Abstract

Despite ample evidence that curiosity plays a significant role in information-seeking, we know little about the influence of Chief Executive Officer curiosity on strategic decisions. Building on established psychology research, we distinguish between two central curiosity types: interest-type curiosity—the joyful pursuit of novel information, and deprivation-type curiosity—the urge to address and close information gaps. We hypothesize that Chief Executive Officer I-type curiosity is positively associated with strategic change, while Chief Executive Officer D-type curiosity is negatively related to it. Since Chief Executive Officer curiosity entails a social aspect, it influences how a Chief Executive Officer acquires information from top management team members. We therefore examine the moderating role of top management team size and change. Applying a novel text measure for Chief Executive Officer curiosity types to S&P 500 firms, we find that the Chief Executive Officer D-type curiosity relates negatively to strategic change, while Chief Executive Officer I-type curiosity does not relate to it significantly. Larger top management teams seem to alleviate Chief Executive Officer D-type curiosity’s negative effect, while top management team changes appear to strengthen Chief Executive Officer I-type curiosity’s positive impact. This study contributes to upper echelons research by providing first insights into Chief Executive Officer curiosity’s multifaceted dimensions and their differential effect on change.

Introduction

Companies are increasingly emphasizing curiosity as a central future leadership trait. Curiosity represents individuals’ drive to seek out, explore, and immerse themselves in situations with the potential for new information or experiences (Kashdan et al., 2020b; Spielberger and Starr, 1994). In its “State of Curiosity Report” the German multinational company Merck, for instance, describes curiosity as essential for thriving in uncertain times: “With the emergence of disruptive technologies—artificial intelligence, big data—the future is ambiguous, but curiosity will ensure organizations can thrive amid change” (Merck, 2018: 15). Similarly, well-known Chief Executive Officers (CEOs), such as Bill Gates, Satya Nadella, and Michael Dell, have emphasized the pivotal role curiosity plays in corporate leadership (Mikel, 2019).

While curiosity research has a long history (Berlyne, 1954; James, 1890), recent research has specifically highlighted its role in the workplace (Kashdan, Goodman, et al., 2020). Individual curiosity, which plays a central role in driving information-seeking behavior (Lievens et al., 2022; Litman, 2019), is important for CEOs as they engage in strategic analysis and decision-making (Samimi et al., 2022). Extant management literature has studied the role of curiosity in socialization processes (Harrison et al., 2011) and how it influences feedback on creative work (Harrison and Dossinger, 2017) and innovation (Liu et al., 2023). To date, most of this research has focused on the role employee curiosity plays (Thompson and Klotz, 2022), while only recently scholars have started to study CEO curiosity as a top executive trait (Liu et al., 2023).

Interestingly, and following practitioners’ suggestions (Ready, 2019), recent research has predominantly highlighted the positive aspects of curiosity as an aggregate personality trait (Liu et al., 2023; Thompson and Klotz, 2022). While this research improves our understanding of curiosity in organizations, it does not consider established psychology research which defines curiosity as a multifaceted personality trait with sub-dimensions that have different implications for individuals’ actions (Jach et al., 2022; Litman, 2005). Specifically, psychology research identified two central types of curiosity, distinguished as interest (I-type curiosity) and deprivation (D-type curiosity) (Litman, 2008; Ryakhovskaya et al., 2022), which are related to different information-seeking processes and behaviors (Lievens et al., 2022). I-type curiosity is defined as the joyful pursuit of novel information and experiences (Kashdan et al., 2020b; Litman, 2008), whereas D-type curiosity is characterized as an internal drive to address and close information gaps (Litman, 2010). In this sense, I-type curiosity represents the common interpretation of curiosity as the excitement of looking for and exploring new information and learning opportunities (Litman, 2008; Harrison and Dossinger, 2017). An example is Larry Page, co-founder and former CEO of Google. From a young age, Page was fascinated by technology and aimed to be an inventor, which led him to pursue projects that pushed technological boundaries (Google Zeitgeist, 2011). His curiosity is evident in his approach to leadership, where he encourages exploring unconventional solutions (Google Zeitgeist, 2013). Page’s interest in diverse fields, including renewable energy and autonomous vehicles, demonstrates his broad inquisitiveness and his interest in crossing knowledge domains. Individuals with D-type curiosity are bothered by having insufficient information and want to close this information gap (Kashdan et al., 2018; Loewenstein, 1994). An example is Louis V. Gerstner Jr., the former CEO of IBM. Upon his arrival at IBM, Gerstner encountered an organization on the brink of collapse (Gerstner, 2002). Driven by a need to understand the root causes of the company’s challenges, Gerstner collected information from different stakeholders. He directly engaged with key customers to collect information on key problems, ultimately cutting prices on the company’s core product to maintain competitiveness. Gerstner emphasized the importance of execution over vision. Importantly, he decided to keep IBM intact instead of splitting it up into different units and, instead, immersed himself in the company’s operations to cut expenses and raise cash (Pratch, 2021).

Research on both curiosity types has explained the nomological network around them by demonstrating how they differ from higher-order personality traits, self-regulatory strategies, and expressions of affectivity (Litman, 2019). In contrast to higher-order traits, curiosity is a specific personality trait that explains behavior more directly (Harrison and Dossinger, 2017; Heinemann et al., 2022). Psychology and neuroscience research has advanced our understanding of the implications of I-type and D-type curiosity on information-seeking and behavior in general (Ryakhovskaya et al., 2022; Smillie et al., 2021). However, we have limited knowledge of how the two curiosity types affect strategic decisions (Ma, 2023). Due to the curiosity types’ different behavioral implications, a closer investigation is required into their effects at the CEO level.

Following psychology research, we challenge the predominant positive view of curiosity in organizations and study its multifaceted dimensions and implications. We argue that differentiating between CEO I-type and D-type curiosity is particularly influential in the context of strategic change, where how CEOs search for, interpret, and act on new information is crucial (Herrmann and Nadkarni, 2014). Since CEOs’ strategic decisions have fundamental implications for an organization, an improved understanding of how the respective CEO curiosity type influences strategic change is important. We hypothesize that CEO I-type curiosity is associated with increases in strategic change, while CEO D-type curiosity is associated with decreases in change. In addition, we build on research that emphasizes the social aspect of curiosity (Kashdan et al., 2020a), specifically in the context of team processes (Ma, 2023). CEO curiosity likely influences how a CEO acquires information from other members on the top management team (TMT). By examining the moderating role of TMT size and TMT change, we address how curious CEOs interact with the amount and the novelty of the information in their immediate social environment.

To test our hypothesis, we use a sample of 757 S&P 500 firms from 2002 to 2019. We develop and validate a novel dictionary-based text measure of CEO I/D-type curiosity, using a corpus of approximately 40,000 earnings call transcripts. Findings show CEO D-type curiosity to be associated with less strategic change. Counter to expectations, we find CEO I-type curiosity not to be significantly associated with more strategic change. In addition, larger TMTs tend to mitigate CEO D-type curiosity’s negative effect on strategic change. In contrast, TMT change predominantly affects CEO I-type curiosity and strengthens its association with strategic change.

Our study contributes to upper echelons research by introducing CEO curiosity’s multifaceted nature and demonstrating its distinct impact on strategic change. While recent research highlights CEO curiosity’s positive effects on strategic actions (Liu et al., 2023), we unveil the diametrically opposed and partially counter-intuitive influence of CEO I-type and D-type curiosity on strategic change. Specifically, CEO D-type curiosity, rather than I-type curiosity, influences strategic change relative to the industry. While recent upper echelons research has studied higher-order traits’ effects (Harrison et al., 2020), a current debate in personality psychology advocates ensuring the predictor’s correct level of specificity (Speer et al., 2022) when studying personality traits’ organizational implications (Heinemann et al., 2022; Seeboth and Mõttus, 2018). Our findings underscore the importance of distinguishing between CEO I-type and D-type curiosity, rather than studying CEO curiosity as an aggregate personality construct, to more accurately understand its influence. A more nuanced conceptualization and operationalization of CEO curiosity enhance our understanding of how different curiosity types impact strategic decisions, thereby laying the foundation for future research on specific executive personality traits.

In addition, our study contributes to upper echelons research by showing that CEO curiosity types’ effect on strategic change depends on the TMT context, since I-type and D-type curious CEOs seek and integrate information differently from their TMT. TMT size, which reflects how much information and expertise a CEO can access (Wiersema and Bantel, 1992), moderates the relationship between CEO D-type curiosity and strategic change. Larger TMTs may challenge D-type curious CEOs, potentially disrupting their problem-solving focus due to the difficulties they experience with reconciling the TMT’s different opinions. Conversely, TMT changes, which introduce novel perspectives and information (Boeker, 1997a), influence the relationship between CEO I-type curiosity and strategic change. I-type curious CEOs benefit from different perspectives in a changing TMT, as they are adept at leveraging different views when strategizing. Our findings deepen the understanding of the social side of curiosity and lay the foundation for research on the interplay between CEO personality traits and the TMT context. Specifically, we advance research on the CEO-TMT interface (Georgakakis et al., 2022) by emphasizing the critical role of specific executive personality traits and the TMT context.

Finally, our study extends research on curiosity in organizations, which has predominantly focused on employees (e.g. Kashdan et al., 2020b), by offering insights into I/D-type curiosity’s effects at the CEO level in the context of strategic decision-making. While existing research has frequently proposed employee curiosity as an antecedent to creativity and innovation (Celik et al., 2016; Lievens et al., 2022), our findings suggest that, at the CEO level, curiosity has differential effects on change, depending on the type of curiosity studied. Future research can build on our insights to study how different types of employee curiosity influence change across hierarchical levels.

Theoretical background

Individual curiosity

Curiosity is often described as the urge to search for new information and experiences, and as such, plays a distinct role in human behavior and development (Kashdan et al., 2018). Research predominantly treats curiosity as a relatively stable trait that is able to indicate the corresponding state’s tendencies (Jach et al., 2022; Kashdan et al., 2020b). 1 Different scientific fields, such as psychology (Spielberger and Starr, 1994) and neuroscience (Kidd and Hayden, 2015), have paid a great deal of attention to curiosity. Over the past decade, management scholars have begun more in-depth investigations into curiosity. Harrison and Dossinger (2017), for instance, showed that trait curiosity leads feedback seekers to ask more open questions, which enhances the amount of feedback they receive. More curious individuals also exhibit greater willingness to revise their product ideas in response to ambivalent feedback. Furthermore, curiosity can lead to creativity via idea linking, that is, using earlier ideas as stepping stones to later ones (Hagtvedt et al., 2019). Nevertheless, a recent review (Lievens et al., 2022) emphasized the limited knowledge we have of the role curiosity plays on the executive level.

In psychology, curiosity research’s history goes back to James (1890), but gained increasing attention after the publication of Berlyne’s (1954) studies on epistemic curiosity and its pivotal role for knowledge attainment and therefore learning. Over the following decades, psychology research considered epistemic curiosity as either a positive affective experience (Spielberger and Starr, 1994), illustrated by the joy of learning new information, or as the unpleasant feeling of lacking certain information (Loewenstein, 1994). This reflected two different and, to a certain degree, contradictory theoretical lenses (Litman, 2019). One lens describes people as searching for optimal levels of arousal who, consequently, are curious about new information (Litman, 2005), while the other perceives curiosity as a drive endeavoring to fill an information gap (Loewenstein, 1994).

Litman’s (2008) I/D model resolved this conflict. I-type curiosity describes the excitement of looking for and exploring new information and experiences, therefore representing a feeling of interest (Kashdan et al., 2018; Litman, 2005). D-type curiosity represents the frustration of not knowing something and wanting to close this information gap (Kashdan et al., 2018; Loewenstein, 1994). While I-type curiosity is a more common, intuitive description of curiosity, D-type curiosity is an important driver of information-seeking and essential for comprehensively understanding curiosity. 2 The psychometric approach of Litman’s (2008) I/D model suggests that curiosity can be both—I-type and D-type—but that the two types of curiosity are activated differently. It is important to differentiate between I-type and D-type curiosity since they correspond to fundamentally different motives for acquiring new information (Hardy et al., 2017; Litman, 2008; Litman and Jimerson, 2004). Consequently, as Lievens et al. (2022: 184) suggest, the “subjective differences between I-type and D-type curiosity experiences manifest in very different learning outcomes, information-seeking activities, and behavioral patterns.” While the two curiosity types correlate (Litman, 2010; Ryakhovskaya et al., 2022), it is important to investigate both to examine how their subjective differences influence particular outcomes.

The I/D-type curiosity traits have become contemporary curiosity research’s central building blocks and have been shown to be stable over time (Kashdan et al., 2020b; Ryakhovskaya et al., 2022). It is important to distinguish between I/D-type curiosity and higher-order traits. Within the hierarchical structure of personality traits, researchers find that I-type curiosity is associated with openness to experience, while D-type curiosity is linked to conscientiousness (Kashdan et al., 2018; Lievens et al., 2022; Litman, 2019). However, in comparison to higher-order traits, curiosity is a narrower concept, directed more agentically and proactively toward action, therefore having a stronger motivational aspect (Harrison and Dossinger, 2017). Openness to experience is frequently mistaken for curiosity, but Mussel (2013) showed that, when analyzing work performance, curiosity has additional predictive value when compared to openness to experience. Similarly, Heinemann et al. (2022) found that curiosity has a stronger influence on entrepreneurial outcomes. Moreover, Jach and Smillie (2020) show that trait curiosity predicts information-seeking, while openness/intellect does not. Overall, research has shown that openness resembles a heterogeneous higher-order trait that only touches on the curiosity concept (Kashdan et al., 2018), making curiosity a more informative construct.

Curiosity seems pivotal in the context of CEOs, because it relates not only to how individuals do their work, but also to how they manage their work and lead others (Harrison, 2012). Thompson and Klotz (2022) find that leaders’ display of curiosity increases their employees’ psychological safety and encourages them to speak out. However, curiosity is also strongly directed toward individual action and influences decision-making, particularly in novel, uncertain, and complex situations (Kashdan et al., 2018). Curiosity might also have a destabilizing function in organizations (Lievens et al., 2022), because CEOs question the underlying assumptions regarding their company’s strategy when preparing for future change. However, to our knowledge, no study has investigated the effects of CEO I/D-type curiosity on strategic decisions.

CEO personality and strategic change

In the light of CEOs’ increasing influence on company outcomes (Quigley et al., 2017), research supports the importance of executives’ self-concepts and how they manifest themselves in firms’ strategic initiatives (Herrmann and Nadkarni, 2014). In an attempt to open the black box of executives’ personalities, research has examined CEO personality in terms of the five-factor model (Harrison et al., 2019; Nadkarni and Herrmann, 2010) or addressed specific traits, such as CEO charisma and humility (Petrenko et al., 2019; Wowak et al., 2016). Studies show how CEO personality, measured using the five-factor model, affects firm performance and how a company’s strategic flexibility mediates this relationship (Nadkarni and Herrmann, 2010). While broader personality models (e.g. the Big Five) help accumulate research findings within a common framework, they might not always be the most adequate approach for studying specific decisions (Mõttus et al., 2020). Others have therefore started to examine specific personality traits. For instance, Petrenko et al. (2019) show that humble CEOs are associated with better market performance due to an expectation discount in the market.

Research on different CEO personality traits that influence strategic change (Harrison et al., 2019) highlights the role of information-seeking and processing capabilities (Herrmann and Nadkarni, 2014). Curiosity helps individuals navigate uncertainty (Kashdan et al., 2018). It leads to information-seeking, specifically the search for new information and the encoding of information (Jach and Smillie, 2020). This could be particularly important for strategic change, which helps organizations adapt to their environment by reallocating resources (Hofer and Schendel, 1978). Despite established research on the I/D model of curiosity, we lack clarity on how the different curiosity types play out at the CEO level, ultimately influencing strategic change.

Hypotheses development

Upper echelons theory’s fundamental premise is that executives view information, events, and options through personalized lenses (Hambrick, 2007; Hambrick and Mason, 1984). CEOs’ personality and cognition influence how they search for information, and how they interpret and respond to internal and external events (Chatterjee and Hambrick, 2007; Nadkarni and Herrmann, 2010). Lievens et al.’s (2022: 185) definition of curiosity highlights its significance for CEOs’ information search; it summarizes curiosity as a “desire to know, activated by collative variables such as novelty, ambiguity, or complexity, that motivates rewarding exploratory behavior to learn and fill pressing knowledge gaps.” This description includes the I/D-type distinction, which is central to our understanding of curiosity’s dimensionality in the organizational context. We argue that CEO I/D-type curiosity exerts a profound influence on CEOs’ information-seeking behavior, thereby impacting strategic change.

Individuals with high levels of I-type curiosity are strongly inclined to seek new information (Litman, 2008; Ryakhovskaya et al., 2022). In their desire to know, these individuals search for completely new learning opportunities and like crossing knowledge domains (Harrison and Dossinger, 2017), resulting in a wide information-seeking scope and novel ways of perceiving situations that form the basis of idea generation (Hardy et al., 2017; Harrison et al., 2011). CEOs with high levels of I-type curiosity have a strong urge to seek new information and are excited by the idea of exploring and generating new strategic ideas (e.g. Litman, 2019). Strategic change is complex and often ambiguous, therefore requiring collecting broad information from multiple sources to assess different strategic options in light of the firm’s internal and external environment, to evaluate constraints and opportunities, and to act on them (Tushman and Romanelli, 1985). We anticipate that CEOs with I-type curiosity will adopt an active approach when seeking diverse information on novel strategic opportunities and potential threats. Such CEOs likely pay more attention to novel opportunities and trends in the firm’s environment, developing a more comprehensive understanding of strategic change opportunities. Overall, CEO I-type curiosity likely exhibits the experimentation and action-oriented behavior required to set up strategic change initiatives (e.g. Herrmann and Nadkarni, 2014).

In addition, I-type curiosity is related to greater risk-taking and to positive appraisals of uncertain situations (Litman, 2019). Research shows that the “status quo bias” (Hambrick et al., 1993) can imply risk aversion and leads to organizational inertia. Specifically, a CEO’s commitment to the status quo has been identified as a barrier to strategic change (Chiu et al., 2022). CEOs with I-type curiosity have a higher tolerance of ambiguity (e.g. Litman, 2008) and are therefore more inclined to question the organization’s status quo. Consequently, they are more receptive to new initiatives, likely positively influencing on strategic change.

Hypothesis 1 (H1). CEO I-type curiosity is positively associated with strategic change.

Conversely, deprivation-type curiosity describes the search for knowledge motivated by a desire to reduce uncertainty (Litman, 2008). Ryakhovskaya et al. (2022) show that D-type curiosity predicts a feeling of being bothered and frustrated by having insufficient information. A knowledge gap often activates this feeling and triggers information-seeking in order to address and resolve it (Litman, 2019). D-type curiosity CEOs have a stronger problem-solving focus and concentrate on refining existing problems rather than initiating change (e.g. Ma, 2023). In addition, this type of curiosity could cause CEOs to become overly concerned about their actions’ negative consequences, due to their incomplete or inadequate knowledge (e.g. Lauriola et al., 2015), which interferes with the risk-taking attitude required for strategic change.

To initiate change, CEOs have to question and update their beliefs about the current strategy (Zhu et al., 2020). D-type individuals are usually highly receptive to new information, but they are, nevertheless, more reluctant to adapt their underlying beliefs (Zedelius et al., 2022). Since D-type curiosity relates to thoughtfulness (Lauriola et al., 2015), it emphasizes caution when making strategic decisions, which hinders CEOs from adapting their beliefs.

Hypothesis 2 (H2). CEO D-type curiosity is negatively associated with strategic change.

Curiosity also entails a social aspect (Kashdan et al., 2020a), which seems particularly influential in the context of team processes (Ma, 2023). This is important since CEOs acquire information from other TMT members. Prior research suggests that CEOs’ strategic change decisions are better understood in light of the TMT’s composition (Barron et al., 2011). Specifically, TMT size and change are important predictors of TMT processes (Herrmann and Nadkarni, 2014). While TMT size reflects the amount of information and expertise available to a curious CEO (Wiersema and Bantel, 1992), TMT changes indicate an influx of new perspectives and information (Boeker, 1997a). As potential connection points in teams, curious CEOs listen to TMT members’ suggestions and invite them to collaborate (e.g. Kashdan et al., 2020a). Therefore, TMT size and change are likely important moderators, indicating the amount and degree of novel information available in the CEO’s immediate social environment.

A key benefit of large TMTs is that they enhance CEOs’ access to information and the available information-processing capacity (Certo et al., 2006). They represent an extensive knowledge pool with options that could ensure a better strategic alignment with the environment (Wiersema and Bantel, 1992). We argue that I-type curious CEOs, who actively search for novel ideas and learning opportunities (e.g. Litman, 2010), likely embrace larger TMTs’ ideas and expertise. Such larger TMTs provide opportunities to explore new strategic ideas that the CEO might not previously have thought about or that could complement the CEO’s change ideas.

However, larger teams can also inhibit effective decision-making (Amason and Sapienza, 1997). Generally, large teams’ collaboration faces challenges due to interpersonal conflict and different opinions and viewpoints. Research suggests that information exchange deteriorates in larger teams, due to difficulties in consolidating different perspectives efficiently (Simsek et al., 2005). Yet, I-type curious CEOs are more likely to appreciate the larger number of TMT members’ different perspectives, because such CEOs are more open-minded and ready to adopt and accept other people’s perspectives (e.g. Kashdan et al., 2020a). Ultimately, I-type curiosity CEOs’ openness to others’ ideas, combined with their thirst for knowledge, may leverage the expertise within a larger TMT—an advantageous action regarding disrupting and reconfiguring the organization’s established patterns (Boeker, 1997b; Wiersema and Bantel, 1992).

Hypothesis 3a (H3a). A larger TMT size strengthens the positive association between CEO I-type curiosity and strategic change.

The desire of individuals with D-type curiosity to close an information gap (Litman, 2008; Loewenstein, 1994) influences how CEOs work with their TMT. Ma (2023) shows that supervisors high on D-type curiosity described that which is unknown as a frustrating problem that needs to be solved. Consequently, such supervisors focus their teams’ efforts on refining existing problems instead of making organizational changes. Considering D-type CEOs’ persistence in seeking answers (e.g. Litman, 2010), they are likely to utilize large TMTs’ increased information-processing capacity to solve specific problems.

However, a large TMT carries challenges, such as managing the different TMT members’ conflicting opinions (Amason and Sapienza, 1997). In small teams, decision-making is more efficient due to lower coordination costs. and D-type curiosity CEOs can instruct the TMT to focus on current problems and seek concrete answers. Conversely, large teams could confront D-type CEOs with many ideas that might diverge from their current problem-solving path. These viewpoints might, however, represent an opportunity for organizational adaptation (Boeker, 1997b), even though they potentially contradict the CEO’s current plan. However, if information exchange deteriorates in larger TMTs and the team members become averse to participating in joint decision-making (Simsek et al., 2005), D-type curiosity CEOs might struggle to maintain the originally charted problem-solving course. When the TMT’s size increases, its members are likely to challenge the existing problem-solving focus of a CEO with D-type curiosity and suggest a broader array of ideas for change.

Hypothesis 3b (H3b). A larger TMT size weakens the negative association between CEO D-type curiosity and strategic change.

In addition to TMT size, TMT changes could be highly influential regarding firms’ strategic adaptations (Hambrick, 2007). The extent of TMT changes is important for curious CEOs, since new TMT members come with different perspectives, which give such CEOs the opportunity to access new information (Boeker, 1997a). At the same time, team changes can reduce team collaboration and cohesion, thereby affecting the TMT’s general decision-making (Li and Van Knippenberg, 2021).

We suggest that more TMT changes could be favorable for I-type curiosity CEOs. New TMT members’ can have different attention foci, leading to distinct environmental scanning processes (Cho and Hambrick, 2006), which could yield new strategic options. These different attention foci can yield problems new to the CEO. I-type curiosity CEOs tend to perceive such problems as new puzzles with which they like to engage. These CEOs also enjoy learning from others (Litman, 2010); consequently, changing TMT members presents an opportunity to broaden their horizon and tap into new knowledge. In general, such CEOs are open to adopting other people’s perspectives (e.g. Kashdan et al., 2020b), thereby appreciating and probably engaging more with the new ideas that the new team members contribute to the TMT.

Still, when TMT members join or leave, I-type curiosity CEOs face the challenge of forming a functioning team. Developing “sharedness” in the TMT, that is, establishing a common understanding of their tasks and experiences (Li and Van Knippenberg, 2021), is fundamental for effective decision-making between the CEO and the TMT (Simsek et al., 2005). We suggest that I-type curiosity CEOs’ openness and their genuine interest in others foster relationship building in the TMT (e.g. Lievens et al., 2022), which can support the integration of new TMT members. We therefore suggest that I-type curiosity CEOs are better equipped to re-establish TMT cohesion in the context of TMT changes and to gain access to a range of novel strategic ideas that provide them additional impetus to make strategic changes.

Hypothesis 4a (H4a). More TMT changes strengthen the positive association between CEO I-type curiosity and strategic change.

In contrast, D-type curiosity CEOs might have a different perspective of and approach toward the TMT changes. Introducing novel experiences and exposing CEOs to diverse stimuli via new TMT members (Boeker, 1997a) could be beneficial to those with D-type curiosity if the information influx aligns with their problem-focused orientation. D-type curiosity individuals are open to others’ perspectives, with a focus on uncertainty reduction. However, they could be reluctant to adapt their belief set and abandon their current problem focus (Zedelius et al., 2022). Consequently, CEOs with D-type curiosity might benefit from some TMT change if this leads to uncertainty reduction, which is one of their core motivations (e.g. Litman and Silvia, 2006).

However, when the TMT change increases, D-type curious CEOs could find it more difficult to maintain alignment between the problem focus and the novel experiences new TMT members contribute. Increasing TMT changes could the TMT’s social cohesion (Simsek et al., 2005), to the extent that these CEOs can struggle to align the TMT with their problem-focused trajectory. While some TMT members probably support the CEO’s current problem focus, increasing TMT change increases the likelihood of TMT disagreement (Li and Van Knippenberg, 2021). New TMT members might challenge and mitigate D-type curiosity CEOs’ problem focus and could push for a more strategic change (Wiersema and Bantel, 1993). Hence, with more TMT change, the D-type CEOs’ problem focus is likely to be increasingly questioned, which will weaken the negative relationship between CEO D-type curiosity and strategic change.

Hypothesis 4b (H4b). More TMT changes weaken the negative association between CEO D-type curiosity and strategic change.

Methods

Sample and data

We tested our hypotheses with a sample of S&P 500 firms covering the years from 2002 until 2019. We focused on the Q&A sections of published quarterly conference calls to analysts in order to measure CEOs’ I/D-type curiosity, because they have a more natural and spontaneous text style and structure (Nadkarni et al., 2016). Recent research on CEO personality examined CEOs of S&P 500 companies, showing the validity of text-based personality measures in this context (Harrison et al., 2019).

We collected conference call transcripts from the Lexis-Nexis database and used all quotes of every CEO in our sample from the Q&A section of conference calls across the identified period. A sensitivity analysis showed that CEOs had to speak at least 150 words across the available conference call transcripts to allow robust curiosity scores. We therefore dropped observations with fewer than 150 words. Companies’ financial and industry-level data were collected from COMPUSTAT. Data on CEOs, TMT demographics, and boards were collected from Capital IQ, BoardEx, and Execucomp. After excluding observations with missing data, our final sample consisted of 7871 firm-year observations.

Independent and dependent variables

Development of a dictionary for CEO I/D-type curiosity

To measure executive personality constructs in text researchers often use validated dictionaries (Short et al., 2010). Research on strategic leadership and executive personality frequently utilizes established dictionaries from the LIWC software (e.g. Graf-Vlachy et al., 2020). Nevertheless, some authors have also developed their own dictionaries (Gamache et al., 2015). We developed a dictionary comprising two sub-dimensions of curiosity, which represent the I/D-type distinction. We combined a deductive and inductive approach (Short et al., 2010) and used natural language processing (NLP) techniques to facilitate the process, relying on the Python packages gensim, NLTK, spacy, and textacy.

First, we conducted a literature review of curiosity and collected more than 30 definitions used in different fields, such as neuroscience, psychology, and management. Lievens et al.’s (2022) definition became our reference point, as it builds on and synthesizes existing research streams. Specifically, it addresses the I/D-type distinction, which is central to our understanding of curiosity’s dimensionality in the organizational context.

Second, we started creating a word list for each sub-dimension by following an iterative deductive-inductive process. In the deductive part, we identified words based on the definition and scale items representing them. Based on this first word list (one for each dimension), we collected synonyms using two approaches: We looked up words in “Rodale’s Synonym Finder,” which is commonly done in the literature (e.g. Short et al., 2010). However, we also utilized NTLK’s wordnet library 3 to collect additional synonyms. Throughout this procedure, the research team discussed all words they found and eliminated false positives.

Our target corpus for measuring curiosity in organizations was a collection of earnings call transcripts (approx. 40,000) from S&P 500 firms between 2002 and 2019. We utilized only the unscripted Q&A sections, which describe the CEO and non-CEO texts. In this context, CEOs are pivotal figures who, therefore, are regularly present (Harrison et al., 2019). This enabled the collection of a significant amount of text per person over a longer time period.

We trained a Word2Vec embedding based on the corpus of our earning calls by means of Python’s gensim library

4

and used the “most

The inductive approach based on Short et al. (2010) advocates investigating the target corpus to identify context-specific words that represent the construct of interest. We first carried out several “cleaning” steps. We lowercased tokens and removed the punctuation, stop words, contractions, and non-alphabetical tokens. The resulting words were ordered according to their frequencies, based on the assumption that rare words would not affect our measurement strongly. This step is consistent with the general LIWC procedure (Boyd et al., 2022) which removes words that hardly ever appear. Next, we used a “knee”-detection algorithm (Satopää et al., 2011) to identify the optimal cutoff point for this list, which yielded a total number of 284 words.

Validation of the dictionary for CEO I/D-type curiosity

Many dictionary validation procedures rely on expert raters or judges (e.g. Gamache et al., 2015), as the LIWC documentation advocates (Boyd et al., 2022). While this approach has benefits, van Atteveldt et al. (2021) point out that there are also shortcomings in terms of replicability and transparency. They suggest crowd-coding platforms as an alternative because they allow researchers to replicate findings. Prolific, a scientific research crowd work site, is regarded as one of the platforms with the highest data quality (Peer et al., 2022). Considering the good results of our pretests, we decided to use the platform to validate our word lists.

We divided our word lists for I-type and D-type curiosity into blocks of 50 words containing both deductive and inductive words. We recruited a gender-balanced sample on Prolific, with the only prescreening criterion being that English had to be the participants’ first language. Each participant had to agree to provide informed consent, to undergo training in one of the sub-dimensions, and then to rate 50 words. The training comprised definitions, exemplary words, and a test rating. The participants had to make a yes/no decision regarding each word in terms of whether it reflected a particular sub-dimension of curiosity. The quality controls included a CAPTCHA test, answering an open-ended question, and correctly choosing a high- and low-signal word (Aguinis et al., 2021). Three persons rated each word independently. In total, 65 people participated; eight respondents were rejected for failing the quality controls. We paid all the participants regardless of their performance (pay rate: £1.25 for 10 minutes + £0.20 bonus). In line with previous publications (e.g. McKenny et al., 2013), we used majority voting to select our final list (e.g. if two of three raters agreed that a word reflects a construct, it was selected for the final word list). Interrater reliability scores show an average pairwise percent agreement of 79.02% for I-type curiosity and 74.98% for D-type curiosity, which are above the commonly accepted threshold guidelines (Short et al., 2010). Cohen’s Kappa for I-type and D-type curiosity was 0.56 and 0.49, respectively.

In a second validation step, we assessed, via LIWC-22’s new workbench functionality, the internal consistency of the two word lists in our target corpus of CEOs’ Q&A sections. The results show Cronbach’s alpha values of 0.48 for I-type curiosity and 0.59 for D-type curiosity. Both values are well above the 0.26 of the LIWC curiosity category, but this metric stems from the “Test Kitchen” corpus, which is more diverse than our CEO Q&A corpus. The Kuder-Richardson Formula 20 values, a less conservative measure of internal consistency (Boyd et al., 2022), are 0.93 and 0.95 respectively.

We measured I/D-type curiosity by loading our custom dictionaries into the LIWC-22 software. Drawing on a conceptualization of curiosity as a stable trait, we merged all Q&A segments from the conference calls for every CEO in our sample over the specified time period into a single text document. We derived the final I/D-type curiosity scores for each CEO from the LIWC analysis, which quantified the percentage of dictionary words present in these documents.

The correlation between curiosity’s two sub-dimensions was 0.6, that is, moderate to high (Jach et al., 2022; Litman, 2010), which corresponds with the conceptual expectations (Jach et al., 2022; Litman, 2010).

Strategic change

We measure strategic change as resource reallocation (Finkelstein and Hambrick, 1990). Following previous studies (e.g. Bednar et al., 2013), we use an established measure of strategic change across six dimensions: (1) advertising intensity (advertising/sales), (2) research and development intensity (R&D/sales), (3) plant and equipment newness (net P&E/gross P&E), (4) non-production overhead (selling, general, and administrative expenses/sales), (5) inventory levels (inventories/sales), and (6) financial leverage (debt/equity).

Larger changes in these ratios reflect significant shifts in a firm’s resource allocation and, therefore, its underlying strategy. Following prior research (Weng and Lin, 2014), we calculated the absolute differences in these ratios between the prior and the current year, adjusting for industry effects and standardizing the values. After investigating outlier values that seemed to be driven by incorrect database entries, we decided to Winsorize each dimension at the 1% level and created a single index by summing up all dimensions (Crossland et al., 2014).

Moderators and control variables

We measured TMT size according to DEF-14A filings, which we retrieved from ExecuComp. By using executive identifiers, we compared the TMT composition in the focal year with that of the previous year and calculated the TMT change as the sum of all executives who had left and joined the TMT. Both variables reflect the skills and knowledge represented in the TMT and therefore influence the strategic decisions’ direction (Herrmann and Nadkarni, 2014).

We controlled for variables on the CEO, TMT, board, firm, and industry levels. On the CEO level, we controlled for variables that had been shown to influence strategic change: CEO age (Boeker, 1997b; Wiersema and Bantel, 1992), CEO duality (Bednar et al., 2013), CEO outsider origin (Karaevli and Zajac, 2013), CEO gender (Triana et al., 2019), CEO education background (Wiersema and Bantel, 1992), and CEO change (Karaevli and Zajac, 2013). In line with prior research (Harrison et al., 2019; Triana et al., 2014; Wiersema and Bantel, 1992), we also controlled for TMT size, TMT change, TMT age diversity, and TMT tenure diversity, as well as for the TMT education level diversity and TMT gender diversity. In addition, we controlled for board size and board independence (the ratio of outside directors to the total number of directors; Zhang and Rajagopalan, 2010). At the industry level, we controlled for environmental dynamism, measured as the standard deviation of industry sales growth during the previous 5 years (Zhu et al., 2020). Finally, we controlled for firm size, measured as the logarithm of the total number of employees, firm age, prior firm performance (industry-adjusted ROA), and industry annual performance, that is, the annual average industry performance (Harrison et al., 2019).

Estimation method

The dataset is structured as an unbalanced panel with a continuous dependent variable and two time-invariant independent variables. Consequently, we used random-effects panel regression to test our hypotheses (e.g. Georgakakis et al., 2017). This is based on the perception of curiosity as a trait and aligned with previous research in this area (Harrison et al., 2019). We led our dependent variable across all the models by 1 year to address reverse causality concerns. Considering the existence of heteroskedasticity and autocorrelation, we used cluster robust standard errors. In addition, we included year fixed effects.

Results

Table 1 shows descriptive statistics and inter-correlations. Table 2 shows the random-effects models predicting strategic change (t + 1). We calculated the variance inflation factors of all models, and the highest value was 1.81. Model 1 is a baseline model that includes control variables only. Model 2 adds both curiosity types, and Model 5 is the full model that includes all interaction terms.

Descriptive statistics and correlations.

Random-effects regression models predicting strategic change (t + 1).

p-values in parentheses. All models include clustered, robust standard errors. Dependent variable is industry-adjusted and Winsorized at the 1% level at both the low and high ends.

The results support our hypotheses that CEO curiosity types have diverging effects on strategic change. H1 predicted that CEO I-type curiosity would be positively associated with strategic change. The coefficient for CEO I-type curiosity in Model 2 is positive, but insignificant (β = 0.01; p = .315). Hence, H1 is rejected. Regarding H2, a negative relationship between CEO D-type curiosity and strategic change (β = −0.04; p = .001) is confirmed. These findings also hold in our interaction model, Model 5. This is particularly important given that the interpretation of the main effects when there are significant interactions could lead to incorrect conclusions (Busenbark et al., 2022a).

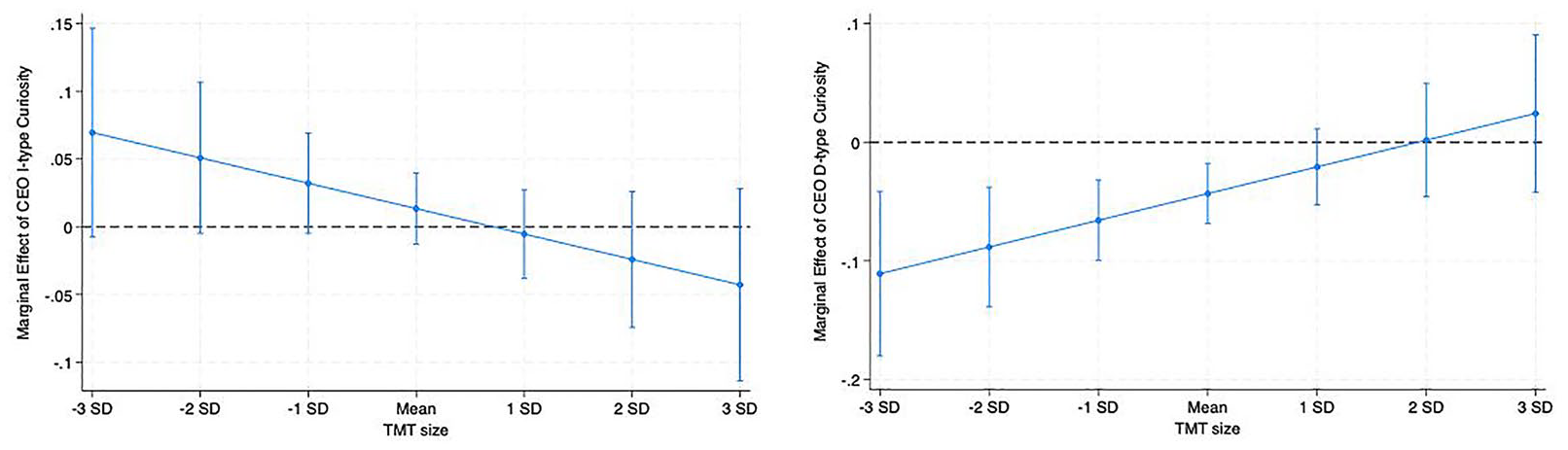

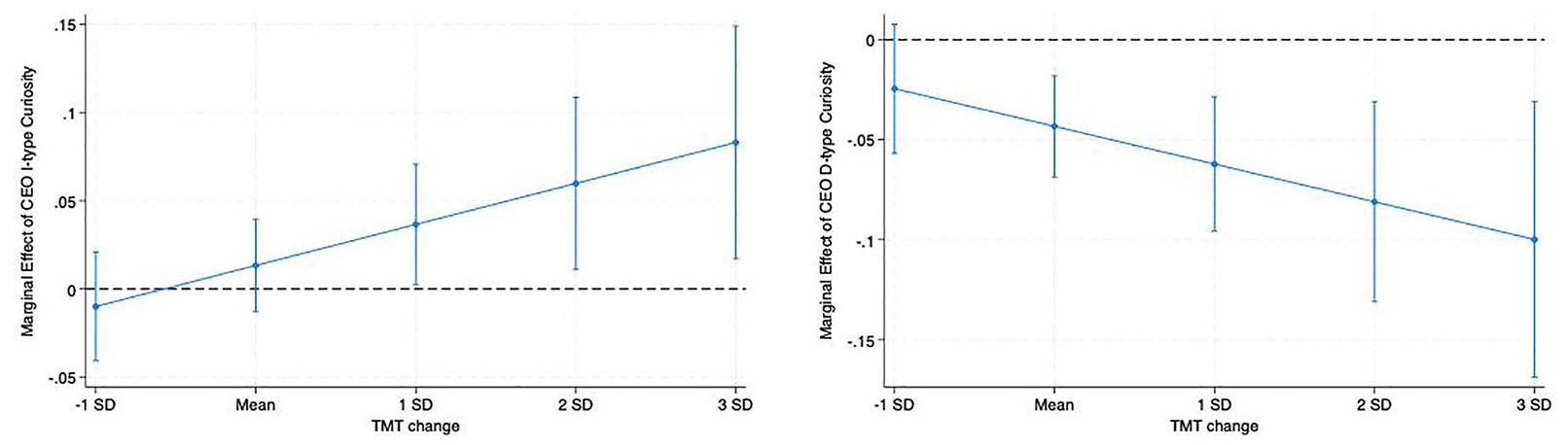

Model 3 does not confirm H3a (β = −0.01; p = .323) but partially supports H3b (β = 0.02; p = .093). We find support for H4a (β = 0.02; p = .056), but not for H4b (β = −0.01; p = .235). Figures 1 and 2 show that marginal effect plots offer a more fine-grained understanding of the interaction results. The left side of Figure 1 indicates no clear pattern across different TMT sizes for CEO I-type curiosity. In contrast, the negative coefficient of CEO D-type curiosity on the right side of Figure 1 approaches zero as the TMT size increases. The negative effect of CEO D-type curiosity may be less pronounced in medium-sized teams than in very small TMTs. Figure 2 shows that CEO I-type curiosity’s positive effect increases significantly when there are more changes in the TMT.

Marginal effects plots for CEO I/D-type curiosity × TMT size.

Marginal effects plots for CEO I/D-type curiosity × TMT change.

Robustness tests and supplemental analyses

To test the robustness of our findings we followed several steps. First, we addressed potential endogeneity concerns stemming from omitted variable bias by conducting an impact threshold of a confounding variable (ITCV) analysis. We used the konfound command in Stata and specified a significance level of 0.1 (Busenbark et al., 2022c). We find that 21.31% (1716 cases) of the CEO I-type curiosity estimate and 50.52% (3976 cases) of the CEO D-type curiosity estimate would have to be biased to affect our results. These values refer to Model 2 of our main analysis, which tested Hypotheses 1 and 2. While there are no absolute standards for the impact threshold, these values are relatively large, suggesting that our results are unlikely to suffer from omitted variable bias. Moreover, recent research indicates that endogeneity may be less of an issue in interaction terms (Bun and Harrison, 2019; Nizalova and Murtazashvili, 2016). We nevertheless addressed potential endogeneity with two instruments for each curiosity type, combining an industry mean approach with the Durbin method. For the industry mean approach, we calculated industry means for both curiosity types for each year (Junge et al., 2024, Krause et al., 2019). In addition, we followed the Durbin method (Kennedy, 2008) to create a second instrument. We created a categorical variable representing terciles of our independent variables (Busenbark et al., 2022b). We find positive associations between our two instruments and I-type curiosity (βindustry = .146, p = .000; βDurbin = .916, p = .000) as well as for our D-type curiosity instruments (βindustry = .053, p = .000; βDurbin = .966, p = .000). Empirically, our instruments proved to be strong (F = 608.72, p = .000; F = 684.17, p = .000), and we ran a Hansen-Sargan test for overidentification (p = .385), which suggests that the exclusion restriction is satisfied. Results are robust when accounting for potential endogeneity.

Second, we controlled for the curiosity measure in the LIWC software (Boyd et al., 2022) in our models and found consistent results. We also replaced our independent variables with the LIWC curiosity measure. This resembled a one-dimensional understanding of CEO curiosity. We found no significant effects for our hypotheses using this approach. This confirms our argument that both CEO curiosity types must be considered to fully understand their strategic implications. Third, our results did not change considerably when we re-ran our models without the restriction that CEOs had to speak at least 150 words. Fourth, our results did not change when we excluded common terms for the two curiosity types and re-ran the analyses. Fifth, we used alternative time lags for our independent variables. With a 2-year lag, the results of Hypotheses 1 and 2 remained consistent, but we did not find any significant results for our interaction hypotheses. Sixth, we used generalized estimating equations (GEE; e.g. Petrenko et al., 2019) as an alternative model specification. Specifying a Gaussian distribution, an identity link function, and an exchangeable correlation structure, we find similar results for our hypotheses.

Seventh, we included CEO tenure as a control variable, since CEOs with longer tenures may be less likely to initiate strategic change (Finkelstein and Hambrick, 1990). CEO tenure was insignificant in our models. Eight, we removed observations relating to CEO succession years and found effects consistent with our reported findings for Hypotheses 1 and 2. This analysis demonstrates that strategic change is influenced by CEOs’ I/D-type curiosity rather than by the selection of CEOs with a particular curiosity type or level that fits the firm’s preference for strategic change. Finally, we tested for the curvilinearity of TMT size, which was insignificant in all models.

In supplemental analyses, we tested the moderating effect of TMT diversity since CEO curiosity types could influence strategic change differently with broader information and more viewpoints. We tested the moderating effect of TMT education-level diversity, gender diversity, tenure diversity, and age diversity on the relationships between CEO curiosity types and strategic change—all of which were insignificant. Moreover, we differentiated between members joining and leaving the TMT as opposed to total TMT change. Our findings suggest that the results are driven more by TMT members leaving the team. In addition, we controlled for attainment discrepancy (Kolev and McNamara, 2022; Iyer and Miller, 2008) as proxy for the motivation to change. In line with prior research (Kolev and McNamara, 2022), we used historical aspiration (i.e. ROA of the focal firm 1 year prior to the observed performance) to compute attainment discrepancy (i.e. the difference between firm performance in t-1 and aspiration levels in t-2). Findings show a negative and significant coefficient for negative attainment discrepancy (β = −2.46; p = .000). This indicates that as performance falls further below aspirations, firms engage in more strategic change (e.g. Kolev and McNamara, 2022). We also find a positive and significant coefficient for positive attainment discrepancy (β = 1.10; p = .002). Our findings for H1–H4 remain consistent. Hence, the motivation to change influences strategic change in addition to CEO curiosity.

Discussion

Integrating upper echelons research with recent psychology research on curiosity, this study investigated the effect of CEO I-type and D-type curiosity on firms’ strategic change. We find that CEO D-type curiosity is negatively related to strategic change, while CEO I-type curiosity shows no significant relationship. Further, the negative relationship between CEOs with D-type curiosity and strategic change is weaker in medium-sized TMTs than in very small TMTs, while the relationship between I-type curiosity CEOs and strategic change becomes stronger under more TMT changes. These findings enhance our understanding of how CEO curiosity types influence strategic changes, and how they are contextualized in the TMT. Our findings contribute to upper echelons and curiosity research in several ways.

Theoretical contributions

Our paper introduces CEO curiosity’s multifaceted nature to upper echelons research and demonstrates the differential influence of two curiosity types on strategic change. Building on psychology research, we conceptually clarify how CEO I-type and D-type curiosity affect strategic change and test their relationships empirically. Our study shows the diametrically opposed and partially counter-intuitive influence of CEO I-type and D-type curiosity on strategic change. Contrary to expectations, I-type curiosity, which aligns with the common perception of CEO curiosity as a driver of change (Lievens et al., 2022), is not significantly associated with industry-adjusted strategic change, while D-type curiosity shows a negative influence. I-type curious CEOs, with their wider information-seeking scope for idea generation and their crossing of knowledge domains, may have a broader perspective and understanding of the industry. This likely helps such CEOs to evaluate whether strategic changes are required and to assess strategic change options in the context of industry changes, potentially avoiding responding to industry fads. Due to their broader perspective, I-type curious CEOs thus refrain from changing their companies’ strategy at a level that exceeds their industry peers. In contrast, D-type curious CEOs, due to their stronger problem-solving focus, focus on refining existing problems and initiate less change. These findings highlight that how CEO curiosity influences strategic change depends on the underlying curiosity type, emphasizing the importance of understanding curiosity as a two-dimensional construct in executive decision-making. This opens new avenues for research on CEO curiosity types’ role in strategic and organizational decisions.

While upper echelons research has increasingly studied higher-order traits’ effects (Harrison et al., 2020), our study advances it by laying the groundwork for future research into the sub-dimensions of specific executive personality traits. A common misconception is that I/D-type curiosity could simply be exchanged with higher-order traits such as openness and conscientiousness because the constructs are associated. This ignores the important differences between domain- and facet-level traits. The former (e.g. conscientiousness) are meant to have high bandwidth, while the latter (e.g. the organization facet of conscientiousness) provide high descriptive and predictive precision (Soto and John, 2017). A fundamental contradiction arises if hypothesis development is based on a subset of facet attributes, while empirically the higher-order trait is measured. Our research design attempts to avoid this common mistake by enhancing construct validity, paving the way for more precise future research.

Moreover, our study introduces a contextualized perspective on CEO curiosity to upper echelons research by disclosing the social aspect of curiosity. We find that the two dimensions of TMTs—size and change—influence the two CEO curiosity types’ impact on strategic change differently. Surprisingly, TMT size influences the relationship between CEO D-type curiosity and change (with partial support), while TMT change affects the relationship between CEO I-type curiosity and strategic change. This implies that I-type curious CEOs benefit from the different perspectives in a changing TMT, since they are better at leveraging different TMT members’ views in strategizing. Moreover, the evolving team dynamics resulting from TMT changes (Wiersema and Bantel, 1993) might serve as a catalyst, thereby enabling CEOs with I-type curiosity to pursue change. Conversely, we find no support for TMT changes alleviating the negative relationship between a CEO with D-type curiosity and strategic change. Instead, the margins plot gives some indication that the opposite occurs. An explanation might be that with increasing TMT changes, D-type curiosity CEOs could become more persuasive in justifying their emphasis on problem-solving (Ma, 2023).

Contrary to our expectations, we find no support for a moderating effect of TMT size on the relationship between CEO I-type curiosity and strategic change. CEOs with I-type curiosity might be unable to successfully reconcile the interpersonal conflict that arises in larger TMTs (Amason and Sapienza, 1997), while their openness and interest in the TMT’s ideas cannot compensate for this effect. The more complex interpersonal dynamics in larger TMTs might even detract such CEOs from pursuing their initiatives. Another possible explanation could be that larger teams may lead to a dilution of individual team members’ contributions, making it harder for new ideas to be heard and integrated. It is also possible that most TMT members’ ideas only serve as substitutes for CEO ideas, resulting in no further enhancement of the CEO’s ideas. Conversely, larger TMTs seem to challenge CEOs with D-type curiosity more, suggesting that more TMT members fragment such CEOs’ specific problem-solving focus. CEOs with D-type curiosity also seem to face challenges with reconciling different opinions in larger teams (Amason and Sapienza, 1997), which have a discernible impact on joint decision-making and ultimately impede their strategic focus. These findings reveal how specific CEO personality traits interact with the TMT context and advance our understanding of the CEO-TMT interface (Georgakakis et al., 2022).

Furthermore, our study contributes to research on curiosity in organizations by offering a more comprehensive understanding of curiosity at the executive level. While most research has focused on employee curiosity (e.g. Celik et al., 2016), recent studies have started examining aggregate CEO curiosity (Liu et al., 2023). We complement this research with first insights into CEO I/D-type curiosity’s effects on strategic change. Importantly, while existing research frequently argues that employee curiosity is an antecedent to innovation, we demonstrate that CEO I/D-type curiosity offers differentiated insights into how CEO curiosity influences strategic change, depending on the type of curiosity studied. Research examining employees’ I-type and D-type curiosity at different hierarchical levels could build on our findings to improve our understanding of how different curiosity types influence organizational change.

Finally, we contribute to recent advances in empirical strategic management research by developing and introducing a novel dictionary-based text measure for CEO I-type and D-type curiosity. We enhanced the dictionary development by including the latest LIWC functionalities (e.g. Workbench) and used word embeddings as an additional step to identify relevant, context-specific synonyms. This provides researchers interested in the two curiosity types with a useful closed-language approach.

Limitations and future directions

Our study is one of the first research endeavors venturing into the executive curiosity realm and, as such, does have limitations. In our study, measurement error is a potential source of endogeneity (Bastardoz et al., 2023). The analyst questions could be biased toward a particular curiosity type—an issue future research needs to address, using different and larger datasets to measure curiosity.

While open-language approaches based on supervised learning outperform closed-language (e.g. dictionary) approaches in terms of external validity, they have weaknesses in face validity, bias replication, and transparency (Bender et al., 2021). The quality of the ratings of both open and closed-language approaches is decisive for the measure’s final performance. We therefore chose a dictionary approach for its transparency regarding how scores are derived. A potential drawback of using crowd raters is that they sometimes choose more frequent but potentially weaker signal words (e.g. questions). We acknowledge this shortcoming, while noting a clear benefit in terms of the transparency and replicability of the results (van Atteveldt et al., 2021). Since there are quality differences between platforms (Peer et al., 2022), we conducted pretests on different platforms, included quality controls, and followed best practice guidelines for using crowd rater platforms (Aguinis et al., 2021). While our validated dictionary approach offers advantages in terms of the transparency and replicability of the results (van Atteveldt et al., 2021), it may, however, not fully capture subtle nuances in language. Future research can build on our work and develop supervised approaches that leverage the power of the latest generation of large language models. While dictionary methods are instrumental in helping us understand causal mechanisms, the application of large-language-model measures can advance our understanding of linguistic context.

Furthermore, although our study design based on secondary data allowed us to investigate a relatively large sample, it does not allow for drawing conclusions about how CEO curiosity types play out in strategic decision-making processes over time. Future research could explore how CEO curiosity types influence information-seeking, strategic analysis, and decision-making for specific decisions. Using a multimethod approach, studies can build on our results to provide a more comprehensive understanding of I-type and D-type curiosity’s effects on organizations (Wellman et al., 2023).

Although our results are a first indication of I/D-type curiosity’s effects on strategic change, future research could build on our study to examine other strategic decisions, including those made in times of crises or during industry shocks. Future studies could, for instance, examine how CEO curiosity types influence the initiation versus the implementation of strategic change under time pressure as well as specific strategic change decisions (e.g. acquisitions).

Future research also needs to examine relevant industry and organizational factors that support or hinder CEOs in leveraging their curiosity for change. It would, for instance, be interesting to examine the role of technological disruption, organizational structure, organizational culture, and TMT functioning in influencing the relationship between CEO curiosity types and strategic change. In this respect, our new text measure of CEO I/D-type curiosity is an important alternative to existing survey scales, providing researchers with the opportunity to study curiosity in large-scale text data.

While our paper draws on a sample of large U.S. firms, future research needs to examine smaller firms and diverse cultural settings. In some cultural contexts, for instance, frequent questioning—an indicator of curiosity—might be interpreted as lacking expertise, and be perceived as intrusive or as spying (Kashdan et al., 2020a). Understanding how different cultural settings view CEO curiosity could shed light on its potential negative side-effects.

Practical implications

Our study has important implications for CEOs, boards of directors, investors, and executive coaches. For CEOs, our findings imply the value of being aware of their curiosity type and how it influences strategic change. Consequently, leadership-development programs need to be tailored to help CEOs and potential leadership candidates understand how their curiosity type shapes their decision-making. Executive coaches could support this process by guiding this self-awareness. Furthermore, boards of directors can integrate assessments of CEO curiosity types into CEO selection, evaluation, and succession planning. Boards and investors need to be aware that CEOs with D-type curiosity could become overly focused on resolving existing problems rather than initiating broader strategic change. Conversely, they should not expect CEO’s I-type curiosity alone to drive strategic change that exceeds their industry peers.

Beyond CEO curiosity, boards and investors need to consider TMT composition and pay attention to leveraging different TMT characteristics for different CEO curiosity types. For CEOs with D-type curiosity, larger teams might mitigate such a CEO’s focus on solving existing problems. In contrast, for I-type curious CEOs, TMT changes might serve as a catalyst, enabling them to drive strategic change.

To conclude, our study shows that the role of CEO curiosity in strategic change depends on the type of curiosity studied. This provides a novel viewpoint for upper echelons research, highlighting a central, multi-dimensional CEO personality trait and the importance of aligning it with the TMT context. We hope our study paves the way for future research on specific, multifaceted executive personality traits.

Supplemental Material

sj-docx-1-soq-10.1177_14761270251325238 – Supplemental material for Chief Executive Officer curiosity and strategic change: The differential role of curiosity types and top management team characteristics

Supplemental material, sj-docx-1-soq-10.1177_14761270251325238 for Chief Executive Officer curiosity and strategic change: The differential role of curiosity types and top management team characteristics by Dieter Gutschi and Patricia Klarner in Strategic Organization

Footnotes

Acknowledgements

We are grateful for discussions with and feedback from John Busenbark, Craig Crossland, Karyn Dossinger, Daniel Gamache, Spencer Harrison, Aaron Hill, Jason Kiley, Andreas König, Tim Quigley, Patrick Mussel, and participants in research seminars at the Vienna University of Economics and Business and the AOM and EURAM Conferences.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We appreciate funding from Vienna University of Economics and Business.

Supplemental material

Supplemental material for this article is available online.