Abstract

In this article, we review Granger causality tests that are robust to the presence of instabilities in a vector autoregressive framework. We also introduce the

Keywords

1 Introduction

Vector autoregressive (VAR) models have played an important role in macroeconomic analysis since Sims (1980). A VAR is a multiequation, multivariable linear model where each variable is in turn explained by its own lagged values as well as current and past values of the remaining variables. Compared with a univariate autoregression, VARs provide both a systematic way to capture the rich dynamics in multiple time series and a coherent, credible approach to forecasting.

Granger (1969) causality is a useful tool for characterizing the dependence among time series in reduced-form VARs, and Granger causality test statistics are widely used to examine whether lagged values of one variable help to predict another variable—see Stock and Watson (2001).

However, VAR analyses in macroeconomic data face important practical challenges: economic time-series data are prone to instabilities (see Stock and Watson [1996, 1999, 2003, 2006]; Rossi [2013]; Clark and McCracken [2006]), and VAR estimates may also be prone to instabilities (see Boivin and Giannoni [2006], Kozicki and Tinsley [2001], and Cogley and Sargent [2001, 2005]).

Thus, given the widespread use of VARs and the evidence of instabilities, it is potentially important to allow for changes over time when doing VAR-based statistical inference. As demonstrated in Rossi (2005), because the traditional Granger causality test assumes stationarity, it is not reliable in the presence of instabilities and may lead to incorrect inference.

In this article, we present the

We first introduce the tests and then present the commands that implement them. Then, we illustrate the empirical implementation of the robust Granger causality tests using a three-variable (inflation, unemployment, and interest rate) VAR model with four lags as in Stock and Watson (2001), as well as a direct multistep VAR–LP forecasting model. Finally, we compare the results with those based on a traditional Granger causality test.

The remainder of this article is organized as follows. Section 2 describes the theoretical framework and the Granger causality robust tests. Section 3 introduces the

2 VAR-based Granger causality test in the presence of instabilities

2.1 Motivation

In the presence of instabilities, as shown in Rossi (2005), traditional Granger causality tests may have no power. Consider one of the equations in a two-variable VAR with one lag and fixed prediction horizon h, for example:

In this example, a traditional Granger causality test would be a t test applied on the full-sample ordinary least-squares (OLS) parameter estimator

because

Equation (2) implies that we do not reject the null hypothesis even if x t − 1 does Granger-cause y t + h in reality. This failure to reject results from the violation of the stationarity assumption underlying traditional Granger causality tests because the predictive ability is unstable across time. Thus, traditional Granger causality tests can be inconsistent if there are instabilities in the parameters. Without losing generality, this conclusion can be generalized to instabilities other than (1) by varying the time and the magnitude of the break. Note that this conclusion is empirically relevant because evidence shows that parameter estimates change substantially in sign and magnitude across time; see, for example, Welch and Goyal (2008) and Rossi (2005).

Considering the possibility of parameter instabilities, Rossi (2005) proposes tests to evaluate the predictive ability in the situation where the parameter might be time varying by testing jointly the significance of the predictors and their stability over time. More generally, let β

t change at some unknown point in time,

Note that a test for structural breaks would not necessarily be the correct approach either. In fact, while in the previous example the researcher would identify a break, a structural break test is not sufficient or necessary for the existence of Granger causality. In fact, imagine that a variable has predictive content for another variable and the predictive ability is constant over time; that is,

Note also that the way the possible presence of instabilities is modeled here is via a one-time break; such an approach has been proven to be more powerful than cumulative sum (CUSUM) tests—see Andrews, Lee, and Ploberger (1996), who derived the optimal tests (the exponential averages of the Wald test statistics) for one or more change points at unknown times in a multiple linear regression model. They compare the power of the optimal exponential tests with that of other tests in the literature such as the likelihood-ratio or supF test; the CUSUM test in Brown, Durbin, and Evans (1975); and the midpoint F test considering a one-time break in parameter. They find that the optimal tests perform quite well in finite samples compared with the other tests considered while the CUSUM test performs poorly.

2.2 Framework

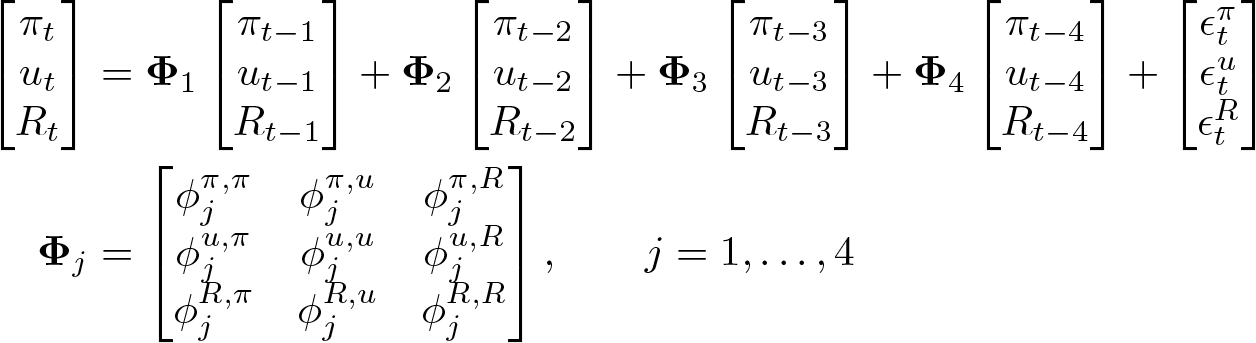

We consider two types of VAR specifications. The first is a reduced-form VAR with time-varying parameters,

where

The second is a direct multistep VAR–LP forecasting model with time-varying parameters. By iterating (3),

where

Let

The statistics to test H 0 in (5), following Rossi (2005), are ExpW* (the exponential Wald test), MeanW* (the mean Wald test), Nyblom* (the Nyblom test), and QLR* (the Quandt likelihood-ratio [QLR] test). 6

The optimal ExpW* and the optimal MeanW* tests are based on the exponential test statistics proposed in Andrews and Ploberger (1994). The optimal MeanW* is designed for alternatives that are close to the null hypothesis, while the optimal ExpW* is designed for testing against more distant alternatives. The optimal Nyblom* is based on the Nyblom (1989) test, which is the locally most powerful invariant test for the constancy of the parameter process against the alternative that the parameters follow a random walk process. The optimal QLR* is based on Andrews’s (1993) Sup-LR test (or the QLR test), which considers the supremum of the statistics over all possible break dates of the Chow statistic designed for a fixed break date.

2.3 A special case: The traditional Granger causality test

The traditional Granger causality test is a special case where the parameters in (4) are time invariant; that is, for j = 1,…, p, we replace

To consider a more concrete example, Stock and Watson (2001) study a threevariable VAR with four lags (p = 4) and h = 0. The variables included are inflation (π t), unemployment (u t), and interest rate (R t). Their reduced-form VAR is

Thus, in Stock and Watson (2001), the reduced-form VAR involves three equations: current unemployment as a function of past values of unemployment, inflation, and the interest rate; current inflation as a function of past values of inflation, unemployment, and the interest rate; and current interest rate as a function of past values of inflation, unemployment, and the interest rate. Stock and Watson (2001) consider traditional Granger causality tests in each equation where the null hypothesis is

If unemployment does not Granger-cause inflation, then lagged values of unemployment are not useful for predicting inflation.

3 The gcrobustvar command

3.1 Syntax

The

depvarlist is a list of dependent variables, that is, all the variables in

3.2 Options

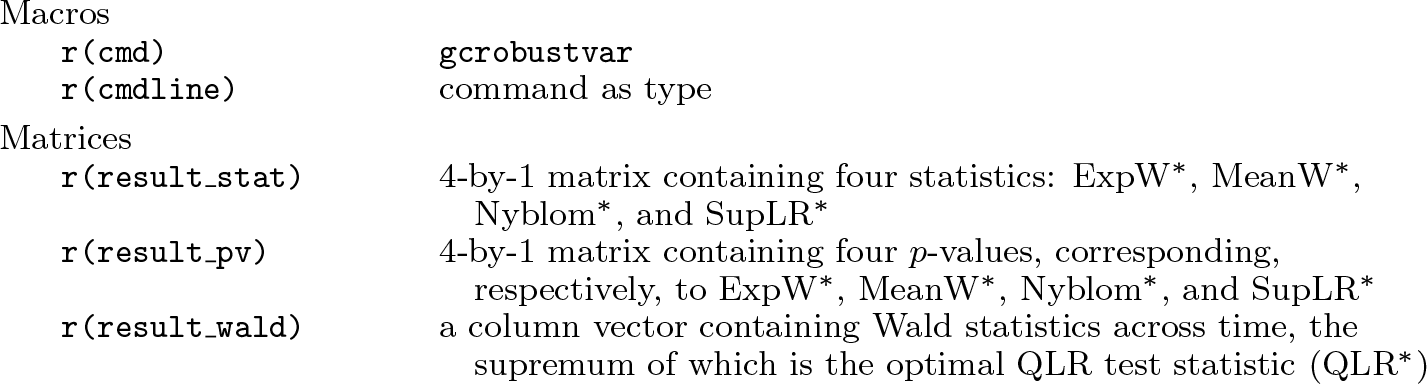

3.3 Stored results

3.4 Empirical example of practical implementation in Stata

In what follows, we illustrate how to use the

Consider the inflation equation in (3):

Suppose we are interested in testing whether unemployment (u) Granger-causes inflation (π), and we want the test to be robust to instabilities over time. That is, we want to test whether the coefficients of lagged values of unemployment (u) are zero across time:

Implementing the Granger causality tests in the presence of instabilities

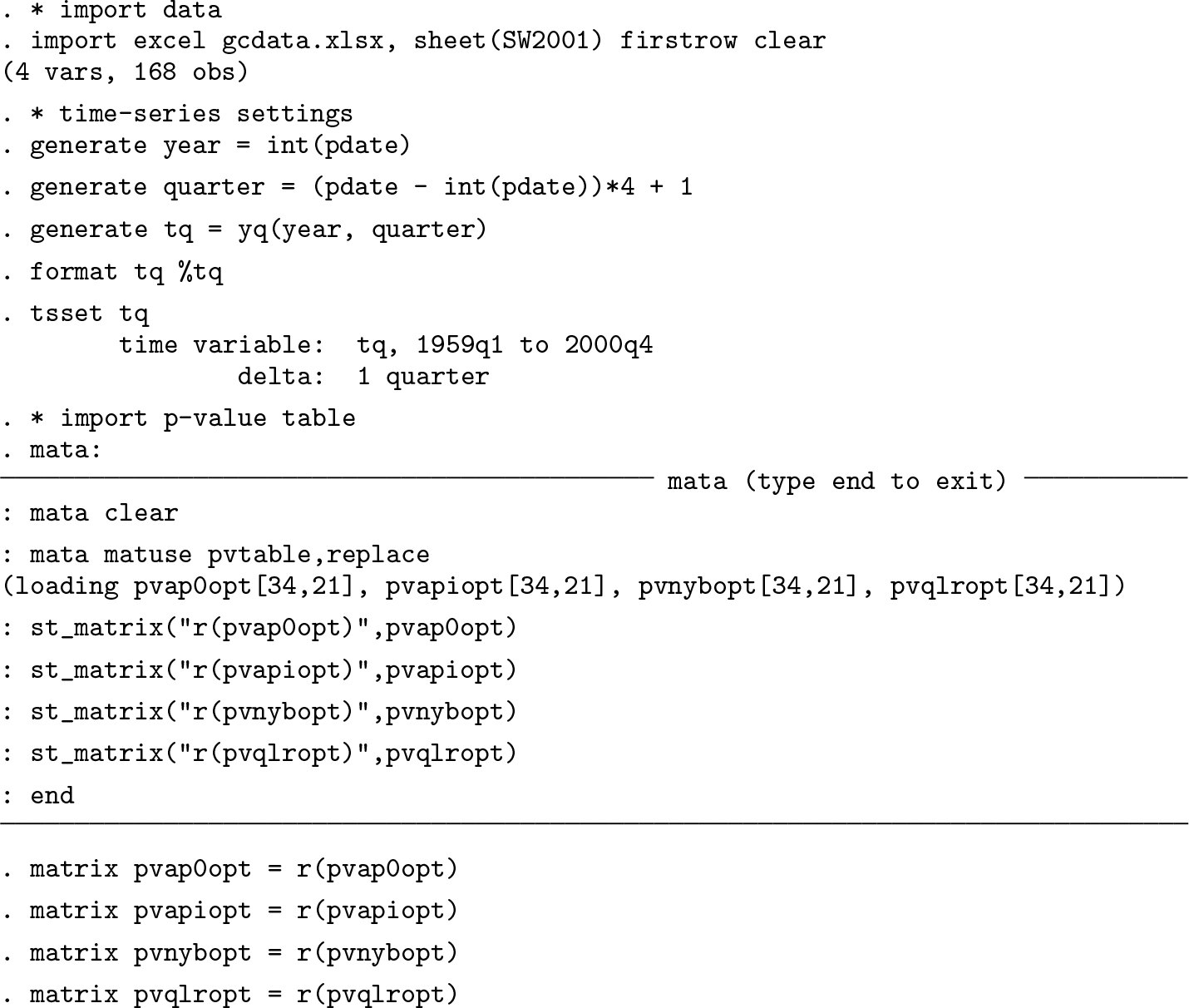

The following scripts implement the Granger causality robust test. We first import the data, claim the data to be time series, and import the p-value tables needed for the tests:

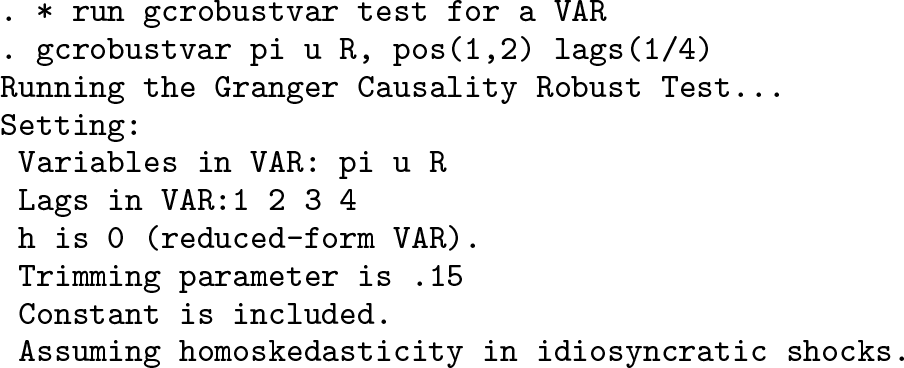

Then, we run the Granger causality robust test using the

The results are displayed in the following script. The

Here is how we get all the inputs of the

Here is how to interpret the results. Let’s take the ExpW* statistics as an example. The value of ExpW* is 9.20, and the p-value is 0.07. Thus, the test rejects the null hypothesis that unemployment (u) does not Granger-cause inflation (π) for all t at the 10% significance level.

4 Comparison with the traditional Granger causality test

In this section, we compare the robust Granger causality tests with the traditional Granger causality test in the three-variable VAR model in Stock and Watson (2001). The VAR includes a constant term and four lags and assumes homoskedastic idiosyncratic shocks.

Table 1 reports the p-values of the traditional Granger causality Wald statistics. The results show that π Granger-causes R, u Granger-causes both π and R, and R Granger-causes u at the 5% significance level.

Table 2 reports the p-values of the robust Granger causality test statistics (for ExpW*, MeanW*, Nyblom*, and QLR*, respectively). We are testing whether the restricted regressor Granger-causes the dependent variable in the presence of instabilities. For example, if we consider the dependent variable π and the restricted regressor R, we are testing whether R Granger-causes π in a way robust to instabilities across time, that is, whether the coefficients of lags of R are constant and equal to zero over time. The p-value of the ExpW* statistics in panel A in table 2 is 0.01, so the test does reject the null at the 5% significance level. Hence, R does Granger-cause π.

Comparing tables 1 and 2, we find the empirical conclusions differ if a researcher uses the Granger causality robust test instead of the traditional Granger causality test. In fact, R does not Granger-cause π at the 5% significance level in the traditional Granger causality test, but R does Granger-cause π at the 5% significance level in the Granger causality robust test according to the ExpW*, Nyblom*, and SupLR* test statistics. Hence, there is empirical evidence that lagged values of R can predict π, but the predictive ability shows up only sporadically over time, which is the reason why the traditional Granger causality test does not detect it.

Traditional reduced-form VAR-based Granger causality tests

NOTE: This table reports p-values of the Wald statistics of the traditional Granger causality test. h = 0 (that is, the reduced-form VAR model), lags = (1, 2, 3, 4), assuming homoskedastic idiosyncratic shocks.

Robust Granger causality tests in the reduced-form VAR

NOTE: This table reports p-values of the statistics of the Granger causality robust test. h = 0 (that is, the reduced-form VAR model), lags = (1, 2, 3, 4), the trimming parameter µ = 0.15, assuming homoskedastic idiosyncratic shocks.

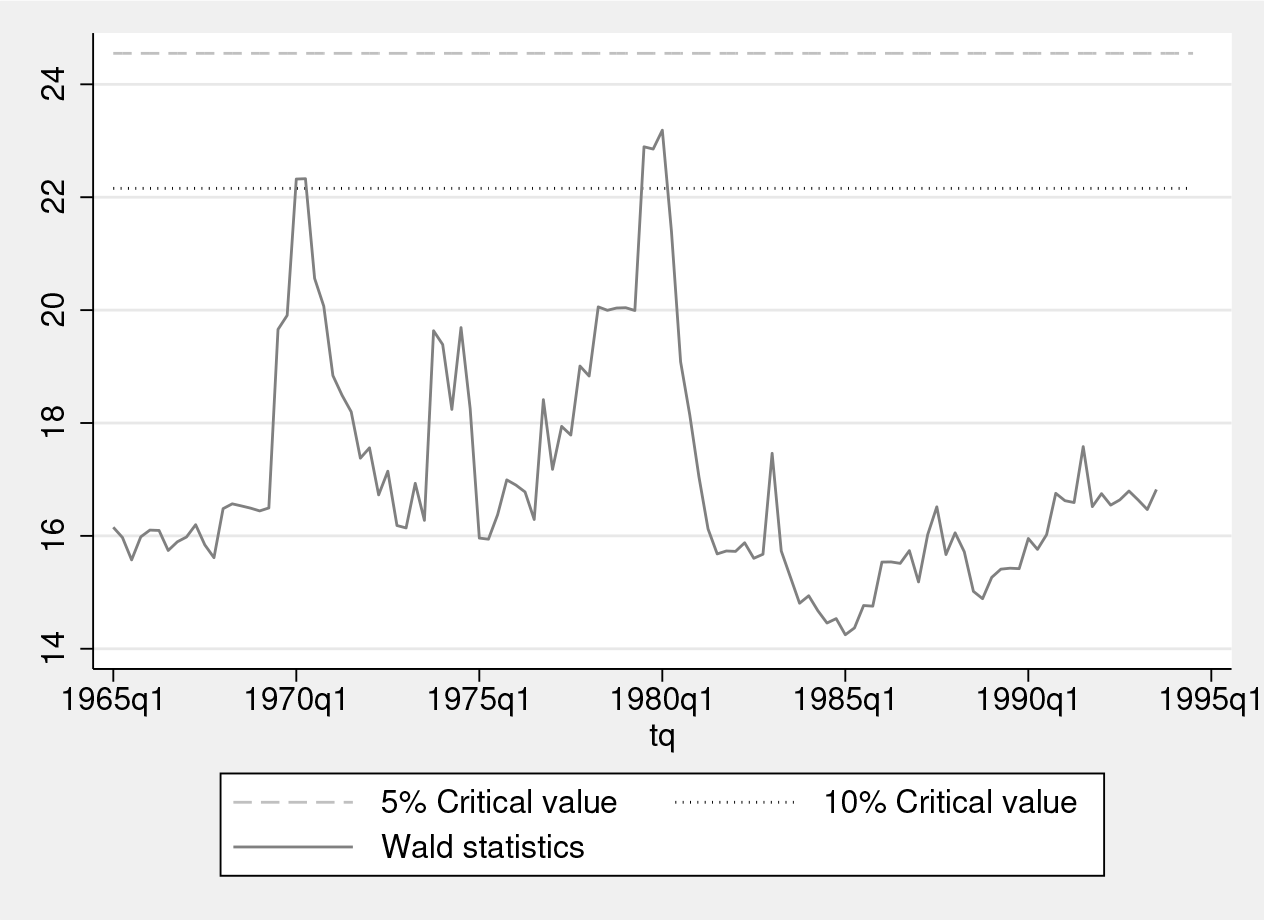

Wald statistics testing whether unemployment (u) Granger-causes inflation (π) against the alternative of a break in Granger causality at time

5 Robust Granger causality tests in LP

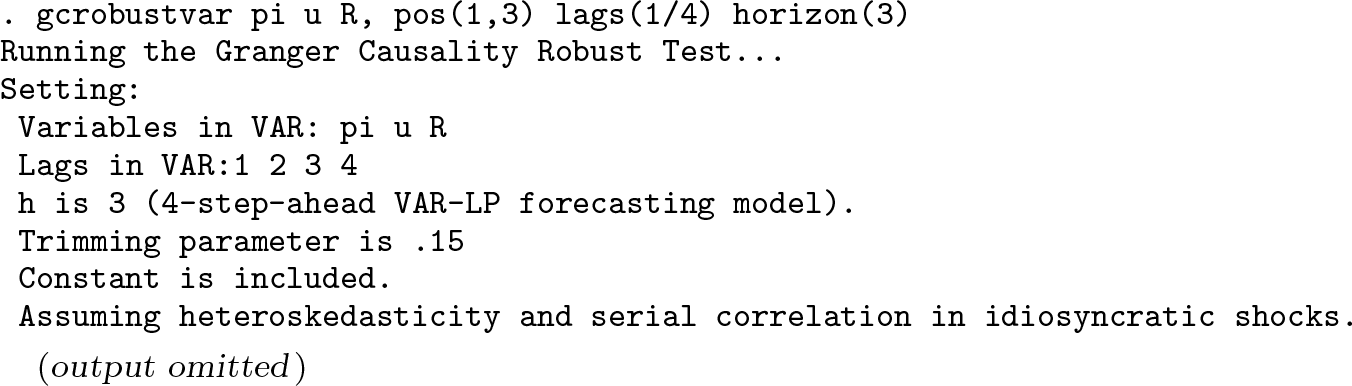

Section 4 considers the reduced-form VAR assuming homoskedastic idiosyncratic shocks. In this section, we extend the VAR analysis to Jord`a’s (2005) LP by implementing the direct multistep VAR–LP forecasting model in (6) and assuming heteroskedastic and serially correlated idiosyncratic errors. Allowing for heteroskedasticity and serial corre-lation is important when the researcher extends the VAR analysis to LP, where the error terms in (6) can be both heteroskedastic and serially correlated.

We consider the one-year-ahead VAR–LP forecasting model with a constant term and four lags. The setting is similar to section 4 except that we specify h = 3 and relax the homoskedasticity assumption.

The following is the command to implement the robust Granger causality test to investigate whether the coefficients on R

t

−

1

, R

t

−

2

, R

t

−

3

, R

t

−

4 are zero across time in the one-year-ahead VAR–LP forecasting model in the equation where the dependent variable is

Table 3 reports the p-values of the robust Granger causality test statistics (the ExpW*, MeanW*, Nyblom* and QLR* statistics, respectively). The results show that lags of inflation (π) can significantly forecast the one-year-ahead unemployment (u) and interest rate (R), lags of unemployment can significantly forecast the one-yearahead inflation and interest rate, and lags of interest rate can significantly forecast the one-year-ahead inflation and unemployment.

Robust Granger causality tests in the direct multistep VAR-LP forecasting model

NOTE: This table reports p-values of the statistics of the Granger causality robust test. h = 3 (that is, the one-year-ahead VAR–LP forecasting model), lags = (1, 2, 3, 4), the trimming parameter µ = 0.15, assuming heteroskedastic and serially correlated idiosyncratic shocks.

7 Programs and supplemental materials

Supplemental Material, st0581 - Vector autoregressive-based Granger causality test in the presence of instabilities

Supplemental Material, st0581 for Vector autoregressive-based Granger causality test in the presence of instabilities by Barbara Rossi and Yiru Wang in The Stata Journal

Footnotes

6 Acknowledgment

The project received funding from the European Research Council (ERC). The Barcelona Graduate School of Economics acknowledges financial support from the Spanish Ministry of Economy and Competitiveness through the Severo Ochoa Programme for Centres of Excellence in R&D (SEV-2015-0563).

7 Programs and supplemental materials

To install a snapshot of the corresponding software files as they existed at the time of publication of this article, type

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.