Abstract

Tax and spending are central to democratic politics in the United Kingdom and elsewhere, but psephologists have paid surprisingly little attention to the practice of manifesto costings or the ways in which fiscal promises shape voting behaviour. This article uses qualitative research to trace how British parties have used manifesto costings to frame prospective choices for voters since the 1950s and develops a theoretical framework for understanding why warnings about ‘tax bombshells’ and ‘black holes’ in parties’ spending plans seem to be so powerful in Britain. The article suggests that the emphasis which governments have placed on budgetary constraints since the 1976 International Monetary Fund (IMF) crisis may help explain the long electoral cycles the United Kingdom has experienced in recent decades. Whereas retrospective economic evaluations can be difficult for governments to control, forward-looking fiscal debates are structurally weighed towards incumbent parties and offer a powerful way for incumbents to offset the ‘costs of governing’.

Keywords

Introduction

The 2019 UK general election is likely to go down in history as the ‘Brexit election’, in which the Conservative victory reflected the appeal of Boris Johnson’s pledge to ‘Get Brexit Done’, but an important subsidiary strand of the Tory campaign involved a robust and familiar attack on the Labour Party’s spending plans. In an appearance on the BBC’s Andrew Marr Show on 10 November, the Chancellor of the Exchequer, Sajid Javid, unveiled a dossier on The Real Cost of a Labour Government which claimed that Jeremy Corbyn would spend an extra £1.2 trillion over five years – equivalent to a ‘£2,400 tax bill for every household’. Although Labour dismissed the dossier as a ‘work of fiction’ and insisted that it would not raise taxes on workers with incomes below £80,000 a year, the Tory figure received wide media coverage (Wickham, 2019) and brought back memories of the ‘tax bombshell’ campaign which John Major had deployed to devastating effect in the 1992 election. In stark contrast to 2017, when Corbyn’s plans to tax the rich and scrap university tuition fees seemed to resonate with many voters, discussions of Labour’s 2019 policy agenda were dominated by questions of affordability. Promises to provide free full-fibre broadband by 2030 (at a cost of at least £20 billion) and to pay compensation to the ‘WASPI women’ affected by the rise in the state pension age (estimated at £58 billion over five years) were particularly contentious. Peter Kellner and Patrick Loughran (2019: 23), who carried out focus groups in Bishop Auckland, Walsall, and Worksop, concluded that ‘a constant refrain of “Where is the money coming from?” underpinned the electorate’s disbelief in the credibility of Labour’s spending programme’.

Tax and spending plans are central to election campaigns in Britain and around the world, as qualitative studies (such as the Nuffield series on UK general elections) have frequently shown. In Britain, parties have repeatedly ‘made the tax system, its fairness or otherwise, and the threat of tax increases or the promise of reductions, a prominent campaign issue’ (Johnson et al., 2005: 394), and the publication of detailed ‘costings documents’ can be seen as the culmination of a century-long trend towards an increasingly programmatic form of electoral competition, as David Thackeray and Richard Toye (2020) have recently noted. To date, however, the issue of policy costings has received surprisingly little attention from political scientists. The detailed analysis of manifestos pioneered by the Manifesto Research Group has focussed on the words rather than the numbers, using language to identify parties’ ideological positions (Budge et al., 2001), policy pledges (Thomson et al., 2017), and appeals to social groups (Thau, 2019) without much reference to the quantitative dimension of these programmes. Likewise, the influential literature on ‘valence politics’ has largely focussed on retrospective evaluations of economic performance, building on the classic reward/punishment model of economic voting (Duch and Stevenson, 2008; Goodhart and Bhansali, 1970). Although retrospective evaluations are important, election campaigns are also forward-looking contests in which parties ask voters to choose between competing programmes. Gordon Brown (2017: 165), for instance, thought it was axiomatic that ‘elections are won not as a reward for what you did in the past but on how voters see their prospects in the future’.

This article seeks to establish a framework for understanding the electoral politics of fiscal policy by reference to a case study of UK general elections from 1955 to 2019. It uses qualitative research to trace the origins of the Conservative Party’s ‘tax bombshell’ strategy and to explore how the practice of manifesto costings has shaped British electoral politics over the last 65 years. The empirical analysis suggests (1) that prospective choices over fiscal policy have been a major focus of debate in most British elections since the 1950s, (2) that this frame has been particularly cultivated by incumbent parties, and (3) that parties have sought to use policy costings not only to appeal to voters in a narrow ‘pocketbook’ way but also to shape wider perceptions of governing competence. Although these claims may seem modest, they have potentially far-reaching implications. For instance, Jane Green and Will Jennings (2017: 196, 249) have recently argued that governments’ reputation for competence generally weakens over time as ‘negative performance information accumulates’, creating ‘common governing cycles in popularity’ which are only partly under the control of political actors. One way in which British governments have offset these ‘costs of governing’ is by focussing voters’ attention on future policy choices and pressing the opposition to show how it would pay for its promises.

The article develops this argument in five steps. The first section situates the argument in the electoral studies literature and develops a theoretical justification for studying the framing of tax and spending proposals. The second section sketches out a preliminary framework for understanding variations in the nature and salience of fiscal promises: why do debates over tax and spending plans seem to play out differently in some contexts than others? The third and fourth sections trace the history of manifesto costings in Britain from the 1950s to the 1990s, showing how the Conservative Party’s relentless warnings of a ‘tax bombshell’ shaped the dynamics of electoral competition, and how Labour sought to demonstrate its fiscal competence in opposition and turn the tables on the Tories in office. A fifth section brings the analysis up to the present by exploring how the politics of tax, spending, and borrowing has evolved since 1997. Both Gordon Brown and George Osborne were aggressive practitioners of fiscal statecraft, using fiscal rules to ‘depoliticise’ their policy choices and draw ‘dividing lines’ with the opposition. Although public support for austerity seems to have waned in recent years, the success of the Conservatives’ 2019 campaign suggests that traditional concerns about taxation and public borrowing continue to resonate with many voters. The conclusion draws out the implications of this study for our understanding of party strategy and identifies possible avenues for further research.

Fiscal policy and electoral choices

Political economists in the Downsian tradition have long seen elections as a prospective choice in which voters seek to maximise their expected utility through a rational evaluation of party programmes. In particular, Allan Meltzer and Scott Richard (1981) took Anthony Downs’ (1957) model of prospective egocentric voting as the starting point for their ‘rational theory of the size of government’. Although Downs’ median voter model has been widely used to explain party strategy, however, psephologists have increasingly emphasised the unreality of its assumptions – noting, for instance, that most voters do not have well-defined policy preferences (Stokes, 1963) and lack the inclination or information to make rationalistic choices (Achen and Bartels, 2016). At best, voters use ‘heuristics’ to judge politicians’ competence and hold them accountable for performance.

The valence politics literature has particularly stressed the importance of leaders’ images, performance evaluations, and ‘issue ownership’ in shaping voters’ decision-making (Sanders et al., 2011). Subjective economic experiences and perceptions of competence feature prominently in this framework (Whiteley et al., 2013). The prevailing emphasis on retrospective voting has also carried over into policy studies through R. Kent Weaver’s (1986) seminal analysis of ‘the politics of blame avoidance’. As a result, much of the literature on the politics of fiscal policy has been state-centred, focussing on the ways in which governments seek to minimise the risk of an electoral backlash against tax increases or spending cuts (Hood and Himaz, 2017; Pierson, 1994).

Despite the abstractions involved in Downsian theory, there are compelling reasons for taking the prospective dimension of electoral choice seriously, as some political scientists have recognised. David Sanders (1991, 1999), for instance, found that voters’ expectations of how their personal finances would change over the next 12 months correlated closely with UK party support during the 1980s and 1990s: indeed, these ‘egocentric prospective’ views of the economy appeared to be more important than retrospective or national-level economic evaluations. Likewise, Richard Nadeau et al. (1996: 258) have argued that ‘voters’ assessments of party leaders are comparative and prospective rather than individual and retrospective’, a claim which they justify by reference to UK polling data. As Nadeau et al. point out, ‘election campaigns by their very nature are centred on what parties and leaders will do in the future’, and past performance is mainly ‘relevant in so far as it is a predictor of the future’, not ‘for its own sake’.

Within a prospective frame of analysis, fiscal promises are likely to be salient to voters for two main reasons. First, the differences between parties’ attitudes to tax and spending are often clearer than differences over economic management (Stigler, 1973), and their impact on voters’ personal finances is likely to be easier to predict and evaluate. In an open capitalist economy, the relationship between economic policy and disposable income is complex and subject to many intervening variables, such as corporate strategies, exchange-rate movements, and the business cycle; by contrast, tax and spending proposals are much more tangible. As Ivor Crewe (1981: 285) has pointed out, a promise of income tax cuts ‘is as clear, tangible, and accountable a campaign commitment as a party can make’. Indeed, incoming British governments have often held an early budget or mini-budget (as in 1964, 1974, 1979, 1997, 2010, and 2015) to deliver on their promises and set new spending priorities.

Second, a party’s fiscal plans may act as a proxy for economic competence more broadly by shaping perceptions of its ability to govern. The idea that governments need to ‘balance the books’ has long been part of lay economic discourse, and conservative politicians have repeatedly warned that deficits will cause inflation and economic instability (Blyth, 2013). In a globalised world economy, fiscal credibility is also tied up with the need to reassure financial markets of the government’s credit-worthiness, in order to avoid the threat of a gilt strike or currency crisis (Hay, 2001). At a deeper level, gaps in a party’s costings evoke the age-old fear that democracy will degenerate into a bidding war, in which parties compete to deliver benefits to client groups and/or make promises which they cannot fulfil. Alongside their immediate financial implications, then, tax and spending proposals may act as a heuristic which helps voters judge parties’ larger economic credentials. Parties must weigh the desire to bid for votes through ‘retail policies’ with the need to reassure voters about their credibility.

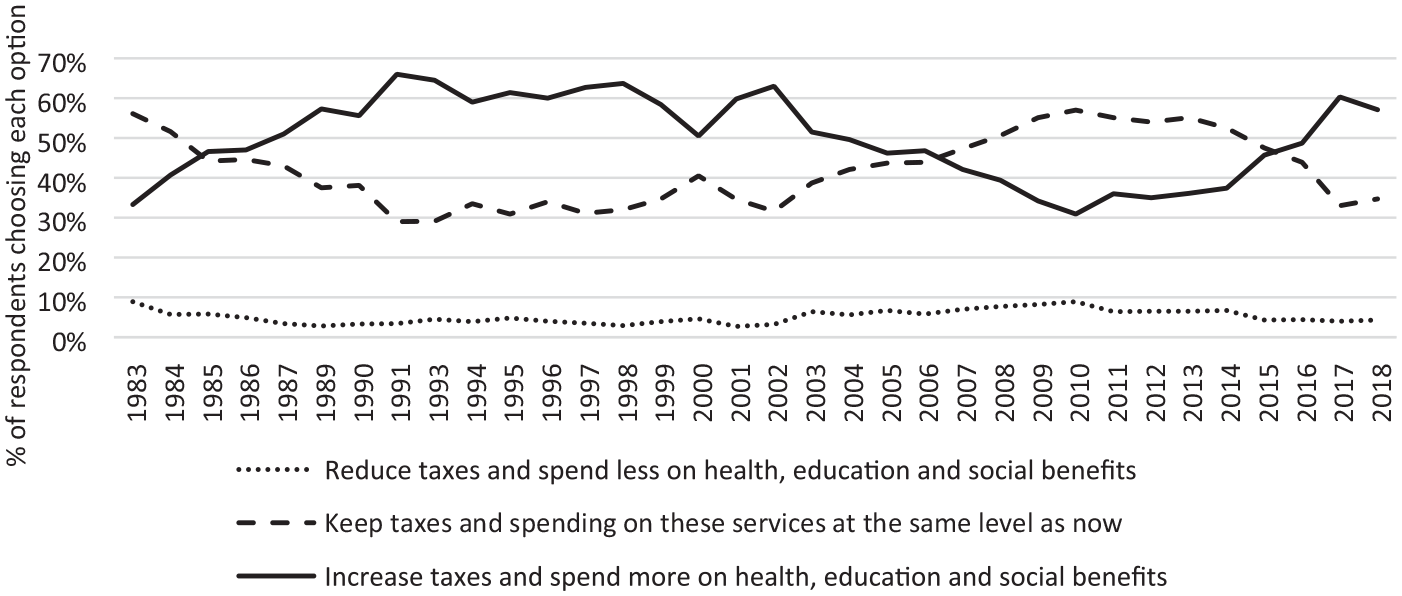

If most voters engage in a ‘rough and ready’ analysis of party programmes rather than a fully fledged assessment of expected utility, then the framing and communication of fiscal plans is extremely important. Even in a developed country such as the United Kingdom, public understanding of tax appears to be relatively poor (Gemmell et al., 2004), and widespread support for the general principle of raising taxes to improve public services (as shown by the British Social Attitudes Survey data in Figure 1) has not always been reflected in voters’ behaviour at the ballot box (Taylor-Gooby and Hastie, 2003). The political psychology literature suggests that voter choices are likely to be shaped by framing effects (which link proposals to prior beliefs, values, and symbols), priming effects (which influence the salience of different policy issues), and a well-documented tendency towards status-quo bias and loss-aversion (Chong and Druckman, 2007; Kahneman, 2011). Warnings of higher tax bills or cuts to public services are particularly well placed to achieve ‘cut-through’ with voters, especially if they are framed in simple terms and amplified by media coverage.

Public attitudes to taxation and government spending on health, education and social benefits, 1983–2018.

When and how do fiscal promises matter?

There is a strong theoretical rationale, then, for seeing tax and spending plans as an important influence on voting behaviour, which can be understood either in the narrow sense of prospective ‘pocketbook voting’ or in broader and less rationalistic ‘valence’ terms. Yet fiscal policy is hardly the only factor that determines voters’ choices; rather, it intersects with social values, group identities, and other policy issues in a complex and iterative process. Why, then – we might ask – does fiscal policy seem to matter more in some contexts than others, and when does Downsian ‘retail politics’ give way to a focus on the cost and credibility of parties’ promises? The comparative politics literature suggests three broad hypotheses.

First, fiscal policy is likely to be more salient to voters where the budgetary process is centralised and clarity of responsibility is high. Westminster systems such as the United Kingdom stand out in both respects, as Sven Steinmo (1993) and G. Bingham Powell (2000) have noted. Under a responsible party model of representation, elections function as collective ‘decision points’ where ‘agendas are aggregated and priorities are established’ (Bevan et al., 2011: 395), and governments can introduce radical changes to tax and public service provision on the basis of a relatively narrow majoritarian ‘mandate’ (Iversen and Soskice, 2006); indeed, manifestos have taken on a quasi-constitutional status in Britain as a result of the ‘Salisbury convention’. High levels of prospective fiscal voting might also be found in proportional representation systems where well-established right- and left-wing blocs alternate in government, such as Denmark and Sweden, since the bloc structure allows voters to carry out ex ante evaluation of prospective governing programmes (Anderson, 2000; Zohlnhöfer, 2017). By contrast, in presidential regimes (like the United States) and ‘consensus democracies’ with fluid and fragmented party systems (such as the Netherlands), the large number of ‘veto players’ in the budgetary process means that voters have less reason to take parties’ proposals at face value. Instead, the manifesto or platform is more like an opening bid in negotiations with legislators or potential coalition partners.

Second, voters are likely to take fiscal constraints more seriously when their governments take them seriously. As Jim Tomlinson (2017) has shown, the public’s understanding of ‘the economy’ is structured by elite narratives – about employment, productivity, debt, ‘fairness’, and so on – which have changed over time in response to new economic ideas, political priorities, and policy problems. In the United Kingdom and other western states, prevailing attitudes to budgetary balance have passed through three broad phases over the last century, from the Gladstonian preoccupation with ‘sound finance’, through the ‘high Keynesian’ era in which fiscal policy was primarily (though never only) a tool of macroeconomic management, to a renewed awareness of fiscal constraints since the mid-1970s in the context of globalisation and financial deregulation (Buggeln et al., 2017; Streeck, 2017). We might expect public concern about deficits and debt to have followed a similar U-shaped trajectory. Within this stylised picture, there is also scope for considerable variation between states: for instance, fiscal constraints are likely to be particularly pressing where governments are committed to fiscal compacts (such as the Eurozone’s Stability and Growth Pact) or vulnerable to sovereign debt crises (Nyblade and O’Mahony, 2014).

Third, voters’ responses to tax and spending proposals are likely to depend on their underlying attitudes towards government activity. These ‘redistribution preferences’ can be modelled in rational choice terms, as in the Meltzer-Richard model, but in practice they are also shaped by voters’ experiences of tax and public services. The structure of tax collection and welfare provision is likely to play an important role here: for example, the British tax system contains a number of features – such as the collection of income tax through Pay-As-You-Earn and the inclusion of VAT in retail prices – which reduce the political salience of taxation (Gamage and Shanske, 2011), whereas the US system makes people more aware of the tax they are paying and so, perhaps, more responsive to tax resistance movements. Stuart Soroka and Christopher Wlezien (2005) have also found that changes in government policy tend to produce a ‘thermostatic’ response in public opinion. When the tax burden rises, complaints about ‘wasteful’ government activity gain traction with voters; when the quality of public services falls, citizens are more receptive to proposals for spending and investment. As the intensity of voters’ desire for tax cuts or spending increases grows, we might expect these positional preferences to become more salient, so that the desire for change eventually outweighs concerns about the cost and credibility of opposition policies.

In any given situation, of course, the reception of fiscal promises is likely to reflect a complex interplay between these different factors, and the fact that voters have agency makes election results intrinsically unpredictable. Parties’ attempts at framing fiscal choices will sometimes work and sometimes not. Retail policies do not always find a market; ‘tax bombshells’ do not always go off.

Inventing the ‘tax bombshell’, 1955–1964

Within this analytical framework, the United Kingdom stands out as a highly centralised Westminster democracy with an adversarial culture, in which fiscal debates are central to election campaigns and parties are routinely expected to ‘cost’ their policies. It can hardly be seen as a representative case study, but the rich literature and archival material available on British elections allow us to trace how fiscal promises have been made by parties and received by voters in some detail. As a first step towards a comparative analysis, the next three sections of this article explore how the practice of manifesto costings has shaped UK party strategy since the 1950s. The historical narrative sketched out here is necessarily selective; more detailed versions can be found in Sloman (2019) and Davies and Sloman (2020), and the costings published by the two main parties at each election are summarised in the Online Appendix.

Tax and spending have always featured prominently in British electoral politics. During the 19th and early 20th centuries, however, programmatic competition was restrained by the tradition of ‘Treasury control’, which established budget-making as a strict Treasury prerogative (Peden, 2000: 6–11). Indeed, one of the purposes of the gold standard and the Gladstonian emphasis on ‘sound finance’ was to insulate the budgetary process from democratic pressures (Daunton, 2001). Where elections were fought over budgetary issues, they generally focussed on fiscal policies which had already come before Parliament (such as the 1846 repeal of the Corn Laws, or David Lloyd George’s 1909 ‘People’s Budget’) rather than hypothetical tax and spending plans. Opposition parties tended to confine themselves to general principles instead of setting out proposals in detail, and the most famous departures from this norm – Joseph Chamberlain’s 1903–1906 tariff reform campaign and the Liberal Party’s 1929 proposal to ‘conquer unemployment’ through public works – were notably unsuccessful. As late as 1950, Winston Churchill (1950) argued that taxation was ‘a matter which should be studied by the Chancellor of the Exchequer, and not a subject for an election campaign’. Under Churchill’s leadership, the Conservatives would not publish ‘detailed rigid programmes’, or ‘try to get into office by offering bribes and promises of immediate material benefits to our people’ (Churchill, 1949).

These restraints on fiscal competition weakened in the 1950s, as British electoral politics became increasingly programmatic. In the context of sustained economic growth and closely fought elections, the parties competed to deliver rising living standards and new forms of welfare provision. The Conservatives set the pace in 1951 by setting out plans to build 300,000 houses a year, and Labour hit back in 1955 and 1959 by attempting to outbid the Tory government on pensions. In 1959, for instance, Labour promised to raise the basic state pension immediately to £3 a week (a 20% increase) and eventually provide ‘half-pay on retirement for the average wage-earner’ through Richard Crossman’s National Superannuation plan (Labour Party, 1959). Labour leader Hugh Gaitskell was convinced that this material appeal would help attract voters: ‘What people want to hear is how little they will pay and how much they will get from our scheme’ (Crossman, 1981: 768).

It was in this context of post-war affluence and state expansion that policy costings became a staple feature of British election campaigns. The Conservatives had briefly ventured into this territory in the 1920s, when they estimated Labour’s spending plans at £279 million a year (Conservative Party, 1929: 7–8) and portrayed Ramsay MacDonald as a highwayman seeking ‘£250,000,000 a year more in taxes’ (Lawrence, 2009: 114), and in office again after 1951 they revived the tactic. The party’s Research Study Group thought that ‘All matters which touch the pocket have the highest E-value’ – that is, electoral value (Conservative Research Department, 1954b) – and Conservative Research Department (CRD) officials suggested that the party should ‘stress the high cost of Socialism and the Socialist programme in terms of taxation to the individual: coining some such slogan as “It’s Your Money They’re After”’ (Conservative Research Department, 1954a). The CRD duly compiled a list of the proposals in Labour’s mid-term programme Challenge to Britain (1953) and claimed that they would cost between £1.76 billion and £2.68 billion a year (Conservative Party, 1954: 10–12).

During the 1955 election campaign, the Chancellor, R. A. Butler, challenged the opposition to explain how it would pay for its policies, and Minister of Health Iain Macleod warned that Labour’s plans could mean ‘on average another £2 per family per week in extra taxes’ (The Times, 19 May 1955, 16). In truth, the figure was tendentious, since it conflated capital investment with current spending, assumed that a Labour government would eliminate the budget deficit (at a cost of about £400 million) in order to reduce interest rates, and bore practically no relationship to the Labour manifesto (Conservative Research Department, 1955). Even so, the gambit was well-designed to reawaken concerns about Labour’s financial competence which had been widespread in the inter-war period, when the collapse of the 1929–1931 Labour government over the spiralling cost of unemployment benefit had fostered perceptions that the party was unfit to govern. David Butler (1955: 84) concluded that Macleod’s attack ‘helped to foster the image of the Labour Party as wildly extravagant’ and so contributed to the Tory victory.

Having deployed the ‘tax bombshell’ strategy successfully in 1955, the Conservatives repeated it in 1959 and 1964: within each party, the experiences of one campaign shaped the next in an iterative process. In 1959, Tory chairman Lord Hailsham (1959) warned that Hugh Gaitskell’s plans for higher spending financed by faster economic growth would lead to inflation and ‘economic disaster’; five years later, Sir Alec Douglas-Home accused Harold Wilson of offering the electorate ‘a menu without prices’ (The Times, 14 September 1964, 6). On the Labour side, Gaitskell blundered half-way through the 1959 campaign by promising ‘no increase in the standard or other rates of income tax so long as normal peacetime conditions continue’ – a pledge which allowed Harold Macmillan and the Tory press to accuse him of turning the election into a ‘mock auction’ (Butler and Rose, 1960: 59–60). After the Macmillan government was re-elected with a majority of 100, Richard Crossman (1981: 787) concluded that Gaitskell’s income tax gambit had been a ‘fatal stumble which enabled the Tories to revive all the suspicion of our disunity, insincerity, financial dishonesty, and so tip the Don’t Knows back into the Government camp’. Wilson parried the Conservative assault more effectively in 1964 by challenging Douglas-Home to a televised debate on the cost of the parties’ programmes (Butler and King, 1965: 112) and arguing that Reginald Maudling’s election-year boom was unsustainable. He told Robin Day in a BBC interview that he would ‘not hesitate’ to raise taxes if necessary – for instance, to deal with the balance of payments deficit – but ‘over the period of a Parliament’ he did not think Labour’s programme would require ‘any general increase in taxation’ (quoted in Hansard, 1964: 1207).

‘The essence of our campaign tactic is to keep to these comparative costs’, 1964–1997

Although Labour narrowly won the 1964 election, Wilson was impressed by the impact of the Conservatives’ ‘tax bombshell’ strategy and sought to emulate it in office. During his 1964–1970 administration, Wilson repeatedly asked Treasury officials to cost opposition proposals and sought to exploit the ‘black holes’ which they identified. In the 1966 election, for instance, Wilson challenged Edward Heath to show how the Conservatives could cut taxes and increase defence spending without means-testing the welfare state. As Crossman (1975: 479) noted in his diary, Wilson was determined to exorcise the ghosts of 1959:

We shall smash Heath as Macmillan smashed Gaitskell by constantly asking how much his promises cost. We have costed ours, and, although it is boring, the essence of our campaign tactic is to keep to these comparative costs.

Labour fought similar defensive campaigns in 1970 and 1979, though with less success. In 1970, Wilson’s Chief Secretary to the Treasury, John Diamond, claimed (accurately) that the Conservatives’ numbers did not add up, and that Heath’s plans for VAT and reforms to agricultural support were likely to be inflationary (Butler and Pinto-Duschinsky, 1971: 157). Likewise, in 1979, Jim Callaghan pressed Margaret Thatcher to show how she would pay for income tax cuts, and Education Secretary Shirley Williams used a blackboard to illustrate what £150 million of cuts would mean for schools in a party political broadcast (Butler and Kavanagh, 1980: 187–188).

It is difficult to trace voters’ responses to these strategies in a consistent way, since the British Election Study (BES) has generally asked respondents for their views on overall economic management and broadly defined policy options, rather than for comparative assessments of party programmes. Nevertheless, the frequent ‘swings of the pendulum’ between 1964 and 1979 suggest that incumbent parties’ efforts to foreground ‘comparative costs’ may have become less effective in this period. One possible explanation is that successive governments fostered expectations of rising living standards which they were unable to deliver, as Anthony King (1975) argued. The Conservative victories in 1970 and 1979 and the Labour victory in February 1974 seemed to bear out Charles Goodhart and Rajendra Bhansali’s (1970) thesis that satisfaction with government was closely linked to economic performance. Indeed, public frustration with the Heath government’s record meant that Labour was able to win the February 1974 election despite signalling that it would put up taxes, and despite the fact that Denis Healey was privately alarmed by the cost of the party’s programme (Whiting, 2000: 228–232).

Some voters may also have recognised that focussing on how government spending would be ‘paid for’ through tax increases was a somewhat artificial exercise in an era of growth-oriented Keynesianism. During the 1960s and early 1970s, the Treasury planned public spending in volume rather than cash terms, and the scope for expansion was primarily framed by the macroeconomic ‘budget judgment’ and the availability of real resources (Pliatzky, 1982). The vulnerability of sterling meant that ‘the confidence factor’ could never wholly be ignored, as Harold Wilson (1971: 32) noted, but both the Conservatives in 1969–1970 and Labour policy-makers in 1972–1973 calculated their fiscal plans on the basis of Keynesian ‘demand weighting’ (Labour Research Department, 1973; Reading, 1969; Sewill, 1970). When inflation and the budget deficit spiked in the mid-1970s, however, the assumption that the British government could finance its borrowing without difficulty was no longer tenable. The 1974–1979 Labour government imposed ‘cash limits’ on departments and published targets for the Public Sector Borrowing Requirement (PSBR) in order to reassure lenders and overseas investors that it was committed to reducing the deficit (Britton, 1991: 203–211), and the 1976 International Monetary Fund (IMF) crisis came to symbolise the emergence of this ‘new realism’. Margaret Thatcher gave the focus on the PSBR a monetarist gloss by emphasising its relationship with the money supply (Tomlinson, 2012), but many non-monetarists also accepted the need for budgetary restraint. The Mitterrand government’s experience in France in 1981–1983 seemed to confirm that large-scale deficit spending risked provoking a devastating reaction from the financial markets.

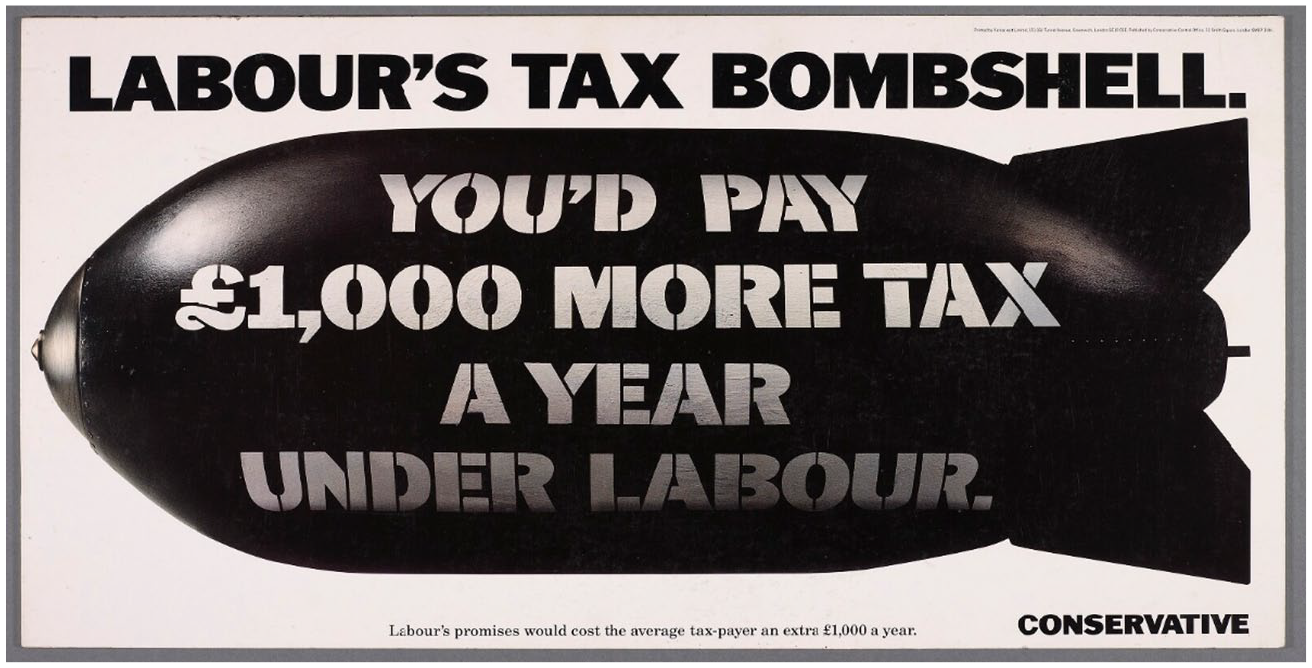

It was during the 1980s that the regular costing of opposition policies was institutionalised within government and returned to the forefront of Tory election campaigns. The Treasury’s Economic Briefing (EB) Division maintained a rolling ‘Checklist of Alternative Economic Policies’ proposed by opposition parties and other groups (Deyes, 1984), and ministers used this as a starting point for costings of the Labour and SDP/Liberal Alliance programmes. The rules of engagement were set out in guidelines circulated by the Cabinet Secretary Sir Robin Butler (1989): ministers could ask civil servants for ‘factual information’ about ‘the policies and pledges of their political opponents’ so long as they (or their special advisers) identified the proposals to be costed and took responsibility for any public presentation. A standard basis for the calculation was also established: the annual cost of Labour’s plans in the fifth year of the next Parliament, over and above existing public expenditure, with one-off costs (such as nationalisation) ‘assumed to be spread over five years’, and ‘[n]o account . . . taken . . . of statements that policies will only be implemented as fast and as far as resources allow’ (Treasury, 1991). In 1986–1987 and 1991–1992, the Chief Secretary to the Treasury coordinated the exercise and published a dossier of Labour’s spending commitments in the summer before the election (Tebbit, 1986). This was then updated and relaunched during the campaign itself and formed a basis of a hard-hitting assault on Labour’s plans – most famously in Saatchi & Saatchi’s 1992 ‘tax bombshell’ poster (Figure 2).

‘Labour’s Tax Bombshell’, Conservative Party poster, January 1992.

As voters became more sceptical about politicians’ ability to deliver on their promises, opposition parties sought to burnish their fiscal credibility in a number of ways. First, they began to publish their own costing documents to show how their policies would be paid for, as Labour had first done with its 1973 mid-term programme. During the 1987 election the SDP-Liberal Alliance (1987) issued a 14-page ‘prospectus’ of tax and spending plans, and the Liberal Democrats continued this practice in an attempt to persuade voters that they should be taken seriously as a party of government. John Smith’s 1992 ‘Shadow Budget’, which he delivered in a heavily trailed speech at the Institute of Civil Engineers, added an extra layer of political theatre and signalled Labour’s renewed commitment to fiscal prudence. The Institute for Fiscal Studies (IFS) – which had been founded in 1969 but expanded rapidly in the 1980s – positioned itself as a non-partisan ‘umpire’ and assumed an increasingly prominent role in verifying policy costings (Akam, 2016).

Second, parties attempted to guard against hostile costings exercises by distinguishing more clearly between their immediate priorities and longer term policy ideas. In 1983, for instance, the Labour manifesto centred on a £11 billion ‘Emergency Programme of Action’, financed by extra borrowing and designed to reduce unemployment by 500,000 in the first 12 months. Four years later, Shadow Chancellor Roy Hattersley (1987) published a £6 billion jobs programme and a £3.6 billion anti-poverty programme and warned that these were ‘the only two items of extra expenditure to which we are firmly committed during our first 2 years in office’.

Third, Labour sought to reassure voters that the party had no intention of raising the tax burden across the board in the way that Conservative propaganda suggested. Kinnock and Hattersley thus insisted that Labour’s 1987 anti-poverty programme could be paid for by reversing the tax cuts which the Conservatives had given to the richest 5% since 1979, though this line unravelled in the final week of the campaign under pressure from Nigel Lawson. John Smith went further in 1992 by using a computer model which Tony Atkinson and Holly Sutherland had developed at the LSE to simulate the distributional effects of Labour’s plans (interview with Holly Sutherland, 6 December 2018). Smith promised that his ‘Shadow Budget’ would make eight out of 10 taxpayers better off, including every employee earning less than £22,000 (Labour Party, 1992).

The unhappy fate of Labour’s 1992 campaign revealed the limitations of these defensive strategies. On the one hand, the attempt to show how Labour would balance the books made it hard to promise improvements in public services. For instance, the £3.3 billion cost of the party’s pledges to raise pensions and child benefit meant that it could only promise an extra £1 billion spread over 22 months for the National Health Service, an increase of less than 2%, and the BES found that the party was damaged by doubts about whether ‘a Labour government would actually improve health and education’ (Heath et al., 1994: 294). On the other hand, the admission that some taxes would rise created an opening for Tory attacks. As the Conservative Party’s communications director Shaun Woodward (1995: 30, 33) put it after the election, ‘prolonged media coverage of our costing of Labour’s spending proposals. . . ensured that the agenda was transformed from health to public spending and the economy’, and so provided ‘supporting evidence’ for the Conservatives’ core argument that ‘You Can’t Trust Labour’.

It was this experience of being placed on the back foot over financial issues, not just in 1992 but during the previous decade, that prompted New Labour’s relentless ‘strategy of reassurance’ on tax in the run-up to the 1997 election (Gould, 1998: 283). Tony Blair and Gordon Brown ruled out increases in income tax rates and promised to stick to the Conservatives’ spending plans for the first two years of the next Parliament, with the exception of a ‘New Deal’ welfare-to-work package paid for by a ‘windfall levy’ on the privatised utilities. All the party’s other pledges, such as reductions in primary school class sizes and NHS waiting lists, would be financed by reallocating resources within existing budgets. Blair and Brown’s income tax pledge succeeded where Hugh Gaitskell’s had failed: partly, no doubt, because their spending proposals were so modest, but also because they had laid the groundwork before the campaign began. Brown announced his tax plans in a carefully choreographed speech in January 1997 and had spent years lambasting the Major government for ‘22 Tory tax rises’.

Fiscal rules and ‘deficit deniers’, 1997–2019

‘Tax bombshell’ attacks have been less prominent in British elections since the turn of the millennium, perhaps partly because New Labour was so effective at neutralising tax as an issue. ONS data suggest that the tax burden on households fell slightly during Labour’s 13 years in office (Corlett, 2019: 26), and even in 2010, BES respondents were broadly satisfied with the government’s handling of taxation. 1 Nevertheless, fiscal policy has remained at the heart of political debate, particularly since the 2008 financial crisis. Both Gordon Brown and George Osborne have attempted to use fiscal rules to frame public perceptions of ‘responsible’ tax and spending levels, placing the onus on opposition parties to justify departures from this baseline. During the 2000s, this helped Labour secure political consent for increased spending on health, education, and welfare; since 2010, it has allowed the Conservatives to characterise Labour as ‘deficit deniers’ and justify ‘austerity’ policies.

The fiscal rules which Gordon Brown established in 1997 provided a basis for reassuring voters and markets that Labour could maintain control of public spending, reflecting a global trend towards the use of policy rules as a precommitment device and a form of ‘depoliticisation’ (Burnham, 2001; Dellepiane-Avellaneda, 2012). In particular, Brown’s ‘golden rule’ stated that the government would only use borrowing to finance capital investment over the course of an economic cycle (Tomlinson, 2017: 111–112). Tight spending control during the late 1990s allowed Brown to set out plans for increased health and education funding in the 2000 Comprehensive Spending Review, and by the 2001 election the government was committed to raising public spending from 38.9% to 40.3% of gross domestic product (GDP) over the next three years (Bloom et al., 2001). As Tim Bale (2016: 114–115) has shown, this presented William Hague with the mirror image of the challenge which Labour had faced in opposition, struggling to satisfy Tory activists’ demands for tax cuts while reassuring floating voters that the party would not dismantle public services. The 2001 Conservative manifesto proposed to hold public spending down to 39.6% of GDP in 2003/2004, matching Labour’s spending plans on health, education, and policing while making room for £8 billion of tax cuts. Although the sums involved were relatively small, Brown exploited the issue to contrast ‘Labour investment’ with ‘Tory cuts’. As David Butler and Dennis Kavanagh noted in the Nuffield study of the campaign,

The public mood had changed from the 1980s when Labour was often on the defensive about its plans for increased public spending (‘Where’s the money coming from?’). In the new climate after 1997 Conservative tax cutters were on the defensive (‘Where will the cuts in services come?’) . . . (Butler and Kavanagh, 2002: 26)

Labour repeated the tactic in 2005, claiming that the £35 billion of efficiency savings that the Conservatives proposed ‘were equivalent to sacking every teacher, nurse and GP in the country’ (Kavanagh and Butler, 2005: 60).

Exploiting voters’ fears of ‘Tory cuts’ was again central to Labour’s strategy in 2010, when debate focussed on the question of how to reduce the mounting deficit. Although David Cameron and George Osborne promised to ring-fence spending on the NHS and schools, the Labour campaign sought to highlight the ‘risks’ of Conservative spending plans at two levels. First, Gordon Brown argued that the Conservatives’ plans for £6 billion of spending cuts in 2010/2011 would put the economy at risk in macro terms, and that deficit-reduction should wait until the recovery from the 2008–2009 recession was ‘secure’. Second, Labour challenged Cameron and Osborne to explain what their plans might mean for particular services, and used direct mail to claim that the Tories would cut child tax credits and scrap cancer waiting-time targets. According to Catherine Haddon (2019), Labour ministers commissioned Treasury officials to carry out 38 costings of Conservative policies between 2008 and 2010, though not all of these were completed or used. As in 1979, Labour’s defensive strategy appears to have shored up its vote, but its impact was weakened by the government’s own loss of fiscal credibility. The 2008 financial crisis had left Brown’s fiscal rules in tatters, and Labour Chancellor Alistair Darling had himself set out plans for tax increases and spending cuts in his 2009 and 2010 budgets. For the first time in a decade, the Conservatives could plausibly claim that they were better placed to protect voters’ personal finances.

Andrew Gamble (2015: 47) has persuasively argued that George Osborne’s deficit-reduction strategy should be seen as a form of ‘statecraft’: an ‘attempt to redefine the terms of the debate on economic policy in the UK’ and ‘to create a new dividing line which had Labour on the wrong side of it, as the party that had got the country into the mess in the first place’. Osborne tightened his fiscal rules in the 2014 autumn statement in order to squeeze Labour’s room for manoeuvre in the run-up to the 2015 election, and unveiled a dossier accusing Ed Miliband of planning £21 billion more borrowing in 2015/2016. Shadow Chancellor Ed Balls attempted to parry the Tory attack by calling for the Office for Budget Responsibility (OBR) to cost all parties’ policies, as public officials do in Ireland, Australia, and The Netherlands, but Osborne predictably rejected the proposal (Munro, 2014; Renwick and Palese, 2019: 98–124). As the election approached, Labour struggled to balance its critique of the coalition’s cuts with the need to reassure voters that it could manage the public finances (Sowels, 2015). The 2015 Labour manifesto began with a pledge to reduce the deficit year-on-year (which it called a ‘Budget Responsibility Lock’) while also promising to invest an extra £2.5 billion a year in the NHS and reduce university tuition fees. Although Miliband and Balls worked hard to ensure that these policy commitments were credible, Labour’s costings were less explicit than in 1992 or 1997, partly because it was so difficult to reconcile the party’s conflicting imperatives.

George Osborne’s success in portraying Balls and Miliband as ‘deficit deniers’ made Labour’s gains in the 2017 election particularly surprising. For the first time since 1987, Jeremy Corbyn committed Labour to an unapologetic ‘tax and spend’ programme, with £48.6 billion of tax increases to pay for policies such as free university tuition (£11.2 billion a year), the lifting of the public sector pay cap (£4 billion), and more money for schools (£6.3 billion) and the National Health Service (£5 billion). Conventional wisdom suggested that this costly manifesto would be an electoral albatross; instead, Labour increased its vote and deprived Theresa May of her majority. Corbyn’s campaign built on themes which Gordon Brown and Ed Miliband had developed over the previous decade – such as opposition to ‘Tory cuts’ and support for a 50% top rate of income tax – but gave them a sharper populist edge through a more forthright critique of ‘austerity’. John McDonnell’s economic advisor James Meadway (2019) believed that the party’s readiness to talk about the losers from its tax plans – particularly corporations and the 5% of individuals with incomes over £80,000 a year – also gave them greater credibility. The recognition that fiscal policy was a ‘zero sum game’ helped Labour tap into growing frustrations about inequality in Britain, especially among the young, female, and lower income voters who had borne the brunt of deficit-reduction measures (Jennings and Stoker, 2017; Sanders and Shorrocks, 2019). Indeed, British Social Attitudes Survey data suggest that support for tax increases to pay for higher public spending had almost doubled (from 31% to 60%) between 2010 and 2017, in a classic thermostatic response to austerity policies.

In his retrospective comparison between the 2017 and 2019 elections, Meadway (2019) suggests that Labour’s 2019 campaign was weakened by a loss of focus. Popular proposals such as scrapping tuition fees and renationalising the railways were now ‘old news’, and many of the ‘new promises’ (such as free broadband) did not seem to be a priority for voters. At least as important, however, were changes on the Conservative side, as the party learned the lessons of 2017 and framed the fiscal argument more effectively. Sajid Javid promised to ‘turn the page on austerity’ in his September 2019 spending review and announced plans for a 4.1% increase in departmental budgets, backing up Boris Johnson’s endlessly repeated pledges to recruit 50,000 more nurses and 20,000 new police officers. Unusually for a governing party, the Conservatives also published their own costings document, based on new fiscal rules which would allow an extra £20 billion a year of capital investment over the next Parliament. These defensive manoeuvres set the scene for a relentless assault on Corbyn’s plans – the latest in the party’s long series of ‘tax bombshells’.

Conclusion

The conclusions that can be drawn from a single-country qualitative study of this kind are necessarily case-specific, and to some extent impressionistic. Nevertheless, this survey of the use of manifesto costings in British election campaigns suggests that UK experience supports the broad hypotheses developed at the beginning of the article. First, it is clear that British politicians and party strategists believe that prospective, egocentric economic expectations are a central determinant of voter choice, and the clear lines of responsibility provided by the Westminster model make it rational for voters to take parties’ tax and spending proposals seriously. Second, although warnings about ‘tax bombshells’ and ‘black holes’ in opposition spending plans date back to the 1950s, they seem to have become more effective since the era of Keynesian demand management gave way to a ‘new realism’ about fiscal constraints in the mid-1970s. The emphasis which governments have placed on the budget deficit since the 1976 IMF crisis has encouraged voters to see fiscal policy in zero-sum terms, in which tax cuts and spending plans have to be paid for and excessive borrowing risks economic meltdown. Third, voters’ awareness of the need for fiscal credibility has only partly dulled the impact of thermostatic responses to government activity. In particular, the long periods of Conservative rule from 1979 to 1997 and from 2010 to the present have been marked by increasingly strong demand for higher spending on the NHS and other public services.

This analysis has significant implications for our understanding of the role which policy plays in parties’ electoral strategies. Whereas retrospective assessments of economic performance can be difficult for governing parties to control, fiscal policy provides more favourable terrain for incumbents, and British governments have repeatedly sought to focus attention on future tax and spending plans in order to offset the ‘costs of governing’. Forward-looking fiscal debates are structurally asymmetric: the rituals of the budget speech and the Treasury red book confer an aura of authority on the government’s figures and force opposition parties to persuade voters that there are good reasons for departing from the baseline set by the incumbents. This may be one reason why the United Kingdom has moved into an era of long electoral cycles since the 1970s (Quinn, 2013). Even so, incumbent parties’ ability to deploy ‘tax bombshell’ attacks is likely to depend in part on their own record in office. Governments may find it harder to appeal to voters’ sense of prudence when the deficit has risen sharply (as in 2010), or to exploit voters’ loss-aversion when they have themselves imposed tax increases and spending cuts (as the Conservatives did between 1992 and 1997). This may help explain why Adi Brender and Allan Drazen (2008) have found that loose fiscal policies tend to weaken governments’ chances of re-election.

The asymmetric nature of budgetary debates means that opposition parties face a different kind of challenge: of reconciling their supporters’ demands for policy change with floating voters’ concerns about credibility. Labour’s defeats in 1983, 1987, and 1992 prompted a shift from a ‘maximalist’ to a ‘minimalist’ fiscal approach; so too did the Conservatives’ defeats in 2001 and 2005, though David Cameron’s promise to match the Labour government’s spending plans was overtaken by the 2008 financial crisis (Dorey, 2009). The results of the 1997 and 2010 elections suggested that ‘shrinking’ the policy offer and prioritising fiscal stability was a winning electoral strategy. On the other hand, Jeremy Corbyn’s strong performance in 2017 shows that ‘big ticket’ retail policies can still capture voters’ imagination, particularly if they are clearly communicated and chime with voters’ own sense of priorities. After a long period of austerity, there are signs that the preoccupation with fiscal credibility which has prevailed since the late 1970s may be losing its force. Despite the success of the Conservatives’ attack on Corbyn in the 2019 election, the 2020s seemed likely to be a period of state expansion even before the outbreak of the COVID-19 pandemic.

The analysis developed here illustrates the potential for using historical evidence to move beyond stylised models of voter preferences and explore how parties have framed fiscal choices in the real world, turning public finance into a performative instrument of campaigning. This article only scratches the surface of a vast topic, and it is not difficult to identify potential avenues for further work. First, there is much to be gained from deepening our historical understanding of the British case – for instance, by re-analysing survey data and focus group evidence to assess voters’ reactions to fiscal promises, and expanding the analysis beyond Labour and the Conservatives to consider the distinctive incentives faced by smaller parties such as the Liberal Democrats. Second, we need to know more about how voters process tax and spending proposals at a cognitive level, particularly when they are confronted by competing frames from different parties (Buchanan, 2019). This takes us into the realm of behavioural psychology and also raises questions about how policy design and media coverage shape public perceptions of ‘fairness’ (Stanley, 2016). Finally, there is scope for developing a comparative perspective, examining how far the patterns identified in Britain have been mirrored in other countries, and so bringing electoral studies into a fuller dialogue with the ‘new fiscal sociology’ (Martin et al., 2009). What is clear is that the fiscalisation of political debate in the United Kingdom and other western states shows no sign of ending. The costing and counter-costing of policy proposals is thus likely to remain one of the defining rituals of modern election campaigning.

Supplemental Material

Appendix – Supplemental material for ‘Where’s the money coming from?’ Manifesto costings and the politics of fiscal credibility in UK general elections, 1955–2019

Supplemental material, Appendix for ‘Where’s the money coming from?’ Manifesto costings and the politics of fiscal credibility in UK general elections, 1955–2019 by Peter Sloman in The British Journal of Politics and International Relations

Footnotes

Acknowledgements

I am grateful to Dr Aled Davies for fruitful discussions on this topic, and to Mr Colm Murphy, Dr Mitya Pearson, Professor Helen Thompson, and the two anonymous reviewers for their comments on early drafts of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.