Abstract

While cultural distance (CD) is a popular construct in international business (IB), most studies confound the distance and country profile effects. There is an ever-growing debate on measurement issues and distinguishing the effect of doing business in countries with different cultural profiles. While the vast majority of studies focus on the implications of CD, the objective of this study is to investigate how the cultural profile in the host country affects the financial performance of foreign subsidiaries in Latin America. We employ a quantitative approach with panel data, including over 4200 firm-year observations of the same foreign subsidiary firms in the 10 largest economies in Latin America. We measure cultural profile of the host country using the four original dimensions of Hofstede's framework. Then, we estimate the effects on the financial performance of foreign subsidiary firms using the original scale and by splitting the scale (e.g. degree of masculinity vs degree of femininity) to compare the effects of the opposite poles of the cultural dimensions. The findings reveal that certain cultural characteristics in the host country profile (e.g., individualism and femininity) positively impact performance. In contrast, other cultural traits have a negative (masculinity and collectivism) or no significant impact (uncertainty avoidance). Also, the firms can adjust positively to high and low power distance scores in the host country. This study offers novel insights into the implications of national culture for financial performance by showing that the host country's cultural profile significantly impacts foreign subsidiary firms’ performance.

Keywords

Introduction

A widely accepted conclusion in the mainstream IB literature is that national cultural dimension scores cannot be considered better or worse. Thus, studies have focused on the implications of cultural distance (i.e., the degree of dissimilarity) between countries (CD) (Beugelsdijk et al., 2018a; b; Cuervo-Cazurra and Genc, 2011; Shenkar et al., 2008; Singh, 2017; Zaheer, 1995). However, despite the popularity of CD, there is an ever-growing concern regarding the theoretical arguments and methodological procedures that affect the credibility of such studies (Maseland et al., 2018; Shenkar et al., 2020; Verbeke et al., 2017). By focusing on a single home or host country, the vast majority of CD studies conflate distance with country profile effects (Bae and Salomon, 2010; Beugelsdijk et al., 2015; Brouthers et al., 2016; Franke and Richey, 2010; Maseland et al., 2018; Van Hoorn and Maseland, 2016). Therefore, while some proclaim that “international management is management of distance” (Zaheer et al., 2012, p. 19), we must take home and host country profiles into consideration (Beugelsdijk et al., 2017). Studies such as Harzing and Pudelko (2016) show that the home country's culture can influence the decision to go abroad using a specific entry mode. On the other hand, the effects on the outcomes, such as the financial performance of foreign subsidiaries, are likely to be conditioned by the context in which the firm operates (i.e., the host country’s cultural profile) as well as by the CD between home and host countries.

Beugelsdijk et al. (2017, p. 43) posit that “cultural differences and cultural distance are not the same.” By comparing the cultural traits in the home and in different host countries, Stor (2021) identified that human resources practices in the foreign subsidiary must conform to the cultural profile of the host country. The implications of the direction of CD towards host countries in the opposite poles of the cultural dimensions were also identified by Correa da Cunha et al. (2022). In their study, these authors identified similar impacts on the financial performance of different groups of foreign subsidiary firms associated with CD towards host countries with specific profiles. Correa da Cunha et al. (2022) found that regardless of the different sizes of CD in each group of foreign subsidiary firms, the results revealed the same positive or negative impacts for CD towards host countries with specific cultural profiles. This evidence indicates that although cultures cannot be compared as better or worse, adjusting to certain cultural profiles in the host country might be easier for some foreign subsidiary firms than others. Adjustment difficulties may be expected to translate into negative financial performance for the subsidiary. Van Hoorn and Maseland (2016, p. 375) state that “extant institutional research is unable to tell whether a particular MNE behavior is a response to the challenges posed by a host country’s institutional profile or to the challenges posed by the dissimilarity between the host country's institutional environment and the MNE's home country environment.”

Institutional distance derives from the institutional pillars of Scott (1995) and represents the degree of dissimilarity between pairs of countries in terms of regulatory, cognitive, and normative institutions between two countries (Kostova, 1996). Formal institutions primarily encompass the regulatory aspects of a society, whereas informal institutions pertain to the normative and cognitive frameworks that shape the society (Peng et al., 2009). Consequently, culture can be understood as a fundamental component of the overall institutional structure, as it forms a part of the informal institutions that provide the foundation for formal institutions (Peng et al., 2009). In that sense, cultural distance measures the degree of dissimilarity between two countries in terms of national culture (Hutzschenreuter et al., 2016), while cultural profile represents the cultural characteristics of a particular country. To contribute to this debate, the goal of this paper is to address the following research question: What are the implications of the cultural profile in the host country on the financial performance of foreign subsidiary firms?

We address the research question using a quantitative approach with panel data, including over 4,200 firm-year observations of the same foreign subsidiary firms operating in the 10 largest economies in Latin America over three consecutive years. Latin America is not only under-researched in the academic literature but also provides an “ideal ‘natural laboratory’ to build and test management theories” due to its societal, cultural, and economic characteristics (Aguinis et al., 2020, p. 615). To provide robustness, we compare the effects of the cultural profile in the host country on different groups of firms, that is all foreign subsidiaries firms, foreign subsidiaries from developed countries only, foreign subsidiaries from emerging markets (including from Latin America) and a sub-sample including foreign subsidiaries from Latin America only. The different characteristics of the cultural profile in the home country allow us to test our assumptions regarding the specific impact on firm financial performance.

We test the hypothesis that due to the unique characteristics of the opposite poles of the cultural dimensions, the effects of the host country’s cultural profile on the financial performance of foreign subsidiary firms can be positive or negative. The cultural profile of the host country is measured using the four original dimensions of Hofstede, and the effects on the financial performance of foreign subsidiary firms are estimated using the original scale and by splitting the scale (e.g. degree of masculinity vs degree of femininity) to compare the effects of the opposite poles of the cultural dimensions.

The rest of the study is organized as: following the introduction, we present the literature review and hypotheses. The third section details the research method and approach to model estimation. The results are presented in the fourth section, while the fifth and final section offers concluding observations.

Literature review and hypothesis development

Cultural distance represents the degree of dissimilarity between countries (Hutzschenreuter et al., 2016). The country profile relates to the environment of a particular home or host country where firms operate and are exposed to different challenges and opportunities (Konara and Shirodkar, 2018; Meyer et al., 2009). An important issue that undermines the credibility of CD studies is distance-profile conflation (Bae and Salomon, 2010; Beugelsdijk et al., 2015; Franke and Richey, 2010; Van Hoorn and Maseland, 2016). According to Brouthers et al. (2016), 80% of CD studies are potentially wrong, as they confound the effects of distance with those of home or host country profiles. Others have criticized the overreliance on the traditional (and simplistic) metrics used to operationalize the construct of CD (Konara and Mohr, 2019; Maseland et al., 2018; Shenkar et al., 2020). The divergence in empirical findings and contradictory theoretical explanations raise concerns that the “knowledge of distance, in terms of conceptual specification and consequences for IB practice, is incomplete and sometimes ambiguous” (Verbeke et al., 2017, p. 17).

More recently, studies have shown that the effects of CD on host countries with specific profiles tend to affect the financial performance of different groups of firms in similar ways depending more on the direction than the distance size (Correa da Cunha et al., 2022). This suggests that although cultures may not be compared in terms of better or worse, the effects of certain cultural profiles in the host country might be easier for foreign subsidiary firms to adjust to, while other cultural traits can create additional challenges and conflicts, making it more difficult for foreign subsidiaries to adjust. The impact of these different cultural profiles on the financial performance of foreign subsidiaries can be either positive or negative (or neutral).

Distance-profile conflation

Several studies have noted the limitations of CD (see, e.g., Harzing and Pudelko, 2016; Tung and Verbeke, 2010; Zaheer et al., 2012). Moreover, the underlying assumptions in the distance and profile-related studies are very different. While most CD studies assume that distance represents a liability, profile studies focus on specific contextual characteristics in a particular country that create more or less favourable conditions for firms to operate. Despite the differences, Van Hoorn and Maseland (2016, p. 375) state that “extant institutional research is unable to tell whether a particular MNE behaviour is a response to the challenges posed by a host country’s institutional profile or to the challenges posed by the dissimilarity between the host country’s institutional environment and the MNE’s home country environment.” According to Brouthers et al. (2016), most CD studies might be confounding distance and profile effects as they focus on a single home or host country. Thus, to differentiate distance and profile effects, it is crucial to include a sufficiently diversified combination of home and host countries (Franke and Richey, 2010) while providing adequate (and relevant) cultural variability within the subsamples (Gupta et al., 2002).

Asymmetric effects and distance-profile conflation

According to Cuervo-Cazurra and Genc (2011), firms can develop nonmarket resources in their home country that can be advantageous when operating in a foreign host country. They propose three classifications of the dimensions: obligating, pressuring and supporting. The direction and size of the distances are essential for the pressuring and supporting dimensions, as countries can be compared as more or less developed. For the obligating dimension, which includes culture, “a country cannot be considered to have a more developed culture (….) moving from Country A to Country B is equally disadvantageous as moving in the opposite direction” (Cuervo-Cazurra and Genc, 2011, p. 445). However, Zaheer et al. (2012, p. 18) argue that “the conceptualization of cultural distance as linear, fixed, objective, symmetrical, homogeneous and always challenging is, as Shenkar (2001) so brilliantly argued, flawed and not particularly useful in its current state”. The assumption that cultures cannot be considered better or worse (Cuervo-Cazurra and Genc, 2011) makes it challenging to discuss and explain CD's different and sometimes asymmetric effects (Correa da Cunha, 2019; Correa da Cunha et al. 2022; Magnani et al., 2018; Selmer et al., 2007). However, some authors posit that the perceived asymmetric effects relate to the characteristics of the countries’ profiles included in the research rather than the CD between countries (Brouthers et al., 2016; Harzing and Pudelko, 2016).

The host country cultural profile

In addition to the cultural dimension’s characteristics and importance, we argue that the opposite poles of the cultural dimensions can positively or negatively impact foreign subsidiary firms’ financial performance. By examining the relationship between national cultures and health systems performance, Braithwaite et al. (2020) found evidence that countries with certain cultural traits achieve better health system performance than countries with other cultural characteristics. In that sense, although cultures cannot be compared as better or worse (Cuervo-Cazurra and Genc, 2011), there are significant differences in cultural dimensions (Hofstede, 1980) and the characteristics of the opposite poles that can impact the financial performance of foreign subsidiaries positively or negatively. Due to the distinct cultural traits, Shenkar et al. (2020) posit that aggregating Hofstede’s dimensions using a composite index violates the framework's assumptions. Therefore, in this study, we use Hofstede’s (1980) four original dimensions: power distance, individualism versus collectivism, masculinity versus femininity, and uncertainty avoidance to assess how the cultural profile of the host country impacts the financial performance of foreign subsidiaries operating in Latin America. Hofstede's model is relevant, as it has the most coverage in Latin America (Deephouse et al., 2016), and the literature cites its validity, reliability, simplicity and usefulness (Jackson, 2020; Kirkman et al., 2006; Li and Parboteeah, 2015; Oyserman et al., 2002).

Next, we highlight the key features of the cultural dimensions and the distinct characteristics of the opposite poles and hypothesize the effects of the host country profiles on the financial performance of foreign subsidiaries.

Power distance index (PDI)

Power distance represents inequality being defined from below, not from above, so a society's level of inequality is endorsed by its leaders and followers. It focuses on “the extent to which the less powerful members of institutions and organizations within a country expect and accept that power is distributed unequally” (Hofstede, 1994, p. 28). Countries can be classified as high or low power distance.

High power distance pole

Cultures classified as the high power distance discourage employees from using their judgment and intelligence in making decisions (Chin and Pun 2002; Tata and Prasad 1998). In high power distance societies, managers must make the decisions, provide clear guidance and control subordinates. Hierarchy means existential inequality to individuals in high power distance cultures (Hofstede, 2011). Foreign subsidiary firms operating in high power distance host countries might be affected negatively as subordinates expect to be told what to do (Hofstede, 1994). Low feedback from the local team makes overcoming the liability of foreignness more difficult. Moreover, high power distance encourages corruption as scandals are covered up, which increases transaction and agency costs (Hofstede, 2011). Thus, a high power distance cultural profile in the host country may be expected to hurt the financial performance of foreign subsidiary firms. In order to test these assumptions, we propose hypothesis H1:

A host country profile characterized by high power distance is negatively associated with the financial performance of foreign subsidiaries.

Low power distance pole

In low power distance societies, employees expect to be consulted and participate in decision-making (Hofstede et al., 2010). Such consultation and participation may serve to overcome the liability of foreignness when foreign subsidiary firms operate in low power distance host countries. In low power distance societies, hierarchy means inequality of roles established for convenience (Hofstede, 2011). When operating in low power distance societies, foreign subsidiary firms' financial performance might be positive as it is easier to obtain feedback from the local team, facilitating the decision-making process. Power is legitimate and may be used to support or hurt members of the society (Hofstede, 1994). Corruption is rare in low power distance cultures, as involvement in scandals will end political careers (Hofstede, 2011). These characteristics of a low power distance cultural profile may positively impact the financial performance of foreign subsidiary firms as it reduces transaction and agency costs. Based on these assumptions, we hypothesize:

A host country profile characterized by low power distance is positively associated with the financial performance of foreign subsidiaries.

Individualism versus collectivism dimension (IDV)

The individualism versus collectivism (IDV) dimension of national culture represents the extent to which individuals integrate into groups (Hofstede, 1980). In individualist societies, the ties between individuals are loose: everyone is expected to look after themselves and their immediate family (Hofstede, 1980). In collectivist cultures, “people are integrated from birth onward into strong, cohesive in-groups, often extended families (with uncles, aunts, and grandparents), protecting them in exchange for unquestioned loyalty” (Hofstede and McCrae, 2004, p. 63).

Individualistic pole

In individualistic cultures, disputes are resolved by working out functional conflict solutions openly and conjointly by emphasizing the importance of addressing incompatible goals/outcomes (Ting-Toomey, 1999). Individuals “are expected to act according to their own interests, and work should be organized in such a way that this self-interest and the employer’s interest coincide” (Hofstede et al., 2010, p. 119). Therefore, foreign subsidiaries operating n individualistic host country contexts can implement incentives to motivate the commitment and participation of individuals. This type of cultural profile creates less resistance and lower costs associated with managing the expectations and demands of local in-groups. Moreover, studies have shown that cultural distances toward individualistic host countries have a more positive impact on foreign subsidiary firms’ financial performance than cultural distances toward more collectivist host countries (Correa da Cunha et al., 2022). We argue that these effects might be associated with the distinct characteristics of the opposite poles of the cultural dimension. In that sense, we argue that individualistic host countries positively impact the financial performance of foreign subsidiary firms. Based on these assumptions, we present hypothesis H3:

A host country profile characterized by individualism is positively associated with the financial performance of foreign subsidiaries.

Collectivist pole

In collectivist societies, “individuals may be induced to subordinate their personal goals to the goals of some collective, which is usually a stable ingroup (e.g., family, band, tribe), and much of the behaviour of individuals may concern goals that are consistent with the goals of this ingroup” (Triandis et al.,1988, p. 324). Conflict management is much more complicated as it involves more subtle negotiation of in-group/out-group face-related issues – pride, honour, dignity, insult, shame, disgrace, humility, trust, mistrust, respect, and prestige – in a given conflict episode. In collectivist societies, the “appropriate facework moves and countermoves are critical for collectivists before tangible conflict outcomes or goals can be addressed” (Ting-Toomey, 1999, p. 211). Foreigners, being considered out-groups, may face costly sanctions for non-conforming to the expectations of local in-groups (Triandis et al., 1988). In that sense, foreign firms will face greater challenges adjusting to more collectivist host countries. Studies have shown that cultural distance toward more collectivist host countries negatively impacts foreign subsidiaries' financial performance (Correa da Cunha et al., 2022). This evidence indicates that collectivist host countries' increased business costs can negatively impact the financial performance of foreign subsidiary firms. Based on these arguments, we hypothesize:

A host country profile characterized by collectivism is negatively associated with the financial performance of foreign subsidiaries.

Masculinity versus femininity dimension (MAS)

Masculinity versus femininity (MAS) dimension of national culture represents the different emotional roles attributed to different sexes (Hofstede, 1980).

Masculinity pole

A more assertive pole (Hofstede, 1980) “pertains to societies in which social gender roles are distinct (i.e., men are supposed to be assertive, tough, and focused on material success, whereas women are supposed to be more modest, tender, and concerned with the quality of life)” (Hofstede, 1994, p. 82). Masculine societies can be more assertive and, in some cases, more aggressive and confrontative, leading to escalating conflicts between members of different cultures. Foreign subsidiary firms operating in masculine host countries will face more conflicts and confrontations that can be time-consuming and costly to resolve. Studies have found that cultural distance toward more masculine host countries hurts the financial performance of foreign subsidiary firms (Correa da Cunha et al., 2022). Similarly, Stor (2021) has shown that in more masculine host countries, human resource practices must be tailored according to the characteristics of the local context. Thus, the cost of operating in masculine host countries might be higher causing a negative impact on the financial performance of foreign subsidiary firms. In that sense, we argue that the more masculine the host country, the more negative the impact on the performance of foreign subsidiaries. In order to test these assumptions, we propose the following hypothesis:

A host country profile characterized by masculinity is negatively associated with the financial performance of foreign subsidiaries.

Femininity pole

The more modest and caring pole “pertains to societies in which social gender roles overlap (i.e., both men and women are supposed to be modest, tender, and concerned with the quality of life)” (Hofstede, 1994, p. 83). Feminine societies favour consensus and avoid confrontation (Hofstede, 1980). Feminine culture tends to avoid confrontation and is more accommodating of the needs of different cultures. Compared with masculine cultures, it is easier to transfer managerial practices from the headquarters to the foreign subsidiaries in feminine host countries (Stor, 2021). Moreover, studies have found that cultural distances towards more feminine host countries positively impact the financial performance of foreign subsidiaries (Correa da Cunha et al. 2022). Therefore, the more accommodating nature of feminine host countries makes it easier for foreign subsidiary firms to adjust and operate, causing a positive impact on financial performance. Based on these assumptions, we hypothesize:

A host country profile characterized by femininity is positively associated with the financial performance of foreign subsidiaries.

Uncertainty avoidance dimension (UAI)

Uncertainty avoidance represents a society's tolerance for ambiguity: “the extent to which the members of a culture feel threatened by uncertain or unknown situations” (Hofstede, 1994, p. 113). It evaluates how members of a society feel uncomfortable or comfortable dealing with unstructured situations (Hofstede, 1980).

High uncertainty avoidance pole

Minimizes the possibility of “surprising” (unpredictable) situations by following strict laws or rules and by adopting safety and security measures (Hofstede et al., 2010). Members of high uncertainty avoidance societies “are also more emotional and are motivated by inner nervous energy” (Hofstede and McCrae, 2004, p. 62). These characteristics can have a negative impact on the performance of foreign subsidiaries operating in high uncertainty avoidance society as negotiations and contracts tend to be more complex and costlier. High uncertainty avoidance societies resist change as any disruption to routine is perceived as a threat. Foreign subsidiaries trying to react to fast-changing market conditions in high uncertainty avoidance host countries will face resistance and take too long to adjust, which can impact performance negatively. Based on these assumptions, we present the following hypothesis:

A host country profile characterized by high uncertainty avoidance is negatively associated with the financial performance of foreign subsidiaries.

Low uncertainty avoidance pole

Low uncertainty avoidance societies are more tolerant and open to different opinions (Hofstede, 1980). In low uncertainty avoidance countries, there is a tendency to have “as few rules as possible, and on the philosophical and religious level, they are relativist and allow many currents to flow side by side” (Hofstede and McCrae, 2004, p. 62). This type of society prefers simpler contracts and tends to be more flexible and tolerant of different opinions as changes are perceived as opportunities. When operating in low uncertainty avoidance host countries, the response to market condition changes is faster, allowing firms to take advantage of opportunities and avoid unnecessary risks. According to these assumptions, we hypothesize:

A host country profile characterized by low uncertainty avoidance is positively associated with the financial performance of foreign subsidiaries.

Data and method

Sample and procedures

The data are from ORBIS and consist of over 4,200 foreign subsidiaries from developed and emerging markets operating in the 10 largest countries in Latin America, ranked by GDP (i.e. Argentina, Brazil, Colombia, Chile, Ecuador, Mexico, Panama, Peru, Uruguay and Venezuela). The data cover the period 2013 to 2015. According to Aguinis et al., 2020, due to its unique societal, cultural, and economic characteristics, Latin America provides an “ideal ‘natural laboratory’ to build and test management theories” (p. 615). Since the early 1990s, the region, previously marked by protected, inefficient, and outdated domestic industrial sectors and unstable political conditions, saw improvements spurned by accelerating domestic reforms (Aguilera et al., 2017; Hallward-Driemeier, 2001; Lu and Beamish, 2001; Santiso, 2013). From 1990 to 2019 (before the COVID-19 pandemic), GDP grew fivefold, final consumption expenditure increased from US$750 billion to US$4.6 trillion, and annual inflation declined from nearly 22% to 2.4% (World Bank, 2022). These changes created favourable conditions for foreign multinational companies – and inward foreign direct investment grew from US$8.5 billion in 1990 to a record high of $345 billion in 2013.

We start with the full sample, including foreign subsidiaries from developed countries and emerging markets. The data are separated into subsamples with unique characteristics to provide more robust estimates when testing the hypotheses. We follow the World Economic Situation and Prospects (WESP) 2015 report from the United Nations to compare the impact of the host country profiles. 1 Three subsamples are created with foreign subsidiaries from (a) developed countries, (b) all emerging markets, and (c) Latin America. The developed country subsample consists of 22 countries (number of subsidiaries in parentheses): Australia (2), Austria (6), Belgium (17), Canada (33), Denmark (1), Finland (6), France (97), Germany (96), Ireland (1), Italy (59), Japan (34), Luxembourg (28), Netherlands (59), New Zealand (4), Norway (4), Poland (1), Portugal (9), Spain (271), Sweden (21), Switzerland (48), the United Kingdom (85) and the United States of America (331). The emerging markets subsample includes firms from 22 different home countries, of which 12 are from Latin America (number of subsidiaries in parenthesis): Argentina (8), Brazil (35), Chile (34), Colombia (14), Costa Rica (7), Ecuador (9), El Salvador (1), Mexico (18), Panama (31), Peru (13), Uruguay (7) and Venezuela (7) and 10 are from countries outside the region: China (38), Hong Kong (9), India (4), Israel (4), Malaysia (1), Pakistan (1), Republic of Korea (3), Russian Federation (2), Singapore (3) and Turkey (1). These foreign subsidiaries are observed over a period of three consecutive years.

The subsidiaries included in our data sample provide a good representation of foreign firms operating in the region. There are 168 combinations of different home and host countries and a comparable number of firms, which, given the large number, provide a robust and credible generalization regarding the effects of distance (Bae and Salomon, 2010; Beugelsdijk et al., 2015; Franke and Richey, 2010; Van Hoorn and Maseland, 2016). Due to the diverse range of the data, we avoid distance-profile conflation while providing adequate (and relevant) cultural variability within the subsamples (Gupta et al., 2002). This is important, as the effects of CD might depend on other contextual characteristics of the home and host countries (Meyer, 2009; Teagarden et al., 2018). Furthermore, our data include approximately 70% service and 30% industrial firms, which, according to the World Bank's value added by activity (% of GDP), provides a good representation of the economic activity in the region (World Bank, 2022).

Panel data method

We use panel data to evaluate the relationship between several variables by following the same firms over a particular period. This approach provides robustness, as it checks the consistency of the models across several periods. We perform the Hausman test to select between fixed and random effects estimators. The results indicate that the generalized least squares (GLS) random-effects estimation method is adequate for our analysis, given its extensive use in the literature (Bertschek, 1995; Kumar and Aggarwal, 2005; Xie and Li, 2018). Additionally, it has the advantage of providing estimates for the effects of time-invariant variables (Xie and Li, 2018), which becomes a relevant feature for our study, as the cultural profile measured using Hofstede’s dimensions remains constant over time.

Dependent variable

Profit margin data from the ORBIS database adequately assess financial performance (Vahlne and Johanson, 2017). They are also less susceptible to changes in asset valuations from investment or depreciation (Geringer et al., 1989; Contractor et al., 2003). The measure provides a more robust alternative to evaluate firm performance when comparing firms from different industries, given the variance in asset values. Moreover, sustaining the company’s profit margins becomes even more challenging in turbulent environments, especially in emerging markets, and offers a representation of the effectiveness of management in investing in projects that add value (Chopra and Mier, 2017).

Explanatory variables - host country cultural profile

The host country’s cultural profile is measured using two scales. (a) The Hofstede Scale tests the impact of different host country profiles using the four original dimensions of Hofstede. While Hofstede’s scale generally ranges from 0 to 100, other scores beyond this range are possible (Minkov, 2012). In this study we use the four original dimensions from Hofstede. (b) The Split Scale: two separate scales to account for the asymmetric effects of the opposite poles of the cultural dimensions. As Hofstede's scales range from 0 to approximately 100, the split scale uses 50 (the midpoint) as the point of reference and values for each split scale increase in opposite directions. For example, an IDV score of 70 in the host country is 20 on the individualism scale (Cultural Dimension HIGH). In contrast, an IDV score of 30 is 20 on the collectivist scale (Cultural Dimension LOW).

We compute the score in each split scale using the following equation:

Control variables

We control for industry sector characteristics (i.e., industrial vs service firms), industry sector and subsidiary annual growth, subsidiary size (i.e., total assets and sales revenue) and subsidiary market share – these have the most significant effects on the financial performance of firms across different industries (Capon et al., 1990). Power distance and collectivism correlate with low economic development (Hofstede, 2011) and weak formal institutions (Cuervo-Cazurra and Genc, 2011). We follow the approach used in the literature and control for the characteristics of the institutions that govern economic activity and social interaction in the host country using the World Governance Indicators (WGI) from the World Bank (Dikova, 2009; Hernández and Nieto, 2015; Konara and Shirodkar, 2018). According to the World Bank, “governance consists of the traditions and institutions by which authority in a country is exercised. This includes the process by which governments are selected, monitored and replaced; the capacity of the government to effectively formulate and implement sound policies; and the respect of citizens and the state for the institutions that govern economic and social interactions among them.”(Worldwide Governance Indicators, n.d.) The WGI includes six variables: Voice and Accountability, Political Stability and Absence of Violence/Terrorism, Government Effectiveness, Regulatory Quality, Rule of Law, and Control of Corruption. These variables relate to the process by which governments are selected, monitored and replaced; the capacity of the government to effectively formulate and implement sound policies; and the respect of citizens and the state for the institutions that govern economic and social interactions among them (Worldwide Governance Indicators, n.d.). The WGI correlates with economic development (Kaufmann et al., 2009), allowing us to control the degree of economic development in the host country while testing the impact of the Power Distance and Individualism dimensions. Due to the high correlation between the six dimensions of the WGI, we use a composite index computed as the arithmetic means of the six variables.

Results and analysis

Preliminary tests

The tests reveal a low p-value for the Breusch-Pagan test and a high p-value for the Hausman test, pointing to the random effects estimation method being the most adequate. Given the presence of heteroskedasticity detected using White's test, we use Heteroskedasticity and Autocorrelation Consistent (HAC) covariance estimation (White, 1980; MacKinnon and White, 1985; Andrews, 1991). The variance inflation factors (VIFs) are lower than 2.0, below the maximum of 10 recommended by Neter et al. (1990), thus indicating no multicollinearity.

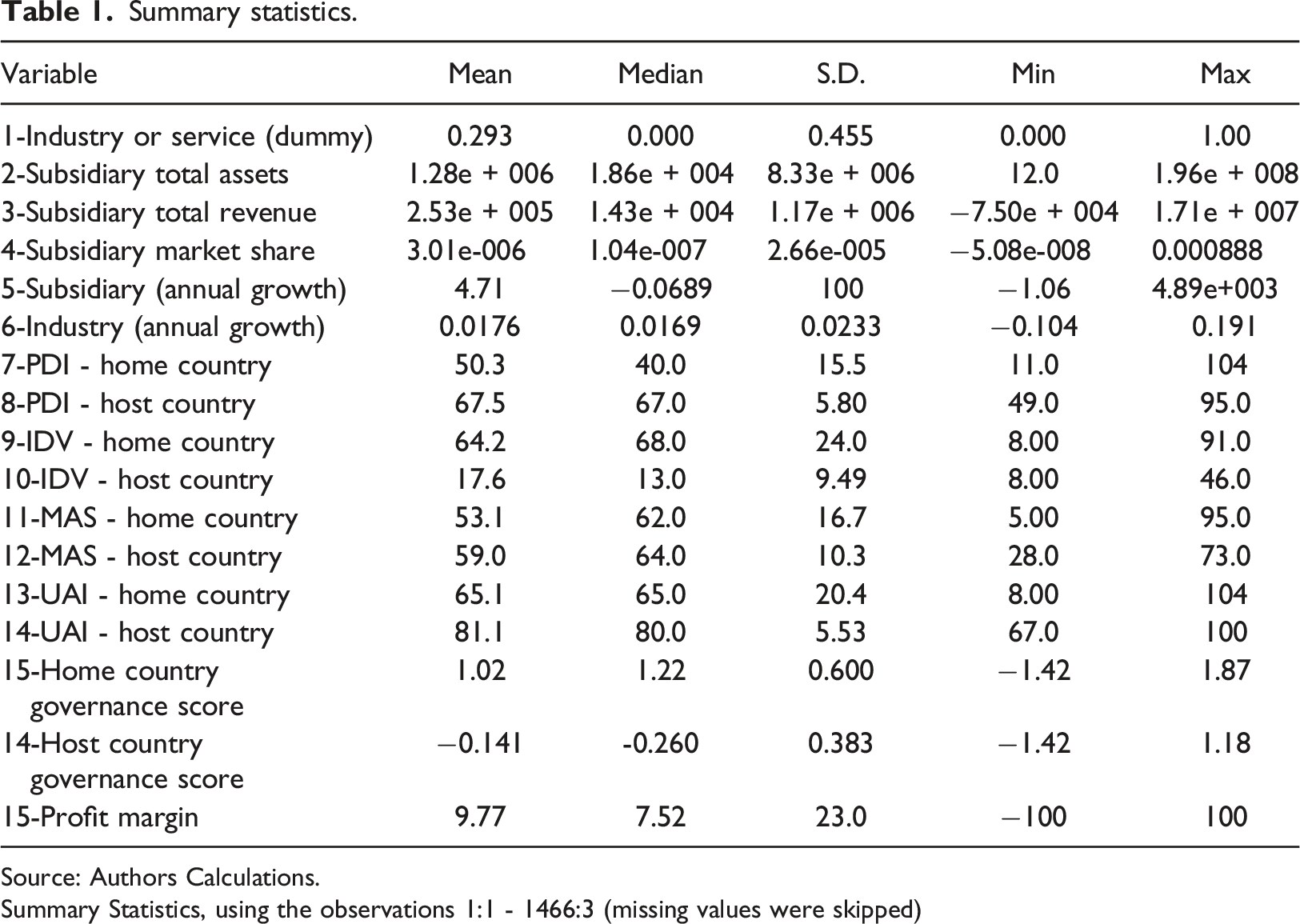

Summary statistics.

Source: Authors Calculations.

Summary Statistics, using the observations 1:1 - 1466:3 (missing values were skipped)

Table 1 shows that the mean value for PDI in the host countries is 67.5, while the minimum is 49 and the maximum 95, which highlights the high PDI scores in countries in Latin America. Table 1 shows that the home countries included in the sample are highly diversified, as PDI scores range from 11 to 104. The data shows that host countries in the sample are collectivist. The mean IDV score for the host countries is 17.6; the minimum is 8, and the maximum is 46. The IDV mean score for the home countries is 64.2 (individualistic), the minimum is 8, and the maximum is 91. MAS scores in the host countries are 59 (mean), 28 minimum and 73 maximum, while in the home countries, the mean score is 53.1, the minimum is 5, and the maximum value is 95. Countries in Latin America score high in UAI (Hofstede, 1980), and the sample highlights these characteristics as the mean score is 81.1, the minimum score is 67, and the maximum is 100. In the home countries, the mean UAI score is 65.1, the minimum is 8, and the maximum is 104. The two (home) countries in the sample that score above 100 are Malaysia, with a PDI of 104 and Portugal, with a UAI of 104. The cultural characteristics in the sample show the diversity of countries included in the home countries and the main characteristics of the host countries, which provide a good representation of the cultural traits in the Latin American region (Hofstede, 1980).

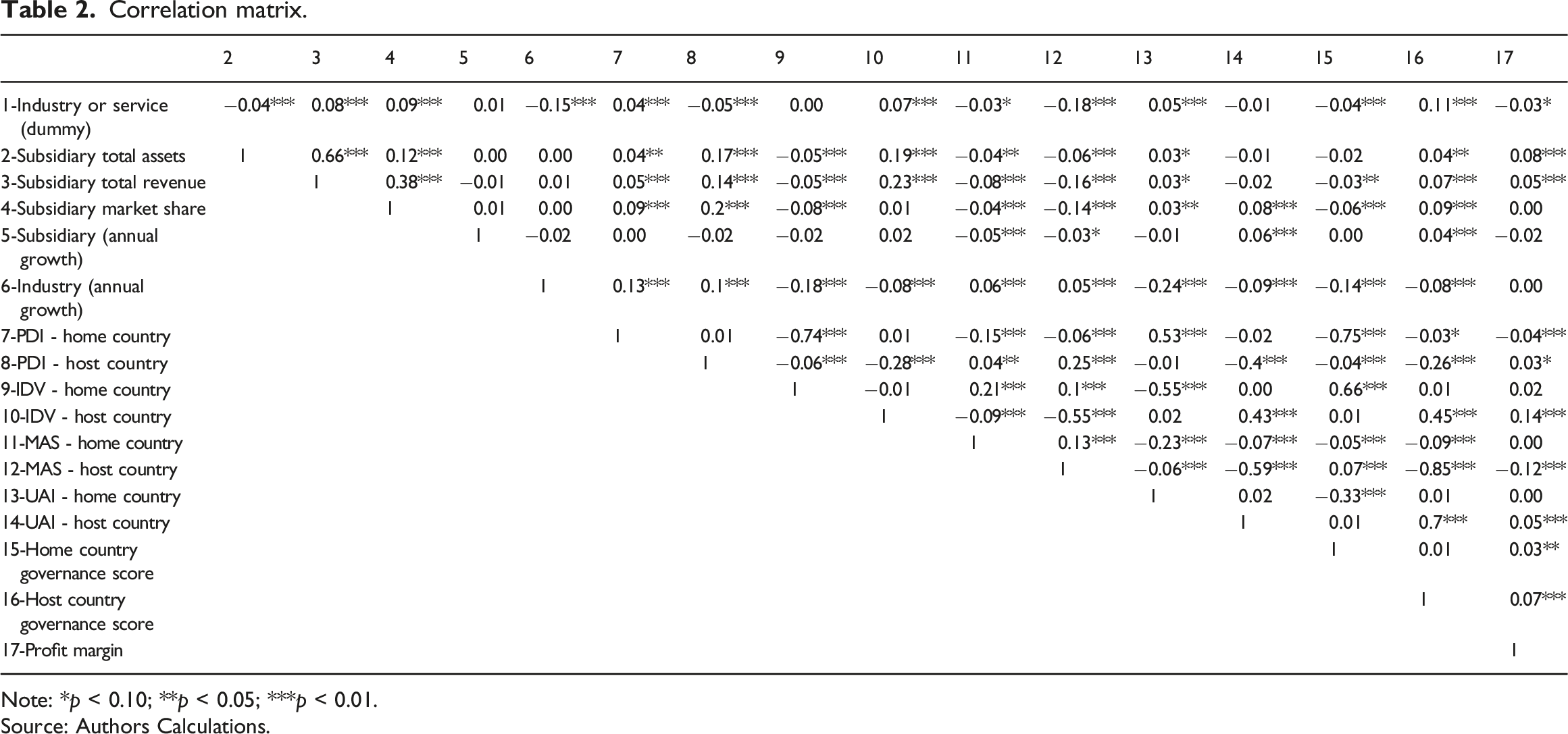

Correlation matrix.

Note: *p < 0.10; **p < 0.05; ***p < 0.01.

Source: Authors Calculations.

Main results

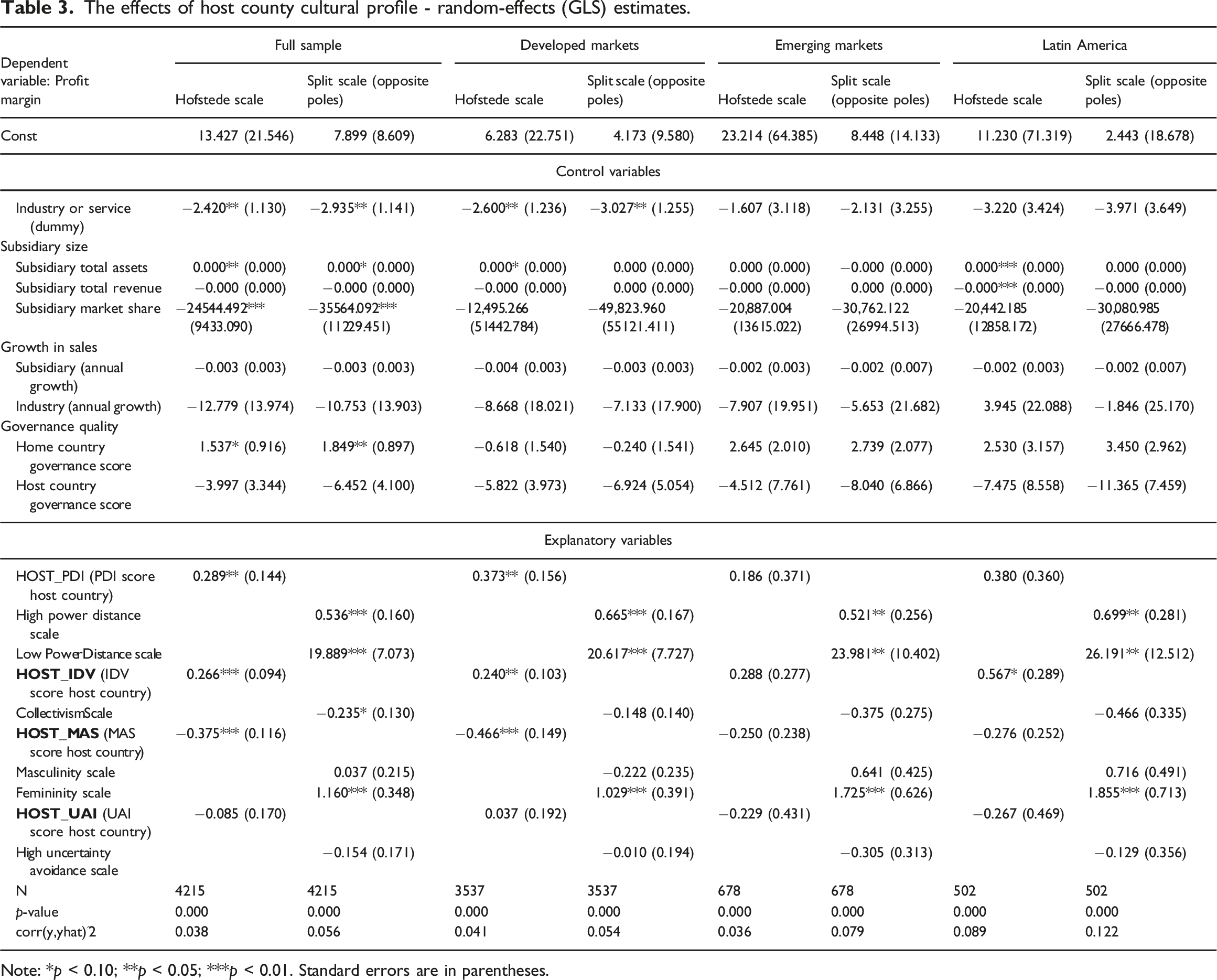

The effects of host county cultural profile - random-effects (GLS) estimates.

Note: *p < 0.10; **p < 0.05; ***p < 0.01. Standard errors are in parentheses.

The results show the increase in the explanatory capacity of the models when the effects of the cultural profiles are measured using split scales – separate variables for the opposite poles of the cultural dimensions. The quality of governance in the home country is positively associated with the performance of foreign subsidiaries from a developed country. In contrast, the quality of governance in the host countries in Latin America, measured as the arithmetic means of the six WGI variables, does not significantly affect foreign subsidiaries’ financial performance. These results alleviate the concerns of confounding the effects of IDV and PDI dimensions with the support characteristics of formal institutions in the host country.

Analysis of main results and discussion

PDI dimension of the host country profile

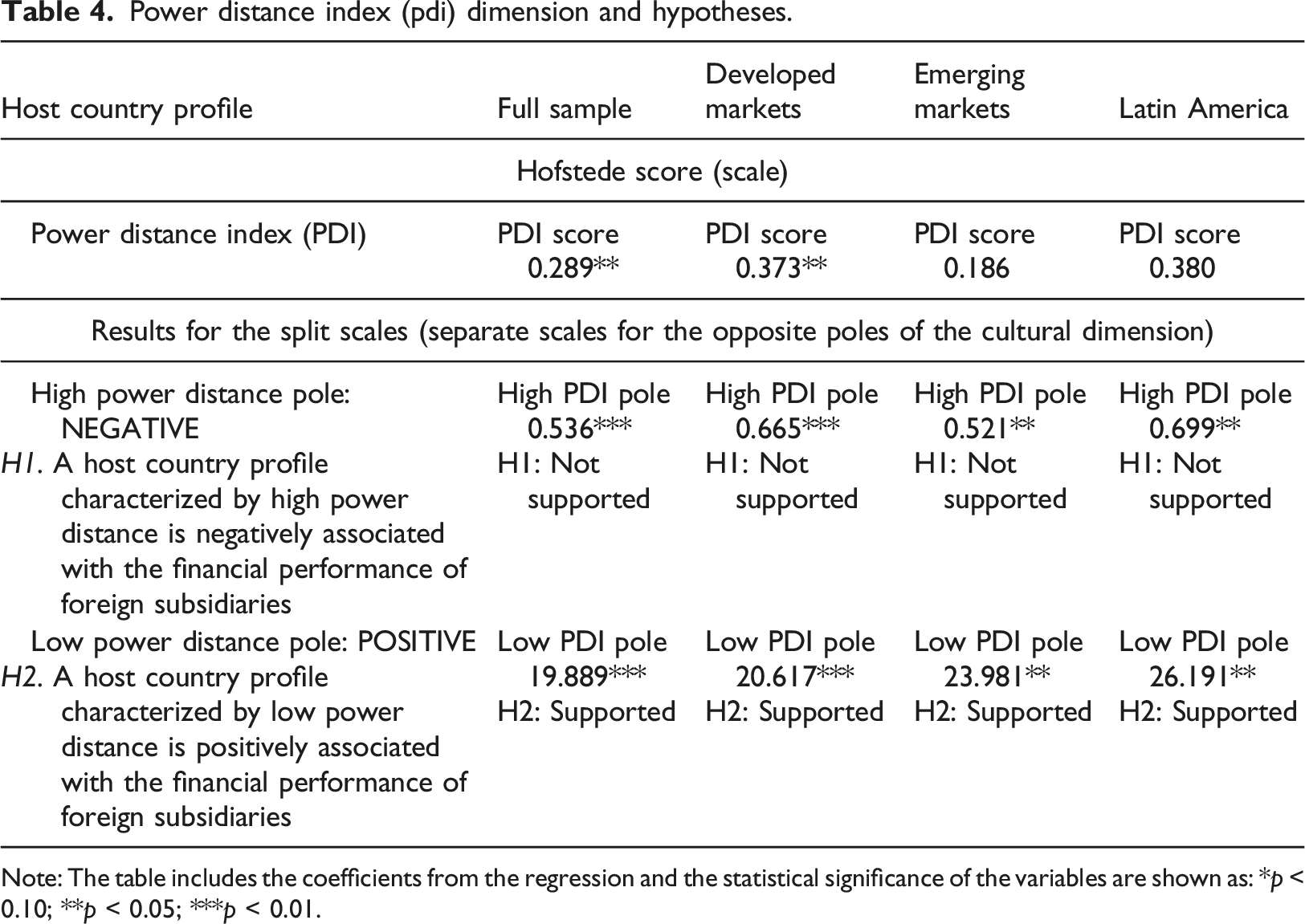

Power distance index (pdi) dimension and hypotheses.

Note: The table includes the coefficients from the regression and the statistical significance of the variables are shown as: *p < 0.10; **p < 0.05; ***p < 0.01.

The results in Table 4 reveal a positive association between Hofstede's PDI score in the host country and the financial performance of firms included in the full sample and the subsample, including foreign subsidiaries from developed countries only. Moreover, the results for the split scale reveal that, contrary to H1, the financial performance of foreign subsidiary firms is positively associated with high PDI scores in the host countries in Latin America. Regarding Hypothesis H2, the findings support the hypothesis, as we detect a positive effect for the split scale measuring low PDI scores. These results provide novel insights into the implications of the PDI dimensions on the financial performance of foreign subsidiary firms – foreign subsidiary firms can positively accommodate high and low PDI scores in the host country. As the positive effects increase towards the opposite ends of the PDI scale (i.e., high and low PDI scores), we conclude that firms can adjust by employing the proper management style when operating in host countries with clear PDI characteristics.

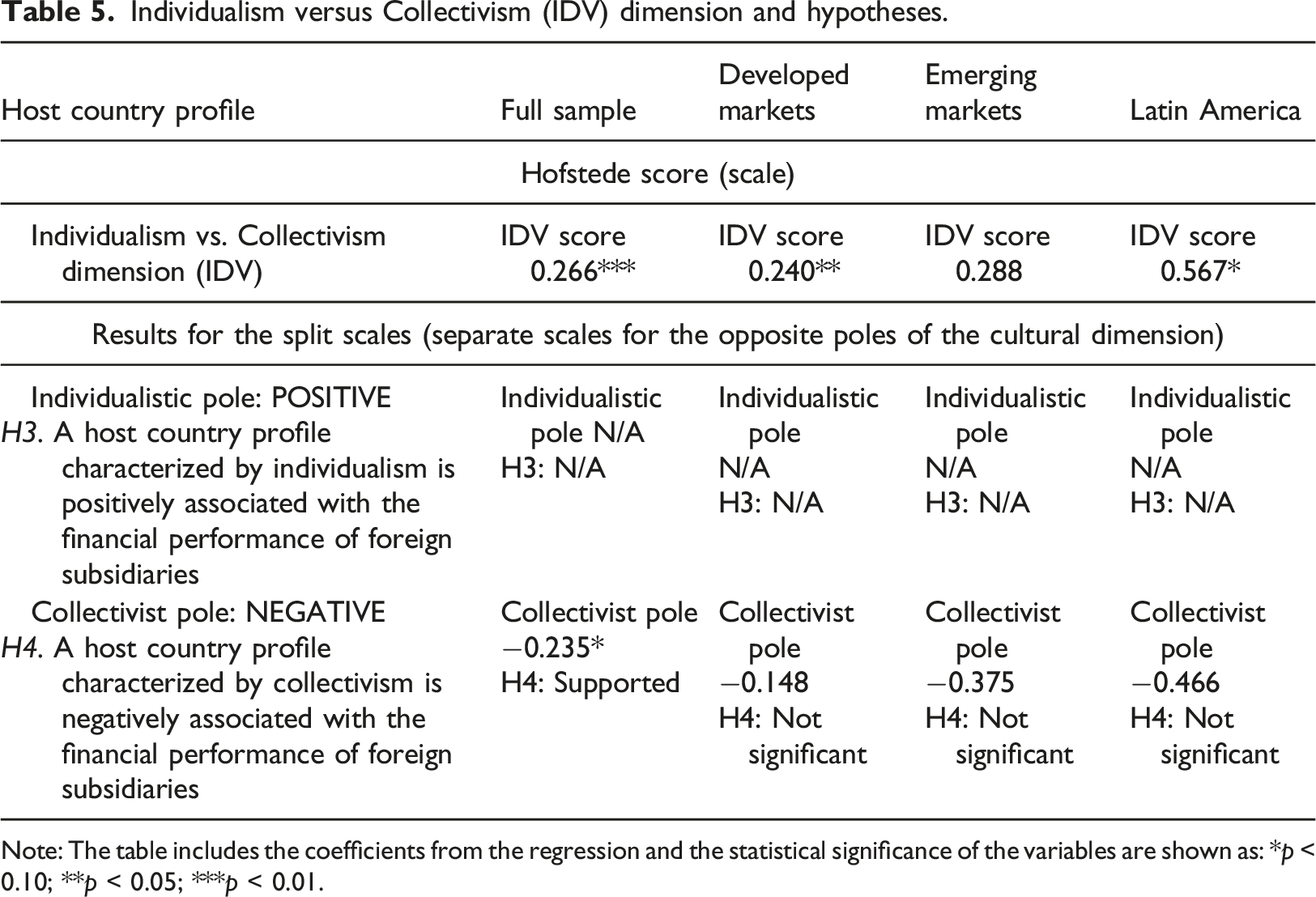

IDV dimension of the host country profile

Individualism versus Collectivism (IDV) dimension and hypotheses.

Note: The table includes the coefficients from the regression and the statistical significance of the variables are shown as: *p < 0.10; **p < 0.05; ***p < 0.01.

The results estimating the impacts for the IDV dimension of the host country profile measured according to Hofstede's IDV scale support Hypothesis H3 by the positive and significant effect on financial performance. Hofstede (2011) notes that Latin American countries are collectivist; therefore, the results for the split scale associated with individualistic host countries’ profiles could not be estimated (Table 5).

Regarding Hypothesis H4, there is a negative and significant effect for the sample, including all firms, supporting the hypothesis. Although nonsignificant, the coefficients for the collectivist pole are negative for all the subsamples. Combining the Hofstede IDV scale (positive and significant effect) with the collectivist pole results (negative effect) indicate that financial performance is positively associated with individualistic host countries and negatively associated with collectivist host countries.

MAS dimension of the host country profile

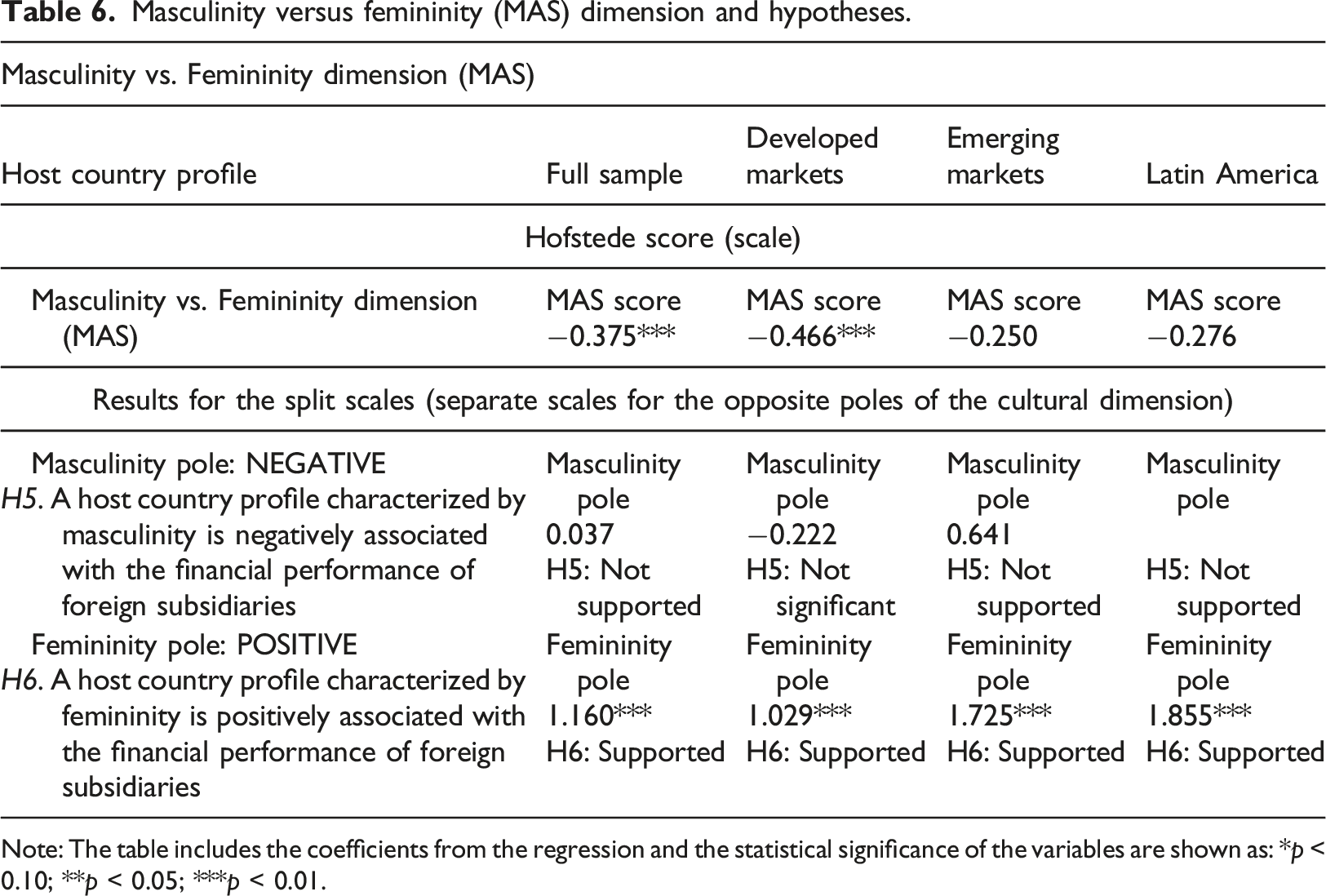

Masculinity versus femininity (MAS) dimension and hypotheses.

Note: The table includes the coefficients from the regression and the statistical significance of the variables are shown as: *p < 0.10; **p < 0.05; ***p < 0.01.

The results in Table 6 partially support Hypothesis H5. The negative effects of Hofstede’s MAS scale in the samples, including all foreign subsidiaries and foreign subsidiaries from developed countries, indicate that financial performance tends to decrease in more masculine host countries. Moreover, the results support Hypothesis H6, given that foreign subsidiaries' financial performance increases when operating in feminine host countries in Latin America. Across all sub-samples, the positive and significant impact of the feminine pole of the cultural dimensions reveals that the higher the degree of femininity in the host country, the higher the financial performance of foreign subsidiary firms. These results indicate that it is easier for foreign subsidiaries to adjust in more feminine host countries. In contrast, the impact on performance in host countries with more masculine cultures is negative.

UAI dimension of the host country profile

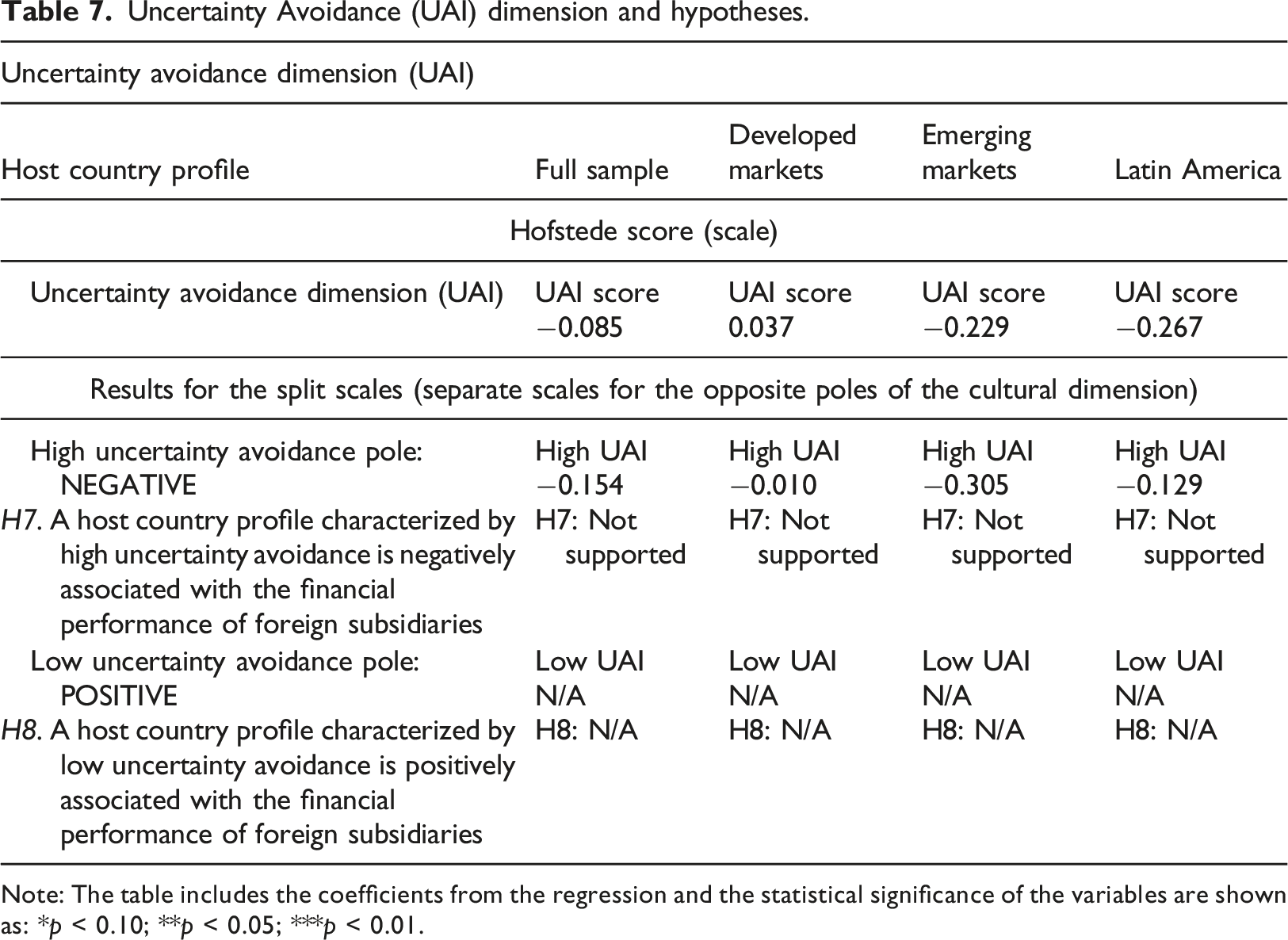

Uncertainty Avoidance (UAI) dimension and hypotheses.

Note: The table includes the coefficients from the regression and the statistical significance of the variables are shown as: *p < 0.10; **p < 0.05; ***p < 0.01.

The results for the UAI dimension of the host country profile do not support Hypothesis H7 (Table 7). Furthermore, Hypothesis H8, which tests the implications of low UAI host countries' profiles, cannot be verified, as the host countries in Latin America included in this study scored higher than 50 in UAI.

Conclusion

Contributions to literature and theory

When discussing the impact of national culture on the decisions and outcomes of internationalization, most studies focus on the impact of cultural distance (CD). By following the assumption that cultures cannot be compared as better or worse (Cuervo-Cazurra and Genc, 2011), studies tend to emphasize the liability effects of CD (Beugelsdijk et al., 2018b). This study contributes to the distance-profile conflation debate by showing that the impact of certain cultural traits on the financial performance of foreign subsidiary firms can be more positive or negative. For instance, the results reveal that host country profiles characterized by collectivism and masculinity harm financial performance. Furthermore, concerning power distance, findings show that the financial performance of foreign subsidiary firms is positively associated with high and low PDI scores in the host country. These results indicate that the financial performance of foreign subsidiary firms tends to increase when the cultural profile in the host country is clearly defined as either high of low power distance. These results are consistent across all subsamples, indicating that regardless of the cultural characteristics of the home country and higher or lower cultural distance, the effects for the PDI dimension of the host country’s cultural profile are the same. The results show that the host country profile has no significant impact regarding the uncertainty avoidance dimension. Thus, for this dimension of culture, CD might provide a better assessment when evaluating how this dimension affects the performance of foreign subsidiaries.

While cultures cannot be compared in terms of better or worse, certain cultural characteristics can have more positive or negative effects on the financial performance of foreign subsidiary firms. We found evidence that some cultural traits in the host country are positively associated with foreign subsidiary performance. In contrast, some other cultural characteristics can have a negative or no impact at all. These findings suggest that the ability of foreign subsidiaries to adjust to the cultural profile of the host country depends not only on the cultural similarities between home and host countries (i.e. the size of the distance) but also on internal and external factors. Thus, the internationalization trajectory, experience, and context of the host country, including colonial ties and other important factors, can help explain the different effects experienced by foreign subsidiaries from developed countries and emerging markets.

This study contributes to disentangling the distance-profile conflation (Bae and Salomon, 2010; Beugelsdijk et al., 2015; Franke and Richey, 2010; Van Hoorn and Maseland, 2016) and provides a more parsimonious explanation to previous studies that have argued that the majority of CD studies are potentially wrong (Brouthers et al. 2016). By highlighting the specific effects of the host cultural profile, we propose that CD studies that focus on a single host country are biased towards the specific effects that relate to the overall cultural traits of the host country's environment. The specific effects of different cultural profiles in the host country help explain the asymmetric effects of CD identified in the IB literature (; Correa da Cunha, 2019; Correa da Cunha et al. 2022; Magnani et al., 2018; Selmer et al., 2007).

Practical implications

A few practical implications can be highlighted. Being aware of how the host country’s cultural profile impacts foreign subsidiary firms' financial performance can help identify the best approach to entering a foreign country. In masculine host countries, foreign firms must be aware that people tend to be assertive, tough, and focused on material success (Hofstede, 1994, p. 82). On collectivist host countries, “individuals may be induced to subordinate their personal goals to the goals of some collective, which is usually a stable ingroup (e.g., family, band, tribe), and much of the behaviour of individuals may concern goals that are consistent with the goals of this ingroup” (Triandis et al.,1988, p. 324). In collectivist societies, conflict management is much more complicated as it involves more subtle negotiation of in-group/out-group face-related issues – pride, honour, dignity, insult, shame, disgrace, humility, trust, mistrust, respect, and prestige – in a given conflict episode. Foreigners, being considered out-groups, may face costly sanctions for non-conforming to the expectations of local in-groups (Triandis et al., 1988). Forming alliances that can facilitate acceptance and legitimacy in the foreign country can be a critical factor for the success of the foreign firm.

While Hofstede’s (1980) framework classifies Latin American countries as collectivist societies, House et al. (1999) provide a more nuanced view by making the distinction between ingroup (family issues) and institutional (public benefits) collectivism. By adopting this approach and focusing on cultural practices (culture “as is”), (House et al. 2004), Salgado (2004) points out that Latin America is characterized by high family collectivism joined with high social individualism. Data from the Global Leadership on Organization Behavior Effectiveness (GLOBE) show that the average for cultural practices for the ingroup collectivism in Latin America is 5.52, higher than the world average of 5.10. On the other hand, in terms of Institutional Collectivism, the Latin American average is 3.86, which is lower than the global average of 4.24. For example, Colombia ranks 10th place in family collectivism but in 52nd place in social collectivism among the 61 countries in the GLOBE project (Salgado, 2004). According to the same author, “while Colombians belong to a collectivist culture (Hofstede, 1984), . . . their in-groups are limited to family and perhaps close friends (Fitch, 1998; Ogliastri et al., 1999; Salgado, 2004, p. 10) This distinction helps to explain the negative impact found for the collectivist pole of the cultural profile of countries in Latin America as foreign subsidiaries are likely to be perceived as out-groups in this context.

Regarding the power distance dimension, findings reveal that performance tends to increase in host countries with high or low scores in this dimension of national culture. These results indicate that firms can adjust more positively when the cultural profile in the host country can be clearly defined as either low or high power distance. While Hofstede separates Individualism and Power Distance in two distinct dimensions, Triandis (1995) provides four categories combining elements of the power distance (horizontal vs vertical) with the collectivism versus individualism dimensions with different behavioral and social effects: horizontal collectivism (HC), vertical collectivism (VC), horizontal individualism (HI), and vertical individualism (VI). Salgado (2004: 8) notes that in “collectivist cultures, horizontality (low power distance in Hofstede’s terminology, 1984) establishes a feeling of oneness with the ingroup, whereas verticality (high power distance) establishes a sense of serving others within the ingroup. In individualistic cultures, horizontality establishes equality, whereas verticality establishes the need to stand out in the crowd. Vertical individualists are the most likely to be prejudiced and to discriminate, while horizontal individualists are the least likely”. In that sense, while we analyse the effects of each pole of the cultural dimensions separately, the degree of power distance will likely moderate the effects of the individualism versus collectivism dimension.

Finally, in regards to the uncertainty avoidance dimension, although results suggest that the effects associated with the host country profile are not significant, the implications of this cultural dimension might be better represented by the cultural distance between the home and host countries. Therefore, in addition to considering the cultural distance between the home and the host country, firms must consider the cultural characteristics of the host country's cultural profile.

Limitations and direction for future research

This study presents significant prospects for future research to advance the crucial discourse concerning the impact of the host country’s cultural profile on the performance of foreign subsidiary firms. It is worth noting that the specific cultural traits, historical factors, and traditions unique to the Latin American context may limit our findings. Consequently, conducting further research in diverse countries and regions would bolster the robustness of our findings and enhance our conclusions’ validity. Furthermore, future studies can make notable strides by exploring the simultaneous and combined effects of various dimensions of culture.

Although this study controls for the quality of governance in the host country when testing the implications of the cultural profile, future research can investigate how the strength of formal institutions in the host country could moderate the effects of the cultural profile on the financial performance of foreign subsidiary firms.

By employing alternative frameworks, such as in-group versus institutional collectivism, as proposed by House et al. (1999), researchers can gain a more nuanced understanding of the cultural characteristics prevalent in Latin America. Moreover, exploring the interactions between various cultural dimensions, such as vertical versus horizontal individualism and collectivism, holds significant potential for advancing our knowledge regarding the influence of the host country’s cultural profile on the performance of foreign subsidiary firms. Future research endeavors incorporating these approaches can deepen our comprehension of the intricate relationships between culture and firm performance, ultimately advancing scholarly knowledge. Moreover, further studies could focus on how cultural distance can moderate the effects of the host country’s cultural profile on the financial performance of foreign subsidiaries from developed and emerging markets in different and specific ways. Due to the distinct characteristics of industrial and service firms, future insights can advance the knowledge of how culture affects firms in various sectors. Furthermore, future research could focus on specific dimensions of national culture using Hofstede and other frameworks to deepen our understanding of the conditions under which host country profiles and CD can have different effects on the performance of foreign subsidiary firms.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.