Abstract

A majority of Americans have health care insurance through their employers, the cost for which is rising at an alarming rate. Unfortunately, higher expenditure on insurance has not translated into healthier employees. In this article, we present a value-based design plan for self-funded employers, administered by lifestyle medicine board-certified providers, which is purported to save money for employers and yet may demonstrate better health outcomes for employees by engaging them in evidence-based lifestyle interventions such as plant-based nutrition, regular physical activity and minimizing sedentary behaviors, sleeping well, tobacco cessation, and so on.

Keywords

‘Employers are finding that the cost to provide insurance coverage has escalated at a much higher rate than inflation . . .’

Introduction: The Health Care Crisis

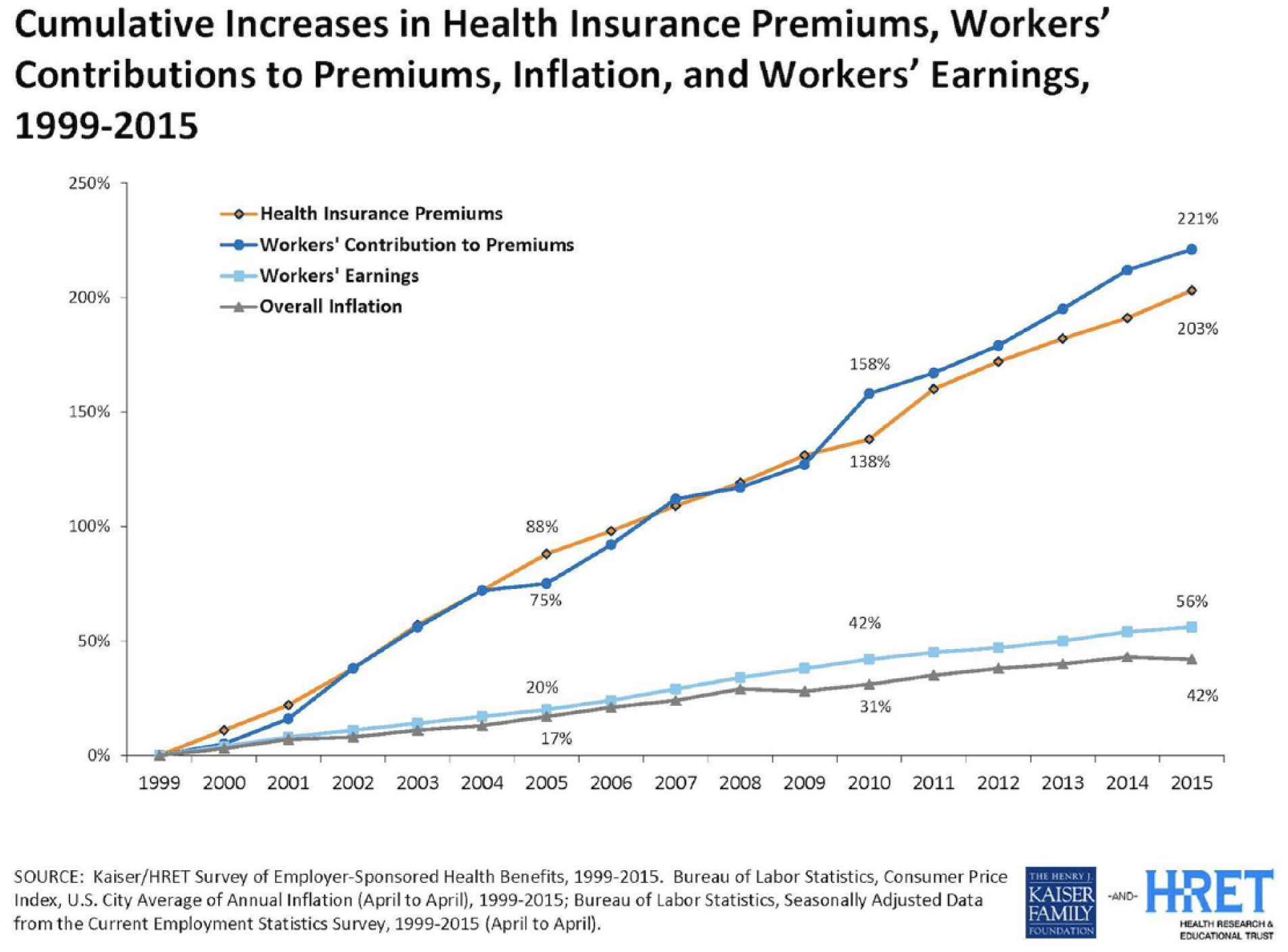

There is no arguing that the modern US health care system is in dire need of reform. A majority of Americans have health care insurance through their employers. 1 Employers are finding that the cost to provide insurance coverage has escalated at a much higher rate than inflation and has therefore limited their ability to provide raises or increase their workforce. Furthermore, we have seen little change in terms of policy that has affected the demand on the health care system or the employer’s budget (Figure 1). 2

Medical and Work Compensation Premium, Employee Earning and Inflation Increases since 1999.

Delaying a Stitch in Time Costs Nine

The current efforts to reform health care are more like shifting the chairs on the Titanic. Some key efforts, like creating a high deductible plan with an accompanying HSA, were implemented as early as 2003. The high deductible health plans were introduced to help create more consumerism, with the belief that shifting costs to the consumer will drive the consumer to take more ownership in their health care costs and indirectly influence their overall health outcomes. 3 Current emphasis in the health market focuses on post-disease occurrence and not enough on how to create a more cost-efficient approach to provide resources for preventative needs.

Any attempt to create consumerism by increasing deductibles may have instead increased barriers to timely care. These efforts may initially show a decrease in medical spending, but the spending decrease is most likely due to a decline in utilization and can create a larger longitudinal dependence on the health care system. 4

Less Health, More Cost

While this may seem obvious, we must make the case to employers first that improved health is critical to decrease medical spending and dependence on the health care system. If an employer is going to improve their health care spending, they must focus on keeping the healthy people healthy, and reversing chronic disease early in its course (“prevention is better than cure”). Since approximately 20% of US adolescents are currently obese, 5 it is estimated that by 2050, more than 1 in 3 adults will have type 2 diabetes. 6 Compare this with the current rate of diabetes, which is 1 in 11 people, from 2015. 7 In Vital Incite’s pool of just under 19 000 persons with diabetes, we found that a person with diabetes costs about $10 000 more per year than someone without the condition. This is consistent with national statistics, which estimate that in people with diabetes, an average $9600 is attributed to diabetes medical expenditures alone. 8 In addition, in our data, we find only 27% of employees are at a healthy weight, and in fact, 22% are morbidly obese and 21% are obese. This is again consistent with national data, that is, 39.8% of all American adults are obese. 9 The medical cost for people who have obesity was $1429 higher than those of normal weight. 9 Furthermore, as of now, 1 in 3 American adults are living with prediabetes. 10 The distance between prediabetes and overt type 2 diabetes is a mere 5 pounds and/or 5 years (ie, on an average, if a patient with prediabetes gains 5 pounds or ages by 5 years without implementing any therapeutic lifestyle changes, they are likely to transition to overt type 2 diabetes). Since prediabetes converts to type 2 diabetes at the rate of 9% per year, 11 reducing its prevalence by addressing obesity will do far more to reduce the total cost of health care than focusing on diabetes treatment alone. 12

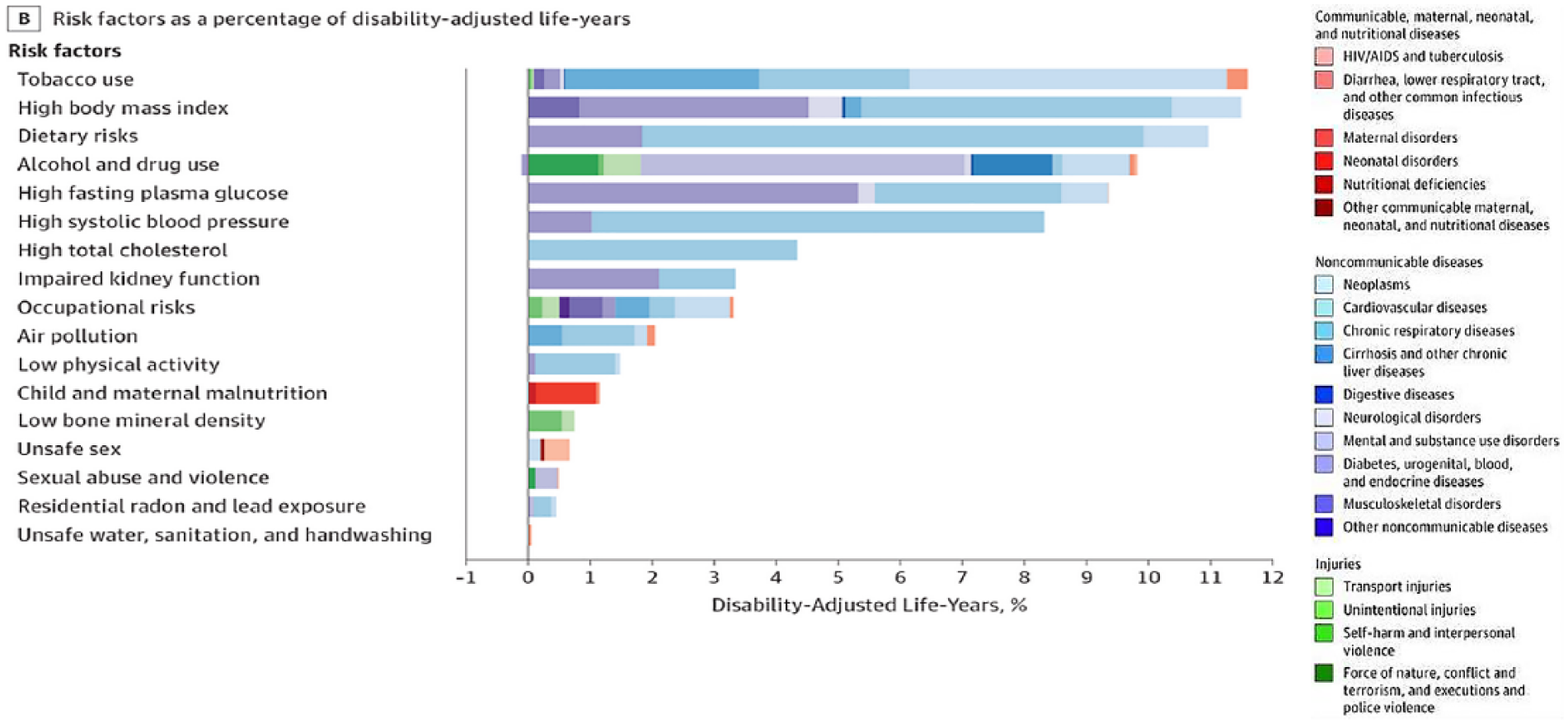

In the “State of US Health” report, high body mass and dietary risks are noted as the second and third highest risk factors affecting disability (Figure 2). 13

State of US Health report.

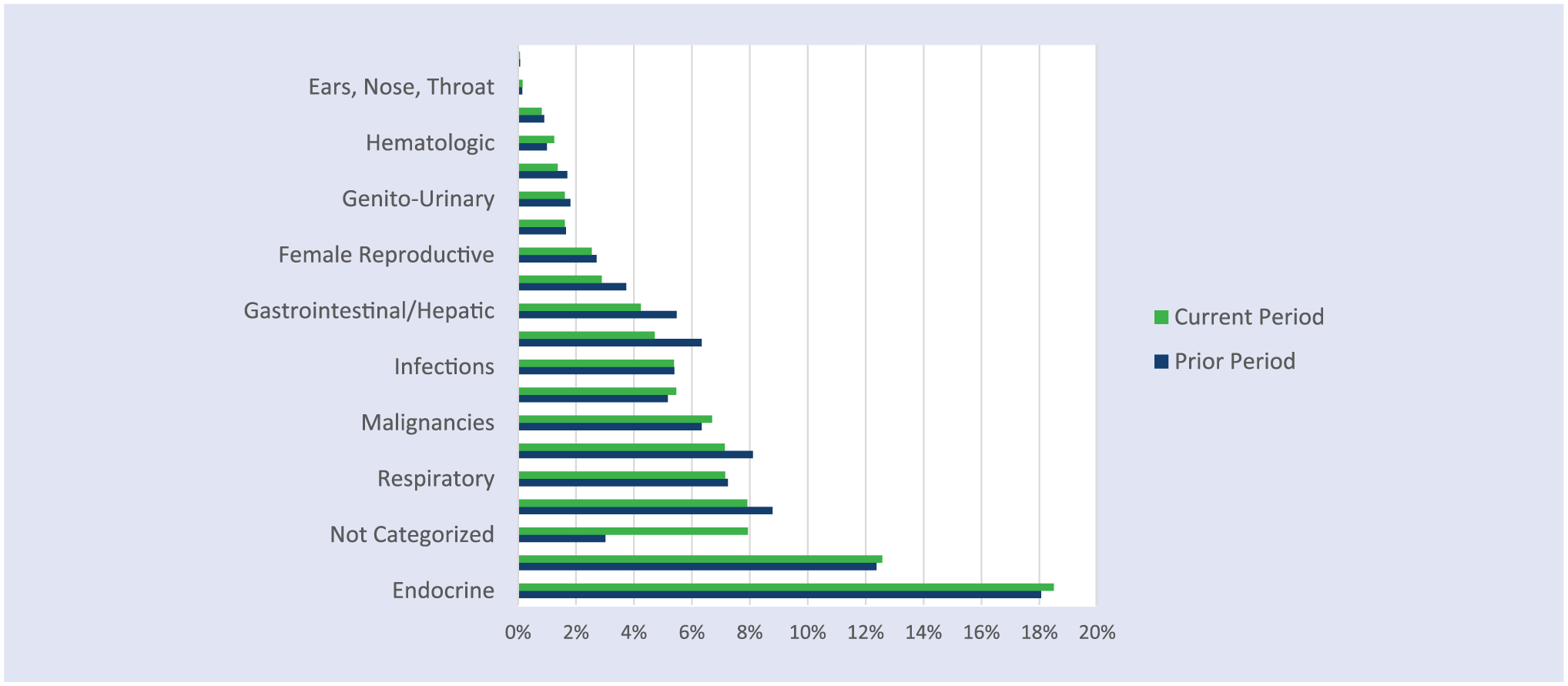

Furthermore, in Vital Incite data, we see that the top drug-related expense in 2018 is coming from endocrine disease, and we know that chief among those diseases is diabetes, with an estimated 90% to 95% of diabetics being type 2 diabetic. This is very much in sync with national statistics, which estimate that of the $329 billion spent annually on the cost of prescription drugs, almost one third ($107 billion) is diabetes drug costs (Figure 3). 14

Total Drug Spend 2017-2018 by Disease Category.

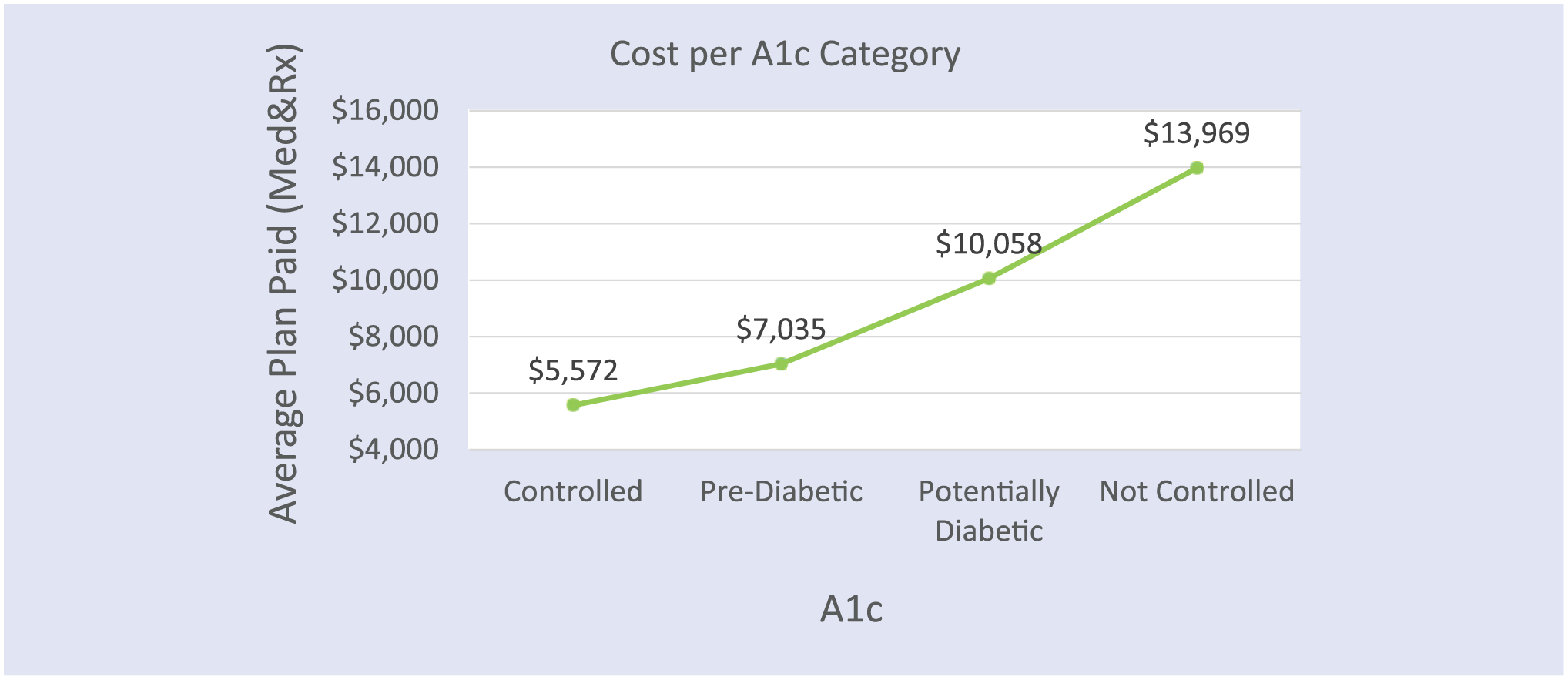

There is a clear correlation between cost, A1c control, and weight, and we find in our data that every increase in body mass index (BMI) category accounts for about $800 more in medical spending for the health plan (or employer) per person per year. When examining the correlation between A1c control and cost, we find that as persons move to less controlled A1c values, their cost incrementally increases as well (Figure 4). This is corroborated from findings garnered by other national-level data sets as well.15,16

Incremental Increase in Plan Spend in Relation to A1c Control.

Value-Based Plan Designs

The irony behind the development of value-based insurance plan designs is that key strategic decisions have been made between the carriers, hospital systems, and the benefit advisors. Providers, especially in independent practices, are not connected to any strategic development and therefore their best interests may not be considered. Essentially, there are 3 main groups paying for health care: the patient, the employer, and the insurance carrier. If the patient has medical insurance, the patient is responsible for the amount that the insurance plan does not cover. The share that is paid by either the employer or the insurance company is dependent on whether the employer is self or fully funded, which a company chooses for itself. In a fully funded account, the carrier takes on the risk of the plan. The employer pays only a prenegotiated monthly rate for their premium and the carrier takes on the risk and responsibility for the total amount due. In the United States, approximately 39% of employers are fully funded. 17 Typically, smaller employers are more likely to be fully funded, but the threshold for the size of these employer groups vary by state. The most progressive self-funded state is Indiana, with more than 70% of employers being self-funded. 18

In 2016, 40.7% of private sector employers reported that they self-insured at least one of their health plans, up from 29.7% in 2000, the Employee Benefit Research Institute reported in February 2018.

From 2013 to 2016, the percentage of employers by size that offered at least one self-insured plan changed as follows:

Small employers (fewer than 100 employees)—rose to 17.4%, up from 13.3%.

Midsize employers (100 to 499 employees)—rose to 29.2%, up from 25.3%.

Large employers (500 or more employees)—fell to 78.5% from 83.9%.

An employer determines if they will be fully funded or self-funded based on the administrative cost differences, their members’ health care risk, and the employers’ ability to take on the risk of a potentially high year of medical spending. The value to be self-funded comes from the ability to be more flexible in plan design and less administrative fees. Furthermore, if an employer is self-funded and can improve the health of their members and reduce the demand for medical care use, they reap the rewards in the long run. It is time for lifestyle medicine board-certified professionals to arouse “the sleeping giant that is the self-funded employee health benefits market.” 19

Employers’ Understanding of Health and Health Care

For the lifestyle medicine practitioner to make the case for the value of lifestyle medicine to self-funded employers, and initiate collaboration is to help meet them where they are in their understanding of health and health care. Employers are accustomed to viewing reports that show trends in medical spending by cost per unit, overall spending by medical services, and pharmacy costs. They will also typically see carrier reports that illustrate how compliant their covered lives are in taking medications if they have a chronic condition or having their age-related tests and procedures performed. They understand when emergency utilization is high or use of a more expensive drug is affecting cost. They also see and are concerned with the fact that average paid amounts for services are increasing year over year. However, there are little data to actually show employers the root cause of the demand on the health care system or the return of investment for their medication investment. An employer does not see data that show them if the investment in health care is improving the health of their people, but instead is provided data to show the cost of the reaction to declining health.

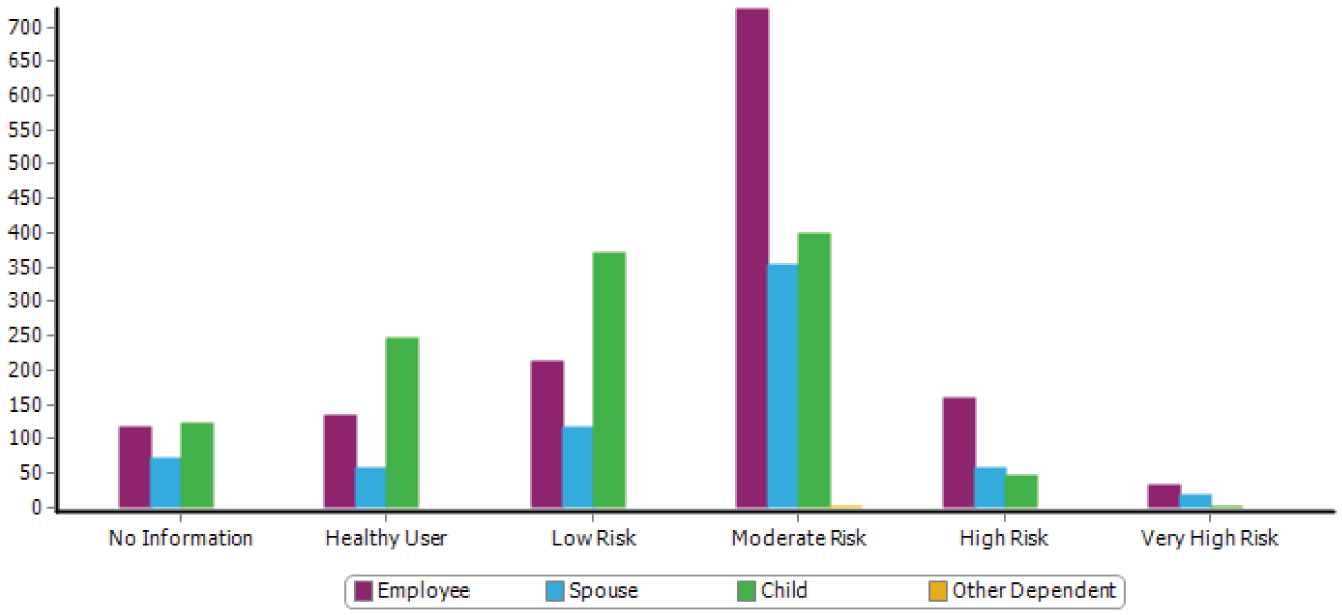

If employers were able to understand root cause and see what is improving health, it is likely they would be making better investment choices. Johns Hopkins ACG system 20 provides an objective view of risk control that helps employers gain insight into the health of their population. By using Resource Utilization Bands (RUB), Johns Hopkins allows us to illustrate which RUB category their members are and the average cost of each of those persons with similarly situated risk. The ACG system places people of similar risk into 6 buckets: persons who have not enough information to identify risk, healthy, low risk, moderate risk, high risk, and very high risk (Figure 5).

Correlation between Employer Cost and ACG (registered) Resource Utilization Band.

Being able to view their population in this structure allows an employer to objectively determine potential cost savings if they were able to improve the control of a person with a chronic condition and move them from a high-risk RUB category to a moderate RUB category. Similarly, the employer also needs to see how important it is to prevent the low-risk people from moving into the high-risk category (or the high-risk people from moving into the very high risk category). Given that one third of our population already has prediabetes, and almost two thirds of workforce is either overweight or obese, this currently so-called “low-moderate” risk population will very soon (but surely) progress to high-risk category (type 2 diabetes or heart disease, etc) if therapeutic lifestyle changes are not implemented. The cost of doing nothing is very high, almost unaffordable!

This objective ACG system view provides the return on investment in real dollars for the employer’s population and creates an insight into the financial impact for interventions such as lifestyle medicine in a simpler way for employers to understand.

It bears mention that this disease progression may indeed affect employees who are otherwise moving up the ladder of work and business experience (eg, a staff who has steadily worked hard over years to be promoted to a senior position, but is now faced with declining health as they grow older, thereby adversely affecting their invaluable skill of experience and job sophistication). It is imperative that employers pay attention to nurturing the health of their employees in the earlier years, so the dividends of experience and skill sophistication can be reaped when the employee ages into a well-deserved higher position.

Leveraging Lifestyle Medicine

Most employers do care about their employees’ health and want to invest in things that are beneficial, but they are frustrated that their efforts are not having a lasting impact. In our data, we found that only 61% of diabetics have controlled A1c values ≤7% and only 27% have an optimally controlled weight (BMI ≤25.0). Out of the 125 employers that we have data on and of those who have programs in place to improve health, only 14% of persons with a BMI of ≥30 improved their BMI category in the last year. The employer sees these results as people not trying to engage, but perhaps it is a result of ineffective programs put in place.

Furthermore, we see most employers having an interest to improve diabetes/prediabetes control, yet we found that only 11% of the persons we know with prediabetes improved their A1c out of the prediabetes range. Unfortunately, 10% of prediabetic employees moved into the diabetic range. For those that are considered uncontrolled diabetics with an A1c >7%, we found that in the majority of cases significant investments in medications and diabetes management programs are only improving A1c levels by 1% or more in <50% of the cases. Unfortunately, most investments aimed at improving diabetes are having less impact than expected in improving overall disease control. Perhaps the real issue is that the wrong products are being implemented. When you compare this to outcomes for lifestyle medicine programs run by board-certified lifestyle medicine practitioners, you quickly understand that these incorrect strategies are not working on the root cause of health, and yet are what are most frequently used in the market.

Employer Value-Based Design: Real Change

With obesity starting at a younger age year after year, the demand on the health care system is only going to continue to increase. 21 Despite best efforts, the average employee in the United States is not getting healthier, which means the demand on the system will only increase. Helping employers identify which programs will improve the root cause of health disparity will create sustainable change. Unfortunately, marketing campaigns and accompanying sales are well funded for so many easy-to-use solutions. This means that employers are trying these programs at a much higher rate 22 than they are investing in lifestyle medicine options. Of course, the easy solutions are also the first choice for the employer, advisor, or insurance carrier who is also very busy and will be attracted to programs that are simple to integrate. The “Herd Theory” also comes into play. Larger advisory firms are notorious for integrating the same type of product among all of their employers so that if something does not work, it is not perceived as poor advice from the benefit advisor, but instead, the best they could do at that time. This is protecting the advisor’s relationship with their employers versus being bold and placing products that actually meet the needs of employees for each particular group. If everyone is doing it, it cannot be perceived as an incorrect choice, right?

Fifteen billion in venture capital dollars were invested in wellness products in the first half of 2018. 19 With that investment, the demand is placed to sell the product and grow the company as quickly as possible. Although dollars are used to improve the product, investing in marketing and sales is critical to hit the goals of the investor. These sleek sales teams, with shiny explanations of why their products are best, catch the eye of advisors and employers. This means that products are put in place that look shinier but might not have the desired impact that will really create the change needed to improve short-term medical spending and reduce the long-term dependence on the health care system. 23

What board-certified providers of lifestyle medicine solutions have to offer are evidence-based products at lower prices, since you do not have as much invested in marketing and sales and will not have the demand for large profit margins from your investors. That means you can offer solutions at reasonable prices and put in place performance guarantees that reduce the perceived risk for the employer and potentially offer greater rewards for you the provider. Unfortunately, in medical school not only are providers not taught how to use lifestyle medicine techniques, but they are also not taught how to improve their “business” of health care. Placing the business of health care back into the providers’ hands is essential to drive better outcomes. This finally gives providers the opportunity to establish the price they would need to be reimbursed to provide the service that will improve the health of those persons they serve. Novel idea in health care, is it not! How this is done is simply by creating the cost to provide the service and adding a reasonable margin, let us say 25%. What will drive your ability to sell this is how efficient the provider is in providing the service required or how much risk they will take in extra incentive compensation.

Employers are seeing performance guarantees more often as they establish their strategies. Performance guarantees can establish that the provider has to pay back part of their fees if they do not reach goals and can also be provided extra incentive compensation if they have surpassed goals. An example of this can be illustrated in a type 2 diabetes management program. The goal might be that at least 55% of diabetics with an A1c >7% reduce their A1c by 1% within 1 year of engaging in a program. That is an easy goal for providers utilizing lifestyle medicine to achieve, but a stretch for most programs. Therefore, when trying to convince an employer to utilize your services, you can determine what their current rate of success is and provide outcomes guarantees to exceed that rate. For the employer, they typically are experiencing a $2000 increased expense for every A1c percentage greater than 7%, and in return they can quickly and objectively understand their return on investment. If you provide your base fee with thresholds you are confident you can achieve and offer extra incentive compensations for hitting outcomes that exceed that base expectation, a provider can share in the savings and work to coordinate appropriate care for the employers/payers.

To further progress health care’s ability to drive down the demand on the health care system, having providers influence the plan design and expectations will be critical. Consider the following options for consideration in creating a value-based plan design.

Primary care for chronic condition management considered part of expanded wellness provisions.

Requirement that persons attend a comprehensive nutritional intervention program administered by a lifestyle medicine board-certified provider prior to bariatric surgery.

Requirement that comprehensive physical therapy assessment/treatment be completed before or in addition to chronic opioid treatment; and planting resources in place to provide this effectively.

Appropriate plan coverage for ancillary services that provide outcomes which could include Nutrition counseling Mental health services Physical therapy Meal replacement

Requirement that all patients with lifestyle-associated chronic diseases, for example, overweight/obesity, cardiovascular disease, type 2 diabetes, prediabetes, hyperlipidemia, fatty liver disease, essential hypertension, gestational diabetes, and, in select cases, even type 1 diabetes and autoimmune diseases, for example, inflammatory bowel disease, attend comprehensive, individually tailored lifestyle medicine education programs administered by qualified certified professionals.

Reduce polypharmacy by Discontinuing medications that have been added but have not proven efficacious for the patient’s condition (eg, discontinuing a hypertensive medication that did not improve the patient’s blood pressure and switching to a better medication individualized to the patient rather than just adding on a new one) Medication de-escalation where possible in the context of lifestyle treatment

Reduce need for novel agents and polypharmacy by reducing disease severity with adjunctive lifestyle treatment: Insurance coverage for lifestyle-related treatment for patients who wish to pursue them alone or in addition to disease modifying agents for inflammatory conditions. Insurance coverage for all patients with anxiety and depression to enroll in behavioral health coaching ± exercise program, as first like treatment or as an adjunct to an antidepressant/anti-anxiety medication.

Using lifestyle medicine techniques and editing plan design to create improved outcomes will help reform health care as we know it. Having products offered to employers where they see an impact from their investment will motivate employers. This year, one such program was evaluated by Vital Incite. The case study showed that with lifestyle medicine techniques, persons were able to improve their control of diabetes, reduce their medication utilization, and decrease excess associated spending. 24

In conclusion, value-based design plan created and administered by lifestyle medicine board-certified professionals for employers presents a sound solution to the burgeoning epidemic of chronic diseases among American adults. Not only does it offer higher chance of reversing chronic diseases like type 2 diabetes, essential hypertension, and so on, it also promotes optimal health among the low-risk, relatively healthy workforce. In addition, further outcomes research and health services research to continue to show the value-added benefit of lifestyle medicine to employers is necessary. To quote Dee Edington: “No company will be successful in a globally competitive world with anything but healthy and productive people.” Lifestyle medicine design plan offers exactly that.

Footnotes

Authors’ Note

This manuscript is based on a speech given at the Annual Meeting of the American College of Lifestyle Medicine 2018 in Indiana, IN.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

Not applicable, because this article does not contain any studies with human or animal subjects.

Informed Consent

Not applicable, because this article does not contain any studies with human or animal subjects.

Trial Registration

Not applicable, because this article does not contain any clinical trials.