Abstract

Keywords

In 2015, Norway introduced a free treatment choice (FTC) reform within specialist health care to reduce waiting time, increase patients’ choice and to increase hospital efficiency. Patients with a granted right to specialist health care may now choose to receive care from a new category of providers introduced by the reform: private providers (for profit and non-profit) approved by Helfo (the Norwegian Health Economics Administration). They offer certain pre-defined services at pre-defined prices. This article focusses on these Helfo-licensed providers. We ask: What developments and consequences of new providers did key actors expect? What development of Helfo-licensed providers do we see and why? How have these Helfo-licensed providers influenced collaboration between public and non-public providers, and public providers’ recruitment of personnel?

Our analysis contributes to the literature on restructuration and marketisation of welfare service provision in Nordic welfare states. While public services overall have been less studied than cash benefits, this applies particularly to addiction treatment, although two recent studies have found Norway to be still rather welfare-oriented in a Nordic comparison (Stenius & Storbjörk, 2020; Storbjörk et al., 2021). We discuss this in light of the FCT reform and its possible consequences for recruitment and public–private collaboration, which are two key factors that may be influenced by the introduction of private welfare providers.

We focus on multidisciplinary specialist substance abuse treatment (MST) and mental health care (MHC) as the treatment choice was first introduced here. Furthermore, although most FTC patients use outpatient somatic services, MST and MHC inpatient care represent the majority of costs. This makes a discussion of development of Helfo-licensed providers and its consequences particularly relevant for these areas. By including statistics for somatic care, we can also consider aspects of different contexts of health provision between these areas.

Helfo-licensed providers may or may not have an additional tender agreement with Regional Health Authorities (RHAs). This particular category of service provders, however, is new (Ringard et al., 2016). Whereas the system of tender agreements involved a collaborative and often long-term relationship between the public and private provider, the reform layer of Helfo-licensed providers explicitly espoused a competitive relationship where public and private actors were to compete for patients.

Thus, the background of Helfo-licensed providers is important. If they were established because of the reform, they represent a stronger potential challenge for recruitment of personnel than established providers that have an existing pool of staff that they can draw upon. Also, if providers existed prior to the FTC reform without tender agreements, they may have offered private services paid by individuals or insurance companies, or only offered primary care level service, meaning that they lack experience of specialist care level service provision. This may complicate coordination in terms of patient pathways and communication between authorities, public and private providers. Hence, while studies of the number of Helfo-licensed providers and their market share would give important knowledge, our analysis, including their influence on collaboration between public and non-public providers and public providers’ recruitment of health personnel, provides a more comprehensive picture of the scope of privatisation in MST and MHC.

First, we describe the reform and introduce earlier contributions to the debate guiding our analysis. Next, we present methods and data. The analysis starts with a study of policy documents. Based on statistics and interview data, we then discuss the development of Helfo-licensed providers, and how they influence collaboration between public and non-public providers and recruitment of personnel. This is followed by a discussion and conclusion.

Reform background

The Norwegian healthcare system, as in the other Nordic countries, is overwhelmingly tax financed, although small co-payments exist and with the clear intention of providing equality of access (Lyttkens et al., 2016). The country is divided into four regions, each with one RHA responsible for providing specialist healthcare services to patients in its catchment area. The RHA secures this through the hospitals they own or through agreements with private providers.

FTC is an extended choice reform as earlier reforms allowed somatic patients to choose between public and private providers contracted by an RHA. The reform covers MST, MHC, some rehabilitation services and somatic illnesses.

The FTC reform is part of an overall policy change of using market mechanisms in healthcare systems, including free patient choice of provider (Brekke & Straume, 2017; Lyttkens et al., 2016; Ringard et al., 2016). The FTC reform had three pillars: (1) Patients with a granted right to specialist health care could now also choose among a new type of providers, i.e., so-called Helfo-licensed providers. This is both the most innovative and the most controversial part of the reform. (2) The RHA was instructed to increase purchase of services from the private sector (via tenders). (3) The public hospitals could, to meet extended competition, increase their number of treatments financed by Diagnosis Related Groups system.

Helfo describes what obligations Helfo-licensed providers must fulfil. This includes having sufficient and competent staff, reporting activity and waiting time, having systems ensuring information exchange and communication with RHAs and municipalities as well as internal quality assurance systems. Helfo follows up, controls and reimburses licensed providers. Helfo charges the RHA for the services provided by the Helfo-licensed providers to patients that belong to the RHA's catchment area.

As an introduction to our analysis, we briefly present how the FTC reform has developed in the years 2015–2019 in terms of patients and costs. 2020 and 2021 are extraordinary years due to the ongoing pandemic, and for part of this period the free treatment choice was suspended.

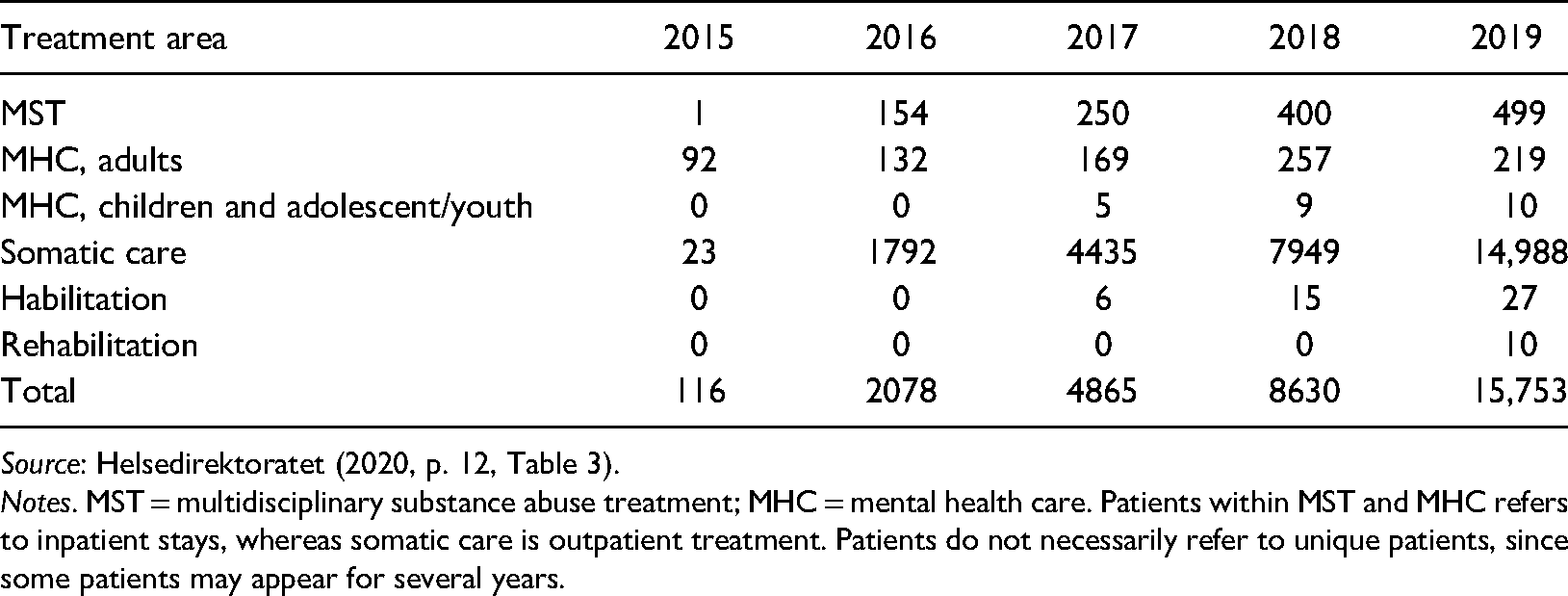

As Table 1 illustrates, total activity within the scheme increased substantially over the five years. The major component of patient growth is in somatic care which accounts for 95% of patients in 2019. Importantly, patients within MST, MHC and rehabilitation refer to inpatient treatment that extends over several days and weeks. For somatic care, patients refer to outpatient care. For instance, within MST the total number of inpatient days (bed days) for 2019 was 603,770, and, of these, 16,799 days were within Helfo-licensed providers, making up 2.7% of total inpatient days (bed days) (Helsedirektoratet, 2019a, Table 2.1., p. 17).

Number of patients within the Helfo license system, 2015–2019.

Source: Helsedirektoratet (2020, p. 12, Table 3).

Notes. MST = multidisciplinary substance abuse treatment; MHC = mental health care. Patients within MST and MHC refers to inpatient stays, whereas somatic care is outpatient treatment. Patients do not necessarily refer to unique patients, since some patients may appear for several years.

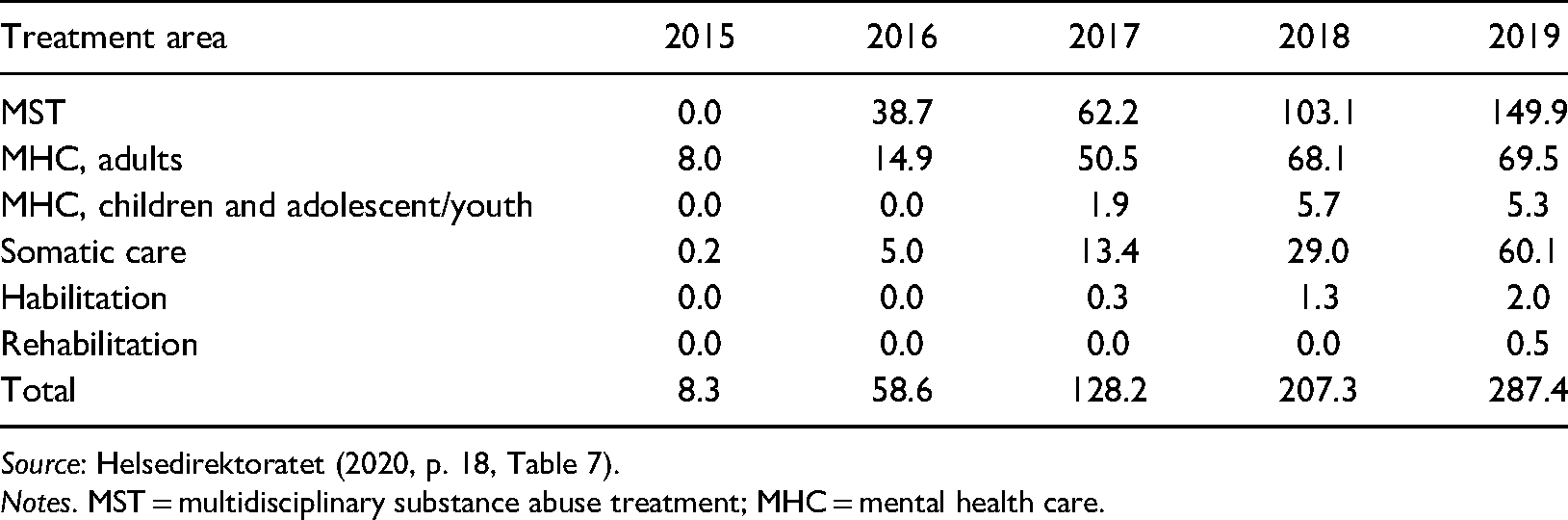

Table 2 reveals a substantial increase in costs since 2015, and a strong growth for each year since the start. Whereas the number of patients is largest within somatic care, the largest costs incur for MST and MHC, making up 78% of total costs in 2019. To point out the relative importance of costs, for 2018 tender agreement purchases from private providers amounted to 15.1 billion NOK (Statistisk Sentralbyrå, 2019). For this year, payment for reimbursements within the Helfo license scheme constituted a share of 1.4% of the above amount. In 2018, the total amount of purchases from the private sector (for-profit and non-profit actors) within MST amounted to 38% of total costs within this service area (Statistisk Sentralbyrå, 2019). Costs for purchases from Helfo-licensed providers were then 5% of this total. Within mental health care the corresponding share was 2.3% and only 0.3% within somatic care.

Costs in mill NOK (reimbursements from Helfo) within the Helfo license system, 2015–2019.

Source: Helsedirektoratet (2020, p. 18, Table 7).

Notes. MST = multidisciplinary substance abuse treatment; MHC = mental health care.

Patient choice reforms and public–private competition

Existing research on reforms promoting private welfare providers is inconclusive on its effect (Petersen et al., 2018). Hagen et al. (2018) refer to earlier studies that have identified recruitment and retention of health professionals and transaction costs as risks for public providers when outsourcing public service provision. Barros et al. (2016) state that competition among healthcare providers may have different effects depending on the context. For the FTC reform, service area (MST, MHC, somatic and rehabilitation services), inpatient or outpatient care, and geography could be relevant. According to Lindberg and Lundgren (2021), earlier research on effects of choice reforms finds that geography is important as private providers tend to locate in urban areas.

As Hehenkamp and Kaarbøe (2020) state, several European countries allow private providers to deliver health services at regulated prices to promote patient choice and service quality. Our findings may thus have relevance beyond Norway. Such patient choice reforms have, for instance, taken place in the Swedish and Danish publicly funded healthcare systems. The 2010 Swedish Primary Care Choice Reform allows patients to choose between private and public providers. Private care providers enjoy freedom of establishment and deliver services at pre-defined prices (Winblad et al., 2021). However, contrary to Norway, local health authorities may set local rules for the providers, e.g., demand a certain scope of services. Denmark offers patients an extended choice of provider if the waiting time is long. This is privately provided and publicly funded care as in Norway, and all treatment areas are included (Simonsen et al., 2020). We are, however, not aware of many studies on consequences within MST and MHC.

While marketisation reforms strengthening patient choice within healthcare are not new (Vrangbaek et al., 2012), the Norwegian FTC reform stands out in its design of the new private providers and the service areas covered. Specialist MST and MHC were given priority in the Norwegian reform whereas other countries have focused more on primary care or somatic services, or at least not emphasised MST and MHC as in Norway. Moreover, the literature on marketisation reforms is dominated by studies in somatic care. There are few studies of effects on addiction treatment (Storbjörk & Stenius, 2019a, 2019b). The analysis of patient choice and new providers within MST and MHC is thus a further important contribution of this study.

The existing studies within addiction treatment provide important insights that our study relates to. As Storbjörk and Stenius (2019a, 2019b) argue, there are few studies on what they refer to as marketisation (privatisation, public procurement and managerialism) and its implications, especially within substance abuse care. Storbjörk and Stenius identify fragmentation and how it “obstructs coordination and continuity of care” as possible negative effects of marketisation in this area that should be studied more closely (2019b, p. 35). Stenius and Storbjörk (2020) compare developments in procurement and regulation of the addiction treatment systems in Sweden, Denmark, Finland and Norway following an EU directive from 2014. In this analysis, they distinguish between different service provision logics. The welfare state logic emphasises public responsibility for welfare, including funding of and actual service provision. The market logic emphasises private service provision which may still be publicly funded. Based on a range of indicators including presence of commercial providers, use of procurement, emphasis on welfare in procurement, and user involvement, Stenius and Storbjörk (2020) classify Norway as very welfare-oriented with little market influence. Storbjörk et al. (2021, p. 154) offer an analysis of residential substance use treatment in the same four countries and classify Norway as welfare-corporatist supporting non-profit providers and as not very market friendly. The few for-profit providers in this area are said to be within the free treatment choice system, limiting their potential to grow.

Methods and data

We combine quantitative and qualitative data to bring a comprehensive account of reform ideas, conflicting views on expected outcomes, and how the reform unfolded. We rely on key public reform documents including the consultation paper , consultation responses of key actors, and the proposition to the Norwegian Parliament (Storting). These documents are used to present the main reform ideas, expected consequences, and the different outlook emanating from different key stakeholders, particularly concerning collaboration between public and non-public providers and recruitment of personnel.

Statistics provided by the Norwegian Directorate of Health describe the development of the reform quantitatively in terms of users, providers and their locations as well as costs. Interviews and documents provide the key sources to further analyse reform outcomes concerning collaboration and recruitment of personnel.

We draw on data from semi-structured interviews with representatives from Helfo and 28 public hospital trust units and all four RHAs. The initial reports from the Directorate of Health documented geographical variation in the localisation and patient use of Helfo-licensed providers (Helsedirektoratet, 2016, 2017). Moreover, we expected that availability of key personnel and extent of competition from private actors would vary between city regions and less populated areas. Hence, when selecting interviewees, we reflected both this geographical variation by including informants from all health regions and by including relatively more informants from regions with a higher incidence of Helfo-licensed providers (particularly health region South-East and health region West). Moreover, since variation could be found between MST and MHC, we recruited managers from both areas. We conducted 65 interviews in two consecutive rounds in 2018 and 2019. For this article, we mainly draw on a subset of 33 interviews (17 in 2018, 16 re-interviews in 2019) with managers based on semi-structured interview guides that explicitly address the introduction of Helfo-licensed providers and its implications for recruitment of personnel and collaboration. Yearly and quarterly reports from the Norwegian Directorate of Health and follow-up reports from Helfo provided additional qualitative data on the reform, complementing the interviews.

Usually, two researchers conducted the interviews together. The interviews were mainly performed by telephone and lasted on average 30 minutes. All interviews were audiotaped. Most interviews were fully transcribed and comprehensive summaries were written for the other interviews, involving both interviewers to assure quality.

The authors read and analysed interviews separately. Notes were made individually. In a second round the authors discussed and agreed on important findings from the interviews with a thematic analysis approach (Braun & Clarke, 2006). Answers to key topics in the interview guide were gathered and sorted under different themes, and then a subset of themes concerning collaboration and recruitment challenges was elaborated. Thematic analyses were also applied in scrutinising documents, using similar topics to those from the interview guide to orient the analysis.

Findings from interviews could be checked against issues reported in follow-up reports and annual reports and vice versa. This strengthened the reliability of findings, compared to relying only on one of these sources.

Informants received an information letter describing the project and were given the opportunity to provide written or verbal consent. The study was notified to the Norwegian Centre for Research Data (NSD), and the study was assessed to be in accordance with data protection legislation (ref. number 59574).

Results

What development and consequences of new providers did key actors expect?

Main arguments in public documents for the reform were that the introduction of competition from a new type of private provider as well as increased use of tender agreements would utilise remaining treatment capacity in the private sector and lead the public hospitals to increase their quality, become more effective and hence waiting times would be reduced. Moreover, the reform allegedly strengthened the freedom to choose, empowering the patient.

Ringard et al. (2016) offer a general account of the consultation process and background of the reform. In our analysis of the Proposition from the Ministry of Health and Care Services, the consultation, and the subsequent committee and parliamentary debates, we briefly present opinions expressed by different actors on Helfo-licensed providers, collaboration between public and non-public providers and implications for recruitment of personnel.

The most supportive statements in the consultation came from business organisations, commercial hospital actors, some of the non-profit providers and to some extent also from the Norwegian Medical Association. The Norwegian Nurse Organization was concerned that public hospitals would lose necessary competence, as key personnel such as specialist nurses would seek employment in private elective health institutions, with less severe shift arrangements than in public hospitals (Norsk Sykepleierforbund, 2014). The patient and disability organisation and the National Association for Heart and Lung Disease raised concerns about potiential lack of personnel within public hospitals (e.g., Funksjonshemmedes Fellesorganisasjon, 2014).

The South-East RHA supported the overall goal of improving availability and providing more choice for patients by purchasing more services from private providers. They were, however, highly critical towards the Helfo-licensed providers. The RHA was concerned about consequences for recruitment, where FTC providers attract key personnel from the public health trusts. In a situation of scarcity of specialist personnel, FTC providers could undermine established and well-functioning public offers (Helse Sør-Øst RHF, 2014). The consultation statements of the three other RHAs and health trusts were in line with this. In their view, one could reach reform aims through ordinary tender agreements.

In the consultation document, the ministry discusses which actors they consider to be possible Helfo-licensed providers (Helse- og omsorgsdepartementet, 2014, p. 58). The consultation document states that many Helfo-licensed providers will also have tender agreements (Helse- og omsorgsdepartementet, 2014, p. 44). The ministry states that to be licensed an actor must first have a general approval, as do all healthcare providers independent of the FTC reform, and then a special approval from Helfo (Helse- og omsorgsdepartementet, 2014, p. 60). As this is said to possibly apply to “some actors” this may be interpreted as implying that most actors applying for Helfo approval will be established actors. In the consultation document on the new regulations following the FTC reform, the ministry writes that it expects many of the private providers applying for Helfo approval to have tender agreements with RHAs (Helse- og omsorgsdepartementet, 2015, p. 61). In sum, this must be understood to imply that the ministry and Helfo expected that many actors applying for an approval would be established actors. This is confirmed in interviews with Helfo representatives.

We find formulations in several of Helfo’s annual follow-up reports to Helfo-licensed providers confirming this interpretation. One common formulation, here exemplified by a Helfo report following a meeting with a Helfo-licensed provider within MHC, is as follows: Helfo briefly accounted for the premise of the Ministry of Health and Care Services that it was most likely that private actors with tender agreements within specialist care would apply for approval within free treatment choice. This assumption is the main reason why one generally has referred to rest capacity at tender agreement providers, and that one in advance expected that fewer private actors would apply for approval within free treatment choice (Helfo, 2018, p. 6, authors’ translation).

In the consultation document, collaboration between public and non-public providers is also discussed. The Ministry states that securing integrated patient pathways is challenging when both public and private providers are involved (Helse- og omsorgsdepartementet, 2014, p. 5). The RHAs were worried that introducing Helfo-licensed providers would make safeguarding of their responsibility to provide services to patients within their catchment area more difficult (Helse Sør-Øst RHF, 2014, p. 3). In the proposition, the ministry acknowledges that securing coordination and integrated patient pathways is challenging without tender agreements as there is no agreement regulating collaboration (Helse- og omsorgsdepartementet, 2014–2015, p. 46).

Based on the proposition (Helse- og omsorgsdepartementet, 2014–2015) and the consultation documents, the Health and Care Services Committee issued their proposition to the parliament (Innst. 224 L, 2014–2015). The proposition was divided into a majority position consisting of the government parties and their parliamentary support parties, and a minority position made up of the opposition parties.

The opposition believed that the FTC reform might lead to loss of competence weakening public hospitals. They pointed to the RHAs’ consultation documents, clearly stating that long waiting times for defined problems often resulted from a lack of personnel, more than being an economic problem. Moreover, increasing capacity outside public hospitals would not solve the problem if this happens by means of leakage of personnel from bottlenecks within the public hospital (Innst. 224 L, 2014–2015, p. 37). This was not a concern for the proponents because the reform was to stimulate the public health service to become more effective, and it was reasonable to expect that most of the patients would still choose the public offer. They also argued that specialists and health personnel mainly wanted to work where the patients are and where professional challenges are extensive (Innst. 224 L, 2014–2015, p. 38).

What development of Helfo-licensed providers do we see, and why?

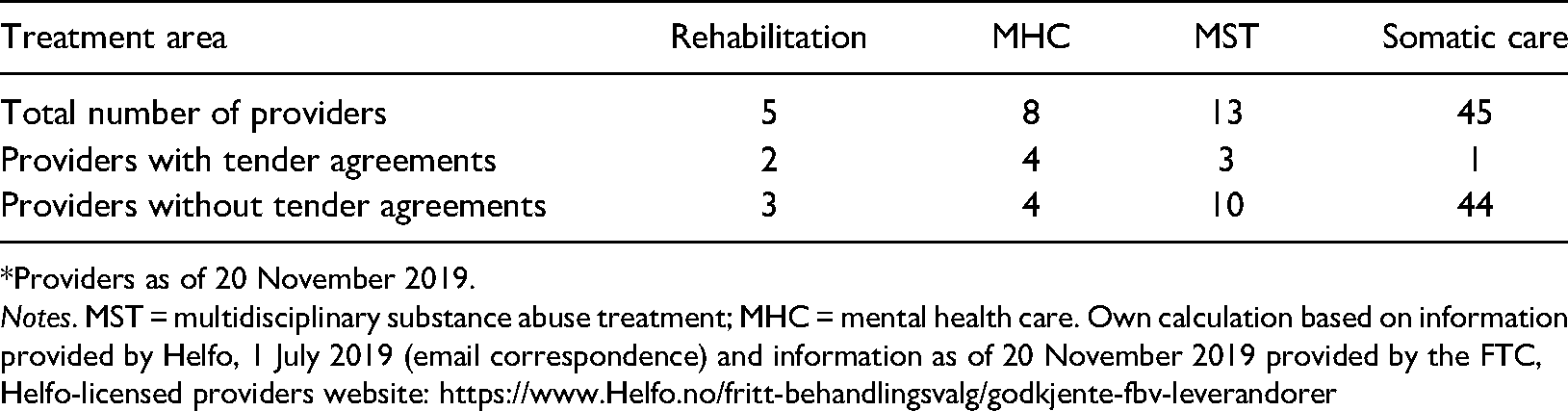

Table 3 provides an overview of all Helfo providers that have been licensed over the period 2015–2019. It details the total number of providers within the four major areas of provision and identifies the number of institutions within each category that also have tender agreements with RHAs or Health Enterprises and those that may be considered as Helfo-licensed providers only.

Overview of Helfo providers 2015–2019.*

*Providers as of 20 November 2019.

Notes. MST = multidisciplinary substance abuse treatment; MHC = mental health care. Own calculation based on information provided by Helfo, 1 July 2019 (email correspondence) and information as of 20 November 2019 provided by the FTC, Helfo-licensed providers website: https://www.Helfo.no/fritt-behandlingsvalg/godkjente-fbv-leverandorer

The numbers include all providers that are or have been Helfo-licensed providers for a certain time span. Table 3 reveals clearly that, contrary to expectations, a large majority are Helfo providers only. This applies to 61 (86%) of 71 providers. This bias was overwhelmingly found within somatic care (44 of 45 providers) and MST (10 of 13 providers). For rehabilitation and MHC, which have fewer providers, the division was more even. Overall, this suggests that the expected utilisation of remaining treatment capacity in the private sector has not occurred. Statistical information from Directorate of Health or other statistical sources related to Helfo-licensed providers does not distinguish between for-profit and non-profit providers. To provide an indication of this division we have checked each eligible provider on the FTC list (updated 12 May 2022) for providers within MST and MHC against the Brønnøysund Register Center. We find that for MHC five of nine provider units, and in MST eight of 16 provider units, were commercial actors. For somatic care, providers were overwhelmingly commercial actors.

For Helfo and public hospitals, interviews show that these new providers have incurred additional burdens on educational and guidance tasks to secure compliance with standards required for providing specialist health care. The first status report issued by the Directorate of Health noted that of 24 applications within addiction treatment only four were licensed, and that: There are several reasons as to why so many MST applications have been rejected or declined, for instance that the provider has not planned with sufficient manning and competence. Particularly within newly established providers we find that several have not got familiar with requirements for being a specialist healthcare provider and therefore requirements for competence and organisation (Helsedirektoratet, 2016, p. 9, authors’ translation).

Interestingly, we note that the number of Helfo-licensed providers varies substantially between RHAs. Of interest is the almost non-existence of Helfo-licensed providers (only one provider within somatic care) in the Central Norway RHA (Helsedirektoratet, 2019b, p. 10).

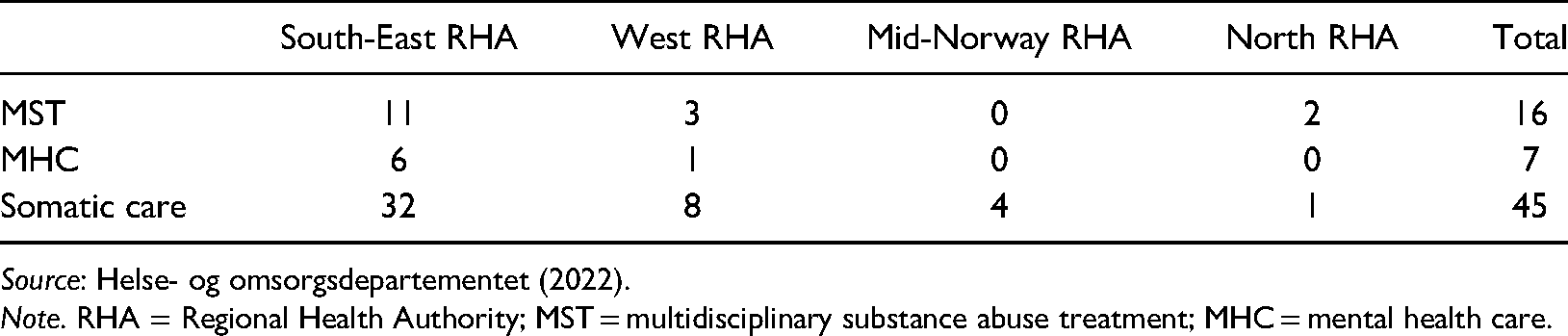

The strong geographical variation in localisation of Helfo-licensed providers is an interesting and persistent characteristic of the approval scheme. In Table 4, we present information as of November 2021 on eligible Helfo-licensed providers related to our areas (Helse- og omsorgsdepartementet, 2022, p. 6, Table 3).

Eligible Helfo-licensed providers by 11 November 2021.

Note. RHA = Regional Health Authority; MST = multidisciplinary substance abuse treatment; MHC = mental health care.

Implications for recruitment of personnel and collaboration between public and non-public providers

Initially, it should be noted that some interviewees were not always clear on the distinction between Helfo institutions and private institutions with a tender agreement. This is further complicated because some institutions have a tender agreement with an RHA and are also licensed as Helfo institutions. Moreover, the healthcare sector is constantly in need of recruiting new workers as the demand for personnel is steadily increasing. Because of this, it is difficult to disentangle isolated effects of the reform.

We need to distinguish between MST and MHC in discussing possible effects of the reform. Overall, possible reform effects were most visible within MST and less so for MHC. Within MST, effects on recruitment must be connected to geographical locations and specific situations of competition, for instance the near location of Helfo institutions to public and private institutions. One interviewee explained that the establishment of one large Helfo-licensed institution close to their own clinics had resulted in a specialist in psychology resigning and starting to work at this new Helfo institution. This informant argued that the reform, and the introduction of Helfo-licensed providers, may reinforce recruitment challenges. For the 33 interviews where recruitment and collaboration were thematised particularly, a minority of four interviewees (all but one covering MST) had experienced some leakage of personnel to Helfo-licensed providers. One of these mentioned the general growth of private providers. The majority had so far not experienced negative effects on recruitment of personnel from Helfo-licensed institutions.

That the large majority (86%) are Helfo providers only rather than being contracted by RHAs has important implications for collaboration between authorities, public and private providers. Whereas somatic patients often are given their final treatment by the Helfo-licensed provider, patients within MST and MHC often have clinical pathways that involve further treatment and/or attention after a stay at a Helfo-licensed provider. This may be within public specialist or primary care. Interviews show that the collaboration of the authorities and of public providers with Helfo-licensed providers without tender agreements is especially demanding. Representatives of Helfo refer to several challenges, including fundamental issues such as ensuring that services are given at the level of specialist rather than primary care, having qualified staff and implementation of routines. Representatives of public providers refer to incomplete patient pathways and insufficient communication compared to collaboration with contracted private providers. An unfortunate consequence is that care may become more fragmented when patients are treated by Helfo-licensed providers than in patient pathways involving contracted providers. Moreover, informants from public providers report that collaboration with contracted providers runs more smoothly. While this may result from new working relations that will improve as time goes by it is an important finding that limited experience with tenders so far may complicate collaboration between authorities, public and private providers.

Discussion

By the end of 2019, only 14% of Helfo-licensed providers had tender agreements. The majority may have been established due to the FTC reform or may be existing providers either without experience in specialist care or having offered private services paid by individuals or insurance companies. Our interviews include many reflections on why most providers are without tender agreements. A possible reason for the establishment of several of the Helfo-licensed providers may be that tenders are only available when agreements are to be renewed. Helfo-licensed providers, on the other hand, may be established at any point without waiting for the next tender and without a demand expressed by public institutions. Our interviews indicate that renewal of tender agreements every 4–8 years is common, and more often within somatic care, where 1–3 years is not uncommon.

One reason private providers with a tender agreement with an RHA choose not to apply to be qualified as Helfo-licensed providers as well is that each treatment centre must be approved. Accordingly, a provider with several treatment centres must fulfil the criteria for each. It is thus for instance not possible to rely on a pool of medical staff that satisfies overall criteria. A further important reason is obviously that the price level for tender agreements is higher than Helfo-licensed providers can charge. The ministry argues that the remuneration must be lower than in tender agreements to avoid an undermining of such agreements (Helse- og omsorgsdepartementet, 2015, p. 69). According to the Norwegian Directorate of Health's annual FTC reports (e.g., Helsedirektoratet, 2020), prices too low to be able to provide reasonable services is a recurrent topic, and several private providers have also expressed this through the media.

Moreover, in terms of payments for planned and conducted treatments the Helfo license arrangement and tender agreements also differ. Providers with tender agreements are paid in advance, with a specified occupancy rate as part of the contract. If the occupancy rate is marginally lower than expected, the provider keeps the payment. More substantial reductions in occupancy rate result in lower payments. A Helfo-licensed provider is paid post treatment, charging for each day of actual occupancy. In this respect, Helfo-licensed providers operate in a context of higher uncertainty regarding volume and payment than providers under contract. However, in a situation where a contracted partner is at risk of not reaching the occupancy level required to avoid payment reductions, incentives (higher payments for contracts than in the license scheme) are geared towards reaching that target within the existing contract rather than as a licensed provider. In addition, since the reform, changes in the tender agreements have reinforced barriers for contracted providers to enter as Helfo-licensed providers. To exemplify, private providers with a tender agreement with the South-Eastern RHA are paid for 100% occupancy rate if the actual occupancy rate is 95% or higher, whereas Helfo-licensed providers are penalised for anything below 100%. In addition, should a private provider with a tender agreement also be approved as a Helfo-licensed provider, the South-Eastern RHA “… requires 100% of the capacity fulfilled, and the possibility of providing only 95% and still receiving the full contractual payment is removed” (Sjøberg, 2019, p. 5). This of course makes it even less attractive for providers with an ongoing tender agreement to apply for Helfo approval. However, while tender agreements have limits on number of treatments, this does not apply to Helfo-licensed providers.

Finally, we add that one reason for contracted providers not to become licensed by Helfo could be a reluctance to show ability to deliver services at a lower cost that in tender agreements. Our speculation here, however, is simply based on how the price level is being deliberately set lower than in tender agreements. This is thus not a reason emphasised by our interviewees.

The FTC arrangement, and Helfo-licensed providers in particular, so far does not lead to much leakage of key personnel from public providers. However, this challenge is relevant for public and private institutions contracted by RHAs with Helfo-licensed providers nearby. As Table 3 shows, there are currently few Helfo-licensed providers within MST and MHC. Thus, there has been little competition for resources from such providers for public providers. It is therefore notable that public institutions with such providers in their area do report tendencies to leakage of resources to competing Helfo-licensed providers. This seems to confirm the point in Lindberg and Lundgren (2021) that choice reforms do not result in an even distribution of private providers, and suggests that further establishment of Helfo-licensed providers may increase recruitment challenges, although the evidence for this so far is inconclusive. Moreover, these challenges are more present within MST, or institutions combining MST and MHC, than in MHC providers. Finally, the unexpected growth of Helfo-licensed providers with no previous experience of tender agreements with RHAs has caused challenges for collaboration between public and private providers. This suggests that Storbjörk and Stenius (2019a) raised a valid concern for multidisciplinary specialist substance abuse treatment when claiming that marketisation may result in fragmentation and reduce coordination of services. We can also understand this as a transaction cost challenge that sometimes follows outsourcing of services (Hagen et al., 2018). With the new private providers, public actors must make sure that service delivery is actually given at specialist level as requested, and demand documentation that is not automatically provided.

Five years ago, Brekke and Straume (2017) identified the FTC reform as a reform giving private providers room to compete with public providers. However, as their article was published scarcely two years after the introduction of the reform they could not discuss its implications in detail. Stenius and Storbjörk (2020) classify Norway as being very welfare-oriented. This rests on an analysis of addiction treatment systems at the municipal level as well as within specialist health care. Our analysis is restricted to specialist health care and developments following the FTC reform, which Stenius and Storbjörk (2020) only study briefly, and we include MHC as well. While we do not question the overall conclusion of Stenius and Storbjörk (2020), we do not consider developments in Norwegian specialist health care within MST and MHC to fit so clearly a welfare-oriented logic. Importantly, Norway has introduced a strong market-influenced steering in the sense that private providers can establish institutions independently of tenders and without public control. To exemplify the importance of this, and how fast changes may occur, we note how Stenius and Storbjörk (2020, p. 15) identify seven Helfo-licensed providers in MST in 2018. We identify 13 providers that were active in the years 2015–2019 (cf. Table 3). Extending the time by one further year would show 11 active providers at the end of 2020 (not displayed in Table 3). And in Table 4, we see 16 eligible providers within MST and seven within MHC. In our opinion, the growth in the number of patients and providers shows that the FTC reform gives private providers new opportunities. Our analysis also shows that Helfo-licensed providers have some – admittedly geographical uneven – influence on collaboration and public providers’ recruitment of health personnel even though the number of institutions is still modest. Moreover, in our interpretation, policies favouring third sector providers, government policy and strict accreditation requirements, which Stenius and Storbjörk (2020, p. 15) see as preventing a prominent commercial role, do not inhibit such providers from entering the market. Our account is also different from that of Storbjörk et al. (2021) in this respect, as they see few signs of market friendly policies and limited room for commercial providers in the free treatment choice system.

This also includes non-profit organisations that both historically and today have been important providers of welfare services directed towards persons suffering from alcoholism and other substance abuse. Their contribution is distinct both in terms of innovating service provision and in terms of their advocacy role for the marginalised groups their service provision address. Although Stenius and Storbjörk (2020, p. 8) state that non-profit organisations complement public service provision, we consider this to add another logic partly different from both welfare and market logics. This could thus be seen as a logic in itself. Key aspects of the non-profit logic – discussed by Stenius and Storbjörk (2020) as well – are the focus on social goals and public value, the avoidance of profit motive and flexibility in experimentation and innovation to adapt to changing needs and secure quality of services (see, e.g., Bogen & Grønningsæter, 2016). This role of non-profit organisations in Norwegian politics is also strongly reflected by Storbjörk et al. (2021, p. 147, cf. Table 1). Particularly interesting for our focus on MST and MHC is thus the share of non-profit eligible Helfo-licensed providers. The strong role of commercial actors represents a break with the historically strong role of non-profit organisations providing services within this area of the welfare state, and thus a strengthening of the commercial logic, although the scope of this reform element (i.e., the Helfo-licensed provider layer) is modest as of yet.

We have provided a slightly different account of developments in Norwegian substance abuse treatment than the more general picture drawn by Stenius and Storbjörg (2020), based on a thorough analysis of the FTC reform of 2015. However, our take-home point is that both forms of analyses are needed in building knowledge on changing welfare state logics of Nordic countries. Comparative and broad outlooks should be combined with more focussed and in-depth analysis.

The reform element of introducing a layer of Helfo-licensed providers was highly contested, providing ongoing political controversy. It was a focus of the election campaign of 2021, of both the government parties and then opposition parties. The incoming red-green government has promised to undo the FTC reform and instead strengthen public health provision. Currently, a ministerial consultation invites written comments on a suggestion of phasing out Helfo-licensed providers yet keeping traditional collaboration with the private sector by letting patients chose between public and private contracted providers (Helse- og omsorgsdepartementet, 2022). This could be expressing a strengthening of the welfare state logic at the expense of market logic, and hence a maintenance of Norway’s position, at least for now, as the most welfare-oriented of the Nordic countries. However, given the political saliency and the clear ideological controversies this reform arouses, we should expect future reappearances of similar market-oriented reform initiatives, framed in the language of free choice.

Therefore, the long-term implications of this reform are still uncertain. Several dimensions of the development of Helfo-licensed providers should be investigated more closely. First, how does the introduction of Helfo-licensed providers affect tender competition? In a recent article on a Swedish primary care patient choice reform, Winblad et al. (2021) show how county councils apply local regulations to shape the services of the new private providers. In Norway, the four RHAs are key actors in the FTC reform when it comes to shaping the services of the new private providers, although it must be done indirectly as regulations are national. One possible response of RHAs to the establishment of Helfo-licensed providers could be to design tenders with corresponding contracts in a way that ensures that RHA needs are satisfied through these tenders (coverage, scope of services), leaving less room for, and reducing demand for, Helfo-licensed providers. This policy of drawing on contracted private providers rather than Helfo-licensed providers may also secure recruitment and retention of health professionals as well as counteracting collaboration challenges. Furthermore, Helfo-licensed providers tend to be established where market conditions in terms of demand, availability of personnel, and possibilities for making a profit are the strongest. We note that the presence of Helfo-licensed providers varies substantially across the country, which might suggest that countervailing contractual policy developments, described above, have already taken place, in particular regions. This also shows that the importance of the FTC reform cannot be measured based on how many patients are making use of the choice alone, as the reform has several other important implications, e.g. that it affects tender competition.

Second, we need more knowledge about why so many Helfo-licensed providers are new. In Sweden, many new providers are for-profit and controlled by international private equity firms (Winblad et al., 2021). Many new providers are for-profit in Norway as well. What kind of ownership structure is developing here?

Third, further research should address more general consequences of the development of Helfo-licensed providers than our focus on collaboration and recruitment of personnel. Bensnes et al. (2022) have for instance identified important variation in the use of somatic care based on socio-economic characteristics. A similar study on who uses Helfo-licensed providers within MST and MHC would be interesting. Such issues and further aspects of the FTC reform are discussed by Holmås and Kaarboe (2021) and Holter (2021).

Conclusion

While existing research on private provision of health care and reforms promoting patient choice to a large extent covers somatic services, our study of the FTC reform sheds light on implications for addiction treatment and mental health care. Given the short amount of time since reform implementation, it is too early to conclude about consequences for recruitment of personnel to public institutions and collaboration between public and non-public providers. So far, effects are limited, but at the same time some interviewees express concerns that this might not be the case in the longer run if competition from these Helfo providers grows stronger.

Importantly, Helfo-licensed providers are not established all over the country, which is also well described in the annual Directorate of Health reports (cf., e.g., Helsedirektoratet, 2019c, p. 5, p. 23) and earlier research by Lindberg and Lundgren (2021). This implies that the FTC reform is not a national, but a geographically delimited reform with different implications in different parts of Norway. Moreover, it implies that our findings are quite region specific, and that the potential establishment of new Helfo-licensed providers in a region may have an influence on recruitment of personnel. This underlines an important finding in earlier research on competition among healthcare providers: evaluation of the influence of competition must be “interpreted in the light of the specific context” as the situation may vary substantially from one region to another, making it difficult to conclude with certainty (Barros et al., 2016, p. 232). In the long term, introducing new private providers may increase the level of market-orientation in this area of the Norwegian welfare state.

Footnotes

Acknowledgements

This paper is written as part of a project on: Evaluering av Fritt behandlingsvalg (“Evaluation of the free treatment choice reform”) (2017–2020). We would like to thank project leader Oddvar Kaarbøe and the project group for valuable comments. We would also like to thank the reviewers for very valuable comments.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Norges Forskningsråd (grant number 272666).