Abstract

In this essay, I attempt to clarify the construct of strategic entrepreneurship from a new angle. By comparing the ideal-type theory of strategy without entrepreneurship with the ideal-type theory of entrepreneurship without strategy, I shed light on what it means to combine the logics of entrepreneurship and strategy and illustrate the value of their complementarity. The key insight is that entrepreneurship is blind without strategy and strategy is paralyzed without entrepreneurship. I further argue that many proponents of strategic entrepreneurship and action-based theories of strategy have prematurely given up on the idea of sustained competitive advantage. Disequilibrium and uncertainty do not automatically mean that no predictable and stable patterns can be relied upon for sustained competitive advantage.

Introduction

There have been debates on the relative scope and boundaries of entrepreneurship and strategic management as two fields of study (Meyer, 2009). Some have argued that the more established strategic management field is taking over entrepreneurship research (Baker and Pollock, 2007), while others have championed entrepreneurship as a distinct domain on its own (Shane and Venkataraman, 2000). While the debates are ongoing (Alvarez and Barney, 2013; Shane, 2012), an increasingly growing body of literature is recognizing the practical importance to both entrepreneurs and incumbent firms of combining the underlying logics of both strategy and entrepreneurship (Denrell et al., 2003; Hitt et al., 2001; Mathews, 2006a, 2006b; Rumelt, 1987; Stevenson and Jarillo, 1990), often using the label of “Strategic Entrepreneurship” (SE) to mark this approach (Hitt et al., 2001; Ireland et al., 2003; Kuratko and Audretsch, 2009). Ketchen et al. (2007) point out that “concentrating on either strategy or entrepreneurship to the exclusion of the other enhances the probability of firm ineffectiveness or even failure” (p. 372) while Hitt et al. (2011) argue that “successfully using SE challenges large, established firms to learn how to become more entrepreneurial and challenges smaller entrepreneurial ventures to learn how to become more strategic” (p. 59).

However, two decades after the introduction of the concept, the strategic entrepreneurship literature faces many challenges. In their scathing critique, Simsek et al. (2017) observe that

strategic entrepreneurship remains ill-defined and under-developed as a theoretical construct. Even as we readily acknowledge that strategy and entrepreneurship overlap in several ways, there is far less clarity around what constitutes the core features and distinctive identity of strategic entrepreneurship. Simply put, what do we gain by considering the two domains in concert rather than independently? (p. 505, italics in original)

In this essay, I attempt to answer this question in a manner not previously attempted by the SE literature, and that is to base my arguments on the underlying economic logics of strategy and entrepreneurship informed by mathematical and computation models. My aim is to clarify what entrepreneurship and strategy would mean as distinct logics from each other and what is gained by integrating these two logics. By using the term “logic,” I emphasize that I am building my arguments on a body of work that clarifies the arguments of strategy and entrepreneurship at an abstract level with formal modeling, thereby achieving greater precision, higher transparency, more consistency, and allowing us to more clearly identify implications (Adner et al., 2009). It is understandable that such an approach has been difficult in the past because the equilibrium-based mathematical models of neoclassical economics that have traditionally formed the economic foundations of strategy have not been able to interact properly with the disequilibrium-based narrative models of Austrian economics that have formed the economic foundations of entrepreneurship. In fact, these underlying economic literatures had already evolved into rather starkly disjoint schools of thought and balkanized communities of scholars even before the scholarly disciplines of strategic management and entrepreneurship were formed.

Two recent developments have informed my attempt to overcome this impasse and bridge the economic logics of strategy and entrepreneurship. First, a literature in strategic management has begun to reformulate the economic logics of equilibrium analysis with the alternative mathematical toolbox of cooperative game theory. This new approach has been able to better clarify the logics of equilibrium analysis and generate new insights in the growing literature known as “Value Capture Theory” (Gans and Ryall, 2017; Ross, 2018; Ryall, 2013) which essentially refers to a body of work utilizing cooperative game theory to formalize and advance strategy theory. Second, the cooperative game theory toolbox has proven to be rather amenable to dynamic disequilibrium analysis using computational models. A recent line of work explicitly incorporates disequilibrium dynamics into cooperative game theory in a manner largely consistent with Austrian economics (Keyhani, 2019; Keyhani and Lévesque, 2016; Keyhani et al., 2015), thereby opening a path to the integration of the underlying economic models of strategy and entrepreneurship. Essentially, given the common underlying mathematical framework, these two developments have finally allowed the theory of entrepreneurship and the theory of strategy to communicate with each other at a mathematical level.

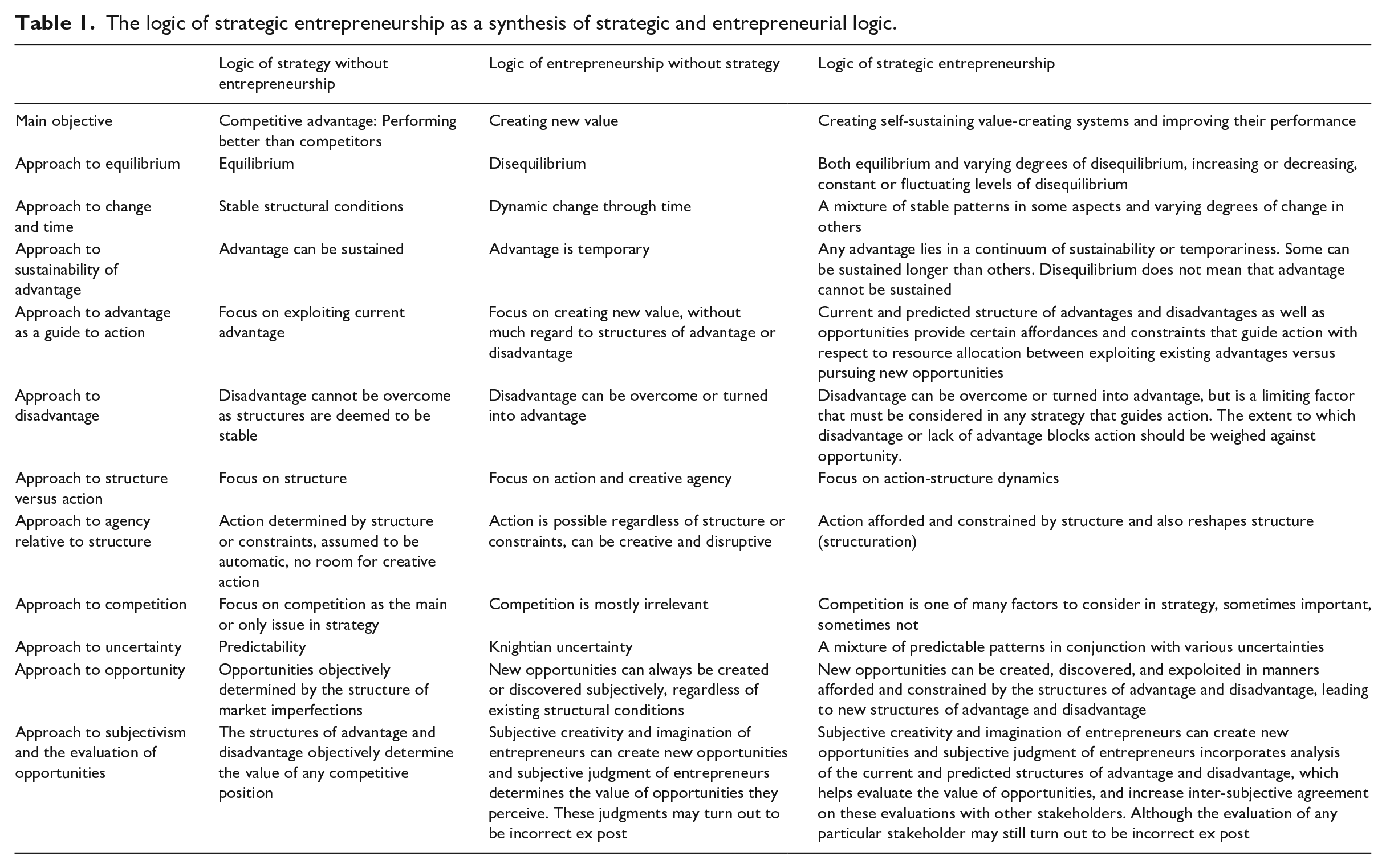

To understand what it means to combine the logics of entrepreneurship and strategy, we can begin by first understanding these logics in isolation from each other. Of course, not all theories of strategy are void of entrepreneurial logic and not all theorizing about entrepreneurship is void of strategic thinking. In fact, most theory in both literatures overlaps with one another. I intentionally employ the technique of highlighting extremes or “ideal types” as a theory development device. Table 1 provides a summary of the key points of comparison between the ideal types and what it would mean to combine their logics.

The logic of strategic entrepreneurship as a synthesis of strategic and entrepreneurial logic.

Based on this comparison and fusion of logics, I will make the following arguments: The logic of strategy without entrepreneurship is a logic of structures and constraints, and the logic of entrepreneurship without strategy is a logic of action and change. Neither is complete without the other. Entrepreneurship is blind without strategy and strategy is paralyzed without entrepreneurship. The disequilibrium-based entrepreneurial approach to strategy is strongest in combination with equilibrium-based analysis, not in isolation from it, and vice versa.

I will further argue that many proponents of strategic entrepreneurship and action-based theories of strategy have prematurely given up on the idea of sustained competitive advantage. Conditions of disequilibrium and Knightian uncertainty do not automatically mean that no predictable and stable patterns can be relied upon for sustained competitive advantage. I provide concrete examples of reliable mechanisms of sustained competitive advantage even in the face of Knightian Uncertainty.

The logic of strategy without entrepreneurship

My reference for theories of strategy that are largely isolated from the logic of entrepreneurship are theories based on the analysis of competitive structure in equilibrium. Consider two of the main theories that have dominated the mainstream of strategic management research in the past three decades (Conner, 1991): one is based on the structure-conduct-performance paradigm in Industrial Organization (IO), famously championed by Michael Porter, (1979, 1980); building on the work of Caves (1984) and Bain (1968); and the other is the resource-based view (RBV) based on the Chicago-UCLA school of economics and the work of Demsetz, (1973, 1982), famously formulated by Jay Barney (1986, 1991) 1 after the seminal papers by Wernerfelt (1984) and Rumelt (1984). Both of these theories take as a point of departure the first fundamental theorem of welfare economics, which states that if markets are perfectly competitive, they will reach an equilibrium in which all profits are dissipated (i.e. competed away). These two theories then proceed to locate “competitive advantage” or “supernormal profit” or “rent” by examining the existence of structural market imperfections or “barriers” that create deviations from the first fundamental theorem of welfare economics, and thus allow non-zero profits to be made in equilibrium (Barney, 1986; Foss, 2003; Mahoney, 2001; Yao, 1988). 2

Based on this logic, the IO-based theories emphasize external market forces such as customer and supplier bargaining power, threat of new entrants and substitutes, and intensity of rivalry among competitors (Porter, 1980). The weakness of any of these forces would indicate a market imperfection that could give the focal firm competitive advantage over competitors and in relation to other stakeholders in the resulting imperfectly competitive equilibrium. Shifting the pendulum from the outside to the inside of the firm (Hoskisson et al., 1999), the RBV emphasizes ownership and control of valuable, rare, inimitable, and non-substitutable resources (Barney, 1991). Control of such resources would be indicative of factor market imperfections that could give the focal firm competitive advantage over others in the resulting imperfectly competitive equilibrium.

Since equilibrium is considered a stable state (Samuels, 1997), rents in equilibrium are considered more desirable than any profits that may be made in disequilibrium. Because they are more sustainable compared to disequilibrium profits that are considered to be temporary (Peteraf and Barney, 2003). Hence, we have the emphasis on the sustainability of competitive advantage in theories of strategy. 3 Strategy scholars have identified and studied multiple “isolating mechanisms” that sustain the structures of advantage and disadvantage over extended periods of time (Oliver, 1997; Rumelt, 1984). In essence, equilibrium-based strategy logic is based on a model of stable structures and analyzes the position of the focal firm or agent within those stable structures.

In this framework, the information or knowledge that economic agents have is taken as constant, and is taken to be perfectly reflected in prices (Eckhardt and Shane, 2003), leaving no room for a change in this knowledge through discovery, creation, or imagination. Advantage is calculated based on what the market structure is now, not what it can or may become in the future. Furthermore, action is taken to be automatic in this framework, merely a corollary of individual rationality, determined by an objective analysis of structural conditions. Everyone is assumed to act swiftly to adjust their production or consumption in order to maximize their utility: given the structure of the market, agents will automatically act in a predictable way that ultimately brings about equilibrium. The initiative and capability to act is overshadowed by structural conditions as the main independent variable. For example, Barney (2001: 53) concedes that the classical formulation of the RBV assumes that, given possession of advantageous resources, “implementation follows, almost automatically” as though “the actions the firm should take to exploit these resources will be self-evident.” As stated by Chadwick and Dabu (2009), “without entrepreneurial knowledge, organizational actors in the RBV’s description of successful firms are reduced to the role of managerial caretakers, blessed by a lucky initial endowment of heterogenous resources and capabilities that they do not understand or fully control” (p. 263).

The logic of entrepreneurship without strategy

The logic of the entrepreneurial approach can be sought in the dynamic disequilibrium-based school of thought known as Austrian economics (Hayek, 1948; Keyhani, 2019; Lachmann, 1986; von Mises, 1949) although it has had influences from outside of Austrian economics as well. Austrian economics has been suggested as an alternative foundation for strategy theory (Jacobson, 1992) but has generally been more welcomed in entrepreneurship theory as the economic foundation of entrepreneurial action. Here, I outline the major tenets of entrepreneurial logic that are largely distinct from equilibrium-based strategy logic.

A distinctive feature of the Austrian approach is an emphasis on subjectivism, which can be defined as taking account of “the facts that individuals hold different preferences, knowledge, and expectations” (Foss et al., 2008: 74). From the subjectivist theory of value, we have the idea that value is in the eye of the beholder and that different people have different preferences. From Hayek, we have inherited the idea that different people have different knowledge, and from Shackle (1979) and Lachmann (1986), subjectivism has been extended to imagination and expectations. The “activeness of the mind” advanced by Shackle is a strong intellectual foundation for the agency of the entrepreneurial actor and her ability to create opportunity, and in line with calls to incorporate creative action into theories of strategy (MacLean et al., 2015). Through imagination, every person is a creator of something out of nothing (Shackle, 1979). Humans are not just the takers and processors of information; they are also creators. They create new information through their choices and actions because they have the capability to imagine.

A corollary to this emphasis on subjectivism and creative agency is the highlighting of three concepts that are absent in equilibrium-based strategy logic: change, uncertainty, and action. Austrian economists have long criticized the neoclassical model for its static approach, which they particularly recognize as the culprit behind the lack of place for the entrepreneur in neoclassical theory (Foss, 2000a). According to entrepreneurial logic, in an economy of creative agents, change is the rule rather than the exception, and no stable equilibrium condition is likely to last long enough to matter. Disequilibrium is the default condition. Thus, any potential advantage is considered temporary (D’Aveni et al., 2010; Farjoun, 2007), but on the flip side, disadvantages can be overcome and possibly turned into advantages (Brush et al., 2001; Madhok and Keyhani, 2012; Miller, 2003). To emphasize the distinctive nature of the entrepreneurial approach in relaxing the reliance on existing structures of advantage and disadvantage, Stevenson and Jarillo (1990) define entrepreneurship as the pursuit of opportunity without regard to the resources currently under control. Worded more generally, entrepreneurial logic without strategy emphasizes action without regard to structural conditions. Action is not automatic or predetermined by structure in entrepreneurial logic.

Much of the knowledge that any agent has at any given time may become obsolete soon, or their subjective judgments may turn out to be wrong. The literature has often referred to the notion of “Knightian Uncertainty” to describe the conditions of unknowability that entrepreneurs often face (Townsend et al., 2018). However, Knightian uncertainty does not just mean that actors are lost in an uncertain and ambiguous world; there is a positive side to this coin. If economic actors are in constant ignorance (O’Driscoll and Rizzo, 1985), and perfect knowledge of the future is unknown and unknowable, it follows that the future can never be perfectly reflected in current prices in the market (Eckhardt and Shane, 2003). This means that potential opportunities for profit can never be assumed away.

Opportunities in turn motivate action. Entrepreneurial action can be defined as acting in pursuit of value creation, which can involve creating new opportunity or to exploit opportunity perceived to have been discovered (Alvarez and Barney, 2007). Entrepreneurial action is judgmental in nature because there is no objective guarantee that it will in fact lead to the envisioned value creation (Foss and Klein, 2012). There is no demonstrably correct procedure to verify these judgments objectively ex ante (Loasby, 2007). Perceived opportunity, or the “business idea” (Shane, 2012), can only exist subjectively as judgments about the future that may later prove to be wrong (Casson, 1982). Nevertheless, creative agency means that unlike equilibrium analysis, being limited to a strictly given set of alternatives to choose from, is the exception rather than the rule. Coupled with the capability to act and influence the world directly, imagination gives the decision-maker the ability to make new alternatives and shape the future, rather than merely choose among given futures (Sarasvathy, 2001). In fact, it can be argued that most structures of advantage can be traced back to entrepreneurial actions based on subjective judgment (Foss and Klein, 2012).

In addition to Austrian economics, entrepreneurial logic has benefited from theory development in the context of new ventures, and the features of this context have allowed it produce insights that are distinct from equilibrium-based strategy logics. For example, entrepreneurial logic has a bias toward action under conditions of Knightian uncertainty because of the learning value of pursuing something rather than nothing (Gans et al., 2019). The lean startup literature stresses that a startup is not so much a smaller version of a larger organization, but a search mechanism for a working business model that is more about the actions that need to be taken before any stable structure is achieved (Blank, 2013). Because of this, the notion of “competition” which is at the heart of equilibrium-based analysis has been almost entirely irrelevant for many startups. The main objective in entrepreneurial logic is not competitive advantage but new value creation. The analysis of competition assumes that multiple firms have already figured out how to create value (i.e. have discovered working business models) with similar products or offerings, and proceeds to compare their competitive positions relative to each other. For many startups, it is too early for this type of analysis to be relevant, as they are focused on first validating that they can create any value at all.

The logic of strategic entrepreneurship (and entrepreneurial strategy)

Let us conduct a thought experiment to consider what the logic of a (disequilibrium-based) entrepreneurial approach to strategy may add to an equilibrium-based approach: suppose two rival firms have practically identical market positions in terms of bargaining power, threat of entrants and substitutes, and rivalry. Suppose also that they have practically identical resources and technologies. Furthermore, suppose that they both operate in all regions of country A but not in the attractive and untapped market of country B. In such a case, both IO theory and the RBV will have little to say on which firm has an advantage over the other, or whether and how such an advantage may be created. These theories have little to recommend firms starting off with no advantage or even with a disadvantage.

Even though pure entrepreneurial logic may not always be concerned with competitive advantage, the logic of action can be applied to this context. An entrepreneurial approach to strategy would have something to say about actions that can be taken under conditions of non-advantage or disadvantage (Brush et al., 2001; Madhok and Keyhani, 2012; Miller, 2003). It would suggest that one firm may gain advantage over the other by being first to discover and identify the opportunity to enter the market of country B. If both firms discover this opportunity at the same time, the entrepreneurial approach would say that one firm may still gain advantage over the other by having the initiative to actually act on this opportunity. If they both act on the opportunity, the entrepreneurial approach would say that one firm may still gain advantage over the other by inventing a new cost-effective technology sooner than the other, or by finding a new way to render a previously unattractive market in a third market (say country C) profitable and entering that market. The entrepreneurial approach would also say that there is no guarantee that any of these efforts will be successful.

Now let us switch the thought experiment to a situation where strategic logic can add value to an entrepreneurial approach. Suppose a machine learning expert who has no prior experience in—nor expert knowledge of—the restaurant business or fast-food industry is considering whether or not to launch a McDonald’s franchise. Purely entrepreneurial logic may emphasize the possibility that this entrepreneur has subjectively perceived an opportunity in launching this franchise that others have not seen, and that they may be successful despite their prior lack of experience in this Industry. Such a logic may emphasize the Knightian uncertainty this entrepreneur faces, which makes it impossible to predict success, and it may encourage an action-biased approach to launch the restaurant and test the opportunity.

Some equilibrium-based strategy logic may be helpful to the entrepreneur here. There are many aspects of this situation that can be analyzed as relatively stable and predictable structural conditions, with a high level of objectivity (or at least inter-subjective agreement). Most people would agree that given the entrepreneur’s expertise in machine learning, there is a high opportunity cost to not leveraging that expertise in the tech industry. Furthermore, the financial performance and work conditions of franchise owners are relatively well known and largely predictable. Due to the entrepreneur’s lack of experience in this type of business, McDonald’s would only allow them to purchase an existing franchise location, and they would not be bringing any special resource advantages to the business. The structure of competition among McDonald’s and its competitors is also relatively stable and well known to be aggressive in this mature industry. Furthermore, the restrictions of franchise agreements would not really allow the entrepreneur to engage in much innovation in customizing the restaurant with their creative imagination or to engage in low-cost ways to test the opportunity before fully committing. All of these arguments are based on analysis of stable and relatively predictable structural conditions and are all useful in guiding the entrepreneur’s decision making.

I want to emphasize here that practicing entrepreneurs and strategists regularly combine the logics of strategy and entrepreneurship in their plans and actions. The conceptual exercise of trying to understand the ideal types of strategy without entrepreneurship and entrepreneurship without strategy helps us better understand the nature of their combined logics, and the nature of how scholarly theories of strategy and entrepreneurship provide guidance to practicing entrepreneurs. It also helps us understand when a given strategy could be described as more or less entrepreneurial, depending on the extent to which it relies on the logics of stable structural conditions or disregards them in favor of an action-biased approach. The logic of strategy without entrepreneurship is a logic of structures and constraints, and the logic of entrepreneurship without strategy is a logic of action and change. Neither is complete without the other, and any given strategy may be biased toward one or the other. In either case, entrepreneurship is blind without strategy and strategy is paralyzed without entrepreneurship.

A combined strategic entrepreneurial logic recognizes that while many aspects of the future are highly uncertain, some aspects are relatively predictable. While change is rampant, some patterns are stable and systematically repeated over extended periods of time. Stable and predictable patterns can be used to evaluate at least some aspects of opportunities and assess the likelihood of success. While creative action is possible, real constraints exist that restrict the boundaries of action, some in our favor and some not. Strategic entrepreneurial logic also recognizes that stable structural conditions do not fully dictate all possibilities of action. Strategists who are entrepreneurial do not limit themselves to only building on existing strengths and exploiting existing advantages. It is possible to build new strengths and overcome disadvantages. On the flip side, advantages can be lost and competitors can take us by surprise but this does not mean that sustained competitive advantage is impossible. 4 Entrepreneurs who are strategic are, from the outset, not looking just to create value but to create self-sustaining value-creating systems that have growth potential and long-term defensible strategic advantages over would-be competitors.

Strategic entrepreneurship and the sustainability of advantage

Combining the logics of entrepreneurship and strategy is not unique to the literature that is explicitly labeled as Strategic Entrepreneurship. A host of more recent theories of strategy have attempted to move beyond an equilibrium framework to incorporate entrepreneurial logic. In order to emphasize a focus on dynamics, all of these theories explicitly refer to the role of action as a centerpiece. The competitive dynamics literature studies competitive moves and countermoves by taking the “action/response dyad” as the central unit of analysis, and examining characteristics of these actions including their aggressiveness, frequency, speed, and scope (Chen, 1996; Chen and Miller, 2012). The resource management literature emphasizes the role of “managerial action” in structuring, bundling, and leveraging resources, in addition to—and distinct from—the characteristics of the resources themselves (Sirmon et al., 2007, 2008). This is closely related to the dynamic capabilities and asset orchestration literature that emphasizes actions of search or selection and configuration or deployment (Helfat, 2007; Sirmon et al., 2011). The term “capability” is often used in the strategic management literature to refer to the dynamic aspects of action taken on resources to produce change rather than the resources themselves, and this distinction has been the hallmark of the dynamic capabilities approach, sometimes with explicit reference to opportunity creation, discovery, and exploitation as the fundamental actions of concern (Teece, 2007). I refer to these theories as action-based theories of strategy. 5

While strategy theories have made considerable progress in incorporating entrepreneurial and action logic, I believe that the emphasis on change, dynamism, disequilibrium, subjectivism, and creative agency may have at times overshadowed the usefulness of analyzing those aspects of strategic situations that are stable and predictable structural conditions with considerable inter-subjective agreement. This is particularly exemplified in discussions of the sustainability of advantage. I argue next that any proponents of strategic entrepreneurship and action-based theories of strategy that have given up on the idea of sustained competitive advantage may have done so prematurely.

While the equilibrium-based theories such as the IO approach and the RBV heralded the prospect of “sustained” competitive advantage as the holy grail of strategy, the entrepreneurial approach appears to offer nothing more than temporary advantage. All of the above-mentioned action-based theories of advantage emphasize its temporary nature (D’Aveni et al., 2010). Sirmon et al. (2007) state that in the face of uncertainty, “sustaining a competitive advantage over time is unlikely, with the result that a firm instead will seek to develop a series of temporary competitive advantages” (p. 274), while Chen et al. (2010) point out that “competitive advantage is time dependent and ephemeral, and any advantage gained by a firm through its actions will be negated sooner or later by competitors’ responses” (p. 142). Eisenhardt and Martin (2000) emphasize that dynamic environments prompt businesses to “compete by creating a series of temporary advantages” (p. 1117). Klein et al. (2013: 781) observe that the field of strategic entrepreneurship “appears to have dropped strategic management’s search for the conditions of sustainability of (any single) competitive advantage, and instead focused on the entrepreneurial pursuit of a string of temporary advantages” (p. 781).

In other words, the hope for advantage sustainability is reduced to the pursuit of multiple consecutive acts of advantage creation (Farjoun, 2007). While in the previous paradigm, a structural advantage could itself provide the grounds for sustainability, in the entrepreneurial paradigm it is not enough to have one such advantage. Rather, it is necessary to continuously create such advantages by incessantly discovering and creating new opportunities and acting to exploit them.

While I agree that no particular advantage is likely to be infinitely everlasting (nor completely ephemeral), and that advantageous structural conditions should be evaluated on a continuum of temporariness and sustainability, I suggest that entrepreneurs and strategists can still rely on some predictable structural conditions and mechanisms to be a source of long-lasting performance advantage, even among all the Knightian uncertainty and disequilibrium conditions that they face in other aspects of their business. This suggestion is supported by my personal observations of how digital entrepreneurs and their investors think and talk about strategy in Internet-based businesses.

In the practitioner world, sources of sustained advantage are often referred to as “moats” and startup investors actively assess new ventures to see if they benefit from such moats. Venture capital investor Jerry Neumann has put together “A Taxonomy of Moats” on his blog (Neumann, 2019). Another investor, Brian Laung Aoaeh (2016) provides detailed discussion of five major economic moats for early stage startups. I delve into three examples of such moats below.

Network effects are probably the most widely recognized moats. Interestingly, the economics of network effects was not developed in equilibrium-based strategy theory but rather in the literature on the economics of information goods. Consider the type of markets that exhibit rich-get-richer and winner-take-all phenomena (Shapiro and Varian, 1999). In these markets, once a small advantage is created, a positive feedback loop such as those created by network externalities (Katz and Shapiro, 1985, 1986), can result in a snowballing effect that renders the advantage over competitors greater and greater over time. Therefore, just “acting” quicker than competitors can by itself create first mover advantage (Kerin et al., 1992) and this advantage can be to some extent sustainable due to such factors as increasing returns mechanisms (Arthur, 1988), path dependencies (Teece et al., 1997), and time compression diseconomies (Dierickx and Cool, 1989). However, the important property of network effects is that the advantage does not go necessarily to the first to enter, or the most superior product, but rather the first to scale (Arthur, 1988; Hoffman and Yeh, 2018). Companies such as Facebook, Twitter, LinkedIn, Uber, AirBnB, Amazon, and many others have scaled with strong network effects that have remained a source of competitive advantage for them for years. Two-sided and multi-sided platforms exhibit two-sided and multi-sided network effects which have their own specific structural patterns that can be relied upon for competitive strategy (Parker et al., 2016; Rochet and Tirole, 2006).

Even if network effect mechanisms are not particularly strong, having a large audience and community is itself a highly coveted strategic advantage. This has led to increasing interest in an audience-first approach to entrepreneurship where the actual business idea is decided on after the audience has been built (Kahl, 2021). The moat is built even before the business itself in order to reduce risk and uncertainty. Recognizing the value of such moats, The Community Fund (https://thecommunity.vc/) is a venture capital fund with the specific aim of investing in community-driven businesses. In the attention economy (Davenport and Beck, 2002), a social media audience can easily be monetized, and this is a relatively reliable and stable pattern no matter what other uncertainties a business faces. As an example of an audience-first approach to entrepreneurship, entrepreneurs can experiment with creating content on multiple social media accounts around specific niches. When one of them catches on, they can monetize this audience with advertising, drop shipping, or other methods (Anderson, 2019). As another example, if a business has a large amount of users on which the business is able to access valuable data and analytics, even if they are not paying customers the data itself are considered to be a competitive moat that can form the basis of various strategic advantages (Newman, 2014).

Finally, a less appreciated mechanism of sustained competitive advantage that can persist under disequilibrium and Knightian uncertainty is that of generativity. 6 Generativity refers to “a system’s capacity to produce unanticipated change through unfiltered contributions from broad and varied audiences” (Zittrain, 2008: 70). An alternative way to describe generativity in the context of strategy is a mechanism that massively increases the participation of external stakeholders (typically “users”) into the value creation process and allows the firm to profit from the resulting innovations. It is taking advantage of user innovation (Von Hippel, 2005) but enabled by features of the product or technology itself that automate the process, detach it from the organizational and managerial constraints and capabilities of the firm, and render it more scalable. In other words, it could be thought of as the automation of open innovation. When companies build products that have built-in features allowing broad audiences to innovate with those products, and when mechanisms are in place for the company to profit from these distributed innovations, generativity can become one of the most powerful competitive moats possible. A generativity advantage can essentially be defined as a firm’s ability to profit from the innovations of others on a massive scale, without incurring the costs of their experimentation or bearing their risks of failure (Keyhani, 2021; Keyhani and Hastings, 2021). For example, Google and Apple profit from successful new apps on their mobile marketplaces, without incurring the costs of building them or bearing the risks of their failure (Tajedin et al., 2019). As another example, no-code app development platforms like Bubble.io allow their users to easily build software products, profiting from the successful ones and even on many of the failed experiments.

Concluding remarks

Many have called for better clarification, definition, and development of strategic entrepreneurship as a theoretical construct (Kuratko and Audretsch, 2009; Simsek et al., 2017). In this essay, I have attempted to clarify the construct of strategic entrepreneurship from a new angle. By comparing the ideal-type theory of strategy without entrepreneurship with the ideal-type theory of entrepreneurship without strategy, I shed light on what it means to combine the logics of entrepreneurship and strategy. A summary of this comparison and synthesis is provided in Table 1. 7

From this exercise, an important insight is gleaned: Neither logic is complete without the other, and any given strategy may be biased toward one or the other. The literature on action-based theories of strategy and strategic entrepreneurship may have become prematurely biased toward disequilibrium and uncertainty, and against the feasibility of sustained competitive advantage. However, computational models show (aligned with practical intuition) that conditions of disequilibrium and uncertainty do not automatically mean that no predictable and stable patterns can be relied upon for sustained competitive advantage. Practicing entrepreneurs and strategists working on validating business ideas under conditions of disequilibrium and Knightian uncertainty, along with their investors, think and talk about competitive moats, barriers to entry and isolating mechanisms regularly. Our theories of strategy and entrepreneurship in the world of scholarship should ideally be in line with these realities.

Footnotes

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Notes

Author biography

![]() as well as an OnDeck No Code Fellow. His other experiences include roles such as business advisor to multiple startups, Lab Strategist at the Creative Destruction Lab Rockies, and a David Rockefeller Fellow at the Trilateral Commission. He received his doctorate in strategic management from the Schulich School of Business, York University in Toronto, Canada, and has a MSc in Entrepreneurship and BSc in Applied Mathematics, both from the University of Tehran, Iran.

as well as an OnDeck No Code Fellow. His other experiences include roles such as business advisor to multiple startups, Lab Strategist at the Creative Destruction Lab Rockies, and a David Rockefeller Fellow at the Trilateral Commission. He received his doctorate in strategic management from the Schulich School of Business, York University in Toronto, Canada, and has a MSc in Entrepreneurship and BSc in Applied Mathematics, both from the University of Tehran, Iran.