Abstract

Objectives. Evaluate the health impact of a novel financial education and coaching program in single mothers of low-income in Omaha, Nebraska. Methods. Employed, single mothers earning no more than 200% of the 2017 Federal Poverty Level (n = 345) enrolled in the study between April 2017 and August 2020 and were randomized to receive a novel financial education and coaching program, the Financial Success Program (FSP) or no intervention control. Demographics, biometrics, financial strain, health behaviors and healthcare utilization were assessed at baseline and the 12-month study visits. Results. Participants who completed the FSP demonstrated significantly reduced financial strain, an increased rate of smoking cessation, and a reduction in avoidance of medical care due to cost compared to participants in the control group. Conclusions. The FSP represents an effective model in promoting economic stability in vulnerable individuals through a reduction in financial strain. Health behavior changes including an increased rate of smoking cessation were demonstrated within the first 12 months of intervention.

“…The current study highlights the effectiveness of a novel financial education and coaching intervention in addressing financial stability determinants of health.…”

Introduction

Extensive evidence indicates financially disadvantaged individuals have poorer health outcomes than their advantaged counterparts.1-3 The relationship between socioeconomic status (SES) and health is multifactorial. SES is often defined using wealth or income. Higher wealth and income can lead to better health by providing material benefits that promote good health: safe homes and neighborhoods, healthy foods and places for exercise, transportation, education and ability to afford medical expenses, among others. 4 Yet, a significant part of the inequality in health is not directly explained by wealth or income, but by the psychosocial stress associated with material resources, or lack thereof. 5

Persistent stress, even at low levels, can lead to chronic disease. 6 The idea of “allostatic load” helps explain this finding.7,8 Allostatic load refers to the wear and tear on an organism that eventually results in compromised resistance to illness and disease. Chronic financial strain, or the persistent struggle to meet daily challenges with inadequate resources, triggers biological cascades (inflammatory and immune dysregulating) that potentiate chronic disease.8,9 Research suggests this wear and tear originates as a result of circumstances experienced well in advance of the morbidity and mortality that become evident at mid-late life and persistent, unrelenting financial strain accumulated over the life course is more strongly associated with poor health outcomes than episodic or transient financial strain.5,10

Financial strain also plays a role in the uptake of healthy lifestyle behaviors. Persons experiencing financial stress are more likely to engage in smoking, alcohol consumption, poor diet and reduced exercise. 11 This can be attributed to the idea that financial strain erodes self-control. People of low-income must overcome more urges and make more difficult decisions more often than individuals with higher incomes. This increased regulation of behavior depletes mental function, exhausts self-control, and leads to behaviors that are harmful to health and increase the risk of obesity and chronic disease. 12 Such “bandwidth tax” is also why interventions to promote healthy behaviors in persons of low-income are often less successful.12,13

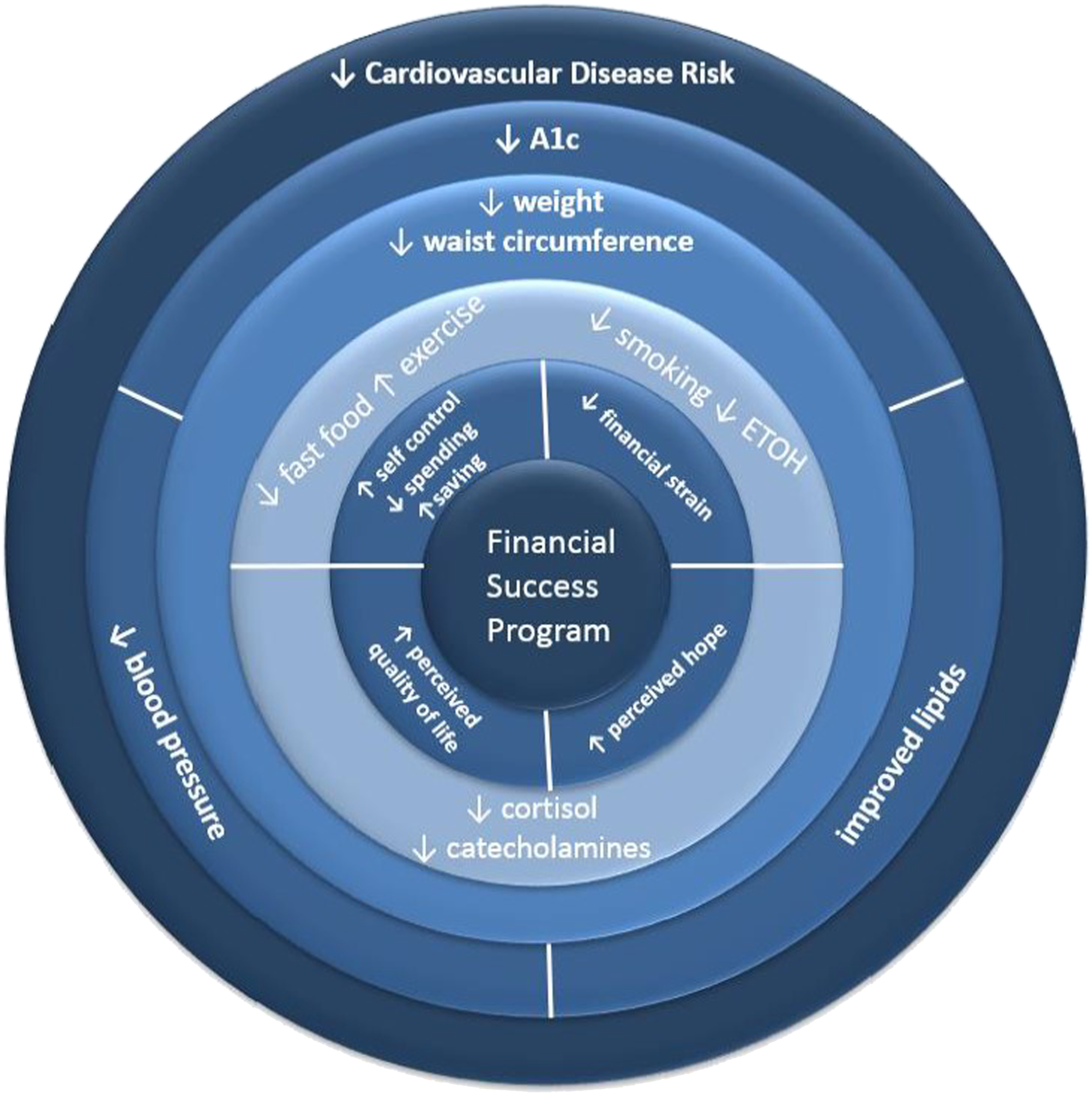

Economic stability is a well-established social determinant of health (SDOH) and financial strain is a key driver of the health inequities observed in persons of low-income. Interventions aimed at reducing financial strain early in the life course may decrease cumulative exposure to allostatic load and alter the health trajectory of the financially disadvantaged. The Financial Success Program (FSP) is a novel financial education and coaching program designed to remove barriers to self-control and reduce stress-related chronic disease risk through improved health behaviors and decreased stress mediators. Figure 1 depicts the conceptual model of effects of the FSP intervention on health.

14

This study sought to assess the effectiveness of the FSP intervention in reducing financial strain and improving health outcomes in single mothers of low-income. To the best of our knowledge, this is the first randomized, controlled trial to examine the impact of financial education and coaching on health. Conceptual model of effect of the financial success program on health.

Methods

The Financial Success Program

The Financial Success Program (FSP) has been operating since 2009 and has demonstrated a consistent track record of promoting durable financial behavior change, reducing financial stress, and improving participant quality of life.15,16 The program was initiated in North Omaha, Nebraska, and enrollment has relied predominantly on word-of-mouth referrals within this tight-knit community. The FSP’s comprehensive model helps families feel connected and supported by training participants to normalize and reframe their financial circumstances into something they feel they can manage and envision themselves as capable of living differently. They take actions to address immediate financial issues, learn and practice skills and behavior changes, and develop decision-making strategies to foster financial confidence. The model’s multiple interactive elements provide ongoing group support; year-long one-on-one financial coaching; and other value-added components that build financial capacity and confidence. The FSP concentrates on 3 core components: an outstanding trainer, financial coaching, and an easy-to-use money management system. The program’s focus on monthly cashflow management and its strategies include education, eliciting emotions, values clarification, pros and cons of making changes, and forming more positive habits to help participants take more effective action to support their financial well-being. The program was offered in English and Spanish and the detailed curriculum has been previously published. 17

Study Design

The Finances First Study, conducted from April 2017 through August 2020, was a randomized, controlled trial to assess the health effects of financial education and coaching (the FSP) in single mothers between the ages of 19 and 55 who were employed, but earned less than 200% of the 2017 US Federal Poverty Guideline; women who spoke English or Spanish were enrolled. Participants were excluded if they were known to be pregnant or planning a pregnancy, currently abusing alcohol or illicit drugs, or living in a domestic violence situation. Participants were recruited on a rolling basis and randomized to the FSP intervention or no intervention control. An equal allocation randomization schedule was created prior to enrollment; however, because the FSP is an existing program with over 10 years of recruitment primarily via word of mouth, women who enrolled in the study upon referral from another participant were assigned to the same group (FSP or control) to which the referrer was randomized. Although a threat to internal validity, this was done to limit contamination of control participants who might receive financial education/coaching indirectly from their FSP-assigned referrer. A total of 20 women referred one or more relatives, friends, and/or coworkers resulting in 32 women enrolling in this study via referral, of whom 27 received the FSP. The referrer–referee relationship was accounted for in the statistical analysis when possible.

Intervention

Participants randomized to the FSP received nine weeks of financial education and 12 months of one-on-one financial coaching. Participants randomized to the no intervention control group were seen at 2 study visits—one at baseline and another 12 months later. The control group received no formal financial education or coaching during the 12-month follow-up. Given the consistently documented success of the FSP, participants randomized to the control group were offered the opportunity to enroll in the FSP after study completion; note that only data collected during their time in the control group was used for this analysis.

Endpoints and Power Analysis

The primary endpoint for the study was the proportion of overweight and obese women that achieved a ≥5% weight loss from baseline; secondary endpoints included tobacco use, healthcare utilization, and financial strain. Based on pilot data, we expected that 30% of participants in the control group would show ≥5% reduction in body weight and hypothesized that women in intervention would be twice as likely to have ≥5% reduction in body weight compared to women in the control group (i.e., relative risk = 2). 18 We estimated that 123 women per group (or 246 women total) would be required to achieve 80% power using two-sided alpha of .05. Considering the pilot study showed approximately 70% of women were overweight or obese at baseline (i.e., needed to lose weight) alongside a conservative FSP completion rate of 80%, we estimated that 440 women would need to be enrolled (or 220 in each cohort) to maintain sufficient statistical power. That said, due to the COVID-19 pandemic, we could not enroll the number of participants required per the a priori power analysis and our final sample consisted of 345 women, of whom 184 received the FSP and 161 were control.

Data Collection

This study was approved by the Institutional Review Board at Creighton University (InfoEd record number: 1011656). Written informed consent was obtained prior to the intervention and participants were seen by study investigators at baseline and at 12 months. Demographics and biometrics including height, weight, BMI, blood pressure, hemoglobin A1c (A1c), and a non-fasting lipid panel, were obtained at the initial and 12-month visit. Two questionnaires were used to measure financial stress at the initial and 12-month visit. The first was a program-developed 5-item questionnaire designed to evaluate the impact of financial stress on sleep, health, relationships and ability to work (see Supplemental Materials). The second was the Family Economic Strain Scale (FESS). The FESS is a 13-item questionnaire used to assess perceived economic strain in both one-parent and two-parent families. The scale provides a composite score; higher scores indicate less perceived economic strain. 19 Due to the COVID-19 pandemic, and in response to a government-required pause on in-person, non-essential research, 12-month visits for participants completing the study after March 2020 were completed by telephone, with an IRB amendment and approval. Therefore, biometric data for these participants could not be obtained.

Statistics Analysis

Data were analyzed in intention-to-treat (ITT), modified ITT (mITT), and per-protocol (PP) analyses. All 3 analyses included all participants randomized to control; as such, between-analysis differences were specific to participants randomized to the FSP. Specifically, the ITT analysis included all participants randomized to the FSP regardless of weeks of completed financial education (including none), the mITT analysis included all participants randomized to the FSP who completed at least 1 financial education class, whereas the PP analysis included participants randomized to the FSP who completed at least 7 of the 9 financial education classes and graduated (i.e., approximately 80% of the intervention). Primary results are based on the ITT analysis.

All descriptive statistics are stratified by group assignment. Depending on data distribution, continuous variables are presented as mean and standard deviation or median and interquartile range. Categorical variables are presented as frequency count and percent. For the primary weight loss outcome, we evaluated the probability of missing the 12-month measurement using a binary indicator for missing data as the outcome and the baseline demographic and clinical characteristics as predictors; no evaluation of missing data was performed for secondary outcomes.

For all analyses, we accounted for the correlation inherent to the referrer–referee relationship using either generalized estimating equations (GEE) or generalized linear mixed models (GLMM). The choice to use GEE vs GLMM was specific to interpretation of the data scale (aka, inverse linked) values given that, for a GEE model, the reported effects represent the (population) average across all participants whereas for a GLMM they are woman-specific (note that when the outcome is conditionally normal, there is no difference between population average and woman-specific interpretations). For both types of statistical models, the choice to account for a two- or three-level sampling structure was dependent on whether the repeated observations from the same woman were included in the analysis (i.e., woman nested within referrer vs observation nested within woman nested within referrer).

To quantify between-group differences in risk of a given binary outcome (i.e., ≥5% reduction in body weight, current tobacco use, and healthcare utilization), we estimated a GEE using the log link, binomial conditional response distribution, and a compound symmetric working covariance matrix. For continuous outcomes (i.e., body weight and FESS), we estimated a GLMM using the identity link and normal conditional response distribution; this model is also known as the linear mixed effects model. For ordinal outcomes (i.e., effects of financial strain), we attempted to estimate a GLMM with the cumulative logit link and multinomial conditional response distribution, but the inclusion of random effects resulted in convergence failures; as such, no random effects were included with between-group differences estimated using the proportional odds model. All analyses were conducted using SAS v. 9.4 (SAS Institute Inc, Cary, NC) was used for all statistical analyses and P < .05 was used to indicate statistical significance.

Results

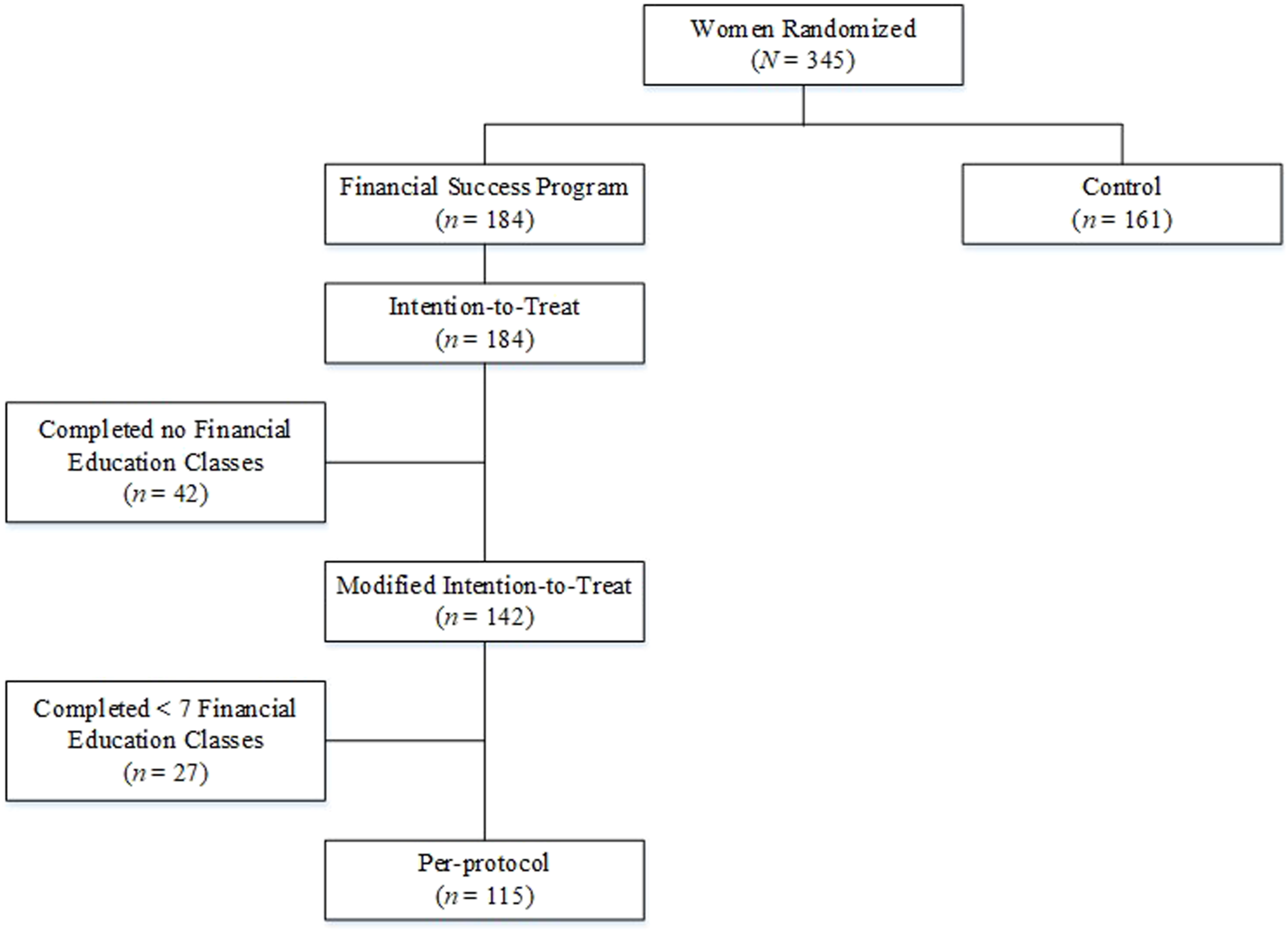

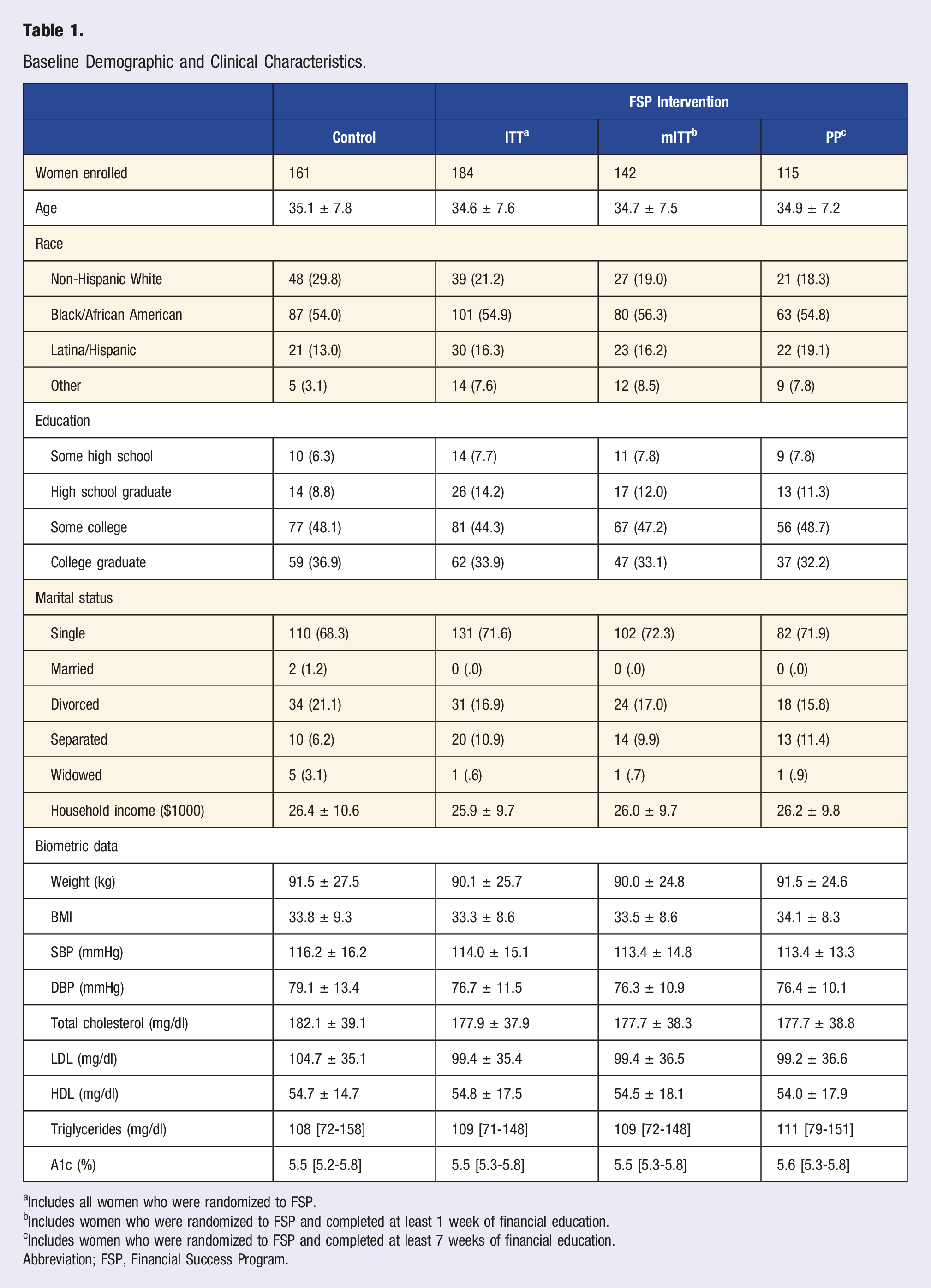

A total of 345 participants were included in the ITT analysis (184 FSP and 161 controls; Figure 2). In participants randomized to FSP, 142 (77.2%) completed between 1 and 6 financial education classes to meet inclusion criteria for the mITT analysis, with 115 (62.5%) completing 7 or more financial education classes to meet inclusion criteria for the PP analysis. Table 1 shows baseline demographic and clinical characteristics. The majority of participants were Black/African American (54.0%), single (68.9%), with at least some college education (85.0%). Study flow diagram. Baseline Demographic and Clinical Characteristics. aIncludes all women who were randomized to FSP. bIncludes women who were randomized to FSP and completed at least 1 week of financial education. cIncludes women who were randomized to FSP and completed at least 7 weeks of financial education. Abbreviation; FSP, Financial Success Program.

Primary Endpoint: Body Weight

At baseline, 286 (82.9%) participants were overweight (20.9%) or obese (62.0%), with statistically similar baseline overweight or obesity rates between the FSP and control participants (83.0% vs 82.6%, respectively; P = .917). A total of 253 participants had a 12-month body weight measurement (125 FSP and 128 controls). Of the 92 participants missing that 12-month weight measurement, 41 (23 FSP and 18 controls) were a result of the government-required pause on in-person, non-essential research amid the COVID-19 pandemic, whereas the remaining 51 (36 FSP and 15 controls) were lost to follow-up for other reasons. The probability of missing the 12-month weight measurement was associated with group assignment (32.1% of FSP vs 20.5% of controls; P = .017); no other baseline demographic or clinical characteristics were associated with missing data (see Supplemental Materials).

For overweight or obese participants included in the ITT analysis, a lower but non-statistically significant proportion in the FSP group lost ≥5% of their body weight compared to participants in the control group (10.2% vs 14.0%, respectively; risk ratio [RR]: .73, 95% CI: .34 to 1.54, P = .404); similar results were observed in the mITT (RR: .59, 95% CI: .25 to 1.38, P = .0224) and PP analysis (RR: .71, 95% CI: .31 to 1.62, P = .409). Further, when considering change in body weight as continuous, in overweight or obese participants, increases in body weight were observed both in participants randomized to FSP (change: +1.16 lbs, 95% CI: +.10 to +2.22, P = .032) and participants randomized to control (change: +.70 lbs, 95% CI: −.35 to +1.75, P = .190); the increase in body weight was statistically similar between groups (intervention-by-time interaction P = .542). A similar pattern of results was observed in the mITT analysis (FSP increase: +1.40, 95% CI: +.29 to +2.51, P = .014; intervention-by-time interaction P = .365) and PP analysis (FSP increase: +1.42, 95% CI: +.19 to +2.65, P = .024; intervention-by-time interaction P = .383).

Secondary Endpoints

A total of 294 participants provided 12-month data for tobacco use, healthcare utilization, and financial strain scores (148 FSP and 146 controls). The increase in 12-month observations compared to observations for the biometric data was due to the ability to collect these data over the phone.

Financial Strain

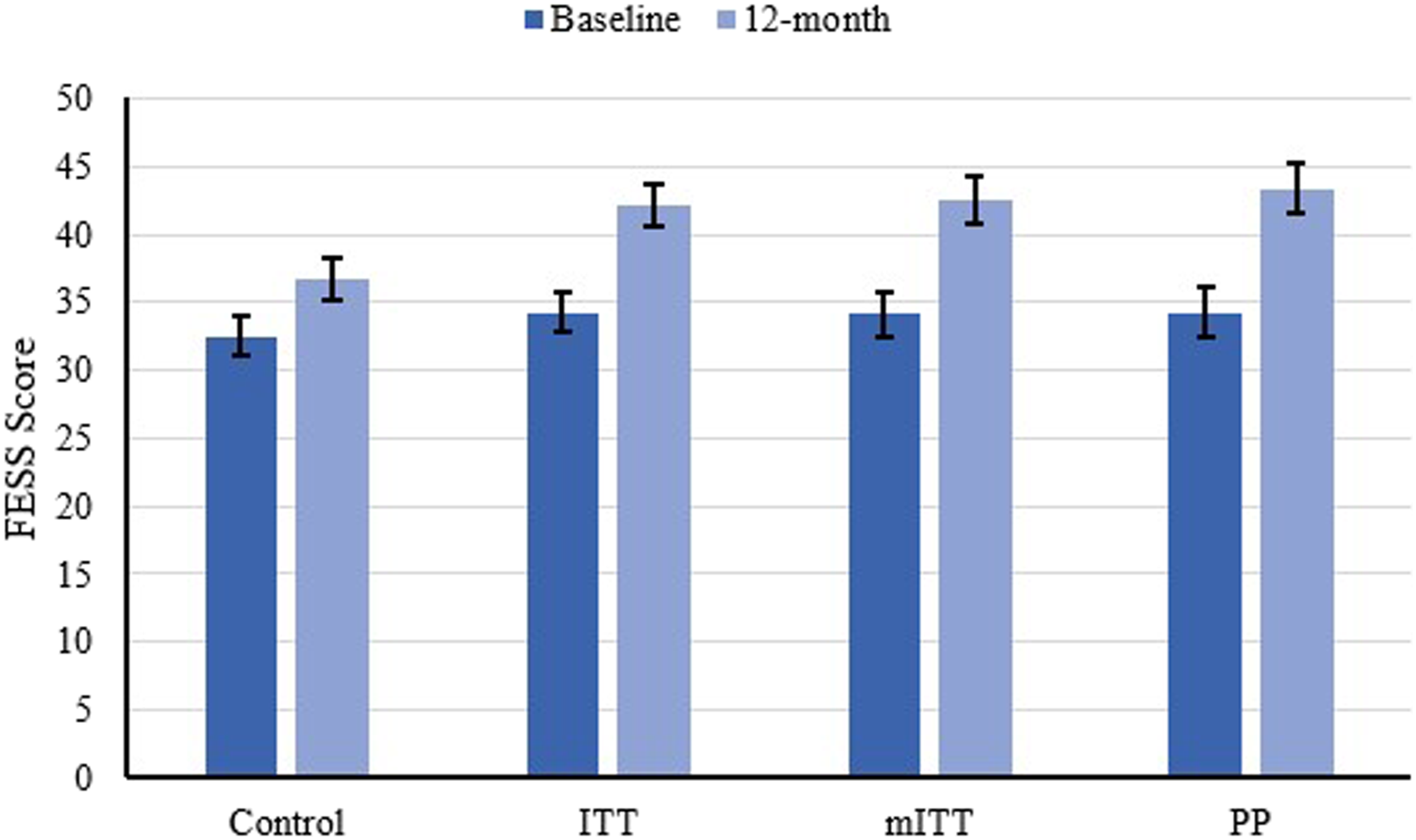

In the ITT analysis, no statistically significant differences in FESS scores at baseline were observed between FSP and control participants (34.24 vs 32.53, respectively; mean difference: 1.70, 95% CI: −.41 to 3.82, P = .113; Figure 3). Statistically significant increases in FESS scores (indicating less perceived stress) were demonstrated by those randomized to the FSP (mean change: 7.83, 95% CI: 6.38 to 9.28, P < .001) as well as participants randomized to control (mean change: 4.16, 95% CI: 2.67 to 5.64, P < .001), with participants randomized to the FSP experiencing significantly greater change (change difference: 3.67, 95% CI: 1.60 to 5.75, P < .001; Figure 3). Slightly larger between-group differences in change were observed in the mITT (change difference: 4.24, 95% CI: 2.07 to 6.40, P < .001) and PP analysis (change difference: 4.98, 95% CI: 2.72 to 7.25, P < .001). Estimated FESS score at baseline and the 12-month measurement. Error bars represent 95% confidence intervals ITT included all women randomized to the FSP. mITT included all women randomized to the FSP who completed at least 1 week of financial education. PP included all women randomized to the FSP who completed at least 7 weeks of financial education. Note. FSP, Financial Success Program; FESS, Family Economic Strain Scale.

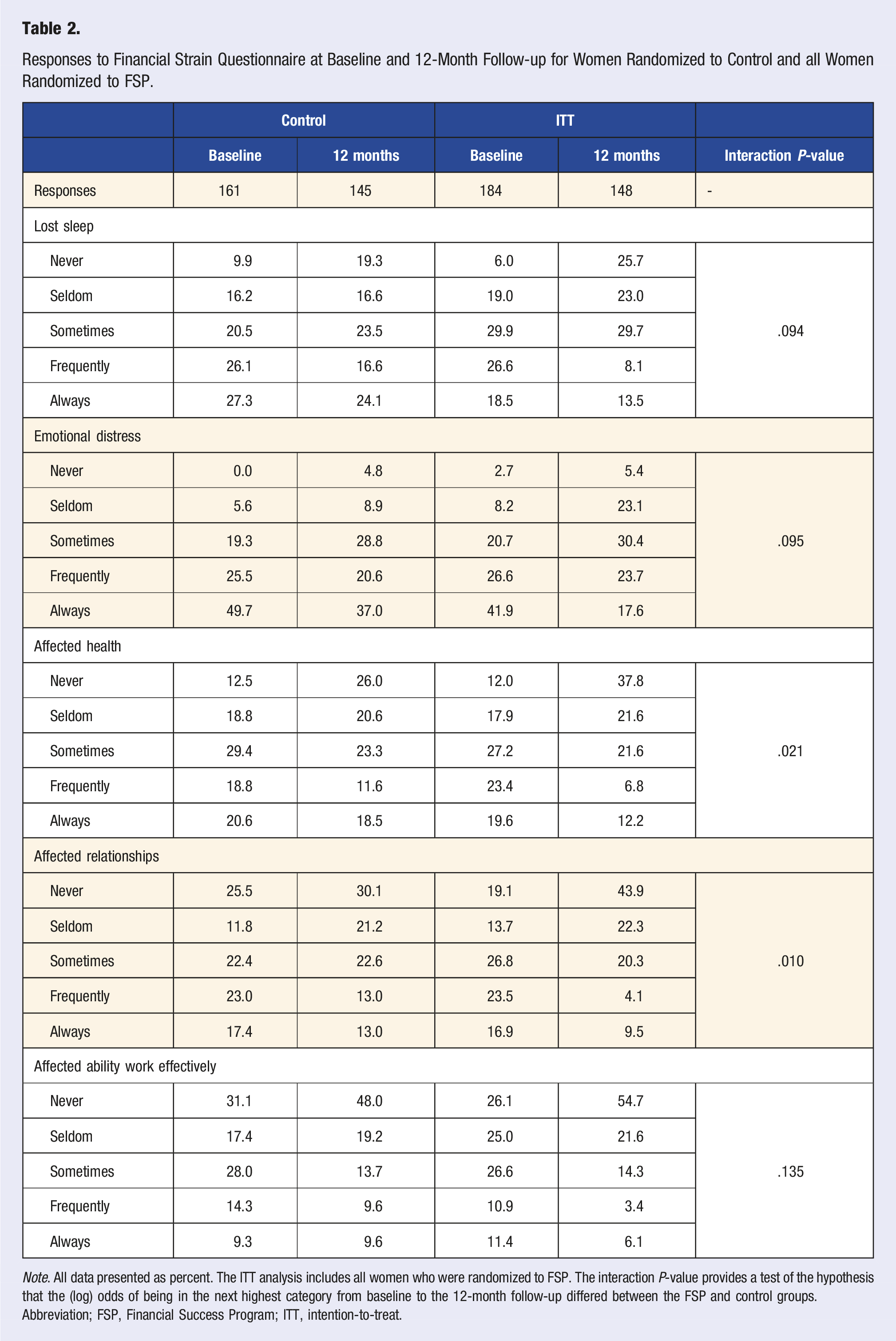

Responses to Financial Strain Questionnaire at Baseline and 12-Month Follow-up for Women Randomized to Control and all Women Randomized to FSP.

Note. All data presented as percent. The ITT analysis includes all women who were randomized to FSP. The interaction P-value provides a test of the hypothesis that the (log) odds of being in the next highest category from baseline to the 12-month follow-up differed between the FSP and control groups.

Abbreviation; FSP, Financial Success Program; ITT, intention-to-treat.

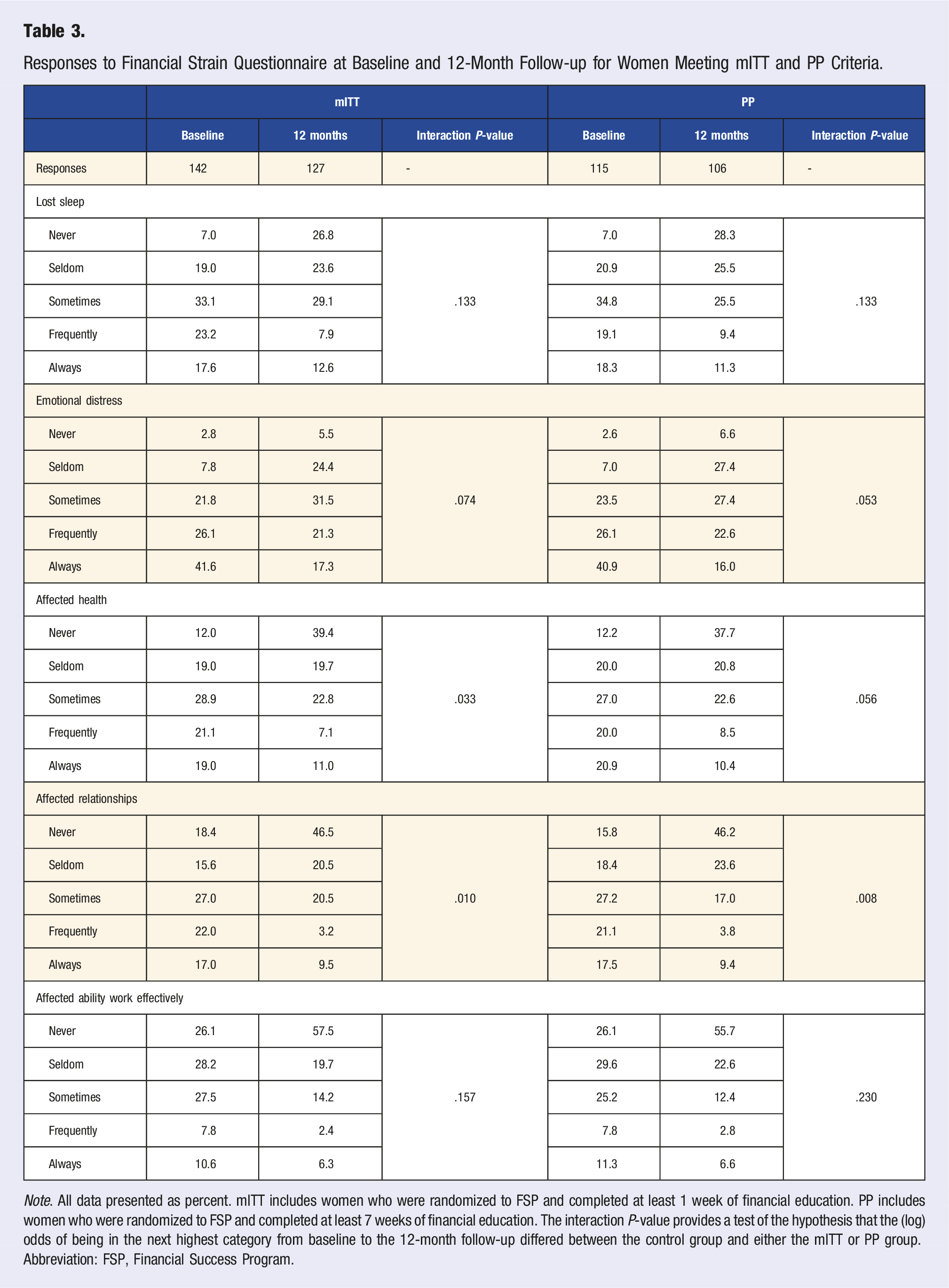

Responses to Financial Strain Questionnaire at Baseline and 12-Month Follow-up for Women Meeting mITT and PP Criteria.

Note. All data presented as percent. mITT includes women who were randomized to FSP and completed at least 1 week of financial education. PP includes women who were randomized to FSP and completed at least 7 weeks of financial education. The interaction P-value provides a test of the hypothesis that the (log) odds of being in the next highest category from baseline to the 12-month follow-up differed between the control group and either the mITT or PP group.

Abbreviation: FSP, Financial Success Program.

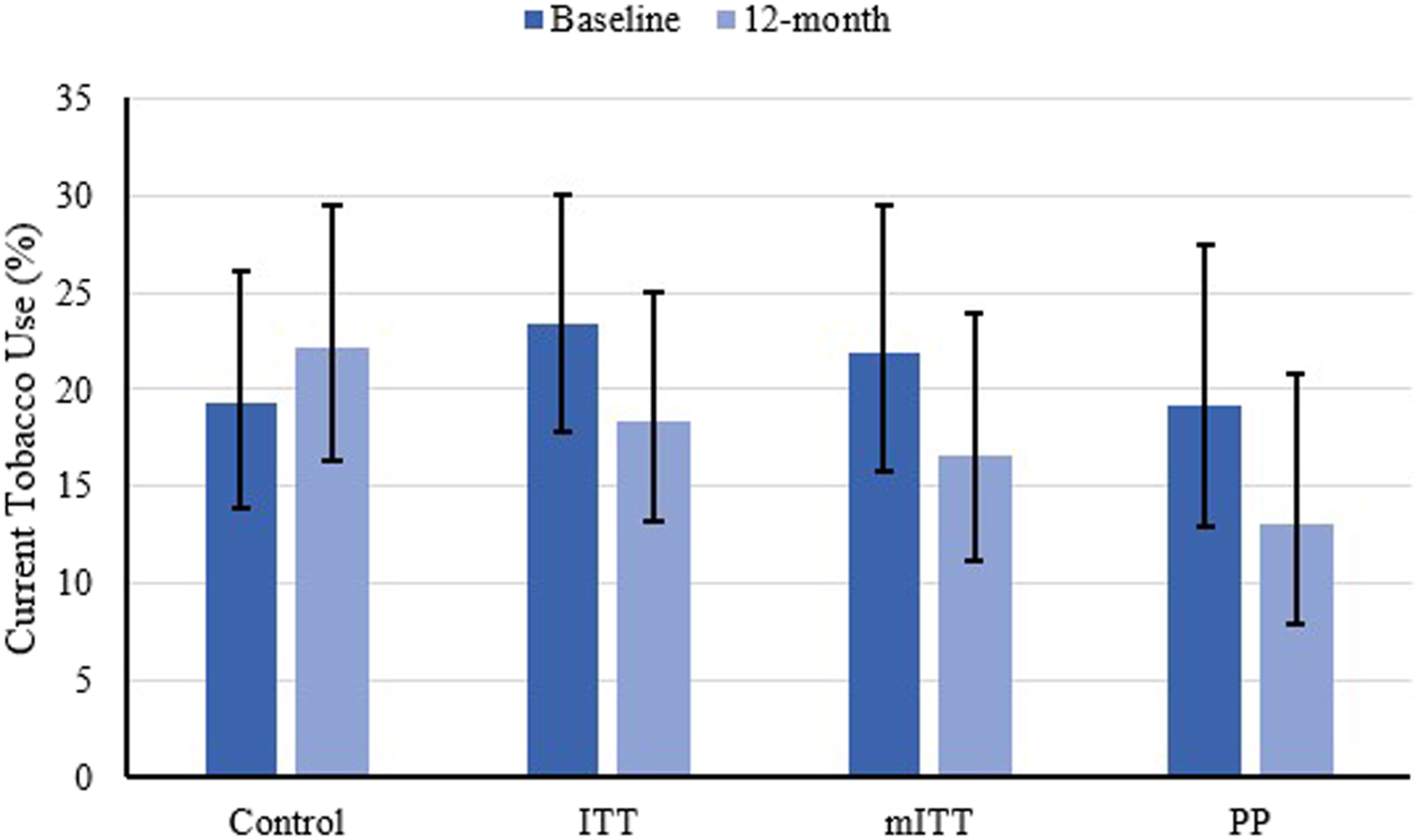

Tobacco Use

In the ITT analysis, the rate of participants who reported current tobacco use at baseline was statistically similar between those randomized to FSP or control (23.4% vs 19.3%, P = .605; Figure 4). At 12-month follow-up, participants randomized to the FSP had reduced their tobacco use to 18.3% (RR: .74, 95% CI: .56 to .96, P = .025), whereas those in the control group reported an increased rate of tobacco use to 22.2% (RR: 1.19, 95% CI: .91 to 1.56, P = .193); the difference in change between participants in the FSP and control groups was statistically significant (intervention-by-time interaction P = .013). Slightly larger reductions in tobacco use were observed in the mITT analysis (FSP RR: .71, 95% CI: .53 to .96, P = .027; intervention-by-time P = .012) and PP analysis (FSP RR: .64, 95% CI: .44 to .93, P = .020; intervention-by-time P = .010). Estimated percent of women who reported current tobacco use at baseline and at the 12-month measurement. Error bars represent 95% confidence intervals.

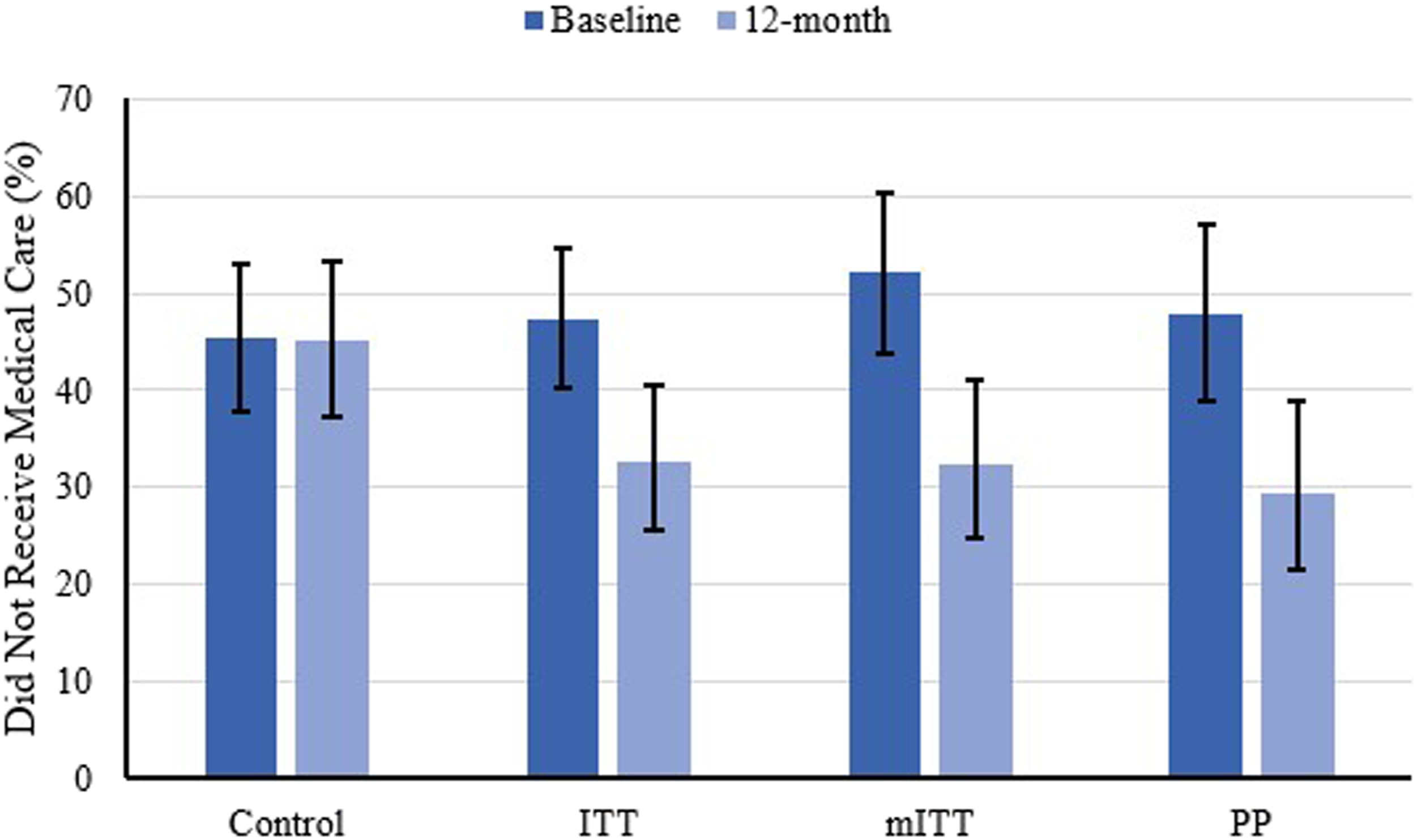

Healthcare Utilization

In the ITT analysis, the rate of participants who reported failing to seek medical care due to cost at baseline was statistically similar between those randomized to FSP or control (49.0% vs 45.5%, P = .529; Figure 5). At 12-month follow-up, participants randomized to the FSP reduced their avoidance of medical care due to cost to 32.6% (relative risk [RR]: .54, 95% CI: .37 to .80, P = .002), whereas those in the control group remained mostly unchanged at 45.1% (RR: .99, 95% CI: .67 to 1.46, P = .966); the difference in change between participants in the FSP and control groups was statistically significant (intervention-by-time interaction P = .030). Larger reductions were observed in the mITT analysis (FSP RR: .44, 95% CI: .29 to .67, P < .001; intervention-by-time P = .005) and PP analysis (FSP RR: .45, 95% CI: .28 to .73, P = .001; intervention-by-time P = .014). Estimated percent of women who reported avoiding medical care due to cost at baseline and at the 12-month measurement. Error bars represent 95% confidence intervals. Abbreviations: ITT, intention-totreat; mITT, modified ITT; PP, per-protocol.

Discussion

In this study, financial education and coaching was not associated with a significant reduction in body weight in overweight or obese participants in the first 12 months of follow-up. As discussed previously, this finding is limited by the inability to enroll the number of women required per the a priori power analysis and the lack of 12-month body weight data for those participants who completed the study during the COVID-19 pandemic via telephone interview. It has been shown in both Nurses’ Health Studies that women gain an average of 3.35 pounds every 4 years. 20 Data from the Behavioral Risk Factor Surveillance System similarly showed a gain of .7 pounds per year. 21 Because the FSP is a 12-month intervention it could be that the impact of the programming on body weight is not realized in the first year. This hypothesis is supported by pilot data, which found that despite no statistically significant reductions in body weight, 50% of women who completed the FSP lost weight after 2 years, with an average weight loss of 2.2 pounds. 16

Although changes in biometric data were not demonstrated in the current study, research suggests these health inequities are a result of circumstances experienced well in advance of the morbidity and mortality that become evident at mid-late life.5,10 A more proximal finding of the current study, was the significantly reduced perceived financial strain. This outcome in and of itself has promise in potentially reducing the disproportionate incidence of chronic disease seen in low SES groups. Data from the National Longitudinal Survey of Mature Women found exposure to any financial strain over the life course increases risk for poor health, but the risk was greatest in women who faced long, unrelenting spells of financial strain. 5 The study authors concluded even temporary relief from financial strain is beneficial to women’s health. This is further supported by a second study that demonstrated persistent financial hardship was a more significant driver of poor health than its episodic occurrence and the health effects of early hardship may be obviated if followed by no further strain. 10 Of particular interest, the study found the association of financial strain and poor health in late-adulthood increases when financial strains are present between the ages of 35–50 and that financial hardship experienced prior to age 35 has an effect on late life health only when it is followed by additional hardship after age 35. 10 The average age in the current study is about 35, suggesting this is a pivotal time in the life course to address financial strain.

Women who completed the FSP reported a reduction in the effect of finances on health and a reduction in allowing finances to affect their relationships. These findings are noteworthy as a supportive social network, when lacking, has been shown not only to cause stress, but to predict how individuals experience and cope with stress. 22 One of the hypothesized pathways of financial strain deteriorating health is through loss of supportive social relationships and family tension. 10 Social support has been shown to reduce stress, improve health and decrease mortality risk. 22 Perhaps participation in the FSP, mediated through a reduction in financial stress, results in enhanced social support, which reduce further stress proliferation and potentiates good health.

Although research indicates an independent effect of financial strain on health above and beyond reported financial resources, participation in the FSP has also been shown to significantly increase income compared to control and at a rate greater than projected mean salary increases for 2020.23,24 Interestingly, the improvements in income and financial stress were observed in women who participated in the FSP during the COVID-19 pandemic. 23 A sub-analysis of 40 women who completed their 12-month follow-up during the pandemic found that in contrast to women randomized to control, women in the FSP experienced fewer job losses and an increase in median salary and ability to save. These factors likely influenced the reduction in perceived financial stress demonstrated by the women in the FSP. Possibly through the financial education, available resources, and coaching, these participants were better equipped to adapt to adversity and demonstrate resiliency despite the pandemic.

In addition to reductions in financial strain, participation in the FSP significantly increased the proportion of women who quit smoking during the 12-month follow-up in the absence of formal smoking cessation education/intervention within the FSP. This finding is particularly impressive as low-SES smokers are less likely to successfully quit smoking than their higher SES counterparts and also more likely to relapse.25,26 These studies highlight the benefit of addressing financial strain in tobacco cessation interventions with vulnerable populations. The notion of scarcity holds that decision-making capacity and self-control erode when financial resources are under strain. Interventions to reduce financial strain may preserve smokers’ self-control reserves and enable them to make healthier lifestyle decisions like smoking cessation. 12 Additionally, tracking the expense of smoking as a part of the FSP intervention may have led to greater awareness of the financial implications of tobacco use, further supporting cessation.

An American Journal of Public Health editorial on the social determinants of health equity identified “lifestyle drift” as a significant barrier to acting on the social determinants of health to address health equity. Lifestyle drift is the tendency in public health to focus on personal behaviors (smoking, healthy eating, physical activity) without considering the drivers of these behaviors (the causes of the causes). 27 Addressing finances first, an upstream cause of unhealthy behaviors, may lead to expanded capacity to engage in healthy lifestyles. The FSP focuses on helping single mothers move from resigned acceptance of chronic financial struggles to envisioning a better future for themselves and their families. Improved monthly cashflow management and other future-oriented actions lead to healthier lifestyle behaviors as financial stress levels decrease. Although greater awareness of the financial implications of tobacco use were salient to their decision-making, their increased sense of empowerment and hope from achieving financial goals likely underpinned their health-related behavioral changes.

Access to medical care is a significant concern for people of low-income. In 2019, data from the National Health Interview Survey found that 17.7% of American adults with incomes below 200% of the federal poverty level reported delaying and/or going without medical care due to cost. 28 This finding is significantly lower than the more than 40% of women in the current study who, at baseline, reported avoiding medical care in the past year due to cost. Women who participated in the FSP reported a reduction in the financial barriers to healthcare access. This may be important in preventing and managing chronic disease and reducing unnecessary disability and premature mortality.

The current study involved several strengths as well as limitations. As mentioned, this was the first study, to our knowledge, to evaluate the health effects of a financial education and coaching intervention using a randomized, controlled trial. Other strengths include the use of a survey tool to assess perceived financial strain that has consistent validity evidence as well as our inclusion of a significant proportion of Black/African American and Latina/Hispanic participants.

An unfortunate limitation of the study relates to a change in collected data as a result of the COVID-19 pandemic. In March 2020, in response to a halt in non-essential clinical research, the US Food and Drug Administration (FDA) issued guidance for the conduct of clinical trials during the pandemic. 29 In lieu of a clinic visit, the Finances First study investigators conducted final follow-up visits between May 8, 2020 and July 29, 2020 by telephone. As a result, biometric assessments including weight, blood pressure, A1c, and lipid panel were not obtained for the last 41 women to complete the study. Although many participants had access to a scale at home or other means to obtain body weight, in an effort to eliminate measurement error or questionable truth, investigators opted to exclude any 12-month data that was not obtained by an investigator using calibrated equipment. While the COVID-19 pandemic presented a barrier to the study visits, the FSP classes and financial coaching continued without pause. The FSP classes were delivered via Zoom and coaching visits occurred over the phone, via email or using a video conference platform.

A second limitation was the self-reported nature of the smoking cessation as urine or salivary cotinine was not collected to confirm objectively that participants had truly quit. Last, based on a history of participants sharing knowledge from the FSP with their friends and family, we modified the randomization schedule to ensure women enrolled to control were not indirectly receiving financial education or coaching from a participant assigned to the FSP group.

Results from the current study highlight the effectiveness of a novel financial education and coaching intervention in addressing financial stability determinants of health. More research is needed to determine the long-term impact of the FSP, particularly as it relates to health trajectory and chronic disease risk mitigation. A 20-year prospective longitudinal study evaluating chronic disease prevalence in women who completed the Finances First study is currently underway. Additionally, research on the cost effectiveness of the intervention is also needed.

Trial Registration Statement

This study was approved as by the Institutional Review Board at Creighton University (InfoEd record number: 1011656). This study was performed in accordance with the ethical standards as laid down in the 1964 Declaration of Helsinki and its later amendments. This trial was registered at clinicaltrials. gov: https://clinicaltrials.gov/ct2/show/NCT03035240.

Supplemental Material

sj-pdf-1-ajl-10.1177_15598276211069537 – Supplemental Material for Improving Health through Action on Economic Stability: Results of the Finances First Randomized Controlled Trial of Financial Education and Coaching in Single Mothers of Low-Income

Supplement Material, sj-pdf-1-ajl-10.1177_15598276211069537 for Improving Health through Action on Economic Stability: Results of the Finances First Randomized Controlled Trial of Financial Education and Coaching in Single Mothers of Low-Income by Nicole White, Kathleen Packard, Ann Ryan Haddad, Kathy Flecky, Jennifer Furze, Lisa Black, Julie Peterson, Julie Kalkowski, Ryan Walters and Lorraine Rusch in American Journal of Lifestyle Medicine

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by a Robert Wood Johnson Foundation Pioneering Idea Grant, the Nebraska Tobacco Settlement Biomedical Research Development Fund, the Sherwood Foundation, the William and Ruth Scott Family Foundation, the Weitz Family Foundation, Centris Federal Credit Union, the Peter Kiewit Foundation, First National Bank of Omaha, Mutual of Omaha Foundation, and the Sokolof Foundation.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.