Abstract

Central and Eastern European (CEE) countries have ratified the United Nations Convention on the Rights of Persons with Disability, necessitating adjustments in tax and benefit policies. However, the eventual outcome of these modifications remains uncertain. To evaluate possible changes, we conducted a comparative analysis of current instruments in CEE countries vis-a-vis Sweden, Denmark, and Finland. Our research discovered that tax and benefit systems in both CEE and Scandinavian countries are built on the same foundational principles, yet differ significantly in their specific solutions and approaches. Notably, benefits systems in CEE countries are considerably more intricate and inclined toward means-tested benefits and specialized instruments dedicated solely to individuals with disabilities. We posit that changes arising from the convention’s implementation will streamline the benefits system, incorporating more generalized instruments with disability added as supplementary eligibility conditions or income parameters. The velocity of this transformation will be influenced by the pace of economic growth, as evidenced by the strong positive correlation between disability expenditure’s proportion in gross domestic product and the European Union countries’ level of economic development.

Introduction

Disability is a complex and multifaceted issue that affects individuals, families, and society as a whole. According to recent data, disability is prevalent across Europe and is often linked to poorer economic outcomes, with those with disabilities being more likely to experience poverty and social exclusion. However, there are significant differences in disability prevalence and outcomes between countries, with some countries faring better than others. The Rawlsian principles of justice as fairness, including the principle of the second difference, highlight the need to address the disadvantages faced by those with disabilities and ensure that policies are structured to improve the lives of the least advantaged members of society (Wolff, 2009). Moreover, recent developments, such as the adoption of the Convention on the Rights of Persons with Disabilities (CRPDs), have the potential to transform policies from a medical model to a social model more consistent with human rights. This article seeks to examine how current social protection policies address disability in Europe, and the implications for reform in light of these recent developments.

According to statistical data from 2012, the average percentage of individuals aged 15 and above with medical disability certificates in the European Union (EU) was 17.5%, with Hungary reporting the highest percentage at 24.6% and France the lowest at 13.7%. However, in 2021, 17.6% of individuals in the EU-27 reported experiencing long-standing limitations in usual activities due to health problems, revealing that the prevalence of disability varies across countries and over time. Interestingly, countries with varying degrees of economic development exhibit similar values, which can be attributed to the different definitions of disability employed in different nations. In particular, more developed countries with robust benefit systems for people with disabilities tend to have a more comprehensive and all-encompassing definition of disability. As a result, the statistical data on disability cannot be fully compared across countries due to the substantial influence of the definition utilized. This issue of incomplete comparability warrants acknowledgment as we explore institutional differences (Grönvik, 2009). Notably, Finland and Denmark have comparable disability rates to Latvia and Lithuania, with rates ranging from 25% to 30%, placing them among the countries with the highest rates in the EU-27, while Sweden, Norway (non-EU), and Bulgaria reported the lowest percentages, with approximately 10% of the population experiencing long-standing limitations. The considerable disparity in disability rates across countries calls for further investigation into the underlying reasons, including institutional differences and variations in the definition of disability.

As of 2019, individuals in the EU aged 16 or over with a disability were at a higher risk of poverty or social exclusion, with a rate of 28.4%, compared with 18.4% of those with no activity limitation. Bulgaria, Latvia, Estonia, and Lithuania were identified as having the highest proportion of individuals with disabilities at risk of poverty or social exclusion, while post-socialistic Central and Eastern European (CEE) countries, such as Slovakia, Czechia, Hungary, and Poland, had rates below the EU average. The relative differences in at-risk-of-poverty or social exclusion rate (AROPE) and severe material deprivation rate (DEP) between individuals with some or severe activity limitation and those without revealed greater disparities in CEE countries than the EU average (European Commission, 2021).

While there may be disagreement over specific statistics and subjective data, it is indisputable that individuals with disabilities, whether formally recognized or not, comprise a significant portion of every European country, and their standard of living is often precarious. In particular, those residing in CEE countries face significant challenges as they lack robust social representation capable of influencing policymakers. The ratification of the CRPDs by all CEE countries is of great significance in this context, as it obligates policymakers to adopt a social model as a guiding principle when making regulatory decisions. This commitment also grants the social side the right to demand that these obligations be upheld.

The implementation of the CRPDs will necessitate a shift in the tools employed in social policy for individuals with disabilities. Current instruments, which are often grounded in the medical model and emphasize direct income support and cash transfers, will need to be reconfigured to prioritize services (such as assistant services) and infrastructure investments (such as the removal of architectural barriers). The adoption of policies in accordance with the CRPD will require a fundamental alteration of the existing system of tax and benefit instruments that reflect the medical model.

The necessity for potentially transformative changes that could impact the disposable income of many households presents a potential barrier to the adoption of a social model framework in social policy for individuals with disabilities. Differences in existing tax and benefit instruments between countries could pose a significant obstacle to implementing the necessary changes. To assess the viability of such changes, a comparison is made between the systems in CEE countries and those in Denmark, Sweden, and Finland, which are considered potential indicators of the direction of change. While the Scandinavian countries are diverse, they provide insights into the path forward.

Our analysis reveals that the general methods of income redistribution in support of individuals with disabilities are similar in both CEE and Scandinavian countries. Consequently, the required changes do not necessitate a complete overhaul of the existing tax and benefit systems, thus simplifying the process. However, significant modifications to individual solutions employed in CEE countries will be required, potentially provoking resistance from current beneficiaries and slowing down the transition. Although changes in tax and benefits should not pose a significant obstacle per se, the status quo may persist for some time. The social model requires substantial investments in infrastructure, and as our findings indicate, the level of economic development has a bearing on disability-related expenditures. Therefore, it is plausible that tax and benefit systems in CEE countries may remain unaltered for the foreseeable future, with income redistribution continuing to play a crucial role in disability policy.

Disability system versus economic development

The convention sets standards for the rights of people with disabilities in the EU. This entails shifting from a medical to a social perspective on disability that sees it as ‘long-term physical, mental, intellectual or sensory impairments which in interaction with various barriers may hinder [a person’s] full and effective participation in society on an equal basis with others’ (White et al., 2018). The social model sees disabilities as restrictions imposed by society distinguishing between ‘functional limitations or impairments’ of a person and ‘physical and social barriers’ that create ‘disabling environments or barriers’. The impending paradigm shift demands a fundamental reorientation of the approach to disability assessment. The assessment system’s significance is most effectively demonstrated in a comprehensive study commissioned by the Academic Network of European Disability Experts (ANED) in 2017. In their report, Waddington et al. (2018) highlight the existence of a diverse range of medical and context-based disability assessment methods, which individual countries combine in various ways, resulting in even greater diversity of approaches. Notably, the CRPD does not offer explicit guidance on how to assess disability, providing countries with significant freedom to introduce customized practical solutions. However, this lack of guidance may not align with the social model of disability underlying the CRPD, as exemplified in the case of disability assessments determining capacity for work. Priestley’s (2022) analysis of the minimum impairment required for eligibility to assistance reveals a broad range, from 20% (Malta) to 66.6% (Portugal and France), and the required level of total incapacity for work varies from 70% (Slovakia and Hungary) to 100% (Sweden, Spain, the Netherlands, Romania, Slovenia, and Portugal). Furthermore, the methods and assumptions used to determine these percentage values differ significantly and are not directly comparable. Given the issue’s importance, this article focuses solely on the benefits’ side of the tax and benefit system, and does not delve into this topic further.

The medical and social models of disability differ fundamentally in their basic assumptions, suggesting that tax and benefits solutions should also differ between the two models. While both models recognize that impairments decrease an individual’s resources and limit their ability to engage in typical activities, they recommend different policy responses. Although they agree that the additional costs associated with employing people with disabilities cannot be fully covered by the employee or employer, they do not apply the same resource allocation principles used in other policy domains (Bonaccio et al., 2020: 147). Instead, public intervention in disability policy is based on the principle of solidarity, which holds that the state has a responsibility to protect citizens from poverty resulting from exogenous determinants, such as disability (Maggini et al., 2021; Milne and Gibb, 2016). Both models endorse social transfers to cover expenses related to rehabilitation, assistive devices, personal support, and increased spending on services like transportation and general health care (Antón et al., 2016; Zachary and Zaidi, 2020). However, differences may arise in approaches to labor market-oriented benefits and the extent of income redistribution, which are more crucial in medical model-based policies.

The adoption of the social model necessitates alterations in taxes and benefits. Surprisingly, this aspect has not received much attention in the literature. The social model has been discussed from various perspectives, such as the legal dimension (Bunbury, 2019; Holler and Ohayon, 2022; Hurst, 2005) and the ethical and philosophical angle (Ralston and Ho, 2010). However, to our knowledge, there has been little exploration of the implications for tax and benefit systems (Côte, 2021)(Côte, 2021). This is remarkable given that tax and benefit instruments are crucial tools in current disability policy (Banks et al., 2017; Inclusion, 2020; Pinilla-Roncancio and Sabina Alkire, 2021: 206; Mitra et al., 2023; OECD, 2010: 77–97). A report published by the Organization for Economic Cooperation and Development (OECD) in 2010, which drew upon data available up to 2007, elucidated a broad range of measures employed by various countries with their relatively unsatisfactory impact on ultimate outcomes. From 1990 to 2007, all countries examined in the report exhibited an escalation in integration measures at the expense of compensation solutions. While this led to a certain degree of legislative convergence among countries, it was observed to be relatively modest in scale. Furthermore, it was recognized that the divergence in legislation is distinct from the diversity in its actual implementation. The authors of the report also caution that a mere shift in rhetoric and policy does not automatically translate into tangible changes in the day-to-day practices of health care professionals, legal caregivers, and service providers for individuals with disabilities. The report explicitly emphasizes that alterations in legislation must be accompanied by the necessary allocation of resources and modifications in the financial incentives of the principal stakeholders.

A disability policy is a product of a multifaceted and long-term process that is shaped by economic, social, and political factors. The emergence of disability rights activism since the 1970s has played a crucial role in the development of policy, but the implementation of regulations has also been influenced by broader considerations of welfare policy and prevailing economic conditions. While the Scandinavian model is often cited as a successful example, it cannot be readily replicated in other countries due to the unique historical and political contexts in which disability policies were developed. In CEE countries, disability policies were primarily the result of political decisions rather than social pressure or agreement. These differences in the regulatory processes reflect the varying roles of different social actors. It is important to acknowledge that disability policy has evolved within a complex social and economic landscape (Beatty and Fothergill, 2015; Priestley, 2007; Tschanz and Staub, 2016).

Despite differences in the way how current systems have been designed, disability-related expenses account for a significant part of total social protection benefits among EU countries in 2019. In 2019, the average total spending among the EU countries was 7.6%. It ranged from 16.2% in Denmark to 3.7% in Malta. Poland, the Czech Republic, and Hungary spent less than 6.5%, and Bulgaria, Slovakia, Latvia, and Lithuania spent between 8.3% and 8.7%. The share of 11.6% in Estonia was exceptionally high among the CEE countries, and it was higher than in Sweden (9.7%) and Finland (9.6%). 1 According to the COFOG (Classification of the Functions of Government), in 2020, Norway spent 7.7% of its gross domestic product (GDP) on ‘Sickness and disability’, while Cyprus spent 0.5%. Surprisingly, Lithuania – 4.7% – and Slovakia – 3.9% – are among the EU countries with the highest spending. Spending by Lithuania is comparable with Denmark (4.6%) and the Netherlands (4.3%), while Slovakia is comparable with Belgium, Luxembourg, and Sweden. Disability – 2.4% – despite relatively large disability-related expenditure for social protection. Its level was the same as in Slovenia, Hungary, and Poland. 2 All these countries spent more than Italy (2.0%) and Austria (1.9%).

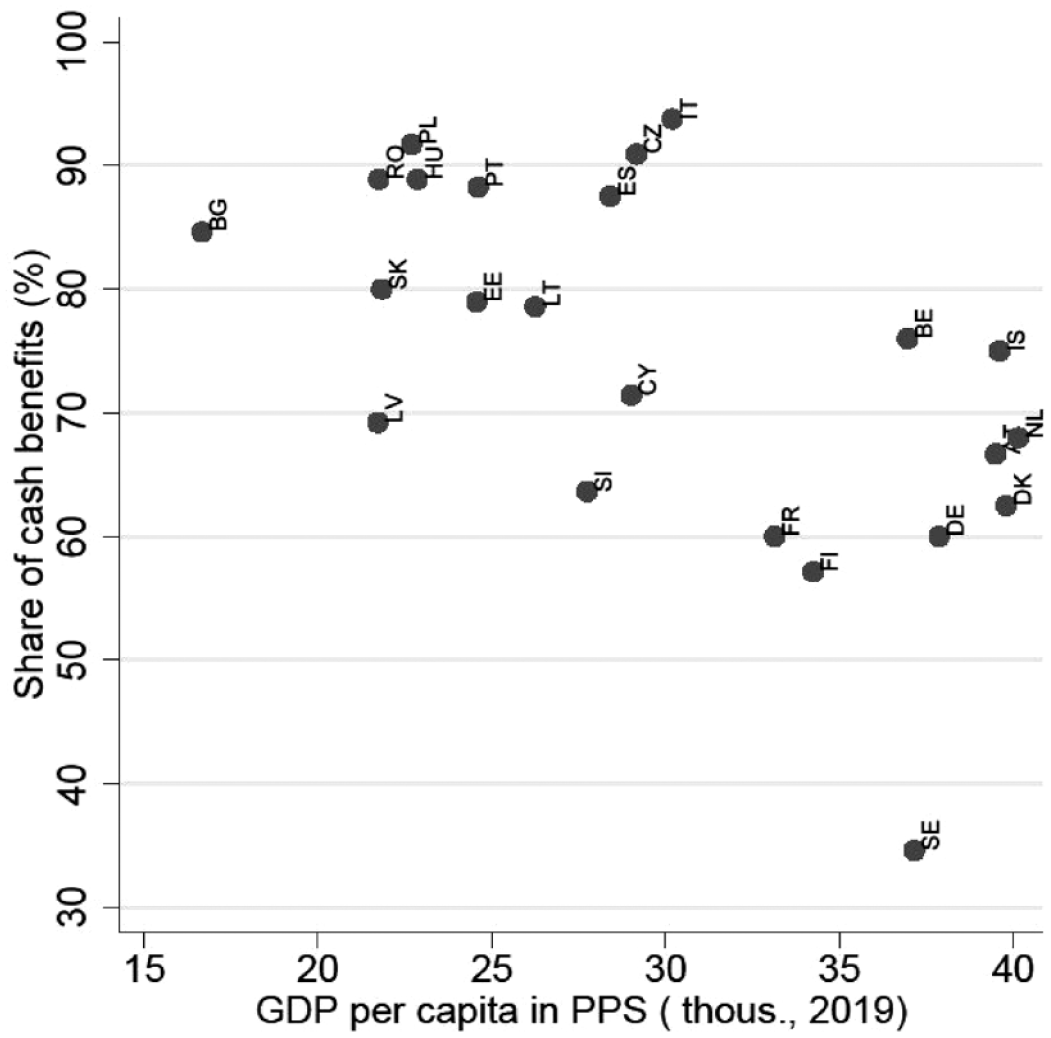

Such statistics show how difficult it is to discuss disability expenditure across countries. The results for some countries may be surprising and unintuitive, but both sources – ESSPROS and COFOG – indicate higher expenditure in more economically developed countries. In the article, we study cash benefits. They constitute a big part of disability expenditures related to social protection in all EU countries except Sweden, which spent more on benefits in kind than other countries (Figure 1). 3 Sweden spent 30% on cash benefits, Finland spent almost 60%, and Denmark spent over 60%. Poland, Hungary, Czechia, and Romania had the largest shares of cash benefits, accounting for approximately 90% of total disability expenditure. All CEE countries had shares close to or above 80%, except for Latvia, with a 70% share.

Cash benefits in disability expenditure and economic development level (%, 2019).

A common policy recommendation of the medical model is to provide labor replacement benefits for caregivers and compensation income for disabled individuals who are unable to work. Under this model, a person’s quality of life is often heavily reliant on the assistance of a caregiver in overcoming barriers in their daily lives. In CEE countries, the proportion of cash benefits is higher than in other regions, which suggests that these countries are more aligned with the medical model.

Disability systems in the selected EU countries

We compare benefits related to disability in selected EU countries using the European Commission’s website on employment, social affairs, and inclusion, documents describing the OECD TaxBEN model, 4 and country reports accompanying the European Commission tax and benefit model EUROMOD. 5 The instruments are distinguished from contributory or non-contributory and means-tested or non-means-tested. In addition, we distinguish instruments payable only in the case of disability from those also available in other situations. Transfers paid only in the case of disability are called specific.

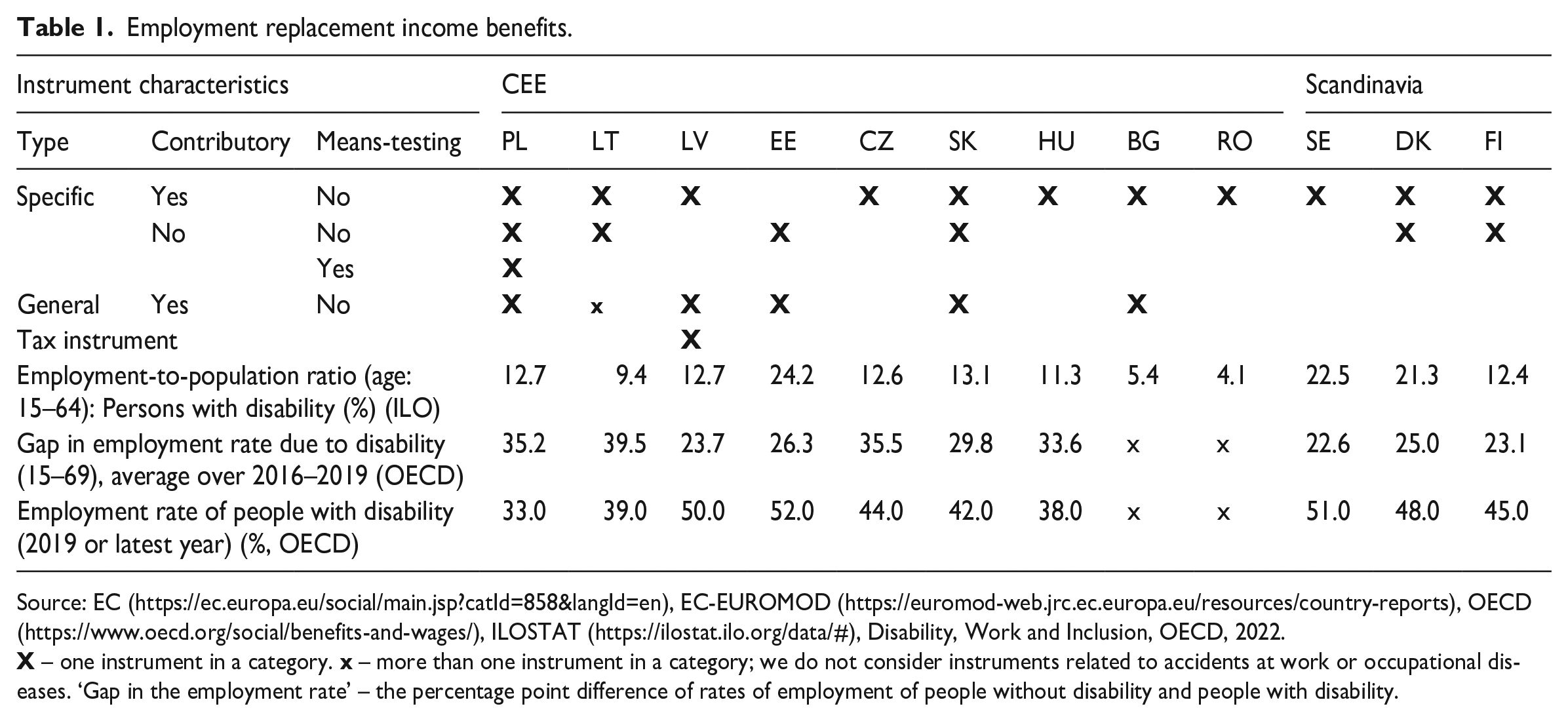

Table 1 describes employment replacement income benefits. Contributory and non-means-tested invalidity/disability pension benefits are the most widely used instruments (Scharle and Csillag, 2016: 6). They are paid to people who have contributed to the social security system and who have lost their ability to work because of health problems. The benefits are specific since eligibility requires a disability certificate. The details of solutions vary across countries, but the instruments have a similar purpose. 6

Employment replacement income benefits.

Source: EC (https://ec.europa.eu/social/main.jsp?catId=858&langId=en), EC-EUROMOD (https://euromod-web.jrc.ec.europa.eu/resources/country-reports), OECD (https://www.oecd.org/social/benefits-and-wages/), ILOSTAT (https://ilostat.ilo.org/data/#), Disability, Work and Inclusion, OECD, 2022.

Non-means-tested benefits, which are typically general and contributory, serve as replacement income instruments frequently used in CEE countries. Such benefits may include pensions paid to the relatives of a deceased person, often to a child or widow. Among the eligibility criteria for these benefits in CEE countries, disability is explicitly mentioned. Meanwhile, in Sweden and Denmark, such benefits are also available, but there is no requirement related to disability in their descriptions.

It is worth noting that labor replacement income is also provided through specific, non-contributory, and non-means-tested benefits in various countries. These benefits are typically paid to individuals whose disability began before reaching adulthood or to their caregivers. For instance, in Poland, there is a social pension, in Slovakia an invalidity pension, in Estonia a workability allowance, in Denmark a carer’s allowance, and in Finland a care pay. However, it should be noted that some of these benefits have certain eligibility requirements. For example, in Poland, the nursing benefit, which is a benefit for caregivers, requires having no labor income, while a special attendance allowance is means-tested.

In Latvia, there is a tax allowance for unemployed, dependent spouses who are responsible for a child with disabilities. Generally, tax solutions are rarely used. At first glance, it is not surprising as we are considering people who are incapable of work or have a low working capacity. On the other hand, exogenous income transfers discourage people from the labor market through income effect and increasing reservation wages. This, combined with the regulator’s imperfect information about the true degree of disability, make arguments to consider in-work tax credit solutions. 7

Employment income replacement benefits seem to be differently organized in CEE and Scandinavian countries. Probably, this part of the tax and benefit system will require significant changes during the implementation of the social model. Public investment in a more-friendly environment will decrease fixed employment costs and facilitate access to the labor market, making work more profitable. Better access to the labor market is the argument for reforming caring and disability benefits, making the system simpler and more efficient. Such changes may help to increase labor market activity among the disabled, which is currently at a low level in CEE countries (Table 1). 8

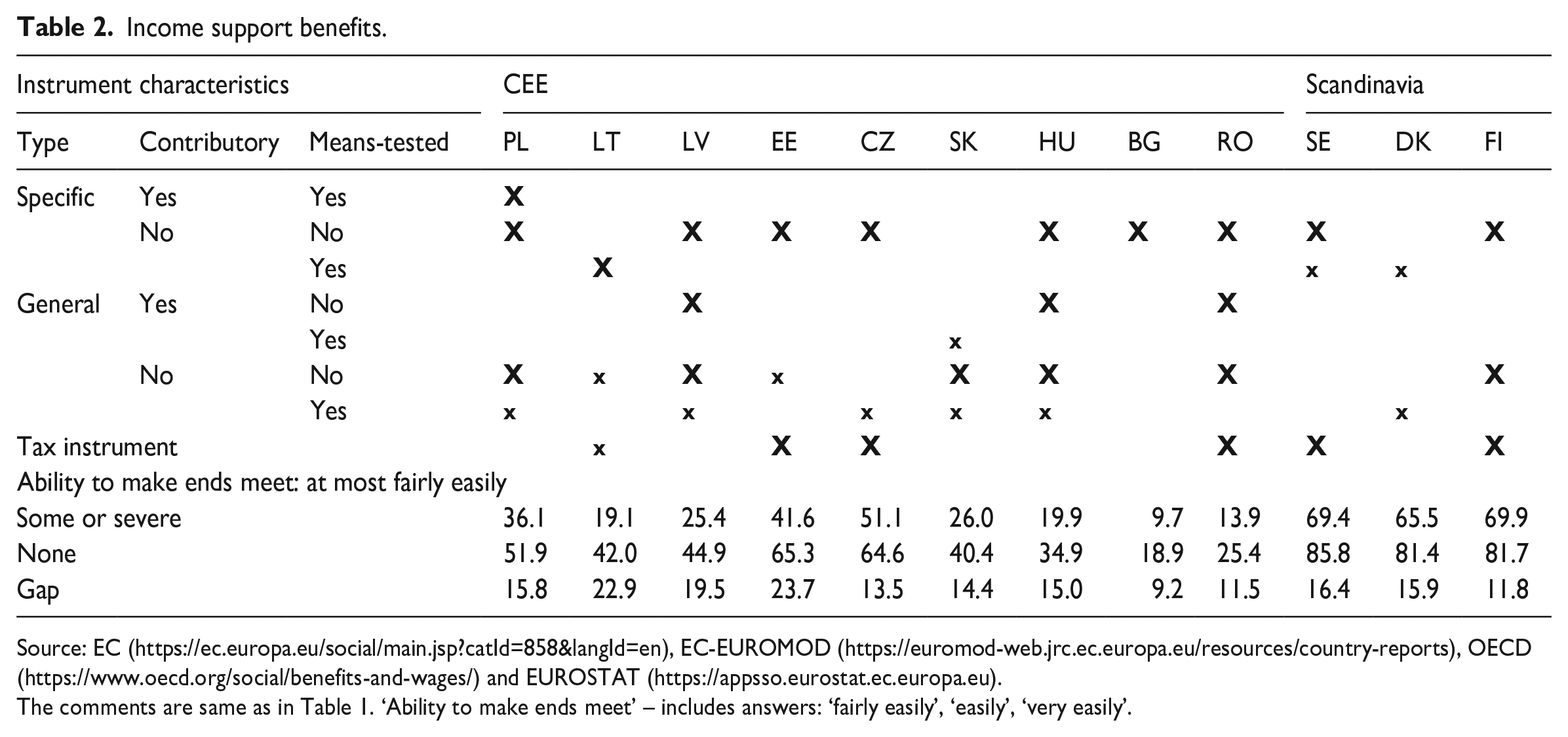

The most common instruments for income support are non-contributory and general benefits (Table 2).

Income support benefits.

Source: EC (https://ec.europa.eu/social/main.jsp?catId=858&langId=en), EC-EUROMOD (https://euromod-web.jrc.ec.europa.eu/resources/country-reports), OECD (https://www.oecd.org/social/benefits-and-wages/) and EUROSTAT (https://appsso.eurostat.ec.europa.eu).

The comments are same as in Table 1. ‘Ability to make ends meet’ – includes answers: ‘fairly easily’, ‘easily’, ‘very easily’.

Both means-tested and non-means-tested benefits are utilized in the CEE countries. Non-means-tested benefits often target specific social groups, such as children or the elderly, and may require additional conditions related to age. Many CEE countries complement their non-means-tested benefits with specific instruments. In contrast, Denmark and Sweden use fewer specific instruments and rely more on general instruments without unique solutions to counteract poverty among people with disabilities. Their systems are generally simpler than those found in CEE countries. When transitioning to a social model, income support benefits are expected to be less impacted than the labor replacement income component. It is anticipated that income support benefits will be less specific and become part of a general last-resort income support system in the future.

Another issue that needs to be taken into account is the additional costs associated with living with a disability, which are often overlooked in policy discussions. These costs can include expenses related to adaptive equipment, home modifications, and health care services, which can be substantial and lead to financial strain for individuals with disabilities and their families (Mitra et al., 2017). In addition, people with disabilities may face barriers to accessing affordable housing, transportation, and education, which can further exacerbate financial challenges (Morris and Zaidi, 2020). The neglect of these costs would engender diminished earnings potential, thereby manifesting in heightened poverty rates, exacerbated economic disparities, and compromised quality of life.

Furthermore, the extra cost of disability may increase when disabled people join the labor market. Ipek (2020) estimates the additional economic cost of disability for households in Turkey using a standard of living approach and a household budget survey data. The results show that households with disabilities need at least 9.1% more income to reach the same standard of living as those without disabled individuals, and that the cost varies depending on the type and severity of disability. Therefore, it is crucial for policymakers to consider the financial burden of disability and develop policies that address these additional costs to ensure full and equal participation in society for people with disabilities.

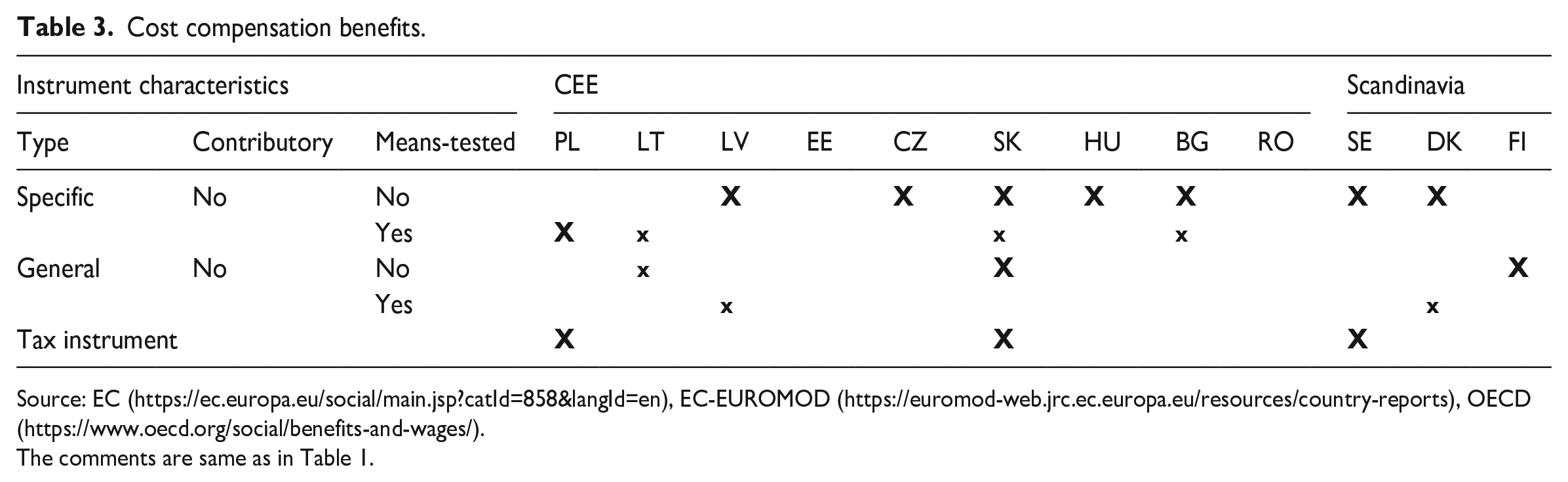

Benefits compensating for higher costs of living included in tax and benefit systems are presented in Table 3. All of them are non-contributory, and the majority of them is non-means-tested. Distinguishing whether a given income transfer should be classified as a labor income replacement, income support or cost reimbursement in many cases is not obvious. Our classification approach is based on the main reason for the transfer. Therefore, care benefits paid to a caregiver due to his or her inability to work are included in Table 1. Care benefits paid to cover the cost of care are included in Table 3. 9

Cost compensation benefits.

Source: EC (https://ec.europa.eu/social/main.jsp?catId=858&langId=en), EC-EUROMOD (https://euromod-web.jrc.ec.europa.eu/resources/country-reports), OECD (https://www.oecd.org/social/benefits-and-wages/).

The comments are same as in Table 1.

Non-means-testing is the dominant but not exclusive approach. There are specific, non-contributory, but means-tested benefits in Latvia, Slovakia, and Bulgaria. 10 In Denmark, we found a contributory and means-tested instrument (heating subsidy). Personal income tax instruments are used in Poland (medical rehabilitation expenses with tax allowance), Slovakia (the spouse tax allowance), and Sweden (disability allowance).

Introducing the social model will require modifying existing instruments and removing some of them, rather than redesigning the entire system. The role of means-testing is a particular issue arising from the review, as means-tested benefits may demotivate people to work and put higher demands on public administration compared with universal benefits. However, means-tested benefits also offer lower financing costs and address redistribution issues.

Research by Autor and Duggan (2007) and Marie and Vall Castello (2012) has shown that means-tested benefits induce a substitution effect that may financially demotivate people to work. Therefore, careful consideration of the role of means-testing is essential when designing a new disability benefits system. Can CEE countries modernize their systems right now? Can they make them less complicated based? Can they rely more on general instruments with disability requirements added as eligibility conditions and amount criteria to general benefits instead of specifically targeted transfers?

At present, income redistribution through taxes and benefits is a common practice to support people with disabilities who face barriers in generating labor income. However, the implementation of the social model could lead to a reduction in these barriers and an increase in opportunities for independent living, achieved through investments in public services and infrastructure. As a result, adjustments to taxes and benefits may be necessary to reflect changes in the external environment. To ensure effective coordination of these processes, investment in public infrastructure and services must precede changes in the tax and benefit system. Unfortunately, the initial investment requires significant financial resources, and there is often reluctance to allocate adequate funding to disability-related issues. Therefore, knowledge and financial resources are essential to advance toward an equitable and accessible society for people with disabilities.

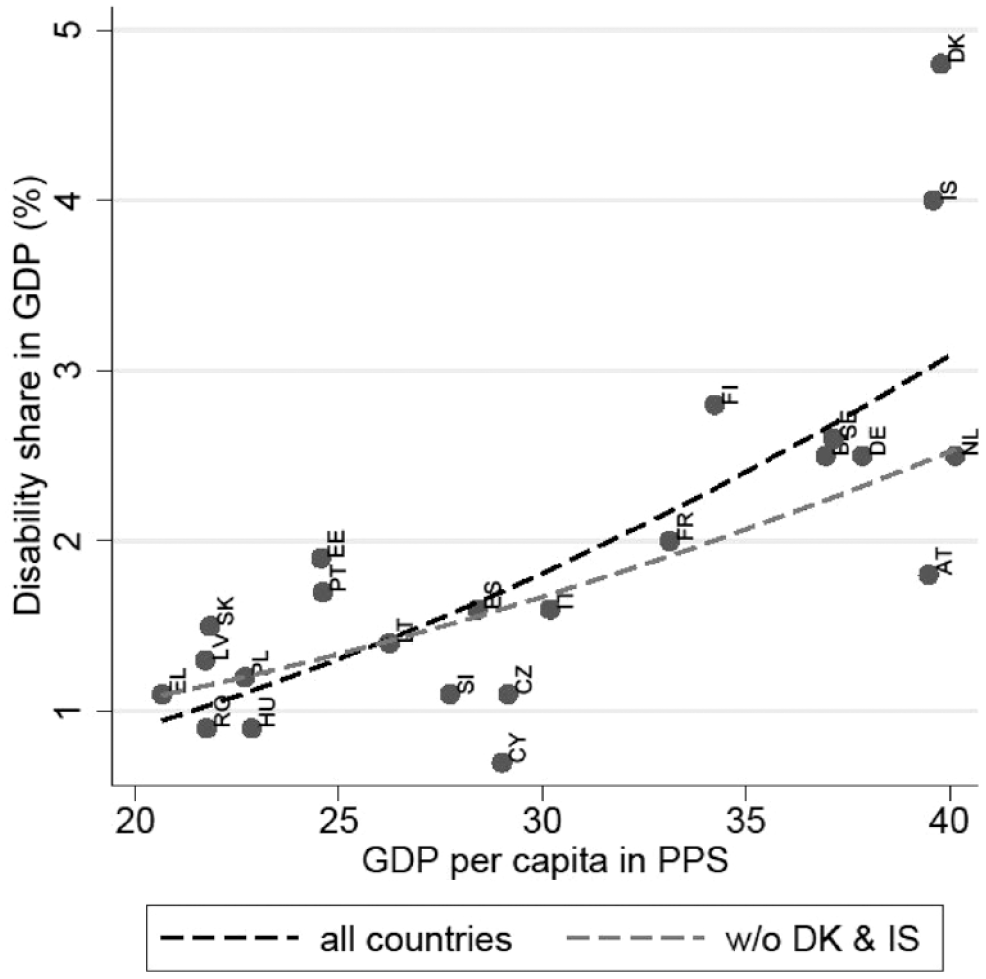

A comparison of the economic development across the EU countries and their corresponding share of disability-related expenditure in terms of GDP reveals a positive association. Specifically, more economically developed (i.e. wealthier) countries allocated higher proportions of their GDP toward social protection measures related to disability, as illustrated in Figure 2.

Economic development and disability expenditure on social protection (2019).

Based on the aforementioned inquiries, it is unlikely that CEE countries will immediately adopt a simplified and reduced direct income redistribution approach to their benefit systems. This is not because of a resistance to change resulting from their ratification of the convention, nor is it due to a need for a major system overhaul. Rather, it is primarily due to the limited availability of financial resources required to implement such modifications.

Conclusion

The modernization of railway stations in Poland in recent years presents a clear illustration of the difficulties that arise in implementing convention recommendations. Despite extensive renovations and the installation of new elevators, architectural barriers in the form of stairs and non-functioning elevators continue to hinder independent travel for individuals with disabilities. This situation exemplifies the persistent coexistence of medical and social models, in spite of the recognition and ratification of social model principles. The issue highlights the challenge of translating principles into practice and calls for a deeper examination of the underlying factors contributing to the persistence of these challenges. Notably, the challenges faced in the modernization of railway stations underscore the need for greater emphasis on practical solutions that enable the full participation of persons with disabilities in society. The study of such cases offers valuable insights into the complexities of implementing convention recommendations and serves as an important reminder of the ongoing need for continued action and collaboration among stakeholders to address persistent barriers to inclusion.

The pace of transition to the social model in CEE countries is unlikely to be hindered by the extent of changes needed in the tax and benefit system. It is worth noting that the tax and benefit systems in CEE countries are similar in structure to those in Scandinavian countries, with differences primarily being in the finer details. While CEE countries have more complex benefits systems that are focused on means-testing and specific benefits, Estonia stands out as an exception. In the future, cash transfers aimed solely at supporting disposable income will become less significant. However, such transfers will remain a critical component of disability policy, as seen in the experiences of more developed countries. Specifically, the new system will likely involve fewer instruments aimed exclusively at people with disabilities. Instead, disability requirements will be incorporated into more general benefits through the inclusion of income criteria and amount specifications.

The pace of change may be impeded by potential economic slowdowns in the upcoming years, as well as the absence of strong social pressure on policymakers to increase the percentage of public expenditure in relation to GDP. For politicians, direct income redistribution and the introduction of new benefits can be politically advantageous. Therefore, it will be crucial for there to be significant public demand to allocate an increasing portion of GDP toward enhancing public services and making investments that eliminate accessibility barriers in the future.

In accordance with the Rawls principle, once a society reaches a certain level of prosperity, priority should be given to basic liberties over economic well-being (Wolff, 2009: 60). In contrast, Scandinavian countries have a unique welfare model that emphasizes universalism and equality (Boheim and Leoni, 2016). Their welfare systems are known for their generosity, and they rank highest among OECD countries in terms of incapacity spending (Navarro et al., 2021; Tossebro, 2016: 112). However, it should be noted that these countries are significantly wealthier than their counterparts in CEE. As a result, the ‘certain level of prosperity’ condition still holds for CEE countries. The formal adoption of the social model may not have a direct impact on social policy instruments, but it has an important indirect impact on shaping the perspectives of policymakers regarding disability (Samaha, 2007).