Abstract

In countries with well-developed welfare state systems, it is often claimed that racial or ethnic minorities impose a heavy burden on social assistance programs without contributing to public goods. In this study, we consider the attitudinal effects of anecdotal reports of tax cheating by minorities. We conduct survey experiments in France and the United States to assess if people react more harshly to tax fraud perpetrated by members of a minority group rather than the majority group. We find no evidence that minority status affects judgments and perceptions about tax fraud, including among those on the right end of the political spectrum. Tax fraud is considered unacceptable regardless of the culprit’s origin.

In countries with well-developed welfare state systems, it is often claimed that minorities impose a heavy burden on social assistance programs without contributing to public goods (Gilens, 1995, 1996; Harell et al., 2016). 1 Previous research on biases in attitudes toward public finance focuses on the spending-side rather than the revenue-side of the fiscal equation. Yet, biases run both ways. We know that people are more willing to fund public spending that benefits their own group (Belmonte et al., 2018; Nemore and Morone, 2019; Xin Li, 2010). We also know that intergroup animus colors views about welfare spending and welfare fraud (Gilens 1995, 1996; Harell et al., 2016). So, when it comes to tax fraud, it follows that culprits’ minority or majority status should color views about taxation.

In this research note, we assess whether individuals react more negatively to anecdotal reports of tax fraud featuring minorities. We field cross-national surveys in the France and the United States, both of which have large minority populations: Arabs in France and Hispanics in the United States. We design a series of vignettes describing common tax fraud schemes, each featuring a small business owner with randomly manipulated minority versus majority status.

Surprisingly, our results show no evidence of outgroup bias in citizens’ reactions to tax fraud. We also find no evidence that people’s political predispositions moderate our treatment effects. These null results have important implications at the intersection of intergroup relations and fiscal policy. Specifically, they suggest that racial and ethnic biases do not influence judgments and perceptions of tax noncompliance. This is likely because people place more weight on the illicit nature of tax fraud than on the identity of its perpetrators.

Background

Taxation is a fertile area for intergroup conflict, because it brings together two sets of reinforcing phenomena, the first socio-psychological and the second economic.

First, socio-psychological theories of intergroup conflict see tensions and discrimination between social groups as the result of deeply entrenched tendencies to favor one’s own group and to hold negative attitudes toward outgroups (Sherif, 1966; Tajfel et al., 1971 see Böhm et al., 2020 for a review). This has far-reaching implications for public finance in diverse societies and for how citizens evaluate government policy to reduce poverty and redistribute income (Gilens, 1995, 1996). Notably, research on welfare chauvinism finds that prejudice toward minorities reduces support for social assistance programs and increases support for limiting these programs to native citizens (Harell et al., 2016; Stichnoth and Van der Straeten, 2013; Van der Meer and Tolsma, 2014).

Second, economic theories of intergroup conflict see prejudice through the lens of competition over scarce resources between social groups. A case in point is immigration. (see Hainmueller and Hopkins, 2014 for a review). The tax burden hypothesis posits that opposition to immigration is driven by concerns pertaining to fiscal policy, with natives fearing that newcomers—particularly those with low levels of formal education—might increase demand for welfare spending without contributing much in taxes (Facchini and Mayda, 2009; Hanson et al., 2007).

Attitudes about taxation are shaped by outgroup biases to a great extent. Residents of diverse countries express more dissatisfaction toward taxation than those from more homogeneous countries (Xin Li, 2010). Belmonte et al. (2018) show that aversion to diversity has negative consequences on tax compliance, particularly among residents of heterogeneous countries. These findings are corroborated by Nemore and Morone (2019), who establish an association between anti-immigrant attitudes and willingness to pay taxes. Nemore and Morone (2019: 12) note that there is “widespread concern that immigrants are making increasing use of public assistance programs” exacerbating dissatisfaction toward taxation among natives. In short, immigration might accrue fiscal concerns, weakening citizens’ support for the tax system.

We expect citizens to react more harshly to tax fraud committed by out-group members. We know that prejudice shapes evaluations of offenses or transgressions committed my members of a minority group: individuals generally tend to be more lenient when members of the majority group commit the exact same acts (Hartman et al., 2014). We expect this relationship to be moderated by people’s political predispositions: tax fraudsters’ minority status should result in more negative reactions among conservatives. This is because conservatism shapes views on taxation and tax compliance (Lozza et al., 2013; Nemore and Morone, 2019) and predicts racial and ethnic prejudice and anti-immigration sentiment (Hainmueller and Hopkins, 2014), which, in turn, worsen dissatisfaction with the tax system (Belmonte et al., 2018; Nemore and Morone, 2019).

Survey Experiment

We field pre-registered online survey experiments in France and the United States. 2 Our 4000 respondents (2000 per country) are adults recruited to meet population quotas for age, gender, education, and region. We present our full survey instrument in the Supplemental Appendix.

France and the United States both have large minority populations stemming from immigration. In France, Arab Muslims represent approximately a tenth of the population (Sahgal and Mohamed, 2019). In the United States, Hispanics account for nearly a fifth of the population (Krogstad and Noe-Bustamante, 2020). Arabs and Hispanics are the subject of stereotypes, both cultural (e.g. they fail to assimilate) and economic (e.g. they have unskilled jobs).

Our experiment consists of three vignettes featuring small business owners who commit tax fraud. We randomly manipulate their name to signal minority status. 3 In France, the control is a French name, and the treatment is a Maghrebi Arab name. In the United States, the control condition is an Anglo-Saxon name, and the treatment condition is a Hispanic name. The American vignettes are as follows 4 :

Car dealership. [Harry Johnson/Enrique Gómez] owns an auto repair shop. For his daughter’s 20th birthday, [Harry/Enrique] buys her a used car. He then tells the Internal Revenue Service (IRS) that the cost of this car is a business expense to save on taxes.

Fast food. [Steven Jenkins/Esteban Jiménez] is the owner of a fast food restaurant. He hires a part-time employee to help wash the dishes, but he pays him in cash, “under the table,” to avoid paying payroll taxes.

Roofing. [Peter Williamson/Pedro Villaseñor] is the owner of a roofing company. He charges $4000 to repair the roof of a customer’s house, but he offers a $500 discount if the customer pays in cash. If the customer agrees, [Peter/Pedro] will not report the cash payment to the IRS.

The order in which these vignettes were shown was random, but respondents could be assigned to two treatment conditions at most. This randomization process prevented a situation in which some respondents would have been presented with illicit scenarios involving only minorities.

Each illegal business transaction is followed by our two outcome variables:

Acceptability. How acceptable or unacceptable is this behavior? 0 means completely unacceptable, and 10 means completely acceptable.

Prevalence. What percentage of people in the United States would do the same thing as [NAME] if they were in his place?

These questions are commonly used in work on attitudes toward tax fraud (Horodnic, 2018). The first is a measure of injunctive norms surrounding tax fraud—what others should do (Hallsworth et al., 2014). The second question accounts for descriptive norms of tax compliance—what others actually do (Hallsworth et al., 2014). Both dependent variables range from 0 to 1 in our analysis.

We measure respondents’ political predispositions using a left–right self-placement scale in France and a threefold party identification scale in the United States. In our analysis, the moderator variable ranges from 0 (left-wing/Democrat) to 1 (right-wing/Republican).

Empirical Analysis

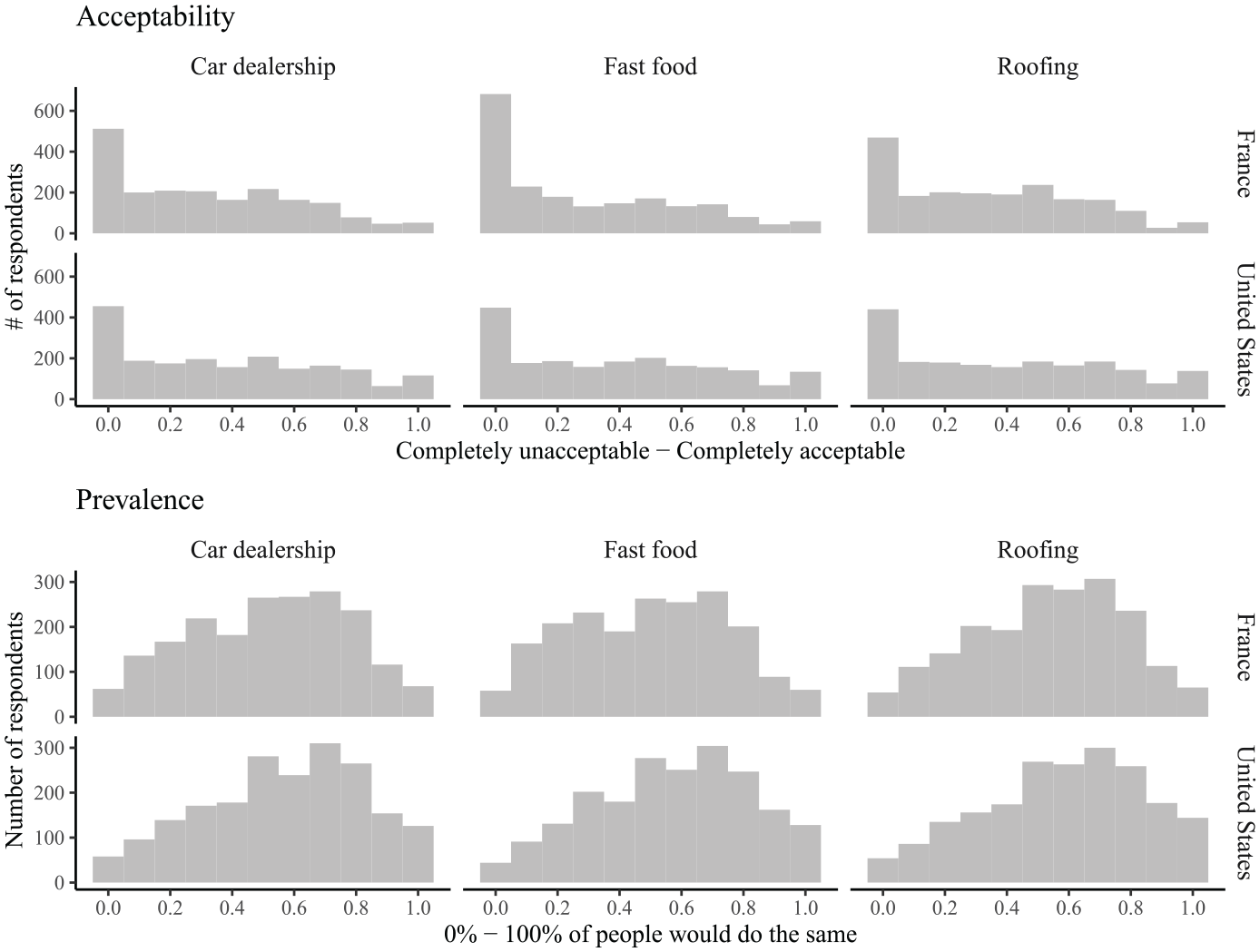

Reactions to the tax crimes featured in our experiment were quite negative. Figure 1 shows the distribution of our two dependent variables. Across all vignettes, the mean of the acceptability outcome is low (0.32 in France and 0.39 in the United States); in each country, around a quarter of respondents said that tax fraud was “completely unacceptable” (0). For the prevalence outcome, again across all vignettes, the mean is 0.52 in France and 0.58 in the Unites States.

Distribution of the Two Dependent Variables in the Three Vignettes and Two Countries.

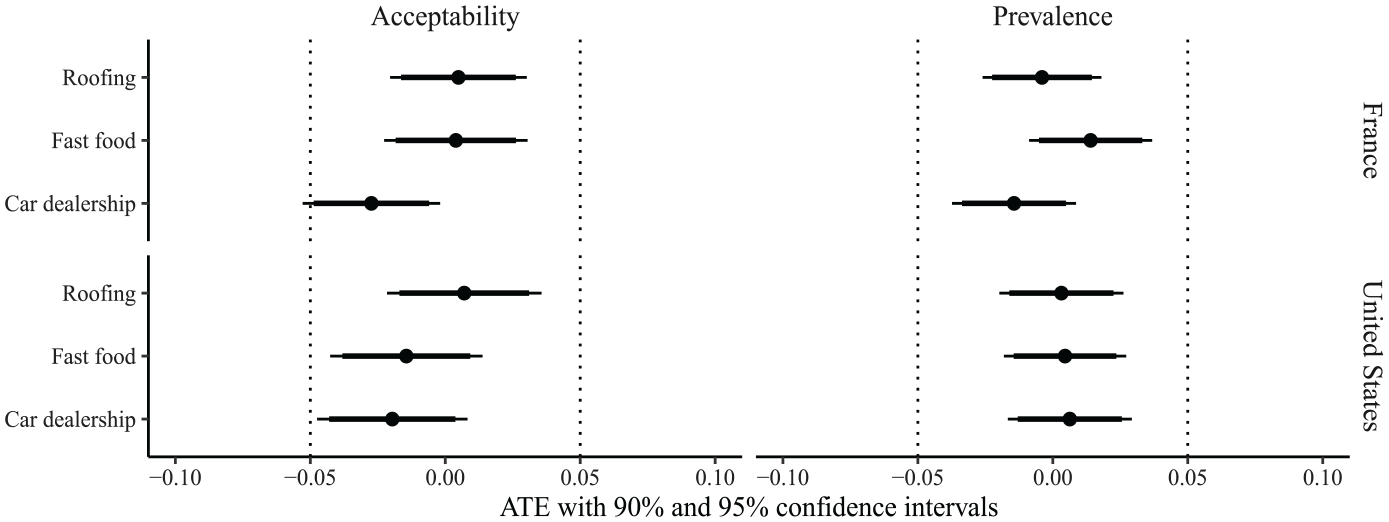

To ascertain the causal effect of our experimental manipulation, we calculate the difference in means between the treatment and control groups separately by outcome, vignette, and country. The resulting 12 average treatment effect (ATE) estimates along with 90% and 95% confidence intervals are plotted in Figure 2 (see the Supplemental Appendix for balance and regression tables). Nearly all ATEs are indistinguishable from zero. The only statistically significant (p < 0.05) ATE is very small, which is most likely due to luck. Assuming that any estimate smaller than |0.05| is substantially negligible, it follows that all possible negligible effects should be greater than −0.05 and smaller than 0.05 (Rainey, 2014). The two vertical, dotted lines in Figure 2 plot these bounds. Since no value contained by the 90% confidence intervals falls outside this region of negligible effects, it is possible to reject the null hypothesis of a meaningful effect with an α level of 0.05. 5

Average Treatment Effect Estimates.

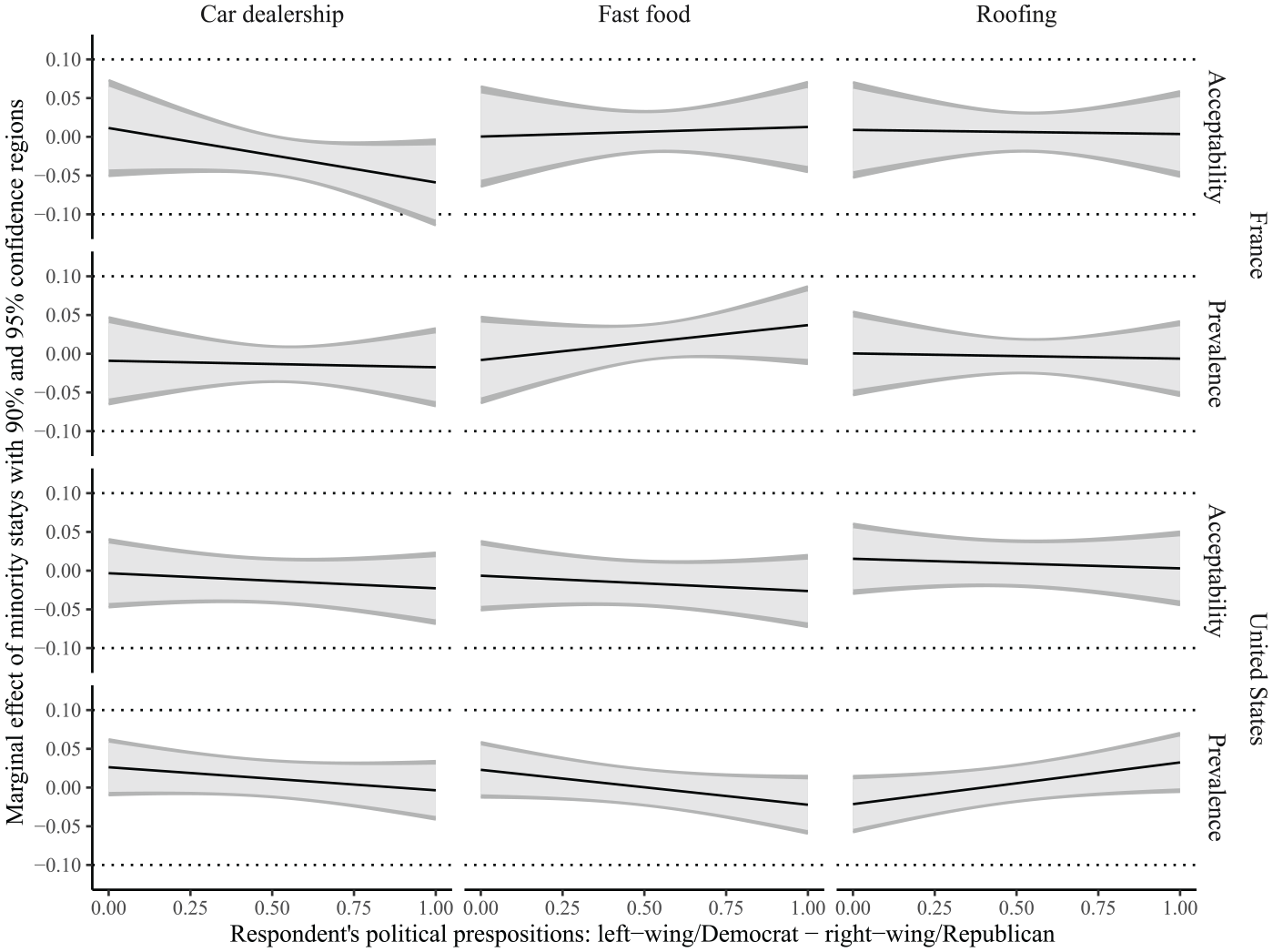

To determine if the treatment effects are moderated by ideological (in France) or partisan (in the United States) predispositions, we estimate 12 models with multiplicative interactions (see the Supplemental Appendix for regression tables). Figure 3 shows that partisanship and ideology do not condition the name treatment effects in any meaningful way for all scenarios, outcomes, and countries.

Average Treatment Effects Estimates Conditional on Political Predispositions.

We fail to reject both null hypotheses: tax fraudsters’ minority status does not affect respondents’ evaluations of the acceptability and prevalence of tax fraud schemes; moreover, these treatment effects are not conditioned by respondents’ political predispositions. 6

Discussion

We administered survey experiments in France and the United States to test two hypotheses: first, that people react more negatively to tax fraud committed by minorities; and second, that this treatment is stronger among conservatives. We do not find empirical support for either hypothesis.

One might assume that public tolerance for tax fraud is higher than for other crimes (Kaplan and Reckers, 1985) since it leads to fewer social and legal consequences (Alldridge, 2017; De La Feria, 2020). Given the strength of prejudice on other areas of public finance (e.g. welfare), one might expect outgroup biases to also shape attitudes related to tax fraud, which should be frowned upon when perpetrated by the minorities but tolerated among members of the majority group. Yet, we find no evidence of this: levels of disapproval are consistently high regardless of the fraudster’s group membership. Judgments and perceptions about tax fraud may be changing, likely because of the financial crisis’ impact on public views about taxation (Christensen and Hearson, 2019).

We see three explanations for our results. One possibility is that our French and American respondents are not biased against Maghrebis and Hispanics. This conclusion seems implausible since it goes against vast bodies of work on prejudice and biases (Böhm et al., 2020; Hainmueller and Hopkins, 2014; Stichnoth and Van der Straeten, 2013; Van der Meer and Tolsma, 2014).

A different explanation is that our name treatments were too weak. While this is certainly possible, we note that the full names of the tax fraudsters appeared at the very beginning of our vignettes, leaving no ambiguity at all about their Hispanic or Maghrebi backgrounds. Individuals can easily infer minority status from just names (Butler and Homola, 2017; Crabtree et al., 2022; Landgrave and Weller, 2022).

A more plausible interpretation is that outgroup biases are outweighed by the negative nature of the tax fraud behavior itself. While these biases are often very strong when it comes to redistribution or welfare (Gilens, 1995, 1996; Harell et al., 2016), they may be weakened by concerns about the viability of the tax system. The sense of unfairness arising from our illicit scenarios may have trumped prejudice, the tax fraud scenarios themselves stirring overwhelmingly negative reactions regardless of the origin of the culprit. This suggests that attitudes toward tax fraud are more negative than previous research on white-collar crime would indicate, and that outgroup biases may not be as pervasive as prior research has found—a noteworthy null result.

Supplemental Material

sj-pdf-1-psw-10.1177_14789299231162017 – Supplemental material for Outgroup Bias and the Unacceptability of Tax Fraud

Supplemental material, sj-pdf-1-psw-10.1177_14789299231162017 for Outgroup Bias and the Unacceptability of Tax Fraud by Marco Mendoza Aviña, André Blais, Vincent Arel-Bundock, Rita de la Feria and Allison Harell in Political Studies Review

Footnotes

Acknowledgements

We thank the journal’s editors and reviewers as well as Stephen Ansolabehere, Fernando Feitosa, Uma Ilavarasan, Jean-François Laslier, Umut Turksen, and Donato Vozza.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was funded by a grant from the Social Sciences and Humanities Research Council of Canada (#435-2019-0434).

Ethical approval

The research design was approved by the ethics review board of the Université de Montréal (#CERAH-2020-020D).

Supplementary information

Additional supplementary information may be found with the online version of this article.

Content Appendix A. Survey instrument. A.1. United States. A.2. France. Appendix B. Balance tables. B.1. United States. Table 1. Car dealership. Table 2. Fast food. Table 3. Roofing. B.2. France. Table 4. Car dealership. Table 5. Fast food. Table 6. Roofing. Appendix C. Regression tables. C.1. United States. Table 7. Average treatment effects. Table 8. Conditional average treatment effects. C.2. France. Table 9. Average treatment effects. Table 10. Conditional average treatment effects. Appendix D. Multiplicity adjustment and clustered standard errors. Table 11. p values from IID standard errors, standard errors clustered by respondent, and standard errors corrected for multiple comparisons following Hochberg (1988). Appendix E. Power analysis. Figure E.1. Power curve to detect an average treatment effect in a model without interaction. Figure E.2. Power curve to detect an average treatment effect in a model with an interaction. Appendix F. Pre-analysis plan.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.