Abstract

A major challenge for CSR managers is the lack of strategic guidance for their decisions. No prior research has offered a framework that clarifies when which CSR initiative is advised. To address this gap, the authors argue that capitalizing on insights from marketing strategy empowers CSR decisions that cater to the demands of stakeholders and in turn pay off for the firm. The first marketing strategy principle—strategy formulation—leads to the distinction of four unique CSR strategies that link different relational approaches to the needs of different stakeholder groups (market stakeholder promotion, institutional stakeholder promotion, market stakeholder protection, and institutional stakeholder protection). The second marketing strategy principle—strategy prioritization—informs how to effectively deploy CSR strategies by matching them with marketing’s relative strategic emphasis (on value appropriation vs. value creation). The novel framework is tested with panel data from 3,572 firms over 19 years. The study reveals that the alignment of CSR strategies with marketing’s relative strategic emphasis is key for CSR’s effect on firm performance. Institutional stakeholder promotion fits best when value appropriation is the dominant marketing emphasis while market stakeholder protection matches best with an emphasis on value creation. A major implication of the study is that bringing marketing strategists to the CSR table helps firms to identify those CSR initiatives that also yield a business case for the firm.

Keywords

Introduction

Corporate social responsibility (CSR) is important. 77% of consumers desire to buy from sustainable brands and 73% of investors consider firms’ efforts to improve the environment and society when making investment decisions (IBM, 2022). The nearly $20 billion spent for CSR annually by Fortune 500 firms indicate that managers consider CSR investments critical for their firms to focus not only on economic stakeholder obligations but also other sustainability goals such as societal and environmental responsibilities (Briscese, 2021; Kim et al., 2024). 1

However, as we discuss in greater detail in the literature review below, academic research has not offered managers a comprehensive framework to strategically guide CSR investments. This endangers firms’ ongoing commitment to sustainable development goals because managers increasingly perceive CSR investments to be a liability and attribute this to a lack in strategic guidance for formulating and prioritizing CSR activities that reconcile with firm performance goals (Benoit, 2019; Fatima & Elbanna, 2023; Havlinova & Kukacka, 2023). Insufficient alignment with the marketing function has been made responsible for the lack of strategic CSR guidance: While 93% of executives state that CSR decisions should adhere to strategic marketing imperatives, only 6% state that marketing strategy is considered in CSR decisions (Accenture, 2021). Indeed, marketing strategy has been highlighted as key for ensuring long-term financial benefits of firm activities such as CSR (Feng et al., 2015). The reason is that marketing strategy is crucial for managing existing and building prospective customer and other stakeholder relationships and for sensing future opportunities and demands (Moorman & Day, 2016; Rosenbloom, 2022). Therefore, only an integration of CSR and marketing at the strategic level ensures firm initiatives that cater to current stakeholder demands without jeopardizing the prospects of future generations.

Thus, the goal of this paper is to examine how marketing strategy can provide guidance for CSR decision makers. Specifically, we ask (1) what are the firm performance effects of CSR initiatives that are informed by marketing strategy? And (2) are these effects moderated by marketing’s relative strategic emphasis?

We develop a framework that highlights how marketing strategy principles can serve CSR executives in two ways. One way is CSR strategy formulation. Marketing strategic thinking requires that CSR executives envision the needs of current and future stakeholder groups and then respond to these needs through appropriate relational approaches (Morgan et al., 2019). In line with arguments from marketing strategy literature on market segmentation (Moorman & Day, 2016), focal stakeholders are associated with distinct needs that emerge from the environments they are embedded in (market vs. institutional). Drawing on arguments from marketing strategy literature on managing customer relationships (Samaha et al., 2011), we argue that stakeholder needs can be catered to by promoting stakeholder wellbeing and/or protecting stakeholders from harm. Integrating both aspects leads to four general CSR strategies: market stakeholder promotion, institutional stakeholder promotion, market stakeholder protection, and institutional stakeholder protection. The framework includes the effects of these CSR strategies on firm performance.

Another way marketing strategic thinking can serve CSR is through CSR strategy prioritization. Marketing specifies the assets firms rely on in order to succeed. However, the idiosyncratic asset configuration of a firm has important implications for the performance consequences of CSR strategies as well (Morgan et al., 2019; Vorhies & Morgan, 2003). For instance, a firm with strong brand and advertising assets can create greater awareness for CSR efforts, resulting in greater financial impact (Servaes & Tamayo, 2013). We capture the idiosyncratic asset configuration of a firm through marketing’s relative strategic emphasis, which describes a firm’s investment preference for value appropriation versus value creation (Han et al., 2017; Saboo et al., 2016). While value appropriation focusses the market’s appreciation of a firm’s existing offerings (reflected in advertising efforts), value creation aims at delivering innovative offerings (reflected in R&D investments; Fang et al., 2011). Firms consider both value appropriation and creation, but budget constraints force them to trade off one against the other (Fang et al., 2011). Because relative strategic emphasis tends to be relatively stable over time, it is particularly meaningful to match it with CSR strategies so that they have a greater impact on firm performance. Thus, the framework accounts for the moderating effect of relative strategic emphasis for the CSR strategy-firm performance link.

To test the new framework, we track 3,572 U.S. firms over almost two decades and use rigorous econometrical methods to analyze the sample. The results contribute to the literature at the intersection of marketing, CSR, and sustainability.

First, we respond to recent calls to elaborate on CSR strategy formulation as a widely overlooked element of CSR management (e.g. Fatima & Elbanna, 2023). Previous research has provided insights on CSR efforts that either distinguish between different stakeholders (Mishra & Modi, 2016) or between different initiatives (Aksoy et al., 2022) but not both. This study is the first to empirically account for the performance consequences of CSR strategies that cover both dimensions of strategy formulation.

Second, we respond to the recent notion that “a company’s strategic approach to CSR . . . should not be one size fits all” (D’Cruz et al., 2022, p. 887). Our study is the first to inform CSR managers on which CSR strategy they should prioritize given a firm’s relative strategic emphasis in marketing (Vorhies & Morgan, 2003). In doing so, we also contribute empirical evidence to the emerging literature stream on sustainability and business ethics by showing that some CSR strategies do not cater to firm performance no matter what a firm’s strategic emphasis is. This fuels a recent debate on potential, irreconcilable tensions between sustainability’s key pillars (people, planet, and profit; Carmine & De Marchi, 2023; El-Bassiouny et al., 2022) and calls for considering CSR as a firm objective in its own right.

Third, we also contribute to breaking down a compartmentalized view of the firm. While marketing strategy and CSR strategy are often treated as separate “silos” (Sun et al., 2019) or even mutually exclusive (Banerjee & Wathieu, 2017), our study suggests that both functions should closely interact in delivering value to both society and the firm.

Literature review

As showcased in the opening examples, managers call for input from marketing strategy to guide their CSR investments. However, their calls have not been sufficiently addressed in the existing literature.

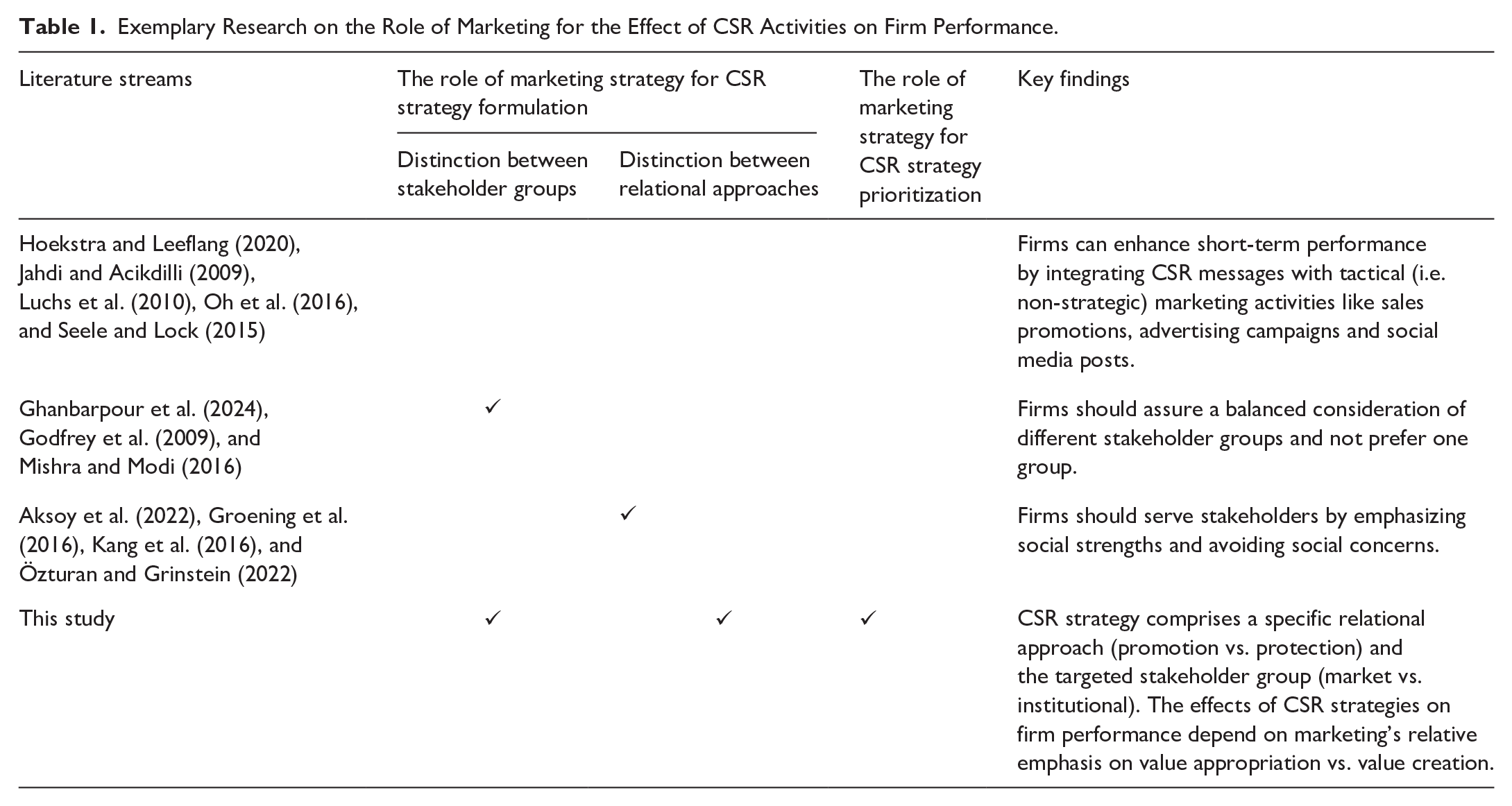

One literature stream has considered coordination between CSR and marketing tactics. These studies examine, for instance, how isolated CSR activities can be included in marketing tactics such as social media campaigns (Seele & Lock, 2015), advertising (Oh et al., 2016), public relations (Jahdi & Acikdilli, 2009), price promotions (Hoekstra & Leeflang, 2020), designing sustainable product features (Luchs et al., 2010), or infusing CSR in marketing departments (Özturan & Grinstein, 2022). While these studies have offered important tactical insight, Table 1 indicates that these studies do not use marketing strategy principles for differentiating between stakeholder segments or generalizable CSR approaches and they also do not account for the role of marketing strategy for the prioritization of CSR strategies, leaving a major gap in the literature. This gap is important as other authors have emphasized that managers are under pressure to integrate CSR with marketing strategy to guide long-term CSR decisions that transcend single products or day-to-day activities (Awaysheh et al., 2020; Keiningham et al., 2024; Loos & Spraul, 2024). The call for marketing guidance of CSR decisions echoes a key message from the strategy literature that strategic marketing guidance is key for achieving sustained financial returns from firm initiatives because it coordinates processes and people across departments and directs their attention to the current and future demands of the firm environment (Feng et al., 2015). It also echoes recent findings that close marketing guidance enhances the firm-internal legitimacy of CSR executives and helps the CSR department to “gain maturity and . . . climb the organizational ladder” (Loos & Spraul, 2024, p. 19).

Exemplary Research on the Role of Marketing for the Effect of CSR Activities on Firm Performance.

Marketing can offer strategic guidance to CSR by informing CSR strategy formulation and CSR strategy prioritization. With respect to CSR strategy formulation, Table 1 shows that previous research streams have either provided insights on firm performance consequences of CSR efforts that distinguish between different stakeholders (e.g. Mishra & Modi, 2016) or between different relational approaches (e.g. Aksoy et al., 2022) but not both. With respect to CSR strategy prioritization, Table 1 also highlights that no study so far informs CSR managers on which CSR strategy they should focus on given a firm’s relative strategic emphasis in marketing (Vorhies & Morgan, 2003). Overall, there is an important gap in prior literature. Closing this gap requires a comprehensive framework that accounts for strategically different stakeholders, different relational approaches and how they align with strategic marketing goals. We conceptualize and test this framework next.

Theoretical framework

CSR strategy formulation

CSR strategy formulation draws on a marketing strategic extension of instrumental stakeholder theory. We first discuss the basics of instrumental stakeholder theory before we expand it through the lens of marketing strategy and formulate the focal CSR strategies.

A marketing strategy perspective on instrumental stakeholder theory. CSR comprises firm activities that relate to the firm’s perceived obligations toward stakeholders like customers, employees, local communities, environmental nonprofit organizations, and public interest groups (Kim et al., 2024). Stakeholder theory argues that a firm is a nexus of implicit or explicit relationships with these stakeholders. Addressing their expectations through CSR proves that the firm’s value system accounts for stakeholder welfare and social issues (Barnett, 2007). Stakeholders in turn develop more favorable associations with the firm, which translate into trusted stakeholder relationships (Sen et al., 2006). The strengthened stakeholder relationships pay off for the firm, because each of the stakeholders holds tangible or intangible resources that are relevant for the prosperity of its business (Barnett, 2007). Firms that systematically address stakeholder expectations gain privileged access to these resources, ultimately outperforming competitors who adopt a less systematic way to developing and maintaining stakeholder relationships (Homburg et al., 2013; Jones, 1995). However, identifying the right stakeholder groups and serving them with the right relational approaches is challenging.

We suggest that viewing the pillars of instrumental stakeholder theory through a market strategy lens is highly useful because it helps to specify stakeholder relationships through the clarification of two elements (Morgan et al., 2019). The first element of strategy formulation is to distinguish between stakeholder groups (Hillebrand et al., 2015; Hult et al., 2011). Different stakeholders are associated with different needs, interests, and unique resources that are critical for firms to survive (Barnett, 2007; Hillenbrand & Money, 2009). The core attribute to distinguish between stakeholders is whether their needs and resource entitlements are contractually formalized and thus can be directly enforced or not (Clarkson, 1995; Shapiro, 1987). Contractual formalization occurs when stakeholders engage in clearly defined market transactions with the firm. Customers, for instance, purchase the firm’s products (on the selling market) and employees enable the firm to produce and offer those products by providing their time and skills (on the labor market). These stakeholders are referred to as market stakeholders. In contrast, stakeholders such as local communities, public interest groups, and NGOs do not engage in contractually defined market transactions with the firm, so they exert influence via non-contractual relations. We refer to them as institutional stakeholders. 2

The second element of strategy formulation is to distinguish between approaches for building and maintaining relationships with these stakeholders (Aksoy et al., 2022; Lin-Hi & Müller, 2013). The most straight forward option is to contribute to stakeholders’ wellbeing which we term stakeholder promotion (Bolton, 2022; Mishra & Modi, 2016). It focusses on maximizing positive outcomes for stakeholders by addressing the firm’s responsibility to reciprocate to its stakeholders for their endorsement of the firm. While firms so far focus on maximizing positive outcomes for stakeholders, managers should also strive for reducing negative impact on stakeholders and society at large (Dacin et al., 2022; Rundle-Thiele, 2009). In particular, stakeholder protection refers to avoiding harmful events at all or minimizing the negative by-products of own business practices for stakeholders. Protecting stakeholder relationships is important because from the moment a company starts its business, negative externalities are likely to occur unless the company implements codes of conduct to avoid them and invests in corrective and mitigating actions (Acuti et al., 2024). A company that does not impose such measures risks generating profits at the expense of its stakeholders. While stakeholder promotion is intrinsically different from stakeholder protection, both are complementary in nature. While the former is often philanthropic and provides added value to stakeholders and society, the latter demonstrates accountability for firm’s own operations and liabilities by mitigating the negative impacts and thereby reduces reputational risks. Interestingly, prior research has overwhelmingly focused on stakeholder promotion (Lin-Hi & Müller, 2013). We are among the first to empirically account for stakeholder protection.

CSR strategies. Through combining stakeholder groups with relational approaches available, we propose four generic CSR strategies. Market stakeholder promotion refers to a firm’s contributions to the wellbeing of stakeholders that engage in contractually defined market transactions with the firm. Typical examples include superior quality of offerings, good union relations or a strong company pension scheme. Institutional stakeholder promotion describes contributions to the wellbeing of stakeholders who do not engage in contractually defined market transactions with the firm. Examples include charitable giving and human rights engagement in the supply chain. Market stakeholder protection refers to refraining from harming contractually related stakeholders. Firms that are strong in protecting their market relationships avoid, for instance, customer safety hazards, violation of customer privacy, and workforce downsizing. Institutional stakeholder protection means that the firm minimizes the harmful effects of own business practices for non-contractually related stakeholders. Examples are the avoidance of environmental harm through voluntary reduction of waste disposal and the continuous investment in preserving lively local communities in which the firm operates.

CSR strategy prioritization

Strategic-fit theory offers the theoretical foundation for CSR strategy prioritization. The key variable to prioritize CSR strategies is relative strategic emphasis in marketing. Thus, we first discuss strategic-fit theory and then define relative strategic emphasis.

Strategic-fit theory. While instrumental stakeholder theory helps in delineating stakeholder groups and relational approaches, even serving the right stakeholder groups with the right approaches is no guarantee for positive effects of CSR on financial performance. In this respect, strategic-fit theory (Moorman & Day, 2016; Vorhies & Morgan, 2003) emphasizes that effectively implementing firm initiatives involves aligning them with strategic marketing priorities. They represent the firm’s preference for an idiosyncratic value proposition that allows for a positional advantage in the marketplace through systematically building the required assets and capabilities (Morgan et al., 2019). Following strategic-fit theory, it is therefore imperative to match the genuine CSR strategies developed above with a firm’s strategic priorities in order to pay off. Only those combinations of stakeholder groups and relational approaches that fit with a firm’s marketing strategic priority have salutary effects on firm performance. A key variable to capture marketing’s strategic priority is relative strategic emphasis, which we discuss next.

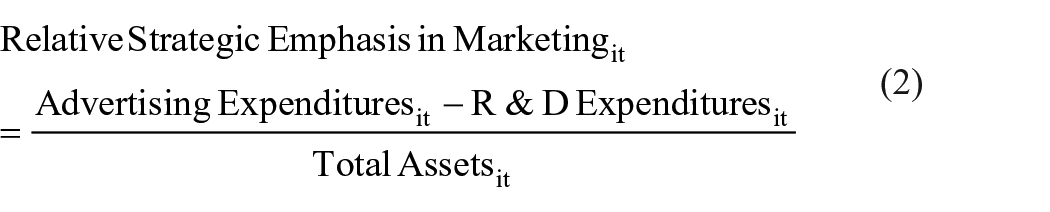

Relative strategic emphasis. Describing a firm’s strategic marketing priority, relative strategic emphasis is defined as marketing’s investment focus on assets for value appropriation versus assets for value creation (Han et al., 2017; Saboo et al., 2016). Value appropriation ensures the market’s appreciation of the firm’s offerings, for example through brand building in terms of high advertising spend (McAlister et al., 2016). Value creation, in contrast, is related to the development of superior offerings through innovation and typically reflected in relatively high R&D spend (Mizik & Jacobson, 2003). Relative strategic emphasis in marketing reflects that marketers invest in achieving both goals but budget constraints force them to trade off one for the other (Han et al., 2017). The continuum of relative strategic emphasis is anchored by a complete focus on value appropriation at the upper end and a complete focus on value creation at the lower end. Note that relative strategic emphasis does not capture operational investments by a firm in value appropriation or creation in absolute terms. Rather relative strategic emphasis does capture the strategic relevance of value appropriation versus value creation in relative terms.

Overview of conceptual framework

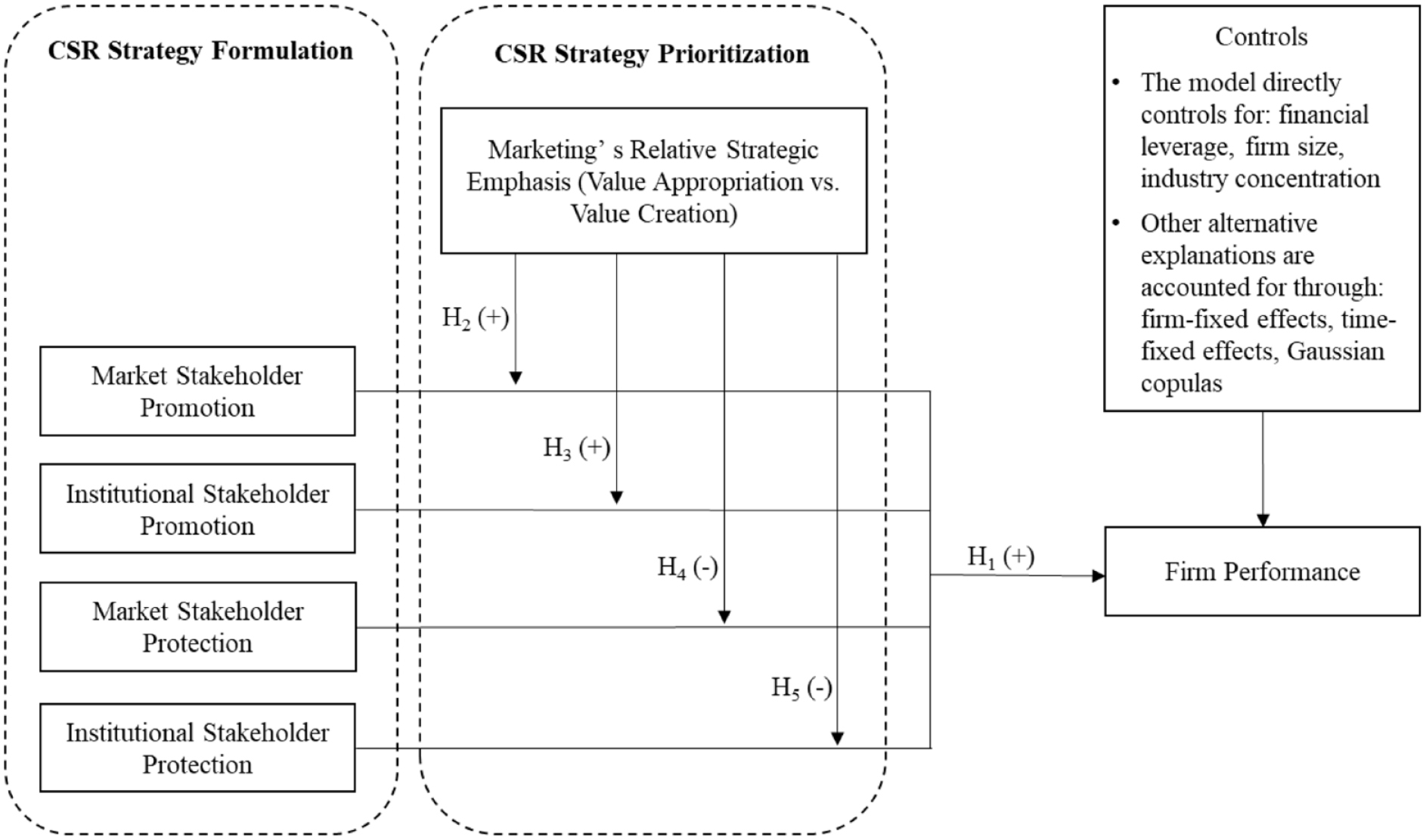

Figure 1 illustrates the novel marketing-strategy centered CSR framework proposed in this study. The framework addresses CSR strategy formulation by combining focal stakeholders (market or institutional) and relational approaches (promotion or protection) to derive a comprehensive set of generic CSR strategies rather than focusing on a selection of stakeholders or CSR tactics or using one aggregate CSR measure. The framework also accounts for the hypothesized effects of these CSR strategies on firm performance and the moderating role of marketing’s relative strategic emphasis for prioritizing the right CSR strategies. We next discuss the hypotheses summarized in the conceptual framework in detail.

Conceptual Framework.

Hypotheses

The effect of CSR strategies on firm performance

Instrumental stakeholder theory suggests that through engaging in CSR a firm invests resources into implicit and explicit relationships with a multitude of stakeholders (Sen et al., 2006; Sun et al., 2019). These investments demonstrate that the firm accounts for stakeholder welfare and social issues (Barnett, 2007). In turn, stakeholders build long-term and trusted connections with the firm, resulting in privileged access to resources at lower costs (Barnett, 2007; Sen et al., 2006). Since strong stakeholder relationships evolve over time, CSR is expected to pay off in the long term by influencing future cash flows and growth potential.

Stakeholder promotion transmits what the firm truly values by furthering the wellbeing of stakeholders and society. Stakeholder promotion presents an anthropomorphic picture of a firm that is characterized by gratefulness, generosity, and other-orientation, setting the firm apart from competitors and making stakeholders’ identification with the firm easier and more attractive (Godfrey et al., 2009; Homburg et al., 2013). In particular, market stakeholder promotion fosters customer and employee relationships. More loyal customers contribute to sales performance by paying premium prices, spreading word of mouth, and providing valuable feedback to improve current offerings (Srinivasan & Hanssens, 2009). Strong employee relationships motivate employees to help firms meet their objectives and serve to attract new talent (Schepers et al., 2012). Market stakeholder promotion eventually improves future cash flows, making the firm a better investment option and enhancing financial performance in the stock market.

Institutional stakeholder promotion leads to improved relationships with local communities, public interest groups and NGOs (for instance for human rights and environmental topics). These stakeholders are critical, for instance, in shaping policy makers’ view of the firm, facilitating access to regulatory resources, scarce information, preferential government endorsements, financial support for new ventures as well as the approval of new products, services, and facilities (Chen et al., 2022). By making business processes smoother through responding to topics important for society such as diversity and human rights, promoting the wellbeing of institutional stakeholders enables firms to drive financial performance in the long run.

As outlined above, we highlight that a firm’s long-term success should depend as much on preventing negative outcomes as on promoting positive outcomes. Reflecting efforts to prevent harmful events, market and institutional stakeholder protection denote compliance with stakeholder norms, emphasize the firm’s accountability, integrity, and fairness, and indicate that the firm is not opportunistically taking advantage of its stakeholders (Jones, 1995). Over time, relationship protection prevents stakeholder relationships from deterioration and hence safeguards fruitful future exchanges.

Market stakeholder protection in particular prevents customer relationship damage, creates a recurring stream of revenues from loyal customers and avoids excessive customer-acquisition costs. Similarly, preventing actions that erode employee relationships, such as inflating job demands and declining working conditions, reduces costs associated with low work performance, absenteeism, and turnover (e.g. Hancock et al., 2013). Market relationship protection hence becomes essential to secure and enhance the firm’s financial performance.

Institutional stakeholder protection maintains relationships with local communities, public interest groups, and NGOs. Mitigating harm to those stakeholders can be critical for overcoming resistance to firm initiatives (such as building a new factory) and concerns about the firm’s impact on broader society and natural environment (Chen et al., 2022). The risk for negative publicity triggered by those stakeholders, the mobilization of customers for boycotts and in turn reputational damage is decreased which ultimately benefits firm performance.

Hence, all else equal, we expect that CSR strategies enhance firm performance:

H1: There is a positive effect of (a) market stakeholder promotion, (b) institutional stakeholder promotion, (c) market stakeholder protection, and (d) institutional stakeholder protection on firm performance.

Using relative strategic emphasis to prioritize among the four CSR strategies helps to leverage their performance effects as we discuss next.

Moderating effects of relative strategic emphasis

Strategic-fit theory implies that firm’s CSR strategies regarding stakeholders cannot be viewed in isolation from the marketing assets and capabilities in place because they interact with stakeholder interests. For instance, focusing on more innovative products such as electric cars (i.e. when relative strategic emphasis is on value creation) may require the use of raw materials like rare earth metals or lithium that may be sourced under questionable human labor conditions. Hence, protecting market stakeholders (which include employees) may become critical for firm performance. More generally spoken, CSR strategies that fit with a firm’s strategic marketing priorities have more salutary effects on firm performance (De Jong & van der Meer, 2017).

In line with strategic-fit theory we argue that market stakeholder promotion and institutional stakeholder promotion are more effective in increasing firm performance when relative strategic emphasis is on value appropriation relative to value creation. This emphasis indicates that investments are primarily directed to enhance brand awareness and brand image (Currim et al., 2012), leading to synergies of market stakeholder promotion or institutional stakeholder promotion and relative strategic emphasis on value appropriation. CSR strategies related to market stakeholder promotion and institutional stakeholder promotion enfold greater positive impact on relationships with the same stakeholders and eventually firm performance because market and institutional stakeholders are more aware of the firm’s efforts, and they like to associate with strong brands (Tavassoli et al., 2014). Thus:

H2: Relative strategic emphasis on value appropriation (vs. value creation) increases the effect of market stakeholder promotion on firm performance.

H3: Relative strategic emphasis on value appropriation (vs. value creation) increases the effect of institutional stakeholder promotion on firm performance.

On the other end of relative strategic emphasis, firms focus on value creation relative to value appropriation (Currim et al., 2012). Firms on this end of the spectrum often focus on radical innovations which naturally entail a lot of change. For instance, customers have to learn about the usage of a new product, employees have to adapt to the requirements of producing changed offerings and local communities might be affected by the sourcing of raw materials or the construction of a new plant. Given that the consequences of the change stipulated by innovation may turn out to be positive or negative for stakeholders, relative strategic emphasis on value creation raises uncertainty among stakeholders about the further development of the firm and creates stakeholder alertness (Sorescu & Spanjol, 2008).

In this context, protective measures are particularly rewarded by stakeholders as they inform stakeholders about the reliability and trustworthiness of the firm (Acuti et al., 2024). Such protective measures reassure stakeholders that they are less likely to be worse off due to the changes triggered by innovation. For instance, when market stakeholders are relieved from product safety and working condition concerns when a new product has been introduced, they are more willing to act in the firm’s best interest in accepting and implementing change (Scarbrough & Moran, 1986). For dealing with institutional stakeholders such protective measures are also relevant because changes in firms’ core businesses often neglect the consequences they entail for society and the natural environment and therefore face resistance. Local communities, public interest groups or NGOs, for instance, energetically oppose changes they feel will breach their interests. Engaging with these stakeholders by demonstrating that the firm protects their interest helps to overcome resistance. As for a value creation focus protective CSR strategies are most effective, their deployment with a value appropriation focus should decrease firm performance. Hence:

H4: Relative strategic emphasis on value appropriation (vs. value creation) decreases the effect of market stakeholder protection on firm performance.

H5: Relative strategic emphasis on value appropriation (vs. value creation) decreases the effect of institutional stakeholder protection on firm performance.

Data and variables

Sample

We use data from the MSCI ESG Stats database (formerly known as KLD) to measure firms’ CSR efforts. Beginning in 1991, the database derives annual ratings on socially relevant outcomes from publicly available information on the majority of the largest publicly traded U.S. firms, representing all important U.S. industries. The ratings refer to clearly defined screening criteria, making them unbiased and objective and comparable across firms and industries over time (Groening et al., 2016). For these reasons, the database has become the de facto standard in empirical CSR research (Mattingly, 2017).

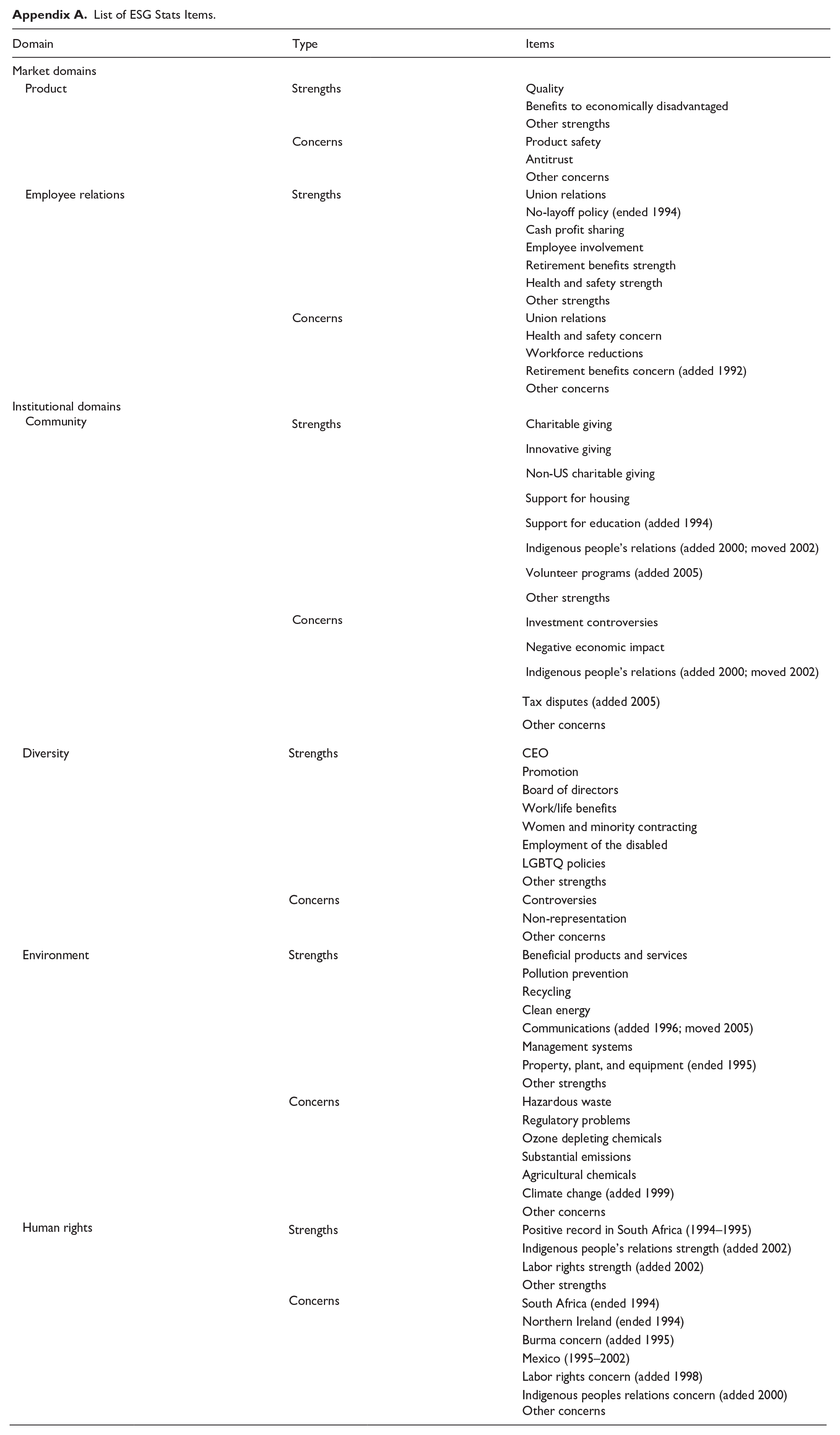

Importantly, the database provides detailed information on CSR efforts. ESG Stats measures CSR with multiple indicators that allow for differentiation between firms’ efforts to strengthen or protect relationships and cover the most important market and institutional stakeholder domains as we explain in greater detail below. We use the ESG Stats ratings from 1991 to 2009. To the best of our knowledge, this is the longest observation period that has been used so far (Lenz et al., 2017). We end the data collection in 2009 because the data provider made substantial changes to the inventory of indicators in 2010, which makes comparisons to prior years very difficult (Kang et al., 2016). However, we note that Eccles et al. (2019) have indicated that findings using more recent ESG stats data mirror findings using samples before the methodological changes were made (such as ours). Further, an additional advantage of the chosen sampling period is that it preempts the CSR bubble that has inflated after 2009 on the stock market (Bloomberg, 2024). Since our focal dependent variable (Tobin’s q) captures firm performance at the stock market, excluding this “boom cycle” from our sample removes the risk of overestimating CSR’s actual market value consequences and therefore offers a more conservative test of our hypotheses. The complete list of indicators used to construct the measures appears in Appendix A.

Further, to capture the remaining variables (relative strategic emphasis in marketing and firm performance as well as control variables), we match ESG Stats data with data from Compustat. After merging data from both sources and removing missing values (we do not remove any industries), we have a final sample of 3,572 firms and 21,481 observations. The average firm in our sample has 17,811 employees.

Variable construction

Firm performance. Following prior research (Jayachandran et al., 2013; Sun et al., 2019), we choose Tobin’s q as the dependent variable. As Tobin’s q reflects the stock market’s expectations regarding all sources of a firm’s future cash flows and growth, it accounts for the diverse ways CSR affects firm performance. It is also forward-looking, capturing CSR’s long-run impact, and it is not biased by accounting conventions, ensuring comparability across firms and industries (Anderson et al., 2004). In line with established practice (e.g. Jayachandran et al., 2013), we use Chung and Pruitt’s (1994) measure to capture the firm’s long-term financial performance, or Tobin’s q.

where i is the firm and t the respective year,

MVE = (closing price of share at the end of the financial year) x (number of common shares outstanding),

PS = liquidating value of the firm’s outstanding preferred stock,

DEBT = (current liabilities − current assets) + (book value of inventories) + (book value of long-term debt),

TA = book value of total assets.

We winsorize Tobins’s q at the 1st and 99th percentiles to avoid problems owing to outliers (Servaes & Tamayo, 2013).

CSR strategies. To construct the CSR strategy variables, we follow other studies and use the indicators from the product (customers), employee relations (employees), community (local communities), diversity (women, minorities, disabled, LGBTQ) as well as environment and human rights domains (NGOs, public interest groups; e.g. Flammer, 2015). ESG Stats provides binary coded strength and concern indicators for each of those domains. A rating of 1 indicates the presence and a rating of 0 the absence of the strength or concern. For instance, ESG Stats rates a firm’s health and safety accomplishments as strength in the employee relations domain. For this indicator, ESG Stats assigns 1 when the company has strong health and safety programs and 0 otherwise. For the retirement benefits concern in the employee domain, ESG Stats assigns 1 when the firm has either a greatly underfunded defined benefit pension plan or an inadequate retirement benefits program and 0 otherwise.

The information provided by ESG Stats allows adequate capture of the four generic CSR strategies. In line with prior research, we refer to product and employee relations domains to reflect the market stakeholder group, and community, diversity, environment, and human rights to reflect the institutional stakeholder group (Godfrey et al., 2009). Within each group we use the respective counts offered by ESG Stats to capture stakeholder promotion through social strength and stakeholder protection through the avoidance of social concern. To capture stakeholder promotion, we count all strength indicators rated 1 because a firm whose publicly observed behavior is rated as a strength has made significant investments to achieve social outcome. To measure stakeholder protection, we use ESG Stats’s concern indicators. A firm that invests more in avoiding undesirable social outcomes has fewer concern ratings, reflected in a higher number of zeros (Kang et al., 2016). Therefore, we count the concern indicators rated 0 to capture a firm’s efforts to protect stakeholders.

The number of indicators varies across domains and years, which means that the anchors of the four count variables are not readily comparable. To ensure measurement comparability we adapt a common scaling procedure (Servaes & Tamayo, 2013). For instance, for market stakeholder promotion, we scale the achieved number of strengths (i.e. the number of strength indicators that were rated 1) for the products domain and the employee relations domain by the maximum possible number of strengths within each of the domains in the respective year. We then sum the scaled domain-specific values. To account for the fact that the number of market domains differs from the number of institutional domains, we divide the sum of the scaled domain-specific values by the number of relevant domains.

Relative strategic emphasis in marketing. We capture relative strategic emphasis in marketing as the difference between advertising and R&D expenditures divided by the book value of total assets (Han et al., 2017; Mizik & Jacobson, 2003). Formally:

Positive values of this measure reflect the degree to which marketing focusses on value appropriation versus value creation. Negative values suggest that the emphasis is on value creation relative to value appropriation.

Control variables. We include financial leverage, firm size, and industry concentration as control variables. We account for financial leverage because it determines a firm’s flexibility in the event of unforeseen developments (Jayachandran et al., 2013). This flexibility could influence a firm’s ability to commit to CSR and may also directly affect financial performance. We measure financial leverage as the ratio of long-term debt to the book value of total assets (Han et al., 2017). Firm size is important to control for because it determines growth opportunities and therefore financial performance in the stock market while presenting more opportunities and choices to be made in terms of CSR. We operationalize firm size as the log of the number of assets (Bharadwaj et al., 1999). Finally, we also include industry concentration because it determines entry barriers and customer choice and therefore may not only call for less CSR but also influence financial performance directly (Groening et al., 2016). Industry concentration is operationalized as the Herfindahl index for each firm observation, using sales for all firms appearing in the Compustat database with the same four-digit SIC code (Lee & Grewal, 2004). Table 2 summarizes the measurement of the variables. Table 3 shows the descriptive statistics of the variables and correlations among them.

Measures.

Descriptive Statistics and Correlations.

Note. Correlations greater than or equal to |.014| are statistically significant (p < .05, two-tailed).

Modeling approach

Model specification

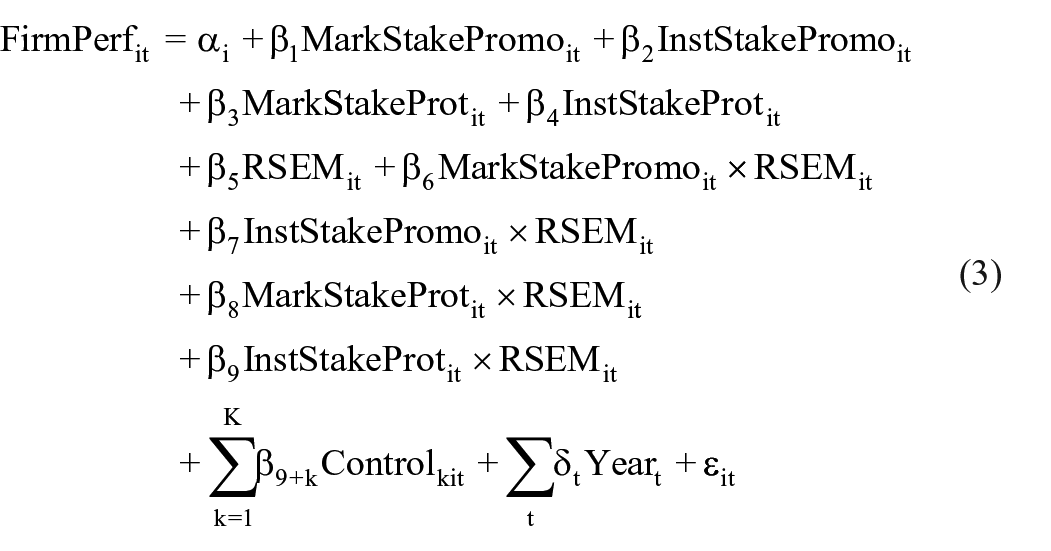

The model enables us to assess the main effects of the four CSR strategies on firm performance and their interactions with relative strategic emphasis in marketing along with the effects of control variables. We start with the following equation:

where i indicates the firm, t the year, and α is the intercept. FirmPerf is firm performance, MarkStakePromo is market stakeholder promotion, InstStakePromo is institutional stakeholder promotion, MarkStakeProt is market stakeholder protection, InstStakeProt is institutional stakeholder protection, RSEM is relative strategic emphasis in marketing, Control is a vector of control variables, Year denotes the time dummies that capture otherwise unobserved longitudinal heterogeneity (Groening et al., 2016), and ε is the residual component.

Model estimation

We estimate the model using the fixed effects estimator, because the fixed effects estimator captures unobserved time-invariant differences between firms, such as the firm’s industry, product and service categories, leadership styles, investment approaches, and other differences between firms (Steenkamp & Fang, 2011). We further estimate the model using cluster-robust error terms because both CSR and relative strategic emphasis in marketing may not vary extensively when they are repeatedly measured over time, potentially leading to an underestimation of the standard errors if they are not accounted for in the model (Cleeren et al., 2013).

Endogeneity correction

Firm- and time-specific factors may cause endogeneity, which we account for by including firm-fixed effects (via the fixed-effects estimator) and time-fixed effects (via year dummies) in the model. However, endogeneity of CSR efforts may also arise from other unobserved factors unique to a specific firm in a specific year that correlate with CSR efforts and firm performance but cannot be explicitly controlled for. For instance, a change in the executive board composition toward more talented members in a specific year could simultaneously affect the firm’s social and financial performance (Flammer, 2015).

We address this potential source of endogeneity through the Gaussian copula approach (Park & Gupta, 2012). This approach has gained popularity in marketing (e.g. Burmester et al., 2015) and CSR research (Lenz et al., 2017), because it is instrument-free and thus does not depend on the choice of strong instruments for the endogenous variables (Rossi, 2014). Gaussian copulas model the joint normal distribution of the endogenous variable and the error term to capture the dependence of both, which causes the endogeneity (Park & Gupta, 2012). We construct four Gaussian copula terms C_, one for each CSR strategy:

where

Results

Model specification tests

Before testing the hypotheses, we assess the appropriateness of the model specification. First, we test for discriminant validity and multicollinearity among the independent variables. Table 3 shows that the highest correlation is .44, which is well below .8 (Hair et al., 2010). Correlations among these variables are less than one by an amount greater than twice the respective standard error, providing evidence for discriminant validity (Bagozzi & Warshaw, 1990). A maximum variance inflation factor of 1.79, which is well below 5, indicates that multicollinearity is not an issue (Hair et al., 2010).

Next, we ensure that the fixed-effects estimator is appropriate. The Hausman test favors the fixed-effects estimator (χ2 = 450.30, p < .01) over the random-effects estimator.

Finally, we examine the usefulness of Gaussian copulas, which hinges on the non-normality of the endogenous regressors (Park & Gupta, 2012). The Shapiro-Wilk test confirms that non-normality applies to all four of them (

Model comparisons

Prior to calculating the interactions and estimating the model, we mean-center all continuous independent variables to facilitate interpretability (Aiken & West, 1991). As summarized in Table 4, we run four models. The effects of control variables are consistent across all models, intuitive, and in line with prior literature. We find negative and significant main effects of relative strategic emphasis in marketing (p < .05). Because a value creation emphasis (i.e. negative values of strategic emphasis) builds on the idea that current investments will pay off in the future, it aligns well with shareholders’ long-term perspective (Gupta et al., 2006). In contrast, a value appropriation focus (i.e. positive values of strategic emphasis) enhances short-term financial performance, potentially to the disadvantage of long-term financial performance (Josephson et al., 2016). We also find negative significant effects of financial leverage (p < .01; e.g. Jayachandran et al., 2013) and firm size (p < .01; e.g. Groening et al., 2016) on firm performance. We find no significant effects of industry concentration (p > .05; e.g. Servaes & Tamayo, 2013).

Model Results.

Note. Coefficients are unstandardized. RSEM = relative strategic emphasis in marketing. We estimate cluster-robust standard errors for the models without copula terms, and bootstrap standard errors with 200 repetitions for the models with copula terms (Burmester et al., 2015; Park & Gupta, 2012). R2 is based on within-firm variance. We also include two dummy variables that equal 1 if advertising (R&D) spending information is disclosed and 0 if that information is not disclosed (Luo & Bhattacharya, 2009).

p < .05. **p < .01 (two-tailed test).

Model 1a and Model 1b account for cross-sectional and longitudinal heterogeneity by including firm and year fixed effects. In Model 2a and Model 2b, we control for potential endogeneity of CSR strategies by incorporating copula terms. Comparing the models that contain the interaction effects between CSR strategies and relative strategic emphasis in marketing (Model 1b and Model 2b) with those that do not (Model 1a and Model 2a), we find that the adjusted R2 is higher when we include the interactions (Adj. R2Model 1b = 20.38% vs. Adj. R2Model 1a = 20.11%; Adj.R2Model 2b = 20.54% vs. Adj. R2Model 2a = 20.27%). However, the comparison between Model 1b and Model 2b suggests that the interaction effects, which are central for testing our hypotheses, are remarkably stable in terms of direction, significance, and magnitude, attesting to the important role that relative strategic emphasis in marketing plays for CSR’s effects on firm performance. As overall the model comparisons favor Model 2b, we ground the hypotheses testing on Model 2b.

Hypotheses testing

Table 4 (Model 2b) shows that none of the four CSR strategies directly enhances firm performance and hence we reject H1a-d. This finding is in line with arguments advanced by CSR skeptics that CSR is often financially ill-determined, as when the respective outcomes serve managers’ personal short-term goals more than the firm’s long-term strategy (Tang et al., 2018). Our results on the interaction effects outlined below show that this might be the case when managers ignore the value positioning set by strategic marketing priority. Hence, whether formulated CSR strategies pay off depends on their fit with strategic marketing goals.

Further, Table 4 (Model 2b) shows that the interaction effect of market stakeholder promotion and relative strategic emphasis in marketing on firm performance is not significant (β = 4.75, p > .05), leading us to reject H2. As a post hoc rationale, we propose that stakeholders in market domains may be relatively well informed about the firm and its existing offerings and have chosen to engage in close exchange based on that information. Thus, enhanced awareness evoked through a relative strategic emphasis on value appropriation also becomes less relevant for leveraging the effect of market stakeholder promotion on firm performance.

However, the effect of the interaction between institutional stakeholder promotion and relative strategic emphasis in marketing on firm performance is significant and positive (β = 12.54, p < .01), in support of H3. Stakeholders in institutional domains (e.g. NGOs and public interest groups) can help the firm to gain a competitive edge. However, these stakeholders often do not follow the firm’s CSR strategies closely. Therefore, for institutional stakeholder promotion to be associated with the firm and to evoke their beneficial effect on firm performance, a firm must differentiate itself from competitors so that institutional stakeholders gain awareness of firm’s CSR activities. Relative strategic emphasis on value appropriation builds this awareness.

Next, market stakeholder protection has a significantly more positive effect on firm performance when marketing’s strategic emphasis is on value creation, but correspondingly a more negative effect when the emphasis is on value appropriation (β = −3.55, p < .05), in support of H4. Market stakeholder protection helps to assure stakeholders in market domains that the firm sticks to the norms that govern the relationship and can be trusted. Since stakeholders in market domains arguably hold the most valuable resources of a firm, avoiding damage to these key relationships is crucial to preserving financial performance. Trusted relationships with market-related stakeholders become particularly important when marketing aims at change and innovation, as relative emphasis on value creation implies.

Finally, institutional stakeholder protection does not interact significantly with relative strategic emphasis in marketing (β = −3.67, p > .05). Hence, we reject H5. Institutional stakeholders may hold the view that, at minimum, firms should not make profits at the expense of the local community and society at large, no matter what their strategic marketing goal is. The result is that financial performance does not gain from stakeholders’ behavioral responses to institutional stakeholder protection.

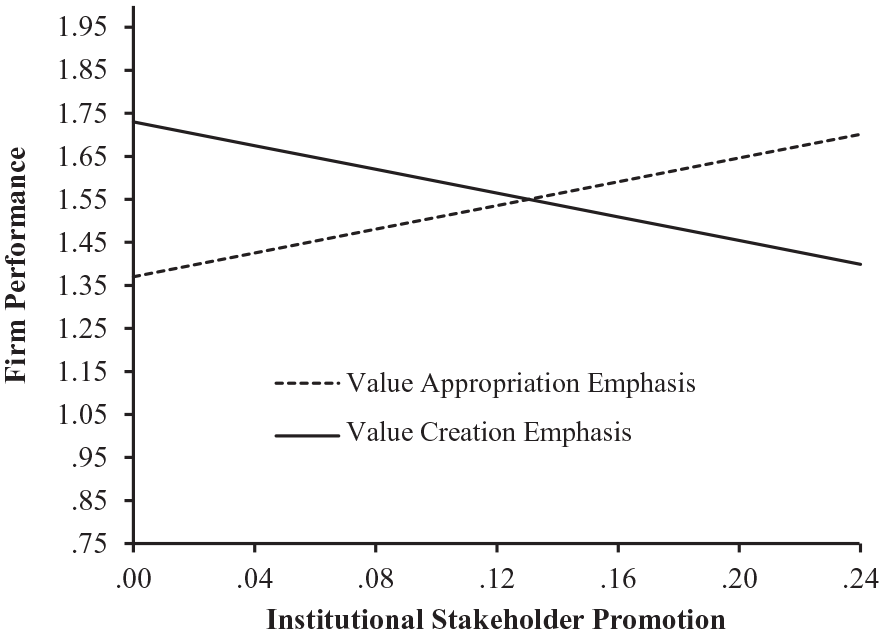

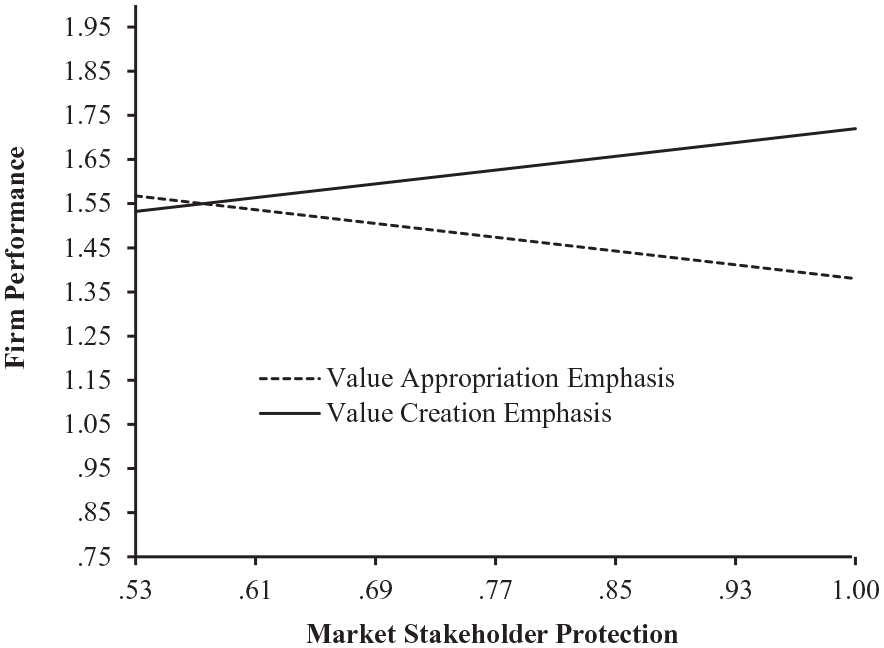

Illustrating the significant interaction effects, Figure 2 shows that institutional stakeholder promotion enhances firm performance when relative strategic emphasis is on value appropriation but reduces firm performance when the emphasis is on value creation. As shown in Figure 3, we find a negative effect of market stakeholder protection on firm performance when relative strategic emphasis is on value appropriation and a positive effect when the emphasis is on value creation. Overall, both figures underline that CSR strategy and marketing goals must intertwine for CSR to pay off.

Institutional stakeholder promotion has a positive (negative) effect on firm performance when relative strategic emphasis is on value appropriation (creation).

Market stakeholder protection has a positive (negative) effect on firm performance when relative strategic emphasis is on value creation (appropriation).

Discussion

This paper employs key principles of marketing strategy to foster CSR excellence. Our first research question was to distinguish between four CSR strategies that target focal stakeholder groups with different relational approaches and relate these CSR strategies to firm performance. The research reveals that only institutional stakeholder promotion and market stakeholder protection have the potential to affect firm performance. Addressing the second research question, we highlight that whether this potential materializes fully depends on their alignment with marketing’s relative strategic emphasis. Institutional stakeholder promotion leads to higher firm performance when relative strategic emphasis is on value appropriation but it lowers firm performance if the emphasis is on value creation. Market stakeholder protection, in contrast, leads to higher firm performance when relative strategic emphasis is on value creation but impairs firm performance when value appropriation is the dominant goal. These results show that close coordination between marketing strategy and CSR is key for achieving returns on CSR strategies.

Implications for research

Distinguishing between target stakeholders and relational approaches matters. In line with prior calls (Lenz et al., 2017), we introduce a theoretically founded framework of CSR strategies by drawing on marketing strategy insights. The theoretical framework offers a seamless connection between the intertwined but previously disconnected thought worlds of CSR and marketing strategy. The framework distinguishes between stakeholder groups (market vs. institutional stakeholders) and relational approaches designed to address stakeholder needs (stakeholder protection and stakeholder promotion).

Coordinating CSR with marketing strategy pays off. While prior research often views marketing strategy and CSR as mutually exclusive (Banerjee & Wathieu, 2017; Luo & Bhattacharya, 2009), we show that integrating both is key. The findings demonstrate how a marketing strategy mindset can serve CSR efforts to become financially sustainable and thus elevate their acceptance within the firm, extending a nascent stream of research that highlights “a strategic recall of CSR” as a means for aligning societal and firm wellbeing (Bolton, 2022; Fatima & Elbanna, 2023; Rosenbloom, 2022). We also offer empirical evidence for the recent conceptual reasoning (Keiningham et al., 2024) that creating a fit between CSR and marketing-strategic priorities might be a means for boosting CSR’s impact on firm performance. By doing so, we showcase a new application context for strategic-fit theory which so far has never been applied to CSR decision making.

Theory triangulation helps to understand the relationship between CSR and firm performance. The findings contribute to the resolution of the ongoing theoretical dispute about the link between CSR and financial performance. Instrumental stakeholder theorists propose that CSR helps to build important relationships with stakeholders and getting access to important resources, thus generally benefiting financial performance (Jones, 1995). However, our finding that CSR effects can turn negative (if not aligned with relative strategic emphasis in marketing) echoes arguments from agency theorists that if CSR fails in creating fit with marketing goals, a CSR strategy comes with costs that impair financial performance and become a liability to the firm (Wright & Ferris, 1997). In the case of a misfit, CSR performance and financial performance are opposing goals, creating a paradoxical situation that calls for the prioritization of one goal over the other. By capitalizing on marketing strategy thinking, we advance instrumental stakeholder theory by highlighting that not all CSR strategies for serving stakeholders pay off for the firm (as in the case of “paradoxical” CSR strategies) and which strategy is most effective for each stakeholder group. By doing so, we help reconciling equivocal theoretical perspectives on CSR, a longstanding challenge in CSR research.

Implications for practice

Depending on the focal stakeholders, the promotion or the protection of their wellbeing matters most. We recommend that managers refrain from making generalizations about CSR. Rather, managers should distinguish CSR strategies as to whether they address market-related or institutional stakeholders and whether they promote positive outcomes for stakeholders (“doing good”) or protect them from negative outcomes (“avoiding bad”). When targeting institutional stakeholders, a more offensive CSR strategy in terms of promoting their wellbeing should be key while a more defensive strategy in terms of protecting relationships should be chosen when market stakeholders are the target. Strikingly, most firms in the sample fail in getting this targeting right in that they underperform in terms of institutional stakeholder promotion (55%) and do not succeed in protecting market stakeholders (61%).

Only specific combinations of CSR strategies and marketing’s relative strategic emphasis pay off financially. In our sample, alarmingly, 71% of all firms have misaligned CSR strategies with relative strategic emphasis set by the marketing function, at least when high financial performance of CSR is the gauge. Fortunately, firms increasingly start to conduct materiality analysis in order to identify which strategic CSR topics are relevant for important stakeholders given the firm’s current market positioning (Havlinova & Kukacka, 2023). Our findings reveal two combinations between CSR strategy and relative strategic emphasis in marketing that are most likely to pay off financially. Protecting market stakeholders preempts uncertainties regarding a firm’s potential negative externalities when the firm’s marketing program emphasizes value creation. An emphasis on value creation comes with continuous or even disruptive change through innovation driving uncertainty of market stakeholders such as customers and employees. In contrast, investments in promoting the benefits of institutional stakeholders yield financial rewards particularly for firms that focus on value appropriation as this increases stakeholders’ awareness and appreciation of the firm and its good deeds. We note that the results should not be misinterpreted as a recommendation to neglect market stakeholder promotion and institutional stakeholder protection. But the results suggest that they do not have direct implications for firm performance.

Pressuring firms to indiscriminately engage in CSR fires back. Our results also suggest that the recent trend, whereby firms are pressured to adopt CSR in an almost unreflective manner (Foss & Klein, 2023; Holger, 2020), is worrisome because it may lead firms to create dissynergies between CSR and marketing that harm their financial performance in the long-run and therefore undermines their ability to contribute to society, for example, through jobs and taxes.

This has implications for policy makers, shareholders, and firms. Public policy makers should create rules preventing firms from discriminating between other firms solely based on CSR considerations when they offer their products and services. Large shareholders who increasingly become CSR activists should ask themselves if they are willing to walk the talk (i.e. accept lower rather than higher returns for some enforced CSR investments). Shareholders who do not aim to become activists could consider shifting their capital from companies in industries that are prone to be pressured into CSR investment that mismatch their marketing strategy to firms in industries in which this scenario is less likely to occur (Henriques & Sadorsky, 2018). Finally, firms should consider that adopting CSR measures in an unreflective manner may be myopic. If a firm adopts CSR strategies that misfit with marketing strategy resulting in them being financially harmful to the firm, the firm’s ability to fulfil their roles as a value provider for customers, employees, and shareholders may suffer in the long-term.

Limitations and future research

The MSCI ESG Stats database is arguably the best secondary data available in terms of (a) the time period the data are available, (b) the distinction between manifold stakeholders, (c) the distinction between CSR strengths and concerns, and (d) the level of detail. No other secondary data source of similar scope yields similar advantages and would be able to capture different CSR approaches and distinct stakeholder groups as comprehensively which is necessary to device different CSR strategies. However, the database also entails some limitations for this study that offer avenues for future research.

For instance, the database only rates CSR efforts of U.S. firms. Some international stakeholders such as suppliers are not explicitly considered in the ratings, even though the human rights domain represents issues and risks that arise in global supply chains. In order to more firmly embed CSR in all firm functions, future research should scrutinize how to trigger CSR decision makers to closely coordinate not only with marketing strategy but also with supply chain management strategy and internationalization strategy. Broadening the participation in CSR decisions to a more diverse group of executives has been suggested to enhance firm resilience (Wieland et al., 2023). The database also relies on CSR analysts to collect information on specific aspects of CSR, which implies that some aspects may have been overlooked. For instance, future research could explore whether different types of analysts (e.g. stock or security analysts) rate CSR strengths and concerns differently. Another limitation of the data set is that the binary indicators adopted by the rating do not account for the intensity of each individual CSR activity (though on a domain level we consider the number of CSR activities a good approximation of CSR intensity in that domain). Doing so would require future research to capture CSR activities on a continuous rather than a binary scale. One potentially promising way to conduct these future studies could be to complement existing secondary CSR data with data collected via digital media listening and analytics tools to represent a broader “buzz” about a firm’s activities (Boegershausen et al., 2022).

Overall, the paper paves the way for the marketing strategic guidance of CSR in order to reconcile CSR performance with financial performance for a more sustainable future. The study’s results empower the marketing function to become an advocate for all stakeholders and society at large.

Footnotes

Appendix

List of ESG Stats Items.

| Domain | Type | Items |

|---|---|---|

| Market domains | ||

| Product | Strengths | Quality |

| Benefits to economically disadvantaged | ||

| Other strengths | ||

| Concerns | Product safety | |

| Antitrust | ||

| Other concerns | ||

| Employee relations | Strengths | Union relations |

| No-layoff policy (ended 1994) | ||

| Cash profit sharing | ||

| Employee involvement | ||

| Retirement benefits strength | ||

| Health and safety strength | ||

| Other strengths | ||

| Concerns | Union relations | |

| Health and safety concern | ||

| Workforce reductions | ||

| Retirement benefits concern (added 1992) | ||

| Other concerns | ||

| Institutional domains | ||

| Community | Strengths | Charitable giving |

| Innovative giving | ||

| Non-US charitable giving | ||

| Support for housing | ||

| Support for education (added 1994) | ||

| Indigenous people’s relations (added 2000; moved 2002) | ||

| Volunteer programs (added 2005) | ||

| Other strengths | ||

| Concerns | Investment controversies | |

| Negative economic impact | ||

| Indigenous people’s relations (added 2000; moved 2002) | ||

| Tax disputes (added 2005) | ||

| Other concerns | ||

| Diversity | Strengths | CEO |

| Promotion | ||

| Board of directors | ||

| Work/life benefits | ||

| Women and minority contracting | ||

| Employment of the disabled | ||

| LGBTQ policies | ||

| Other strengths | ||

| Concerns | Controversies | |

| Non-representation | ||

| Other concerns | ||

| Environment | Strengths | Beneficial products and services |

| Pollution prevention | ||

| Recycling | ||

| Clean energy | ||

| Communications (added 1996; moved 2005) | ||

| Management systems | ||

| Property, plant, and equipment (ended 1995) | ||

| Other strengths | ||

| Concerns | Hazardous waste | |

| Regulatory problems | ||

| Ozone depleting chemicals | ||

| Substantial emissions | ||

| Agricultural chemicals | ||

| Climate change (added 1999) | ||

| Other concerns | ||

| Human rights | Strengths | Positive record in South Africa (1994–1995) |

| Indigenous people’s relations strength (added 2002) | ||

| Labor rights strength (added 2002) | ||

| Other strengths | ||

| Concerns | South Africa (ended 1994) | |

| Northern Ireland (ended 1994) | ||

| Burma concern (added 1995) | ||

| Mexico (1995–2002) | ||

| Labor rights concern (added 1998) | ||

| Indigenous peoples relations concern (added 2000) | ||

| Other concerns | ||

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project was funded by the German Research Foundation (Deutsche Forschungsgemeinschaft; grant number: 258935253).