Abstract

Status dynamics play a critical role in venture capital (VC) syndication. Prior research on multiparty syndicates has shown how status differences among current syndicate members affect how the syndicate searches for new investors in later investment rounds. However, it is unclear how potential newcomers evaluate whether or not to join a syndicate based on the degree of status disparity among current syndicate members. We adopt an alter-centric approach by examining how an existing syndicate’s status disparity affects a potential newcomer’s willingness to join. For potential newcomers, we contend that syndicate status disparity is a double-edged sword, both deterring newcomers due to low perceptions of syndicate trust while simultaneously attracting newcomers at the prospect of accessing diverse future investment opportunities. Whether the perceived costs of syndicate status disparity outweigh the perceived benefits for newcomers depends upon the degree of risk associated with the venture deal. Across two studies—a field experiment of 193 institutional investors and an archival study of 3644 multiparty syndicates—we found that newcomers are attracted to syndicate status disparity when deal risk is low but deterred from syndicate status disparity when deal risk is high. Our article highlights how newcomer additions to multiparty syndicates entail a complex interplay between features of co-investors and features of the venture deal.

Keywords

Multiparty syndicates—investment groups comprised of two or more investors—play an increasingly significant role in the financing of new ventures (Hochberg et al., 2007). Multiparty syndicates help investors integrate diverse perspectives, amass complementary resources, defray financial risk, bolster collective legitimacy, and access future investment opportunities (Ferrary, 2010; Gompers and Lerner, 2001; Hindle and Yencken, 2004; Ngah and Jusoff, 2009). Multiparty syndicates accrue further benefits by adding new investors during subsequent rounds of funding (Lerner, 1994). Controlling for underlying differences in venture quality and venture capital (VC) performance with prior investments, multiparty syndicates that add new members in subsequent investment rounds earn a higher internal rate of return (Brander et al., 2002) are more likely to achieve a successful exit (De Clercq and Dimov, 2008; Tian, 2012), reach those exits faster (Giot and Schwienbacher, 2007), and receive higher initial public offering (IPO) valuations (Nahata, 2008).

Given these benefits, it is important to understand the dynamics that leads to the evolution and growth of multiparty syndicates over time. Perhaps no concept on the topic of multiparty syndication has received more scholarly attention than status disparity: the degree of stratification, differences, and variation in status among group members (Zhang et al., 2017). Beyond the underlying characteristics of the venture, syndicate status differences are among the most important factors that affect decisions about who to invite to join a syndicate (Zhang et al., 2017). Prior research has shown that syndicates are reluctant to add newcomers with a strong tie to just one syndicate member because other syndicate members are worried that the newcomer could tip the balance of power within the syndicate. However, syndicates are willing to overlook this issue when the newcomer is connected with a syndicate member with relatively high status because of other syndicate members’ interest in maintaining a positive relationship with the high-status member and, ultimately, in accessing that high-status member’s deal flow (Zhang and Guler, 2020). Other work has shown that status disparity decreases trust among existing members because status differences often correspond with potentially incompatible interests. However, that wariness can be attenuated when there is a prior history of co-investment among current syndicate members (Zhang et al., 2017). This research highlights how syndicate status disparity can create a trust deficit among existing syndicate members, and how this lack of trust, in turn, affects which new investors the syndicate is willing to add in subsequent investment rounds.

While this research has illuminated how syndicate status dynamics affects which newcomers are more likely to be sought in later funding rounds, we have surprisingly little insight into the other side of the equation. How do newcomers evaluate syndicate status disparity in deciding whether or not to join an existing multiparty syndicate? Examining this question provides a more complete picture of how status disparity affects the syndication process. Furthermore, as we will argue, understanding whether syndicate status disparity will attract or deter newcomers is not straightforward based upon current theory.

In developing our framework, we contend that syndicate status disparity evokes two countervailing forces that simultaneously attract and repel potential new investors. On one hand, newcomers are likely wary of status disparity because it implies divergent interests among syndicate members (Bunderson and Van der Vegt, 2018; Katila et al., 2008). And, status disparity affects how those divergent interests are ultimately reconciled. As a result, newcomers are less likely to trust syndicates characterized by status disparity (Zhang et al., 2017). On the other hand, status disparity could offer new investors access to a more diverse set of future investment opportunities. Because deal flow is a major concern for most VC firms, investors are often evaluating their choice about whether to join a syndicate not just in the context of the focal deal but also in terms of how that collaboration could yield future investment opportunities (Manigart et al., 2006). Evidence of the role of status in shaping these decisions can be seen in how those holding distinct status positions tend to participate in different types of venture deals (cf. Plummer et al., 2016; Podolny, 2001; Sorenson and Stuart, 2008; Zott and Huy, 2007). Newcomers who join a multiparty syndicate characterized by status disparity, therefore, could leverage these ties to diversify their own future investments, beyond the scope of the focal deal.

To reconcile these opposing mechanisms and definitively answer the question about when syndicate status disparity attracts versus when it deters newcomers, we suggest it is important to attend to the contingencies around the decision to join a syndicate. Specifically, we propose that the risk associated with the focal venture deal is a key contingency since it shapes the collaborative context around which syndicate members interact (Zhelyazkov and Tatarynowicz, 2021). Deal risk—the chance that a venture investment’s actual return will differ from what is expected (Tyebjee and Bruno, 1984)—can either trigger or suppress collaborative pressures among syndicate co-investors (Zhang et al., 2017). We propose that understanding whether new investors prioritize the benefits of syndicate status disparity (i.e. access to diverse future investment opportunities) over its costs (i.e. a lack of trust in the context of the focal deal) depends upon this risk.

We test our theory in two studies: an experiment with institutional investors and an archival study of VC investments. In Study 1, we conduct an experiment with 193 experienced institutional investors attending a “Demo Day” event in the Northeast United States. In this study, we manipulate syndicate status disparity and deal risk to test their impact on an investor’s interest in joining a new syndicate. In Study 2, we test the ecological validity of the experimental context using the Preqin Venture Capital Online database (www.preqin.com/data/venture-capital), which provides a comprehensive set of new venture investments (Ewens et al., 2013; Hochberg et al., 2018). Using a cross-industry sample of venture-VC transactions from 1999 to 2016, we construct a sample of 3644 multiparty syndicates to examine the effects of Round 1 syndicate status disparity on attracting new investors in the second round of financing. Results across both studies support our theoretical arguments.

Our study offers three theoretical contributions. First, theory and research on multiparty syndicates has emphasized how status disparity affects the search for new investors, with relatively less attention devoted to how newcomers evaluate status disparity (e.g. Zhang et al., 2017; Zhang and Guler, 2020). We augment this research by offering an alter-centric view that considers how the newcomer evaluates syndicate status disparity by clarifying when it will attract versus deter new investors from joining the syndicate in subsequent funding rounds. Second, theory and research on syndication has traditionally focused on the formation of bilateral partnerships between pairs of VC firms (e.g. Bellavitis et al., 2020; Vedula and Matusik, 2017; Weber et al., 2016), examining dyadic mechanisms, such as status similarity between a newcomer and a lead investor (e.g. Zhelyazkov and Tatarynowicz, 2021). However, multiparty syndicates are more complex and involve higher-order relational mechanisms that make these multi-member partnerships more than a mere collection of dyads (Das and Teng, 2002; Lavie et al., 2007; Stuart and Sorenson, 2007; Zeng and Chen, 2003). Our article examines mechanisms operating at the collective level (e.g. status disparity, syndicate trust) to understand their unique impact on the addition of newcomers. Finally, we contribute to the literature on power and status in teams. Prior theory and research in this domain have traditionally emphasized how status disparity affects interactions among group members (e.g. top management team members) in the course of completing shared tasks (Bunderson and Van der Vegt, 2018). Our theory suggests that status disparity is also a cue that prospective newcomers use to “size up” the group before joining. Thus, status disparity not only shapes how group members interact with each other after the group has formed but also affects whether prospective members will join the group in the first place.

Syndicate status disparity and newcomer additions

VC syndication involves the formation of ties among VC firms as they choose with which other firms to co-invest in a specific entrepreneurial venture (Lerner, 1994). Research on how VC firms select investment partners has enumerated a range of variables that predict co-investment. VC firm status—the cumulative pattern of relations as reflected in the network centrality of one’s ties (Podolny, 2001)—is perhaps the most widely-studied concept in research on syndication (Chung et al., 2000; Dimov and Milanov, 2010; Meuleman et al., 2010). At the individual firm level, this work has shown that high-status VCs are attractive as co-investors because partnering with a higher status member can lower transaction costs in acquiring additional resources for their investment (Podolny, 1994), provide access to superior information across the network of investors (Lee et al., 2011), increase the odds of a successful exit (Stuart et al., 1999), and increase the firm’s own status via affiliation (Sauder et al., 2012). At the dyadic level, co-investment ties tend to exhibit status homophily (Chung et al., 2000), such that high-status VC firms often co-invest with other high-status firms because affiliating with low-status investors increases the possibility of “status leakage” for the high-status firm (Sauder et al., 2012). Status asymmetric ties do form but such connections often come at a cost for the low-status firm, such as when low-status firms offer favorable financial terms to the high-status firm (Ahuja et al., 2009; Castellucci and Ertug, 2010; Shipilov et al., 2011; Zhelyazkov and Tatarynowicz, 2021).

Recently, research on the role of status in syndication has shifted to focus on understanding the impact of status dynamics at the syndicate level. This research has emphasized how status disparity—the degree of status variation across a group—affects the evolution of syndicates, specifically in the search for newcomers in subsequent funding rounds. For instance, syndicates prefer to add newcomers who have ties to many current syndicate members and are hesitant to add newcomers with a tie to just one member (Zhang and Guler, 2020). This is because syndicate members are wary that such a newcomer might create an imbalance of influence that favors the interests of the member tied to that newcomer. However, syndicates are more willing to bring in a newcomer when that newcomer is tied to a high-status member. Syndicate members are willing to defer to the high-status member in these cases because those syndicate members have a longer-term interest in maintaining a positive relationship with the high-status member since it can lead to future co-investment opportunities (Zhang and Guler, 2020). Other work echoes this point that status disparity can sow distrust among syndicate members. Zhang et al. (2017) explain that syndicate members are generally wary of status disparity because they anticipate that status differences correspond with different preferences, risk tolerance, and ultimately, incompatible interests (Zhang et al., 2017). These differences, in turn, are likely to be adjudicated on the basis of status, such that syndicate decisions reflect the interests and preferences of the highest status members and potentially at the expense of other syndicate members. However, despite the general tendency for status disparity to cause wariness among current syndicate members, this research also shows that the distrust that arises from status disparity can be overcome when syndicate members have co-invested with each other in the past because this prior history enhances perceptions of dyadic trust (Zhang et al., 2017).

A common theme across this recent work on multiparty syndicates is the emphasis on how status disparity affects the search for newcomers. For example, Zhang and Guler (2020) note, “a prospective newcomer endorsed by a high-status member is more likely to join than one endorsed by a low-status member . . . [because other members] defer to the high-status member. . . even though it may not be in their own best interests” (pp. 125–126). And in describing the search for new co-investors, Zhang et al. (2017) point out that status differences, “create a lack of trust” (p. 1369) that pre-existing ties can help overcome. This work highlights how status disparity affects how syndicates evaluate prospective newcomers.

However, the syndication process also involves newcomers’ response to an invitation to join the existing syndicate. Thus, even though we have an understanding about how status disparity affects the syndicate’s search process, we have relatively less clarity on how newcomers respond to opportunities to join syndicates characterized by status disparity, beyond the general preference of newcomers to join a single high-status investor (Zhang and Guler, 2020). Understanding how newcomers evaluate the status disparity of syndicates is important because it reflects an important aspect of the syndication process and because it has an ambiguous effect based on current theory. We contend that newcomers will view syndicate status disparity as a double-edged sword, which entails both costs and benefits.

In the following section, we first elaborate on the two countervailing mechanisms that underpin how syndicate status disparity influences newcomers’ decisions to join. Next, we explain why the effect of status disparity on attracting newcomers depends upon the level of risk inherent in the venture deal, specifically highlighting the role of deal risk: the chance that a venture investment’s actual return will differ, either positively or negatively, from what is expected (Tyebjee and Bruno, 1984). We focus on deal risk because it pertains to the potential degree of collaborative challenges as well as the potential financial rewards that the syndicate may encounter over the course of its work in developing the venture.

Status disparity and syndicate trust

Prior research has shown that status disparity within groups undermines perceptions of trust among members of those groups (Mo and Brion, 2021). Status disparity increases the salience of status as a dimension along which members differ from each other (Tzabbar and Vestal, 2015). And when status disparity is more salient, members are more likely to ascribe malevolent intentions and motives to other group members (Edmondson, 2002; Schaerer et al., 2021). This is because status differences can be deployed in ways that favor the high-status group member to the detriment of the rest of the group members (Katila and Mang, 2003). As a result, members tend to, on average, experience less trust in hierarchical groups (Bunderson and Reagans, 2011; Greer et al., 2017; Mo and Brion, 2021). These findings from research on groups and teams suggest that newcomers are more likely to be wary about joining multiparty syndicates characterized by status disparity (Zhang et al., 2017).

Potential new investors may be especially sensitive to the trust deficit that arises from status disparity because differences in investor status correspond with divergent preferences and motives (Zhang and Guler, 2020). First, status differences correspond with varying degrees of dependence on the focal venture, with high-status VC firms participating in greater volume of investing compared with low-status firms (Podolny, 2001). Low-status investors, therefore, tend to be more dependent on any given focal deal than high-status investors. This discrepancy in dependence is likely to translate to different ideas about which course of action the focal venture should pursue. For instance, high-status investors may be more willing to recommend that a venture adopt an aggressive growth strategy, whereas low-status investors might prefer a more conservative approach (cf. Lewellyn and Muller-Kahle, 2012). As Zhang et al. (2017) note, “Given a larger portfolio of ventures, high-status VCs are less dependent on the success of any particular venture; thus, they are likely to be less risk averse than lower-status VCs in any single deal” (p. 1369). Second, status differences among syndicate members also correspond with different levels of financial aspiration associated with the focal venture. Low-status members typically have lower financial goals compared with high-status members (Zhang et al., 2017). These differences in financial aspirations can lead to tension when considering, for example, whether to accept an acquisition offer that yields a somewhat lower return-on-investment (cf., De Dreu and Van Kleef, 2004; Wolfe and McGinn, 2005). Third, status disparity can also affect timing preferences (Katila et al., 2008). Low-status investors are more likely to seek a quick venture exit that allows them to “grandstand” their accomplishment (Gompers, 1996). In contrast, high-status VCs may prefer to wait for a potentially more lucrative deal in the future. Zhang et al. (2017) suggest that status-based differences are likely to create a lack of trust among syndicate members, making them more apt to notice potentially incompatible interests.

Taken together, status disparity and the divergent preferences that arise from it are likely to undercut syndicate trust. Newcomers’ decreased perceptions of syndicate trust, in turn, should decrease their attraction to joining these multiparty syndicates (Mo and Brion, 2021). Trust is a critical element for group functioning because it enables information sharing and minimizes the risk of destructive conflict (Bendersky and Hays, 2012; De Jong and Elfring, 2010; Edmondson, 2002). For that reason, members are drawn to groups that are characterized by trust (Francis and Sandberg, 2000; Katila and Mang, 2003; Ruef et al., 2003) and often fail to develop a sense of trust if they do join groups characterized by status disparity (Mo and Brion, 2021). Thus, we expect newcomers are especially wary about joining syndicates characterized by status disparity because it undermines their perceptions of trust in the syndicate.

Status disparity and perceived future deal flow

Even though status disparity may undermine syndicate trust for newcomers in the context of the focal deal, status disparity may simultaneously offer newcomers longer-term benefits by providing them access to a more diverse mix of future investment opportunities. Status disparity implies that syndicate members occupy distinct, non-overlapping positions in the investor network, with some members holding central positions and others occupying more peripheral positions (Podolny, 2001). Syndicate members that hold distinct network positions tend to have access to different types of venture investments (Sorenson and Stuart, 2001). Status disparity corresponds with differences in investment type with respect to the amount of capital committed, syndicate membership and size, and the focus of the ventures (Zhang et al., 2017). For instance, low-status investors, relative to high-status investors, tend to invest in fewer deals that are smaller in scope and fund earlier stage ventures (Podolny, 2001; Shipilov et al., 2011). As a result, joining a syndicate characterized by status disparity offers newcomers direct access to future investment opportunities that vary along these important dimensions of venture investing (Baum et al., 2003). Past research has suggested that having access to a more diverse set of future investment opportunities investors increases financial returns and defrays risk (Hochberg et al., 2007; Sorenson and Stuart, 2001, 2008). Prospective newcomers may, therefore, be drawn to the prospect of accessing diverse investment opportunities afforded by status disparity (Baum et al., 2003; Shipilov et al., 2011). Relatedly, investors often seek opportunities to establish partnerships with those located in distinct parts of the network (Sorenson and Stuart, 2001, 2008). And because investors often struggle to access diverse investment opportunities (Hochberg et al., 2007; Sorenson and Stuart, 2001), joining a syndicate characterized by status disparity can serve as a ready-made means for diversifying future investments. Thus, prospective investors are likely attracted to status disparity because it could increase access to a wider variety of future investments among syndicate members.

Moderating role of deal risk

In light of these differing views, it remains an open question about how status disparity impacts newcomer attraction to the syndicate. Newcomers could be wary of status disparity due to a lack of trust in the syndicate; alternatively, newcomers could be drawn to status disparity if they believe it will increase access to a more eclectic mix of future deals. Under what conditions do the syndicate trust costs outweigh the deal flow benefits?

We contend that whether the perceived benefits of status disparity outweigh its perceived costs depends on the degree of deal risk. We define deal risk as factors that increase the variation in possible future outcomes regarding the focal venture deal, including both upside return and downside risk (Tyebjee and Bruno, 1984). While the very nature of entrepreneurship implies a certain degree of risk, there is still significant variation in the degree of risk across deals (MacMillan et al., 1985). According to Tyebjee and Bruno (1984), deal risk entails four underlying components: product-related factors (e.g. patents, product differentiation), industry dynamics (e.g. sales growth rate, volatility), environmental threats (e.g. competitors, partnerships), and managerial risk (e.g. skills, experience). For the purposes of our exposition here, we conceptualize deal risk at this broader level of abstraction rather than developing distinct predictions about each underlying component.

We expect that deal risk will affect how newcomers evaluate the potential costs relative to the potential benefits of syndicate status disparity. Specifically, since venture deal risk increases the probability of an unpredictable collaboration among co-investors, newcomers are likely to anticipate that the costs of status disparity will outweigh its benefits as deal risk increases. This is because trust-related concerns are more likely to manifest in the context of a high-risk venture that entails the potential for many unforeseen challenges and ambiguous circumstances. Furthermore, the expectation of any future deal flow-related benefits associated with status disparity is likely diminished if newcomers doubt the focal venture will be successful. Thus, the extent to which newcomers are attracted to syndicate status disparity depends on the degree of deal risk such that newcomers are attracted to status disparity when deal risk is low but deterred from status disparity when deal risk is high.

Hypothesis 1. Deal risk negatively moderates the relationship between syndicate status disparity and the likelihood of attracting new investors.

For venture deals with a high degree of risk, status disparity in the syndicate will likely deter newcomers because it undercuts perceptions of trust in the syndicate. Research on social hierarchy has shown that when tasks are more uncertain or complex, conflict is more likely in hierarchical structures (Bunderson et al., 2016). In these situations, decision-making becomes more ambiguous, meaning that syndicate members are more likely to arrive at discrepant interpretations about how the venture should proceed. In the absence of clarity about the optimal choice for the venture, members are likely to adhere to options that more clearly serve their own interests (Hays and Bendersky, 2015; Maner and Mead, 2010). As one investor stated, “When everything is going well, this isn’t an issue, but the minute the business goes sideways or worse strange things start to happen. As the situation degenerates, the knives or flamethrowers come out” (Zhang et al., 2017: 1366).

These detrimental actions can take many forms. Certain syndicate members may extract more resources, such as time or money, from the rest of the syndicate (Ahuja et al., 2009; Castellucci and Ertug, 2010; Hochberg et al., 2007; Hsu, 2004) or punish dissenting syndicate members by structuring subsequent investment rounds in a way that dilutes their shares (Guler, 2007). Because the venture development process is long and the decisions surrounding how to build the venture are often ambiguous, newcomers that join syndicates characterized by status disparity may be especially vulnerable to the actions of the other syndicate members if the venture flounders. Thus, we expect that status disparity is likely to have negative effects when deal risk is high because it decreases the perception of syndicate trust for potential newcomers.

Hypothesis 2. The moderating effect of deal risk on the relationship between syndicate status disparity and the likelihood of attracting new investors is mediated by perceived syndicate trust.

In contrast, we expect that for venture investments with relatively low deal risk, status disparity in the syndicate will be positively related to newcomer tie formation. In this case, the potential for greater access to future investment opportunities becomes more salient for newcomers in comparison to the lack of trust in the syndicate (cf., Katila et al., 2008). New investors are likely to anticipate that the tangible rewards reaped from the focal deal will increase the odds of future collaboration (Cropanzano and Mitchell, 2005). In contrast, if newcomers are concerned that the focal deal will be unsuccessful, it is less likely that they would expect future investment opportunities to be available. Thus, for ventures with low deal risk, prospective newcomers may be better able to appreciate the potential for future deals since they anticipate the chances of venture success in the initial collaboration to be higher.

Hypothesis 3. The moderating effect of deal risk on the relationship between syndicate status disparity and the likelihood of attracting new investors is mediated by perceived future deal flow.

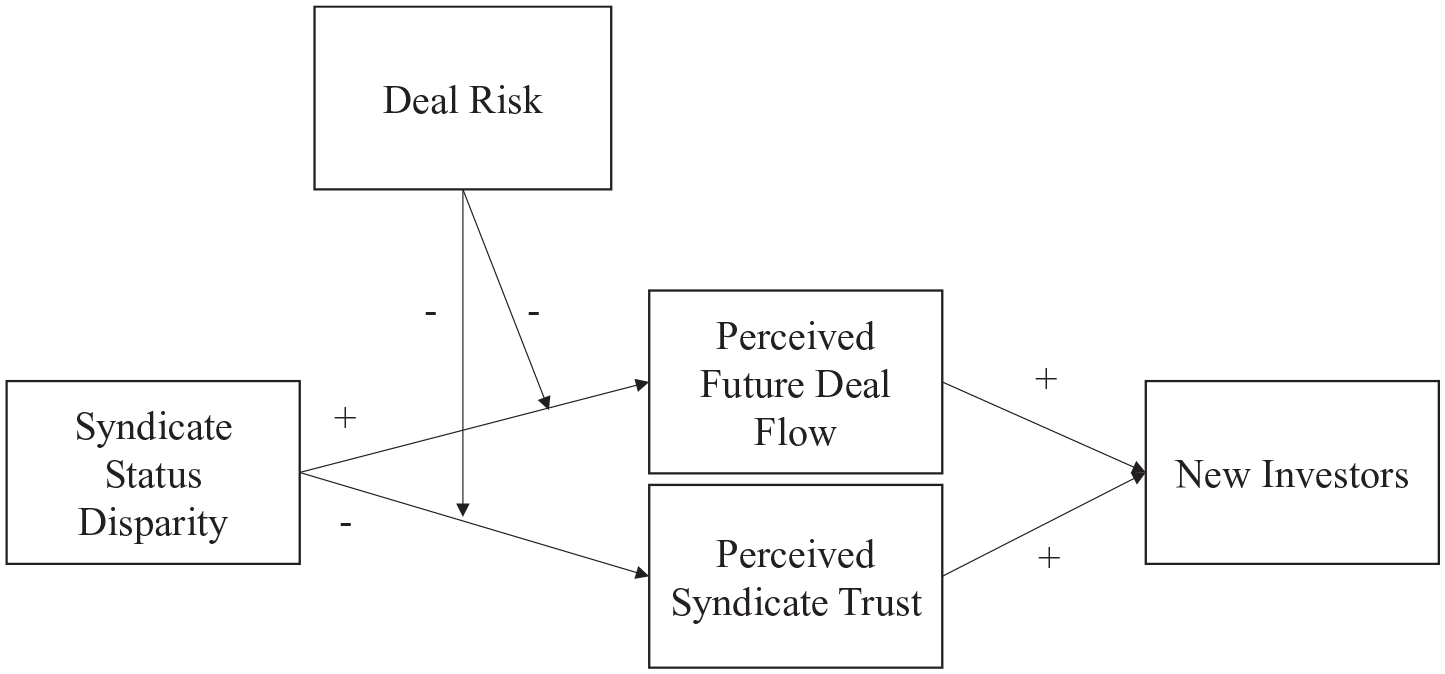

To summarize our model, we expect that status disparity is negatively related to attracting new investors through its effect on perceived syndicate trust and is positively related to attracting new investors through its impact on perceived future deal flow. Whether the costs of status disparity outweigh its benefits depends upon the level of deal risk. If deal risk is low, status disparity attracts newcomers. In contrast, if deal risk is high, status disparity deters newcomers. Our full conceptual model, shown in Figure 1, depicts the effects of status disparity on venture investment as operating through two mechanisms—perceived syndicate trust and perceived future deal flow—with deal risk affecting the relative strength of each mechanism.

Conceptual model of the effects of syndicate status disparity on newcomer additions.

Data and methods

We test our hypotheses by pairing two studies utilizing complementary methods. In our first study, we use a between-subjects 2 × 2 experimental design in which we randomly assign institutional investors to conditions of status disparity and deal risk. The experimental study permits a direct test of our hypothesized psychological mechanisms and better isolates newcomer choice from syndicate partner search. In our second study, we examine the ecological validity of the experimental findings using archival data on historical venture investments. This approach allows us to determine how likely VC firms are to join an existing syndicate as a function of that syndicate’s status disparity and the risk associated with the venture deal. By using multiple complementary research methods, we attempt to capture the mechanisms underlying investment choices while increasing generalizability through the archival study (Grégoire et al., 2019).

Study 1: an experimental test

The objective of Study 1 is twofold. First, we seek to explore the investment decision context by employing an experimental method using actual investors which allows us to directly measure investors’ decisions and the rationale for those decisions. As such, an experiment allows us to empirically test our mediating mechanisms: perceived future deal flow and perceived syndicate trust. And second, an experiment allows us to isolate the effects of newcomer choice from multiparty syndicate partner search, something which would be more difficult in a field study. Thus, while not as realistic as behavior from the field, demonstrating the mechanism in this context and following it up by exploring whether we observe the same pattern of results in the field bolsters the test of our theory.

Study 1: sample

We recruited 193 participants attending an investor event located in the Northeast United States. The event was a “Demo Day,” which is essentially a showcase event where start-up companies are invited to provide a demonstration of their product or service and pitch to investors. The event was invitation-only for both entrepreneurs and investors. The 100 early-stage entrepreneurs pitching at this event were invited from leading incubators, accelerators, and research institutions to showcase their new ventures. The investors in attendance were composed of approximately 500 active investors affiliated with VC firms that had a prior history of investments in similar companies as those presenting.

We offered each of the 500 investors an opportunity to participate in our study. They were told that the study was for academic research examining investment decisions and that it would require no more than 5–10 minutes of their time. A US$10 Amazon gift card was given to each of the 193 investors who agreed to participate to thank them for their time. Participants in our study had an average of 10 years of investing experience, which provided us with confidence regarding their familiarity with evaluating new ventures and their experience co-investing with other firms. Participants also represented a wide range of major industries, such as Education (4%), Financial Services (14%), Healthcare (9%), Media and Entertainment (6%), Retail (6%), and Technology (17%), among others.

Study 1: design and procedure

After agreeing to participate in our study, investors were given a brief description of a new venture and asked to evaluate that investment opportunity. The description included an overview of the new venture, a summary of its flagship product and two new products currently under development, background information on its founders, a synopsis of its financials, a description of three first-round investors, and an outline of the second-round investment details such as the investment amount and equity stake. These materials were provided on-site, and participants filled out paper surveys at our booth at the Demo Day event. They were given no other information other than these materials, and participants were not told anything further related to our hypotheses or the purpose of the study. We also did not provide any debrief sessions for the participants but instead provided a contact email for any investors who wanted to get more information on the study.

We developed the venture descriptions and materials by following a systematic process. First, we adapted the venture description from one of the nascent ventures in our archival sample to enhance external validity. Second, three institutional investors reviewed the venture description and our survey items, offering suggestions and refinements to bolster content validity. Third, we administered our materials to an online sample of 275 individuals on Amazon MTurk to confirm the factor structure and internal consistency of our scales (Hinkin, 1998). Fourth, we conducted a small pilot study at an annual investor event located in the Southwest United States. This pilot study allowed us to calibrate the amount of venture information to provide as well as the number of survey items that is feasible among a population that mirrors our study sample (see Appendix for study materials).

Participants were randomly assigned to one of four conditions in a two (high-status disparity versus low-status disparity) by two (high deal risk versus low deal risk) between-subjects design. In the high status disparity condition, one of the three first-round investors was described as being “seen by your peers as a high-status VC firm,” another investor was described as being “seen by your peers as a low-status VC firm,” and the final investor was described as being seen as “neither high nor low status (i.e. average).” In the low status disparity condition, all three investors were “seen by your peers as neither high nor low status (i.e. average).” To manipulate deal risk, we explained how the venture’s ultimate success hinged upon two new products currently under development. We focus on the product-related dimension of Tyebjee and Bruno’s (1984) model of deal risk for the sake of parsimony and the ease with which participants can interpret this information. In the high deal risk condition, we stated, “It is unclear whether these products will be successful.” In the low deal risk condition, we stated, “It seems likely that these products will be successful.” Following the venture description, investors were asked to respond to a series of items about the venture and the first-round investors.

Study 1: measures

Newcomer investment intentions

Following Lee and Huang (2018) and Huang and Pearce (2015), investors’ propensity to invest was measured using a 1–7 Agree-Disagree Likert-type scale based on the item, “If given an opportunity, I would invest in this venture.”

Perceived syndicate trust

We measured trust by adapting a trust scale (Mayer and Davis, 1999). Items included: “This group of investors will not take advantage of me,” “This group of investors will be concerned about my welfare,” and “The first-round investors will look out for my interests.” We used the mean across the items (alpha = .86).

Perceived future deal flow

We measured perceived future deal flow based on a scale we developed for this study. Items included: “I expect to do future deals with these investors,” “By investing in this deal, I will increase future deal flow,” “I would like to be associated with these firms,” and “I am interested in working with the first-round firms.” We used the mean across the items (alpha = .83).

Study 1: results

To verify the internal validity of our findings, we conducted a manipulation check. First, to check our status disparity manipulation, we asked, “The status of the first-round investors is similar.” We reverse-scored the item to match our conceptualization of status disparity. Investors in the high status disparity condition had a higher mean (on the reverse-scored item) than investors in the low status disparity condition (t(1, 192) = 7.06, p < .05, Mhigh status disparity = 4.28, Mlow status disparity = 2.70). Second, for our deal risk measure we asked, “There is uncertainty about whether this venture will succeed.” Investors in the high deal risk condition rated this item higher than investors in the low deal risk condition (t(1, 192) = 1.87, p = .06, Mhigh deal risk = 4.43, Mlow deal risk = 3.99).

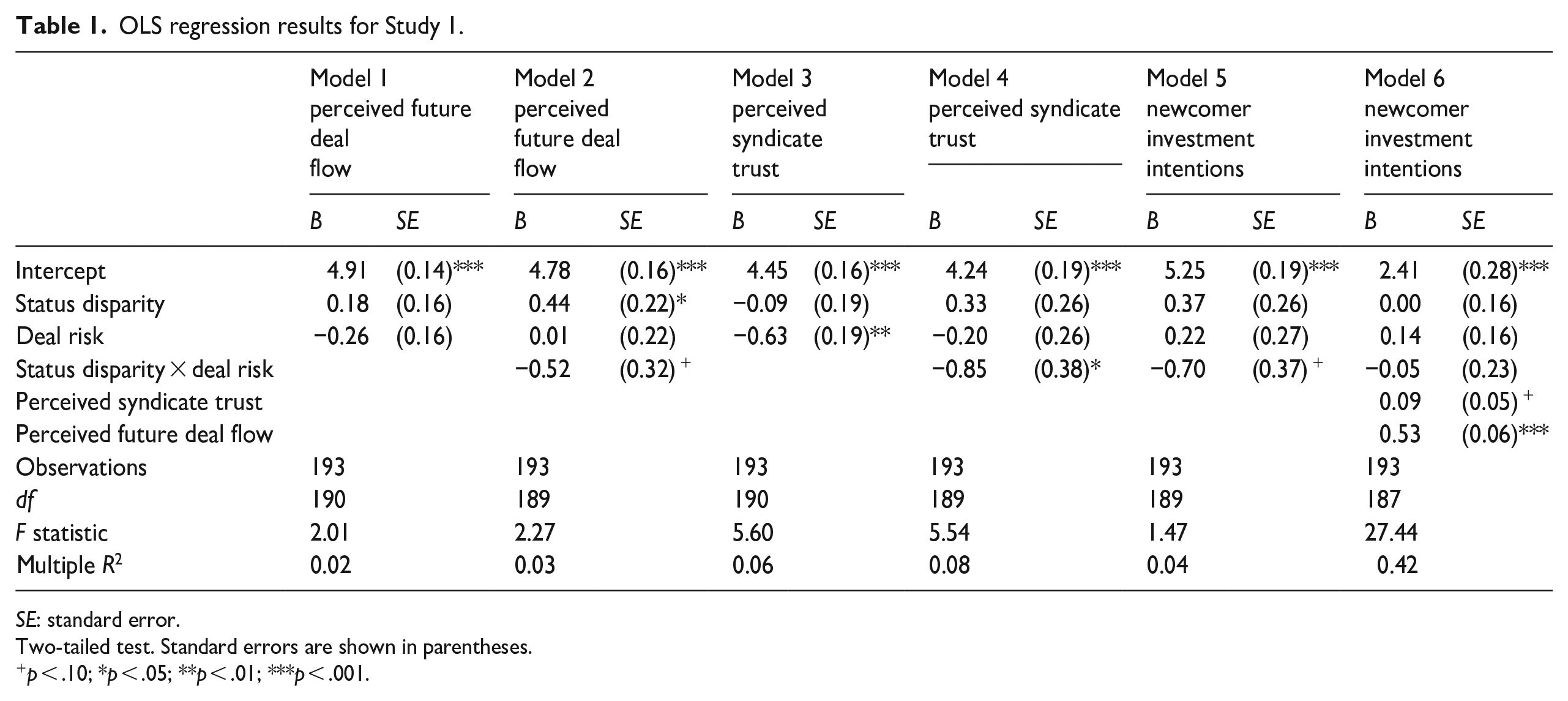

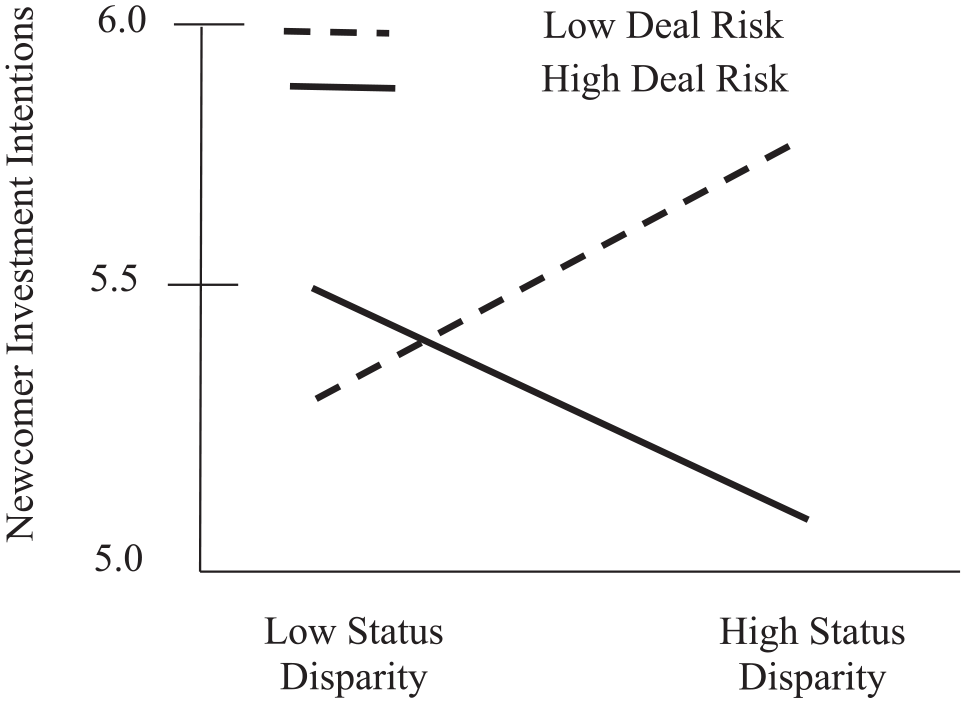

Second, we tested Hypothesis 1, which states that deal risk negatively moderates the relationship between status disparity and newcomer attraction to the syndicate. Model 5 of Table 1 shows our ordinary least squares (OLS) regression results testing Hypothesis 1. We found a marginally significant negative moderation effect (B = −0.70, SE = 0.37, p = .06). We plotted the interaction in Figure 2, which shows that the effect of status disparity on newcomer investment intentions becomes marginally more negative when deal risk is high compared with when deal risk is low. This finding provides partial support for Hypothesis 1.

OLS regression results for Study 1.

SE: standard error.

Two-tailed test. Standard errors are shown in parentheses.

p < .10; *p < .05; **p < .01; ***p < .001.

The moderating effect of deal risk on the relationship between syndicate status disparity and newcomer investment intentions (Study 1).

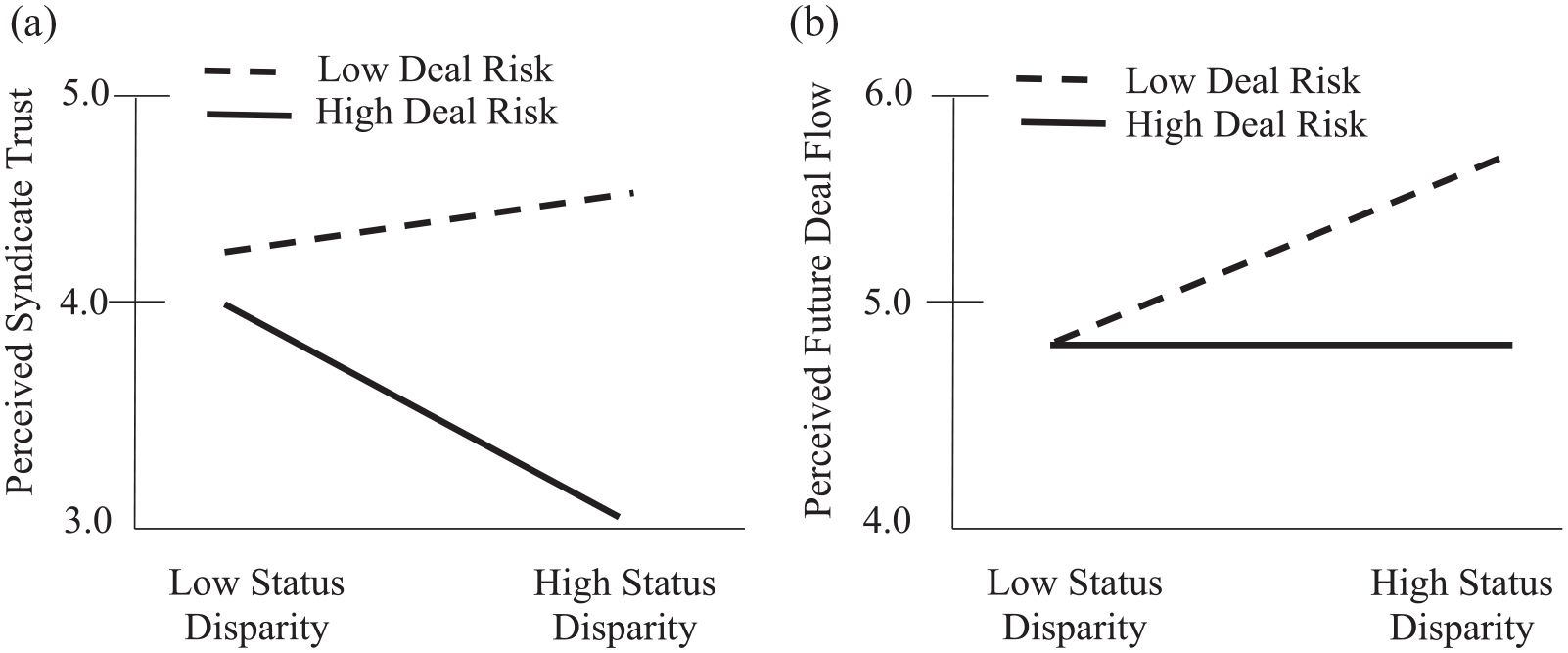

Next, we examined the relationship between status disparity and deal risk in predicting syndicate trust. We calculated a 2 (status disparity) × 2 (deal risk) analysis of variance (ANOVA) predicting syndicate and found a significant interaction between status disparity and deal risk F(1,189) = −5.17, p = .02. Our OLS regression analysis, presented in Model 4 of Table 1, also shows a significant negative interaction (B = −0.85, SE = 0.38, t = −2.27, p = .02).

Figure 3(a) shows that when deal risk is low, perceptions of syndicate trust were no different for ventures with high status disparity (Mhigh-status disparity = 4.57, SD = 1.24) compared with ventures with low status disparity (Mlow-status disparity = 4.24, SD = 1.39, t = 1.24, p = .22). However, when deal risk is high, ventures with high status disparity (Mhigh-status disparity = 3.51, SD = 1.28) were marginally negatively related to perceptions of trust than ventures with low status disparity (Mlow-status disparity = 4.03, SD = 1.30, t = 1.97, p = .05). Thus, status disparity is marginally negatively related to trust but only when deal risk is high (Est. = −0.52, SE = 0.27, t = −1.95, p = .05).

The moderating effect of deal risk on the relationship between syndicate status disparity and trust and future deal flow (Study 1).

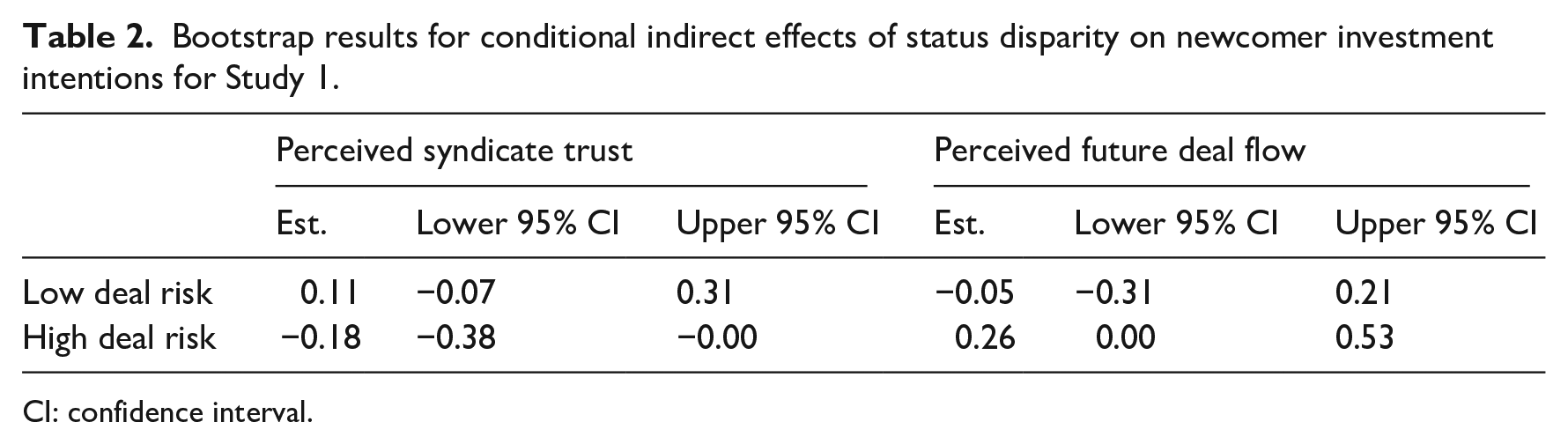

To test Hypothesis 2, we employ Hayes’ (2012) procedure for moderated mediation with bootstrapping (10,000 draws), presented in Table 2. At high levels of deal risk, we found an indirect effect of status disparity on newcomer investment intentions through perceived trust (Est. = −0.18, 95% CI(−0.38, −0.00)). However, at low levels of deal risk, we did not find evidence of an indirect effect of status disparity on investment decisions through trust (Est. = 0.11, 95% CI(−0.07, 0.31)). Status disparity is negatively related to newcomer investment intentions because it undermines syndicate trust but only when deal risk is high. These indirect effects are consistent with Hypothesis 2.

Bootstrap results for conditional indirect effects of status disparity on newcomer investment intentions for Study 1.

CI: confidence interval.

Next, we examined the relationship between status disparity and deal risk in predicting perceived future deal flow. We calculated a 2 (status disparity) × 2 (deal risk) ANOVA predicting perceived deal flow. The main effect of status disparity was not significant F(1,189) = 1.41, p = .24, and the main effect of deal risk was also not significant F(1,189) = 2.64, p = .11). We found a marginally significant interaction between status disparity and deal risk F(1,189) = 2.75, p = .099. The OLS regression analyses, presented in Table 1, also show a marginally significant interaction (B = −0.52, SE = 0.32, t = −1.66, p = .099).

Figure 3(b) shows that when deal risk is low, ventures with high status disparity (Mhigh-status disparity = 5.22, SD = 1.10) were more positively related to perceptions of future deal flow than when status disparity was low (Mlow-status disparity = 4.78, SD = 1.09, t = 2.00, p = .049). However, when deal risk is high, ventures with high status disparity (Mhigh-status disparity = 4.70, SD = 1.12) are no more attractive as an investment than when status disparity was low (Mlow-status disparity = 4.78, SD = 1.08, t = −0.37, p = .71). Thus, status disparity is positively related to perceptions of future deal flow but only when deal risk is low (Est. = 0.45, SE = 0.22, t = 2.00, p < .05).

To test Hypothesis 3, we again employ Hayes’ (2012) procedure for moderated mediation with bootstrapping (10,000 draws) to test the conditional indirect effect of status disparity on newcomer investment intentions via perceived future deal flow at different levels of deal risk. At high levels of deal risk, we found no indirect effect of status disparity on investment intentions through perceived future deal flow (Est. = −0.05, 95% CI(−0.31, 0.21)). However, at low levels of deal risk, we found a significant indirect effect of status disparity on investment intentions through perceived future deal flow (Est. = 0.26, 95% CI(0.00, 0.53)). These results are consistent with Hypothesis 3. Status disparity is positively related to newcomer investment intentions because it enhances perceptions of deal flow benefits but only when deal risk is low.

Study 1: discussion

Study 1 uses an experimental context to demonstrate that status disparity enables syndicates to attract newcomers when deal risk is low but deters newcomers when deal risk is high. In the context of a controlled study design with actual venture investors, we were also able to directly measure and test the mechanisms proposed in our theory. We found support for the notion that, at low levels of deal risk, status disparity increases perceptions of future deal flow. In addition, we found evidence consistent with the prediction that at high levels of deal risk, status disparity decreases perceptions of syndicate trust.

Study 1 should also be interpreted in light of two important limitations. First, we only measure hypothetical newcomer investment intentions and do so on the basis of limited information. Investors often conduct extensive due diligence when choosing whether to join a syndicate. Conducting an experiment that required in depth due diligence was not practically feasible with our sample and thus constitutes a limitation in our results. Second, our experiment did not allow us to disentangle the effects of syndicate status disparity from syndicates that have a single high-status investor. We aim to address these limitations in Study 2.

In Study 2, we examine the ecological validity of our model by examining newcomer additions to multiparty syndicates in the field. Even though this approach cannot fully isolate the syndicate’s search from the newcomer’s decision to join, as we did in our experiment, this setting does allow us to see if the overall pattern of newcomer additions in the field is consistent with the experimental results we observed in Study 1. In addition, our field data also allow us to disentangle the effects of having a single high-status investor from the effects of high syndicate status disparity as well as the impact of the newcomer’s status, neither of which was measured in the first study.

Study 2: sample and procedure

To demonstrate the ecological validity of our theory, we drew data from the Preqin Venture Capital Online database (www.preqin.com/data/venture-capital) which provides comprehensive information on US VC investments (Ewens et al., 2013; Hochberg et al., 2018). This database includes new venture-VC funding transactions across industries. Investors include both large VC funds, such as Sequoia Capital, as well as corporate VC funds, such as Siemens Venture Capital (now called next47). Our data spans 1999–2016, including 9241 new ventures, 6052 unique investors, and 35,766 funding rounds. Since we were investigating the impact of status disparity of the syndicate on attracting additional investors, we only considered for our analyses new ventures that had received first-round funding between 1999 and 2010, allowing for a 6-year time lag between first-round and second-round funding. In our sample the average time lag between first- and second-round funding is 1.53 years with 99.6% of all second-round investments occurring within 5 years of the first round, which reduces concerns over censoring. We also focused only on syndicates that had at least two investors in the first round and second round, which is consistent with past research on multiparty syndicates and syndicate status disparity (Zhang and Guler, 2020). Our final sample includes data from 3644 multiparty syndicates.

In addition, we also constructed intellectual property portfolios based on US Patent and Trademark Office data. For ventures included in our sample, we gathered information about their patenting activities between 1999 and 2006 using the National Bureau of Economic Research, and patent data from 2006 to 2010 using the Fung Institute database. We also used SDC Platinum to collect industry-related data and strategic alliances formed between 1999 and 2010. For each of these additional data sources, we matched the new venture names from Preqin with the firm names listed in the other databases using a language-matching algorithm that computes text similarity based upon Jaccard’s distance. We accepted as matches all ventures with a similarity score of 1.00 and manually identified matches with a similarity score between 0.90 and 1.00 (533 ventures with at least one patent, 326 ventures with at least one alliance).

Study 2: measures

New investor tie

Our primary outcome variable involves a tie forming between a new investor and an existing syndicate. Because we are interested in the behavior of prospective investors rather than the continued investment of existing investors, we examine the ties formed between a syndicate and new investors that were not previously part of the first round of funding. To do this, we focus on which multiparty syndicate a new investor joins in the second round of funding.

Status disparity

We operationalize syndicate status disparity using the coefficient of variation in status among second-round investors (Harrison and Klein, 2007). This operationalization of disparity accounts for variation in syndicate status relative to the syndicate’s mean status level. This operationalization is beneficial because it enhances the comparability of disparity effects across syndicates that differ with respect to their mean status level (Harrison and Klein, 2007). To calculate status disparity, we followed four steps. First, we constructed the social network of each second-round investor that was also a member of the first-round syndicate. We consider a tie to exist between two investors when the focal investor has co-invested with another investor in any of the 5 years preceding the year of the focal investment (Sorenson and Stuart, 2001; Ter Wal et al., 2016). Second, we calculated the status of each investor using an eigenvector centrality measure (Bonacich, 2007). In the context of VC networks, eigenvector centrality is based upon the total number of ties held by all co-investors; that is, eigenvector centrality considers the centrality of a focal investor’s co-investors (Podolny, 2001). This measure of status, therefore, captures not just degree centrality of the focal investor (i.e. the total number of co-investors) but also the connectedness of those co-investors within the broader network of investors (Shipilov and Li, 2008). Third, we calculated the status disparity of the syndicate using the standard deviation of the status level for each second-round continuing investor. Fourth, we divided the standard deviation of the status for continuing second-round investors by the syndicate’s mean status level to account for the degree of variation relative to the mean (Harrison and Klein, 2007). In our robustness checks, we also considered alternative operationalizations of status disparity, which we describe below.

Deal risk

We operationalize deal risk based on three out of the four factors identified by Tyebjee and Bruno (1984). First, for the product-related component of deal risk, we include a binary measure based on whether or not a venture holds a patent. Patents are often interpreted by investors as a signal of underlying product quality (Zott and Huy, 2007) and serve as a barrier to entry that protects the new venture’s competitive advantage from expropriation by rival firms (Hsu and Ziedonis, 2013). We reversed-scored this measure to match our conceptualization of deal risk. Second, as part of the environmental threats component of deal risk, we include a binary measure of strategic alliances because partnering with incumbent firms can help new ventures gain legitimacy and provide access to additional markets and resources to grow the venture. Yet, alliances can also pose downside risk to the venture to the extent that the incumbent firm expropriates value from the venture (Katila et al., 2008). We reverse-score this measure to match our conceptualization of deal risk. And third, based on the market dimension of deal risk, we included a measure of industry dynamism to reflect the extent to which the industry environment in which the venture operates has a high degree of volatility. Specifically, we employ Dess and Beard’s (1984) widely used measure of industry dynamism (Girod and Whittington, 2017) and operationalize industry dynamism as the volatility in the rate of change of annual industry sales (i.e. the standard error of the rate of change of annual industry sales). We did not include a component for the fourth dimension of deal risk, managerial capabilities, because we did not have access to detailed information about the human capital of the venture’s founding team. Before combining these three components into an index of deal risk, we first standardized them (since they operate on different scales) and then used the mean values for each unique venture. In our robustness checks, we also examined alternative operationalizations of deal risk, which we describe below.

Control variables

Our control variables are organized according to two levels of analysis. First, we measure certain control variables at the venture level to account for the fact that characteristics of the venture contribute to downstream funding. Because downstream financing is influenced by initial funding (Shane and Cable, 2002), we include first-round funding amount. The second set of control variables is at the level of the syndicate. Because our interest focuses on the effects of status disparity, we calculated maximum status of the second-round syndicate members to disentangle the effect of status disparity from having a single high-status investor in the syndicate. We account for newcomer status since high-status newcomers are likely more attractive partners to add to existing syndicates (Podolny, 2001). We also included syndicate size as a control variable since larger syndicates might have a larger pool of resources, enhancing the venture’s future attractiveness to newcomers (Lerner, 1994). Furthermore, we include a control variable for repeat first-round investors based on the proportion of first-round syndicate members who were also part of the second-round syndicate since this could affect the syndicate’s willingness to search for newcomers and newcomers’ interest in joining. Since brokerage opportunities could attract new investors, we included a control for structural holes based upon the extent to which each investor in the syndicate had access to disconnected segments of the broader investor network. We calculate structural holes by first calculating network constraint based upon the number of ties among network actors over the maximum number of possible ties, N × (N−1) / 2, where N is the network size. The measure is then reversed to match the conceptualization with Burt’s measure with scores ranging from 0 (fully closed network) to 1 (fully open networks) (see also Fleming et al., 2007). We also accounted for industry knowledge diversity of the syndicate since access to different knowledge bases could aid the development of the venture (Sorenson and Stuart, 2001; Ter Wal et al., 2016), thus increasing its ability to secure new investors. To calculate this variable, we first identified the number of different industries each investor in the syndicate had invested in since 1999. We then aggregated the number of unique industries of investment across all continuing investors in the second-round syndicate. Finally, we calculated the variety of industries represented in the syndicate using Blau’s (1977) heterogeneity index. To address the potential that new investors’ ties to the syndicate might shape the decision to join, we calculated each newcomer’s total number of prior co-investments with every other syndicate member, which we denote as newcomer prior co-investment (Zhang et al., 2017). Finally, we also recognize that investment patterns may vary by year based on economic cycles and thus included year fixed effects. And, because VC investment varies by industry, we included fixed effects for each industry.

Analytical approach

Because our dependent variable is based on whether or not a tie forms, we use logistic regression to model our binary outcome variable of newcomer tie formation. To test our hypotheses, we follow the “potential dyads” approach as outlined in Ter Wal et al. (2016). We used a coarsened matching approach to match each newcomer that joined a syndicate in the second round to 10 random alternative second-round syndicates that also invested in a venture in the same year but did not form a tie with the focal newcomer. We therefore test our model using a sample of newcomer-syndicate dyads that did and did not form ties.

Study 2: results

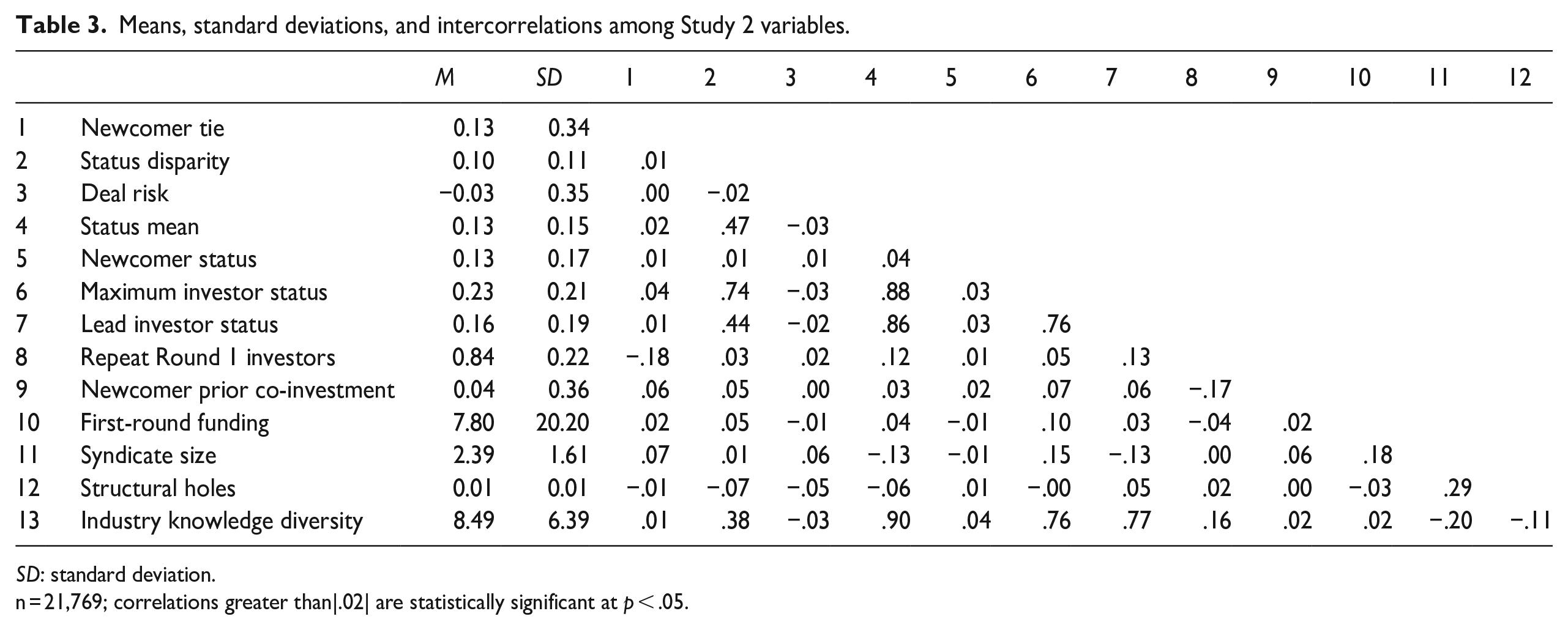

Table 3 provides descriptive statistics for and correlations among study variables. Table 4 is used to test Hypothesis 1 regarding the negative moderating effect of deal risk on the relationship between status disparity and newcomer tie formation.

Means, standard deviations, and intercorrelations among Study 2 variables.

SD: standard deviation.

n = 21,769; correlations greater than|.02| are statistically significant at p < .05.

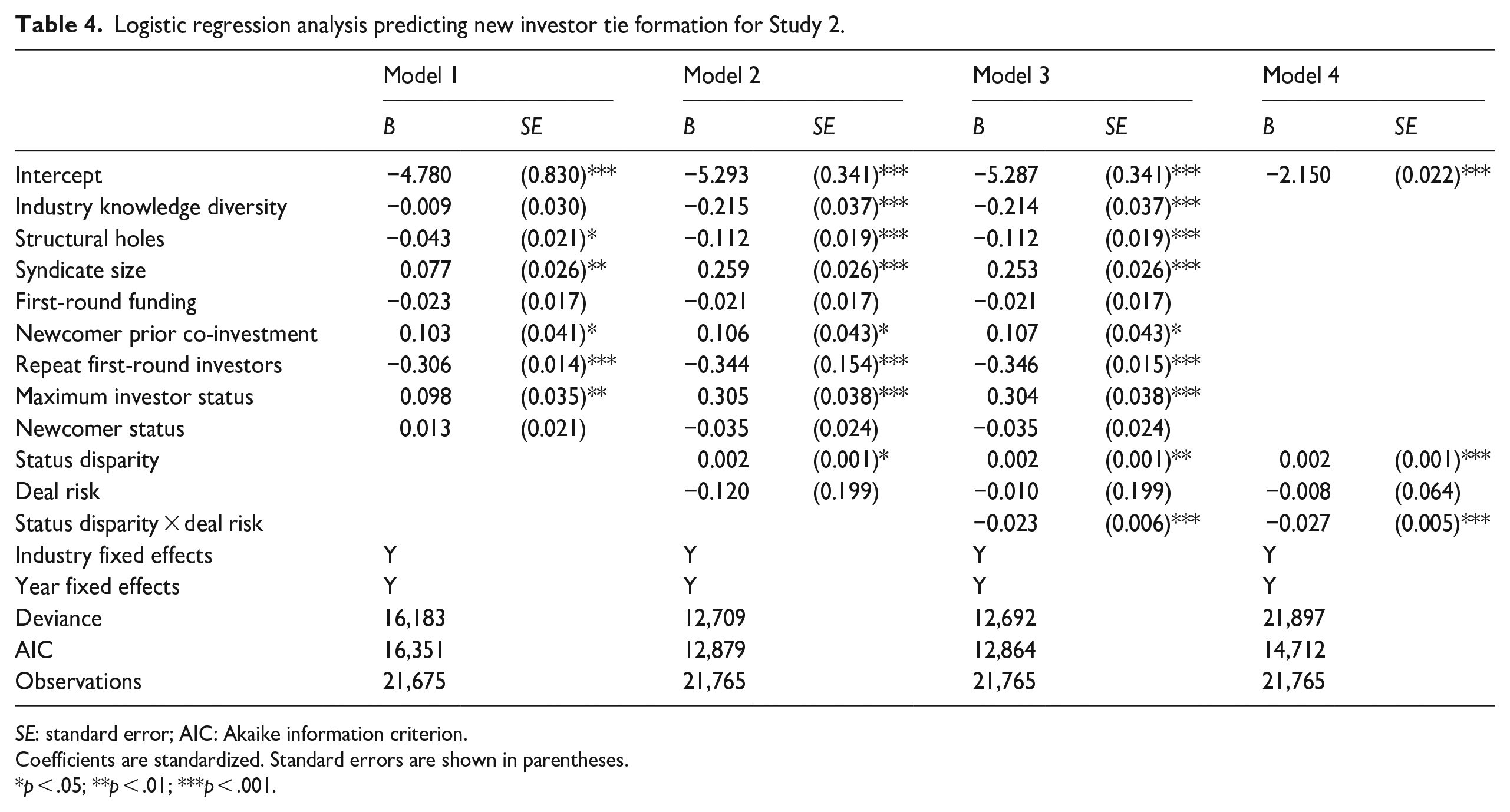

Logistic regression analysis predicting new investor tie formation for Study 2.

SE: standard error; AIC: Akaike information criterion.

Coefficients are standardized. Standard errors are shown in parentheses.

p < .05; **p < .01; ***p < .001.

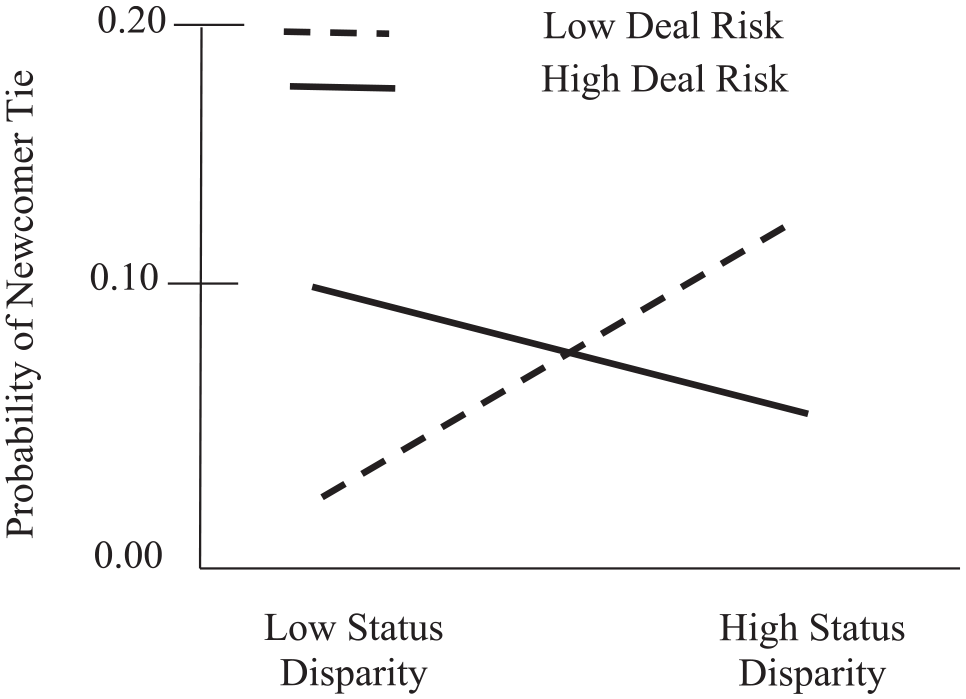

Model 3 of Table 4 shows the results of our logistic regression models. We found a significant interaction between status disparity and deal risk predicting the new investor tie formation (B = −0.023, SE = 0.004, p < .001). We plotted the interaction in Figure 4. At high levels of deal risk, there is a negative relationship between status disparity and newcomer tie formation (Est. = −0.044, SE = 0.018, t = −2.46, p = .014). At low levels of deal risk, there is a positive relationship between status disparity and tie formation (Est. = 0.104, SE = 0.021, t = 5.04, p < .001).

The moderating effect of deal risk on the relationship between syndicate status disparity and attracting new investors (Study 2).

Our results suggest that deal risk negatively moderates the relationship between status disparity and attracting new investors to the syndicate. When deal risk is low, status disparity is positively related to newcomer tie formation, but when deal risk is high, status disparity is negatively related to newcomer tie formation. Collectively, these findings provide support for Hypothesis 1.

Robustness checks

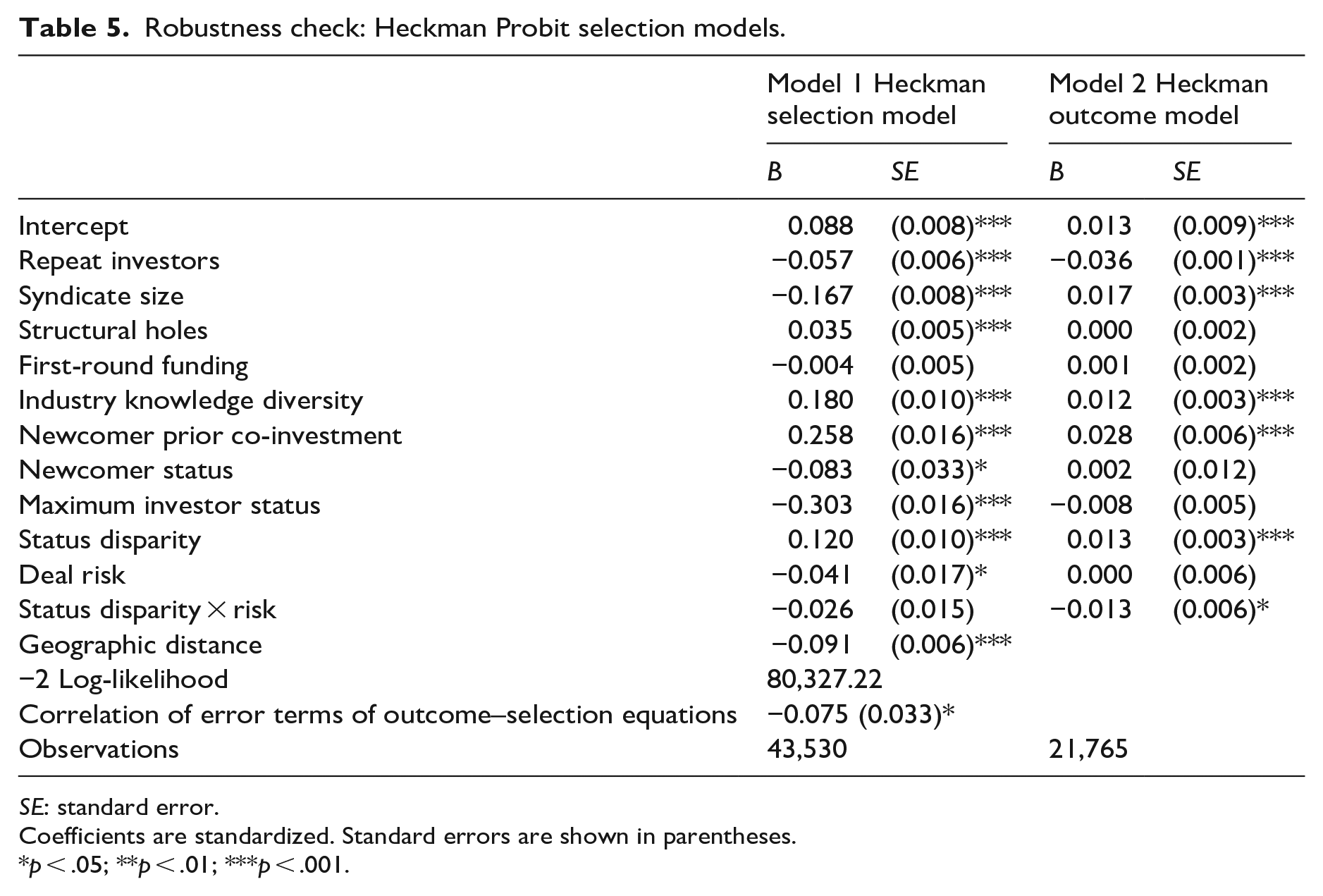

To provide further confidence in our findings, we conducted a series of robustness checks to examine the sensitivity of our modeling assumptions. Rather than including the maximum investor status as a control variable, we included models with the mean status level of the syndicate. Because the mean status of the syndicate is so highly correlated with the maximum investor status, we did not include this control in our final models. Our findings are similar when including mean status rather than maximum investor status as a control. Next, we examined the sensitivity of our models to the exclusion of all control variables (see Model 5 of Table 4) and again found consistent effects. We also conducted a series of robustness checks examining alternative operationalizations of status disparity (e.g. standard deviation of syndicate status, dyadic status differences, Bonacich power, Coefficient of Variation for first-round syndicate status). Furthermore, we examined the effects of different forms of our deal risk index, including either individual components of deal risk (i.e. patents, alliances, industry dynamism) or different combinations of two index components (e.g. patents and dynamism, patents and alliances). Across each of these different operationalizations of status disparity and deal risk, we found that our results were consistent with our main analyses.

We also addressed potential selection effects. We examined the possibility that our results might be driven by the ability of syndicates with high status disparity to select more promising ventures. Specifically, we constructed Heckman Probit selection models by adopting the approach by Hallen (2008: 717). We matched a focal venture where a syndicate in our sample made a first-round investment to a random alternative venture that also received first-round investment in the same year but from a different syndicate. In our first stage model, we predicted the likelihood of a venture-syndicate dyad to be successfully paired (i.e. syndicate funds venture) in the first round, among both the observed focal dyads and the randomized venture-syndicate potential dyad. In our first stage model, we also included geographic distance between the venture and the lead investor as our instrumental variable. We chose geographic distance because the proximity of a venture may make the lead investor more aware of some particular ventures than others, thus affecting the odds of its selection for initial funding (Sorenson and Stuart, 2001). But, at the same time, geographic distance should not have a meaningful effect on the likelihood of further funding by a newcomer in the second round and thus was excluded from our second stage model (Ter Wal et al., 2016). In our second stage model, we predict the formation of a newcomer tie. These models are estimated simultaneously based on maximum likelihood estimation. Table 5 shows the results of these analyses. Model 1 is the first stage selection model, and Model 2 is the second stage outcome model. The results in Model 2 show that our findings remain robust.

Robustness check: Heckman Probit selection models.

SE: standard error.

Coefficients are standardized. Standard errors are shown in parentheses.

p < .05; **p < .01; ***p < .001.

Post hoc analysis

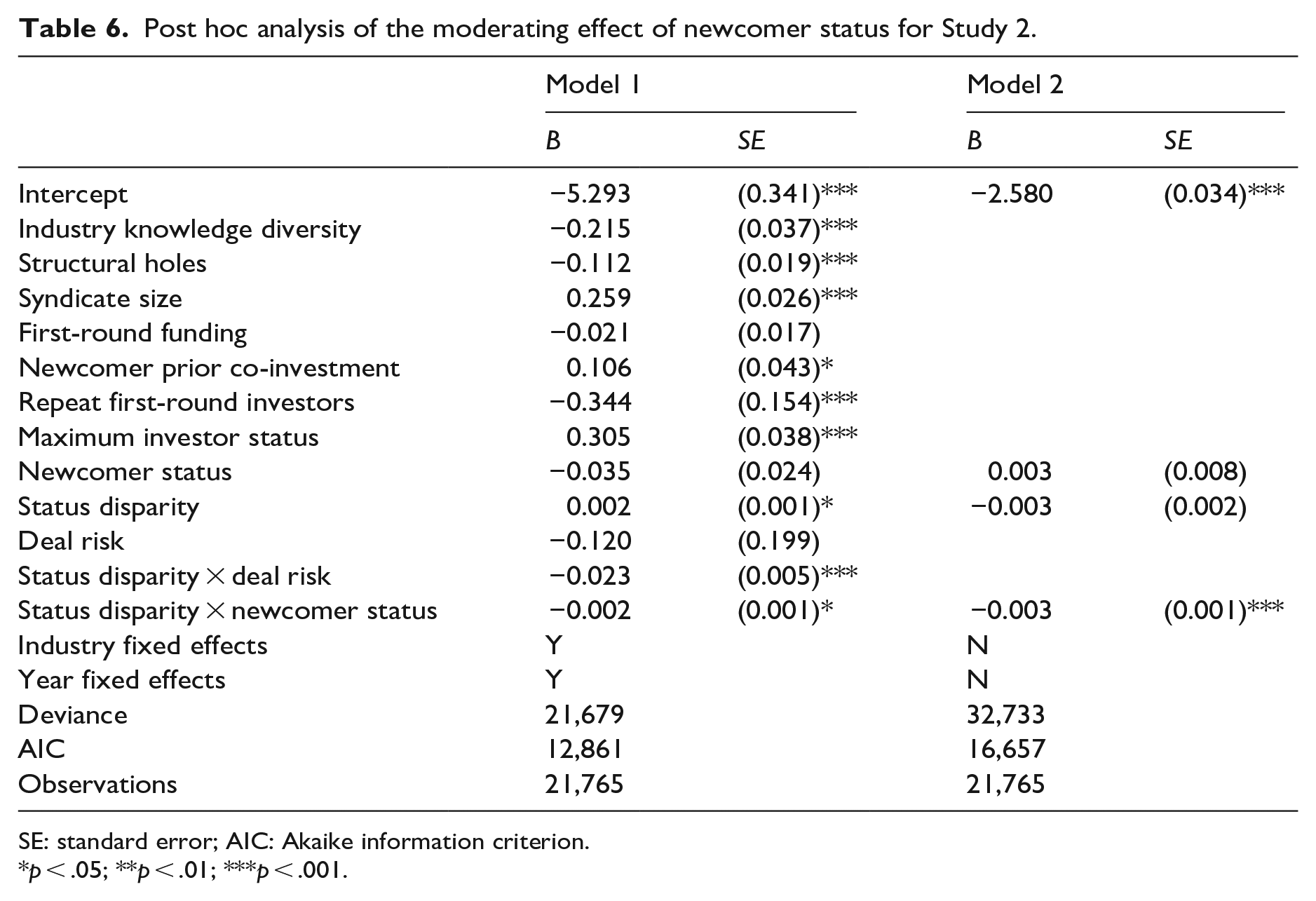

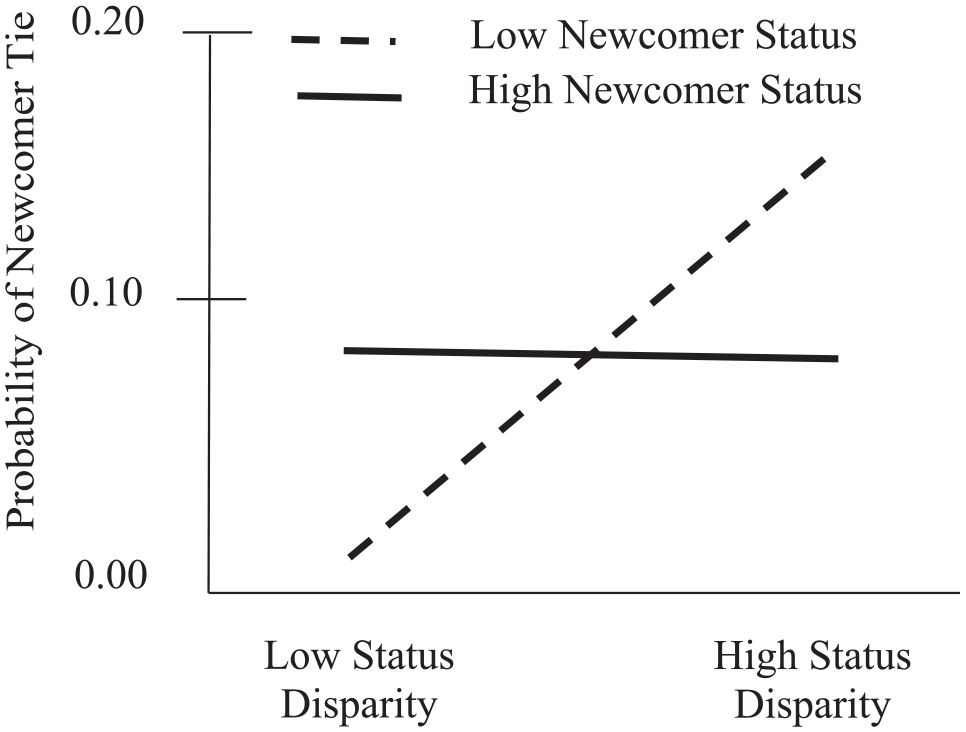

We incorporated newcomer status as a control variable in our main analyses. However, it remains an open question about whether the effects of status disparity might depend upon the newcomer’s status. Even though the theoretical logic is unclear regarding the precise nature of how newcomer status might moderate the effect of status disparity on newcomer additions, we were able to explore this question empirically with our Study 2 data. Model 1 of Table 6 shows a significant moderating effect of newcomer status on the relationship between status disparity and newcomer additions (B = −0.002, SE = 0.001, p = .022). To understand the nature of the interaction, we plotted it in Figure 5. At high levels of newcomer status, there is no relationship between status disparity and newcomer tie formation (Est. = −0.000, SE = 0.000, t = −0.29, p = .773). At low levels of newcomer status, there is a positive relationship between status disparity and tie formation (Est. = 0.001, SE = 0.000, t = 3.42, p < .001). These findings raise several new questions about newcomer status. Specifically, why are newcomers with low status more attracted to status disparity than high-status newcomers? Do these moderation effects operate through our proposed mediators of perceived future deal flow and perceived syndicate trust? If so, why are low-status newcomers are willing to sacrifice on potential trust-related concerns for the sake of generating future deal flow? And, is it the case that high-status newcomers are not drawn to status disparity because their own status directly affords ample access to deal flow? Examining these questions and others about how newcomer status affects the syndication process could be a promising direction for future research.

Post hoc analysis of the moderating effect of newcomer status for Study 2.

SE: standard error; AIC: Akaike information criterion.

p < .05; **p < .01; ***p < .001.

Post hoc analysis of the moderating effect of newcomer status on the relationship between syndicate status disparity and attracting new investors (Study 2).

Study 2: discussion

The findings from Study 2 provide support of our hypothesis that deal risk moderates the relationship between status disparity and attracting newcomers. When deal risk is high, newcomers are deterred from syndicates with high-status disparity, but when risk is low, newcomers are attracted to syndicates with high-status disparity. An advantage of this study is that it provides ecological validity to the findings from the experiment, meaning that our results suggest that status disparity seems to operate in a way that is consistent with the findings from Study 1 and in the context of actual venture investment. Study 2 also allowed us to address certain limitations of Study 1. Specifically, we can disentangle the effects of status disparity from the effect of having a single high-status investor. Furthermore, we can account for the status of the newcomer to address the robustness of these effects relative to the newcomer’s own status.

Despite these, however, our results should be interpreted in light of three empirical limitations. First, our use of archival data limits our ability to directly measure the mediating mechanisms in our model. Thus, we did not replicate our full model, which included our intervening mechanisms. Second, our archival data only capture successfully formed newcomer-syndicate ties. This conflates the effect that status disparity has on the search for newcomers with the newcomer’s attraction to syndicates characterized by status disparity. Our inability to disentangle these two aspects of the tie formation process using our archival data further complicates our ability to directly test our proposed mechanisms.

General discussion

We theorized that status disparity among investors within an existing syndicate is a double-edged sword for potential newcomers to the syndicate. On one hand, status disparity implies an imbalance of status within the group that may signal a wide range of preferences that can undermine syndicate trust. On the other hand, status disparity also implies that syndicate members occupy an eclectic mix of network positions, which could increase newcomers’ access to a diverse set of future investment opportunities. We reconcile these countervailing mechanisms by proposing that whether the benefits of status disparity outweigh the costs depends on deal risk. For ventures with lower risk, the future deal flow benefits of status disparity appear to become more salient for newcomer, whereas for ventures with higher risk, a lack of syndicate trust seems more significant.

Consistent with our model, we found that the effects of syndicate status disparity can be either negatively or positively related to attracting new investors. In our experimental study, we showed that new investors’ perceptions of future deal flow and syndicate trust partially mediate the effect of status disparity on investment intentions. In our archival study of new venture investment, we found that syndicate status disparity was positively related to attracting new investors when deal risk was low but negatively related to attracting new investors when deal risk was high.

Theoretical implications

Our findings offer three theoretical contributions. First, prior theory and research on multiparty syndicates has traditionally emphasized how status disparity affects the search for new investors (e.g. Zhang et al., 2017; Zhang and Guler, 2020). Less emphasized in theory regarding multiparty syndicates is the effect of status disparity on attracting newcomers. We augment that research by offering an alter-centric view of status disparity to consider how a newcomer evaluates syndicate status disparity and thus clarify when such disparity will attract versus deter new investors from joining in subsequent funding rounds. Consistent with prior research on multiparty syndicates, we highlight how status disparity evokes concerns over trust (e.g. Zhang et al., 2017). Unlike this prior work, however, we find that those trust concerns are resolved based on features of the venture deal itself. This finding illuminates an important distinction between the two sides of the syndication equation. Whereas the syndicate’s search for newcomers revolves around attributes of the newcomer, for the newcomer, the choice is twofold: they must opt-in to both the syndicate and the venture. In addition, we show that these two aspects of the newcomer’s decision are interrelated. The same features of a syndicate (i.e. status disparity) that attract a newcomer can, in some circumstances, deter them, depending upon the interrelationship between the syndicate’s social context and the nature of the venture. The newcomer, therefore, faces a fundamentally different decision in choosing to join an existing syndicate than the syndicate faces in choosing a newcomer to add in a later investment round. Our article illustrates the newcomer’s side of the syndication process and shows the ways each side of the syndication process differs from the other.

Second, we also contribute to the literature on multiparty syndication by building upon recent work which focuses on the impact of collective, group-level mechanisms. Prior theory and research on syndication has traditionally emphasized the formation of bilateral partnerships between pairs of individual firms (Das and Teng, 2002; Lavie et al., 2007). Yet, syndication often entails more complex relational configurations that invoke higher order mechanisms (Zhang et al., 2017). By examining the role of status disparity in multiparty syndicates, we extend recent research on how group-level phenomena impact these collaborations. This work has initially focused on how group qualities (e.g. faultlines, status disparity, syndicate size) shape the selection of specific newcomers. Our article considers how newcomers evaluate those group qualities prior to joining a group and thus demonstrates that newcomers see certain group qualities as a double-edged sword, entailing both costs and benefits. We highlight the need for research on collective mechanisms in multiparty syndication to consider both the group’s structure (e.g. status disparity) and the group’s task (e.g. deal risk). Our work also suggests that there are other group-level properties (e.g. diversity) that affect the evolution of multiparty syndicates, thus broadening the conversation on venture syndication and entrepreneurship.

Third, and more broadly, we contribute to theories of power and status in teams. This literature has focused heavily on the role of status disparity in shaping group functioning and decision-making after the group has already formed (Bunderson and Van der Vegt, 2018). We highlight how status disparity acts as a signal that potential newcomers use, ex ante, to decide whether to join the group in the first place. In other words, status disparity affects not only the functioning of a group after it has formed but also how prospective group members choose whether or not to join the group. In explaining how status disparity affects new member additions, we show how newcomers weigh the potential trust-related costs versus the deal flow-related benefits of joining a group characterized by status disparity and then how newcomers resolve this tension by assessing the degree of risk involved in a particular collaboration. In developing our model, we build upon resource dependence theory, which argues that entrepreneurial firms carefully weigh the risks of misappropriation versus resource gain when choosing partners (Pahnke et al., 2015). This work highlights how entrepreneurial firms resolve this tension through the use of certain defenses (e.g. trade secrets, third-party monitors) that they can put in place prior to forming a tie with an incumbent firm (Hallen et al., 2014; Katila et al., 2008). We extend this work by showing that even in the absence of these protective mechanisms, newcomers may still be willing to “swim with sharks” by strategically selecting lower risk collaborations that are less likely to trigger the possibility of misappropriation.

Limitations and avenues for future research

We acknowledge several limitations which present opportunities for future research. First, our findings about the effects of status disparity should only be interpreted in the context of new venture investment by VC firms. It is unclear whether these effects of status disparity would generalize to other forms of group collaboration. Future research should explore whether status disparity works differently in alternative contexts. Second, our results cannot speak to the impact of syndicate status disparity on later-stage ventures. Because our sample involves early-stage ventures, we cannot assert that the pattern of results would be similar for more mature ventures. It is likely that for more developed ventures the magnitude of the benefits and costs posed by status disparity could weaken as the performance track record of the venture becomes more established. Additional work is needed to examine how status disparity operates for more established ventures. Third, our sample includes only institutional investors, which collectively represent a small fraction of the total population of investors. Even though VC funding does account for a significant portion of all startup investment, other forms of investment are becoming increasingly popular and warrant further examination. How status disparity is perceived by angel investors or crowdfunding investors, for example, remains an open question.

Conclusion

Multiparty syndicates are an increasingly common vehicle for venture investment. To unlock the full potential of these syndicates, new investors often need to be added in subsequent rounds. We extend prior work on the role of status in the syndication process by considering the impact of syndicate status disparity on newcomers’ willingness to join a multiparty syndicate. We show that syndicate status disparity is a double-edged sword for attracting new investors to join in later rounds of financing, simultaneously offering newcomers possible access to future deal flow as well as undercutting perceptions of syndicate trust. For newcomers deciding whether to join a syndicate, the benefits of syndicate status disparity outweigh its costs when deal risk is low, but its costs outweigh its benefits when deal risk is high. Given that status differences are ubiquitous in VC syndicates, our findings provide insights to entrepreneurs and investors about how status disparity affects the investment process.

Footnotes

Appendix

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.