Abstract

Behavior is a critical aspect of public budgeting research. However, much of the scholarly focus has been on collective budgeting behavior, leaving a gap in understanding individuals’ pre-negotiation judgment behavior. This oversight is concerning given evidence from adjacent fields that highlights predictable information-processing irrationalities due to human cognitive limitations. While it is plausible that cognitive biases also influence individuals’ judgments of budget proposals, behavior-informed insights from Economics, Psychology, and Public Administration have yet to be fully integrated into public budgeting research. In this article, we differentiate between individual budget judgment and collective budget negotiation, advocating for renewed attention to budgeting behavior at the micro-level. Through a scoping review, we gather empirically verified effects of cognitive biases on private financial decision behavior and discuss these findings within the context of public sector decision-making. Our theoretical contribution includes the development of an advanced behavioral model of Public Budgeting and hypotheses to test cognitive bias effects on individual budgeting action. Amid recent criticisms of behavioral public administration, we are developing research agenda aimed not only at testing the existence of bias but also at identifying solutions to change judgment behavior, thereby better equipping individuals for collective budgeting action.

Introduction

The government’s engagement with pressing public concerns, such as climate change, digitalization, migration, and inclusion, are increasingly pivotal (Moynihan, 2022). Despite the diverse nature of these concerns, they all necessitate resources, which are typically allocated by politicians (Sicilia & Steccolini, 2017). The behavior of these politicians during the budgetary process holds significant sway over final budget settlements (Rubin, 2020). Hence, it is unsurprising that extensive research spanning eight decades has delved into the behaviors of various budgeting actors.

Early scholars of budgeting sought to formulate normative theories to aid politicians in maximizing the utilization of public resources (e.g., Key, 1940), involving methodologies such as analyzing and comparing the marginal costs and returns of budget proposals (Lewis, 1952). However, the perception of budgeting as a political rather than purely economic process has redirected much of the focus in behavioral budgeting research toward individuals' behavior in relation to others. In numerous studies, behavior transcends mere intellectual conduct, evolving into a collective endeavor characterized by interactions aimed at achieving collective budget decisions. Given the constraints on human cognitive capacity and the recognition that individuals can only make boundedly rational decisions at best (Simon, 1944), it was considered more pragmatic to investigate how individuals navigate the political dynamics of budgeting to achieve their objectives. As a result, we now know, for example, that politicians systematically resort to actions such as inflating budgetary requirements, being mindful that others in the system advocate for fiscal restraint (i.e., spender-guardian framework, Wildavsky, 1988).

Despite the wealth of insights derived from this research, we argue that there is a need for renewed focus to gain a deeper understanding of individuals’ behavior when they evaluate spending alternatives, prioritize savings opportunities, weigh priorities, and consider other factors before engaging in collective action. First, much Public Administration research, including budgeting, has focused on understanding behavior in negotiations without considering the development of negotiators’ preferences, which determine their initial approach to negotiations (Bouwman, 2018). Due to this lack of insight, starting points are often assumed or generalized based on factors such as political profile, party affiliation, gender, and other characteristics. Second, and perhaps more significantly, empirical evidence from behavioral science literature indicates that individuals generally make flawed judgments due to cognitive fallacies (Ariely, 2008; Kahneman & Tversky, 1974). However, the mechanisms through which politicians establish budget preferences, the influence of cognitive bias on these individual budgeting actions, and the implications of these preferences for further collective budgeting actions remain unexplored. Consequently, our study is warranted in addressing these knowledge gaps.

This study aims to broaden the understanding of budgeting behavior by proposing a multi-level model of public budget decision-making, where individual judgments are decoupled from collective negotiations. This allows for a deeper exploration of the formation of initial budget decisions—termed “predecisions”—which consistently serve as the foundation for collective action. Both judgment and negotiation involve distinct activities and behavioral patterns, which we will explore in greater detail below. The focus in this study is on the judgment phase, particularly the impact of cognitive biases on the formation of predecisions. Naturally, there will be variation in predecisions due to the diverse societal perspectives and political ideologies of politicians. However, this variability among individual politicians does not imply immunity from cognitive biases in micro-level budget decision-making. Below, we delineate the potential influence of bias on individual budgeting action and propose methods to investigate bias while recognizing the wide spectrum of individual preferences. Insight into these bias effects is crucial for enhancing budget judgment and better equipping individuals for negotiations.

The research question is: How do cognitive biases affect decision-making in private-financial and public-nonfinancial settings, and what are the implications for politicians’ budget judgment?

We employ smart screening software to identify pertinent studies from a pool of 2,753 abstracts resulting from a scoping review of the literature. Each of the 44 selected studies provides empirical evidence on the impact of cognitive biases on the decision-making behavior of individuals in private sector, financial settings. The scoping review encompasses an array of distinct biases. This article examines the influence of the eight most extensively researched biases: overconfidence, herding, representativeness, anchoring, availability bias, loss aversion, regret aversion, and mental accounting. For each bias, we describe how the behavior of financial decision-makers is influenced. We augment these insights with empirical evidence in non-financial public settings to enhance our comprehension of politicians’ budget judgment behavior. Finally, we formulate concrete hypotheses for each bias that can be examined in the context of public budget decision-making.

Toward a Behavioral Model of Budgeting Behavior

Budgeting behavior refers to the actions, decisions, and strategies employed by individuals or groups involved in the budgetary process. This encompasses various aspects, including how people assess information, negotiate settlements, and decide collectively about the use of public resources. In addition to fiscal and procedural autonomy, the behavior of politicians plays a significant role in determining the utilization of resources (Rubin, 2020). Given the critical role of politicians in making decisions, as well as the responsibilities of civil servants in preparing them, it is not surprising that scholars have dedicated considerable attention to studying their behavior.

Interestingly, a significant body of research highlights the behavior of individuals within the context of their interactions during the budgeting process. Insights gleaned from these studies delve deep into unraveling the dynamics of the “budgeting game”. They shed light on the reasons behind actors’ specific behaviors, such as systematically over-asking due to their awareness that others will push back on budget requests, unreasonably inflating certain events to persuade others to punctuate existing allocations or delaying decision-making to foster collective momentum (Jones & Baumgartner, 2009; Rubin, 2020; Wildavsky, 1988). Additionally, these studies demonstrate how individual conduct can be depoliticized by procedural interventions, such as establishing a fixed base and negotiating only on additional resources or minor adjustments (e.g., Lindblom, 1959; Schick, 2003). However, there has been relatively less emphasis on investigating the processes of individuals as they engage with budgetary information, leaving it unclear how individuals prepare for collective decision-making (see Litton, 2023). Do politicians possess the ability to logically process budgetary information, or do they, like decision-makers in other domains, face cognitive limitations that lead them to “overreact or underreact” to certain information features (cf. Cantarelli et al., 2023)? If so, this leads to biased predecisions that are less well-aligned with the objectives of politicians and complicate further negotiations.

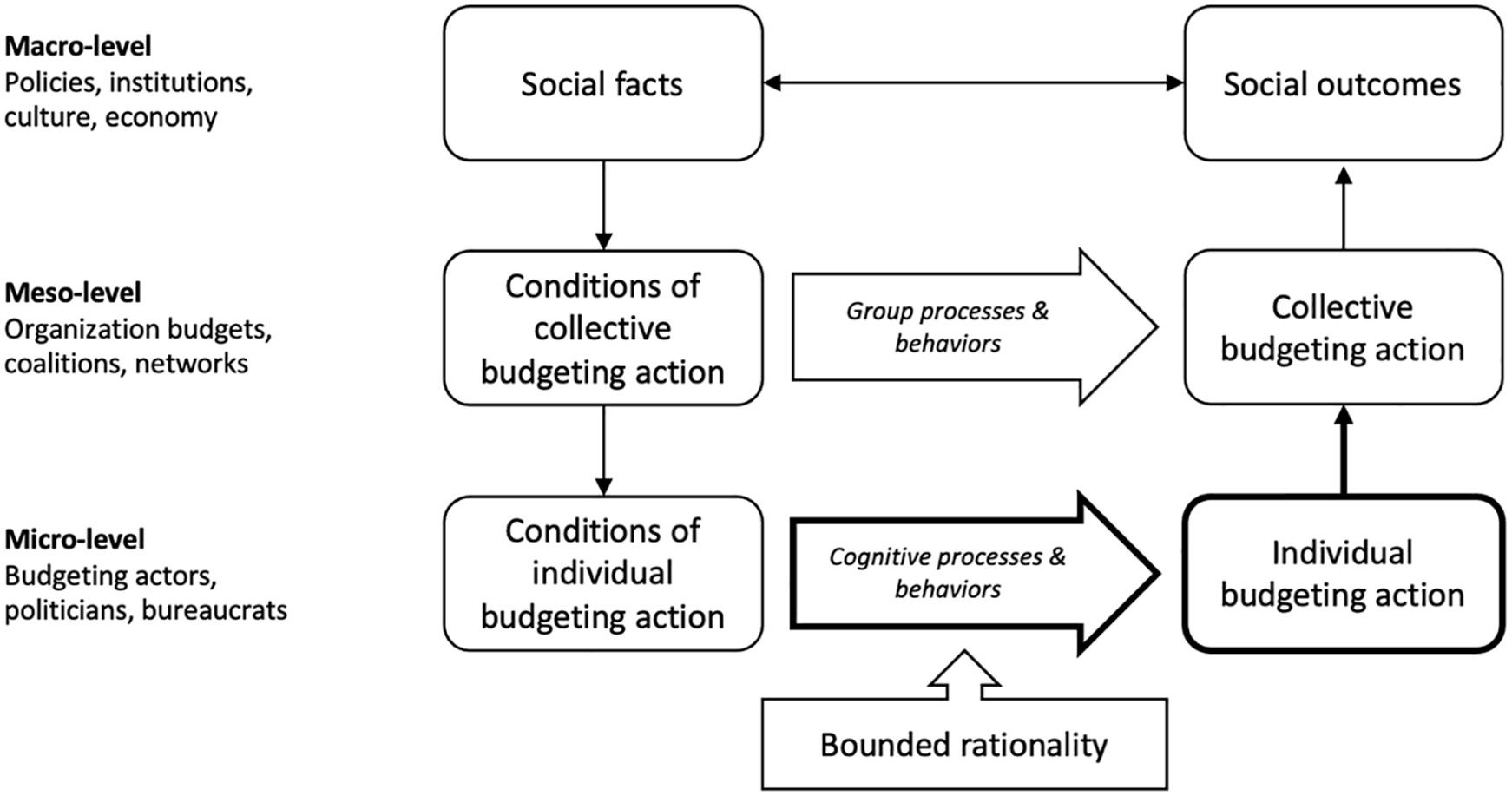

To explore the cognitive aspects of politicians’ budgeting behavior, alongside their interpersonal interactions, we refine the behavioral model of the policy process created by Ewert et al. (2020) (refer to Figure 1). Our behavioral model of the budgetary process delineates actions and outcomes across micro-, meso-, and macro-levels, highlighting their interconnectedness. It implies that collective budget negotiations at the meso-level should be considered in relation to actions and outcomes at the other levels. This multi-level perspective is crucial because individual budgeting actions (i.e., judgments made by individuals on budget proposals) set the stage for collective action, directly influencing its course. Additionally, social changes at the macro-level resulting from negotiated expenditure, investment, and taxation decisions indirectly determine the conditions for both collective and individual behavior in the future.

Behavioral model of the budgetary process

Building on this model, we can explicitly focus on the micro-level where politicians, driven by their ambitions and ideologies, and process budgetary information to form preferences, or predecisions, for collective budget negotiations. These distinct levels of budgeting entail different activities and behavioral dynamics, adding complexity to budgeting decision-making. Addressing gaps in the literature, this study specifically examines the judgment behavior of individuals and the connection between individual and collective budgeting actions, highlighted by bolded boxes and arrows in the model.

To delve deeper into budget judgment behavior, we draw upon two bodies of knowledge. Research on microbudgeting provides one foundation (Thurmaier, 1995; Thurmaier & Willoughby, 2001). This literature underscores that individual budgeting action extends beyond mere economic-rational considerations of information. Instead, it involves multiple rationalities. Initially proposed by Key (1940), there exists an economic rationality where politicians seek efficient resource allocation. However, alongside this, there is also a political rationality aimed at securing future votes and preventing political turmoil, as well as an incremental rationality wherein politicians adhere to rules and procedures to varying degrees. Research among various budgeting actors indicates that especially political considerations hold paramount importance (Thurmaier, 1992). This understanding is crucial as it elucidates why politicians occasionally make decisions that defy economic logic. Budget decision-making encompasses multiple rationalities, with political considerations often wielding decisive influence over final outcomes. The research we suggest here does not oppose microbudgeting theory; instead, it should be viewed as a further clarification, inspired by recent insights into the limited capacity of decision-makers to process information. While microbudgeting research has successfully demonstrated the importance of different types of information in budget decisions, it has yet to determine the extent to which politicians can effectively process that information. In this line of thinking, inefficient—or rather inexplicable—decisions can arise not only from a certain hierarchy of information types but also from erroneous processing of that information.

Insights from behavioral studies in the fields of Economics, Psychology, and Public Administration, in particular, are instrumental in advancing this line of reasoning. A recent literature review on information use in public sector decision-making reveals that over 30% now adopt a behavioral lens, often focusing on cognitive biases and decision noise (Cantarelli et al., 2023). By integrating theories and methodologies from the behavioral science literature, new avenues emerge for comprehending and predicting individual’s budget judgment behavior. It is probable that budgeter’s preference formation is subconsciously influenced by the cognitive limitations of their brains. Consequently, they may, for instance, automatically gravitate toward numbers, ratios, or amounts presented in a proposal. Decision-makers tend to do that, irrespective of the relevance of these so-called “anchors” (Ariely et al., 2003). In budgeting, anchoring bias could manifest as follows: if politicians prepare a collective decision on the split between increasing income and reducing expenditure to address a budget deficit, there will probably be significant differences between their individual preferences. However, what if information presented in a proposal, such as a suggested split of 50-50 or 80-20, systematically pushes people in a certain direction, causing them to unconsciously develop predecisions that deviate from their own preferences? Can we then still attribute differences to subjective preferences and ideologies, or is such a deviation indicative of erroneous decision-making?

Directly extrapolating insights from prior research to budget judgment behavior proves unfeasible. This limitation arises because much of the previous research in Economics and Psychology often neglects to differentiate between various types of information (cf. Head, 2016). Typically, the primary focus is on economic rationality and the logical processing of numerical information. However, considering that budget judgment encompasses multiple rationalities, thereby adding an extra dimension to information processing by individuals, it becomes imperative to explicitly explore the impact of cognitive biases on budget decision-making. In this article, we leverage existing literature to identify which biases have the most significant influence on financial decision-making in other domains. This process helps us formulate hypotheses for targeted research into the judgment behavior of individual politicians as they assess budget proposals and prepare for negotiations.

Methodology

We employ a two-step method to formulate a research agenda for Behavioral Public Budgeting. Initially, we utilize the relatively innovative approach of scoping review (see, Nagtegaal et al., 2020), to systematically map the extant evidence regarding the impact of bias on financial decision-making behavior in the private sector. Substantial research exists beyond the public sector on individuals’ overreaction or underreaction to information features when making financial decisions related to investment, saving, or consumption, among others. This endeavor is complemented by incorporating empirical evidence from non-financial decision-making in public settings, acknowledging that financial decisions in the private sector may not be entirely analogous to public budget decisions. Deliberating on more generic public decisions enables the integration of the unique attributes of publicness into the hypotheses being developed.

Search Strategy and Study Selection

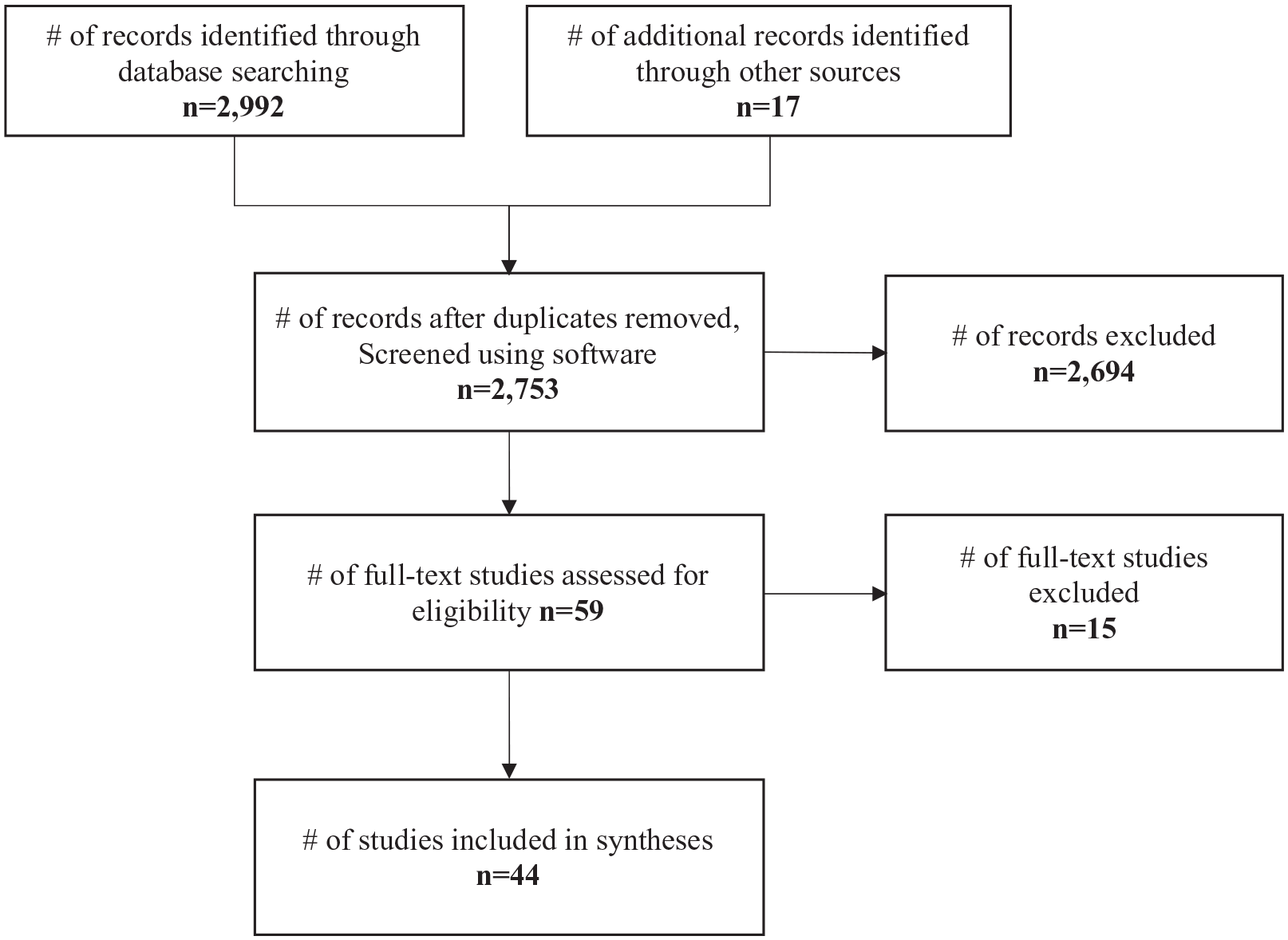

We utilized three search strategies to locate pertinent publications that explore the influence of bias on financial decision-making. We searched the Scopus database, focusing on the period post-2000, considering most empirical work would follow Barberis and Thaler’s (2003) seminal survey on Behavioral Finance. In October 2021, we executed a search to identify empirical publications on the behavioral dimensions of financial decision-making, utilizing the query “Bias and financial decision-making” with the constraint “pubyear > 1999.” This generated 2,992 publications (refer to Figure 2). Subsequently, we searched Google Books and consulted scholarly experts to identify any missing records, resulting in an additional 17 records. After deleting 256 duplicates, we had 2,753 unique records for screening. Using ASReviewLab, we screened abstracts to identify their alignment with the eligibility criteria. Entries were included in the review if the study pertained to financial decision-making, contained empirical evidence regarding cognitive bias, was conducted between 2000 and 2021, and concerned a published or accepted peer-reviewed journal article, book, or book chapter. This process resulted in 59 relevant publications. In the second step, we screened these articles fully, excluding 3 studies for substantive reasons and 12 records due to accessibility issues. The exclusion of 15 records resulted in a total of 44 publications for further review. In the final step, we used a data extraction form to summarize study characteristics and utilized NVivo for systematic organization and analysis of findings. Despite the inherent subjective nature of qualitative coding, we believe our classifications facilitate the analysis of cognitive bias in financial decision-making behavior.

Scoping review flowchart

Utilizing Insights From the Review

Our scoping review reveals that 44 different biases have been investigated, with a significant portion of insights collected in Asian countries (73%), followed by Europe (15%) and the USA (4%). Behavioral research in financial decision making is contemporary, as most studies (84%) are published in 2018 or later. While the majority of these studies focus on investigating the effects of bias, a significant portion (41%) also delve into its antecedents. The predominant research approach is observational, with 71% of studies employing surveys to collect data. Eleven studies utilize interventional methods, including vignette and lab experiments.

A comprehensive list of biases is available on the journal website; however, we focus on the eight most prevalent ones in this article. This selection is primarily driven by numerical prevalence, with each of these biases examined in at least 10 separate empirical studies. It is important to acknowledge that alternate selections may have been made by other researchers. Furthermore, it is essential to note that the biases discussed herein are not exhaustive, and there exist additional cognitive fallacies that impact financial decision-making. Our decision to focus on these biases was made to allow detailed analysis, recognizing that certain biases, such as confirmation bias, disposition effect, and gambler’s fallacy, may possess equal importance despite generating less empirical material in our review.

This study centers on investigating the effects of overconfidence (empirically examined in 29 different studies), herding (21), representativeness (19), anchoring (18), availability bias (16), loss aversion (12), regret aversion (10), and mental accounting (10). For each bias, we elucidate its influence on individual’s financial decision-making behavior. Moreover, we augment these insights by integrating empirical evidence from the public administration literature to enhance our comprehension of judgment and decision-making behavior within the public sector. Ultimately, we formulate specific hypotheses for each bias that are amenable to empirical testing in the context of budget judgment.

The most prevalent cognitive bias in our review is overconfidence bias, characterized by individuals disregarding common assessment standards when they perceive themselves as superior decision-makers. Despite believing their behavior to be logical and thoughtful, research demonstrates otherwise. Overconfident investors tend to trade excessively, nullifying potential profits with associated costs of trading (Ahmed & Noreen, 2021). Overconfidence bias has been examined in 29 studies, with 16 confirming its significant impact, while 4 studies found no evidence (Dar et al., 2021; Hala et al., 2020; Kamran et al., 2020; Pandey & Jessica, 2018).

In the realm of Public Administration, overconfidence remains relatively underexplored, despite its “undeniable importance warranting more focused research” (Battaglio et al., 2019, p. 314). Nonetheless, evidence suggests its relevance in public decision-making. For instance, Liu et al. (2017) demonstrate that overconfident bureaucrats, who overestimate their knowledge levels, consistently make poorer estimations. Similarly, Sheffer and Loewen (2019) find that overconfident politicians are more inclined to ignore information and take risks.

This suggests that overconfidence bias also distorts budget judgment behavior. When politicians overlook essential budget information features, their judgment is compromised. Overconfidence bias can lead politicians to be overly optimistic and develop predecisions with greater risk than they intend. Failure to utilize information may also result in implementation problems, especially when overly positive goals and estimates prove unattainable in practice. To investigate the influence of overconfidence bias, we posit the following hypothesis:

Herding bias manifests as the inclination to choose an alternative because it aligns with the majority’s choice. People seek social acceptance and are therefore reluctant to make divergent decisions. This tendency to conform to group behavior has also been demonstrated in microbudgeting studies, where politicians understand the necessity of reaching a consensus to go along. The key difference with herding bias lies in the degree of awareness. While existing theory primarily focuses on the conscious strategies politicians use to advance budget decision-making in relation to others, behavioral research highlights the subconscious impact of herding when processing information to arrive at a decision. Studies in the review affirm the hidden influence of herding bias on financial decisions, indicating that few individuals base their decisions on independent investment analysis (Kartini & Nahda, 2021). Instead, they imitate peers’ decisions without verification (Rasheed et al., 2018). Herding has been examined in 21 studies, with its effect demonstrated in thirteen studies. Herding diminishes individual profits and contributes to inflated prices. Two studies found no influence: the behavior of young investors (Rahman & Gan, 2020) and university lecturers making retirement decisions (Salleh et al., 2020) was not significantly influenced by peer preferences.

In Public Administration literature, herding bias relates to social norms, wherein scholars explore whether group behavior can influence individual behavior. Like herding, social norms tap into people’s reluctance to deviate from their groups. Research indicates, for instance, that health professionals are more likely to adopt a vaccine if they know their colleagues are doing so (Belle & Cantarelli, 2021). Moreover, field experimentation reveals that social norms play a significant role in citizens’ willingness to pay taxes compared to enforcement techniques (Larkin et al., 2018). Herding can yield either advantageous or disadvantageous outcomes. While peer preference information serves as a valuable tool for policymakers in guiding individuals toward desired courses of action, dependence on group behavior may lead them to disproportionately emphasize that information in their predecision making.

We hypothesize that herding bias influences budget judgment by causing politicians to assign disproportionate value to peer preference information. Politicians not only take deliberate actions to facilitate group decision-making but are also likely to be unconsciously influenced by their peers’ preferences. If politicians rely excessively on this information and ignore other inputs, they are more likely to formulate predecisions that do not effectively align with their personal goals. Instead of determining how to best achieve their own objectives by weighing various pieces of information, they primarily observe and follow the voting behavior of their colleagues. We propose the following hypothesis for empirical testing:

Representativeness bias refers to the tendency to assess probabilities based on the similarity of one event to another, commonly resulting in two notable phenomena: conjunction error and scope neglect. Conjunction error occurs when people perceive a subset of events (e.g., accumulating wealth for a college fund) as more likely than the superset (accumulating wealth), contrary to probability theory. Scope neglect, on the other hand, arises when individuals rely on overly narrow samples to make judgments. Nineteen studies have explored representativeness bias. Regarding conjunction error, research indicates that investors often rely on stereotypes and prior beliefs to evaluate investment desirability, with a company's reputation exerting more influence than solid financial analysis (Khan et al., 2020). Such behavior diminishes profits and increases financial risks. Furthermore, studies demonstrate the impact of scope neglect, as investors tend to gauge long-term performance based on recent performance (Raut et al., 2020), and home buyers determine asking prices solely based on a narrow comparison with properties viewed (Jain et al., 2020). One study found no significant impact (Al-Dahan et al., 2019).

In Public Administration literature, representativeness bias has been a subject of study, with its impact varying across different contexts. Stolwijk and Vis (2021) demonstrate that politicians frequently make conjunction errors when estimating someone’s occupation and often overlook the broader scope when assessing earthquake probabilities. This observation aligns with the findings of Nielsen and Bækgaard (2015), who observed that politicians’ propensity to invest in a particular policy increases when recent performance in that policy area is strong. However, if they overreact to recent performance and neglect to consider the broader scope, there is a risk of overspending on approaches that have poor long-term performance.

We anticipate that representativeness influences judgment behavior, particularly through scope neglect. Similar to how financial decision-makers often base their forecasts of future profits on recent profit trends, we hypothesize that politicians tend to base their budget predecisions on overly narrow samples or limited past experiences. We expect that scope neglect will have a more pronounced effect on politicians’ behavior compared to experts. This expectation is grounded in microbudgeting research, which indicates that experts possess greater proficiency in evaluating and delineating the ramifications of budgetary decisions (Thurmaier, 1995). We propose the following hypothesis for empirical testing, which can be tailored to explore differences among various types of budgeting actors:

Anchoring bias concerns the tendency to rely excessively on a single piece of information when making decisions. The scoping review includes 18 studies focusing on anchoring, demonstrating that financial decision-makers often anchor themselves to specific values. They consistently overspend by relying on asking prices (Waweru et al., 2014), pay higher prices as anchors increase (Raut et al., 2020), and refrain from selling loss-making shares until the initial purchase value is recovered (Kartini & Nahda, 2021). Even seemingly irrelevant numbers can influence spending preferences. For instance, individuals primed with the last two digits of their social security number systematically paid more for identical items as that particular number increased (Ariely et al., 2003).

In Public Administration literature, the influence of anchoring is extensively documented and consistently supported (Battaglio et al., 2019). Studies indicate that managers exposed to high anchors tend to rate identical subordinates more favorably (Belle et al., 2017) and allocate employees more time to respond to emails (Belle et al., 2018). Anchoring also impact the preferences of politicians, leading them to accept higher taxes when primed with a high starting point, even when the possibility of tax abolition is emphasized (McCaffery & Baron, 2006).

Drawing from a wealth of empirical evidence, we anticipate that anchoring influences politicians’ judgment behavior, prompting their predecisions to gravitate toward the provided anchors. Despite anticipated diversity in individual preferences, it is likely that politicians unconsciously yet systematically align their decisions with anchor values. In budgeting contexts where numerical values play a crucial role, careful consideration of anchors, whether relevant or not, is essential. While anchors can sometimes aid decision-making, they may also distort judgment. This aligns with Sanders et al.’s (2018) suggestion that politicians are significantly swayed by the previous year's budget when tasked with applying a zero-based budgeting approach. To investigate the impact of anchoring bias, we propose the following hypothesis:

While the effect of high and low anchors has been extensively examined, there remains considerable uncertainty regarding the influence of anchors relative to the absence of anchors. LeBoeuf & Shafir (2006) observed that high anchors significantly impacted individuals’ estimates, whereas the low anchor and no anchor conditions yielded comparable results. We advocate for specific research aimed at investigating the effect of anchors in scenarios where no anchors are employed. The following hypotheses provide guidance for such inquiry:

Availability bias refers to the inclination to assign greater significance to information that is readily accessible, although such information may not necessarily be entirely representative. This phenomenon has been examined in the review sixteen times, with its impact evident in various contexts. For instance, portfolio returns are suboptimal as property buyers limit their investments to familiar local markets (Pandey & Jessica, 2018), or when traders overly rely on information from acquaintances (Ahmed & Noreen, 2021). Nine studies find a significant impact of availability, while one study finds no evidence (Baker et al., 2019).

In Public Administration literature, availability bias effects are also evident (Battaglio et al., 2019). When assessing public performance, people often overlook objective data and instead rely on easily recalled cues, such as recent events (Andersen & Hjortskov, 2016). Butler and Vis (2023) illustrate that topics receiving extensive news coverage disproportionately attract more attention from politicians. Sunstein and Zeckhauser (2011), on the other hand, find no impact of availability bias on people’s willingness to pay based on the perception of fearsome risks.

We posit that the influence of availability bias persists in budget judgment, particularly regarding spending on newsworthy items. It would be valuable to determine whether politicians overspend in such items compared to prevalent matters with lower news value. Drawing from insights across various decision domains, we hypothesize a correlation between the perceived newsworthiness of items and politicians’ propensity to allocate resources. This relationship can be examined through experimental manipulation of event characteristics. If, under otherwise identical circumstances, politicians demonstrate a higher willingness to allocate funds to “exceptional, well-publicized events” than to “prevalent, neglected events,” it suggests biased decision-making. In the discussion section, we will explore potential debiasing strategies. We expect that enhancing estimation quality could play a crucial role in reducing bias, prompting politicians to adjust their preferences based on objective assessments of event frequency. These propositions can be empirically tested using the following two hypotheses:

Loss aversion bias is characterized by the inclination to assign greater significance to avoiding losses compared to achieving gains. This ensures that investors are more inclined to protect existing capital than to seek increased returns (Shah et al., 2021). Loss aversion bias has been examined in eight studies, revealing that individuals often go to great lengths to postpone losses: they hold onto loss-making stocks, sell assets when it may be more prudent to buy, or sell profitable assets prematurely to secure gains (Kartini & Nahda, 2021). Loss aversion is associated with risk propensity, with most evidence indicating that loss-averse decision-makers are more willing to take risks to mitigate losses, although some people may become risk-averse (Iram et al., 2021). Two studies found no impact of loss aversion (Al-Dahan et al., 2019; Pandey & Jessica, 2018).

In Public Administration literature, loss aversion has garnered increasing attention. People may seek unreasonable reimbursements to offset losses (Battaglio et al., 2019), and managers’ overreaction to information about losses prompts unethical behavior (Belle & Cantarelli, 2017). Managers appear to take greater risks to compensate for losses (Deslatte et al., 2021). The relevance of loss aversion in budget decision-making is explicitly demonstrated by Litton (2023), who found that students and managers are more likely to choose risky options and are willing to spend more when a proposal is framed in terms of potential losses. Loss aversion is closely related to the endowment effect, which suggests that people react differently based on their perception of the baseline. They overreact to losses from a high baseline, and underreact to corresponding gains from a low baseline (McCaffery & Baron, 2006). This is particularly pertinent in budgeting, where multi-year baselines are common.

The insights derived from the review, supplemented by the findings of Litton (2023), lead us to believe that loss aversion bias also influences the formation of budget predecisions by politicians. In Litton’s study, both students and managers exhibited a preference for safer approaches when the budget proposal was framed in terms of gains. Therefore, we expect that also politicians exhibit a propensity to spend on safely framed approaches. The hypothesis can be articulated as follows:

On the contrary, when budget proposals in Litton’s (2023) experiment were framed in a loss-emphasizing manner, preferences shifted, with students and managers more frequently opting for the risky approach. To ascertain whether politicians exhibit a similar change in preference, and whether their willingness to spend consequently increases, we have formulated a second hypothesis regarding loss aversion:

Regret aversion bias refers to the tendency to prioritize the avoidance of potential regret, valuing future outcomes more highly than present ones. While this tendency can be advantageous in some contexts, it often proves detrimental in private financial decision-making. Studies indicate that investors tend to prioritize avoiding mistakes over making accurate decisions. For instance, they refrain from purchasing shares not because they anticipate growth potential, but rather to avert the regret of not buying them (Hala et al., 2020). Homeowners hold onto property in declining markets due to the fear of regretting selling too early, although this behavior is less prevalent in emerging markets (Waweru et al., 2014). The influence of regret aversion has been observed in seven studies, although two studies found no significant evidence (Iram et al., 2021; Rasool & Ullah, 2020).

Regret aversion remains relatively underexplored in Public Administration literature, yet it holds significant relevance for budgeting practices. It aligns closely with notions of incrementalism in microbudgeting, where politicians are hesitant to make sweeping, potentially riskier changes to existing allocations. Instead, they tend to favor incremental adjustments out of concern that disruptive changes could provoke political complications, impacting the balance of power. Insights from organization theory, such as Zeelenberg and Beattie’s (1997) research on the motivation to avoid regret, shed light on regret aversion beyond financial contexts. Individuals may adjust their risk-taking behavior based on past experiences and may deviate from rational decision-making principles when anticipating regret over potentially unjustified decisions. In such scenarios, individuals often opt to maintain the status quo or conform to prevailing preferences.

Building upon these insights, we propose that regret aversion affects budget judgment behavior. We argue that politicians’ preference for maintaining the status quo stems not only from a desire for political stability but also from their instinctive aversion to regret. Politicians intuitively anticipate the regret they may experience if disruptive changes to existing allocations do not yield favorable outcomes. Therefore, they tend to prefer the status quo or incremental changes that are easily reversible. The systematic consideration of regret may also deter politicians from initiating new projects or implementing new taxes, thereby contributing to a tendency toward inaction. To empirically investigate the impact of regret aversion, we propose the following hypothesis:

Mental accounting bias encompasses the tendency to treat discrete elements in isolation, neglecting the broader context within which these elements exist. This phenomenon leads households to take out loans for contingencies even when they possess sufficient savings (Lekovic, 2020). It also prompts individuals to respond differently depending on the source of their money or their intended use for it (Thaler, 1985). Individuals are highly susceptible to mental accounting, as evidenced by portfolio managers who focus on maximizing the profit of individual properties rather than optimizing the overall portfolio for a greater chance of substantial returns (Waweru et al., 2014).

Despite its significance, mental accounting is understudied in Public Administration literature. To contextualize the insights from the review within the public sphere, we must draw upon the Public Finance literature. Here, it is revealed that citizens tend to assess the fairness of taxes by considering individual components rather than evaluating taxes as a whole (McCaffery & Baron, 2006). This behavior is associated with the disaggregation effect, wherein individuals struggle to comprehend how changes in one part of the system can offset changes in another part (see Guragain & Lim, 2019). Moreover, studies have investigated the influence of mental accounting on spending preferences, showing that municipal bureaucrats respond differently to various types of windfalls and resources based on their source (Becker et al., 2020; Heyndels & Van Driessche, 1998). These findings are consistent with the flypaper effect, which suggests that municipal expenditures increase more rapidly in response to additional government grants compared to increases in private municipal income of an equivalent size (Hines & Thaler, 1995).

We anticipate that mental accounting also plays a role in shaping the formation of budget predecisions by politicians. Particularly in a context where a large budget is compartmentalized into increasingly smaller parts, the cognitive processing of these various labels will present a challenge. Despite the distinct legal status of actual budgetary accounts compared to mentally created accounts, it is evident that politicians become psychologically attached to designated accounts once they have been established. Politicians wield the authority to allocate the budget and create accounts, including the power to redirect funds from obsolete accounts. However, the termination of unused reserves or altering their designated purposes is not commonly practiced (Van der Lei, 2019). This reluctance to change may be linked to mental accounting bias that impedes the exploration of alternative expenditures, particularly when those expenditures are unrelated to the original earmark of a reserve. We formulate the following hypothesis to test the effect of mental accounting bias:

We consolidate the findings pertaining to common cognitive biases, alongside the formulation of 12 hypotheses, within Table 1.

Overview of Evidence and Hypotheses

Research Agenda

This study responds to recent calls for renewed attention to public budgeting behavior by leveraging insights from decision-making research in the private sector to refine and update existing perspectives in behavioral budgeting research. It acknowledges the complexities of comparing decision-making between the private and public domains, given the significant group dynamics involved in public budgeting compared to individual decision-making in the private sector. Also, while much of the reviewed literature focuses on investment decisions, this represents only one facet of public budget decision-making. Nevertheless, this perspective proves valuable in uncovering dynamics of financial decision-making behavior at the micro-level, particularly concerning the influence of cognitive biases. Rather than further refining concepts and effects through more precise and detailed reviews, we propose investigations to empirically explore the influence of biases and potential solutions. Below, we outline several research avenues aimed at validating and refining the theoretical foundations presented.

First, we advocate for targeted research to understand the impact of cognitive bias on budget judgment. Conducting this research using survey experiments, where specific features of budgetary information can be manipulated, seems essential. For instance, employing high and low anchor points in otherwise comparable vignette scenarios can provide insight into the extent to which politicians’ predecisions gravitate toward numbers provided in a proposal, even when their preferences differ. If this tendency is observed, extra caution is required when formulating proposals and deciding whether to include specific information features. The advantage of experiments lies in their high internal validity, which can effectively demonstrate the targeted influence of specific biases. However, the Behavioral Public Administration literature is rapidly evolving, and it is crucial to consider valid criticisms of existing research when outlining behavioral budgeting studies. Bhanot and Linos (2020) highlight methodological rigidity and call for non-experimental behavioral research. In behavioral budgeting research, this can be achieved through direct observation of how politicians use information to formulate budget predecisions comparable to the work in other domains by Van der Voet and Lerusse (2024) or by shadowing individuals in real or simulated judgment settings. Ethnographic research can also enhance understanding of individual budgeting action, for example, by asking politicians to create visual representations of how they process information through cognitive mapping (see Axelrod, 2015).

Second, we emphasize the need for targeted research on solutions aimed at improving budget judgment behavior, specifically addressing overreaction or underreaction to information features. Instead of solely documenting the existence and effect of bias, future studies should investigate methods to effectively alter behavior. Suppose that, due to availability bias, politicians systematically overspend on exceptional, well-publicized events. As researchers, our task is to identify interventions capable of changing this flawed behavior. One avenue of inquiry, in this case, could involve determining whether targeted infographics presenting factual information can successfully correct availability bias. Increasing attention to the contextualization of solutions is essential (Cantarelli et al., 2020). This means tailoring interventions to the specific budgeting setting, as copying and pasting solutions from other settings often does not work or even has adverse effects (Merrick, 2020). Collaboration with subject matter experts is invaluable for developing substantively appropriate solutions, as is the adoption of design science methods for iteratively refining ideas related to both content and process (Dorst, 2015). Methodological innovation is crucial, particularly when exploring research methods beyond survey experiments to observe behavioral changes in real settings.

Finally, a significant criticism pertains to the focus of behavioral research on individuals, whereas decisions in the public sector are predominantly made by groups (Mohr & Davis, 2023). While this article intentionally and explicitly highlights the behavior of individual budgeters, we acknowledge actions and outcomes at other levels (cf. Ewert et al., 2020; Roberts, 2020). Behavioral budgeting research could play a crucial role in this area, given the central role of financial decisions in public organizations. Empirical research spanning multiple levels can concurrently investigate the impact of cognitive bias on individual actions and its implications for collective actions. Addressing ethical considerations, it initially makes sense to test this in a simulated setting. For instance, through a serious budgeting game a future study can examine the influence of bias on participants’ judgmental behavior at a micro-level, while also assessing how debiased predecisions influence subsequent collective negotiation behavior and outcomes. Galinsky and Mussweiler (2001) have demonstrated the influence of starting points (micro-level) on negotiation outcomes (meso-level). Therefore, correcting divergent predecisions may lead to different collective budget decisions and thereby impact social outcomes (macro-level). To address the criticism that behavioral research often relies excessively on samples of students, paid respondents, and citizens, it is essential to conduct such serious games with real politicians. This contributes to the applicability of insights, given that the behavior of elite decision-makers such as politicians often differs significantly from other respondent types (Christensen & Moynihan, 2024). It would also be insightful to involve civil servants to assess how their judgmental behavior and susceptibility to bias differ from that of politicians, which necessitates refining the hypothesis accordingly.

Conclusion

This conceptual study draws on empirical evidence from adjacent academic fields to illustrate how cognitive biases distort politicians’ budget judgment behavior on the micro-level. While politicians’ preferences vary due to diverse societal, political and personal factors, their susceptibility to bias likely remains consistent. We propose twelve hypotheses and outline a research agenda to investigate whether biases lead to systematic and predictable judgment behavior. Although budget decisions ultimately involve group deliberations, the impact of biases on individual judgment behavior merits careful consideration. Systematic overreactions or underreactions to information features pose inherent risks and can significantly influence the collective allocation of public funds. Therefore, it is crucial to develop and test solutions aimed at mitigating these biases and correcting behavior. Doing so will facilitate negotiations with clearer starting positions, thereby enhancing the likelihood of securing adequate resources to effectively address public concerns that are deemed important by politicians themselves.

Footnotes

Acknowledgements

This article is from a special symposium on Budgeting Mechanisms and Behaviors, with guest editors Dr. Can Chen (Georgia State University) and Dr. James Douglas (University of North Carolina at Charlotte).

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funded by Dutch Review Council (NWO, grant number VI.Veni.211R.001).