Abstract

The monetization of the modern Triple-A game has undergone severe changes, as free-to-play revenue models and game as a service distribution strategy have become standard for game developers. To date, the established tradition of the industry’s political–economic analysis focused on the value extraction and user exploitation of video game as a cultural commodity, centered on the video game as generating value through the selling of boxed or digital units. In this article, we present a new analytical framework grounded in understanding the modern video game as an asset that continuously generates revenue for its owners. This theoretical lens encapsulates the changes in contemporary game development, distribution, and value generation. To demonstrate, we apply it to the analysis of the monetization strategies of three recent free-to-play Triple-A titles: Fortnite (2017), Apex Legends (2019), and Call of Duty: Warzone (2020).

Introduction

In the early to mid-2000s, the gaming industry followed a publishing approach based on big annual releases with large production and marketing budgets. Characterized by high risks and high returns, this premium strategy aimed at a niche audience of dedicated gamers who owned home consoles or powerful desktop PCs (Kerr, 2017). A typical game made with this strategy would make most of its revenue during the first months of its release through one-off sales of retail copies and supply a few downloadable content updates to extend its shelf life (Nieborg, 2014). The gaming industry has coined the term Triple-A to represent games of such caliber, similar to the blockbuster category in the movie industry, and it was picked up by players, journalists, and academia alike.

Etymologically, the Triple-A or AAA rank games refer to the bond credit classification system developed by the largest American credit rating agencies—Moody’s, S&P, and Fitch (Finney, 2019). On their scale, the AAA is the highest mark, assigned for the safest bonds that have the strongest capacity to meet financial expectations (Global, 2020). Game publishers borrowed the AAA grade to classify the titles with the largest budgets on game conventions starting in the 1990s (DeMaria, 2019). While scholars attempt to tie the term to a specific logic of production and circulation, such as reliance on the established genres and gameplay modes (Nieborg, 2014; Parker, 2017), or premium pricing, physical sales, and marketing strategy (Kerr, 2017; Nieborg, 2016a), what it essentially stands for are games with large teams, larger budgets, and largest prospective returns, aimed as selling the highest possible number of final products to recoup the astronomical investment: games as commodities. In effect, this has led to “the commodification of everyday digital play… based on continual mass marketing effort” (Nieborg, 2011, p. 16).

Today, with the growing role of smartphones and tablets as gaming devices and new indirect monetization models earning most of the gaming industry’s revenue, the business of gaming changes (Kerr, 2017). The model dominating the gaming industry, and the Triple-A segment in particular, today holds the name of game as a service (GaaS), similar to other rising “aaS” practices, for example, software as a service. Like its non-gameful counterparts, GaaS entails continuous player retention stimulated through regular content updates, often by requiring the players to access it via cloud computing. Combined with the emergent free-to-play monetization strategies, characterized by free access to the core game experience (Nieborg, 2016a), it can generate the immense (and still growing) industry’s revenues recorded in the last years (Wijman, 2019).

As Triple-A publishers turn away from churning out sequels toward continuous support of the existing catalog of games (Hiller, 2017; Tassi, 2019), the classic premium monetization model of singular unitary high-value commodities becomes amalgamated and replaced with alternative approaches (Perks, 2019). Platform capitalism shifts toward assetization or “the transformation of things into resources which generate income without a sale” (Birch, 2015, p. 122). We trace this shift primarily through the work of political geographer Kean Birch (2015, 2017, 2020) and media scholar Jathan Sadowski (2019, 2020). Drawing on both the classical economic theory of Ricardo and Marx, and more recent literature on rent and ownership (Maso, Robertson, & Rogers, 2019; McGoey, 2016; Purcell, Loftus, & March, 2019), they argue that today human knowledge and labor are assetized, rather than commodified (Birch, 2017), and monetized through the extraction of economic rents, instead of direct sales (Sadowski, 2020).

In this article, we adopt this line of thought to the modern realities of game production. First, we contextualize our claims by investigating the industry’s shift from commodity-based production toward the GaaS formula. Next, we highlight the changing role of analytics and telemetry in contemporary game development. This allows us to critique the game as a stand-alone object and present our new, asset-based conceptual framework as better equipped to interpret the political economy of the contemporary gaming industry. Finally, to demonstrate its analytical potential, we analyze three recent Triple-A titles as case studies and draw conclusions about the dynamic nature of console games’ monetization.

The Triple-A Game, from Commodity to an Asset

The game as a boxed product and as a service

The original conception of a video game as a commodity was suggested by David Nieborg (2011, 2014). By tying Mosco’s (2009) understanding of commodification of cultural products to video games, he proposes to analyze them through the study of their development, circulation, and monetization (Nieborg, 2014). Following Bill Ryan’s (1991) line of thought on capitalist cultural production, Nieborg (2014, p. 51) introduces the notion of the formatting strategy as the pervasive governing systems of creative control constructed by the technical and economic affordances of platforms and market demand. Nieborg later (2016a) reframes it as the contingent cultural commodity, to highlight how cultural production is constantly shaped by platforms and user feedback (Nieborg & Poell, 2018). In this subsequent revision, the contingent cultural commodity becomes dynamic and responsive to more accurately reflect the process of the modern game development, powered by the game as a service publishing strategy (Kerr, 2017). However, here, we can already begin our initial questioning of the existing model: can such modular, endlessly recirculated, and dynamically monetized media as a modern video game could be even considered a commodity?

Indeed, during the first six generations of home consoles, video games’ profit generation and distribution logic strongly resembled a typical commodity-based business. Characterized by the impact-upon-release strategy and sold in the form of premium-priced packaged discs (Nieborg, 2016a), Triple-A games were usually purchased in physical stores. However, as Nieborg (2014) notes, the seventh cycle of consoles introduced a new, digital way to sell games, afforded by the digital marketplaces launched by main gaming platforms’ manufacturers—Sony, Microsoft, and Nintendo. The postlaunch paid extensions to existing games, or DLCs, which Nieborg regard as one of the generation’s formatting strategies, were also enabled by the new network capabilities of the consoles and the rise of these digital stores.

A product of its time, Nieborg’s initial assessment was soon complicated by the emergence of a new publishing strategy, which occurred during the lifecycle of the seventh generation of consoles and entrenchment of the PC digital storefronts (Joseph, 2018)—that of a live service. Also called game as a service (GaaS), this model is defined by the continuous support of the existing game with a consistent stream of large content and gameplay updates, paid or free, and was pioneered by Valve in their Team Fortress 2 (2007) (Bycer, 2019). With GaaS, the players do not buy a finished product, but instead gain access to a continuously updated, improved, altered game with the potential to bring new experiences in the years to come. In return, game publishers receive the opportunity to extract revenue for a longer period of the game’s extended support—or kill it off quickly should it fail to generate sufficient profit.

What Nieborg initially identified as brancherd serialization (Nieborg, 2011, p. 38), or a DLC-based formatting strategy of seventh generation of platforms, was the inception of the live service Triple-A game. Beginning with the 7th console generation in mid-2000s and it has subsequently reached its peak during the following console cycle of PlayStation 4, Xbox One, WiiU, and Switch in early 2010s. Throughout the lifespan of this, eighth generation of consoles, the gradual development of the GaaS model has resulted in a noteworthy growth of the Triple-A industry value (Batchelor, 2018; Makuch, 2019; Taylor, 2017; Winslow, 2019) and a no-less considerable drop in the number of largest publishers’ annual releases (Hiller, 2017; Tassi, 2019). With this strategy governing the production of the Triple-A game, the industry’s focus has shifted from the regular production of sequels to the continuous substantial updating of existing games. Here, we see the first step towards assetization, in rejecting sales numbers as the only revenue indicator. Rather than being a supplement aimed at extending the large titles’ shelf life (Nieborg, 2014, p. 55), post-release support has become a part of the games’ experience, expected by default. Particularly as modern Triple-A games often launch with detailed roadmaps of future updates, which, if not followed through with, can cause players’ dissatisfaction and outcry (Macgregor, 2019).

Games political economist Aphra Kerr thoroughly documented and analyzed the GaaS impact on the gaming industry. In Global Games (2017), she captures how between 2012 and 2016 this approach altered the industry’s value chain by diminishing the need in distributors and retailers; encouraged the rapid expansion to mobile devices; reshaped the power balance by putting new companies, such as Chinese Tencent on top of the revenue rankings; allowed postlaunch game development and extensive behavioral tracking; and introduced new business models. Her research shows that “game as a service means that production is never finished” (Kerr, 2017, p. 190), as the developers have to continuously maintain and update the game to ensure that it provides fresh experiences for players throughout its lifecycle. Overall, she points at a new, iterative game design logic that is informed by players’ feedback and does not stop after the game’s release.

The major publishers’ adoption of GaaS suggests a departure from the commodity form. The new approach to game development entails the rejection of a finalized form of a product, independent of the producer and available exclusively to the player. Callon and Çalışkan, who theorized the establishment of markets, call the process of pacification inherent to the commodity exchange, as only a passive object could be valued, alienated from the producer, and assigned to an owner(s) (2010, p. 5). In the realities of the live service strategy, a finished and passive game is a dead game, doomed to lose its audience and profits (Stephen, 2019). Similar to the rise of “perpetual beta” culture in software, the developer has no economic motivation to ever release a finite version. With GaaS undermining games’ existence in a passive form, it thus becomes harder and harder to associate the modern Triple-A game with a commodity from the economic theory standpoint.

The assetization of the Triple-A game

If the modern Triple-A game departs from the commodity form, what does it turn into? Following a growing theorization of modern platform capitalism’s shift toward assetization—as “the transformation of things into resources which generate income without a sale” (Birch, 2015, p. 122)—our answer is assets. This shift is characterized by the turn to rentiership as a new dominating mode of capitalization (Muniesa et al., 2017), based on deriving economic rents from providing access to assets (Birch, 2020; Sadowski, 2020). The current Triple-A developments suggest that this industry follows a similar trend. Just like landed property—a traditional form of an asset—the modern Triple-A game provides a continuous stream of income, alllowed by the GaaS formula. Sadowski (2020) sees this approach, just as any X as a service model, as a different name for rentier relations, where rentiers capture revenue from providing access to digital assets.

Contrary to a commodity, an asset is a property that can generate revenue in other ways, rather than from directly trading it (Birch, 2017). The modern video game, be it a social game on a mobile device or a Triple-A title for home consoles, is similar in that sense, as GaaS provides a source for continuous postlaunch monetization, instead of relying on maximizing the profits upon release (Nieborg, 2014). Essentially, this extended approach to revenue generation is what separates property (to be monetized) from products (to be sold). Any analysis of contemporary Triple-A industry would be fallacious from the ground up, if it treated games as singular products, detachable from their owners (Çalışkan & Callon, 2010; Nieborg, Young, & Joseph, 2020).

Depending on the type of asset, value can be generated in various ways. From land and real estate, which has gone through the process of assetization long ago (Ward & Swyngedouw, 2018), owners can extract a number of traditional differential and monopoly rents, tied to the property’s unique features, quality, and investments (Birch, 2020), while intangible assets, such as intellectual property, can generate revenue through royalties, partnering, or licensing (Birch, 2017). Platforms—the main business structure of contemporary capitalism (Srnicek & De Sutter, 2017)—are the most lucrative assets of today, as, according to Sadowski (2020), their owners capture value by providing multiple actors with access to existing digital resources in exchange for different types of rent. Similarly, the modern video games, with their planned massive content update, and indirect monetization approaches (Nieborg, 2016a), which require smaller but more frequent transactions to access a richer gaming experience (Perks, 2019), can also be seen as (small) platforms. What unites these types of property is that they all capture value through economic rents extracted over time from property users.

One could think that the payments that players make in free-to-play games do not correspond to rent because they are made voluntarily. However, as Sadowski (2020) notes, the modern rentiers extract two types of rent: the monetary rent and the data rent. Unlike the direct monetary rents, which can indeed be omitted in a free-to-play game, the players have no choice but to pay the data rent in full through telemetry, as they have to consent to publishers’ privacy policies to enter the game. This reliance on extractive business models has been continuously highlighted in recent scholarship on surveillance capitalism (Zuboff, 2019) and platform surveillance (Murakami Wood & Monahan, 2019). Crucially, monetary and data rent are not interchangeable or similarly valuated, as, according to Sadowski (2020), there are more ways to capitalize data, than to sell them directly. For example, data can be used for profiling and targeting people, optimizing existing systems, improving management, generating models, creating new products, and bringing new value to existing assets (Sadowski, 2019). Simply selling the data is also always an option, of course, as most of the mobile gaming sector relies on advertising-based free-to-play models, or, essentially, selling audiences to advertisers (Nieborg, 2016a, 2016b). Indeed, the free-to-play monetization models are the ones that depend most heavily on data extraction, as, according to Kerr (2017, p. 16), “[i]n free-to-play games, the financial success of the game relies on player surveillance, actionable insights from data, and game customization.”

Moreover, the free-to-play approach is not one, but a plethora of models, which are characterized by a lack of up-front payment from consumers (Nieborg, 2016b). These models can either be driven by advertising, or additional in-game purchases of virtual items, called microtransactions (Perks, 2019, p. 7), or provide players access to a fuller gaming experience through a one-time payment or a continuous subscription fee. With these models, players’ customer lifetime value, or the total revenue generated by a user via in-game purchases (Voigt & Hinz, 2016, p. 108), becomes central to the games’ economic successes, rather than the number of premium sales or preorders (Burelli, 2019; Nieborg, 2016b).

Motivated by players’, critics’, and developers’ frustration with the traditional model (Perks, 2019), and inspired by the success of the mobile gaming industry, which generated a US$68.5 billion revenue in the last year (Luz, 2019), large publishers increasingly implement free-to-play models in their Triple-A titles or switch to them completely. The direct influence of this adoption is fundamental changes to the Triple-A formula. Free games lose the material form of packaged goods, skip the retailers’ shelves in favor of digital platforms, and swap the impact-upon-release strategy for prolonged revenue generation by being designed as a data-driven service. Thus, the modern Triple-A game is neither produced nor monetized as a commodity.

Today, with the GaaS approach setting the standard for the industry, game development as a segment of cultural production becomes dependent on user data. Even if these data are not turned directly into revenue, they are reinvested into the assets (games) to increase their capitalization. To demonstrate how exactly the collected data bring value to the game designers and publishers, in the next section we examine contemporary game analytics’ practices.

Game Analytics as Alternative Rent

The premise of the XXI century’s platform capitalism and platform surveillance lies in the centralization of high-income economies around the extraction and utilization of data as a “new raw material” (Srnicek & De Sutter, 2017, p. 39). While it is important to note that data are never raw, as without an interpretation they provide no insight, and therefore, no value (van Dijck, 2014; Gitelman, 2013), the increasing importance of data for today’s economy is indeed noted by many scholars (Fourcade & Healy, 2016; Kenney & Zysman, 2016; Langley & Leyshon, 2017; Sadowski, 2019). Rendered as a new form of capital, data are collected and stored by companies to potentially create value, which comes in many forms. Even organizations that do not know how to utilize collected data right away are driven by the data imperative to extract and store as much data as possible due to the potential for their future monetization (Fourcade & Healy, 2016, pp. 14). To amass the new form of capital, companies change their products and services and tune their business processes to achieve the utmost datafication, or the conversion of human behavior into quantifiable data (Cukier & Mayer-Schoenberger, 2013; Van Dijck, 2014).

Consequently, modern Triple-A game development relies heavily on the data-mining practices summarized as game analytics (Seif El-Nasr, Drachen, & Canossa, 2013a; Wallner, 2019). Since the seventh generation of consoles, the game industry has started to increasingly extract game telemetry (Seif El-Nasr, Drachen, & Canossa, 2013b)—players’ behavioral data transmitted online from installed games’ clients. The online capabilities of these consoles afforded unprecedented surveillance over the players, letting the developers accumulate players’ aggregated feedback and track individuals’ behavior. As Drachen, Seif El-Nasr, & Canossa (2013) explain, every aspect of players’ interaction with the game, ranging from in-game purchasing behavior and settings’ adjustments to physical movement on game’s levels and communication with other players, can be constantly collected from the game client. This telemetry is later interpreted into game metrics, or more concrete quantitative measures of the game’s technical performance, and players’ behavior, which are utilized by various stakeholders at all stages of the game production processes, further cementing the game as an asset generating value through data rent.

Sometimes, these metrics are displayed back to the players to empower them and foster community building (Wallner, 2019), for example, in the form of in-depth statistics of players’ gameplay performance in online games, which is used to provide insights that will improve their efficiency (Egliston, 2019). However, most of the time these metrics are operationalized to improve game design and player experience, inform business decisions, and innovate and optimize game technology (Wallner, 2019). Moreover, as much as these metrics are used in game development, they are also put at the core of marketing campaigns and community management (Kerr, 2017).

One of the most important types of metrics in the analysis of a game’s monetization are user metrics. These metrics track users both as customers and as players since they provide insights about players’ engagement and efficiency of monetization models that drive game design and publishing strategy (Drachen et al., 2013). The customer-oriented user metrics afford game developers to build the demographics of their customer base, perform microtransaction analysis, and predict average customer lifetime value (Voigt & Hinz, 2016), or how much value can be extracted per player, while potentially “nudging” them into patterns beneficial to the platform (Yeung, 2017; Ash, Anderson, Gordon, & Langley, 2018). Player-oriented metrics, on the other hand, are used to identify the most problematic, boring, or engaging parts of the gameplay and improve user experience (Drachen et al., 2013). Representing the opposite poles in the revenue chain in the game development process, these two directions of user metrics are important to be balanced out, as any game has simultaneously to be enjoyable while also making a profit (Drachen et al., 2013).

Game analytics thus further challenge the commodification lens since value is no longer generated only via player’s purchase of the boxed or digital game but also throughout their continuous co-engagement. Telemetry collected throughout gameplay, while not necessarily producing revenue by itself, becomes a part of the companies’ business intelligence that drives the decision-making of game designers, marketers, project managers, and other types of stakeholders in the company (Canossa, Seif El-Nasr, & Drachen, 2013; Drachen et al., 2013). Beforehand, game developers used primarily to rely on data gathered from UX tests and feedback forums (Kerr, 2017), which may not have always represented a typical player and were resources-consuming at scale. Today, with the game analytics-fueled development, aggregated players have more impact on the continuous development cycle than ever, as every one of them is “both implicitly or indirectly involved in game production through behavioral metrics” (Kerr, 2017, p. 91).

In the Triple-A industry, therefore, data collection is exclusively tied to the improvement of assets—their performance, enjoyment by the audience, and monetization. Shoshana Zuboff, a social psychologist and theorist of surveillance capitalism, characterizes such configuration as a behavioral value reinvestment cycle (Zuboff, 2019). Moreover, publishers pursuing free-to-play models can also rely on behavioral surplus (Zuboff, 2019, p. 68), or offering excessively collected user data to third parties, as targeted advertising plays a major role in their monetization (Nieborg, 2016b). In generating the player commodity (Nieborg, 2015), or, in other words, sets of user profile information, and selling them, ad-driven free-to-play games resemble the surveillance assets’ monetization logic established by Google (Zuboff, 2019).

While it is difficult to estimate the exact monetary value of players’ data, it is clear that the modern GaaS game development is inseparable from massive-scale player surveillance and monetization, firmly establishing it as assets rather than commodities. To further demonstrate how our proposed conceptual framework resonates with the modern game industry, in the next section we apply it to analyze three successful recent Triple-A action titles: Fortnite (2017), Apex Legends (2018), and Call of Duty: Warzone (2020). In each case, we look at the game’s monetization model and the extracted player data.

The Triple-A Game in its Eighth Generation

The battle pass business model

Inspired by the eponymous Battle Royale (2000) movie and Hunger Games (2008) novel, the Battle Royale (BR) genre was first transferred into gaming through fan-made modifications to Arma II (2013), Minecraft (2011), and a few other games. After Brendan "PlayerUnknown" Greene, the creator of the original Arma III modification, signed a deal with South Korean company Krafton to create a stand-alone game in this genre in 2017, its massive growth in popularity officially took off (Fillari, 2019). The premise of the game genre stayed close to the idea of the original Japanese movie: BR game mode is an online deathmatch of large scale, both in the size of the map and the number of players in one session (up to 150), where the goal is to become the last player or team alive with the use of weapons scattered across the playable area. By offering a tough competition in every session, a sandbox for great variety in gaming experiences and fast-paced gameplay, this genre quickly attracted a large audience and was picked up by other game publishers.

Gameplay aside, the main novelty of the BR games comes from their monetization model. In 2017, Epic Games decided to make the BR game mode of their newly released Fortnite free-to-play in order to compete with Krafton’s PUBG (2017), which still used the premium monetization model. In 2018, EA joined the arena with their Apex Legends, the company’s first free-to-play Triple-A title (Electronic Arts Inc., 2019a). In the consequent year, Activision followed Epic’s tactic and published a stand-alone BR game mode called Warzone in addition to Call of Duty Modern Warfare, the 16th installment in the Call of Duty series. Nieborg (2014) rightfully called the CoD franchise an epitome of Triple-A game design for the standardization of its games, their annual release schedule, and the establishment of DLCs as a common practice in the market. Years later, these series continue to reflect the modern state of the Triple-A industry, with their adapting monetization strategies and evolving gameplay modes demonstrating the shift toward assetization.

Therefore, three companies, famous for their previous blockbuster (read: commodities) game production, released free-to-play titles with microtransactions and Triple-A budgets. While this alone is unprecedented and noteworthy, more importantly, BR games introduced a new monetization approach called the battle pass. Battle passes generate a significant part of these extraordinary economically successful games’ revenue (Gilbert, 2019), providing perfect case studies for the analysis of the gaming industry’s assetization.

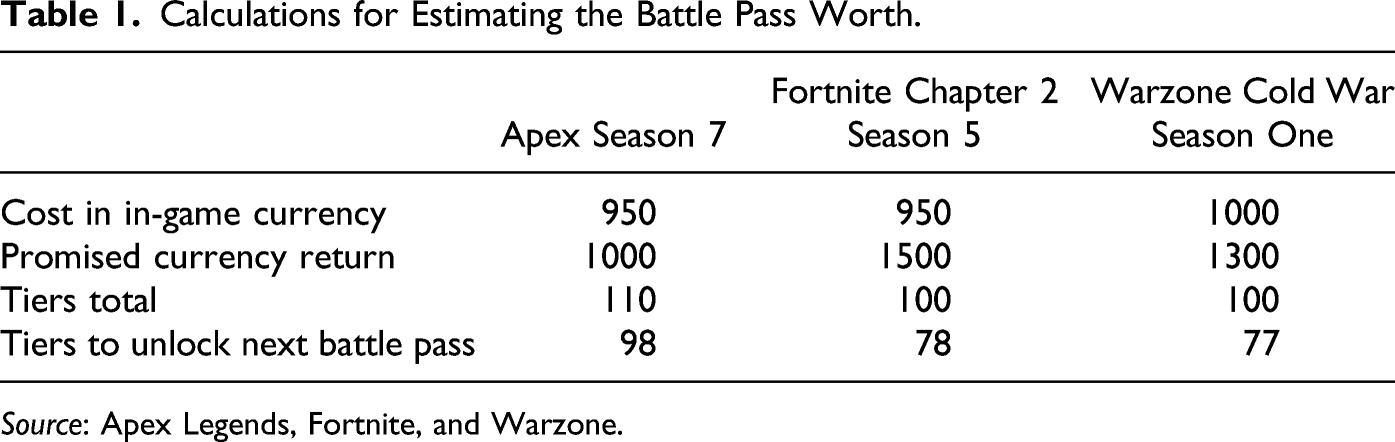

Battle pass purchase grants the player access to a limited-time tiered progression system with additional in-game rewards. Both the rewards and the battle pass itself are tied to seasons—time frames during which the most substantial gameplay and content updates are introduced, usually lasting around 10 weeks. If the modern Triple-A game can be understood as a service, then the battle pass is an optional subscription to a premium version of this service paid seasonally. Just as any other subscription (Sadowski, 2020), it constitutes a rental device for property owners (i.e., game publishers) to continuously extract value from their assets. The purchase of a battle pass can be viewed as a form of economic rent because it is purchased regularly to access the fuller or quicker game experience, consisting of a stream of additional rewards.

At the time of writing, Warzone and Apex Legends count seven battle pass-supplied seasons each, while Fortnite has entered its 15th one. The idea of the battle pass turned out to be so successful that, in some form or another, it spread to the games of all genres and on all platforms. Older service-driven games, such as For Honor (2017) and Destiny 2 (2017) added battle passes years after initial release to generate additional profit. More recent games take the idea further, with Marvel’s Avengers (2020), featuring not one but several battle passes—one for each playable character. Today, even something as casual as Penguin Isle (2019), an idle game for iOS and Android, features its own sort of battle pass, disguised as an anniversary event. However, the original implementation used in the aforementioned BR games is still worth analyzing, as it inevitably serves as a reference point for the rest of the industry.

Calculations for Estimating the Battle Pass Worth.

Source: Apex Legends, Fortnite, and Warzone.

The value that the pass creates for the player has to be estimated for each game depending on its offer, however, and this discussion lies outside the scope of this article. What is important about the pass model is that it changes how people spend money on the games, that is, less money, but more often. The trend toward the pass-based (or, essentially, rent-based) gaming is not only present on the level of single games, but across the whole industry. Today, major publishers like EA, Sony, and Microsoft offer access to libraries of on-demand games and cloud gaming services for a monthly fee.

The data rent paid in full

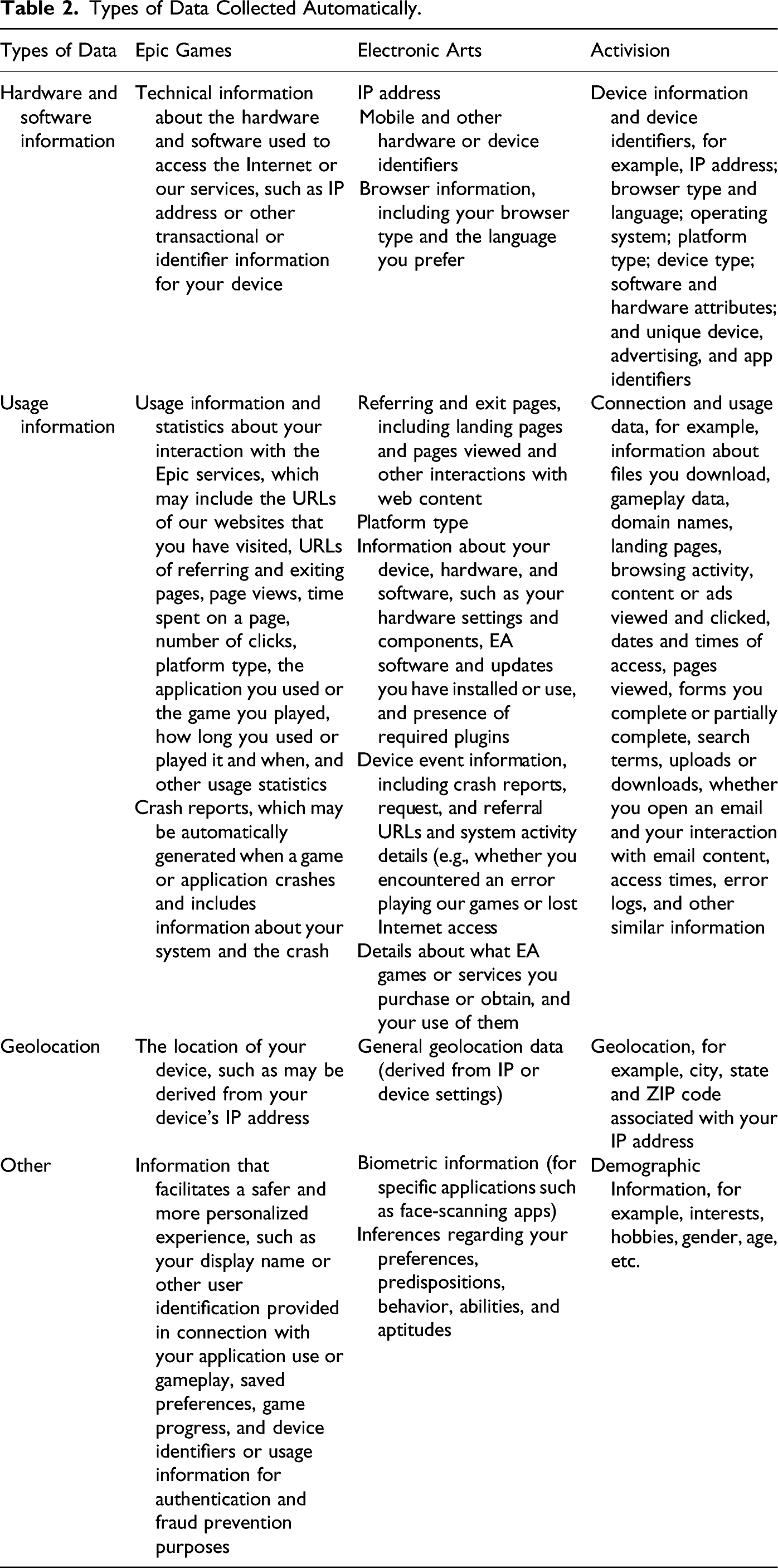

Now that we established the role that battle pass plays in generating revenue and extracting data, the final section of our analysis shows what kinds of data are extracted, and why are they valuable. To do so, we analyze the terms of use and privacy policies of the selected games’ publishers, as carefully reading through these legal documents reveals the scale of the companies’ data collection and application.

Types of Data Collected Automatically.

By consenting to these companies’ user agreements, you let them know about who you are, where you live, what are your interests, and preferences (derived from said cross-platform data collection), as well as allow them to record your every action within their products. With this player-centered game design approach and data collection of such scale, everything you do with the publishers’ products can and will be used for your retention and further rent extraction.

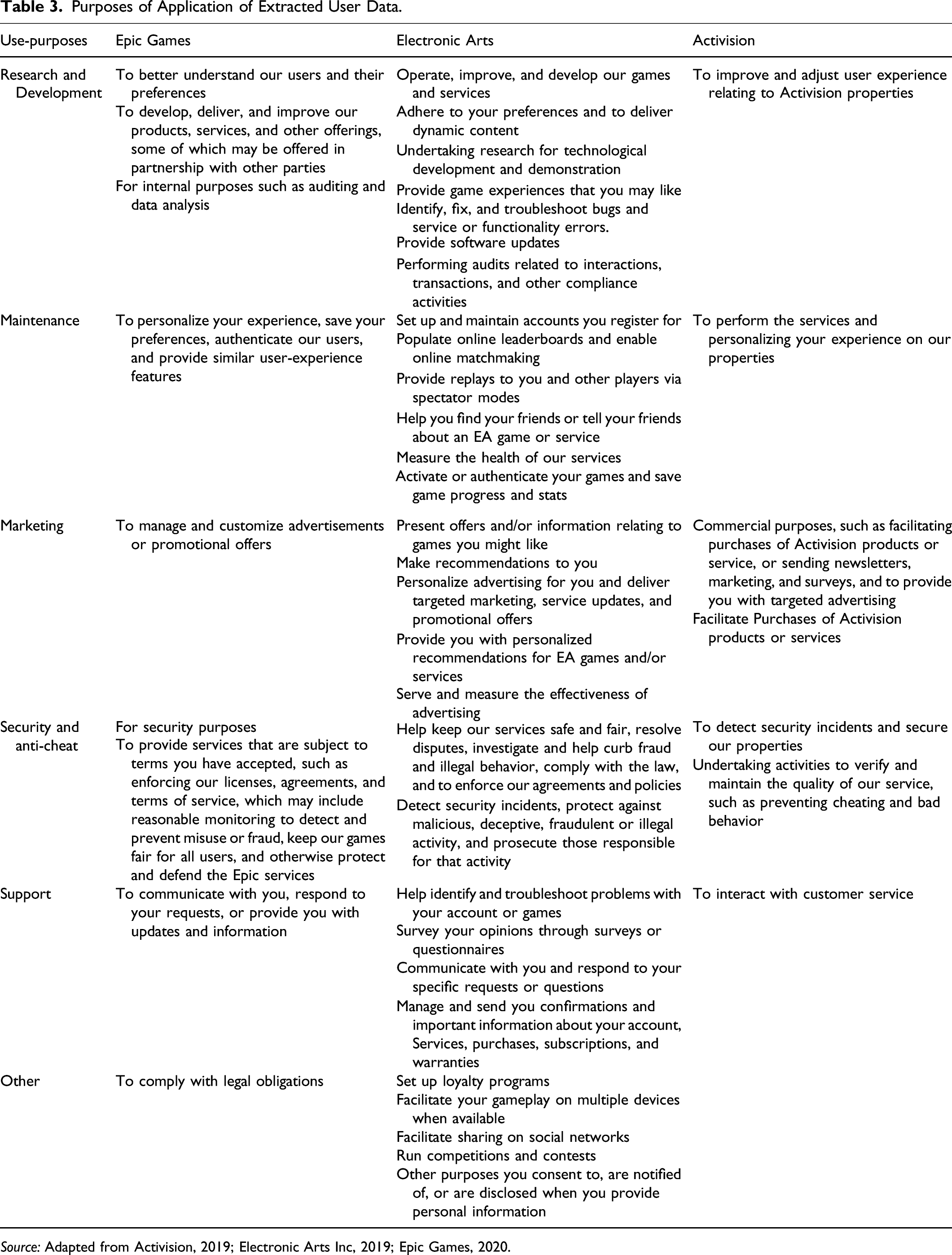

Purposes of Application of Extracted User Data.

Source: Adapted from Activision, 2019; Electronic Arts Inc, 2019; Epic Games, 2020.

User data extracted by the publishers are not only operationalized inside these companies, as, according to their privacy policies, they are also shared with several third parties to execute the organizations’ strategies and further generate asset revenue. These third parties include service providers, who provide payment engines or assist with data collection, storage, and analysis; business partners, like external game development studios that provide their games through the publishers’ digital platforms; and marketing partners, who use the data collected by publishers for targeted advertising.

Notably, while Epic Games and Activision specify that they only share user data with the marketing partners to deliver their advertisements (Activision, 2019, sec. 6; Epic Games, 2020, second. How We Use Information (2)), EA’s policy lacks such statements. This suggests that data collected by this publisher may be utilized by some third parties for their own purposes. Additionally, EA could be suspected to be the only company to benefit from the behavioral surplus (Electronic Arts Inc., 2019b, sec. 4), as the other two publishers explicitly state contrariwise in their policies (Activision, 2019, sec. 6; Epic Games, 2020, second. Your Choices and Controls). Moreover, EA’s policy states that the company may or may not anonymize your personal data and only specifies their de-identification when sharing with advertising partners. Meanwhile, their business partners gain direct access to users’ personal data (Electronic Arts Inc., 2019b, secs. 3, 4).

The goal of this analysis is not to pick out the most suspicious data extraction practices, of course, as all these companies aim to increase the capitalization of their assets and collect the highest possible data rent. Rather, we show that for game publishers, data are indeed a form of capital (Sadowski, 2019), and even players who do not spend a dime in those games pay the rent for accessing them with their quantifiable traits and/or actions.

Collected user data allow publishers to research their audience, target it with the right promotions, and create and attune the games to their preferences, and thus giving players “what they want” (Schüll, 2012, p. 98). However, a deep understanding of who are the players, what do they like, and what do they do in the games, produced by the analysis of these data, also allows the developers to monetize the players like never before. Modern Triple-A games are not only designed in accordance with insights derived from data but also designed to extract more data, as free-to-play monetization make them accessible to a wider audience and continuous refreshment of gaming experiences with seasonal updates keeps player retention high. Therefore, those games do not only extract literal, monetary value from the player via regular microtransactions and battle pass subscription but also constantly generate valuable user data, which are applied in the behavioral value reinvestment cycle (Zuboff, 2019) and sometimes even sold directly.

Conclusion

By analyzing the three picked BR games, we aimed to unveil the assetisized logic of the modern console and PC game, reveal the rentier positions of the major game publishers, and demonstrate that the Triple-A segment is more dynamic and adaptive in its monetization than commonly thought (Kerr, 2017; Nieborg, 2016a).

The assetization in the game industry is not only present at the level of a single game. The cloud-based platforms, which stream the games on-demand to users’ devices from remote data centers, constitute a perfect example of this phenomenon and a telling indication of the future of the whole industry. Two of the biggest console manufacturers, Sony and Microsoft, who used to rely on selling console hardware units, are now at the forefront of the cloud gaming industry. Currently, they are developing their cloud-based platforms—PlayStation Now and XCloud—which have launched with the release of ninth generation consoles (Warren, 2019; Warren & Hollister, 2019).

While the next consoles will remain the form of commodified discrete units, these companies are already heavily investing in the powerhouses, data centers, and underlying infrastructure, leaning toward platformization and subsequent assetization. With cloud gaming, players will pay a subscription to use the hardware stored in these powerhouses to stream gameplay, or, in other words, pay monthly rent to access the property of “internet landlords” (Sadowski, 2020, p. 564). What this development suggests is that not only the Triple-A gaming itself but also the platforms of its distribution are moving away from the traditional commodity form of console units. This affords us a glance into the future of fully assetized gaming, where the gamers will own neither the games nor the consoles.

However, the commodification logic has not yet disappeared entirely from the Triple-A game industry and is unlikely to disappear in the future. Instead, it is being integrated into the games themselves in the form of cosmetics, purchased with microtransactions. This is what makes the modern blockbuster game a highly productive asset: not only is it monetized through the rent of seasonal battle passes or subscriptions but is also produced and maintained in a way to generate revenue through the commodification of in-game items. By combining the rent-based and commodity-based models, the analyzed games are able to continually draw income, and players’ data extraction and application in game design and maintenance allows game publishers to further optimize the productivity of their assets.

Here, we further contribute to the development of the asset-based theoretical lens (Birch, 2020; Sadowski, 2020). We applied this framework to the analysis of the eighth generation Triple-A games, but it could be as easily utilized to investigate the economic relationships in the mobile industry (Nieborg et al., 2020) or the market of social games (Nieborg, 2020). With the Triple-A turning to free-to-play and console manufacturers investing into cloud platforms, our proposed framework this aims to be useful in future political–economic critique performed by both game and platform studies’ scholars.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.