Abstract

The COVID-19 pandemic worsened Italy’s fiscal outlook by increasing public debt. If interest rates were to rise, it would become more likely that Italy experiences a financial crisis and requires a European bailout. How does making EU funds conditional on austerity and structural reforms affect Italians’ support for the euro? Based on a novel survey experiment, this article shows that a majority of voters chooses to remain in the euro if a bailout does not involve conditionality, but the pro-euro majority turns into a relative majority for ‘Italexit’ if the bailout is contingent on austerity policies. Blaming different actors for the fiscal crisis has little effect on support. These results suggest that conditionality may turn Italian voters against the euro.

Introduction

The COVID-19 pandemic has led to a severe deterioration of the fiscal outlook of eurozone governments, particularly in Italy. Italian public debt increased to nearly 160% of gross domestic product (GDP) in 2020. Furthermore, for the past 25 years, Italy’s growth rate has usually been lower than the interest rate it pays on the stock of debt. If such circumstances were to persist, financial markets may perceive Italy’s public debt to be unsustainable. This makes a resurgence of tensions in sovereign bond markets and a revival of the euro crisis a distinct possibility.

According to the rules introduced in the first stage of the euro crisis, a country that is unable to finance its debt at acceptable interest rates should apply for an emergency loan from the European Stability Mechanism (ESM). To reduce moral hazard, countries that receive financial assistance have to sign a Memorandum of Understanding with the ESM (and possibly with the International Monetary Fund (IMF) and the European Central Bank (ECB) as well), pledging to introduce a series of austerity measures and structural reforms as a condition for assistance. An ESM program is a prerequisite for Outright Monetary Transactions (OMT) by the ECB, 1 i.e., potentially unlimited purchases of government bonds by the central bank.

One of the problems with this crisis resolution mechanism is that the austerity measures imposed on crisis countries are highly unpopular (Fernández-Albertos and Kuo, 2016, 2020; Franchino and Segatti, 2019; Jurado et al., 2020) and lead to electoral volatility, public protests, and the emergence of anti-system forces (Bojar et al., 2021; Bremer et al., 2020; Hübscher et al., 2020). Still, existing research shows that voters in most crisis-ridden countries strongly support the euro and are unwilling to leave it despite the costs associated with austerity (Clements et al., 2014; Hobolt and Wratil, 2015; Roth et al., 2016). In July 2015, Greek voters rejected the European Union (EU) bailout package in a popular referendum, but research shows they still wanted to remain in the common currency (Jurado et al., 2020; Walter et al., 2018; Xezonakis and Hartmann, 2020). This unwillingness to leave, despite the costs of austerity, strengthened the hand of ‘creditor’ countries and allowed them to shift the burden of adjustment on ‘debtor’ countries during the euro crisis (Copelovitch et al., 2016; Frieden and Walter, 2017).

In this article, we ask how Italian voters would evaluate the trade-off between remaining in the euro and implementing austerity in case of a fiscal crisis. To what extent would they accept the costs of austerity for the promise of a bailout and continued membership in the common currency? Italy is the third-largest economy in the eurozone, which makes it systemically important. Many commentators, therefore, believe that the euro stands or falls with Italy, and the possibility of exit is far from purely academic. In the wake of the euro crisis, Eurosceptic parties emerged that questioned Italy’s membership in the eurozone. The Five Star Movement (M5S) included the promise of a referendum on the permanence in the euro in its electoral manifesto of 2014, 2 while the Lega proposed a negotiated exit from the eurozone in its 2018 and 2019 manifestos. 3 Moreover, support for the euro before and after the COVID-19 outbreak was significantly lower in Italy than in other crisis-ridden countries (as we show below). Still, we know little about how Italians weigh the costs and benefits of staying in the euro in case of a financial crisis.

We use a novel framing experiment that exposes individuals to six different hypothetical scenarios to elicit preferences for the trade-off between austerity and euro membership. Some scenarios mention that the bailout package comes with the standard set of austerity policies included in previous European bailouts, while other scenarios do not. 4 Moreover, some scenarios suggest that the Italian government is responsible for the crisis due to its fiscal profligacy, while others hint that the EU, led by Germany and other northern European countries, has precipitated the crisis due to its fiscal inflexibility. The study is based on a large survey (n = 4200) fielded among a representative sample of Italian voters in October 2019, in the wake of a standoff between the Italian government and the European Commission over the country’s government deficit.

We find that in the control group, a majority of respondents favours remaining in the euro. However, informing participants about the conditionality associated with a bailout package changes the majority for remaining in the euro into a majority for ‘Italexit’. In contrast, foreign blame attribution and domestic blame attribution do not significantly influence preferences. Overall, our results suggest that opposition to further austerity trumps support for the euro in Italy. This implies that the European approach to crisis resolution, based on fiscal consolidation and structural reform in exchange for financial support, may lead to greater resistance in Italy than it did in other countries and even to a break-up of the eurozone.

Preferences for eurozone membership and exit during the euro crisis

The 2008 financial crisis and its aftermath fundamentally shook the political and economic system in Europe and led to an exceptional politicisation of the euro (Copelovitch et al., 2016; Matthijs and Blyth, 2015). The Maastricht Treaty did not foresee any mechanisms for financial assistance to member states and even included an explicit no-bailout clause (Article 125 of the Treaty on the Functioning of the European Union (TFEU)). However, when Greece lost access to financial markets in 2010 and several other member states followed suit, the EU decided to bail them out. The bailouts helped countries to service their debt and avoid bankruptcy, but they came with strict conditionality. The euro crisis was perceived as issuing primarily from government profligacy (Buti and Carnot, 2012), and the existing mechanisms of fiscal surveillance (the Stability and Growth Pact (SGP)) were further strengthened through the introduction of the Fiscal Compact. Countries receiving financial assistance were required to sign a Memorandum of Understanding, committing them to structural reforms and austerity policies (Frieden and Walter, 2017; Walter et al., 2020).

The bailout packages were controversial in both creditor and debtor countries. Voters in creditor countries were sceptical about financial transfers to other countries (e.g., Bechtel et al., 2014; Beramendi and Stegmueller, 2020; Kleider and Stoeckel, 2019; Stoeckel and Kuhn, 2018; Walter et al., 2020), whereas voters in debtor countries opposed the conditionality attached to the bailouts (Fernández-Albertos and Kuo, 2016, 2020; Franchino and Segatti, 2019). Overall, the eurozone crisis further politicised the EU and the euro (Hutter and Kriesi, 2019) and substantially increased dissatisfaction with the EU (De Vries, 2018; Guiso et al., 2016; Hobolt and De Vries, 2016).

Remarkably, however, support for euro membership remained high across the continent (Clements et al., 2014; Hobolt and Wratil, 2015; Roth et al., 2016). In some countries, the adverse effect on growth and unemployment was severe, and the incremental approach in resolving the crisis proved ‘catastrophic for the citizens of many crisis-plagued member states’ (Jones et al., 2016: 1010). Yet, existing research finds that even in the crisis-ridden south, voters still fundamentally supported the euro despite austerity and a prolonged recession. There was a broad consensus in debtor countries that a unilateral exit from the euro should be avoided at all costs, not just in Greece but also in other countries (Walter et al., 2020: 4). Even pro-euro individuals were not enthusiastic about austerity, but they ‘believe[d] it [was] preferable to alternatives and worth the costs, particularly regarding maintaining the benefits of the EU and euro’ (Fernández-Albertos and Kuo, 2020: 216). As citizens compared the status quo against possible alternatives (De Vries, 2018), the prospect of leaving the euro was even less attractive than austerity for voters in the south.

Events around the third Greek bailout in 2015 illustrate how popular support for the euro reduced the room for manoeuvre of national negotiators. In his reconstruction of the negotiation process, the Greek chief negotiator, finance minister Yannis Varoufakis argued that ‘unless [Syriza] fear[s] Grexit less than [it] fear[s] surrender, there [i]s no point in being elected’ (Varoufakis, 2017: 478). However, Jurado et al. (2020) show that while the far-left government led by Syriza was trying to renegotiate the terms of the agreement with the creditors (the ‘Troika’), support for the euro remained very high in Greece (around 75%) despite the negative consequences of austerity for the Greek population (Xezonakis and Hartmann, 2020). Survey evidence suggests that, in summer 2015, when a majority of voters rejected the third bail-out package in a popular referendum, more than three-quarters of respondents wanted to keep the euro, and only 13% preferred exit (Walter et al., 2018: 982). In the course of the negotiation, the Greek government never explicitly threatened exit but tried to convince the counterpart that exit may come about by accident (Pitsoulis and Schwuchow, 2017). Popular support for the euro thus deprived the Greek government of a credible exit option and reduced its bargaining power. This made it easier for the creditor countries to shift the burden of adjustment on debtor countries during the euro crisis (Copelovitch et al., 2016; Frieden and Walter, 2017).

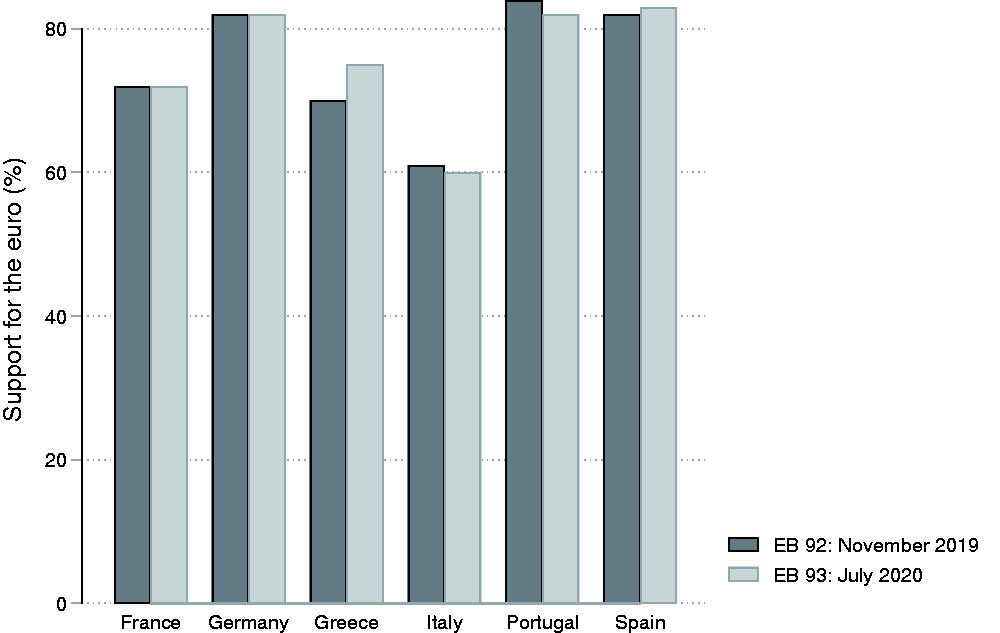

Overall, previous episodes of crisis suggest that voters have conflicting preferences: on the one hand, they strongly support the euro; on the other hand, they strongly oppose austerity (Clements et al., 2014; Fernández-Albertos and Kuo, 2016, 2020; Franchino and Segatti, 2019). Due to the parlous state of Italian public finances, voters in Italy may have to face exactly this dilemma at some point. Given that support for the euro is significantly lower in Italy than in other crisis-ridden countries according to data from the Eurobarometer shown in Figure 1, it is important to ask: how would they respond to the prospect of having to agree to a structural adjustment plan as a condition for financial support?

Support for the euro in selected European countries before and after the COVID-19 outbreak according to the Eurobarometer.

Framing effects on support for the euro

Preferences for euro remain or exit are unlikely to be fixed. A large literature has shown that framing effects substantially affect individual-level preferences (Amsalem and Zoizner, 2020; Chong and Druckman, 2007a, 2007b; Lupia, 1994; Slothuus and de Vreese, 2010) as individuals update their preferences based on new information (Zaller, 1992). This literature has highlighted both the effect of equivalence frames, which ‘present the same information in either a positive or negative light’, and emphasis frames, which ‘vary how the information is presented and its content’ (Amsalem and Zoizner, 2020: 4; also see Cacciatore et al., 2016; Chong and Druckman, 2007b). Emphasis frames usually have a stronger effect than equivalence frames because they provide information the receivers may not possess or focus their attention on aspects they may not be attentive to when considering an issue. 5 These effects also have been found in more realistic settings involving natural experiments (King et al., 2017; Slothuus, 2010), and they can persist over time beyond the immediate experimental setting (Lecheler et al., 2015).

We expect framing effects to influence support for euro membership and exit in Italy. Research on international disintegration shows that elites have a central role in shaping public discourse and mobilizing opposition to international integration (De Vries et al., 2021; Walter, 2021). Although the eurozone crisis strongly politicised the currency union, it remains a complex arrangement. Cognitively, it is difficult for individuals to fully evaluate the costs and benefits of a policy change. Bechtel et al. (2017) thus find that only some individuals are fundamentally opposed to bailouts in creditor countries. Most citizens rather have contingent attitudes, i.e., their attitudes ‘depend on the specific features of the policy and could shift if those features are altered’ (Bechtel et al., 2017: 864). More generally, European voters are likely to use benchmarking to compare possible reform scenarios to the status quo (De Vries, 2018). For example, Bansak et al. (2020: 510) show that preferences towards Grexit and the European bailouts are shaped by ‘different views about the likely effect of Grexit on the larger European economy’. These expectations about alternative states of the world change based on new information, and therefore, preferences for euro membership and exit should be susceptible to framing. Specifically, we focus on two different mechanisms: information about the costs associated with continued membership and blame attribution.

First, support for euro exit may decline when respondents are alerted to the conditionality associated with euro bailout packages. During the recent economic crises, financial assistance to debtor countries was conditional on highly contentious policies being implemented in receiving countries, including spending cuts, tax increases, and structural reforms, such as industrial relations liberalisation and pension cuts (Frieden and Walter, 2017: 372). Although elites and media were successfully able to sell austerity to voters in some countries like the United Kingdom (Barnes and Hicks, 2018) or Denmark (Bisgaard and Slothuus, 2018), most evidence suggests that voters in the crisis-ridden southern European countries oppose austerity policies (Fernández-Albertos and Kuo, 2016, 2020; Franchino and Segatti, 2019; Hübscher et al., 2020). The experience of the crisis and austerity did not only contribute to a large amount of electoral volatility and protests (Alonso and Ruiz-Rufino, 2020; Bremer et al., 2020), but it also weakened support for the euro (Hobolt and Wratil, 2015) and influenced the result of the 2015 Greek referendum on the bailout package (Jurado et al., 2020; Xezonakis and Hartmann, 2020). Given that utilitarian considerations remain strong predictors of public support for European integration (Foster and Frieden, 2021), we expect that individuals presented with a scenario that requires Italy to implement austerity due to EU conditionality would increase their support for euro exit. It remains an open question whether the decline in support is large enough to tip the balance in favour of exit. H1: Public support for Italexit is higher when voters are informed that the government is required to implement EU-enforced austerity measures as a condition for financial assistance. H2: Public support for Italexit is higher when voters receive information that attributes responsibility for the fiscal crisis to foreign actors. H3: Public support for Italexit is lower when voters receive information that attributes responsibility for the fiscal crisis to the national government.

Data and methods

Our study is based on an original survey fielded in Italy in October 2019, at a time when the Italian government was under pressure from the European Commission for not complying with the fiscal rules of the EU and shortly after the anti-establishment government coalition between the Lega and M5S had broken up over the wisdom of challenging the European Commission on the European fiscal rules. 6 The survey was conducted among a large sample of Italian adult citizens (n = 4200) by SWG, a leading polling company in Italy. Respondents were sampled from a pool of more than 60,000 individuals, who were recruited online and by telephone to ensure a balanced composition of the population. Sample quotas were used to ensure a representative sample based on age, gender, and economic sector. We used survey weights to further correct for deviations in our sample from the true population on other dimensions (region, age, gender, education, and past vote choice) as explained in the Online appendix. However, results do not depend on whether or not we use weights, and on the type of weights.

Experiment design and dependent variable

In the survey, we used a pre-registered 3x2 factorial experiment to study attitudes towards Italexit. We asked all respondents to imagine the following scenario:

Italy faces a crisis of confidence in financial markets. The European Central Bank is no longer willing to lend to Italian banks; capital flows out of the country; customers try to withdraw their deposits from banks; and the interest rate spread with Germany increases. As a result, the Italian government is unable to meet its financial obligations. Other European countries and European institutions offer a bailout package.

Before deciding whether or not to accept the bailout package, the government calls a referendum. The referendum asks citizens whether they want to stay in the euro and thus accept the bailout package, or whether they want to reject the bailout package and therefore exit the euro

At the time the survey was fielded, the Italian public debt was by no means considered a safe asset. In fact, it was rated BBB, just two notches above junk status (see Buiter, 2020: 142). This means that an unfavourable shock could deprive it of its investment-grade status, which is an assessment given by rating agencies and is frequently used by institutional investors to manage their portfolios. If Italian bonds were to lose investment status, institutional investors would have to sell them. Even the ECB would not be able to accept Italian sovereign bonds as collateral if their rating went below the minimum requirement of BBB- (Orphanides, 2017), at least according to the ECB’s collateral policy before the COVID-19 outbreak. In brief, an unfavourable development, such as the Italian public deficit increasing above European targets, could unleash a crisis of confidence and cause the Italian government to lose access to international financial markets. This would either lead to a request for a European bailout or Italexit.

After the basic scenario, we asked respondents how they would vote in a hypothetical referendum about euro membership. This was a heuristic device aimed at eliciting preferences about a real decision-making situation as opposed to simply expressing an opinion (Landa and Meirowitz, 2009: 494). In reality, it seems unlikely (but not impossible) that a decision about Italexit would be preceded by a popular referendum. Nonetheless, the possibility of such a referendum has been repeatedly discussed by key political actors in Italy before and after the Greek referendum of 2015 and is highly salient in the Italian public sphere. 7

Our basic scenario diverts from the Greek course of events in 2015 in one crucial way. In Greece, the consequence of a no vote was ambiguous because it was not clear whether it implied renegotiation of the bailout package or euro exit (Walter et al., 2018). We eliminated the ambiguity and created a stark choice between accepting the bailout package and remaining in the euro or rejecting it and exiting the euro. We use vote choice in this hypothetical referendum as our dependent variable. The dependent variable has four categories: ‘accept the bailout plan and remain in the euro’, ‘reject the bailout plan and exit the euro’, ‘would not vote’, and ‘don’t know’. To simplify the analysis, we merge respondents from the last two answers categories in the analyses below.

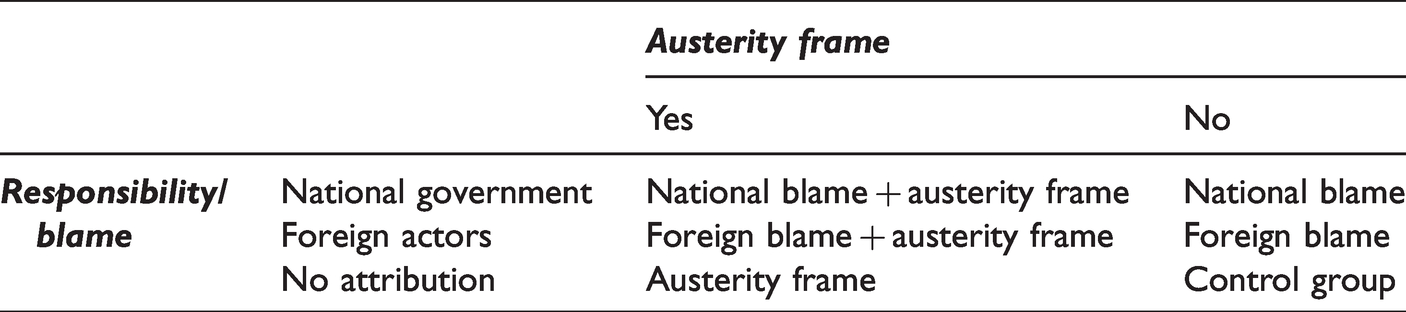

We randomly combined the basic scenario with variation in blame attribution for triggering the crisis (national government/foreign countries/no attribution) and variation in the conditionality associated with the bailout (austerity frame/absence thereof). This resulted in six different scenarios, as summarised in Table 1. Some experimental groups received the information that the offer of a bailout package was contingent on the implementation of policy changes. This austerity scenario was written trying to replicate the experience of other countries in the past. It mentions several different policies that were requested from countries that were bailed out during the euro crisis (Jacoby and Hopkin, 2020) and incorporates the recent rules about depositors’ participation (bail-in) in case of bank resolution (Quaglia, 2019).

Combination of frames in the 3 × 2 experimental design.

Moreover, for some experimental groups, the basic scenario was preceded by one of two blame attribution frames. These emphasis frames had the same basic informational content – Italy’s public deficit increases and this induces the rating agencies to downgrade Italian public bonds – but tried to stimulate two plausible interpretations of the informational content, i.e., why the financial crisis came about and who was primarily responsible for it. In the foreign blame frame, the EU is the culprit since it ‘launches an excessive deficit procedure against Italy’, while the government tries to ‘rekindle growth and reduce unemployment’. In the national blame frame, the Italian government is the culprit because ‘it has decided to ignore the European fiscal rules and has allowed the public deficit to exceed the figure agreed with the European Commission’, even though Italian public debt is ‘already very high to begin with’.

We decided not to introduce a frame about the costs of exit in our study for the following reasons. First, adding another frame would have necessitated a 3×2×2 factorial design and a much larger sample than we had available. Second, while it is possible to specify with some degree of assurance the kind of conditionality that would be included in a bailout package for Italy based on previous bailouts, a scenario emphasizing the costs of exit is more difficult to specify because there is no precedent for it. The costs of exiting the euro would depend on several assumptions: orderly vs. disorderly exit; how other countries would respond; the type of exchange rate regime that would be chosen (a flexible exchange rate or entry into the European Exchange Rate Mechanism); whether there is a return to the lira or the creation of a smaller southern eurozone, etc. Third, the literature on Brexit suggests that the perceived costs of exit and international disintegration may be less important than the perceived costs of remaining (Carreras, 2019; Grynberg et al., 2020). Therefore, we decided to focus on the cost of austerity and blame attribution in this article.

Note that, in an effort to be as realistic as possible, our frames combine various elements. Thus, while we can identify any overall treatment effect of the frames thanks to randomisation (which ensures exogeneity by design), we are unable to specify the role that specific elements of our frames play. For example, for the austerity frame, we are not able to determine to what extent any shift in preferences is due to easier rules for layoffs, expenditure cuts, privatisation, etc. This is acceptable, in our view, because these elements have historically been bundled together in bailout packages.

The specific wording of the frames is included in the Online appendix. All frames were written as pure issue frames and provided no information about endorsements by parties or other political actors.

Independent variables

To estimate the experimental treatment effect, the key independent variables of interest are the six different scenarios that result from our factorial design. We present results both without controls and with the following controls: gender, age, age squared (to capture non-linear effects of age), educational attainment, household income, respondents’ assessment of the export dependence of their firm or organisation, employment contract (indeterminate duration, fixed-term, part-time, or agency work or having no work contract), economic knowledge (based on responses to three economic knowledge questions) and region (North versus South). In an additional model, we add past vote choice as a separate variable to assess how variation in preferences towards the euro might be correlated with party choice. The detailed coding and summary statistics of all variables are presented in the Online appendix.

Empirical strategy

Our analysis proceeds in three steps. First, we analyse the experimental treatment effects of austerity and variation in blame attribution. Since our dependent variable can take three values (‘remain’, ‘exit’, and ‘don’t know’) and since we are interested in how the frames change support for each option, we estimate multinominal probit regression models. The results do not change if we use dichotomous transformations of the dependent variable and estimate linear probability models or logit or probit models instead, as shown in the Online appendix. Due to random assignment to treatment, we present results without control variables, but they are unchanged if we include control variables (reported in the Online appendix). We calculate and plot the average marginal effects of the frames and the associated predicted probabilities of vote choice in the hypothetical Italexit referendum. Second, to examine how preferences towards the euro vary by individual socio-economic background and political orientations, we add other independent variables to the model specifications. Third, as a synthesis of the two preceding steps, we examine whether the experimental treatment effects vary by respondents’ characteristics.

Results

Results from the survey experiment

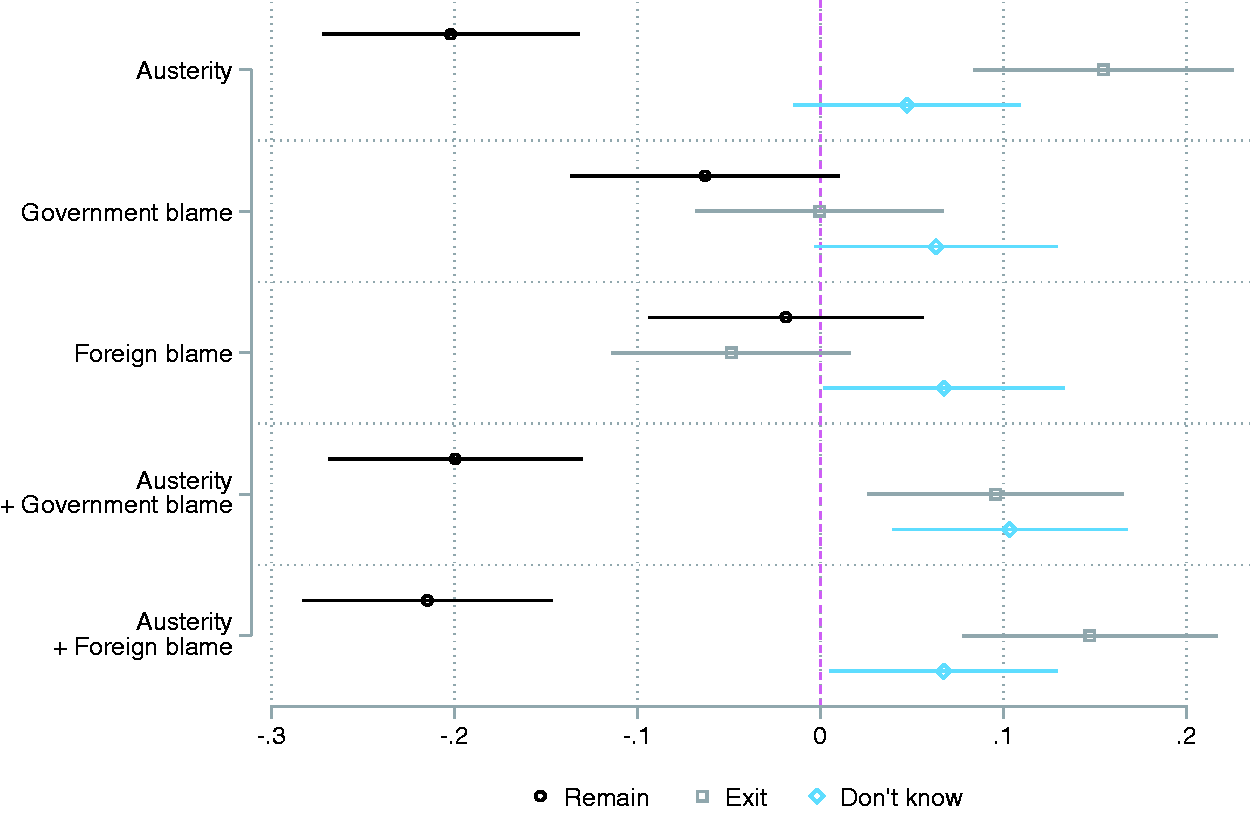

How strong is support for the euro when respondents are faced with the Greek-style scenario of a financial crisis? And how susceptible are individuals to information about austerity requirements and about who is to blame for the crisis? Figure 2 reports the average treatment effects of the austerity frame, the domestic blame and the foreign blame frames, and their combinations. The results show that the austerity frame has the strongest effect: it reduces support for remain by about 20% and increases support for exit by about 15%, which is in line with hypothesis 1.

Average treatment effects of austerity and blame attribution on vote choice in hypothetical Italexit referendum.

However, our expectations are not confirmed for the domestic and the foreign blame frames, for which the effects are insignificant. Interestingly, the percentage of respondents who are uncertain increases by a significant margin when the EU and other governments are blamed for the fiscal crisis. It similarly increases when the domestic government is blamed, but this effect is not statistically significant. These insignificant findings are in line with evidence from Greece, where blame attribution is found not to have significantly influenced electoral vote choice during the euro crisis either (Karyotis and Rüdig, 2015; Kosmidis, 2018). It is possible, however, that the frames for blame attribution were not formulated strongly enough to have an effect on preferences. 8

The dominant effect of austerity also stands out in the combined treatment conditions. When the domestic and foreign blame frames are presented together with the austerity frame (the two lower treatment conditions in Figure 2), the effects are similar to the treatment effect of austerity alone (Table 1). This is confirmed by a formal test, which shows that the interaction effects between the austerity (Table 1) and the blame attribution treatments are insignificant (see the Online appendix). Interestingly, support for exit is about five percentage points lower under the combination of austerity and the government blame frame than under the combination of austerity and the foreign blame frame. This is in line with hypotheses 2 and 3, but the difference between these two treatment conditions is statistically insignificant.

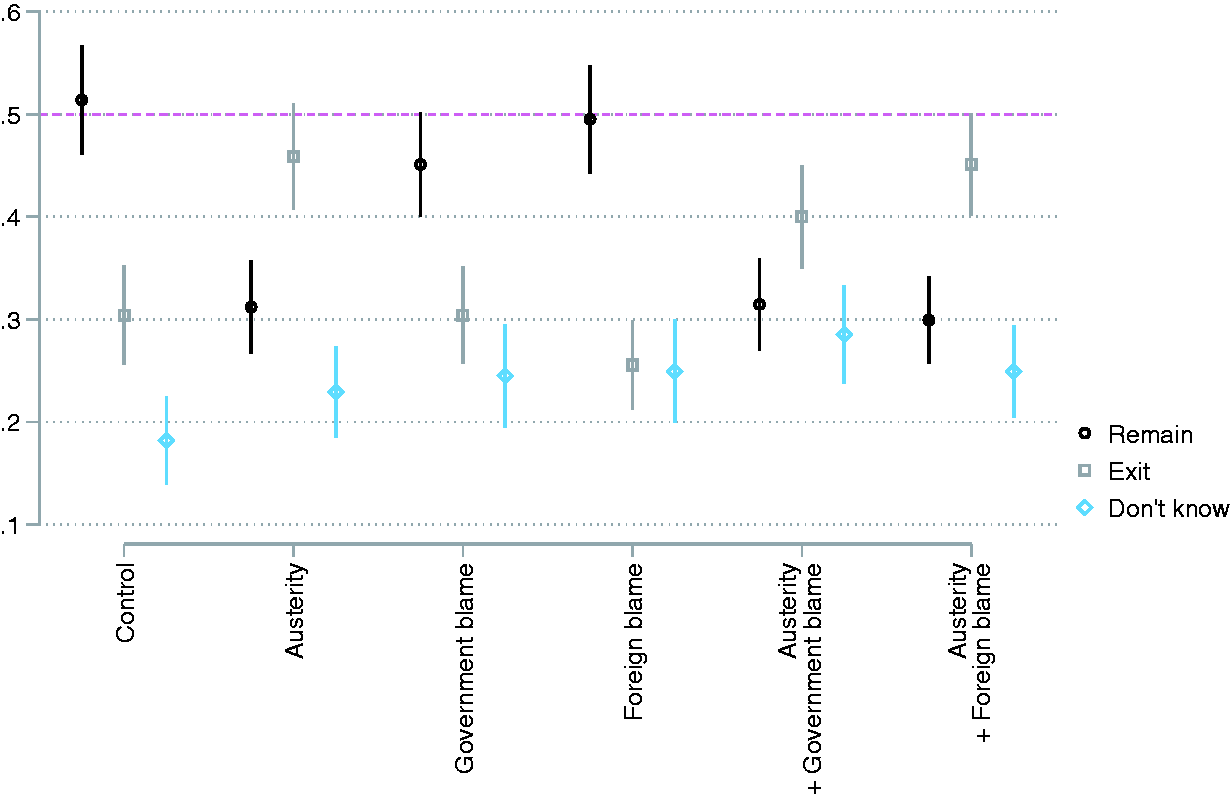

Do the frames shift democratic majorities? Figure 3 shows the predicted probabilities of voting in the referendum by treatment group. In the control group, where respondents did not receive any treatment, 51.4% of respondents would vote to accept the bailout package and remain in the euro. In contrast, 30.4% of respondents would vote to reject the bailout package and exit the euro. This confirms existing findings that, in principle, the euro is still relatively popular in southern Europe despite the euro crisis. Yet, the share of undecided respondents is also large (18.2%), which indicates that politicians have substantial room for manoeuvre. The distribution of preferences is similar in the two blame attribution treatments which do not include information about conditionality. Yet, the situation changes drastically when respondents receive the austerity frame: a relative majority of 45.9% of respondents now prefer exit, 31.2% still support remain, while 22.9% are uncertain. Variation in blame attribution does not alter this relative majority for Italexit under austerity.

Predicted voting probabilities in hypothetical Italexit referendum by treatment.

Overall, these findings suggest that support for euro membership and exit is contingent upon the costs of continued membership in Italy. Apparently, Italians are strongly opposed to austerity, and this opposition trumps support for the euro.

Individual-level determinants of the vote in the referendum

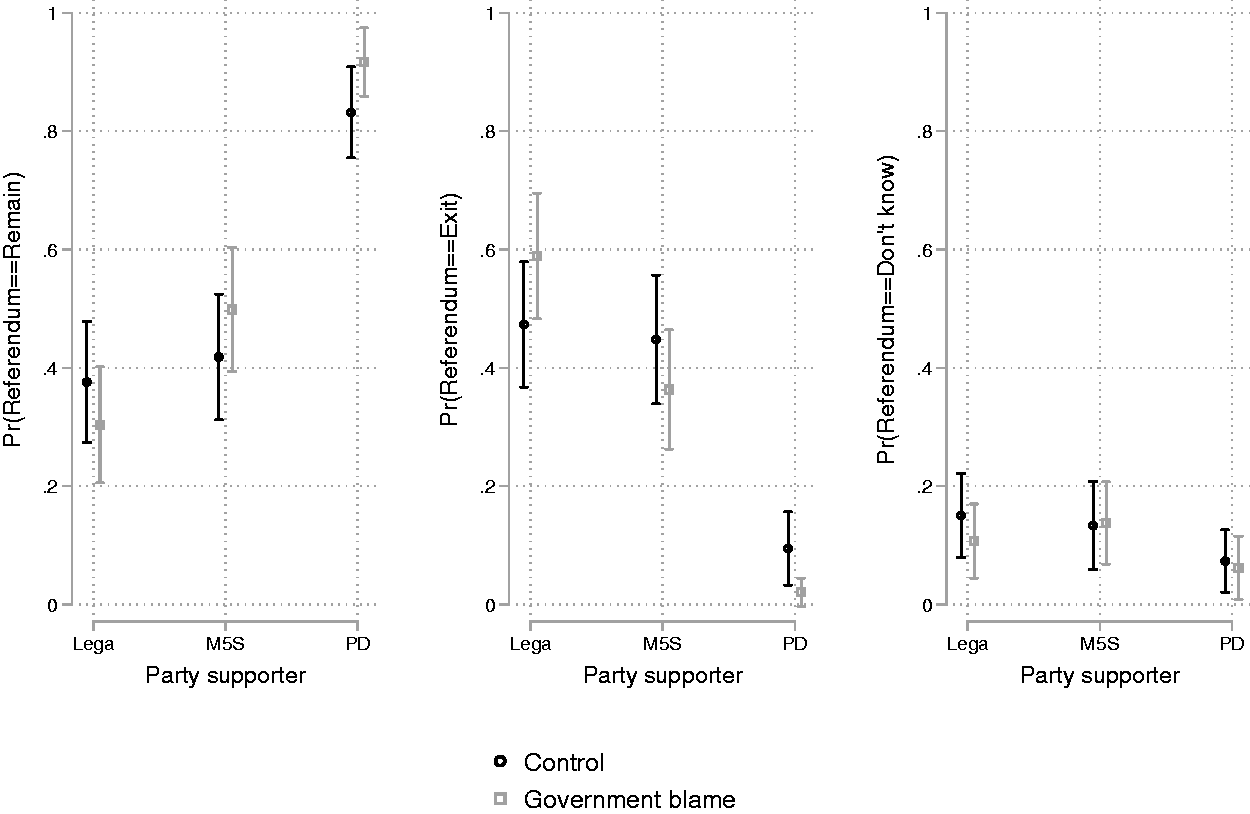

How does support for Italexit vary by socio-economic background and political orientations? In Table 2, we examine how the vote in the hypothetical referendum relates to individual characteristics, controlling for our frames. Higher educational attainment and a higher position in the income distribution are associated with stronger opposition to Italexit. Moving from an individual with a university degree to an individual with lower secondary education increases support for Italexit by 13 percentage points. Similarly, moving from the highest to the lowest income decile increases the likelihood of supporting Italexit by 13 percentage points. These results suggest that support for the euro increases with the respondents’ socioeconomic position.

Determinants of vote choice in a hypothetical Italexit referendum; average marginal effects based on multinomial probit regressions.

Note: t-statistics in parentheses, *p < 0.05, **p < 0.01, ***p < 0.001.

Survey weights applied. M5S: Five Star Movement; PD: Partito Democratico.

We do not find significant effects for other individual-level predictors except age. Gender, export exposure, employment contract, and region are not associated with euro preferences, but there is a curvilinear effect of age. Middle-aged individuals (between 40 and 60) are more supportive of exit than remain, whereas younger and older age cohorts are more supportive of remain (see the Online appendix for an illustration). We can only speculate about the reason for this pattern. Younger individuals have no memory of the pre-euro phase; hence, they may be more likely to want to remain in the euro. In contrast, older, retired individuals are less directly exposed to the difficult labour market situation in Italy than individuals below 60, and they are more likely to fear the loss of purchasing power that may be brought about by exit from the euro due to devaluation.

Finally, in Model 1, higher economic knowledge is associated with stronger support for remain, but this effect disappears when we control for partisan preferences in Model 2. 9 According to this model, preferences are strongly associated with respondents’ partisan preferences. Voters of the Lega (the reference category) are the strongest supporters of Italexit (although the difference with Fratelli d’Italia is statistically insignificant), while voters of the Partito Democratico (PD) are least likely to support Italexit. The marginal effect of shifting from the Lega to the PD, keeping all other individual characteristics (including frames) constant, decreases the probability of voting for Italexit in the referendum by 47%. The marginal effects of the M5S and Forza Italia reduce the probability of voting for Italexit by 9 and 12% relative to Lega, while the marginal effects of no party (which accounts for 37% of the sample) and other party are 33 and 21%, respectively.

Heterogeneous framing effects

In this section, we check whether some of the individual variables associated with attitudes towards the euro moderate the treatment effects of our experimental frames (austerity, government blame, and foreign blame). For most interactions with individual-level predictors, heterogeneous treatment effects are absent. For example, we did not find heterogeneous effects for the role of trade exposure, neither at the individual (perceived export dependence) nor at the regional level. Still, effects for three variables are worth highlighting, namely knowledge (education and economic knowledge), material interest (income) and political (partisan) preferences.

First, for some frames, effects are larger for individuals with low economic knowledge and low education, as shown in the Online appendix. However, the differences are small and do not alter our assessment of the degree of empirical support and non-support for our hypotheses. In particular, even high-knowledge individuals still react strongly to the austerity frame. Overall, this suggests that knowledge plays a limited role for preferences (see also Armingeon, 2021).

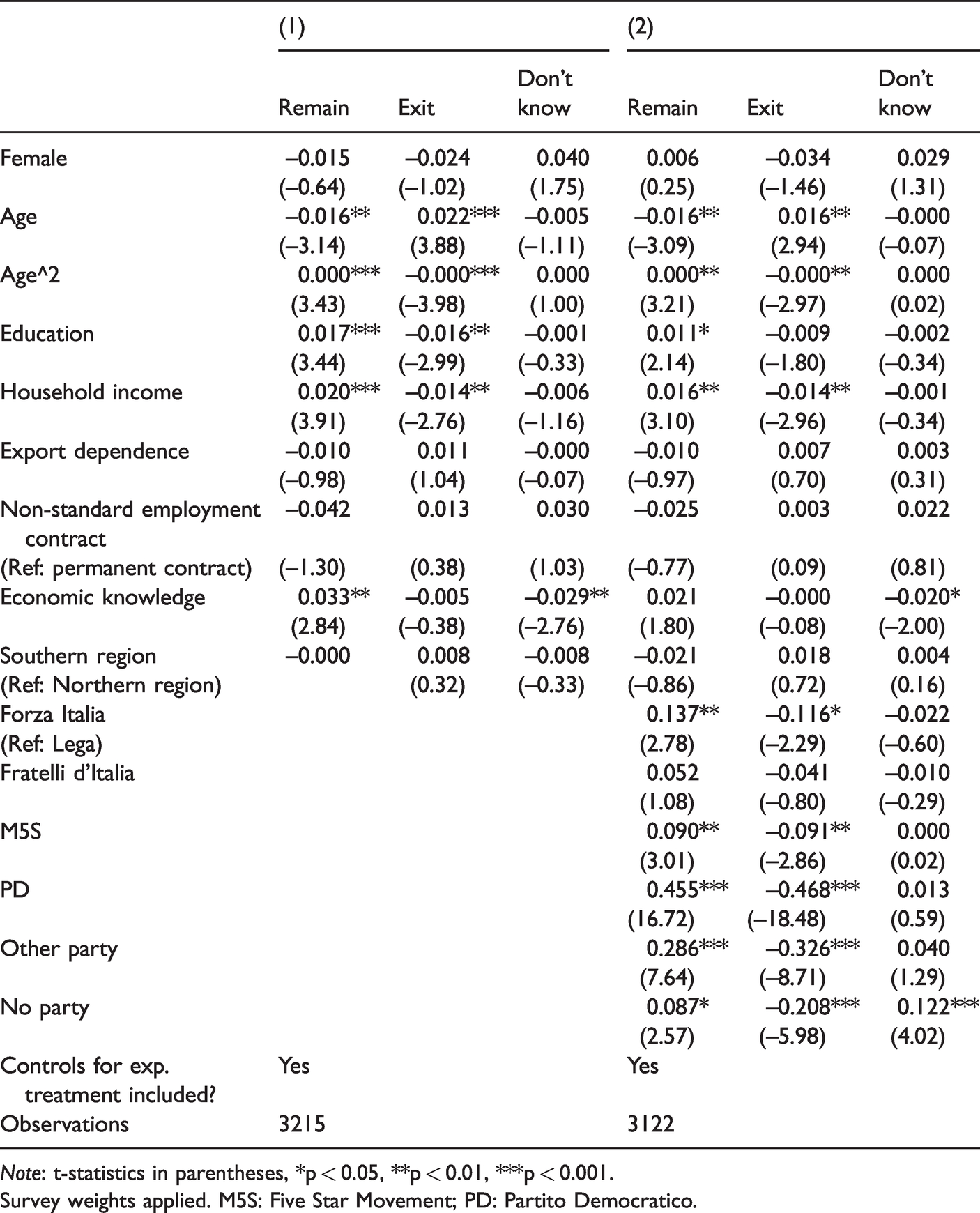

Second, Figure 4 shows that the effect of the austerity frame on the propensity to vote for exit is muted for individuals at the upper end of the income distribution, and it is much stronger for individuals at the lower end. In particular, the effect of austerity on the likelihood to vote for remain is insignificant for the two highest income deciles, and it is insignificant for the three highest income deciles for the likelihood to vote for exit. This finding suggests that information about austerity resonates more strongly with less well-off individuals, who are more likely to think that they will be negatively affected by the scenario, than richer individuals, who probably consider themselves immune from the negative consequences of austerity.

Heterogeneous austerity treatment effects for household income.

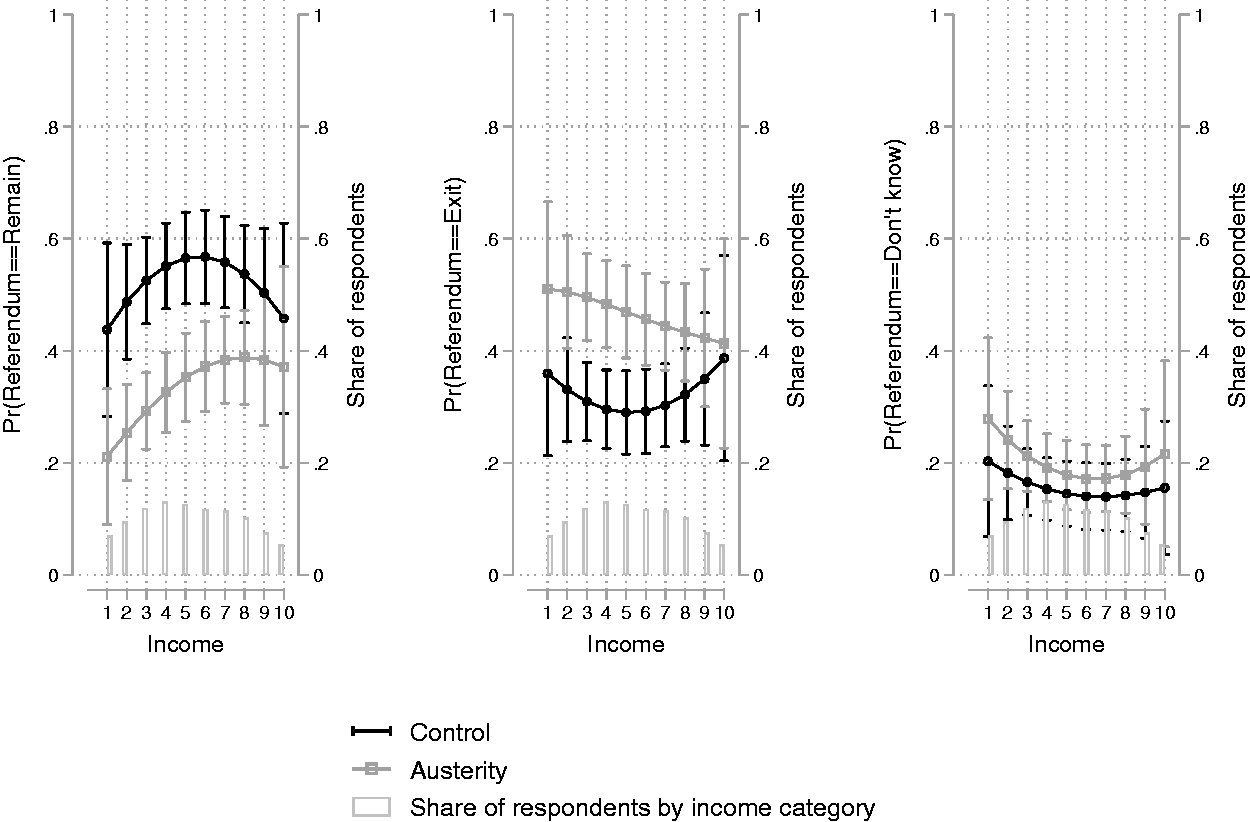

Although partisan choice is a strong predictor of the referendum vote (Table 2), it only modifies the effect of the treatments in one instance: PD and M5S supporters react differently to the blame attribution treatments than Lega supporters (Figure 5). While the government blame frame tends to increase support for exit among the Lega supporters, it decreases support among voters of the PD and M5S, who were in government when we fielded the survey. For the PD, this effect is non-negligible (seven percentage points) and statistically significant. Thus, PD voters are not only the most supportive of Italy’s membership in the euro (Table 2, Model 2), but they are also likely to further reduce their support for Italexit when the Italian government is blamed for the crisis.

Heterogeneous domestic government blame treatment effects for partisan preferences.

Conclusion

The literature on the euro crisis has found that voters in southern European countries are cross-pressured: on the one hand, they are opposed to austerity; on the other hand, they are attached to the euro. So far, the attachment has trumped the opposition: despite the high costs of structural adjustment policies, no democratic majority has supported exit in any eurozone country. This situation strengthened the bargaining position of northern governments: as southern governments were constrained by domestic preferences for remaining in the euro, they had to accept the terms of the northern European countries.

Using a survey experiment, we presented a large representative sample of Italian voters with the trade-off between accepting the conditionality of a European bailout plan or exiting the euro. Our results suggest that Italian public opinion is strongly sensitive to the costs of remaining in the euro (Franchino and Segatti, 2019). If voters are informed that eurozone membership comes at the cost of austerity, support for exit increases by 15% and support for remain decreases by almost 20%. Importantly, the pro-euro majority that we find in the control group turns into a relative majority for Italexit if Italy’s continued membership comes at the expense of austerity. In contrast, we do not find any significant effect of blame attribution. Apparently, Italian voters do not care much about whose fault the crisis is but they strongly oppose further austerity. This opposition is strong enough for them to consider leaving the common currency.

The large effect of the austerity treatment indicates that eurozone membership can easily become contested in Italy. Support for the euro is lower in Italy than in other countries, but public opinion is also malleable by elite framing. Moreover, there is a large share of undecided voters who are likely to follow elite cues about the euro. Preferences towards the euro in Italy are, therefore, contingent and likely to shift depending on how the issue is framed. Individuals who are better-off and who support the PD are less likely to react to the threat of austerity, but their number is not large enough to ensure Italy’s continued membership in the eurozone. Therefore, European policymakers may hit the limits of their preferred crisis resolution strategy if there was a fiscal crisis in Italy: conditional financial support, provided by the ESM or other European institutions, may antagonise voters and push them out of the common currency.

Our findings have to be interpreted with caution, however. First, we did not present respondents with a frame that highlights the cost of exiting the euro, which narrows our findings. Although it is uncertain how such an exit would unfold and it is likely that its economic consequences would differ dramatically depending on whether exit is negotiated with the European partners or not, it is possible that preferences for remain would increase significantly if the costs of exit were to be emphasised and they could counterbalance the decline due to the emphasis on the costs of remain (austerity). At the same time, if the case of Brexit is any guide, it is also possible that citizens discount the costs of exit in formulating their preferences (Carreras, 2019; Grynberg et al., 2020). Therefore, we plan to analyse how citizens evaluate the cost of remain vs. exit in the future, given that considerations about alternative states are crucial to explain support for European integration (De Vries, 2018).

Second, preferences for the euro are likely to change over time depending on the economic situation of a country. We ran our survey before the COVID-19 pandemic hit Italy. Although preferences towards the euro did not change according to the Eurobarometer (Figure 1), other surveys indicate that in spring 2020, when Italians felt they had been left alone by the other European countries in responding to the first wave of the pandemic, sentiments towards the EU became less favourable in Italy. 10 Our research indicates that attitudes towards the euro are likely to deteriorate in these circumstances, but future research should verify that this is the case.

Third, in this article, we studied the case of a southern European country. However, the possibility that a systemically important member state could exit the euro will have knock-on effects and may shift preferences in northern EU member states as well. Future research should also investigate whether the threat of disintegration increases popular support for institutional reform and a more equitable sharing of the burden of adjustment in ‘creditor’ countries such as Germany or the Netherlands.

Supplemental Material

sj-zip-1-eup-10.1177_14651165211004772 - Supplemental material for Till austerity do us part? A survey experiment on support for the euro in Italy

Supplemental material, sj-zip-1-eup-10.1177_14651165211004772 for Till austerity do us part? A survey experiment on support for the euro in Italy by Lucio Baccaro, Björn Bremer and Erik Neimanns in European Union Politics

Supplemental Material

sj-pdf-2-eup-10.1177_14651165211004772 - Supplemental material for Till austerity do us part? A survey experiment on support for the euro in Italy

Supplemental material, sj-pdf-2-eup-10.1177_14651165211004772 for Till austerity do us part? A survey experiment on support for the euro in Italy by Lucio Baccaro, Björn Bremer and Erik Neimanns in European Union Politics

Footnotes

Acknowledgements

We are grateful to Fabio Bulfone, Donato Di Carlo, Sinisa Hadziabdic, Martin Höpner, Kostas Gemenis, Mischa Strathenwerth, and three anonymous reviewers for extremely helpful comments. A previous version of this article was published as a MPIfG Discussion Paper. Cassandra Fuchs provided excellent research assistance.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.