Abstract

This article repositions planners as central actors in multi-scalar capital flow governance, moving beyond planning’s traditional focus on local value capture intervention within the United States. By exploring multi-scalar regulators – from national to local actors – and intra-national dynamics that shape capital flows, the article highlights the limited spatiotemporal character of contemporary economic value capture instruments, drawing on a typology of these tax, fee, and land-based instruments. Ultimately, I call for planning scholars to reimagine planners as strategic urban governors responsible for safeguarding public interest goals and measures by coordinating multi-scalar regulatory responses to capital flows that assemble the built urban environment.

Introduction

This article positions planners as key urban governance actors who can shape property market investment outcomes by coordinating multi-scalar regulators. Many scholars trace the unrelenting financialization of cities globally (Aalbers, 2020; Jiang and Waley, 2022; Lin et al., 2019). Within these accounts, the city morphs into a space of economic value extraction (Robinson and Attuyer, 2021; Wu, 2020), commodification (Pierce and Hankins, 2019; Serin et al., 2020), and unyielding asset-price speculation (Kholodilin et al., 2018; Sajor, 2003; Sisson et al., 2019), generally fueled by or attributed to the actions of property industry actors. However, within their day-to-day roles, planners increasingly design regulatory instruments that aim to capture, redistribute, and even value within specific geographies, bolstering key goals, such as infrastructure development, affordable housing, sustainability, etc. Yet, while planners design instruments that bolster key goals, they are also frequently implicated in the extraction of rents (Henneberry et al., 2005; López-Morales et al., 2019; Öktem Ünsal, 2023), speculative development (Hjalager et al., 2022; Sisson et al., 2019), and inflated property prices (Cotteleer and Peerlings, 2011; Einstein, 2021) in cities across the globe.

Within this underlying paradox between curtailing economic value extraction and accommodating investment within the city, planning literature traditionally assumes that planners are equipped with economic value capture tools that help redistribute excess value from specific projects or within particular areas (Kresse et al., 2020; Muñoz Gielen et al., 2017; Sharma and Newman, 2020). Planning scholarship similarly details approaches to capture and redistribute different forms of value, from economic to social value within development and investment (Crook and Whitehead, 2019; Kim, 2020; van der Krabben and Needham, 2008). This article moves away from value capture and instead explores planners’ potential to govern capital flows. In doing so, it calls for a shift within planning scholarship that recharts the planner’s interventionist role of capturing value to a new strategic coordinator position that more actively governs multi-scalar regulatory responses that shape capital allocation and movement within urban development and investment. More specifically, this article calls for this refocus within American planning practice by mapping intra-national regulators and regulations, exploring the intra-national dynamics between planners and various other multi-scalar regulators that shape urban development and investment.

This article contributes to the interdisciplinary dialogue on value by focusing on economic value, conceptualized as monetary worth generated through investment into or financial interactions with the built environment within the context of urban property markets. If planners could better trace, monitor, and engage with property market capital flows (herein referred to as capital flows for conciseness), generally out of the scope of planning practice, they could focus less on capturing value and more on governing responses that shape how capital flows influence urban change. These capital flows denote specific movements, transactions, or allocations of financial resources by property market actors. By better understanding and monitoring capital flows and regulatory landscapes, planners can begin to focus on responses that acknowledge the multi-scalar capital and regulatory landscapes that transcend the traditional spatiotemporal limits of contemporary economic value capture instruments.

Within this context, the article surveys different forms of value capture instruments within contemporary planning practice, developing a typology of instrumentation – from tax-based to land-based economic value capture instruments. Within this survey, current value capture instruments stimulate public good by evening or redistributing excess value from real estate investment and development. However, these instruments generally have narrow spatiotemporal footprints, making them ineffective in responding to increasingly mobile capital that assembles urban change. In response to these limitations, the article widens its approach and maps the position of planning regulation vis-à-vis other regulators within the United States, such as the Federal Reserve or State Housing Departments, that influence capital flows that assemble urban change, enabling planners to better identify strategic intervention points and coordinate responses across regulatory scales if it threatens public interest.

This broader approach highlights how regulation influencing urban capital flows is multi-scalar and complex, with disparate regulators on different levels affecting urban change. However, within this complexity, planners remain central in permitting or prohibiting changes to the built environment within most contexts – and, in effect, help legitimize a vast chain of capital flows associated with urban changes. In doing so, I argue that planning scholars should increasingly work to reimagine planners as not just local interveners or actors who capture value from investment or development. Instead, scholars should acknowledge the planner’s centrality in urban change and recast planners as strategic coordinators within the broader governance of multi-scalar regulators that shape capital flows that assemble our cities today.

The article develops this argument by first surveying existing value capture instruments in American planning practice – creating a typology of land capture instruments to zoom into their spatiotemporal limitations in addressing increasingly mobile capital flows that assemble contemporary cities. Thereafter, I move to systematically map the multi-scalar regulatory landscape that influences urban change, highlighting how a wide range of regulators within the United States, from the Federal Reserve to local planning departments, shape how capital associates with the built environment. In return, I demonstrate how planners can leverage their position and shift their role from narrow interventionists to central actors coordinating regulatory responses to capital flows related to local public interest. Through this analysis, I call for planning scholarship to more systemically rethink the planner’s interventionalist role and revision the planner as a strategic governor – moving beyond traditional planning norms.

Charting the growth of real estate investment and development within cities

Property investment within major cities across the globe has grown at a quick pace following the global financial crisis. Following the dip in financial investment during the recessionary period, most cities experienced increased investment volume and transactions (Taşan-Kok, Özogul, et al., 2021a), with increased activity from property market actors and economic value creation that originated from new investment and development. Increased investment volume within cities demands granular, careful insight into the economic and financial dynamics at play within built environments – with more systematic attention to the role that investors, developers, financiers, and other property market actors play in shaping our cities (Raco et al., 2019; Wainwright, 2015). Coupled with the widening volume and number of investors within our cities, a wide range of literature on contemporary cities’ growing unaffordability and inaccessibility, driven by property market actors, rests within the rich field of financialization scholarship (Aalbers, 2020; Fernandez and Aalbers, 2020; Ward, 2019).

However, financialization scholarship is not only urban in its focus. Scholars explore financial institutions’ widening impact and role on political, economic, and social institutions or outcomes. From the financialization of universities (Engelen et al., 2014) to nature (Keucheyan, 2018), financial instruments, measures, and vernacular shape how different institutions or actors make decisions and respond to current global financial conditions. Nevertheless, while some describe processes of financialization as “profoundly spatial phenomenon[s]” (French et al., 2011), contemporary property market financialization literature sometimes loses its connection to the built environment – or, more specifically, the spaces, objects, and infrastructure developed or utilized by property market actors, generally encompassing real estate investments or developments. On a broader level, scholars have focused on entanglement of housing markets and financial markets (Aalbers, 2019; Fuller, 2021) to new accounts of the reaches of financial metrics and measures within global extremes (Fernandez and Aalbers, 2020; Pereira, 2017). Within these works, financial markets, instruments, and approaches demarcate how housing production and consumption morph into financial objects for consumers and producers – and trace important trends that help us understand housing production and consumption. Within this growing body of scholarship, the vehicles of financialization (August, 2020) – or, more specifically, the capital flows associated with these assets and processes – are not always tied directly back to the specific changes within the built environment.

However, capital flows associated with the financialization of housing (or any other property type) are intrinsically connected to the built environment. Capital flows are connected to global or local financial circuits and are the precursors to the development or changes in property tenure. In tracing capital flows, scholars can better unravel how financialization helps materialize contemporary built environments. For instance, Duval and Bahers (2023) explore how capital and material flow structure space and drive territorial development and expansion, focusing on the relationship between material and space, arguing that by analysing, mapping, and tracing these underlying capital flows, practitioners can gain a more comprehensive understanding of how urban and regional spaces are assembled.

By more carefully connecting materials or capital with space, scholars can create more balanced and textured accounts of financialization as Brett Christophers urges: “[s]o, while attending to the forces propelling financialization forward, it is imperative also to consider counterforces and the limits to financialization they impose. That way, it is possible that a more textured and balanced account of financialization and its natures may ultimately, haltingly, emerge?” (Christophers, 2015b).

A textured and balanced account of financialization not only acknowledges what David Harvey (1982) previously theorized as the financial treatment of land. But this textured and balanced account of financialization can also help us examine counterforces or the limits to financial currents by providing space to more systematically account for the shapes of capital and actors that assemble urban change. So, while contemporary financialization literature quickly elides the contemporary city with the financialized one, the processes, performances, and actors that shapes cities require more in-depth exploration and accounts.

By focusing on capital flows, planning scholars move beyond concepts of value or worth that sit difficultly and remain grounded in land and property, with a new focus on our ability to highlight specific movements, transactions, or financial allocations that relate to urban change, providing an entry-point toward the very transfers that help assemble the built environment – and shape property market actors’ interactions with space. In combination, scholars can build on the tools and approaches that unravel the specific performativity associated with property market actors’ interactions and actions in relationship with the built environment (Weber, 2016). In this framework, it is easy to critically reflect on contemporary planning instruments and how these instruments shape the built environment (Adams and Tiesdell, 2012). Moving beyond the black box of financialization (Christophers, 2015a) and towards the concept of capital flows allows us to more carefully account for how urban space is assembled, providing more detailed insights into the interactions between capital and actors that produce the built environment.

In this broader approach, it also quickly becomes clear that many regulators influence capital flows that assemble urban space. In response to these complex landscapes, multi-level governance approaches help account for a wide range of regulatory and property-market actors. Some introduce governance and multi-scalar techniques in depicting property market actors’ interactions with urban property markets beyond the local – for instance, by focusing on the role of national policy in the build-to-rent sector (Brill and Özogul, 2021). Others focus on the international character of regulation, highlighting how non-national policy and regulation can influence property market investment within specific contexts, such as London (Raco et al., 2020). Others explore how the financialization of contemporary cities is multi-scalar, attributing outcomes to different levels of public policy and private sector interactions with cities (Li et al., 2022; Zhang, 2020). These inquiries bring additional attention to the complex web of regulators and regulations that shape urban outcomes. But at the same time, these approaches point towards an urgent need to rethink the scale and scope of planning instruments.

Nevertheless, these depictions of regulation alone could risk de-emphasizing the role that verifiable (traceable and measurable) capital flows – in relation to multi-scalar regulation – play in shaping built urban environments. Underlying changes in regulation, it is essential to remember that property market actors and their interactions with spaces are fluid, with actors quickly responding to new regulatory demands or capital-market conditions (Taşan-Kok, Özogul, et al., 2021b). As such, comprehensive governance approaches require us to simultaneously unravel how both multi-level regulations and capital flows help assemble urban spaces. In short, within this multi-dimensional and multi-scalar focus, an urban governance approach refers to strategies by which planners, in collaboration and consultation with other regulators, can understand, shape, or coordinate responses to capital flows that assemble changes in the built urban environment. But how do we start?

The financialization of urban spaces is closely associated with the inaccessibility and unaffordability of contemporary cities. However, it is not financialization (itself) that makes cities more inaccessible or unaffordable. Rather, it is more aptly, say, the capital flows of international institutional investors and their rent extraction that point more directly at the widening unaffordability of housing stock within many cities. It is the rise in short-term rental landlords that also limits housing inventory for locals, placing additional upward pressure on purchase prices or rental amounts. I could continue. In short, these are each measurable through capital flow and actor analysis. If we can start from empirical accounts and measures of capital flows and regulations that assemble landscapes, we can then expand planners’ abilities to point toward specific flows and regulations that produce the outcomes that planners are tasked with responding to. Within this context, planners are understood as representatives of public interest – but to represent the public interest, planners need tools to understand the flows of capital and regulation that help configure urban spaces.

Ultimately, by approaching the city from measures of public interest (e.g., affordability or accessibility) in connection with capital flows and regulations, we can more carefully tie capital flows to urban-specific outcomes. Within measuring and determining public interest, the central role of coordinating multi-scalar regulatory responses that shape capital flows should not come at the expense of the planner’s local, place-based knowledge. Rather, contemporary planners and planning processes can help a wide range of regulators better understand – and, perhaps, respond to – public interest, gauge preferences, and support local goals. A growing number of scholars are increasingly connecting rental data with trends to displacement, home price outcomes, or access to nearby employment with careful attention toward local capital and regulatory landscapes (Barron et al., 2021; Brotman, 2021; Meltzer and Ghorbani, 2017; Raymond et al., 2021). At the same time, the presence of certain investment actors or capital flows can influence future outcomes. For instance, some focus on how predominate actors can shape future perceptions of risk and return within spaces, which, in return, influences future capital flows or the entry of particular investors to a market (Halbert and Rouanet, 2014). Building on this, the expectations of future value and liquidity shape the decisions and expectations of investors within specific geographies, texturing the character of urban change (Guironnet et al., 2016).

However, generally, property market actors, which comprise individuals and entities that participate in buying, selling, developing, or financing property investment, are implicated in cities becoming less affordable and accessible. However, while these actors are generally implicated as the actors responsible for cities becoming less aligned with the public interest, the actual capital flows and regulations that produce these urban outcomes should be more balanced and addressed within the financialized accounts of the city (Christophers, 2015a). We can move away from these black-boxed urban accounts by starting from public interest measures and tying these measures to the specific capital flows and regulations that assemble these same spaces.

Following, building on accounts of public interest, it is important to highlight capital flows and regulatory landscapes that produce these unwanted outcomes (e.g., less affordable or accessible housing) within the built environment. Capital flows are empirically verifiable with access to investment and development data. In contrast, the worth – or economic value – that originates from these same changes within the built environment is far trickier to pinpoint or measure within the context of property market actors’ interactions and associations with the city. By examining capital flows within spaces, we can measure these flows’ impact on space.

The task to local interest with multi-scalar capital and regulatory landscapes, requires scholars to first more carefully measure the presence and impact of regulation and capital flows within different empirical contexts. Along this goal, a growing body of scholarship explores how different development models are shaped by goal setting across geographies and scales (Robinson et al., 2021, 2022), but these depictions miss a systematic reflection on the limits to the instruments that planners have to shape these development outcomes. Simply, the spatiotemporal limits of contemporary economic value capture instruments – associated with contemporary urban planning interventions – stunt practitioners’ ability to intervene in capital and regulations that shape contemporary cities while limiting our ability to reimagine the planner as a strategic governor that helps coordinate how capital and regulation assembles contemporary cities.

The spatiotemporal limits of contemporary economic value capture interventions

Economic value capture instruments are a focus of contemporary planning scholarship. Economic value capture instruments – from specific value capture instruments, such as land value capture, to more general approaches to economic value capture, such as property taxation – represent most financially-driven contemporary urban property market instruments. These instruments are generally premised on concepts and understandings of social justice to redistribute public goods from excess value creation by private market actors associated with property investment, development, or ownership. This section introduces approaches to economic value capture by focusing on different types of economic value capture instruments currently found within planning – and then moves to raise the spatiotemporal limits of these contemporary instruments.

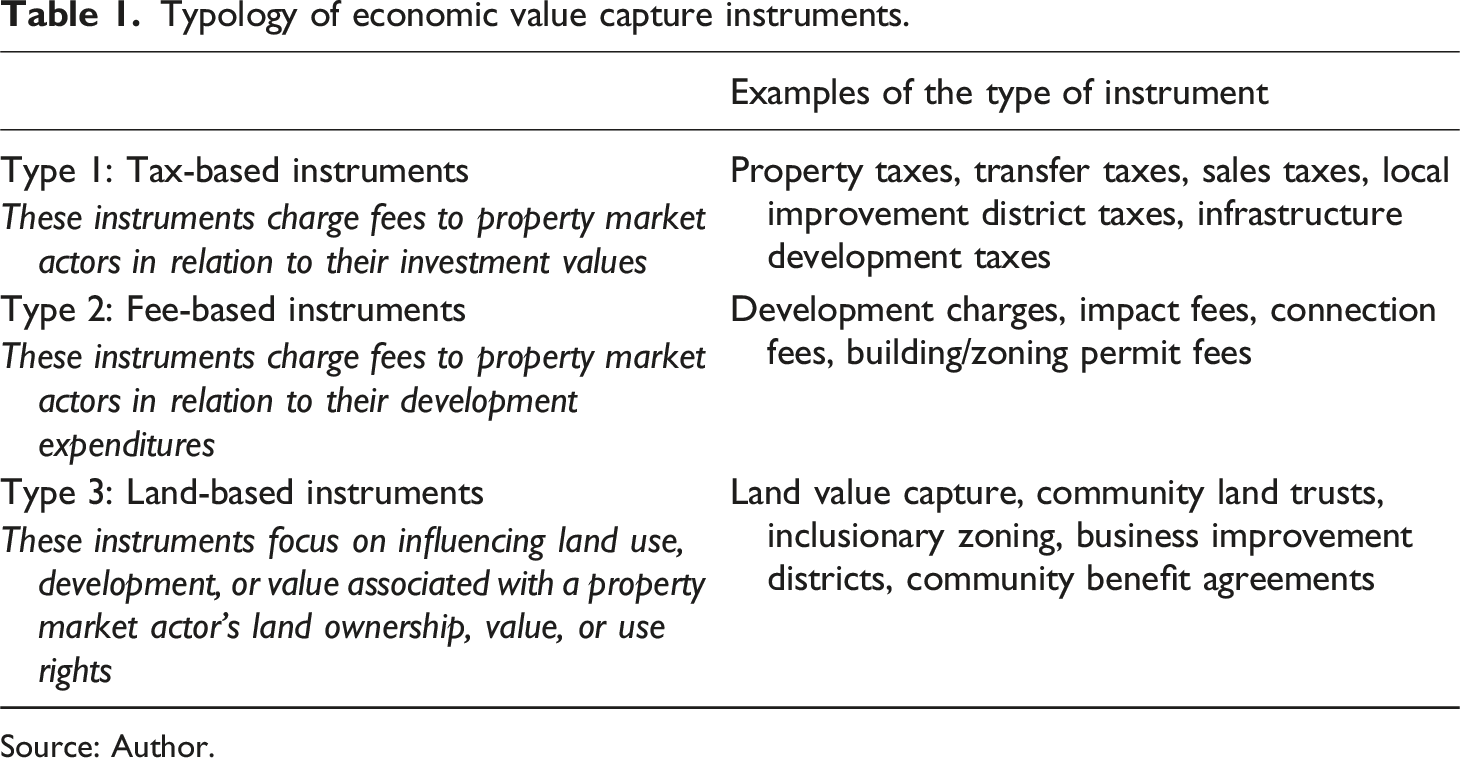

Typology of economic value capture instruments.

Source: Author.

Type 1 or tax-based instruments help urban planners and local-level public administrators capture value through various forms of taxation – from property to construction taxes. These instruments are generally designed to charge recurring or regular amounts to investors, developers, or property owners based on their investment values into a property – or the valuation of a specific property. Ultimately, like other instruments, tax-based instruments aim to even urban outcomes, levying charges on property market actors to further public goods, from public safety to education. Within these instruments, some work to measure the benefits derived and costs associated with property taxation (Berry, 2021). Here, the balance between tax-based instruments and the well-functioning of the property-market is delicate, with municipal-level officials – from planners to tax assessors who determine property values and collect property taxes – tasked with balancing public good with their private market burden. But within this category of instruments, charges are generally levied on property market actors on a recurring basis, whereas Type 2 instruments, fee-based instruments are levied at a single point in time, generally associated with development expenditures.

Fee-based instruments focus on the development of land. These instruments include charges from development charges to building or zoning permitting fees. By tying fees levied on property market actors, municipalities can generate revenue specifically tied to the impact of new development within specific areas. Within this context of single-source and point-in-time revenue, municipalities, and planners can better address the incremental, predictable demands of development, allowing the provisioning of additional public goods and services that new development traditionally demands. Some scholarship on fee-based instruments attempts to measure how fees relate to the cost of new developments, for instance, in relation to affordable housing development (Zhu et al., 2021). Like tax-based instruments, these fee-based instruments are generally based on some measure of value or cost associated with investment within the built environment. However, unlike tax-based instruments, fee-based instruments are generally single point-in-time charges to developers. Developers or investors are usually responsible for these fees at the project permitting or completion stage, whereas tax-based instruments are recurring levies based on specific values.

Type 3, land-based instruments, differ from the previous instruments in their focus on influencing land use, development, or value associated with a property market actor’s land ownership, value, or use rights. Type 3 instruments are more explicit in their focus on ownership, value, or use rights as opposed to the previous instruments. These instruments are generally led by municipal officials or planners, specifically, with a target to manage and mitigate the escalation of land values or landscapes of ownership and use rights within an area. Employing land-based instruments requires an in-depth understanding of property market dynamics, specifically focusing on land economics and the local real estate market. Scholars are increasingly working to examine the effectiveness of these different instruments – exploring how cities design land-based instruments and execute these within specific areas or projects or outcomes related to these instruments, focusing on displacement or retention of residents over different periods (Cahen et al., 2022).

While each type of instrument varies in its approach, each instrument redistributes economic value associated with urban development to further public goods. All instruments result in economic value generated from property investment or development being shared more equally across stakeholders within specific geographies – and contribute to the well-being of the wider community as opposed to a narrow handful of property market actors. However, each type of instrument focuses on different approaches to doing so. Type 1 instruments leverage taxation with broader impacts, affecting various property market stakeholders. Type 2 instruments are more targeted, addressing the specific impacts of a development project. Type 3 instruments focus on land values within specific geographies, targeted at specific public good aims – from bolstering housing affordability to combatting the displacement of residents.

Additionally, some of these instruments are planning-specific, while some of the instrumentation is not specific to urban planning. However, most of these instruments are administered on a local level. For instance, elected officials generally adopt property taxes, and assessors are tasked with collecting tax rolls. Nevertheless, planners and the development of planning policy generally interact with tax policy while also shaping fee structures within fee-based instruments, along with spearheading the development and implementation of land-based instruments.

Each type of these economic value capture instruments allows planners or other local officials to redistribute and disperse value from specific development or investment decisions within a geography for specific public interest goals. More importantly, these instruments are tied back to actual, geographically defined changes within the built environment within specific moments. As they are currently implemented within most urban contexts, economic value instruments are confined to specific, narrow spatial geographies. Spatial limits stunt these instruments’ effectiveness when intervening within capital flows. Simultaneously, each economic value capture instrument requires a specific geography to derive value – as opposed to capital flows that are secondary to actual transactions and investments, which can be less spatial in nature, as financialization scholars have highlighted in their descriptions of subsequent resecuritization of property that is currently difficult to trace back to specific spaces or projects (Goulding et al., 2023).

In addition, each type of instrument is constrained by its concentration towards specific moments in time. These instruments are neither temporally dynamic nor quickly respond to changes within the built environments. Even if these instruments change across time, say property tax rates increase, each generally adjusts to changes in value or worth instead of capital flows. So, while some land and tax-based instruments are somewhat dynamic, the instruments do not respond to capital flows that assemble changes with the built environment – but rather respond to increases in property worth or new popular mandates for updated instrumentation. This temporal unresponsiveness to capital flows makes it difficult for planners to quickly adjust to new market conditions or different capital stacks that help assemble property development and investment decision-making. Others have also hinted at the temporal limits of planning or housing policy, tracing path dependencies associated with changes in urban regulatory landscapes and urban change (Kurt Özman et al., 2023).

Investors and developers realize the limitations of current economic value capture instruments – and, at minimum, work to navigate these instruments or, at worse, leverage these benefits to reach better outcomes for their interests. Along this line, some point toward property market actors’ responsiveness to instruments or the ability to sway planners or other public officials to accommodate specific projects (Robin, 2018). Property market actors also have significant resources and robust knowledge networks that help them navigate and construct proformas that inform investment decision-making to respond to specific economic value capture instruments. Within this approach, contemporary economic value capture instruments could be seen as an ‘end of the pipeline’ intervention compared to the wider scope of regulators that influence capital flows within the built environment. 1 As such, the next section moves beyond the limited scope of instruments introduced in this section to explore the range of multi-scalar regulations that shape how capital flows assemble the built environment.

Delineating multi-scalar regulators that influence capital flows

This section widens our approach to analyzing urban property markets by focusing on the wider concepts of regulations and regulators within the United States, as opposed to instruments, building on the previous limits of these instruments. While the connection between the Federal Reserve’s rate-setting and zoning code might not be immediately clear, both regulations shape capital flows that help configure changes in the built environment.

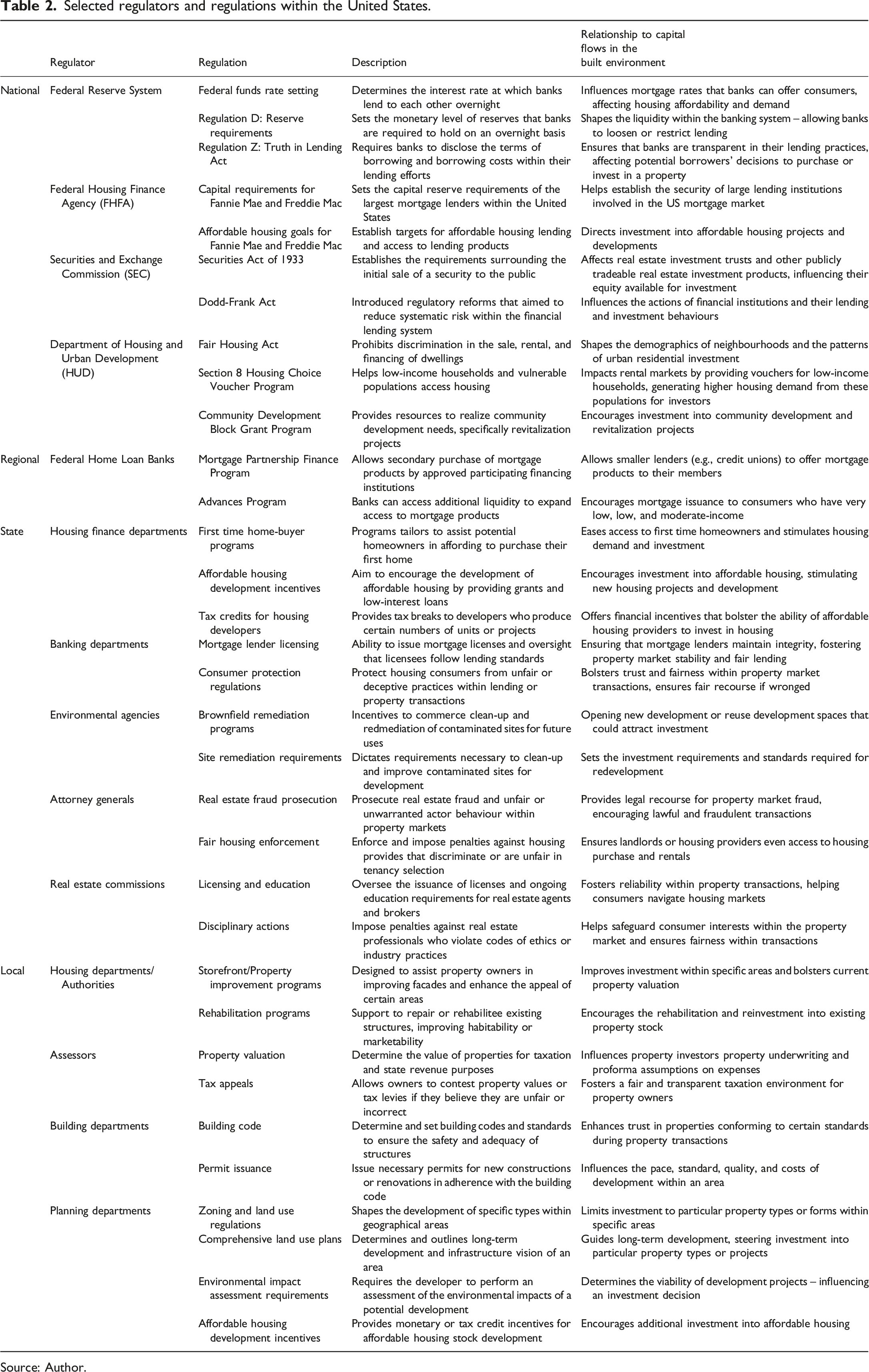

Selected regulators and regulations within the United States.

Source: Author.

The United States provides a distinctive case that differs from other contexts through its legal system, instruments available to planners – or regulators, in general – that shape how inter-relationships, responsibilities, and mandates between regulators developed over time. This section aims to provide a high-level starting point towards an attempt to map and examine relationships between regulators across scales within the United States with the hope of future research that will work to systematically explore and develop similar approaches within a wide range of alternative contexts and across a wider range of regulatory scales that interact with capital flows that assemble the built environment.

Table 2 connects each regulation to a regulator, typically an official body or authority responsible for overseeing, administering, or enforcing a specific regulation. Moving from the description of both the regulator and regulation, the Table then discusses a relationship that each regulation could have with capital flows within the built environment. In short, by introducing regulation in relation to factors that influence specific movements, transactions, or allocations of financial resources by property market actors, scholars can better understand how a regulation connects to the built environment. Here, regulations have multiple or wide impacts on capital flows within the built environment. However, the main aim of this Table is not to list every relationship that a specific regulation could have on capital flows within the built environment; however, the aim is to recount the multitude of regulators and regulations that can influence capital flows associated with the built environment.

Table 2 provides a high-level, selective overview of the regulations that influence property market capital flows. While these regulations might seem outside the traditional scope of an urban planner focus, introducing this wider typology that connects regulating organizations to regulations aims to move beyond the current spatiotemporal limits of contemporary planning-centric economic value capture instruments. There are a wide range of regulations and regulators shape capital flows and produce measurable impacts on built environments – that planners attempt to shape and stimulate with their contemporary economic value capture instruments.

At a national level, regulators influence financial landscapes and wider property market behaviours and capital flows that shape the built environment. For example, Regulation D: Reserve Requirements, along with the Federal Funds Rate, both influence lending behaviours, which impact mortgage availability for consumers purchasing homes or developers (or large-scale builders) that construct new homes. In this, national-level regulation influences local consumer behavior and the affordable housing or even business lending required for commercial construction projections. Other national regulators, such as the FHFA, also directly impact capital flows by providing lending oversight and mechanisms bolstering production and investment into specific housing types or projects. These regulations are tied to the decision-making of property market actors that result in the development of specific housing projects, level of construction activity, and end-state housing availability for residents. After that, these regulations also influence subsequent rent payments, and limits on rent amounts are due to deeded property owners, representing capital flows in themselves.

On state levels, Housing Finance Departments help bolster local housing production or constrain the supply of certain market-rate housing in favor of affordable housing development. Policies targeting first-time or low-income buyers influence developers’ interactions with space and future landlord and tenant relationships through affordable housing rules and regulations. Local regulators also influence capital flows with a diverse set of regulations that shape how property market actors interact, along with specific rules and procedures for investment or development, influencing project proformas, designs, and overall approaches to construction or investment underwriting. These local, state, regional, and national regulations all shape the outcomes within the built environment. And, within this fragmented landscape of regulations and capital flows scattered across different levels with a wide range of influences on capital flow, planners could position their roles as practitioners who coordinate and shape how regulators respond to capital flows that they witness within their cities.

Importantly, understanding how different regulatory scales intersect to assemble the built environment poses new methodological challenges that planning scholars have yet to explore. For instance, determining how Federal Reserve rate decisions interact with local zoning to affect affordable housing production requires both local and macroeconomic data indicators over wide periods of time. In addition, there is no framework to systematically inter-relate these wide arrays of metrics. However, the absence of a framework points towards the limited scope of our understanding of the regulations that drive urban change. We urgently need to develop new frames to systematically interrelate regulators and describe how various regulations, together, influence urban change. Within this, by tracing capital flows and connecting these same flows to changes and outcomes within the built environment, planners have space to help govern the regulatory responses from a wide range of regulators.

Acknowledging the centrality of planners in governing regulatory responses and capital flows

Planners sit in a central position in investment and development decision-making. However, within this central position, few planners track day-to-day property transactions, market churn, rents, etc. Planners also rarely map actor landscapes across their cities, analyzing the number of different investors or examining the relationships between developers and banks that have financed investment properties. Yet these payments, transactions, and actor arrangements configure urban property markets – and, more importantly, changes within the built environment that planners regulate.

Property transactions within today’s cities are not isolated events. Certain real estate transactions or investor interactions with space might make areas less affordable. Others might fuel the displacement of existing residents. At the same time, some investors might have short-term investment aims, looking to quickly increase rents, whereas others might be in for long-term cashflows with more stable rent increases, focused on impact investment aims (Anglin and Gao, 2011; Chernobai and Hossain, 2012). Each approach results in different tenant outcomes for residents, which can be represented in capital flows between tenants and landlords. Furthermore, lending conditions given by a financial institution (or lender) influence a developer’s proforma and risk assumptions, influencing whether a spatial change will take place (Özogul and Tasan-Kok, 2020).

These capital flows are not out of reach of contemporary planning departments. Planners can work to increasingly demand financial transparency, proformas, and financing agreements from property market actors or gain access to industry-specific datasets – from CoStar to the Multiple Listing Service to monitor property transactions, churn, rents, etc. Each property market actor-driven decision and capital flow can be traced with the right tools or dataset that enriches planners’ understanding of capital flows. At the same time, the complex regulatory landscape that influences that decision can be traced through systematic regulatory analysis and mapping. But these regulatory landscapes and capital flows behind the veil of planning scholarship – or outside the scope of today’s planning policy.

At the same time, planners might intuitively understand the different levels of multi-scalar regulators that can influence the decisions of property market actors; however, planning regulation is generally seen as disparate from other forms of regulation that could influence capital flows. For instance, it is not easy to find an article that connects planning zoning regulation with the Federal Reserve’s rate-setting regulation in the United States; nevertheless, both planning zoning and Fed Reserve rate-setting regulation influence capital flows that assemble built environments. For instance, Federal Reserve rate-setting impacts mortgage rates (Guirguis and Trieste, 2020); whereas zoning policy affects housing supply (Garriga et al., 2020), which each help configure the built urban environment through their effects on home purchases, construction, urban expansion, etc. However, within the complexity and distance between each regulator, it is important to clarify and delineate how planners can conceptualize their position in this broader landscape of diverse multi-scalar regulatory infrastructure.

Yet, within all this complexity, one pre-condition to many capital flows remains the same. That is, planners are often the actors that can allow or prohibit changes within the built environment. Yet even within this central position, planners are far too frequently associated with drafting zoning codes, performing application reviews, or developing transport infrastructure plans. While these traditional planning routines are important, planners could benefit from increasing the visibility afforded to the planner in determining changes within the built environment. Within these more central positions, planners have increasingly focused on championing environmental or social goals, focusing on how local planning regulation can foster and monitor more sustainable urban outcomes, focused on property investment behaviour and decisions (Esmailpour et al., 2021; Runhaar et al., 2009). In addition, planners are increasingly narrowing in on intervening within post-development or investment property tenure, implementing new regulation that prohibits non-owner occupancy of property or limiting rent increases, which respond to unwanted capital flows that are directly tied to widening unaffordability and inaccessibility of housing within particular cities (Raymond et al., 2016). However, these examples also point towards contemporary planning norms and planning practice’s narrow and interventionist character.

Perhaps, rather than focusing on intervening, future planners could also benefit from more actively coordinating and organizing wider regulations in partnership with regulators that could intervene within capital flows with stronger toolsets that are less attached to specific spaces or moments in time. Building on detailed accounts of the multi-scalar character of regulators in today’s increasingly financialized cities, local responses to capital flows act as mere band-aids to the wider frameworks that configure how capital flows hemorrhage built environments. While this article introduces this complex task, future planning scholars could benefit from focusing on (1) in-depth mapping of planner’s regulations vis-à-vis regulations of capital flows, (2) measurement of the impact of planning’s regulations in relation to others, and (3) advancement in planners’ tools to monitor capital flows. This repositioning of planning literature could better respond to previous calls to see planners as network managers – or even metagovernors (Sehested, 2009) of networks within urban spaces.

Some planning-centric scholarship examines the different types of non-local regulation and how it can influence sustainability outcomes within the context of new urban development (Holden, 2012; Yigitcanlar and Teriman, 2015). Others explore the technical dimensions or measurements of sustainable building, development, and transformation within cities across the globe (Retzlaff, 2009; Talen et al., 2013). More generally, public administration and legal scholars explore how regulation is multi-scalar, with many regulators generally responsible for similar objectives or aims (Aagaard, 2011; Robb et al., 2022). However, few planning scholars examine the relationship between local capital flow regulations in relation to provincial, regional, national, or international regulation – and how these regulations shape changes within the built environment.

Within the context of expanding planners’ understanding of the multi-scalar character regulations that impact capital flows, it is also important to understand the impact of different regulations on specific capital flows. Here, planning scholars are quick to measure the effectiveness of specific instruments, such as inclusionary zoning (Kontokosta, 2015; Mukhija et al., 2010). So, while planning literature continues to point towards the complexities of multi-scalar regulatory landscapes within a wide range of geographical contexts - from the Netherlands (Evers and Tennekes, 2016) and the United Kingdom (Goulding et al., 2023) to China (Ngo et al., 2017) and Brazil (Taşan-Kok, Atkinson, et al., 2021a), planners must work to connect regulation more closely with capital. Planning scholars can systemically work to measure the effectiveness of different regulations on capital flows related to changes within the built environment. But to bolster our ability to coordinate responses to these complex, multi-scalar regulatory landscapes that influence capital flows, we must also refine our toolkit to analyze and understand capital flows associated with the built environment.

For instance, by paying close attention to capital flows in connection to measures of public interest (e.g., access to housing), planners can also see varieties within investment capital stacks or actor typologies that help realize new projects or expand access to and the affordability of housing (Aigner, 2022). We could also aim to bolster our multi-level regulatory coordination to bolster accessibility or affordability if we also better understand how property market actors interact with wider geographies of the built environment (Taşan-Kok et al., 2023). At the same time, planners can work to chart regulatory landscapes and capital flows that produce desirable outcomes – focusing on the inter-relationships and path trajectories that are associated with outcomes within the built environment that are desirable within a specific context. With this knowledge, planners can better respond and move on to questions of conflict between regulatory actors and levels. Future planning practice could morph into a rhythm centered on leveraging local expertise and weighing the public interest against multi-scalar regulations that influence specific urban change – systematically examining to what extent particular regulators represent the public interest in shaping how capital flows associate with space.

So, while bolstering affordability or accessibility to housing stock might not be the goal of each planner today, planners’ local expertise and ability to effectively measure and gauge public interest can help them translate local interest against capital flows and multi-scalar regulators that shape urban change. While it is not an easy task, if future urban planners are increasingly equipped with knowledge centered around strategic governance approaches as opposed to economic value instruments, they could start to trace the landscapes of regulation and capital flows that materialize changes to the built environment – and compare these landscapes with the public interests that they aim to represent.

Conclusion

Most cities are becoming less accessible and affordable to households that wish to access them. Nevertheless, a wide range of contemporary economic value capture and redistributive instruments ought to equip planners with the tools to widen affordability and access within the geographies that planners are tasked with governing. But cities are less affordable and accessible. Empirically speaking, fewer households can afford and access today’s cities.

This article argues that if planners increasingly tracked, monitored, and assessed capital flows into cities, they could possibly help better govern regulatory responses that move beyond planning’s territorial and temporal traps and create meaningful governance responses to the wider capital flows that assemble with the built environments that planners are tasked with regulating. While this transformation requires new capabilities and relationships between planners and regulators, planners already have access to much of the necessary data, along with relationships with other local and regional actors to begin this endeavor. In this, planning, as an endeavor, becomes more explicitly tasked with monitoring, assessing, and, most importantly, governing capital flows that configure today’s cities. The challenges lie not in access to the tools or data to change outcomes – but rather in developing new frameworks that allow planning practitioners to connect these data points to measures of public interest. In return, planning becomes grounded in empirically verifiable capital flows where planners can coordinate multi-scalar regulatory responses to capital flows that assemble changes within the built environment.

Planning scholars should work to investigate good practices where planners play a more central role in strategically coordinating multi-level regulatory responses to urban-related capital flows. Such studies could provide insights into how integrated approaches to capital flow governance could be implemented within different contexts. Additionally, future research could more systematically lay out the groundwork of effective urban capital flow governance, exploring how planners can most effectively safeguard public interest within complex, multi-scalar regulatory landscapes, redefining strategies that help planners address their public mandates. Undoubtedly, this article posits that the future of planning is different from today. Planners could be increasingly tasked with measuring the impact of a wide range of regulators on specific capital flows within the spaces they are tasked with governing. At the same time, planners might need to increasingly focus on measuring the impact of how a wide range of regulator influence outcomes that they see within their city.

But within these tasks, the fundamentals of planning remain the same. Planners remain the actors that measure and represent local public interest. Planners persist as the actors that shape real estate investment decisions. But within these fundamental traditions, planning could begin to move beyond its territorial and temporal traps, with planners morphing into actors responsible for governing the wider set of capital flow regulations that help assemble today’s cities. This shift coincides with a call for action not only for planners – but also for planning scholars. There is an urgent need for a concerted effort to develop, systematize, and disseminate knowledge on how planners can more effectively engage in the governance of capital flows instead of narrow attempts to capture economic value.

In doing so, planners might just begin to see their ability to effect changes that bolster public interest. Planning might just move into a practice that can more instrumentally respond to today’s unaffordable and inaccessible cities rather than a practice that merely attempts to even, or even legitimize contemporary uneven economic value extraction from cities.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.