Abstract

‘Super apps’ are on the rise. This study explores the characteristics, origins, and manifestations of these apps worldwide, presenting the concept of ‘super-appification’ to describe processes of conglomeration in the global digital economy. Super apps aim to become deeply integrated into people’s everyday lives, capturing and monetising essential activities. By analysing 41 super apps, we identify four distinct types of ‘super-app constellations’, showcasing different patterns and dynamics of conglomeration: ‘Swiss-Army Knife’ apps that consolidate services in one app, ‘Family’ apps that expand through subsidiaries, and ‘Host’ and ‘Hub’-style apps that leverage external developers. This typology offers a comprehensive understanding of the conglomeration patterns underpinning the rise of super apps, involving corporate, development and international expansion strategies. Ultimately, super-appification represents an intensified form of ‘appification’, as these apps increasingly pervade and commodify various aspects of everyday life, such as payment, insurance, grocery delivery, mobility and travel, with significant sociopolitical implications.

Keywords

Introduction: the rise of ‘super apps’

Got an app for everything? Now, get everything in one app. (Avo)

‘Super apps’ are on the rise (Schumpeter, 2022). Such apps are characterised by a wide range of seemingly unrelated services built onto a core functionality, creating an immersive and unified experience for everyday activities that resembles both an operating system and brand. For Chan (2022), a super app is like ‘a single app that allows you to shop for groceries, pay your rent, review work documents, refill prescriptions, book a trip, and chat with friends, interest groups, and businesses’. Here, the term ‘super’ does not necessarily mean superb or indispensable, but rather refers to an app that goes beyond a single-purpose activity to combine many different services across typically isolated industry sectors.

Although the term was first introduced by BlackBerry founder Mike Lazaridis back in 2010 to describe an ecosystem of everyday apps that provide an integrated experience, companies have over the past few years increasingly referred to themselves as ‘super apps’ in their app descriptions and materials. There is a significant amount of industry hype associated with the term: some tech sector consultants and analysts predict that over half of the global population will use super apps daily soon (Perri, 2022), while others argue that it is an ‘inevitable’ trend that will produce a US$10 trillion tech company (Galloway, 2021). This publicity around super apps has mainly focused on Chinese and Southeast Asian apps such as WeChat, which is often referred to as the ‘poster child for super apps’ (Chan, 2022); however, it can also be seen as part of a wider global trend of consolidating services into fewer dominant platforms. Companies in the Western context, including WhatsApp, PayPal and Spotify, are rushing to rebrand themselves as super apps (O’Brien, 2022), with Elon Musk even stating that he acquired Twitter to create ‘X’, ‘the everything app’. 1 As a promotional discourse, the term ‘super’ has thus taken on a significant rhetorical function in reflecting an app’s suggested, imagined and aspirational uses. According to Pitre (2022: iv), many apps aspire to become super as a marketing strategy to attract investment, regardless of whether their product resembles one or not: ‘calling oneself a super app is now a strategy for marketing and a way to signal corporate ambition’.

Empirically speaking, the super app initially does not seem like a well-defined or distinct category. It has become a label used for a variety of reasons; different companies that are attached to the term have different strategies, functionalities, user groups and operating contexts. While it may have originally served primarily as a rhetorical device, it has since evolved into an aspirational target, reflecting many practical realities associated with expansive digital media industries. The rise of super apps is, accordingly, a complex phenomenon that requires detailed exploration, one that recognises, but also goes beyond its use for promotional means. As Goggin (2021) has pointed out, ‘the super app concept does not really pass muster analytically [. . .] [but] it offers insights into the economic and industrial trajectories of apps’ (p. 74). Indeed, we take the term as an invitation to reconsider the political economy of data, platforms, apps and services in the mobile ecosystem, yet in doing so, we also take up the challenge of its apparent insufficiency as a basis for effective analytic or conceptual frameworks. In our view, super apps, through bundling services and expanding their offerings, break with the idea of apps as small, bounded entities and create new opportunities for relational and comparative critical app studies.

Interdisciplinary platform studies – an area our work is closely engaged with – has at times similarly grappled with the politics of terminology, including definitional slippages and conceptual ambiguities, despite efforts to strictly ground the term as digital intermediation processes in economic and business literature (Cristofari, 2023). Like super apps, such ambiguity has arisen both through the entanglement of the platform concept with promotional discourses – at once driving and reflecting on changes in industry – and as new disciplinary perspectives have been brought to bear on its theorisation. One response in this domain has been the development of emergent typologies that take stock of its variation, new insights, and the ongoing refinement of its conceptualisation. This can be seen, for instance, in contributions such as Gillespie’s (2010) etymological platform framework, Srnicek’s (2016) typology of platform capitalism, and Steinberg’s (2019) historical typology of the platform economy. Our research here takes on a similar approach with regard to taking stock of super apps by building upon existing research on super apps (Athique, 2019; Chen et al., 2018; Mukherjee, 2018; Plantin and de Seta, 2019; Steinberg et al., 2022), while introducing a unique typology that delineates the geographical contours and characteristic features of the super app. This serves as a foundational understanding of the super-app phenomenon, paving the way for further critical analyses and theoretical contributions. A central commitment of this study that we outline below is precisely to embrace its diversity, as Steinberg et al. (2022) have also suggested, rather than trying to limit the concept of a super app in advance.

This article explores the characteristics, origins and diverse manifestations of the global phenomenon of super apps by providing a comprehensive and comparative analysis, asking, what are super apps, who develops them, when did they emerge, and where are they prevalent? Rather than attempting to pin down a specific app type, we introduce the concept of ‘super-app constellations’, illustrating how mobile apps have transformed into platforms and platforms have adopted app-like characteristics in a larger trend, we refer to as ‘super-appification’. While previous studies have primarily focused on individual popular examples like WeChat in China, East Asia, and Southeast Asia, our empirical analysis of 41 super apps from around the world reveals four distinct types of super-app constellations, reflecting different patterns and dynamics of conglomeration, which we call the ‘Swiss-Army Knife’, ‘Family’, ‘Host’, and ‘Hub’. As such, we are the first to provide a global perspective on super apps, not only in terms of geographic scope but also our comprehensive overview of the whole phenomenon. Our typological framework holds value not only for empirical analysis of super apps, but also as a foundational basis for improving conceptual clarity, adding analytical rigour to their study, conducting comparative studies, as well as for guiding policymakers in understanding and addressing the negative consequences of super-appification and its different forms of consolidation.

Our findings demonstrate that apps become ‘super’ by integrating various essential everyday services across industries and borders within super-app constellations. The concept and typology of super-app constellations provide a broader understanding of the distinct patterns and dynamics of conglomeration that drive super-appification in the global digital economy, involving various corporate, development and international expansion strategies. Thus, as we propose, super-appification aligns with the dynamics of ‘platformisation’, conceptualised as the process driving the infrastructural and economic expansion of platforms into new areas on the Web (e.g. Helmond, 2015); however, it exhibits unique characteristics, whereby services spanning diverse industries are amalgamated into a single constellation, a process we refer to as conglomeration. Behind these dynamics lie a drive for super-app companies to become more deeply integrated into people’s daily lives, capturing and monetising a wide range of essential everyday activities.

The article is structured into four main sections. First, we situate the super app as a global phenomenon and an emerging object of study in the literature. Second, we detail the methods used to source a representative list of super apps from across the world and explain the analytical approach used to identify their characteristics, origins and diverse manifestations. Third, the analysis explores the global landscape of super apps, encompassing the typology of super-app constellations and the wide range of consumer services offered. It also discusses the corporate, development and international expansion strategies of super apps. Finally, we reflect on the findings of this study, focusing on conglomeration in the global digital economy.

Super-appification as a convergence of app and platform logic

Existing super app research has drawn insights from various fields and disciplines, particularly app and platform studies. There is a shared recognition that the super app represents a convergence of app and platform logic, resulting in an amalgamation of diverse services, the emergence of unique business models and a transformative impact on everyday activities. In line with our argument, we distil three pivotal features of super apps as highlighted in the scholarly literature and by industry observers.

To begin with, super apps are understood as applications that incorporate multiple services in one place. They are described as ‘all-in-one apps’ (Chen et al., 2018), ‘Swiss-army-style apps’ (Steinberg, 2020) or ‘do-everything apps’ that represent ‘a particular model of an app that assumes most functions of the smartphone can be done within either a single app or a suite of apps’ (Steinberg et al., 2022: 1409). Steinberg et al. (2022) further emphasise that their ability to integrate various functionalities, from music to ride-hailing to money, is what makes them ‘super’ (p. 1409). Industry literature defines super apps as apps that incorporate seemingly unrelated services that users want or need in one place (Chan, 2022). However, Goggin (2021: 74) cautions against adopting a novelty discourse, arguing that they do not represent the ‘next level up for apps’ but instead highlight the ‘dominance of some digital platform companies’.

In addition, super apps are understood as a specific type of corporation or business strategy. Goggin (2021) describes them as ‘an integrative technical, user, and business approach to leverage existing customer bases and to expand into other product and service opportunities’ (p. 77). This involves mergers and acquisitions, partnerships, and other strategic alliances that play a crucial role in their development. Super apps are viewed as the outcome of specific corporate strategies, including conglomeration and financialisation (Jia et al., 2022), as ‘digital platforms that leverage a business’ core assets across multiple use cases or service verticals’ (Ajene, 2021), and are considered both ‘a product and a form of organising value’ (Chai, 2021). They have a unique business strategy that involves aggressive horizontal and locally oriented expansion, compared to the vertical and globally oriented strategy of US or Silicon Valley-based companies (Atkins, 2019; Goggin, 2021: 75; Jia and Kenney, 2022). Super apps are seen as ‘digital born, mobile first multi-sided platforms’, which involve a shift from Western advertising-based platform business models towards models that combine ‘four primary categories of transaction, subscription, escrow, and advertising fees’ (Chai, 2021). Of particular significance are new affordances for digital payments, or how many super apps infuse ‘cloud-money’ with social media as a structure of everyday life (Scott, 2022). They can additionally be understood as an effort to counter US ‘platform imperialism’ (Jin, 2015) in smartphone devices, software operating systems and app stores. The companies behind these super apps are described as the new ‘megacorps’ (Steinberg et al., 2022) that have become key players in the digital economy, where media power is being asserted, consolidated and contested.

Finally, super apps are conceptualised as ‘mega-platforms’ to highlight new forms of enclosure by powerful ‘megacorps’ like Tencent. According to Chen et al. (2018), super apps function as mega-platforms to expand and grow, with their ability to ‘glue together an increasing array of activities’ (p. 5). They evolve into super apps by becoming a platform for other applications to develop within (Steinberg, 2020), as demonstrated by Tencent’s WeChat (Chen et al., 2018; Plantin and de Seta, 2019) or LINE (Steinberg, 2020). This leads to a form of enclosure in which super apps commodify various types of mobile and networking services into their platforms (Goggin, 2021: 76). Consequently, super apps have been described as ‘choke points within the platform economy’ (Steinberg et al., 2022: 1414) that create ecosystems monopolising a user’s time (Atkins, 2019) by serving as portals for distributing their own content and apps (Jia et al., 2022). The creation of a stripped-down version of an app that runs within an all-in-one platform allows users to bypass the app store altogether and adds to this enclosure effect. With the centrality of ‘the transaction layer’ to many super apps, moreover, this can result in a unique reshaping of markets by ‘ensur[ing] that every peer-to-peer exchange generates a commission that can be captured’ (Athique, 2019: 77).

At present, existing studies of super apps have largely focused on single apps or app companies located in China and Southeast Asia, such as WeChat (Chen et al., 2018), Tencent (Jia et al., 2022), LINE (Steinberg, 2020), and Gojek and Grab (Qadri and D’Ignazio, 2022). A Platform Lab report notably covers nine apps focused on the Asian context, yet they are examined as individual case studies (Pitre, 2022). By contrast, in our contribution, we present a relational and comparative approach to the global super-app landscape through the notion of ‘super-app constellations’. This concept describes the transformation of mobile apps into platforms and the adoption of app-like features by platforms as part of the larger trend of super-appification. It additionally contributes to the existing literature by integrating the various understandings of the super-app phenomenon, while shedding light on the distinct patterns and dynamics of conglomeration within distinct geographical contexts.

Exploring the global landscape of super apps

To examine the global landscape and evolution of super apps, we compiled a dataset comprising 41 apps. These were sourced from the previously mentioned studies and various web sources, including technology blogs and news articles that feature existing lists of super apps. The apps included were those that either self-identified as super apps or those that exhibited notable characteristics of conglomeration. Aspirational super apps, which mainly promise an amalgamation of services rather than actually delivering them, were excluded from the dataset.

Additional information about each app was collected from Google Play, including app details, developer names and locations, and app store categories. 2 As a result, this study is based on data from Google Play and does not cover iOS apps, with some implications for the subsequent results; for instance, China is absent from our geographic analysis because Google Play is unavailable there. Additional data about the apps were obtained from market intelligence firms data.ai and Sensor Tower. These companies offer valuable information about apps that would otherwise remain inaccessible. However, it is worth noting that certain aspects of the data can be unclear at times. From Sensor Tower, we obtained data on the primary countries or regions served by the apps (‘Top Countries/Regions’). These data are derived from a combination of app store metrics (such as download counts) and usage statistics (consumer spending; Sensor Tower, 2022). Furthermore, Sensor Tower also furnished data about the countries where the apps are labelled as ‘inactive’, meaning they are not accessible through Google Play. Using data.ai, we collected further information on the apps’ release dates, version histories and parent company names. In addition, we collected the service categories (referred to as ‘genres’ and ‘subgenres’) of all apps, as provided by data.ai’s ‘App IQ’ and ‘Game IQ’ classifications. 3 This extensive taxonomy provides a detailed overview of the global app economy’s key industries and sub-industries, which is useful when studying how super apps operate across multiple industries. Finally, we visited the apps’ websites to identify whether they offer an application programming interface (API) or other development tools.

The dataset was then appended with additional apps from the developers of the initial 41 super apps. Ownership information about the companies and developers behind the apps, including their ultimate ‘parent’ holding companies, headquarters, and other members of the same corporate ‘families’, was gathered from data.ai. In total, 12,719 apps across all super-app families were identified, with 8442 apps having been previously removed from the app stores since their initial launch.

The analysis of this dataset focused on four guiding subquestions regarding the process of super-appification and the diverse manifestations of super apps worldwide. It drew upon a previous study on the global COVID-19 app landscape, employing a similar multifaceted approach to map and characterise a thematic set of apps (Dieter et al., 2021). The first question, focused on what super apps are, explored the nature of super apps, including their discursive positioning, organisational models and range of consumer services. We employed data.ai’s industry taxonomy to identify both the primary and secondary consumer services offered by each app. The study builds on previous efforts to categorise super apps (Chai, 2021: 4) by substantially expanding the sample size to encompass 41 apps spanning 22 countries, providing a more comprehensive categorisation and understanding of the global super-app landscape. Based on this, a typology of super-app constellations is presented, offering insights into consolidation patterns and dynamics. The second question, focused on who, delved into the current ownership and industry origins of super apps, examining the companies, partnerships and involvement of third-party developers based on data from data.ai and the super-app companies’ websites. The third question (when) explored the evolution and discontinuation of specific super-app families, also using data from data.ai, emphasising patterns of conglomeration and the role of mergers, acquisitions and investments. Finally, the geographic dimension of super apps was explored (where), including their emergence in different countries and regions, variations at the local level, and the influence of local infrastructures, market conditions and regulatory frameworks. The study also examined the operation of super apps across multiple regions in the global super-app economy.

The types of super apps found around the world

The analysis is structured into two parts. The first part focuses on the nature of super apps, delving into their descriptions and the diverse range of consumer services they offer. The second part explores the corporate and international expansion strategies of super apps, specifically focusing on their corporate ‘families’ of (subsidiary) apps and companies. By exploring both dimensions, the study provides a unique relational perspective on the distinctive characteristics, origins and manifestations of super apps, revealing their operation across various industries, across corporate ‘families’ and their expansion across borders and regions.

Super-app taglines and descriptions

First, through qualitative thematic analysis of the taglines and descriptions for all 41 super apps, we gain valuable insights into their discursive positioning. This reveals how these apps self-identify and offers a deeper understanding of their capabilities, intended uses, company strategies, and target audiences.

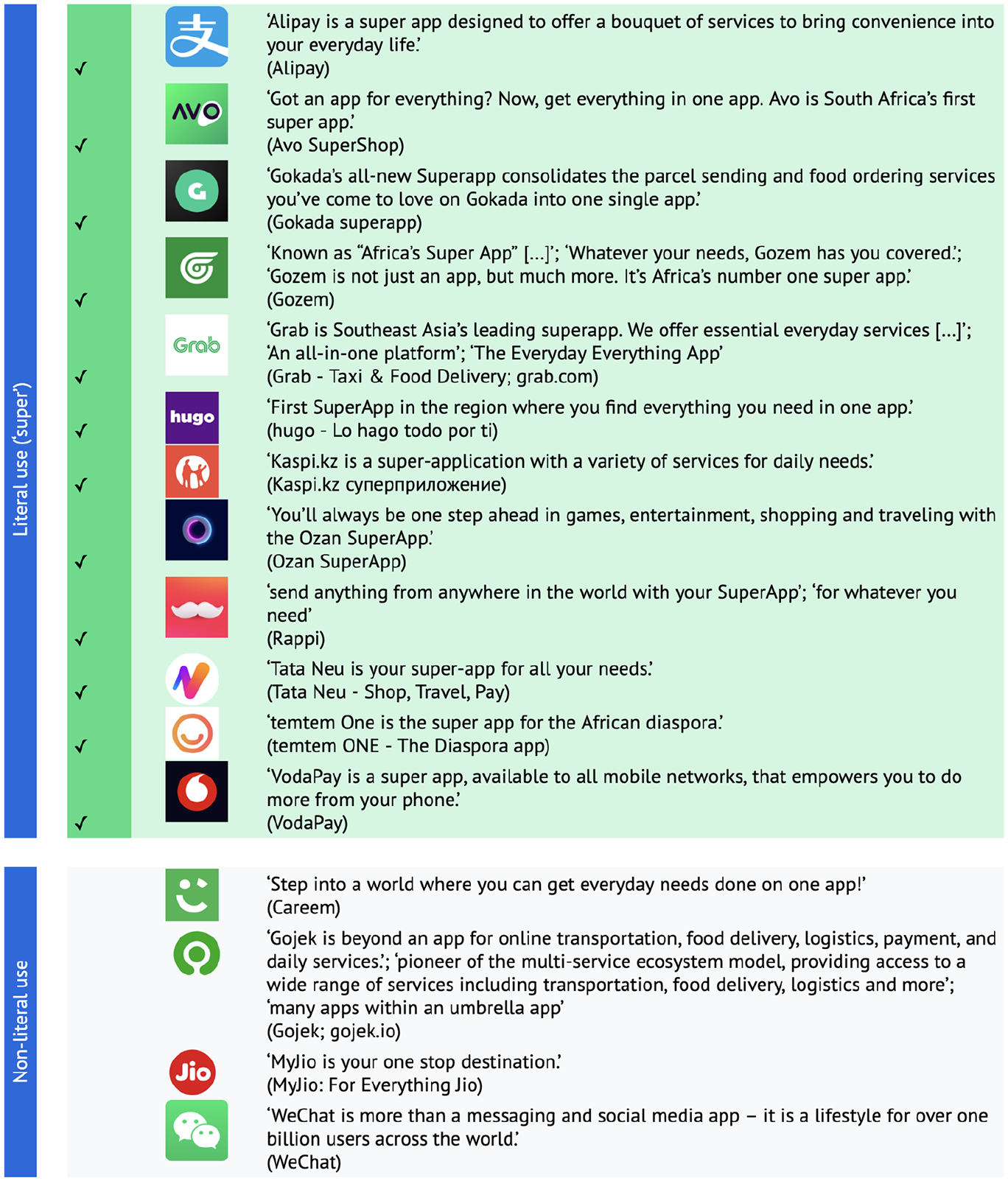

Although super apps have been on the rise for several years, only 12 (29%) of them explicitly self-identified as such in their taglines and descriptions with four additional apps using related terms (Figure 1). While Alipay, Avo SuperShop, Gozem, hugo, Kaspi.kz, Rappi, Tata Neu, temtem ONE, and VodaPay used the term only in their descriptions, Gokada superapp, Grab, and Ozan SuperApp used it in their titles. Some use the term to assert their dominance in the region, as evidenced by Grab’s claim to be ‘Southeast Asia’s leading superapp’, Gozem’s self-proclaimed status as ‘Africa’s number one super app’, and hugo’s claim to be the ‘First SuperApp in the region’. Others openly express their infrastructural ambitions to build ‘the digital ecosystem of tomorrow in West and Central Africa’ (Gozem), or to develop ‘products that nations run on’ (Gojek). Most, however, do not explicitly self-identify as ‘super apps’. Instead, many claim to provide essential everyday services (Careem; Grab; Kaspi.kz) and convenience by consolidating diverse services and needs within a single app (Alipay; Gozem; Tata Neu). In addition, they showcase their roles as a ‘one-stop destination’ (MyJio) or ‘umbrella app’ (Gojek) to capture user activities in a single place, reminiscent of the ‘portal’ model that was born with the Web, serving as an entry point to content or services.

Selected super-app taglines and descriptions.

Notably, some exemplary super apps, such as WeChat, do not use the term at all. Instead, WeChat positions itself as ‘more than a messaging and social media app – it is a lifestyle for over one billion users across the world’. This reinforces the observation that ‘super app’ is not only an actor’s term but also a label applied by external observers. In certain instances, apps may refrain from using it altogether to mitigate suspicion and potential scrutiny from authorities regarding antitrust issues, data privacy concerns, fines and regulatory oversight.

Overall, the taglines and descriptions of super apps reveal various common themes related to everyday needs and activities, consolidation, indispensability, security and convenience. With this consolidation of ‘essential everyday services’ (Grab), super apps are instrumental to the ‘appification’ of everyday life. This is a phenomenon that various app studies researchers have explored in depth (Dieter et al., 2019; Goggin, 2021; Morris and Murray, 2018), especially how apps as ‘mundane software’ have introduced datafication into what were seemingly unreachable social contexts and practises. According to Steinberg et al. (2022), the super app is ‘one form in which these [corporate] monopolies are experienced as a vernacular, everyday infrastructure; a condition for life’ (p. 1411).

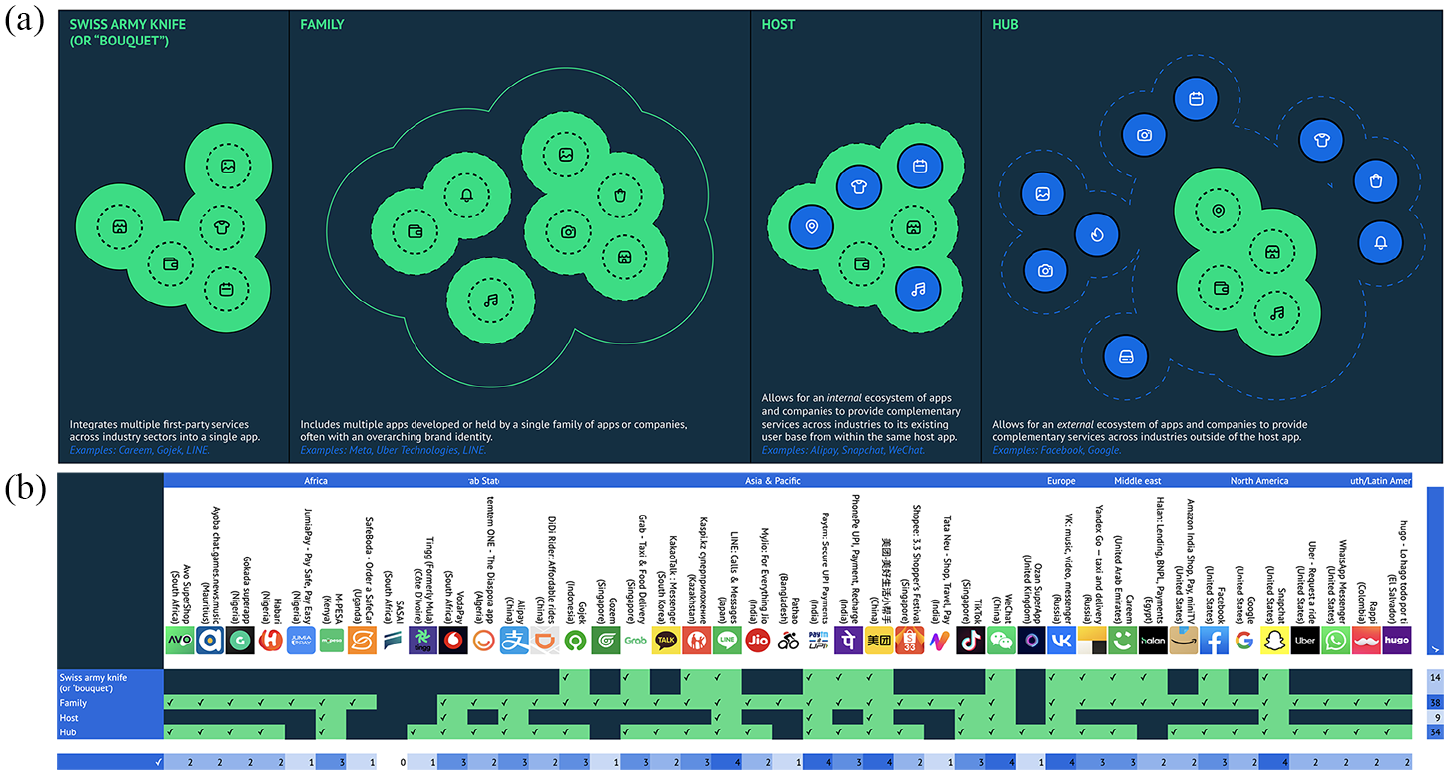

A typology of ‘super-app constellations’

Against this background of commonly identified themes, we proceed to explore the apps themselves and the range of ‘essential everyday services’ they provide. Within this context, our analysis reveals the existence of four distinct types of ‘super-app constellations’, each characterised by distinct patterns and dynamics of conglomeration, as depicted in Figure 2(a). In addition, these constellations are linked to specific corporate, development and international expansion strategies. By drawing inspiration from the notion of ‘platform constellations’ put forth in a case study of KakaoTalk and LINE (Staykova and Damsgaard, 2016), the identified super-app constellations serve as tangible examples of the various manifestations of the process of super-appification. These constellations underscore the integration of highly modular systems and services spanning multiple industry sectors and borders.

(a and b) Typology of ‘super-app constellations’.

First, the ‘Swiss-Army Knife’ (or ‘Bouquet’-style) super app integrates multiple services across industries into a single app. It provides a comprehensive range of functionalities and services within a unified platform and app interface. These services can include first-party (or in-house) services directly provided by the same company that owns the super app, such as ride-hailing, food delivery, e-commerce, financial services, entertainment, travel bookings, messaging, and social networking. In addition, they can encompass services provided through integrations with digital payment providers, collaborations with local businesses or partnerships with external service providers or governments. Fourteen (34%) of our apps met the criteria for this type, as shown in Figure 2(b).

Second, the ‘Family’-style super app represents a cohesive ecosystem of multiple apps developed or owned by the same app or holding company, seamlessly integrating services across various industries while maintaining a unified brand identity. Each app within this ‘family’ serves specific user needs and niches, often leveraging a shared technological infrastructure. Exploring apps within a family framework allows us to gain valuable insights into the corporate strategies employed by super apps, which may not be readily apparent when examining individual apps in isolation. Remarkably, nearly all apps in our dataset (38 apps, or 93%) fall into this ‘Family’-style category. This highlights how this approach is a core strategy for many super apps aiming to expand across sectors and industries. The significance of this corporate dimension will be the primary focus in the subsequent part of our analysis.

The third type we call the ‘Host’, where third-party ‘mini’ apps or complementary services are developed and distributed within the host app itself, such as QQ and WeChat’s ‘mini-programs’ and Snapchat’s ‘Minis’. This allows for the creation of an internal ecosystem where apps and companies provide complementary services to the existing user base from within the same app. According to Schreieck et al. (2023: 85), these ‘mini-app ecosystems’ are collections of ‘lightweight apps that can be used without prior download and installation’, relying heavily on the host app or platform. This type of app ecosystem is also known as an ‘in-app ecosystem’, wherein the apps are often created by individual developers, app companies or official partners based outside of the platform (van der Vlist et al., in press). Ten (24%) of the examined apps belong to this category and offer a mini-app development programme.

The fourth type we refer to as the ‘Hub’ (or ‘Hub-Spoke’), which is similar to the Host type but involves an external app ecosystem where a co-evolving collection of complementary services across industry sectors is created by various third parties outside of the app. In this type, the super app serves as a central hub that connects various third-party apps and services created by external contributors using APIs, software development kits (SDKs), and other developer tools provided by the hub platform. Within this category, 34 (83%) of the examined apps offer a development platform with one or more APIs or SDKs.

In contrast to the first two types, the third and fourth platform-style super-app types adopt an ecosystem strategy. Rather than consolidating multiple services within their own app or company, these types focus on attracting third-party developers to create and distribute complementary services on their platform (Gerlitz et al., 2019). Furthermore, platform-style super apps often employ ‘coring’ strategies, integrating externally developed apps and services into their core platform itself (van der Vlist, 2022: 166). Tencent, for example, is known for copying and incorporating third-party modules into their own apps like QQ (Chen et al., 2018). By incorporating external functionalities, these super apps aim to enhance the user experience and expand their service offerings.

Significantly, most apps we analyse belong to multiple types, which unveils unique and overlapping patterns of conglomeration that may not be readily apparent without a relational approach to app research.

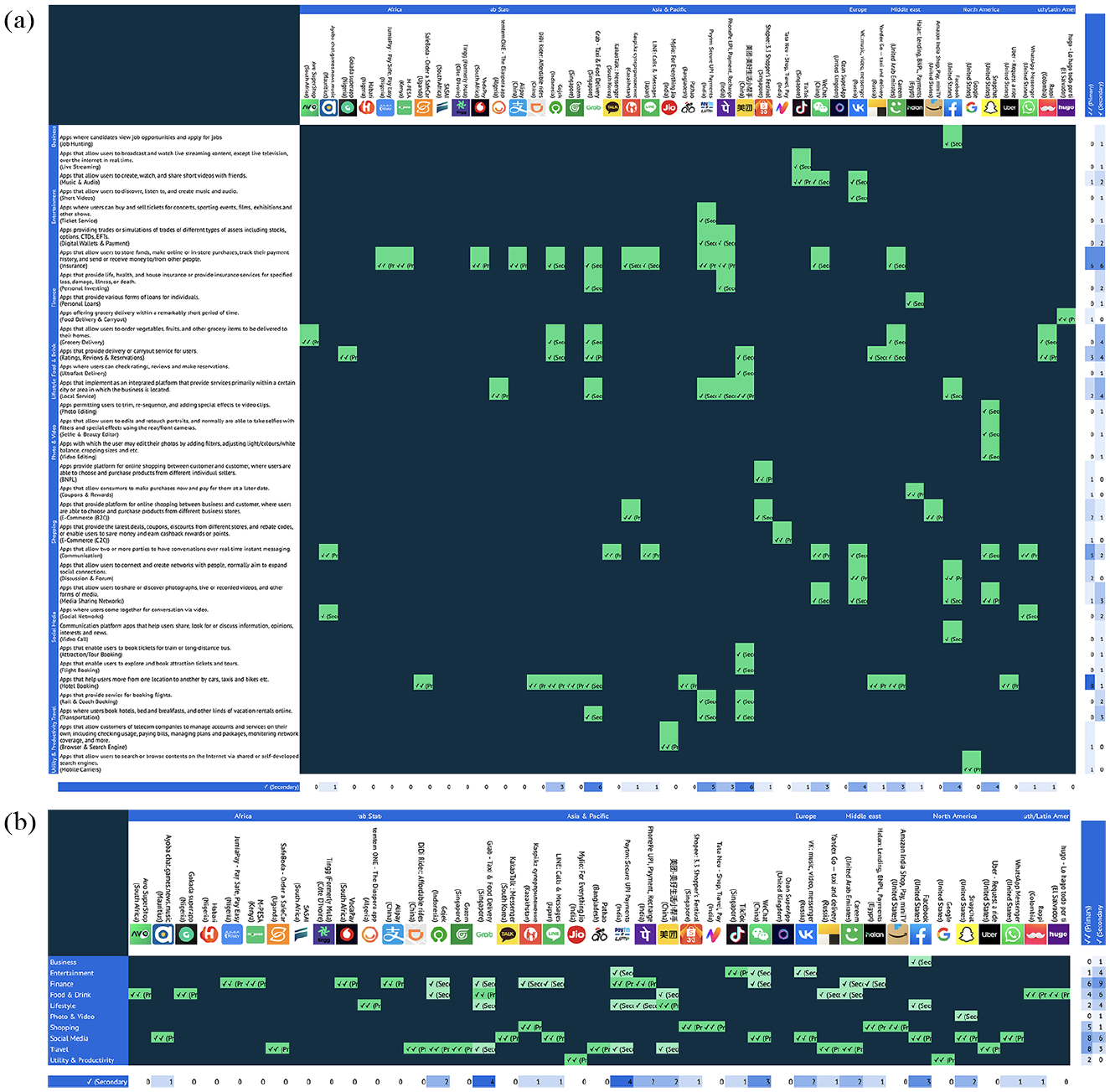

Range of consumer services offered

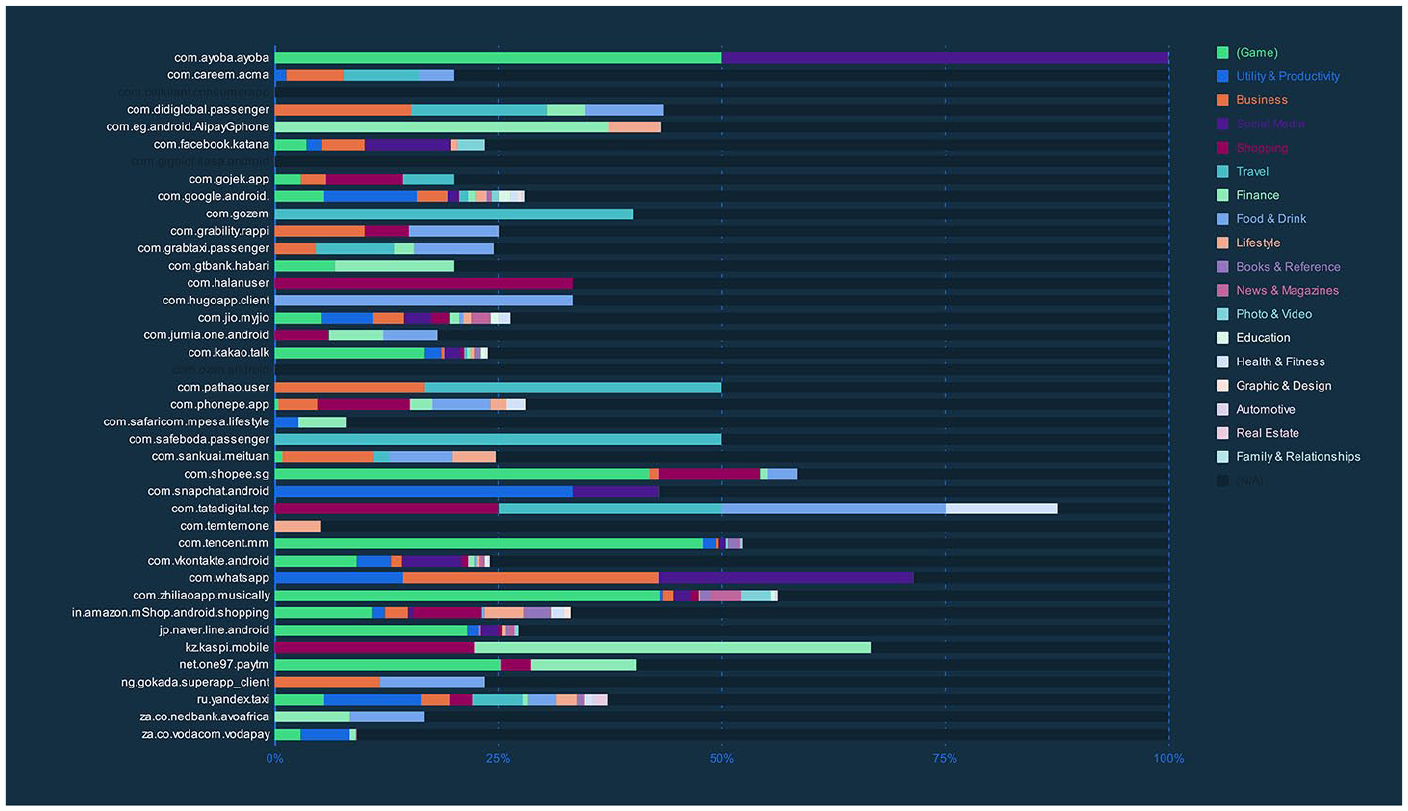

Our review of the consumer services provided by the super apps in our dataset reveals the range of everyday needs that these apps address as their primary and secondary services (Figure 3). Overall, the distribution of service categories among super apps reflects the effective ‘super-appification’ of everyday needs and activities into these apps across different regions of the world.

Consumer services offered primarily and secondarily by super apps, shown (a) by subgenre and (b) by genre. Data: data.ai.

Among the primary service categories, the most prevalent in our dataset of super apps were ‘Social Media’ and ‘Travel’ (8 apps), ‘Finance’ (6), and ‘Food & Drink’ and ‘Shopping’ (5). These primary genres reflect the core business of each super app. Based on these genres and subgenres, we also examined whether each super app offers services across multiple industries and sub-industries. This distinctive characteristic of super apps sets them apart from other app types and raises concerns regarding cross-side network effects and cross-industry consolidation.

Paytm (India) and Grab (Singapore) both offer services across as many as four distinct genres, while WeChat (China), Meituan (China), Gojek (Indonesia), Careem (UAE), and Facebook (the United States) each offer services across three distinct genres. Popular secondary genres are ‘Finance’ (9, particularly ‘Insurance’), ‘Food & Drink’ (6, particularly ‘Grocery Delivery’), ‘Social Media’ (6), ‘Local Service’ (4), ‘Entertainment’ (4), and ‘Travel’ (3).

Services that have very limited association with any of the super apps in our dataset include ‘Automotive’, ‘Books & Reference’, ‘Health & Fitness’, ‘News’, ‘Real Estate’, and ‘Sports’. These categories shed light on everyday needs and activities that have not yet been effectively super-appified.

Finally, it is worth noting that most of today’s super apps were not ‘born’ as super apps, as this analysis has shown. By tracing the evolution of specific cases (Helmond and van der Vlist, 2021), we can observe the process of super-appification and how apps gradually transitioned into ‘super’ apps over time. A noteworthy example of an app expanding its service offering is Gojek, which initially launched in 2015 with just four services but expanded to 12 service offerings across various industries under the same Gojek brand within a year. By 2023, Gojek included 23 locally oriented services such as ‘GoMart’ for local grocery delivery, ‘GoPay’ for mobile payments, and ‘GoMed’, linking users to healthcare providers in Indonesia. The evolution of Gojek from a ‘two-wheeled ride-hailing company’ in 2009 to a ‘app-based transport and lifestyle service provider’ in 2019, and ultimately, to a company creating ‘products that nations run on’ in 2023, provides an archetypal example of a super-appification trajectory. 4

The corporate ‘families’ of super apps

Our analyses of super-app constellations demonstrate how distinct strategies are deployed to amalgamate various services from across industry sectors. While the Swiss-Army and Host-style super apps consolidate services within a single platform or app interface, the corporate ‘Family’-style app takes a different approach by leveraging a portfolio of apps and companies under the same ‘parent’ holding company. Several super apps in our dataset explicitly identify themselves as a family of apps or companies, such as ‘Meta’s Family of Apps’ and ‘the Snap family of companies’. Notably, most apps in our dataset belong to a family. In this section, we delve deeper into this corporate dimension of super apps.

Tracing family lineages and composition

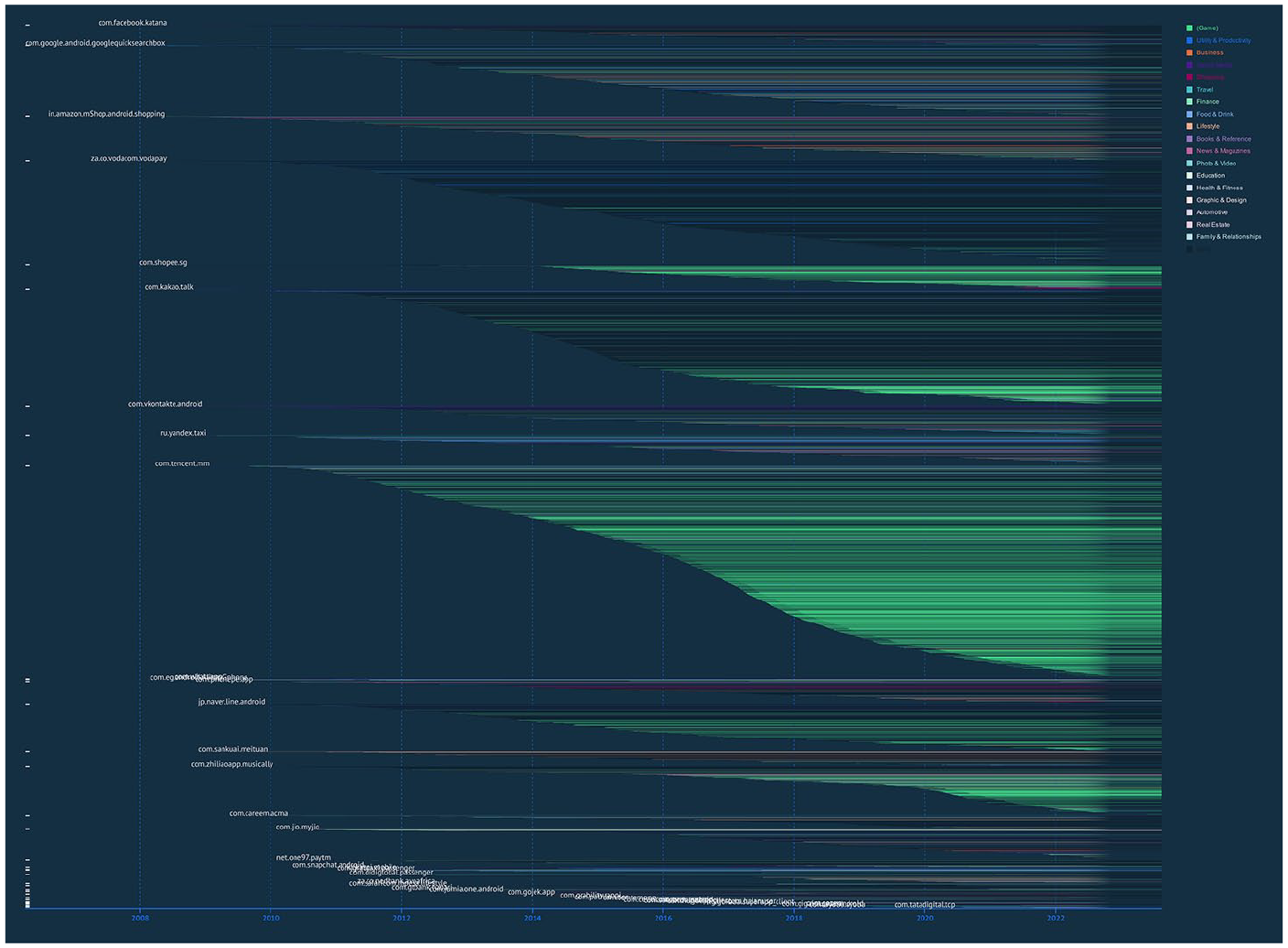

Tracing the complete lineage of a super-app family offers a more comprehensive perspective on how the super app evolves as part of a corporate conglomerate’s offering(s). By combining the lineages of all super-app families in a chart, Figure 4 displays the trajectories of each app and provides insights into related corporate strategies and distinct growth trajectories. The chart, moreover, illustrates the dynamic nature of super-app constellations and the relationships between apps within the same family, including the service categories they primarily address.

Super-app family lineages, including apps that have previously been removed from a store, 2008–2023. Each horizontal bar is an app, and its trajectory is shown from its initial release date. Colour-coding: by primary genre; groups: by super-app family. Data: data.ai.

The first aspect to consider is family size. Here, we identified the immediate owners of the 41 super apps, which are frequently subsidiaries of larger holding companies, and examined the size of their families. We found that apps like KakaoTalk (140), LINE (117) and MyJio (99) have relatively large immediate families. However, when considering the entire families of each super app at the ‘parent’ holding company level, including all subsidiary app companies, even larger extended corporate families are revealed. For example, KakaoTalk (Kakao Corp) has 277 relatives (1637 removed), LINE (Softbank) has 544 (5061 removed), VodaPay (Vodafone) has 445 (771 removed), WeChat (Tencent) has 909 (2380 removed), and Careem (Uber Technologies) has 86 relatives (57 removed). All these cases involve a notable degree of experimentation with new apps, some of which may be later removed. Tracing the historical lineages of super-app families allows for a temporal comparison of their expansion or contraction. Our findings indicate that although WeChat and KakaoTalk began expanding their app families around the same period, their strategies differ significantly. WeChat has mainly focused on launching new apps in the ‘Games’ category, while KakaoTalk has opted for a more diverse expansion, introducing new apps in the ‘Social Media’ and ‘Travel’ categories and others. This graphical representation serves as a valuable starting point for the comparative analysis of super-app family evolution over time.

Second, we identified the ultimate ‘parent’, or head of family, for each super app and examined the size of their families at this level. Notable families include Facebook (part of Meta, 65 apps), Didi (DiDi Global, 48 apps), and Uber (Uber Technologies, 86 apps). These families offer services aimed at different types of users. Both Uber and Didi show a growing range of services offered across the family. For instance, Uber’s family consists of distinct consumer-facing services like Uber, Uber Eats and JUMP, along with supporting apps for these services such as Uber Fleet, ‘Uber – Driver’, and ‘Uber Eats Manager’.

We subsequently delved into the composition of these families, which provides a unique perspective on how services are conglomerated. The findings demonstrate that while most families have a focus, they all offer services across multiple industry sectors, as shown in Figure 5. Games emerged as the most prominent category overall, covering various online gaming genres. Holding companies like Tencent (WeChat) had 1574 game apps in their family at one point, followed by Kakao Corp (KakaoTalk) with 365, ByteDance (TikTok) with 223, Sea (Shopee) with 121, and Softbank (LINE) with 120. Games are a key segment of the app economy, serving as a primary source of consumer engagement and revenue through in-app advertising and monetisation for many companies. Other significant genres offered by family members include ‘Utility & Productivity’, ‘Business’, ‘Social Media’, ‘Shopping’, ‘Travel’, ‘Finance’, and ‘Food & Drink’ apps.

Primary consumer services offered within the same super-app families (i.e. family composition). Data: data.ai.

Growing families through corporate strategy

A second aspect to consider is the growth of new family members. While new members can be offspring of the same parent app or company, they are more commonly ‘adopted’ through corporate strategies such as mergers and acquisitions (M&As). For example, while Facebook Messenger was born from Facebook, the company also acquired Instagram and several other subsidiaries, which were subsequently unified into the same infrastructure (van der Vlist et al., 2022: 18). Similarly, Uber Eats emerged from Uber Technologies, which later acquired Careem to expand its operations into a new region. Another instance of corporate strategy is the merger between Gojek and marketplace app Tokopedia, resulting in the GoTo Group holding company (Indonesia) with the aim to create ‘a unique and complementary global ecosystem’ to better compete with other super apps such as Grab and e-commerce platforms like Shopee (Singh, 2021).

In addition to M&A strategies, corporate families are formed through strategic partnerships and investment initiatives. These strategies are commonly used to expand a super app’s range of services and strengthen its market position. While Careem, Grab, and Uber refer to their drivers, restaurants, and merchants as ‘partners’, Careem additionally partners with companies such as Amazon, Ikea, McDonald’s, and Zara for its on-demand and food delivery services. Similarly, JumiaPay partners with insurance companies, public transportation companies for bus ticket booking, and educational institutions and councils for paying for educational services and obtaining graduation certificates. In 2020, VodaPay (Vodafone Group) partnered with Alipay (Alibaba Group) to establish a super app for financial services in South Africa. This partnership aims to replicate China’s investments in mobile digital infrastructure and other types of infrastructure across the African continent, enabling the extraction of data and value (Avle, 2022). In India, digital wallet apps Paytm, PhonePe and MyJio have formed partnerships with the government to provide payment services and contribute to the government’s vision for India’s digital ‘cashless’ future (Mukherjee, 2018).

Capital investments, along with mergers and acquisitions, can indicate shifts in corporate strategy. An example is PhonePe, previously owned by the Indian e-commerce giant Flipkart, as of 2023 it is majority-held by Walmart. This demonstrates Walmart’s interest in expanding its fintech capabilities globally and combining its retail and financial services offerings into a unified platform (Shevlin, 2021). Similarly, Uber’s acquisition of Careem and the subsequent 2023 investment of US$400 million from e& (UAE) led to a bifurcation of Careem into two units: Careem Rides and Careem Technologies. Careem Technologies is tasked with ‘supercharging’ the super-app vision by establishing verticals in key markets. 5 This strategic approach envisions Careem as the ‘regional technology, marketing, and organizational platform’ for local startups, utilising their existing market position and infrastructure to drive further diversification and evolve into a Hub-style app.

Geographic specificity or profiles: international expansion and cross-border operations

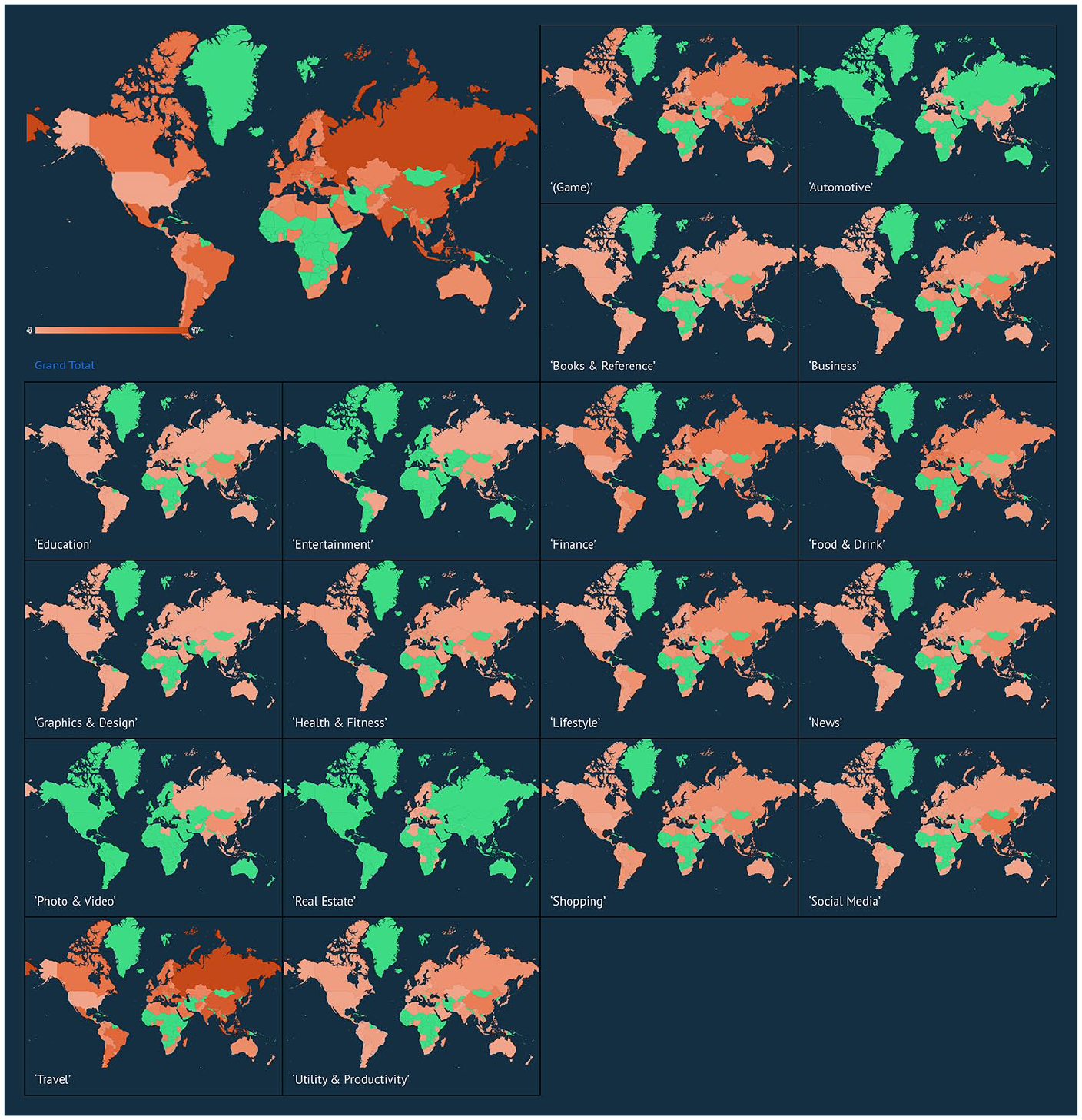

Finally, super apps are characterised by their ‘cross-border nature’ as they operate across multiple countries and regions, both as individual apps and corporate families (Chai, 2021: 45). Previous studies have highlighted that their evolution is profoundly shaped by regional context (Jia and Kenney, 2022; Jia and Ruan, 2020; Kaye et al., 2021; Pitre, 2022; Steinberg et al., 2022). As super apps expand their operations internationally, they must navigate diverse cultural norms, local regulations and infrastructural variances, leading to distinct geographic profiles and tailored corporate strategies. Figure 6 illustrates the geographic availability of all super apps in relation to the restrictions imposed by their developers or by the Google Play Store. That is, for various reasons, these super apps are not accessible in every country or region around the globe. The figure also shows the geopolitical tensions reflected in the app stores, with the sanctions imposed against Russia following the 2021 Ukrainian invasion. These restrictions are visible, for instance, in the ‘Finance’ service category. Inversely, apps tend to be the least restricted in African countries or regions, shown in green.

Local availability restrictions on super apps: super apps in each of these service categories are most frequently not available in these countries or regions through Google Play. Counting: by the number of apps, not their users; colour-coding: red indicates restrictions, with darker shades signifying more frequent restrictions, while green indicates no restrictions, making the apps available in those areas. Data: Sensor Tower and data.ai.

For instance, Shopee expands internationally with a geofenced approach, releasing region-specific versions of its app. Others, like LINE and KakaoTalk, offer a wide range of services in Asia while limiting their functionality to messaging in Europe. VK, in contrast, adapts to EU regulations in Europe, functioning primarily as a messaging, music, and video app, while in Russia it integrates with the country’s Health Ministry registers and education institutions, offers VK Pay for virtual banking services, and broadcasts live sports. WhatsApp, primarily a messaging app in Europe, becomes a super app in Brazil and in India by including shopping and payment services. Apps like TikTok employ a dual-version strategy – Douyin in China, adhering to state regulations, and TikTok elsewhere, catering to both market and governmental requirements (Kaye et al., 2021). These different strategies underline the adaptability of super apps to regulatory environments and their ability to segment their offerings to target local markets. Consequently, many super apps operate by developing a suite of apps tailored to a national context, indicating that the process of conglomeration is often nationally oriented.

In conclusion, most super apps, because of their primary focus on specific services, have a unique geographic profile and are region-specific, popular in certain countries or regions rather than globally available through the main app stores.

Furthermore, the findings indicate a strong association between service categories and countries or regions, indicating a preference or alignment towards particular service categories (Figure 7). Super apps from the Global South primarily focus on ‘Finance’, particularly ‘Digital Wallets & Payment’, ‘Food Delivery & Carryout’, and ‘Grocery Delivery’, ‘Local Service’, and ‘Transportation’. In contrast, super apps from the Global North tend to be centred around ‘Communication’ and ‘Media Sharing Networks’ (‘Social Media’) and ‘Transportation’. Notably, the Asia-Pacific region is home to numerous apps in the ‘E-commerce’ (‘Shopping’) category, as well as Flight, Hotel and Rail, and Coach-Booking apps.

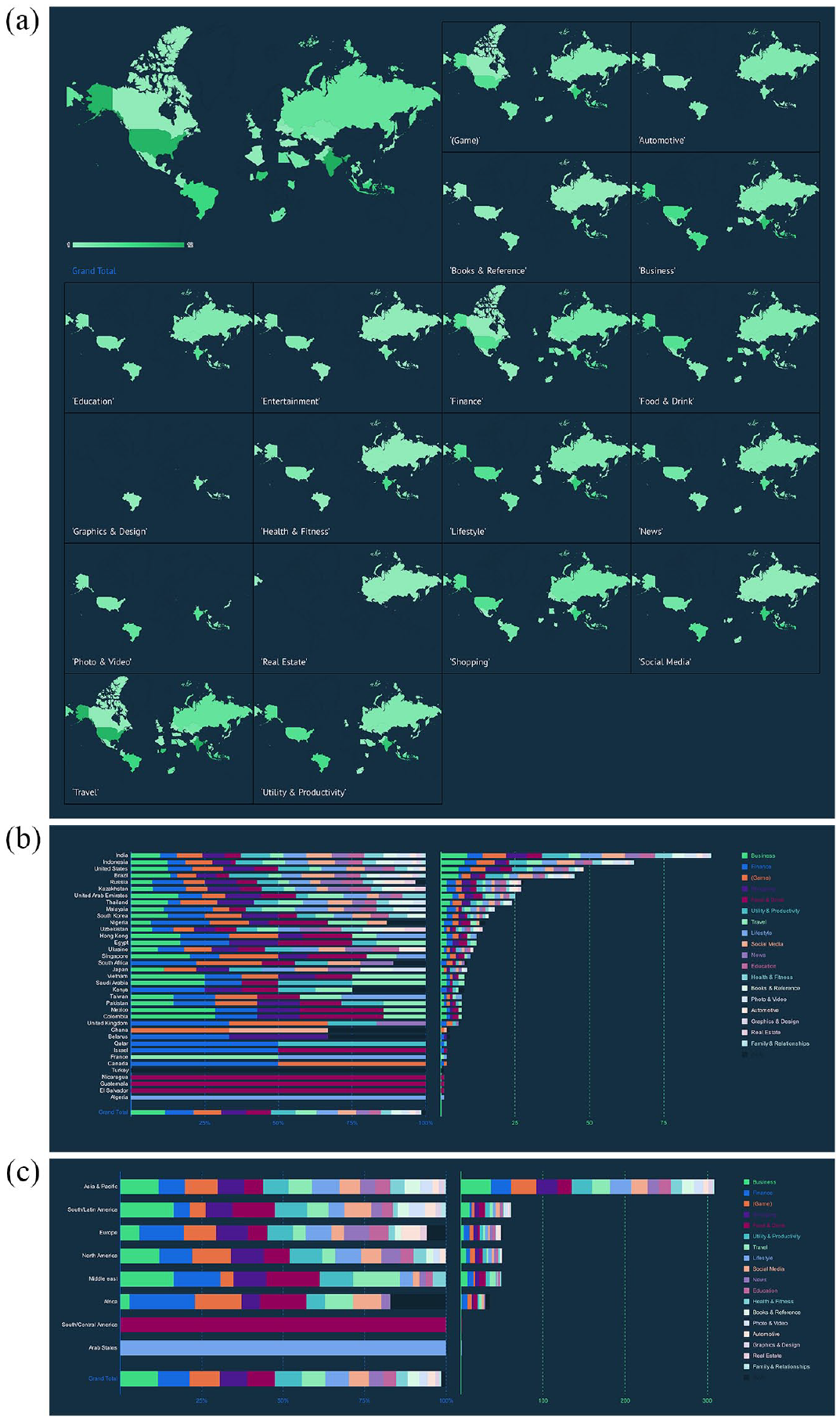

(a) Global countries or regions of importance for super apps: super apps in each of these service categories most frequently target these countries or regions as ‘top’ markets. Counting: by the number of apps, not their users; colour-coding: green indicates countries or regions of importance, with darker shades signifying more frequent importance. Data: Sensor Tower and data.ai. Geographic specificity or profiles: global countries or regions of importance for all super apps, including family members, shown (b) by country and (c) by region. Data: Sensor Tower and data.ai.

Pivoted by country (Figure 7(b) and (c)), we see that India is by far the most diversified and frequent ‘top’ market according to Sensor Tower, followed by Indonesia, the United States, Brazil, Russia, Kazakhstan, the United Arab Emirates (UAE) and Thailand. Furthermore, many countries, especially in Europe, are rarely or never categorised as ‘top’ markets, highlighting that super apps are a global phenomenon with a clear geographic specificity and a primary focus outside of Europe. It is also important to note that China is absent as a ‘top’ market due to the unavailability of the Google Play Store in that region.

An examination of African super apps aligns with Ajene’s (2021) observation that their focus predominantly lies in mobility, financial services and telecommunications. The ownership and origins of super apps in non-Western countries, which frequently originate from or are closely affiliated with telecommunications companies, contrast with the strategic initiatives pursued by Western Big Tech companies in those countries like Facebook Basics, and Internet infrastructure investments by Google and Facebook. In our analysis, African super apps are predominantly classified under ‘Finance’, including notable examples like JumiaPay, M-PESA, and VodaPay. However, we also identified apps categorised under ‘Food & Drink’, such as Gokada and Avo SuperShop.

In Southeast Asia, ride-hailing apps such as Grab and Gojek have emerged from the transportation industry, while in China, super apps like WeChat and Alipay have emerged from the communications and financial services sectors. This highlights the varied origins of super apps in different regions. Notably, the prevalence of finance services in Asia and Pacific, Africa, and the Middle East reflects the manifestation of gig platforms in the Global South, creating new markets that operate within the realms of both formal and informal economies (Heeks et al., 2020). However, it is important to note that certain categories are absent in specific regions. For instance, the limited presence of finance services in Europe, America and the Middle-East and North Africa can presumably be attributed to strict financial regulations that impose restrictions on the availability of such offerings in these areas.

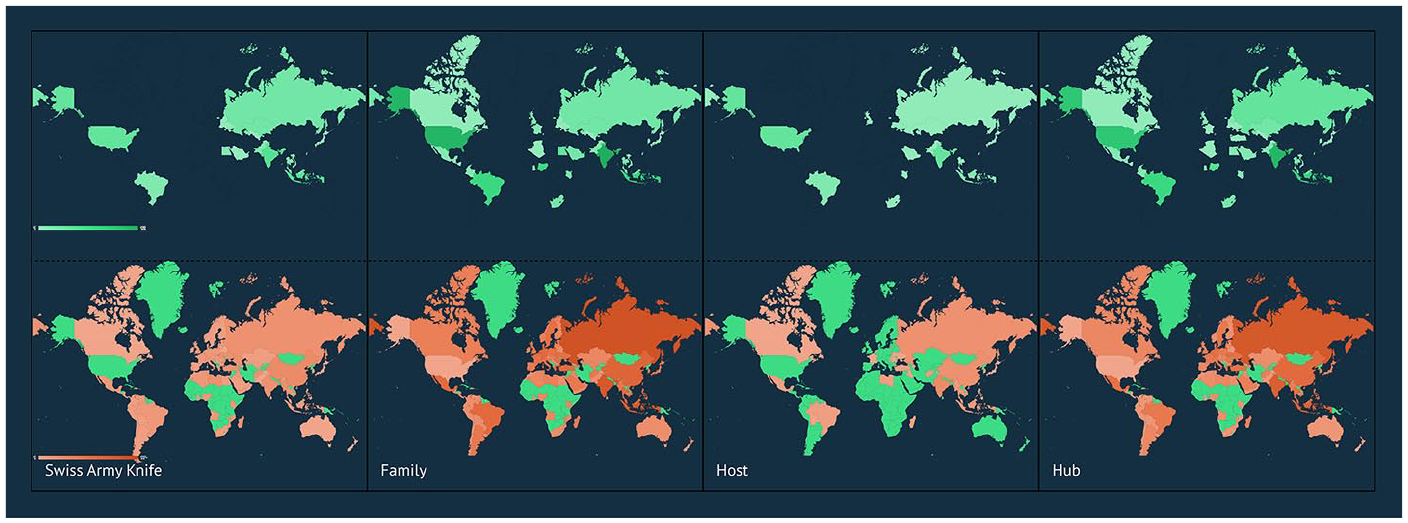

Regarding the types of super-app constellations, we find that the Asia-Pacific region exhibits the highest prevalence of Swiss-Army and Host-style super apps, with a notable presence of Family super apps as well (Figure 8). In contrast, North America and Europe have relatively fewer Hosts that incorporate internal mini-app ecosystems. Remarkably, none of the apps in the source list for Africa and South/Latin America were categorised as Swiss-Army Knife.

Geographic distribution of super-app constellations: global countries or regions of importance (upper) and local availability restrictions (lower). Data: Sensor Tower.

Conclusion: conglomeration in the global digital economy

In October 2022, a fire at a KakaoTalk data centre in South Korea set off a chaotic days-long nationwide blackout to the company’s manifold services, from groceries delivery to digital payments, taxi travel, and social media messaging, leading President Yoon Suk-yeol to describe the super app as ‘nationwide infrastructure’ and announcing an investigation (Che and Young, 2022). The event duly illustrates the entanglements and potential risks that arise as super-app companies deeply integrate into people’s daily lives, capturing and formatting all kinds of essential activities. ‘Super-appification’ represents an intensified version of the broader trend of ‘appification’, with super apps assuming an increasingly pervasive role in reshaping various aspects of everyday life. For Athique (2019), writing in the Indian context, this potentially leads to ‘the expansion of a “mediated economy” through which an increasing number of market exchanges are aggregated within portals that allow value capture at the transactional level (through data, certainly, but more explicitly through commissions and subscriptions)’ (p. 73). The rise of super-appification blurs the boundaries between apps and platforms, with apps assuming platform-like characteristics and platforms embracing app-like functionalities in both the technical and ‘multi-sided’ market-based meanings of the term (van der Vlist, 2022: 32). Super apps thus manifest as unified platform-like constellations that consolidate services across diverse industry sectors and countries, offering an integrated, all-encompassing user experience.

In this study, we offer a distinct, global overview of ‘super apps’, enabling comparative analysis of their characteristics and origins worldwide, and paving the way for further theorisation of this phenomenon. The process of super-appification is accompanied by different patterns and dynamics of conglomeration, as demonstrated through our analysis of 41 super apps from around the world. Super apps achieve their ‘super’ status by integrating a wide range of essential everyday services across industries and borders within constellation types. ‘Super-app constellations’, as a concept and typology, offer a comprehensive framework for understanding the conglomeration dynamics that drive super-appification in the global digital economy. Conglomeration patterns involve corporate strategies, development approaches, and international expansion strategies. We identified four distinct types of super-app constellations, each exhibiting unique patterns of conglomeration. Swiss-Army-style super apps expand their service offerings within a single app, consolidating industries previously served by separate app companies. Family apps expand through their app and company portfolios, extending services and entering new markets through subsidiaries. Host and Hub-style super apps leverage third-party developers to provide complementary services, capitalising on network effects either internally or through an external app ecosystem. This typology establishes an empirical foundation for understanding ‘super-appification’ both as a form of conglomeration in the app economy and as an app-specific form of platformisation. Unlike platformisation, which involves a single platform branching into new sectors, app conglomeration creates various distinct forms by bundling services into unique constellations, potentially as a strategy to circumvent regulations.

The analysis of super-app constellations illustrates how these apps are typically embedded within large corporate infrastructures and leverage their networks and portfolios to expand their services and enter new markets. While some may be awaiting the emergence of Western super apps like WeChat, it is important to take a broader view and recognise the diverse types of super apps that already exist across different regions. Our study reveals that, in contrast to Musk’s perspective, super apps have already gained substantial presence in the areas he targets for launching his ‘everything app’. It showcases the regional variations and complexities of the super-app model, emphasising the need for a global perspective when examining the cultural and economic aspects of mobile apps and platforms.

In general, the emergence of super apps calls for reevaluating traditional industry taxonomies and developing new approaches to define and understand their expansion strategies. Our study lays the groundwork for addressing these challenges by providing a framework for analysing conglomeration; shedding light on their dimensions, and for evaluating their potential governance implications. These include understanding the crucial role of app stores in shaping the global app landscape, including restrictions in place by Google and Apple to prevent downloading and installing additional apps or code from sources other than the respective app stores, a characteristic found in Host-style apps like WeChat. 6 Furthermore, recent changes and restrictions on third-party tracking underscore the advantage of Family-style conglomerates, which can leverage first-party data collected directly from customers within their super-app ecosystem. As such, GrabAds, a service offered by Grab, facilitates connections between advertisers of various sizes and millions of individuals across Southeast Asia during their daily activities ‘as they eat, shop, and commute every day’. The service harnesses ‘rich first-party data insights to create personas and audiences based on actual consumer behaviour within our superapp ecosystem’ (Grab, n.d., emphasis added), all without relying on cookies or third-party trackers.

More broadly, the trend towards new forms of conglomeration in the global digital economy has significant sociopolitical implications. It involves deeper integration of technology companies horizontally and vertically across industries, raising concerns about data enclosure, erosion of local public infrastructure, and the implications of ‘leapfrogging’ strategies in developing countries for the consolidation of corporate power. It is important to monitor whether super apps, particularly those of the Host type, prioritise their own services over third-party complementor offerings, as well as the implications of the growing dependence on apps as social infrastructure, including issues of national infrastructure and potential monopolistic practises, as exposed by the KakaoTalk data centre failure. Various apps in our dataset demonstrated aspirations to attain such infrastructural status within their respective countries through their development of ‘products that nations run on’ (Gojek), essentially spreading ‘cloud services’ as a ground-level everyday enveloping ‘mist’ (Scott, 2022). By conducting a global exploration of the characteristics and dynamics of super-app constellations, along with presenting a novel typology, our study offers decisive insights into the continually evolving digital landscape. Furthermore, our research highlights the crucial role that these super apps play in shaping people’s access to essential services on a daily basis across different regions of the world.

Footnotes

Acknowledgements

Data visualisations and analysis were primarily conducted by the first author. The authors would like to thank the participants of the initial pilot study, titled ‘The Evolution of Super Apps’, conducted during the 2022 Digital Methods Summer School at the University of Amsterdam, as well as the anonymous reviewers for their generous and constructive comments.

Data availability

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Parts of this work were supported by the Dutch Research Council (NWO) Spinoza Prize grant number SPI.2021.001 (awarded in 2021 to José van Dijck, Professor of Media and Digital Society at Utrecht University); the German Research Foundation (Deutsche Forschungsgemeinschaft, DFG), project number 262513311 (SFB 1187: ‘Media of Cooperation’); and the Dutch Research Council (NWO), project number VI.Veni.191C.048.