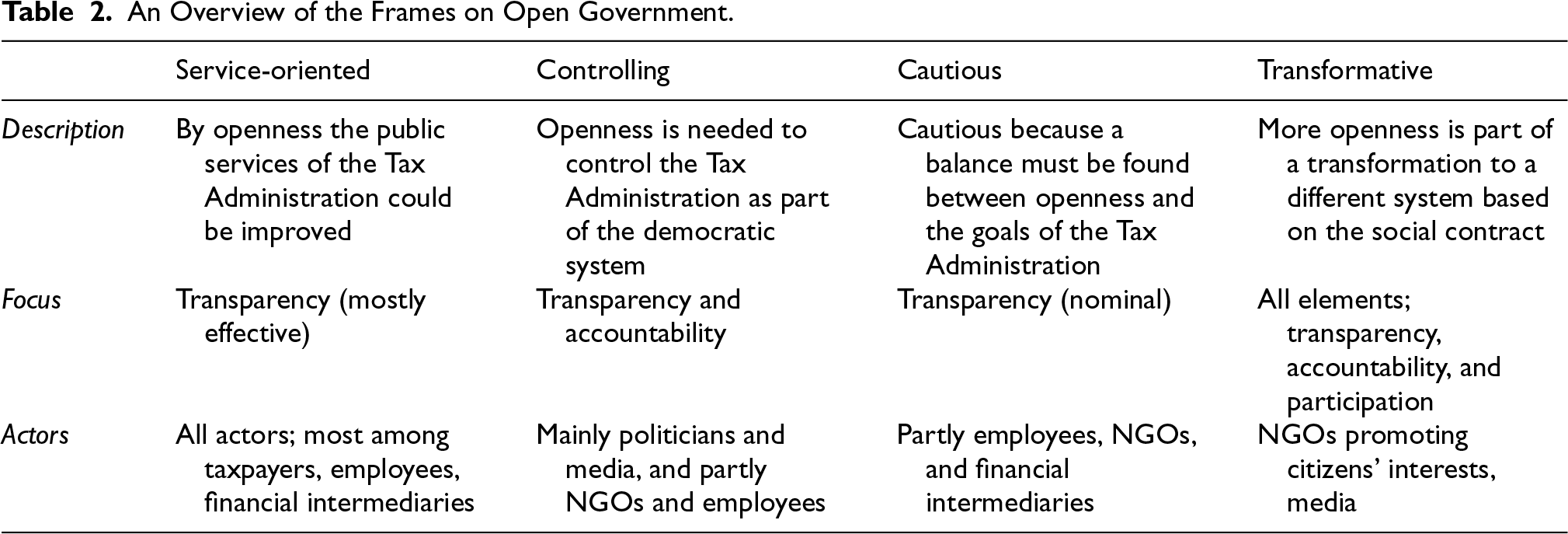

The four frames, their focus, and the actors among which we found them are summarised in the table below (Table 2).

An Overview of the Frames on Open Government.

An Overview of the Frames on Open Government.

The four frames identified—service-oriented, controlling, cautious, and transformative—bear significant connections to the preliminary frames found in the literature, yet also exhibit notable divergences based on the specific context of the Dutch Tax Administration The service-oriented frame aligns with the service delivery frame from the theoretical framework, emphasising transparency for operational efficiency (Janssen et al., 2012). Similarly, the controlling frame echoes the public accountability frame, where transparency is used for scrutiny and democratic oversight (Harrison & Sayogo, 2014). The cautious frame, however, adds a layer of pragmatism not emphasised in previous research. It highlights the risks of excessive transparency, such as privacy concerns and information overload (Yu & Robinson, 2011), which is less discussed in the literature. Meanwhile, the transformative frame closely parallels the multi-purpose transformation frame (Valli Buttow & Weerts, 2022), envisioning openness as a catalyst for systemic shifts toward digital and participatory governance. Interestingly, the technological framing, which is prominent in much of the OG literature, was hardly seen in our data. This absence is notable but not surprising, as societal actors in the context of the Dutch Tax Administration seem to prioritise democratic values over concerns about ICT infrastructure and digitalisation.

The comparison of the four frames reveals that while openness is a shared goal, the values driving it differ fundamentally across actors. For some, like politicians and the media, openness is tied to democratic accountability and oversight. They frame transparency as a tool to scrutinise government actions and prevent abuses of power. In contrast, employees and taxpayers view openness as crucial for improving service delivery, aligning transparency with efficiency and responsiveness. This service-control divide highlights a dichotomy of values, where what is seen as necessary oversight by one group may be viewed as obstructive to effective service by another.

The transformative frame goes further, advocating for a systemic shift in governance, where transparency is the foundation of a more participatory and digitalised model. This contrasts sharply with the more incremental improvements sought by the service-oriented and controlling frames. The cautious frame, on the other hand, tempers enthusiasm for openness by pointing out the risks—such as information overload, privacy concerns, and declining trust if transparency is poorly managed. Actors here push for targeted transparency that balances openness with operational efficiency.

The comparison of the four frames on openness shows that, although openness in policy is described as a widely shared norm and goal, the values behind openness differ fundamentally. For some actors it is related to democracy, while for others it is about performance and service delivery. For some actors, openness is about transparency, for others it is also related to accountability and even participation. Participation is strikingly absent in the frames, with the exception of the transformative frame. While the attention to participation increases in other domains, this is not (yet) the case for the topic of open government (see also the special issue by Kempeneer & Wolswinkel, 2023).

Furthermore, the beliefs about the level of openness differ. From the service-oriented and controlling frame, improvements and optimizations are needed. From a transformative point of view, a transition is needed to ‘open government’ in all aspects. The cautious frame is the only frame in which more openness is doubted and discussed. Acknowledging these differences has the consequence that policy regarding openness must consider these different frames. While the frames differ in focus, they all share a common emphasis on transparency as a foundational element. Transparency is broadly understood by the actors, by not only looking at the availability of information (nominal transparency), but also the accessibility (effective transparency). The alignment between actors and their respective frames reflects their distinct roles and responsibilities within the system—politicians focus on control, employees on service delivery, and NGOs on transformation—highlighting how each group engages with open government practices according to their specific incentives and priorities.

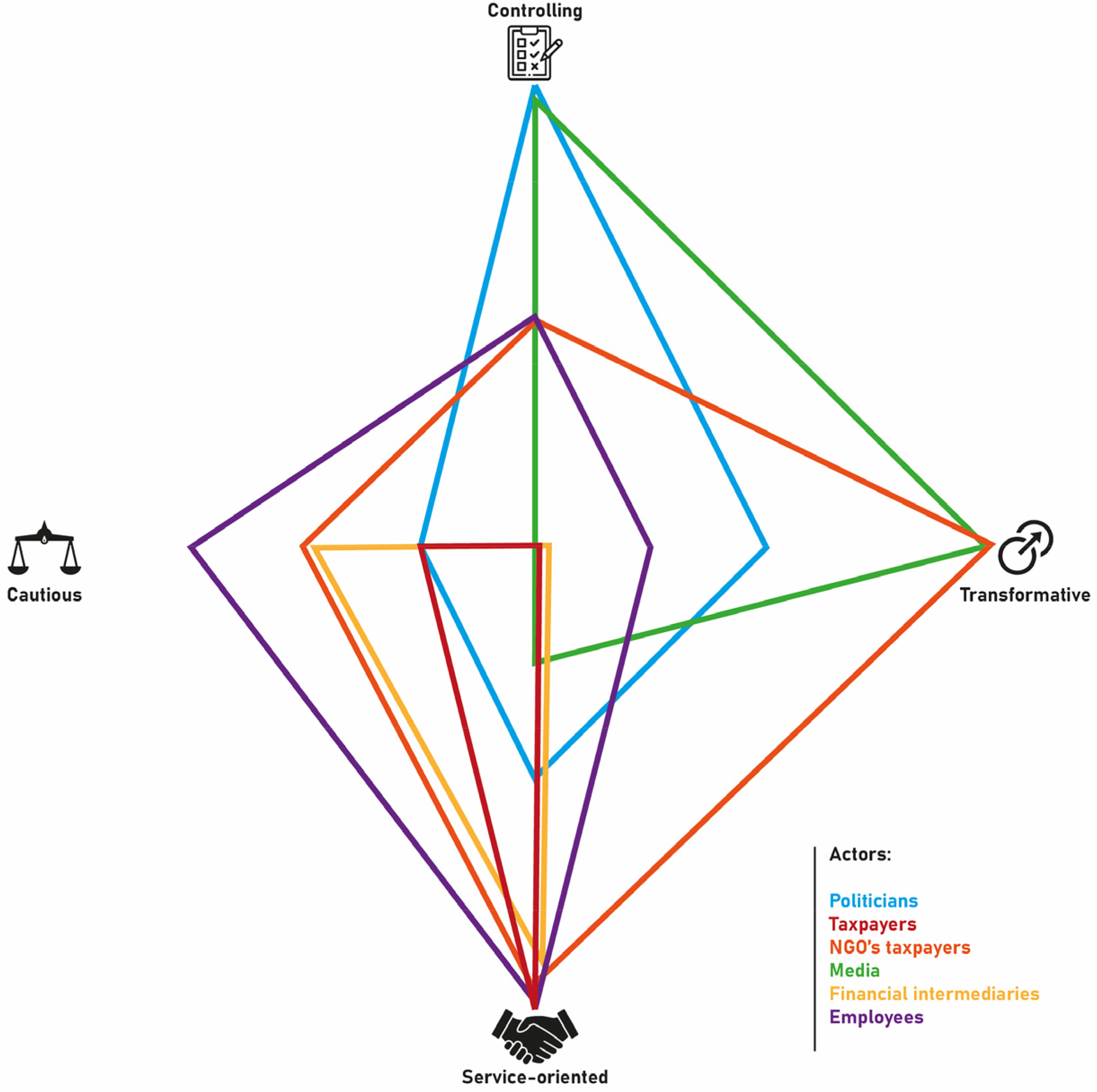

We have plotted the six societal actors in an arena of frames, to provide a more comprehensible overview of how these frames overlap and diverge. (We constructed the figure qualitatively, based on the document analysis, to visually represent the diverging and converging interests of the actor groups. While no quantitative measures were used, the figure effectively captures the relationships between frames and actors, highlighting their distinct roles and shared focus on OG) (Figure 1).

Arena of Societal Frames Open Tax Administration.

We will now go into some of the most salient patterns that can be seen in this arena. Firstly, most actors, aside from the media, converge around the service-oriented aspect of openness. These actors view an open way of working through increasing transparency, accountability and participation as essential for enhancing the Tax Administration's role in public service delivery. Therefore, positioning openness as a way to enhance public service delivery could be a good starting point for creating a shared cognitive framework for societal actors to engage in discussion about what openness entails in practice (Ruijer et al., 2020). This shared cognitive framework will help all actors move beyond seeing OG as a ‘Swiss army knife; always useful, but without a single and clearly defined purpose’ (Valli Buttow & Weerts, 2022; p. 220).

Second, notable tensions arise from the differing priorities of politicians and the media versus other actors. Both frame OG as a controlling issue, which is much less valued by the other actors. This could be an explanation for the tensions between for instance the employees on the one hand and the media and politicians on the other hand (Ministry of Finance, 2021). Their interpretations thereof differ in such a way that it often leads to negative interpretations of the other's intentions. For the sake of both practitioners dealing with societal actors and the academic advancement of the concept of open executive agencies, it is important to address this seeming dichotomy of values and stress the overlapping interest in openness to control government and hold people and organisations accountable (Park & Gil-Garcia, 2022).

When speaking of overlapping and diverging interests, another striking finding is the fact that the interests of taxpayers are remarkably different from other societal actors. Our analysis showed that taxpayers often assume that transparency and clear lines of accountability are in place, and that they only worry about openness when it directly concerns their personal tax affairs. Other groups, such as financial intermediaries and NGOs, are more vocal about the need for these preconditions on a higher level than mere personal business. One last finding that should be pointed out is the fact that the actor's frames on openness are not homogenous or clear-cut and might even seem contradictory; this is mostly visible within the NGOs. NGOs are both cautious and transformative when it comes to open Tax Administration. They wish that governmental agencies would become more transparent about their data use and algorithms, but are simultaneously wary of wrong implementation of these developments. Therefore, in talking about practical implications for open government, one should not assume that a certain actor only has one specific outlook on the issue at hand.

This article sheds light on the different societal frames on open government in the context of the Dutch Tax Administration. Open government contributes to democratic ideals by ensuring more accessible, responsive, and accountable governance and the topic has gained prominence in recent years (Open Government Partnership, 2024; Wirtz & Birkmeyer, 2015). Despite this interest, there remains a lack of understanding regarding the different frames that exist on this topic and how they overlap, diverge, and interact (Ruijer et al., 2020), especially within executive agencies (Neuroni et al., 2013). This article aims to address these gaps by analysing over two hundred documents related to open government in the Dutch Tax Administration context.

Our analysis identified four distinct frames on open government:

Service-oriented: transparency to improve service delivery Controlling: accountability and transparency for oversight and control Cautious: balancing the limits and opportunities of open government Transformative: openness and participation as drivers for systemic change

These frames illustrate how different societal actors perceive and engage with the principles of open government. Comparing the empirical societal frames with the preliminary frames from the literature highlights the importance of examining these theoretical constructs in practical settings. Our findings show that societal frames largely align with those in the literature, particularly the service-oriented and transformative frames. These frames focus on effective transparency for efficiency and systemic change, respectively. As we are specifically looking at an executive agency, it is unsurprising that the economic and technological frames, which are more prominent in the literature, were less evident in our findings. This suggests that while the theoretical framework provides a broad understanding of open government, its real-world application tends to prioritise democratic and service-oriented aspects, especially in the context of the Dutch Tax Administration.

Acknowledging the differences in frames is crucial, as policy regarding openness must consider these diverse perspectives and position the government within this social process. The most important takeaway is that researching or engaging in discussion with practitioners or other stakeholders about open governmental agencies, is not unequivocal; even within the groups of actors there might be diverging interests, desires or apprehensions. This aligns with our vision on open government as a socially constructed process, where various actors co-produce the concept through their interactions, beliefs, and roles (Visser et al., 2021). Future research could investigate whether these frames hold in other governmental contexts and executive agencies, or whether those arenas consist of significantly different societal actors and frames.

Theoretically, our findings highlight the dual role of OG: it serves both democratic values and instrumental purposes. Empirically, the service-oriented frame was the most prevalent, focusing on effective transparency and accountability to ensure public service delivery (Heald, 2012; Tough, 2011). This observation raises important questions about the gap between the theoretical ideals of OG and its practical application. Should we interpret the dominance of the instrumental view—centered on service delivery—over the democratic one as indicative of the practical priorities for OG? This insight is critical for policymakers, as it suggests a need to balance the democratic potential of OG with its day-to-day application in public service improvement.

Another striking finding is the absence of participation as a part of open government in most of the documents. Although it has been gaining academic interest lately, see the special issue on open government and participation as edited by Kempeneer and Wolswinkel (2023), it does not yet arise as a matter of practical urgency for most of the actors. This lack of focus on participation in the documents suggests that embedding participatory practices into open government remains a challenge. To succeed, OG initiatives must recognise the competing frames, tailoring policies that account for the specific demands of each actor. Future research could explore how to better integrate participation into existing OG frameworks, examining the barriers—such as institutional resistance, lack of public engagement, or insufficient digital infrastructure—that prevent participation from being fully realised in practice.

Despite these contributions to research and practice, our study is subject to some limitations which are to be discussed. First of all, most documents that were analysed for this article were secondary documents, accessed through online libraries or government repositories. For some internal documents, we relied on a contact within the Dutch Tax Administration (author 4). On the one hand, this could be an advantage, as we were able to analyse documents that would otherwise not be at hand. On the other hand, because we only had one source providing us with internal documents, it remains unclear whether we have included all possible communications and reports on the topic (Wirtz et al., 2023). Moreover, the data used for this article revolves exclusively around open government in the specific context of the Dutch Tax Administration. Future research could dive into other executive agencies or different national contexts to see whether the frames and distribution of actors across these frames are similar.

Secondly, as we only looked at documents from 2018 onwards, the childcare benefit scandal had a significant influence on the discourse of openness in the analysed documents. This goes mostly for the documents on political actors and NGOs. This might have distorted the frames. However, the political agenda is always influenced by societal occurrences happening at that time. If it had not been the childcare benefit scandal, it would have been another controversy on openness that might have steered the debate. Lastly, we extracted the media's frame from commentary columns, not from interviews or other ways of reporting. Opinions stated might therefore have been distorted by considering the interests of the newspaper itself.

The global trend towards more open forms of governance may at first glance seem straightforward and universally beneficial (OECD, 2016). However, our analysis revealed that the process of opening government is actually multi-faceted and requires a joint effort from various stakeholders. Therefore, the topic should not be analysed from a sender's (i.e., governmental) perspective alone, but societal points of view should be taken into account (Maanen, 2023). Policymakers must navigate the tenstions between actors who demand more transparency for the sake of control or service-delivery, and those who worry about the risks to privacy and efficiency. This is part of the social process of openness. Transparency as a keyword for open executive agencies should be further examined, and it would serve researchers and practitioners well to keep the distinction in mind between making data public (nominal transparency), and the quality and accessibility of data (effective transparency). While transparency is a critical component, it must be balanced with accountability and participation to fully realise the benefits of open government. If the goal is truly to enhance democracy and inclusive growth, merely making information available simply will not do. Many frames depend on a more active role of the government in the dissemination and explanation of information, as well as being reachable, providing humane service and creating space for the voice of other target audiences.

Across different groups of stakeholders, there is an array of frames on this topic, sometimes complementary and sometimes contradictory. These frames do not merely reflect societal expectations; they also shape the policies and approaches adopted by government agencies in their OG efforts. Therefore, acknowledging the impact of these frames is crucial, as they inform the tangible direction in which OG practices evolve. ‘Doing’ open government thus becomes a practice of weighing off people's perspectives, possible actions and desired democratic outcomes instead of a mere ambition on the strategy level. Governments, including their departments and executive agencies, are constantly positioning themselves in this arena of frames. From drawing up a national action plan, to being reachable on the phone, and adopting comprehensible use of language on a website, embodying the social practice open government for executive agencies is anything but uniform. Practitioners and researchers should consider these diverse perspectives when defining or shaping policy on open government.

Footnotes

Funding

This research was partly funded by the Dutch Tax Administration as part of the Strategic Knowledge and Innovation Agenda (SKIA) research programme, within the project “Openheid gewenst” (“Openness Desired”). The project aimed to explore perspectives on openness in relation to the Dutch Tax Administration.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author Biography

Appendix 1: Overview of Actors,Documents and Search Strategy

For this study, we purposefully selected documents representing a diverse range of societal actors. This outside-in approach aligns with prior research emphasizing that open government is a socially co-produced concept shaped by competing expectations and institutional pressures. By integrating sources beyond internal governmental documentation—such as media commentary, political debates, and civil society reports—we aimed to capture the broader societal discourse that would serve as the basis of our frame construction.