Abstract

In an era where women's economic empowerment is of paramount importance, this study aims to unravel the mechanisms through which microfinance interventions can catalyse entrepreneurship among women in Pakistan. A stratified random sampling is conducted to ensure a representative sample of women entrepreneurs who use microfinance services. A total of 313 responses are obtained and subjected to statistical analysis is conducted using structural equation modelling, specifically Smart PLS (Partial Least Squares). The findings reveal that microfinance services significantly impact women's entrepreneurship endeavours. This effect is, in part, mediated by the enhancement of economic security, underlining the pivotal role of financial stability in fostering entrepreneurial pursuits among women. Furthermore, this research sheds light on the moderating influences of household decision-making dynamics, mobility, and prior work experience. The study underscores the importance of considering not only financial aspects but also sociocultural and experiential factors when designing microfinance interventions. The findings have implications for promoting entrepreneurship as an integral component of Sustainable Development Goals (SDGs), such as no poverty, gender equality, decent work and economic growth, and reduced inequality.

Keywords

Introduction

Microfinance has emerged as a contemporary development approach, offering financial and nonfinancial services to low-income individuals and communities to foster entrepreneurial activities and stimulate economic growth (Khavul et al., 2013). With a dual emphasis on poverty reduction and empowering marginalised populations, particularly women, microfinance has become a critical tool in international development debates (Khursheed, 2022). However, despite its substantial coverage in research, a universally accepted definition of microfinance remains elusive (Sriram and Upadhyayula, 2002). This ambiguity prompts a need for explicit articulation of the concept, as it encompasses a broader range of activities beyond small loans, including savings, insurance, money transfers, payments, and remittances (Littlefield and Rosenberg, 2004).

The correlation between microfinance and Sustainable Development Goal (SDG) – in particular, SDG 5, gender equality, aims to achieve gender equality and empower all women and girls (UN Environment, 2019) – becomes particularly evident when examining its role in the entrepreneurship-based empowerment of women. Microfinance plays a crucial role in achieving SDGs, specifically those related to gender equality and economic independence (Saner and Yiu, 2019). The intersection of women's entrepreneurship and microfinance is a potent force in attaining targets, fostering inclusive and sustained economic growth. By granting women control over their financial resources and enabling them to establish and manage their businesses, microfinance becomes a transformative agent that aligns with the broader objectives of the SDGs. The venture of a business is considered a significant contributor to societal financial development, with entrepreneurs playing an instrumental role in initiating and sustaining economic progress (Adula and Kant, 2022). Despite the increasing participation of women in entrepreneurial activities, gender-based economic inequalities persist, particularly in entrepreneurial activities in certain regions (Akula and Singh, 2022). Past studies highlight that a lack of initial capital often impedes women's participation in entrepreneurial pursuits (Bastian et al., 2023).

Microfinance institutions in Pakistan can address this capital limitation by offering microcredit and encouraging women's business participation. The supply of microcredit also has the potential to enhance women's economic security, a crucial component for entrepreneurial success in Pakistan. This study aims to unravel the intricate relationship between microfinance, microcredit, and self-help groups and their combined impact on women entrepreneurship. It explores the moderating role of women's economic stability and factors such as previous work experience, mobility, and decision-making in this interaction (Sharma, 2022). The intersection of Sustainable Development Goal (No Poverty) with microfinance and women entrepreneurship unveils a transformative pathway towards economic inclusivity. Microfinance catalyses breaking the cycle of poverty by providing financial tools tailored to empower women entrepreneurs (Raman et al., 2022). The symbiotic relationship between microfinance, women's entrepreneurship, and SDGs underscores the potential for targeted financial support to serve as a potent tool in the global effort to eradicate poverty and build resilient, economically vibrant societies. Microfinance, women's entrepreneurship, and SDGs are interconnected, emphasising the transformative power of focused financial interventions in promoting a more inclusive and just society while lowering gender-based economic disparities.

With an emphasis on empowering women in emerging economies, this research explores the critical role that microfinance and microcredit programmes play in reducing poverty and promoting economic growth. The research acknowledges that self-help groups have developed into dynamic forums for the exchange of resources and group mobilisation, empowering women to launch and grow their enterprises and thereby improving their financial situation (Hatoum et al., 2023). This study will, in addition, examine the economic feasibility of participating in self-help groups, obtaining small amounts of credit, and getting microfinance as important elements to promoting an upsurge in women entrepreneurship. Furthermore, the study looks at the methodological aspect of Women's Economic Security as a crucial intermediary mechanism bridging the gap between financial inclusion initiatives and successful female entrepreneurship. This research also attempts to significantly advance the multidisciplinary fields of entrepreneurship, development economics, and women's empowerment by analysing the intricate relationships between microfinance, female empowerment, and sustainable development. By throwing light on this complex subject, the study expands the existing body of knowledge and provides valuable insights for designing effective programs and policies. It is equally important to establish an atmosphere that supports women's success as business owners, ultimately promoting gender equality and long-term economic prosperity. Subsequently, this study may impact how programs and policies are designed by policymakers and institutional decision-makers responsible for fostering an atmosphere that encourages women to succeed as entrepreneurs. Deeply rooted in many SDGs, especially those concerning gender equality, decent employment and economic growth, poverty reduction, reduced inequality, and partnerships for broader global goals, microfinance emerges as a crucial tool with transformative potential.

Literature review

Theoretical foundation

In empowerment theory, empowerment is influenced by people's context (Sun et al., 2024). Social and historical characteristics influence the interest in empowerment. The desire for influence in a specific domain leads to individual initiative (Perkins and Zimmerman, 1995), which enables the acquisition of the necessary capabilities to engage in social activities (Chen et al., 2024). Empowerment theory helps people escape poverty by enabling them to obtain what is necessary to improve their lives (Eki et al., 2024). Women are a pillar of development through the efforts made within the family to improve living conditions in Pakistan, by expanding their capabilities (Sen, 1989) through the various dimensions that form the theoretical foundation of this study.

The increase in the family's economic capacity through economic empowerment occurs via access to resources that allow the exploration of opportunities (Buvinić and Furst-Nichols, 2013). Cultural practices and social connections influence a woman's ability to make economic decisions for herself and her family. Weak decision-making abilities regarding activities that strengthen the family's economy do not encourage initiative in wealth-generating activities (Kagotho and Vaughn, 2018). This context of household economic decision-making presents constraints that limit women's choices. In line with Sen (1989), capabilities represent the freedom of decision regarding what people, in a given context, want to be and achieve, that is, what is important to them, namely their economic empowerment. Certain social norms about property rights and difficulty obtaining family support determine personal achievement capacity and women's economic security. Fear of failure, self-assessment, and unfavourable social perceptions are barriers to engaging in entrepreneurial activities (Wieland et al., 2019).

Moreover, when society associates a woman's role with family obligations, social norms tend to view female entrepreneurship with reluctance and do not favour access to institutional and financial support (Wu et al., 2019). Initial financing affects the decision of women entrepreneurs to enter the market (Elkafrawi and Refai, 2022). This makes female entrepreneurship more likely to rely on informal networks as a source of financing. Community associations and specific groups serve as a source of low-cost credit.

Women entrepreneurs do not enjoy equal opportunities to men due to discriminatory sociocultural values and customs. This happens in developing countries in Asia, where women are deprived of independence (Raghuvanshi et al., 2017). Other studies on female entrepreneurship, conducted in countries such as Bangladesh and Nepal, confirm issues such as lack of social support, risk aversion, lack of self-confidence, sole responsibility for the family, and limited access to financing (Acharya et al., 1999; Das, 2000). Microfinance provides the poor with loans at an affordable interest rate, without requiring collateral, thus creating employment and income opportunities. Access to microfinance influences the household income, helps improve the standard of living for the poor, and reduces poverty (Choudhury et al., 2017). This economic development enhances social and human development, as it expands a person's capabilities to do and be what they aspire to in life, resulting from the expansion of choices, to achieve SDG 5, particularly gender equality and the empowerment of all women and girls.

Hypothesis development

The importance of microfinance in fostering small-scale businesses by women

Microfinance is conceptually distinct throughout the world; however, it is also obvious that practices and implementation programs that have been successful in one nation may not be successful in another. In this regard, Muhammad Yunus's “Grameen” concept, introduced in Bangladesh (1976), may not be effective in Sri Lanka or any other country. Microfinance provides financial assistance to low-income or jobless individuals or organisations without exceptional access to monetary administrations. Individuals are permitted to assume sensible independent venture credits securely and in a fashion that is foreseeable with ethical loaning assessment through microfinance. Microcredit defines the unsecured lending of small sums of money at low interest to emerging enterprises; the main security is peer guarantee via an organised framework. This credit is made available to the consumer when needed (Bashir et al., 2017). Microfinance has the potential to improve women entrepreneurs through the offer of microloan and non-microloan services and hence improve their intra-household bargaining power. Among microfinance services, microcredit has been the most researched regarding its impact on empowering women, with a plea for more scholarly investigation of other services such as savings and insurance (Kivalya and Caballero-Montes, 2024).

The qualities of this microcredit are that it makes small loans available directly to small-scale business visionaries in order to empower them to either start up or grow small-scale businesses, as well as independent ventures. Microcredit is often used to target groups that would otherwise not be able to meet all of their needs for advances from formal establishments. This includes the vast majority of those living below the poverty level (Gupta and Sharma, 2023). Understanding the relationship between microfinance and women's entrepreneurship required the creation of a conceptual framework based on Feminist Theory (Turner and Maschi, 2015), Empowerment Theory (Perkins and Zimmerman, 1995) and Randomised Control Trial theory (Heckert et al., 2019). The interaction of self-help groups (SHGs), microfinance, and microcredit in encouraging women's entrepreneurship is a dynamic and diverse research area (Raimi et al., 2023). H1: There is a positive relationship between microfinance and women entrepreneurship, suggesting that increased access to microfinance services leads to higher levels of women's entrepreneurial activities.

Microfinance institution and women’s entrepreneurship

Women suffer a double burden because it is culturally and possibly legally obligatory that they do domestic duties, asserting that appropriate financial services are necessary for women's income-generating activities (Mayoux, 2006). Microcredit is the most crucial service needed for WE activities. A new entrepreneurial enterprise or the expansion of an established one both require capital. Microfinance institutions (MFIs) services can help meet these capital needs, with credit distribution to women entrepreneurs being one of the most important (Sharma et al., 2012). H2: Microcredit is positively associated with women entrepreneurship, indicating that greater utilisation of microcredit facilities is linked to increased engagement in entrepreneurial ventures among women.

Micro-Saving and women entrepreneurship

Micro-savings, according to Anoke (2023), are MFI services that enable customers to save aside small sums of money for use in the future. With this type of account, families can set aside smaller sums of money to prepare for future business growth and pay for unforeseen expenses, meeting the current standards of living. Savings are a rise in a company's total assets that act as a sort of capital. Future monetary obligations are covered. Robinson and Stubberud (2014) claimed that microfinance banks (MFBs)’ savings options are depositors are safeguarded and have a safety net they can rely on when things get tough. When women entrepreneurs are unable to save and effectively utilise their resources, their business performance is negatively impacted (Olu, 2009). Despite being highly influenced by efficiency and asset level, banks’ size. Microfinance banks employ the microfinance savings service as a strategy to help active, underprivileged individuals in their daily lives. The efforts of society have lowered the risks and expenses of borrowing. Most academics who define micro saving services neglect to consider the risk of borrowing because people who don't save must borrow to live a satisfying life (Anoke, 2023). H3: Micro saving has a positive influence on women's entrepreneurship, such that women who engage in micro-saving are more likely to participate in entrepreneurial activities.

Mediating role of women's economic security

Additionally, financial security encourages women to engage in income-generating activities like entrepreneurship. The most important prerequisite for beginning company activity is financial security. In this approach, microfinance and women's entrepreneurship, proposed in the study hypotheses, are mediated by women's economic security (Akula and Singh, 2022). H4: Women's economic security mediates the relationship between microfinance and women's entrepreneurship. Specifically, microfinance's positive impact on women's entrepreneurship is partially explained by the enhancement of women's economic security.

Moderating role of previous work experience

Women's entrepreneurship is influenced by prior work experience as well as microcredit and women's economic security. An important aspect of entrepreneurial behaviour is the entrepreneur's prior experience or knowledge (Lacap et al., 2018). When examining the connection between microfinance organisations and women's entrepreneurship, it is uncommon. Entrepreneurs with extensive expertise or experience in a specific sector will occasionally start their own businesses. Women own 47% of micro and small enterprises (MSEs), according to Blumberg et al. (2003), and later data indicate that this figure will likely rise further. Lapidus (1993) listed three features of the past communist system that should be highlighted for their role in impacting women's economic standing (which often apply to other places): women must overcome the sexual preconceptions of professions supported by cultural norms and governmental legislation; men's authority has a considerable impact on the occupations that women pick; and women entrepreneurs in the global economy women who picked difficult careers have to deal with subtle societal preconceptions. H5: Previous work experience moderates the relationship between microcredit and women's entrepreneurship. It is expected that women with previous work experience will exhibit a stronger positive association between microcredit utilisation and entrepreneurial activities compared to those without prior work experience.

Moderating role of household economic decision

Women's entrepreneurship adoption is encouraged by women's participation in decision-making and their mobility. According to Mayeux's Feminist Empowerment Theory, this study built a model based on the connection between MFIs, women's decision-making, and mobility. In theory, microfinance can improve women's decision-making and mobility by fostering the growth of small businesses and other sources of income. Similar to the previous study, the present one looked into how MFIs affected women's decision-making and mobility, which can have a positive effect on WE. MFIs provide low-income people with various financial and non-financial services (Bardhan et al., 2021). Low-income people are encouraged to participate in profitable industries by providing financial services. MFIs provide financial services such as credit, savings, and insurance. Low-income people and women are offered small loans to stimulate economic activity (Omar et al., 2012). MFIs offer savings accounts to individuals and groups, allowing them to accumulate the cash needed to start or grow their businesses. H6: Household economic decision-making moderates the relationship between microfinance and women entrepreneurship. Women who have a greater say in household economic decisions are expected to experience a stronger positive impact of microfinance on their entrepreneurial pursuits compared to those with limited decision-making authority.

Moderating role of mobility

Women's access to credit increases decision-making since it allows them to select how to use the company's financial resources. As a result, decision-making helps women become successful entrepreneurs. Microfinance and decision-making are linked in the literature (Shohel et al., 2023). Women's mobility is also more vital than ever for WE activities. Women's movement outside the home is restricted in most families due to cultural restraints. 51% of female respondents reported mobility concerns. Women's inability to freely move limits their ability to contribute to business endeavours. When women have freedom of movement, they support WE programs. Microfinance can be quite useful in this situation. The availability of finance improves women's business mobility, discovering that microfinance can boost women's mobility (Sujatha Gangadhar and Malyadri, 2015). Thus, microfinance can help to boost WE by promoting women's mobility. H7: Mobility moderates the relationship between micro-saving and women entrepreneurship. It is anticipated that women with higher mobility levels will experience a more significant positive effect of micro-saving on entrepreneurial engagement compared to those with limited mobility.

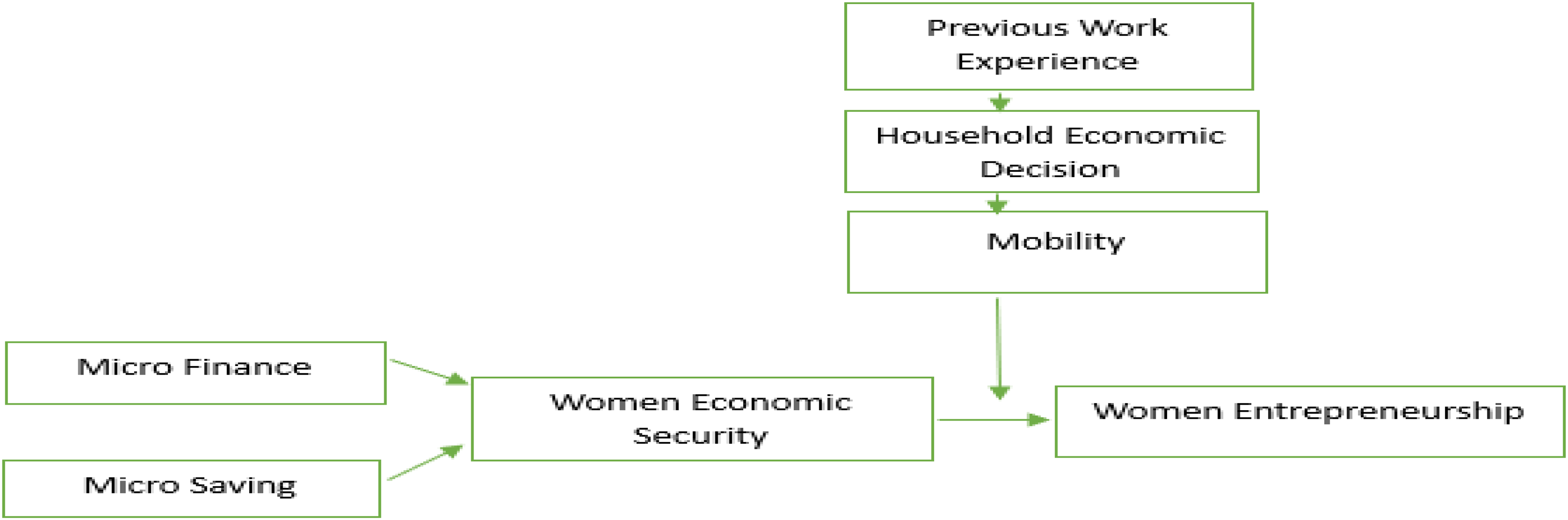

Model of proposed research study

With the ultimate goal of promoting SDGs, the suggested model demonstrates the complex interaction between numerous factors influencing women's economic empowerment and entrepreneurship. Initiatives aimed at microfinance and micro savings work as catalysts, directly affecting women's financial security, which in turn encourages entrepreneurship. In order to illustrate the model here, Figure 1 provides an in-depth research approach similar to the literature review previously introduced above.

Conceptual framework.

Women's economic security is a mediating variable that serves as a crucial link between financial access and entrepreneurial prospects. Additionally, the model takes into account the complex ways in which moderating factors like mobility, household economic decision-making, and prior employment experience alter the effectiveness of interventions. The concept greatly advances several Sustainable Development objectives, such as gender equality, decent work and economic growth, decreased inequality, and partnerships for the objectives, by empowering women economically and encouraging entrepreneurship.

Research methodology

Research design

The study uses a quantitative research approach to investigate the structural relationship between the postulated latent variables. The target group of the study consists of women microfinance users who own small-scale businesses in Pakistan. In this study, the definition of small businesses aligns with the criteria set by the Small and Medium Enterprise Development Authority (SMEDA) of Pakistan, which categorises small businesses as enterprises with fewer than 50 employees and a turnover of up to PKR 150 million.

The population is stratified based on the geographical regions where microfinance institutions actively operate in Pakistan. The random sample of participants is based on the proportion of female entrepreneurs in the regions of Lahore (50%), Faisalabad (30%), and Islamabad (20%) (Pakistan Bureau of Statistics, 2022), reflecting the regional population and the concentration of female entrepreneurs in microfinance programs.

A questionnaire was adopted to collect data from women entrepreneurs, as they are more likely to understand the study's objective and respond to the survey. The cross-sectional research design allowed for data collection at a single point in time. Since the respondents are clients of microfinance institutions, the individual is the unit of analysis in this study.

This study adopts a cross-sectional research design to investigate the relationships among the independent variables (microfinance, microcredit, and micro savings), the dependent variable (women entrepreneurship), the mediating variable (women's economic security), and the moderating variables (previous work experience, mobility, and household economic decision-making).

Data collection

The number of samples for the current study was selected by examining past study sample sizes. As a consequence of the area cluster sampling, 500 questionnaires were delivered to MFI clients. The response rate was 63%, with 313 responses received and analysed. A stratified random sampling technique was employed to ensure a representative sample of women entrepreneurs utilising microfinance services. The population was stratified by geographical regions or areas within which microfinance institutions operate. Subsequently, a random sample of participants was also drawn from each stratum based on the proportion of women entrepreneurs in that area. This approach ensures diversity in terms of geographic location and enhances the generalizability of the findings.

The study adhered to ethical guidelines to ensure the integrity and respect of participants. Informed consent was sought at the initial stage of data collection. Participants were provided with detailed information about the study's purpose, their rights, and the confidentiality of their data.

Data analysis

Data is collected through structured questionnaires administered to the selected participants. The questionnaire was designed to capture information about the variables. The survey instruments include validated scales and items from existing literature, adapted to the specific context of this study. The collected data was analysed by using a combination of statistical techniques. Multiple regression analysis examined the direct relationships between microfinance, microcredit, microsavings, and women entrepreneurship. Mediation analysis is also employed to assess the mediating role of women's economic security in the relationships between the independent variables and women's entrepreneurship. Moderation analysis is used to explore how previous work experience, mobility, and household economic decision-making moderate these relationships. We utilised the statistical software packages SPSS and SmartPLS for our study analysis due to their complementary strengths. SPSS was employed for descriptive statistics and demographic analyses, offering robust tools for data management and summarisation. SmartPLS was used for structural equation modelling to assess complex relationships between observed and latent variables, providing a visual interface for model specification and evaluation.

Results

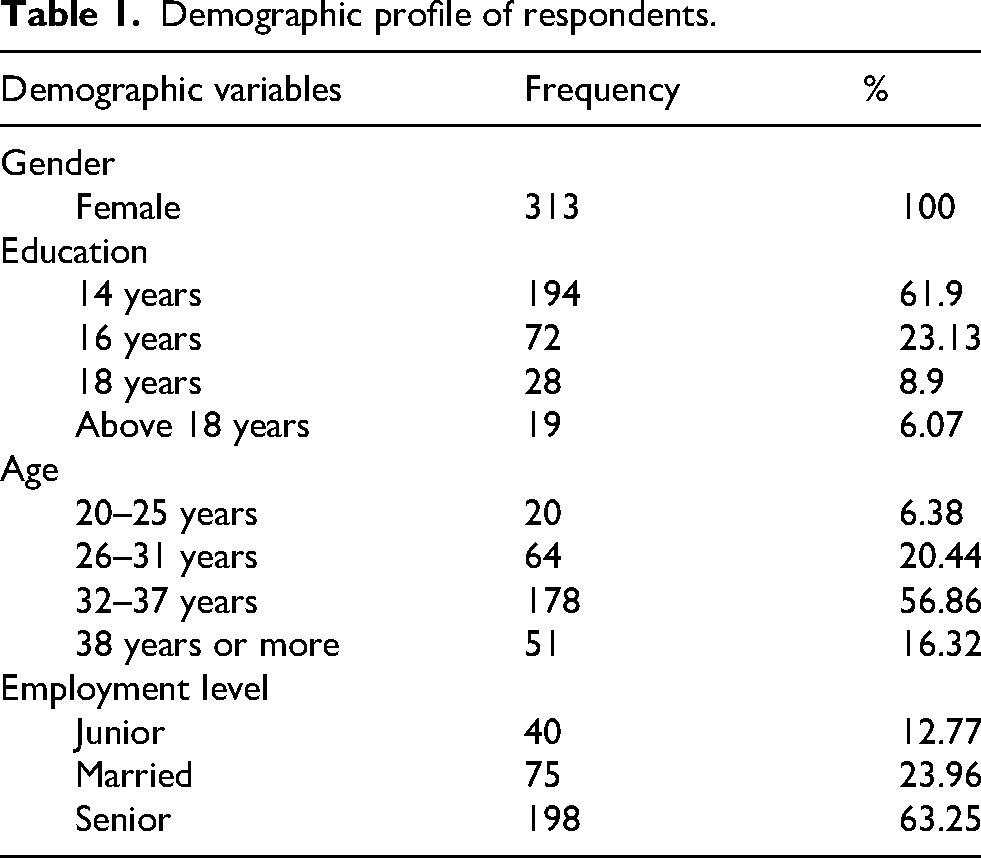

An outline of the demographic traits of the 313 female entrepreneurs included in the study can be seen in the descriptive table (Table 1). Interestingly, all the sample's members are female, highlighting the study's particular emphasis on female entrepreneurs. In terms of education, a sizable fraction of participants (61.9%) have finished their 14 years of school, but lesser percentages have completed their 16 and 18 years of school (23.13% and 8.9%, respectively. A minority (6.07%) has completed 18 years of education or more. The respondents’ age distribution is varied; just a tiny percentage (6.38%) of them are between the ages of 20 and 25, while a significant amount (56.86%) is between the ages of 32 and 37. Furthermore, 20.44% of participants are between the ages of 26 and 31, and 16.32% are beyond the age of 38. Regarding employment levels, respondents are categorised as Junior (12.77%), Married (23.96%), and Senior (63.25%), reflecting a varied range of employment statuses among the women entrepreneurs, with the majority falling into the senior category.

Demographic profile of respondents.

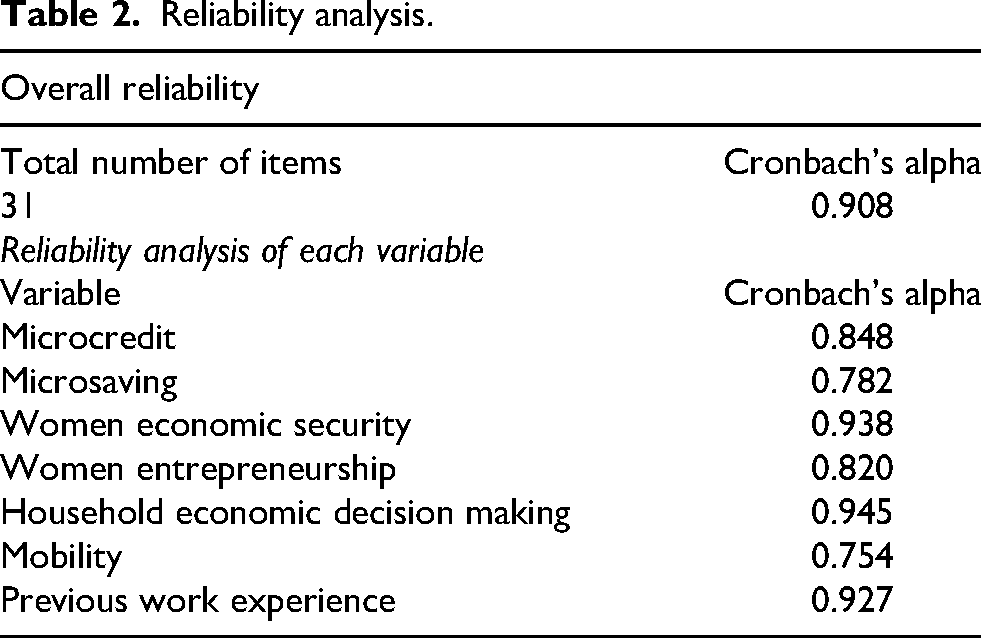

The overall reliability analysis indicates a high level of internal consistency among the study's variables, with a Cronbach's Alpha coefficient of 0.908 for the entire set of 31 items, as can be seen from Table 2. This suggests that the questionnaire items collectively exhibit strong reliability in measuring the constructs under investigation. Furthermore, when examining the reliability of individual variables, we observe that women’s economic security and household economic decision making demonstrate exceptionally high internal consistency with Cronbach's Alpha coefficients of 0.938 and 0.945, respectively. These findings indicate robust reliability in these constructs’ measurement. Microcredit, previous work experience, and women entrepreneurship also display substantial reliability with Cronbach's Alpha values of 0.848, 0.927, and 0.820, respectively, suggesting that the items assessing these constructs maintain consistent measurement. Microsaving and mobility exhibit good but slightly lower reliability, with Cronbach's alpha coefficients of .782 and .754, respectively, indicating that the items assessing these variables are still reasonably reliable but may benefit from further refinement

Reliability analysis.

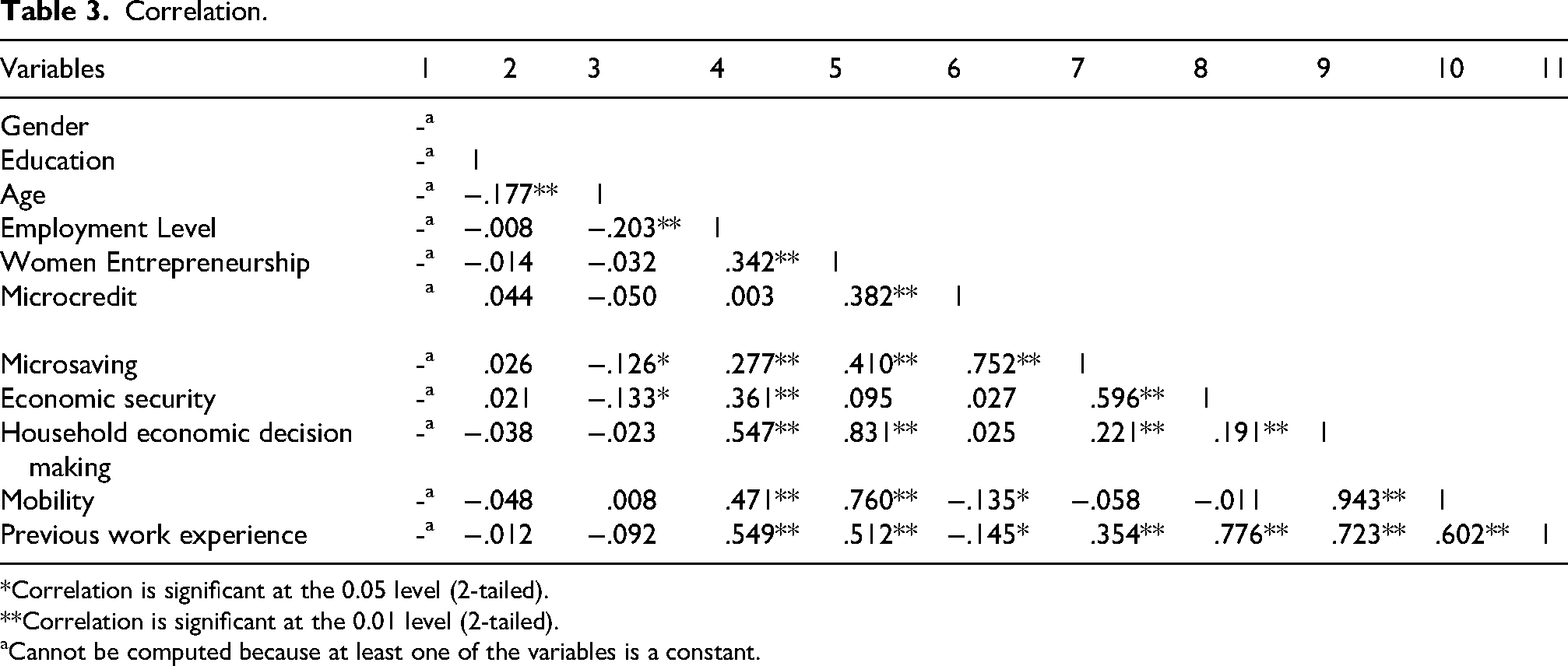

Overall, the correlation Table 3 helps to understand the strength and statistical significance of relationships between the demographic variables and the key variables of interest in this study. It provides valuable insights into how demographic factors may be associated with or influence the variables related to women entrepreneurship, microfinance, and other aspects of this research. The significance levels help to assess whether these relationships are statistically meaningful. Moving on to the key study variables, several significant correlations stand out. Women’s entrepreneurship (WE) is positively and significantly correlated with microcredit (MC), microsavings (MS), women's economic security (ES), household economic decision-making (HEDM), mobility (MB), and previous work experience (PWE). This implies that as these factors increase, women's entrepreneurship tends to increase as well. Among the moderating variables, employment level displays a substantial positive correlation with women's entrepreneurship, indicating that participants in senior employment positions are more likely to engage in entrepreneurial activities. Additionally, mobility (MB) and household economic decision-making (HEDM) both exhibit significant positive correlations with women entrepreneurship, suggesting that women with higher mobility and more influence in household financial decisions are more inclined toward entrepreneurship.

Correlation.

*Correlation is significant at the 0.05 level (2-tailed).

**Correlation is significant at the 0.01 level (2-tailed).

Cannot be computed because at least one of the variables is a constant.

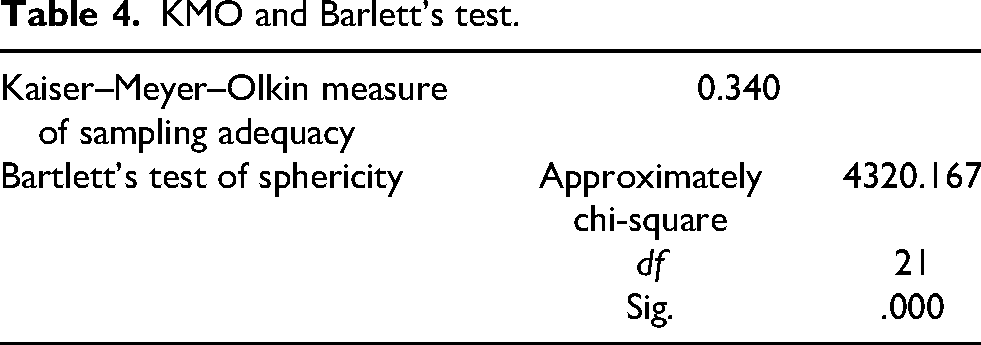

The Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy is a statistical metric used to evaluate whether the data in this analysis is suitable for conducting a factor analysis or other multivariate statistical techniques. The KMO value ranges from 0 to 1, with higher values indicating better suitability for such analyses. In this case, the KMO measure is 0.740, which is relatively high. This suggests that the variables in this dataset are moderately to highly correlated, making them suitable for factor analysis. Bartlett's Test of Sphericity, on the other hand, is used to determine whether the correlation matrix among these variables is significantly different from an identity matrix, which would imply that the variables are unrelated. In this analysis, Bartlett's Test yields an approximate Chi-Square value of 4320.167 with 21 degrees of freedom and a significance level (Sig.) of 0.000 (or p < .001) (refer Table 4). This very low p-value indicates that the correlation matrix is not an identity matrix, confirming that there are significant correlations among these variables.

KMO and Barlett's test.

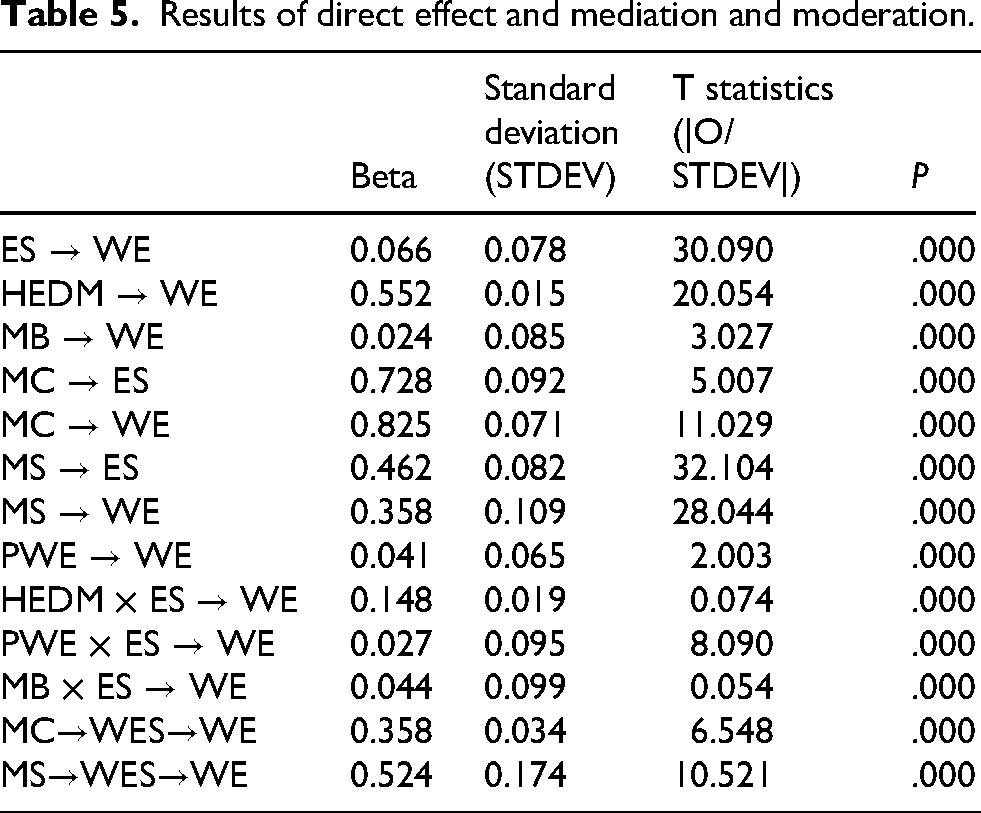

Table 5 presents the results of a statistical analysis conducted using structural equation modelling, specifically Smart PLS (Partial Least Squares). The table provides information on the direct effects, mediation, and moderation effects of various variables on a target variable denoted as “WE” (which could represent an outcome or dependent variable).

Results of direct effect and mediation and moderation.

Direct effects (Beta, STDEV, t statistics, p values)

“ES → WE": This row represents a direct effect with a beta coefficient of 0.066. It indicates that a one-unit change in the variable “ES” leads to a 0.066 unit change in “WE.” The T statistics (30.090) and p-value (.000) suggest that this direct effect is highly statistically significant. “HEDM → WE": This row represents another direct effect with a beta coefficient of 0.552. It implies that a one-unit change in “HEDM” results in a substantial 0.552 unit change in “WE.” Like the previous effect, this one is highly statistically significant with a T statistic of 20.054 and a p-value of 0.000. Similar direct effects are observed for “MB → WE,” “MC → ES,” “MC → WE,” “MS → ES,” “MS → WE,” and “PWE → WE,” all of which show strong statistical significance.

Mediation effects

MC → WES → WE

“MC → WES” represents the relationship between the variable “MC” and the mediator variable “WES.” It has a beta coefficient of 0.358, indicating that a one-unit change in “MC” leads to a 0.358 unit change in “WES. “WES → WE” represents the relationship between the mediator variable “WES” and the target variable “WE.” It signifies that a one-unit change in “WES” results in a 0.358 unit change in “WE.” The combined effect of “MC → WES” and “WES → WE” results in an indirect effect of 0.358 on “WE.” The T statistics (6.548) and p-value (0.000) suggest that this mediation effect is highly statistically significant. This means that the variable “WES” partially mediates the relationship between “MC” and “WE.”

MS → WES → WE

“MS → WES” represents the relationship between the variable “MS” and the mediator variable “WES.” It has a beta coefficient of 0.524, indicating that a one-unit change in “MS” leads to a 0.524 unit change in “WES.” “WES → WE” represents the relationship between the mediator variable “WES” and the target variable “WE.” It signifies that a one-unit change in “WES” results in a 0.524 unit change in “WE.” The combined effect of “MS → WES” and “WES → WE” results in an indirect effect of 0.524 on “WE.” The T statistics (10.521) and p-value (0.000) suggest that this mediation effect is also highly statistically significant. This means that the variable “WES” partially mediates the relationship between “MS” and “WE.”

Moderation and interaction effects

The table includes moderation and interaction effects denoted by “HEDM × ES → WE,” “PWE × ES → WE,” “MB × ES → WE,” “MC-WES-WE,” and “MS-WES-WE.” For example, “HEDM × ES → WE” represents an interaction between “HEDM” and “ES” with a beta coefficient of 0.148. The T statistics (0.074) and p-value (0.000) indicate that this interaction is highly statistically significant. Similarly, the other interaction effects such as “MC-WES-WE” and “MS-WES-WE” show significant statistical interactions.

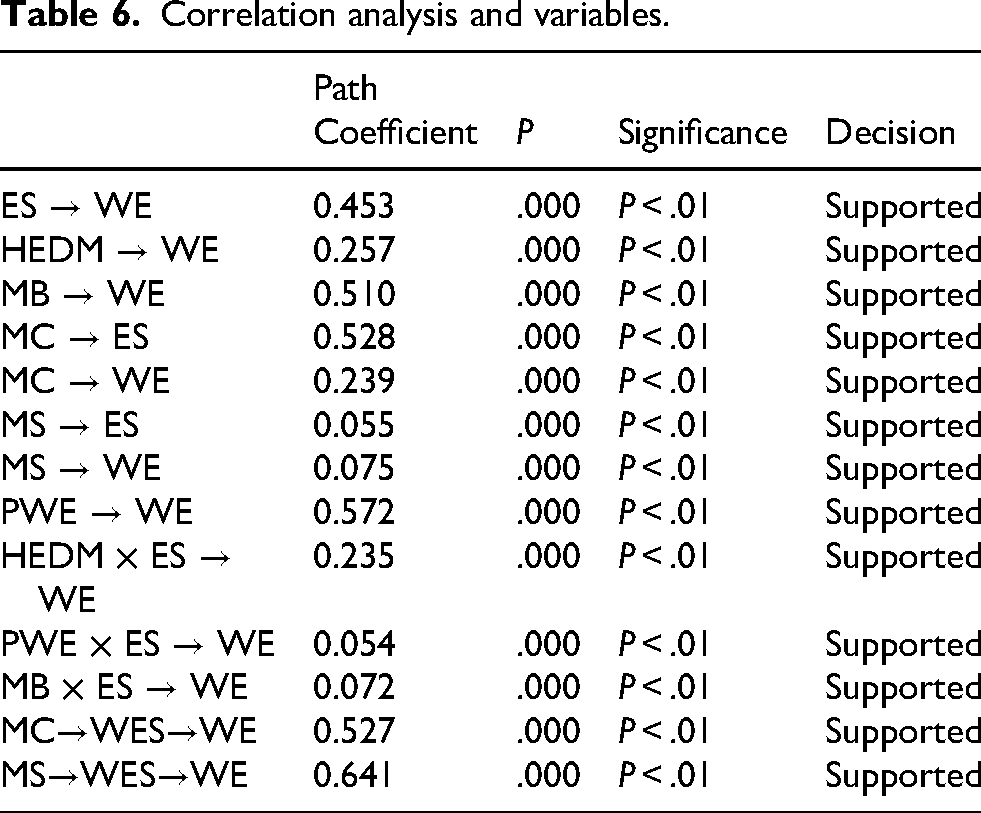

The results of a correlation study are given in Table 6, which also includes path coefficients, p-values, significance levels, and conclusions on the links between different variables. Significantly, a strong positive correlation is found between workplace effectiveness (WE) and employee satisfaction (ES), with a p-value of .000 (showing p < .01) and a path coefficient of 0.453, indicating a statistically significant and supported link. Other correlations that show statistically significant and supported positive associations include those between Management by Objectives (MB) and WE (path coefficient = 0.510), Human Resource Development Mechanisms (HEDM) and WE (path coefficient = 0.257), and Management Control (MC) and Employee Satisfaction (ES) (path coefficient = 0.528). Positive correlations are also shown by interactions between specific variables, such as HEDM × ES and PWE × ES, which also exhibit positive correlations with WE, with corresponding path coefficients of 0.235 and 0.054, respectively. Additionally, mediated relationships, such as MC → WES → WE and MS → WES → WE, indicate strong positive correlations, reinforcing the significance and support for these associations in the context of workplace dynamics.

Correlation analysis and variables.

Discussion

This study endeavours to explore the pivotal role of microfinance in fostering women's entrepreneurship, with a particular focus on the mediating influence of women's economic security and the moderating factors of prior work experience, mobility, and household decision-making. Data for this research were gathered through comprehensive questionnaires distributed among female clients of microfinance institutions in Pakistan. The study posits seven primary hypotheses, from one pertaining to mediation and three addressing moderation.

This study shows the significant association between microfinance and women's entrepreneurship, suggesting that microfinance positively influences women's entrepreneurial activities. This is in line with the studies by Yogendrarajah (2011) and Basumatary et al. (2023), whose results show a positive correlation between microcredit and women's empowerment. Microfinance is instrumental in propelling women towards entrepreneurship, offering them access to microcredit that can serve as a catalyst for initiating or expanding business ventures. This hypothesis aligns with the findings of previous research by Akula and Singh (2021), which highlight the positive correlation between microfinancing and women's entrepreneurship.

Also, this study delves into the relationship between microfinance and women's economic security, revealing that microfinance has a beneficial impact on enhancing women's economic security. Increasing access to microcredit services shows that it augments women's economic well-being, in line with findings from Hameed (2019). In this sense, microcredit services connect with financial services (e.g., from donors, government entities or the institutional financial system), and allow women entrepreneurs to diversify and increase their income. Therefore, women in developing countries need to develop their skills in terms of training, social capital, and capturing opportunities in the market. This confirms what is stated by Idris and Agbim (2015) about the importance of obtaining market information, identifying new opportunities and business ideas, accessing financial support, and acquiring resources (e.g., human, technological), which provides emotional support and encourages women to engage in entrepreneurial activities that improve their personal and family living conditions. The nexus between women's economic security and women's entrepreneurship explores the establishment of a positive connection between the two. This study demonstrates that women who accumulate savings and possess financial resources within the family are more inclined towards entrepreneurial endeavours. The availability of financial resources fosters female entrepreneurship, as it reduces the fear of taking risks and increases the propensity of Pakistani women to engage in entrepreneurial activities. The opposing results of other studies – namely, Raghuvanshi et al. (2017) – partly confirm our results: the lack of family support hinders the development of entrepreneurial activity. Weak autonomy over family economic resources and the absence of economic empowerment guidance within the family, such as savings, limit women's ability to invest (Kagotho and Vaughn, 2018).

This study also illuminates the constructive influence of previous work experience on women's entrepreneurship, underlining that women with prior entrepreneurial exposure are better equipped to engage in entrepreneurial activities. This finding corroborates the significance of work experience in entrepreneurial success, as noted by Hameed et al. (2020). By deepening the mediation, the study discerns, in line with Sujatha Gangadhar and Malyadri (2015), the mediating role of women's economic security in the relationship between microfinance and female entrepreneurship.

The results confirm that women's economic security serves as an intermediary mechanism through which microfinance positively influences women's entrepreneurial pursuits. This corroborates the results obtained by Aravamudhan et al. (2024) regarding the success of women being, in part, related to their financial and economic independence, and its involvement in decision-making, based on capabilities and resources that provide opportunities and improve its position in the family and social spheres, as mentioned by Gupta et al. (2024). Finally, the bolstering role of previous work experience in strengthening the connection between microfinance and women's entrepreneurship. Women with prior business experience are shown to leverage microfinance resources more effectively to initiate entrepreneurial activities. This is consistent with Shabsough et al. (2021) at the level of entrepreneurial behaviour influenced by prior experience, and the social support (both formal and informal) obtained in women's entrepreneurial initiatives.

The exploration of the empowering role of female entrepreneurship through microfinance in achieving the 5th SDG of women's empowerment represents a significant and timely effort. Microcredit serves as an incentive for women entrepreneurs by improving their training levels and economic empowerment. This is a strategy aligned with Littlefield et al. (2003) for poverty reduction and sustainable development, empowering individuals to make decisions and generate wealth through self-employment, with similar outcomes achieved by Nkpoyen and Bassey (2012). The intersection of women's entrepreneurship and microfinancing presents a strategic avenue for fostering sustainable development on multiple fronts. By delving into this realm, we can uncover nuanced insights into how economic empowerment, particularly through entrepreneurship, can contribute to broader societal goals. Microfinancing, as a strategic tool, not only facilitates the initiation and growth of women-led enterprises but also addresses financial inclusion challenges. This discussion holds particular relevance in the context of SDGs, emphasising the interconnectedness of economic empowerment, gender equality, poverty alleviation, and community well-being. The exploration of this dynamic relationship offers opportunities to identify effective strategies, policy frameworks, and support mechanisms that can enhance the impact of women's entrepreneurship on sustainable development. Moreover, it underscores the importance of acknowledging and addressing the unique challenges faced by women entrepreneurs, ultimately contributing to the broader discourse on fostering inclusive and sustainable development pathways.

Conclusion

In conclusion, this research has shed valuable light on the intricate relationships within the realm of microfinance and women's entrepreneurship. The study's primary objective is to explore microfinance's role in fostering women's entrepreneurial activities, while simultaneously investigating the mediating effect of women's economic security and the moderating influence of prior work experience, mobility, and household decision-making.

The findings from this study offer significant insights into these relationships.

Firstly, microfinance, particularly in the form of microcredit, has a substantial and positive impact on women's entrepreneurship. Access to microcredit services emerged as a catalyst, motivating women to initiate and expand their entrepreneurial ventures. This aligns with previous research and emphasises the pivotal role that microfinance institutions play in promoting women's economic empowerment through entrepreneurship.

Secondly, the research demonstrates that microfinance, including both microcredit and microsavings, contributes positively to enhancing women's economic security. The availability of microfinance services, such as savings and credit, is instrumental in improving the economic well-being of women. This is consistent with existing literature highlighting the correlation between microfinance and women's economic security.

Thirdly, the study unveils the affirmative connection between women's economic security and their engagement in entrepreneurship. Women who accumulate savings and exert financial control within their households are more inclined to venture into entrepreneurial activities. This underscores the significance of economic security as a driving force behind women's entrepreneurship.

Theoretical implications

This study contributes to empowerment theory by showing that women's empowerment enables them to gain control over their lives and improve their personal and family living conditions. This stems from their motivation to carry out tasks in their businesses in a controlled and efficient manner (psychological dimension), which in turn results from their individual autonomy and access to resources (e.g., microcredit) to develop their entrepreneurial activities (structural dimension), revealing the interconnection between the structural and psychological dimensions of empowerment.

The research confirms that previous work experience is vital to women's entrepreneurship. Women with prior entrepreneurial exposure are better equipped to navigate the challenges of entrepreneurship and make more effective use of microfinance resources.

Additionally, the study delves into mediation and moderation. It revealed that women's economic security acts as a mediating mechanism through which microfinance positively influences women's entrepreneurship. Furthermore, prior work experience strengthens the relationship between microfinance and women's entrepreneurship, highlighting its moderating role.

The findings underscore the multifaceted nature of the microfinance-women's entrepreneurship nexus. Microfinance, encompassing microcredit and microsavings, stands as a potent instrument for promoting women's entrepreneurship, with women's economic security mediating this relationship.

Furthermore, prior work experience enhances the positive impact of microfinance on women's entrepreneurship.

Practical implications

These findings hold critical implications for policymakers, microfinance institutions, and organizations working towards women's economic empowerment. By recognizing the pivotal role of microfinance and the mediating and moderating factors at play, stakeholders can formulate targeted strategies to further empower women entrepreneurs, promote economic security, and foster sustainable development.

It is recommended that governments should encourage MFIs and the management of savings by offering more attention to MFIs and savings programs, especially in rural and less developed regions. Some of these could include government allowed low interest rates for women of low income, or giving institutions favored with tax rebate because they lend mostly to women. Therefore, Micro-financing and micro-savings are central to improving women's economic status, thereby nurturing entrepreneurial ventures. Availability of these services to the women would enhance the women engage in business activities.

Teach citizens financial literacy programs that can help them save money, budget their income, and manage microloans nationally. These programs should be mainstreamed within current community-based programmes and targeted at women in low-income homes. It is, therefore, necessary to work on the financial literacy of the beneficiary populace in order to get the most from micro-savings and micro-financing. Empowerment of women by providing better knowledge of financial situations results in better economic performance and good business.

Housed within the framework of this research, the findings foreground the roles of household economic decisions and household mobility on women's business ventures. These are some of the barriers that need to be eliminated to ensure women are not hindered in their attempts to set up and grow their businesses. Gender sensitive polices can assist in eliminating these barriers. In this way, introducing such policies encourages and supports women's decision-making at the household and community level economically.

Limitations and suggestions for future research

While this study delves into several crucial aspects of women's entrepreneurship that remained unexplored in previous research, there are still noteworthy facets that remained beyond the scope of this investigation. These unaddressed dimensions could serve as the focal points for future research endeavours.

The data in this study were collected from female clients of microfinance institutions in Pakistan. This geographic and demographic focus may limit the generalizability of the findings to a broader population.

While this study examines women's economic security as a mediator and prior work experience as a moderator, other relevant variables, such as cultural factors, social support networks, and access to resources, were not explored. Future research can consider a more comprehensive set of mediating and moderating variables.

Moreover, future studies can compare the impact of microfinance on women's entrepreneurship across different regions and cultures. Understanding the regional variations can inform tailored microfinance strategies. In addition, assess the effectiveness of government policies and regulations in promoting gender-inclusive microfinance programs and their impact on women's entrepreneurship.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.