Abstract

The prevalence of in-school savings programs (ISSPs) for children and youth is widespread, but research on their effectiveness is limited. This study investigates the long-term effects of an ISSP conducted in one U.S. elementary school. Survey data were collected on the financial behaviors of high school students, who participated in or did not participate in an ISSP while attending the same elementary school at the same time. The results from a probit analysis of data controlling for demographic variables showed that ISSP participants compared with non-participants were more likely to have a bank account in high school. They also were more likely to have opened a bank account before attending high school. Further results show that high school students with bank accounts are more likely to save regularly, indicating that ISSP contributes indirectly to saving regularly through its direct influence on getting students to open a bank account and open it early.

Saving is a financial behavior that directly contributes to personal well-being and thus improves the welfare of society (Browning and Lusardi, 1996; Lusardi and Mitchell, 2014). Saving money in the present is important for accumulating funds and building wealth to pay for desired goods and services in the future, such as for further education, housing, or retirement. The availability of savings gives people more financial control over the timing of their purchases of goods and services and can help them reduce reliance on high-cost debt for making purchases. In addition, savings offers a cushion from the adverse shock of unexpected expenses, which in turn reduces financial stress that arises from financial emergencies (Babiarz and Robb, 2014). Public recognition of the personal and societal benefits from saving is a major reason that this topic is included in the financial literacy curricula for schools and taught to students beginning in elementary school (Council for Economic Education [CEE] 2021; Organization for Economic Cooperation and Development [OECD], 2015).

In the United States, some elementary schools use in-school savings program (hereafter ISSP) to give students an experiential activity to learn about saving, develop a regular habit of saving, and use a bank account to save. The program does this by establishing an actual branch of a depository financial institution, such as a bank or credit union, within an elementary school. Each week a representative of the financial institution visits the school to give students an opportunity to make deposits of real money into their savings accounts. Students can continue making saving deposits in their accounts each year until they graduate from elementary school. At the end of the program, which is typically the fifth or sixth grade, ISSP students receive their accumulated savings from their accounts for personal use and the accounts are closed. They then are encouraged to open their own accounts at a financial institution of their choice and continue to save regularly. 1

This study evaluates the long-term effectiveness of this experiential program for elementary students. The study was designed as a quasi-experiment with a treatment and a control group. The treatment group consists of students who participated in the ISSP in the elementary school but are now high school students. The control group consists of students who attended the same elementary school and high school at the same time as treatment students, but they did not participate in the ISSP. Both treatment and control students are now attending high school. The data for the longitudinal assessment come from a survey on the banking and saving behaviors administered to both groups of the high school students, who are three to six years removed from elementary school and their participation in the ISSP. The research focuses on whether the financial behaviors of ISSP participants differs from non-ISSP participants in the years after the ISSP ended.

Following this introductory section, the remainder of the study is divided into additional sections. The second section offers a literature review to provide perspective and context for ISSPs. The third section describes the setup, operation, and student participation in an ISSP. The fourth section discusses the data collection, study variables, and experimental design for the study. The fifth section explains the hypotheses, empirical analysis, and the results. The sixth section discusses robustness checks on the findings and describes some limitations of the study. The seventh section discusses the implications from the study. The concluding eighth section briefly summarizes the major findings.

Literature review and ISSPs

In a systematic research review published in this journal, Amagir et al. (2018) assessed 32 studies in detail on the effectiveness of financial education programs, 8 in elementary schools and 24 in secondary schools. Their conclusion summarized the findings, identified research gaps, and offered suggestions for sound pedagogy. One conclusion was that the “findings support the notion that financial-literacy education must start as early as elementary school” (p. 75). One research gap was that “longitudinal experimental research is needed to investigate the long-term effects of specific financial education programs on financial knowledge, behavior, and attitudes” (p. 75). One suggestion for pedagogical practice was that “experiential learning” was a “promising method” for teaching financial literacy, particularly for elementary school students where the focus should be on “hands-on pedagogy” and “learning by doing” (p. 76).

The three conclusions from this review have salience for this study. First, it assesses the effectiveness of a financial literacy program in elementary school, where the review recommends that financial education should begin. Consequently, it contributes to the limited research at this educational level. Second, it investigates the long-term effects of the elementary school program on the financial behaviors of high school students. Longitudinal studies of program effects on financial behavior are relatively rare, as the main outcome typically assessed is financial knowledge at the end of a program. Third, the in-school saving program that was investigated used experiential learning as the only pedagogical method. It emphasized hands-on activity and learning by doing to teach elementary students about the basics of saving and banking.

Saving and banking are generally seen as adult financial activities, although research shows that children are capable of understanding savings and banking concepts at an early age. Berti and Monaci (1998) found that children between the ages of 6 and 10 understood the concepts of deposits and withdrawals. Furthermore, Webley (2001) describes a series of studies he carried out with his colleagues on saving and delayed gratification in children. He concluded that “by age 6, children know that saving is a “good thing”: They have learnt that self-control, patience, and thrift are virtuous” (p. 57). He also reported major improvements in savings for children between the ages of 6 and 9, a noteworthy finding related to this study as ISSPs targets children in this age range.

Saving is an important topic to be taught to children and adolescents according to the educational content guides for financial literacy. In the United States, for example, the National Standards for Personal Financial Education lists saving as one of six major topics, along with earning an income, spending, investing, managing credit, and managing risk (CEE, 2021). The content associated with each major topic is explained in detailed standards and learning outcomes that are recommended for completion by the grades 4, 8, and 12 in U.S. schools. Saving also is a major topic in the core competencies framework on financial literacy for youth worldwide (OECD, 2015).

Although saving is an important topic, a logical follow-up question is how it should be taught to children. One answer with broad support is experiential learning, whereby students participate in hands-on activities and learn by doing from the activity. The concept is not new because in the first half of the twentieth century, John Dewey, a major educational reformer, called for more experiential learning in school education because he saw that “there is an intimate and necessary relation between the process of experience and actual education” (Dewey, 1938: 20). More recently, researchers studying financial education recognize the value of experiential learning. Kasman et al. (2018) concluded from their review of the financial education literature that “many experts agree that financial education that includes opportunities for student participation, discovery, and exploration—in other words, “participatory learning”—can have a strong, positive impact on financial literacy” (p. 3).

Research on the effectiveness of financial education programs on savings for elementary students are rare, but two studies provide perspective for this study. An investigation of the I Can Save program used a quasi-experimental design with elementary students in an urban school (Sherraden et al., 2011). The treatment group received financial education over four years, a savings account, and monetary incentives for savings. The financial education used lessons from the Financial Fitness for Life curriculum. Experiential learning was incorporated through a voluntary after-school club that met once a week. The club activities included games and monthly field trips to deposit savings in a bank. The control group received no financial education and did not participate in club activities or have a savings account. The main result showed a significant increase in the financial knowledge of the treatment group compared with the control group after four years. Interview data were collected on financial attitudes and behaviors, but only for the treatment group, so there was no comparison of the program effects on those outcomes.

Batty et al. (2015) reported the results from an in-school savings program for fourth and fifth grade students in two school districts. Randomization was used to assign financial education to classrooms. The treatment groups received financial education from the Financial Fitness for Life curriculum. The control or baseline group of students did not receive any financial education. The results indicated that students receiving financial education showed a significant increase in financial knowledge that persisted one year afterwards. Some positive effects for the treatment group were found for financial attitudes and self-reported behaviors based on student survey data. Of most interest for this ISSP study is the recognition in the conclusion (pp. 87–88) that the measured outcomes might be increased with more experiential learning instead of the traditional of lectures and lessons that were used by classroom teachers.

An ISSP for an elementary school is substantially different in its pedagogy than the saving programs for elementary schools assessed in the two previous research studies. The main difference is that an ISSP relies exclusively on experiential learning that emphasizes student participation and learning by doing (as explained in the next section). It does not require teacher-led instruction and classroom lessons. It does not focus on testing financial knowledge related to a published curriculum. Of course, a school could complement an ISSP by adding more traditional instruction with a published curriculum, but that pedagogical practice would be a major exception. It is more likely to be the case that the ISSP is considered to be an experiential activity for enhancing understanding of state or school standards related to personal finance and saving.

ISSPs are encouraged by U.S government agencies such as the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC) as is evident in several of their publications (FDIC, 2017a; OCC, 2017). The FDIC website states that “School-based experiential financial education is among the most promising frontiers in the field of financial capability” and reports that youth savings programs are operating in 27 states. 2 The FDIC conducted a pilot study of youth savings programs in schools that reported benefits based on anecdotal comments collected from 21 banks in 17 states (FDIC, 2017b). However, no research study with treatment and control groups has investigated the effectiveness of such programs.

ISSPs also are popular within states. Nebraska, the state in which this study was conducted, has a 20-year history with ISSPs as the first one was established in 2002. 3 In 2022, 36 ISSPs operated in elementary schools throughout the state or in several nearby locations in the state of Iowa. These schools partnered with 19 financial institutions (banks and credit unions) to establish ISSP branches, with some institutions partnering with multiple schools. As was the case nationwide, no research assessments have been conducted on the effectiveness of these ISSPs.

Methodology: ISSP implementation

What follows is a description of how an ISSP operates in U.S. schools and how students participate in it. It is a generic description because an ISSP may operate slightly differently in each school depending on the school circumstances and conditions. Despite any differences, the basic purposes of an ISSP are the same in each elementary school. First, it gives students a real-life experience with having their own savings account. Second, it offers students participatory opportunities weekly to use that account to save their own money to meet a financial goal. Third, it encourages the habit of saving regularly during the year and across the grades that the ISSP is offered within an elementary school.

Technically, an ISSP is a partnership between a local financial institution (bank or credit union) and an elementary school. A special operating branch of the financial institution is established in the school. In some locations, a state government agency that oversees and regulates financial institutions within a state approves the opening of the school branch and has the legal authority to regulate its operation, should it choose to do so. Agencies of the U.S. Federal government also have issued regulatory guidance on the opening of savings programs in schools. 4

A signed parent permission letter to participate in the ISSP is required for students to open their bank account. The account is a non-interest custodial account opened in the name of the school. The principal and other key individuals are signers on the account. Student “account numbers” within the master school account are typically their school identification number or something similar. The student accounts are for deposit only as students are not allowed to make withdrawals. The account is only available within the school branch, meaning that students cannot make deposits at the local branch of the partner financial institution.

ISSPs typically operate for 25–27 weeks each school year with the branch open one day a week for about 30 to 60 min for ISSP students to make deposits into their savings accounts. The school assigns a teacher to oversee student participation across grades, obtain and validate the permission slips, and communicate with parents. A representative of the financial institution visits the branch during its operating hours to supervise operations. The records on student account balances are kept in a spreadsheet that is updated weekly by the representative or another employee of the financial institution. The financial institution audits the school account.

Each year, upper elementary students are selected to work at the school branch as tellers and are supervised by the teacher-coordinator. Students who want to be tellers apply for the job. The application requires students to show math competencies and to submit a written paragraph on why they should be selected as a teller. Often, finalists undergo a final oral interview with members of the partner financial institution. Depending on the size of the school, branches generally designate 12–24 students as tellers, which allows students to work one day a month. Once tellers are chosen, the financial institution conducts training sessions for the new “employees.” The training is similar to training that regular bank tellers receive. Students are taught how to fill out and check deposit slips for accurate math. Students learn about customer service skills and the importance of privacy for account holders.

Three to six tellers work each day the branch is open. To minimize out of class time for students who wish to make a deposit, one of the student tellers acts as a runner to let each classroom know it’s their turn for any students who have a deposit to make into their account that day. This procedure avoids wasting classroom time to wait in line. Other tellers work to assist younger depositors in completing deposit slips and helping at the incentive table.

Students receive different incentives for habitual saving and for reaching savings levels. A student’s first deposit, up to $5, is typically matched by the partnering financial institution. For each deposit a sticker is placed on the outside of the student’s savings register. In lieu of interest, students earn trinket incentives, such as pencils or coin pouches. The incentives can increase as students reach higher deposit frequency or meet higher savings levels, such as having lunch with bank personnel. All earned rewards are designed to encourage the habit of saving.

To create additional excitement around the program, many school branches include additional program incentives. For example, several schools have a travelling trophy that moves weekly to the classroom with the highest percentage number of savers for the week. To keep focus on the habit of savings, many programs offer monthly incentives. For example, if a student makes a deposit three of the four savings opportunities in a month, they may receive coupons for a free ice cream cone at a local establishment or other special prizes from community partners for the school.

Students can begin participating in the ISSP in whatever grade the school starts the program (e.g., second or third grade). ISSP participation for each student can continue in each grade to the end of elementary school (e.g., fifth or sixth grade). Students only receive their accumulated savings when they graduate from the elementary school or leave the school and transfer to another school.

Data, variables, and research design

The location for the study was a community school (hereafter CS) that serves students in a Nebraska community that includes a town and surrounding rural areas with a population of less than 2000. The ISSP at this CS opened during the 2000s. This school site was selected for the study because of its history and experience with an ISSP, which was a necessary condition for conducting this longitudinal assessment.

A survey of CS high school students was constructed with input from CS administrators. It collected data on basic demographics, ISSP participation, having a bank account, having a job, and saving regularly. Field testing of the survey instrument was conducted at another Nebraska high school with students who did and did not participate in an ISSP in that school district. After revision, the survey was approved for student use by the CS school board, subject to parental permission for students. It was administered by CS teachers in December 2018, and again in January 2019 to students who missed the first administration. The CS staff matched student information on their status for receiving free or a reduced cost lunch and whether students were in a “gifted” program. All identifiable student information was deleted from the file for data analysis. 5

The high school student population at the CS consists of 113 full-time students in grades 9 through 12. A total of 102 students completed the survey, for a 90.2 percent response rate. Three reasons account for the missing data on 11 students: (1) did not answer any questions; (2) absent on the days the survey was administered; or (3) no parental permission to participate. It is unlikely, however, that this minor attrition adversely influenced the survey results because of the high response rate over all grades and for each grade level (90 percent average).

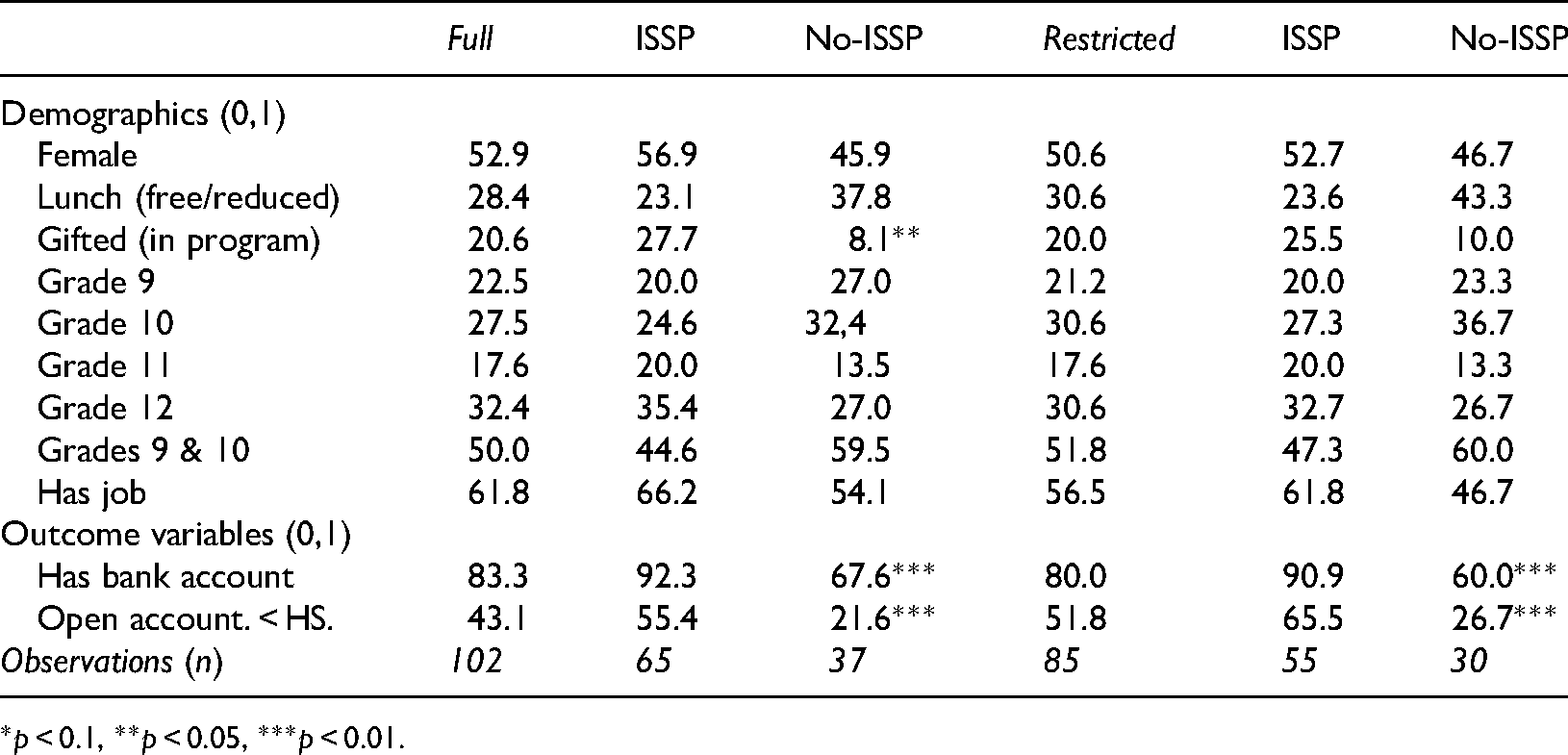

Table 1 presents data on the full sample (n = 102). The demographic variables in the table show that in the sample 52.9 percent are female, 28.4 percent receive a free or reduced cost lunch (a household income indicator), 20.6 percent are in a gifted program (an ability indicator), and 61.8 percent have a job while attending high school. 6 Also shown are the percentages by each high school grade (9 to 12). Combining the grade data reveals that half of the survey responses came from students in lower high school grades (9 or 10) and the other half from upper high school grades (11 or 12). The lower part of the table presents data on the two outcome variables: 83.3 percent of students have a bank account and 43.1 percent opened that account before attending high school.

Variable statistics in percent for full or restricted samples.

*p < 0.1, **p < 0.05, ***p < 0.01.

A key variable for the research is participation in ISSP. The study is conceptualized as a quasi-experiment with a treatment and a control group using ex post facto data (Shadish et al., 2002). During elementary school, some CS high school students (n = 65) participated in the ISSP (treatment) while other students (n = 37) attending the same elementary school at the same time did not participate (control). The ex post facto data comes from the survey administered to the high school students to assess whether the ISSP influenced their banking and savings behaviors.

Table 1 shows the separate percentages for the demographic and outcome variables of the ISSP and non-ISSP groups in the full sample (n = 102). The two groups appear to be quite similar as no statistically significant difference in the percentages were found in the z-test comparisons, except for whether a student was in the gifted program. As for the two outcome variables, highly statistically significant differences between the two groups are evident for having a bank account, and if the bank account was opened before high school.

The descriptive statistics from a more restricted sample (n = 85) also is presented in Table 1. One main outcome variable for the study was whether students had established a bank account after the end of elementary school (sixth grade). Some parents, however, had established bank accounts for their children prior to sixth grade. This restricted sample eliminates those 17 observations (10 in ISSP and 7 not in ISSP) as they already had bank accounts. The z-tests comparing the percentages differences for the ISSP and non-ISSP groups showed no statistically significant differences for any of the demographic variables. The results for the outcome variables are essentially the same as with the full sample. ISSP students relative to non-ISSP students are significantly more likely to have a bank account and have one before high school.

Both the full and restricted sample were used in the analysis, as there are trade-offs with each one. The case for the full sample is that it is almost 20 percent larger than the restricted sample, and the full sample is already small. Furthermore, the possible influence of having opened an account before the end of ISSP is muted as the percentage differences in treatment and control students (15.4 versus 18.9) is not statistically significant (z = 0.46). The case for using the restricted sample is that it eliminates any possible influence of having opened a bank account prior to the end of ISSP. Another advantage with the restricted sample is that there are no statistically significant differences between the ISSP and non-ISSP groups on any of the demographic variables. Overall, however, the sample differences are minor so the results from using either one for the analysis is expected to be about the same and using both samples can serve as robustness checks. 7

Hypotheses

Three hypotheses related to the ISSP were investigated using the longitudinal data. The first one was whether participation in the ISSP appeared to increase the number of students who had a bank account when they were in high school. The rationale for this hypothesis is that a primary purpose of the ISSP is to encourage students to be banked, so ISSP graduates would be expected to show a more positive association with this financial behavior than non-ISSP graduates.

The second hypothesis focused on when students opened a bank account. Students could have opened a bank account from the end of sixth grade (end of ISSP) until they were surveyed in high school (three to six years later). The second hypothesis was that participation in the ISSP is likely to influence opening a bank account in the years before attending high school (from the end of ISSP through eighth grade). One reason for this expected outcome is that in these pre-high school years the main message from ISSP about the importance of having a bank account and saving would still resonate with students and encourage them to start saving earlier rather than later in life. Another reason is that during high school many students have jobs and earn an income. For many of these students participating in the job market and having income to save is likely to be a more motivating factor for having a bank account than participation in the ISSP years ago.

The third hypothesis targets the regularity of saving that is emphasized in the ISSP. Having a bank account is a first step towards accumulating savings in the ISSP. The second step is to make regular contributions to savings. If ISSP participation is highly influential in opening a bank account, and having a bank account is important for encouraging regular savings, then by extension ISSP participation is likely to have significantly influenced regular savings. The way to test this third hypothesis, therefore, is to assess whether having a bank account affect saving regularly.

Model

Probit estimation is used for testing each hypothesis. The expected financial behavior that serves as the dependent variable in each estimation is dichotomous (1 = yes; 0 = no). The dependent variable for the first estimation is whether a student has a bank account in high school. The dependent variable for the second estimation is whether a student opened a bank account prior to high school. The dependent variable for the third hypothesis is whether a student reports saving regularly in high school.

The probit estimation is nonlinear with coefficients fitted with maximum likelihood using the function

The control variables for other student characteristics are dichotomous. They include gender (1 = female), qualifying for a free or reduced cost lunch (1 = yes), being in a gifted program (1 = yes), and having a job (1 = yes). For parsimony, the four variables for high school grades are reduced to one variable. It assesses whether the survey responses from high school students differed based on being in a lower grade (1 = grades 9 or 10) and being closer in years to elementary school, compared with being in a higher grade (1 = grades 11 or 12) and farther in years from elementary school.

Results

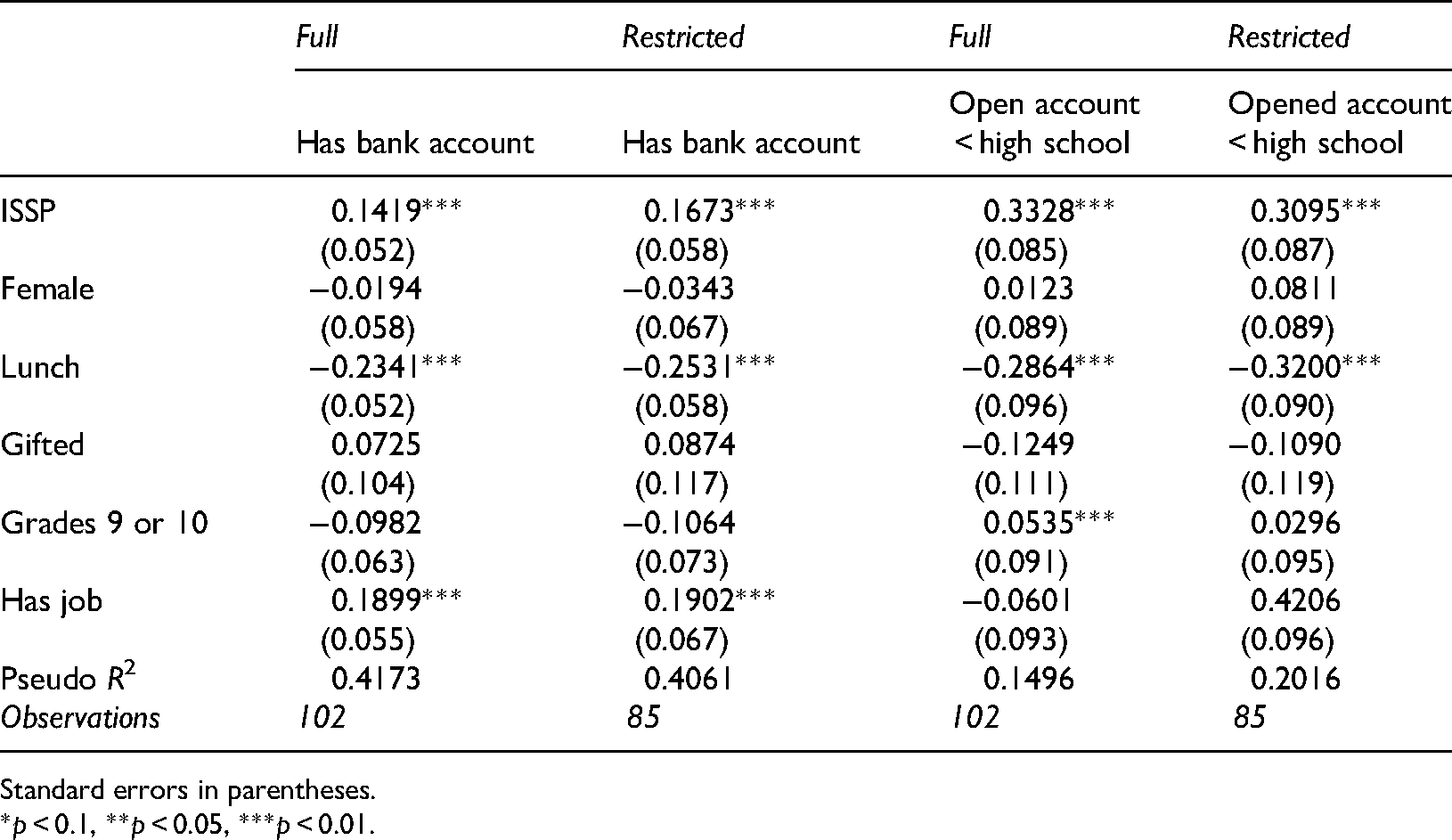

Table 2 reports the results from the probit analysis testing the first hypothesis that the ISSP influences whether a student has a bank account by the time they were surveyed in high school. The findings appear to confirm this hypothesis. The results show that ISSP graduates are significantly more likely to have a bank account, by 14.2 percentage points with the full sample and 16.7 percentage points with the restricted sample.

Probit marginal effects on bank account variables by sample (full or restricted).

Standard errors in parentheses.

*p < 0.1, **p < 0.05, ***p < 0.01.

As for the other variables in estimation, only two seem to affect the banking outcome. As expected, having a job in high school seems to be a major motivator for having a bank account. Students with a job have earned income and need a safe and convenient place to store their earnings and savings. Employers also may want their workers to have a bank account so they can transfer earnings electronically to an account. Whatever the reason, those students who have a job are 19 percentage points more likely to be banked in each sample than students without a job.

Household income appears to influence the results. Those students who qualify for a free or reduced cost lunch, an indicator of low household income, appear less likely to be banked by a sizable 23 to 25 percentage points depending on the sample. This income finding, however, is not surprising as students in low-income households might not see benefits from being banked if household savings are non-existent or if high fees reduce access to banking. Nevertheless, the finding is unsettling as it shows that poor financial practices related to banking begin at an early age and appear to be income-dependent.

Table 2 also reports the results for testing the second hypothesis that focuses on when students opened a bank account. The probit analysis shows that ISSP graduates were significantly more likely to have opened their bank account before high school. The differences are a sizable 33 percentage points more likely for students in the full sample and 31 percentage points for students in the restricted sample. This apparent ISSP effect is important as it indicates that the program encourages banking and saving at an earlier age. Early adoption of such sound financial behaviors can compound savings over time.

None of the other control variables appear to affect the results, except for the income indicator of whether a student qualifies for a free or reduced cost lunch. As was the case with the results the first hypothesis, and probably for the same reasons, the findings from the second hypothesis show that students with lower household incomes are less likely to open a bank account before high school (by 29 and 32 percentage points depending on the sample). This finding also is unsettling as it indicates how hard it can be to change financial behaviors across generations given differences in household income.

What also is noteworthy in the results is that although having a job in high school apparently increases the likelihood of having a bank account, it has no effect on opening an account before high school. This difference in the effect of a job on having bank account or when one is open is to be expected given the timing of when a student gets a job, which is typically during high school. The only factor, beyond the proxy for household income, that appear to influence having a bank account before high school is participation in the ISSP.

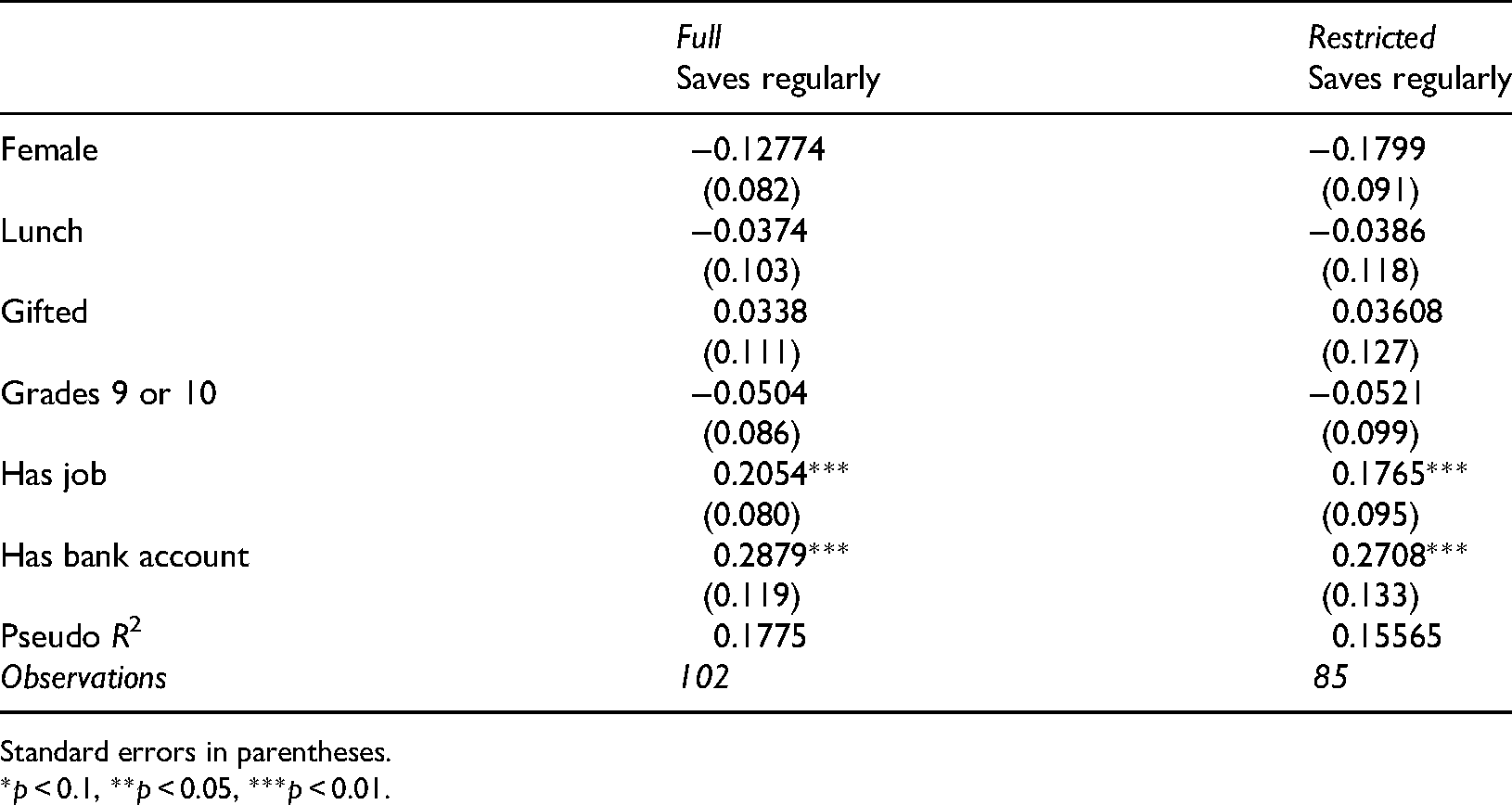

The results from the analysis of the third hypothesis are reported in Table 3. They show that students with a bank account are 27 to 29 percentage points more likely to save regularly compared with other students. Although not all high school students with bank accounts are ISSP graduates, the great majority in the probit analysis are: 70.5 percent in the full sample and 73.5 percent in the restricted sample. Consequently, this result suggests that ISSP participation influences saving regularly through its sizable effect on bank account formation. The only other variable that appears to affect whether high school students save regularly is whether they have a job (by 20 to 18 percentage points depending on the sample). The main reason that the job variable probably affects saving is that having a job generates income for saving. The other variables in the estimation provide no significant insights about why students save regularly.

Probit marginal effects on saving variable by sample.

Standard errors in parentheses.

*p < 0.1, **p < 0.05, ***p < 0.01.

Robustness checks and limitations

One potential concern with an ISSP is that the financial institution that partners with the school may have a promotion influence on where ISSP graduates eventually establish a bank account. 8 If this is the case, the partnering financial institution most likely would have a significantly greater percentage of accounts established at that institution by ISSP graduates compared with non-ISSP graduates. A positive outcome would provide evidence for criticizing an ISSP as mostly a promotional activity for the partnering financial institution rather than an experiential learning activity for elementary students.

An analysis of the available evidence sample does not support this criticism. The restricted sample of 85 students excludes students whose parents established bank accounts before the end of ISSP. Among the 55 ISSP graduates, the percentage distribution (number) establishing accounts was: 30.9 percent (17) at Bank1 (partnering institution); 45.5 percent (25) at Bank2; 14.5 percent (8) at other banks; and 9.1 percent (5) at none. Among the 30 non-ISSP graduates the respective percentages were: 30 percent (9) at Bank1; 16.6 percent (5) at Bank2; 13.3 percent (4) at other banks; and 40 percent (12) at none. The percentage of ISSP graduates and non-ISSP graduates who established accounts at Bank1 are essentially the same, which indicates that Bank1 receives no promotional benefit from ISSP in terms of increased accounts.

Several other robustness checks were conducted to assess whether the statistical relationships in the data hold with changes in variables. The estimation as reported in Tables 2 and 3 was conducted with non-linear probit analysis. A linear probability model (LPM) also could be used for the estimation. These LPM results (not reported for brevity) show that the difference in the results from non-linear or linear estimation are minimal. For example, with LPM estimation the results also show that participation in ISSP significantly increases the probability of being banked as did the non-linear probit estimation.

Furthermore, estimation with differences in sample size can be a robustness check. The results in Tables 2 and 3 show that increasing the sample size by 17 students (from 85 to 102), which is a 20 percent change, produces relatively minor changes in the effects of the key explanatory variable in Tables 2 and 3. For example, the marginal effect for ISSP participation on having a bank account is 14.2 percentage points with the full sample and 16.7 percentage points in the restricted sample.

Despite the positive findings for ISSPs from the study, it has three limitations that should be acknowledged. First, the survey data from high school students are self-reported. Although efforts were made to ensure reliable data were collected, the survey responses rely on the honesty and accuracy of students. Second, the study data are cross-sectional, which means that the reported statistical relationships are correlational and not causal. In recognition of this issue, the text often uses modifiers such as “likely” when describing “effects” or “influences,” Third, the sample size is small, as is the number of variables. These data limits, however, were due to the study’s location in a small, rural community, restrictions on survey length, and lack of student records during their elementary years. In general, these three limitations (self-reported data, correlational data, and limited data) are not unique to this study, as they are present in other research studies of financial education with children and youth (Amagir et al., 2018).

Discussion

Several implications are worth noting from the ISSP study findings. First, as suggested by Dewey (1938), experiences create an environment for learning by doing. He also recognized that such an environment is social and relies on communications among the participants. The ISSP offered students an opportunity to learn about banking and saving by doing and through a social and communicative experience within their school. The participatory environment of the ISSP probably helped the students become more interested in and more willing to establish their own bank account by the time they are high school students. Such a stimulus may be nearly as influential as having a job and earning an income, which is a prime reason high school students establish a bank account.

Second, it is logical that learning about banking and saving at an early age should increase the opening of a bank account at an earlier age, and the evidence from the study indicates that it does. This outcome is especially important as it means that students who open a bank account earlier in life (before high school) are more likely to start saving earlier in life. Learning to save earlier in life has the potential to benefit a financial future and help people achieve financial goals sooner.

Third, the importance of having a bank account should be viewed as more than a place to accumulate savings. Establishing a bank account should be viewed as a first step towards saving regularly. Obviously having a high school job helps too as it provides an income to be saved, but it is not the only explanation for saving regularly. High school students who report having a bank account are more likely to also report saving regularly, perhaps because they know they have an alternative to spending and know what to do with excess funds or income they do not spend.

A further point focuses on future research. The study was conducted with a small and homogeneous sample of students in a rural Midwestern school in the United States. Whether these ISSP results are similar when such research is conducted in schools with diverse student populations, in urban areas, or in other regional locations is not known. Given the widespread popularity of ISSPs in elementary schools in the United States, however, it seems reasonable to think that the findings would generalize to ISSPs in other locations and with more diverse student populations. Nevertheless, more research is called for on the effectiveness of these savings programs with other schools, student samples, and locations to substantiate such claims.

What also merits more research is how parental involvement influences saving behavior. In this study, for example, 17 percent of students had parents who established a bank account while the students were in elementary school and before the end of ISSP. Whether that percentage is representative for students from other cultural, racial, or ethnic backgrounds is unknown. More generally, further study should be devoted to understanding how parental involvement affects savings behavior in other ways than opening a savings account for students.

Conclusion

In-school savings programs (ISSPs) in U.S. elementary schools are popular experiential learning activities to help students participate in banking and saving. In these “hands-on” programs, a financial institution (bank or credit union) establishes a branch within a school. Students who participate in the ISSP can deposit their own money into a savings account under the supervision of the representative from the financial institution. At the end of elementary school students receive the accumulated funds from their years of participation in the ISSP. They are then encouraged to establish a bank account at a financial institution of their choice and continue saving.

This study fills a research gap by assessing the long-term effectiveness of ISSPs in influencing financial behavior. The assessment was setup as a quasi-experiment with a treatment group who participated in the ISSP while attending elementary school and a control group who did not participate in the ISSP. Both groups attended the same elementary school at the same time and are now attending the same high school. The results showed that ISSP participants compared with non-participants were more likely to be banked in high school than non-participants. They also were more likely to have opened their bank account before attending high school. Additional analysis reveals that high school students with a bank account are more likely to save regularly, which means the ISSP appears to contribute indirectly to saving regularly in high school through its direct influence on having a bank account and opening it before attending high school.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.