Abstract

The EU reformed the regulatory rules of the Eurozone in response to the European sovereign debt crisis, empowering the EU to more effectively enforce the Stability and Growth Pact (SGP), which is designed to prevent debt crises. Given recent empirical evidence that the EU’s willingness to enforce EU law depends on public opinion, under what conditions will EU residents view SGP enforcement as an effective way of tackling the crisis? I theorize how individuals will evaluate SGP enforcement and test my theory’s predictions using cross-national survey data from all Eurozone member states and Bayesian multi-level models. I find that respondents’ preferences over SGP enforcement depend on the interaction of their political support for the European Economic and Monetary Union and their member state’s noncompliance with the SGP criteria. Public buy-in for SGP enforcement is lower precisely when enforcement is most important.

Keywords

Introduction

The European sovereign debt crisis threatened the future of the crowning economic achievement of the European Union (EU) – the Eurozone. After adopting the euro, and gaining access to cheaper credit, many Eurozone member states over-spent and over-borrowed, violating the Stability and Growth Pact (SGP) criteria – the Eurozone’s statutory limits on the size of member states’ deficits and debts. Yet, the Council of the European Union (Council) and the European Commission (Commission), jointly tasked by the EU treaties with enforcing the Eurozone’s rules, failed to enforce the SGP criteria, paving the way for a sovereign debt crisis. The crisis erupted in 2009 when bond investors, reacting to new information about the size of Greece’s sovereign debt, launched a speculative attack on Greek bonds, causing financial contagion that threatened to destabilize the Eurozone.

EU member states responded to the crisis by passing a series of legislative reforms on the SGP (the Sixpack in 2011 and the Twopack in 2013) and by signing the Fiscal Compact, an intergovernmental treaty, in 2012 (Lehner and Wasserfallen, 2019; Lundgren et al., 2019; Roger et al., 2017; Târlea et al., 2019; Wasserfallen et al., 2019). These reforms enhanced the SGP’s enforcement mechanisms to reassure bond investors that the EU would enforce the SGP in the future. The Commission can now pre-screen member states’ budgets (ex ante enforcement) and more easily impose sanctions on member states for violating the SGP criteria (ex post enforcement).

Under what conditions are residents in Eurozone member states more likely to think that SGP enforcement (whether ex ante or ex post) is an effective response to the Eurozone crisis? In this paper, I argue that individuals’ attitudes towards the effectiveness of SGP enforcement depend on the interaction of three key independent variables: (a) whether the individual’s member state is violating the SGP deficit criterion; (b) whether the individual’s member state is violating the SGP debt criterion; and (c) whether an individual supports the European Economic and Monetary Union (EMU) as a political project. In brief, noncompliance with the SGP criteria conditions the effects of SGP enforcement on member states’ economies and on the stability of the Eurozone, and an individual’s political support for the EMU shapes the conclusions they will draw about the effectiveness of SGP enforcement, given these effects. I test the theory’s observable implications using cross-national survey data covering all Eurozone member states from 2013 (over 35,000 respondents) and Bayesian multi-level models.

My findings have important implications for our understanding of individuals’ evaluation of economic policies and the future enforcement of the Eurozone’s rules. First, I show that how individuals evaluate the policy of SGP enforcement depends not only on its likely effects on their member state’s economy and on the stability of the Eurozone, but also on how they interpret those effects through the lens of their political commitment to the EMU. My findings suggest that individuals who support the EMU interpret the effects of SGP enforcement differently than those who do not support the EMU, leading them to hold heterogenous opinions on the effectiveness of the policy, even when likely effects on their member states’ economies are the same.

The literature on public opinion in the EU has generally focused on explaining public support for the EU (e.g. Armingeon and Ceka, 2014; Gomez, 2015; Maier et al., 2015; Ringlerova, 2015) and for the euro (e.g. Gabel, 2001; Tillman, 2012; Roth et al., 2016). There is also a long-standing debate, as in the broader international political economy (IPE) public opinion literature, on the degree to which material self-interest (i.e. pocketbook effects) shapes public opinion. However, fewer studies theorize individuals’ preferences over the effectiveness of specific economic policies (e.g. Kanthak and Spies, 2018). Consistent with Gabel (1998) and Carrubba and Singh (2004), my findings speak to the importance of theorizing how individuals evaluate tradeoffs across the various effects of a policy and how individuals’ political preferences interact with their economic context to shape their preferences over specific policies.

Second, I show that patterns in how individuals evaluate the policy of SGP enforcement could undermine EU enforcement of the SGP. The recent literature on compliance in the EU suggests that EU institutions strategically enforce noncompliance, and are less likely to take enforcement action against violations by member states when they expect the member state to ultimately comply to a smaller extent (Baerg and Hallerberg, 2016; König and Mäder, 2014; Fjelstul and Carrubba, 2018), such as when there is less buy-in from the domestic public for compliance or enforcement. I find that individuals are generally less likely to think that SGP enforcement is an effective response to the Eurozone crisis (i.e. there is less public buy-in for enforcement) precisely when effective SGP enforcement is most important for maintaining the stability of the Eurozone. This raises doubt as to whether the Commission will be more willing to enforce the SGP going forward. The broader lesson for EU decision-making is that it is important for EU policy-makers to carefully consider how the public will respond to a policy and whether a lack of buy-in could undermine the EU’s political will to enforce it, jeopardizing the policy’s effectiveness.

SGP enforcement and the European sovereign debt crisis

To lay the groundwork for theorizing how individuals will evaluate the effectiveness of SGP enforcement as a political response to the Eurozone crisis, we need to consider three key issues: (a) how a moral hazard problem contributed to the Eurozone crisis; (b) how the EU can resolve this moral hazard problem, and why SGP enforcement is one solution; and (c) the political and economic tradeoffs that SGP enforcement presents.

We also need to draw a distinction between the EMU and the Eurozone. The EMU is a political initiative to converge the economic policies of EU member states. There are three stages and member states can only adopt the euro once they reach the third stage, which requires satisfying a set of criteria called the convergence criteria. The Eurozone is the group of EU member states that use the euro (i.e. that have reached the third stage of the EMU). All 27 EU member states participate in the EMU, and there are currently 19 Eurozone members. The SGP applies to all EMU members, but the economic and political consequences of SGP enforcement are different for Eurozone members than for non-Eurozone members (the monetary policy of Eurozone members is more constrained), which explains why my theory applies specifically to Eurozone members.

First, how did a moral hazard problem contribute to the Eurozone crisis? The stability of the Eurozone depends on a non-credible promise: member states will adhere to sound fiscal policies when the economy is good and credit plentiful. If a member state violates this promise, and its sovereign debt becomes so unwieldy that investors doubt that it will be able to pay the interest on its debt, they could launch a speculative attack – a sudden, uncoordinated sell-off of a member state’s sovereign bonds in anticipation of a precipitous drop in their value. By flooding the bond market, investors increase supply, which decreases the price, causing the crisis to spiral out of control. Investors then demand higher interest rates to compensate for the risk of owning a bond that is currently decreasing in value (Bølstad and Elhardt, 2015). Spiking interest rates make it that much harder for the government to meet its short-term debt obligations.

This is what happened to Greece (Featherstone, 2011). Investors launched a speculative attack on Greek bonds when a newly elected government announced that Greece’s fiscal position had been vastly overstated. Usually, debt-burdened countries decrease the real value of their debt burden by devaluing their currencies (e.g. Eichengreen, 1995). As a member of the Eurozone, Greece did not have that option. Its inability to borrow as interest rates on its bonds spiked pushed the government towards sovereign default, which threatened to destabilize the entire Eurozone.

Economists and politicians have warned that letting Greece default and exit the Eurozone (to reclaim monetary policy autonomy) could create financial contagion. A Greek sovereign default would hurt investors who hold Greek sovereign bonds – investors that include other EU member states. Non-performing Greek assets would imperil other member states’ already-weak financial positions, leading to downward pressure on the euro (Goldbach and Fahrholz, 2011). Highly indebted member states knew they were too big to fail, and this expectation of a bailout incentivized over-spending and over-borrowing to stimulate the domestic economy. In short, Eurozone members do not internalize the costs of their own risky behavior. This is a textbook example of moral hazard.

Second, how can the EU resolve this moral hazard problem? The EU either needs to prevent Eurozone members from over-spending and over-borrowing or prevent a member state’s risky fiscal behavior from spilling over to other members. On one end of the spectrum, the EU could strictly enforce the SGP. The architects of the Eurozone created the SGP – an agreement among all EU member states designed to underpin the stability of the Eurozone by placing caps on member states’ deficits (3% of GDP) and debts (60% of GDP) – specifically to prevent irresponsible fiscal behavior (Buti and Carnot, 2012). The SGP has been ineffective in practice because the Council and the Commission have declined to enforce the SGP criteria (Baerg and Hallerberg, 2016; Hallerberg, 2011). Recommitting to strict SGP enforcement would help to reassure investors that member states will not over-spend and over-borrow. On the other end of the spectrum, the EU could dissolve the Eurozone and return monetary policy autonomy to member states so a speculative attack against one member state would not destabilize a shared currency.

Third, what tradeoffs does SGP enforcement present to individuals evaluating it as a policy to address moral hazard? Effective enforcement by the EU constrains a member state’s deficit spending, thereby limiting marginal increases to its sovereign debt (Alesina et al., 2019). This helps to mitigate the probability of a debt crisis. In short, enforcement means EU-imposed austerity, which can be costly. Austerity measures can include expenditure-based and tax-based approaches (i.e. reducing spending or raising taxes), and member states have discretion over how to implement austerity. Recent research in economics finds that cutting spending is relatively less harmful to the economy than raising taxes (Alesina et al., 2019). Nevertheless, contracting public spending can still hurt short-term economic growth, which can increase public support for exiting the Eurozone (Baccaro et al., 2021). This tradeoff between the stability of the Eurozone and short-term economic costs of austerity is at the heart of the public discourse about the future of the Eurozone (Jurado et al., 2020).

Theory

Under what conditions will individuals think that SGP enforcement is an effective way of tackling the Eurozone crisis? This section builds on the IPE literature on economic crises and the IPE and EU literatures on public opinion to theorize when individuals are more likely to view SGP enforcement as an effective response. Although the SGP applies to all members of the EMU, my theory applies exclusively to members of the Eurozone because SGP enforcement has different consequences for Eurozone members than for non-Eurozone members.

Importantly, I do not argue that individuals are carefully evaluating the policy of SGP enforcement themselves. The policy preferences of individuals are far more likely to be the product of cues from political elites and their domestic media than of their own careful consideration of the policy and its likely effects (e.g. Kanthak and Spies, 2018). In this article, I do not theorize or test the mechanisms by which individuals come to acquire their preferences or take a position on the relative importance of these two mechanisms. Rather, the objective is to identify the conditions under which individuals are more likely to view SGP enforcement as an effective response to the Eurozone crisis.

Theoretical mechanisms

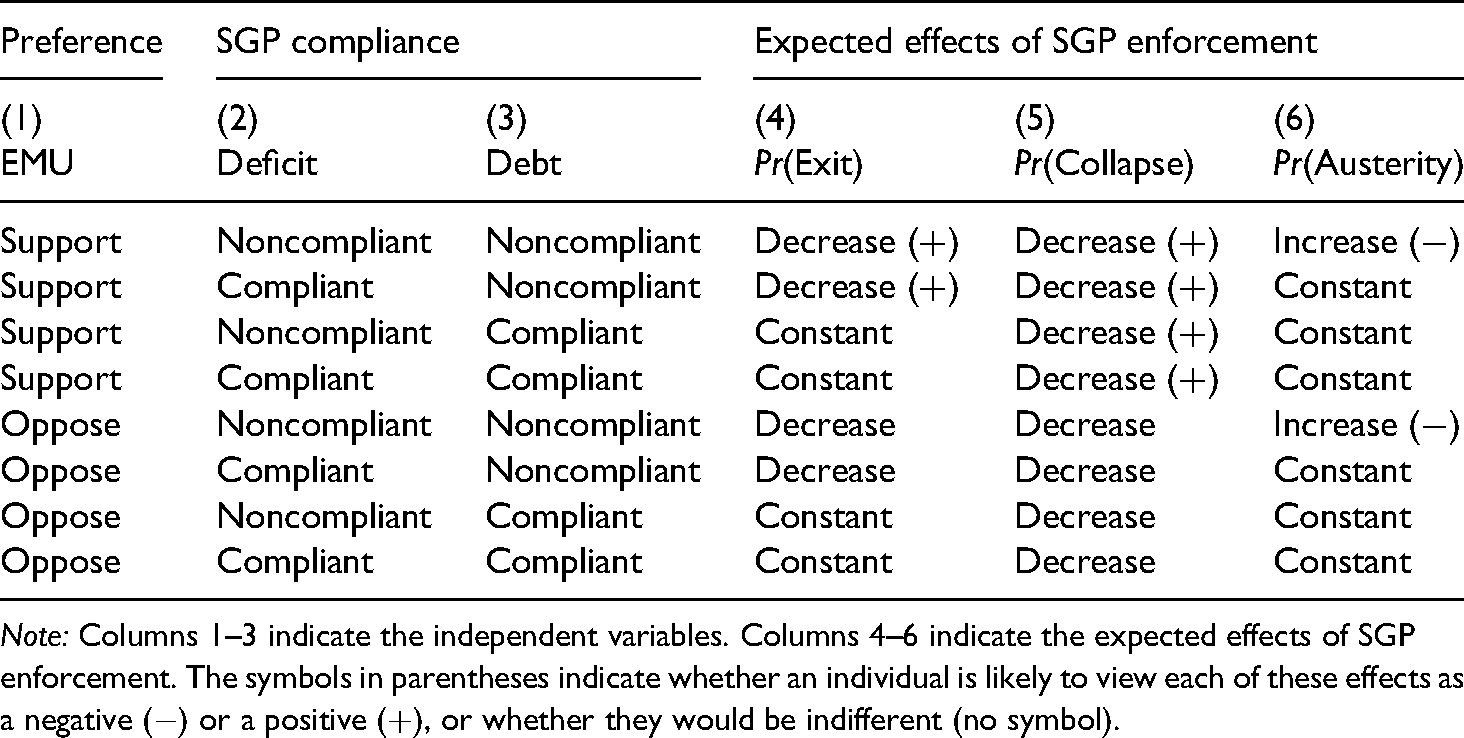

I argue that an individual’s evaluation of the effectiveness of SGP enforcement as a way of tackling the Eurozone crisis depends on the interaction of three key independent variables: (a) whether an individual’s member state is violating the SGP deficit criterion; (b) whether an individual’s member state is violating the SGP debt criterion; and (c) whether an individual supports the EMU as a political project. In this section, I present the theoretical mechanisms by which I expect these variables to interact to shape public opinion about the effectiveness of SGP enforcement. Table 1 summarizes this discussion.

Summary of the theory.

Note: Columns 1–3 indicate the independent variables. Columns 4–6 indicate the expected effects of SGP enforcement. The symbols in parentheses indicate whether an individual is likely to view each of these effects as a negative (

To start, I explain how the first two independent variables – noncompliance with the two SGP criteria – shape the likely effects of SGP enforcement on three outcomes that individuals care about: (a) the probability that an individual’s member state will have to exit the Eurozone to recover from a debt crisis; (b) the probability that the Eurozone will collapse due to financial contagion caused by a debt crisis; and (c) the probability of EU-imposed austerity, which is a negative side-effect of enforcement for noncompliant member states. Then, I explain how the third independent variable (an individual’s support for the EMU) will shape an individual’s perception of SGP enforcement with respect to these three outcomes. When an individual perceives more of the effects as positive, they will be more likely to see SGP enforcement as an effective policy.

First, I consider how noncompliance with the SGP criteria conditions the effect of SGP enforcement on the probability that a member state will have to exit the Eurozone in order to recover from a debt crisis. SGP enforcement will decrease this probability when a member state’s debt is SGP-noncompliant (Table 1, column 4). However, the mechanism depends on whether the member state’s deficit is SGP-compliant.

Noncompliance with the debt criterion shapes the probability that a member state will experience a debt crisis, which drives the probability that the member state will have to exit the Eurozone to recover. A debt crisis does not necessarily mean that a member state will have to exit the Eurozone, as it could receive a bailout (e.g. Greece), which may reassure creditors. However, there is no guarantee of a bailout, or that a bailout will be sufficient to restore confidence. Even if a bailout is a realistic possibility, the probability of a member state exiting the Eurozone is still increasing in the probability of a debt crisis, which is increasing in noncompliance with the debt criterion.

When a member state’s debt is compliant, there is no credible risk that it could face a debt crisis, regardless of its compliance with the deficit criterion. Yet, there is a risk of a speculative attack when the debt is noncompliant. That risk exists even when a member state’s deficit is compliant, as even a small SGP-compliant deficit is a marginal contribution to the debt. But it is much higher when the member state is also violating the deficit criteria, as the marginal contribution to the debt is relatively larger. If a member state’s sovereign debt is expanding at a quickly accelerating rate, investors are more likely to panic and launch a speculative attack.

SGP enforcement reduces the risk of a debt crisis when a member state’s deficit is SGP-noncompliant by incentivizing the member state to adopt austerity measures, restoring investor confidence and reducing the probability of a speculative attack. In the absence of SGP enforcement, and especially if a member state does not receive a bailout, a crisis could force the government to exit the Eurozone in order to reintroduce and depreciate its domestic currency. Depreciation would stimulate the member states’s economy, improve its current-account deficit, and reduce its real debt burden (e.g. Eichengreen, 1995). The barrier to depreciation is lower for EMU members that are not in the Eurozone, as they do not have to reintroduce their own currency. When a member state’s deficit is SGP-compliant, SGP enforcement also reduces the risk of a crisis by locking in fiscal discipline, which limits marginal contributions to a member state’s sovereign debt. Governments have a political incentive to over-spend in order to get reelected, but SGP enforcement counters this incentive.

Second, I consider the effect of SGP enforcement on the probability of the Eurozone collapsing due to financial contagion caused by a debt crisis. SGP enforcement will decease this probability of collapse across the board, regardless of whether an individual’s member state is complying with the SGP criteria (Table 1, column 5). If a member state experiences a debt crisis, causing their sovereign bonds to drop in value, other member states and their financial institutions that own those bonds would take a loss (as with Greece), which could lead to banking crises across Europe. This financial contagion could prompt the worst-hit member states to withdraw from the Eurozone in order to re-introduce their own domestic currencies, which they could then depreciate to speed up their recovery (e.g. Eichengreen, 1995). By getting member states’ sovereign debts under control, SGP enforcement reduces the risk of a debt crisis, increasing the stability of the Eurozone.

Third, I consider the effect of SGP enforcement on the probability of EU-imposed austerity, which is the primary negative side-effect of SGP enforcement. SGP enforcement will only increase the probability of EU-imposed austerity when a member state’s debt and deficit are both SGP-noncompliant (Table 1, column 6). This is because the EU can only directly enforce the SGP deficit criterion. Even if a member state’s debt is SGP-noncompliant, and the EU wants the member state to take corrective action by adopting austerity measures, if the member state’s deficit is SGP-compliant, there is nothing the EU can legally do about it–the damage is already done.

The EU can use the SGP’s ex ante and ex post enforcement mechanisms (i.e. pre-approving budgets and imposing financial sanctions) to pressure a member state with an SGP-noncompliant deficit to adopt some combination of expenditure-based or tax-based austerity measures, the latter of which tend to be more harmful to the economy (Alesina et al., 2019). When the member state’s deficit is SGP-compliant, these enforcement mechanisms are not legally available. However, the EU has discretion over enforcement, and recent research shows that the EU selectively enforces compliance with EU law (Baerg and Hallerberg, 2016; Fjelstul and Carrubba, 2018; König and Mäder, 2014). As such, the EU is only likely to actually use these enforcement mechanisms when a member state’s debt is also highly SGP-noncompliant, as this is when there is a legitimate risk of a debt crisis. In other words, the threat of EU-imposed austerity when a member state’s debt is SGP-compliant is not credible.

Finally, an individual’s political support for the EMU will shape the conclusions they draw about the effectiveness of SGP enforcement, given these likely effects (see Table 1). When evaluating a policy, individuals will often benchmark by comparing outcomes under the status quo to expected outcomes under a proposed policy (De Vries, 2017, 2018). They will also weigh tradeoffs across the various effects of a policy (Carrubba and Singh, 2004). When there are multiple alternatives to the status quo–the Eurozone’s moral hazard problem could be solved by stricter SGP enforcement or by returning monetary policy autonomy to member states (i.e. dissolving the Eurozone) – how they evaluate the effectiveness of one alternative (e.g. SGP enforcement) will depend on whether the expected outcomes are more or less consistent with their political preferences than the other alternatives (e.g. dissolving the Eurozone).

SGP enforcement decreases the probability that the Eurozone will collapse (Table 1, column 5) and, when a member state’s debt is SGP-noncompliant, it also decreases the probability that a debt crisis could force that member state to exit the Eurozone (Table 1, column 4). Individuals who support the EMU are more likely to see these effects as positives than those who do not support the EMU because SGP enforcement is consistent with their political support for the EMU – it stabilizes the Eurozone and protects their member state’s membership. Individuals who oppose the EMU, on the other hand, are more likely to prefer to resolve the crisis by reverting back to the pre-Eurozone era of national currencies, which would restore the monetary policy autonomy of their member state. Because they would prefer to resolve the crisis in a different way, they are relatively less likely to see these effects as positives than individuals who support the EMU. In other words, they are more likely to be indifferent.

Importantly, an individual’s political support for the EMU should not affect what they think about an increase in the probability of EU-imposed austerity. Supporters and opponents of the EMU will, on average, tend to view the increase in the probability of austerity (Table 1, column 6, rows 1 and 5) that comes with SGP enforcement as a negative. The problem with austerity is that it increases the risk of an economic recession, especially when the austerity measures include tax increases (Alesina et al., 2019).

Hypotheses

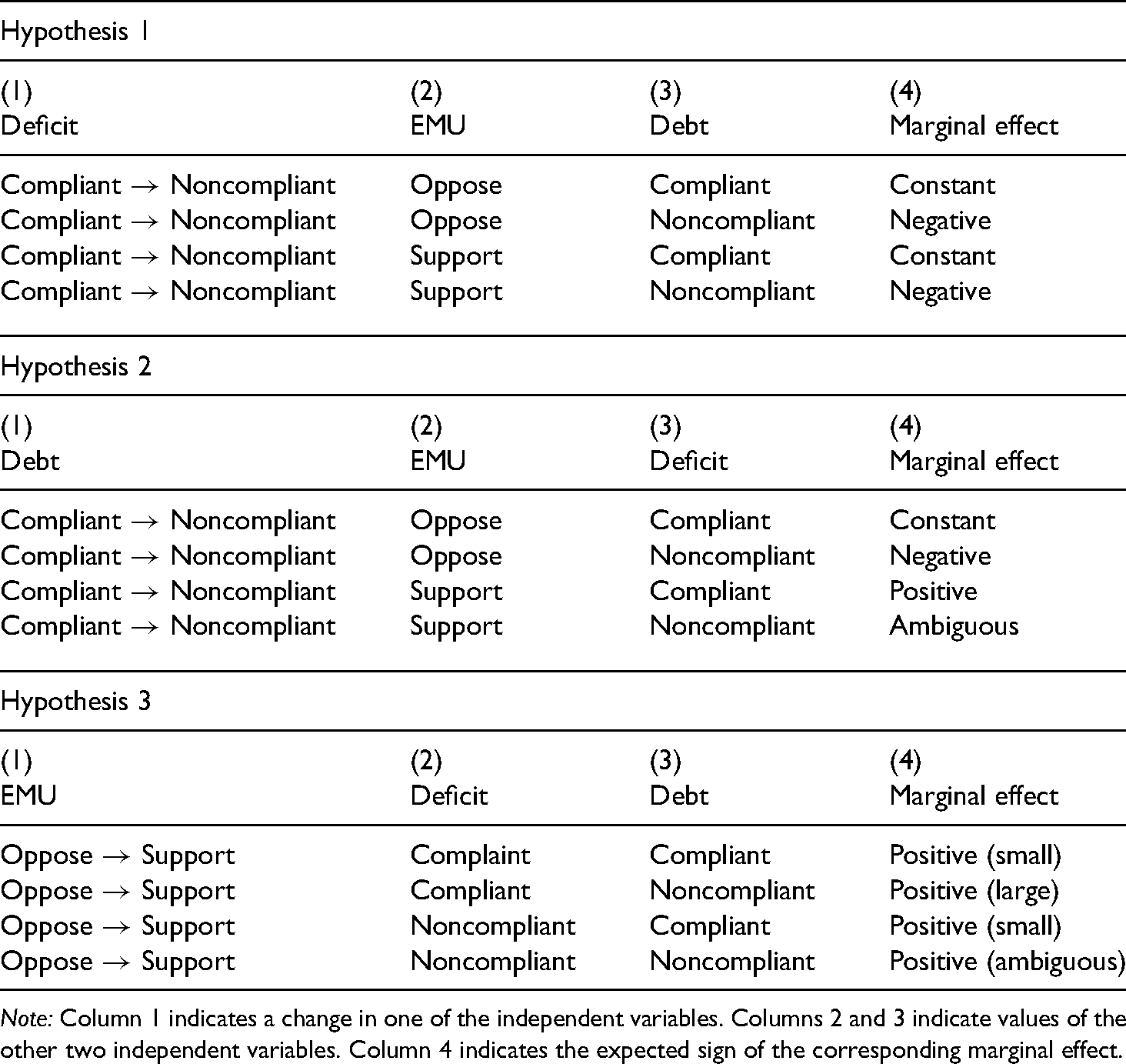

Following best-practices for specifying hypotheses that involve interactions (Berry et al., 2012; Brambor et al., 2006; Franzese and Kam, 2009), I systematically derive predictions about how the effect of a change in each of my three independent variables depends on the other two. This ensures that I do not overlook testable hypotheses. To do this, I compare across rows in Table 1 and consider how a change in one of the variables, conditional on the other two, will affect the degree to which an individual sees SGP enforcement as an effective policy, based on the effect of SGP enforcement on the three key outcomes I have identified (see Table 1, columns 4 to 6). In my empirical analysis, I estimate these conditional effects to evaluate the theory.

First, I consider how the effect of an individual’s member state’s noncompliance with the SGP deficit criterion depends on (a) their member state’s noncompliance with the SGP debt criterion and (b) their political support for the EMU (see H1 in Table 2). In this case, their support for the EMU is not critical.

Summary of hypotheses.

Note: Column 1 indicates a change in one of the independent variables. Columns 2 and 3 indicate values of the other two independent variables. Column 4 indicates the expected sign of the corresponding marginal effect.

Given compliance with the SGP debt criteria, an increase in a member state’s noncompliance with the SGP deficit criterion (Table 1, moving from row 8 to row 7 or from row 4 to row 3) will not increase the risk of EU-imposed austerity because there is no real risk of a debt crisis. Therefore, there will be no change in an individual’s evaluation of SGP enforcement, regardless of their political support for the EU. Given non-compliance with the SGP debt criteria, an increase in the member state’s noncompliance with the SGP deficit criterion (Table 1, moving from row 6 to row 5 or from row 2 to row 1) will have a negative effect on an individual’s evaluation of SGP enforcement. This is due to the higher likelihood of EU-imposed austerity. When a member state’s debt is highly SGP-noncompliant, the probability of a debt crisis is higher, which creates an incentive for the EU to actually enforce the SGP deficit criterion.

H1: The marginal effect of an increase in an individual’s member state’s noncompliance with the SGP deficit criterion will be negative, but only when their member state’s debt is highly SGP-noncompliant.

Second, I consider how the marginal effect of an increase in an individual’s member state’s noncompliance with the SGP debt criterion depends on (a) whether the individual supports the EMU and (b) whether their member state’s deficit is SGP-noncompliant (see H2 in Table 2).

When an individual supports the EMU and their member states’s deficit is SGP-compliant, an increase in their member state’s noncompliance with the SGP debt criterion (Table 1, moving from row 4 to row 2) will have a positive effect on their evaluation of SGP enforcement. SGP enforcement decreases the probability that their member state will have to exit the Eurozone, which is an outcome they will prefer. When an individual does not support the EMU and their member state’s deficit is SGP-noncompliant, an increase in their member state’s noncompliance with the SGP debt criterion (Table 1, moving from row 7 to row 5) will have a negative effect on their evaluation of SGP enforcement. SGP enforcement decreases the probability that the individual’s member state will have to exit the Eurozone, which the individual does not see as a benefit, and increases the probability of EU-imposed austerity, which they will perceive as a cost.

In the other two cases, theory does not point to a prediction. When an individual opposes the EMU and their member state’s deficit is SGP-compliant, an increase in their member state’s noncompliance with the debt criterion (Table 1, moving from row 8 to row 6) will not change their evaluation of SGP enforcement. SGP enforcement decreases the probability that their member state will exit the Eurozone, which the individual will not see as a benefit. When an individual supports the EMU and their member state’s deficit is SGP-noncompliant, the effect of an increase in their member state’s noncompliance with the debt criterion (Table 1, moving from row 3 to row 1) is ambiguous. SGP enforcement decreases the probability of a debt crisis, but it also increases the probability of EU-imposed austerity. In other words, SGP enforcement presents a tradeoff, and it is not clear a priori how individuals will weigh these effects. However, we can examine at the data to assess how survey respondents evaluate this tradeoff.

H2a: If an individual supports the EMU and their member state’s deficit is SGP-compliant, the marginal effect of an increase in their member state’s noncompliance with the SGP debt criterion will be positive.

H2b: If an individual opposes the EMU and their member state’s deficit is SGP-noncompliant, the marginal effect of an increase in the member state’s noncompliance with the SGP debt criterion will be negative.

Third, I consider how the effect of an individual’s support for the EMU depends on (a) whether their member states’s deficit is SGP-noncompliant and (b) whether their member state’s debt is SGP-noncompliant (see H3 in Table 2).

SGP enforcement increases the stability of the Eurozone by preventing debt crises and financial contagion. As an individual’s political support for the EMU increases, they will increasingly see this as a mark of effectiveness, because it resolves the crisis in a way that preserves the Eurozone (as opposed to dissolving it), consistent with their political preferences. Yet, the magnitude of this positive effect will depend on their member sate’s compliance with the SGP criteria.

When an individual’s member state’s debt is SGP-compliant, there is no real threat of EU-imposed austerity and no risk of their member state experiencing a debt crisis, so the only effect of SGP enforcement is that it lowers the probability of a debt crisis involving another member state, which decreases the probability that the Eurozone will collapse. An increase in an individual’s political support for the EMU (Table 1, moving from row 8 to row 4 or from row 7 to row 3) will have a positive effect on their evaluation of the effectiveness of SGP enforcement, regardless of their member state’s noncompliance with the deficit criterion.

In contrast, when a member state’s debt is SGP-noncompliant, the effect depends on whether the member state’s deficit is SGP-compliant. If the member state’s deficit is SGP-compliant, then SGP enforcement also decreases the probability of exiting the Eurozone due to a debt crisis by locking in good fiscal behavior – a second benefit. Consequently, the effect of an increase in an individual’s political support for the EMU (Table 1, moving from row 6 to row 2) will be even larger than in the case when the member state’s debt is SGP-compliant. However, if the member state’s deficit is SGP-noncompliant, then SGP enforcement increases the probability of EU-imposed austerity, which will be generally unpopular, even among individuals who support the EMU. We should still expect an increase in an individual’s political support for the EMU (Table 1, moving from row 5 to row 1) to have a positive effect, but because of the tradeoff that austerity presents, it is not clear how the size of the effect should compare.

H3a: The marginal effect of an increase in an individual’s support for the EMU will be positive regardless of their member state’s compliance with the SGP deficit criterion or the SGP debt criterion.

H3b: This positive marginal effect will be smallest when an individual’s member state’s debt is SGP-compliant regardless of their member state’s compliance with the SGP deficit criterion.

H3c: This positive marginal effect will be largest when an individual’s member state’s deficit is SGP-complaint and their member state’s debt is SGP-noncompliant.

Empirics

To test the predictions of the theory, I use cross-national survey data from two Eurobarometer waves and Bayesian multi-level models. I consider individuals’ attitudes towards two methods of SGP enforcement: the pre-approval of member state budgets (ex ante enforcement) and financial sanctions for noncompliance (ex post enforcement).

Since the start of the Eurozone crisis, the Standard Eurobarometer has included a special bank of questions about it. Moreover, the Eurobarometer is the only cross-national survey that includes questions on SGP enforcement. Testing the theory requires a cross-national sample of all Eurozone members as two of the three independent variables are member state-level characteristics. My sample includes data from waves 79 and 80, which were administered in the spring and fall of 2013, respectively. 1 These two survey waves are the only two that include questions on SGP enforcement. Since the theory applies only to Eurozone members (which face difference incentives that non-Eurozone EMU members), I subset the sample accordingly. 2 I pool the surveys to construct a cross-sectional sample of 36,531 individual respondents.

Measurement

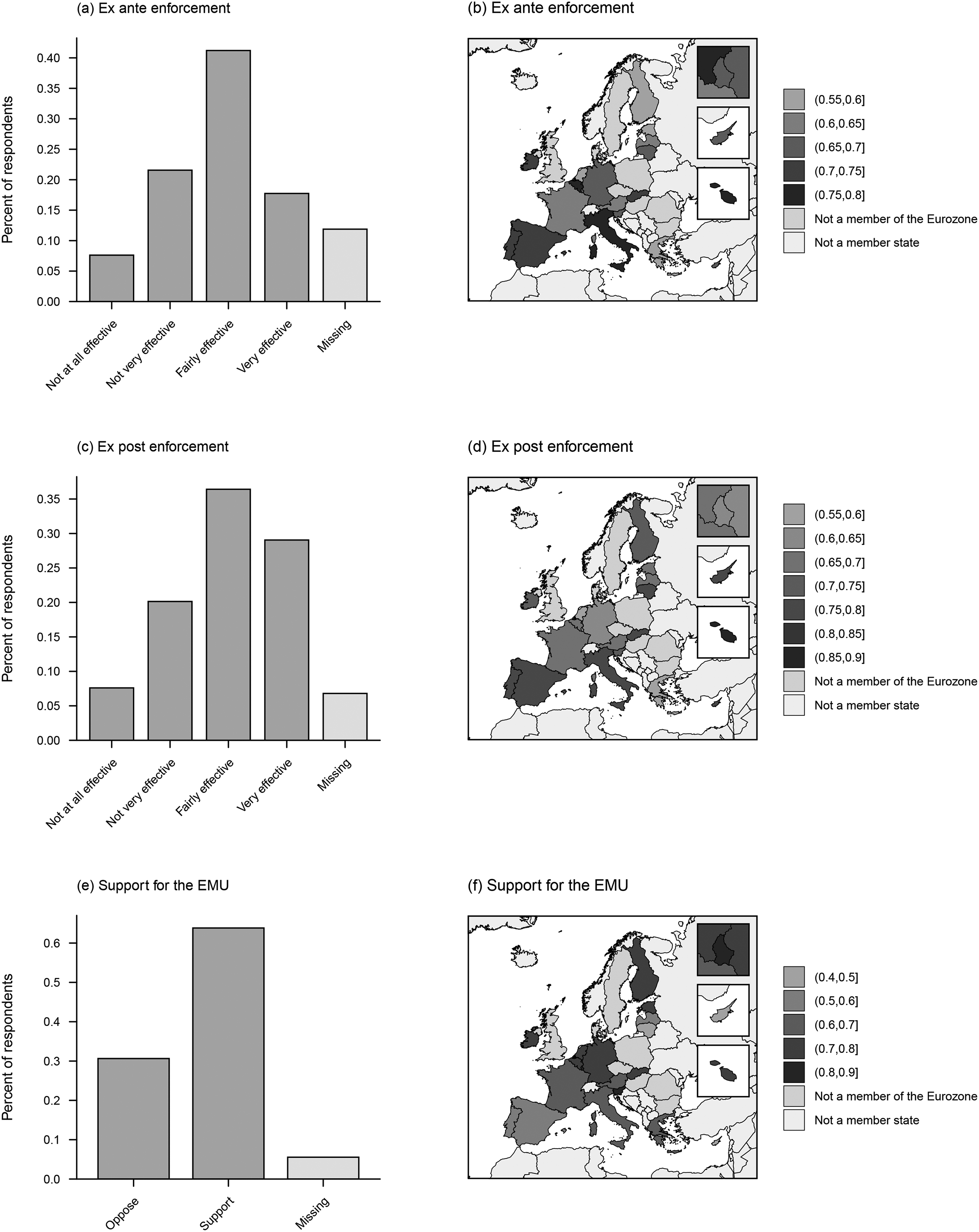

To create individual-level measures of support for ex ante enforcement (i.e. pre-approval of member state budgets by the EU) and ex post enforcement (i.e. financial sanctions for noncompliance), I use the following Eurobarometer question: ‘A range of measures to tackle the current financial and economic crisis is being discussed in the European institutions. For each, could you tell me whether you think it would be effective or not?’ The interviewer then shows the respondent a list of policies. For each policy, the respondent can answer on a 4-point Likert scale from ‘Not at all effective’ to ‘Very effective.’ One of the policies is: ‘EU approval in advance of EU Member States’ governments’ budgets.’ This captures ex ante enforcement. Another of the policies is: ‘Fines for EU Member States’ governments that spend or borrow too much.’ This captures ex post enforcement. I create a 4-point index for ex ante and ex post enforcement, with higher values indicating that the respondent views SGP enforcement as more effective (see Figure 1).

Descriptive statistics for respondent-level measures. Note: This figure shows descriptive statistics for the key respondent-level variables. (a), (c), and (e) show how respondents answered each question; (b) and (d) show the percent of respondents who see SGP enforcement as effective; (f) shows the percent of respondents who support the EMU.

I use the following question to create an individual-level measure of support for the EMU: ‘What is your opinion on each of the following statements? Please tell me for each statement, whether you are for it or against it.’ One statement is: ‘A European economic and monetary union with one single currency, the euro.’ There are only two response options for this question: ‘For’ and ‘Against.’ The variable takes a value of 1 if the respondent supports the EMU and 0 otherwise (see Figure 1).

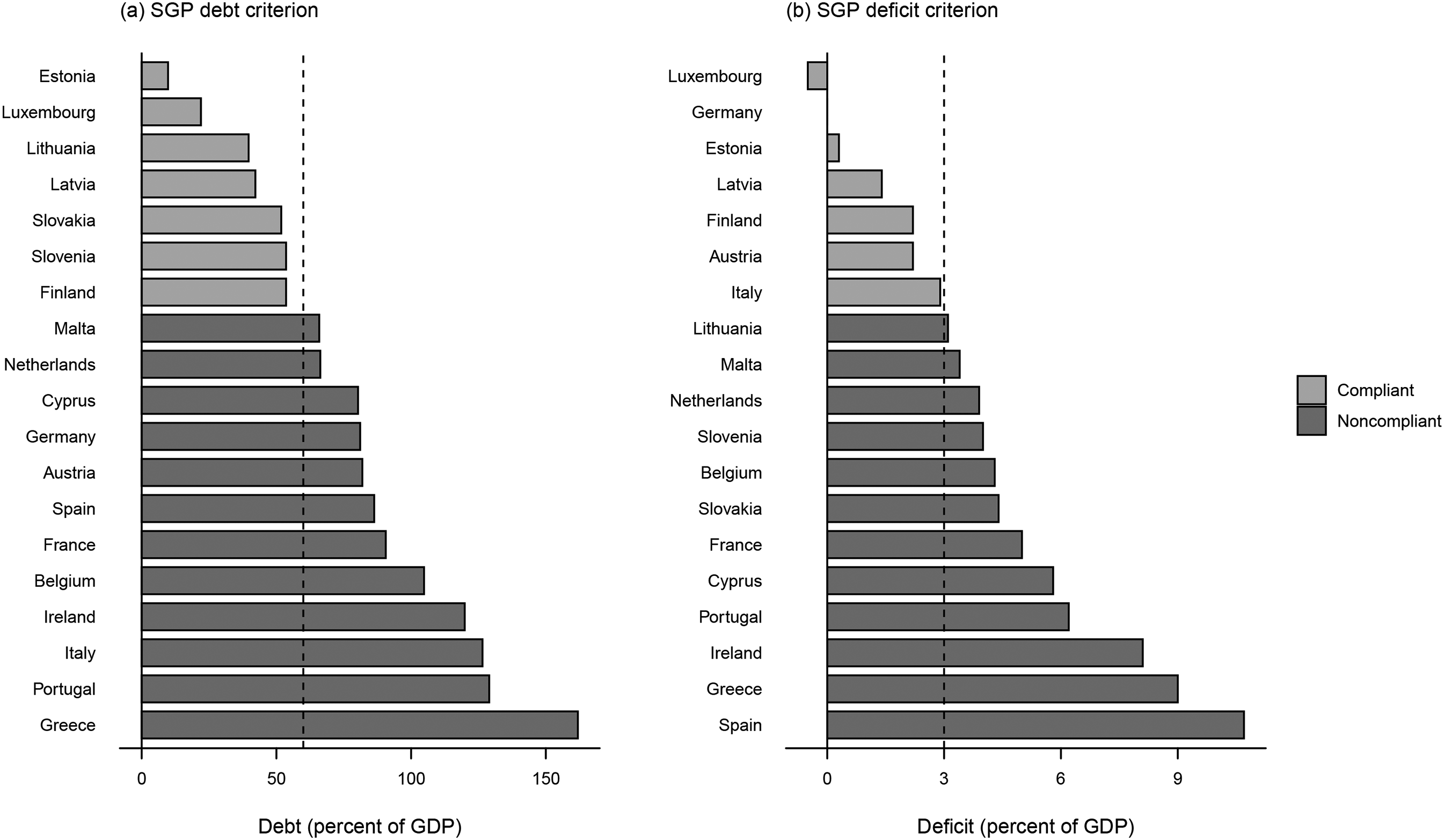

I measure noncompliance with the SGP debt criterion as the degree to which a member state’s debt exceeds the SGP criterion of 60% of GDP, expressed as a percent of GDP. I measure noncompliance with the SGP deficit criterion using a dummy variable that indicates whether a member state’s deficit exceeds the SGP criterion of 3% of GDP. For both measures, I use Eurostat data from 2012. Figure 2(a) shows noncompliance with the debt criterion for each of the 19 member states. Only seven member states in the sample are in compliance with the debt criterion. Figure 2(b) shows noncompliance with the deficit criterion. Again, only seven member states are in compliance.

Noncompliance with the SGP criteria. Note: This figure shows noncompliance with the SGP debt criterion (debt as a percent of GDP in excess of 60%) and with the SGP deficit criterion (deficit as a percent of GDP in excess of 3%) in 2012.

We can control for a variety of respondent-level factors using other Eurobarometer questions: (a) whether a respondent thinks the EU is best able to take effective action, compared to their member state, in response to the crisis (a measure of Euroscepticism); (b) a respondent’s sophistication (based on their factual knowledge of the EU); (c) their cosmopolitanism (based on how frequently they exhibit a set of cosmopolitan behaviors); (d) their household financial situation; (e) their level of education; (f) their gender; and (g) their age. Naturally, the respondent-level controls are limited by the questions asked in the survey (e.g. these waves do not contain a measure of political ideology).

To capture macroeconomic conditions, I control for the severity of austerity measures and the unemployment rate. The austerity measure is the percent change in a member state’s deficit from the onset of the sovereign debt crisis in 2009 to the administration of the survey in 2013. This accounts for both expenditure-based and tax-based austerity measures (Alesina et al., 2019). I employ Eurostat data for these two measures.

It is also important to control for the preferences of domestic political parties, which we can measure along three dimensions that are relevant to SGP enforcement: Euroscepticism, support for Keynesian economic policies (e.g. deficit spending during a crisis), and support for orthodoxy economic policies (e.g. deficit reduction and austerity during a crisis). Party-level data on these dimensions is taken from the Manifesto Project. 3 To create a member state-level measure, I use data on parties’ preferences from the most recent election prior to the survey and average the positions of each domestic political party that won seats in the lower house, weighting by seat share.

Estimation strategy

The structure of the data is multi-level: individuals are nested within states (e.g. Armingeon and Ceka, 2014; Gomez, 2015). Bayesian multi-level modeling provides a way to account for this structure (Gelman and Hill, 2006). 4 I estimate varying-intercept multi-level linear regression models that include individual-level predictors, member state-level predictors, and cross-level interaction terms. 5 The intercept varies by member state. The model includes a three-way interaction between noncompliance with the SGP deficit criterion, noncompliance with the SGP debt criterion, and an individual’s support for the EMU, including all constituent terms.

A common approach to missing survey data is list-wise deletion (e.g. Gomez, 2015; Stoeckel, 2013). However, missing data due to item non-response can bias inferences about the population if those non-responses are correlated with the outcome variable. To avoid this problem, I impute respondent-level missing data using multiple imputation by chained equations (MICEs), which uses an iterative procedure to model the conditional distribution of a variable based on other variables, estimate a multi-level model on each dataset, and pool the posterior samples (Van Buuren and Groothuis-Oudshoorn, 2011). 6

Analysis and findings

This section presents the results of two models estimated using the imputed sample, one for ex ante enforcement and another for ex post enforcement. The non-imputed results are substantively similar. Across the board, the sizes of the substantive effects of the variables of interest are fairly small, as are those of the control variables. This is not surprising, however, because public opinion data on such a complex topic can be extremely noisy. As many scholars have found, non-opinions are common (e.g. Curtis et al., 2014; Stoeckel, 2013). And even during a crisis, issue salience is limited.

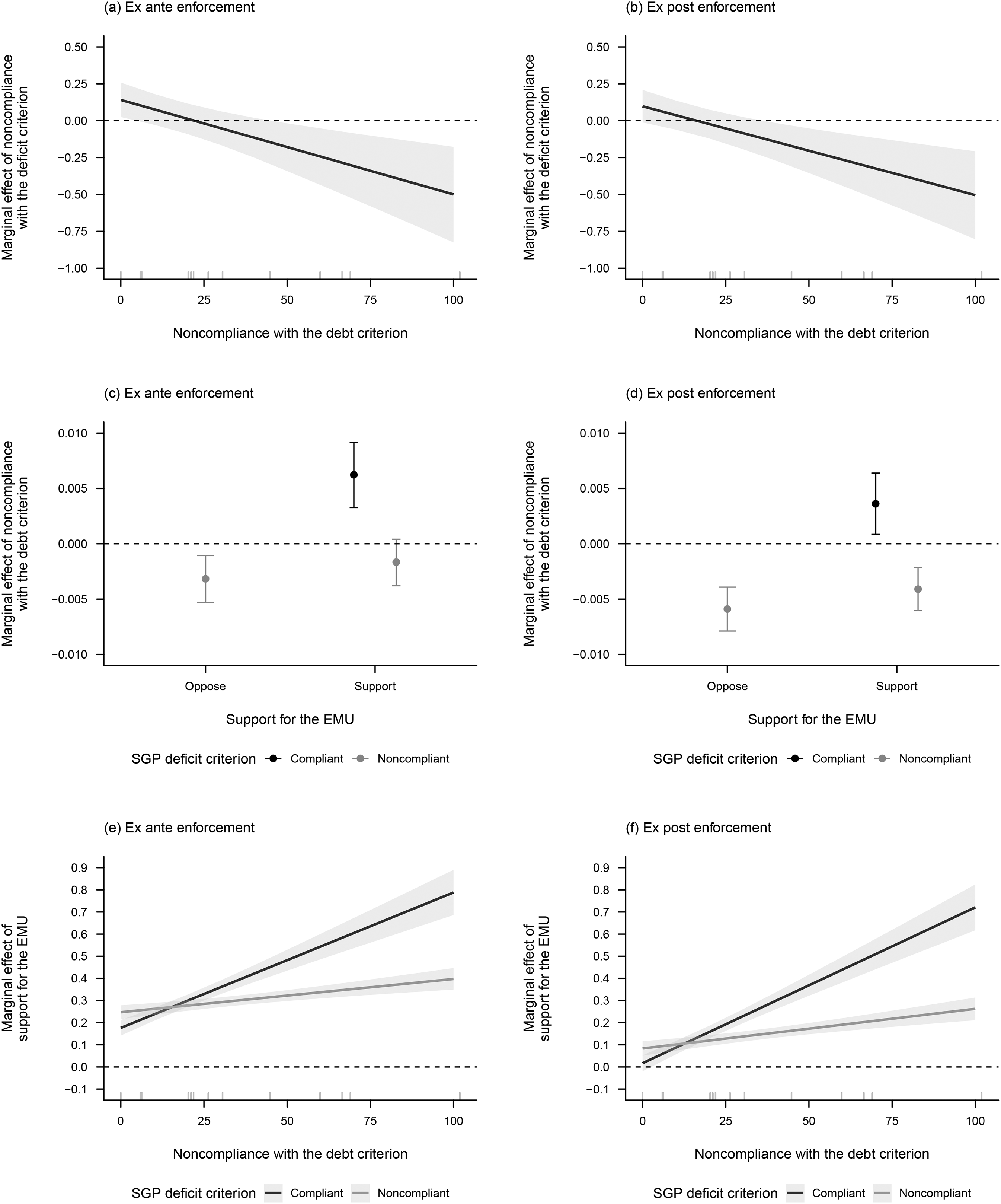

In both models, the 90% Bayesian credible interval for the three-way interaction term does not overlap 0. To evaluate the hypotheses, we need to examine conditional marginal effects plots (see Figure 3) because other parameter estimates do not provide useful information for evaluating the theory on their own. Figure 3(a) and (b) test H1, Figure 3(c) and (d) test H2a and H2b, and Figure 3(e) and (f) test H3a, H3b, and H3c. There is more uncertainty in the estimates of the SGP noncompliance variables, as these only vary by member state and the sample is small (19 member states).

Estimated conditional marginal effects. Note: This figure shows the results based on the imputed sample: (a) and (b) show the conditional marginal effects of noncompliance with the SGP deficit criterion, (c) and (d) show noncompliance with the SGP debt criterion, and (e) and (f) show support for the EMU.

H1 predicts that the marginal effect of noncompliance with the SGP deficit criterion will be negative, but only when the member state’s debt is highly SGP-noncompliant, which occurs when enforcement is most likely. Looking at Figure 3(a) and (b), this marginal effect is negative and the magnitude increases as a function of noncompliance with the SGP debt criterion. Consistent with H1, we can be confident that the effect is negative only for high levels of noncompliance with the SGP debt criterion.

H2a predicts that the marginal effect of noncompliance with the debt criterion will be positive when an individual supports the EMU and their member state is complying with the deficit criterion. H2b predicts that the marginal effect will be negative when and individual does not support the EMU and their member state is not complying with the deficit criterion. Theory does not make a prediction for the other two cases. Looking at Figure 3(c) and (d), the results are consistent with these predictions. A marginal increase in noncompliance with the debt criterion has a positive effect when the respondent supports the EMU and the respondent’s member state is complying with the deficit criterion and a negative effect when the respondent does not support the EMU and the respondent’s member state is not complying with the deficit criterion.

As mentioned previously, theory does not make a clear prediction about the marginal effect of an increase in a member state’s noncompliance with the SGP debt criterion when an individual supports the EMU and their member state’s deficit is SGP-noncompliant. However, this is a substantively interesting case because respondents have to weigh a decrease in the probability of exiting the Eurozone due to a debt crisis against an increase in the probability of EU-imposed austerity. In the ex ante model, this estimated effect is not distinguishable from zero, whereas in the ex post model, the effect is negative. When the respondent’s member state’s deficit is SGP-compliant, the effect is positive. Thus, the data suggests that, when their member state’s deficit is SGP-noncompliant, respondents heavily weigh the higher risk of austerity.

H3a predicts that the marginal effect of support for the EMU will be positive, regardless of a member state’s noncompliance with the SGP criteria. H3b predicts that the effect will be smallest with a member state’s debt is SGP-complaint, whereas H3c predicts that the effect will be largest when its deficit is SGP-compliant and its debt is SGP-noncompliant. Figure 3(e) and (f) provide clear support for these predictions, for both ex ante and ex post enforcement. The marginal effect is always positive, the effect is smallest when the member state’s debt is SGP-compliant, and the effect is largest when the member state’s deficit is SGP-compliant and its debt is SGP-noncompliant.

Overall, I find empirical evidence that the preferences of survey respondents are consistent with my theoretical predictions. Moreover, I find that a member state’s noncompliance with the SGP criteria generally undermines public buy-in for SGP enforcement. Specifically, the effect of a member state’s noncompliance with the deficit criterion is negative when its debt is highly SGP-noncompliant. In addition, the effect of a member state’s noncompliance with the debt criterion is negative when a member state’s deficit is SGP-noncompliant, among respondents who oppose the EMU. Given the EU’s strategic enforcement behavior, this means we should expect enforcement to be less likely precisely when it is most needed to prevent a crisis.

Conclusion

In light of the EU’s reforms to the SGP, which enhanced the SGP’s enforcement mechanisms and recommitted the EU to enforcing the SGP, this article develops and tests a theory that predicts the conditions under which individuals are more likely to think that SGP enforcement is an effective solution to the Eurozone crisis. I argue that noncompliance with the SGP criteria conditions the effects of SGP enforcement on an individual’s member state, and an individual’s political support for the EMU shapes the conclusions they will draw about the effectiveness of SGP enforcement, given those effects.

My findings suggest that individuals’ evaluations of EU economic policies depend not only on the likely effects of the policy, but also on how individuals interpret those effects through the lens of their political preferences. This speaks to the importance of theorizing the process by which individuals evaluate tradeoffs across the various effects of a policy given their other political commitments (Carrubba and Singh, 2004; Gabel, 1998). The literature on public opinion should continue to focus more on theorizing public opinion on specific policies (e.g. Kanthak and Spies, 2018).

I also show that patterns in public opinion about the effectiveness of SGP enforcement could undermine EU enforcement of the SGP. Recent studies on compliance and enforcement find that the Commission is strategic (e.g. Fjelstul and Carrubba, 2018; König and Mäder, 2014). I show that public buy-in for SGP enforcement is lower precisely when enforcement is more important for preventing a debt crisis, raising doubt as to whether the Commission will enforce the reformed SGP. EU policy-makers should carefully consider how the public will respond to policies and whether a lack of buy-in could undermine the EU’s political will to enforce them, just as happened in the lead up to the Eurozone crisis.

Finally, future research should examine whether respondents’ policy preferences are more sophisticated when they are asked to evaluate concrete policies, like SGP enforcement, compared to when they are asked about their support for abstract concepts, like European integration. Even if individuals do express sophisticated preferences over a complex policy, this does not necessarily mean that they are doing the cognitive work of evaluating the policy themselves. Future research should also consider the mechanisms by which political elites and the media shape public opinion over specific policies in times of crisis, when the public is paying close attention to the media.

Footnotes

Acknowledgements

I thank Cliff Carrubba, Matt Gabel, Pablo Montagnes, Adam Glynn, the editor, and the anonymous reviewers for their helpful comments and suggestions. An earlier version of this article was presented at the Graduate Workshop on the European Union at the University of Washington in 2017. I thank the participants for their helpful comments and suggestions. I also thank Hannah Langsam for research assistance.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.