Abstract

This article considers how TV retailers shape public understanding of television as a cultural technology and household device. Drawing on interviews with Australian TV retailers, we identify four sales strategies used when selling smart TVs in-store: simplification, avoidance, empathy, and exploitation. Our analysis shows how these sales strategies seek to minimize and manage the smart TV’s technological complexity, thus downplaying its interactive potential. We critically assess the assumptions about technological expertise that underlie these strategies.

Introduction

Recent scholarship in television industry studies has emphasized the importance of workers who play a key, but under-appreciated, role in delivering television to the consumer. This research, which often uses interview and observational methods, draws attention to labor practices that have traditionally fallen outside the discipline’s definition of television work, especially in areas such as television distribution, hardware, and customer service. Among other studies, Mayer’s (2011) ethnography of assembly-line workers in Brazil’s export processing zones and Patterson’s (2021) interviews with pay-TV call center workers challenge our discipline to think more broadly about how we define television industries. Such research foregrounds the tacit knowledge of workers and their “cultural sense making” (Caldwell 2008, 14), which both reflects and shapes the industries of which they are a part.

The present article extends this line of inquiry to a remarkably under-studied area of the television industries: TV retailing (i.e., sales of TV sets in electronics stores). Here we explore the everyday “micro-encounters” (Boddy 1998, 137) between retail floor staff and their customers that collectively help to shape public understanding of television as a technology. Taking the electronics store seriously as a space of contemporary culture, our analysis explores a specific aspect of everyday retail practice: how retailers describe, and respond to, the technological expertise of their customers, specifically in relation to their use of “smart” (internet-connected, app-enabled) TVs. Our aim here is to critically investigate the assumptions about expertise that underwrite these interactions.

Recent adoption of smart TV devices provides a valuable context in which to undertake this inquiry. Today’s smart TVs are fundamentally different devices from the TVs sold a decade or more ago. Designed as multipurpose, convergent devices equipped with voice assistants, search engines, payment gateways, and personalized recommendations—a feature set that aligns the smart TV more closely to the mobile phone than a traditional TV—smart TVs are platform media in the sense that they involve multisided markets, automated advertising, data capture, and algorithmic discrimination. Users require ever-more complex skills to get the most out of smart TVs—skills which are unevenly distributed across the population (Lobato et al. 2023). For example, the ability to use an app store or de-install a buggy app can make a significant difference in whether the TV lives up to its potential as a smart device, or whether it is more likely to be used primarily for broadcast viewing or on default settings with only the preinstalled apps. In this way, the smart TV is becoming a “boundary object” (Star and Griesemer 1989) between computing and traditional TV viewing. Hence, media industries research needs to understand how this device is discursively framed to consumers in, and beyond, the retail environment, if we wish to understand the wider implications of its use in households.

This article seeks to provide such analysis, drawing on interviews conducted with TV retailers in Australia. Our analysis is located within a critical tradition of research on television device consumption (Boddy 1998; Chambers 2016; Silverstone 1994) and retail cultures (du Gay 1996; Herbert and Johnson 2019), rather than within applied marketing research. The article proceeds as follows. First, we review existing historical and current literature on TV retailing within media studies. Second, we explain our methods. Third, we describe the changing dynamics of the TV retail sector in Australia: its structure, the key players, and the characteristic patterns of work. We then present our findings from qualitative interviews with Australian electronics retail floor staff. We identify four strategies that retailers regularly use to sell smart TVs once they have assessed the customer’s level of expertise: simplification, avoidance, empathy, and exploitation. Our analysis shows how these sales strategies seek to minimize and manage the smart TV’s technological complexity, thus downplaying its interactive potential.

The Significance of Retail

Retailers are a conduit to the consumer. In stores and online, retailers are responsible for constructing how electronic devices are presented. This occurs both verbally, through conversations with customers, and visually via visual merchandising and display of TVs as commodity objects. Silverstone’s (1994) foundational work on television and consumption describes retail as part of the “imagination” stage of consumption, when commodities are idealized and conceived prior to their assimilation into the moral economy of the household. In his account, retail is “a transformative activity, marking a boundary between fantasy and reality, opening up a space (or not) for imaginative and practical work [. . .] on the meaning of the object” (Silverstone 1994, 126). This is a point echoed by du Gay (1996, 98), who stressed how “the economic folds into the cultural in the practice of retailing,” and by Cowan (2012, 254), who describes the “consumption junction” as embedding consumers’ choices in a “network of social relations that limits and controls the technological choices that she or he is capable of making.” Other scholars have emphasized the liminality of the electronics retail environment as “a prismatic space of consumption and communication” characterized by “intersecting passages of people and media goods” (Fornäs et al. 2007, 65; see also Dowling 1993; Oreglia and Kitner 2013).

While a vast literature explores television’s role in commodity culture (Kaplan 1987; Margaret 1998), only a handful of studies examine the spaces in which TVs are sold to the consumer. Among these rare works are archival studies (Arceneaux 2018; Boddy 1998; Gaillard 2012, 2013; McCarthy 2001), a retail ethnography (Fornäs et al. 2007), and the edited collection Point of Sale: Analysing Media Retail (Herbert and Johnson 2019; see also Santo 2019). In addition, Silverstone (1994) and Chambers (2016) theorize retailing as part of the life cycle of media devices and Turow (2017) investigates in-store retail business practices from a media industry studies perspective. However, few of these studies use retailer interviews as a primary source, as we do here.

Reading across the historical literature reveals some important insights into the relationship between retailing and television. In Ambient Television, McCarthy (2001) explores how television was used within department stores in the United States during the 1950s. Drawing on retail merchandising literature, McCarthy (2001) emphasizes the gendered nature of this interaction, arguing that “retailers approached the new medium as a [means] to control female consumer vision within the store” (p.67). Gaillard’s (2012, 2013) analyses of the political economy of TV retailing in France show how institutions such as small retailers and consumer credit companies decisively shaped the retail environment in the post-war years. In addition, national, regional and international histories of television reception (e.g., Horrocks 2018; Spigel 1992; Thurlow 2022) have noted in passing the variable economic, regulatory, and cultural conditions that shape TV retailing—for example, whether televisions were historically sold in manufacturer-controlled specialist stores, as in France, or in large department stores, as in the United States.

Among the most insightful historical studies of TV retailing is Boddy’s (1998) analysis of TV retailing in the United States during the 1940s. Drawing on retail trade journals, handbooks, and manufacturer training resources, Boddy’s (1998) analysis focuses on “micro-encounters of customer and salesperson in the television showroom” (p. 137). He describes two competing imaginaries that shaped retail markets for TVs, and which in turn were based on stereotypes that first emerged in the radio era (Arceneaux 2006). First, there was the imaginary of the “hobbyist”—the committed enthusiast (presumed to be male) who had come of age in the DIY culture of early radio and who already knew their way around broadcast technology. Second, there was the competing imaginary of the “housewife,” assumed by retailers to be “perceptually distracted” (p. 135) and pathologically addicted to soap operas. Boddy shows in his research how these “persistent discursive conventions” (p. 139) shaped both the retail environments in which TVs were sold and the larger public understanding of television as a domestic technology.

Together, these various studies remind us that retail—more than the mere distribution and sale of media goods—is a key space in which the possibilities of those goods and their appropriate uses are defined for the consumer. In this tradition, our analysis seeks to explore what Herbert and Johnson (2021, 351) describe as the “everyday contexts in which meaning and value are generated in the retail circulation of media culture.” To understand these everyday contexts, we conducted empirical research with retailers as described below.

Methods

This article emerges from a four-year research project examining the design, marketing, adoption and use of smart TVs in Australia. Over the course of this project—which used methods including archival research, trade press research, interface analysis, device testing and user surveys—our research team became particularly concerned with the uneven distribution of expertise among smart TV users in Australia. This was a theme that emerged strongly in our survey research (Lobato et al. 2023, 10), which revealed that a quarter of Australian smart TV users are “defaulters” (they do not know how to download apps, customize the order of the apps in the app launcher row on their TV home screen, or know how to adjust their privacy settings). At the other extreme, around a third of Australians are “customizers” that are very confident, autonomous and intentional in their use of the smart TV. We wanted to know more about this skills divide, and how this might relate to changing discourses about television culture in the age of smart TVs.

After examining demographic factors including education, income and technological literacy (Lobato et al. 2023), our research began to look into the role of intermediaries in shaping this expertise. The epistemological aim here was to understand “the network of social relations in which a consumer is embedded” (Cowan 2012, 271) rather than pursuing an individualist explanation focused on the sovereign consumer. All our prior research had suggested that retail was an important part of this picture. We therefore decided we needed to know more about how consumers understand smart TVs before they buy them, the questions they ask at the point of sale, and how retailers respond to these questions. So we designed an empirical research project to explore the cultures of smart TV retailing in Australia.

Our first step was to conduct field visits to electronics retailers in Melbourne to note store layouts, display techniques, promotional strategies and the “navigational dynamic” of consumer movement through each store (Herbert and Johnson 2021, 346). We then analyzed retailer websites, retail trade publications (Appliance Retailer, Inside Retail), industry reports (IBISWorld) and retailer publications (JB Hi-Fi’s STACK, Harvey Norman’s Behind the Screens) to understand current business practices. This enabled us to compile a list of open-ended questions for TV retailers, addressing issues such as sales strategies, training, commissions, common questions and purchase drivers for customers, and consumer awareness of smart TV platforms and features.

Our next step was to conduct a series of semi-structured interviews with retail floor staff (TV product specialists), using follow-up “probes” (Roulston 2010) to elicit participants’ accounts and insights. In this regard, we were inspired by other small-sample qualitative research in media industry studies that use ethnographic methods and professional interviews with backstage occupations in the screen industries (Caldwell 2008; Mayer 2011; Patterson 2021; Santo 2019). We began data collection in July 2022, and we completed ten interviews with retailers over the next few months. 1 Participants had a minimum of six months TV retail experience and were based in stores across the eastern states of Australia, including inner-city stores, home-center shopping districts, and regional outposts. 2 Three of our interviewees identified as female; the remaining participants identified as male—a gender ratio that roughly corresponds to the staffing that we observed in stores.

After concluding ten interviews we had reached saturation and were hearing similar perspectives repeatedly, so we decided to cease data collection. The resulting data pool of nearly 50,000 words proved to be a fascinating resource for understanding “how media retail organizes itself, makes cultural meanings out of daily work activities, and ultimately shapes media’s place within culture” (Herbert and Johnson 2019, 7). We now explain the specificity of TV retailing in Australia, where our study is based.

Changing Dynamics of TV Retailing in Australia

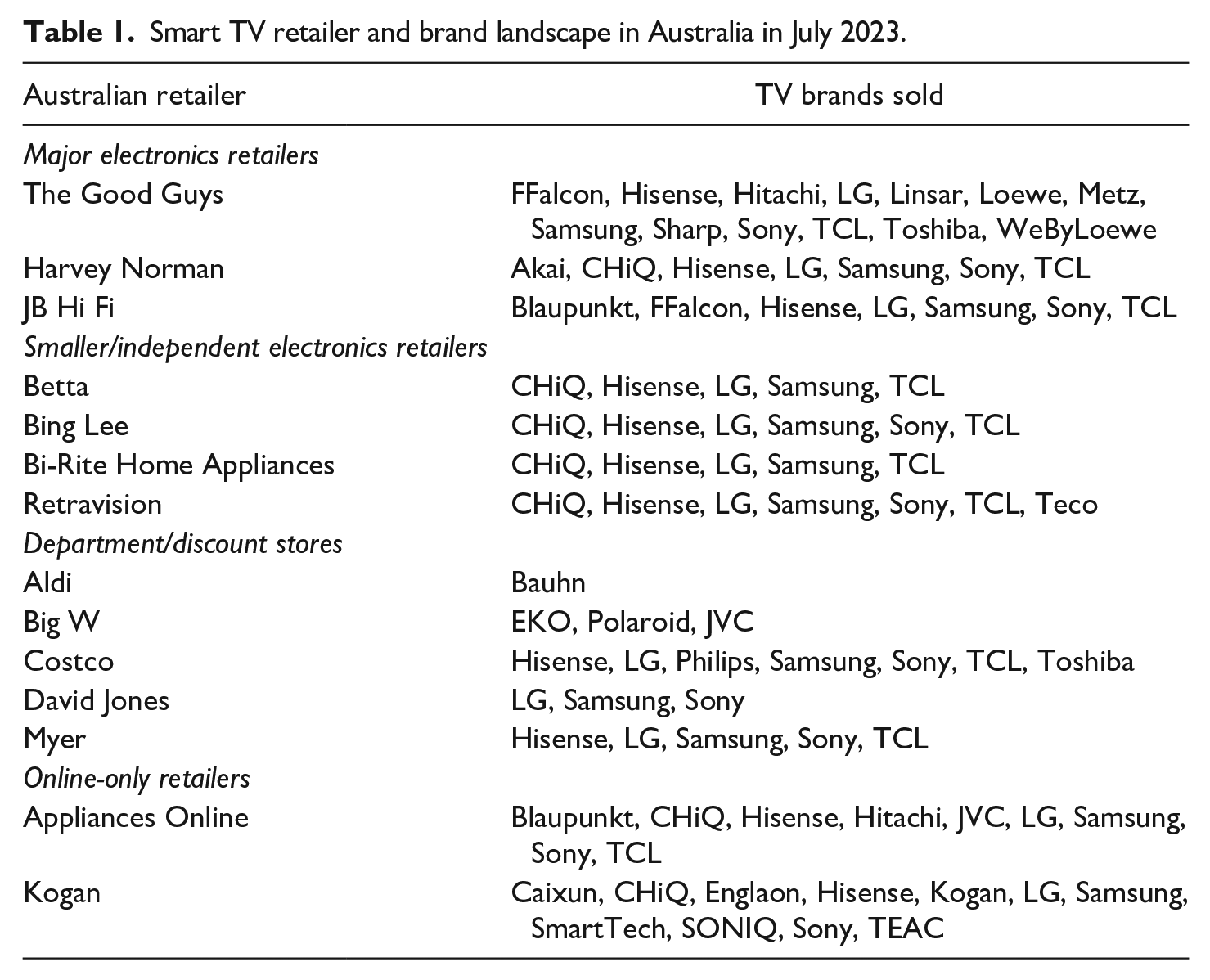

In Australia, the domestic appliance retail sector employs more than 40,000 workers and generates revenue of around AU$17 billion per year, with TVs estimated to account for fifteen per cent of this (IBISWorld 2023). As outlined in Table 1, three national electronics chain-stores (The Good Guys, 3 Harvey Norman and JB Hi-Fi) control about half of the market, competing with smaller chains (Betta, Bing Lee, Bi-Rite, Retravision), independent stores, and online-only retailers (Appliances Online). Additionally, discount retailers Aldi, Big W and Costco offer a small range of TVs, often at marked-down prices, and sold in large volumes during advertised sales. Together, these retailers represent a substantial but frequently overlooked labor force within the wider media and electronics industries.

Smart TV retailer and brand landscape in Australia in July 2023.

The function of bricks-and-mortar retail has changed with the rise of online retailing. For some customers, the electronics store is a space to research and examine TVs which will ultimately be purchased online. For others, the store is the primary/only site of research and purchase. As one industry report notes, “consumers remain partial to purchasing. . . TVs instore, leveraging the expertise and knowledge of staff while physically engaging with floor stock to make informed decisions” (IBISWorld 2023). Hence, while the traditional functions of TV retailers—to inform the customer and guide purchase decisions—are now also performed by review websites, unboxing videos and other online resources, retailers remain an important information source for many customers. This is especially the case for customers with low digital literacy and those customers (including many elderly customers) who prefer face-to-face interactions.

Upon entering the retail store, the customer is presented with a curated spectacle of goods which varies according to the type of store. In electronics stores TVs are in a dedicated zone that take up around a quarter of the sales floor. TVs typically cover one wall running the length of the store, so that they can be seen from almost any vantage point. Inventory is organized by brand, with major brands paying for a prominent display position and supplying signage and plinths to highlight the latest models. This display strategy reflects the enduring importance within consumer electronics retailing of TVs, which function as a flagship appliance to lure people into the store. In contrast, the discount stores we visited afford TVs significantly less visibility on the sales floor, with only a few models on display, if any. Here TVs often remain in their boxes and are positioned near household appliances like phone chargers and vacuum cleaners. At times we also observed stacks of TV boxes placed in high-traffic areas, such as the entrance and near the check-out, to encourage impulse buying. These different visual merchandising strategies frame the TV differently to consumers: as a flagship consumer electronics device versus a generic household appliance.

Floor staff in electronics retailers work on commission and are strongly incentivized to maximize sales. They are supported by brand reps—traveling representatives from manufacturers such as Samsung and LG—who visit the stores regularly to promote their brands to staff and assist with customer inquiries. They must also regularly complete training modules to keep up to date with the latest trends in TV manufacturing. 4 In contrast, employees in discount stores work do not work on commission or have brand reps to support them, and do not offer the same expertise as specially trained staff in electronics stores.

These long-established practices in TV retailing have been disrupted by smart TVs. According to survey research commissioned by the Australian government, the primary feature that Australian consumers rank as the most important to consider when buying a new TV is that it is internet-enabled (Social Research Centre 2023, 59). Retailers must now remain up to date with an ever-changing ecology of TV hardware and software. Meanwhile consumers now weigh traditional decision factors (price, picture quality, screen size) alongside newer factors such as the range of built-in apps or the design of the home screen (TiVo 2023).

As TVs have become more technologically complex, increased competition in global TV manufacturing markets has resulted in falling TV prices and reduced profit margins for manufacturers (Perry 2022). This price competition has driven manufacturers to aggressively pursue “post-purchase monetization” of smart TVs through content sales and advertising (Lobato and Scarlata 2022; see also Pot 2023). Electronics retailers seek to increase their margins by selling add-on items such as soundbars with every TV purchase. Manufacturers also regularly slash prices on the previous year’s models to make way for the new ones, sometimes offering electronics retail staff bonuses (known as “spivs”) on top of their regular commissions to move these quickly.

So, how do retailers go about selling this increasingly complex device? And how might these sales strategies shape the public understanding of the smart TV as a cultural technology and household object? We now explain our key findings from the interview research.

Gender and Expertise in TV Retailing

TV retailers are trained, in line with industry norms, to spend the first moments of a customer interaction sizing up the customer’s needs and preferences. Based on this initial assessment, retailers then form an opinion about who they are dealing with and what kind of TV they might need, want, or be convinced to buy. One retailer described this process as “qualifying” the customer. By the end of this interaction, the retailer can establish the customer’s level of expertise, or how much they actually know about TVs.

One electronics retailer observed that selling TVs, more than any other product in his store, now requires considerable time due to the complexity of the product range and the constantly changing feature set: [The TV is] probably the one (product) the customers rely the most on us to sell. I’ve found with computers or game consoles or camera or phones, most of those customers will come in knowing basically what they want, maybe have a couple extra questions. . . TVs seem to the one that they come and ask the most questions about, the one we have to spend the most time with. . . TV marketing is very convoluted. . . So a lot of customers are confused as to what it all means (and what’s better).

When selling to these average customers, retailers need to describe the TV and its features in a way that the customer will not find intimidating or overwhelming. At the same time, they need to reassure the customer that the TV will be both functional and enjoyable to use. In other words, they must engage in a carefully calibrated performance of expertise, in which retailers supply expertise as needed, while also convincing the customer of their own expertise as a technology professional and user.

Some retailers observed that customers’ expectations of staff expertise were often strongly gendered. One experienced female retailer we spoke to observed that customers often treat her differently from male staff at the same store: I have noticed, as a female, the sexism in tech and TVs is rife – from both males and females. . . they point blank will either not come to me or go to the male trainee. . . that is a problem for me as a technology female. But I don’t put up with that shit very much.

Stories such as this indicate that the TV retail floor remains a strongly gendered space, as Boddy’s work on the hobbyist/housewife distinction in 1940s TV marketing found. This pattern can be seen in current TV marketing campaigns, with large-screen and outdoor TVs depicting sports-loving males whereas “lifestyle” TVs like Samsung’s The Frame are marketed to women.

We also found that retailers have their own assumptions about technological expertise which are gendered in subtle ways. For example, several retailers told us in interviews that there exist two types of customers—those with technological expertise and those without: [Y]ou’re generally able to pick the ones who know a lot out straight away because they’ll pretty much come in and say, “I want this and this. Can you tell me the difference between this and this. . .” Whereas other people will come in and sort of say, “I’m looking at these two, I’m just asking for some ideas.”

Another retailer observed: You get some people who think they know everything. And they’re like, “Yep, cool. I’ve done all this. And I want to try and whatever.” And then the other customers were just like, “Yeah, I’m just looking for a TV, I have no idea. You tell me what I need.”

Retailers described knowledgeable customers as “nerd[s]” or “aficionados [who] look at different review websites.” One suggested that well-informed shoppers comprise around 10 percent of the customers he meets. We expected that retailers might observe that these nerds were mostly male customers, however no retailer went so far as to make this distinction unprompted. Interestingly, staff at discount stores frequented by price-sensitive shoppers did not mention nerds at all, which suggests that these customers prefer to shop at electronics stores where a full range of high-end brands are stocked. Notably, retailers in our study did not generally refer to nerds with warmth or appreciation; nor did they enthusiastically relay their interactions with such customers. Overall, we got the impression that retailers try to limit their interactions with this type of customer and even avoid them entirely.

However, all our interviewees—across all stores and all levels of experience—were eager to describe their encounters with regular customers with low or average levels of technological expertise. Unlike nerds, these technologically un-savvy customers tended to ask rudimentary questions (namely some iteration of “What’s a good, cheap smart TV?”) or enquire about price and size. Many asked about the availability of certain apps (“the first thing they ask now is ‘Does it have Netflix?’”) and whether the TV is “a smart TV”—a distinction that is increasingly meaningless now. More than one retailer noted with bemusement that “every TV we sold was a smart TV!”

Here we see how retailers quickly leap to judgment about customers’ expertise—a necessary part of the sales role—and also how these judgments entail implicit assumptions about good and bad expertise, with a lack of expertise often being seen as a sales opportunity whereas nerd expertise is received warily as an obstacle to sales.

The Nuts and Bolts of Smart TV Sales Discourse

In his research on TV retailing in the 1940s, Boddy notes that industry handbooks at the time “advised dealers to avoid attempting to sell specific features of the apparatus which might be of interest only to technically minded amateurs” (Boddy 1998, 137–8). Instead, “the rhetoric of mobility, omnipotence, and adventure familiar in the established literature of amateur radio was quickly enlisted to serve the consumer imperatives of postwar commercial television” (Boddy 1998, 137–8). A trade press article in Radio and Television News warned, “DON’T Sell ‘Nuts and Bolts’:” [Y]ou may explain how the article you sell operates, but it will be helpful only insofar as it appeals to or awakens one of more of the prospect’s desires to possess it. Technical explanations that go beyond this do not help the sale, and if the prospect is not able to understand or appreciate your explanation, it may “kill” the sale. . . It is especially important that the salesman with a technical background keep this in mind, because many of the sales that he loses. . . are forfeited because he sells “nuts and bolts,” or should we say “coils and condensers,” instead of what his product could do to fulfill the desires of the prospect (Christiansen 1949, 40).

To what extent do these age-old sales strategies still apply in the age of smart TVs? And what other ways of managing varied customer expertise do TV retailers use today? In the next section we describe four common strategies we observed in our study, which we describe as simplification, avoidance, empathy, and exploitation.

Simplification

Remarkably, we found that the simplification strategies described by Boddy in his research on TV retailing in the 1940s continue to be used today. It remains essential for retailers to downplay the technological complexity of smart TVs to reassure customers these devices will be usable in their everyday lives. We found that retail staff deal with the complexity of smart TVs by focusing the customer’s attention solely on the physical attributes of the TV: the image, the sound, and the product design. Retailers we spoke to seldom show customers how to use a TV before they buy it. As one retailer put it, “there’s no point us sort of talking through it because we can’t set theirs up for them.” Retailers also note that customers rarely ask to see or try the remote control and are not actively encouraged to do so.

Some retailers suggested to us that consumers do not want to know too much information; that if the conversation gets too technical, it might overwhelm the customer. They run the risk of putting them off entirely and losing the sale. “It’s rare that they actually ask what the operating system’s like,” said one retailer. “That’s never really a selling point. . . I’ve never really included that in the sale,” said another. It is enough, according to one interviewee, to describe to a customer what the TV will do for them, “without actually having to go through and show them physically.”

This strategy of simplification is carried through to the in-store visual merchandising. TVs set up in major electronics retailers are generally programed to play a specific brand reel designed to highlight picture quality. As such, consumers do not see the cluttered home screens of smart TVs—overflowing with apps, ads, and recommendations—in the retail store environment. Additionally, stores do not display details of smart TV operating systems in in-store labeling, relegating these technical details to the product specifications available online.

These examples suggest that simplification operates in current TV retail much the same way as it did in the mid-twentieth century. As early TV manufacturers encouraged, retailers today know to sell the smart TV not for its “nuts and bolts,” but for what it can bring to the customer’s lifestyle.

Avoidance

In other circumstances, retailers avoid complexity because they themselves do not know the answers to customer questions. Indeed, some retailers confessed that they actively resist discussions about a smart TV’s “nuts and bolts” when they feel out of their depth. As one retailer put it, “Customers don’t seem to really do that much research because they assume that we’re such a wealth of knowledge that we’ll be able to tell them everything, and then I feel really bad [about how wrong they are].”

Training is a factor here. As mentioned above, different types of stores provide different levels of training. Floor staff with experience at JB Hi-Fi, The Good Guys and Dick Smith report receiving regular instruction. These staff are provided training modules that they are required to complete during their shifts. They can scan the barcode of items using a provided personal digital assistant to access a PDF of the product’s specifications on their personal devices. Brand representatives also regularly visit these stores to explain product features (“They basically go, ‘This is our product range, these are the new features, this is why it’s better.’”) Brand reps are also available to answer queries by phone and, when in store, help set up TVs and displays.

However, some electronics retailers describe being told on their first day to “work it out yourself” and “just go sell.” Some are forced to “brush up on websites in our spare time” and “memorise what brands [have] what apps.” According to one such retailer, “The best way to describe it is that anyone can bullshit their way through it. . . 90% of sales is just being confident. . . if you’re confident enough in what you’re saying, it doesn’t matter if it’s right.” Retailers working at discount stores consistently told us that they are provided with no training whatsoever and that this impacts their ability to “do our jobs properly:” I don’t get paid to do any tech research in my own time or anything like that. . . Why should someone go above and beyond in relation to the job when they’re not getting paid any more than someone who’s just ringing you up at the front door? So there’s no incentive for us to do any better.

This retailer reported actively petitioning their manager for access to a computer in the tech or home entertainment section, or for permission to use their personal device during their shift to be able to look up the answers to customer questions—a request which was denied. They also described never receiving visits from or participating in training sessions with manufacturer representatives: “They don’t come – there’s no rep. We just set (the TVs) up, put them out and away we go.” For these discount and department store retailers it is often a case of “let’s read the box [to] figure out what’s going on in this TV,” or “we learn off of customers who come back and report to us on things that we didn’t know.” When we asked one department store retailer if customers know that there are different operating systems in different TVs they responded, “Absolutely not. We were selling them for a couple of months before we figured it out.”

The result, then, is that retailers selling smart TVs in Australia have varied and often limited understanding of these products. For this reason, many staff deliberately avoid discussing more complex features with customers, such as app stores and operating systems. As a result, customers are often in the dark about how their TV is going to work, and the range of apps and services they can expect to access through the TV, until they get it home. This variable expertise feeds into the final strategies that we identified: empathy and exploitation.

Empathy and Exploitation

Unsurprisingly, all retailers we spoke to were proud of their customer service and claimed to be looking out for the best interests of the customer in their sales strategies. However, we did notice some variation in how retailers at different stores talked about the ethics of their sales approaches, especially in relation to vulnerable customers or those that needed extra help. Interestingly, these variations were closely related to the type of store (electronics or discount store) and thus the commission structure for retail staff.

Department and discount store retailers employed on fixed wages were much more likely to respond empathetically to the limited expertise, and often financial capacity, of their customers. A Big W employee described themselves as able to be “brutally honest” with customers “because I’m not on commission. . . I get paid no more than the door greeter.” She noted that she happily tells customers if a sale is coming up, and to come back when it begins, rather than buying that day. Discount store retailers in our study spoke compassionately of older customers and their limited technical competencies: “You have to remember, when you’re dealing with anyone who’s older, first question is, ‘Do you have Wi Fi?’” These retailers also seemed more aware of practical challenges facing customers—factors like limited internet speeds and the impact of weather events in regional areas. They have more time to learn and respond to a customer’s challenges, without the pressures of meeting budgets and amassing bonuses.

One retailer from a discount store in a regional area of Australia had extensive knowledge of the very specific product needs of people in her semi-tropical, regional community. She spoke in detail about a range of quite specific scenarios her customers deal with—including geckos infesting TVs, sets blowing up during storm-related power surges, and the need to install TVs in caravans and mobile homes. Overall, this participant impressed us both with her product knowledge and her obvious concern for her customers. Expertise, for this retailer, seemed to be about understanding the social context of her customers, especially their specific household and living situation, clarifying their consumer rights, and recommending the most cost-effective TV to satisfy their needs.

In contrast, retailers from electronics stores were less empathetic in their discussion of customer needs. Unlike the discount store retailer above who actively tried to save her customers money, one electronics store retailer we interviewed expressed resentment at price-sensitive customers who reduce his sales commissions: So what’s kind of crappy is that you’ll take (the customer) through those options, qualifying, giving them all the information. . . and then (they’ll go) “oh I saw that this is available for this” – so it’s all price driven: price, price, price, percentage, “I’ve seen it cheaper, I know it’s cheaper, I know that you can do it cheaper”. . . But it (comes) out of our commission, we lose our commission essentially, if you go under a certain margin.

This retailer, who was authorized to give discounts to customers at his discretion, told us he avoids doing so wherever possible to protect his commissions. However, the high number of customers requesting price-matching means that his expected sales quotas are “rarely achieved at the moment”—a source of considerable frustration to him. Another retailer described how he purposefully rebuffs difficult clients: “If you’re mean to me, you’re paying full price for the TV, but if I like you, you’re going home with a Chromecast.” This retailer will show only the customers that he likes how they can avoid spending money on a new smart TV if a connected TV device can extend the life of their existing setup or fulfill their app needs.

More explicitly, several retailers working at electronics stores went so far as to reference their ability to exploit the customer’s lack of knowledge. These retailers freely admitted that commissions and spivs “absolutely” impact the brands and models that they recommend to customers: If we’re looking at TVs with very similar specs, and they want to know the difference between, brand wise, which brand I’ll recommend, I personally 100% of the time will look at whichever gets me more commission and say ‘that one’. . . [T]hat’s not exactly a lie because it’s the same specs.

Predictably, we learned that “a lot of [other] sales guys just say whatever to meet their budget.” The term “guy” here is revealing, as we found that all of the retailers who spoke to us about protecting their commissions were men. One JB Hi-Fi staff member described their employer’s policy as selling the “full solution:” “You shouldn’t just be selling just a TV. The customer doesn’t need just a TV. They need other things to go with it to enhance and improve the experience of that particular TV.” We learned that when a commission structure impacts a retailer’s employment, our interviewees could and often would take advantage of limited customer expertise and upsell certain brands and products.

As these examples suggest, TV retailers today respond to their own varied expertise and that of customers using a range of strategies. We found this to be closely related to the type of store they work at, as this largely determined the training they receive and the commission structure in place. We now consider the implications of these sales strategies—simplification, avoidance, empathy, and exploitation—in light of the new consumer risks that smart TVs pose.

Discussion

The interview research that we have presented in this article demonstrates remarkable continuity in TV retailing practices over the course of a century. While retailers no longer seem to make the kind of explicitly gendered assumptions about customers described by Boddy, we found that retailers certainly make judgments about their customers’ expertise, which in turn determine what kind of sales pitch to offer. However, the end result of “qualifying” the customer, and the variety of store types, training, and commissioning structures currently in place, is that customers shopping for a smart TV in Australia can encounter a wide variety of experiences on the retail floor. Some customers are offered thoughtful advice that takes into consideration their needs, preferences, and even social contexts, and may even receive technical advice from retailers about how a smart TV works—advice that may help them to use these devices in ways they would not otherwise be able to. Others will receive a cursory needs analysis and then be ushered toward certain TV brands (often those with active brand reps and enticing sales incentives). Interestingly, the discount store staff we interviewed—who receive little training and no financial incentive to sell TVs—seem to better serve the actual needs of their customers than the electronics store retailers who work on commission.

Why does all this matter? There are several implications here for television studies. As Boddy (1998) argued, “communications technologies have no ‘natural’ place in our homes or our culture” (p. 30). Our research confirms that retail is one of the factors that helps to shape consumers’ ideas about the place of TV and its proper uses. Along with other factors, including marketing and advertising, retail helps to define “the meaning of the object” (Silverstone 1994, 126). Our interviews suggest that for many customers the meaning of a smart TV, as defined in the retail encounter, will likely be a simplified version of what the smart TV is capable of. By avoiding and simplifying the more complex aspects of the smart TV, retailers discourage their customers from thinking about the smart TV as an interactive device.

This finding has some practical implications for debates about technological literacy. Our interviews suggest that customers rarely view the smart TV home screen or use the remote control in store. Nor are retailers likely to discuss the more technical aspects of the TV, such as its operating system or interoperability with other devices. As a result, the smart TV buyer in many cases enters blindly into a long-term relationship with a particular device that they may not understand, and whose particular app ecosystem may limit their viewing choices for years to come.

If users are not well informed at the point of purchase about how their smart TVs function, and if they lack the skills to work this out for themselves, then it follows that the default settings of the smart TV possess considerable power to shape users’ content consumption. By making certain apps and content more prominent than others, smart TV interfaces inevitably funnel user attention in particular directions. This fact has not escaped the attention of regulators in several nations, who are presently examining the cultural and commercial impacts of smart TV preinstallation (which apps are preinstalled on the TV), positioning (which apps are most visible on the home screen), and integration (which apps are included in search results and recommendations). 5

Retailers are not responsible for these commercial arrangements, of course. It is not their role to assume the burden of explaining a smart TV to every customer, especially when they themselves may have limited understanding of the device. But, as we have shown in this article, retailers do play a part in shaping the user cultures of the smart TV and normalizing particular uses over others. In this way they are helping to implicitly construct what the smart TV means to users and defining its cultural potential.

Supplemental Material

sj-docx-1-tvn-10.1177_15274764241241267 – Supplemental material for Electronics and Expertise: Constructing the Smart TV on the Retail Sales Floor

Supplemental material, sj-docx-1-tvn-10.1177_15274764241241267 for Electronics and Expertise: Constructing the Smart TV on the Retail Sales Floor by Alexa Scarlata and Ramon Lobato in Television & New Media

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: ARC Future Fellowship FT190100144, chief investigator Ramon Lobato.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.