Abstract

When can corporate social responsibility become a reliable strategic asset? There is a scarcity of both theoretical arguments and empirical evidence investigating the trade-off between the risk and return of corporate social responsibility. We intend to fill this gap by (1) investigating corporate social responsibility’s simultaneous impact on firm value and the reliability of this impact and (2) exploring the conditions under which corporate social responsibility’s impact on firm value becomes more or less reliable. The presented findings suggest that corporate social responsibility by itself is an unreliable value enhancer, in that it not only increases firm value but also increases the variance of expected value distribution. Yet, the impact of corporate social responsibility on firm value becomes more reliable when a firm has immediately redeployable slack or when a firm has stronger risk management capabilities. This research provides practical implications to managers and investors regarding the riskiness of corporate social responsibility investments and strategies for mitigating such risks.

Keywords

Introduction

The relationship between corporate social responsibility (CSR) and firm value is one of the most important yet controversial topics in the management field. Over the past few decades, scholars have made countless attempts to shed light on the fundamental proposition about whether firms can do well financially by doing good socially (e.g. Barnett et al., 2020; Gras and Krause, 2020; Hillman and Keim, 2001; Jayachandran et al., 2013; Lu et al., 2021; Orlitzky et al., 2003). Along these lines, the instrumental approach to CSR treats CSR engagement as a deliberate investment for long-term financial gain (Jones, 1995). By considering stakeholders’ interests in a firm’s resources allocation, a firm accumulates moral capital (Godfrey et al., 2009) or builds stakeholder trust (Mishra and Modi, 2013), thereby buffering itself from negative shocks (e.g. Muller and Kräussl, 2011; Shiu and Yang, 2017) and increasing efficiencies of business operations (e.g. Flammer, 2018; Flammer and Luo, 2017).

Although a majority of researchers point out that firms can do well by doing good from an instrumental point of view (Flammer, 2013, 2015; Godfrey et al., 2009; Orlitzky et al., 2003), this proposition has also been doubted by many others (e.g. List and Momeni, 2017; Masulis and Reza, 2015). On one hand, scholars argue that the proposition of “doing well by doing good” is contingent on contextual factors, such as economic development (e.g. Wang et al., 2016), organizational attributes (e.g. Sun et al., 2019), institutionalization stage of CSR (Brower and Dacin, 2020), industry characteristics and dynamics (e.g. Gras and Krause, 2020), and stakeholders’ characteristics (Wiengarten et al., 2017). On the other hand, the opponents of the “doing well by doing good” proposition stress that it is not uncommon to observe a non-significant, in many cases even negative, relationship between CSR and firm value. This negative relationship between CSR and value may be caused by a high opportunity cost (Friedman, 1970) or agency problem (Masulis and Reza, 2015). A negative relationship might also occur when the costs of CSR are higher than the benefits accrued from it. For example, through an experiment, List and Momeni (2017) found that CSR performance increases employee misbehavior and shirking through the cognition effect of moral licensing: When employees feel that they have done “good” in one dimension, they later feel less morally constrained and hence misbehave in other dimensions (Bénabou and Tirole, 2010).

The abundant current research regarding the possible negative impact of CSR for certain firms questions the monotonicity of the efficacy of CSR. In other words, even though CSR has shown to increase value for some firms, it may make many other firms worse off. If CSR does not always lead to better performance, diverting valuable and scarce resources to CSR activities is fundamentally a risky investment decision to make. This uncertainty of achieving the expected outcome from CSR constitutes the risky nature of CSR. However, when assessing CSR’s impact on firm value, the current literature generally overlooked the riskiness of CSR investments. In other words, it mainly focuses on the change in the level of firm value (statistically: the change in the mean of the resulting distribution) (e.g. Flammer, 2018; Hillman and Keim, 2001; Hull and Rothenberg, 2008; Jayachandran et al., 2013), neglecting the possible simultaneous impact on the reliability of the effect (statistically: the change in the variability of the distribution).

Scholars have shown the danger of understanding an investment’s impact on firm value without considering the risk associated with it (e.g. Duffee, 1995; Figenbaum and Thomas, 1986; Parida et al., 2016). High volatility of the expected outcome of an investment is usually unacceptable for firms because of the danger of falling into tail risk, which can often bring about severe financial distress (Osiyevskyy et al., 2020; Stulz, 1996). Therefore, for managers, it is just as important to understand the variability of the potential return of an investment as it is to measure the expected (average) return (Osiyevskyy et al., 2020; Parida et al., 2016). Measuring return without considering the risk associated with the investment is problematic because the risk nature of investment reflects the likelihood of it reaching the expected return. With an emphasis on only the expected return, the abundant current research only reveals one side of the coin, and thus provides limited guidance to managers and investors. Without understanding the risk associated with CSR, managers are practically taking a gamble when they invest in CSR activities: it may look good, but there is no guarantee that they can achieve it.

This article intends to fill these research gaps by answering two research questions: (1) What is CSR’s impact on the variability of firm value distribution? (2) Are there contingencies that make CSR’s impact on firm value more reliable (less volatile)? Empirically, we investigate CSR’s simultaneous impact on both the mean and the variance of the resulting value distribution, with the latter representing the risk nature of CSR. Moreover, anchored in the resource-based view (RBV), we aim at understanding how this CSR–variance relationship is affected by two main types of resources that may affect the riskiness of CSR: slack (tangible resources) and risk management capability (intangible resources).

With the primary objective of understanding how firms can realize “doing safe while doing good,” this article aims to add a second layer to the proposition of “doing well by doing good,” and, therefore, makes two important theoretical contributions. First, the study enhances our understanding of the uncertainties and riskiness of CSR and develops a holistic view of CSR’s effects in real business situations. By investigating CSR’s simultaneous impact on both the level and the variability of value distribution, we aim to provide insightful theoretical contributions in understanding the risk-reward trade-off of CSR. Second, this research supplements current knowledge of the instrumental value of CSR by exploring the contingencies under which CSR may be more successful in producing expected instrumental value. We propose that understanding how to make CSR’s impact on firm value more reliable is just as important as understanding how to increase such impact.

This research provides practical guidance to managers and investors and answers the call to contribute to practical implications of CSR research (Wang et al., 2020). First, we help managers determine when investing valuable resources in CSR will be more likely to succeed and when having high CSR performance is likely to be a risky gamble given certain contexts. We show managers that although having a high CSR performance may lead to possible abnormal returns, they should not make decisions to invest in CSR without considering the risk-return trade-off of CSR. Second, it provides managers with guidance on building appropriate channels to improve the efficacy of CSR and ensures that managers realize a reliable value increase from CSR. To improve the reliability of CSR’s impact on value, managers may need to explore avenues to develop relevant resources and capabilities to mitigate the risk of CSR.

Theory background and hypotheses development

CSR and reliability of firm value creation

From the RBV perspective, whether a corporate strategy or action leads to competitive advantage depends on the ability of the strategy or action to accumulate a stock of valuable resources or capabilities (Dierickx and Cool, 1989). The traditional proposition of “doing well by doing good” suggests that CSR engagement has a positive impact on firm value through building social recognition (e.g. Godfrey, 2005; Hillman and Keim, 2001), developing corporate reputation (e.g. Brammer and Pavelin, 2006; Fombrun and Shanley, 1990; Turban and Greening, 1997), fostering efficient technologies (e.g. Porter and Kramer, 2006), reducing firm risks (Boutin-Dufresne and Savaria, 2004; Godfrey et al., 2009; Lu et al., 2022; Luo and Bhattacharya, 2009; Shiu and Yang, 2017), and attracting responsible investors (e.g. Chava, 2014; Cheng et al., 2014; Graves and Waddock, 1994; Kim et al., 2019). From the perspective of asset stock accumulation (Dierickx and Cool, 1989), the flow of investment of organizational resources toward CSR activities leads to the accumulation of a stock of “moral capital” (Godfrey, 2005), which can underpin the set of value-creating mechanisms listed above. Importantly, the accumulated stock of moral capital is firm-specific and not tradable on the strategic factors market (Dierickx and Cool, 1989). As such, following the RBV framework, CSR performance can lead to the emergence of valuable, rare, inimitable, and non-substitutable resources of a given firm (e.g. corporate reputation and social recognition developed from CSR performance), which ultimately underpin the firm’s sustained competitive advantage to outperform its rivals (Barney, 1991).

To achieve the desired financial outcome from CSR, it is necessary to translate a firm’s CSR activities into its stock of moral capital and utilize this stock to gain rent. Yet, a positive outcome from this process is not guaranteed. The pay-off from CSR performance is highly unreliable considering the complex and multi-stage mechanisms of translating CSR investments into shareholder value. That is, while CSR can lead to an increase in firm value for many firms, it can also make many others worse off. For example, Danone CEO Emmanuel Faber’s ambition in CSR changed the firm into an “enterprise à mission,” a company with a purpose, and made it one of the only 10 companies worldwide to receive the “AAA” rating in global environmental rating (Van Gansbeke, 2021). But the company’s success in CSR did not help it thrive financially. Compared to its rivals, the company fell far short in profitability and shareholder returns, leading to the forced resignation of its CEO in 2021 (Kostov, 2021).

Many current studies have identified the possible non-significant or even negative impact of CSR on firm value. For example, Masulis and Reza (2015) found that shareholders react negatively to increases in corporate philanthropic activities. Wang et al.’s (2015) results show that only the economic pillar of CSR positively impacts firm performance in Taiwan, whereas the environmental and social pillars of CSR generally have no impact on performance. Servaes and Tamayo (2013) argue that CSR is detrimental to firms with low consumer awareness.

Such unpredictability of achieving a desired financial outcome by having a good CSR performance represents the risky nature of CSR investment. In practice, the riskiness of an investment is measured using the variance of its expected outcome (Tobin, 1958). The understanding and estimation of variance are important to practitioners since variance reflects how likely it is that the investment will achieve its expected outcome. A high-risk investment, one that has a high probability of generating high reward but also of suffering high loss, is usually unacceptable for firms, because the tail risk may exceed the firms’ risk tolerance level, and a high volatility in expected cash flow creates a high cost of financial distress for both the shareholders and the stakeholders (Cornell and Shapiro, 1987). Therefore, estimating and managing the volatility of expected returns is essentially important for a corporation’s strategic actions (Engle, 2004). Discussing the expected return of CSR without considering the volatility of such expected return provides limited guidance to practitioners in terms of the fate of their investment in this activity and the subsequent formation of moral capital. In other words, although we may observe a general financial reward of achieving high CSR performance on average, the fate of any particular participant in its adventure in CSR remains uncertain ex-ante, making CSR investment a gamble for any given firm: you either win big or lose big.

In essence, the riskiness of CSR lies in a firms’ ability, or inability, to transfer CSR performance into its stock of moral capital and exploit rent from the stock that outweighs the direct cost and opportunity cost of CSR. Given that the mechanisms that lead to a positive impact of CSR on firm value have been extensively discussed in the current literature (e.g. Godfrey, 2005; Godfrey et al., 2009; Lu et al., 2022; Porter and Kramer, 2006), this study focuses on the unpredictability of such impact from a reversed perspective. That is, to explain the risk nature of CSR, we focus on establishing the reasons why CSR can be detrimental to some firms while acknowledging that it will lead to financial benefit for many other firms. As is the case with all accumulated stock assets (Dierickx and Cool, 1989), the development of CSR-based moral capital is always a context-dependent, sometimes even stochastic, process, with causal ambiguity preventing not only competitive imitation but also the firm’s own ability to scale up CSR programs by repeating what worked or modifying what did not work in the past.

Many reasons contribute to the risk nature of CSR. Such reasons may either prevent a firm from accumulating a stock of moral capital or increase the direct cost and opportunity cost of such accumulation, leading to a higher deviation from the expected outcome. First, from the classic Friedman perspective, CSR diverts valuable resources from business operations (Friedman, 1970), which may force a firm to forego other potentially profitable projects. The opportunity costs may offset the benefits of CSR for many firms; furthermore, opportunity costs have their own dynamics and hence add to the lack of reliability in CSR’s outcomes. For example, for a firm experiencing financial hardship, CSR may be detrimental to its economic performance and may lead to negative value implications if it cannot transfer high CSR performance into its stock of moral capital. As another example, an employee-oriented CSR program may involve paying for employees’ continuing education or providing service for their schoolchildren (Mirvis, 2012). Although these CSR programs may improve employee efficiency and build their loyalty (Edmans, 2011), such investment may also limit a firm’s ability to provide competitive compensation, especially when the firm’s budget is tight, leading to an increase in opportunity cost.

Second, the riskiness of CSR in value creation can be manifested in the diverse opinions of shareholders about high CSR performance. On one hand, high CSR performance is often welcomed by many investors (Graves and Waddock, 1994; Hawn et al., 2018), especially those portfolio investors with a social goal (Arjaliès, 2010). For such social responsibility investors (SRI), social screening helps build a stronger portfolio and leads to higher expected returns (Auer, 2016). Therefore, increasing CSR performance can lead to a positive stock market reaction. On the other hand, achieving high CSR performance can also be viewed by shareholders as a sign of an agency problem and thus lead to shareholder sanctions (Masulis and Reza, 2015). CSR may be employed by CEOs to pursue self-interests and satisfy personal needs for attention and image reinforcement, and consequently is perceived by the public as not being genuine (Petrenko et al., 2016). The pursuit of managerial self-interest through CSR might cause shareholders to penalize high levels of CSR if the motivation for CSR is not well justified (Masulis and Reza, 2015). Essentially, the unpredictability of shareholder perception about high CSR performance contributes to the riskiness of CSR.

Finally, an established view suggests that CSR’s impact on corporate financial performance (CFP) is not monotonic in nature, that is, that high CSR performance only leads to high financial performance under certain conditions (e.g. Du et al., 2011; Hull and Rothenberg, 2008; Jo and Na, 2012; Liu et al., 2020; Servaes and Tamayo, 2013; Wang and Bansal, 2012). For example, Hull and Rothenberg (2008) argue that CSR is only value-enhancing for less innovative firms and in industries with less differentiation. Servaes and Tamayo (2013) found that the CSR–CFP relationship is positive only when customer awareness is high, whereas CSR may impact performance negatively for firms with low customer awareness. Du et al. (2011) show that a CSR strategy is effective only when customers actively participate in the CSR initiative; otherwise, it becomes detrimental to performance. CSR is also found to increase value only for firms in an informationally opaque industry (Ramchander et al., 2012), firms with a long-term orientation (Wang and Bansal, 2012), and firms in industries with high institutionalization of CSR (Brower and Dacin, 2020).

As such, we argue that although CSR has the potential to lead to value creation, as shown by the general consensus in the current literature (Barnett et al., 2020; Orlitzky and Benjamin, 2001), this effect is unreliable, since CSR also increases the volatility of value distribution across firms. This increase in the volatility of value distribution represents the risk nature of CSR. In other words, we hypothesize that CSR is a strategic asset, but it has a risky nature. That is, whereas, ceteris paribus, firms with low CSR performance are likely to achieve similar value outcomes, the firms with high CSR performance are likely to obtain a broad range of value outcomes.

Hypothesis 1. CSR has a negative impact on the reliability of firm value (i.e. a positive impact on the variability of value distribution). That is, firms with higher CSR performance have higher variability in value distribution compared to firms with lower CSR performance.

RBV and the moderating effect on the reliability of value creation

When CSR does not reliably lead to expected value creation, it becomes a risky choice for managers and raises concerns for investors and stakeholders (Barnea and Rubin, 2010; Cheng et al., 2016). The risky nature of CSR requires managers to exercise discretion when diverting valuable resources to it and be able to justify their actions. Thus, understanding the factors that increase the reliability of the efficacy of CSR is important because it guides managers to make more robust CSR decisions and helps them solicit support for their actions. The RBV framework provides insight into the resources that possibly influence a firm’s performance and risk (Aragón-Correa and Sharma, 2003; Barney, 1991; Barney et al., 2001; Helfat and Peteraf, 2003). Of the full spectrum of possible resources that may influence the riskiness of CSR investment, we limit our exposition to two salient factors that might be the most relevant, both stemming directly from the argument presented above for the baseline hypothesis. We propose that the reliability of the CSR–value relationship, that is, the risk nature of CSR, is moderated by the availability of two fundamental types of resources that are important for managing such risk: organizational slack (tangible resources) and risk management capability (intangible resources) (Helfat and Peteraf, 2003; Henderson and Cockburn, 1994).

Organizational slack

The first focal moderator, organizational slack, occupies a prominent role in the RBV framework, determining the availability of the resources that influence a firm’s allocation decisions, risk, and asset stock accumulation (Aragón-Correa and Sharma, 2003; Barney, 1991; Barney et al., 2001; Helfat and Peteraf, 2003). Organizational slack is defined as the additional resources, especially financial assets, held by a firm in excess of the minimum required amount given the current output level (Cyert and March, 1963; Nohria and Gulati, 1996). Considering that the source of CSR investments, as well as their direct and opportunity costs, could to a large extent be determined by organizational slack, prior studies stress the non-trivial role of this internal factor in shaping the performance outcomes of CSR engagement (e.g. Arora and Dharwadkar, 2011; Bhandari and Javakhadze, 2017; Mattingly and Olsen, 2018; Zhang et al., 2018).

The argument about the slack–CSR interaction stems from the “slack resources theory” as summarized by Orlitzky et al. (2003: 406). The theory finds its deep roots in RBV, treating organizational slack as available resources for discretionary investments such as CSR (Orlitzky et al., 2003; Shahzad et al., 2016). Organizational slack helps a firm reconcile its internal conflicts of resource requirements among different functions of operations, increases internal operation flexibility (Miller and Leiblein, 1996), and buffers a firm from external environmental turbulence (Cooper et al., 1994; Cyert and March, 1963). It influences the enactment of organizational activities when a firm reconfigures its resource endowments by shifting resources into different operations and markets (George, 2005). Organizational slack is thus regarded by organization theory as a valuable asset for firm growth and organizational performance (e.g. Barney, 1991; Daniel et al., 2004; George, 2005; Penrose, 1959).

Given the availability of resources, firms often need to make decisions to allocate valuable resources to a broad range of functional areas, such as CSR development, diversification, and other value-added projects. The resource allocation process becomes more challenging when different functional areas compete for a scarce resource (Noda and Bower, 1996). In contrast, substantial slack relaxes a firm’s decision-making and allows it to take on multiple competitive projects (Dolmans et al., 2014). Therefore, firms with more slack are less likely to experience difficulties in allocating resources to CSR, thus reducing the opportunity cost of CSR investment. For example, energy firms sometimes need to invest in clean energy and carbon reduction technologies to reduce their carbon footprint under institutional pressures (Petersen and Vredenburg, 2009). Such an investment may drain resources from other value-added operations for firms with less slack, but not for firms with excess slack (Evans, 1991; Miller and Leiblein, 1996).

Moreover, managers with more available slack have more flexibility in choosing the most suitable CSR strategy. Taking CSR related to employee engagement as an example, firms may have choices among paid leave, lunch programs, and education rebates as superior employee benefit programs to increase employee productivity and employee retention (Mirvis, 2012). The required investment varies among these different benefit programs. Managers with limited slack may be stuck with non-cash incentives regardless of the employees’ preferences. Consequently, inflexibility caused by limited slack increases the uncertainty of the CSR outcome, leading to an increased variance in firm performance. In contrast, managers with more slack can choose the best combination of cash incentives and non-cash incentives, leading to decreasing firm performance variance. As suggested by Waddock and Graves (1997), firms with a higher level of slack are more flexible to participate in CSR which could lead to a reliable outcome but may require more resources, whereas firms with a lower level of slack have limited options, if any, in their choice of CSR strategy. Also, the flexibility of choosing among different options improves the speed of response to external changes (Evans, 1991). As such, organizational slack provides a cushion for firms to maintain a lower performance variance because of the flexibility and the quick response speed (Cyert and March, 1963).

However, it should not be ignored that slack represents inefficiency in business operations (Antle and Eppen, 1985; Jensen and Meckling, 1976), which stems from the holding cost of excess organizational slack (Galbraith, 1973; Tan and Peng, 2003). Scholars also believe that holding excess slack can be a sign of an agency problem where managers are overly risk-averse in making investment decisions (Jensen and Meckling, 1976; Leibenstein, 1969; Nohria and Gulati, 1996). Therefore, to consider whether organizational slack reduces the riskiness of CSR, we need to understand and evaluate the relationship between the value addition of using slack to create a stock of moral capital through CSR and the value disruption represented by the inefficiency in holding slack. When a firm has an aggressive CSR strategy and maintains high slack, it reduces the chance of falling into an unsuccessful CSR strategy but increases its cost of operations. In other words, the firm trades off efficiency for certainty. A low-slack firm, in contrast, may benefit more from its CSR performance because its CSR effort may be considered as more sincere. For example, during the 2021 Henan rainstorm disaster, both ANTA, the industry leader in sports equipment in China, and ERKE, a market follower who was thought to be “broke” at the time, donated 50 million Yuan to the Red Cross for the province’s recovery. After the donation gained social attention, ERKE received much higher recognition from society and had a 52 times short-term increase and a 280% annual increase in sales, a much better outcome compared to ANTA (Faithfull, 2021; Lv et al., 2021). The risk, however, is that the financial outcome due to CSR is not guaranteed. If a low-slack firm cannot convert its high CSR performance into high rewards, the overconsumption of resources may lead to financial distress. In other words, when a firm has an aggressive CSR strategy but maintains a low level of slack, it gambles between higher performance and higher losses. Thus, Hypothesis 2 is developed:

Hypothesis 2. Organizational slack positively moderates CSR’s impact on the reliability of value creation, such that CSR’s impact on firm value is more (less) reliable for firms with higher (lower) slack.

Although slack should have a significant impact on the riskiness of CSR in creating firm value, this effect may not be universal for all types of organizational slacks. Not all slack is created equal. Each type of slack differs from others in terms of availability, cost, and redeployability (e.g. Bourgeois and Singh, 1983). Therefore, to further understand the impact of slack on the risk nature of CSR, we need to compare such impact between different types of slacks.

Bourgeois and Singh (1983) defined three types of organizational slack: available, recoverable, and potential slack. Available slack refers to the type of slack that is readily available for out-of-pocket expenses, such as cash and cash equivalents. Recoverable slack refers to uncommitted resources that are not immediately available but can be changed into available slack with some effort, that is, accounts receivable, prepaid expenses, and inventory (Bourgeois and Singh, 1983; Tyler and Caner, 2016; Vanacker et al., 2017). Finally, potential slack refers to a firm’s capability to generate future slack (Bourgeois, 1981; Bourgeois and Singh, 1983; Tyler and Caner, 2016). The availability and redeployability of different types of slacks are different (Bourgeois and Singh, 1983). Available slack, which consists of mostly cash and cash equivalents, represents the highest redeployability, whereas potential slack, which represents the expectation of a firm’s future financing capability, has the lowest redeployability (Bourgeois and Singh, 1983).

As discussed previously, organizational slack reduces the riskiness of CSR performance by reducing the opportunity cost of CSR and increasing the flexibility of CSR strategies, at the cost of the reduced efficiency that is associated with holding slack. The key argument about the risk-reduction effect of slack is that it helps firms balance between non-market strategies such as CSR and the core business operations. As a result of this, redeployable slack is more likely to create such a risk-reduction effect. First, when a firm faces discretionary expenses, highly redeployable slack has higher priority in consumption due to its high flexibility and availability for discretionary use by managers (Sharfman, 1985; Sharfman et al., 1988). As CSR often requires immediate out-of-pocket expenses that lead to a reduction in a firm’s current and future cash flow (Sprinkle and Maines, 2010), highly redeployable slack is more likely to create a flexible CSR strategy than slack with low redeployability. Second, liquidating recoverable slack and financing through potential slack increases operation costs and creates uncertainty (Sharfman et al., 1988), making their effect in reducing the riskiness of CSR unpredictable.

We predict that available slack, being the most redeployable slack, should have the strongest effect in reducing the volatility of value creation through CSR. Although recoverable slack is less flexible and less redeployable compared with available slack, it can be changed into immediately available resources with some effort and at a cost. A firm may have a certain level of choices and flexibility in developing its CSR with recoverable slack, which can lead to a decrease in the variance of firm performance. Moreover, a firm may directly use its inventory to support its CSR by donating the inventory as goodwill or using it to create social benefit. For example, Amazon implemented a donation program in August 2019 for third-party sellers that store their inventory in Amazon’s warehouses. In this program, called “Fulfillment by Amazon Donations,” sellers could choose to donate their unsold or unwanted products through a network of US non-profits instead of destroying them (Eugene, 2019). In contrast, since potential slack does not reflect a firm’s capability to meet short-term obligations, it should not have a significant impact on the reliability of value creation through CSR. In sum, we hypothesize that more redeployable slack is more effective at reducing the risk associated with CSR than less redeployable slack.

Hypothesis 3. The moderating effect of slack on CSR’s impact on the reliability of value creation is contingent on the redeployability of the type of slack, such that highly redeployable slack has a higher effect than less redeployable slack.

Risk management capabilities

The second moderator of our study emphasizes the possible organizational capabilities embedded in enterprise risk management (ERM) practices that might mitigate the riskiness of CSR. RBV stresses the importance of organizational capabilities as a valuable source of competitive advantage and provides insight into the possible moderating effect of organizational capabilities on CSR’s effect on firm performance reliability (Aragón-Correa and Sharma, 2003; Barney, 1991; Barney et al., 2001; Helfat and Peteraf, 2003). Organizational capabilities are embedded in firm routines and involve the transformation of physical inputs into outputs (Collis, 1994). Broadly speaking, organizational capabilities can be classified into three categories (Collis, 1994): (1) capability to perform the basic functional activities of the firm (e.g. risk management); (2) capability to learn, adapt, change, and renew over time (e.g. innovation); and (3) capability to recognize the intrinsic value of other resources or to develop novel strategies that transform into profitability (e.g. CSR). The riskiness of CSR is reflected by the heterogeneous capability in transforming CSR performance into financial benefit, which should intuitively be impacted by a firm’s capabilities in performing basic functional activities such as risk management (Kuo et al., 2021). In other words, we believe that a superior risk management practice, that is, the ERM practice, should function as a costly risk mitigation mechanism that reduces the uncertainty of CSR performance.

ERM is defined by the Committee of Sponsoring Organizations (COSO) as “a process … designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives” (COSO, 2004: 16). Firms with ERM have sophisticated risk management capabilities to manage corporate risks at the head office level and support two-way communication between the head office and each business unit.

As stated previously, the three main mechanisms that lead to the riskiness of CSR are the opportunity cost of financial hardship, diverse investor perceptions of CSR, and non-monotonic impact of CSR on value. We propose that firms’ risk management capabilities developed through ERM can help mitigate these mechanisms. First, scholars have argued that ERM helps firms reduce the cost of financing (Berry-Stölzle and Xu, 2018) and reduce the marginal cost of risk-bearing (Eckles et al., 2014). This means that when a firm requires additional funding from the capital market due to its aggressive CSR strategy, ERM firms will experience lower direct and opportunity costs of financing. Moreover, the residual risk caused by CSR strategies can also be better managed since ERM help reduce the cost of risk-bearing by considering corporate risk as a holistic portfolio. This reduces the possibility of financial hardship when a firm pursues an aggressive CSR strategy.

Second, a firm’s CSR strategy is often considered as a sign of an agency problem between the shareholders and the firm (Masulis and Reza, 2015). Moreover, if a firm increases its external financing for CSR, it also inevitably incurs additional financial risk, which is often triggered by the agency cost (between the debt holders and the firm) of excessive leverage (Jensen, 1986; Kim and Sorensen, 1986). In contrast, investors usually consider ERM as a sign of good managerial capabilities (Nair et al., 2014). It reduces information asymmetry between a firm and its stakeholders since it requires a firm to build sound relationships with a variety of stakeholders and incorporate their concerns into its risk management process (Dickinson, 2001; Lu et al., 2022; Nocco and Stulz, 2006). Therefore, a firm can achieve alignment by having complementary CSR strategy and ERM practices. This alignment enables the firm’s investors to achieve a better understanding of the risks associated with CSR and incorporate their risk management considerations into CSR decision-making.

Finally, since the ERM program facilitates two-way communication between business units and the head office, and between stakeholders and the firm (Lee and Kleffner, 2003), it enables a firm to adapt its CSR strategy to the changing external environment. The two-way communication channel also helps a firm develop idiosyncratic CSR strategies to accommodate the different environments its business units experience. This makes the financial outcome of CSR performance more monotonic. In other words, firms with ERM programs may experience a more reliable outcome of their CSR engagement. For example, scholars have argued that CSR creates more value when customer awareness is high (Servaes and Tamayo, 2013) and when customers actively participate in making the CSR strategies (Du et al., 2011). One significant difference between ERM and traditional risk management practice is that ERM considers stakeholder concerns when assessing the risk portfolio and incorporates stakeholder interests in risk treatment, including that of the customers (COSO, 2004, 2017). Therefore, customer preferences are inherently an important component of a firm’s risk assessment, analysis, and treatment process for ERM firms (D’Arcy and Brogan, 2001). This allows ERM firms to pursue an aggressive CSR strategy while effectively incorporating customer interests in the decision-making process, thus reducing the probability of backfire due to a lack of trust from customers.

However, similar to the discussion about organizational slack, the buffer provided by ERM on the reliability of value creation through CSR is not without cost. ERM itself is a costly process that requires a significant input of both financial and human resources (Harner, 2013; Lin et al., 2012). Therefore, firms that use ERM to reduce the risk of CSR need to consider the trade-off between the risk borne by having an aggressive CSR strategy and the cost to mitigate such risk through ERM. Considering this trade-off leads to a decreased probability that high CSR firms fall under the tails on both sides of the value distribution. In other words, the outcome of CSR is more predictable when a firm has an ERM program. Hypothesis 4 is thus developed:

Hypothesis 4. Risk management capability positively moderates CSR’s impact on the reliability of value creation, such that CSR’s impact on firm value is more (less) reliable for firms that adopted (did not adopt) ERM.

Research method

Sample and data

We constructed our sample by combining the Compustat, MSCI ESG (formally the KLD database), Standard and Poor’s (S&P) Capital IQ, and Rating Specific databases. The number of rating criteria in each dimension and the definitions of some remaining rating criteria of ESG were changed significantly after 2011. Therefore, we chose 2011 as the cut-off year and obtained data between 2002 and 2011. Our final data consist of 4713 firm-year observations (down to 3914 observations after considering Dynamic Panel Structures).

Dependent variables

Following previous literature (e.g. Albuquerque et al., 2019; Hawn and Ioannou, 2016; Jayachandran et al., 2013; Servaes and Tamayo, 2013; Surroca et al., 2010), we used Tobin’s Q to measure firm market value because of its forward-looking nature (Jayachandran et al., 2013), its long-term orientation (Surroca et al., 2010), its independence of managerial manipulation (Jayachandran et al., 2013), and its comparability among firms from different industries (Nekhili et al., 2017). Tobin’s Q is measured as the sum of the market value of equity, the liquidation value of preferred shares, and the book value of debt, divided by the book value of assets (Chung and Pruitt, 1994; Jayachandran et al., 2013).

The variance of firm value represents the predictive power of the line of best fit. It is measured as the level of deviation of the actual value from the predicted value (Fleming and Sorenson, 2001; Sørensen, 2002; Sorenson and Sørensen, 2001). A high level of variance represents a low level of reliability of the mean prediction, that is, a high risk of not being able to achieve the predicted mean. Following previous literature (e.g. Fleming, 2001; Fleming and Sorenson, 2001; Harvey, 1976; Sørensen, 2002; Sorenson and Sørensen, 2001), we measure the variance of market value as the log-squared residuals of Tobin’s Q in the mean regressions.

Independent variables

We measure CSR using the commonly adopted MSCI ESG database. MSCI measures CSR using a well-developed matrix of strengths and weaknesses. Each of the three dimensions (environmental, social, and governance) is assessed using a series of strengths and weaknesses criteria, with each criterion given a value of “0” or “1.” The value of “1” in a strength criterion means that the firm met or exceeded the minimum requirement of the criterion, whereas the value of “1” in a weakness means that the firm did not meet the minimum requirement (MSCI ESG Research, 2015). Many scholars have criticized the combination of strength and weakness criteria for creating an indexed CSR because they measure different concepts of CSR and corporate social irresponsibility, respectively (e.g. Godfrey et al., 2009; Mattingly and Berman, 2006). Therefore, we used CSR strengths to measure our CSR variable.

The rating criteria of the MSCI ESG database constantly change over time. In order to enhance the comparability of the criteria over time, we followed the current literature and used the CSR strength percentage score (rate) instead of the raw number of CSR strengths (e.g. Albuquerque et al., 2019; Deng et al., 2013; Servaes and Tamayo, 2013). The CSR rate in each dimension was calculated as the sum of the strength scores of each dimension divided by the number of strength criteria of the dimension. The final CSR was calculated as the sum of strength rates of all dimensions in MSCI.

Moderators

The first moderator is organizational slack. In this article, we focus on three types of organizational slack: (1) available slack, (2) recoverable slack, and (3) potential slack. Following previous research (e.g. Bourgeois and Singh, 1983; Kim et al., 2008; Singh, 1986; Tyler and Caner, 2016; Vanacker et al., 2017), we use financial ratios to measure different types of slacks. As available slack represents the availability of immediate cash resources as a percentage of total assets (Vanacker et al., 2017), it is operationalized as cash and short-term assets as a percentage of total assets. A high level of available slack means that the company has extra cash and short-term assets to pay for immediate obligations or make prompt investments. As recoverable slack measures the availability of resources that have not been absorbed by current operations, such as accounts receivable, inventory, and prepaid expenses, we measure it using the current ratio (Bourgeois and Singh, 1983; Iyer and Miller, 2008; Tyler and Caner, 2016). A higher current ratio means that a larger portion of current assets has not yet been committed to paying current liabilities and hence represents higher available slack. Potential slack measures a firm’s ability to obtain further debt financing (Daniel et al., 2004; Iyer and Miller, 2008; Tyler and Caner, 2016). We use the debt-to-equity ratio to measure potential slack (Iyer and Miller, 2008; Tyler and Caner, 2016). A high debt-to-equity ratio represents a low ability to obtain further debt financing, hence a low level of potential slack; whereas a low debt-to-equity ratio represents a high ability to borrow more (Bourgeois and Singh, 1983; Iyer and Miller, 2008; Tyler and Caner, 2016).

The second moderator measures a firm’s risk management capability. As stated above, based on the current literature in risk management, it is generally believed that a holistic risk management practice, for example, ERM, imparts superior capability to identify, analyze, and treat risk in a strategic manner, and thus represents better risk management capability. Therefore, we measure risk management capability using a binary variable that identifies the existence of an integrated risk management practice (i.e. ERM). Extensive literature in the risk management and insurance discipline has established a standard method to measure the existence of ERM (e.g. Berry-Stölzle and Xu, 2018; Eckles et al., 2014; Hoyt and Liebenberg, 2011; Lu et al., 2022; Pagach and Warr, 2011). Following this standard method, we first conducted a thorough company-by-company search in Factiva, company annual reports, and social media using keywords of “ERM, chief risk officer, risk committee, integrated risk management, consolidated risk management, strategic risk management, and holistic risk management” (Berry-Stölzle and Xu, 2018; Eckles et al., 2014; Hoyt and Liebenberg, 2011; Lu et al., 2022). We then carefully read each hit and identified whether and when a firm established its ERM program. The dummy variable, ERM, takes the value of “1” starting in the first year that a firm established an ERM program and thereafter “0” if it does not have an ERM program in a given year.

Control variables

We include control variables that are commonly used in CSR value literature. We control for firm size, operationalized as the logarithm of total assets because larger firms have more resources and are under higher external pressure regarding social obligations. We control for the market-to-book ratio because it has a positive correlation with Tobin’s Q (Villalonga, 2004) and CSR (Cheung et al., 2010). We control for firm sales growth, measured as the change in sales in the current year divided by sales in the previous year, because it impacts firm performance (McGuire et al., 1988) and CSR (Cai et al., 2012). We control for systematic risk, operationalized as S&P 1-year beta, because CSR interacts with systematic risk in determining firm performance (Albuquerque et al., 2019). Previous literature shows that innovation influences both a firm’s CSR strategy (Candi et al., 2019) and value creation. Therefore, we also control for R&D intensity, which is operationalized as R&D investment divided by total sales (e.g. Hull and Rothenberg, 2008; Kelm et al., 1995). We also control for dividend, operationalized as dividend per share, as dividend reflects future earning capability (e.g. Arnott and Asness, 2003; Nissim and Ziv, 2001; Zhou and Ruland, 2006), which influences both CSR and firm expected value. We include year-fixed effects in all regressions to eliminate the confounding effects of the time trend. The possible time-invariant covariates (most notably, fixed effects of the firm’s industry) are not included in the regressions because we employ a within-firm specification that accounts for all time-invariant factors. All independent and control variables are lagged by 1 year.

Model specification and identification strategy

In order to assess CSR’s impact on the level (statistically: mean) and the reliability (statistically: variance) of firm value simultaneously, we apply the multiplicative heteroscedasticity estimation (MHE) model (Davidian and Carroll, 1987; Harvey, 1976). This method has been widely used to investigate the simultaneous effect of the independent variable on the mean and variance of the dependent variable in various disciplines (e.g. Davidian and Carroll, 1987; Fleming and Sorenson, 2001; Harvey, 1976; Kim and Seltzer, 2011; Shirokova et al., 2020; Sørensen, 2002; Sorenson and Sørensen, 2001). The MHE model has two sets of regressions (mean and variability equations) in each estimation to test the associations between the dependent variables and the independent variables simultaneously, as shown below

where

A problem with the estimation is that CSR is endogenously determined, leading to a possible overestimation of the significance and effect size of the parameter. To address this issue, we apply the Arellano–Bond dynamic panel data (DPD) estimator (Arellano and Bond, 1991; Arellano and Bover, 1995; Blundell and Bond, 1998). The DPD model treats the focal predictor (CSR) and the interaction terms derived from it as endogenous. It controls for unobserved time-variant and time-invariant trends by applying the lagged independent variables at (t – 1) and further lags, as well as lagged dependent variable at (t) and further lags as instruments (Arellano and Bond, 1991; Arellano and Bover, 1995). It also provides an unbiased estimation regardless of whether reverse causality exists by treating the independent variables with both the lagged self and the lagged dependent variable (Leszczensky and Wolbring, 2022; Wintoki et al., 2012). In sum, for the mean regressions, we apply the dynamic panel structure to mitigate endogeneity, and for the variance regressions, we use ordinary least squares (OLS) regression.

Results

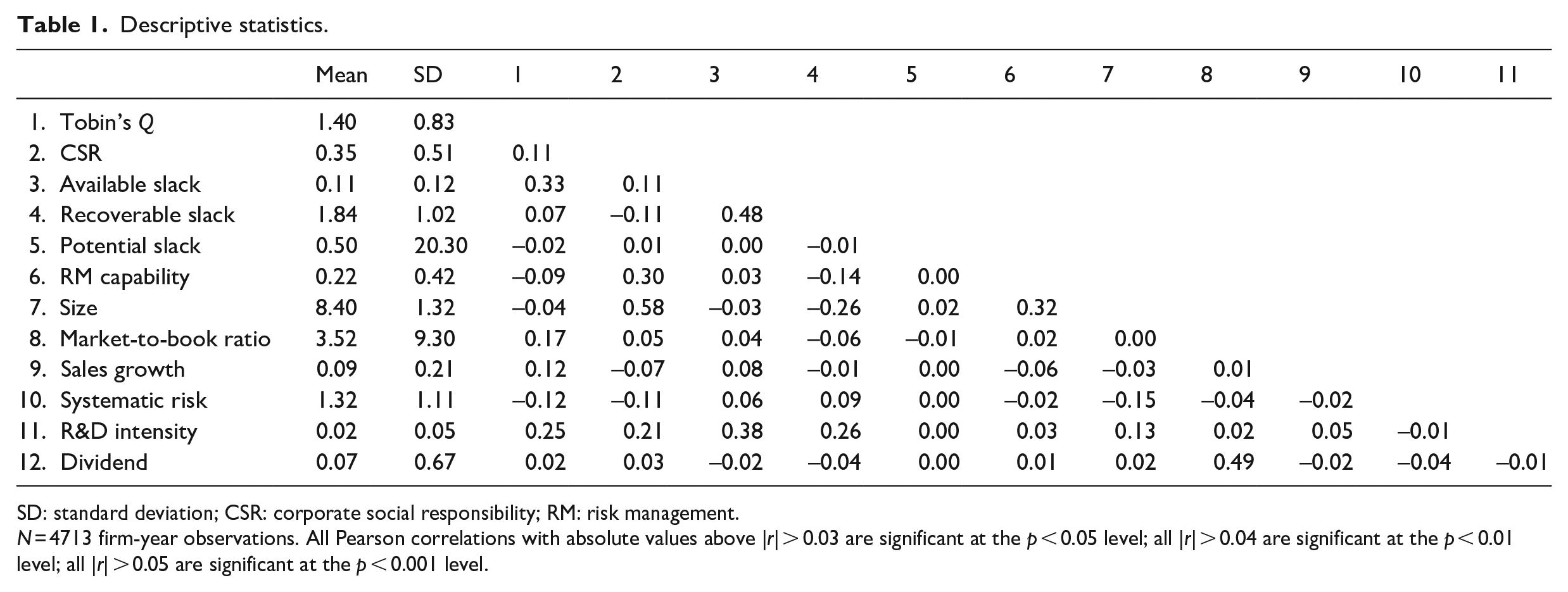

The descriptive statistics and Pearson correlations of all variables are shown in Table 1. The results show no collinearity issues as no correlation is greater than 0.5 or less than –0.5 (except for the correlation between size and CSR: 0.58).

Descriptive statistics.

SD: standard deviation; CSR: corporate social responsibility; RM: risk management.

N = 4713 firm-year observations. All Pearson correlations with absolute values above |r| > 0.03 are significant at the p < 0.05 level; all |r| > 0.04 are significant at the p < 0.01 level; all |r| > 0.05 are significant at the p < 0.001 level.

CSR and market value distribution

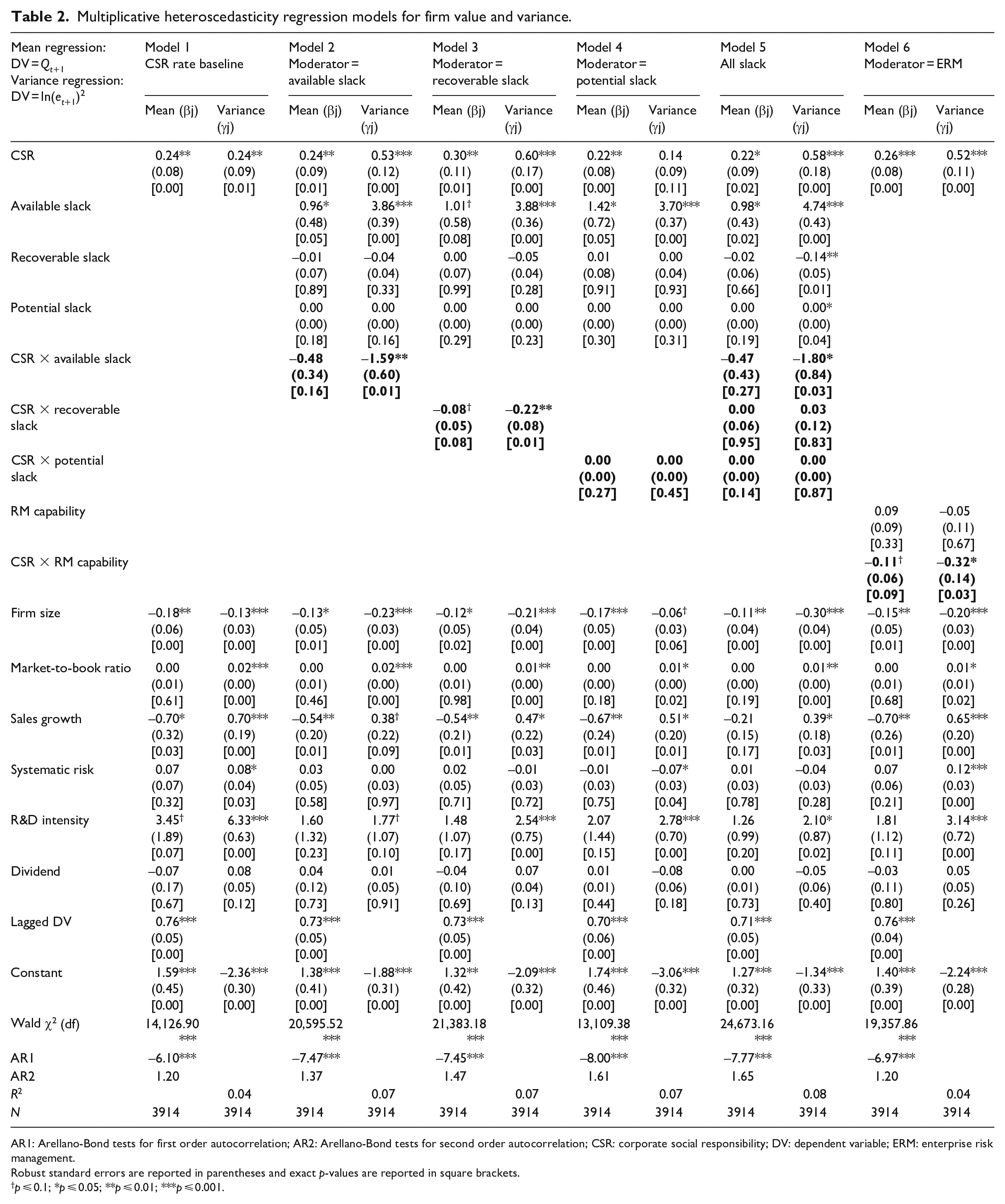

We report the test results for Hypothesis 1 in Model 1 of Table 2. The results show that CSR has a significant positive impact on both the mean (β = 0.24, p ⩽ 0.01) and the variance of Tobin’s Q (γ = 0.24, p ⩽ 0.01). The coefficients also have a strong economic size: a 1 standard deviation increase in CSR (0.51) leads to an increase in Tobin’s Q by 0.122 or an 8.7% increase in the mean of Tobin’s Q (|mean| = 1.40). More importantly, a 1 standard deviation increase in CSR increases the variance of Tobin’s Q by 0.122 or a 3.9% increase in the variance of Tobin’s Q (|mean| = 3.13). Therefore, Hypothesis 1 is supported. As shown in Model 1, CSR is a strategic asset in that it significantly increases firm value, with the cost of increased dispersion of Tobin’s Q distribution. In other words, CSR’s positive impact on Tobin’s Q is not reliable.

Multiplicative heteroscedasticity regression models for firm value and variance.

AR1: Arellano-Bond tests for first order autocorrelation; AR2: Arellano-Bond tests for second order autocorrelation; CSR: corporate social responsibility; DV: dependent variable; ERM: enterprise risk management.

Robust standard errors are reported in parentheses and exact p-values are reported in square brackets.

p ⩽ 0.1; *p ⩽ 0.05; **p ⩽ 0.01; ***p ⩽ 0.001.

The moderating effect of organizational slack

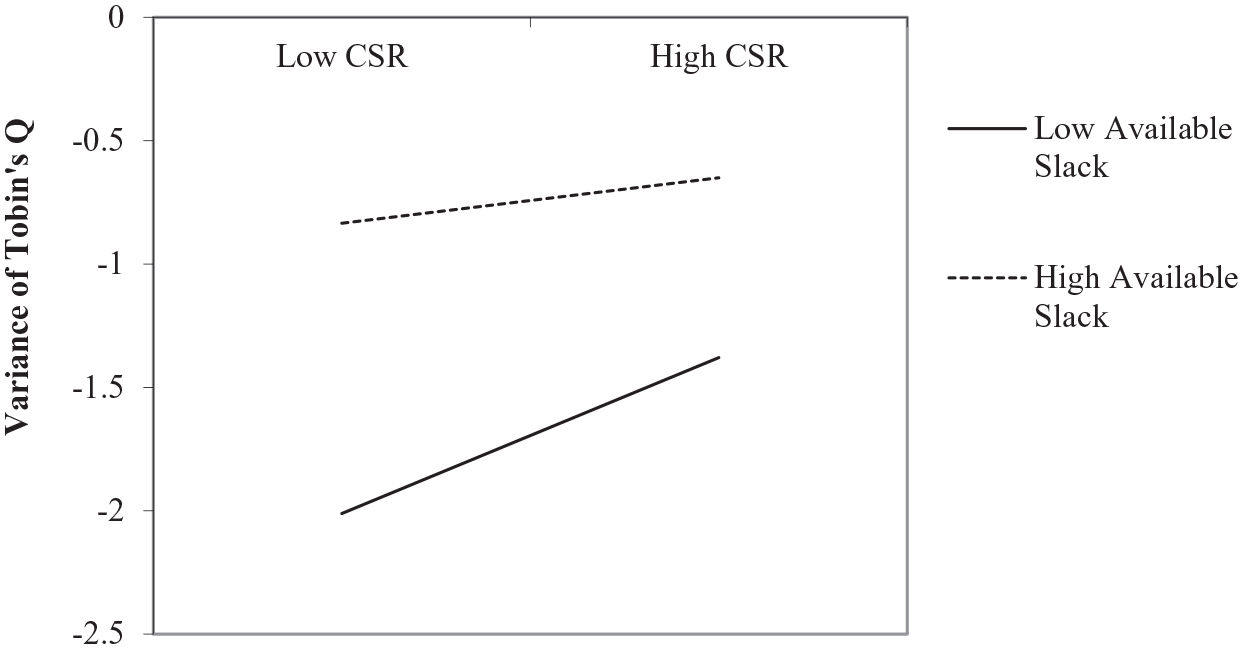

The moderating effects of organizational slack on the CSR and firm value variance relationship are reported in Table 2. We tested the moderating effect of each type of organizational slack separately in Models 2–4 and the combined effects in Model 5. The results show that the interaction of CSR and available slack significantly reduces the variance of Tobin’s Q in both the separate model (γ = –1.59, p ⩽ 0.01) and the combined model (γ = –1.80, p ⩽ 0.05). We plotted the interaction effect of available slack at ±1 standard deviation based on the coefficients in Model 2 (as shown in Figure 1) to help visually interpret the results. The figure indicates that when a firm processes high available slack, higher CSR leads to a much lower increase in the variance of Tobin’s Q compared to low-slack firms. Moreover, recoverable slack also has a negative and significant moderating effect (γ = –0.22, p ⩽ 0.01) on the CSR–variance relationship, as shown in Model 3 of Table 2. Therefore, CSR’s impact on the mean of Tobin’s Q (positive from the first stage regression) is more reliable for firms with high available (recoverable) slack than low-slack firms. Therefore, Hypothesis 2 is supported.

The moderating effect of available slack.

Hypothesis 3 states that highly redeployable slack should have more impact on the CSR–variance relationship than less redeployable slack. We can see some evidence of this in Table 2. First, more redeployable slack, such as available and recoverable slack, has a significant moderation effect in the separate models (Models 2 and 3). In contrast, the interaction of CSR and potential slack does not have a significant impact on the variance of Tobin’s Q in either the separated model or the combined model, as shown in Models 4 and 5. Second, in the full model considering all interaction effects of different types of slacks, only available slack, being the slack with the highest redeployability, has a significant moderation effect on the CSR–variance relationship. Therefore, Hypothesis 3 is supported.

The moderating effect of risk management capabilities

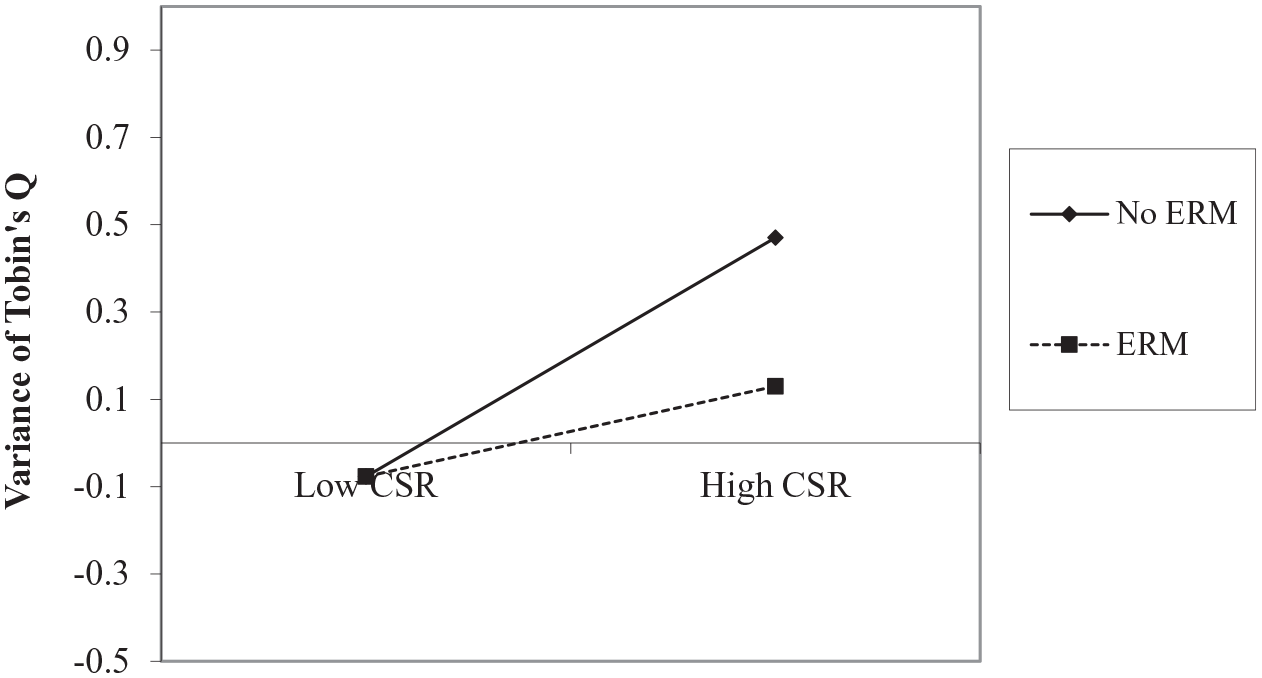

We reported the moderating effect of risk management capabilities in Model 6 of Table 2. Model 6 shows that the interaction of CSR and ERM has a negative correlation with the variance of Tobin’s Q (γ = –0.32, p ⩽ 0.05), indicating that ERM firms have a lower impact of CSR on the variance of Tobin’s Q. We plotted the change in variance of Tobin’s Q at ±1 standard deviation of CSR in Figure 2, separating the impact of ERM firms from that of non-ERM firms. Figure 2 reveals that the positive impact of CSR on the variance of Tobin’s Q is significantly weaker when a firm implements ERM. Therefore, Hypothesis 4 is supported.

The moderating effect of risk management capability.

Endogeneity control

As stated before, one of the major concerns with the data is that CSR is endogenously determined, leading to possible omitted variable bias (OVB). Although the dynamic panel method can reduce OVB by controlling for biases from the possible time-fixed or path-dependent omitted variables, there could still be residual biases from unobserved time-variant variables that may impact both CSR and firm value. To further control for endogeneity, we applied the two-stage instrumental variable (IV) regression method combined with the dynamic panel structure as a robustness check. In the first stage, we used non-profit organization (NPO) density as the instrumental variable to purge out possible endogenous variance from CSR (Lu et al., 2022). NPO density is measured as the number of NPOs, in 1000, in the state where the firm resides divided by the population density of the state. The number of NPOs in each state is obtained from the National Center for Charitable Statistics, a third-party agency that works closely with the Internal Revenue Agency to provide data for the non-profit sector (NCCS, 2017). The population density data is collected from the US Census Bureau. Because NPOs usually exercise their power against firms through their monitoring functions (Lu et al., 2022; Rivera-Santos and Rufín, 2010), areas with high NPO density should have a higher demand for high CSR performance. However, it is hard to argue that a firm should have higher (or lower) value just because it is headquartered in an area with more NPOs. Therefore, since the number of NPOs can be considered as exogenous to firm value (except for its influence on CSR performance), it is a good instrumental variable for our analysis.

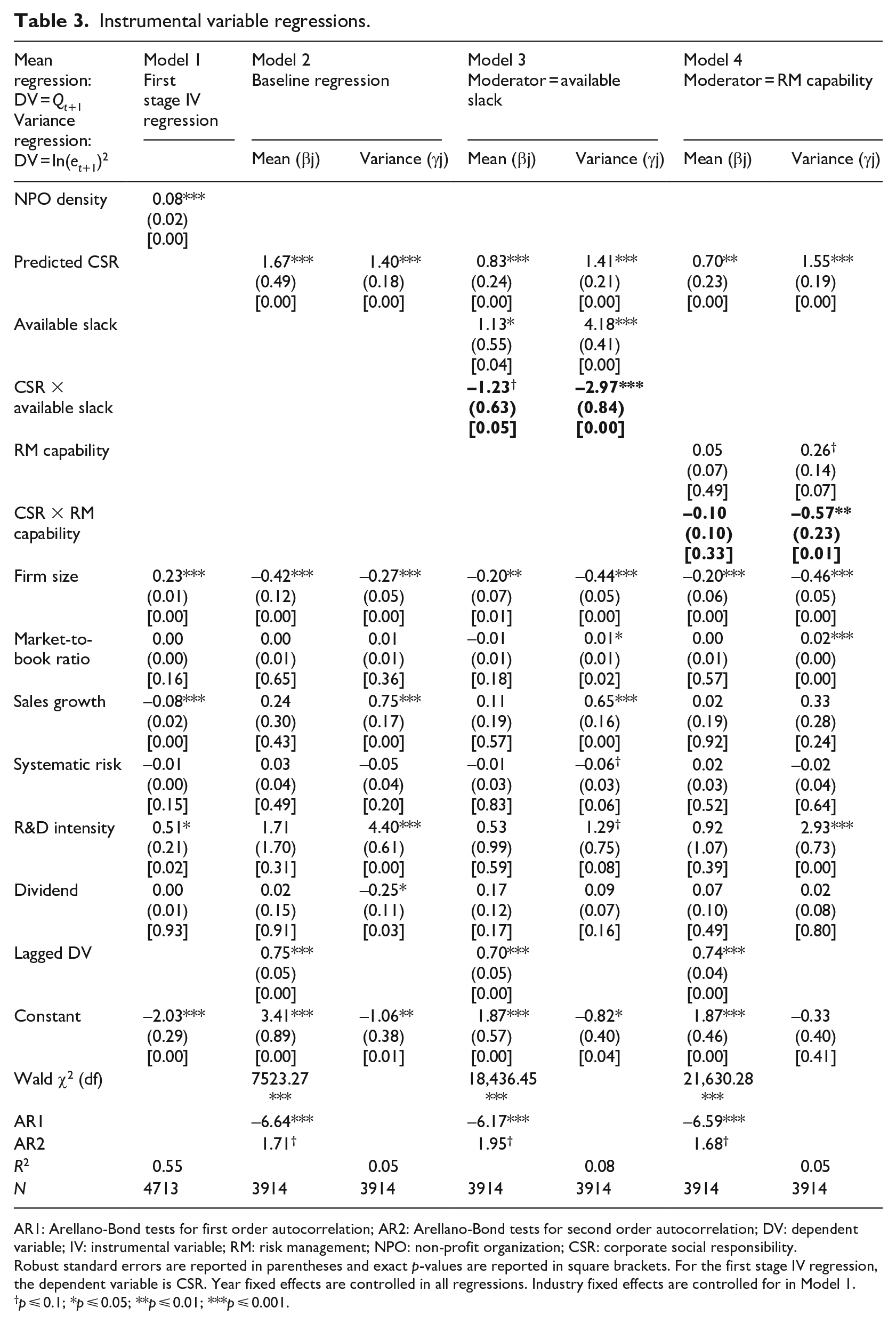

Table 3 reports the results from combining the IV regression and DPD estimation. In Model 1, we report the first stage IV regression using CSR as the dependent variable and NPO intensity as the independent variable. The results show that NPO density significantly predicts CSR performance. As expected, firms in states with a higher NPO density have higher CSR performance (β = 0.08, p ⩽ 0.001). In the second stage, we calculated the fitted value of CSR (predicted CSR) and used it in the Arellano–Bond DPD regressions as the independent variable. Model 2 shows the baseline regression of CSR’s impact on the level and variability of Tobin’s Q using predicted CSR. The results show that CSR significantly increases both the mean and the variance of Tobin’s Q, providing further support for Hypothesis 1. Models 3 and 4 showed that the moderation effects of both available slack (γ = –2.97, p ⩽ 0.001) and risk management capability (γ = –0.57, p ⩽ 0.01) are still significant, even when we control for endogeneity using IV regressions. Therefore, we conclude that it is unlikely the results are caused by OVB.

Instrumental variable regressions.

AR1: Arellano-Bond tests for first order autocorrelation; AR2: Arellano-Bond tests for second order autocorrelation; DV: dependent variable; IV: instrumental variable; RM: risk management; NPO: non-profit organization; CSR: corporate social responsibility.

Robust standard errors are reported in parentheses and exact p-values are reported in square brackets. For the first stage IV regression, the dependent variable is CSR. Year fixed effects are controlled in all regressions. Industry fixed effects are controlled for in Model 1.

p ⩽ 0.1; *p ⩽ 0.05; **p ⩽ 0.01; ***p ⩽ 0.001.

Robustness check: ES score

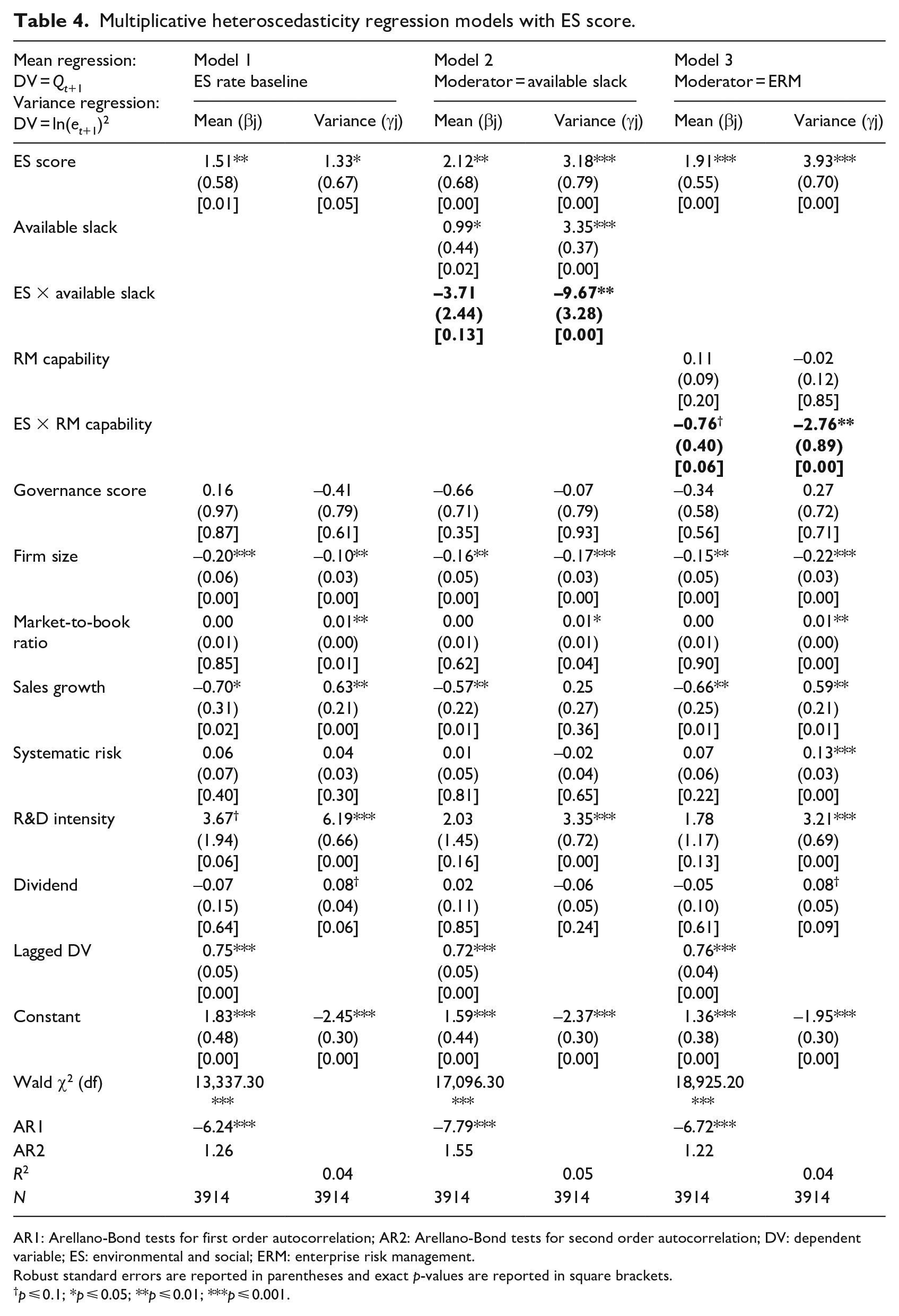

Many scholars argue that the CSR score should focus on the environmental and social aspect rather than the governance component in the MSCI rating (e.g. Albuquerque et al., 2019; Greening and Turban, 2000) because, unlike the other two components, the governance component is an important aspect of the core operations. To address this possible concern, we ran the main regressions using the environmental and social (ES) rate scores instead of the CSR rate. The ES rate is calculated as the average score rate for the six dimensions in the MSCI database: environment, community, product, human rights, employee, and diversity. We included the governance rate as a control variable in all models in Table 4 to control for possible confounding effects caused by agency aspects.

Multiplicative heteroscedasticity regression models with ES score.

AR1: Arellano-Bond tests for first order autocorrelation; AR2: Arellano-Bond tests for second order autocorrelation; DV: dependent variable; ES: environmental and social; ERM: enterprise risk management.

Robust standard errors are reported in parentheses and exact p-values are reported in square brackets.

p ⩽ 0.1; *p ⩽ 0.05; **p ⩽ 0.01; ***p ⩽ 0.001.

Table 4 shows the results of the regressions using the ES score as the independent variable. The results in Model 1 show that the ES score has a positive and significant relationship with both Tobin’s Q and the variance of Tobin’s Q, which provides further support for Hypothesis 1. More importantly, the interaction effects of both available slack and risk management capability on the variance of Tobin’s Q are still significant at the p ⩽ 0.01 level. Therefore, we confirm that our results are robust even if we only consider the environmental and social aspects of CSR.

Discussion and conclusion

For decades, CSR has been treated as a non-market strategy that helps firms build moral capital and enhance performance (Godfrey et al., 2009; Goldstein and Pauzner, 2005). From this instrumental approach, CSR is considered a social investment that should lead to long-term benefits for shareholders. Scholars have shown that CSR can create value through various channels, including the “insurance-like effect” hypothesis (Godfrey et al., 2009; Shiu and Yang, 2017), stakeholder management hypothesis (Jones, 1995; Wood, 1991), and efficiency enhancement hypothesis (Flammer and Kacperczyk, 2019; Flammer and Luo, 2017). However, the current instrumental approach to CSR has an emphasis on the return of CSR but neglects the risk associated with an investment in CSR. For decades, we as academic scholars have been trying to promote the idea of “doing well by doing good” to practitioners, as if CSR’s impact on firm value is monotonic. The problem with this idea, obviously, is that such impact is never monotonic, as shown by many current studies (e.g. Du et al., 2011; Gras and Krause, 2020; Servaes and Tamayo, 2013). The non-monotonicity leaves managers and investors in a baffling position: without knowing the conditions under which CSR can lead to more reliable value creation, their investment in CSR is at best a risky gamble. The recent discharge of Danone’s CEO Emmanuel Faber—due to his inability to transfer an aggressive CSR strategy into profitability of the company—is a good example of this problem (Kostov, 2021; Van Gansbeke, 2021). Therefore, to provide meaningful guidance to managers regarding the CSR–value relationship, we need to show the uncertain nature of CSR investment and determine the conditions under which such uncertainty can be reduced.

This article tries to fill this gap by investigating the reliability of the value creation effect through CSR and exploring the conditions under which CSR can create value more reliably (i.e. contingent factors that reduce CSR’s positive impact on the volatility of value distribution). By exploring how firms realize “doing safe (financially) while doing good (socially),” this article adds a second important layer to the proposition of “doing well by doing good,” thus incorporating the uncertainty of CSR investment into considerations of the efficacy of CSR. Using the MHE model and dynamic panel regression structure, we find that CSR by itself is an unreliable value enhancer and a risky choice (not only increases value but also increases the volatility of value distribution) (Barnea and Rubin, 2010; Cheng et al., 2016). With further investigation based on the RBV of firms (Barney, 1991; Barney et al., 2001; Helfat and Peteraf, 2003), we find that the reliability of the efficacy of CSR is moderated by two fundamental resources: organizational slack and risk management capability. Specifically, the impact of CSR on firm value is more reliable when a firm has more slack on hand or when a firm has stronger capability in risk management.

In addition, we found that the moderating effect of slack is more significant for highly redeployable slack than slack with low redeployability. This means that the flexibility and immediate availability of organizational slack play a critical role in determining its impact on the riskiness of CSR investment. A possible reason is that unlike highly redeployable slack (measured by the availability of cash and cash equivalents), recoverable slack is measured by the availability of short-term assets that are, at least to a certain extent, tied up in business operations. Although liquid, most current assets, such as accounts receivable, stock inventories, supplies, and prepaid liabilities (Wharton Research Data Services, 2020), are not as readily available as cash and cash equivalents. However, CSR investment usually requires the input of highly liquid assets that are immediately turned into out-of-pocket expenses. For example, if a firm’s liquid assets are heavily tied to accounts receivable, investing in CSR may still cause the firm to experience financial hardship. Similarly, potential slack is not a measurement of resources on hand, but rather a measurement of a firm’s ability to borrow from external sources. In other words, a firm with high potential slack may still experience difficulties paying immediate out-of-pocket CSR expenses if it cannot transform potential slack into resources. Moreover, raising debt to invest in CSR increases not only the transaction costs of CSR (in terms of interest) but also the opportunity costs (in terms of reduced debt capacity). Third, increasing debt to invest in CSR is likely a hard story to sell to investors and could be regarded as a sign of an agency problem (Masulis and Reza, 2015). Therefore, the risk-reduction effect of less redeployable slack, such as recoverable and potential slack, may not be as strong as that of available slack.

Gras and Krause (2020) argue that CSR’s impact on financial performance is more prominent when a firm is in a munificent industry. Firms in the munificent industries have more slack to invest in discretionary strategies such as CSR; therefore, they experience more pressure due to imitation by rival firms and a higher industry standard for CSR. As a result, the efficacy of CSR as a differentiation tool is marginally less significant compared with firms in less munificent industries. The assumption for this argument, as stated by Gras and Krause (2020), is that pursuing CSR in resource-scarce industries is riskier due to the lack of organizational slack. In other words, slack provides a risk-reduction effect for CSR investment. We show that slack does have a positive risk-reduction effect on CSR, providing evidence for this important assumption for Gras and Krause (2020). Therefore, our research not only complements Gras and Krause (2020) by providing important support for their arguments but also extends their argument to the perspective of firm-level volatility.

Slack is an important component of the behavior theory of the firm (BTOF) (Argote and Greve, 2007; Cyert and March, 1963). According to the BTOF, slack provides a buffer for unexpected expenses to deal with internal or external disruptions (Bourgeois, 1981; Cyert and March, 1963). This leads to two types of possible functions of slack: increase innovation and resolve conflict (Argote and Greve, 2007). The former has been substantially discussed while the latter draws less attention in previous literature (Argote and Greve, 2007). This article provides some evidence for the role of slack in resolving conflicts in operations. When CSR needs to compete for valuable resources with the core operations, conflicts occur between the economic and social/environmental goals of the firm (Symeou et al., 2019). Our findings suggest that this conflict may be reflected as the risk nature of CSR: without a proper level of slack resources, investing in CSR activities is fundamentally a risky choice. Moreover, our findings regarding the moderating effect of slack on the CSR–variance relationship provide evidence for the stabilizing function of slack (Cyert and March, 1963).

Aiming to fill current research gaps in understanding the reliability of the impact of CSR on value, and the factors that influence this reliability, this research provides both significant theoretical contributions in the field of CSR and managerial implications. Theoretically, by considering uncertainty as well as the effect of the relationship between CSR and firm value, this research enhances the field’s understanding of the role of CSR as a value enhancer. The investigation of the risk-return trade-off of CSR sheds light on the situation, moving research on CSR into theoretically fruitful areas compared to the investigation of a single aspect.

Previous organization theorists have argued that organizational slack buffers a firm’s technical core strategies from environmental turbulence and thus enhances its financial performance (Bowen, 2002; Tan and Peng, 2003). Building on these arguments, we link the “risk buffering” effect of slack to the uncertainty of CSR. We supplement the current understanding of the instrumental value of CSR by exploring when CSR may fail to reliably produce the expected instrumental value, and when it may succeed. We further identify that the nature of organizational slack, in terms of its flexibility and immediate availability, determines its buffering effect on firm value in this article. In addition, by showing that the uncertainty of CSR investment can be reduced by having superior risk management practice, we bring theories from the risk management discipline into the understanding of the riskiness of CSR. These findings provide a valuable avenue to advance CSR research and answer the call for the further theorization of CSR investigations (Wang et al., 2020).

Our research provides a strong tie to link current CSR theoretical development to CSR practices, thus answering the call to increase the practical implications of CSR research (Wang et al., 2020). From a practical point of view, shareholders and managers are concerned about the variability of firm performance (Orlitzky and Benjamin, 2001) because it plays a key role in performance-driven organizational change (Donaldson et al., 2012). Managing the variability of firm value can make a difference between “future bankruptcy and organizational health” because organizational activities that increase firm risks may be penalized over the long term (Orlitzky and Benjamin, 2001).

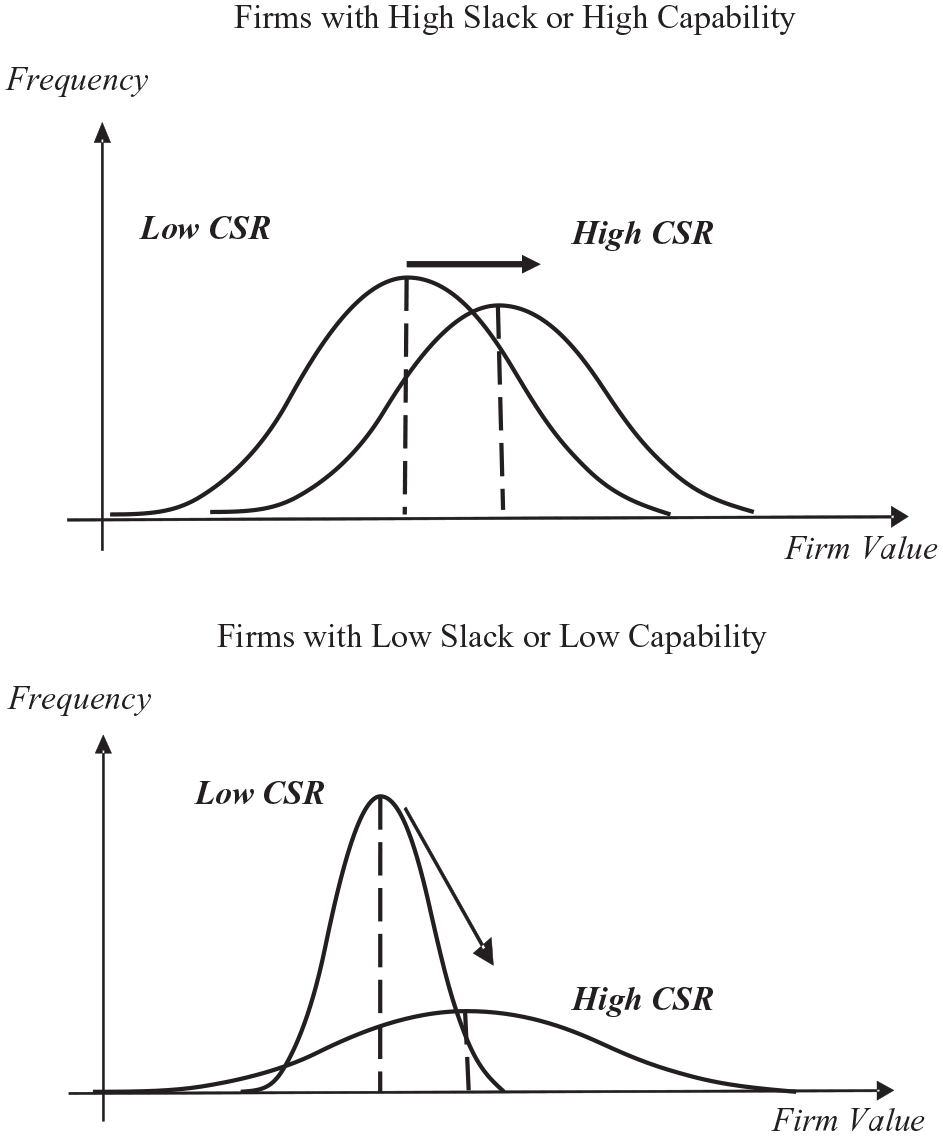

This study helps find an optimal balance between CSR investment, firm growth, and reliability of corporate performance. We propose that managers should be cautious about the timing of CSR investment to avoid unexpected negative impacts on firm value. We show that CSR’s impact on value is more reliably positive when a firm has sufficient highly redeployable slack or organizational capabilities in risk management, as shown in Figure 3. That is, allocating resources to CSR will be more likely to succeed when a firm possesses a high level of slack and when a firm exhibits superior capabilities in mitigating risk associated with CSR. Otherwise, investing in CSR is like a risky gamble, and the outcome of CSR is not reliable. Therefore, an important question a manager may need to ask before investing in CSR activities is: Do we have the resources and capabilities to ensure the success of our CSR strategy?

Illustration of the empirical results.

Our research may have several limitations that justify future research on this topic. We used the MSCI database to measure CSR. Although the MSCI database is frequently used in CSR research, it has certain issues. First, its rating criteria constantly change over time, raising data reliability issues. Second, MSCI’s sample universe relies heavily on the United States, which confines our sample to US companies only. Future research should explore CSR’s impact on firm value, and the reliability of this impact, using other CSR databases and firms from other countries.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Informed consent

This study does not involve human participants, their data or biological material.