Abstract

Financial literacy is crucial for making sound financial decisions and living a better life. However, the field of finance is full of abstract concepts, such as inflation, liquidity, asset allocation and credit. Abstract concepts may be harder to comprehend than concrete concepts due to their lack of tangible referents in the physical world. In contrast, concrete concepts (e.g., car or house) have a palpable form and can be directly experienced through the senses. Against this background, the question arises of how instructional material can be designed in a way that helps people acquire knowledge about abstract financial concepts. Multimedia learning theories suggest complementing verbal information with visuals that represent the respective topic or concept. Since abstract financial concepts lack palpable, concrete forms, these representational visuals are not simply available but have to be developed. Based on grounded cognition theory, this article discusses three approaches, ‘situations’, ‘emotions’ and ‘metaphors’, which might be used to generate representational visuals of abstract financial concepts. This study aims to provide ideas and enhance our understanding of how grounded cognition theory can be utilized as a guideline to create representational visuals of abstract financial concepts and thus multimedia learning material, which in turn may support increasing people's financial literacy.

Introduction

Financial literacy is crucial for making sound financial decisions and living a better life. The benefits of financial literacy are assumed to be manifold, among them higher financial inclusion, which in turn directly supports the overall economy (Ahmad et al., 2021). Financial illiteracy, in contrast, may lead to poor retirement planning, mismanagement of financial assets, or taking on high-interest debts (Lusardi and Mitchell, 2014). The need for a financially literate society is even more evident since today's social and financial systems pressure people to personally take responsibility for important financial decisions related to savings and investments, post-retirement financial security, health care, or home buying (Alqahtani, 2018). More challenges are the increasing complexities of financial systems and the digitization of financial services, which, despite offering a huge number of benefits, still put a twofold burden on learners, especially those who have low prior financial knowledge: one, to learn about finance, and two, to learn about financial technologies.

Although the importance of financial literacy is evident, many people find it a difficult subject to learn and fail to even have rudimentary knowledge of finance (Goyal and Kumar, 2021). Studies show that about 3.5 billion people around the globe are financially illiterate (Klapper et al., 2015). Less than half of young adults (aged 23–27) understand concepts such as compound interest, inflation, risk diversification (Lusardi et al., 2010; OECD, 2023). Also, the pension system seems to be hard to understand: As seen in Sweden, it took more than a decade of governmental campaigns about the pension system, after which only 40% of the contributors recognized that, in the new system invented in the 1990s, the pension fund would be based on lifetime earnings (Larsson et al., 2009). In the Netherlands, 79% of citizens believe that those who are currently employed pay the pension of those who are already retired (Pensioenfederatie, 2016). However, the correct mental model would be that Dutch employees gradually accrue their own retirement income. Such misunderstandings can lead to precarious financial decisions that may result in substantial financial losses, and thus financial ill-being. One reason for misconceptions and financial illiteracy might be that many concepts in finance are highly convoluted and abstract.

Abstract concepts in general and thus also abstract financial concepts (AFCs) lack palpable, concrete forms that can be directly experienced through the senses. Other than concrete financial concepts such as a gold bar or a check, which can be seen or touched, concepts such as compound interest, risk diversification, or asset valuation, are often abstract constructs that describe complex relationships and principles within the financial system. For example, compound interest refers to the process of earning interest on both the initial principal and the accumulated interest from previous periods. This concept is not immediately visible or tangible in everyday life. Similarly, risk diversification involves spreading investments across various assets to reduce exposure to any single risk, an idea that requires understanding abstract notions of probability and correlation. Asset valuation, the process of determining the worth of an asset, involves complex calculations and projections that are not inherently visible. These abstract concepts are fundamental to financial literacy but are challenging to grasp without concrete representations.

To improve financial literacy, the meaningful learning of AFCs should be fostered. Multimedia learning theories such as the cognitive theory of multimedia learning (CTML) (Mayer, 2005), which is an influential theory in its field, suggest including representational pictures along with words in instructional materials. Usually, financial information is presented in the form of text and numbers only (Schroeder et al., 2020). Graphs are also extensively used, but to understand graphs, prior knowledge of financial constructs and imaginative capacity is essential in most cases. According to the CTML, the rationale for adding pictures is that they open up the visual resources of the mind that aid in better understanding the concepts. However, the question arises of how to generate representational visuals of AFCs, such as pensions. Whereas it is comparatively easy to make visuals of concrete financial concepts, such as a dollar-note, it is more challenging to create those of AFCs such as risk diversification, market value, compound interest, and asset valuation since they do not have a defined physical shape. Prior scientific contributions have rarely focused on visualizing such AFCs to improve learning.

This study describes three approaches, namely situations, emotions, and metaphors, which could assist in making representational visuals of AFCs for enhancing meaningful financial learning, especially for those who have low prior knowledge. These approaches match the ideas of grounded cognition theory, and although they may not be exhaustive, they are based on studies from other domains where they have been used relatively extensively. In addition, these approaches are likely to support making visuals of AFCs because they are close to visual sensory experiences. This study may support researchers and educationalists whose focus is on making financial education more effective. In particular, it may provide ideas for making visuals of AFCs for learning purposes, to further test and possibly develop them. It is important to note here that this stream of research in finance is very new, and so it may appear as equivocal. However, the need to make representational visuals in finance is so important that we dare introduce our ideas.

Financial literacy

Noctor et al. (1992) are among the early scholars who defined financial literacy. They described it as financial knowledge that leads to informed financial decisions. This definition encompasses two main components: financial knowledge acquired through education and the ability to apply that knowledge to make informed decisions. These elements are distinct but interconnected. Huston (2010) concurs, emphasizing the separation of financial knowledge from the ability to make informed decisions. She notes that financial decisions can be influenced by factors beyond knowledge, such as economic conditions, time preferences, and culture. Additionally, a solid mathematical ability is also crucial as it supports the comprehension and analysis of financial data, enabling individuals to make precise calculations and informed decisions (Lusardi and Mitchell, 2007). However, Hilgert et al. (2003) argue that some studies favour a more direct relationship, suggesting that increased financial knowledge will inherently result in better financial management practices.

The US President's Advisory Council on Financial Literacy (PACFL) expanded the definition by including skills and emphasizing financial decision-making. According to PACFL (2008), financial literacy is “the ability to use knowledge and skills to manage financial resources effectively for a lifetime of financial well-being” (Hung et al., 2009: 3). Similarly, Lusardi and Mitchell (2014) stress the importance of financial decision-making, extending beyond mere financial knowledge. They define financial literacy as the ability to analyse financial information and use it for informed decision-making. Lusardi and Mitchell argue that individuals with high financial knowledge but lacking the capability to make sound financial decisions are still considered financially illiterate.

The Organisation for Economic Co-operation and Development (OECD) offers a comprehensive definition of financial literacy. In 2005, they described it as the process by which consumers improve their understanding of financial products and concepts through information, instruction, or advice, thereby developing the skills and confidence to recognize financial risks and opportunities and make informed choices. By 2013, the OECD refined the definition to include “a combination of financial awareness, knowledge, skills, attitudes, and behaviours necessary to make sound financial decisions and ultimately achieve individual financial well-being.” This definition incorporates various aspects, such as financial knowledge, analysis, perceived knowledge, and the skill to use acquired knowledge for making sound financial decisions.

Additionally, mathematical skills are crucial for effective financial literacy as they underpin the ability to perform critical financial analyses and calculations. Research demonstrates that mathematical competency correlates strongly with improved financial decision-making and management. For instance, Lusardi and Mitchell (2007) found that individuals with better mathematical skills are more likely to engage in financial planning and to understand complex financial products. Similarly, a study by van Rooij et al. (2011) revealed that numerical ability significantly impacts financial literacy, as individuals with stronger mathematical skills were better equipped to understand interest rates, inflation, and investment concepts. This correlation emphasizes the importance of integrating mathematical training into financial education programs to enhance overall financial literacy and decision-making capabilities (Behrman et al., 2012).

While we embrace the comprehensive definition of financial literacy, which includes knowledge, skills, attitudes, and behaviours, we recognize the value in narrowing the focus of the definition for research purposes. By honing in on specific aspects, researchers can gain deeper insights and provide more detailed analyses, thereby enriching our overall understanding of financial literacy.

Learning abstract financial concepts

Abstract financial concepts

An abstract concept is often described as one that lacks a tangible referent in the physical world (Paivio, 1965). In almost all theories about the meaning of abstract concepts, the lack of physical attributes or physical substance is an important component (De Koning and Tabbers, 2011). Abstract concepts are commonly defined as “entities that are neither purely physical nor spatially constrained” (Barsalou and Wiemer-Hastings, 2005). Concrete concepts, in contrast, can be experienced through our senses of sight, smell, sound, taste, or touch. This means that the connection between concrete concepts and perceptual referents is straightforward, whereas the same does not apply to abstract concepts. Consequently, abstract concepts might be harder to learn compared to concrete concepts (Zuckerman et al., 2005).

As an example of a concrete financial concept, we can think of a banknote. Most people would agree on what a banknote looks like. If people were to describe a banknote, they usually would say that it is made of paper with numbers on it, referring to its amount. There is a photo of an important person or place printed on it, along with different designs. It can be put in a pocket, or it can be kept in a wallet or purse. If a picture of such a thing is shown to someone, the answer would likeliest be that it is a banknote. This is because we recognize and represent banknotes with such properties.

In contrast, one example of an abstract financial concept is the idea of inflation. Inflation refers to the rate at which the general level of prices for goods and services is rising, subsequently eroding purchasing power. Unlike a banknote, inflation cannot be touched, seen, or directly measured with physical senses. It is observed indirectly through the changes in prices over time. The complexity of inflation arises from its numerous influencing factors such as supply and demand dynamics, monetary policies, and global economic conditions. Understanding inflation involves grappling with concepts like the consumer price index (CPI), inflation rates, and economic indicators, making it abstract and challenging to visualize.

Another intricate financial concept is the time value of money (TVM). TVM is the idea that a specific amount of money today has a different value compared to the same amount in the future due to its potential earning capacity. This concept underlies various financial decisions and calculations, such as present value, future value, interest rates, and discounting cash flows. Like inflation, TVM does not have a physical presence; it is conceptual and relies on understanding and applying mathematical formulas and financial principles. This abstraction requires learners to think beyond physical money and grasp how its value changes over time, influenced by interest rates and investment opportunities.

People may frequently struggle to provide clear and consistent explanations of concepts like TVM because such concepts are inherently abstract and intangible. Unlike a banknote, which can be experienced through sight, touch, smell, and taste, inflation and TVM cannot be directly perceived through our senses. This lack of sensory experience leads to diverse and often unclear interpretations, underscoring the difficulty of comprehending abstract financial concepts compared to concrete objects.

Against this background, the question arises of whether and how it is possible to find perceptual referents of abstract financial concepts to help people learn those concepts. According to cognitive science theories, and specifically CTML, we focus on visual representatives (i.e., representational visuals of abstract concepts). The idea of CTML is that meaningful learning is better supported when people learn using material including text and representative visuals than just text (e.g., Boadum, 2020; Çeken and Taşkın, 2022).

CTML and the role of visuals in learning concepts

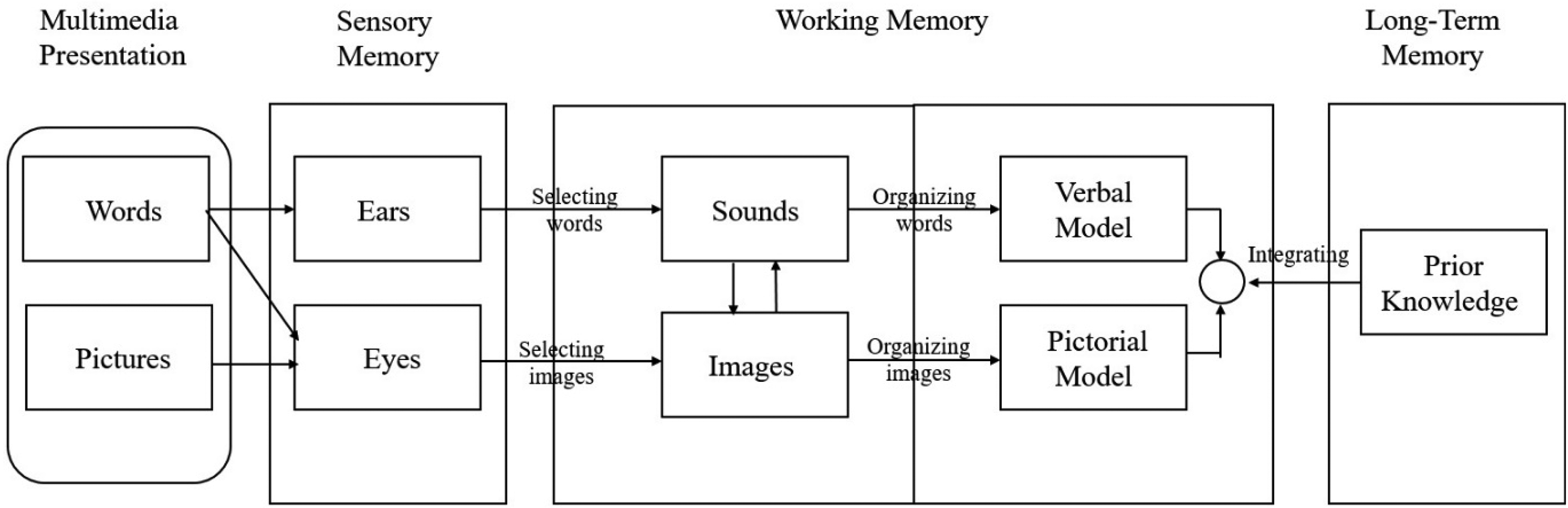

CTML suggests that the human brain consists of three memories, the sensory memory, the working memory and the long-term memory. Information presented in written words and pictures is perceived with the eyes, information presented in spoken words is perceived with the ears. Only selected information is processed further into the working memory either phonetically or pictorially whereby written text or pictures can be translated into sounds and the other way around. In the working memory, information is organised into separate cognitive representations, that is, verbal or pictorial models. Afterwards, these newly developed cognitive models have to be integrated with the relevant prior knowledge from the long-term memory in order to result in meaningful learning (see Figure 1).

The learning process defined by the CTML (Mayer, 2003).

To foster meaningful learning, CTML suggests presenting instructional material with both words and relevant pictures instead of words only (Mayer, 1997). This view asserts that words and pictures are two distinct modes of presenting the same information. The characteristics of both modes are inherently different from each other (Fein, 2017). Pictures represent information in an original form, that is, an as-it-is form, which is close to our visual sensory experience. In contrast, words represent information in an interpretive form, that is, language as symbolic form. Both forms of representation can complement but not substitute each other (Mayer, 2002). In addition, utilizing both forms of representation, that is to say dual coding of information, facilitates retention of information (Paivio, 2014).

Based on the CTML, various principles for the design of instructional materials have been developed and tested (for an overview, see Mayer et al., 2018; Mayer and Fiorella, 2014). The basic, and at the same time, the principle of utmost importance, is the so-called multimedia principle, which advises the presentation of instructional material in multimodal form using words and pictures instead of words alone. If the multimedia principle is applied to learning material, and using this material does not result in better learning compared to just-word materials, then most of the other principles of CTML would not work as well (Fletcher and Tobias, 2005). The importance of this principle results from the fact that it directly regards dual coding processes in the human brain. However, an important prerequisite of the multimedia principle is that the pictures should be relevant and represent the learning content (Mayer, 2005). If pictures are not representational, they would be categorised as irrelevant. Irrelevant pictures are considered extraneous material that competes for limited cognitive resources. It deviates learners’ attention from the essential material and thereby obstructs deep learning (Cavanagh and Kiersch, 2022). In particular, this may hinder the process of organising learning materials in working memory and may result in connecting or integrating the material with an incongruent theme (Moreno and Mayer, 2000). An incongruent theme here refers to the misalignment or mismatch between the provided instructional content and the unrelated concepts introduced by irrelevant images, leading to confusion and ineffective learning.

Although the multimedia principle suggests adding representational visuals to verbal material, it does not explain which visuals are categorised as representational to learning materials. Furthermore, in the case of abstract concepts, or AFCs, it is challenging to develop representational visuals. This applies, in particular, when people have no, or only limited knowledge about making visuals and guidelines are missing. Given this situation, it is likely that visuals would be based on mere guesswork and could emerge as nonrepresentational. In other words, it is difficult for designers and educators to create visuals of AFCs that are relevant and represent financial content in learning material. To contribute to solving this problem, we present a theory that aims to explain how abstract concepts can be learned, and in line with this theory we present three approaches providing some hints with regard to generating representational visuals of AFCs. This will also improve the application of CTML principles in the financial learning context.

Visualising abstract financial concepts

Grounded cognition theory

Traditional theories of cognition propose that the brain's modal systems convert representations of concepts—whether concrete, like a chair, or abstract, like justice—into amodal symbols, which are then stored in semantic memory (Anderson, 1983; Mahon and Caramazza, 2009; Tulving, 1983; Tyler et al., 2001). This semantic memory holds knowledge that is distinct and separate from the brain's systems responsible for perception, action, and introspection. In other words, the information in the semantic memory is not directly tied to our sensory experiences or motor actions. Examples of such traditional theories include semantic network models, which map out how concepts are connected to one another in a network-like structure (Collins and Loftus, 1975; Quillian, 1969). Other examples are various forms of connectionist network models that describe how information might be processed and stored through networks of interconnected nodes (Caramazza et al., 1990; Devlin et al., 1998; McClelland and Rogers, 2003). Despite the insights provided by these amodal theories, they still provide limited understanding about which specific brain systems are responsible for storing these amodal symbols, and how the brain's neural computation processes align with and support these amodal symbols (Barsalou, 2008).

In contrast, grounded cognition theory rejects this classical view and suggests that, instead, all concepts are rooted in perception and action (Barsalou and Wiemer-Hastings, 2005; Gallese and Lakoff, 2005; Kiefer and Pulvermüller, 2012; Martin and Chao, 2001). Grounded cognition theory encompasses theories that highlight the importance of sensory-motor systems, introspection, and emotional states in processing experiential information (Barsalou, 2008). These theories emphasize that our bodily states significantly influence our cognitive states. For instance, various perspectives within grounded cognition illustrate the critical roles of the body in shaping cognition, underscoring the idea that physical states can affect how we think and process information (e.g., Barsalou et al., 2003; Lakoff and Johnson, 1980b).

According to grounded cognition theory, conceptual characteristics are thoroughly rooted in our perceptions of actions in the physical environment and in our bodies. It explains that people make images of concepts (both concrete and abstract) in their minds, whereby the sensory-motor region is activated in the brain when people think. The thoughts could be ‘mental images’, ‘imagined movements through space’ or imagined ‘simulated sequences of actions’. For instance, the verb “kick” is understood through the motor regions of the brain, which is activated when a “kick” is physically performed (Hauk et al., 2004). This highlights that a greater number of factors play a role in the comprehension of all types of concepts. Barsalou (2008) explained it as an interaction between perception, action, body and environment.

Grounded cognition theory explains how we understand abstract ideas through various methods, notably including situations, emotions, and metaphors. This theory links these methods directly to our physical actions and feelings. Situations provide a framework for understanding by interacting with our environment (Barsalou, 2003). Emotions illustrate how our feelings are intertwined with our physical actions (Niedenthal, 2007). Metaphors, as discussed by Lakoff and Johnson (1980a), help us grasp abstract ideas by connecting them to concrete experiences. This theory highlights how our senses, movements, and emotions help us to understand concepts, making these approaches particularly effective for educational purposes.

Since the idea is gaining traction in contemporary theories of cognition that thoughts are not comprised merely of words or symbols but also of visual and motor images (Glenberg, 2015), it becomes plausible to represent abstract financial concepts (AFCs) through visuals that people can easily relate to. The rationale behind this is that if we incorporate the perceptual referents of the body and environment into the development of visuals for AFCs, we could create representational images that may enhance financial learning. For developing these visuals, three key approaches—situations, emotions, and metaphors—are relevant from the perspective of grounded cognition theory. Because these approaches are particularly tied to perceptual experiences, making them more suitable for translating abstract concepts into understandable visuals compared to more introspective methods, such as self-reflection (Borghi et al., 2017).

Three approaches to visualise abstract financial concepts

Situations

The situation-specific view emphasises that the situation is part of learning abstract concepts (Schwanenflugel et al., 1992). Whereas concrete concepts are relatively clearly entrenched in time and space, abstract concepts lack situational referents. Nevertheless, this does not mean that learning abstract concepts cannot be related to real-world situations. In fact, the cognitive representation of abstract concepts depends on complex interactions occurring in space and time (Zwaan, 2016). For example, grasping the idea of “justice” involves recognizing how it plays out in different legal systems, historical contexts, and cultural practices. Thus, knowledge of situations is an essential component of learning and using abstract concepts. Although the link between tangible perceptual referents and abstract concepts is not as direct and clear as for concrete concepts, situation-based perceptual information is part of many abstract concepts (Davis et al., 2020; Pecher and Boot, 2011). The situation-based view of abstract concepts argues that concepts are not present in a vacuum (Schwanenflugel, 2013); they exist in a situation, and it is difficult to understand them apart from individual's situated experience.

The concept of “risk” can be better understood, for instance, in a situation when a person evaluates the potential losses and gains of a particular investment opportunity. Abstract concepts can be regarded as facets of situations (Van Oers, 2001). Therefore, the meaning of an abstract concept remains relatively unclear when it is presented out of context, as its meaning relies on objects, actions, people and settings that are together considered as situation (Wilson-Mendenhall et al., 2011). In contrast, for the comprehension of concrete concepts, due to their tangibility, a specific situation is not required. A concept of a banknote, for example, can be understood independent of whether it is used in a supermarket or in a restaurant. In essence, while both abstract and concrete concepts help us make sense of the world by highlighting different aspects of a situation, abstract concepts need context to be fully understood. Concrete concepts, however, are inherently more straightforward and can often be grasped without needing a specific situational backdrop (Barsalou, 1999). Beyond the importance of situations, research by Zwaan (2016) underscores the significance of mental simulations of situations in comprehending abstract concepts. Mental simulations are dynamic processes in which individuals reconstruct experiences in their minds, integrating situational elements to form a coherent understanding of abstract concepts. This approach aligns with the situation-specific view by highlighting that abstract concepts are not only tied to situations but that these situations are actively reconstructed through cognitive simulations. When individuals encounter abstract concepts, they often engage in such mental simulations that draw upon previous situational experiences, enabling a richer and more nuanced conceptual understanding. This process is particularly crucial in educational settings, where linking abstract concepts to situations can enhance learning.

McRae et al. (2018) tested whether visuals of situations facilitate the learning or processing of abstract concepts. They conducted two experiments and applied a lexical decision task. In the first experiment, relevant and irrelevant visuals of situations were presented, followed by abstract words for which the participants had to decide whether they match the preceding visuals. For instance, a picture of two kids sharing food illustrated the abstract word ‘share’ (see Figure 2(a)). In the second experiment, abstract words were presented first, followed by visuals, whether relevant or irrelevant. Participants were asked to decide whether the picture depicts a situation that matches the preceding abstract word. For instance, an irrelevant picture in Figure 2(b) is paired with the abstract word ‘convocation’. This picture shows a woman buying groceries and a musical instrument that is bizarrely placed against the shelf, so clearly, this picture does not represent a situation of ‘convocation’. The results of both experiments show that decision latencies were significantly shorter for visuals and abstract words that were relevant to each other, meaning that the picture represented the word. This study provides evidence that relevant visuals of abstract concepts based on situations are favourable for comprehending these concepts.

Visuals showing relevant (a), or irrelevant (b) situations related to abstract concepts (McRae et al., 2018).

Wiemer-Hastings and Xu (2005) analysed the role of situations in understanding abstract and concrete concepts in a different manner. In an experimental study, they conducted a feature listing task using several abstract and concrete concepts. Participants had a choice to list for each abstract and concrete concept either the item's own properties or relevant situational properties. The participants listed a huge amount of situational properties for abstract concepts. This means that abstract concepts were related to experiences, specifically social contexts, which underlines the situation-based view of processing abstract concepts (Roversi et al., 2013).

Emotions

The use of emotions is another possible approach for making visuals of AFCs. Although no study has directly examined the role of the emotional content of abstract concepts in the form of visuals in fostering learning, other relevant investigations may provide prospects for the idea. The study by Ponari et al. (2020) suggested that emotional valence (either positive or negative) provides a ‘bootstrapping mechanism’ in learning abstract concepts. In this study, one group of participants received information related to abstract concepts in an emotional state, whereas the other group received this information in a neutral state, providing more ‘encyclopaedic, non-emotional’ information. For example, ‘reform’ was used as one of the abstract concepts. The emotional version was, “I am extremely cross about the government's planned ‘reform’ of the health service, which is hugely unpopular. The change will make health care worse, and many people will suffer” (Ponari et al., 2020: 12). The neutral version of this concept was, “I read an article about the government's planned reform of the health service, which will take place next year. They are often changing things, and many people will change jobs” (Ponari et al., 2020: 12). The results show that emotional valence better supports the acquisition of abstract concepts compared to non-emotional information.

Park et al.'s (2015) eye-tracking study examined the influence of emotional design on learning achievement. Participants received learning material with and without anthropomorphism (see Figure 3), which included emotional facial expressions of lifeless objects. Anthropomorphism was used to induce positive emotions in the learning material. The eye-tracking data show that the learners’ attention was stimulated by learning materials with anthropomorphism, which resulted in the highest learning outcomes. In a similar study, Uzun and Yıldırım (2018) applied emotional design to instructional material and assessed it on various factors crucial for better learning. The learning material comprised science topics, including work, energy and energy conservation. They used an experimental method in which four different treatments were applied. The findings indicated that emotional design features lead to less mental effort, more positive emotions and better recall.

Instructional material with and without the use of anthropomorphism (Park et al., 2015). The English translation of “Wie Immunisierung funktioniert” is “How immunisation works”.

Metaphors

Metaphors are known to be a potent technique for the effective learning of abstract concepts. The comprehension of abstract concepts is supported through metaphors driven from concrete domains; thus, metaphors aid in gaining a better and in-depth comprehension of abstract concepts by connecting them to concrete, physical experiences (Lakoff and Johnson, 1980a). They are used in a way that lets people apply their knowledge of the base that is more concrete to the target that is more abstract to enhance their understanding of the target (e.g., Holyoak and Stamenković, 2018; Veale et al., 2016). For example, financial markets are often described metaphorically as ‘a bull market’ and ‘a bear market’. The bull shoves its horns upwards, whereas a bear swipes its paws down towards the ground. These actions are used as metaphors for describing the movement in financial markets. If the prices are going up, then it is a bull market; if they are going down, then it is a bear market.

Language plays an important role in generating and understanding metaphors, wherein both target and source domains are verbal (Thibodeau et al., 2019). Yet, metaphors are not limited or exclusive to verbal boundaries for understanding abstract concepts (Refaie, 2003: 76). Lakoff and Johnson stated that “the essence of metaphor is understanding and experiencing one kind of thing in terms of another” (Lakoff and Johnson, 1980a: 5). This denotes that abstract concepts can be represented in non-verbal ways too, because, as discussed, people understand abstract concepts in terms of more concrete phenomena (Ge et al., 2022). The description of ‘concrete’ here refers to objects that can be perceived through senses or experienced through bodily interactions. Thus, the abstract concept (the target) that needs to be comprehended is compared to an object (the base) that can be touched, seen, heard, smelt, tasted or experienced through physical actions. Taking this further, metaphors of abstract concepts can be depicted in visuals that may represent those concepts (e.g., Forceville, 2017; Forceville and Renckens, 2013) and considered relevant visuals because of their representativeness.

Forceville and Paling (2021) provide evidence that visual metaphors can be used to explain abstract concepts. Their study included an abstract concept of ‘depression’. The authors analysed nine short, animated films on depression. These films did not use any words but only used visual metaphors to describe the abstract concept of ‘depression’. The authors used Lakoff's (1993) theory of object–location duality to analyse the films. This theory suggests two ways, object and location, through which people conceptualize abstract ideas in metaphorical form. The ‘object’ here shows what one can possess, in this context the authors used the example, “I have finally found love”. The ‘location’ refers to a place one can be in for such types of concepts, another example, “I am in love”. By analysing the films, the authors concluded that they feature two dominant metaphors: (1) “depression is a dark monster” (object) and (2) “depression is a dark confining space” (location). In one of these films on depression (see Figure 4), a cloud first appeared on a young man and then began to rain. Later, the man takes action to solve this problem by going to a psychiatrist who, in vain, tries to destroy the clouds. Then, the raining clouds merge with the raining clouds of the other person. Finally, as they continue their journey toward healing, the clouds gradually start to fade away, representing the slow but eventual easing of their depressive symptoms.. In this film, it is cued that the cloud is depression, the rain is (alcohol) drinking, and merging of raining clouds with the other person is the collective problem of depression and drinking. The authors concluded that animations or visuals provide affordances for presenting metaphors of abstract concepts in a multimodal form.

Animation of an abstract concept of ‘depression’ (Forceville and Paling, 2021).

Illustrating the use of the three approaches for visualising abstract financial concepts

To provide guidance on generating visuals of AFCs using situations, emotions, and metaphors, this section presents some ideas and directions based on theories discussed earlier. These suggestions, from the authors’ perspective, aim to assist in structuring future empirical studies.

Situations

Starting with situations, the concept of ‘credit’, for instance, is broadly defined as money borrowed from a lender by a borrower. There are various sub-categories of credit, including ‘revolving credit’ and ‘instalment credit’. Imagine walking into a bustling marketplace in your city. Here, the concept of credit comes to life through the daily interactions of its residents. In one corner, you see a shopper holding a credit card – this represents revolving credit. With this card, the shopper can buy goods up to a certain limit, for example, 500 dollars. Each time he or she uses the card, it deducts from the available credit. But once he or she repays what he or she borrowed, the limit resets, allowing the shopper to spend up to 500 dollars again. It's a continuous cycle of borrowing and repaying, providing flexibility for everyday purchases. The shopper swipes his or her card at various stores, enjoying the ease and convenience of this revolving system, which can be recharged through online banking, or an ATM whenever needed.

As another example, one can imagine a nearby bank, where a couple is discussing a significant loan with a banker—this is instalment credit in action. The couple is applying for a large sum to buy a house. The banker carefully reviews the application, checking the couple's financial history and ability to repay. Once approved, they receive the full amount upfront but agree to repay it in fixed monthly payments over a set period, like 20 years. This structured approach is crucial for long-term commitments, ensuring that both parties understand the repayment terms.

These two scenes—the shopper with his or her revolving credit card and the couple securing an instalment loan for their home—illustrate the situational elements of revolving and instalment credit. The ease and flexibility of revolving credit contrasts with the structured, scrutinized process of instalment credit, each serving different financial needs in the vibrant marketplace. Thus, if visuals (e.g., as a sequence of scenes) are generated which support the comprehensibility of these two concepts and follow the relevant situational properties of each concept, then these visuals may be deemed representational or relevant to that particular concept, which may eventually assist in learning these AFCs.

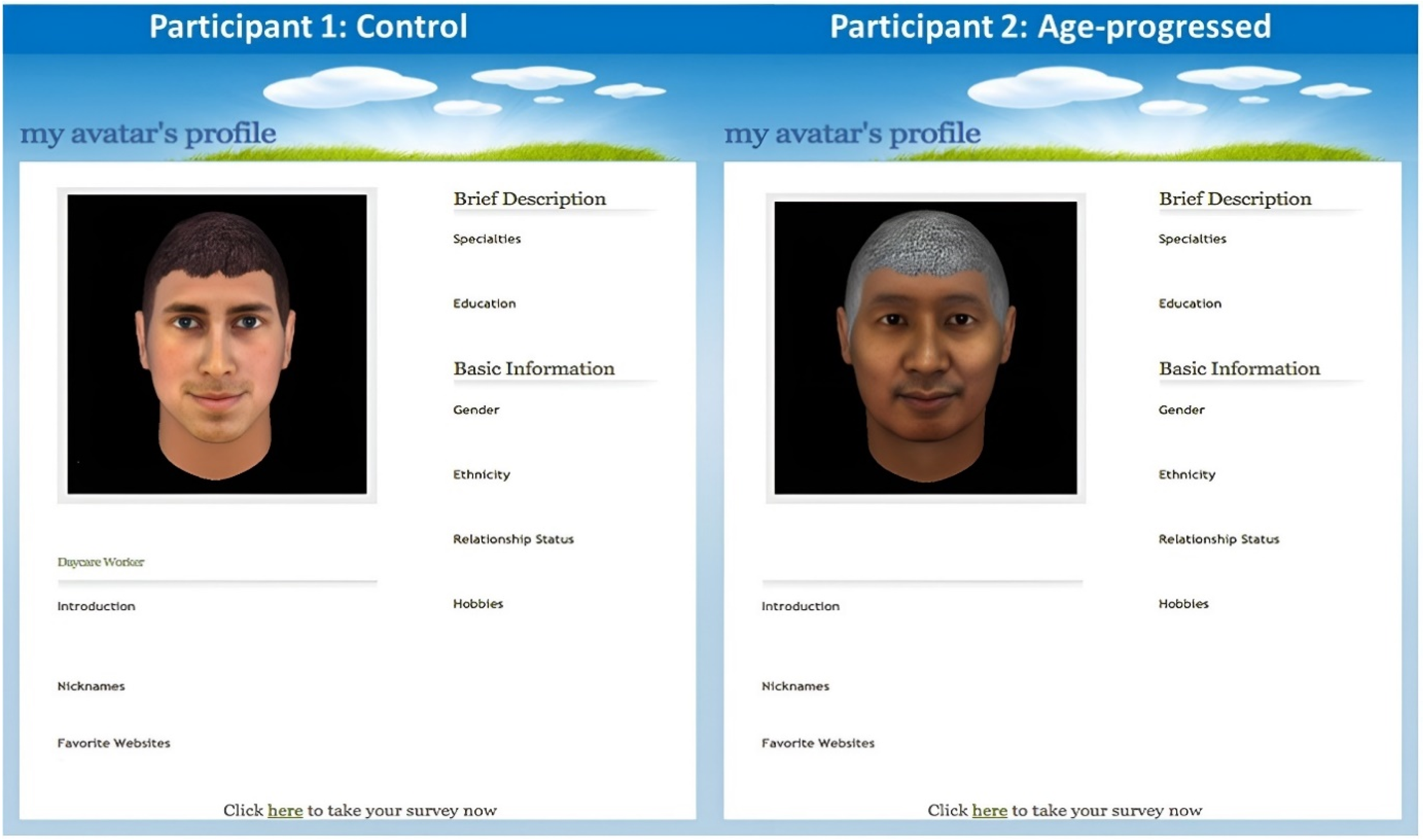

Another idea for generating situation-based visuals can be found in Sims et al.'s (2020) study. The authors examined the challenges of young people regarding their difficulty in visualising their future selves, which hindered their preparation for post-retirement funds. The study applied experimental research, in which participants were shown their age-progressed avatars in the treatment group and their same-aged avatars in the control group (see Figure 5). The visuals were shown while participants took a financial education course. The results of the financial literacy test revealed that participants receiving age-progressed avatars gave more correct answers and showed higher confidence (i.e., fewer “don’t know” responses). Moreover, they reported an interest in attending long-term financial planning programmes. Drawing from this research study, visuals of an elderly person, for instance, can be generated in a comparative manner, which could increase the learners’ engagement in understanding the post-retirement funds planning. Engagement is a crucial part of learning for understanding the concepts. Therefore, creating situation-specific visuals may boost learners’ engagement and improve learning outcomes.

The non-aged (left) and aged-progressed (right) avatar of the same person (Sims et al., 2020).

Emotions

When discussing emotions, it is important to remember that they can be vividly perceived through our senses, and their use is particularly significant in processing abstract concepts. Emotional imagery has the potential to illustrate AFCs and enhance learning. Financial issues are deeply intertwined with people's lives, invoking a wide array of emotions. For instance, the joy and elation one feels upon gaining profits from investments are powerful emotional responses that can be harnessed to teach concepts related to financial gains. Conversely, the despair and frustration that come with financial losses evoke strong negative emotions, such as sadness and anger, which can also be used to elucidate the repercussions of poor financial decisions.

Fear and greed, emotions that frequently overpower rational thought, often result in misguided financial choices. For example, during a stock market crash, fear can lead investors to sell off assets in a panic, while greed during a market boom can cause reckless investments. These emotions are critical in understanding why people make certain financial decisions (Gaies et al., 2023). Furthermore, the discussion of money is often considered taboo in various cultures, impeding financial planning and education. This taboo is linked to feelings of shame or fear (White et al., 2021). For instance, an individual might feel embarrassed to discuss their debt, leading to avoidance of financial planning. Similarly, fear of financial insecurity can prevent open conversations about money, further hindering effective financial management (Sadek, 2020).

To create an emotional picture explaining the concept of risk diversification, it is essential to highlight feelings of security and balance. An effective image might depict an individual calmly managing a portfolio, thoughtfully allocating investments across different asset classes. This scene can evoke a sense of careful planning and control, illustrating the emotional reassurance that comes from knowing one's investments are diversified and protected against potential losses. Additionally, the image could show the individual feeling content and at ease, symbolizing the stability and peace of mind that diversification brings. By focusing on these emotional aspects—calmness, security, and satisfaction—the picture effectively conveys the benefits of risk diversification, making the abstract concept more relatable and easier to understand. This emotional connection helps to enhance engagement and retention of the financial principle.

Metaphors

AFCs can be effectively represented through visual metaphors by translating complex ideas into relatable and understandable visuals. An example for a visual metaphor explaining budgeting and expense management is that of a balanced diet. Imagine a plate divided into different food groups, each representing a category of expenses such as housing, groceries, entertainment, and savings. Just as a balanced diet requires appropriate portions of various nutrients for overall health, a well-planned budget ensures that financial resources are allocated appropriately across different needs. In this metaphor, overspending on non-essential items is akin to consuming too much junk food, which can lead to financial health problems just as poor nutrition can harm physical health. Conversely, maintaining a diverse and balanced “diet” of expenses ensures that all financial needs are met without overindulging in any one area. This metaphor makes the abstract concept of budgeting more tangible by comparing it to everyday choices in nutrition, emphasizing the importance of balance, moderation, and thoughtful planning in maintaining financial well-being.

Recent studies in financial literacy have investigated visual metaphors of financial concepts as a unique method to foster learning through visuals. Van Hekken and Das (2019) used the ‘navigation metaphor’ as a visual for communicating about the basics of pension accrual. Schröder et al. (2022) incorporated the visual metaphoric storytelling of pensions using a tree metaphor (see Figure 6). This metaphor shows a set of different stages that starts with watering the ground; then a plant pops out, which eventually becomes a whole tree and starts giving fruit. This represents the early planning of post-retirement funds that accumulate over time, and when the person retires, he/she starts to receive a pension. These studies illustrate how metaphors can visually present complex financial concepts, making them more accessible and easier to understand. By engaging learners visually, these methods can significantly enhance financial literacy and planning.

Visual metaphoric storytelling of the concept of ‘pension’ using a tree metaphor (Schröder et al., 2022).

The visuals of AFCs can be applied in both formal and informal contexts. In a formal learning context, the use of visuals of AFCs can greatly enhance the educational experience by making abstract and potentially complex ideas more accessible and engaging. Formal learning environments, such as schools, universities, and professional training programs, often rely on structured curricula and standardized materials. Integrating visual representations of AFCs into these materials can help bridge the gap between abstract concepts and practical understanding. For example, textbooks can include visuals that depict the flow of money in an economy or the process of investment diversification. During lectures, instructors can use real-world examples and case studies as visuals to illustrate financial principles like risk management and asset allocation. Digital learning platforms can employ interactive visual aids, such as animations, to demonstrate the impact of financial decisions in real-time scenarios. These visual tools can cater to different learning styles, making it easier for students to grasp and retain information.

The informal learning context, however, may pose a special challenge for financial learning, in which visuals of AFCs might be supported. Informal learning is rapidly increasing in the field of financial literacy, particularly as more and more people tend to refer to the internet to learn about financial concepts and products whenever a need arises (Rudeloff, 2019). The information on the internet is often extensive and unorganised (Morente-Molinera et al., 2019), which may impede learning, and the problem exacerbates as users have to navigate themselves and self-learn about financial topics online in informal contexts. Informal learning, with regard to objectives and procedures, is lowly structured, experiential and particularly not organised (Schürmann and Beausaert, 2016: 131). This may have serious consequences because, if users do not learn about finance effectively or if their learning is inaccurate, it may impact their financial planning and decisions, which can result in substantial financial losses. The visuals of AFCs may mitigate this issue, as representative visuals are relatively easily understandable compared to complex financial equations or information in the form of text only or graphs.

To further support the use of visuals of AFCs in both formal and informal learning contexts, it is essential to consider the evolving technological landscape and the diverse ways people access information today. Interactive digital platforms and mobile applications can leverage visuals to make financial concepts more accessible. For instance, educational apps can use gamified elements with visual aids to engage users in learning about budgeting, investments, and savings. Additionally, social media platforms can disseminate infographics and short videos that succinctly explain complex financial topics, making learning more engaging and less daunting. Collaborations with influencers and financial educators on these platforms can also help reach a broader audience. Moreover, incorporating augmented reality (AR) and virtual reality (VR) technologies can create immersive learning experiences where users can interact with visual representations of financial scenarios, further enhancing understanding. These innovative approaches can complement traditional learning methods, ensuring that financial education is comprehensive, inclusive, and adaptable to various learning preferences. By providing a clear and engaging visual context, representational visuals of AFCs can help learners develop a deeper and more intuitive understanding of financial concepts, ultimately improving their ability to apply this knowledge in real-world situations.

Discussion

Today's social and financial systems pressure people to individually take responsibility for important financial decisions related to saving and investing, post-retirement financial security, health care or home-buying (Alqahtani, 2018). However, regardless of the importance of this topic, people are remarkably low in financial literacy (e.g., Artavanis and Karra, 2020; Dewi et al., 2020). Consequently, financial education programmes have surged around the world with the aim of increasing financial literacy. The potential of financial education is immense and can improve people's financial decisions (Hastings et al., 2013). Moreover, it can also aid in securing their futures from economic uncertainties (Frisancho, 2020). While such financial education programmes are emerging rapidly, meta-analyses show that they are not as effective as they should be (Kaiser and Menkhoff, 2020; Miller et al., 2014).

Against this background, this article aims to support these financial education interventions by suggesting ways in which representational visuals of AFCs can be generated. According to CTML (Mayer, e.g., 2020), visuals significantly enhance learning outcomes (Andrä et al., 2020; Renkl and Scheiter, 2017). However, simply adding visuals to text does not automatically ensure successful learning. The effectiveness of these visuals depends on how well they represent the content of the learning material and align with the learners’ mental structures. For visuals to be truly beneficial, they must be thoughtfully designed to support and enhance the understanding of abstract financial concepts. This involves creating visuals that are not only relevant to the text but also structured in a way that complements human cognitive processes, facilitating easier comprehension and retention of the material. Properly integrating visuals with textual content can maximize the potential of human cognitive architecture, leading to more effective learning outcomes. This approach ensures that learners can more easily connect new information with their existing knowledge, thereby enhancing comprehension and retention.

The three techniques discussed in this study are potential ways in which AFCs can be represented by visuals: situations, emotions, and metaphors. The situational view suggests that the situations or contexts in which abstract concepts occur play an important role in visualising them. The emotional view suggests that adding emotional elements supports visualising abstract concepts. Finally, the metaphor view proposes that abstract concepts can be visualised using the knowledge about concrete phenomena.

Having given some hints as to which approaches can be used to create more representative images, we must also highlight some important points subject to be further discussed:

There does not seem to be the one and only way to create representational visuals. Since the link between tangible referents and the concept is not determined, using the one or other approach, several representative visuals might be creatable, and the one used could depend on the subjective taste, or ideas of the person creating the visuals. As far as to the authors’ knowledge there is no scale available measuring the optimal degree of representativeness. In addition, it is not clear at this point how we can most effectively stimulate mental simulations. Since the effective use of visuals depends on the learner, his or her prior knowledge, experiences and mental simulation capacities, there might be no ‘one size fits all’ picture. In contrast, adaptive designs might be necessary to enhance learning outcomes. AFCs vary widely in terms of complexity. e.g., whereas ‘interest’ is a comparatively simple concept, a 401(k) plan, i.e., a tax-advantaged retirement account that employers offer employees to help them invest for retirement, is a complex concept. So far, there is no empirical evidence of whether and how complex AFCs can be adequately represented by visuals without taking the risk of oversimplification. However, our approach is not to present visuals only in instructional material, but to add visuals to text. Thus, text and picture together should not oversimplify the explanation of a concept. In some cases, it might be advisable to use more than one picture, e.g., a series of visuals. While all of these techniques are unique, no study has provided evidence of the superiority of one technique over the others. However, each of these techniques may not be suitable for all types of AFCs. Perhaps a specific approach might be suitable for certain AFCs, while a different method could be more effective for other financial concepts. In addition, at the moment we cannot be sure whether the approaches can or should be combined.

Conclusion and outlook

Although the discussion opens up numerous unanswered questions, we believe we have made a contribution in that we systematised ways to create representative visuals and ground these ways theoretically. This study presents a view of the method-based approach, according to which instructional design is developed on the basis of ‘how people learn’ or—in other words—according to which learners are placed at the centre. This is in contrast to the media-based approach, which keeps technology at the centre of instructional design, with less focus on learners. According to Mayer (2022), the method-based approach is more productive, especially in an era of rapid technological expansion. Finally, for future research, empirical studies testing these approaches to making AFC visuals would be an appropriate direction.

Particularly, studies may focus on the effectiveness of various visualisation techniques to determine which methods best support learners in understanding and applying these concepts. Visualising AFCs can bridge the gap between theoretical knowledge and practical application, making learning more accessible and engaging. This approach, if successful, may not only aid in comprehension but also fosters better retention and application of financial knowledge, which is crucial for making informed financial decisions. Therefore, ongoing research and development in visual learning tools are essential to enhance financial education and literacy.

To set up future empirical studies testing the effectiveness of suggested visualisation approaches for abstract financial concepts, researchers may design comprehensive experimental frameworks. One approach could involve assessing the impact of visual metaphors on understanding AFCs, an experimental design can be implemented where participants engage with metaphorical visual. In this setup, participants can be randomly assigned to the treatment and control groups. In the treatment group, participants receive visuals that represent AFCs through visual metaphors and a control group receive only textual explanations. For example, to explain the concept of “market volatility,” participants might view a visual metaphor of turbulent ocean waves. This approach will enable an evaluation of how effectively visuals based on metaphors, situations, and emotions enhance the comprehension and retention of AFCs compared to traditional text-based methods.

In conclusion, the integration of representational visuals in financial education represents a promising frontier for enhancing comprehension and retention of complex financial concepts. By systematising the creation of representative visuals and grounding these methods theoretically, this study advocates for a learner-centred approach that aligns with modern educational practices. Future research should focus on empirically testing the effectiveness of various visualisation techniques to identify the most impactful methods for different learner demographics. Additionally, leveraging emerging technologies such as AR, VR, and interactive digital platforms can further enrich the learning experience, making financial education more accessible and engaging. These efforts will not only support formal educational settings but also empower informal learners, ultimately fostering greater financial literacy and informed decision-making.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.