Abstract

In 2017, more than 22 percent of all U.S. households used an alternative financial service at least once. While fringe-banking enterprises mainly serve people with low or moderate incomes who lack access to more conventional banking services, pawnshops in particular also provide an important and distinct last resort for many customers.

Beyond the Display Windows

It’s a few days after the first polar vortex in early January 2014 and business is slow at Second City Pawn, a pawnshop in a small strip mall on a nondescript intersection of a Chicago neighborhood.

The shop’s doorbell rings, and a man clutching a Mac laptop computer is buzzed through the front door. He walks through the meticulously arranged showroom, past walls that are lined with flat screen televisions, laptop computers, musical instruments, air conditioning units, blenders, and toasters. He continues past a glass case with neatly ordered cell phones, GPS devices, and digital cameras; past another stocked with jewelry. At the back of the shop, he places the laptop on the main service counter and says he wants to pawn it.

Anthony, one of the store’s employees, stands behind the counter. (Pseudonyms are used and other identifying features of people and places may have been changed to protect participants’ identities.) He takes the laptop and inspects it, looking for damage to the body, turning it on to make sure it works, and checking the model and memory. While Anthony goes through his process, the customer offers an explanation—unprompted— for his presence in the shop:

I think because of the budget cuts the city is cracking down on collecting all kinds of tickets. [pause]. I have no problem paying, I just have a really low-paying job right now [pause]. My mom just sold me the computer and I’m really happy with it, but I can’t borrow money from my parents to pay the city.

Without a comment, Anthony offers the man a loan of several hundred dollars and directs him into a booth next to the counter.

From the backroom, with several inches of bulletproof glass between them, Anthony enters some information into his computer and prints two copies of the loan receipt, or “ticket”: one for the store and one for the customer. After signing the store’s copy, the customer takes the cash Anthony slides under the teller window. Thank yous are exchanged, and the customer takes his money and exits the store as uneventfully as he entered, his laptop left sitting on the counter.

The prevailing tendency is to think of pawnshops as marginal operations in the lending economy, sharply contrasted with mainstream loan and credit operations. However, I demonstrate here that thinking of the “fringe” economy as neatly divided from the mainstream banking economy is misleading and ultimately wrong. From the breadth of the customer base and the calculation of credit eligibility to the underservicing of neighborhoods of color, pawnshops mimic many of the features of the mainstream lending economy.

Customers of the Fringe Economy

Second City Pawn’s unassuming storefront represents just one piece of a vast collection of businesses referred to as Alternative Financial Services or the “fringe economy.” These legal businesses, including pawnshops, payday loan centers, and money order and check-cashing outfits, among others, provide credit and payment services to the public but are regulated by different laws than banks. The Federal Deposit Insurance Corporation (FDIC) estimates that the transaction volume of the fringe economy is more than $320 billion annually.

Fringe-banking enterprises mainly serve people with low or moderate incomes who lack access, or have limited access, to more conventional banking services. They make their money off of the high interest rates and fees charged for their services. For pawnshops, an object of some specified market value, as determined by the shop, is used as collateral for a cash loan. To renew the loan and maintain ownership of the object, customers must pay the interest and fees, generally upward of 20 percent per month in the United States. To retrieve the object, customers must pay the principal amount in full—that is, one lump sum—in addition to the outstanding monthly charges.

The word “fringe,” however, is perhaps a bit of a misnomer. In 2017, over 22 percent of all U.S. households used an alternative financial service at least once, according to the FDIC. That figure rises to 50 percent among the approximately 8.4 million U.S. households that are “unbanked,” or lacking a checking or savings account. In reality, a financial system used by nearly a quarter of all households each year is not “fringe.” Instead, these services are a crucial component of the financial lifeway of many Americans.

Pawnshops hold an important place within this alternative financial system. According to the same FDIC survey, they are one of the most popular alternative credit sources in the U.S., with 1.4 percent of all U.S. households having used a pawnshop at least once in 2017, down from nearly 3 percent of all households in 2011. Comparatively, payday loan businesses were used by 1.7 percent of U.S. households in 2017, only a 0.3 percentage point higher usage rate despite the fact that these businesses have received the lion’s share of regulatory attention in recent federal-level policy discussions. The rate of usage increases among the unbanked population, with 4.3 percent of unbanked households using a pawnshop at least once in 2017 compared to 2.9 percent for payday loans.

Pawnshops also offer an important safety net in times of financial crisis. For example, in the years following the Great Recession of 2008, the rate of usage was nearly double. More recently, news outlets such as Business Insider reported a spike in pawnshop use by federal employees during the 2019 thirty-five-day government shutdown, the longest shutdown in U.S. history.

This substantial customer base is also socially and economically diverse. An average day at Second City might bring in a middle-aged woman who lifts her floor-length fur coat as she gets out of her Lexus to avoid the winter slush. It might also see an older man with a scraggly beard and worn clothes who drives to the shop in an old red sedan from his subsidized apartment nearby. Parents arrive with their children, and college-aged adults come in boisterous small groups, cracking jokes and teasing one another all the way through a transaction.

Pawn Shops, where people can get money for things they leave at the shop

Life Pilgrim, Flickr CC

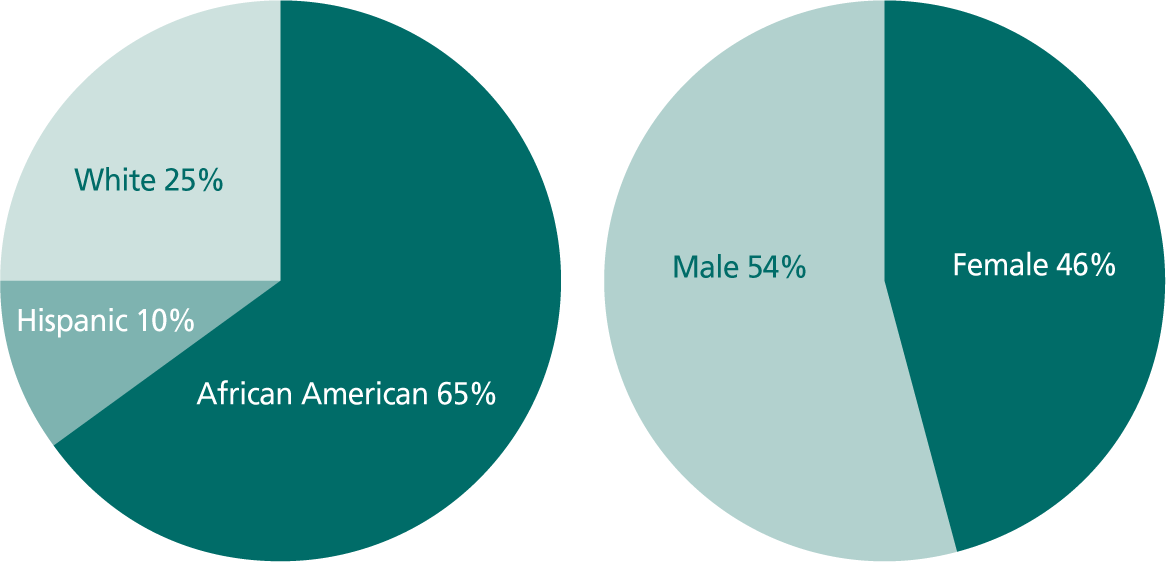

Second City Pawn’s customer demographics by number of loans

Source: Data collected from Second City Pawn, 10/22/2011 – 10/22/2013.

Racial and ethnic minorities are overrepresented in the fringe banking economy at both the local and federal levels, though nearly 40 percent of Black households, 36 percent of Hispanic households, and just shy of 18 percent of Asian households used alternative financial services in 2017, while just over 15 percent of White households did according to the FDIC. Pawnshop patrons are also disproportionately likely to be young and female, without a high school degree—though nearly 15 percent of college-educated households used at least one alternative financial service in 2017.

In other words, no one demographic group dominates the alternative banking sector’s clientele. At the same time, fringe banking use is disproportionate among groups that already face barriers to social and economic equality, including racial and ethnic minorities, women, the less educated, and the young, not to mention lower income households. What’s more, as reported in a 2015 article in The Atlantic, these same individuals are more likely to fall behind on even small debts due to lower wealth and higher rates of legal prosecution, fueling debt-spirals that can be nearly impossible to escape.

The Economy of a Pawnshop

After the customer leaves, Anthony emerges from the backroom to attend to the Mac waiting for him on the showroom counter. The laptop is now legally in pawn and cannot be sold, or even shown to customers, as long as the loan is active. It will sit untouched, accumulating 20 percent interest. To keep the loan active—and to keep the computer in Second City Pawn’s back room—its owner must pay that interest each month. To take the laptop back, he must pay back the loan’s principal in full. If he defaults on the monthly interest payments, the laptop becomes another secondhand acquisition for the shop.

At Second City Pawn, customers generally receive a loan for 50 percent of their object’s used value, though they can get up to 60 percent for gold, thanks to its more reliable global market. Loans are extended for 30 days at a time, and interest and fees for loans under $300 are 20 percent, or the equivalent of a 240 percent APR on a credit card. Of course, a standard credit card or bank loan at 240 percent interest would be unheard of. However, pawnshops are regulated separately from bank branches and credit cards.

In Illinois, most “mainstream” credit is regulated by the Interest Act, which caps annual interest rates at 9 percent. Pawnshops, however, are regulated by the aptly titled Pawnbroker Regulation Act. Still, if 20 percent monthly interest sounds too usurious to be legal even for pawnshops, it is. The Illinois Pawnbroker Regulation Act caps interest at 3 percent per month, or 36 percent APR. However, shops may charge additional “non-interest” fees. Second City Pawn’s interest is technically 3 percent per month for loans less than $300, but the “service charge” is 17 percent per month for these same loans.

Legally, pawnshops cannot sell an item in pawn, but these interest rates mean that it would make little economic sense for them even to want to. Only if a customer stops making the interest payments does the pawnshop obtain legal possession of the object and then try to sell it. However, this is generally a less lucrative outcome, and pawnshops try to prevent loan defaults, often extending the short-term loans indefinitely so long as the customer is paying the interest each month. As an owner of a pawnshop in Beverly Hills reported to the Los Angeles Times, “We like to get the ring back on the finger, the watch back on the wrist and the art back on the wall.”

That does not mean that retrieving the object is made easy. Customers can only take their items back by paying the entire principal loan amount in one lump sum, in addition to the outstanding monthly interest and fees. Since this can be financially difficult for many customers, items often remain in pawn for many months and even years. This is precisely what the pawnshop wants, as collecting interest involves little work on their end.

During my time at Second City Pawn, Joey, the owner, extolled the virtues of his business model to me, proudly declaring that he serves many people who might otherwise be financially destitute, particularly in a moment of crisis. For example, if someone lacking a good credit history is suddenly laid off, he or she can still receive a financial lifeline from Second City Pawn. However, these same theoretical characteristics, Joey explains, make his loans “high risk” and justify the interest rates he charges.

During my time at Second City Pawn, Joey, the owner, extolled the virtues of his business model to me, proudly declaring that he serves many people who might otherwise be financially destitute, particularly in a moment of crisis.

It’s true that pawnshops provide an important, and distinct, last resort for many customers, even compared to other fringe-banking services. Unlike almost all other kinds of credit lenders, including payday lenders, pawnshops extend loans without running a customer’s credit report. For this reason, customers who might be denied credit for unemployment, low income, absence of a checking account, or previous loan defaults would not be denied a pawn-based loan—such information would never be known by the pawnshop.

Less intuitive factors that show up on credit reports may also significantly reduce the likelihood of receiving a traditional bank loan, including not having a high school degree, not being married, or having any kind of arrest or criminal conviction history. The fact that having a criminal conviction, particularly a felony conviction, ruins a person’s credit should not be diminished in an era of mass incarceration, where an estimated 8 percent of all adults have felony records in the United States according to a recent sociological study led by Sarah Shannon. Ruined credit represents yet another collateral consequence of incarceration, or what political scientist Marie Gottschalk refers to as “civil death,” leaving tens of millions of Americans potentially in need of an alternative route to financial assistance.

Joey’s observation that his loans are “high-risk” for these reasons is not entirely accurate, however, because in practice, pawnshops mitigate almost all actual risk through the collateral of the pawned object itself. After just five months of interest payments, a customer has paid the store the total amount of the principal in interest alone. While it may be true that pawnshops such at Second City Pawn offer a “lifeline” to individuals from all walks of life that have fallen on hard times, it can hardly be said to help individuals get out of debt.

Being a Good Customer

Miguel, the store’s assistant manager, tells me about Kay, a repeat customer I often see, who has eight tickets out right now, including a few for more that $1,000 each. One of those is an $1,100 loan from the previous year on which she has already paid $900 in interest. I must look surprised because Miguel adds that Kay is a prototypical “good” pawnshop customer: someone with multiple large tickets, but who reliably pays interest. If taking out more loans means the prolongation of older loans, then that is the best possible outcome for the store, so long as the monthly interest on all the loans is being paid. In other words, a good pawnshop customer looks strikingly similar to someone with good “mainstream” credit. In a pawnshop or on a credit card application, the ideal customer is one who is already indebted but who has established a good payment history.

Thomas Hawk, Flickr CC

For example, FICO, one of the leading credit scoring agencies, places the greatest amount of weight on payment history (35 percent) when composing their scores, followed by credit utilization, or existing lines of credit (30 percent), and the age of one’s open credit lines (15 percent). Each of these would have factored heavily into the decision to not only extend Kay a new line of credit, but to bump-up the credit line. The calculation of creditworthiness at the pawnshop involves far fewer total factors than the complex tabulations made by credit rating agencies, but the bottom line is largely the same.

The gap between traditional banking and alternative credit services shrinks even further when one compares pawnshop lending practices with the subprime mortgages extended at high rates in the early- to mid-2000s. Credit card companies were engaging in similar predatory lending practices over the same period. Furthermore, recent reporting has shed light on the increasingly common mainstream lending practice of small, short-term, high(er) interest loans banks are extending to customers with a wider range of credit scores for “emergency” situations.

The gap between traditional banking and alternative credit services shrinks even further when one compares pawnshop lending practices with the subprime mortgages extended at high rates in the early- to mid-2000s.

The New York Times reported that U.S. Bank, one of the largest banks in the U.S., began offering loans between $100 and $1,000 to help customers cover “unexpected” expenses. Such loans are a response to the creation of the Office of the Comptroller of the Currency in 2018. While the interest and fees are not as high as pawnshops and payday lenders, at 70 percent APR they are still significantly higher than traditional, underwritten bank loans. Such predatory practices thrive on higher fees and high interest rates that are supposedly justified by their customers’ higher risk. Ultimately, the high APR’s make the loans less affordable for the people who take them out, and thus more at risk of default. Such a debt structure led the Center for Responsible Lending to declare in a 2012 report on high fee, high interest rate credit cards that “high-cost penalty fees and interest didn’t mitigate risk, they were the risk.”

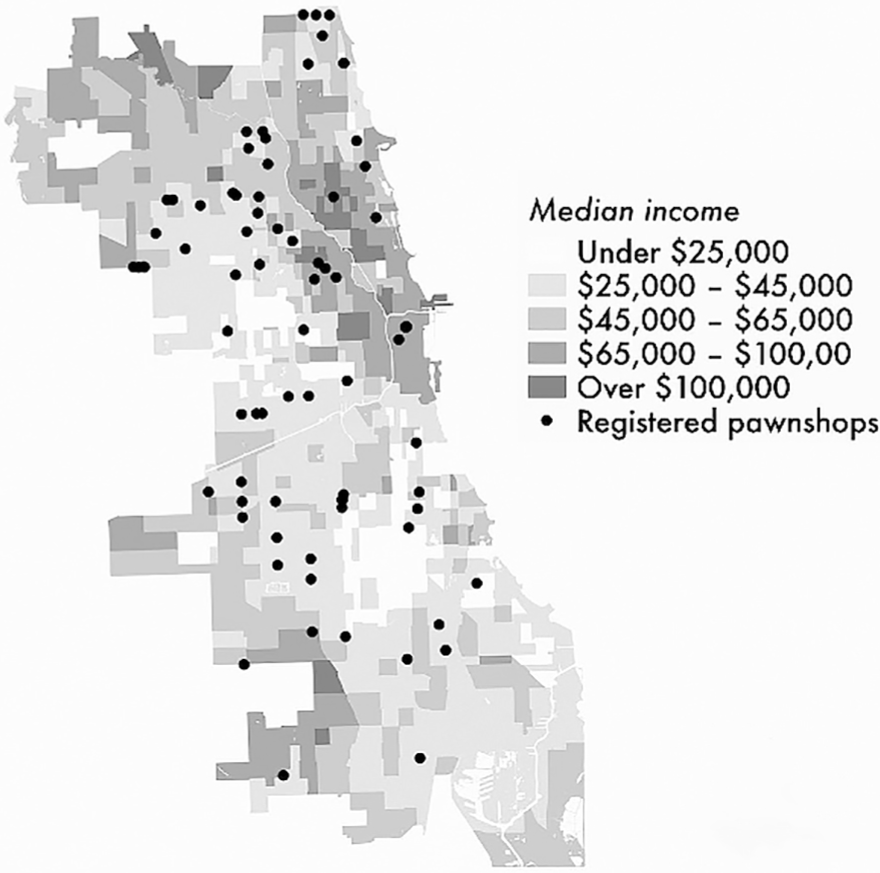

Chicago Median Income and Registered Pawnshops Block-level income data from the 2011 U.S. Census; IL registered pawnshop information from The Illinois

Source: Department of Financial and Professional Regulation 2012 “Directory of Pawnshops in Illinois.”

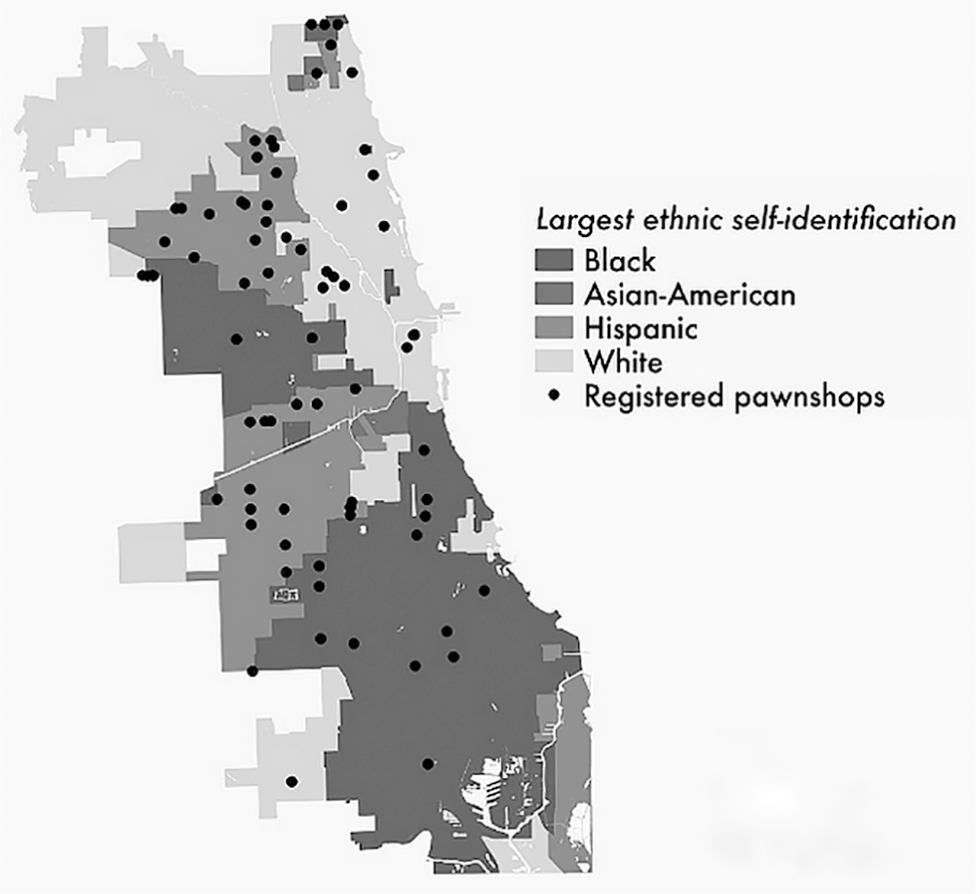

Chicago Racial and Ethnic Self-Identification with Registered Pawnshop

Racial and ethnic self-identification from 2011 U.S. Census

What’s more, existing evidence suggests that pawnshops and other short term, high interest, alternative credit sources are used for more essential living expenses than are credit cards. A 2011 FDIC survey shows that the top reasons for use of alternative services are basic living expenses (such as food, gas, bills, and even rent), making up for lost jobs or decreases in income, buying a home appliance, and house or car repair.

The shop certainly still feels like a different banking model, though, even if many of the practices—and the majority of customers—overlap with the traditional banking sector. After all, Second City is a place where an employee might cajole a well-known Chicago blues musician into playing a few chords of “Foxy Lady” on the guitar he is about to pawn yet again. It is a place where employees tease a regular who is seemingly intoxicated and isn’t wearing shoes, but will still give him a loan.

In addition to the structural factors that make Second City Pawn a potentially more inclusive financial space, the owner and employees also actively cultivate an environment that accepts the transcendence of many norms in banking decorum. This does not go unnoticed by customers. During my research at Second City Pawn, several customers mentioned to me that they felt less judged or simply had a more enjoyable banking experience at fringe banking locations as compared to traditional banks.

Miguel’s remarks about Kay are all the more striking, then, since Miguel is a participant in the cultivation of this looser, less judgmental customer service environment. In fact, Miguel can often be heard poking fun of the customers he perceives act like they are “above” the store or “too good for” it after they leave. Miguel and the other employees also regularly expressed sympathy for customers they knew were going through a period of financial hardship, such as being laid off. They would speak more abstractly about customers as people who just needed a little help making ends meet.

What Kind of Alternative?

Beyond the practices and assessments that occur within the pawnshop, the socio-geographic patterning of pawnshops across the city of Chicago tells its own, related story of connectivity to traditional banking practices in other deeply troubling, but also perplexing, ways.

The map, above on the left, plots shop location against median income in Chicago, clearly showing that pawnshops are not located in the poorest neighborhoods of the city, but instead largely in low- to medium-income areas, as well as areas with a significant range in income. Given the description of a “good customer” as someone with both objects of value to pawn as well as the means to pay the interest each month, but perhaps not quite enough income to pay off the entire loan, this makes sense.

However, this is not a simple story of economics. The second map plots registered pawnshop locations against racial and ethnic identification. This map on the right on p. 22 shows that while pawnshops are located in many racially and ethnically diverse neighborhoods of the city, pawnshops are not well represented in mixed income, majority-Black neighborhoods in Chicago. Much like their conventional counterparts, then, pawnshops appear to be discriminatory in their provision of services to Black residents of the city. This is ironic both because pawnshop customers are disproportionately Black, and also because the business model largely depends on people who have few other options, a group we know to be disproportionately Black. It appears, then, that Black residents of the city have less access even to a banking service that many would describe as predatory.

Local reporting suggests that national pawnshop chains, such as Cash America and EZ Pawn, began an aggressive expansion campaign in Chicago in the early 2010s, following the Great Recession. The Chicago Reader reported in 2012 that the companies had each hired “high-powered” lobbyists with deep connections to local politics. Further, Cash America donated more than $130,000 to Illinois politicians between 2002 and 2012, including aldermen, state legislators, and even the Cook County Board President—and 2019 mayoral hopeful—Toni Preckwinkle. The same article suggests that the ambitions of such shops have been met with resistance in numerous communities by residents, implying that the absence of more pawnshops in predominantly Black low-to-moderate income neighborhoods may be a combination of (historically) discriminatory practices and community efforts to prevent the opening of new pawnshops.

Still, this absence in majority-Black neighborhoods calls the “alternative” offered by pawnshops into question yet again, as its banking model seems ever more closely patterned off of the conventional banking sector, but with an even more vulnerable population and looser regulation. It is another way in which the localized economy of the pawnshop ultimately reproduces and lends greater credibility to the practices that undergird current social and economic inequalities.

The existence of a true alternative is, at least in part, illusory. The financial instruments of the pawnshop are crafted of different working components than their mainstream counterparts. However, calculations ranging from who is deserving of (more) credit, to where pawnbrokers should open a shop, hinge on exceedingly mainstream and often incredibly destructive economic reasoning, masking discriminatory and profit-driven practices in financial calculations and determinations that only appear objective, but in fact, are not.

wild.sproket, Flickr CC

That said, in questioning the labels “fringe” and “alternative,” I don’t wish to suggest that the differences between pawnshops and other alternative financial institutions and traditional banks, in both who and how they serve, are insignificant. However, I do wish to probe the assumptions that labels like “fringe” and “alternative” can hide. For if we do not probe, we will only continue to reify socially constructed labels that justify discriminatory economic practices rather than offering a true means to escape them.