Abstract

Does culture have a causal effect on institutional trust? We answer this question by assessing the non-economic determinants of public trust in the European Central Bank. To analyse institutional trust, we employ a novel dataset of citizen perceptions and knowledge about the European Central Bank. Cultural traits are measured by indicators of social trust at the level of Euro area sub-national regions. We show that individuals living in regions with lower social trust systematically exhibit less trust in the European Central Bank. An instrumental variable approach based on historical variables of education and political institutions supports a causal interpretation of our findings. These results are robust across different model specifications and measures of trust.

Introduction

Trust in policy-making institutions is an essential aspect of domestic and international governance. Institutional trust is critical because the efficacy and legitimacy of policy-making institutions depend on it (Dellmuth and Schlipphak, 2020; Zürn, 2018). Many studies have analysed the determinants of trust in domestic and international institutions. A growing body of research in this area has focused on the sources of trust in central banks, and especially the European Central Bank (ECB) (e.g. Bergbauer et al., 2020; Bursian and Fürth, 2015; Hayo and Neuenkirch, 2014; Roth et al., 2014; Roth et al., 2016; Roth and Jonung, 2020; Wälti, 2012). Notably, most attention has been devoted to assessing the socio-economic determinants of trust in central banks at the individual- and country-level. Scholars have neither systematically considered the non-economic determinants of trust in the ECB, nor have they attempted to shed light on the patterns of sub-national regional heterogeneity in central bank trust in the Euro area. This article aims to fill this gap by addressing the following research question: do cultural differences at the regional level affect public trust in the ECB?

To answer this question, our examination combines insights from research on European public opinion (e.g. Bechtel et al., 2014; Dellmuth and Tallberg, 2020; Hooghe and Marks, 2005; Inglehart and Norris, 2016) and cultural economics (e.g. Guiso et al., 2004; Guiso et al., 2006; Knack and Keefer, 1997; Tabellini, 2010). We hypothesise the trust in the ECB is not only about the assessment of the output performance of the institution, but also about cooperative expectations that are ingrained in sub-national regional cultures. In essence, we argue that people residing in areas with higher localised cultural predispositions for cooperative behaviour are more likely to display trust in joint European institutions. Importantly, as highlighted by Hobolt and De Vries (2016, 421), previous studies assessing the effect of culture and identity on trust in the European Union (EU) and its institutions have often relied on measures that are endogenous to EU support. This article employs a research design that overcomes this limitation.

To measure trust in the ECB, we rely on a new dataset of citizens’ perception and knowledge about the ECB. Data were collected in all the 19 countries of the Euro area in 2016, 2017 and 2018. To measure cultural traits across Euro area sub-national regions, we follow previous studies in the economics literature (e.g. Beugelsdijk and Schaik, 2005; Tabellini, 2010) and quantify cultural differences with indicators of regional social trust (i.e. the percentage of people who state that, generally speaking, most people can be trusted) from the European Social Survey.

The key difficulties in estimating the causal effect of culture on institutional trust are given by reverse causation and omitted-variables bias. To overcome this endogeneity issue, we resort to an instrumental variable approach. We take inspiration from the strategy advanced by Tabellini (2010) and rely on historical data to isolate the exogenous component of regional social trust. In particular, we use data on institutionalised constraints on the decision making powers of chief executives in the 1600–1850 period and literacy rates at the end of the 19th century to build a measure of social trust that does not suffer from reverse causation or omitted variable bias.

After controlling for country fixed effects and individual socio-economic determinants, the results show that individuals living in regions with lower social trust systematically exhibit less trust in the ECB. The use of historical variables as an exogenous source of variation in social trust supports a causal interpretation of our findings. These variables are a predictor of today’s regional social trust and are positively and significantly associated with individual trust in the ECB. Employing data from the World Values Survey and the Eurobarometer Survey, we show that our findings on the causal effect of culture on institutional trust are robust to different model specifications and across different sources of data for both social trust and ECB trust. Furthermore, we document that this effect extends to the EU and other European institutions (i.e. the European Commission and the European Parliament), while the estimated effect is weaker for national institutions (i.e. national parliaments and governments).

Trust and central banks

The notion of institutional trust occupies a prominent position in social science research. Most definitions of institutional trust in the literature focus on the concept of citizen expectations about institutional performance. For instance, Hudson (2006) conceptualises public trust in institutions as the confidence that a given institution will fulfil its role in an adequate manner. This definition emphasises the notions of perceived competence of an institution to achieve the objectives of its mandate, and is in line with the view of Mishler and Rose (2001: 31), who see institutional trust as the ‘expected utility of the institution performing satisfactorily’. Other definitions have taken an either narrower or broader stance with regard to the scope of citizen expectations about institutional competence and values, but they do not fundamentally differ in the centrality attributed to expected institutional performance (e.g. Hakhverdian and Mayne, 2012; Levi and Stoker, 2000; OECD, 2017; Sønderskov and Dinesen, 2016).

Many studies have attempted to assess the foundations of trust in domestic (e.g. Dellmuth and Tallberg, 2020; Foster and Frieden, 2017; Marien and Hooghe, 2011; Mishler and Rose, 2001; Stevenson and Wolfers, 2011) and international institutions (e.g. Armingeon and Ceka, 2013; Dellmuth and Schlipphak, 2020; Muñoz et al., 2011; Roth, 2009; Torgler, 2008). Within this literature, trust in central banks has increasingly captured the attention of scholars across disciplines for at least two reasons.

First, trust in central banks is essential for an effective transmission of monetary policy. In particular, it is the economic expectations of the general public (e.g. consumers and small-medium enterprise owners) that affect prices. As noticed by Ehrmann et al. (2013), low public trust in monetary authorities may contribute to leading inflation expectations astray from their inflation target, thereby undermining central banks’ ability to deliver on their mandate. Consistent with this hypothesis, recent evidence shows that central bank trust significantly contributes to lowering individuals’ expectations about future inflation and facilitates the anchoring of these expectations around the ECB’s target (e.g. Baerg et al., 2018; Christelis et al., 2020; Mellina and Schmidt, 2018). Hence, in order to control inflation expectations, a high level of public trust in central banks is essential.

Second, public trust is crucial for the legitimacy of central banks, and the ECB in particular. The ECB has an unusual status of being both a supranational institution and an independent central bank. Despite being committed to an increasingly higher degree of transparency and accountability (Fraccaroli et al., 2018), the ECB has been criticised for being free ‘from democratic oversight and control’ (Berman and McNamara, 1999) and the legitimacy of its unconventional monetary policies has often been challenged (e.g. Högenauer and Howarth, 2016; Sinn and Wollmershaeuser, 2011). Lacking direct electoral support, the ECB’s legitimacy rests on the layer of public trust. If this trust plummets, citizens may pressure their politicians to restrict the ECB’s independence, which may lead them to alter the ECB’s mandate or even to regain control over the national monetary policy (Kaltenthaler et al., 2010).

For these reasons, a growing body of research in this area focuses on the sources of trust in central banks, and especially the ECB. Notably, the existent literature relies primarily on data from the Eurobarometer survey and assesses determinants of central bank trust either at the country level or at the individual level. Most of these studies focus on macroeconomic, financial and socio-economic determinants of trust in the ECB.

Focusing on country-level macroeconomic determinants, in a pooled cross-section analysis of Eurobarometer data from 1999 to 2004, Fischer and Hahn (2008) show that trust in the ECB decreases with higher inflation rates and active labour market policies, while higher GDP and unemployment spending are positively associated with central bank trust. Extending the time frame to 2010, Wälti (2012) investigates the aggregate dynamics of declining trust in the ECB after the global financial crisis and shows that trust has decreased more in those Euro area countries that have experienced increasing sovereign bond yields and financial market turbulence. Roth et al. (2014) document a negative and significant relationship between unemployment and trust in times of crisis. This relationship has been confirmed by Roth et al. (2016): they show that the pronounced increase in unemployment in the Euro area led to a marked decline in trust in the ECB during the crisis, while unemployment was more weakly related to support for the Euro. Furthermore, Roth and Jonung (2020) provide evidence that ECB trust has been only partially restored by the improvement of employment conditions in the post-Euro crisis period, suggesting that the loss of trust in the ECB will take time to recover.

Focusing on individual-level determinants, Kaltenthaler et al. (2010) show that economic perceptions and attitudes towards the EU and democracy correlate with trust in the ECB. Considering a set of 12 Euro area countries, Bursian and Fürth (2015) find that individuals with left-leaning political views and low educational attainment are less likely to show trust in the ECB. Ehrmann et al. (2013) find that individual demographic factors and attitudes towards EU institutions are good predictors of trust in the ECB. Also, Farvaque et al. (2017) provide evidence that expected inflation has a greater effect on trust than the actual inflation rate. Highlighting the disconnect between attitudes towards the ECB and support for the Euro, Bergbauer et al. (2020) show that trust in the ECB is driven by citizens’ evaluation of the EU’s policy performance, while support for the single currency is largely based on underlying values relating to European integration.

More closely related to this article, some studies have departed from the traditional focus on individual- and country-level socio-economic determinants of ECB trust, and have tried to expand the analysis of its dynamics in two different directions. First, Bursian and Fürth (2015) have shed light on sub-national regional variation of central bank trust in the Euro area. Their study highlights that regional macroeconomic conditions are associated with public trust in the ECB, with this association becoming stronger after 2008. Second, Hayo and Neuenkirch (2014) have assessed some non-economic determinants of central bank trust. They document that specific knowledge about the ECB’s mandate has a positive effect on central bank trust, while the intensity of media usage is negatively and significantly associated with trust in the ECB, at least in Germany.

However, very limited attention has been paid to the effect of cultural factors and sub-national regional heterogeneity on central bank trust in a joint perspective. Despite not being focused on central bank trust, an interesting exception is given by Jost (2018), who shows that linguistic differences in Switzerland are associated with different preferences with regard to inflation and unemployment, thereby suggesting that divergent preferences about central bank policies may be driven by distinct cultural backgrounds. This article aims to fill the gap by investigating how cultural differences at the regional level affect public trust in the ECB.

The cultural roots of trust in European institutions

Does culture have a causal effect on trust in the ECB and other European institutions? To answer the question, we first have to clarify how culture is conceptualised in our study. We adopt the definition provided by Guiso et al. (2006, 23), who formalise culture ‘as those customary beliefs and values that ethnic, religious and social groups transmit fairly unchanged from generation to generation’. In this article, we focus on cultural differences across Euro area regions. To do so, we consider social trust – defined as the degree of trust a person has towards another (Guiso et al., 2008) – as a proxy of cultural orientations. Social trust is the most studied and frequently considered one of the main cultural traits in political economy studies (Roland, 2015).

Why should we expect culture to affect trust in the ECB? One important reason has to do with the double nature of the ECB. On the one hand, the ECB is an independent monetary authority in charge of maintaining price stability in the Euro area. Given the narrow mandate of the ECB, one may expect citizen trust in the ECB to be exclusively driven by economic and financial considerations. Most of the studies reviewed above start from this assumption and primarily focus on the socio-economic and financial determinants of trust in the ECB. Seen in this light, the ECB constitutes a hard test to evaluate the hypothesis of a connection between culture and institutional trust.

On the other hand, the ECB is a European institution embedded in the wider framework of the EU. Over the past decade, the ECB has increasingly played a pivotal role in EU governance and has received growing public attention, especially due to its shift to a proactive approach to tackle financial turmoil in the Euro area (e.g. Ferrara, 2020), its political leadership in the Euro crisis (Tortola and Pansardi, 2019), and its responsiveness to the pressures of the European public (e.g. Moschella et al., 2020). Thus, it is reasonable to expect citizen trust in the ECB to be driven by antecedent factors affecting a broader range of views and opinions about European integration and EU institutions. When taking the ‘Europeanness’ of the ECB’s institutional nature into consideration, it is possible to extend the analytical perspective beyond the work on central bank trust reviewed in the previous section and build upon the insights of a broader range of studies in the field of European politics and political economy.

First, research on European public opinion suggests that culture may shape attitudes towards the EU and European institutions, including the ECB. The idea that cultural traits may affect confidence in European institutions is in line with explanations that emphasise how collective identities are important determinants of public support for the EU (Hobolt and De Vries, 2016: 420-421; Kuhn and Nicoli, 2020). Scholars have argued that a broad range of EU-related attitudes of European citizens reflects purely cultural factors, such as the tension between nationalist and cosmopolitan identities (Carey, 2002; Hooghe and Marks, 2005; Hooghe and Marks, 2009) or the level of altruism within the public (Bechtel et al., 2014). A particularly influential argument is that lower EU support and trust in European institutions can be explained as a social psychological phenomenon, reflecting a nostalgic reaction against long-term processes of value change (Inglehart and Norris, 2016) and subjective perceptions of social status loss (Gidron and Hall, 2017).

While this strand of the literature has emphasised more the notion of identity than that of culture, it follows from these studies that trust in the ECB and other European institutions may not be only about monetary policy and the single market, but also about a pooling of sovereignty that clashes with different cultural perspectives inside the EU (Hobolt and De Vries, 2016: 420). Thus, inasmuch as the ECB is part of the realm of European institutions, it is reasonable to expect cultural differences, including those at the sub-national regional level, to play a role in the way it is perceived by the public.

This raises the question of why it is worth focusing on regional variation in culture across the Euro area. A large literature in economics and political economy has uncovered the impact of different cultural traits on economic, political and institutional variables (for reviews, see Castellani, 2019 and Fernández, 2010). This literature is largely inspired by important contributions in political science (e.g. Fukuyama, 1995; Putnam, 1993), which provide evidence that social trust and participation in social activities differ strikingly across regions and countries, and have important consequences for economic and institutional development. In particular, this literature has shown that regions with higher levels of social trust tend to have better working democratic institutions (Putnam, 1993), better economic performance (Beugelsdijk and Schaik, 2005; Knack and Keefer, 1997; Tabellini, 2010; Zak and Knack, 2001), higher levels of financial sophistication (Guiso et al., 2004) and tend to be more willing to push for the creation of multilateral institutions (Rathbun, 2011).

In line with these contributions, some scholars have examined the presence of a link between cultural factors, such as social trust, and trust in international institutions. For instance, using original survey data on citizen attitudes toward four international organisations in three countries, Dellmuth and Tallberg (2020) provides evidence for social trust as an antecedent factor of attitudes towards international institutions. This study draws from previous research on social capital (e.g. Brehm and Rahn, 1997) and relies on the hypothesis that people who expect cooperative behaviour from other people have higher confidence in joint political institutions.

We extend this argument to the sub-national regional level in Europe. In this article, we hypothesise that citizens residing in areas characterised by stronger cultural predispositions for cooperative behaviour are more likely to display trust in the joint institutions of the EU. Thus, we expect regional social trust, taken as a proxy of a wider set of cultural traits, to exert a causal impact on trust in the ECB and other European institutions. Crucially, as highlighted by Hobolt and De Vries (2016: 421), most of the previous research concerning the effects of culture and identity on the opinions of the public towards the EU has fallen short of addressing issues of endogeneity in the evaluation of this relationship. This article attempts to overcome this limitation of previous studies.

Data and methods

Data

The main independent variable in our analysis is the level of social trust in sub-national regions of Euro area countries. In line with the literature on cultural economics discussed in the previous section, we take this as a proxy of differences in cultural traits across European regions. Following the approach employed by several authors (e.g. Beugelsdijk and Schaik, 2005; Tabellini, 2010), we create our main independent variable by aggregating at the regional level – either NUTS1 or NUTS2 based on data availability – individual responses collected in opinion polls. In particular, for the measure of social trust we rely on the European Social Survey (ESS) data between 2002 and 2016. 1

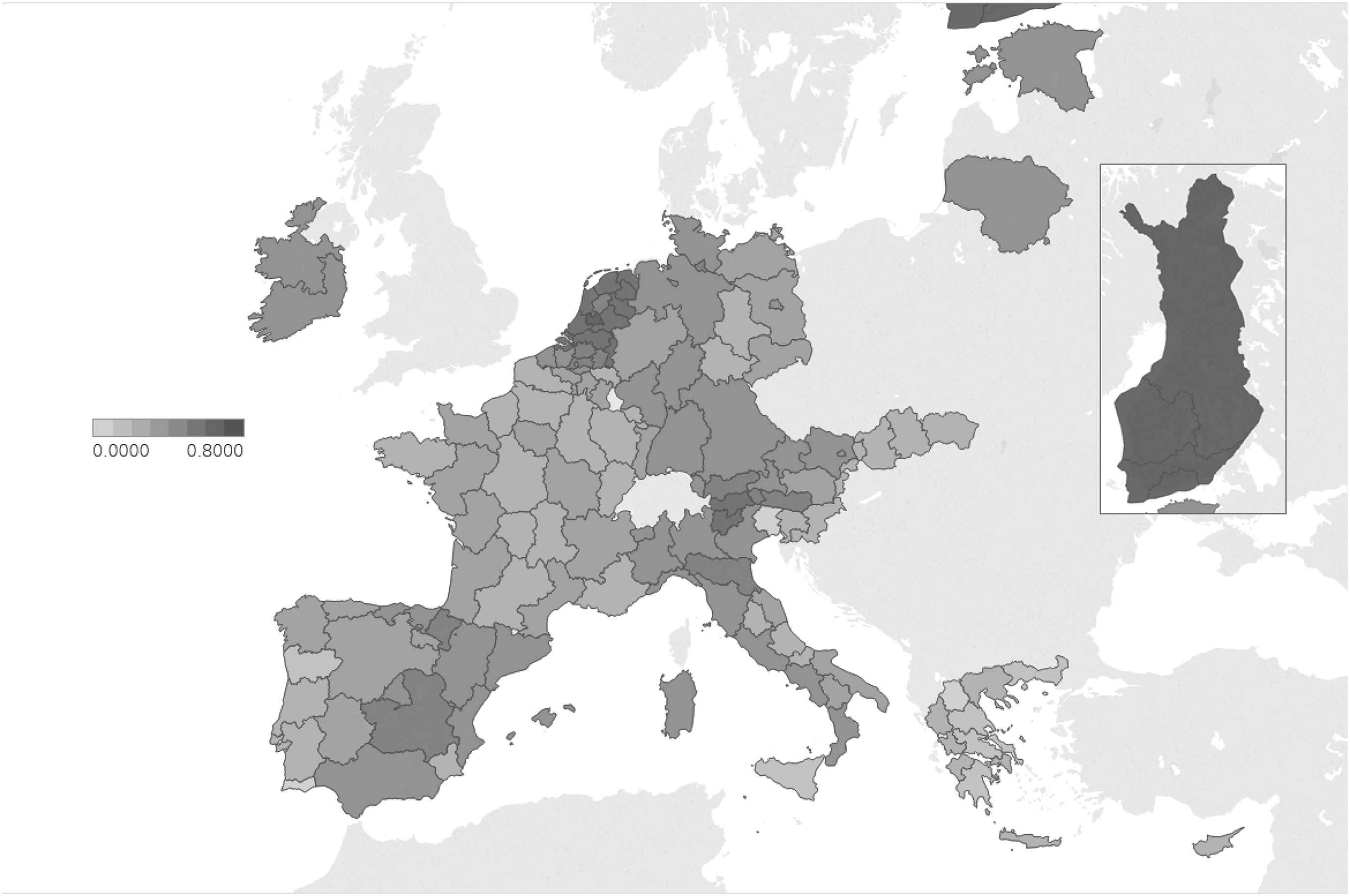

Consistent with previous studies using responses to the World Values Survey, we employ the following survey item from the ESS: ‘Generally speaking, would you say that most people can be trusted, or that you can’t be too careful in dealing with people?’. Respondents are provided with a scale from 0 to 10. For our main independent variable, we compute the regional share of respondents who state that most people can be trusted, namely individuals who choose a value higher than 5. Figure 1 displays the variation in strength of social trust across regions.

Social trust across Euro area regions.

For the other variables taken into account in the analysis, such as trust in the ECB, we rely on novel data collected in the 19 Euro area countries in 2016, 2017 and 2018 for the ECB Knowledge & Attitudes Survey (K&A). The K&A is a survey conducted for the ECB once a year during the first few weeks of December since 2015 2 by Kantar, the same external provider of the Eurobarometer for the European Commission. In the Online appendix, we discuss how the K&A compares with the Eurobarometer and the advantages of employing the former survey for our primary analyses. We resort to Eurobarometer data to test the robustness of our results.

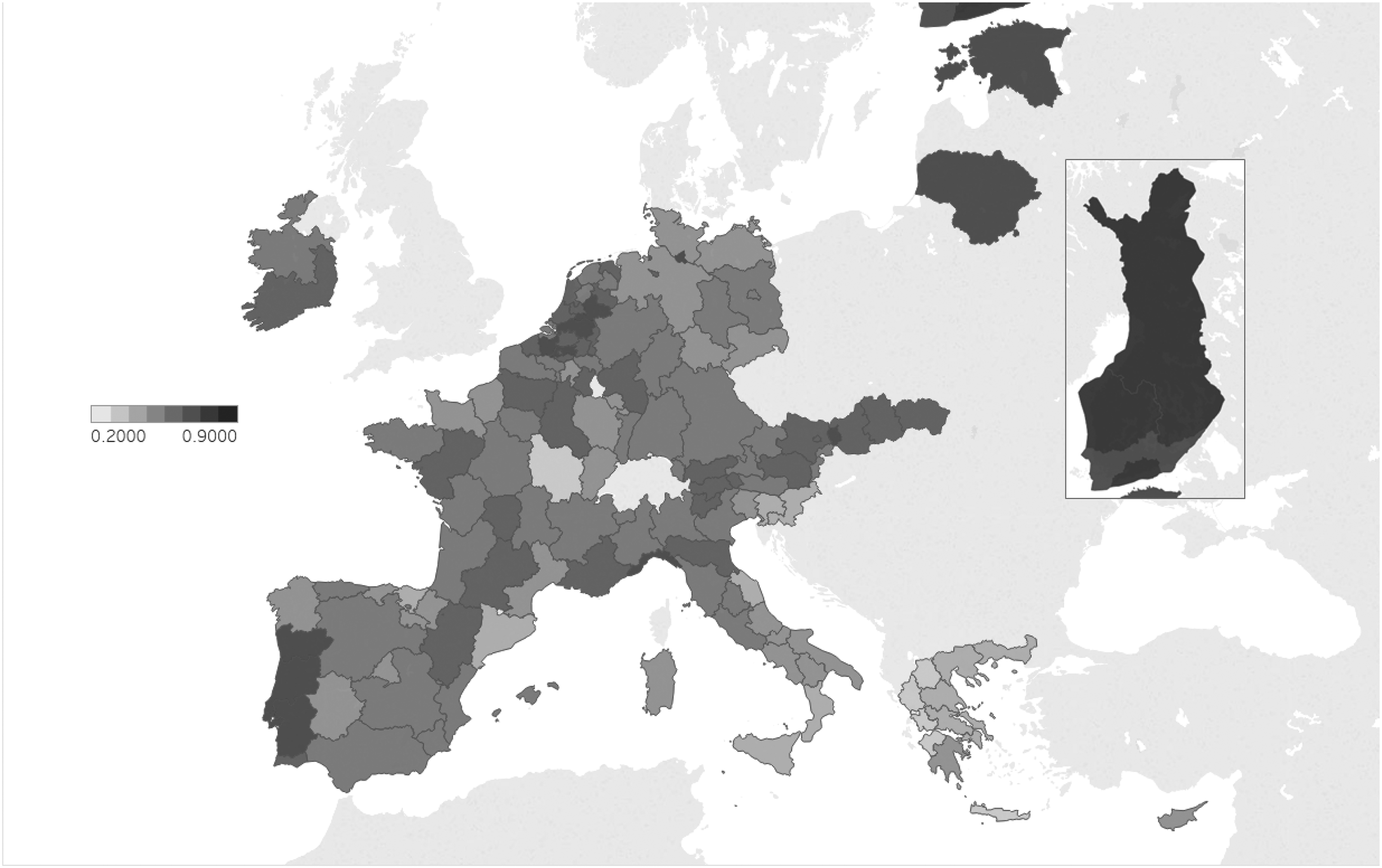

The main dependent variable in our analysis is measured by the question ‘Do you tend to trust or not to trust the ECB?’. The wording and the possible answers (‘Yes’, ‘No’, ‘Don’t know’) are exactly the same as the trust question in the Eurobarometer. We do not take into account non-responses to the trust question and use a dummy equal to 1 if the person trusts the ECB and 0 if she does not. Figure 2 displays the share of respondents who trust the ECB across Euro area sub-national regions. The Online appendix presents the summary statistics of all the variables in the K&A and Eurobarometer datasets we employ in our analysis.

Trust in the ECB across Euro area regions.

To better assess the non-economic determinants of central bank trust at the individual-level, data collected in the K&A survey on factual and self-assessed knowledge about the ECB are also included in some of our models. These data are not available in the Eurobarometer. For factual knowledge, people are asked to pick what they deem to be the ECB’s main objectives from a list. The knowledge score built using these answers ranges from 0 to 6, based on the number of correct answers. 3 The score for respondents who answered ‘Don’t Know’ is set to 0. Finally, we create a new variable dividing individuals according to their factual knowledge score in three categories, ‘Low’ (0-2), ‘Average’ (3-4) and ‘High’ (5-6).

Respondents provide their subjective evaluation of their knowledge about the ECB and the Eurosystem on a scale from 0 to 9. In this case as well, we recode ‘Don’t Know’ answers as 0 and build a new variable with three levels, ‘Low’ (0-3), ‘Average’ (4-5) and ‘High’ (6-9). Furthermore, as a measure of individual financial culture, we create a proxy for respondents’ financial sophistication based on the type of financial products that they use. Again, this variable has three ordered categories. 4 Finally, we consider a standard set of socio-demographic characteristics, such as a dummy equal to 1 if the person is female and the person’s age. Education is collected as the age at which one has stopped full-time education, which we recode as a categorical variable, with each level being a proxy for middle-school or lower education (<15 years old), high school (16–20) and college education (>20).

Causal identification strategy

The key difficulty in estimating a causal effect of culture is that it is endogenous to institutional trust. Indeed, trust in national and international institutions may affect cultural orientations and social norms at the regional level, which raises issues of reverse causation. For instance, using individual-level survey data from Denmark, Sønderskov and Dinesen (2016) show that trust in state institutions is a prominent explanation of social trust. Furthermore, the relationship between social trust and institutional trust is potentially confounded by unobservable factors, thereby engendering omitted-variable bias.

To overcome endogeneity issues, we need to find some exogenous source of variation in culture in order to identify a causal effect of culture on trust in the ECB. We resort to an instrumental variable approach. We focus on within-country variation among Euro area regions, and use historical data to isolate the exogenous component of regional social trust. In particular, we rely on data from Tabellini (2010) on regional levels of institutionalised constraints on the decision making powers of chief executives in the period from 1600 to 1850 and literacy rates at the end of the 19th century. After controlling for country fixed effects, Tabellini (2010) shows that regions with historically looser constraints on the executive power and lower literacy rates tend to have specific cultural traits today, most notably lower levels of social trust. In order to be valid, our estimation strategy rests on two premises:

Past education and early political institutions explain social trust at the regional level (relevance condition). Past education and early political institutions affect trust in the ECB only through their effect on regional culture after relevant economic channels are controlled for (exclusion restriction).

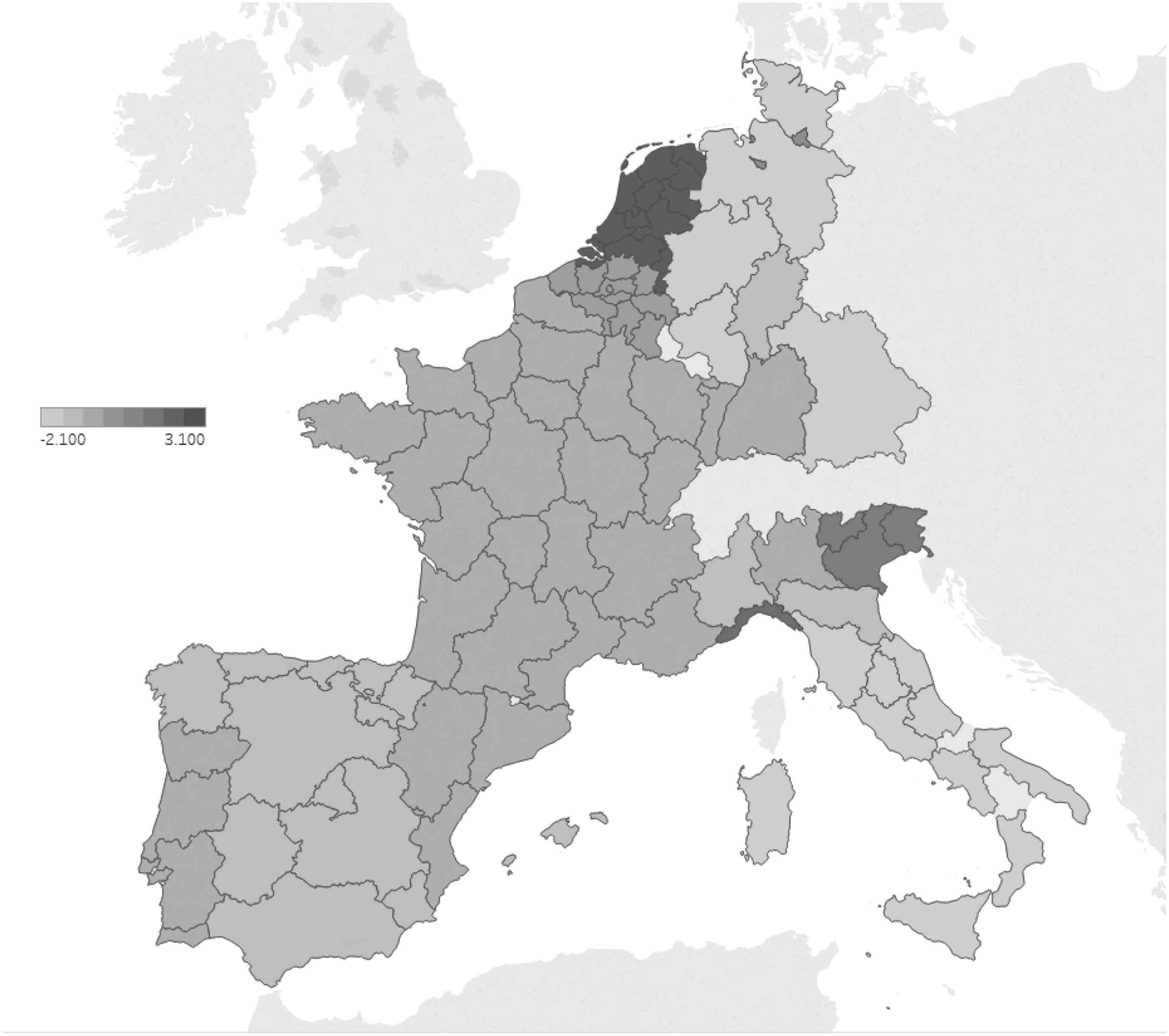

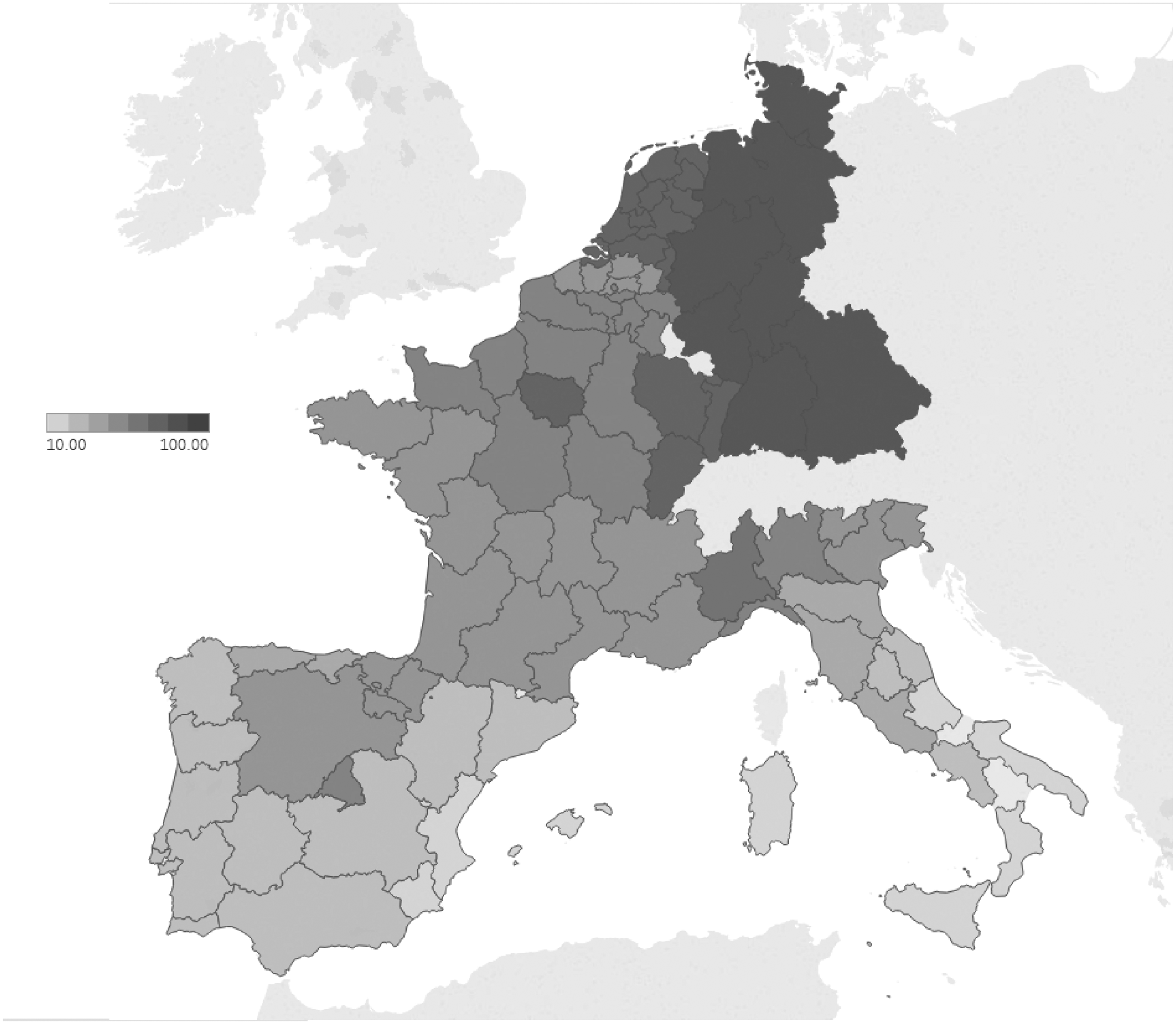

Data on past political institutions and early literacy rates are available only for a subset of 56 regions in seven Euro area countries: France, Germany (except East Germany and Berlin), Italy, the Netherlands, Belgium, Spain and Portugal. These data are illustrated in Figures 3 and 4.

Levels of institutionalised constraints on the executive power across Euro area Regions, 1600–1850.

Literacy rates across Euro area regions at the end of the 19th century.

The lower number of regions for which these data are available implies that, for our instrumental variable analysis, we have to restrict our sample of respondents to these regions only. The summary statistics in the Online appendix account for these differences in sample size across the different analyses performed below.

Empirical model

We estimate the effect of regional culture on institutional trust at the individual level through the following baseline equation:

In our analysis, we will also augment equation (1) by adding variables for financial sophistication, factual knowledge and self-assessed knowledge (

Results

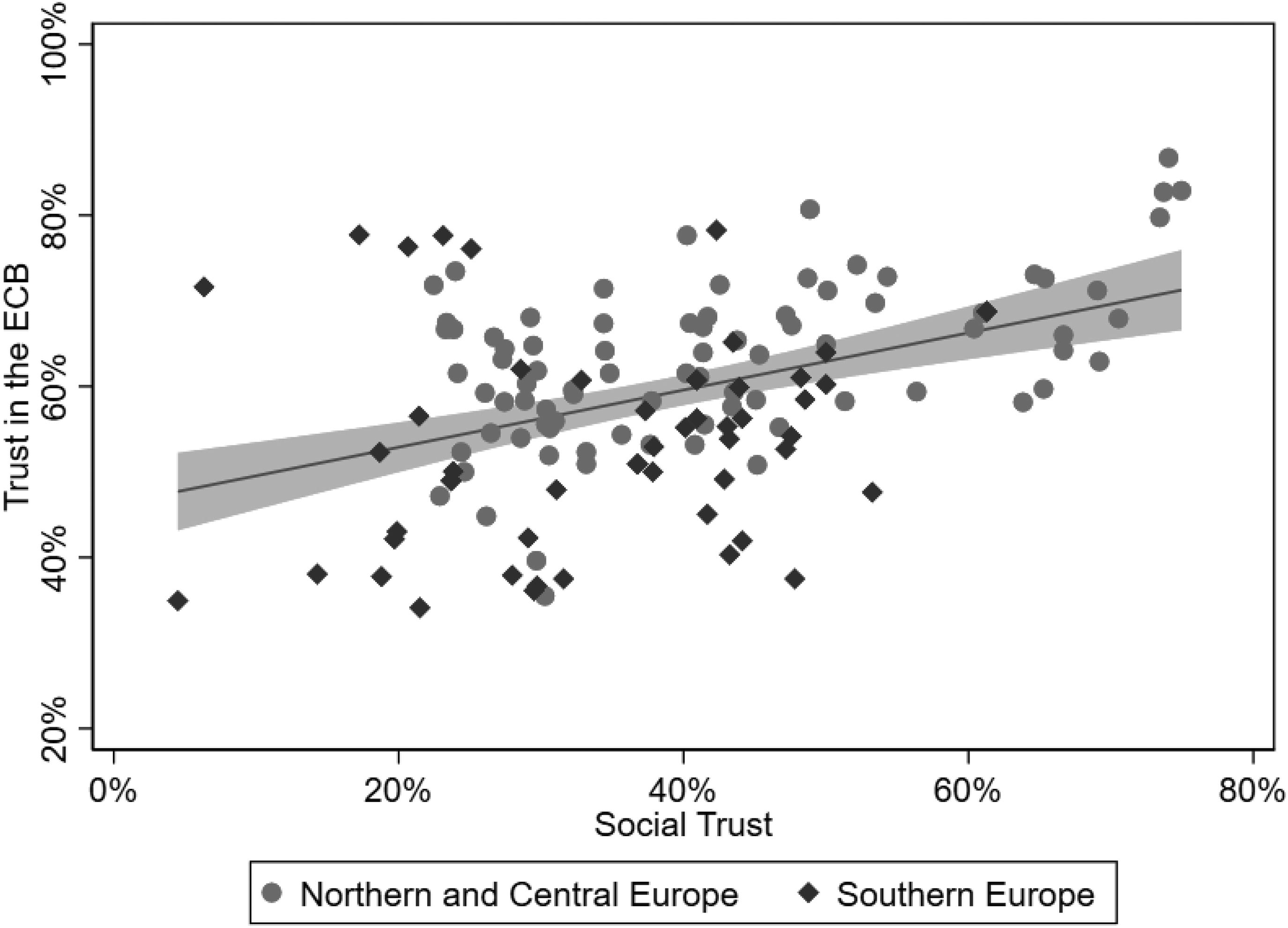

We start by considering the presence of correlational evidence between social trust and trust in the ECB at the aggregate level by Euro area sub-national regions. Figure 5 displays the share of ESS respondents who state that most people can be trusted (on the horizontal axis) and the share of K&A respondents who state they trust the ECB (on the vertical axis).

Social trust and ECB trust across Euro area regions.

The positive correlation between social trust and ECB trust is not due to specific outliers. Interestingly, Southern European countries (i.e. Cyprus, Greece, Italy, Portugal, Spain) exhibit a higher variance in ECB trust than Central and Northern European countries. As within-country regional differences are more pronounced in Southern Europe, most notably in Italy and Spain, this ensures that the relationship is not driven by few specific countries.

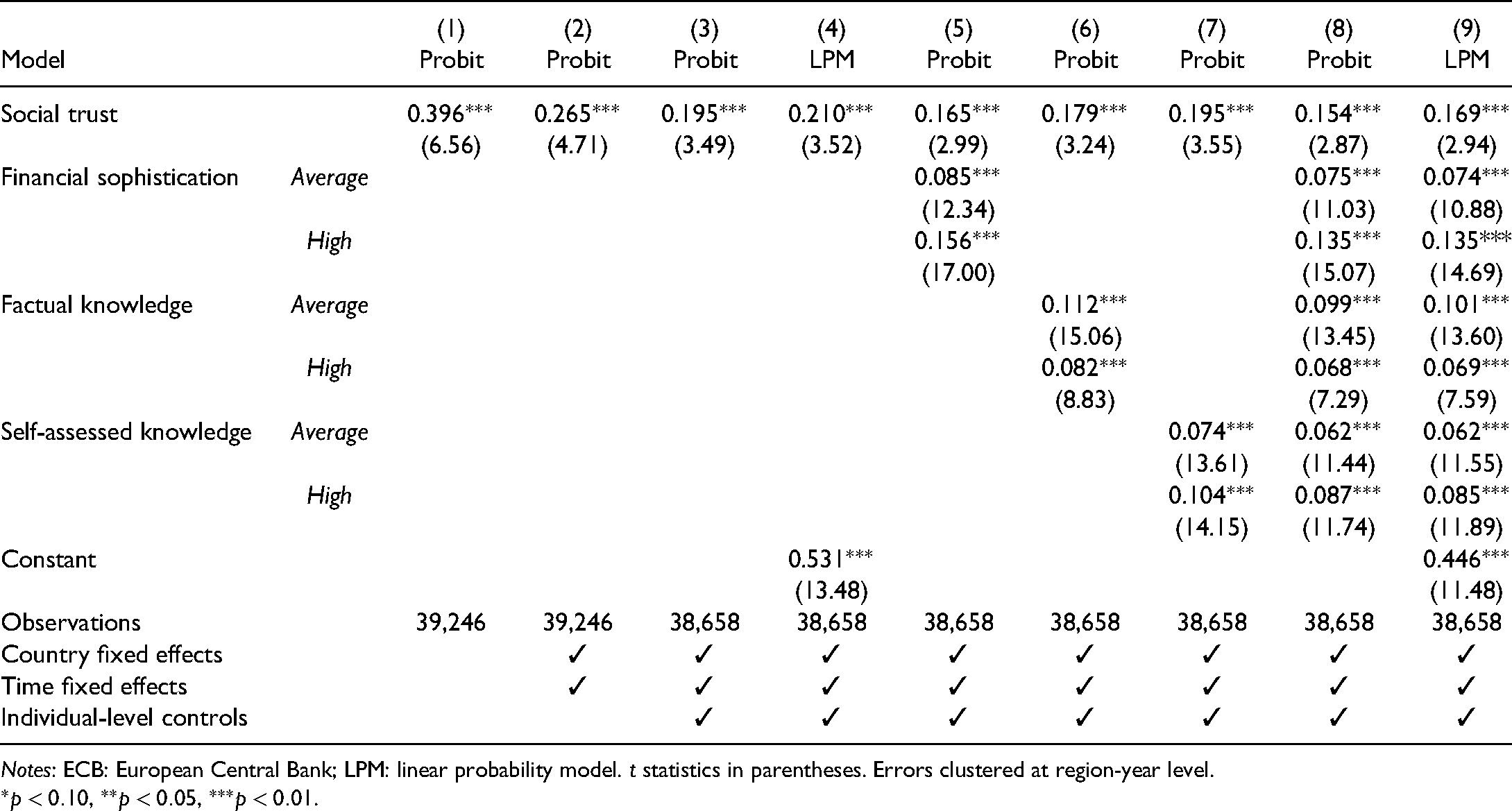

Table 1 presents the first set of results of our individual-level analysis. We estimate the relationship between regional social trust and individual trust in the ECB using different model specifications. We show marginal effects from probit models, as well as estimates from linear probability models (LPMs). In all models we cluster standard errors at the region-year level.

Cultural determinants of trust in the ECB: probit marginal effects and LPM regressions.

Notes: ECB: European Central Bank; LPM: linear probability model. t statistics in parentheses. Errors clustered at region-year level.

Column (1) presents results from a probit model without any controls. In column (2), we introduce country fixed effects and year fixed effects. In column (3), we include the individual-level controls. In column (4), we estimate a LPM with the same covariates included in the specification in column (3). In columns (5) to (7), we introduce, respectively, the variables for financial sophistication, factual knowledge and self-assessed knowledge in the probit specifications. In column (8), we include all three variables jointly in the probit model. Column (9) presents the results for the LPM specification with all variables.

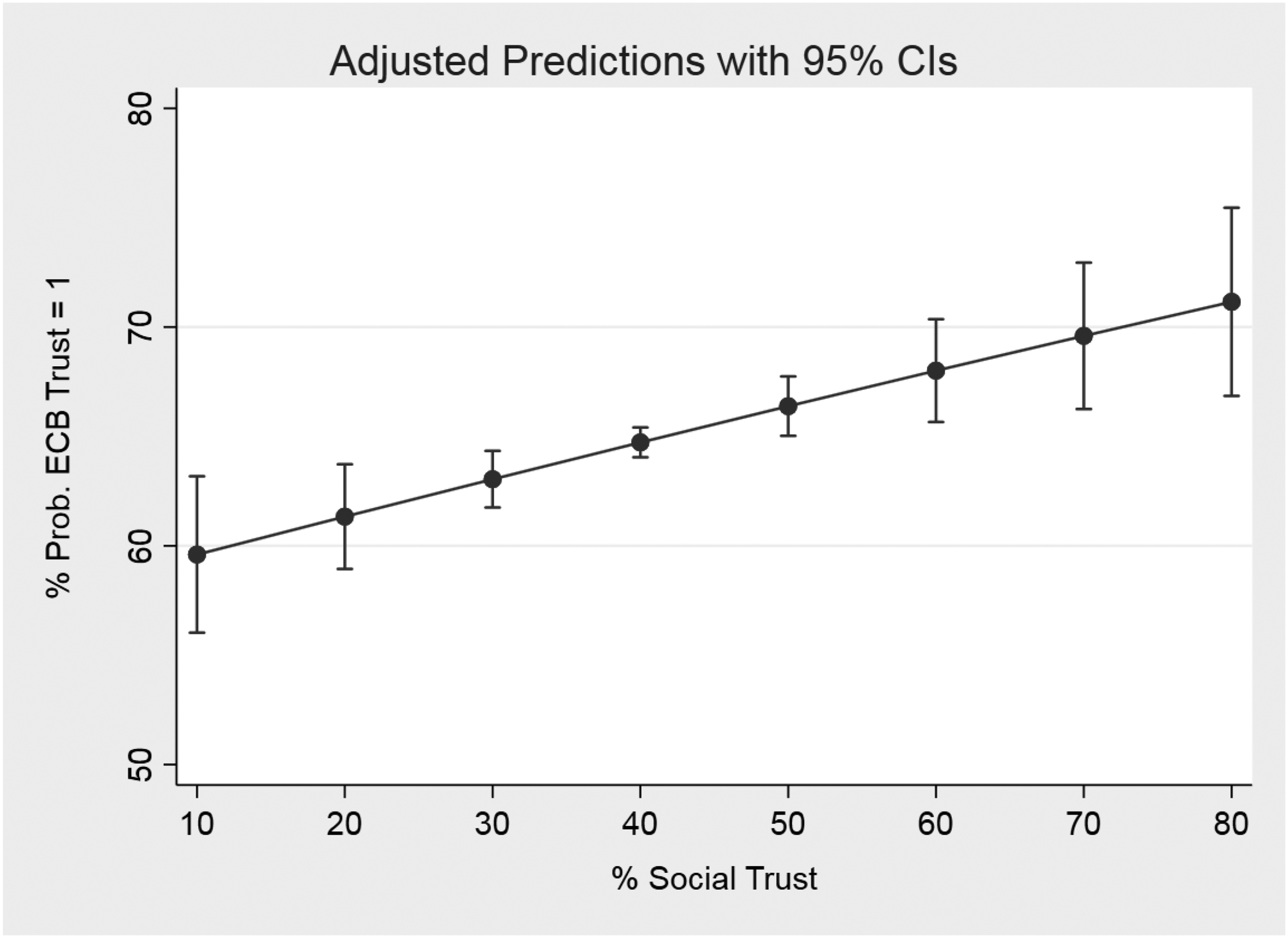

Results from column (1) of Table 1 show the presence of a positive and strong correlation between respondents’ trust in the ECB and the degree of social trust in their region of residence. The introduction of country and time fixed effects in column (2) and individual controls in column (3) only slightly reduces the magnitude and precision of the estimated coefficient. To better quantify the importance of this correlation, Figure 6 presents the predicted probability of trusting the ECB conditional on the level of regional social trust for an average individual. The strength of the association is sizeable: an individual residing in a region in the bottom 5% of the distribution of regional social trust (lower than 20%) is estimated to be 11% less likely to trust the ECB than an individual living in a region in the top 5% (higher than 70%), everything else being equal.

Predicted probability of trusting the ECB conditional on social trust.

Results from column (5) show that individuals with medium or high financial sophistication tend to trust the institution more than respondents with low levels of sophistication. The same conclusion holds for factual and self-assessed knowledge, as shown in columns (6) and (7). However, different from financial sophistication, the relationship between trust and knowledge appears to be non-linear: individuals with high levels of objective knowledge of the institution are not significantly more likely to trust the institution than respondents with medium levels. This result is displayed in the Online Appendix, which presents the predicted probability of trusting the ECB conditional on the levels of, respectively, financial sophistication, factual knowledge and self-assessed knowledge for an average individual.

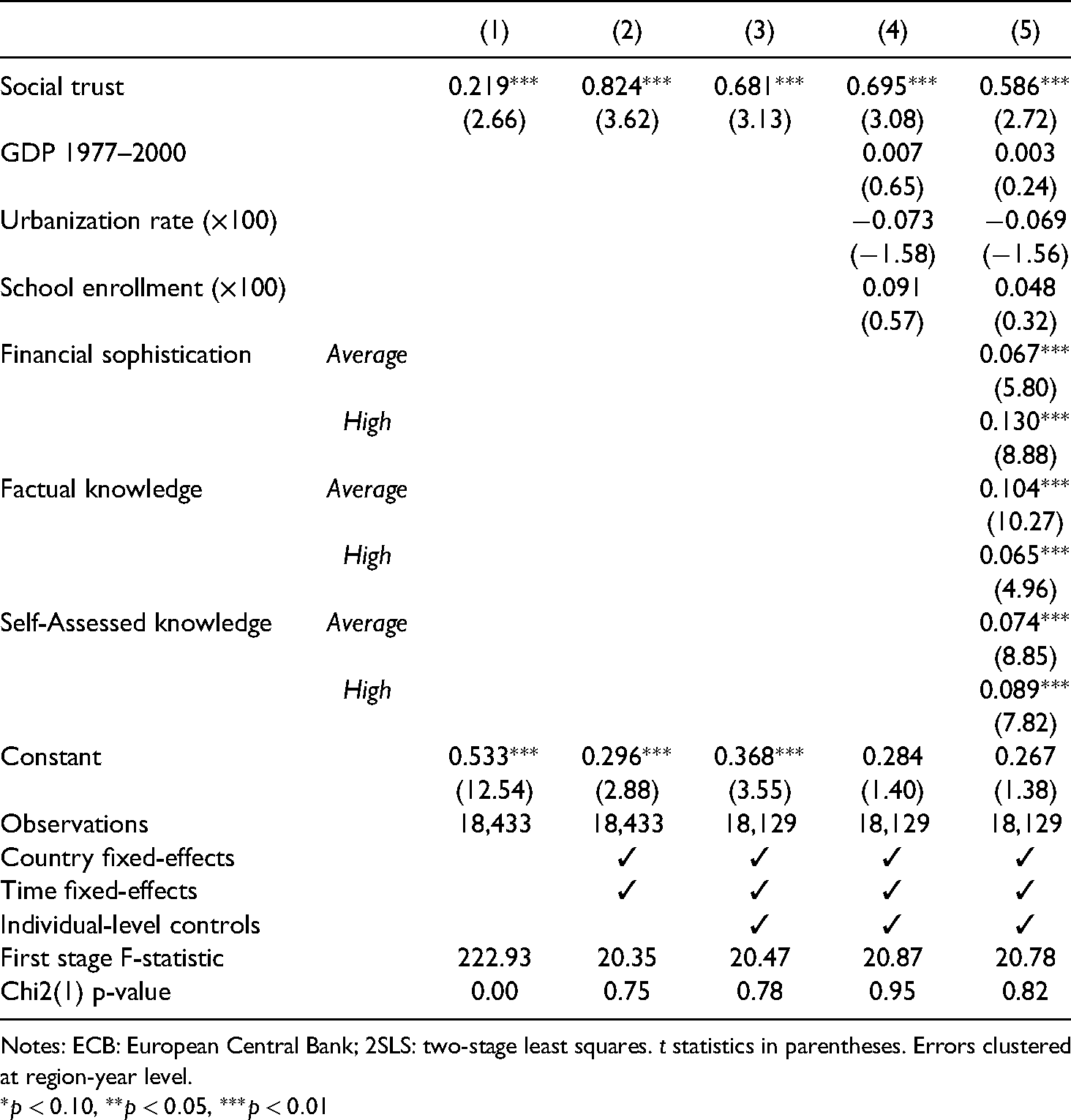

The following step in the analysis is to employ an instrumental variable approach to verify whether the exogenous component of regional social trust correlates with individual trust in the ECB. Table 2 presents the estimates from two-stage least squares (2SLS) regressions, in which regional social trust is instrumented with data on regional literacy rates and constraints on the executive power from Tabellini (2010). In line with the indication of Angrist and Pischke (2008), we estimate a linear model.

Cultural determinants of trust in the ECB: 2SLS regressions.

Notes: ECB: European Central Bank; 2SLS: two-stage least squares. t statistics in parentheses. Errors clustered at region-year level.

In column (1), we estimate the 2SLS model without any controls. In column (2), we include country and year fixed-effects. In column (3), we augment the model with individual socio-demographic factors. In column (4), following Tabellini (2010), we introduce controls for the rate of regional school enrolment in 1960 and urbanisation in 1850: these variables are aimed at ensuring that culture is not just used as a proxy for human capital in the region, thereby guaranteeing that the exclusion restriction is not violated. Additionally, we control for the average regional GDP from 1977 to 2000, to remove additional concerns about the effects of the economic channels via which past education and early political institutions might affect trust in the ECB. Finally, in column (5), we add the variables on financial sophistication and knowledge of the ECB.

In all cases, the first stage F-statistic for the joint significance of the instruments is above the threshold of 10. Moreover, with the exception of the model specification with no controls, the over-identification restriction is not rejected, as suggested by the p-value for of the Hansen J-statistic. The Online appendix presents the results of the first stage regressions for each of the model specifications estimated in Table 2. The results confirm the high statistical significance our two instrumental variables in explaining variation in the endogenous regressor.

It is worth highlighting that the conditioning on financial sophistication and ECB knowledge might distort the treatment effect estimates, as the two variables are significantly affected by the exogenous variation in sub-national regional culture. In other words, this could generate post-treatment bias (Montgomery et al., 2018). This is why we prefer the model specification used in column (4) for the robustness checks and the additional analyses in the following section. Precisely for this reason we also decide to employ historical, rather than contemporaneous, measures of regional economic performance as control variables, as in Tabellini (2010). The validity of our identification strategy should ensure that the effect of culture on institutional trust is accurately estimated independently of other drivers of trust in the ECB, such as unemployment, as shown by Roth et al. (2016).

Results from Table 2 show that the exogenous component of regional social trust is positively and strongly correlated with individual trust in the ECB. While no causal interpretation can be attributed to the effects of sophistication and knowledge on central bank trust, it is interesting to observe that this relationship maintains predictive value and remains statistically significant – something that may contribute to informing policy implications about the appropriateness to actively promote citizen knowledge of the ECB to foster public trust in the institution, as we discuss in the final section.

Robustness checks and additional analyses

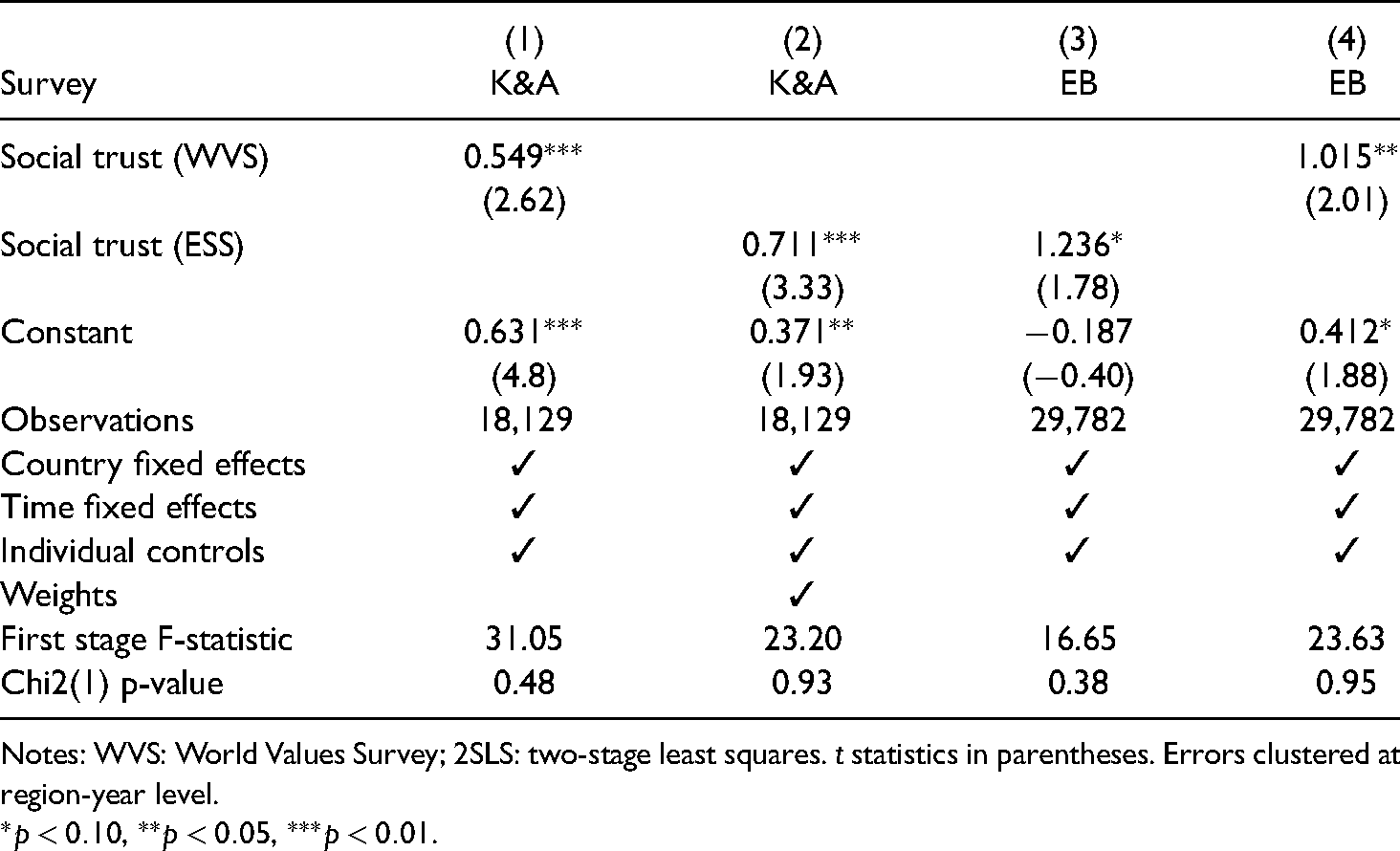

In this section, we discuss the robustness of the results to different model specifications and measures of social trust and ECB trust. Moreover, we verify whether social trust has a causal impact also on other institutions. Table 3 presents estimates from 2SLS regressions, using the same model specification of column (2) in Table 2. 5 We decide not to include individual financial sophistication and knowledge of the ECB out of concerns of post-treatment bias induced by these measures.

Robustness checks: 2SLS regressions.

Notes: WVS: World Values Survey; 2SLS: two-stage least squares. t statistics in parentheses. Errors clustered at region-year level.

In column (1) of Table 3, we maintain the same dependent variable used above, but employ a measure of regional social trust from the World Values Survey (WVS). The WVS question on social trust has the same wording of the ESS. The advantage of using the WVS is that it allows to measure social trust even before the 2000s. Thus, as in Tabellini (2010), we aggregate at the regional level individual responses collected in the opinion polls of the WVS in the 1990s to obtain the WVS social trust measure. In column (2), we regress the measure of ECB trust from the K&A survey on the ESS measure of social trust, but introduce weights in our specification. In both cases, the coefficient for regional social trust remains highly statistically significant.

In columns (3) and (4), we analyse whether regional social trust has a causal effect on trust in the ECB and other institutions based on Eurobarometer responses. In order to have a sample that is comparable to that of the K&A, we make use of data from Eurobarometer waves fielded in 2016, 2017 and 2018. 6 In columns (3) and (4), we consider trust in the ECB based on Eurobarometer responses as a dependent variable. In column (3), we make use of the ESS measure of regional social trust as the main independent variable. In column (4), we employ the WVS measure. Both variables attain statistical significance at conventional levels, although the coefficient of the WVS measure is more precisely estimated. In all cases, the first stage F-statistic is higher than the recommended threshold of 10 and the null hypothesis that the over-identifying restrictions are valid cannot be rejected.

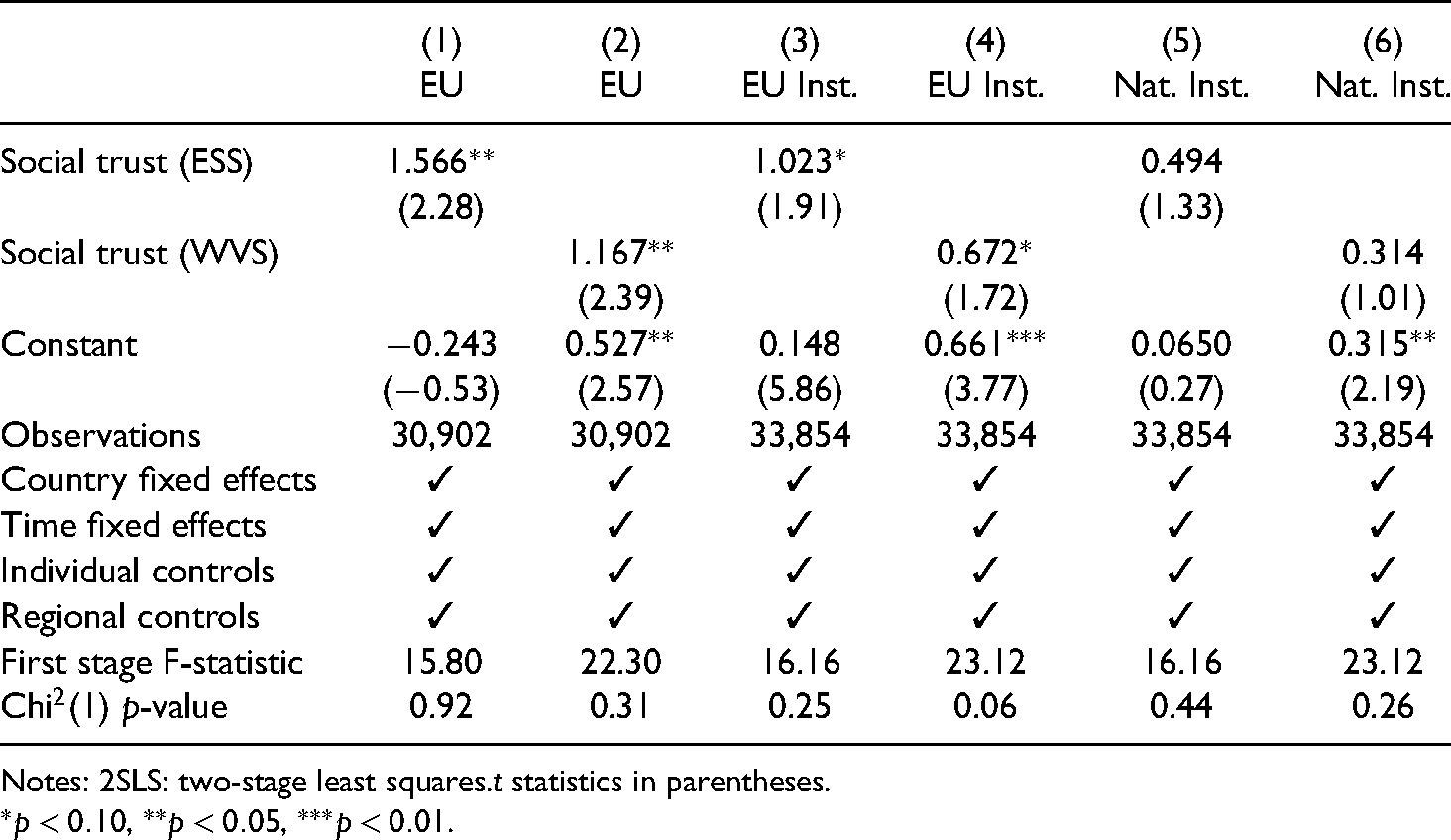

In Table 4, we extend the analysis to trust in other European institutions covered in the Eurobarometer survey. Even in this case, we use 2SLS regressions.

7

In column (1), we employ trust in the EU, which we take as a proxy for trust in the European project as a whole, and use the ESS measure of social trust. In column (2), we consider the same dependent variable, but we use the WVS social trust measure instead. In columns (3) and (4), we employ an index that summarises Eurobarometer respondents’ trust in the European Commission and the European Parliament. This offers a measure of individual attitudes towards other European institutions. The index is created by adding up the results of the responses, after attributing value 1 to each response in case the respondent indicates that she trusts the institution, value 0 if she doesn’t know, and value

Additional analyses: 2SLS regressions.

Notes: 2SLS: two-stage least squares.t statistics in parentheses.

In columns (5) and (6) of Table 4, we consider an index of trust in national institutions as a dependent variable, and the ESS and WVS as measures of social trust, respectively. Here, the trust index is given by the sum of respondents’ answers to the trust question for the national parliament and government. This allows us to assess whether the causal effect of social trust on institutional trust is specific to the ECB (and potentially other EU institutions), or whether this extends to a much broader set of economic and political institutions. In each pair of columns in Table 4, we employ the ESS and WVS measure of trust, respectively.

In columns (1) to (4), social trust is estimated to be statistically significant at the 5% level for trust in the EU, and at the 10% level for trust in the European institutions excluding the ECB. 8 Based on the results, it seems that the effect of social trust on institutional trust is not limited to the ECB, but it also extends to the European project as a whole and other European institutions.

Instead, in columns (5) and (6), social trust is not estimated to be statistically significant at conventional levels for trust in domestic institutions. The lack of statistical significance of the social trust variable in this case suggests that the link between culture and institutional trust is stronger for European institutions than for national ones. This may be due to several reasons. For instance, citizens may face greater difficulty in evaluating policy outcomes at the European vis-à-vis the national level, thereby relying more on their cultural priors. Relatedly, higher salience attributed to national issues in the media might make citizens more subject to a wider array of cues in the formation of their attitudes towards national institutions. This may downplay the importance of cultural factors. We leave these questions and hypotheses for future research.

Conclusion

This article has argued that in Europe institutional trust is affected by non-economic determinants at the level of sub-national regions. Considering the case of public trust in the ECB, the study makes use of a novel dataset of citizen perceptions and knowledge of the ECB and measures regional culture with indicators of social trust at the level of Euro area sub-national regions. Evidence shows that individuals living in regions with lower social trust systematically exhibit less trust in the ECB. An instrumental variable approach based on historical variables of regional literacy rates and political institutions before the 20th century supports a causal interpretation of our findings. These results are robust to different model specifications and measures of trust. The causal effect of regional culture extends to trust in the EU and other European institutions.

The findings of our examination suggest that, to a obtain an accurate picture of citizens’ views of the ECB, future analyses will have to consider cultural attitudes as an explanation for potential variations in institutional trust in the Euro area. Thus, our results have important implications. First, by highlighting the explanatory power of cultural variations in relation to trust in European institutions, our results resonate with a broader literature highlighting the renewed importance of cultural factors in shaping mass attitudes and preferences in the Western world over the past decade (e.g. Hooghe and Marks, 2009; Inglehart and Norris, 2016).

Second, our results are all the more important in the light of potential drops in social and institutional trust brought about by the COVID-19 crisis. While it is still too early to assess the long-term effects of the COVID-19 shock on citizens’ socio-political attitudes, there is already evidence pointing to a link between the experience of the COVID-19 crisis and lower levels of social and institutional trust (Brück et al., 2020; Daniele et al., 2020). These findings resonate with studies documenting that epidemic exposure has a persistent negative effect on individuals’ social trust (Aassve et al., 2020) and confidence in institutions (Aksoy et al., 2020).

Third, the ancillary evidence provided in the article on the relationship between knowledge and trust suggests that efforts to promote a greater understanding of the ECB’s functions should be targeted at individuals in the low end of the distribution of factual and self-assessed knowledge. Additional analyses show that younger, female, less educated and low income individuals residing in low social trust regions are more likely to have reduced levels of both factual and self-assessed knowledge of the ECB. 9 Thus, reaching out to these segments of population may be especially useful to promote knowledge of, and trust in, the ECB.

Future research may extend these findings to consider trust towards other European institutions, measured with surveys different from the Eurobarometer. Moreover, the evidence of this examination may be strengthened by considering different proxies of cultural traits at the regional level and how these affect household economic expectations and behaviour in a cross-country setting. Finally, a deeper and more rigorous scrutiny is needed with regard to the causal relevance of financial literacy and knowledge as driving factors of trust in the ECB and other European institutions.

Footnotes

Acknowledgements

Previous drafts of this article were presented at workshops organised at the European Central Bank and at the 2021 Online PEIO Seminar. We thank seminar participants and are especially grateful to Nicole Baerg, Stefanie Walter, Federica Genovese, Simon Hug, Bernhard Winkler, Klaus Masuch, Jean-François Jamet, Marius Gardt and Michael Ehrmann for helpful comments. The views expressed in the article are those of the authors. They do not necessarily reflect those of the European Central Bank and should not be reported as such.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.