Abstract

This article reflectively applies measurement tools to gage whether a renowned financier and champion of shareholder capitalism, in 20th century business history, might be categorized as a corporate psychopath. The article examines aspects of the career of the outstanding financial investment manager, Bernie Madoff. Psychopaths and corporate psychopaths are defined as background to the article. Gauges of corporate psychopathy and psychopathy are outlined which could be modified by market research companies to identify corporate psychopathy in organisations as a way of aiding investment decisions into such organisations. The current article concludes that insolvencies such as those at Madoff’s investment company, have been distinguished by CEOs being present who were simultaneously the lauded agents of financial market capitalism and who embodied the traits of the corporate psychopath. The examination of potential corporate psychopaths using this historical methodology helps inform ideas about what the effects of psychopathic leadership may be within economies and gives new insights into the reasons for the greed, risk taking, and unethical practices found in financial markets. Findings support the accepted view that corporate psychopaths can be discovered in senior roles in the financial services sector. This current paper provides new avenues for research offerings from market research companies. For example, business to business researchers could undertake research to identify firms more likely to be longitudinally viable, sustainable and less likely to collapse (i.e., non-psychopathic firms). Investment companies like pension funds could use such research to identify firms that are less risky, more ethical, better led, and therefore safer to invest in.

Keywords

Introduction

Marketing and market research can be seen as the offshoots of classical economics which are dedicated to understanding the dynamics of markets. In classical economics a market is where buyers and sellers come together to exchange goods and services. The amount of supply and demand for those goods and services determines their value or price and this in turn determines how resources will be allocated. For example, in a financial market in a capitalist economy if the price of a financial good such as a currency or service such as a capital loan goes up then more resources may be allocated into supplying those goods or services. This, in theory, produces an efficient economy as resources are allocated, via the price mechanism, to where they are in most demand. However, when financial markets are manipulated or misrepresented by agentic leaders then market failure occurs, meaning that resources are misallocated and inefficiently distributed due to faulty price signals. In this case, information is misleading or incorrect leading to overpayment for the effected goods and services. Poverty can be a result of market failure because of resultant inequalities in wealth distribution. For example, in the last global financial crisis the price of financial derivatives was inflated due to (among other things) miscommunication as to the true value and risk associated with those derivatives (Boddy, 2011c). When the bubble burst and their true value was exposed, those left holding the derivatives were left out of pocket and those who held the underlying housing assets (homeowners) saw their housing capital diminished in value. Some of these homeowners were left with mortgage debt greater in value than their homes were worth and some of these lost their homes as banks took ownership in lieu of defaulted mortgage payments. While those bankers responsible were bailed out and rewarded, homelessness and poverty resulted for some ordinary consumers (Taibbi, 2010).

Market researchers tend not to question the philosophical or ethical underpinnings of the markets they conduct research into and usually assume that markets are well functioning, more-or-less rational and economically efficient. For example, after the last global financial crisis market researchers examined its effects on consumer sentiment (Lozza et al., 2016) rather than on the causes of the crisis. Nonetheless other market researchers have discussed the threat to the global economy that very large financial collapses represent, discussing WorldCom and Enron as examples of these collapses (Gosschalk & Hyde, 2005). Academic management researchers and financial insiders concluded that psychopathic individuals and systemic greed were prominent in the antecedents of the collapses of WorldCom and Enron (Boddy, 2015b) and played a part in the global financial crisis (Cohan, 2012b; Boddy, 2011c). Predictions are that the financial crisis will reoccur due to the personalities of the people involved and the perverse incentives inherent in the system (Blake, 2022; Boddy, 2011c). Indeed, some banks in the USA, Switzerland and Germany are now technically bankrupt as has been reported in recent financial news. This has the makings of another global financial crisis.

Despite these macro-economic events financial market research is commonly into the minutiae of consumers within the markets concerned rather than into the qualities of those markets. However, the nature of those markets effects consumers and investment firms in consequential ways and research into the nature and leadership of these markets is therefore of high importance to consumers and investment firms and could be influential in their decision making. For example, if a financial institution was known to be headed by leaders high in psychopathy, then consumers and organisations such as pension funds may choose not to invest in, buy from or engage with those financial institutions because they would be better informed about the risks of doing so. As speculated by financial insiders (Cohan, 2012a) Wall Street does have higher levels of psychopathy than other industry sectors (Howe et al., 2014) and corporate banking is often systemically corrupt (West, 2018), dishonest, reckless and greedy (Cohn et al., 2014; Lui, 2015). The identification of financial firms particularly low in psychopathic leadership could arguably save consumers and firms like pension funds from reduced wealth or increased poverty as their investments and purchases would be more stable and less likely to suffer from economic collapse. If market research companies do not offer these research services then other groups such as management consultants may do so and market research will lose out on this business as it has in other areas (Cowley, 2000). Market researchers have recognised the existence of psychopaths in business (Mouncey, 2011) but not yet engaged with researching them.

Financial market research has tended to focus on practical issues such as the material benefits of establishing relationships in B2B financial sectors e.g., (Theron & Terblanche, 2010). An uncritical perspective is usually taken with the premise being that financial capitalism is beneficial to the actors involved. However, financial markets have been implicated in scandal and crisis since the last global financial crisis in 2007/2008 (Taibbi, 2010; Boddy, 2011c) and continuing into recent times (West, 2018) and these crises affect consumer sentiment and behaviour (Lozza et al., 2016). Thus, a more critical examination of the finance sector is arguably warranted. While greed, excessive risk taking and ruthlessness have been identified as antecedents of financial crisis, the underlying personality trait of psychopathy has also been identified as existing at heightened levels in the finance sector (Howe et al., 2014). This current paper uses a structured, historical examination of the ex-head of one of the world’s leading stock markets, Nasdaq, for evidence of psychopathic traits.

While the reasons for business success may include structural and environmental factors (Boddy, 2001) and the pragmatism of the businesspeople involved (Boddy & Croft, 2006), personality also plays a part. The existence of a virtuous personality is key within research into commercial ethics (Alzola, 2012) with an amount of moral maturity being thought of as significant in terms of the development of an ethical approach (Cavanagh, 2010). In particular, leader’s personalities are exceptionally important due to the tremendously significant character of organizational leadership vis-a-vis its influences on effective organizational functioning and with respect to the wellbeing of employees (Hogan et al., 1994; Hogan & Kaiser, 2005).

Dark, dysfunctional or toxic leadership can be particularly caustic (Hogan & Hogan, 2001). In marketing, toxic leadership like this can disrupt the effective functioning of a marketing department (Boddy & Croft, 2016) and cause emotional distress to employees (Boulter & Boddy, 2020). Furthermore, as Nicholson regretfully notes in his book on leadership (p. 266), in modern organizations, by the time the upper hierarchy of senior management is reached, many of the candidates with integrity have long since been weeded out. The choice of top leaders is then restricted to those without integrity (Nicholson, 2013). Corresponding with this viewpoint, some psychopathic personality traits in leaders have been linked with immoral behaviour and unethical values (Boddy, 2011a). Additionally, Shank finds that higher psychopathy levels are related to the deception of others for financial gain (Shank, 2018).

The morality of current and past champions of capitalism, like Bernard Madoff, is also important because market capitalism is under intense criticism. For example, Wolf, a chief economics writer for the Financial Times, argues that capitalism has become dysfunctional (Wolf, 2009). Leading figures in 20th century capitalism such as Robert Maxwell, Albert Dunlap and Ken Lay have also come under scrutiny (Boddy, 2016). Robert Maxwell ran the Mirror group of newspapers in the UK and his companies owned the market research firms Audits of Great Britain (AGB) and the Far-East firm the Survey Research group (SRG). Maxwell’s group of companies went bankrupt after he was found to have stolen GBP 400m from the pension funds of the companies he ran (Hill-Tout, 2004; Boddy, 2016).

Bernie Madoff, a prominent figure and former idol in Wall Street, and champion of shareholder capitalism, has been described as having a narcissistic, sociopathic personality and as being psychopathic. According to leading writers on leadership, Madoff along with Maxwell and Lay are leaders who went beyond the law and are among the “major villains” of business history (Nicholson, 2013). However, although many nominate him as a probable psychopath, a leading ‘dark triad’ researcher, Paulhus, reportedly nominates Madoff as a Machiavellian and not a psychopath (Konnikova, 2017).

A Machiavellian is someone in politics or business who manipulates others for their own advantage. Like psychopathy, Machiavellianism exists on a continuum (Mouncey, 2011) and some traits exist across the adult population. The dark triad is the trio of personalities called narcissists, Machiavellians and psychopaths (Paulhus & Williams, 2002). However, two of these, Machiavellians and psychopaths, have such an extensive personality overlap that some researchers see them as essentially the same personality who has been named differently by researchers coming from different academic disciplines (McHoskey et al., 1998). Why Madoff would be classified as not being psychopathic is not elucidated in Konnikova’s report of his Machiavellianism. Therefore, to analyse this more thoroughly, in this current paper a structured and systematic examination of Madoff’s behaviour against the most highly proto-typical characteristics of psychopathy is made.

Bernard Madoff, in one of the greatest examples of financial fraud in business history, appropriated billions of US dollars from individuals, not-for-profit organizations and businesses investment and retirement funds (Glodstein et al., 2010). His investment company was basically a Ponzi scheme which is where funds from new investors are used to provide apparent returns to existing investors. The scheme depends on increasingly large amounts of funds becoming available. Funds originating from 40 countries were involved in this fraud (Jackall, 2010) demonstrating its global impact. While several investigators and psychopathy researchers have characterised Madoff as a likely psychopath no structured analysis of his character has been carried out (to this author’s knowledge) and this current paper is the first to analyse Madoff’s behaviour against that which would be anticipated from corporate psychopaths. Using two gauges of psychopathy (described below), on one (the PM-MRV2) Madoff displays all (100%) of the characteristics of a corporate psychopath while on the other (the CAPP) he scores about 90% which is well within the psychopathic range.

Portrayed as charismatic and as a persuasive financier who mingled comfortably amid power brokers in Washington and on Wall Street, Madoff owned all the trappings of a grandiose lifestyle including a penthouse in Manhattan, shares in private jets, a house in France and a yacht anchored off the French Riviera (Creswell & Thomas, 2009). Such grandiosity is a characteristic of psychopaths. In terms of self-importance Madoff long enjoyed his role as a senior figure on Wall Street, permitting him to sit on notable organizational commissions and boards in which his opinions aided in moulding financial regulations. There was, however, reported to be another side to Madoff who was also said to be carefully attuned to managing his image, down to the tiniest detail. For example, as per his instructions, the design within his firm’s New York and London offices was stark. It’s colour scheme was black, white and grey — or “icily cold modern,” as reported by one recurrent visitor to those offices (Creswell & Thomas, 2009). He also dressed to impress and carefully matched his wedding rings with whatever vintage gold or platinum watch he wore on any particular day (Creswell & Thomas, 2009).

Corporate psychopaths are defined as sub-clinical psychopaths who operate selfishly in the commercial world with a callous, ruthless and unemotional indifference to how their actions detrimentally impact their colleagues and other stakeholders. The ways in which corporate psychopaths destabilize organizations from within has already been well delineated. For example, in line with previous research showing that employee involvement is a crucial element in predicting greater job satisfaction the presence of corporate psychopath correlates with lower employee involvement and job satisfaction (Boddy et al., 2015a; Boddy & Taplin, 2016). They undermine employee voice and union influence through their divide and conquer tactics (Boddy et al., 2015a) adopting an uncollaborative approach (Heery et al., 2012) to trade union relationships. This insight is important because sociologists have started to argue that a structuralist view of society cannot single-handedly account for the greed and risk taking which are pervasive in recent capitalism, as demonstrated by the global financial crisis and other examples of unethical financial behaviour.

It has also been reported that in this time of “casino capitalism” (Strange, 1997; Sinn, 2010), where managers and workers are experiencing increasingly extreme pressures at work (McCann et al., 2008; Chesley, 2014) including bullying behaviour linked to work overload (Boyle et al., 2013); researching the part played by corporate psychopaths can provide beneficially insightful understandings of the modern corporation (Boddy, 2015a).

Further, it has been suggested that the characteristics of corporate psychopaths as being financially oriented, ultra-rational managers, embodying negligible emotional apprehension of or empathy for their colleagues (Boddy, 2018b), denotes them as valuable to the ‘profit first’ type of capitalism promoted by many senior managers (Friedman, 1970). Studying such leaders is important because writers on destructive and toxic leadership have stated that insufficient is grasped concerning the essence and dimensional features of the behaviour of destructive leaders (Thoroughgood et al., 2012).

This present article helps to understand this behaviour in relation to Bernie Madoff. The benefits of this historical method of studying organizational events are well accepted (Clark & Rowlinson, 2004; Busha & Harter, 1980) and this type of procedural approach concerning the analysis of those who have governed organizations may impart crucial incremental comprehension. The triple aims of this article are firstly to describe and use an empirically grounded investigative method for examining a potential corporate psychopath within the history of capitalism. This is consistent with the goals of business historians who seek to participate in empirical, considered, investigations of corporations so as to enhance our understanding of their development and characteristics (Tucker, 1972).

Secondly the objective of this research is to explore the behavioural qualities of one corporate executive in contemporary business history. The many benefits of being aware of history are acknowledged by market researchers (Crawford, 2022) and this current paper examines an aspect of financial market history. If corporate breakdowns and scandals may apparently be distinguished by the presence of high-ranking directors who could well have been psychopathic, then this strengthens arguments that psychopaths ought to be screened away from senior leadership positions (Deutschman, 2005; Boddy, 2006). Lastly, the current paper proposes a way for British market research companies, with their renown for creativity and innovation (Boddy, 2001; Boddy & Croft, 2006), to identify, via research using psychopathy measures, firms worthy of investing in (i.e., non-psychopathic firms).

Leading psychologists and theorists in management, have suggested that numerous agency issues concerning corporate scandals and collapses may have been averted if firms vetted employees for psychopathic traits or did not elevate these people to positions where they may harm the corporation (Deutschman, 2005). Deutschman, in writing about these workplace psychopaths, prophetically stated a concern that instead of utilizing a gage of psychopathy to vet psychopaths, some corporations could otherwise utilize such a gage as a recruitment tool. This looks to have taken place within investment banks (Basham, 2011). Doubtless the alleged utilization of a psychopathy identification tool by investment banks to recruit new employees was intended to find appropriately conscience-free personnel who may treat rival banks with competitive mercilessness and moral inconsequence. Unfortunately, such people are also callously indifferent to any other damage they may do, for reasons explained below.

Psychopaths

Psychopaths are the around one per cent (0.6%–1.2%) of the adult populace who possess no conscience, shame, guilt or ability to experience love for or feel empathy towards other people (Blackburn, 1988; Stout, 2005). However, psychopathy exists on a continuum and up to 23% of males may have enough psychopathic traits to make them behaviourally problematic for society (Levenson et al., 1995). Their dearth of emotion and integrity is apparently linked with neurobiological factors (Weber-Papen et al., 2008) but this debate is beyond the scope of this article. However, this lack of scruples and sentiment creates psychopaths who are unsympathetically intellectual, self-interested and callous to other people and thus potentially dangerous to their colleagues and their employing organizations (Viding, 2004; Brinkley et al., 2004).

Relatively dissimilar categories of psychopath exist (Murphy & Vess, 2003). One sub-type christened “successful psychopaths” by some; (historically a common nomenclature has not existed); seem better able to control their aggressive, anti-social impulsive inclinations than criminal psychopaths typically can. These successful psychopaths are reported to work relatively undetected in corporate society and they have been called Industrial, Organizational, Executive and Corporate Psychopaths (Boddy, 2016). The current paper refers to them as corporate psychopaths.

Corporate psychopaths

Corporate psychopaths, simply put, are just those well performing psychopaths who work in commercial settings. Consistent with forecasts from theory, investigation has revealed that corporate psychopaths have an influence on employee’s experience of corporate communications, abuse, conflict, bullying, job satisfaction, workload, corporate social responsibility, experience of organizational constraints and their withdrawal behaviour (Boddy, 2011b). Corporate psychopaths unconstructively influence employee stress and well-being (Boddy, 2014; Mathieu et al., 2014) and psychopaths have a propensity to be willing to take part in environmental transgressing in the shape of the illegal discarding of toxic waste substances (Ray & Jones, 2011).

With the realization that there is empirical evidence for the existence of corporate psychopaths in business it was recognised they have existed through history. An on-line search for “business psychopaths” revealed some outstanding individuals who have been named as prospective corporate psychopaths. Some of these people are considered in the following paragraphs. Firstly, an appraisal of the main findings from writings on corporate psychopaths is examined, to facilitate an appreciation of their qualities and to afford some comprehension of the gauges used to identify workplace psychopaths.

Cleckley, a pioneer in psychopathy research, describes a psychopath as someone who, at least at first meeting, can appear to be more attractive than average, and who can come over during dialogue as judicious in discernment, ethics, morals and values (Cleckley, 1941). Alternatively, reports Cleckley, these psychopaths cannot experience love and can undertake action which has severely deleterious results for those associated with them (involving infidelity, financial dishonesty, embezzlement and serial sexual promiscuity), while having no repentance or responsibility of any type for their actions (Boddy, 2016). They are also accomplished at deceiving others in respect of their participation or blameworthiness in these atrocious acts, thereby talking themselves out of difficulty and side-stepping any personal consequences or examination (Cleckley, 1941).

Cleckley identified 16 personality traits possessed by psychopaths (Cleckley, 1941). After Cleckley’s book, psychologists working within prisons became interested in the study of psychopaths and based on Cleckley’s list they devised measures of psychopathy (Boddy, 2016). These psychopathy measures were extensively utilized among psychopaths in prison populations and consequently psychopathy and criminality became confused in both the popular imagination and amongst psychologists. Nevertheless, the presence of organizational leaders with personality disorders, and the theoretically detrimental effects they may produce within corporate life and on organizational performance, gradually became apparent as a topic of academic interest in the concluding years of the 20th century (de Vries 1985) and was discussed in a succession of articles and manuscripts from academics in psychology and management e.g., (Babiak, 1995; Clarke, 2005). More recently the concept of the corporate psychopath has emerged as the nomenclature coalesces around this term. This has focused the concentration of researchers onto psychopaths inside corporations rather than inside prisons. Findings from modern research support the expectations from theory that have been made. It has been discovered that corporate psychopaths have a negative influence across an assortment of organizational outcomes and their behaviour is the opposite of being moral within business and is counterproductive in terms of constructing and nourishing effective teams and organizations which perform competently (Babiak et al., 2010; Boddy, 2010; Boddy et al., 2009).

Theories have arisen from the extant corpus of research into workplace psychopaths which endeavour to elucidate ways in which modern commerce has enabled the surfacing of psychopathic managers who have then influenced capitalism in an intemperate manner (Cohan, 2012c). It has been noted that neo-liberal corporations and corporate psychopaths share an offensive management style and an immoral lack of concern (Baines, 2004; Yates et al., 2001) for employees (Boddy et al., 2015b). It has therefore been reported that the possible role of corporate psychopaths as the praised agents of capitalism marks them as worthy of additional investigation (Boddy et al., 2015b).

Research materials and methods

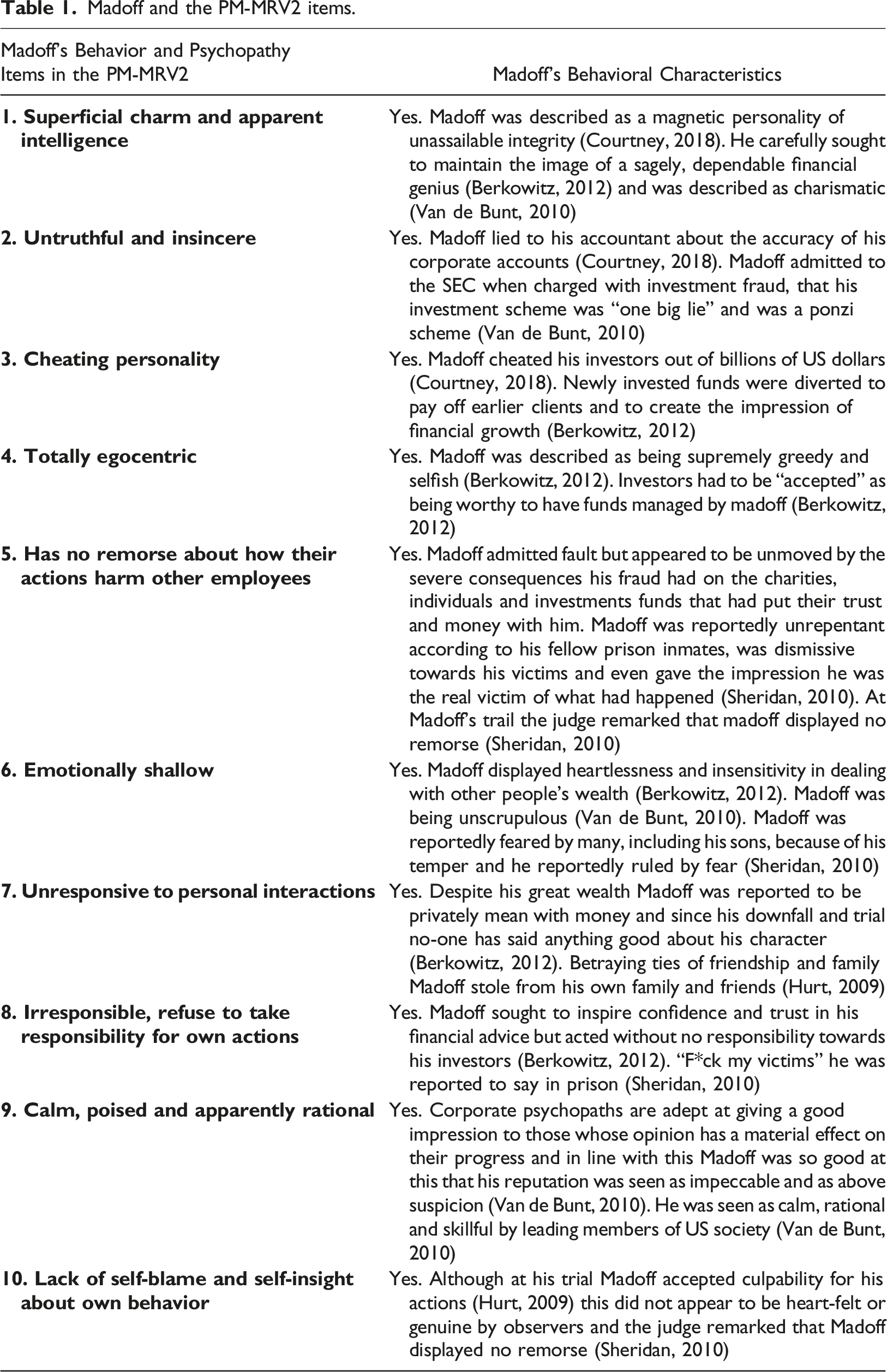

Madoff and the PM-MRV2 items.

Using these two psychopathy measures, an appraisal was carried out in terms of matching behavioural evidence from biographic materials and historical documents with the frequently acknowledged and highly proto-typical indicators of psychopathy. Where reported behaviour and the items in the gauges of psychopathy used overlap, then psychopathy may be deduced. Madoff can be examined because of the obtainability of recent authoritative reports of his conduct which may be compared versus the psychopathy gauges used.

Results

In an article concerning sociopaths, a term often used synonymously with that of psychopaths; Bernard Ebbers was nominated in respect of his leading part in the $11 billion fraud at WorldCom (Boddy, 2016). In similar vein Ken Lay, Jeff Skilling and Andy Fastow were also mentioned as having psychopathic traits in relation to their role in the Enron scandal. Enron’s Skilling was nominated as owning the qualities of a corporate psychopath being conniving, lacking in remorse, slick, lying, bullying, and egocentric. Enron is characterized as having been a spectacular fall from grace for a business (Rippin & Fleming, 2007) and the fall of Madoff’s financial empire was along similarly fraudulent lines. These macro-economic scandals jeopardize trust among consumers by striking at the foundations of free-market capitalism (Gosschalk & Hyde, 2005) and so are worthy of closer investigation. This is especially the case as calls for research of consequence, relevance and interest to real life have been made in this journal (Roberts & Adams, 2010) and the results of large financial scandals are consequential to many, who may also welcome their future avoidance.

Bernard Madoff was an ex-Chairman of Nasdaq, a rival organization to the New York Stock Exchange, and he has been called a sociopath (Henriques, 2012), and a psychopath (Winarick, 2010). Reportedly, Madoff reveals many of the qualities of a psychopath and could come across as pleasant and charismatic but be an avaricious manipulator, careless of whom he hurt in his acquiring wealth (Creswell & Thomas, 2009). A prominent figure in financial circles, Madoff was an outstanding salesman but was described as demonstrating no remorse or repentance when made to face up to his crimes (Creswell & Thomas, 2009). Madoff managed perhaps the biggest Ponzi scheme in history and fraudulently appropriated greater than $18 billion from investors. This was initially reported as being up to $65 billion (Monaghan & O’Flynn, 2012) but during receivership some funds were recovered while others never really existed except in Madoff’s fraudulent and overly-inflated accounts.

Described as being conning, untruthful, manipulative and deceptive (Henriques, 2012) Madoff sounds like a model candidate for the designation ‘corporate psychopath’. He left investors financially impoverished and emotionally traumatized (Glodstein et al., 2010) with several people committing suicide once their losses had been quantified.

Discussion

In line with the view that corporate psychopaths present a charming and apparently intelligent image when first met, Madoff was described by a reporter who interviewed him as being an innovator and of having a magnetic personality of ostensibly unassailable integrity (Courtney, 2018). With regards to corporate psychopaths being untruthful and insincere Madoff displayed these traits in abundance. He carefully sought to maintain the image of a sagely, dependable, financial genius while simultaneously running a fraudulent investment enterprise (Berkowitz, 2012). Madoff admitted to the Securities and Exchange Commission (SEC), when it charged him with investment fraud, that his investment scheme was “one big lie” and was a Ponzi scheme (Van de Bunt, 2010).

In terms of psychopaths having a cheating personality, newly invested money in Madoff’s investment fund was diverted to pay off earlier clients and to create the impression of financial growth (Berkowitz, 2012). Financial statements sent to clients were entirely fabricated but made to look credible by being in line with actual events in the stock exchange over corresponding time periods (Van de Bunt, 2010).

Corporate psychopaths are egocentric and self-centred and Madoff was likewise described as being supremely greedy and selfish (Berkowitz, 2012). In prison his ego was reported to be “intact” and Madoff was described as being totally unrepentant; for example, “F*ck my victims” Madoff was reported to have said (Sheridan, 2010). The frequent use of profane language is typical of psychopaths.

With respect to the psychopathic trait of emotional shallowness Madoff displayed heartlessness and insensitivity in dealing with other people’s wealth (Berkowitz, 2012). Further, when being told of the murder of a hedge fund manager he reportedly said “Why the f*ck would I be interested in some shit like that”, displaying a callous indifference to the fate of other people (Sheridan, 2010). In terms of being irresponsible Madoff sought to inspire confidence and trust in his financial advice and was held in awe by many, however he acted with no responsibility towards his investors (Berkowitz, 2012).

Corporate psychopaths are adept at giving a good impression to those whose opinion has a material effect on their progress and in line with this Madoff’s reputation was seen as impeccable and above suspicion (Van de Bunt, 2010). He was viewed as calm, rational, skilful and even charismatic by leading members of US society (Van de Bunt, 2010). So impressive was he that members of European royal families reportedly invested with him (Jackall, 2010). Even a Professor of Psychiatry who was an expert on financial scams, was fooled by the steady gains apparently on offer under Madoff’s investment scheme (Greenspan, 2009). Madoff reported that this reputation protected him from scrutiny from regulators such as the SEC (Van de Bunt, 2010).

Madoff called his apparently invincible and impressively titled investment strategy the ‘split strike conversion strategy’ although he did not actually invest anything in this scheme for at least the last 14 years of his fraudulent company, ‘Bernard L. Madoff Securities LLC’ (Jackall, 2010). In terms of psychopaths being unresponsive to personal interactions and lacking an appreciation for what others have done for them Madoff, as part of his fraudulent scheme, stole money from his own family and friends (Hurt, 2009) including people who felt very close to Madoff (Jackall, 2010).

Corporate psychopaths also tend to use bullying to challenge and disorientate their detractors and in line with this Madoff was described as deploying (apparently) ill-tempered outbursts towards any examiners who questioned his incredibly consistent returns on investment (Jackall, 2010). A climate of fear is created by corporate psychopaths to deter close examination of their behaviour (Boddy, 2017) and Madoff was reportedly feared by many, including his sons, because of his temper and he reportedly ruled by fear (Sheridan, 2010). Madoff generated fear and even as a child he was reported to treat his brother badly in front of household staff. People at work were reportedly afraid of his temper (Sheridan, 2010). Perhaps because of their lack of emotion and close inter-personal ties psychopaths are predatory in their behaviour towards others (Hare, 1994) and Madoff was described as being predatory towards possible investors and as an ‘archetypal predator’ (Sheridan, 2010).

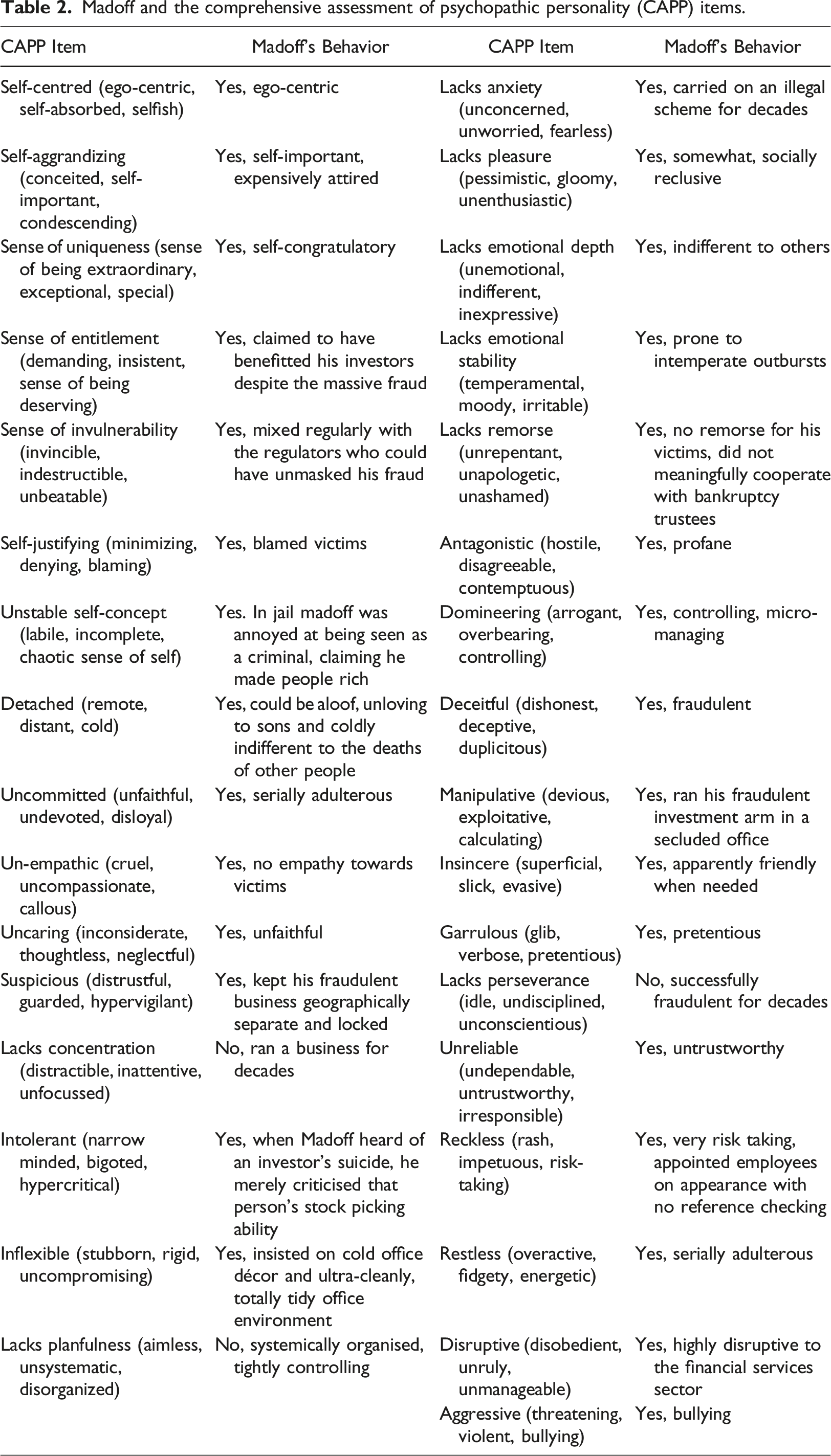

Madoff and the comprehensive assessment of psychopathic personality (CAPP) items.

One aspect of psychopathy which is not usually included in the identification of potential corporate psychopaths is their sexual promiscuity, because evidence for this would typically be difficult to gather in management research. However, in line with the other evidence for Madoff’s psychopathy is the finding that he had several affairs and was a ‘serial Casanova’ who paid off at least one female employee in order to keep her quite (Sheridan, 2010). Other investigators, including an FBI agent, have also ventured the opinion that Madoff displayed several of the traits of the typical psychopath including callousness towards his victims, grandiosity, manipulation and lying (Sheridan, 2010). Madoff used his impressive social relations and networking skills to widen the net of those caught in his fraudulent scheme (Manning, 2018).

Academic and popular curiosity into corporate psychopaths has expanded while corporate psychopathy theory conceives corporate psychopaths will be connected with fluctuating amounts of corporate destructiveness including fraud, dishonesty and organizational negativity. This article contributes to corporate psychopathy theory by supporting the idea that corporate leaders who tally highly against gauges of corporate psychopathy, can be lauded by the financial establishment as champions of shareholder capitalism (e.g. Bernie Madoff, Albert Dunlap, Ken Lay) and operate without restraint, while contemporaneously demolishing capital, incapacitating organizational effectiveness and reducing trust in financial markets (Boddy, 2016, 2018a). Research findings exhibited here help answer the appeal (Hannah et al., 2011) for additional research into the effects of leadership on ethical outcomes. Conclusions support the theoretical arguments that the leaders’ personality is significant in elucidating organizational results and this is an additional contribution of this current research. The current research also contributes to agency theory by suggesting a personality gauge – that of corporate psychopathy – which can identify characters who are very likely to proceed in their own interests rather than as organizational custodians.

A practical contribution is also highlighted in that psychopathy measures could be used by business market researchers to identify firms more likely to succeed or fail. Psychopathically led organizations like Maxwell’s Mirror group, Lay’s Enron, Dunlap’s Sunbeam, Ebbers’ WorldCom, and Madoff’s investment firm, ultimately fail and/or go bankrupt. Typically, investors, pension funds, pension holders and other stakeholders are impoverished, often severely. Helping avoid these scenarios via business market research could be an opportunity for market researchers to grasp. Market researchers have long acknowledged the benefits of making decision based on good intelligence and this article outlines a methodology which could provide an additional source of intelligence gathering for investment decisions (Cowan, 1994).

Further research opportunities for market research companies

In the future, business to business researchers may offer reputational surveys to major investment companies such as pension funds to evaluate the psychopathy of the leaders of companies that may be potentially invested in. Those institutional investors may then make their investment decisions in a more informed manner and could avoid investing in firms like Lay’s Enron, Ebbers WorldCom, Maxwell’s Mirror Group and Madoff’s investment scheme. Such research could open a brand-new area of research for market research companies to engage in. Doing so may also make the world more sustainable as it helps avoid investment companies making investments in unsustainable, polluting and short-term oriented businesses (Boddy & Baxter, 2021).

Conclusions

The contribution of this article is to illustrate that highly psychopathic senior businesspeople who were quite plausibly genuine psychopaths are visible in commercial history. This finding was entirely foreseeable given that psychopaths constitute approximately one per cent of the adult population and are more adept at getting ahead in organisations than other people are.

This current article intended to understand whether some corporate scandals and bankruptcies look to be typified by the attendance of senior corporate officials who might be workplace psychopaths. Using gauges of conduct largely developed from Cleckley’s classifications, and related to reports of concrete behaviour, this has demonstrably been the case. Bernie Madoff is commonly nominated as a potential corporate psychopath, and he scored highly on both the gauges of psychopathy utilized within this investigation. Further, like other potential corporate psychopaths such as Maxwell, Ebbers, Dunlap and Lay, Madoff was associated with corporate failure and fraud. This article arguably adds to critical contemporary views of prevailing capitalism by illustrating the traits, behaviour and outcomes of one of its more infamous 20th century leaders. This innovative insight can be used by future financial market researchers to further explore the role of personality in financial markets.

Furthermore, the article offers the insight that Madoff’s fraud was an outcome of his personality and that similar personalities such as Maxwell, Fastow, Lay and Dunlap, behave in similar ways. Previous research indicates that psychopaths have stable personalities over time and that corporate psychopaths have a common modus operandi. Therefore, similar outcomes can be anticipated from comparable personalities into the future. Corporate psychopaths may be identified before they ascend to power in financial institutions. A remaining question is whether society will allow this ascension.

Opportunities for market research companies to offer research services which help identify business leadership that is non-ruthless, socially responsible, non-polluting (i.e., non-psychopathic) may be available via the use of survey research versions of the psychopathy measures identified here. Consumers, pension funds and other ethical investment firms can then make more informed decision about the types of firms they want to invest in. Improved and more sustainable societal outcomes may result from this such as helping to avoid further global financial crises.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.