Abstract

Corporate governance research suggests that boards of directors play key roles in governing company strategy. Although qualitative research has examined board–management relationships to describe board involvement in strategy, we lack detailed insights into how directors engage with organizational members for governing a complex and long-term issue such as product innovation. Our multiple-case study of four listed pharmaceutical firms reveals a sequential process of board involvement: Directors with deep expertise govern scientific innovation, followed by the full board’s involvement in its strategic aspects. The nature of director involvement varies across board levels in terms of the direction (proactive or reactive), timing (regular or spontaneous), and the extent of formality of exchanges between directors and organizational members. Our study contributes to corporate governance research by introducing the concept of board behavioral diversity and by theorizing about the multilevel, structural, and temporal dimensions of board behavior and its relational characteristics.

Introduction

Boards of directors of large publicly traded corporations play key roles in their company’s strategy (Zahra and Pearce, 1989). Prior studies have often examined these roles to better understand the nature of director involvement, also termed engagement, in strategy (Golden and Zajac, 2001; Rindova, 1999). Much of the research has adopted an agency-theory lens and emphasized the board’s role in monitoring managers’ strategic decisions by overseeing and incentivizing them to make decisions that optimize shareholder value (Eisenhardt, 1989a; Jensen, 1993). Other studies, in line with the resource dependence perspective, have emphasized the board’s role in advising managers on strategy by providing them with information, resources, and counsel (Hillman and Dalziel, 2003; Pfeffer and Salancik, 1978). Both perspectives assume that directors are involved in strategy, but they do not explain how they engage.

Scholars have argued that directors’ knowledge and expertise is a precondition for effective board involvement in strategy (Hambrick et al., 2015). Indeed, to provide an informed foundation for monitoring or advising management on strategic issues, boards require substantial human capital (Carpenter and Westphal, 2001), defined as the aggregate knowledge, skills, experience, and expertise of its directors (Becker, 1964). Individual directors often have specific, deep human capital that allows them to engage in complex decision-making and problem-solving in their areas of expertise and bring a more complete understanding about critical issues in such areas (Glaser and Chi, 1988; McDonald et al., 2008). The full board often seeks a diverse blend of this human capital across its members (Hillman et al., 2000).

Director human capital is particularly important for governing a complex and long-term strategic issue such as innovation, which can be defined as the adoption of a new idea, whether a new product, process, service, technology, or practice (Hage, 1999; Van de Ven, 1986). Researchers have recently given more attention to the board’s role in product innovation (Hoskisson et al., 2002; Kor, 2006), a research focus that we follow. It is of particular interest, since the effective creation and adoption of new products have a major impact on a company’s long-term strategy and growth (Penrose, 1959), areas central to any board’s governance responsibilities. However, the research and development (R&D) required to generate innovative products usually entails high risks, large uncertainties, and major investments (Hoskisson et al., 2002). Thus, its governance calls for deep and diverse human capital within the board.

Yet board human capital remains inert unless directors find ways to tangibly apply it to their roles via direct involvement (Forbes and Milliken, 1999). It is very difficult to observe and measure directors’ knowledge application, however, since it takes place behind closed doors (Hoppmann et al., 2019). Consequently, scholars have often reverted to using the board’s human capital composition as a proxy for its involvement (Tian et al., 2011).

Other research, however, has pointed to ways in which director engagement can be more directly observed. Selective qualitative research has shown that boards engage in strategic issues by working with managers inside and outside the boardroom (Carter and Lorsch, 2004; Stiles, 2001). This research focuses on interactions between directors and executives (Hendry et al., 2010; McNulty and Pettigrew, 1999), between directors and the CEO (Garg and Eisenhardt, 2017), or among board directors (Hoppmann et al., 2019). Emerging research on behavioral corporate governance has found that these interactions are shaped by directors’ past experience and social context (Westphal and Zajac, 2013).

Nevertheless, to engage in an uncertain and long-term strategic issue such as innovation, which involves complex technical and scientific challenges, director involvement will likely involve interactions beyond those with top management. Directors need to understand the specific organizational context in which innovations are to be advanced if they are to apply their human capital to the detailed aspects of innovation. By engaging directly with those on the forefront of research, development, and innovation in the organization, directors can gather and process company-specific information and integrate it into their knowledge base (Forbes and Milliken, 1999). Furthermore, to reduce the information asymmetries normally present between directors and managers (Eisenhardt, 1989a), directors can not only rely on the information that the top management provides but will also need to gather and process information about the firm’s innovation from deeper within the organization.

To date, extant conceptualizations of direct board involvement in long-term strategic issues such as innovation have been fairly coarse, limiting the power of our theoretical and empirical models. We lack consistent theorizing about how directors interact with organizational members (employees at different organizational levels). In addition, no study has explored how directors’ human capital is directly applied and leveraged for innovation—an important issue to be addressed if we are to fully understand how boards operate. Since directors’ monitoring and advising can have a major impact on innovation, we need to better understand what happens inside of what has been too much of a black box.

Our aim is to help open this black box by studying how directors interact with organizational members for monitoring and advising on product innovation. Since directors’ involvement in innovation leaves so little accessible evidence, we applied inductive methods to study four major pharmaceutical companies. Firms in this industry are especially research-intensive and dependent on new products to keep pace with their competitors (Kor, 2006). Furthermore, ongoing scientific and technological developments have led to frequent product changes, and firms must invest significantly in innovations to remain competitive (Datamonitor, 2009).

Our findings reveal a sequential board involvement process: Directors with scientific expertise first interact directly with organizational members (hereafter: OMs) to learn about and govern scientific innovation. They then take their insights to the full board for its governance of strategic innovation. Director involvement varies between these board levels in its proactive or reactive triggers, regular or spontaneous expression, and formal or informal exchanges.

Our study contributes to corporate governance research in several ways. First, to our knowledge, this is the first study to introduce and provide in-depth insights into board behavioral diversity, that is, the differences in board involvement across board levels and over time. This advances the behavioral theory of corporate governance (Westphal and Zajac, 2013), which has primarily focused on strategic interactions between the board and executives, by showing that board involvement in innovation is a process during which specific directors focus sequentially on different contents and interact with distinct members at varying organizational levels.

Second, our study extends agency theory (Eisenhardt, 1989a) and the resource dependence perspective (Hillman and Dalziel, 2003) and addresses the corporate governance debate on the board’s involvement in strategy (Carpenter and Westphal, 2001) by showing how directors apply their human capital to monitor and advise, helping to open the black box of board involvement. Specifically, our findings allow us to theorize about board involvement by conceptualizing its (1) multilevel (individual directors, board subgroup, and the full board), (2) structural (extent of pro-activeness and formality of exchanges between directors and OMs), and (3) temporal (regular vs spontaneous exchanges; sequential board involvement process) aspects, and (4) the role of relational characteristics (trusting working relationships between directors and OMs). By showing that board involvement in innovation is more multifaceted than previously assumed, this study presents a more nuanced and comprehensive account of board involvement than prior research.

Third, our study contributes to research on the role of board human capital by showing that it is a necessary but insufficient condition for board involvement: Despite similar human capital configurations (board diversity), the extent and form of board involvement varied between companies. Corporate governance research has traditionally studied the relationships between directors’ human capital and firm outcomes (McDonald et al., 2008; Sundaramurthy et al., 2013). By contrast, our study provides a more detailed elaboration of the mechanisms that enable directors to apply and leverage their human capital to govern company innovation.

Finally, our study contributes to innovation research by providing fresh insights into intra-organizational knowledge transfers between the board and the firm’s operating levels, revealing the importance of vertical relationships across hierarchical levels.

Board roles in strategy

Corporate governance research has generally viewed the board of directors as a team at the apex of a firm that can impact its strategy and direction, including the means by which it achieves future growth (Forbes and Milliken, 1999; Zahra and Pearce, 1989). Prior research has predominantly studied board roles in strategy, focusing on board monitoring and advising.

The monitoring role, with its foundations in agency theory (Fama and Jensen, 1983; Jensen and Meckling, 1976), calls for directors to oversee managers (Jensen, 1993). Because of the separation of ownership and control (Fama and Jensen, 1983), boards are obligated to monitor managers to ensure that they act in the shareholders’ best interests ((Eisenhardt, 1989a; Jensen and Meckling, 1976). Executives suggest, initiate, and implement strategic initiatives, while directors are responsible for monitoring and ratifying them (Rindova, 1999). A second role, board advising, has its underpinnings in the resource dependence perspective (Pfeffer and Salancik, 1978), which views directors, particularly outsiders, as boundary-spanners who provide management with externally obtained information and advice (Hillman et al., 2000; Pfeffer and Salancik, 1978). Directors are regarded as creating connections (Useem, 1984) and attracting resources to enhance company performance (Pfeffer and Salancik, 1978). They modify or even drive strategies and provide influential advice on issues ranging from restructuring to execution (Carpenter and Westphal, 2001; Lorsch and MacIver, 1989). While these two theoretical traditions describe board roles, they do not explain how directors perform their monitoring (Zahra and Pearce, 1989) or advising roles (McNulty and Pettigrew, 1999).

Studying how boards are involved in strategy is challenging, since this involvement is largely invisible (Carter and Lorsch, 2004). Prior research has therefore long-examined the elements of board design that should enable directors to monitor or advise on strategy, such as the ratio of outsiders, director shareholdings, board size, CEO duality (Baysinger and Hoskisson, 1990; Finkelstein and Mooney, 2003), and the time boards devote to strategy (Golden and Zajac, 2001; Tuggle et al., 2010). In the context of product innovation (hereafter: innovation)—our study’s focus—available research has focused on the impact of director holdings, board outsiders, and interlocking directorates on R&D intensity, as well as on whether companies opt to build or acquire innovation (Dalziel et al., 2011; Geletkanycz and Hambrick, 1997; Hoskisson et al., 2002). Yet, this research offers no insights into how boards engage directly in innovation.

A developing research stream in corporate governance endeavors to better understand what influences directors’ ability to monitor and advise on strategy by studying their human capital (Hambrick et al., 2015; Haynes and Hillman, 2010). According to agency theory, specific director knowledge is required to oversee complex decisions in organizations (Fama and Jensen, 1983). The prevailing notion in prior studies is that boards can act as teams that monitor due to their members’ combined knowledge (Fama and Jensen, 1983; Zahra and Pearce, 1989). Furthermore, as suggested by the resource dependence perspective, outsiders can contribute the varied human capital that they have accumulated during their professional careers and as directors of other firms (Carpenter and Westphal, 2001; Useem, 1984). This allows them to learn from engaging in strategic decisions and to better assess particular decisions’ consequences (McDonald et al., 2008).

Consequently, corporate governance research has often focused on either directors’ specialized human capital (e.g. their experience with acquisitions or innovations) (Kor and Sundaramurthy, 2009; McDonald et al., 2008) or on the diversity of human capital within the board (Golden and Zajac, 2001; Haynes and Hillman, 2010). However, in order to understand board involvement, one must consider both dimensions: specialist directors who share their experience and learn about company activities in their area of expertise, and the full board, composed of experts with varied backgrounds. Specialized directors’ deep understanding of specific areas and the full board’s diverse human capital are both important, and we need to better understand whether and how expert directors directly share and apply their knowledge when governing strategy both individually and through the full board.

Emerging research on board behavior

Two research streams have begun to investigate board behavior more directly. First, the behavioral perspective on corporate governance has addressed how social context and past experience shape actors’ behaviors (Westphal and Zajac, 2013). Studies have examined interpersonal relationships between the CEO and directors, showing that CEOs who have friendship ties with outside directors seek more advice from them. Furthermore, directors are more likely to offer strategic advice to top managers if they have gained relevant strategic experience from board appointments at other firms (Carpenter and Westphal, 2001). While this research has examined the microsocial processes that underlie the relationship between management (the CEO) and the board, it has not yet sought to provide a larger theorizing on board involvement in strategy (Garg and Eisenhardt, 2017), particularly in the area of innovation.

Second, selective qualitative research has examined board involvement in strategy (Carter and Lorsch, 2004; Rindova, 1999; Stiles, 2001). In studying part-time directors’ interactions with executives, McNulty and Pettigrew (1999), for instance, revealed that while all boards make strategic decisions in the boardroom, only a minority of boards continuously shaped the context, content, and conduct of their company’s strategy. Directors interacted with management not only during board meetings but also outside of meetings to enhance their knowledge of the company or to discuss the feasibility of an executive’s proposed plan (Hendry and Kiel, 2004; Roberts et al., 2005). Garg and Eisenhardt (2017) studied how venture company CEOs engaged in effective strategy making with their board. They found that the CEOs captured useful advice from their directors, while also maintaining control of the strategy-making process. Ravasi and Zattoni (2006) found that board members’ relevant knowledge relates to the scope of their strategic involvement and that boards can help reconcile shareholders’ conflicting views on strategic options.

In sum, qualitative research has provided insights into the practices that boards use to engage in strategy and the importance of directors’ relevant knowledge for their involvement, and has found that board involvement not only takes place in formal meetings—as often studied in quantitative research (Tuggle et al., 2010)—but also outside of such meetings. Despite the important insights of this research, it has largely focused on interactions between boards and management around more general strategic issues, and has not differentiated much between directors’ varied areas of human capital.

We thus lack a fuller understanding of how directors apply their specialized human capital to strategic issues and how they interact with different OMs in doing so. The information processing literature has long shown that individuals process information in line with their expertise (Huber, 1991), suggesting that directors engage in and contribute differently to strategic issues as a function of their expertise. It is important to better understand such potential behavioral differences, since directors’ monitoring and advising influence critical strategic actions. Although prior research has provided first insights into board involvement, we lack coherent theorizing on board involvement in complex and long-term strategic issues such as innovation. We address this gap by studying how board directors engage directly with OMs to govern innovation.

Methods

Research setting

Our research design entails a multiple-case study (Eisenhardt, 1989b) of four major pharmaceutical firms. We have opted for a deeper study of a small set of cases to gain a more holistic understanding (Yin, 2003) of board involvement. Multiple cases also allow for a replication logic, in which cases are treated as discrete experiments that confirm or disconfirm emerging conceptual insights (Eisenhardt, 1989b). We chose to focus on product innovation in large, publicly traded pharmaceutical companies, because creating new, commercially viable products in this industry is research-intensive and the firms’ high visibility and investor vigilance make them particularly susceptible to intense pressure to innovate. Thus, boards are likely to be involved in a subject as complex as innovation. Symptomatic of the intense demands on executives and directors in this industry, investors forced the CEO and the board chairman of AstraZeneca, the world’s seventh largest pharmaceutical company, to step down in 2012 because it had failed to create and sustain a strong and innovative product pipeline (Pollack, 2012: B3).

We sampled cases on the basis of four criteria. First, given our focus on how boards engage in innovation, we sampled more innovative and less innovative firms (Yin, 2003). We measured each company’s innovativeness (Ahuja and Katila, 2004) over the 5 years preceding our interviews as the number of new patents assigned to it—a proxy for the extent to which its R&D efforts resulted in patents (e.g. Kor, 2006)—and as patent citations in other firms’ patent applications—a proxy for the value of a firm’s existing patents (Trajtenberg, 1990). Three of the firms had high innovativeness scores and one had low scores. Second, we selected firms that reported at least US$30 billion in sales and had at least 90,000 employees, since we presumed that large firms’ boards would face significant challenges when engaging in innovation. The firms were among the 10 largest pharmaceutical firms in Europe and in the United States, respectively, as defined by their revenues in 2008. Third, we focused on firms where we could conduct at least four interviews to compensate for shortcomings in participant observer reports. Fourth, to maintain comparability, we selected cases with a single-tier board system, which combines executive and supervisory responsibilities in one legal entity (Weimer and Pape, 1999).

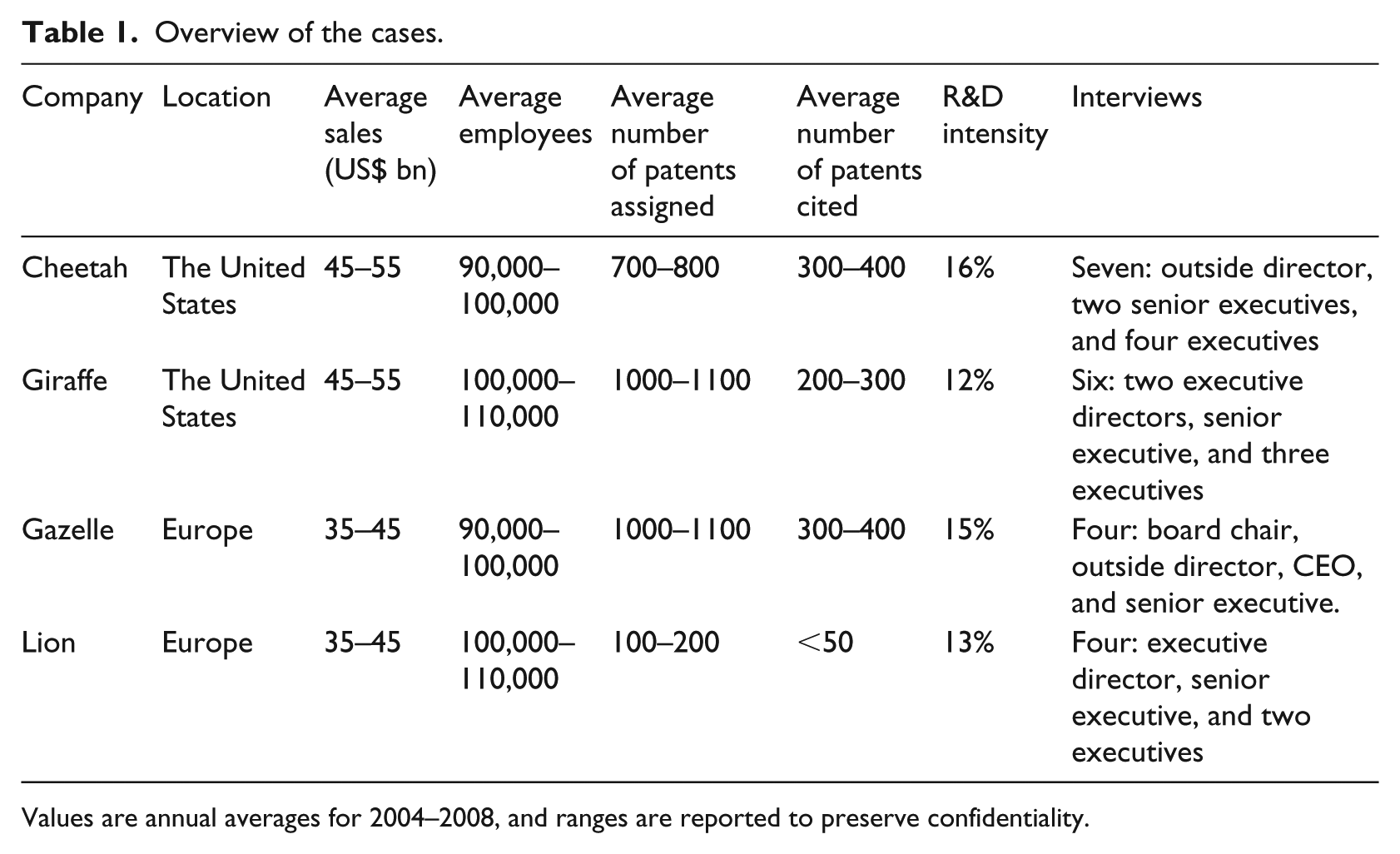

Following these criteria, we examined the four cases described in Table 1. The median of these cases’ innovation was 1028 assigned patents; the median value of their innovation was 293 cited patents. Their R&D intensity (the average annual R&D expenditure as a percentage of the firm’s revenue) (Hoskisson et al., 2002) ranged between 12% and 16%. Two of the firms are based in the United States and two in Europe, a geographic variety that should enhance the sample’s representativeness and the results’ generalizability (Graebner and Eisenhardt, 2004). All were founded more than a century ago. We assigned pseudonyms from the African savannah to the firms.

Overview of the cases.

Values are annual averages for 2004–2008, and ranges are reported to preserve confidentiality.

Data collection

We draw on qualitative data from our semi-structured interviews with directors and executives, as well as on quantitative data collected from company websites and annual reports, media accounts, industry publications, pharmaceutical industry databases, and the Marquis Who’s Who.

To test and refine our interview questions, we first contacted a European pharmaceutical company that was not part of our sample. We interviewed the board chairman and the CEO separately in 1 hour face-to-face meetings. We then reviewed our questions with the informants and modified them in light of their comments and suggestions. Utilizing the revised guide, we conducted 21 interviews with executives and directors at the four firms (see Table 1). Most firms initially referred us to one person—usually the board chairman, an outside director, or the CEO—as the most knowledgeable person given our topic. After completing the first interview, we asked our informants to identify other knowledgeable executives or directors and requested a personal referral to them to draw on the observations of diversely positioned individuals in each company (Marshall, 1996). We assessed the informants’ face validity by comparing their names to those in the board and management structures (Graebner and Eisenhardt, 2004).

At least two of the authors—and often all three—conducted the interviews. Our interview guide included a set of specific, but relatively open-ended, questions on director involvement, which we complemented with follow-up questions that emerged during the interviews (Eisenhardt, 1989c). Prior to each interview, we notified our informants of the topic and our study purpose by letter, email, or phone. The interviews with the directors started by soliciting background information on the company’s innovation process and the industry’s evolution. We clarified our focus on product innovation, and our informants explained that, in their industry, it was closely interwoven with technology. For instance, monoclonal antibodies, which are generated to treat cancer, cardiovascular disease, and multiple sclerosis, are considered both a product and a technology. Our discussions therefore evolved around the closely linked domains of technology and product innovation in health interventions. The informants also referred to different innovation stages, since drug development includes clinical trials that often proceed through different stages over a long time span (DeMets et al., 2010).

We then asked about the board’s involvement in and its activities regarding product innovation. We explored how directors gathered information on innovation activities in the firm, and how they specifically used their human capital to engage in innovation, by asking with whom and how they interacted within the firm. We also requested examples of board involvement and concluded each interview by asking the informants whether they would like to add anything that seemed relevant to our topic (Isabella, 1990). Our interview guide for the executives followed a similar structure, but was adapted to their specific role in innovation. For instance, we probed for detailed accounts of how they worked and communicated with directors. We took detailed notes during the interviews, and digitally recorded and transcribed them (Yin, 2003).

To motivate the informants to provide accurate data, we repeatedly assured them of information confidentiality (Graebner and Eisenhardt, 2004; Miller et al., 1997). We also interviewed multiple individuals in very influential positions and with in-depth knowledge of our research topic. These individuals are likely to have different perspectives and their recollections of their firm’s strategic and innovation issues were likely to be most reliable (Huber and Power, 1985; Seidler, 1974). Furthermore, we cross-checked the information received from the different individuals at the same firm (Miller et al., 1997).

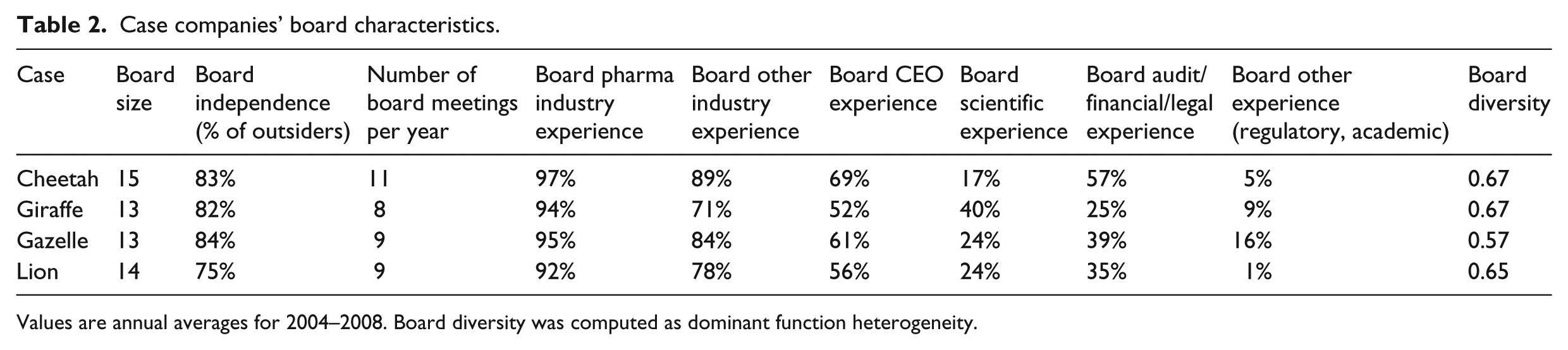

We also sought to understand each case’s specific context by complementing the interview data with secondary data on the board’s composition, displayed in Table 2. Since directors’ abilities to monitor and advise are shaped by their human capital (Hillman and Dalziel, 2003), we collected data on their experience. We indicate each experience category as a percentage, measured as the number of directors in a specific category divided by board size. The industry categories include professional experience in the pharmaceutical or another industry. CEO experience includes a current or prior CEO position and indicates general management and strategy experience; scientific experience is holding a professorship or PhD or MD in medicine, biomedical sciences, pharmacology, and related areas; audit, financial, and legal experience includes service as an accountant, chief financial officer, investment banker, or lawyer; and other experience includes regulatory experience (i.e. service with a major regulatory agency such as the US Food and Drug Administration or the European Medicines Agency) or academic leadership experience (e.g. as a dean of a major research-driven university).

Case companies’ board characteristics.

Values are annual averages for 2004–2008. Board diversity was computed as dominant function heterogeneity.

Based on these data, we computed board diversity as dominant function heterogeneity—an indicator of the extent to which directors differ in the functional areas in which they have the longest career experience (Bunderson and Sutcliffe, 2002). This was measured with Blau’s (1977) heterogeneity index,

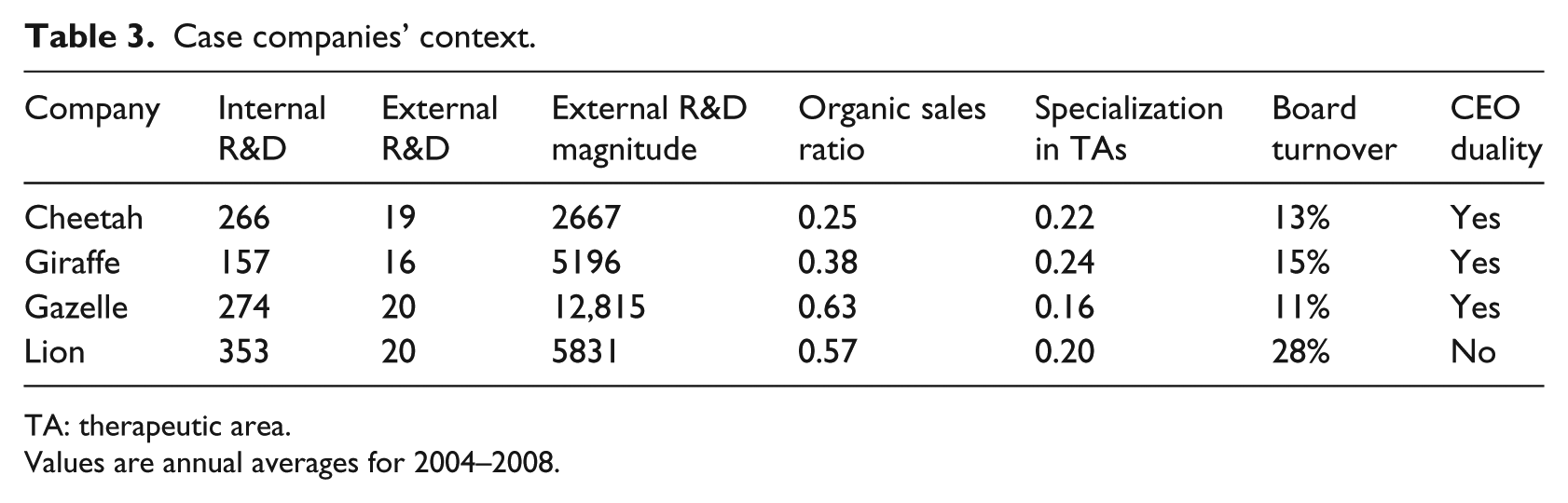

We also collected data on the firms’ contexts and additional board information (see Table 3). We measured internal R&D as the number of internal drug development events, and external R&D as the number of acquisitions, collaborations, and licensing events. For these external events, we also report the magnitude, measured as the sum of external R&D activities’ value (in US$ million). The table also shows data on the focus of the firms’ growth strategy (organic vs external, determined by the organic sales ratio, that is, the sales generated through the firm’s own R&D). Therapeutic area (TA) specialization is a firm’s specialization in therapeutic areas, such as cardiovascular conditions, oncology, or dermatology. We measured it via the Herfindahl index for TAs; a higher score suggests stronger specialization. Notable differences between the case companies were that Lion had more internal development activities, while Gazelle had larger R&D deals and a higher organic sales ratio.

Case companies’ context.

TA: therapeutic area.

Values are annual averages for 2004–2008.

We measured board turnover as the average number of entering and exiting directors in any given year divided by the board size (Tushman and Rosenkopf, 1996). We also collected data on CEO duality, when an individual serves as both CEO and board chair—an indicator of the CEO’s influence on boardroom discussions (Westphal, 1999). Lion had a higher board turnover than the other firms and no CEO duality. All four firms had scientific advisory boards for their scientific organization or the scientific senior executives.

Data analysis

All the authors read the interviews and formed independent views of the emerging themes in each case. We prepared individual case histories—of 40 to 60 pages—for each company to synthesize the data from the different sources (Eisenhardt, 1989b) and sought to triangulate the interview and secondary data in the case writing to create a reliable and consistent account of board involvement in innovation (Graebner and Eisenhardt, 2004; Jick, 1979).

We then used the case histories for within-case and cross-case analyses (Miles and Huberman, 1984). The within-case analysis focused on identifying the generative elements and relationships that constitute board involvement at a firm. The data collection and analysis followed an iterative process, during which we refined the interview questions to pursue the emerging themes in each case. We first used open coding to identify similar data instances for each first-order concept (Corbin and Strauss, 1990). To explore how boards engaged in innovation, we coded data instances indicating with whom directors engaged and how. This process resulted in several first-order concepts or data-based open codes (Corbin and Strauss, 1990). For instance, our informants often explained how directors engaged through “spontaneous interactions with employees.” We compared the data across all informants for each case to understand how the concepts related to similar issues or relationships (Anand et al., 2007) concerning board involvement.

In the next step, we aggregated several first-order concepts into theoretical second-order dimensions (Strauss and Corbin, 1990). For instance, the first-order concepts “interacting with employees at regular intervals” and “spontaneous interactions with employees” were aggregated into the second-order dimension “differentiated timing of knowledge exchanges.” We chose theoretical labels for the second-order dimensions that combined the first-order concepts (Anand et al., 2007). We then aggregated the dimensions into generative elements (e.g. differentiated involvement) (Strauss and Corbin, 1990). We labeled these elements by referring to the existing literature or by capturing themes at a higher level of abstraction (Anand et al., 2007).

We then started the cross-case analysis by looking for similar generative elements and relationships across multiple cases (Eisenhardt, 1989b; Miles and Huberman, 1984). We grouped the cases according to their potential variables of interest and compared case pairs to identify the similarities and differences between them (Graebner and Eisenhardt, 2004). We refined the emerging elements through replication, often revisiting the data and using tables, overviews, and charts to facilitate the comparisons (Miles and Huberman, 1984). The analysis process was iterative and lasted 5 months. For confidentiality reasons, we could not have an external independent rater code the data. Instead, two of the authors coded the data independently to assess intercoder reliability. There was very strong agreement between the coders, as indicated by a Cohen’s (1968) kappa of 0.92. Disagreements were resolved through discussion.

Generative elements of board involvement

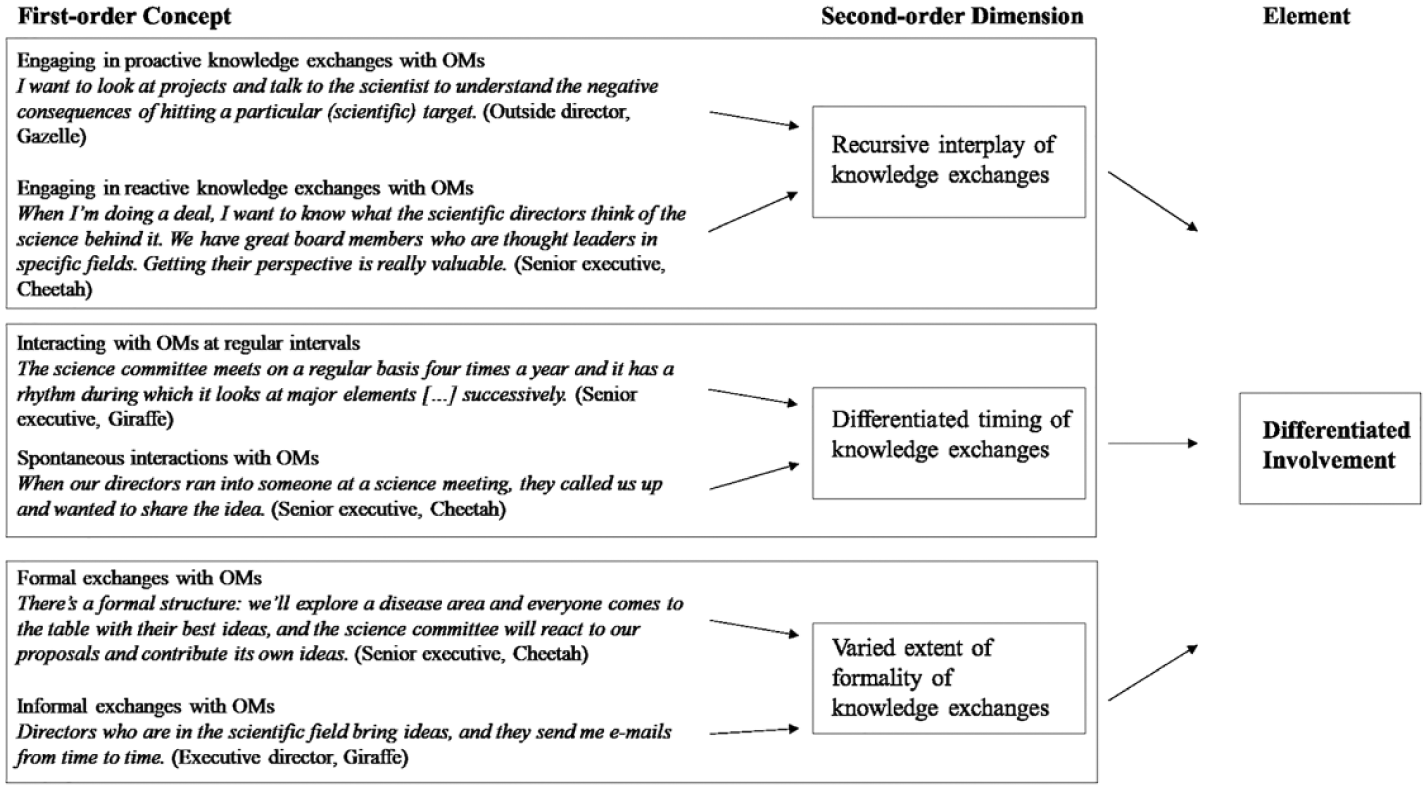

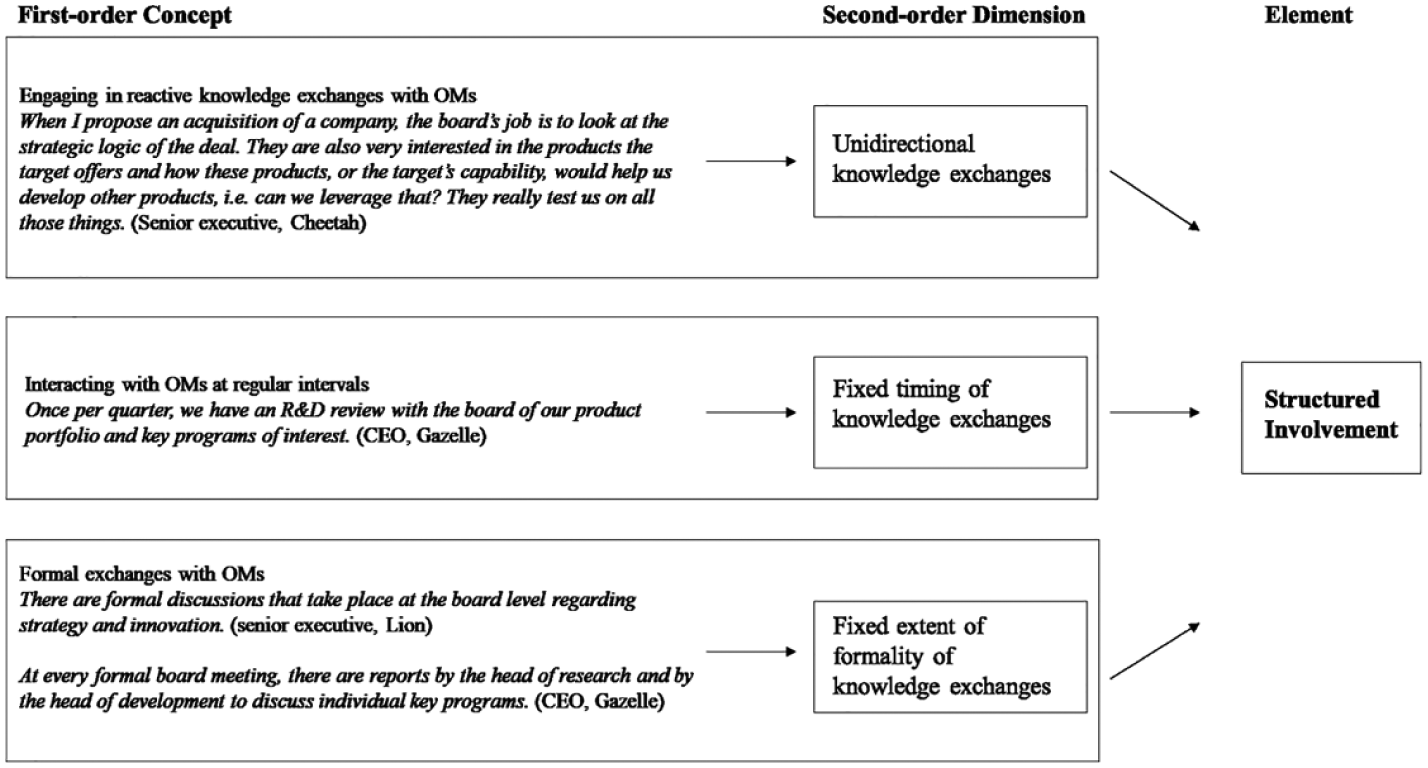

Our analysis revealed that two generative elements constitute board involvement in product innovation. First, scientific directors engage through differentiated involvement, characterized by knowledge exchanges that differed in their direction, timing, and formality. During such exchanges, directors shared their human capital with several OMs (executives and employees at the lower echelons), and the latter provided information on company-specific innovation activities. Second, the full board monitors and advises through structured involvement, characterized by unidirectional knowledge exchanges with a fixed timing and formality. Directors were involved in innovation from the early research stage (i.e. idea generation and testing) to the more advanced innovation stage (i.e. implementation). The generative elements, their second-order dimensions, and their first-order concepts appear in Figures 1 and 2.

Differentiated board involvement.

Structured board involvement.

Differentiated involvement

The first element that emerged from our data was differentiated involvement, which describes how selective directors—those with specialized scientific expertise—monitored and advised on innovation. Our informants highlighted scientific understanding as key for engaging in innovation. We refer to these individuals as scientific directors to emphasize their involvement in focused, scientific innovation issues. We found that differentiated involvement has three dimensions that vary in the direction of exchanges with OMs, their timing, and the exchange setting (see Figure 1). The first dimension concerns knowledge exchanges between scientific directors and OMs characterized by recursive interplay: The directors reacted to executives’ scientific proposals and interacted proactively with OMs at different organizational levels. Through such exchanges, the directors learned about the firm’s scientific innovation activities and monitored them, and they shared their expertise in advising on particular issues. The scientific directors were involved in such exchanges individually and as members of a board subgroup of scientific directors, such as a science committee or a loosely structured expert subgroup. An executive director at Giraffe noted, We have a number of scientists on our board that are very versed. As we either go into a new therapeutic area or bolster our therapeutic areas with actions, there are times when we’ll actually call on the science committee on the board. […] For instance, in the past, we entered a specific field. I called the science committee ahead of time and said, “I just want you to be aware that we’re looking at this,” and we solicited their opinion—if they had knowledge of the field, or if they knew people in a given area we should be talking to.

A Cheetah informant noted the importance of recursive exchanges: Outside directors’ site visits are important to ask very different questions and gain specific insights, since boardroom time is used for asking more general questions about innovation. For example, there are disease areas at the frontiers of science. Our lab scientists will tell us about their early understanding of causes and effects. We try to assess the likelihood that they will have a better sense of the cause-effect model in the near term. You wouldn’t get the same sense of the risk-reward tradeoff if you were only talking to the departmental level later.

The second dimension highlights the differentiated timing of scientific directors’ knowledge exchanges with OMs. Directors interacted with OMs during regular meetings, but also spontaneously. Thus, they could maintain a consistent interaction rhythm with the organization but could also remain adaptive to and raise ideas about emerging scientific issues. A Giraffe senior executive explained that, besides its regular meetings, members of the science committee who have an idea bring it forward in an ad hoc way. These directors encounter something, whether it’s through their reading, or attending a scientific meeting—remember these are professional scientists—or through interactions with a colleague, and they’ll call up or send emails and say, “I think this is really interesting, and can you follow up?”

The third dimension concerns the varied extent of formality of knowledge exchanges between scientific directors and OMs. Formal exchanges occurred through meetings with pre-set agendas and presentations about scientific activities, while informal exchanges occurred outside such meetings (e.g. phone calls or emails). A Cheetah senior executive described an informal exchange: The scientific directors […] call me and say, “I met with a company. Will you guys take a look and tell me what you think and call me back?” Then I call my team, do the development, and we meet with the company.

We found that scientific directors especially used such informal knowledge exchanges to share their expertise for advising.

As a Cheetah senior executive explained, One of the advantages our scientific directors offer is ideas outside the box. These can be ideas within a disease area in which we operate, but in a modality or mechanism that we don’t have and that they want us to consider. An example would be Alzheimer’s. Nobody actually knows what causes Alzheimer’s, so there are lots of theories, and the directors may meet a company with an interesting theory that we should consider. Or it could be something like a business we’re not in.

Structured involvement

We identified structured involvement as a second generative element of board involvement in our data. Specifically, the entire board, comprising directors with different human capital, was involved in broader strategic questions and innovation issues. Structured board involvement has three dimensions (see Figure 2). The first dimension pertains to unidirectional knowledge exchanges between the board and OMs. The board reacts to executives’ proposals for innovation and scientists’ presentations about progress made with scientific programs. A Giraffe executive director noted that, During our strategic plan discussions, or when we review our portfolio with the board, or even if we’re just going forward with a deal proposal, they’ll challenge us, asking questions such as “Do we need to acquire this company? Are there other ways we can go about this? What other options have you considered?”

The board also conducts site visits to varied parts of the company, such as research laboratories or other facilities, to learn about product innovation. In the words of a Cheetah outside director, “the board meets with scientists at research sites to inquire about and understand the challenges related to innovation programs.”

The second dimension describes fixed timing of knowledge exchanges between the board and OMs. The boards had set a regular rhythm of interacting with OMs through scheduled meetings, ranging between 8 and 11 per year (see Table 2). These meetings provided a board with regular updates on innovation, as required for its monitoring, and opportunities to share its expertise in advising activities. The boards also discussed the broader innovation strategy with senior executives at specific intervals. As noted by a Lion senior executive, “We have a major strategy session with the board every September. There we lay out to the board the strategy, including the innovation strategy.”

The final dimension describes boards’ interactions with OMs during formal meetings. A Cheetah outside director explained, “In formal board meetings, the time is used for asking broader strategic questions about our ongoing product innovation activities.” Yet, despite pre-set agendas for board meetings and the limited time available for discussing innovation, focusing on formal exchanges did not prevent the board from thoroughly monitoring executives’ innovation proposals. If questions about a proposal could not be answered during a meeting, executives were asked to conduct additional analyses and present again at the next meeting. A Giraffe executive director provided an example of such repeated iterations: We did a deal on a novel mechanism of action for a compound. We went to the board three times about this deal construct. […] Through the different meeting iterations with the board, the most important thing for them was, and the thing that got us to where we got to, dealing with the scientists and understanding the pluses and minuses. I think it was very clear where they were comfortable and where they weren’t, as we were putting the construct together, and they gave us feedback along the way, and we ended up doing the deal. Everyone felt that we were able to mitigate risks, had a potential opportunity that we wouldn’t have had otherwise. It was more than saying, “Okay, this is the deal. Can you approve it?”

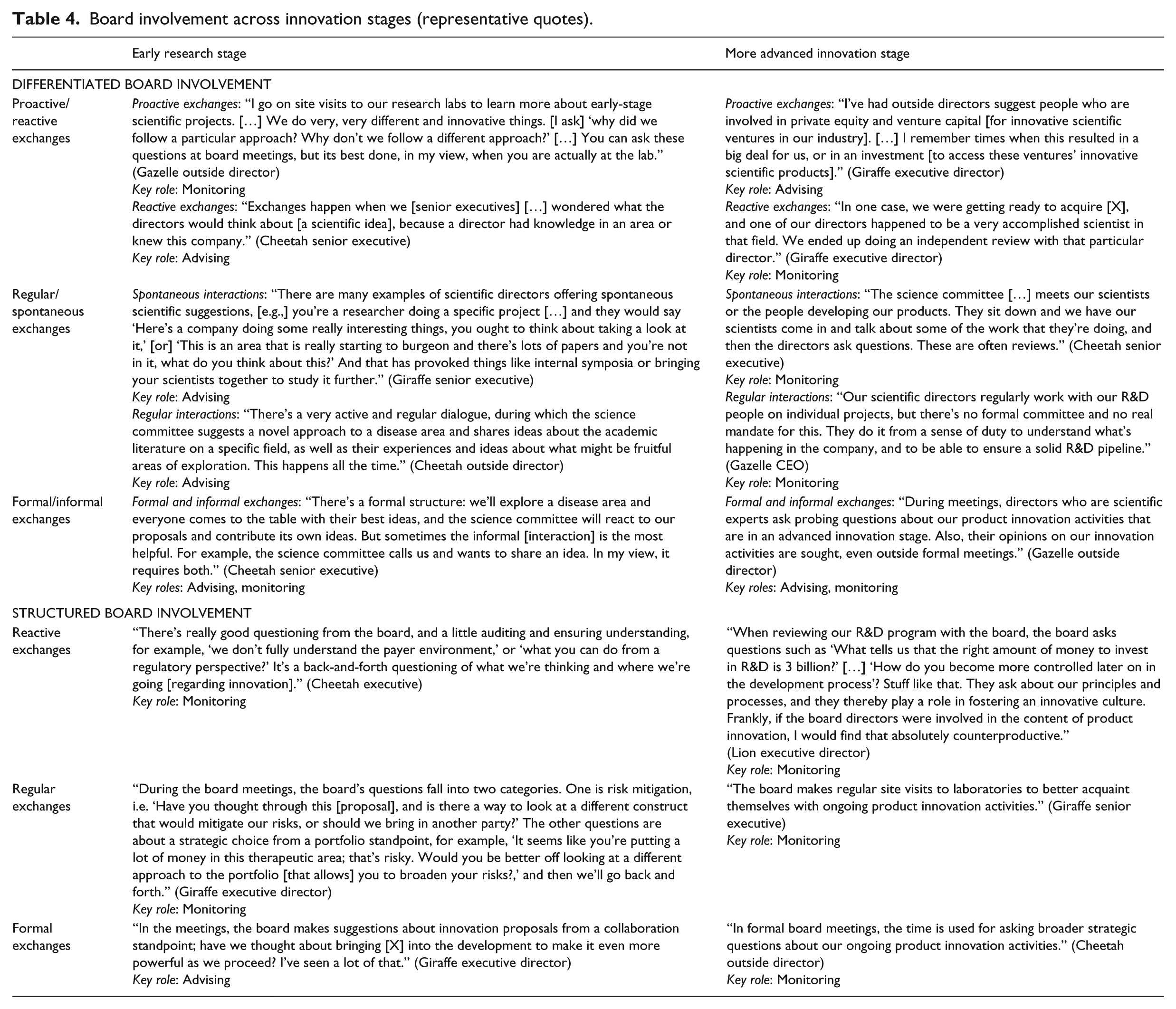

To illustrate how the board directors were involved across different stages of the innovation process, Table 4 in Appendix 1 presents additional quotes for differentiated board involvement in the early research stage and the more advanced innovation stage. The early research stage is characterized by generating and testing new scientific ideas, while the later stage is characterized by implementing innovation projects and broader programs. For each quote, we indicate the key role that a director or directors played in the interaction (i.e. monitoring or advising).

While there is evidence that board directors partly influenced innovation decisions and their implementation, we cannot claim a causal link between board involvement and firm innovation more generally. Innovation, as an outcome of scientific undertakings, often takes decades to be implemented and become measurable, particularly in pharmaceutical firms, and that is beyond the scope of our study. Thus, the scientific directors (at the more innovative firms) had a selective but, owing to their expertise, an important influence on the innovation process.

Scientific directors often challenged executives’ proposals for internal R&D and external innovation. A typical outcome of differentiated board involvement was that, based on directors’ inputs, the decision to acquire an innovative firm could be reassured or executives were asked to undertake additional analyses of a potential target and present the results to the board prior to a decision on it. Some firms even invested in an innovative company that the scientific directors had suggested or for which they had functioned as gatekeepers to connect executives with the targets. Company researchers refined internal scientific innovation ideas with the inputs of scientific directors and others whom the directors had recommended, and they started evaluating and studying new and promising scientific areas. Based on directors’ proposals, they also began to study a new theory or approach that might explain a new disease area. Without the directors’ inputs, such disease areas would have gone unnoticed at the time of the proposal. Director inputs also led to starting internal research symposia on an emerging scientific area. In the later innovation stage, the interactions between scientific directors and OMs resulted, for instance, in the modification or justification of the decision to acquire a company with late-stage innovation projects and ensured that it would bring sufficient value to the firm. The internal resource allocation to R&D programs was also modified if changes were required after detailed evaluations with scientific directors.

An outcome of structured board involvement in the early research stage was, for instance, that the board and the senior executive team started rethinking the strategic approach to external versus internal innovation, and such involvement helped ensure that strategic innovation decisions were made to mitigate risks. Examples of outcomes of structured board involvement in the later innovation stage included modification of the organization design for implementing the innovation strategy, and mitigation of the risks of acquiring a company with late-stage innovative products in its pipeline.

While our comparison of more and less innovative firms revealed that all four firms’ boards used structured involvement, we found differences in scientific directors’ involvement and resulting outcomes across the firms, as discussed in the following section.

Sequential board involvement

Our analysis revealed that the two generative elements of board involvement follow each other in a temporal sequence, with differences found between more and less innovative firms.

Unfolding board involvement

Despite their similar board compositions, more and less innovative firms differed in their board involvement paths. As shown in Table 2, the firms’ board sizes ranged from 13 to 15 directors, and on all the boards, at least 75% of the directors were outsiders. More than 90% of the directors had experience in the pharmaceutical industry, and at least 17% had scientific experience. The boards were also diverse in terms of functional experience.

Directors at the three more innovative firms applied their human capital sequentially for innovation, in which scientific directors engaged through differentiated involvement before the full board engaged through structured involvement. A Giraffe senior executive described this path: “[The science committee looks at] latent space for the corporation, or they want to understand the R&D behind this in-depth before the entire board has that discussion.” Scientific directors transferred their knowledge and the insights gained to the full board, making them an informed voice in the boardroom. The boards had even institutionalized a process that facilitated such knowledge transfers: At Cheetah and Giraffe, the science committee chair reported the committee’s evaluations and recommendations to the board. At Gazelle, directors with scientific expertise took this role.

The senior executives valued this sequential path, since they could test and discuss proposals with the scientific directors in greater depth, gain their insights, and identify potential challenges prior to presenting such ideas to the full board. A Giraffe executive director noted, If we are looking at a new approach to treat [a cancer type], the board will turn to the scientific experts and say, “How do you feel about this?” So, it’s advantageous and saves me a lot of time to meet with our science committee separately prior to bringing something to the board. I’ll bring my scientists, and we go back and forth on matters like, “Here’s the risk.” The committee can go into many more detailed questions, so when I later go to the board, it’s much easier from a flow perspective, because the scientists have been able to take it to a deeper level.

The non-scientific directors also valued the sequential path, since they could ask questions to their scientific colleagues during board meetings in order to better understand product innovation. Gazelle’s board chair explained, There are numerous examples of [scientific] directors communicating their points of view to the board, after having done a thorough examination [of scientific programs]. It’s almost as if the other board members look at this and say, “You’ve looked at this in-depth. What do you think?” And the opinions of the directors who took the time to examine the matter strongly influences the rest of the board.

Although our informants stressed the value of a diversified board to look at innovation from different perspectives, they also emphasized that the board could not monitor or advise on all the innovation details since this would require many directors with scientific expertise. For instance, a Gazelle senior executive emphasized, Our R&D head is involved in product innovation with thousands of employees worldwide, and the board cannot evaluate it at the same degree of granularity. However, it has to evaluate whether the research and innovation activities make sense, challenge and test proposals, and ensure that the innovation efforts comply with our strategic direction.

Thus, knowledge transfers from the scientific directors to the full board were even more important to enable the directors without scientific expertise to better understand the innovation portfolio and pipeline. A Gazelle outside director explained, There are a number of scientific experts on our board, all of whom are eminent scientists in their own right. They are there to give us more input on whether scientific approaches related to product innovation make sense and have the potential to succeed.

Our comparative analysis of the four cases revealed that the board of Lion, the less innovative firm, also engaged sequentially with scientific directors interacting with executives and scientists prior to the full board. However, both the scientific directors and the full board engaged via more structured involvement. Specifically, scientific directors engaged in unidirectional knowledge exchanges with fixed timing and formality. They monitored but were not approachable for executives to discuss innovative proposals and programs. Spontaneous and informal exchanges between scientific directors and OMs did not occur. Yet, the informants at the three more innovative firms particularly valued the spontaneity and informality of director–organizational exchanges. For instance, spontaneous interactions enabled scientific directors to engage during transition periods between board meetings rather than wait until the next meeting. Furthermore, the informants at the three innovative firms highlighted that formal interactions (on which Lion’s directors largely depended) were insufficient for comprehensive knowledge-sharing. Instead, “both formal and informal interactions” were important, as noted by a Cheetah senior executive. Informal interactions offered opportunities to discuss ideas with specific experts and conduct more in-depth probing and testing than in formal meetings.

Thus, in contrast to the other three boards, Lion’s directors’ scientific expertise was not highly leveraged, particularly for advising. This is surprising, since the innovative firms considered directors’ advising particularly valuable. According to a Cheetah senior executive, The science committee members helped us see things that might have escaped notice elsewhere in the business, because although we have all these people out there looking for innovation, we don’t find everything. For example, our scientists were made aware of a cancer therapy innovation very early on, but it was a potential breakthrough and they followed up with a series of very early investments. We’ve seen this therapy progress to the point where it’s becoming very interesting for us [to pursue].

Lion’s scientific directors did not advise, and they did not engage in deep probing of scientific issues. Due to the structured involvement of scientific directors and the full board, Lion’s board was less involved in innovation activities than the more innovative firms’ boards. Our data did not show any evidence that Lion’s board engaged, for instance, in a detailed risk assessment of innovation projects or offered suggestions for promising new scientific areas or potential acquisition targets, like we had observed at the other three boards.

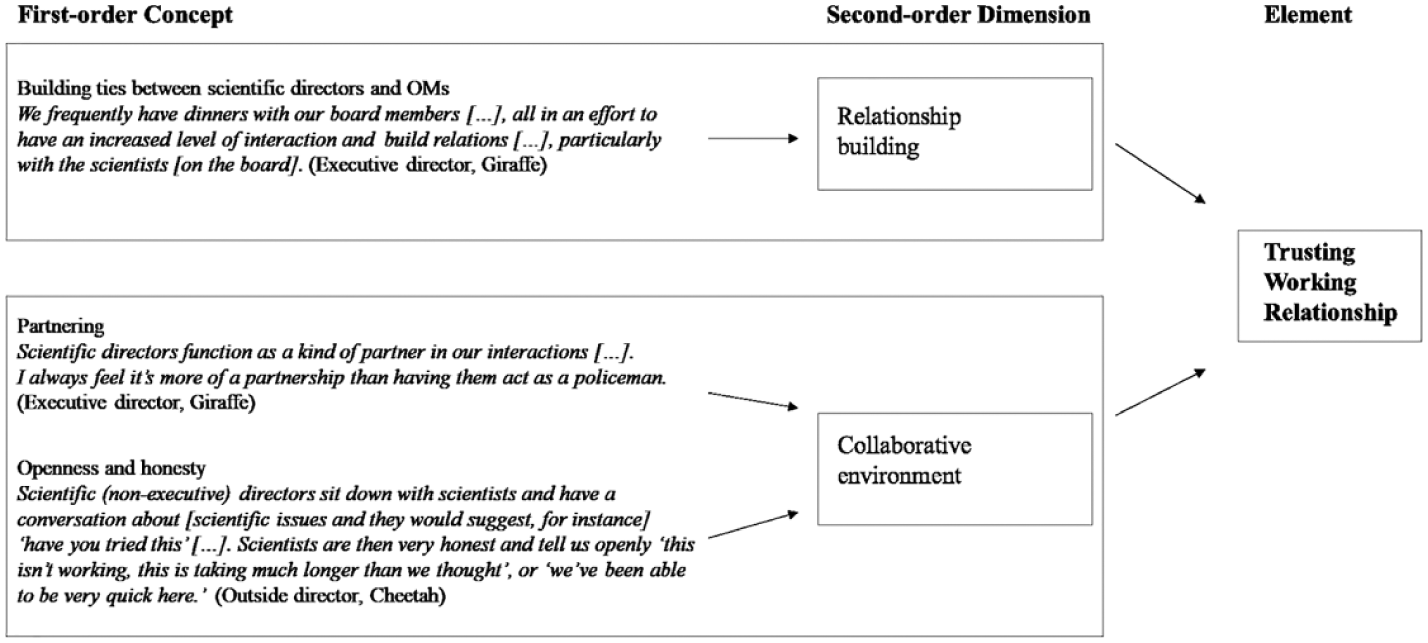

The influence of a trusting working relationship

Since scientific directors’ differentiated involvement resulted in deeper knowledge than structured involvement, it is important to understand what influenced it. Our data analysis revealed a trusting working relationship between scientific directors and OMs as a generative element that facilitated differentiated involvement. We found evidence of this element at the three more innovative firms, Cheetah, Giraffe, and Gazelle, but not at Lion. Figure 3 describes this element, along with the second-order dimensions and the first-order concepts.

Trusting working relationship.

The first dimension concerns the importance of relationship-building between scientific directors and OMs to share knowledge and information. A Cheetah senior executive stressed that “[It’s important to] interact and build relationships [with scientific directors], because then our senior scientists know they can call them if they have a question or an idea, and they know they can call on our senior scientists.” Such relationships were particularly important to facilitate knowledge exchanges “even outside the meetings,” as noted by our informants, since directors and OMs who knew one another engaged more in spontaneous and informal interactions.

The second dimension, a collaborative environment, emphasizes a complementary factor—the importance of the right context for knowledge exchanges. Our informants often referred to “partnerships” or “collaborations” between scientific directors and OMs when describing their knowledge exchanges. In the words of a Cheetah outside director, When (non-executive) scientific directors discuss with R&D people to talk through challenges and issues, it’s like you expect a scientific collaboration would look like, where people talk about ideas in a lab. It’s not like a “here’s a formal presentation of an idea.”

It may be easier to establish such a collaborative environment between scientific directors and organizational scientists, since they speak a common language. However, even the interactions between scientific directors and executives who lacked scientific expertise were described as collaborative. Furthermore, openness and honesty among scientific directors and OMs were identified as important elements. For instance, scientists were unafraid of talking about failures or challenges during their discussions with directors; they felt valued and respected by scientific directors, who sought their inputs on how to improve the scientific process and who also shared their knowledge of means to improve. From the board’s perspective, these open exchanges were important for the directors, as they opened many doors for learning about innovation and rendering advice on it. As Gazelle’s CEO noted, It’s a very open environment here. It’s kind of open book that directors have interests in different areas, some in R&D. Our [scientific directors] feel the need to get into the company and hear what’s going on […] to thoroughly understand what’s happening here. It makes them more effective.

Informants at all three innovative firms emphasized that directors’ openness to employee concerns and their partnering approach were an expression of the board’s commitment to product innovation as a foundation for the company’s growth.

Conversely, at Lion, there was no evidence of a trusting working relationship. An executive director noted, We struggled many times, for the board members who come from various backgrounds, to actually understand what the heck we’re doing. It’s difficult for them to make a judgment call as to whether what we’re doing is good or not, particularly given the fact that our innovation process effectively takes between 10 and 15 years before you actually reach the final outcome. A very, very long time.

Thus, Lion’s board did not “get into the details of things” of innovation programs and projects, according to its executive director. Instead, it relied on two scientific directors to obtain an “independent perspective” on the company’s innovation activities and on the information that the executive management provided. Interestingly, while board directors sometimes attended executive team meetings during which innovation was discussed, even the scientific directors stayed “out of intervening in the meetings,” looking only “at the dynamics of how decisions were made,” according to its executive director. Thus, they did not build ties with OMs, as the directors in the other three companies did.

Yet, Lion’s board directors exerted strong pressure to accelerate the company’s innovation. An executive director explained, Our board members think we’re pretty slow and ponderous. […] I think the board’s frustration […] is that we’re not growing fast enough. We have a lot of products that have come off patent in the past five years. We’ve had to absorb over [several] billion in sales. We’ve been able to make up quite a bit of that, but […] we’re [still] really struggling. So there’s pressure to speed up.

Paradoxically, despite the board’s frustration with Lion’s growth trajectory and weak innovativeness, its scientific directors did not engage via differentiated involvement, which could have enabled them to learn more about the challenges and problems in the company’s innovation programs and to share their knowledge about promising areas. Directors showed an almost naive reliance on executives concerning innovation, despite the firm’s poor innovation performance. For instance, an executive director reported, The directors have been extremely supportive of the proposals we make to them. They have almost never gotten into the various specifics, including for instance, when we suggested acquiring highly innovative biotech companies for $700 million. I would say, what the board decides and discusses is our appetite for financial aid.

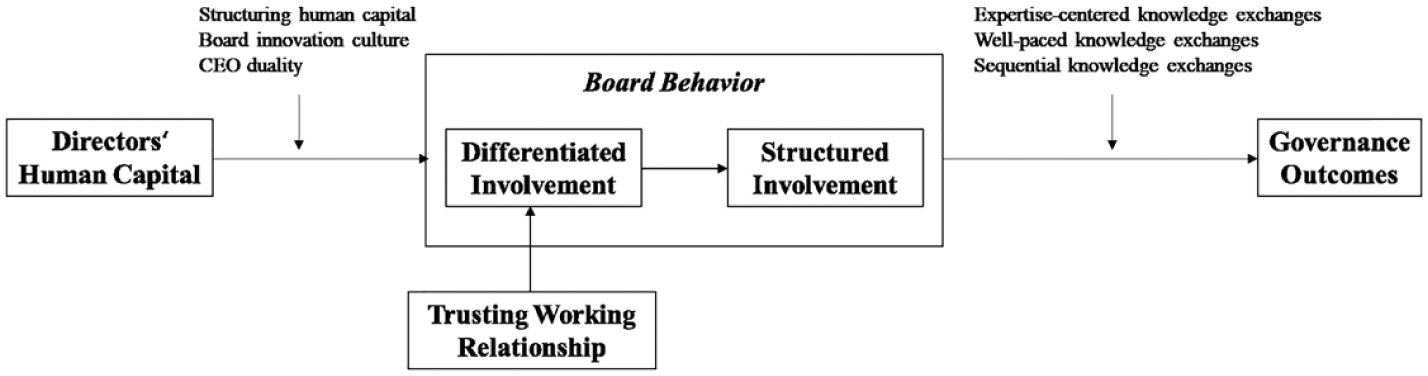

Why do boards of more and less innovative firms differ in their involvement and governance outcomes?

Our data analysis revealed that more and less innovative firms’ boards differed in their involvement as well as the resulting governance outcomes. Drawing on the interviews and the quantitative data, several factors appear to explain the differences in board involvement, summarized in Figure 4. The figure displays our emergent framework, which indicates that boards of innovative firms engage in sequential board behavior to leverage and apply their human capital to govern innovation.

Emergent framework on board governance of innovation.

First, while all of the boards’ directors spoke to OMs on varying levels, only the more innovative firms’ directors used these encounters for detailed advising on scientific pathways, proactively suggesting ideas, and engaging in substantive informal discussions. At Cheetah and Giraffe, the board’s science committee, a means to structure directors’ human capital, fostered directors’ scientific interactions with OMs. The science committees met quarterly and engaged executives and scientists in detailed assessments of their work from the early research stage to the regulatory review. It reviewed internal R&D activities as well as the products and scientific components of major acquisition and licensing deals, including targets’ innovative capabilities and their pipelines. A Giraffe senior executive reported that, owing to the high number of deals that the company did, the science committee evaluated proposals “beyond a certain threshold of investment” or if the proposals “may involve getting into a new area that could be controversial.” Depending on the complexity of the science and the risk profile of an innovation proposal, the committee vetted proposals in detail from a scientific standpoint before executives presented them to the entire board. Directors with scientific expertise also brought insights from their individual monitoring to the committee’s reviews. Furthermore, directors on the committee engaged in informal exchanges with OMs involved in or responsible for scientific activities. Hence, the committee enabled directors to reach out to the organization more informally and spontaneously to present their ideas, and the executives and scientists could approach directors to discuss their proposals.

Conversely, Gazelle did not have a formal science committee, but its scientific directors interacted with different OMs due to the strong innovation culture (Rousseau, 1990; Trice and Beyer, 1984) on the board. A Gazelle outside director explained that this board culture manifested itself through the board’s “willingness to experiment and learn, and to [be] open to failures” and its courage to “not sacrifice innovation to meet a particular quarterly earnings figure.” Board members shared the belief that innovation was central to the company’s long-term success, and its innovation culture made “everybody engaged and active in innovation.” Driven by this innovation culture, its scientific directors, including “worldwide leaders” in several areas, advised by proactively reaching out to the OMs to suggest opportunities for innovative directions.

While at first sight Lion, the least innovative company, had a board with a similarly loose scientific knowledge structure, it had a less established innovation culture. The board was characterized as largely a monitor, responsible for ensuring the right context for and sufficient resource allocation to innovation, but providing little direct guidance. Symptomatic of the difference, a Lion executive involved in scientific innovation reported that the company could use the outside directors’ expertise far more: I see the expertise level that directors have as a critical asset to be shared across the organization, especially regarding their exposure to the external world. It could be beneficial for the organization to have a better sense of their inputs and their experience.

Yet, an executive director responsible for innovation warned that “if the board of directors were involved in the content of product innovation, I would find that absolutely counterproductive.” The involvement of Lion’s directors was thus limited to asking strategic questions and overseeing major decisions. It could be that the turnover (Table 3) on Lion’s board (which was higher than the other firms’) made it more difficult to develop an innovation culture among its directors. Thus, even its scientific directors who had served on the board for several years did not engage in detailed advising. Overall, without a science committee or a strong innovation culture, Lion’s board made less use of its own expertise than the boards of the other firms did.

Second, the more innovative firms’ boards had CEO duality, while the less innovative firm separated the CEO and the board chair functions (Table 3). CEO duality is often considered an indicator of CEO power, which can limit the board’s ability to monitor the CEO (Finkelstein and D’Aveni, 1994; Jensen and Meckling, 1976). Conversely, in the context of innovation, CEO duality may facilitate the board’s involvement. A CEO-chair has deep knowledge of the company’s innovation activities, and can simultaneously prioritize innovation issues on the board’s agenda (Finkelstein and D’Aveni, 1994; Sundaramurthy et al., 1997). As a mediator between the board and the organization, this individual can influence interactions between the directors, executives, and scientists. For instance, when a Giraffe senior executive wanted to discuss a scientific proposal with the science committee prior to presenting it to the board, she contacted the CEO for approval. Similarly, a Cheetah executive mentioned, “If I speak to one of the non-executive scientific experts on the board, I always let my CEO know. He’s happy that I’m talking to them and that they’re calling me, and he encourages this interaction.”

Directors also contacted the CEO-chair when they wanted to meet with OMs about innovation activities, and such exchanges were actively supported by the CEO-chair of Cheetah, Giraffe, and Gazelle. For instance, Gazelle’s outside director mentioned that innovation is “often put at the top of the agenda by our chairman,” who “strongly encouraged” directors’ exchanges with the organization. Its CEO noted that “I formally encourage directors to interact with different people in the company. It makes them a more effective board.” Conversely, Lion’s chair restricted the full board’s focus to strategic issues, instead of supporting scientific directors’ advising.

Despite the suggested benefits of CEO duality for director involvement, a CEO-chair could also hinder such involvement if the directors disagreed with the CEO-chair on a fundamental innovation issue. The more innovative firms’ informants, however, indicated no opposition from the CEO-chair. The latter was aware of the benefits of drawing on the directors’ expertise for direct advising, and therefore supported their involvement.

Finally, as explained above, the trusting working relationship between scientific directors and OMs facilitated differentiated board involvement. Such a trusting working relationship was absent at Lion, whose board did not engage in differentiated involvement. By contrast, other factors differed little between the more and less innovative firms’ boards, including R&D intensity, board size, board composition, and number of board meetings.

Another important question is why differences in board involvement result in different governance outcomes of more and less innovative firms. Directors’ involvement at the more innovative firms resulted in more thorough risk assessments of the innovation activities and pipeline, improved decisions regarding internal and external innovation, and more director suggestions for promising scientific areas. Conversely, the less innovative firm’s directors remained more passive in their governance and engaged in less thorough monitoring and advising, resulting in fewer governance outcomes.

As shown in Figure 4, several factors explain the difference. One factor is the expertise-centered knowledge exchanges. Scientific directors, through their differentiated involvement, focused on scientific innovation during their exchanges with OMs, enabling them to critically assess scientific projects in their area of expertise, provide targeted and constructive feedback on current projects, and propose ideas for investing in new disease areas. The full board, in its structured involvement, focused on strategic aspects of the innovation pipeline, on which directors with diverse expertise could better contribute their views. This resulted, for instance, in a more thorough assessment of the strategic risks associated with different innovation areas. Conversely, such expertise-centered knowledge exchanges were missing at the less innovative firm’s board, resulting in fewer governance outcomes.

Another reason for the different governance outcomes is well-paced knowledge exchanges. Innovative firms’ scientific directors could react to specific scientific proposals when called upon, and could suggest promising innovation areas or targets in timely fashion to relevant OMs. More frequent interactions led to a better information exchange between the scientific directors and OMs. This resulted in recommendations and assessments from directors that proved valuable to the firm’s scientific activities. The full board performed a detailed strategic risk assessment of innovation opportunities and activities in regular discussions. Its consistent reviews resulted in improved strategic decisions. The lack of such well-paced knowledge exchanges at the less innovative firm, especially for scientific directors’ involvement, resulted in more passive governance and fewer outcomes.

A final factor pertains to sequential knowledge exchanges by the scientific directors, followed by the full board, as described above. This process freed up board time to focus on strategic aspects while relying on scientific directors’ detailed assessments and recommendations, resulting in improved governance outcomes for differentiated and structured board involvement.

Discussion

We began this article by identifying the need to better understand how boards apply their human capital in organizational exchanges to monitor and advise on product innovation. Our study showed that board involvement develops in a sequential order, revealed its underlying dimensions, and showed how and why the case companies’ boards differed across these dimensions. This provides a foundation for explaining the key theoretical dimensions of board involvement, which are essential for researching and understanding board behavior. Our findings contribute to corporate governance and innovation research in several ways.

A new perspective on board behavioral diversity

Research adopting a behavioral perspective on corporate governance (Westphal and Zajac, 2013) and qualitative research (Garg and Eisenhardt, 2017; Stiles, 2001) have made some strides in examining board behavior, providing important insights into the microsocial processes that underlie board–management relationships and the practices boards use to strategize. However, this research has examined general board behavior. To the best of our knowledge, our study is the first to introduce and provide in-depth insights into the concept of board behavioral diversity, that is, differences in director involvement across board levels and over time. Reconceptualizing board behavior in terms of behavioral diversity provides several insights for our understanding of board involvement.

A first insight is that board behavior is more diverse than previously assumed, comprising different types of board involvement. This specifically advances the behavioral theory of corporate governance (Westphal and Zajac, 2013) by showing that board involvement in innovation is a process during which different directors focus sequentially on different contents and interact with distinct OMs at varied levels. Our study helps pave the way for a new research stream on board behavioral diversity in the context of strategic actions, enhancing our understanding of corporate governance.

A second insight is that board behavioral diversity is an important mechanism for leveraging directors’ deep and diverse human capital for a long-term and complex strategic issue such as innovation. By studying either specialized director human capital (Kor and Sundaramurthy, 2009; McDonald et al., 2008) or aggregated and diverse board capital (Haynes and Hillman, 2010; Tuggle et al., 2010), corporate governance research has proxied board involvement; it has often implicitly assumed behavioral homogeneity, suggesting that directors engage similarly on a board (Baysinger et al., 1991; Miller and Triana, 2009). In contrast, by addressing both individual directors’ and boards’ diverse human capital, our study revealed that expert directors engage differently in innovation (i.e. deep scientific involvement) than the full board as a team (i.e. broader strategic involvement) and that such different engagements serve to leverage directors’ expertise.

A third insight is that behavioral diversity helps explain how expert directors function on a board composed of diverse experts. In diverse teams, each member processes new information in line with their own cognitive map (Huber, 1991), and they may face information overload (O’Reilly, 1980) if they need to process information outside their specific expertise. Discussing scientific topics in detail in the boardroom could prevent directors without scientific expertise from contributing to the discussion. Scientific directors’ deep scientific probing and advising outside of board meetings and their reporting to the full board before discussing higher lever strategic questions during such meetings ensure that directors’ expertise is integrated into board discussions. As shown in Figure 4, expertise-centered knowledge exchanges were an important reason for why directors’ scientific and the full board’s strategic involvement lead to enhanced governance outcomes.

A fourth insight is that board human capital is a necessary but insufficient condition for board involvement. Despite similar human capital configurations, board behavior differed across our four companies. Corporate governance research has traditionally studied the relationships between directors’ human capital and firm outcomes (McDonald et al., 2008; Sundaramurthy et al., 2013). In contrast, our study provided a more detailed elaboration of the mechanisms that enable directors to apply and leverage their human capital to govern innovation.

Unpacking the complexity of board involvement

Our study extends agency theory (Eisenhardt, 1989a) and the resource dependence perspective (Hillman and Dalziel, 2003) by showing how directors apply their human capital to monitor and advise, thereby opening the black box of complex board involvement. Specifically, we theorize about board involvement by conceptualizing its multilevel, structural, and temporal aspects, as well as the role of relational characteristics. This speaks to the corporate governance debate on the board’s involvement in strategy (Carpenter and Westphal, 2001; Johnson et al., 2012) by providing a more nuanced and comprehensive account of board involvement than previous research.

A first insight is that board behavior has a multilevel dimension: Director involvement differs across board levels, depending on whether specialized directors interact with OMs individually, as a subgroup, or as part of the full board. It is therefore important to examine director interactions with the organization from a multilevel perspective to better understand their behavioral diversity when they engage in strategy. While our focus was on director–organizational interactions for innovation, additional work is needed to examine how directors differ in applying their human capital to engage in other strategic issues.

A second insight is that director behavior differs across board levels in terms of the structural dimension of directors’ interactions with OMs (direction and formality of exchanges). A prevailing research assumption about board involvement is that directors govern reactively, with directors seeking information from managers (Fama and Jensen, 1983). In contrast, our findings show that specialized directors use both reactive and proactive exchanges with OMs. Such exchanges are beneficial for monitoring specialized topics, since they facilitate more comprehensive knowledge flows from directors to the organization and vice versa, enabling directors to become more informed and fulfill their monitoring role (Bosse and Phillips, 2016). The organization can better incorporate director expertise in strategic issues through such knowledge flows (Hillman and Dalziel, 2003).

Corporate governance research continues to focus on director involvement in formal board meetings (He and Huang, 2011), although qualitative studies have found that director involvement also occurs through informal exchanges (Roberts et al., 2005; Stiles, 2001). Less is known about when and why such exchanges are combined for board involvement. Our findings fill this void by, first, showing that expert directors engage in focused scientific innovation through both formal and informal interactions. Informal interactions are particularly vital for discussing issues candidly and without formal routines (Bouty, 2000), facilitating communication flow. Informal interactions between scientific directors and OMs in smaller teams also offer opportunities to deliberate ideas in depth among experts.

On the contrary, the full board engaged in formal knowledge exchanges. Owing to its larger size and greater diversity, formal exchanges provided all directors with rules for their meeting agendas. Larger teams can suffer from problems of coordination and reduced communication, resulting in decreased performance (Smith et al., 1994). Formality, however, can reduce these process losses, enabling all directors to contribute their expertise during systematic interactions with their colleagues in meetings.

A third insight is that director behavior differs across board levels in the temporal dimension of directors’ interactions with OMs. Prior corporate governance research has largely neglected time’s influence on board–company interactions for monitoring and advising. Scholars who focused on episodic board meetings (Forbes and Milliken, 1999; He and Huang, 2011) have implicitly assumed that boardroom exchanges occur regularly, but provided little insight into temporal variations in director exchanges. Our study revealed the temporal dimension of director–organizational interactions by showing that specialized directors combined regular meetings with spontaneous interactions to ensure continuous updating on and discussion of company activities, and to use windows of opportunity between board meetings to discuss emerging issues. They therefore remained responsive to the pace of innovation and emerging industry trends. By contrast, the full board engaged in regular exchanges. The potential advantages of board diversity may be reduced if directors do not interact with one another, and their regular exchanges in board meetings helped counter such limiting effects by ensuring consistent knowledge exchanges. Such well-paced knowledge exchanges were an important reason for why differentiated and structured board involvement led to enhanced governance outcomes (see Figure 4).

Another aspect of the temporal dimension is the sequential combination of different board involvement types and corresponding knowledge exchanges, resulting in enhanced governance outcomes (see Figure 4). While there is evidence that boards engage in their meetings as teams (e.g. Tuggle et al., 2010), and individual directors monitor company operations outside such meetings (Hendry and Kiel, 2004), it remains unknown how such activities are temporally synchronized. Addressing this issue, our findings show that directors’ differentiated and the board’s structured involvement were combined sequentially, which ensured synchronized knowledge transfers from specialized directors to the full board. Scientific directors shared their insights with fellow directors in a language the latter could understand. While our informants insisted on making “team decisions” on innovation, the other directors respected and valued the scientific directors’ expertise highly. Thus, expert directors are not only important for governing areas within their expertise (Khanna et al., 2014); they also need to communicate their insights and guidance to other directors. This introduces a new, dual view of expert directors not addressed in prior research—their within-company and within-board influences regarding monitoring and advising.