Abstract

Young people's financial and digital literacy have been studied independently and in-depth during the last decades. However, digital financial literacy as a compound concept is novel and still needs to be explored in the scientific literature. This work investigated young people's perception of their digital financial culture, identified factors that hinder or facilitate it, and explored their preferences in the training modalities for improvement. Twenty-two focus groups were carried out in different Mexican educational institutions based on diversity criteria. The evidence shows that: (1) young people perceive the need for digital financial education linked mainly to the understanding of critical concepts, the use of mobile applications, online financial operations, and digital financial security; (2) some voluntarily exclude themselves from online finance, this being one of the main obstacles in the development of digital financial culture; (3) the digital financial culture gap is accentuated more among young people in public educational institutions and upper secondary education; (4) they have a preference for emerging technological and digital resources for their training in digital finance. These findings make it possible to contextualize training proposals that favor the financial inclusion of young people in complex scenarios brought about by the digital transformation of the economy and society.

Keywords

Introduction

Financial literacy is essential in an increasingly complex society. Developing financial capacities is essential for inclusive growth and financial health, empowering people throughout life and improving their social well-being (Hasan et al., 2021). Within the international framework of the United Nations declaration, “Transforming our world: the 2030 Agenda for Sustainable Development” (2015), financial education must position to enable responsible access to financial products and services, thus contributing to the creation of more inclusive, resilient, and sustainable societies. The acceleration of technology and digitalization in finance makes digital competency essential. Prestigious world reports such as the Human Development Report 2021/22 (United Nations Development Programme, 2022) or the World Development Report 2022 (International Bank for Reconstruction and Development and The World Bank, 2022) have repeatedly pointed out that digitalization and inclusion are the main challenges that must be addressed within the financial education agenda, especially for groups with greater social vulnerability and poverty. Therefore, financial and digital skills must be integrated into training proposals.

The promotion of inclusive and sustainable economic development requires the study of the financial literacy level of the population. According to a study on Financial Literacy Around the World (Klapper et al., 2015), precarious financial culture is a worldwide concern. Specifically, in Mexico, according to the National Survey of Financial Inclusion 2021 (Comisión Nacional Bancaria y de Valores y el Instituto Nacional Estadística y Geografía [National Banking and Securities Commission and the National Institute of Statistics and Geography] (2022), only 32% of the adults surveyed have a financial education. In more detail, it reveals essential data on this country comprising the Financial Literacy Index, which is higher among men, in urban locations with more than 15,000 inhabitants, and with bachelor's degrees. Regarding the latter, there is no clear evidence that young people use less cash than adults. However, youth is a stage of the life cycle in which there is usually no independent income; instead, there is economic dependence on parents; more and more young Mexicans alternate studies with paid work.

According to the Centro de Investigación en Política Pública [Center for Public Policy Research] (2022), 48.8% of young Mexicans between the ages of 15 and 24 work between 38 and 48 h a week, and 44.9% receive a minimum wage. In Mexico, a 2019 law change allowed working people between 15 and 17 attending school with scholarships to open bank accounts without the intervention of their legal guardians. However, 34% and 39% of young people have secondary education and upper secondary education or baccalaureate as the highest educational level, respectively (Organization for Economic Co-operation and Development [OECD], 2020). These data reveal that there are young people who can make their own financial decisions. As the National Banking and Securities Commission and National Institute of Statistics and Geography [National Banking and Securities Commission and the National Institute of Statistics and Geography] (2018) point out, the financial situation of young people is an essential factor that affects their financial inclusion. However, it is not the main one because 22.5% affirmed that they did not have a bank account or debit card, and 37.6% consider that they are not interested in obtaining one or believe they do not need one. This organization points out that not having a bank account is one issue that influences unemployment. Likewise, the study by the Instituto Tecnologico Autonomo de Mexico and Nacional Monte de Piedad [Autonomous Technological Institute of Mexico and Nacional Monte de Piedad] (2020) indicates that 7 out of 10 Mexicans delay financial education. Given this panorama, the need to educate young people about their finances is evident, as well as to encourage savings habits and the proper use of financial services.

In this country, relevant political measures have been taken in this regard. An example is the National Financial Inclusion Policy 2020–2024 (Consejo Nacional de Inclusión Financiera [National Financial Inclusion Council], 2020), which explicitly considers health and financial education as the primary objective for increased access and efficient use of the financial system, the development of economic-financial skills, and user empowerment. Due to the digital transformation in this sector, digital competency is considered a vital factor for young people's financial inclusion. In addition, the OECD International Financial Education Network (2023) promotes the digital financial inclusion of young people to ensure adequate protection as financial consumers and invites studies on social inequalities derived from diversity imbalances. Likewise, the Secretaría de Educación Pública Mexicana [Mexican Secretariat of Public Education] (2017) promotes the new educational model called Curricular Autonomy that calls for specific programs beyond the curriculum in educational centers and expands training; among the topics it includes is financial education.

Theoretical Background

Youth digital financial literacy

The technological, digital era has produced complex transformations in various sectors of society. Digital technology in the financial sector (Fintech) is changing consumer behavior and the demand for financial services. Their proficient use requires digital and financial literacy to make the right decisions. Some studies show the risks of digital financial services when digital financial education is lacking. For example, the correlation between mobile phone users, compulsive purchases, and financial risks on the internet has been verified (Joshi et al., 2017). Despite its importance, as indicated by the OECD (2017), there still needs to be consensus on the definition of digital financial literacy, which means researching the most precise way to define and measure it. Traditionally, scientific literature and prestigious international organizations have dealt independently with the study and promotion of digital and financial competency, although both are supported and involve the dimensions of “competency:” knowledge, skills, and attitudes.

On the one hand, the OECD (2015) established the Core Competencies Framework on Financial Literacy for Youth, which contains four sections: money and transactions, financial planning and management, risk and reward, and financial outlook. Each section, in turn, comprises three factors: (1) awareness, knowledge, and understanding, (2) skills and behaviors; and (3) confidence, motivation, and attitudes. On the other hand, UNESCO (United Nations Educational, Scientific and Cultural Organization), as the leading organization that promotes digital literacy, established that it includes (2021): knowledge (rights and risks in the digital world, sources of information, specific digital language, computer science applications); skills (searching and processing information adequately, using technological resources for communication and resolving problems of daily life, creating digital content) and attitudes (critical attitude toward technological means, assessment of their strengths and weaknesses, curiosity and interest in learning about using technology, and respect for ethical principles). Therefore, the development of financial education implies connecting with other learning domains to achieve digital competency.

Various authors have recently contributed to a conceptual approach to financial and digital education. For example, Prasad et al. (2018) refer to the knowledge to access online banking and make payments and purchases online. However, Morgan et al. (2019) provide a complete definition, focusing not only on knowledge but also on critical awareness, pointing out four fundamental elements: (1) knowledge of digital financial products and services (payments, asset management, or financing through digital means); (2) awareness of digital financial risks (online fraud and cybersecurity risks such as phishing, pharming, spyware, and SIM-card swapping); (3) control of these (knowing how to protect yourself from the risks derived from the use of digital financial services); and (4) knowledge of consumer rights and fraud-redress procedures (in the case of being a victim of fraud or loss, knowing your rights, where to go for help, and how to obtain redress). These contributions to digital financial literacy allow progress in developing specific training programs and evaluation tools (Lyons & Kass-Hanna, 2021; Platz & Jüttler, 2022).

The digital financial literacy gap among young people

Digitalization represents a revolution in financial inclusion, facilitating access to a wide variety of essential financial products and services for people who were previously removed from them (Gálvez-Sánchez et al., 2021). International organizations such as the International Bank for Reconstruction and Development and The World Bank (2022) affirm that this new generation of financial services accessed through mobile phones and the internet helps to bring finance closer to more sectors of the population. However, gaps remain, especially for people at risk of social exclusion and disadvantaged groups. This reality has become more apparent after the crisis caused by the pandemic, in which financial institutions have made widespread use of digital banking, and for many people, this was the only way to access banking services (Mhlanga, 2020). In addition, there is no consensus on the results of studies that have been carried out with young Mexicans on financial literacy.

On the one hand, the study by Arceo-Gómez and Villagómez (2017) concludes that their scores are low in financial concepts, intermediate in financial behaviors, and high in positive financial attitudes, and there are differences in gender, type of educational center, or socioeconomic status. However, another study with Mexican high school students showed that they generally have a low level of financial literacy. There are differences due to the type of educational center they attend (private or public) and different family socioeconomic levels (Diez-Martinez, 2016). On the other hand, digital competency in young Mexicans has been studied (Cuevas-Salazar et al., 2016). They perceived a moderate to high level of this competency. Furthermore, other studies have pointed out the gaps in the digital competency of young Mexicans due to geographic location, gender, and socioeconomic level: women and young people from rural areas and low socioeconomic status are those with lower performance (Pérez-Escoda et al., 2021; Vincent-Lancrin et al., 2022). In general terms, young people are more digital consumers than prosumers or creators of digital content due to their few skills (Navio-Marco et al., 2022).

The level of digital financial literacy of young people has been studied only in recent research. Some studies suggest that students with fewer digital skills find applications related to the use of money and investments less attractive (Saini, 2019). Added to the gaps due to diversity traits is the perception-reality gap. In digital financial literacy, young adults thought they had a higher level of financial literacy than they did (Latheef and Sunitha, 2016). Specifically, the Gallego-Losada et al. (2021) study evidences the disparity in measuring digital financial competency in young people. There is an intermediate level in the self-perception of digital financial knowledge, skills, and attitudes and a lower level when they must tangibly demonstrate digital financial competency. The causes of young people's low digital financial literacy have not yet been explored.

Technological advances can accentuate the disparities between people with and without digital financial literacy. The technological transformation of the financial sector makes it necessary to adapt financial training to digitalization to achieve the digital financial literacy of consumers of different ages, reduce existing gaps, and promote financial and social inclusion. Studies on the digital financial literacy of young people shed light on the positive impact of digital competency on using i-banking services and effective financial decision-making (Panayiotis and Anyfantaki, 2021). There is a consensus on the favorable impact of digital financial education on young consumers’ spending and saving behavior (Setiawan et al., 2022). Likewise, the effectiveness of technological applications has been evaluated to level young people in a situation of inequality in learning to achieve digital financial literacy, thus attaining financial well-being (Zhang, 2021). Even though it has been proven that students with high financial competency are more likely to cope with complex scenarios, develop more effective savings practices, complete higher education, or work in higher-qualified jobs (D'Angelo, 2022; Suri and Jindal, 2022), more studies are needed that assess young people's training for integrated financial and digital literacy. Among the training modalities that young people prefer are those utilizing emerging media and digital platforms (Pereira et al., 2019).

Method

Design

This research aims to explore and analyze the digital skills that young people need in the finance sector, which are essential in building an inclusive and sustainable society. From this general goal, three specific objectives are derived:

To know the perception of young people about their level of digital competency applied to financial services. To identify the obstacles and facilitators to a digital financial culture, considering the possible gaps among young people related to personal and contextual variables. To explore young people's training preferences in digital financial literacy.

A qualitative study was carried out to achieve these objectives using focus groups as a research technique. In the development of the group conversation, dialogical narratives impregnated with multiple types of intertextualities emerge, which allows for obtaining different perceptions, identifying different trends and commonalities in opinions, sharing experiences and opinions, and generating different reactions (Carey and Asbury, 2016; Krueger and Casey, 2014).

Participants

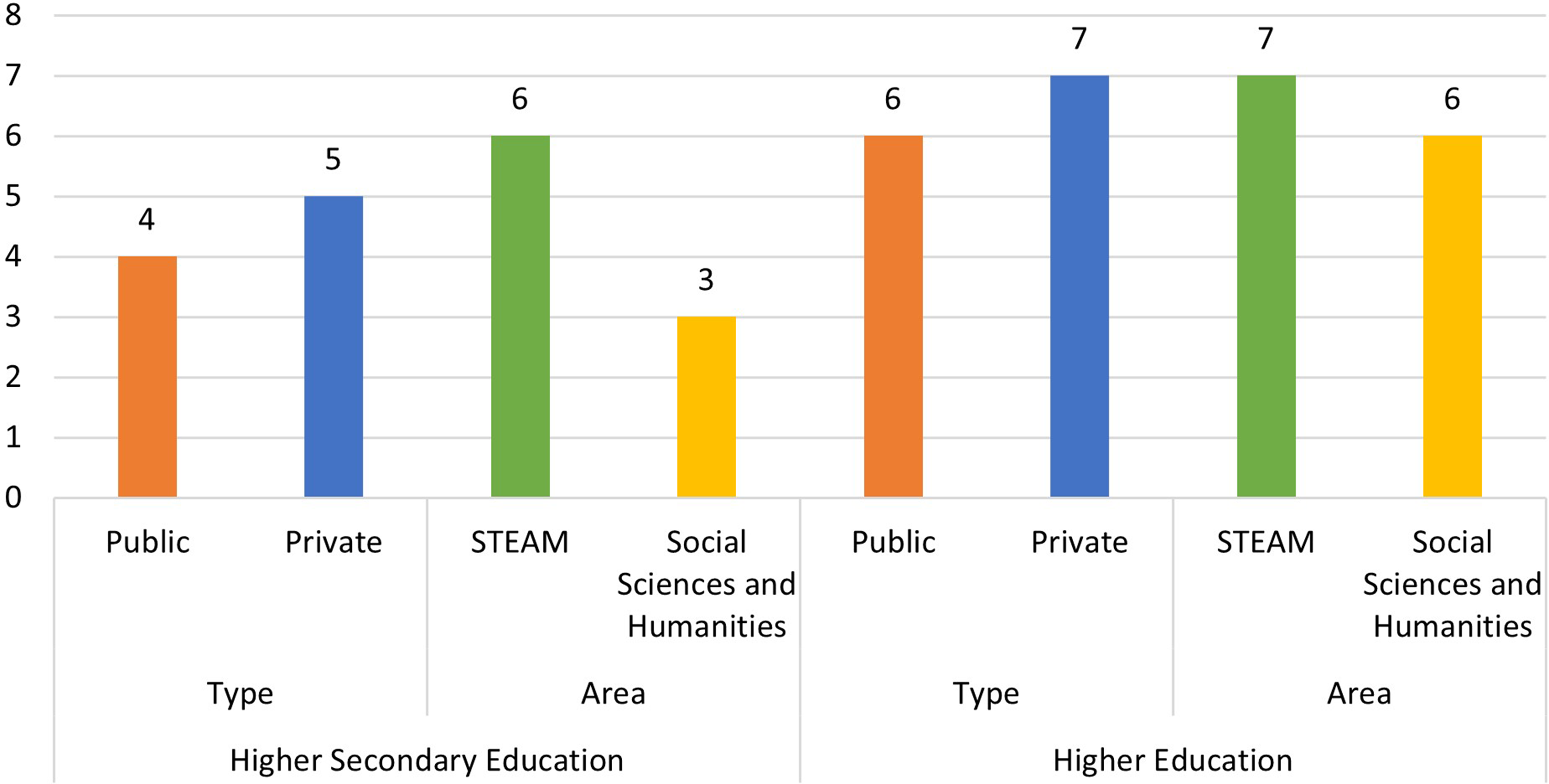

There were 22 focus groups of between eight and ten young people from four cities in Mexico. According to the population ranking of the National Institute of Statistics and Geography, three were within Mexico's ten most populous cities, and one was within the top 20. The participants were selected considering different diversity criteria or personal and contextual variables. Thirteen focus groups were held in higher education (university) settings and nine in upper secondary education (upper high school levels) after prior contact with the different educational institutions and the teachers. Figure 1 shows that within each educational stage, focus groups were formed according to criteria such as the type of educational institution (public/private) and different areas of knowledge (STEAM/Social Sciences and Humanities).

Number of focus groups according to diversity criteria.

A total of 200 young people participated. Their average age was 20.1 years in higher education and 17.3 years in upper secondary education. It was guaranteed that in the configuration of the focus groups, there would be diversity in terms of gender (women = 96; men = 104). Socioeconomic status was determined based on whether the young people had scholarships. 68% and 30.1% of young people from public and private educational institutions had scholarships, respectively. Regarding whether they used any financial products, 55.3% of young people answered affirmatively and 44.7% negatively.

Instrument and data analyses

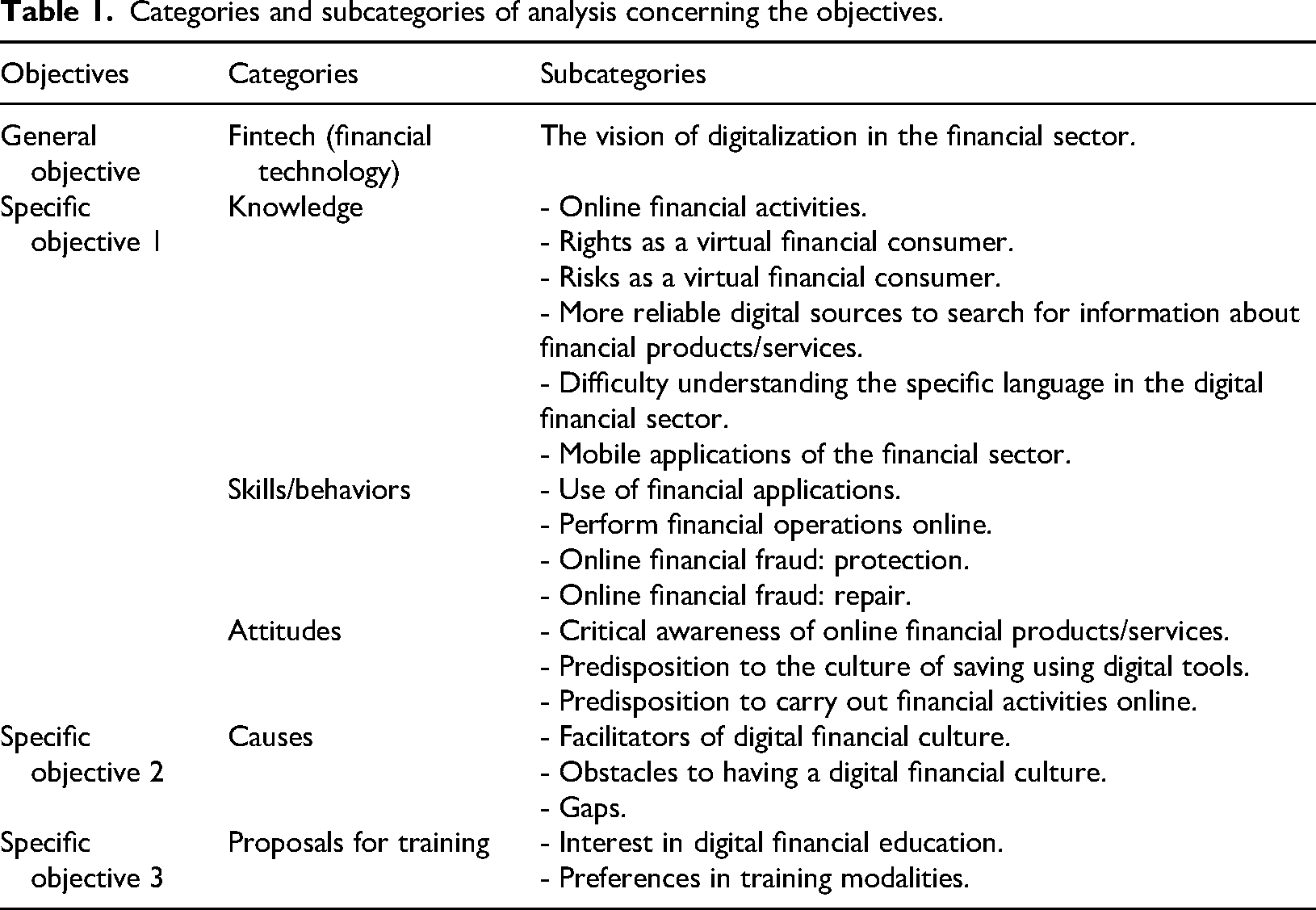

The three proposed objectives elaborated a protocol of open questions. For its elaboration, the bibliographic review was started, from which the conceptual categories of the term “competency” and the dimensions of digital financial culture were deduced (Morgan et al., 2019; Prasad et al., 2018). People independent of the study ensured compliance with the conditions that a system of categories must meet clarity, relevance, exclusivity, and objectivity (Cohen et al., 2017). Two pilot focus groups allowed the evaluation of the established protocol of questions, which led to some reformulation of the questions to achieve greater clarity for the young people. Finally, deductive analysis was carried out using the ATLAS. ti version 22 program. Table 1 shows the categories and subcategories of analysis for the previously stated objectives:

Categories and subcategories of analysis concerning the objectives.

Procedure

A team of eight researchers was formed to carry out the focus groups. They wrote a document to define the requirements that the participants in the focus groups had to meet, the role of the moderator and the observer, and other aspects to consider during the discussion (a relaxed, quiet, comfortable, and trustworthy environment for young people):

Moderator: responsible for question formulation and dynamic interactions but intervening as little as possible in the opinions and answers of the young people. Observer: in charge of writing down possible aspects that the audio might not pick up.

Before starting the focus groups, we obtained informed consent regarding the privacy of the information, confidentiality, and audio recording. The discussion groups were held in classrooms in different educational institutions. The duration of the discussion groups was between 50 and 90 min. All groups were audio recorded and transcribed for later coding and categorization.

Results

The results are presented per the specific research objectives. The ideas and contributions have been grouped in the categories defined in the instrument's design, indicated in bold text. The textual citations used in this section include the enumeration of the focus group and the educational stage (Higher Education -H.E.- / Higher Secondary Education -H.S.E.-) in parentheses.

Know the perception of young people about their level of digital competency applied to financial services.

The results obtained about the categories of analysis intrinsic to the concept of competency are detailed below:

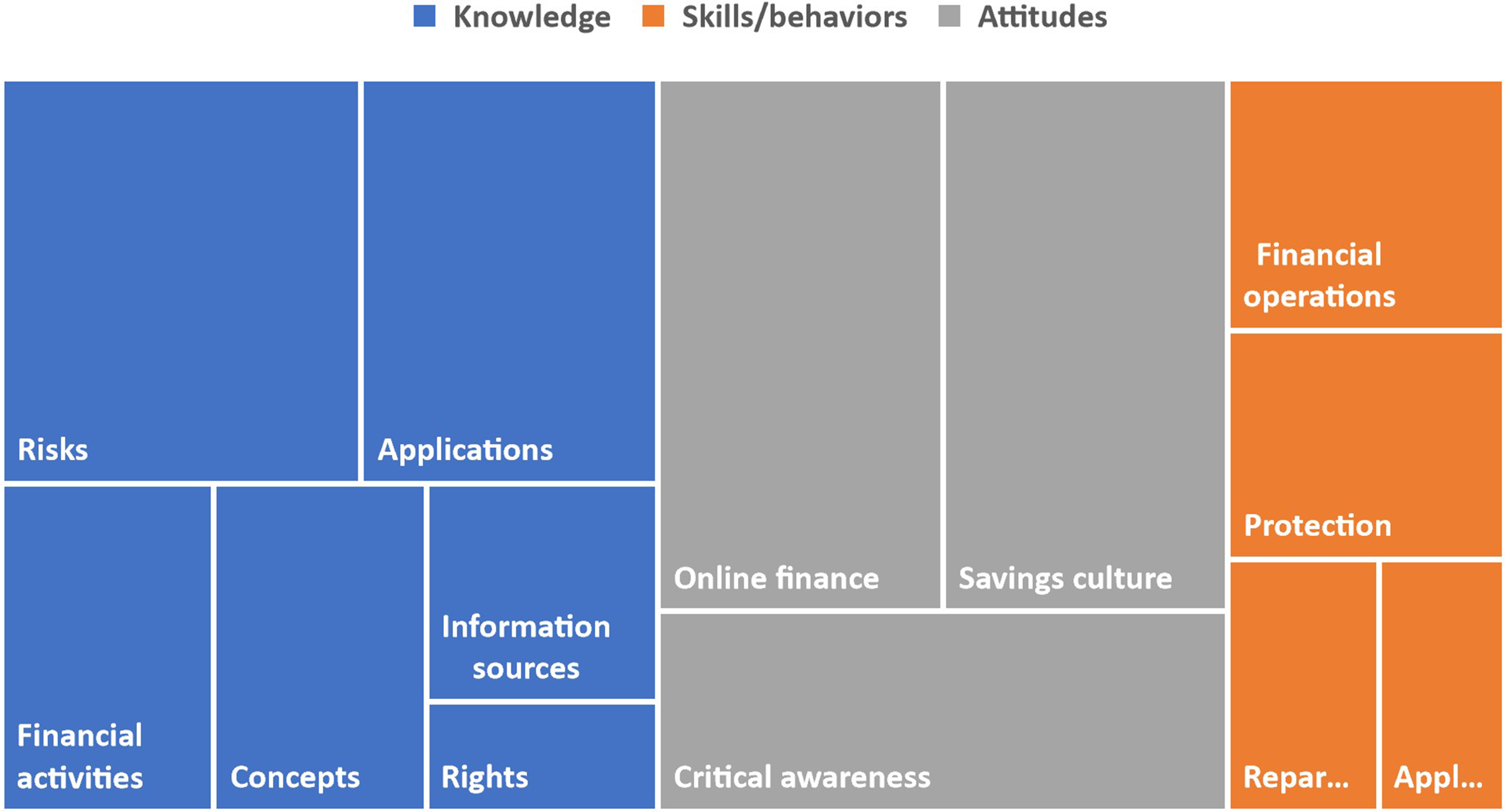

Knowledge: Young people know some Behaviors or skills (knowing how): Even though they know the existence of mobile applications in the financial sector, they are unaware of all their Attitudes (knowing how to be): There is no consensus regarding the

Figure 2 shows the dimensions considered in analyzing the self-perception of digital financial competency. The larger blocks indicate higher feelings of competency by the young people.

Self-perception of digital financial competency per the established dimensions.

Identify the obstacles and facilitators to a digital financial culture, considering the possible gaps among young people related to personal and contextual variables.

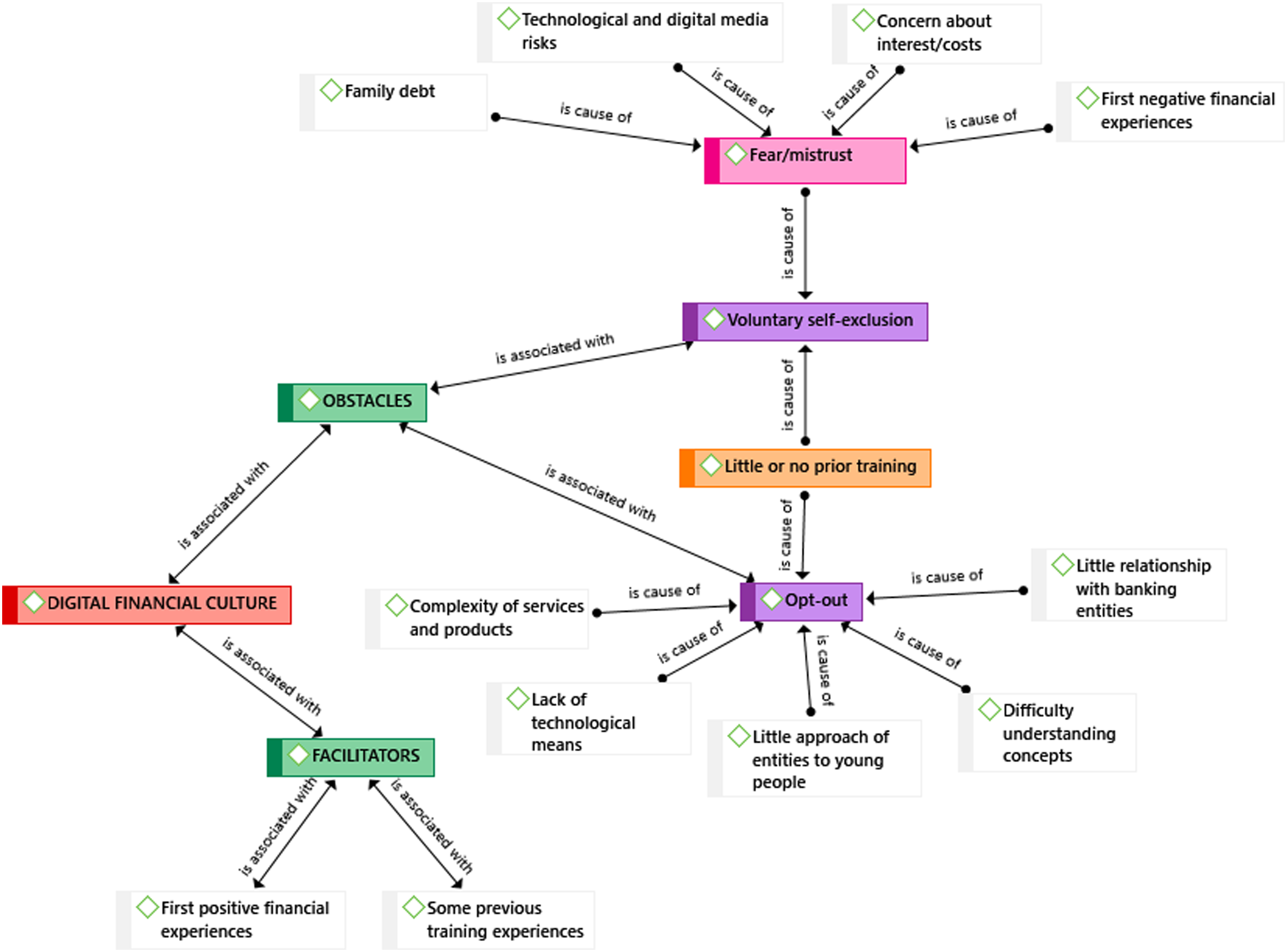

Young people have identified obstacles and facilitators affecting their digital financial culture. Training in financial and digital literacy is relevant to young people's digital financial culture. Some point out that thanks to the previous training, they have a more incredible financial culture: “The conference Banorte gave here on campus helped me to understand some things” (F.G._5_H.S.E.). Some consider that the lack of prior training is a reason to exclude themselves from digital finance: “We have barely received a financial education that lets us learn how to use these applications or know what we can do with them, so we cannot use them” (F.G._6_H.S.E.).

Young people consider Some factors that lead them to exclude themselves voluntarily are: difficult family experiences with financial institutions [“My father was in debt from a very young age because the bank did not inform him well” (F.G._5_H.S.E.)]; risks of technological and digital media [“I am afraid to use my credit card when shopping online because they can take my data and I will be left with nothing” (F.G._6_H.S.E.)]; concern about interest or commissions [“I prefer money in cash; if I have a card I am worried that they will charge me money"(F.G._7_H.S.E.)]; and negative banking experiences [“I went to several banks to open a bank account, and none of them let me. I am over 18, I have a job, and they still did not let me create an account” (F.G._7_H.S.)]. These elements provoke fear and distrust in young people. Other factors make them feel involuntarily excluded from digital finance, such as the complexity of financial services and products [“They are designed for older generations, not for us” (F.G._12_H.S.)]; the lack of digital media [“In my case, I have problems accessing the internet, and I need to buy a computer. I do not know how I could benefit if now the banks put everything online” (F.G._11_H.S.E.)]; the limited approach of financial institutions to young people [“They do not think about us, young people, because we do not have money. Our parents or grandparents can have money. So, they do not come close to us” (F.G._15_H.S.)]; the difficulty in understanding the language used by financial institutions [“They use words we do not know because we have not studied them at school. If I do not understand what is sent to me (product and service offerings), I cannot know if I want it or not” (F.G._17_H.S.E.)]; and the limited relationship with financial entities [“We still do not have much experience with banks because we do not know how they can help us, whether they can offer us loans for our studies, transportation, food…” (F.G._19_U.S.)].

Young people also highlight

Figure 3 shows the elements that affect the digital financial culture of young people.

Young people's perception of obstacles and facilitators to a digital financial culture.

All young people generally demand more training to improve their digital financial culture. However, differences in knowledge, behaviors, and attitudes were found between the young people depending on the educational stage (higher education/higher secondary education) and the institution's ownership (public/private). No differences were attributed to the other personal and contextual variables. Specifically, young people from public institutions and upper secondary education emphasize the difficulty in accessing technological and digital media and have fewer ties to financial institutions than those attending private institutions and in higher education: “We need some financial aid that allows us to buy computers. Besides, the internet does not always work for me at home; I have connection problems. So, I see it difficult to make a purchase online” (F.G._17_H.S.E.).

Explore young people's training preferences in digital financial literacy.

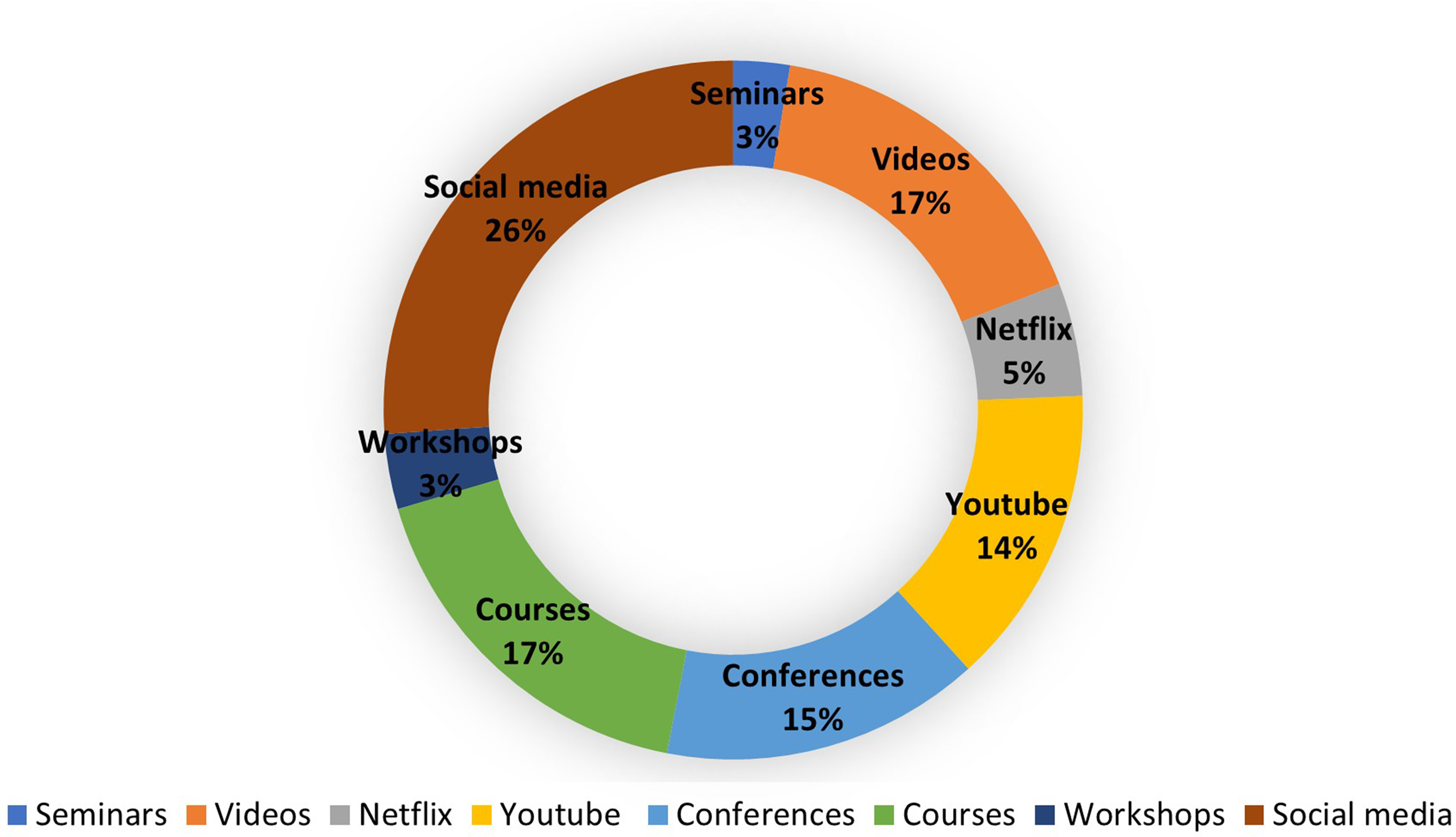

Young people express interest in receiving training in digital financial competency adapted to their age: “Sometimes information reaches you, the bank offers you things, but it is not what you need, it has nothing to do with your situation” (F.G._13_H.S.). Likewise, they do not want the information to reach them in the form of advertising on their mobile phones or by email: “I do not like advertising to arrive in my mailbox; if I see it, I delete it; the same with the messages that you receive from advertisements. I like more the videos in which things are explained” (F.G._19_H.S.). As Figure 4 shows, young people prefer traditional training modalities, such as courses or conferences, but also newer ways familiar to them, such as social networks or digital platforms: “I think that putting more banks will not be beneficial to our financial literacy, but investing more in digital instruction would help; people watch a lot of Netflix or YouTube. There are things like more commercials… that give information and can be digested more easily” (F.G._1_H.S.).

Preference in the training modalities for the acquisition of digital financial competency.

Discussion

The present study aimed to determine young Mexicans’ perceptions of their digital financial competency, obstacles, facilitators, and training preferences for improvement. This analysis is original, given the lack of discussion of this composite concept in the scientific literature. Advancing the training of young people in digital competency in specific areas or fields, such as finance, and the approach to these by financial institutions are the most relevant aspects of digital financial literacy obtained in our results. This finding supports previous research on the financial literacy of young people in Mexico by evidencing the gaps in financial education (Instituto Tecnologico Autonomo de Mexico and Nacional Monte de Piedad [Autonomous Technological Institute of Mexico and Nacional Monte de Piedad], 2020).

Concerning the first objective, this research found the training deficiencies that young people perceive regarding digital financial competency. They are aware they need digital financial literacy since they know some digital financial applications and financial activities that can be done with them. However, they need to learn all their functionalities because they lack an understanding of the specific terminology and have difficulty finding reliable information about it. Likewise, they are critically aware of the risks of digital and technological media in the world of finance, but they do not know the rights they have as financial consumers or how to protect themselves in the event of fraud. This finding partially corroborates the conclusions reached by the study by Arceo-Gómez and Villagómez (2017), in which young people had a low score in financial concepts, intermediate in financial behaviors, and high in positive financial attitudes.

Regarding the second objective, this work identified the obstacles and facilitators encountered by young people in digital financial culture. The existence or absence of previous training experiences is a critical element in their exclusion from the digital financial world. This finding supports previous research by Saini (2019) that suggests that students with fewer digital skills find applications related to the use of money and investments less attractive. Other studies have shown that young people with digital financial education are not excluded from the digital financial world but rather make greater use of i-banking (Panayiotis and Anyfantaki, 2021) and make better decisions in their savings and spending (Setiawan et al., 2022). On the other hand, it has been shown that some young people voluntarily exclude themselves from digital finances due to fear or mistrust. This is in line with studies by the National Banking and Securities Commission and the National Institute of Statistics and Geography (2018), which found that approximately one-third of youth did not have a bank account or debit card, were not interested in obtaining one, and believed that they were not going to need one. The lack of digital financial training is detrimental to employment and financial inclusion in a country where approximately half of the young people work (Centro de Investigación en Política Pública [Center for Public Policy Research], 2022) and only a third complete secondary education (OECD, 2020). On the other hand, the analysis of the digital financial gap based on diversity criteria allowed us to deduce that young people from public educational institutions (of lower socioeconomic status and with a more significant number of scholarships) place greater emphasis on the difficulty in accessing technological and digital means and banking entities. This gap is associated with the already-demonstrated gap in financial literacy (Diez-Martinez, 2016) and digital literacy (Vincent-Lancrin et al., 2022).

Finally, concerning the third objective, we explored young people's preferences for the training modalities for digital financial literacy. It was found that young people prefer emerging media and digital platforms to receive this training. This result coincides with the work of Pereira et al. (2019), in which young people do not prefer traditional training modalities such as courses. Discussion of these findings invites further educational practice and research.

Conclusions and Implications

This work highlights the importance of digital financial literacy of young people to construct a more inclusive and sustainable society. The findings point to the design of a contextualized training proposal for digital financial literacy, based on: (1) the understanding of critical concepts, the use of mobile applications, online financial operations, and digital financial security; (2) overcoming the obstacles that determine voluntary self-exclusion or involuntary exclusion from digital finance, among which is the feeling of trust, previous training, family and financial experiences, and the proximity of financial institutions to young people; (3) the reduction of existing gaps in the digital financial culture, especially among young people from public educational institutions and upper secondary education; and (4) the emerging digital media, platforms, and applications that promote learning.

This work's main limitation is having selected a sample of students from a particular country, with a predominance of STEAM and Social Sciences and Humanities disciplines. Likewise, the perceptions and opinions of their teachers and families have not been considered, nor has the analysis of the previous study plan on financial and digital competency been taken into account. Also, the scarcity of studies that empirically address the analysis of digital financial culture reduces the ability to analyze the results by comparison.

This study serves as a basis to open new lines of research. This work is based on young people's perceptions rather than their actual digital financial literacy and performance. It remains to be determined whether those who perceive more excellent skills are also users who leverage the opportunities that financial institutions offer them. Previous studies (Gallego-Losada et al., 2021; Latheef and Sunitha, 2016) have shown that the literacy level is even lower when evaluating the implementation of the competency, which has implications for future research. Higher digital financial literacy could lead to better results in managing personal finances.

Additionally, this study could be carried out periodically to follow in real-time the adaptation of the students to the changing and demanding digital financial environment. Students from other countries and studying other degrees would enrich the sample. The study plans that students have followed in previous stages of their training vary in different countries; thus, different results can be expected. Finally, it would be interesting to extend the study to other groups who are not students, such as the older population, to analyze whether, as it appears, there may also be a digital financial gap, which could translate into potential exclusion in this part of the population.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors would like to acknowledge the financial support of Tecnologico de Monterrey through the “FINTEC 4.0: Financial literacy of young Mexicans in the context of reasoning for complexity” and “Challenge-Based Research Funding Program 2022. Project ID # I001 - IFE001 - C1-T1 – E”. Also, the authors acknowledge the financial and technical support of Writing Lab, Institute for the Future of Education, Tecnologico de Monterrey, Mexico, in the production of this work.