Abstract

This study examines how sudden shifts in tourism demand affect the Earnings Management (EM) strategies of hotel firms, using Portuguese companies as the study context. This paper uses accounting data from 490 non-listed Portuguese hotel firms collected from the ORBIS database over the 2016–2021 period. The presence of EM practices is investigated using the methodology developed by Burgstahler and Dichev (1997), while panel data regression is used to explore the impact of the COVID-19 pandemic on the sample firms’ EM practices. Portuguese hotel firms use EM practices upward or downward depending on their starting position. In general, these firms tend to manipulate results in order to avoid reporting losses, a practice they intensify when faced with a sharp decline in demand. In particular, this paper finds that, during the recent pandemic period, such companies have aggressively used the discretionary component of accruals to disclose higher results. To the best of our knowledge, this is the first article exploring how a sudden decline in tourism demand affects the EM behaviour of firms operating in the hospitality sector. Our findings have important implications for such companies’ stakeholders, especially investors and regulators.

Introduction

The Travel and Tourism (T&T) sector is a major contributor to the Gross Domestic Product (GDP) of many nations. For instance, in 2019, tourism had one of its best performances, accounting for 10.3% of the global GDP and providing 10.4% of the available jobs (WTTC, 2020). This results from very high levels of demand for tourism services and activities. In particular, international tourist arrivals grew at an average annual rate of more than 5% during the last decade (OECD, 2020), peaking at 1.5 billion in 2019. In the same year, international visitors spent in tourism-related services and activities about USD 1.7 trillion and their domestic counterparts around USD 4.3 trillion (WTTC, 2021).

Nevertheless, at the beginning of 2020, the world had to deal with a sanitary crisis that required extreme measures such as social distancing, border closures and the interruption of external supply chains. As such, the COVID-19 pandemic severely affected the world economy, causing a 3.3% drop in the global GDP (WTTC, 2022a), also having a profound impact on the tourism industry (e.g. Clark et al., 2021; Dreshaj et al., 2022; Henseler et al., 2022). In fact, the pandemic completely disrupted tourism demand (Chen and Tan, 2025; Henseler et al., 2022; Mwamwaja and Mlozi, 2020) to an unprecedented level and much more than around previous global negative events, such as the terrorist attacks on 11 September 2001, the 2003 SARS epidemic or the 2008 economic and financial crisis (Henseler et al., 2022). Not surprisingly, the T&T industry lost 62 million jobs in 2020 relative to 2019 (WTTC, 2021), with the sector’s contribution to the global GDP plummeting by 50.4% (WTTC, 2021).

In their current activity and influenced by several factors, companies may engage in Earnings Management (EM), which is considered a “purposeful intervention in the external financial reporting process, with the intent of obtaining some private gain” (Schipper, 1989: 92), that occurs when “managers use judgement in financial reporting and in structuring transactions to alter financial reports to either mislead some stakeholders about the underlying economic performance of the company or to influence contractual outcomes that depend on reported accounting numbers” (Healy and Wahlen, 1999: 368). EM can be carried out using two main techniques: Accruals-based Earnings Management (AEM) and Real Earnings Management (REM). While AEM implies that managers use their discretion in accounting methods and/or estimates to prepare financial statements, REM requires managers to make operating decisions (e.g. manipulating sales by offering price discounts of light credit terms, reducing discretionary expenditures or overproducing to spread fixed costs and lower the cost of goods sold) that affect cash-flow levels and is easier to camouflage as normal activity, making it more difficult for stakeholders to detect it (Kothari et al., 2016; Roychowdhury, 2006; Ruiz, 2016; Zang, 2012).

Although scarce, the empirical evidence on EM within the hospitality industry confirms the presence of such practices (Costa and Mota, 2021; Jiao and Lu, 2019; Paiva and Lourenço, 2016; Parte-Esteban and Alberca-Oliver, 2016; Poretti et al., 2020). Nevertheless, the extant literature is mainly focused on the magnitude of the absolute value of Discretionary Accruals (DA) instead of its real value, missing the effect of the manipulation that is being applied to the earnings component (Gonçalves et al., 2024). Also, the existing studies analyse listed firms or a combination of listed and non-listed firms, which may bias results since the influence of the capital markets faced by the former affects their behaviour (Campa, 2019; Lin and Li, 2012). Furthermore, the literature on EM in the hospitality industry does not provide evidence of how the business agents operating in this important sector use EM practices to deal with a sharp and unexpected reduction in tourism demand. In fact, Poretti et al. (2024) have recently called for the necessity of studying the practices of unlisted EM hospitality companies and analysing the impact of an exogenous shock, such as COVID-19, on such practices.

In order to fulfil these research gaps and address the call of Poretti et al. (2024), this study resorts to a sample of 490 Portuguese non-listed hotel firms, with data collected from 2016 to 2021 and finds that Portuguese hotel firms manage earnings through discretionary accruals to alter their financial reports, a practice they intensify when facing a sharp decline in demand, as during the recent pandemic period, aggressively resorting to discretionary accruals to increase their reported earnings.

Background and research hypotheses

Earnings management in the hospitality industry

The study of the EM behaviour of tourism-related companies is particularly interesting. In fact, traditionally this industry has a high proportion of tangible assets and high fixed costs (Chen, 2010; Turner and Guilding, 2011) although there is a gradual shift towards asset-light and/or fee-based strategies (Poretti et al., 2024), high debt-to-equity ratios and financial risk (Li and Singal, 2019; Serrasqueiro and Nunes, 2014; Singal, 2015; Tang and Jang, 2007), and significant expenditures on human resources (Jiao and Lu, 2019; Shin and Hong, 2020). Also, seasonality, cyclicity and very high levels of competition are relevant intrinsic characteristics of such an industry (Chen, 2010; Jiao and Lu, 2019; Poretti et al., 2020; Yeh, 2019).

Nevertheless, only a few studies explore the presence of EM within the hospitality industry (Gonçalves et al., 2024). The limited empirical evidence, however, suggests that such practices are influenced by firm-specific characteristics such as size, growth opportunities or leverage (Paiva and Lourenço, 2016; Parte-Esteban and García, 2014; Poretti et al., 2020), country factors like the legal systems or the level of investor protection (Paiva and Lourenço, 2016; Poretti et al., 2020) and macroeconomic and regional factors such as the hotel occupancy rates, the number of arrivals or the number of visitors staying overnight (Parte-Esteban and Alberca-Oliver, 2016). There is also some evidence that EM behaviour may differ across industry segments (Jiao and Lu, 2019; Paiva and Lourenço, 2016) and that financial crises influence the behaviour of hospitality managers (Parte-Esteban and García, 2014; Seetah, 2017).

Costa and Mota (2021) is the only paper looking at the Portuguese case. Using a sample of 1615 listed and non-listed firms in the 2007 to 2013 period and focusing only on the small positive results segment, they conclude that, in such context, EM practices are, in general, used to avoid reporting losses. However, companies belonging to different segments may also manipulate their results. Also, in their article, the authors mix listed and unlisted firms in the sample, which can affect the results since listed and unlisted firms have distinct characteristics and face different motivations, determinants and consequences when engaging in EM (Burgstahler et al., 2006; Campa, 2019; Coppens and Peek, 2005). In fact, there is evidence that non-listed firms present higher levels of EM given that they are not under the pressure of capital markets nor legally obliged to apply transparency norms and have lower auditing requirements (Burgstahler et al., 2006). Furthermore, Costa and Mota’s (2021) sample comprehend the financial crisis of 2008, but the authors do not explore its impact on the sector’s EM practices. In contrast, our research aims to deepen the understanding of Portuguese hotels by analysing the EM behaviour of non-listed firms exclusively and across the entire spectrum of the results segment, looking at a more recent period in which the tourism industry has seen significant growth (World Tourism Organization, 2021), but also by exploring the question of how a sudden change in tourism demand, caused by the COVID-19 crisis, impacts this reporting behaviour.

COVID-19 and earnings management

Recent empirical works suggest that the COVID-19 pandemic influences EM practices both at the country and the industry level. For instance, Azizah (2021) compare the first quarter of 2019 with the first quarter of 2020 and concludes that Indonesian-listed manufacturing companies engaged less in EM practices during the coronavirus pandemic than before such a dramatic event. Conversely, resorting to a sample of listed firms from 15 European countries, Lassoued and Khanchel (2021) find that, during the COVID-19 pandemic, firms attempt to rebuild investors’ and shareholders’ confidence by manipulating earnings upwards and minimising reported losses. Similar conclusions are put forward by Yan et al. (2022) and Aljughaiman et al. (2023), both of which consider a sample of Chinese-listed firms. Their results reveal that the COVID-19 shock intensifies companies’ EM behaviour, which leads to upward earnings manipulation, especially when financial constraints are binding. Yan et al. (2022) also show that their sample firms engage in EM differently depending on whether or not they belong to an industry severely affected by the COVID-19’s epidemic prevention and control policies. Aljughaiman et al. (2023) add to the existing literature by showing that listed companies affected by the pandemic are more likely to engage in accruals-based EM than real activities-based EM. Finally, studying non-financial unlisted Polish companies, Lizińska and Czapiewski (2023) find that discretionary accruals decline significantly during the COVID-19 crisis, while real activities-based EM increases.

Research hypotheses

Previous studies report that hospitality firms manage their earnings to achieve small and positive results (Costa and Mota, 2021; Jiao and Lu, 2019; Parte-Esteban and Alberca-Oliver, 2016; Parte-Esteban and Devesa, 2011a, 2011b; Parte-Esteban et al., 2011). The study of the Portuguese case is interesting for two reasons. First, the importance of the T&T sector has steadily increased in Portugal in the last years. This sector accounted for 16.5% of the total economy in 2019 (WTTC, 2020), while in 2023, in a recovery phase from the pandemic crisis, the sector’s contribution to the Portuguese’s total economic output further increased to 19.6% (WTTC, 2024).

Second, such dramatic growth is fuelled by considerable bank financing and foreign investment (Mafrolla and D’Amico, 2017; OECD, 2020). This leads to an interesting paradox. On the one hand, the previous literature shows that firms with high needs for external capital may avoid manipulating earnings to increase the quality of financial reporting and benefit from a lower cost of capital (Francis et al., 2004). On the other hand, there is evidence that operating in highly competitive industries leads companies to manipulate their reported results to avoid reporting losses and consolidate their market position (Datta et al., 2013; Wasiuzzaman et al., 2015). Given this context, this study defines the first research hypothesis as follows:

Hospitality firms in Portugal engage in EM to disclose small and positive net earnings.

Managers can manipulate the earnings component by exerting their professional judgment on accounting methods or estimates or by making operational decisions that deliberately affect their firm’s cash flow level (Ruiz, 2016). Accounting accruals have been widely studied in the EM’s context, outside and inside of the hospitality industry (Costa and Mota, 2021; Gim et al., 2019; Jiao and Lu, 2019; Paiva and Lourenço, 2016; Parte-Esteban and Devesa, 2011b; Poretti et al., 2020; Ruiz, 2016). Importantly, there is evidence that the hotel sector appears to rely more on accruals-based EM (Jiao and Lu, 2019; Yan et al., 2022) since such practices are less costly for managers (Parte-Esteban and Devesa, 2011a). As such, this paper explores its second research hypothesis, which is defined as follows:

Portuguese hospitality managers use accounting accruals to manipulate results in order to report financial information in line with their objectives.

In 2019, Portuguese tourism was at its best. The sector’s GDP grew by 4.2% and the country was ranked twelfth as the most competitive tourist destination, receiving the Best Destination in the World award (European edition). However, the COVID-19 pandemic led to a very significant crisis (Guedes et al., 2022). Compared to 2019, in 2020, the Portuguese tourism sector almost halved its contribution to the country’s GDP, reduced the direct jobs by 16.5% and recorded a significant drop of 73.7% (41.1%) in non-resident (domestic) tourist arrivals (travelling) (Brilhante and Rocha, 2023; Instituto Nacional de Estatística, 2021; WTTC, 2022b). As a result, tourist accommodation establishments sustained a loss of 66.3% in their revenue (Instituto Nacional de Estatística, 2021). Therefore, it is important to examine how this situation influenced the EM behaviour of Portuguese hotel firms, as the previous literature suggests that such practices are widespread during challenging economic periods. (Byard et al., 2007; Chia et al., 2007; Kousenidis et al., 2013; Lisboa and Kacharava, 2018). This leads to the final research hypothesis of this article:

The COVID-19 pandemic crisis influenced the EM practices of Portuguese hospitality firms.

Data, variables and methodology

Sample selection

This paper collects data for all Portuguese companies registered with the Standard Industrial Code (SIC) 70 (Hotels, rooming houses, camps and other lodging places) as the primary code, available on the ORBIS database between 2016 and 2021. Listed firms, companies not incorporated as either “Limited liability company” or “Public limited company” according to Portuguese law, and those reporting consolidated financial statements are then deleted. After dropping all firm-year observations with missing information, the final sample is composed of 490 non-listed firms with complete data for the period from 2016 to 2021.

The reported net earnings

Following the extant literature, this investigation applies the methodology of Burgstahler and Dichev (1997) to test H1. According to the authors, unmanipulated earnings present a smooth frequency distribution. Conversely, if the distribution presents uncommonly low (high) frequencies of firms presenting small losses (profits), there is evidence of EM. Therefore, we calculate net earnings,

The reported earnings before discretionary accruals

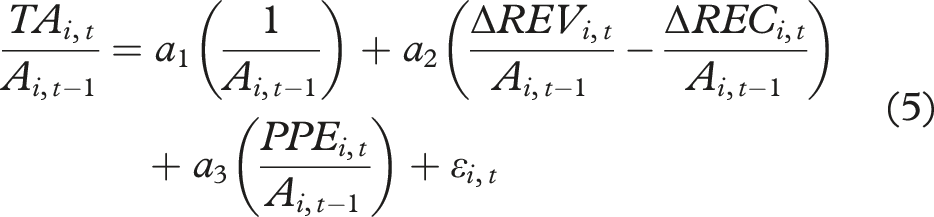

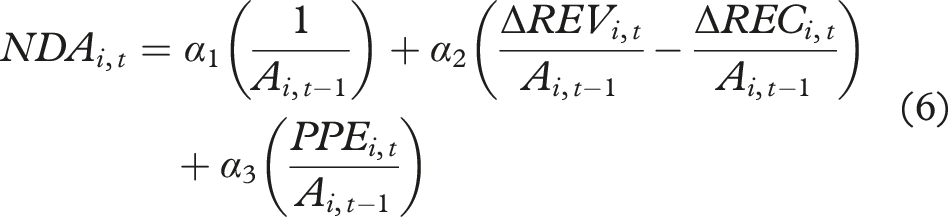

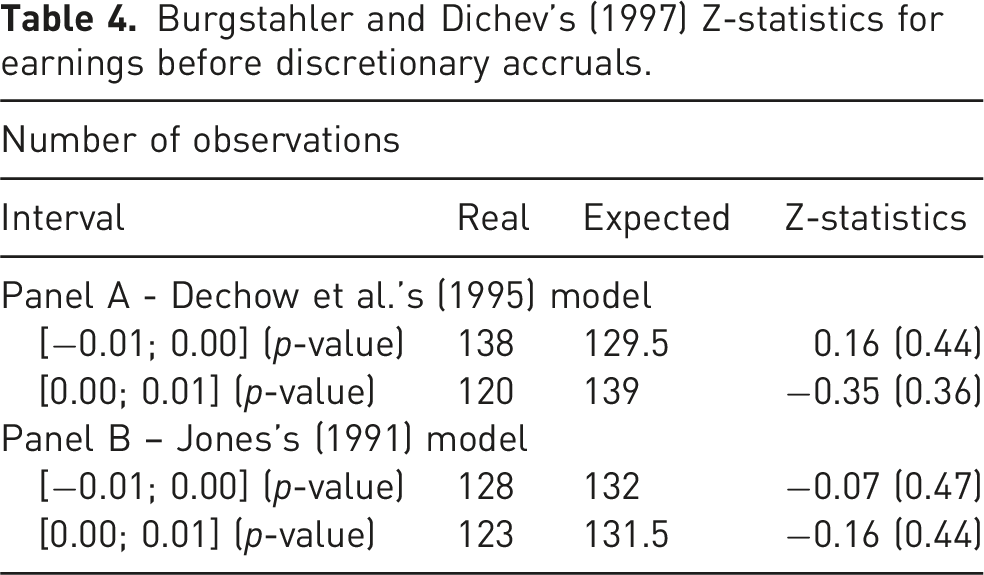

As mentioned above, reported earnings show a discontinuity around zero in the presence of EM practices. In this sense, we can expect a smooth distribution of earnings before the accounting manipulation (Coelho, 2022; Ferreira et al., 2020; Leone and Van Horn, 2005). We investigate H2 based on these arguments and resorting to the methodology of Burgstahler and Dichev (1997). In particular, the Earnings Before Discretionary Accruals of company

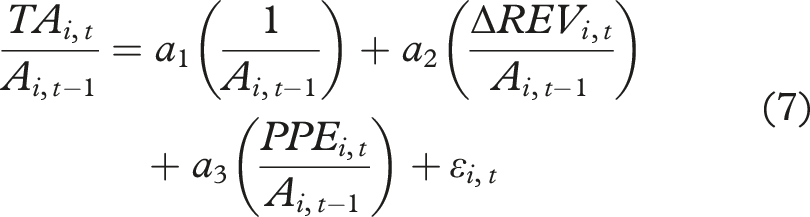

Following Parte-Esteban and Devesa (2011b), Paiva and Lourenço (2016) and Poretti et al. (2020), this paper confirms the robustness of the results by replicating the process with the Jones Model (Jones, 1991). It differs from the modified Jones Model by assuming that earnings can not be managed through revenues and, thus, that revenues are non-discretionary (Dechow et al., 1995). Therefore, the receivables component

As with the modified version of the Jones Model (Dechow et al., 1995), Jones (1991) estimates

The impact of Covid-19 on the EM practices of hospitality firms

This study resorts regression analysis to explore how the COVID-19 pandemic affects the EM behaviour of Portuguese hospitality firms. Drawing on Paiva and Lourenço (2016), Poretti et al. (2020) and Costa and Mota (2021), this paper employs the following panel regression model:

Consistent with prior literature, six control variables are used in Equation (9) in

Results

The reported net earnings

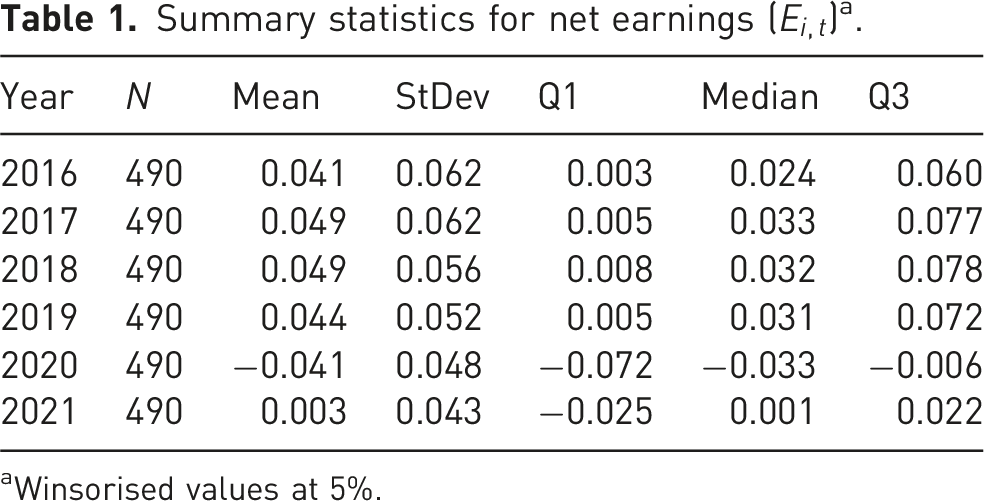

Summary statistics for net earnings (

aWinsorised values at 5%.

The reported statistics show positive average net earnings from 2016 to 2019, which coincides with a high-performance period of the tourism sector in Portugal. The descriptive statistics also highlight the impact of the COVID-19 pandemic on the sample firms’ profitability. As can be seen, companies were caught by surprise and their results plummeted, leading to the negative net earnings reported in 2020. The year 2021 was, however, better: the mean and median net earnings are now positive (although close to zero).

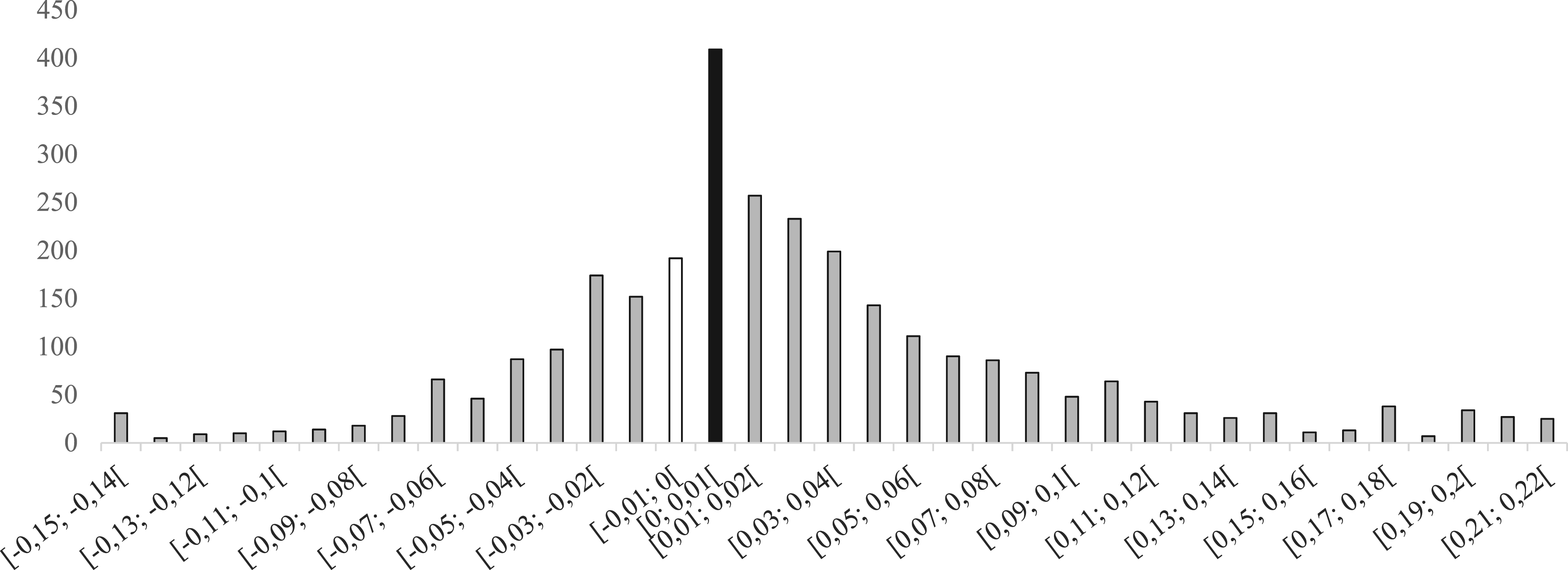

According to Burgstahler and Dichev (1997), companies frequently avoid reporting losses, a behaviour that can be observed through the frequency histogram of the net earnings. Figure 1 represents the case of the sample firms and, as can be seen, the histogram seems to denote a discontinuity around zero. In particular, the number of companies disclosing small losses seems to be lower than expected (i.e. those in the first interval to the left of zero, highlighted in white), while the number of companies disclosing small profits seems to be much higher than expected (i.e. those in the first interval to the right of zero, highlighted in black). Histogram of the frequency of distribution of cross-sectional net earnings.

Burgstahler and Dichev’s (1997) Z-statistics for net earnings.

The reported earnings before discretionary accruals

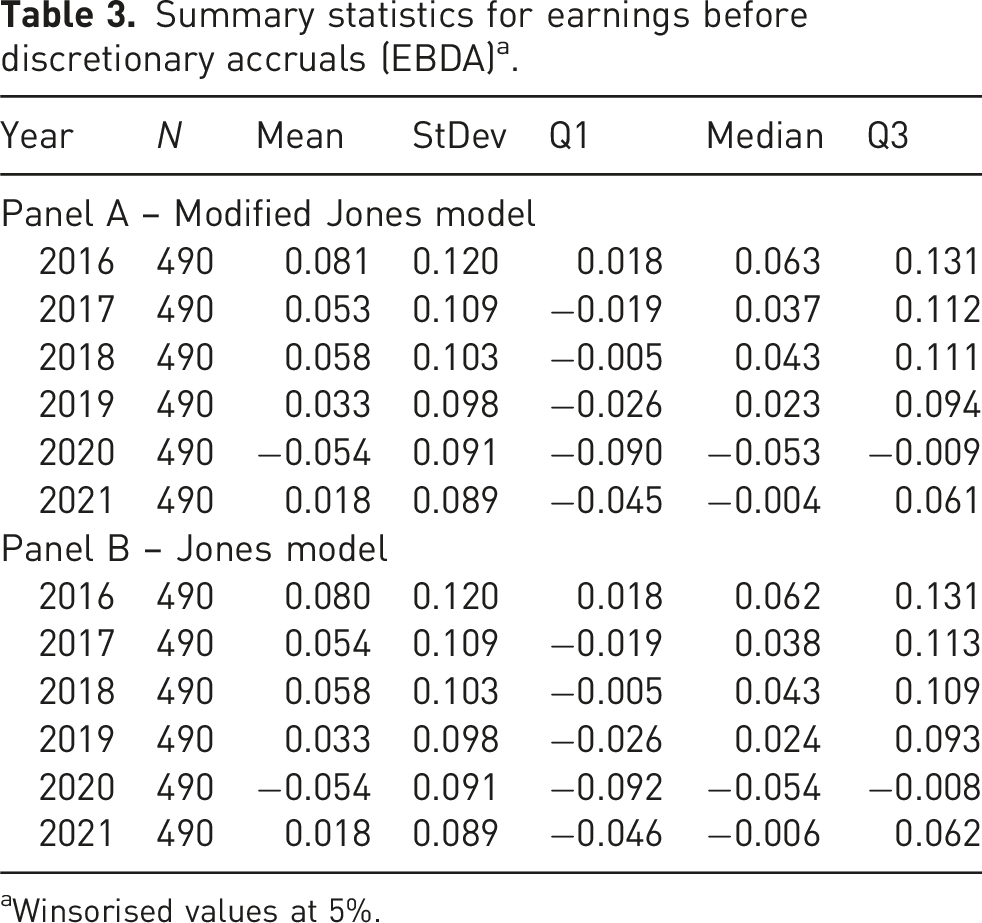

Summary statistics for earnings before discretionary accruals (EBDA) a .

aWinsorised values at 5%.

As can be seen, in general, the average and median earnings without the DA’s effect are higher than that of the reported earnings, suggesting that managers use their discretionary accounting choices to manipulate earnings downwards. This conclusion, however, does not hold for 2020. In this year, EBDA is lower than reported earnings, both in average terms and in all three quartiles. Hence, the evidence suggests that, in the presence of an event that drastically reduced demand, Portuguese hotel companies resort to aggressive EM practices to increase the disclosed net earnings.

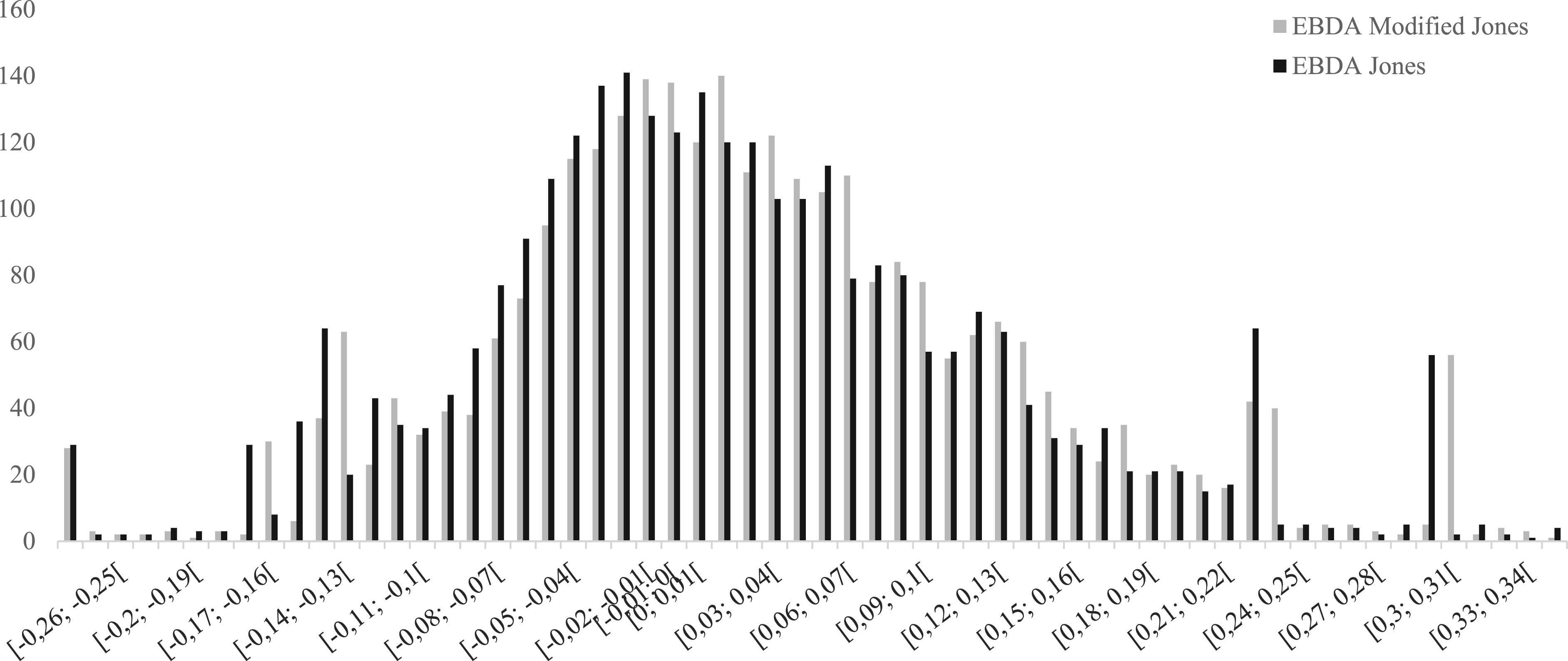

Figure 2 shows the frequency histogram of EBDA. As can be seen, there is no sign of a discontinuity around zero, a conclusion that holds when using the models of Jones (1991) and the Dechow et al. (1995) to measure DA. While the distribution of reported earnings is centred in zero, the distribution of EBDA (i.e. the pre-managed earnings) moves to the left, corroborating the idea that Portuguese hospitality firms manage earnings to increase results, namely to report small positive earnings instead of reporting losses. Furthermore, Figure 2 shows that, in a favourable economic environment, the companies with better results manage earnings downwards since the right side of the graph (i.e. that with positive EBDA values) presents higher frequencies than in the reported earnings’ histogram. Histogram of the frequency of distribution of cross-sectional earnings before discretionary accruals.

Burgstahler and Dichev’s (1997) Z-statistics for earnings before discretionary accruals.

Thus, this paper’s findings show that the earnings component of Portuguese non-listed hotel firms behave differently depending on whether one considers the DA’s effect or not, suggesting that earnings are managed through accounting accruals. This conclusion supports the evidence collected from other studies focusing on the hotel industry (Costa and Mota, 2021; Jiao and Lu, 2019; Parte-Esteban and Devesa, 2011a, 2011b; Parte-Esteban et al., 2011) and leads us to support H2.

Evidence of the impact of Covid-19 on the EM practices of hospitality firms

Summary statistics – variables in the regression model.

aWinsorised values at 5%. All variables are defined in Appendix A.

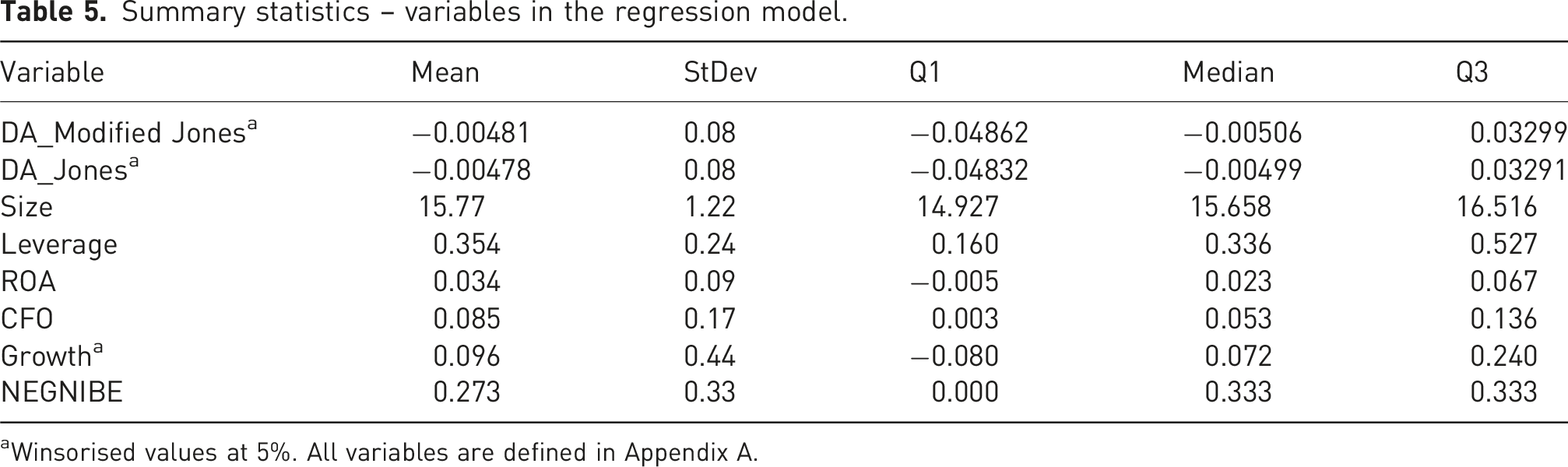

The statistics of DA are very similar when estimated with the modified Jones model and the Jones model. The mean and median estimates for the Dechow et al. (1995) DA is −0.00481 (−0.00506), and that for the Jones’s (1991) model is −0.00478 (−0.00499), revealing that Portuguese hospitality firms engage in EM practices mainly to decrease their reported earnings, which is consistent with this paper’s previous findings.

Table 5 shows that the sample companies’ SIZE is quite homogeneous, firms present high financial LEVERAGE and low ROA, while the CFO ratio is in line with the industry’s characterisation worldwide (see, for instance, Paiva and Lourenço, 2016). GROWTH is, however, relatively low when one compares the results in Table 5 with the evidence tabulated by Paiva and Lourenço (2016). Finally, NEGNIBE tells us that most of the sample companies present only 1 year of negative results over each consecutive 3-year period (mean = 27.3%; median = 33.3%; Q3 = 33.3%); furthermore, 25% of the sample companies do not register a single year with negative results.

Spearman correlation coefficients.

All variables are defined in Appendix A. *, **, *** indicate statistical significance at the 10, 5 and 1% level, respectively.

VIF test of multicollinearity.

aWinsorised values at 5%. All variables are defined in Appendix A.

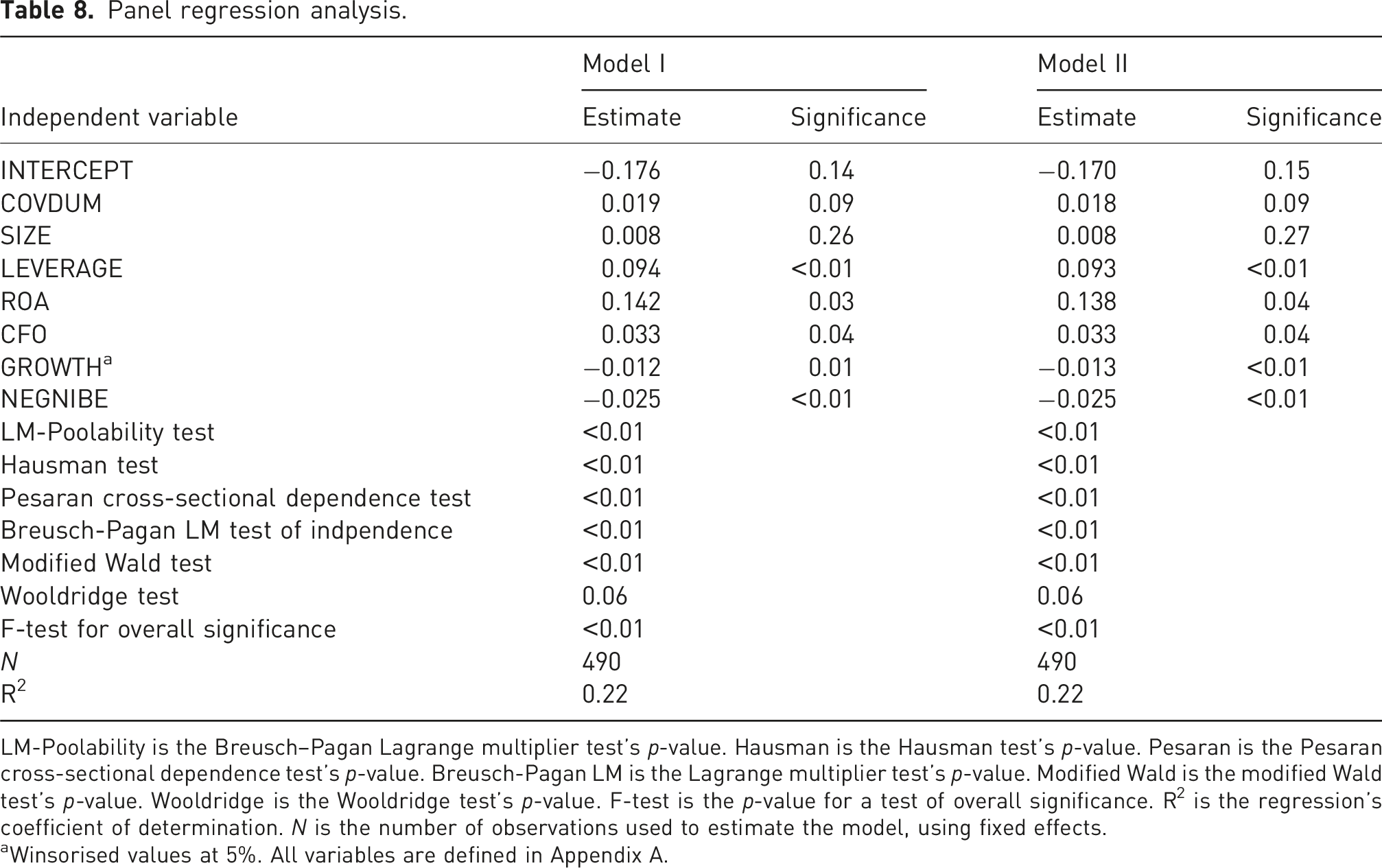

Panel regression analysis.

LM-Poolability is the Breusch–Pagan Lagrange multiplier test’s p-value. Hausman is the Hausman test’s p-value. Pesaran is the Pesaran cross-sectional dependence test’s p-value. Breusch-Pagan LM is the Lagrange multiplier test’s p-value. Modified Wald is the modified Wald test’s p-value. Wooldridge is the Wooldridge test’s p-value. F-test is the p-value for a test of overall significance. R2 is the regression’s coefficient of determination. N is the number of observations used to estimate the model, using fixed effects.

aWinsorised values at 5%. All variables are defined in Appendix A.

As can be seen, Table 8 shows a positive and statistically significant value for COVDUM (

Furthermore, the hospitality industry is highly competitive and reputation, brand recognition and loyalty are critical (Rhou and Singal, 2020). Based on this rationale, companies started to voluntarily assume the social and environmental impact of their decisions, which is named Corporate Social Responsibility (CSR), reporting “actions that appear to promote some social good beyond the interests of the company and what is required by law” (McWilliams and Siegel, 2001: 117). CSR practices are considered an investment that can be instrumental in achieving bottom-line financial performance, influencing several aspects of organisational performance, namely the financial reporting quality (Rhou and Singal, 2020). In fact, the study of Xiao and Xi (2021), which explored the moderating effect of CSR in the EM practices during the COVID-19 outbreak, revealed that there was an increase in AEM and a significant decline in REM in companies in the most severely affected regions, but less pronounced in companies with higher CSR performance. This behaviour is also reflected in our results to some extent, as there was an increase in AEM during the pandemic period, which is expected to have been widespread, considering that the adoption of CSR practices in Portugal is not yet widespread and only began to be required for large companies from 2022 onwards.

The results presented in Table 8 also provide evidence of other factors that may affect the EM practices of the companies under study. Regardless of whether we estimate DA using the modified Jones model (Model I) or its original version (Model II), SIZE does not seem to affect the EM practices, while LEVERAGE, ROA and CFO positively affect DA, suggesting that highly leveraged companies and firms with high ROA and CFO ratios are more likely to employ EM-based strategies to increase their disclosed earnings, something already noted by Paiva and Lourenço (2016), Gim et al. (2019) and Costa and Mota (2021), among others. Interestingly, to the best of our knowledge, this is the first paper to document that hospitality firms facing higher growth opportunities and those reporting successive negative results tend to manage earnings downwards. The negative impact of GROWTH on DA is supported by the Political Cost Hypothesis of Watts and Zimmerman (1978), which posits that firms manage earnings downwards to minimise the likelihood and size of wealth transfers imposed politically by government legislation or regulation, such as higher taxes. As growth opportunities increase, firms are expected to be more profitable, which may result in higher political exposure (Monti-Belkaoui and Riahi-Belkaoui, 1998). On the other hand, the negative association between NEGNIBE and DA is referred to in the literature as “taking the big bath” and is based on the assumption that, in difficult periods such as an economic downturn, managers prefer to reduce results and sift earnings to future periods to create an idea of improvement in the company’s financial performance (Degeorge et al., 1999; Hope and Wang, 2018; Parte-Esteban and Devesa, 2011b).

Conclusions and implications

Main conclusions

The main purpose of this research was to examine the EM behaviour of hotels operating in Portugal, a country whose economy is highly dependent on the tourism sector, and to investigate whether their EM practices change in the sequence of abrupt shifts in tourism demand, as happened during the COVID-19 crisis, answering to a call of Poretti et al. (2024).

This investigation finds that Portuguese non-listed hotels use the discretionary component of accounting accruals to understate their economic performance. However, this behaviour does not remain immutable and can change in the face of unfavourable business conditions. In particular, this investigation reveals that, when facing sharp falls in tourism demand caused by an extreme negative event such as the COVID-19 pandemic, management reacts by engaging in income-increasing EM. Furthermore, regardless of the economic context, Portuguese hotel firms engage in EM to avoid reporting losses in earnings, which is in line with previous studies of Parte-Esteban and Devesa (2011a, 2011b), Jiao and Lu (2019) and Costa and Mota (2021). In addition, this investigation shows that managers engage in EM practices differently according to their pre-managed earnings positioning. Companies with negative pre-managed earnings tend to use EM to increase results, especially to avoid reporting losses, while companies with significant positive pre-managed earnings tend to manage them in a downward direction.

This study also resorts to panel regression analysis to explore the impact of the COVID-19 pandemic crisis on the EM behaviour of Portuguese hospitality firms. The results show that, when facing such a dramatic event, Portuguese hotels use discretionary accruals to manage earnings upwards. Yet, there is also evidence that in the pre-event period, some companies manage earnings downwards, which may be related to their outstanding performances and/or their desire to avoid sanctions, like paying higher taxes or undergo stricter supervision and regulation (Hamza and Zaatir, 2020; Watts and Zimmerman, 1978). Furthermore, as documented in previous studies, this paper finds that Portuguese hotel managers use their discretionary power in accounting accruals to increase their disclosed earnings in the presence of higher debt levels (Costa and Mota, 2021; Paiva and Lourenço, 2016), higher return on assets (ROA) (Gim et al., 2019) and higher cash flow from operations (CFO) (Paiva and Lourenço, 2016). However, when facing higher growth opportunities and a higher frequency of negative earnings, the accounting accruals are used to reduce the earnings disclosed by these companies. These results are supported by Watts and Zimmerman’s (1978) Political Cost Hypothesis and the “big bath” EM strategy, respectively.

Theoretical and practical implications

This study makes three main contributions to the literature. First, it explores the behaviour of Portuguese hospitality managers regarding their disclosed net earnings, something that is not well documented in previous studies (Gonçalves et al., 2024). Also, although accruals-based EM is widely studied, most of the existing literature on EM within the hospitality industry only explores its magnitude (i.e. the absolute value of DA) (Gonçalves et al., 2024). Therefore, this paper contributes to the literature by analysing the real value of DA to conclude that, under normal circumstances, such Portuguese hotel managers tend to use DA to manipulate their results to report lower earnings (i.e. DA is negative).

Second, to the best of our knowledge, this is the first paper relating the changes in tourist demand to the practice of EM by looking at a particular event that devastated the T&T sector, namely the COVID-19 pandemic crisis. In this sense, this paper finds that Portuguese hospitality firms change their behaviour in the presence of such a dramatic event by aggressively using discretionary accruals to increase their reported earnings (i.e. DA is positive). This is a significant contribution since there is evidence that crisis periods influence the behaviour of hospitality managers (Parte-Esteban and García, 2014; Seetah, 2017) and considering that Costa and Mota (2021) did not analyse the impact of the 2008 crisis on the EM practices of Portuguese hotels.

Finally, this paper analyses non-listed hotels exclusively, providing a significant contribution to the extant literature that is focused mainly on listed firms or a combination of listed and non-listed firms without any distinction (Gonçalves et al., 2024). In fact, listed and non-listed firms have distinct characteristics and motivations to engage in EM. Furthermore, most firms in the hospitality sector are not publicly traded (Parte-Esteban and Alberca-Oliver, 2016) and, given their nature, have particular incentives to manage their earnings as they are not under the pressure of capital markets (Arnedo et al., 2007; Campa and Camacho-Miñano, 2014; Mafrolla and D’Amico, 2017; Watts and Zimmerman, 1978). Together, these arguments clearly justify separating listed from non-listed firms when investigating the EM behaviour in the hospitality sector.

This research also has important practical implications. Tourism is one of the key sectors of the global economy and one with the highest potential for attracting investment. Therefore, investors and other stakeholders must have access to reliable financial statements to support their decisions and analyses, something that is questionable in the presence of EM. This research reveals that Portuguese hospitality firms resort to EM tactics, primarily to circumvent reporting losses, which should be relevant for their stakeholders. Furthermore, this paper shows that such a tendency is even more clear when such companies face a disruption in tourism demand. Such manoeuvres, that end up boosting the firms’ reported net income, may stem from the necessity to ensure consistent financing and/or to maintain heightened investor confidence and investment willingness. However, these practices clearly harm the interests of the stakeholders, stressing the importance of this paper’s empirical results for practice.

On the other hand, the empirical evidence of this study shows that the standard behaviour of Portuguese hotel managers is to manipulate earnings downwards. By adopting this behaviour, Portuguese non-listed hotels may reduce the amount of taxes paid, as preconised by the Political Cost Hypothesis of Watts and Zimmerman (1978), something that policymakers must consider.

Limitations and suggestions for future research

This study is not free from limitations. Although we resort to two of the most widely accepted models to estimate discretionary accruals, there are some alternative models that could be applied in future research to confirm the robustness of the presented results. For example, Dechow and Dichev (2002) developed the modified Jones model proposed by Dechow et al. (1995) to consider the relation between current period working capital accruals and operating cash flows in the prior, current and future periods, while Kothari et al. (2005), developed the same model to capture the impact of performance on discretionary accruals.

Moreover, earnings can be managed through real activities, which can be a complement or a substitute for AEM. The economic context, institutional factors and the companies’ industry characteristics influence such a decision. For example, managers tend to choose REM in countries where the legal environment constrains AEM, i.e., countries with stronger investor protection (Enomoto et al., 2015; Leuz et al., 2003), while the hotel industry, which is intensive in fixed assets, provides managers with an opportunity to manage earnings through AEM (Jiao and Lu, 2019). Nevertheless, there is a lack of evidence on how the EM behaviour of hotel managers is affected when facing negative external shocks that reduce tourism demand (Henseler et al., 2022; Mwamwaja and Mlozi, 2020; Seetah, 2017). Therefore, to mitigate this limitation, further research could explore the presence of REM, namely through the Roychowdhury's (2006) model, which uses several proxies for estimating abnormal levels of cash flow from operations, abnormal levels of production costs and discretionary expenses, to explore the effect of the simultaneous practice of intentional operating decisions to manage earnings.

A further limitation relates to the existence of unobserved intrinsic characteristics of companies, such as the profile of the manager, namely their propensity to take management risks, or access to unconventional credit lines. In fact, such unobserved characteristics may explain the EM behaviour of the companies studied and vice versa, raising questions of endogeneity. To mitigate this concern, robustness tests could be carried out in future research to validate the results.

An additional limitation of this study is the fact that it has only considered unlisted Portuguese firms, which disclose limited financial information, justifying the sample’s length. Given the specific characteristics of this country, namely the high economic and social dependence on tourism activity, the results of this research should be generalised with caution. Furthermore, Portugal’s institutional or sectoral specifics, for instance, whether the small-firm structure or government support schemes, might have affected the incentives for EM. For future investigation, we suggest studying a group of European countries with strong tourism activity (e.g., Italy, Greece, Spain) in order to ascertain whether countries with identical characteristics exhibit a similar EM behaviour or whether this is a country-specific effect. Also, considering that the COVID-19 pandemic has changed the dynamics of the tourism sector and tested the resilience levels of its participating companies, it would be interesting to understand whether the hotel sub-sector changed its behaviour after the recovery and extend this analysis to other tourism sub-sectors. Finally, it would also be relevant to explore different industries to ascertain whether non-touristic sectors reacted similarly.

Footnotes

Ethical considerations

This article does not contain any studies with human or animal participants.

Consent to participate

There are no human participants in this article and informed consent is not required.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper is financed by National Funds of the FCT – Portuguese Foundation for Science and Technology within the projects UIDB/ 04020/2020, UID/ ECO/04007/2020 and UI/BD/150797/2020.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author biographies

Appendix

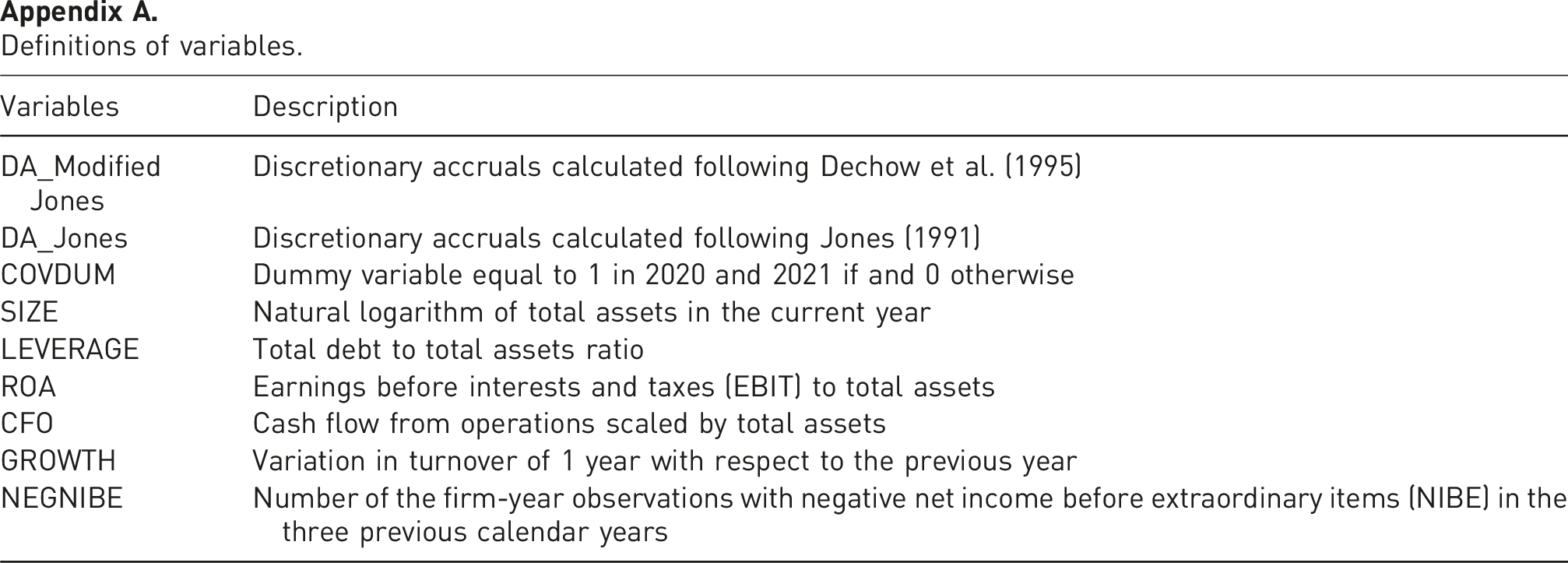

Definitions of variables.

Variables

Description

DA_Modified Jones

Discretionary accruals calculated following Dechow et al. (1995)

DA_Jones

Discretionary accruals calculated following Jones (1991)

COVDUM

Dummy variable equal to 1 in 2020 and 2021 if and 0 otherwise

SIZE

Natural logarithm of total assets in the current year

LEVERAGE

Total debt to total assets ratio

ROA

Earnings before interests and taxes (EBIT) to total assets

CFO

Cash flow from operations scaled by total assets

GROWTH

Variation in turnover of 1 year with respect to the previous year

NEGNIBE

Number of the firm-year observations with negative net income before extraordinary items (NIBE) in the three previous calendar years