Abstract

In late 2017, the first unified Republican government in 15 years enacted the Tax Cuts and Jobs Act, which cut taxes for corporations and the wealthy. Why did so many citizens support a policy that primarily benefited people richer than them? The self-interest hypothesis holds that individuals act upon the position they occupy in the income distribution: richer (poorer) taxpayers should favor (oppose) regressive policy. Associations between income and policy preferences are often inconsistent, however, suggesting that many citizens fail to connect their self-interest to taxation. Indeed, political psychologists have shown compellingly that citizens can be guided by partisan considerations not necessarily aligned with their own interests. This article assesses public support for the Tax Cuts and Jobs Act of 2017. Using data from the 2018 Cooperative Congressional Election Study as well as contemporaneous ANES and VOTER surveys to replicate our analyses, we show that self-interest and partisanship both come into play, but that partisanship matters more. Personal financial considerations, while less influential than party identification, are relevant for two groups of individuals: Republicans and the politically unsophisticated.

Introduction

In late 2017, the passage of the Tax Cuts and Jobs Act ignited concerns about economic and political inequality (Bartels, 2017; Hacker & Pierson, 2017). The law’s main objective was to reduce the tax burdens of corporations and wealthy individuals (Gale et al., 2018). The ensuing “massive tax relief” (The White House, 2017) proved popular with the Republican base, but not so much with the rest of the country (Newport, 2019; Williamson, 2018). Still, around 40% of voters favored a reform that primarily benefited the top 1% (Scott & Chang, 2017). Why did so many people approve of a policy from which they stood very little to gain?

Despite rising levels of inequality—and public discontent with inequality—political support for redistributive policy remains stagnant (Bartels, 2008; Erikson, 2015; Scheve & Stasavage, 2016). In the past two decades, citizens have tended to reject progressive taxation (Boudreau & MacKenzie, 2018; Franko et al., 2013) and even embrace regressive tax reforms (Bartels, 2005; Krupnikov et al., 2006; Lupia et al., 2007; Slemrod, 2006). This is puzzling, as research on fiscal policy preferences shows widespread support for the principles of tax fairness and progressivity (Ballard-Rosa et al., 2017; Stantcheva, 2020) as well as redistributive programs targeting the poor (Piston, 2018).

In this article, we elucidate public opinion about the Tax Cuts and Jobs Act by bridging self-interest and partisanship, two complementary sources of influence. 1 We show that personal financial considerations shape support for the tax cuts, but only among Republicans. Furthermore, a third factor, political sophistication, produces two opposite patterns of heterogeneity. Our analyses leverage the 2018 Cooperative Congressional Election Study and a policy-focused measure of public support for the Tax Cuts and Jobs Act. We also replicate our results using alternative measures of approval from two separate electoral studies conducted after the 2018 midterm elections. This allows us to validate our hypotheses on more than one dataset and with conceptually distinct measures of public opinion, ensuring the robustness of our findings.

The rest of this paper is structured as follows. We first provide background on the Tax Cuts and Jobs Act and its distributional impact. We then present the literature on public preferences for tax policy, before developing hypotheses about self-interest and partisanship, as well as the interactions of these factors with political sophistication. We describe our dataset, present our model specifications, and report our results and replication tests. We conclude by discussing the relevance of our findings.

The Tax Cuts and Jobs Act

In December 2017, President Donald Trump signed into law the Tax Cuts and Jobs Act (TCJA). Arguably the biggest overhaul of the tax system since the Reagan presidency (Gale et al., 2018), the TCJA was passed by Congress without a single Democratic vote (The New York Times, 2017), fulfilling the President’s promise to give Americans a “big beautiful Christmas present in the form of a tremendous tax cut” (The White House, 2017). The 2017 tax law was seen as Donald Trump’s sole legislative accomplishment, and his party’s last-ditch attempt to enact major legislation to appease its base—and donors—ahead of the 2018 midterm elections.

The TCJA repealed the Affordable Care Act’s individual mandate penalty, scaled back the estate tax, eliminated federal deductions for state and local taxes, and lowered the corporate tax rate from 35% to 21% (Slemrod, 2018). Most significantly, income tax rates were cut for all income groups, giving 80% of Americans an average tax cut of $2,800 in 2018 (Gale et al., 2018). These tax cuts disproportionately benefited the wealthy, however, with 65% of the total federal tax change going to the top 20% of taxpayers (Gale et al., 2018). By Gale et al.’s (2018) estimations, taxpayers in the lowest quintile got an average tax cut of $60 in 2018; by comparison, the top 1% got $51,140, and the top 0.1%, $193,380. After-tax income increased by 0.4% for the lowest quintile, 1.6% for the middle quintile, and 2.9% for the top quintile. Five out of 10 taxpayers in the bottom 20% got a tax cut, compared with nine out of 10 of those in the top 1%. As a result, the U.S. deficit for the 2018–2027 period is projected to be $1.9 trillion larger than it would have been had the TCJA not been enacted (Congressional Budget Office, 2018, p. 5). 2

In 2017, a majority of Americans thought that corporate taxes should be raised rather than lowered, and only a small minority approved of tax cuts for wealthy taxpayers (Fingerhut, 2017). As a result, the public response to the TCJA was negative. The bill was deemed to be regressive and fiscally unsound by academics, tax policy experts, and political commentators alike (Bartels, 2017; Hacker & Pierson, 2017; Scott & Chang, 2017). Even though it initially received support from fewer than 40% of Americans, the TCJA proved popular with the Republican base and the party’s donor class (Bartels, 2017; Green & Deatherage, 2018; Jacobson & Liu, 2020). Nevertheless, the tax law’s overall unpopularity likely contributed to Republicans’ loss of the House of Representatives in the 2018 midterm elections (Newport, 2019; Williamson, 2018).

Explaining Tax Policy Preferences: Self-Interest and Partisanship

According to the self-interest hypothesis, citizens’ political preferences are determined by their economic standing (Chong et al., 2001; Franko et al., 2013; Sears & Citrin, 1982). Meltzer and Richard’s (1981) rational theory of the size of government predicts that, as income inequality rises, the median voter will come to support higher levels of taxation in order to increase revenue transfers from the top to the bottom half of the income distribution. Indeed, lower-income Americans sometimes enact their self-interest by supporting redistributive proposals (Newman & Teten, 2021). As to wealthy Americans, they often hold views on the economy, regulations, taxes, inequality, and public spending that are more conservative than those of the general electorate (Cohn et al., 2019; Page et al., 2013). Research on policy responsiveness suggests that self-interest plays a key role in the policy process, which often sides with the political priorities of the wealthy (Bartels, 2008; Branham et al., 2017; Erikson, 2015; Gilens & Page, 2014).

Oftentimes, however, political predispositions can prove more influential than self-interest. Partisan group loyalty molds political behavior and public opinion (Campbell et al., 1961; Zaller, 1992). Party identification dictates policy preferences, especially for issues on which political elites are polarized (Barber & Pope, 2019; Druckman et al., 2013). On such issues, self-interest can sometimes prove a weak or unreliable predictor of opinion (Lowery & Sigelman, 1981; Sears & Funk, 1990). The Bush tax cuts of the early 2000s are a case in point. In a study linking ignorance to public approval, Bartels (2005, p. 16) argues that “Americans supported tax cuts not because they were indifferent to economic inequality, but because they largely failed to connect inequality and public policy.” His analyses show that that low- and middle-income taxpayers were more likely than the wealthy to support Bush’s fiscal agenda. In the same vein, Slemrod (2006) finds that the poor were not less likely than the rich to support the estate tax repeal, suggesting that fiscal misinformation was at play. Reviews of these findings by Krupnikov et al. (2006) and Lupia et al. (2007) point toward a simpler explanation: voters adopted their parties’ positions. 3

Previous research suggests that fiscal preferences are often determined by political predispositions, but that self-interest can sometimes prove influential (Chong et al., 2001; De Benedictis-Kessner & Hankinson, 2019; Franko et al., 2013; Klar, 2013). With respect to the TCJA, self-interest and partisanship could thus operate simultaneously. Self-interest should matter when “clear, substantial costs and benefits” are at stake (Sears & Funk, 1990, p. 255). This is often the case for issues pertaining to economic policy (Anzia & Moe, 2017; Chong et al., 2001; De Benedictis-Kessner & Hankinson, 2019; Franko et al., 2013; Sears & Citrin, 1982). Differences of opinion between low- and high-income citizens should also arise in the context of inter-class conflict, which can sometimes cut across partisanship (Piston, 2018).

We formulate a first set of hypotheses:

In the weeks leading up to the passage of the TCJA, the Republican Party and particularly President Trump framed the bill as a “massive tax relief for American families,” appealing explicitly to taxpayers’ self-interest: “The typical family of four earning $75,000 will see an income tax cut of more than $2,000, slashing their tax bill in half. It’s going to be a lot of money. You’re going to have an extra $2,000” (The White House, 2017). Moreover, a common argument in favor of the TCJA was that it would lead to economic growth, thus benefiting the American public by delivering not only tax cuts, but also new jobs and higher wages (Slemrod, 2018, pp. 73–74). It is thus clear that economic considerations shaped public views about this policy.

Of course, in addition to its explicit financial appeal, a defining characteristic of the TCJA was its overtly partisan nature. The bill did not receive a single Democratic vote in Congress and was only popular among Republican voters (Bartels, 2017; Williamson, 2018). For the most part, the set of policies included in the TCJA responded to partisan, conservative preferences for a smaller government and a more regressive tax system (Fingerhut, 2017). Republican members of Congress rallied around the TCJA hoping that their prospects in the 2018 midterm elections would improve (Green & Deatherage, 2018). Unsurprisingly, partisan cues played a large role in shaping (and polarizing) public approval for the TCJA (Hacker & Pierson, 2017; Williamson, 2018).

Personal Financial Considerations Better Predict Republicans’ Views

Considering how the Republican messaging on the TCJA leaned on taxpayers’ self-interest, the prospect of a financial gain should have a stronger appeal among these partisans:

Three complementary mechanisms should lead to this heterogeneous relationship. First, class cleavages inside the Republican Party—but not the Democratic Party—result in intra-partisan differences in policy preferences that can be explained by income (Newman & Teten, 2021, p. 248). Rich Republicans are more likely than their poorer co-partisans to have regressive views on taxation; mainly, they disproportionately favor cutting taxes on the wealthy and corporations (Fingerhut, 2017). The TCJA’s explicit appeal to high-income taxpayers may have proven less popular with the party’s working-class segment.

A second reason for expecting self-interest to yield stronger effects among Republicans stems from the competing identities inside their party (Chong et al., 2001; Klar, 2013). High-income Republicans should favor the TCJA more strongly than low-income Republicans, as the latter group of citizens might be “cross-pressured” by their self-interest and partisanship (De Benedictis-Kessner & Hankinson, 2019). Rich Republicans should be among the strongest supporters of the Trump tax cuts because—at least in this policy debate—their partisan allegiances align with their self-interest. As for poor Republicans, their party’s fiscal agenda is at odds with their class interests: their level of support for the TCJA should be more tepid. Finally, if high-income Democrats were solely guided by self-interest, they would embrace the TCJA; but their party identification should bring them to oppose the TCJA as much as their low-income co-partisans.

A third reason why self-interest should differentially predict partisans’ views about the TCJA is that Republicans and Democrats have different core values and beliefs. Republicans’ worldview is centered on free enterprise and self-determination (Feldman, 1988); their decision-making prioritizes personal gain, which in the case of the TCJA was roughly proportional to one’s family’s income. As for Democrats, their egalitarian attitudes should lead them to prefer progressive policy (i.e., redistribution) over regressive policy (e.g., tax cuts), regardless of which might personally benefit them the most. This is not to say that only self-interested individuals can support tax cuts, or that none of those opposing them are self-interested. For example, a low-income voter who favors redistribution is acting upon her own interest, as she would likely benefit from a more equalitarian economy. 4 Our argument is simply that, whereas high-income Republicans might favor the TCJA because this policy personally benefits them, high-income Democrats should not be moved by the prospect of a tax cut, because such a tax cut would lead to a more regressive tax system and a more unequal society, which goes against their ideology.

The Conditioning Role of Political Sophistication

Well-informed citizens have different opinions than the ill-informed (Althaus, 1998; Converse, 2006; Gilens, 2001). Previous public opinion research has pointed to citizens’ low levels of sophistication to explain public support for regressive tax policy (Bartels, 2005; Piston, 2018; Slemrod, 2006). Yet, this line of research does not ask if some individuals might be more prone than others to act upon their self-interest.

Citizens use information shortcuts rather than “encyclopedic” knowledge to form opinions on complex, technical issues (Lupia, 1994). Party identification is likely the most powerful voter heuristic (Cohen, 2003). Reliance on partisan cues may lead individuals to support policies that undermine their own financial interests (Boudreau & MacKenzie, 2018). Conversely, those who lack such partisan shortcuts (i.e., those unaware of the parties’ positions on a given issue) may turn to other easily available information to make up their mind.

Political sophistication should condition self-interest and partisanship in opposite ways. Since poorly sophisticated individuals exhibit little ideological constraint (Converse, 2006), their decision-making need not follow a party line, allowing them to rely on financial considerations instead. This entails that the highly sophisticated are guided first and foremost by partisan considerations (Krupnikov et al., 2006; Lupia et al., 2007):

Data, Measurements, and Method

We use data from the 2018 Cooperative Congressional Election Study (CCES) Common Content, a nationally representative, large, online survey conducted by YouGov. 5 The dataset includes 60,000 respondents who completed pre- and post-election questionnaires. 6

In 2018, the CCES asked the following question about the TCJA: Would you support or oppose a tax bill that does all of the following? Cuts the Corporate Income Tax rate from 39 percent to 21 percent. Reduces the mortgage interest deduction from $1 million to $500,000. Caps the amount of state and local tax that can be deducted to $10,000 (previously there was no limit). Increases the standard deduction from $12,000 to $25,000. Cuts income tax rates for all income groups by 3 percent.

This policy-focused question provides respondents with an overview of the TCJA’s main components without mentioning the law by name. 7 The dichotomous dependent variable indicates whether respondents have a favorable opinion about the TCJA. Overall, 56% of respondents support the described tax bill.

We construct three explanatory variables: self-interest, partisanship, and political sophistication. Since financial benefits from the TCJA were proportional to taxpayers’ income (Tax Foundation Staff, 2017), our proxy for self-interest is the respondent’s family income, a 16-level variable ranging from less than $10,000 (0) to more than $500,000 (1). For partisanship, we use the traditional sevenfold classification, coded 0 for a strong Democrat and 1 for a strong Republican. To measure political sophistication, we construct an index by averaging two distinct but complementary indicators: political knowledge and political interest. 8 Political knowledge scales based on answers to factual questions have been used robustly to measure political awareness (Zaller, 1992). Yet, this measure alone fails to capture information about “specific policy-relevant facts” (Gilens, 2001, p. 280). Thus, we also account for political interest, which conveys “exposure to the information environment” (Jerit et al., 2006, p. 269). 9

Empirical Strategy

To test our first two hypotheses, we simply regress (using OLS) public support for the TCJA (

For our third hypothesis, we simply add the multiplicative interaction of income and party identification (

Here, the parameter of interest is the interaction coefficient,

The last equation incorporates respondents’ political sophistication (

The parameters

Results

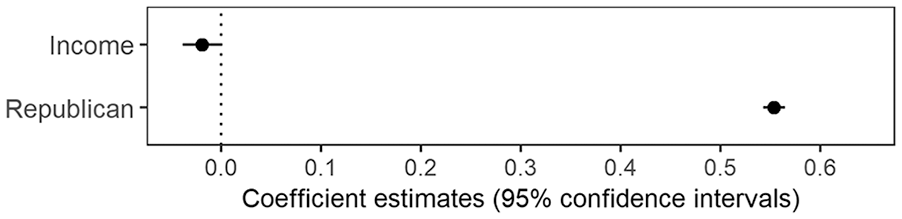

Figure 1 plots the first model’s coefficients. This allows for the baseline comparison of self-interest and partisanship’s effects on support for the TCJA. In this additive model, it is clear that party identification has more influence on opinion than self-interest, the effect of which is indistinguishable from zero. The difference of opinion between the poorest and richest respondents is negligible. As for party identification, its effect is quite large: the probability of supporting the tax cuts increases by 55 percentage points for a strong Republican relative to a strong Democrat. 12

Income, party identification, and public support for the TCJA.

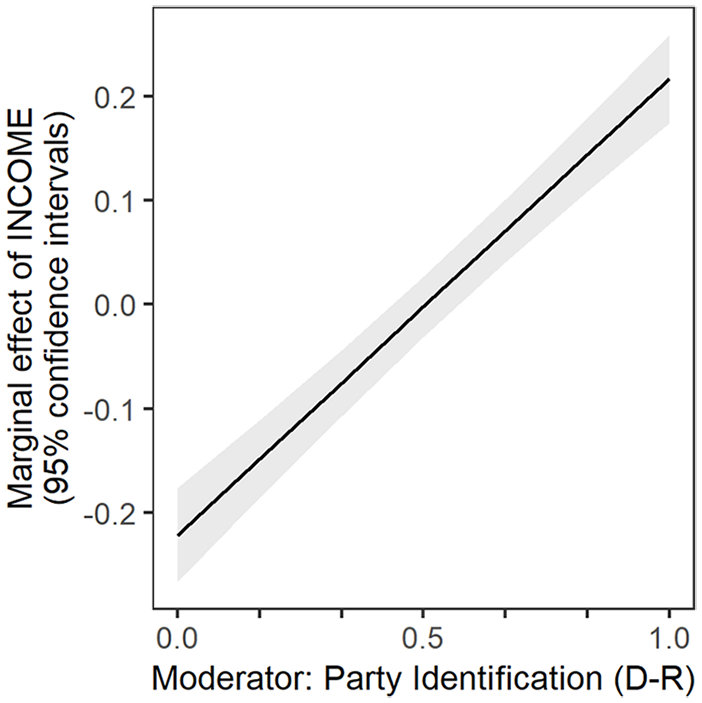

These results conceal significant heterogeneity. Figure 2 plots the second model’s interaction between self-interest and partisanship. The interaction coefficient is positive: as party identification increases from strong Democrat to strong Republican (horizontal axis), the marginal effect of income becomes larger and shifts from negative to positive (vertical axis). It appears that the difference in opinion between low- and high-income respondents is only consistent among Republicans (a similar dynamic between income and party identification is observed by Newman & Teten, 2021). The average predicted probability of supporting the tax cuts is 100% when income is set at its highest value, and 79% when it is set at its lowest value. Intriguingly, among Democrats, the marginal effect of income is negative: the average probability of supporting the tax cuts is greater for low- than for high-income Democrats (39% compared to 17%).

Interaction of income and party identification.

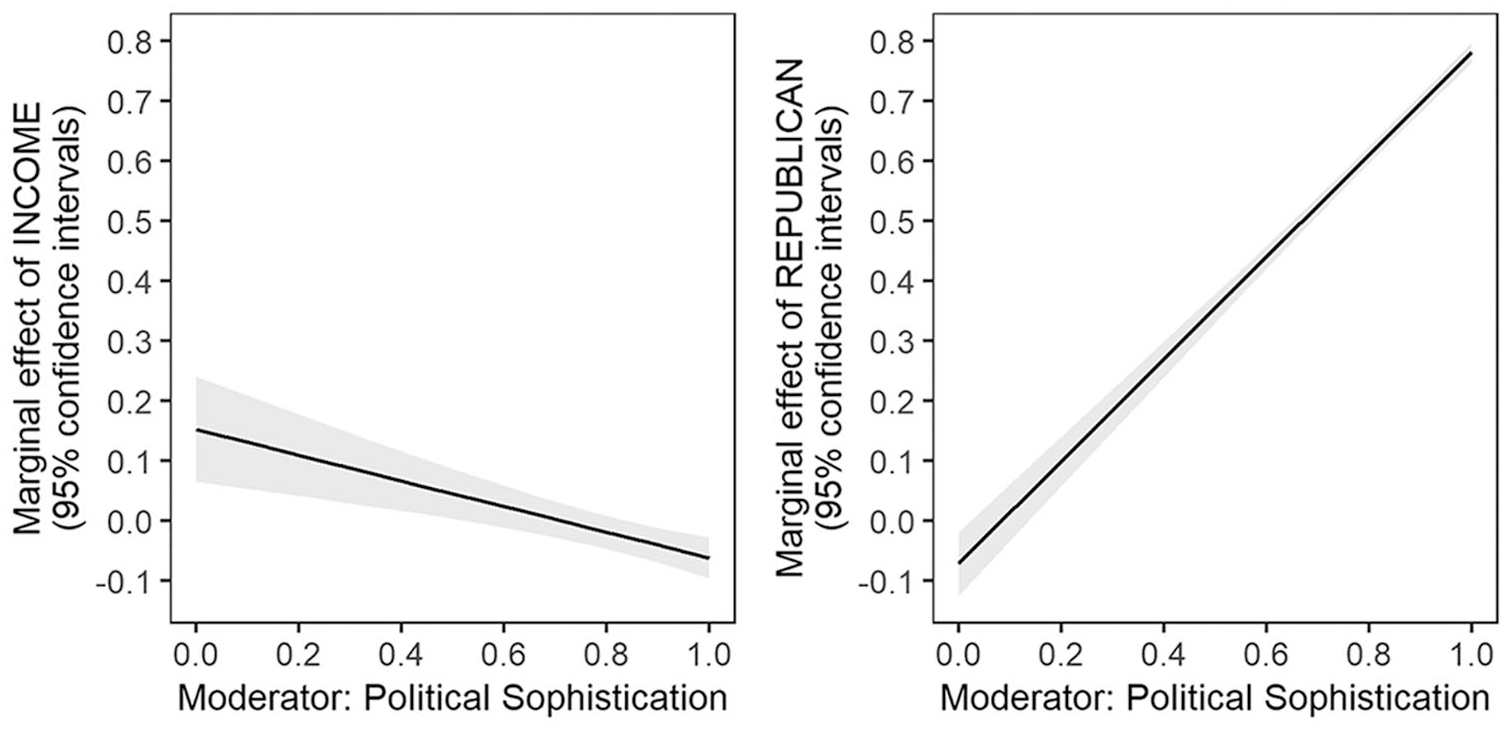

Taking respondents’ political sophistication into account allows us to draw a richer picture of this self-interest-partisanship dynamic. Figure 3 plots the two interactions specified in the third model. Political sophistication produces two opposite patterns of moderation.

Interactions of income, party identification, and political sophistication.

The interaction between income and sophistication (left panel) is negative: as political sophistication increases (horizontal axis), the gap between the richest and poorest respondents shrinks (vertical axis). Indeed, among the least sophisticated respondents, the poorest are 15 percentage points less likely than the richest to support the TCJA; among the most sophisticated, the poor are no less likely than the rich to approve of the tax cuts.

The interaction between party identification and sophistication (right panel) is, as expected, positive: political sophistication (horizontal axis) widens the partisan gap in opinion (vertical axis). Looking at the least sophisticated respondents, strong Republicans are no more likely than strong Democrats to voice support for the tax cuts; among the most sophisticated, strong Republicans are 78% points more likely than strong Democrats to support the TCJA.

In these analyses, we measure political sophistication using political knowledge and political interest. While this ensures that our moderator captures more than one dimension of citizens’ political awareness (Zaller, 1992), one limitation remains: this measure is focused on information about politics, whereas the policy debate we analyze is economic in nature. Taxation-specific knowledge scales are absent from most electoral studies. If specific knowledge about tax policy and the TCJA had been measured, our analyses would more faithfully have captured the role that political sophistication played in this policy debate.

Does the Self-Interest-Partisanship-Sophistication Model Replicate?

While the dependent variable we analyze is a straightforward measure of support for (or opposition to) the TCJA, it is divorced from the political context surrounding the TCJA. The CCES question is overly technical, leaving little room for respondents to evaluate the tax law more broadly. Replicating our analyses on different data is necessary to guarantee that our findings are robust.

To achieve this, we examine two conceptually different dependent variables from two additional datasets: the 2018 Pilot Study from the American National Elections Studies (ANES) and the 2019 Views of the Electorate Research (VOTER) Survey. Like the CCES, these are online, nationally representative surveys fielded by YouGov following the 2018 midterm elections. The ANES survey comprises 2,500 respondents, and the VOTER survey more than 6,000. Both surveys tap into respondents’ approval of the TCJA, although the VOTER question is the only to mention the Republican President by name. 13 We code two continuous dependent variables ranging from 0 to 1, where 1 means the respondent fully supports the TCJA: 14

Do you approve, disapprove, or neither approve nor disapprove of the 2017 tax cuts?

Do you favor or oppose the tax plan that was passed by Congress and signed into law by President Trump?

Overall, 36% of ANES respondents and 40% of VOTER respondents hold a favorable view about the TCJA (the variables’ means are 0.49 and 0.46 respectively). We code the same explanatory and control variables as we do for the CCES. 15

Appendix G presents a regression table for each survey. All in all, these results closely match those presented above. In the baseline model, income has a weak or negligible effect on support for the TCJA, whereas party identification yields very large effects. Here, too, partisanship moderates self-interest’s effects on opinion, with high-income Republicans emerging as the strongest supporters of the tax cuts. Allowing both explanatory factors to vary based on political sophistication produces the same patterns of moderation as those observed before. The interactions of self-interest and sophistication are negative, whereas the interactions of partisanship and sophistication are positive. Among the most sophisticated respondents, income yields null effects; among the least sophisticated, income moderately increases approval. Inversely, party identification has dramatically large effects when sophistication reaches its highest value, but null or inconsistent effects when the moderator is set at its lowest value.

Discussion

This study sought to determine the influence of self-interest and partisanship on public opinion about the TCJA. We validate our theoretical expectations about the conditional importance of both factors using three independent electoral studies with conceptually distinct dependent variables. Despite differences in measurements and samples, we observe very similar results in the three surveys, which confirms our findings’ robustness and external validity.

Our results tell a relatively simple story. First, party identification is the main factor driving opinion—Republicans support their party’s tax agenda, which Democrats oppose. The sheer magnitude of this party effect is striking. As to self-interest, its effects are limited in size and scope. The story becomes more intriguing when political sophistication enters the scene. Self-interest has a moderate effect among the least sophisticated respondents; it yields no influence whatsoever among the most sophisticated. Conversely, partisanship does not consistently shape the views of the least sophisticated respondents; it very strongly predicts the preferences of the most sophisticated. Put differently, party identification does not matter for the least informed citizens, who instead tend to rely (to an extent) on self-interest. Self-interest does not influence the most informed citizens, whose opinions about the TCJA simply reflect their partisanship. It would be surprising if these dynamics were specific to the policy debate at hand; most likely, they offer evidence for a novel self-interest-partisanship-sophistication model of tax-related public opinion.

Our findings about partisanship’s role in shaping public support for the TCJA might seem unsurprising, but they allow us to draw a novel conclusion about mass preferences for taxation more broadly. The prospect of personal financial benefits seems to only be important for those already predisposed to favor their party’s tax law; a higher income yields additional support (i.e., a “bonus”) among these individuals. In no case do personal financial considerations reverse opinion, but they do seem to (slightly) “cross-pressure” some partisans (De Benedictis-Kessner & Hankinson, 2019). Self-interest explains the difference between strong and overwhelming support among Republicans; it does not really make a difference among Democrats. In short, GOP partisans are more likely not only to support their party’s tax cuts, but also to recognize and act upon their individual financial considerations. Partisan cleavages—at least where taxation is concerned—extend to self-interest, inasmuch as this framework only seems to be compatible with the (conservative) worldview of Republicans. Future research on self-interest would benefit from taking partisan heterogeneity into consideration.

One might hope that higher levels of knowledge, information, and awareness about public policy could translate into more consistent, rational opinions (Converse, 2006). Following this intuition, political sophistication should strengthen, rather than weaken, the link between self-interest and public opinion (as argued by Piston, 2018). But our data show that sophistication simply fuels partisanship. Our evidence confirms that well-informed citizens are for the most part well-behaved partisans (Lodge & Taber, 2013; Zaller, 1992).

Previous studies have tackled similar research questions as ours, but without considering how political sophistication conditions self-interest. Fifteen years ago, Bartels (2005, p. 24) asserted that the popularity of the Bush tax cuts was “entirely attributable to simple ignorance.” We reach a different verdict regarding the Trump tax cuts. Far from being “confused about what is in their own interests” (Bartels, 2005, p. 26), ill-informed citizens display preferences that are (slightly) more consistent with self-interest than those of their well-informed peers. The former are unconstrained by partisan loyalty, whereas the latter simply line up behind their parties’ policies. We are unable to determine which of these two groups of citizens is more “simple-minded” (Bartels, 2005, p. 21, 28) than the other.

Appendices

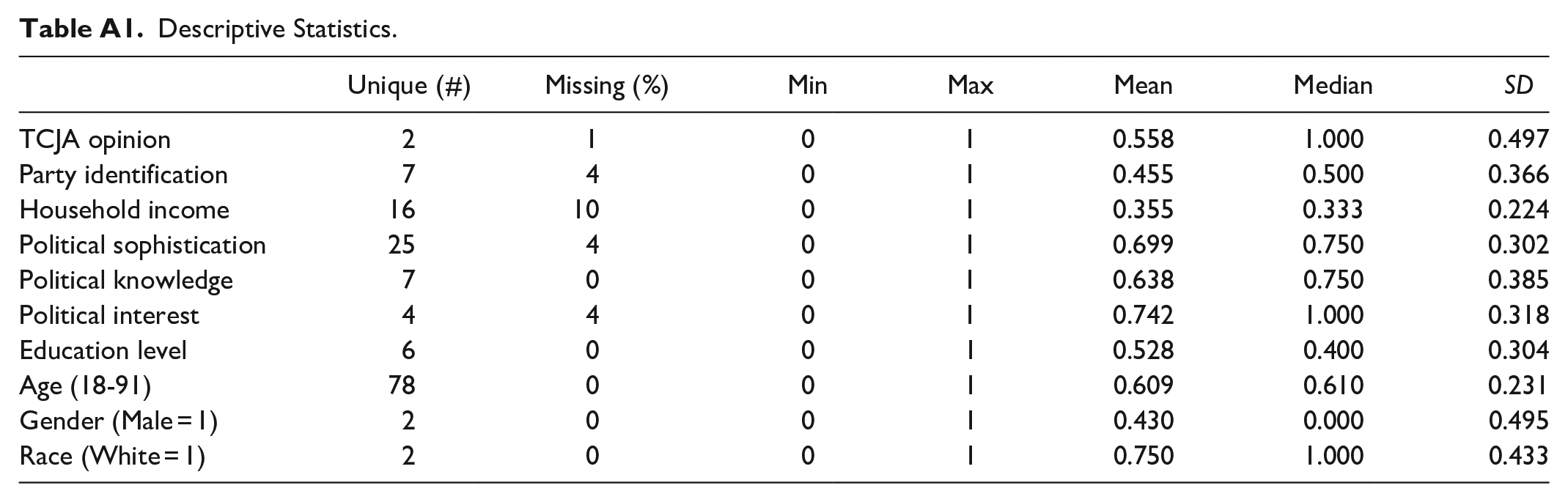

Appendix A. Descriptive Statistics

Descriptive Statistics.

Appendix B. Questions Used for the Political Sophistication Index

Political Knowledge Scale (Cronbach’s

Which party has a majority of seats in [U.S. House of Representatives]? [Republicans; Democrats; Neither; Not sure]

Which party has a majority of seats in [U.S. Senate]? [Republicans; Democrats; Neither; Not sure]

Which party has a majority of seats in [State Senate]? [Republicans; Democrats; Neither; Not sure]

Which party has a majority of seats in [State Lower Chamber]? [Republicans; Democrats; Neither; Not sure]

Political Interest:

Some people seem to follow what’s going on in government and public affairs most of the time, whether there’s an election going on or not. Others aren’t that interested. Would you say you follow what’s going on in government and public affairs. . .

[Most of the time; Some of the time; Only now and then; Hardly at all; Don’t know]

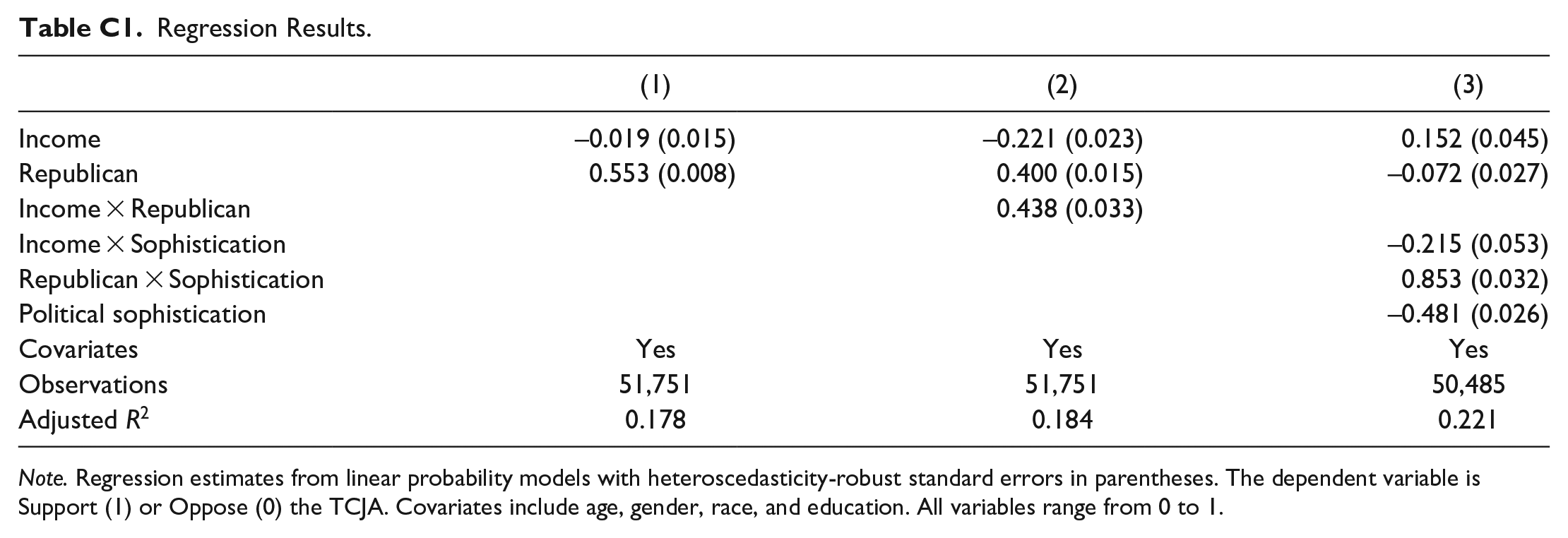

Appendix C: Regression Results

Regression Results.

Note. Regression estimates from linear probability models with heteroscedasticity-robust standard errors in parentheses. The dependent variable is Support (1) or Oppose (0) the TCJA. Covariates include age, gender, race, and education. All variables range from 0 to 1.

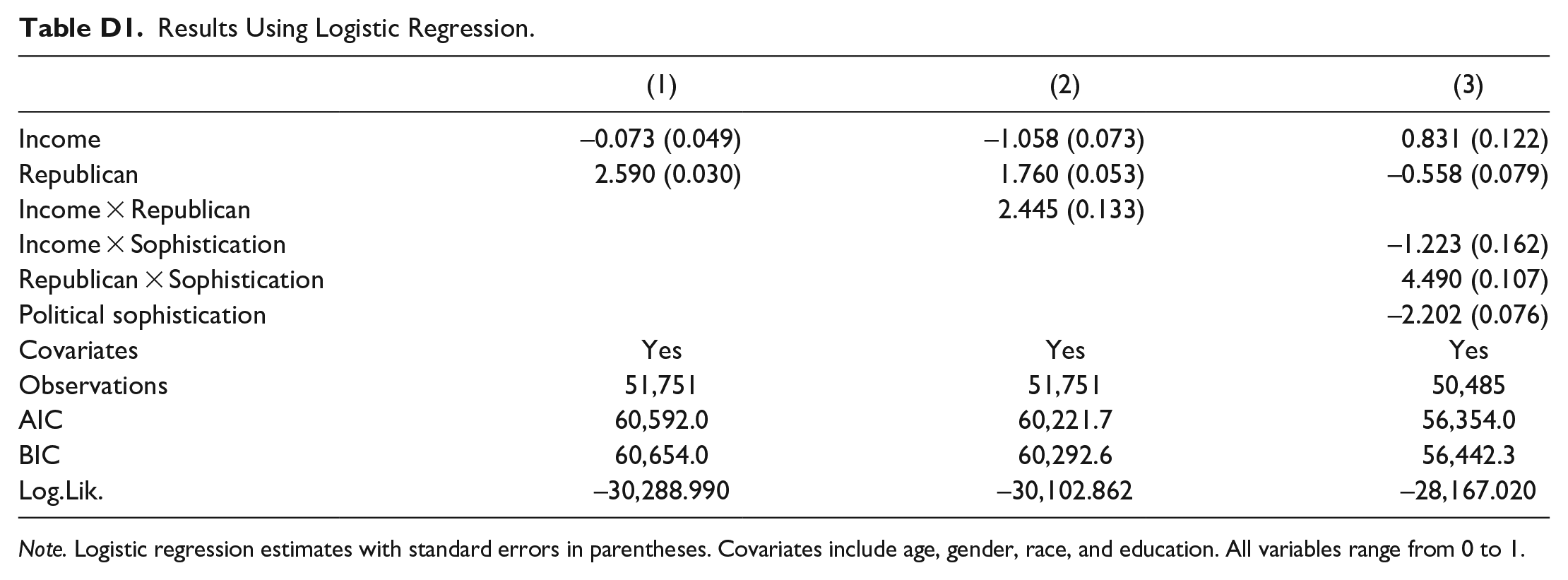

Appendix D: Alternative Estimations

Results Using Logistic Regression.

Note. Logistic regression estimates with standard errors in parentheses. Covariates include age, gender, race, and education. All variables range from 0 to 1.

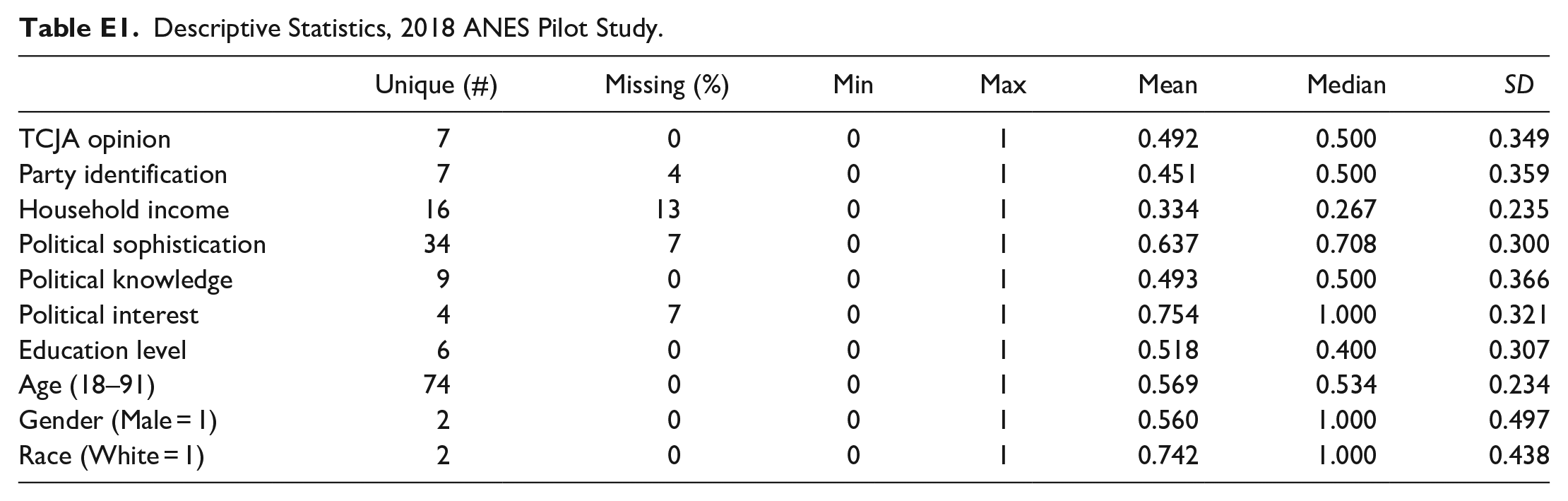

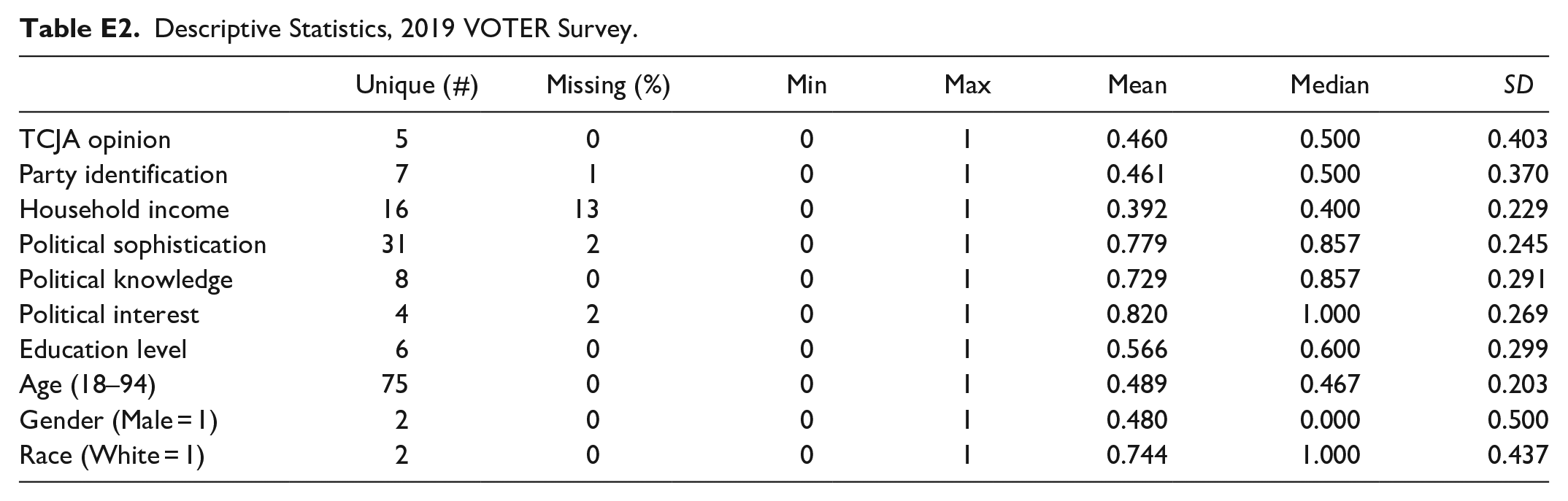

Appendix E: Descriptive Statistics, ANES and VOTER

Descriptive Statistics, 2018 ANES Pilot Study.

Descriptive Statistics, 2019 VOTER Survey.

Appendix F: Political Knowledge Scales, ANES and VOTER

2018 ANES Pilot Study (Cronbach’s

What job or political office is now held by John Roberts? [Open-ended]

What job or political office is now held by Angela Merkel? [Open-ended]

For how many years is a United States Senator elected—that is, how many years are there in one full term of office for a U.S. Senator? [Open-ended]

On which of the following does the U.S. federal government currently spend the least? [Foreign aid; Medicare; National defense; Social Security]

2019 VOTER Survey (Cronbach’s

For how many years is a United States Senator elected—that is, how many years are there in one full term of office for a U.S. Senator? [Open-ended]

Taking the November election results into account, which party will have the most members in the U.S. House of Representatives? [Republicans; Democrats; Don’t know]

Taking the November election results into account, which party will have the most members in the U.S. Senate? [Republicans; Democrats; Don’t know]

What job or political office does Theresa May currently hold? [U.S. representative; Secretary of Education; Prime Minister of the United Kingdom; President of Australia; Don’t know]

What job or political office does Neil Gorsuch currently hold? [U.S. Senator; Governor; Supreme Court Justice; White House Chief of Staff; Don’t know]

How many votes does it take for the U.S. Senate to override a presidential veto? [50; 51; 67; 100; Don’t know]

According to the Constitution, which part of government has the power to declare war on another country? [The President; Congress; The Supreme Court; The Secretary of Defense; Don’t know]

Appendix G: Regression Results, ANES and VOTER

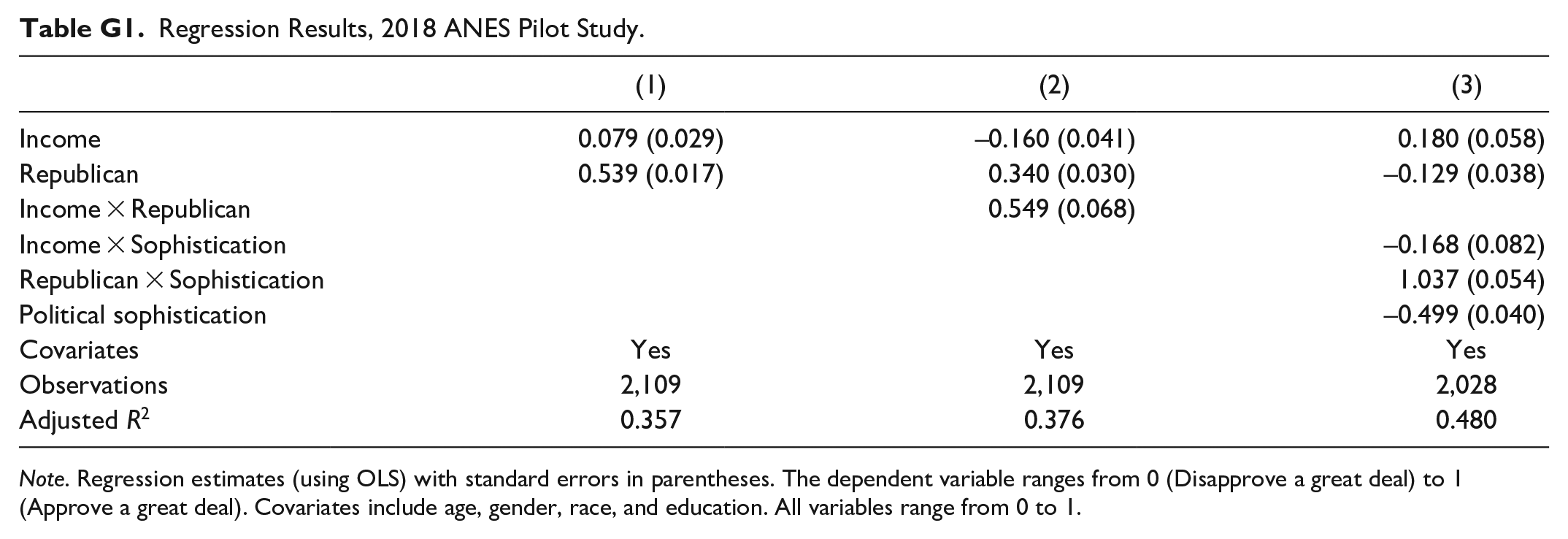

Regression Results, 2018 ANES Pilot Study.

Note. Regression estimates (using OLS) with standard errors in parentheses. The dependent variable ranges from 0 (Disapprove a great deal) to 1 (Approve a great deal). Covariates include age, gender, race, and education. All variables range from 0 to 1.

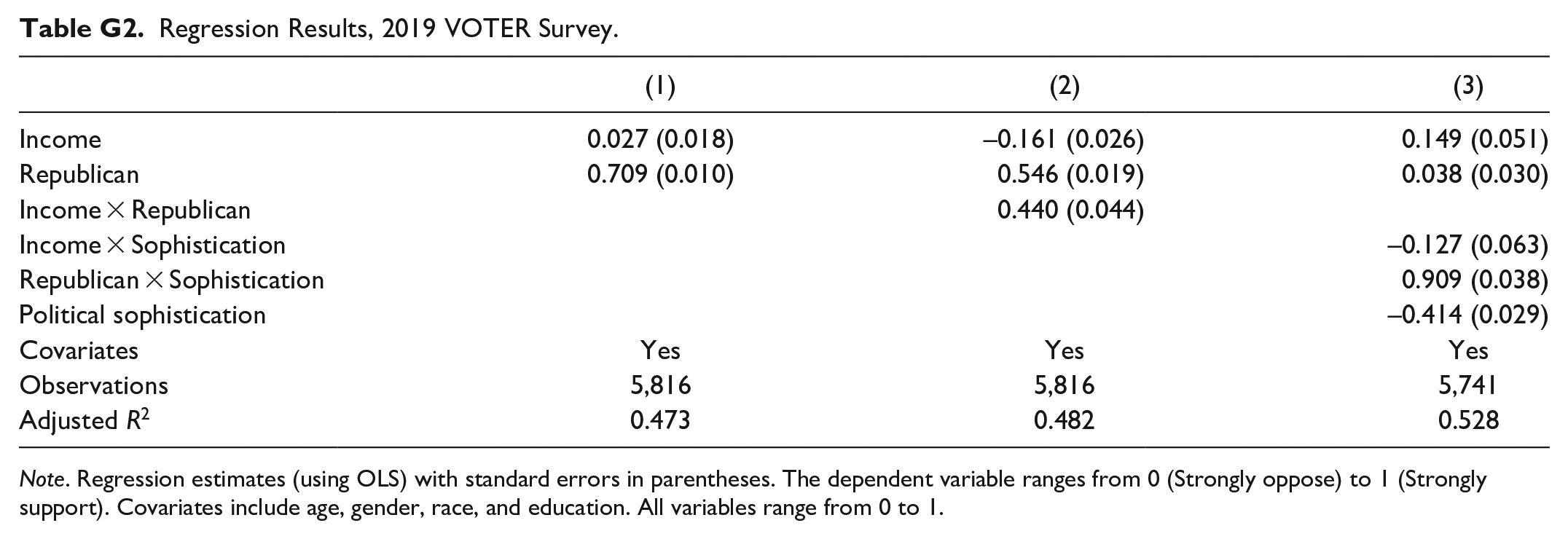

Regression Results, 2019 VOTER Survey.

Note. Regression estimates (using OLS) with standard errors in parentheses. The dependent variable ranges from 0 (Strongly oppose) to 1 (Strongly support). Covariates include age, gender, race, and education. All variables range from 0 to 1.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.