Abstract

Low profitability and high failure rates remain chronic challenges within the restaurant industry. Despite the strategic importance of cost management, scholars have noted the limited attention this topic has received in restaurant-related research. This study aims to map the conceptual structure, methodological approaches, and key research gaps in cost and management accounting studies within the restaurant context. A comprehensive systematic literature review was conducted following the Scientific Procedures and Rationales for Systematic Literature Reviews (SPAR-4-SLR) protocol. Searches were performed in the Scopus and Web of Science databases; however, given the limited number of retained articles, the dataset was expanded using a forward snowballing technique. The study finally comprises 107 documents. The findings reveal that research activity remained minimal until 2007, after which publications increased, though inconsistently. Methodologically, most studies adopt descriptive or exploratory approaches, with case studies being the predominant method to address practical issues, which constrains the generalisability of findings. A co-word analysis identified five thematic clusters: cost by nature, variable costing, activity-based costing (ABC), efficiency, and absorption costing. The results indicate that advances in contemporary management accounting have not yet been fully incorporated into the restaurant management literature. Furthermore, key research trends in management accounting—particularly behavioural and organisational approaches—have received limited attention. Empirical evidence remains scarce concerning the management accounting practices (MAPs) adopted by restaurant managers, the factors influencing their implementation, and the impacts of MAPs and management systems on efficiency and performance. Accordingly, this study advances knowledge by clarifying how cost and management accounting research in the restaurant industry has evolved, identifying dominant and underexplored research streams, and highlighting key theoretical and methodological gaps that constrain the development of the field.

Keywords

Introduction

In many economies, the restaurant sector plays a crucial role as a driver of economic growth and employment. In the United States, it was projected to generate around USD 1.1 billion in sales and employ 15.5 million people by 2024 (Riehle et al., 2024). In the European Union, the food and beverage services industry represent a major component of the hospitality economy, accounting for 80% of enterprises, 78% of employment, and 69% of value added within the accommodation and food services sector (Eurostat, 2024). The economic contribution of restaurants is therefore undeniable and, in some contexts, exceeds that of hotels in terms of turnover and employment. Despite these positive figures, the sector continues to face persistent challenges, including high vulnerability to economic fluctuations (Cabiedes-Miragaya, 2017), intense competition stemming from low entry barriers (European Commission, 2023), and low profit margins and labour productivity (Lee et al., 2016; Mun and Jang, 2018; Riehl et al., 2023). Staffing shortages and rising operational costs further exacerbate these problems, resulting in lower survival rates for restaurants compared to other businesses (Cabiedes-Miragaya, 2017; European Commission, 2023; Parsa et al., 2015, 2021).

The relevance of the restaurant sector to national economies is also reflected in the growing body of research focusing on foodservice and restaurant management (DiPietro, 2017; Lee et al., 2016), second only to research on the hotel sector (Rodríguez-López et al., 2019). Although some researchers have acknowledged the sector’s importance and the expanding body of literature (Okumus et al., 2018), few studies have conducted a systematic analysis of publications adopting a business management approach. Okumus et al. (2018) analyzed 462 documents with a food and gastronomy focus, excluding topics under restaurant management. Rodríguez-López et al. (2019) and Park and Jang (2014) found that much of the literature is customer-oriented, emphasizing food, service quality, and their impact on satisfaction and behavioral intentions. DiPietro (2017) highlighted trends and recommended further research in menu engineering, pricing, and costing, a finding echoed by Rejeb et al. (2023) and Cao et al. (2025), who noted that financial domains receive the least attention from researchers. Elkhwesky et al. (2023) revealed that the impact of implementing cost and management accounting practices on business performance has largely been overlooked. This is concerning, as research suggests that restaurants could enhance performance with improved cost and management information (Lavia López and Hiebl, 2015; Linassi et al., 2016; Uyar and Kuzey, 2016), whereas poor cost management can contribute to failure (Parsa et al., 2005).

Restaurant failures have been linked to both external and internal factors. External causes include economic conditions, legal restrictions, cultural shifts, and strong market competition (Parsa et al., 2005, 2011; Yim et al., 2014). Internally, insufficient financial resources, poor planning, and weak cost control systems have been identified as critical drivers of failure (Frazer, 2012; Lee et al., 2016; Parsa et al., 2011). Effective cost management is therefore essential to improve profitability, particularly through the control of labour, utility, and occupancy costs (Hesford and Potter, 2010; Mun and Jang, 2018; Riehl et al., 2023). Recent industry reports also highlight staff retention, rising food costs, and increasingly demanding customers as key challenges (Hosteltur, 2024, Tablein, 2023; Klein, 2024). While these operational and financial challenges have been addressed in both industry and academic literature, no study has yet provided a systematic and comprehensive synthesis of how cost and management accounting research in the restaurant industry has evolved, how is conceptually structured and which methodological approaches have been adopted. As a result, the extent to which existing research can inform managerial decision-making in this sector remains unclear. Prior research shows that high-quality cost information (Pizzini, 2006) supports the adoption of management accounting practices, which impact performance (Uyar and Kuzey, 2016). Different MAPs have been grouped into stages according to their level of sophistication. These stages are not mutually exclusive; rather, they reflect how the adoption of MAPs responds to the need to provide relevant information to support managerial decisions under evolving internal and external contextual conditions (Abdel-Kader and Luther, 2006). From a theoretical perspective, researchers have adopted contingency theory to examine the extent to which factors such as uncertainty, centralisation, size, operational complexity, strategy, and industry-specific factors influence the level of sophistication of MAPs.

Therefore, the general objective of this study is to address this gap by making two contributions. From a theoretical perspective it provides a systematic mapping of the conceptual structure, the methodological approaches, and research gaps in cost and management accounting research in the restaurant industry, outlining directions for future research. From a practical perspective, it informs restaurant managers and other industry stakeholders, such as restaurant associations and hospitality education and training organizations, the extent to which restaurant research can inform cost management decisions and highlighting areas empirical evidence is still lacking. The following research questions arise from this general objective:

What has been the evolution of cost and management accounting research in the restaurant industry?

Which journals lead this field in terms of publication output?

What methodological approaches do authors use?

What are the main topics addressed, and what is the thematic structure of research in this area?

Which topics should be prioritized in future research on cost and management accounting in the restaurant industry?

The remainder of the paper is structured as follows: first, the research methods are presented, emphasizing the rationale behind methodological choices; next, the results of the descriptive and thematic analyses are reported. This is followed by a discussion of findings and identification of research gaps. Finally, conclusions are drawn.

Methodology

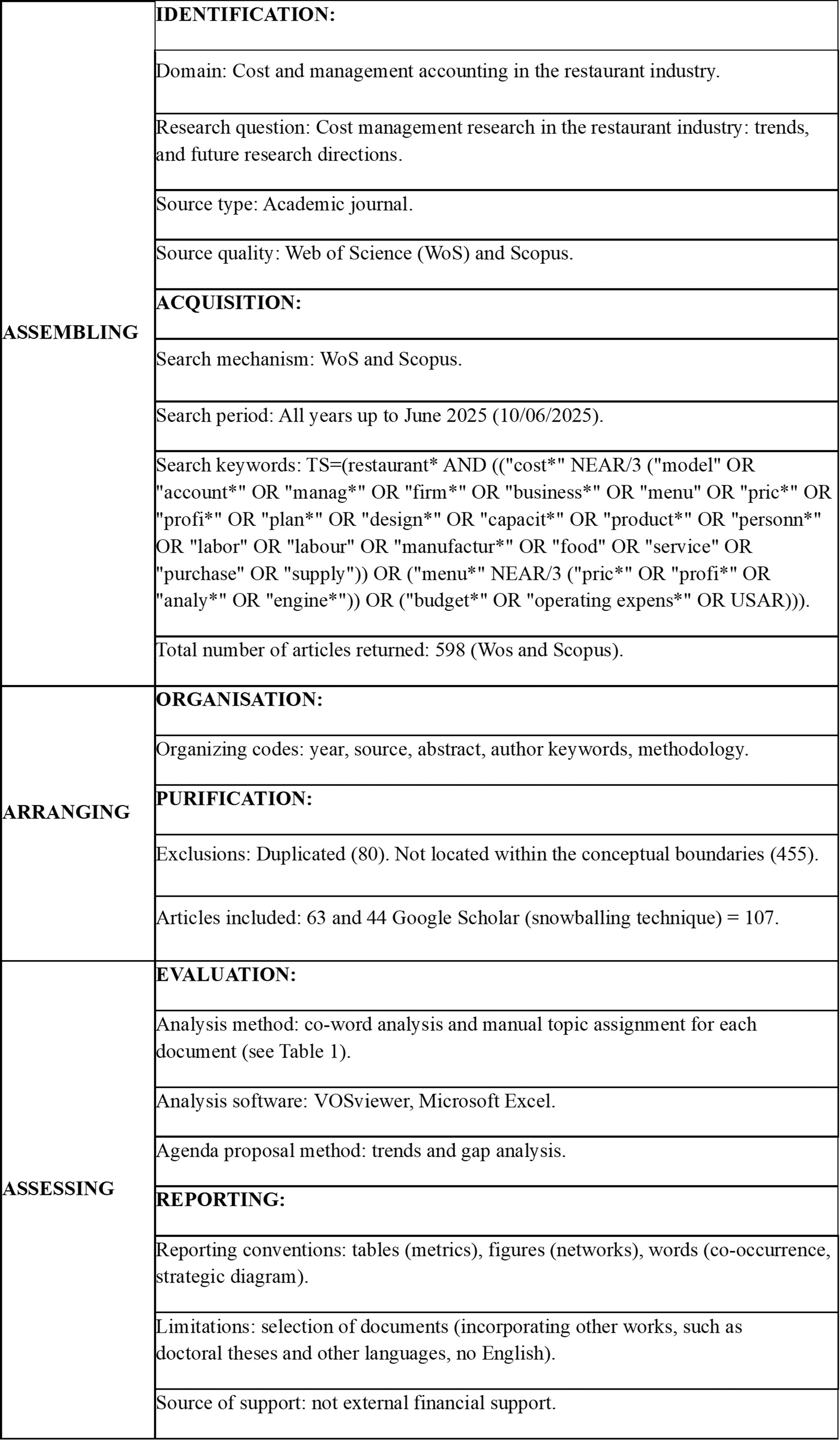

To address the research questions posed, a systematic literature review was conducted following the Scientific Procedures and Rationales for Systematic Literature Reviews (SPAR-4-SLR) protocol (Paul et al., 2021). While many authors rely on the PRISMA-P protocol (Moher et al., 2015), SPAR-4-SLR was selected as it incorporates several elements from PRISMA-P while offering clearer guidance and rationale for the various decisions made throughout the review process. The SPAR-4-SLR protocol comprises three main stages, each divided into two sub-stages: Assembling (Identification and Acquisition), Arranging (Organization and Purification), and Assessing (Evaluation and Reporting).

The first stage, Identification, comprises decisions that define the scope of the review—namely, the domain, research questions, type of sources, and source quality. The domain of this study is cost and management accounting in the restaurant industry, and the research questions were delineated accordingly. Regarding the sources, only peer-reviewed journal articles published in English and indexed in the Web of Science (WoS) (in SCI, SSCI, or ESCI) or Scopus were included. These databases constitute the most common sources for bibliometric and systematic reviews in business and management (Zupic and Čater, 2015). Both databases offer several advantages that facilitates subsequent analysis and apply quality criteria to the journals they index, ensuring the academic reliability of the documents.

The Acquisition sub-stage involved determining how to collect the documents. Searches were conducted without time restrictions, as the research team perceived that academic attention to this topic has been limited despite the industry’s economic significance. After an iterative process testing various keywords, the final search string (WoS syntax) was as follows:

TS=(restaurant* AND ((“cost*” NEAR/3 (“model” OR “account*” OR “manag*” OR “firm*” OR “business*” OR “menu” OR “pric*” OR “profi*” OR “plan*” OR “design*” OR “capacit*” OR “product*” OR “personn*” OR “labor” OR “labour” OR “manufactur*” OR “food” OR “service” OR “purchase” OR “supply’)) OR (“menu*” NEAR/3 (“pric*” OR “profi*” OR “analy*’ OR “engine*”)) OR (“budget*” OR “operating expens*” OR USAR))).

This search yielded a total of 598 documents.

The second stage, Arranging, focused on constructing the final database for the review. The first step, Organization, involved coding the relevant information from each document to enable further analysis. Basic bibliographic data were collected—year, source, abstract, and author keywords—which supported the Purification step. At least two researchers independently screened the documents based on these fields. In cases of disagreement, the full text was jointly reviewed by the entire research team to reach a consensus. After this initial purification, 63 documents remained.

Excluding duplicated records (80 documents), the remaining excluded documents were mainly associated with adjacent research domains. The categories accounting for the largest number of exclusions were marketing and consumer behaviour (73 documents), finance and taxation (49 documents), sustainability (45 documents), nutrition and food science (45 documents), tourism and gastronomy studies (43 documents), menu design and pricing, reservation and capacity management, and delivery and takeaway services (18 documents), energy efficiency (17 documents), and human resources management (11 documents).Although many of these studies used the restaurant industry as an empirical setting, cost and management accounting practices, systems, or cost-based decision-making frameworks were not central to their analysis. Consequently, they fell outside the conceptual boundaries of this review. Additional documents were excluded because their primary focus lay outside the restaurant industry, even when the term “restaurant” appeared in the abstract (e.g. studies on agriculture, transportation, aviation, or household consumption), where restaurants were mentioned only illustratively or in policy or managerial implications.

Given the limited number of retained articles, the dataset was expanded by applying a forward snowballing technique, which involved examining the references that cited the initially selected documents. Only peer-reviewed journal articles, book chapters, and conference papers meeting specific quality criteria were included: (i) no duplication with existing entries (especially conference papers later published as journal articles) and (ii) adequate methodological and conceptual quality as assessed by the research team. This process added 44 documents (41 journal articles and three conference papers). The source of each document is reported in the supplementary database (Appendix A). Consequently, the final dataset consisted of 107 documents. Figure 1 summarises the process of constructing the final database. The SPAR-4-SLR protocol. Source: Adapted from Paul et al. (2021).

The third stage, Assessing, began with Evaluation, which involved selecting the analysis methods. Given the study’s objectives, a co-word analysis was performed. Callon et al. (1983) define this technique as a form of content analysis that maps a domain’s conceptual structure based on the co-occurrence of words (topics) within documents. The assumption is that topics appearing together are conceptually related. As Zupic and Čater (2015) note, co-word analysis is the only bibliometric method that builds similarity measures from document content rather than metadata. Other techniques—such as co-citation, bibliographic coupling, and co-authorship analysis—use reference lists or author information. Co-word analysis produces a visual map of key topics and their interrelations.

A main criticism of co-word analysis concerns the word source (He, 1999). Researchers often rely on author keywords, which are limited by semantic ambiguity (Leydesdorff, 1997). To overcome this, co-word logic was applied, with topics being manually assigned after a detailed content analysis of each document, instead of using indexed keywords such as Keyword Plus® or Index Keywords.

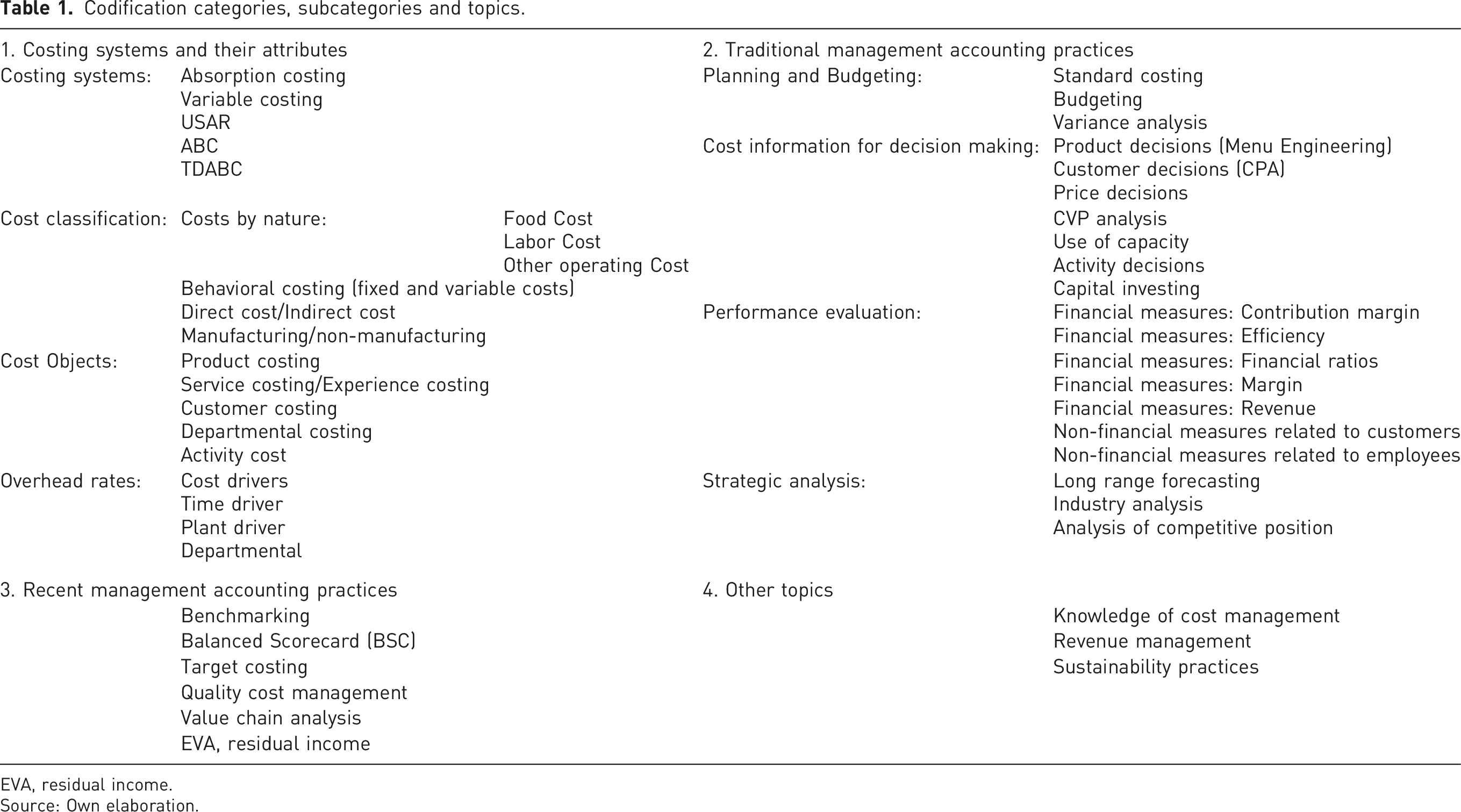

The process of topic assignment began with the development of a topic scheme. This scheme grouped the main topics into categories such as costing systems, planning and budgeting, information for decision-making, performance evaluation, and strategic analysis. These categories have been widely used in the management accounting literature (Abdel-Kader and Luther, 2006; Nandan, 2010; Pavlatos and Kostakis, 2015; Pavlatos and Paggio, 2008; Pizzini, 2006; Uyar and Kuzey, 2016; Yalcin, 2012). In addition, a new category labelled recent management accounting practices (MAPs) was incorporated to capture the techniques addressed in more recent studies, such as the balanced scorecard and target costing (Abdel-Kader and Luther, 2006; Horngren et al., 2012). Each category included several subtopics. For instance, within the costing systems category, subtopics reflecting the main attributes of these systems, such as cost objects, cost classifications, and cost rates (Pavlatos and Paggio, 2008) were identified.

Codification categories, subcategories and topics.

EVA, residual income.

Source: Own elaboration.

To assign topics, one researcher read each document’s title, abstract, introduction, and theoretical framework, assigning topics and noting the rationale for each choice. To mitigate subjectivity in topic coding, a multi-coder procedure was employed. Two researchers independently reviewed each document, with three researchers involved in the coding process overall. Initial agreement was achieved for 78 of the 107 documents (72.9%), and any remaining discrepancies were resolved through joint discussion until full consensus was reached. Each document received between one and 15 topics, completing the Codification sub-phase. Once topic occurrences and co-occurrences were identified, the data were normalised using a similarity measure and clustered. Following Van Eck and Waltman (2009) and Waltman et al. (2010) association strength was applied as the similarity measure and the VOS (Visualization of Similarities) algorithm was used for clustering, using VOSviewer software (Van Eck and Waltman, 2010).

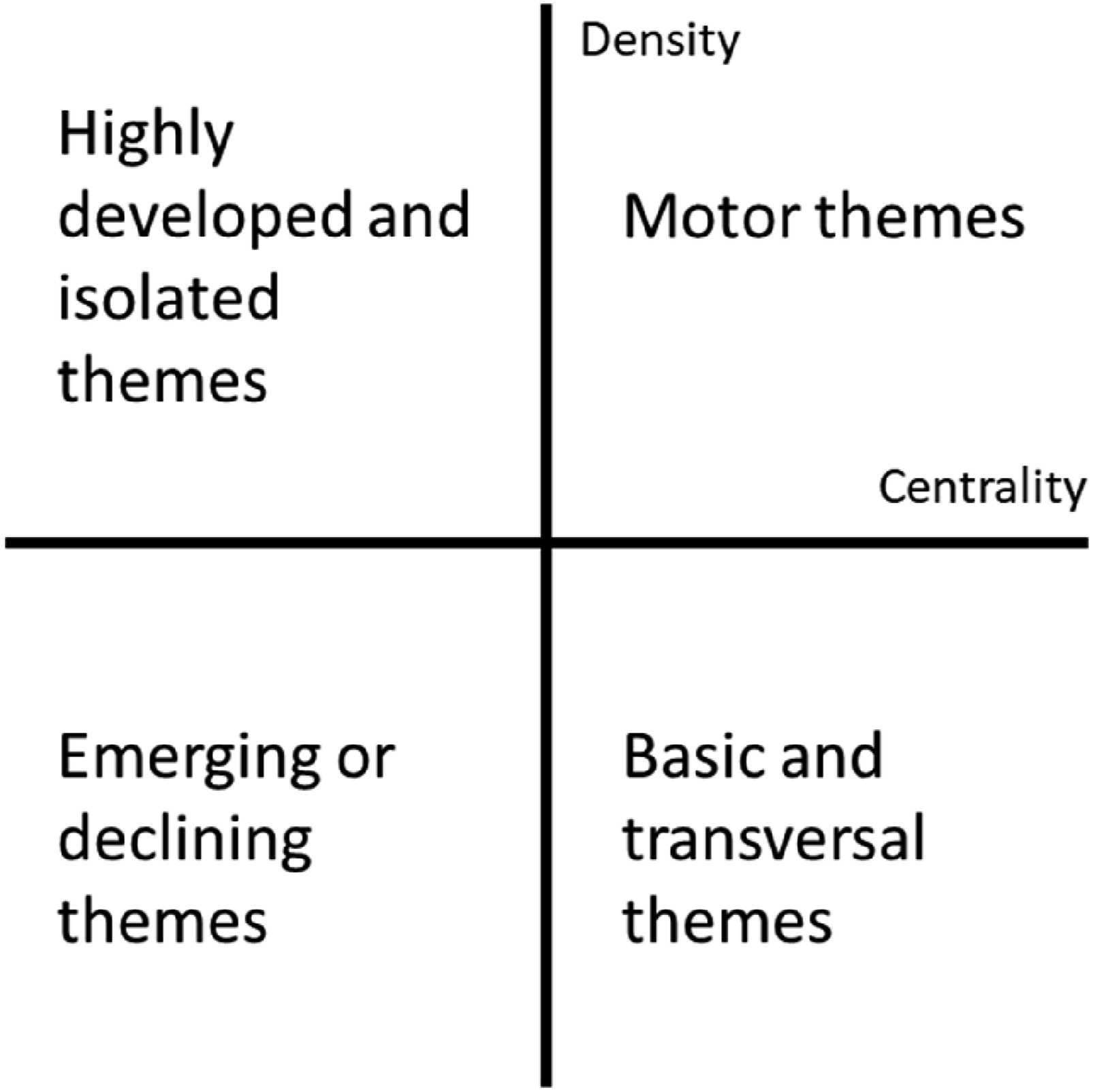

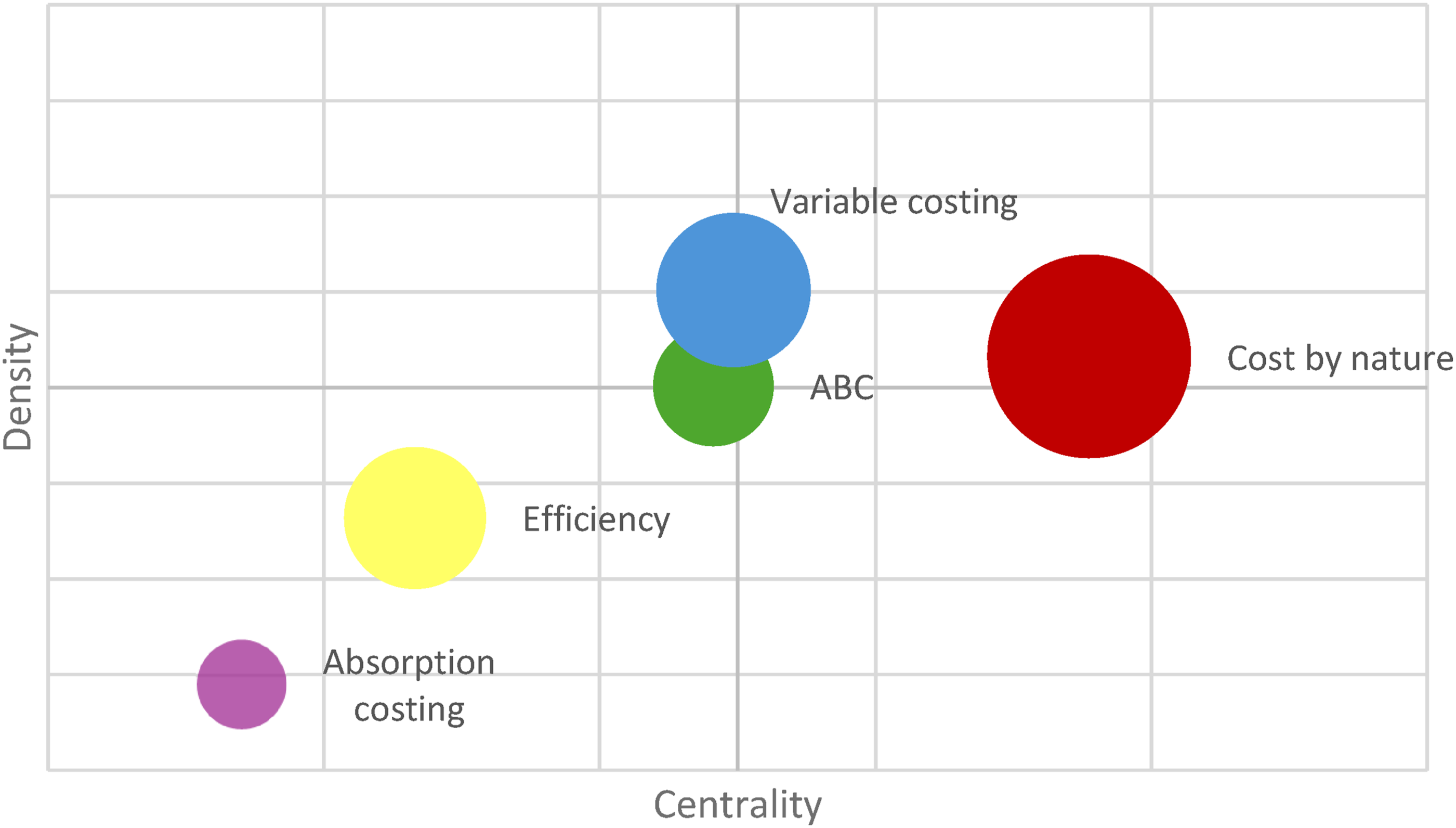

To interpret results, additional metrics were computed for each topic and cluster based on Callon et al.’s (1991) strategic diagram, which characterises clusters by density and centrality. Density reflects the internal cohesion of a cluster, while centrality indicates its connections to other clusters and thus its overall relevance. Density was calculated as the average internal link strength, and centrality as the total external link strength. Plotting density against centrality positioned clusters within four quadrants of the strategic diagram (Figure 2). Finally, to complement the analysis, two researchers classified each document by research approach (Sukamolson, 2007), resolving disagreements collaboratively. Strategic diagram. Source: Adapted from Cobo et al. (2011, p. 151).

Results

Descriptive analysis

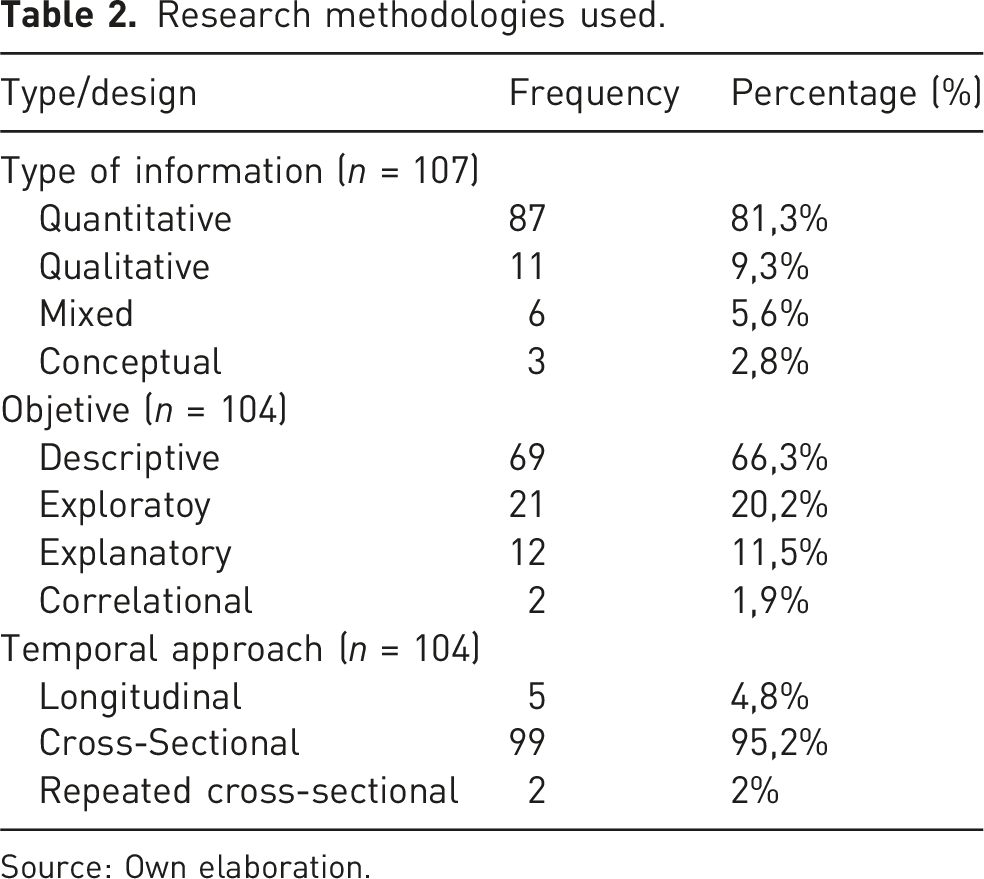

Research methodologies used.

Source: Own elaboration.

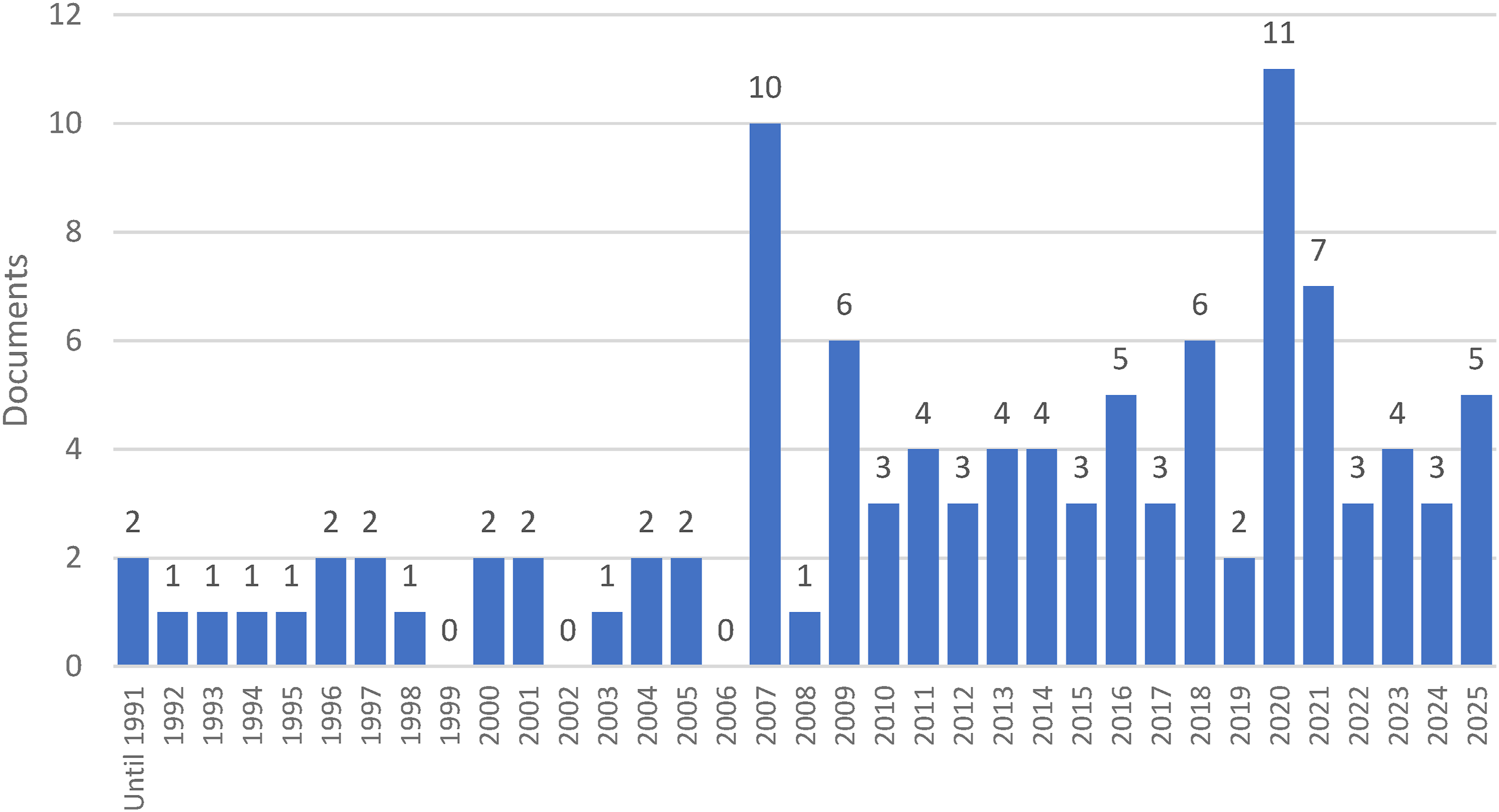

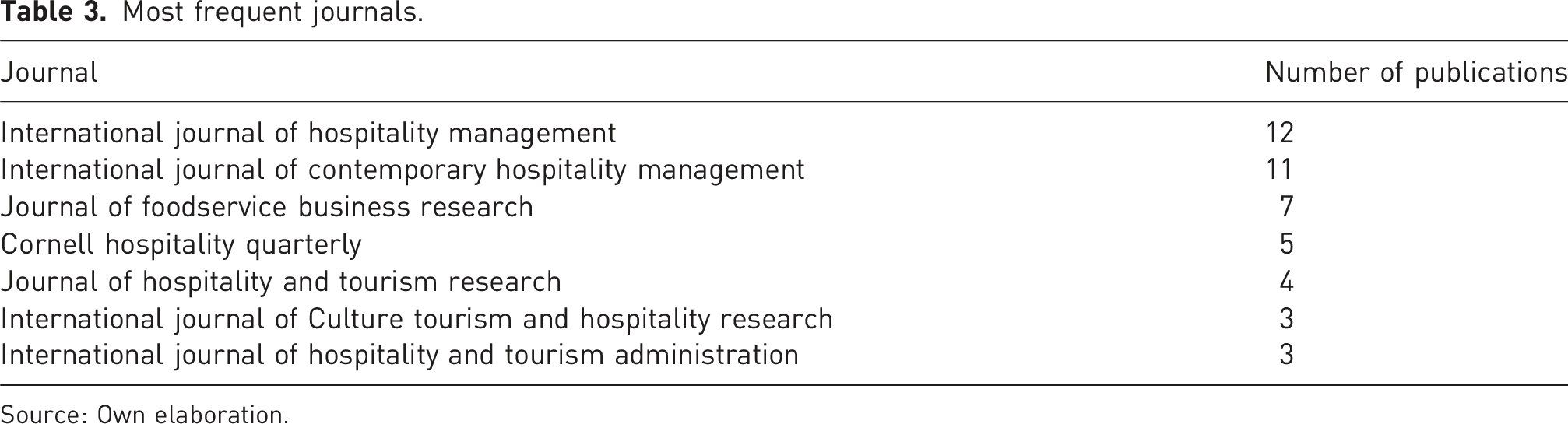

Research on cost and management accounting in the restaurant industry remained scarce for the first 24 years, with only one or two papers published annually. After 2007, the number of studies increased, though irregularly, with peaks in 2007 and 2020 (Figure 3). Early research appeared mainly in tourism or food science journals, but by 2020 the subject areas had diversified. The most frequent journals were the International Journal of Hospitality Management and the International Journal of Contemporary Hospitality Management, followed by the Journal of Foodservice Business Research and Cornell Hospitality Quarterly (formerly Cornell Hospitality and Restaurant Administration Quarterly) (Table 3). Documents distributed by publication year. Source: Own elaboration. Most frequent journals. Source: Own elaboration.

Content analysis

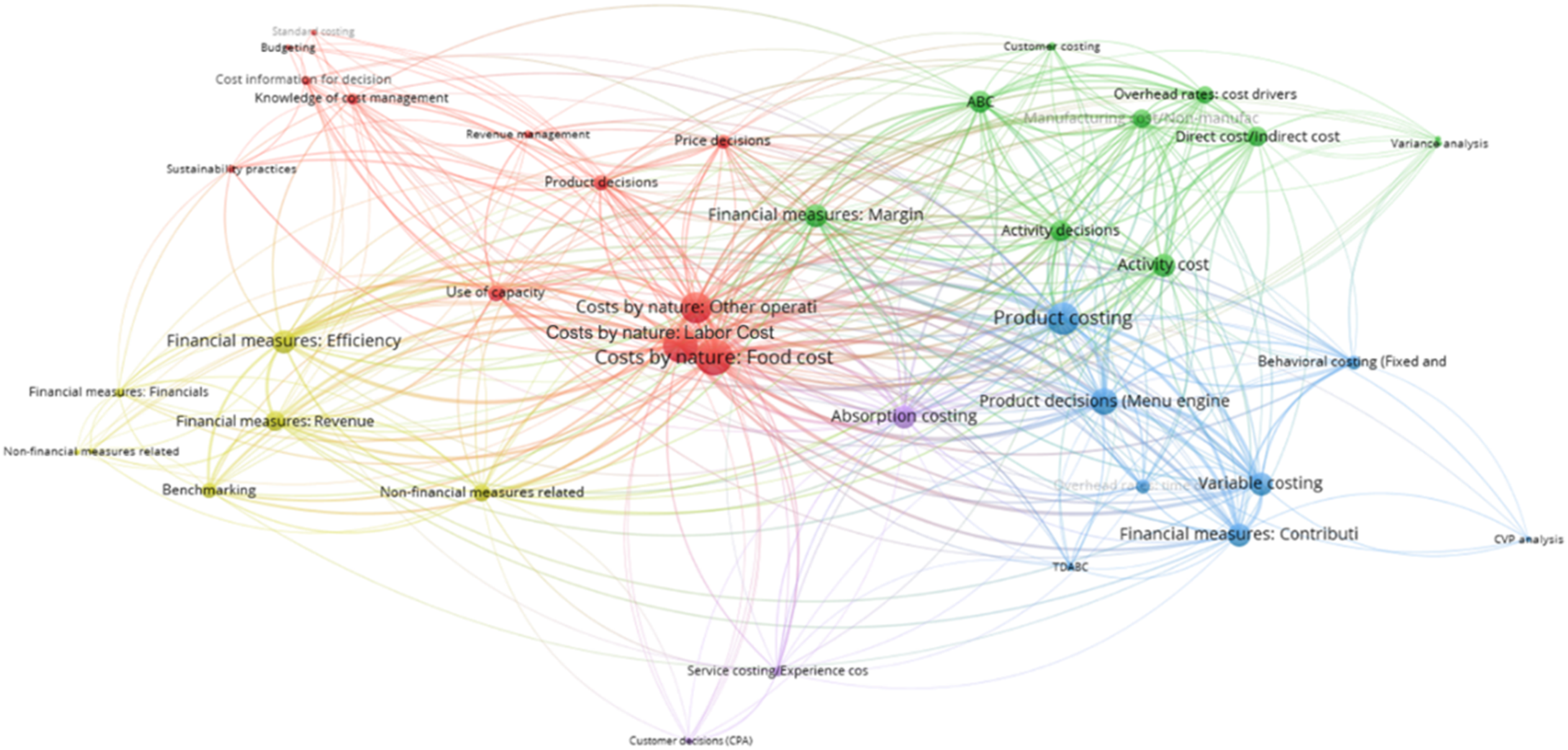

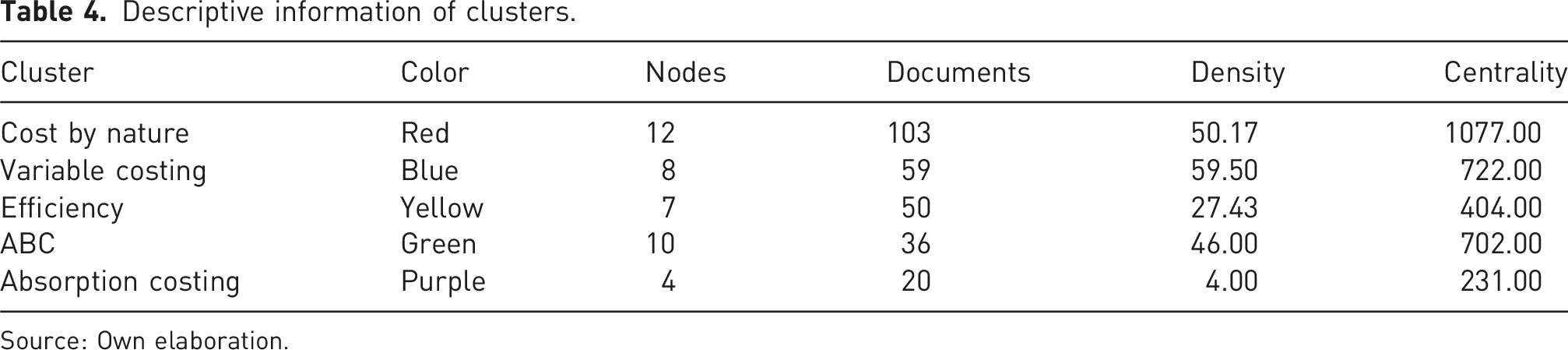

The study’s main contribution is the thematic analysis of the 107 articles in the database. Figure 4 displays the thematic map generated using the VOS algorithm on the network of topics assigned to each document. Node size indicates association strength, and colour denotes the cluster identified by the algorithm. After testing, the analysis produced five clusters (resolution = 0.9), selected for their stability and interpretability after sensitivity testing. Figure 5 presents these clusters in a strategic diagram, using the same colours as in the network. Bubble size represents the number of documents containing at least one topic from each cluster (Table 4). Cluster labels were assigned by the research team based on topic representativeness. Thematic Network Map. Strategic diagram of restaurant cost and management research. Source: Own elaboration. Descriptive information of clusters. Source: Own elaboration.

In the thematic network (Figure 4), the red cluster (Cost by nature) is the most central, including the three most connected nodes—key cost components in restaurant operations. Other relevant nodes are use of capacity, product decisions, and price decisions. The blue cluster (Variable costing), located in the lower right, contains several central nodes; product decisions (menu engineering) and product costing bridge the red and green clusters. The green cluster occupies the upper right quadrant, while the yellow cluster (efficiency-related topics) and the purple one (Absorption costing) are less central, except for the absorption costing node itself.

The strategic diagram confirms these patterns and shows low thematic density. Except for Cost by nature, topics are dispersed with few recurring links, indicating limited maturity and cohesion. Only one cluster (red) appears as a motor theme, two (blue and green) are transitional, and two (yellow and purple) correspond to emerging or declining topics. The efficiency and absorption costing clusters are disconnected from the other research streams.

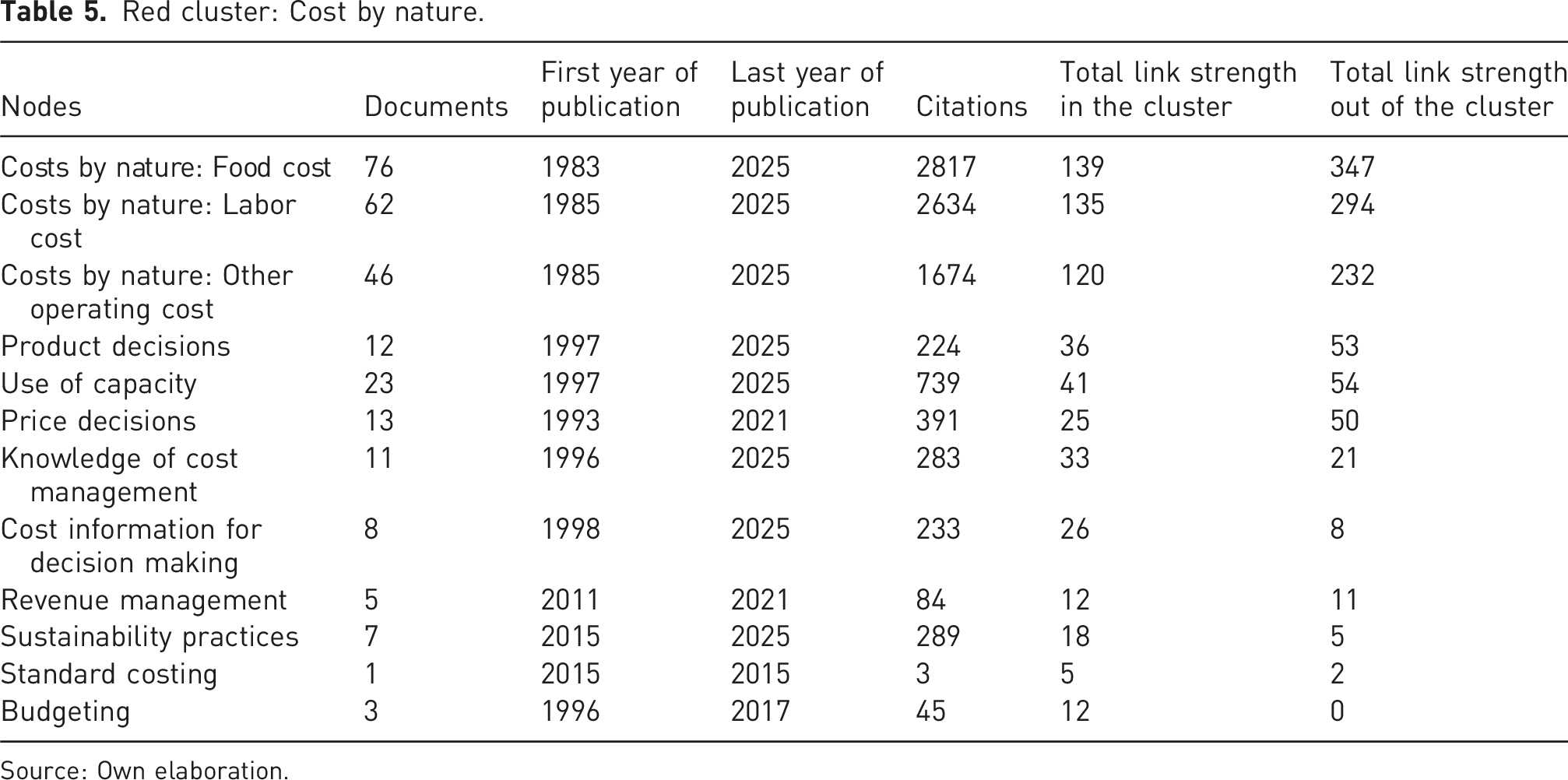

Red cluster: Cost by nature.

Source: Own elaboration.

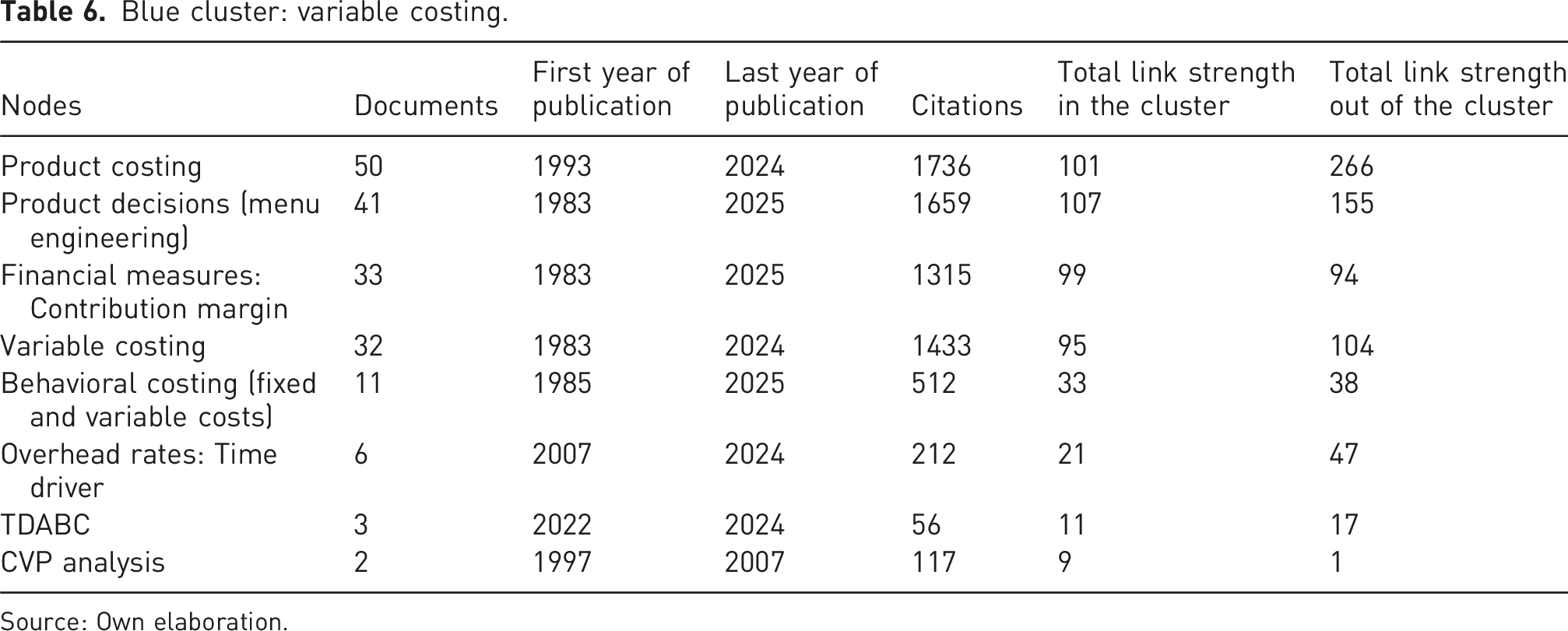

Blue cluster: variable costing.

Source: Own elaboration.

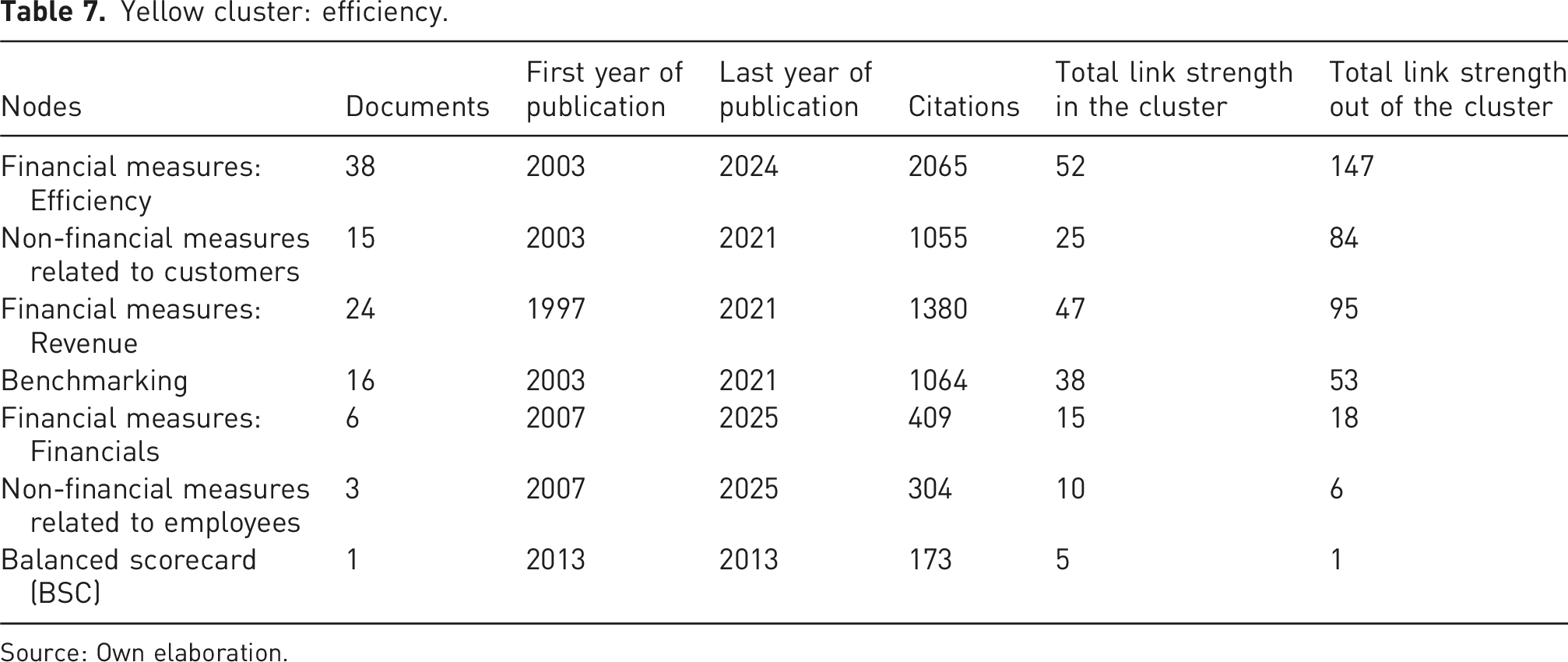

Yellow cluster: efficiency.

Source: Own elaboration.

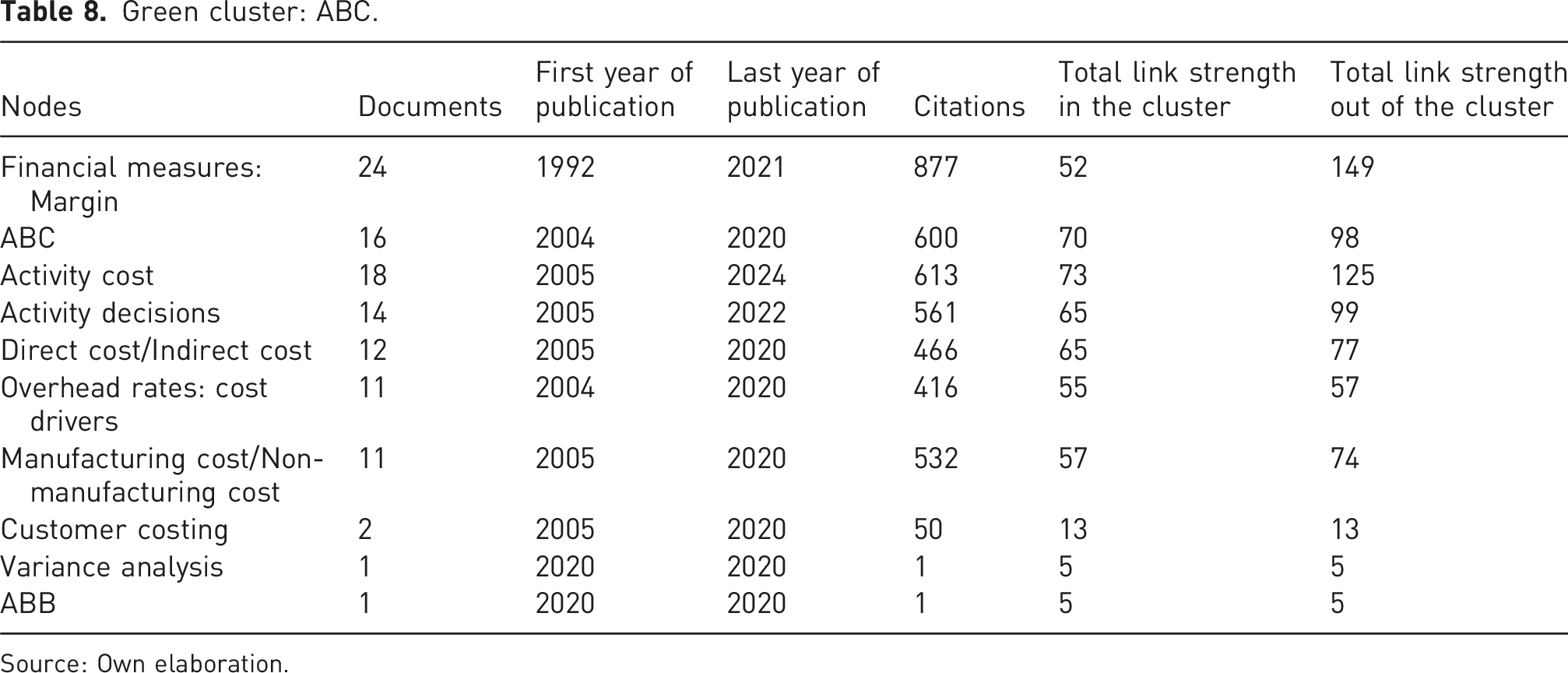

Green cluster: ABC.

Source: Own elaboration.

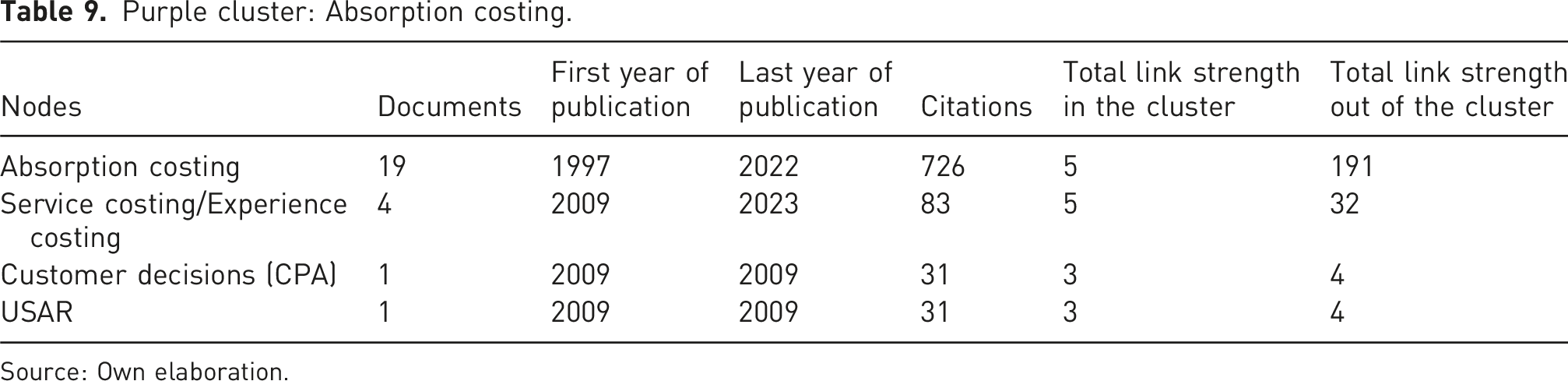

Purple cluster: Absorption costing.

Source: Own elaboration.

Discussion and future research lines

While existing literature on cost and management accounting in the restaurant industry is largely descriptive or case-based and rarely adopts explicit theoretical frameworks, the identified clusters provide insight into the field’s main themes and reveal underdeveloped theoretical perspectives in the restaurant context. This research has produced a thematic analysis, resulting in a conceptual structure comprising the following five clusters: cost by nature, variable costing, ABC, efficiency and absorption costing.

Variable costing emerges as the most frequently examined costing system, largely due to its use as the accounting basis for menu engineering—a widely adopted tool in the restaurant industry due to the centrality of menu decisions and its simplicity (Linassi et al., 2016). Variable costing has also been used to value production, but academics have typically limited themselves to classifying food costs as the only variable costs or have assumed labour costs to be variable without further justification. Paradoxically, despite this method’s reliance on cost behaviour, little research has empirically examined how restaurant costs actually behave. This oversimplification constrains understanding of the industry’s cost structure and weakens managerial decision-making, particularly during periods of crisis (Alonso-Almeida et al., 2015; Mun and Jang, 2018).

By the mid-1990s, management accounting research had reached a consensus on the need to move beyond the traditional linear relationship between cost drivers and costs toward more refined systems, such as activity-based costing (ABC) (Berg and Madsen, 2020). Within the broader management accounting literature, ABC is conceptualised as a context-dependent system whose relevance hinges on factors such as firm size, cost structure, and the proportion of indirect costs.

The predominance of descriptive, case-based applications within the ABC cluster confirms insights from the wider management accounting literature regarding the instrumental and practice-oriented phase of ABC research, which has seen relatively limited theoretical engagement in recent decades (Berg and Madsen, 2020). Research in the restaurant industry followed this trend, albeit belatedly: the first ABC application appeared in 2005. Since then, most studies have used case studies to demonstrate the system’s applicability across restaurant types, often concluding that it provides more accurate information for product costing and pricing decisions, either independently or in combination with other management accounting tools, particularly menu engineering. Nevertheless, research in the restaurant industry has largely focused on technical feasibility rather than examining whether the organisational, behavioural and structural conditions identified in prior theory are present in this context. As a result, the ABC cluster highlights a disconnect between the contingent view of ABC developed in the management accounting literature and its application within restaurant studies.

As Kaplan and Anderson (2004) noted, implementing ABC entails significant challenges, which partly explains the shift towards time-driven ABC (TDABC) a simplified model. Within the restaurant literature, although some recent studies adopt more sophisticated cost analyses (Göde and Ekergil, 2023), this evolution still remains largely confined to assessments of technical feasibility, and the evidence remains predominantly case-based, limiting the generalisability of findings (Elshaer, 2020; Raab et al., 2005, 2007; Vaughn et al., 2010). As a result, research has not yet enabled systematic testing or refinement of existing ABC theories in the restaurant context.

Before developing further case studies to demonstrate the advantages of ABC or TDABC, researchers should first assess whether the enablers, drivers, and barriers to implementation identified in other contexts are applicable to the restaurant industry (Berg and Madsen, 2020). Future research could address questions such as:

What is the level of awareness and adoption of ABC among restaurant owners and managers? Which mechanisms facilitate the diffusion of management systems within the industry? Are managers prepared for the cultural and organizational changes that implementing ABC will require, and do they possess the necessary skills? Do existing restaurant management systems for ABC implementation requirements?

The variable costing and activity-based costing (ABC) clusters indicate that cost management research in the restaurant industry adopts a mechanistic view of the relationship between costs and their drivers. This finding is theoretically relevant because contemporary cost and management accounting research recognises that cost behaviour patterns are not mechanical but result from managerial decisions about how to allocate resources in specific contexts. Adjustment costs, managerial expectations, incentives, and personal characteristics influence these decisions (Banker et al., 2018).

Despite evidence from prior research showing that industry characteristics and firm-specific contexts influence the degree of cost stickiness (Calleja et al., 2006), and recent empirical studies analysing cost stickiness in the hospitality sector (Zhang et al., 2019), the impact of managerial choices on margins and cost behaviour in restaurant firms has received limited attention from scholars, with the notable exception of Kim et al. (2007). This gap is particularly noticeable given that the restaurant industry is characterised by high fixed costs, capacity constraints and dominated by micro and small firms, which makes it particularly sensitive to adjustment costs and personal characteristics of managers (Yazarkan et al., 2022). Researchers are encouraged to fill this gap by investigating:

How different types of costs behave? What is the degree of cost stickiness? and what are the determinants of cost behaviour? This is particularly relevant for labour costs, which are the second largest operating expense (Mun and Jang, 2018), as well as being a recognised capacity constraint. Do labour costs behave differently depending on a national labour legislation (Banker et al., 2013), business models or culinary level?

Although cost and management accounting aim to support informed managerial decisions that enhance efficiency and profitability, most studies assessing restaurant efficiency overlook the role and peculiarities of costing systems. This neglect helps explain why research in this area appears disconnected from other research streams, reflecting the persistent gap between management accounting and finance scholarship. Nevertheless, this line of research has expanded the range of variables considered in input–output analyses of business efficiency—for instance, incorporating indirect operating expenses as inputs or including non-financial outputs such as customer satisfaction. Most empirical studies rely on case studies or simulated data, which limits the generalisability of findings. Only a few authors adopt explanatory approaches to identify factors influencing efficiency. Further research is needed to analyse restaurant cost structures and their relationship with efficiency across different types and sizes of establishments, as well as in relation to managers’ individual characteristics.

Capacity management represents a promising area for future research. One emerging topic is the widespread adoption of food delivery services. Changing consumer preferences and mobile technologies have made delivery a standard practice and strategic opportunity, even for fine-dining restaurants and cafés. However, the outcomes of introducing food delivery or takeaway channels are not straightforward (Stern, 2019). Managers face risks such as (i) demand cannibalisation (a reduction in dine-in demand due to these customers opting for delivery), (ii) price differentials between dine-in and delivery services, and (iii) kitchen production bottlenecks (Ma et al., 2021). Key research questions include:

How does delivery affect costs and capacity? How can menu engineering be adapted to a parallel delivery menu that incorporates packaging costs, kitchen production time, and the risk of service deterioration for dine-in customers?

Moreover, research has tended to measure restaurant capacity primarily in physical terms (number of seats) (Pullman and Rogers, 2010), rather than human capacity. Yet, the workforce—restaurants’ second largest operating expense (Mun and Jang, 2018)— constitutes a recognised capacity constraint due to high staff turnover (Auberry et al., 2019; Azevedo and Silva, 2024). Although performance measurement systems linked to compensation or career development programmes have been studied in hospitality (Ghani et al., 2022; Michael and Fotiadis, 2022), this has not been done for restaurants. Furthermore, the impact of these measures appears to be short-lived (Kim and Jang, 2020). Future research could therefore explore:

How can labour contracts, reward systems, and career development plans be used to retain employees? How can these plans be integrated with performance measurement systems to improve employee retention, and what will be the impact of these measures on restaurant performance?

The concept of sustainability has a long tradition in hospitality and tourism literature, and a more recent stream of literature has emerged focusing on food waste (Filimonau and Delysa 2019). However, food waste was not examined from a cost management perspective until sustainability concerns entered the restaurant business (Charlebois et al., 2015; Christ and Burrit, 2017; Filimonau et al., 2020; Gruia et al., 2021). Given its implications for the efficient use of resources, sustainability offers further opportunities for research in cost and management accounting. Future studies could examine whether restaurateurs integrate sustainability into their strategic and operational objectives and how this is reflected in their choice of key performance indicators, costing systems, and management control practices.

These challenges are particularly relevant in the restaurant sector, where around 90% of businesses in the restaurant industry are SMEs (Eurostat, 2024; McCauley, 2025). Management accounting research consistently reports a low level of adoption of management accounting practices (MAPs) among SMEs, yet findings remain inconclusive regarding (i) how MAPs are used in real-world settings (Lavia López and Hiebl, 2015; Roffia et al., 2025), (ii) the factors influencing their adoption (Roffia et al., 2024), and (iii) the effects of their implementation (Ciambotti et al., 2020). Previous studies attribute this low adoption to resource constraint, lack of managerial training, scepticism, and inadequate information systems (Bhimani and Willcocks, 2014; Lavia López and Hiebl, 2015; Roffia et al., 2024).

Restaurant managers need to combine managerial, entrepreneurial, and creative skills. The industry integrates manufacturing and service processes and has been described as a culinary art demanding innovation and customer orientation (Choi and Lee, 2024). Consistent with prior research on SMEs (e.g. Cardoni et al., 2023), the broader management accounting literature reports inconclusive evidence on how MAPs are actually used in practice, the factors influencing their adoption, and their effects on organisational performance. Within the restaurant literature, however, this gap is even more pronounced, as research addressing managers’ and chefs’ knowledge and perceptions of cost management remains scarce, and even fewer studies examine how such knowledge shapes the adoption and effective use of MAPs. Key questions include:

How do MAPs affect performance? Do budgeting practices shape organizational performance? How do managerial differences influence planning and budgeting decisions?

A related area concerns the role of management information systems. Scholars have analysed how MAPs evolve alongside information system adoption and its implications for performance (Bhimani and Willcocks, 2014; Papiorek and Hiebl, 2024). Beyond point-of-sale (POS) systems—the most common technology (Cavusoglu, 2019)—numerous digital tools now support both front- and back-of-house operations (Alt, 2021; Kocaman, 2021). Recent studies highlight the benefits of restaurant management systems (RMSs) for operations, customer experience, and competitiveness (Rosnan et al., 2023), yet their impact on cost management remains underexplored. Future research could therefore investigate:

How do MAPs evolve alongside RMS adoption? To what extent do managers exploit RMS capabilities? Which functionalities are perceived as most critical for success? Does RMS adoption improve performance?

Finally, building on the thematic clusters and methodological patterns identified in this review, the analysis points to several ways in which future research in the restaurant sector could be broadened. These include exploring restaurants in new geographical contexts (Mhlanga, 2018; Raucci et al., 2020; Reynolds and Taylor, 2011), analysing the full range of menu offerings (Chou and Fang, 2013; Fang et al., 2013; Fang and Hsu, 2014; Linassi et al., 2016; Noone and Cachia, 2020; Taylor et al., 2009), and extending data collection to capture different consumption occasions (Nemeschansky et al., 2020; Salem-Mhamdia and Ghadhab, 2012).

Conclusions

This study maps the conceptual structure of research on cost and management accounting in the restaurant industry over a period of more than four decades. To our knowledge, it is the first to provide such a map. Given that cost management is an essential mechanism for performance measurement and operational control, this research contributes to addressing the challenges faced by the restaurant industry—high failure rates, intense competition, and high operating costs.

Academic output in this field has increased systematically but not consistently. Considering that the search was not limited to WoS and Scopus, and that the sample included articles, books, and conference papers, 107 documents (an average of fewer than three per year) represent a modest production volume. This can be explained by the difficulty management accounting researchers face in accessing internal data (Kim et al., 2007) and in publishing in top-tier journals due to editorial preferences (Merchant, 2012). Furthermore, there are fewer scholars specialising in this field compared to those focusing on consumer or organisational behaviour (Cao et al., 2025), disciplines that traditionally hold greater weight within tourism studies. These findings underscore the need for interdisciplinary collaboration.

The analysis identified five thematic clusters: cost by nature, variable costing, ABC, efficiency, and absorption costing. Three of these clusters correspond to costing systems—variable costing, activity-based costing (ABC), and absorption costing. Variable costing is the most extensively studied, followed by ABC, while absorption costing appears less frequently. Cost by nature is the only motor cluster; it encompasses topics addressed in most documents, such as the main cost components of restaurants—food, labour, and other operating costs—as well as less explored but related topics representing avenues for future research. In contrast, the efficiency cluster appears disconnected from the others.

Overall, the results reveal that cost management research in the restaurant industry lags behind broader developments in the field. Accordingly, this study proposes specific future research areas for each cluster, emphasising that established themes in management accounting—such as the actual use and behavioural dimensions of management accounting—remain underexplored. The same applies to organisational perspectives, including contingency-based analyses that could improve our understanding of how management systems operate within organisations.

Most documents adopt a descriptive or exploratory rather than explanatory approach. Management accounting aims to support managerial decision-making and problem-solving, yet much of the research remains prescriptive, relying on case studies that, while practical, are difficult to generalise. This kind of research can serve as a preliminary step, but more systematic empirical studies are needed to enable comparison and assess the consistency of findings. Besides, given the diversity of the restaurant industry, future research should also incorporate different contextual factors such as restaurant categories and business models.

This research has organisational and managerial implications. It suggests that restaurant managers should move beyond traditional assumptions about cost structures and pay greater attention to cost behaviour, particularly with regard to labour costs. These represent the second largest operating expense and are a recognised capacity constraint, requiring informed managerial decision-making. Additionally, the limited evidence on management control systems and other MAPs suggests that managers could benefit from critically evaluating their current use of MAPs and leveraging the potential of RMSs to inform managerial decision-making. Finally, this study can help to raise awareness of managers of cost and MAPs to improve performance.

This study is not without limitations. The review included articles, books, and conference proceedings, but incorporating other sources, such as doctoral theses, could further enrich the results. In addition, only English-language academic publications were analysed, which reflects common practice in systematic literature reviews but may exclude studies published in other languages. In an industry that is overwhelmingly composed of SMEs, incorporating additional sources could further enrich the understanding of management accounting practices beyond the mainstream academic literature. Moreover, the co-word analysis relied on a topic scheme developed by the authors, which may introduce some subjectivity in topic selection and coding, despite the use of a multi-coder procedure. Finally, the analysis did not account for citation-based measures of document influence. Despite these limitations, this work provides a comprehensive review of the most significant research on cost and management accounting in the restaurant industry.

Supplemental material

Supplemental Material - Mapping cost management research in the restaurant industry: A systematic review and research agenda

Supplemental Material for Mapping cost management research in the restaurant industry: A systematic review and research agenda by Amparo Ruiz-Fernández, María Jesús Bonilla-Priego, Juan-José Nájera-Sánchez, Eva Pelechano-Barahona in Tourism and Hospitality Research

Footnotes

ORCID iDs

Ethical considerations

This article does not contain any studies with human or animal participants.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Madrid Regional Government (PHS-2024/PH-HUM-294), Ministry of Science and Innovation (Spain) (PID2023-14010NB-100), Research Group Strategor of Universidad Rey Juan Carlos and Universidad Francisco de Vitoria.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data will be made available on request

Supplemental material

Supplemental material for this article is available online.