Abstract

In Germany, economic and financial concepts are characterized by the prevailing Western economic legal system. These are not always in line with the economic and financial concepts in Islam (e.g., prohibition of interests in Islamic law). The more important Islamic financial institutions are in a country, the stronger the impact of Islamic financial principles on the economic and financial knowledge of the population. People who migrated from predominantly Muslim countries were usually family-socialized with concepts of Islamic Economy and Finance and impart this information to their offspring. Young adults who grow up in an environment that is not shaped by Western (cultural) views may be particularly affected. The lack of systematic inclusion of economic and financial content in German general education curricula leads to challenges in understanding these concepts. Here, a two-part qualitative interview procedure was used to investigate possible challenges in the understanding of economic and financial terms and concepts by people with a Muslim background (eight respondents were interviewed in summer 2022). In this article, the findings on the identified barriers are presented and discussed. Subsequently, the implications for economic education are outlined, including the need to raise awareness among (prospective) teachers for migration-specific concepts, the special needs of heterogeneous classes with regard to migration backgrounds and the development of target group-oriented teaching and learning materials in economic and social education.

Keywords

Introduction

Higher levels of economic and financial knowledge enable individuals to make better financial decisions, achieve greater personal financial well-being (Council for Economic Education (CEE), 2021; Klapper et al., 2015), minimize the chance of financial hardships and social welfare dependencies and thus improve the stability of the economy as a whole (Lusardi and Mitchell, 2014). To make sound economic and financial decisions on an individual level and as a society it is mandatory that each individual citizen and the society both have a certain level of economic and financial knowledge. Due to the outlined importance, researchers see these facets of economic and financial knowledge as part of a citizenship education that enables sound and informed decisions (Davies 2015; Greimel-Fuhrmann, 2013; Sherraden and Ansong, 2012).

Studies show that the level of economic and financial knowledge correlates with various factors, such as age, gender, level of education, socio-economic background and MB 1 (Cwynar, 2022; Lusardi and Mitchell, 2011; Worthington and Marzuki, 2022; Wuttke et al., 2020). Both in Germany and internationally, people with MB score lower on tests of economic and financial knowledge than people without MB (Happ and Förster, 2019; Kaiser et al., 2020a; OECD, 2017; Walstad et al., 2013). There are several reasons for this, some of which are mutually reinforcing (Lokhande, 2016). In addition to language, the level of economic development, the economic system, financial instruments, experience in financial services and the level of education in the home country (Cwynar, 2022; Worthington and Marzuki, 2022) as well as the socio-economic background of people with MB are important for the acquisition of economic and financial knowledge (Happ and Förster, 2019). Following the forementioned aspects and the backdrop of increasing migration movements in Germany (Federal Statistical Office, 2022), a more in-depth examination of the barriers in understanding the economic and financial terms and concepts of migrants is relevant. According to the current micro census, 24.9 million people in Germany have some sort of MB, which adds up to almost a quarter of the total population (Federal Statistical Office, 2024). At around 5.6 million, the group of people with a Muslim background is the largest group of people with MB in Germany (Pfündel et al., 2021). In terms of hindering factors for a lack of economic and financial knowledge of people with a Muslim background the literature (e.g., Pohlhausen and Beck, 2010; Worthington and Marzuki, 2022) mention concepts of Islamic finance like the prohibition of Riba (interest) and Gharar (transaction with an unacceptable level of uncertainty or deceptive uncertainty) as challenging. These concepts are seen as far distanced from the prevailing Western-style economic legal system in Germany and its economic and financial system 2 (Pohlhausen and Beck, 2010; Worthington and Marzuki, 2022). In contrast to laws of a certain country, the Islamic finance concepts cannot be seen as limited to countries. These concepts are derived from Sharia. 3 As consequence these concepts are affecting people across borders.

In addition to the identified influences on and lack of economic and financial knowledge, there are hardly any systematic formal economic and financial education programs in schools in Germany to foster economic and financial knowledge (Kaiser et al., 2020b). Complementary to the lacking formal opportunities Karakaşoğlu et al. (2017) point out that the intercultural skills and awareness for migration-specific topics of teachers in Germany are only poorly developed. Thus, teachers in Germany are not sufficiently prepared to address the migration specific needs of the few economic and financial topics in school appropriately. One of the reasons cited is that there is limited coverage of these topics in teacher education (Karakaşoğlu et al., 2017), so awareness of them is low and it is therefore almost impossible to address them appropriately in lessons. By identifying migration-specific concepts, a contribution is made to raising awareness. Due to the few formal learning opportunities and the additional lack of appropriate migration-specific addressing in the classroom, other sources are necessary for the acquisition of economic and financial knowledge. The family is not only the most important source (Danes, 1994; Gudmunson and Danes, 2011), but also almost the only source for the acquisition of economic and financial knowledge. In the case of parents with MB, this can lead to an unfavorable situation in which they impart knowledge that is outdated or is shaped by distant economic and financial systems (Cwynar, 2022; Worthington and Marzuki, 2022) that do not fit the circumstances of the German economic and financial system.

To date, it has mainly been quantitative studies that have investigated the influence of MB on economic and financial knowledge. Few studies have focused on exploring the specific challenges and causes in the understanding of economic and financial concepts of young adults with a Muslim background. In order to explore these challenges, qualitative studies are beneficial (Kruse, 2014).

From these research gaps, the overarching aim of this article is to identify challenges in understanding Western-style economic and financial terms and concepts among young adults with a Muslim background. Section 2 presents the theoretical concepts and the current state of research on economic and financial knowledge and the Islamic financial concepts of Riba and Gharar. In addition, the research questions for the study are formulated in this section. Section 3 outlines the research design and the survey instruments before presenting the results in Section 4. Based on the findings and the research methods used, Section 5 discusses the limitations of the study and educational implications for raising awareness of migration-specific concepts for (potential) teachers.

Theoretical background and state of research

Economic and financial knowledge and its (religious) influences

In economic education, the terms economic and financial knowledge are sometimes used and systematized inconsistently (Haupt, 2022: 79). This study follows the definition and classification of the “integrative framework model” by Happ (2020: 10), which understands financial knowledge as a component of economic knowledge. 4 The integrative model offers a unifying approach that combines various interrelated concepts such as basic economic and financial knowledge (Happ, 2020: 14).

The CEE (2010) developed standards for 20 fundamental economic core concepts, which are based on the Western economic legal system with its modes of operation and principles and form the content framework for economic knowledge. Based on this theoretical conceptualization, basic financial knowledge is located as a component of economic knowledge (Happ, 2020: 10–15). The CEE (2018) developed a six-content area encompassing framework for financial knowledge. Förster et al. (2017) adapted this framework to Germany and consolidated from six to three areas (everyday money management, banking, insurance 5 ) as the content framework for the assessment of the respondents’ financial knowledge in Germany.

With respect to the findings of Brown et al. (2018) and the assumptions of Happ and Förster (2019) a lower score of economic and financial knowledge in tests by young adults with MB cannot be exclusively explained by a language barrier. Consequently, there are more facets which should be considered like non-cognitive factors (e.g., affective components such as interest in, attitudes towards, and experience with economic and financial facets). Furthermore, as outlined in the introduction a lower score of economic and financial knowledge of people with a MB can be assumed due to deviating economic and financial systems in the country of origin (Cwynar, 2022; Worthington and Marzuki, 2022). Thus, people who migrated from those countries were not able to acquire and had no experience with comparable economic principles (planned economy vs. market economy) and financial instruments (e.g., stock market, interest and insurances) in their countries of origin and country of arrival (Frijns et al., 2013). In tracing this argumentation, Worthington and Marzuki (2022: 471–472) suggest that due to Islamic financial concepts, the concepts of interest, inflation, risk, money as an asset and diversification are challenging for Muslim people according to the Western understanding of financial literacy. Especially two Islamic Finance concepts are contradictory to the prevailing western economic and financial concepts on individual and societal level: Riba and Gharar (Oberauer, 2017; Worthington and Marzuki, 2022). However, the awareness and observance of Islamic financial concepts by Muslims is subjective and depends on the degree of religiosity (cf. Ilfita and Canggih, 2021). According to Worthington and Marzuki (2022: 471), one of the fundamental differences between the two systems is that “[I]n Islamic finance, money cannot serve as an asset or commodity to generate profits but can only be a medium of exchange to create social value rather than wealth”. This principle and the general orientation of Islam to promote the well-being of humanity, to prevent social inequality, injustice and the exploitation of vulnerable groups in order to promote the well-being of all and protect it from harm is also reflected in the two concepts of Riba and Gharar (Worthington and Marzuki, 2022: 471; Suleiman, 2021: 179–180).

Riba is determined in Sharia as surcharge on capital and literal translated as a surplus, increase or supplement. This surcharge is declared as an unjustified increase and unsocial distribution of income (Visser, 2009: 31), which leads to social inequalities (Suleiman, 2021: 174). It is forbidden in Islam to pay interest or to demand interest (cf. e.g., in the Qur'an: al-Baqara: 275; in ahadith 6 : An-Nawawi, 2013: 462, hadith no. 1614: 463, hadith no. 1615). The prohibition is based on the fact that personal enrichment of one's own wealth without a return is unlawful and not in the interest of general prosperity (Visser, 2009). In Germany, paying or charging interest applies to almost every form of investment, every conventional current account or every credit card (El-Din and Hassan, 2007) and represents restrictions for Muslims. In this paper, the focus is on Riba al-qarud, which refers to the prohibition of charging interest when borrowing or lending money (Algaoud and Lewis, 2007). 7

The prohibition of Gharar (cf. e.g., in the Qur'an: al-Māʾida: 90–91; an-Nisāʾ: 29) is predominantly intended to ensure transparency, fairness and calculability in business activities (Visser, 2009: 45). Gharar is translated as an unacceptable degree of uncertainty or deceptive uncertainty in business activities that violates the fairness between business partners or the transparency of the business are prohibited under Islamic law (Aboguddah, 2020: 15; Suleiman, 2021: 180). The term Gharar is connoted with the terms misleading, deception or fraud (Visser, 2009). Transactions with low or unavoidable uncertainty are permitted (Suleiman, 2021: 181). Transactions are also acceptable if uncertainty arises about a possible additional benefit that is not known in advance and does not disadvantage any of the contracting parties (Suleiman, 2021: 181). Furthermore, agreements that are based on unavoidable needs are valid. Specific reference is made here to mandatory insurance, such as car or health insurance in certain countries (Suleiman, 2021: 182). Transactions that do not precisely define the contractual components of performance and consideration are considered haram 8 (Algaoud and Lewis, 2007; Suleiman, 2021: 181). This includes transactions in which the quality and quantity of products are not yet known or foreseeable at the time the contract is concluded or at the time of contract fulfillment (Algaoud and Lewis, 2007; Suleiman, 2021: 180–181).

For the German financial system, these definitions of prohibitions include refraining from transactions in stock exchange trading (El-Din and Hassan, 2007: 241), investment transactions 9 , in particular futures or options transactions on the stock market (Algaoud and Lewis, 2007: 40) and insurance (Visser, 2009: 46). In the case of insurance transactions, the problem is that when the contract is concluded, it is not possible to foresee whether the loss event is adequately covered by the payments and amounts agreed at the time the contract is concluded or how the contents of the contract should be viewed if no loss event occurs, as the risk must be minimized from all sides (Visser, 2009). Furthermore, transactions in which traders are not yet in possession of the goods or consumers are unable to assess the quality of the goods are also affected.

Given the insufficiently investigated state of research on the reasons for a lack of understanding of Western-influenced economic and financial terms and concepts among people with Muslim MB, two research questions arise:

Research question 1 (RQ 1): Which Western-influenced economic and financial terms and concepts are challenging for young adults with a Muslim background to understanding Western economic and financial concepts?

Research question 2 (RQ 2): What reasons can be identified for the challenges young Muslims face in understanding Western economic and financial concepts and terms?

Research method

Design of the study

A qualitative research design is suitable for the outlined research objective (Section 1). Qualitative methods make it possible to determine causes and their correlations by asking open questions, allowing the respondents to formulate statements freely and justify them in detail (Kruse, 2014). In order to answer the research questions, a two-part approach was developed using two qualitative research methods. The first part is a problem-centered interview (PCI) (Witzel, 2012). The second part is a think-aloud interview (TAI) (Leighton, 2017). In order to avoid cognitive overload (see Cognitive Load Theory (Sweller, 2011)) of the respondents, the interviews took place on two separate days. In line with the methodological principles (Witzel, 2012), the overall aim of the study was presented to the respondents when they were contacted. In addition, the legal provisions on data protection and anonymization of the data were explained.

Based on the findings of previous research (Happ and Förster, 2019; Haupt, 2022; Worthington and Marzuki, 2022), the problem-centered interview consists of the following blocks of questions:

- socio-demographic and economic background, - religion and values of the test persons and their parents, - migration-related issues and - financial socialization.

The think-aloud interview consists of a simultaneous (periactional) and a retrospective part. In the periactional part, the focus is on the disclosure of problem-solving processes. Leighton (2017: 21) explains that the problems must be so new and complex that they cannot be answered immediately with existing knowledge. These requirements are justified by the fact that this is the only way to prompt the working memory to transform information and design new solution patterns, to initiate problem-solving processes and not merely to retrieve information/knowledge (Leighton, 2017: 21–22). The aim of the TAI is to generate insights into the respondents’ problem-solving processes. In addition to these, the approach and its background as well as explanations of what knowledge was used for solutions are of interest. Retrospective questions that follow the conclusion of the periactional interview part are suitable for gaining this information (Leighton, 2017: 48–49). Both parts of the TAI require different instructions so that the respondents can focus clearly on the respective processes (Leighton, 2017: 43, 49). Items from the Test of Economic Literacy (Walstad et al., 2013) are used to identify the respondents’ challenges in the area of economic knowledge. Items that have been used in quantitative studies to assess economic (TEL) and financial (TFL) knowledge were selected for the survey (Förster et al., 2018; Happ and Förster, 2019).

10

The items were selected based on the average number of correct answers given for the individual items, differentiated by group (with MB and without MB). One item with a large, small and no difference between the two groups with MB and without MB was selected from the TEL questionnaire and the respective EDM, banking and insurance sections of the TFL.

11

The items were arranged in such a way that the difficulty of the questions initially increases (Krohne and Hock, 2015: 50) and then decreases again slightly at the end to avoid test fatigue (Leighton, 2017).

Sampling

The age range between 18 and 25 is considered a sensitive area for financial socialization (Gudmunson and Danes, 2011) and is of particular importance, as it is during this phase that financial and economic decisions are made for the first time and in which test subjects bear personal and legal responsibility (Förster and Happ, 2018). It is also possible to draw conclusions about previous influences in this phase, for example, experiences from childhood and adolescence (Hurrelmann, 2015: 315–317). Against this background, this age range was chosen as an initial criterion for the selection of test subjects. Due to the unsystematic curricular anchoring of economic and financial education content in the general education system, differences in economic and financial knowledge can be partly explained by culturalist approaches (Ramirez-Rodriguez and Dohmen, 2010). In these approaches, the family serves as the central educational authority and ensures the formation of attitudes, values and the acquisition of knowledge in many areas (Gudmunson and Danes, 2011; Ramirez-Rodriguez and Dohmen, 2010). Given these influences and the research questions, the characteristic of Muslim background was identified as a second selection criterion. 12 Another factor influencing financial and economic knowledge is the educational background of the respondents (Happ and Förster, 2017). In order to minimize potential bias within this survey, the high school GPA and active student status at a German university were used as a third selection criterion. In order to reduce the influence of acquired knowledge from formal learning environments on the understanding of economic and financial concepts and thus to reveal other underlying influences to a greater extent, a fourth criterion was defined, namely that no previous knowledge of economics in the form of a completed business school leaving certificate, commercial/administrative vocational training or a completed degree with economics content in a major or minor subject may be present. Based on Jacobsen and Meyer (2017: 189), who point to 82% of the minimum and 94.69% of the average problems found with a number of ten respondents, a number of eight to ten respondents was planned.

Qualitative evaluation and sample description

Data analysis

The data material was transcribed according to simple rules and with verbal and paralinguistic features (Kowal and O'Connell, 2005). The qualitative evaluation was based on content analysis according to Kuckartz (2014).

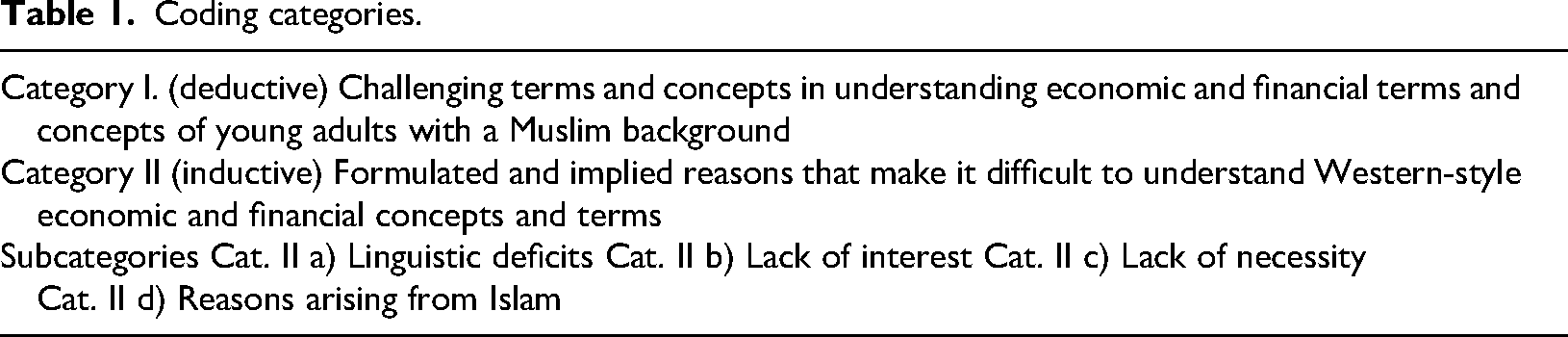

In view of the exploratory nature of the study, the sensitivity to the topic and the resulting openness of the evaluation, only the first category was developed deductively in accordance with the first research question and the underlying study results (Cwynar, 2022; Happ and Förster, 2019; Kaiser et al., 2020a; Worthington and Marzuki, 2022). The second category and its four subcategories were developed inductively from the material (for a summarized category system, see Table 1). The process of consensual coding (Schmidt, 2010) offers the potential to consider different perspectives and thus ensure a more open approach to the material through the discussion process and consensus building regarding the categories and assignments. The interviews were first coded independently by three researchers and then the coding was revised in discussions where necessary. 13 The definitions of the categories are provided in the section qualitative results.

Coding categories.

Socio-demographic background of the sampling

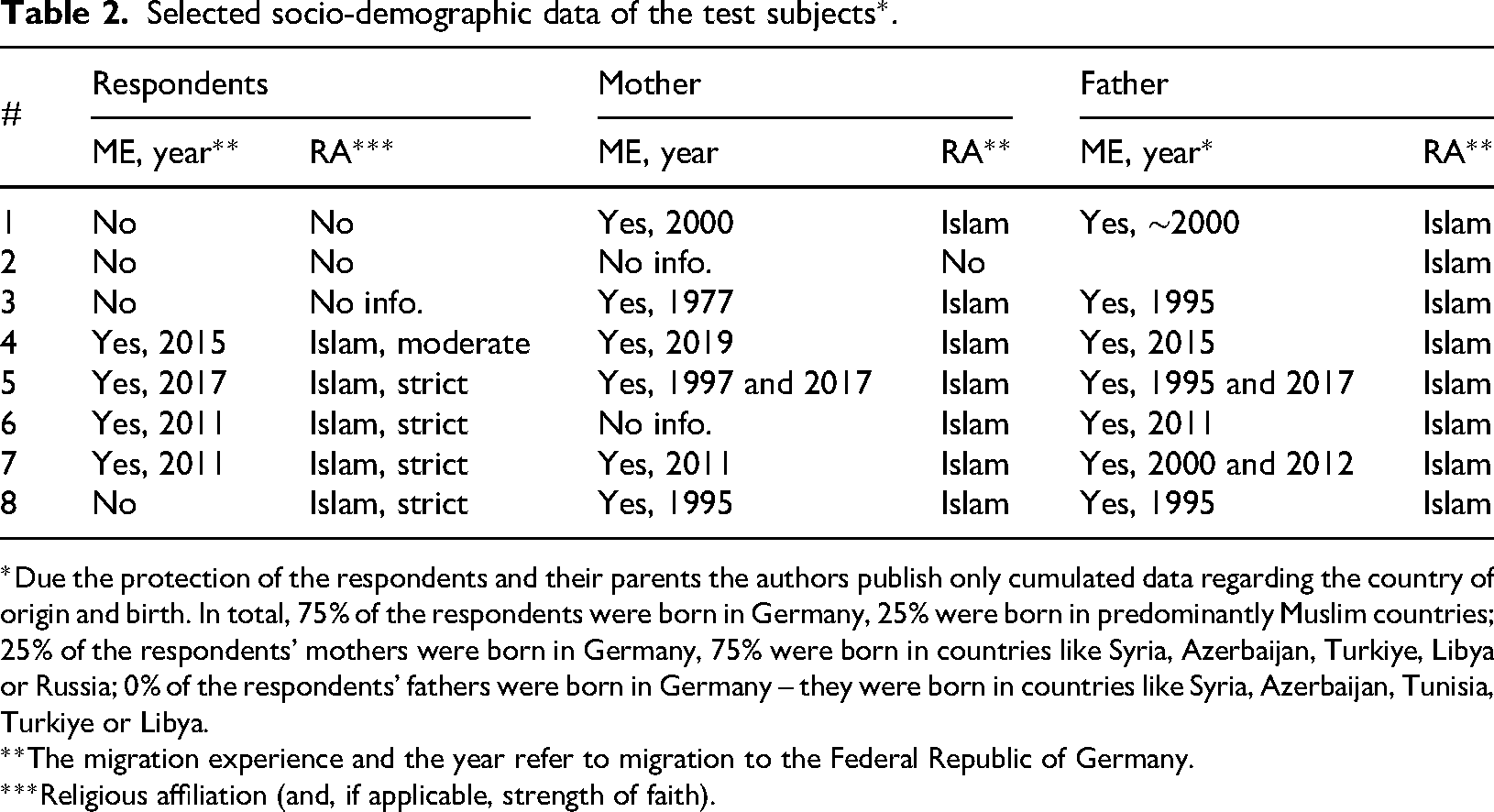

In Table 2 the two parents are categorized according to the following characteristics in addition to the socio-demographic data of the respondents: Country of birth, migration experience (ME), religious affiliation (RA) and their degree of religiosity. 14 In addition to the main criterion of own religious affiliation and its degree (Ilfita and Canggih, 2021), a further differentiation was made using the criterion ME. The country of birth and the ME are intended to measure the influence of socialization processes. Gudmunson and Danes (2011), among others, showed that the socialization experiences of parents and children influences economic and financial knowledge. In relation to the test subjects, there is an equal ratio here: four of the eight test subjects have no ME of their own and four test subjects have their own ME (three from Syria and one from Libya). The four respondents without own ME have at least one parent with ME from Azerbaijan, Tunisia, Syria or Turkiye. The heterogeneity with regard to the different countries of origin as well as the characteristics of RA offer great potential for discovering different influences.

Selected socio-demographic data of the test subjects*.

*Due the protection of the respondents and their parents the authors publish only cumulated data regarding the country of origin and birth. In total, 75% of the respondents were born in Germany, 25% were born in predominantly Muslim countries; 25% of the respondents’ mothers were born in Germany, 75% were born in countries like Syria, Azerbaijan, Turkiye, Libya or Russia; 0% of the respondents’ fathers were born in Germany – they were born in countries like Syria, Azerbaijan, Tunisia, Turkiye or Libya.

**The migration experience and the year refer to migration to the Federal Republic of Germany.

***Religious affiliation (and, if applicable, strength of faith).

In consideration of language as an important factor (Happ and Förster, 2019) the samples’ language distribution is described in the following. Four of the eight respondents proclaim German as their mother tongue. 15 However, the family language is predominantly German for only two respondents. All other respondents communicate primarily with their parents in languages other than German. Additionally, these six respondents have different characteristics. For P1, Azerbaijani is spoken by everyone in the household. P7 changes the language depending on the parent: they communicate with their mother in German and with their father in Arabic. They also communicate with their siblings in German. The other test subjects always use their parents’ native language when communicating with their parents. When communicating with siblings in their own household, on the other hand, German is spoken almost exclusively. The language used in the parental home was not included in table 2, as only P2 uses German as the lingua franca in the parental home.

Descriptive analysis

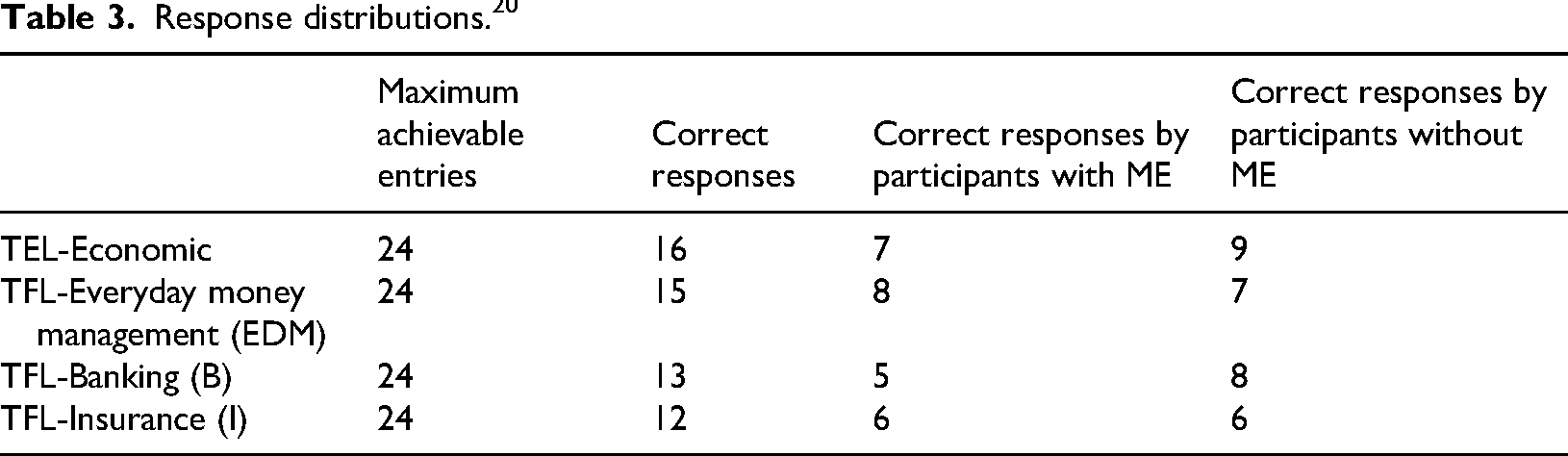

There were three questions for each area TEL, TFL-Everyday money management, TFL-Banking, TFL-Insurance and the correct answers of the eight respondents were totaled for each area. 16 Each question had four predefined answer options, with only one answer option being correct. The descriptive evaluations of the TAI questions show consistent trends with other findings. Analogous to the findings of Schmid (2006), the evaluation of the TAIs shows that the respondents gave the most correct answers in economic knowledge, with 16 out of 24 correct answers (see Table 3). This indicates that there are fewer challenges for the respondents in economics. In the retrospective section, respondents were asked about the subjectively easiest and most difficult tasks they perceived. Here, four respondents stated that they subjectively found tasks from the TEL area the easiest. No respondent indicated a question from the TEL area as the subjectively most difficult question. However, the low level of knowledge of the main function of money when buying a cinema ticket (item A23) should be emphasized.

Response distributions. 20

In the TFL, a total of 15 correct answers were obtained in everyday money transactions (EDM), 13 correct answers in banking and 12 correct answers in insurance out of a possible 24 correct answers (see Table 3). Five out of eight respondents stated that the most difficult question belonged to insurance. Of these five respondents, three stated that the question on insurance measures that lead to risk reduction for insured persons (item A45) was subjectively the most difficult. In the retrospective section, three respondents named items of the TFL in banking as subjectively the most difficult. The response frequencies to two items are particularly noteworthy. Item A7 from the EDM section on income deduction options to reduce income tax (item A7) received only one correct answer, making it the item with the fewest correct answers. Only two correct answers were given to the question from insurance, which asks about the type of insurance that settles a self-inflicted damage to one's own car (item A48). Although the results of the descriptive analysis indicate that the respondents have problems with the items on the function of money and insurance, no conclusion or justification can be drawn at this point that is based on the deviating religious concepts of Islamic finance with the sole function of money as a means of exchange and the prohibition of Gharar.

Qualitative results

Four central challenges (RQ 1) have been identified:

In economic knowledge, determining the function of money when buying a movie ticket is challenging (1). For this transaction, the respondents stated that it was a flow of capital or a store of value. Only three of the eight respondents answered the question correctly. Four of the eight respondents opted for the answer option capital flow and also justified their decision with the literal semantics of the word that money flows to the cinema operator as capital.

Challenges are identified in all three areas of financial knowledge.

In insurance (TFL-I), the types of insurance and their instruments are challenging (2). Only two respondents correctly answered the question about the insurance that covers damage to their own car in the event of a self-inflicted accident. Only two respondents were able to make an appropriate distinction between fully and partially comprehensive insurance in this question. All other respondents were unfamiliar with the terms. In addition, the non-native German-speaking respondents explained that they had problems understanding the word components “Teilkasko” and “Vollkasko”. 17

In everyday money management, there is a widespread lack of understanding of the concept of income tax (3). Here, only one respondent gave the correct answer to the question which of the specified items were deductible from income tax. When answering the questions, the other respondents stated that they did not know what could be added to or deducted from income tax or how the deduction procedure works. Two people answered speculative gains from the sale of shares and three said interest income from savings. It became clear that the majority of respondents were unclear about the procedure for deducting income tax.

In banking, the respondents experienced challenges with the concepts of retirement provision and in connection with the stock market (4). With regard to the correct answers to the question on the main task of stock market supervision, there is a difference in terms of the respondents’ degree of faith. The respondents who describe themselves as believers (see Table 2 in the column RA) only gave one correct answer here. It was clear from the individual answers of these respondents that the term “stock exchange” was implied in the tasks of banking supervision. The constructs of bank and stock exchange were blurred in the statements of this group. “That I simply um don't know what the task of a stock exchange really is” (P4, TAI, par. 98).

The subcategories of the second category are intended to summarize the identified reasons for the challenges faced by the respondents.

The language barriers are cited by respondents (P5, P6) when it comes to understanding terms such as cash flow or overdraft interest. In line with the findings of Happ and Förster (2019), one explanation for the poorer performance of young adults with MB with a family language other than German may be that terms cannot be adequately understood. Another challenge mentioned by P6 is that there is no known equivalent translation due to a lack of comparable concepts in the native language and in the home country, which means that no understanding of certain terms such as liability or partial coverage insurance can be generated. These differences between the country of origin and the country of arrival are seen by various authors as possible obstacles to understanding economic and financial terms and concepts (Cwynar, 2022; Worthington and Marzuki, 2022; Zuhair et al., 2015) and are particularly relevant in this sampling for respondents with their own ME. “Overdraft interest? Phew. I always have to translate some words into my language, so that I can understand them. […] Because I really can't really understand or comprehend the answers, the rest of the answers.” (P6, TAI, par. 135)

Six respondents stated that they had little to no interest in economic and financial topics in general. Only two respondents stated that they were interested in topics relating to their personal finances. Even if the respondents are personally affected by economic and financial matters, they show little interest in economic and financial topics. Specifically, the respondents mentioned inflation, which was rising comparatively sharply at the time of the interviews. In addition, the respondents stated that other topics such as politics or justice are discussed within the family and that financial and economic issues only play a subordinate role. P4 also cites religious reasons for the lack of interest: “The answer may sound a bit strange, but money is not and never has been important to me. Maybe it's not that smart, but I live every day knowing that I'll be fine tomorrow, no matter how much money I have in my pocket. That's also very much connected to my religion, that God takes care of me, so to speak. No matter how bad I am and that's why money is not so important to me.” (P4, PCI, para. 515–519)

Furthermore, respondents stated that in their current life situation, they are primarily concerned with ensuring that their usual expenses are covered. For this reason, they do not yet consider a long-term and more in-depth examination of economic and financial issues to be significant. The reasons given here can be seen as a supplement and explanation to previous findings on the significance of interest in economic and financial topics for economic and financial knowledge (Förster et al., 2018).

One respondent explained her lack of knowledge by saying that her mother is the expert in her own household on such issues and therefore she does not deal with the topic herself: “So that I'm immediately like “Mom what is this? Can you explain that to me?” Um, yes, but I just think that the more I have to deal with everyday economic problems etc. and then get my mother's advice for help […] But I think I'd be pretty lost on my own […] For example, partial coverage insurance, comprehensive insurance, I don't know what that is.” (P8, TAI, para. 60–86)

Another respondent commented as follows: “Well, that's very difficult for me to answer in detail because I don't know much about finances, and I don't actually earn my own money and don't have to manage it myself. So, I haven't got to that point yet, so I can't talk much about it now, but I think it's very noticeable.” (P5, PCI, par. 125)

Further statements from this interviewee make it clear that the family's good socio-economic background makes it unnecessary to deal with financial and economic terms and concepts. At first glance, the parents did not want their children to deal with these topics and possibly worry about them. In retrospect, however, the parents realized that dealing with economic and financial matters at an earlier age helps to deal with these issues in a sensible way. Consequently, in the case of respondents’ younger siblings, parents have adjusted their attitudes and realized that giving their children a safe framework in which they can gain their own economic and financial experience and guide them through economic and financial issues together creates more benefits than problems (P5).

In the interviews, the respondents did not directly state a challenge in understanding economic and financial terms and concepts due to the Muslim faith. Muslim respondents can, for example, explain the function of interest (P5, P8). In addition, however, the Muslim respondents state that they avoid all transactions involving interest and do not deal with related products or transactions (e.g., P5, TAI, par. 137; 139). This means that products such as loans, bonds, certificates or hedging and provision are out of the question. The requirements of religion are the guiding principle here. Furthermore, the non-Muslim respondents largely do not engage with the Islamic laws of Riba and Gharar. This is consistent with the findings of Ilfita and Canggih (2021) that one's own degree of faith and the application of Islamic law are important, and that faith is also reflected by parental influence on the financial socialization of children (Gudmunson and Danes, 2011). Additionally, it has to be noted that this information was elicit in the retrospective part of the interview. This assumption that religious precepts are not directly affecting challenges in understand western influenced economic and financial terms and concepts can be strengthened by a more detailed consideration of the identified challenge in the function of money. It is noteworthy that none of the interviewees referenced the religious restriction in Islamic finance that considers money as a medium of exchange. Given that the interview method only elicits conscious thoughts during the response (Leighton, 2017), it is not possible to determine whether interviewees are influenced by this religious restriction. However, this unconscious belief is not significant enough to be included in the task solution. A statement by P5 can be regarded as an articulation of this assumption: “Money is only a medium of exchange, a means of buying and selling goods and services” (P5, TAI, para. 45). This statement can thus be understood as an initial reference to the religious restriction of money as the sole medium of exchange. However, to be fully substantiated by religious precepts, a subsequent reference to Islamic finance is necessary.

Conclusion, limitations and implications for economic education

Conclusion

The study explores challenges and their reasons in understanding Western-shaped economic and financial concepts from the perspective of young adults with a Muslim background. Thus it provides an important basis for target group-oriented economic and social education. With regard to RQ 1, it can be stated from the initial findings that the difficulties in understanding economic terms and concepts primarily relate to the function of money. With regard to challenges in understanding financial terms and concepts, difficulties arise when solving questions about insurance, pensions, the concept of income tax and the concept of the stock market. With reference to RQ 2, it is clear that the reasons for these challenges are manifold. The findings of this study show that language deficits which are coming with missing similar or comparable economic and financial terms in the country of origin and the native language, lack of interest and the lack of necessity to deal with economic and financial terms and concepts were identified as reasons for challenges. Although we theoretically assumed – based on the literature (e.g., Oberauer, 2017; Pohlhausen and Beck, 2010; Worthington and Marzuki, 2022) – that Islamic concepts like Riba and Gharar could causes challenges, we were not able to identify reasons for challenges that could be explicitly attributed to the Islamic religion. The principles of the religion were cited to the effect that transactions that are forbidden as Riba and Gharar should be avoided. The further findings obtained go hand in hand with many previous research findings and complement them by providing a deeper understanding of the reasons for identified hindering factors on economic and financial knowledge - for example, language deficits (Happ and Förster, 2019), cultural and religious differences, MB (Cwynar, 2022; Happ and Förster, 2019; Worthington and Marzuki, 2022) or a lack of interest in economic and financial terms and concepts (Förster and Happ, 2019).

Limitations

The study is designed to discover in an explorative manner challenges in understanding economic and financial terms and concepts by young adults with a Muslim background. Here the critical view from Nowicka (2010) and El-Mafaalani (2017) on subsumption of persons in a statistical category become obvious. The selection of the sample under the criterium of Muslim background is very heterogeneous in questions like religious affiliation and strength of faith, countries of origin, their legal specifications, migration experience, family socialization, and family language spoken. Among other things, this has the advantage of revealing many different facets of barriers to understanding. However, this prevents a stronger focus on certain subgroups. With regard to the further differentiation beyond the MB category, it can be seen that deeper insights can be gained. A more differentiated view according to other characteristics, such as one's own ME and thus other economic and financial socialization experiences (Gudmunson and Danes, 2011), as well as the predominant language in the family and the educational background of the parents (Happ and Förster, 2019), offer further explanatory approaches. The extent to which the findings of the group studied differ from others can only be determined through analyses (e.g., see Heidel and Happ, 2023, 2024) with comparison groups. The limited sample size is primarily due to the regional distribution of potential participants and the exploratory nature of the study. To address the finding that the group itself is highly heterogeneous, it is mandatory to examine several groups within the population of people with a Muslim background in greater detail. To identify additional specific challenges and their reasons, a qualitative design is promising. Any challenges discovered and their reasons should then be examined with the help of a quantitative design.

Implications for economic and social education

The identified subject and country specific challenges in understanding economic and financial terms and concepts in this study were caused by different reasons such as lack of interest, lack of necessity as well as lack of language skills. We were not able to identify any reasons that the religious prohibitions of Riba and Gharar cause any direct problems of understanding. However, we found that the prohibitions lead Muslims to avoid prohibited economic and financial products. According to Frjins et al. (2013), exposure to specific economic and financial aspects is an important factor in the acquisition of economic and financial knowledge. If people with Muslim MB aren't exposed to these concepts in their everyday life, it is beneficial for them to learn about economic and financial terms and concepts in school to understand western-influenced economic and financial processes. The specifics of the German economic and financial system can be understood more comprehensibly, above all, through a concrete approach in the classroom with the associated content, personal experience with financial products and services and an examination of terms in the German language. However, to address the reasons for challenges and the topics of economic and financial knowledge in a heterogeneous classroom in a proper educational manner requires certain considerations. We are presenting three approaches, which should be taken into account.

Teachers (in Germany and internationally) do not feel and are not adequately prepared for teaching cultural diversity (European Commission, 2017: 23) but it is one of the key factors for successfully teaching and promoting integration (Barrett, 2018). Heterogeneity, as a theoretical construct, is frequently addressed in teacher training programs. However, the actual inclusion and handling of different facets of heterogeneity, and their operationalization in didactic and methodological action in the classroom, is rarely dealt with in such programs (Karakaşoğlu et al., 2017). Teachers should act as cultural mediators. Subsequently they need knowledge and understanding of the culture of their students with migrant background and how to integrate those aspects interactively in the classroom in the country of arrival (Eliyahu-Levi and Meishar, 2021; Hanna, 2023). Connected to the findings of this study it means that teachers should be confronted in their subject specific education with deviating economic and financial terms and concepts like Riba and Gharar. In addition, teachers need to be aware of their own beliefs, privileges and attitudes to reflect on them and be open to differences (Juang and Schachner, 2020; Hanna, 2023). The forementioned is also supportive to raise teachers’ awareness of migration-specific characteristics. This includes a consideration of different needs, backgrounds and previous knowledge and specific cultural learning setting of students with MB (Eliyahu-Levi and Meishar, 2021). This can include the following facets:

- migration-sensitive analysis of previous knowledge

19

, e.g., with AVIVA-Model (Städeli, 2024) and MB (cultural, religious and national specifications), or - migration-sensitive didactical-methodological preparation of lessons, e.g., addressing different economic and financial systems with interactive methods and social forms which facilitates intercultural exchange (e.g., through consideration and realization of heterogeneity, advantageous inclusion of varying living worlds of students) and - diverse teaching and learning materials regarding the migration specific aspects (e.g., including deviating economic and financial terms and concepts, and addressing the heterogeneity of the society)

To create an inclusive and supportive atmosphere that enhances knowledge acquisition, all of these specific measures must be accompanied (1) by school policies that value cultural diversity (Celeste et al., 2019), and (2) by teachers as role models who are representatives of an open-minded and welcoming society without prejudice and create a classroom climate in which all students feel like they belong (Heikamp et al. 2020).

Following on from the results of this study, formal education programs should be created that address these conditions and offer young adults a basis for competent economic and financial action, particularly in the case of divergent prior knowledge due to heterogeneous religious, cultural and socio-economic conditions.

Footnotes

Data availability

For data protection reasons, the data collected cannot be passed on.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We thank the Joachim Herz Foundation for funding the research for this publication.

Ethical considerations and informed consent statements

There were no ethical considerations given by the Ethical Board of Leipzig University.

The respondents received an informed statements of consent before the data was collected and agreed to this.