Abstract

In February 2016, BBC Three became the first television (TV) channel in the world to close its linear broadcasting operation and instead prioritize offering its programming on demand, via the internet. Two Danish channels – both also youth-focused – followed in January 2020 for the same reason: budget cuts. Although the effects of ending offline distribution on the size and behaviour of newspaper and magazine audiences have been investigated, this article is the first to investigate the effects on a TV channel. The results show that BBC Three’s audience shrank by 60–70% after it closed its linear TV channel. The intensity with which the channel was viewed was even more sharply reduced: annual viewing minutes after the switch were 89% less than the channel achieved on linear TV before (and around 72% less if viewing of BBC Three-commissioned/acquired content on other BBC TV channels is included). The mix of programme genres consumed changed too, although further research is required to establish the part played by the change in distribution mechanism. This study furthers our understanding of media platform cessation by showing how change in the size of a media outlet’s audience after ending offline distribution may be affected by the proportion of its audience that consumes it exclusively offline before and how, irrespective of media platform, ending offline distribution seems to cause a sudden and substantial fall in the time spent with a media brand by its audience.

Keywords

Introduction

On 16 February 2016, BBC Three became the first television (TV) channel in the world to close its linear broadcasting operation and instead prioritize offering its programming on demand, via the internet (Ellis-Petersen, 2016). Although it was the first, it was not the last. On 2 January 2020, two of the Danish Broadcasting Corporation’s channels, DR3 and DR Ultra, followed suit (Boier, 2020), in a move that had a number of parallels with BBC Three. The Danish Broadcasting Corporation is Denmark’s equivalent of the BBC, and the cessation of broadcasting was prompted by budget cuts imposed by the government (Franks, 2018). Moreover, the Danish channels, like BBC Three, are youth-focused. Further such moves seem likely. Helen O’Rahilly, the former director of TV at Raidió Teilifís Éireann (RTÉ), Ireland’s national broadcaster, has said that RTÉ’s youth channel ‘will possibly go the way of BBC Three’ (Blake Knox, 2020: 6–7).

Ending offline distribution, while exceptional for TV stations, is more common among newspapers and magazines. Between 2006 and early 2020, for financial reasons, dozens of titles went online-only, including the magazine Marie Claire (UK) and newspapers such as The Independent.

There is limited literature on such ‘media platform cessation’ (Thurman and Fletcher, 2019). In the context of periodicals, one study examined the impact within the newsroom (Thurman and Myllylahti, 2009) and another two the effects on audience size and behaviour (Thurman and Fletcher, 2018, 2019). In the context of TV, the history of, and rationale for, BBC Three (Doyle, 2016; Ramsey, 2018; Woods, 2016, 2017) and DR3’s (Andersen, 2018) decisions to close their linear channels have been analysed, but there have been no published studies on the audience effects on a TV channel of ceasing offline distribution – a gap this article aims to fill.

Although the BBC sought to justify their decision to close BBC Three’s linear TV channel with reference to ‘changing audience consumption’ (BBC, 2015: 2), forecasting commissioned by the Corporation predicted that the time viewers were spending watching BBC Three on live TV and catch-up would primarily be ‘redistributed amongst other linear channels’, and although there would be a ‘21%’ increase in the consumption of BBC Three online, that increase, because it built on such a low base, was unlikely to have a ‘material market impact’ (Communications Chambers, 2015).

This study puts such predictions about the post-broadcast performance of BBC Three to the test by comparing data – on audience size, viewing intensity and programme genre availability and consumption – from before and after the channel ceased linear broadcasting. Source data come from the UK’s official supplier of TV audience measurement (Broadcasters’ Audience Research Board (BARB)), the long-running Touchpoints Hub Survey and the BBC.

This study estimates that BBC Three’s audience shrank by 60–70% after it closed its linear channel, a much steeper decline than experienced by the channel’s competitors, who have continued to broadcast. Furthermore, the intensity with which BBC Three was viewed fell even more steeply, with 86% fewer gross half hour claims (GHCs) and viewing minutes 89% less than the channel achieved on linear TV before. Even factoring in the minutes viewers spent watching BBC Three-commissioned/acquired programmes on the BBC’s remaining linear TV channels (e.g. original BBC Three shows Killing Eve and Fleabag were both broadcast on BBC One), the decline in viewing time was around 72%. The mix of programme genres consumed changed too, although no attempt is made to determine whether the change in distribution mechanism was a cause, given that other factors – such as changes in programme availability – are also at play.

As well as considering the implications of the findings for BBC Three and other TV channels, this article discusses how they might contribute to the nascent ‘theory of media platform cessation’ (Thurman and Fletcher, 2019) – by revealing how change to the size of a media outlet’s audience after ending offline distribution may be affected by the proportion of its audience that consumes it exclusively offline before and how, irrespective of media platform, ending offline distribution seems to cause a sudden and substantial fall in the time spent with a media brand by its audience.

BBC Three and its reinvention online

BBC Three was launched in 2003 by the UK public service broadcaster the BBC as a free-to-air TV channel aimed at 16- to 34-year-olds. Its remit was ‘to bring younger audiences to high quality public service broadcasting through a mixed-genre schedule’ including ‘innovative UK content’ (BBC Trust, 2013: 1). The channel became known for its ‘creative and edgy programming’ (Ramsey, 2018: 156) and was ‘popular among its target audience’ (Plunkett, 2014), with, between 2010 and 2015, an average TV audience share among 16- to 34-year-olds of 6.4%, placing it consistently in the top 10 performing UK channels. By 2008, its programmes were available to watch online via the BBC’s broadcaster video-on-demand (BVOD) service, iPlayer.

The freezing of the BBC’s licence fee in 2010, however, required BBC TV to deliver ‘savings of £250 million by 2016–17’ (BBC Trust, 2014: 7). In the context of this financially challenging climate, the Corporation stated that it could not ‘keep doing the same amount for less’ (BBC, 2015: 1) and that to protect the quality of its main TV services, BBC One and BBC Two, it would eschew a ‘continued salami-slicing of existing TV programme budgets’ and instead close BBC Three’s linear broadcasting operation, reinventing the channel online (BBC, 2015: 1), primarily through the BBC’s BVOD service, iPlayer. It was said that the move would allow savings of about £50 million (BBC, 2015: 2), though the savings would in fact derive not from reduced distribution costs but from a reduced content budget, with this budget cut from £80 million to £30 million (Doyle, 2016: 699).

While acknowledging that the move was ‘driven by financial necessity’ (BBC, 2015: 2), the BBC also sought to frame it as ‘a strategic opportunity’ (p. 2), a canny response to a ‘changing TV landscape’ and ‘changing audience consumption’ (pp. 1–2). This latter change involved a ‘transition to greater on-demand consumption’, with the 16–24 age group in particular shifting to non-linear viewing (p. 2), and it was stated that reinventing BBC Three online would ‘enhance the BBC’s reputation with young audiences’ (p. 3). The BBC’s statements on this matter involved varying amounts of positivity and pragmatism. In its more positive mode, it spoke of giving the audience what it wants, and in its more pragmatic mode, it spoke of giving the audience what it would put up with. Damian Kavanagh, the then digital controller of BBC Three, spoke of meeting the needs of the BBC Three audience (Kavanagh, 2014), while Tony Hall, the then director general of the BBC, spoke of the BBC Three audience as the audience most ‘ready to move to an online world’ (Plunkett and Sweney, 2014). There was acknowledgement that the move was ‘earlier than we might have liked’, with the young’s adoption of non-linear viewing ‘the direction of travel’ (Kavanagh, 2014) rather than a fully established reality.

In the channel’s new incarnation, 80% of the budget would be spent on long-form content and the other 20% on ‘new form digital content’, the latter including ‘short-form video’ and ‘blog posts’ (Kavanagh, 2014). The content would revolve around the two pillars of ‘Make Me Think’ and ‘Make Me Laugh’ (BBC, 2015: 24), by which was signified drama, documentary, news and current affairs in addition to ‘scripted comedy’ and ‘personality-led entertainment’ (BBC, 2015: 24–25). The BBC claimed that this represented ‘a focus on the content areas which audiences tell us they value most from BBC Three’ (BBC, 2015: 23), though it also involved the removal of the channel’s ‘popular, yet often criticized, US animation imports and factual entertainment programming’ (Woods, 2017: 142). The channel’s long-form content would also receive transmission on BBC One and BBC Two. Some content would appear on services such as YouTube, Facebook and Twitter (BBC, 2015).

In February 2016, the channel became the first ‘in the world’ (Ellis-Petersen, 2016) to cease linear broadcasting and instead prioritize offering its programming on demand, via the internet. In its post-switch form, the channel received some critical acclaim, with the Royal Television Society naming it Channel of the Year in 2017.

Literature review and research questions

In the absence of any previous research on the effect on a TV channel – in terms audience size and the content watched – of ceasing its broadcast operation and prioritizing its online presence, it is necessary to look elsewhere for guidance on what to expect.

Viewers’ attitudes and intentions

One useful source is a survey (N = 1,133) the BBC commissioned that asked viewers (aged 16+) about their attitudes to the proposal to shutter BBC Three’s broadcast channel and how they would behave if the plans were enacted. In general terms, just 14% of respondents ‘expressed broad favourability’ when told about the plan (Communications Chambers, 2014: 4). In terms of their future behaviour, only 29% said they would use the revised service at least once a month, a much lower proportion than the 64% monthly reach the channel had at that time (p. 4). Respondents were asked how they would behave if, in the future, they tuned their TV to BBC Three and saw a message saying the channel was only available on the BBC iPlayer. The largest proportion (40%) said they would change channel to watch something else on TV, 27% said they would seek out BBC Three’s content on the iPlayer, 23% said they would do something else and 11% didn’t know (p. 9).

Other media’s moves online-only

BBC Three may have been the first TV channel to cease its offline operation and prioritize its online service, but it was not the first media brand to do so. Scores of newspapers and magazines have quit print in favour of digital distribution, and there are, at the time of writing, two studies that have explored the consequent audience effects using quantitative data. The first explored the case of The Independent, a ‘quality’ British daily newspaper brand, which went online-only in 2016. The authors found that although The Independent’s net monthly readership rose slightly (by 7.7%) in the 12 months after it made the switch compared with the 12 months before, the annual minutes of attention it received fell dramatically, by 81% (Thurman and Fletcher, 2018). The story was similar at the New Musical Express (NME) – a weekly British music magazine that quit print in 2018 – where net monthly readership rose 27% but annual minutes of attention fell by 72% (Thurman and Fletcher, 2019).

Substitution and displacement

Although, in 2016, BBC Three stood alone among broadcast TV channels in choosing to cease its offline operation and prioritize its online service, many broadcasters have, for a number of years, also offered their content online, and there are, of course, other sources of online televisual content, notably subscription video-on-demand (SVOD) services, such as Netflix, and video sharing sites, such as YouTube. A number of studies have sought to investigate the extent to which viewing online video content (including from traditional TV channels) on devices such as PCs or smartphones displaces TV viewing. The results of these studies may also help guide our expectations.

Taneja et al. (2012) analysed data from 2008 on a representative sample of US adults who were observed at intervals of 10 s for 2 days, with their media consumption recorded. Among the study’s findings was that ‘access to on-demand media…does not displace linear TV viewing’, which led the authors to conclude that ‘linear television remains a predominant visual media source’.

Cha and Chan-Olmstead (2012) analysed data from a survey (N = 388) conducted in 2009 of US adult internet users to examine the perceived substitutability of online video platforms (used to watch video in real-time via a computer) and TV. Their study found that ‘timely learning’ and ‘relaxing entertainment’ were the ‘most salient motives for why people watch video content’ (p. 269) and that ‘the more consumers watch video content for timely learning’ and ‘relaxing entertainment’ the ‘less likely they are to think that online video platforms and television are substitutable’ (p. 269). They concluded that ‘television might better fulfil consumers’ relaxation and entertainment needs than do online video platforms’ (p. 272).

The first author of that study analysed the same data for another publication (Cha 2013), concluding that the ‘time consumers spent using the Internet to watch user-generated video content reduced the time they spent watching television’ (p. 79). However, the study found that using TV-network websites to watch video content did not affect the amount of time spent watching TV (p. 79).

Jang and Park (2016) analysed 2010–2012 diary data from the Korea Media Panel to estimate the extent to which different media devices – as used for particular activities – complement each other or substitute for each other. They found that the computer did act ‘as a substitute for television when “watching real-time”’ televisual content but phones did not (p. 83). However, the size of the effect led them to suggest that the ‘computer is not a perfect substitute for television thus the risk of cannibalization is not high yet’ (p. 83).

A more recent study was conducted by Budzinski et al. (2020) who, between November 2018 and February 2019, surveyed approximately 3000 Germans, with the final sample biased towards young, low-income, and highly educated respondents. Nearly half agreed that YouTube-style ad-supported video-on-demand services were an alternative to TV. Furthermore, most respondents strongly agreed that Netflix-style SVOD services were a ‘close alternative’ to TV. However, there were ‘deep differences’ between younger and older respondents, and the authors concluded that, while for ‘younger generations…these services represent close alternatives’, older generations ‘remain more focused on TV’.

It should be noted that most of the substitution and displacement studies cited above were based on data collected between 2008 and 2012 and all used data from countries other than the UK. Since 2012, the availability and quality of online video services – and the devices on which they can be viewed – have increased. Furthermore, full-scale BVOD services were available earlier in the UK than in some other countries. For these reasons, it is possible that, after BBC Three had ceased linear broadcasting, UK viewers saw online video services, including BVOD platforms such as iPlayer, as a better substitute for traditional linear broadcast TV than most of these studies suggest.

It is important to note that studies on substitution and displacement effects of the type mentioned above consider audiences’ use of media types – such as TV and the internet – in their entirety. This is important because, in line with Thurman and Fletcher’s (2019) observations in a related study, the case in hand does not concern the general consumption of TV and internet media but rather the consumption of the broadcast TV and online platforms of a single media brand.

Also consistent with Thurman and Fletcher’s (2019) observations is that such studies have limitations with respect to the case in hand because they ‘describe the consequences of the introduction of new media alongside media that already existed’ (p. 5). This study is interested in the sudden withdrawal by an outlet of one of its existing media platforms. Can, then, what is known – about the effects on TV viewing of online video services – help anticipate what might happen to the consumption of a TV channel when its linear TV platform is withdrawn altogether? If, as some of the research (e.g. Budzinski et al., 2020; Jang and Park, 2016) discussed above suggests, online video services can, in some circumstances and for some people, substitute for broadcast TV, might a channel’s online video service become a substitute for some – or many – of its former linear TV viewers when it ceases to broadcast? After all, if a TV channel’s streaming service can entice some viewers away from its linear TV service while the two media platforms coexist, then, perhaps, when the linear TV service is withdrawn, more viewers ‘will be enticed online – the only place where that brand’s content is now available’ (Thurman and Fletcher, 2019: 5). On the other hand, the fact that relatively few viewers appear to stop consuming linear TV as a direct result of the introduction of BVODs suggests that their loyalty might be ‘more to the medium – or at least the combination of medium and content – than to the content alone’ (Thurman and Fletcher, 2019: 6).

These two hypotheses, although apparently contradictory, might both hold true. The research that exists on other media outlets – a newspaper and a magazine – that have gone online-only shows how this can be the case. For The Independent and the NME, monthly readership did not fall, but the attention they attracted from their readers fell hugely. This suggests that the titles were able to maintain audience numbers through attracting new readers and/or converting former print-only readers into online visitors but that those readers either were, or became, less loyal and/or less attentive than their print readers had been.

The survey data (Communications Chambers, 2014) on the public’s attitudes and intentions regarding the BBC’s plan to close BBC Three as a linear TV channel indicated that, as with The Independent and the NME, the attention attracted by the channel could fall substantially after it ceased offline distribution. However, the survey also indicated that – unlike with The Independent and the NME – the size of the channel’s audience could also fall substantially.

Given the lack of any prior research on the closure of a TV channel’s linear broadcast and the mixed signals given by the other, related research that has been discussed, it was decided to formulate open research questions rather than specific hypotheses. The first of these concern changes in the channel’s audience size

1

and the intensity with which it is viewed:

Change in content availability and consumption

Previous quantitative studies on media brands’ moves online-only (Thurman and Fletcher, 2018, 2019) have focused on changes in the consumption of the outlets in their entirety and have not attempted to analyse the mix of content available – and consumed – before and after or the extent to which any differences therein can be attributed to the change in distribution mechanism. The reason for this is that data about the particular stories consumed within these publications – particularly in print – were difficult or impossible to acquire.

By contrast, in the United Kingdom – as in many other markets – data on the consumption of individual TV programmes are available, meaning that, for the case in hand, it was possible to analyse changes in content consumption. However, any changes are unlikely to be attributable solely to the change in distribution mechanism. Other variables, such as programme availability and audience demographics, will play a part too. Because it is out of the scope of this article to conduct a multivariate analysis of changes in the genres of BBC Three content consumed, descriptive statistics will be employed to answer the following research question:

Methodology

Determining changes in audience size

To answer RQ1, data were acquired from the IPA’s Touchpoints Hub Survey via a specialist data bureau, Telmar. The survey, which uses a representative sample of 5000–6000 British adults, was first fielded in 2005 and then again in 2007/2008, 2009/2010, 2011, 2013 and 2015. Since 2016, it has been fielded every year. Data on changes in the size of BBC Three’s weekly and monthly audience come from questions in the online survey about which TV channels respondents have watched (in any way) over the ‘past 7 days’ and ‘past 4 weeks’.

Determining changes in viewing intensity

To answer RQ2, two different metrics – GHCs and annual viewing minutes – from two different data sources – Touchpoints and BARB – were used.

As part of the Touchpoints Hub Survey, respondents keep an e-diary detailing their activities – including live, catch-up and on-demand TV viewing – every half hour over a week. As a result, Touchpoints was able to provide an estimate of the total number of weekly half hour periods (GHCs) during which British adults watched BBC Three (and other popular TV channels). Because respondents can report multiple activities in any given half hour period, one GHC for BBC Three does not necessarily mean that one person watched the channel for a full 30 min but rather it was watched at some point during that half hour period.

BARB data were used to determine the total minutes of viewing of BBC Three via linear broadcast TV in the year before it closed its linear TV channel; the total minutes of viewing of BBC Three via non-linear TV, PCs, smartphones and tablets for a 12-month period (November 2018 to October 2019) after its linear TV channel was closed and the minutes viewers spent watching BBC Three-commissioned/acquired programmes that were aired on the BBC’s remaining linear TV channels in the ‘after’ period. This ‘after’ period was not the 12 months immediately after BBC Three closed its linear TV channel in February 2016 because, until August 2018, BARB only collected limited information about the video-on-demand consumption of BBC Three. BARB is the official source of TV audience measurement for the United Kingdom and their data were acquired via a specialist data bureau, Digital-i, and Enders Analysis. BARB’s methodology combines passively collected data from their representative panel of approximately 12,000 UK residents with device-based census data collected via tags embedded in BVOD services, such as iPlayer. Further details about BARB’s methodology are included in the Supplemental Material.

Digital-i queried the BARB database to find the total minutes of viewing of each programme broadcast on BBC Three via linear TV in the 12 months up to the closure of the channel’s linear broadcast. However, determining the total minutes of viewing of BBC Three via non-linear TV, PCs, smartphones and tablets for the selected 12-month period after the closure necessitated a large-scale coding exercise. Specifically, although Digital-i were able to query the BARB database to provide a list of every BBC programme that had been watched via the iPlayer between November 2018 and October 2019 (inclusive), and for how many minutes, that list did not identify which programmes belonged to BBC Three and which to other BBC TV channels. In total, tens of thousands of unique programme episodes were consumed on BBC iPlayer during November 2018 to October 2019. To identify which belonged to BBC Three, for each programme title, BBC iPlayer was searched to determine to which channel it belonged. In total, around 1251 unique episodes (of around 270 unique programmes) were identified as belonging to BBC Three. With that information, it was possible to estimate the total number of minutes that each episode belonging to BBC Three was watched for and how those minutes of viewing were split between non-linear TV, PCs, tablets and smartphones (see Supplemental Material for more information). To determine the minutes viewers spent watching BBC Three-commissioned/acquired programmes that were aired on the BBC’s remaining linear TV channels in the ‘after’ period, the BARB database was queried by Enders Analysis using AdvantEdge.

Determining changes in content availability and consumption

To answer RQ3, data from BARB and from the BBC were used. As described above, BARB data were used to generate lists of BBC Three programmes consumed before the channel closed its linear broadcast platform and after and to estimate the number of minutes each programme had been watched for. To each programme in those lists, a genre classification was added, using data from the BBC. 2 With each programme classified in this way, it was possible, through simple addition, to determine the minutes of viewing of programmes of each genre on BBC Three via linear TV before it closed its broadcast TV channel and via its BVOD service after.

To compare the availability of BBC Three programming of different genres on linear TV before the channel closed its broadcast platform, and via its BVOD service after, the metric of ‘minutes of programming broadcast/available to stream’ was used. The list of episodes consumed on iPlayer after BBC Three closed its broadcast platform included each episode’s length. The list of programmes consumed on BBC Three’s linear broadcasting service in the 12 months up to the closure of its broadcast platform did not include information on each programme’s length, so this information was manually added. Working on the assumption that these lists represented all BBC Three episodes available in the before and after periods, 3 it was straightforward to calculate the minutes of programming of each genre available.

Results

RQ1: How did the size of BBC Three’s weekly and monthly audience change after it closed its linear TV channel?

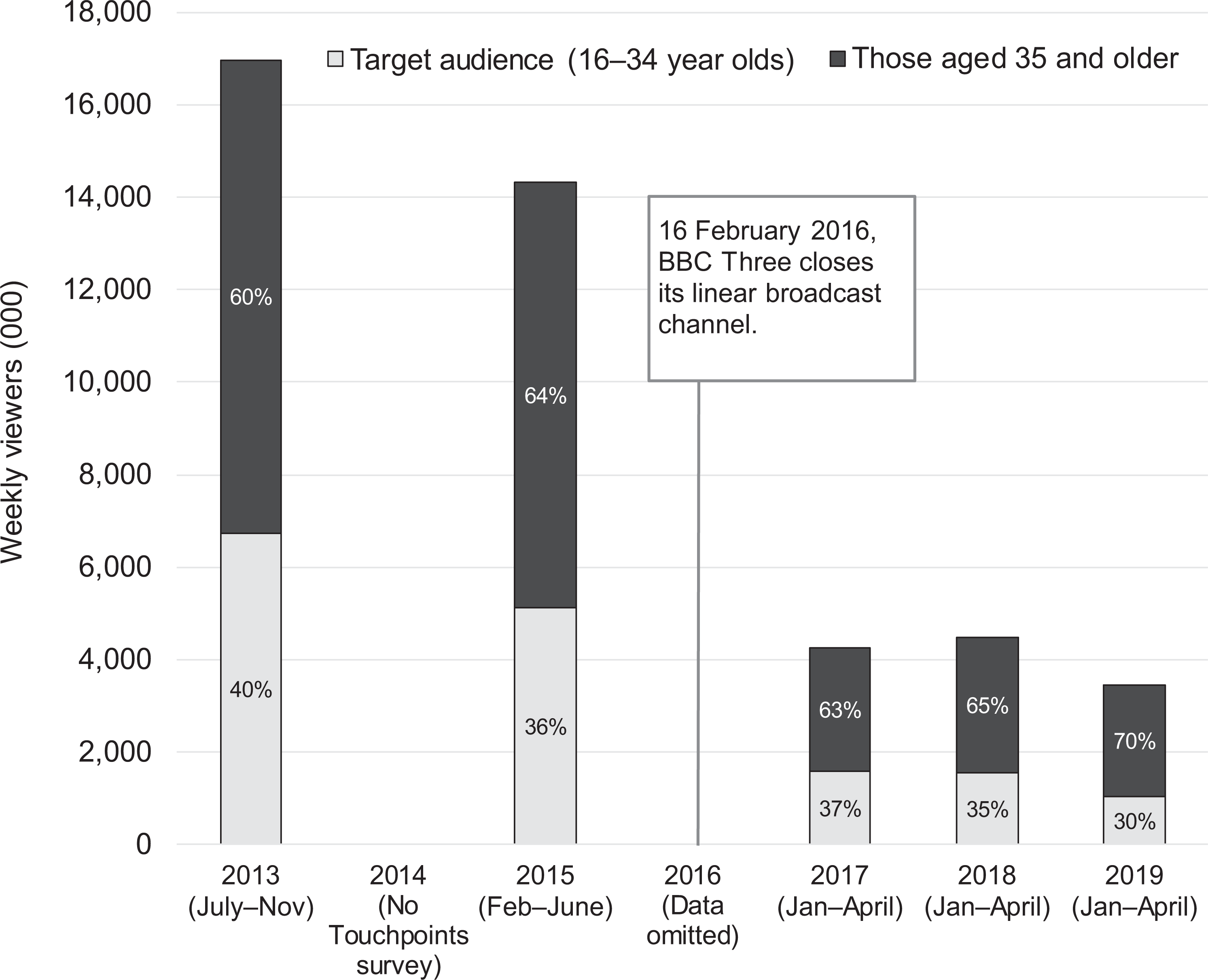

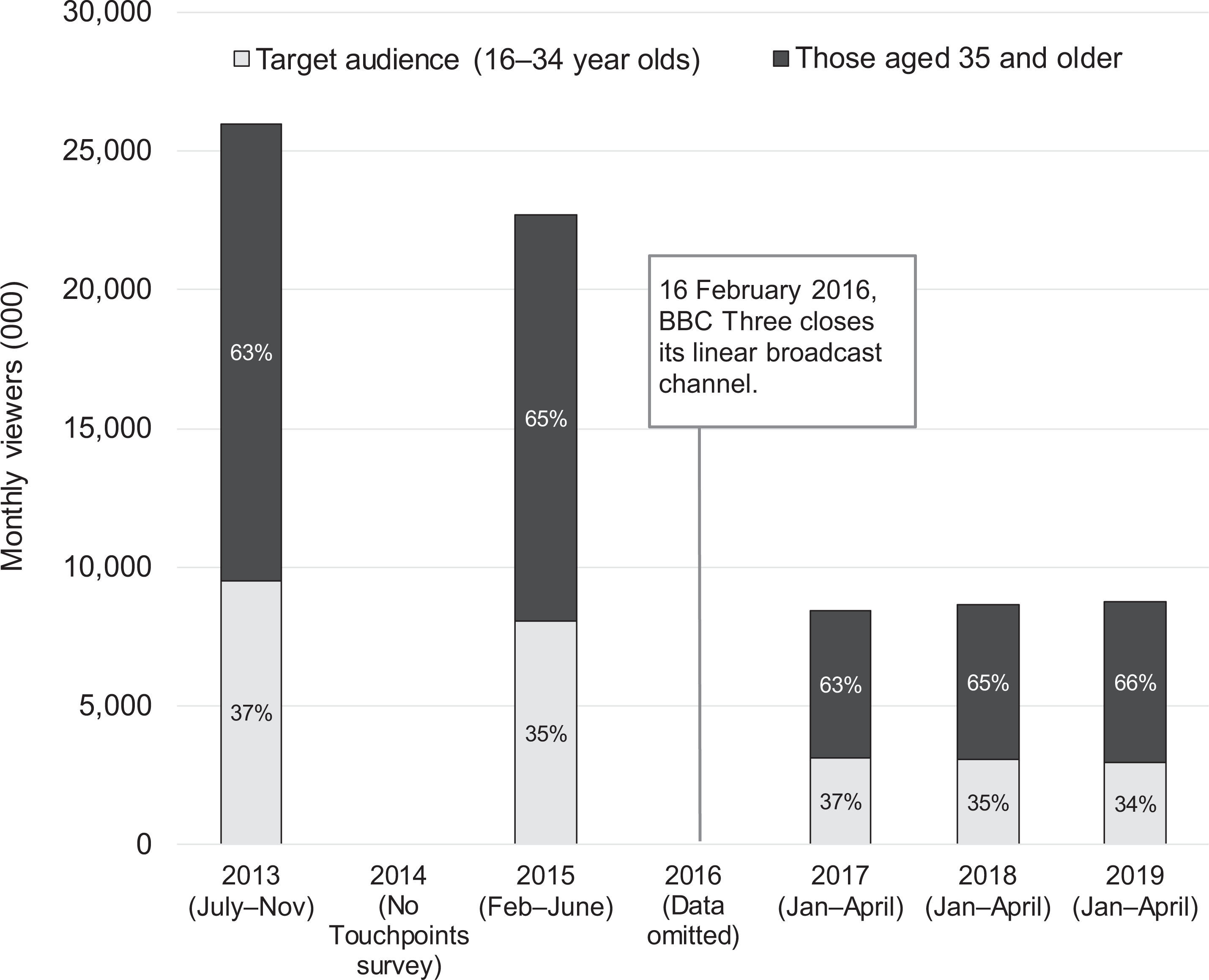

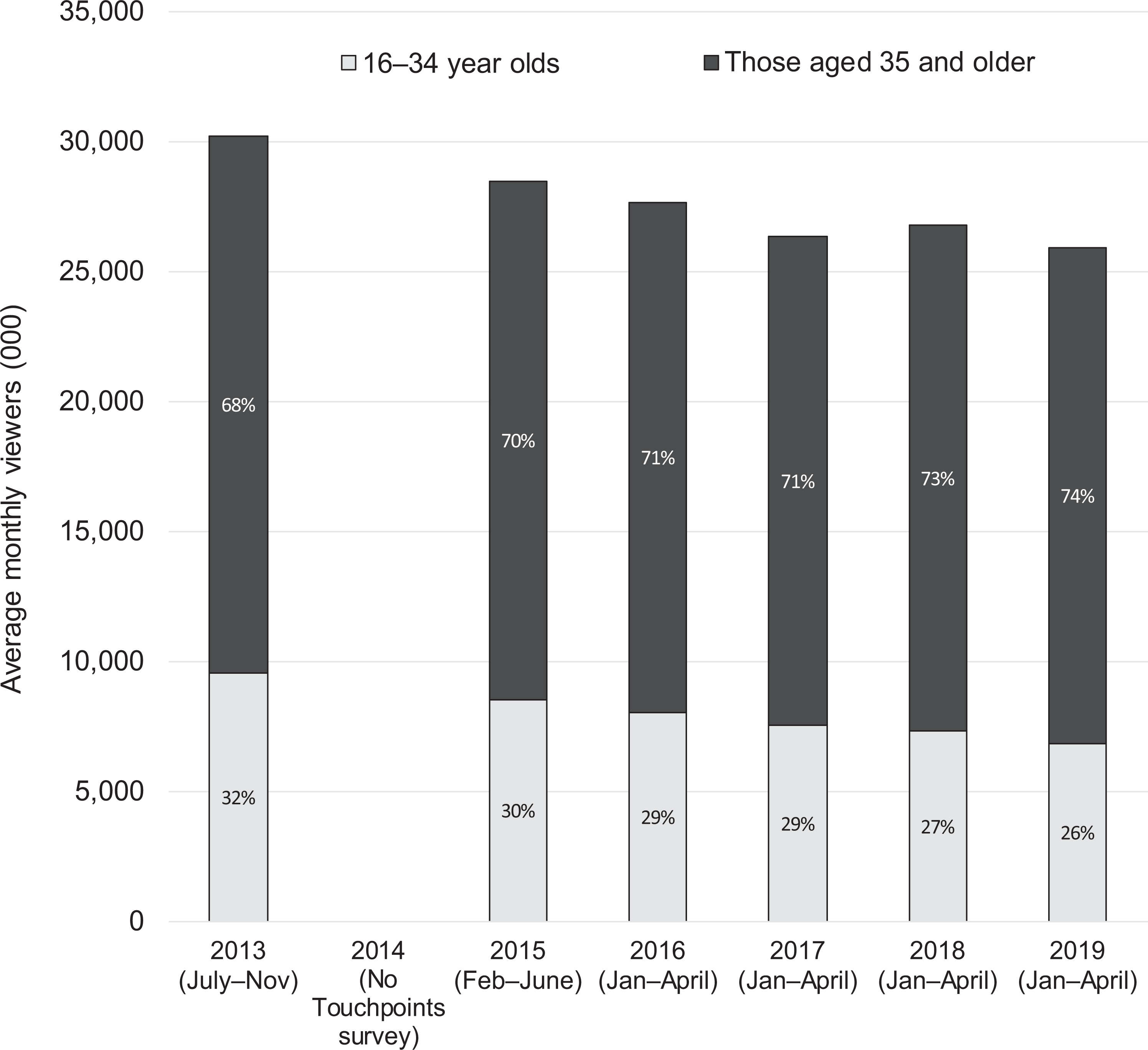

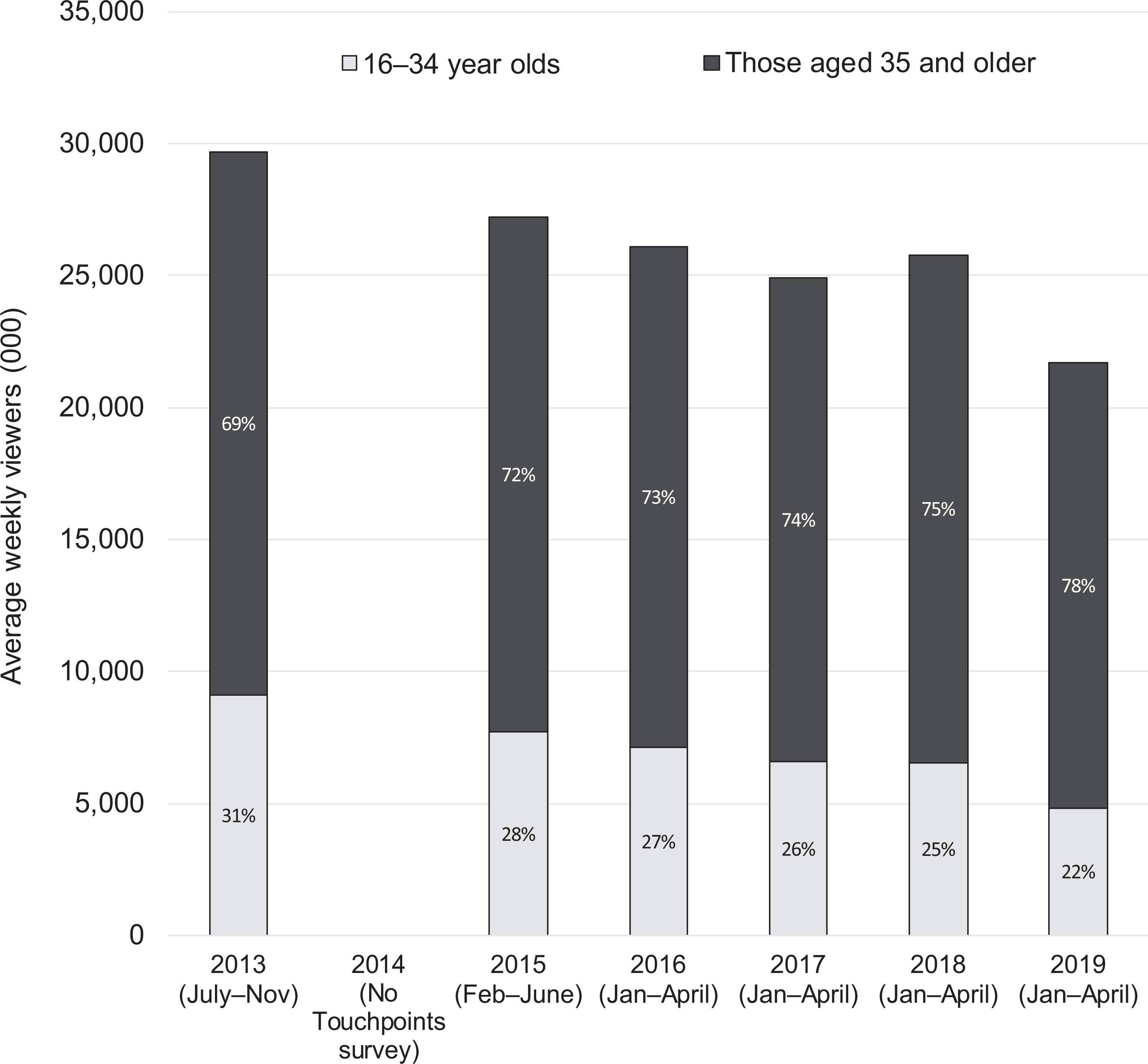

The size of BBC Three’s weekly and monthly audience, in common with most of its competitor TV channels, was declining before it closed its broadcast platform. However, its decision to stop broadcasting resulted in sharp drops. Comparing 2015 – the year before the channel closed its broadcast platform – against 2017 – the year after 4 – shows that BBC Three’s 16–34 audience (its target group) shrank 69% on a weekly basis and 60% on a monthly basis. The losses in weekly (70%) and monthly (63%) adult British viewers of all ages were similar (see Figures 1 and 2). These falls were about three and five times higher than the falls that took place over a comparative period – 2013 to 2015 – when BBC Three was still broadcasting. After 2017, the channel’s monthly audience stabilized – the number of 16- to 34-year-old viewers fell slightly (by an average of 2.9% year-on-year), while the adult audience of all ages rose slightly (by an average of 1.2% year-on-year). Changes in weekly audience numbers followed a similar pattern between 2017 and 2018, but worsened between 2018 and 2019.

Number of weekly British viewers of BBC Three in 2 years before and the 3 years after it closed its linear TV channel. Source: IPA Touchpoints Hub Survey.

Number of monthly British viewers of BBC Three in 2 years before and the 3 years after it closed its linear TV channel. Source: IPA Touchpoints Hub Survey.

RQ2: How did the intensity with which BBC Three was viewed – expressed in (1) annual minutes of viewing and (2) weekly GHCs – change after it closed its linear TV channel?

Annual minutes of viewing

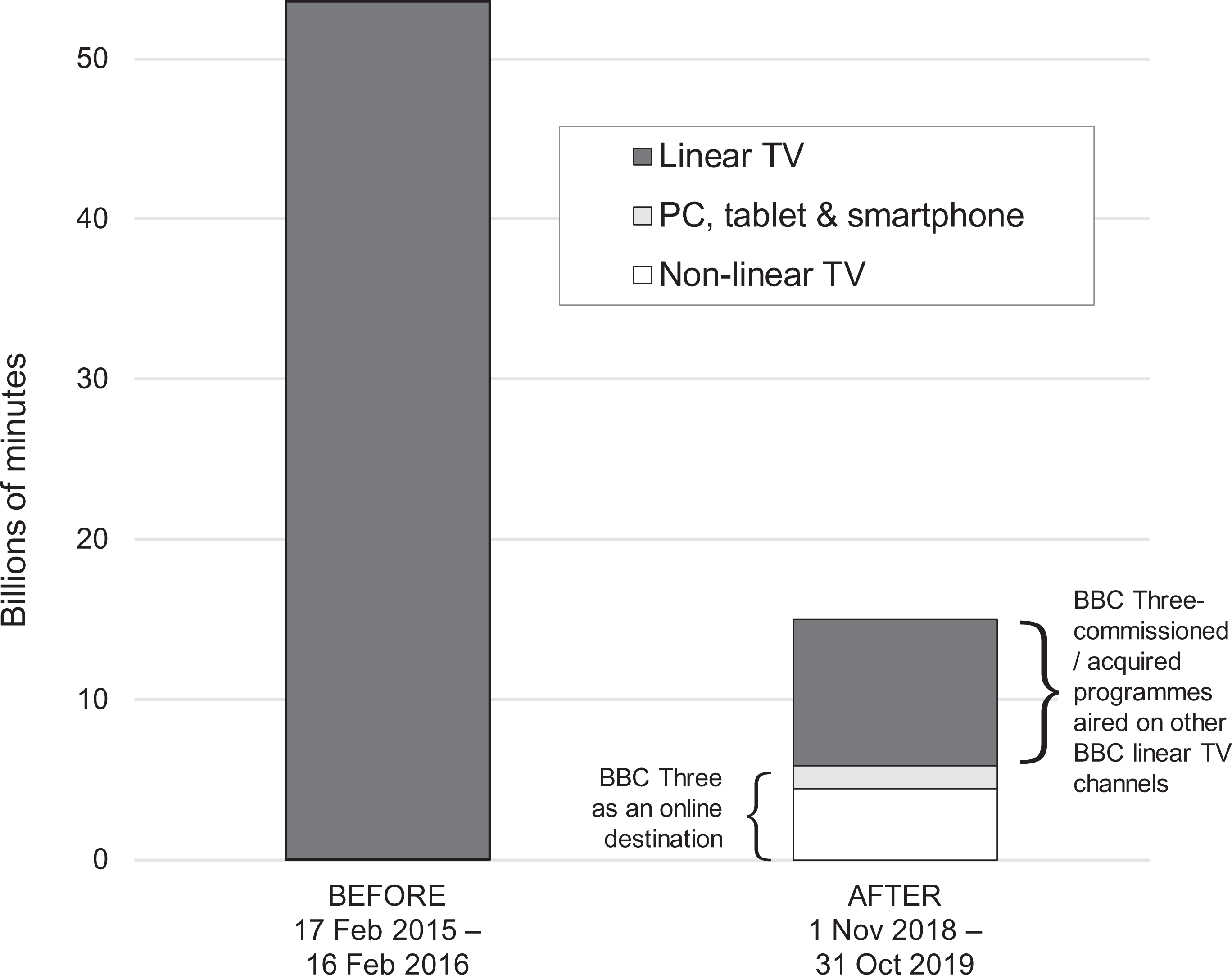

The BARB data show that the annual minutes of viewing of BBC Three via linear broadcast TV in the year before it closed its broadcast platform were 53.59 billion. The minutes of viewing of BBC Three in a 12-month period (November 2018 to October 2019) after were 5.8 billion, 89% less (see Figure 3). Even factoring in the 9.14 billion minutes viewers spent watching BBC Three-commissioned/acquired programmes on the BBC’s remaining linear TV channels, the decline in viewing time was at least 72%. Looking in more detail at how BBC Three was watched online after it closed its linear TV channel reveals that the vast majority of viewing minutes (79% of the total) were via TV sets, while only 9% were via PCs, 7% via smartphones and 6% via tablet computers. For clarity, the online viewing of BBC Three via TV sets is mainly attributable to viewers watching the channel on iPlayer via an internet-connected smart TV or via internet-connected devices – such as Google Chromecast or Apple TV – that are plugged into the TV set.

Minutes of viewing of BBC Three by UK residents (aged 4+) via linear TV in the 12 months before it closed its linear TV channel and via non-linear TV, PCs, smartphones and tablets in a 12-month period (November 2018 to October 2019) after. Also shown for the ‘after’ period is minutes of viewing of BBC Three-commissioned/acquired programmes that aired on other BBC linear TV channels. TV: television. Source: BARB.

Gross half hour claims

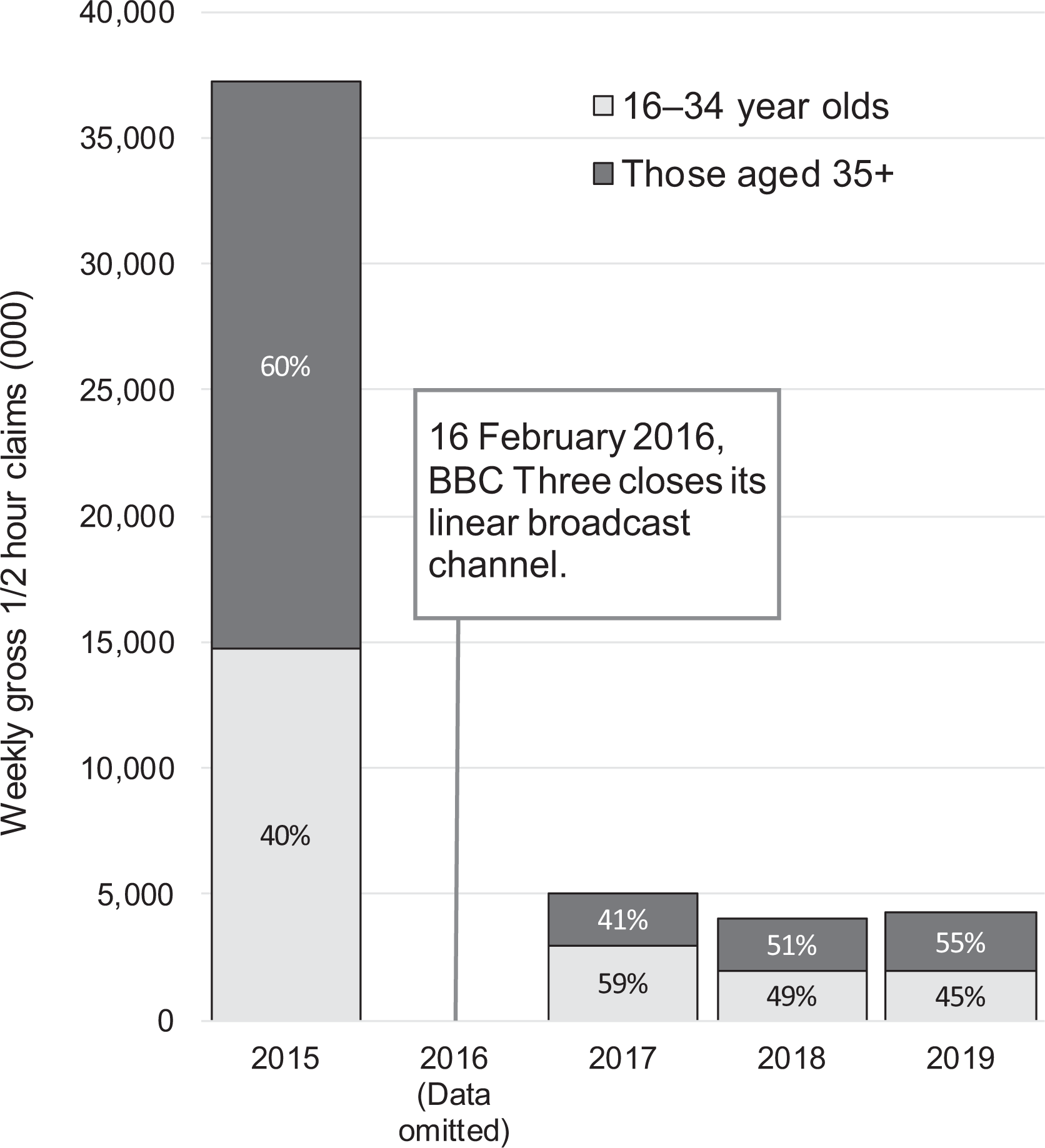

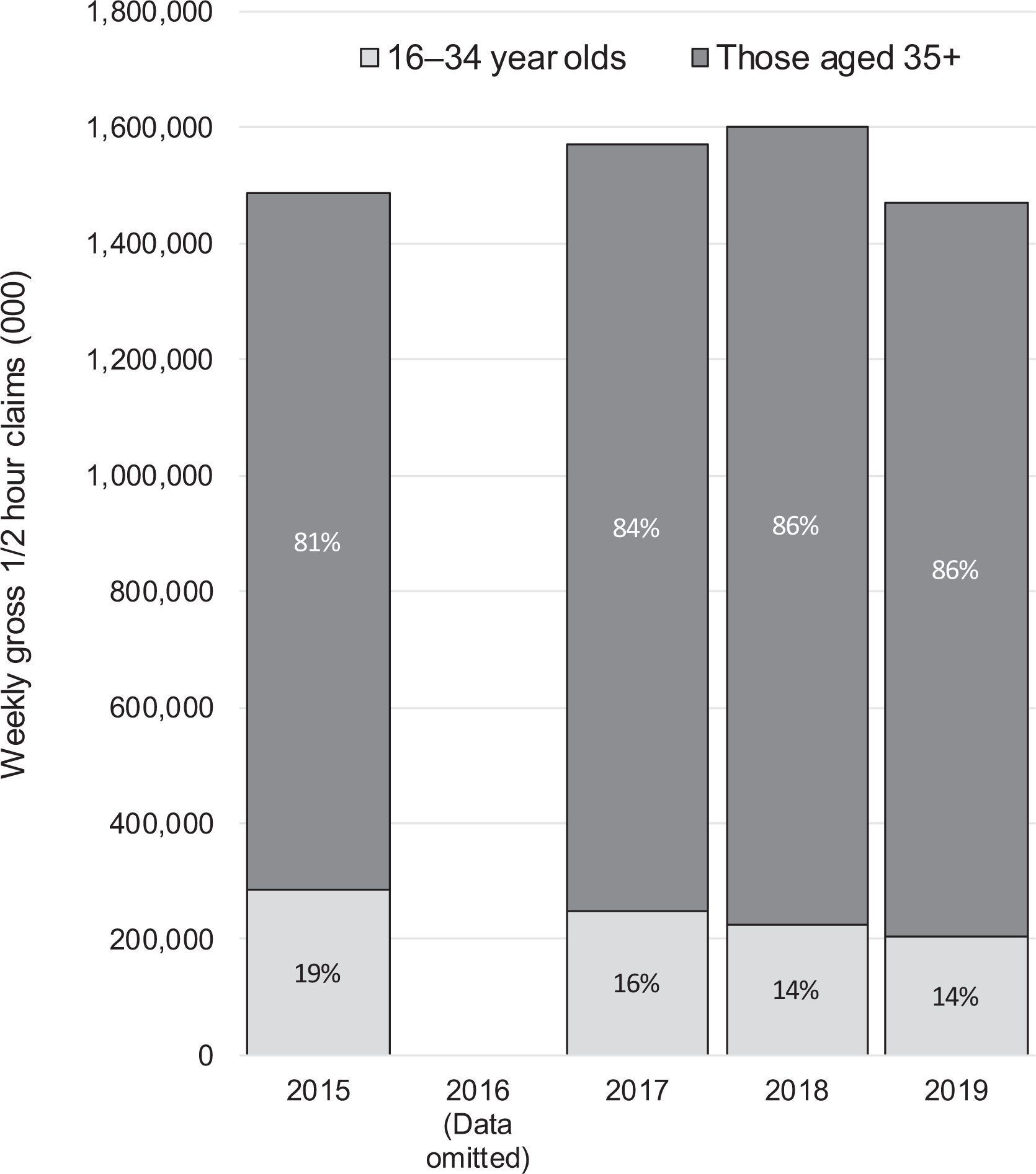

The Touchpoints e-diary data show that, in 2015, the year before BBC Three closed its broadcast platform, the channel attracted 37,208,000 weekly GHCs from British adults aged over 15. In 2017, the year after, that figure had fallen to 5,062,000, a drop of 86%. Weekly GHCs were even lower (4,033,000) in 2018 but stabilized in 2019 (see Figure 4). Among the channel’s target audience of 16- to 34-year-olds, the fall in GHCs between 2015 and 2017 was slightly less (80%) than among all adults. However, by 2019 that difference had all but disappeared, with BBC Three receiving 87% fewer GHCs from its target audience than it did before it closed its linear TV channel, only one percentage point less than the drop for all adults.

Weekly GHCs for BBC Three among its target audience of 16- to 34-year-olds and those aged 35+ in the year before and the 3 years after it closed its linear TV channel. One GHC is registered when one viewer claims to have watched the channel for at least part of a designated half hour period. GHC: gross half hour claim; TV: television. Source: IPA Touchpoints Hub Survey (e-diary).

RQ3: How did the content made available by BBC Three, and the consumption of that content by its audience, change after the channel closed its broadcast platform?

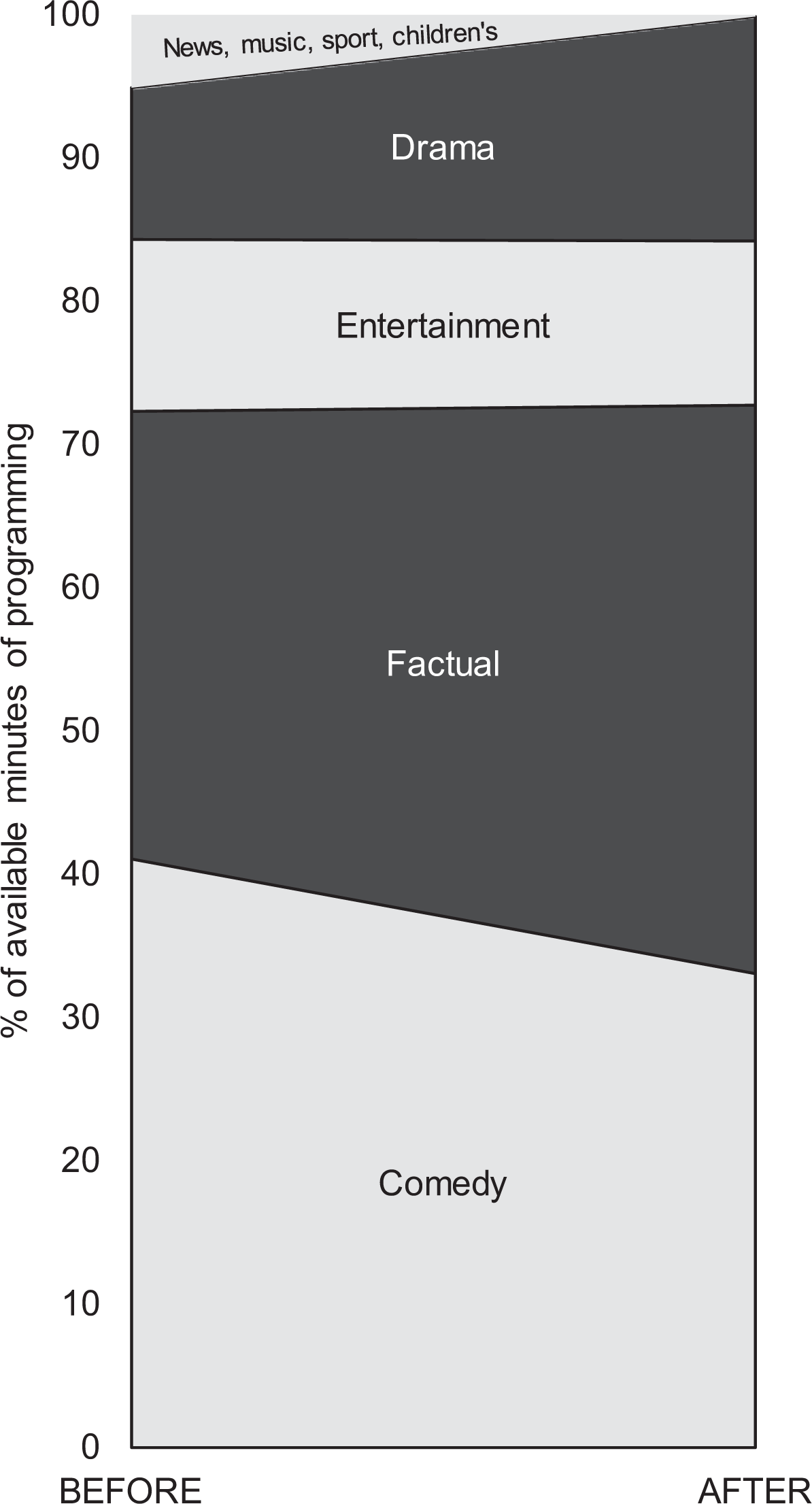

Given that BBC Three’s content budget was reduced – by around 63% – as part of its reinvention online, it is no surprise that the number of minutes of programming available after the switch also fell, by around 80%.

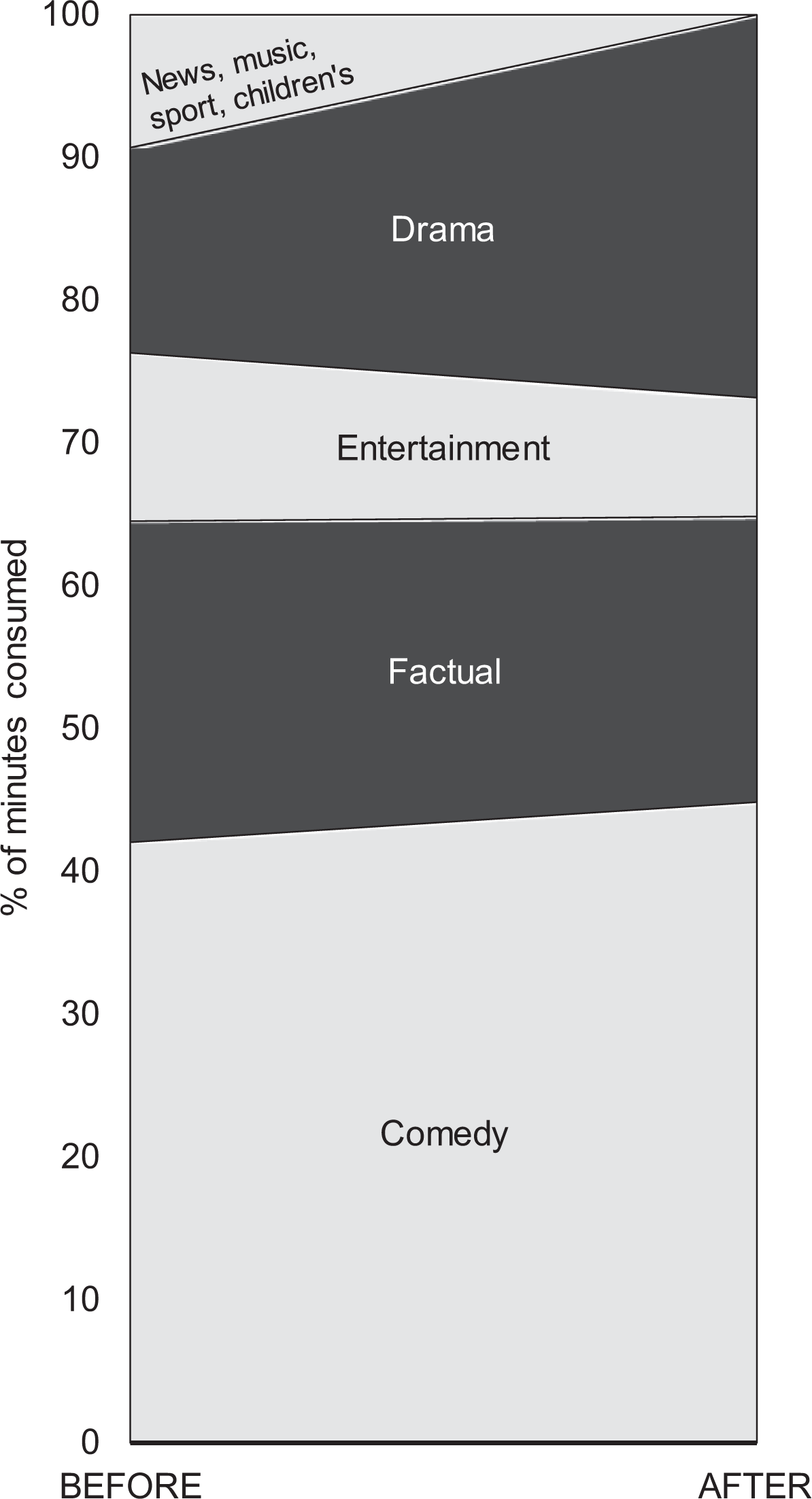

The drama, entertainment, factual and comedy genres represent the vast majority of programming available – and consumed – before and after BBC Three’s reinvention online. Although BBC Three decided that one of the two ‘editorial pillars’ of its reinvention online should be ‘Make Me Laugh’, a term that encompassed comedy and ‘personality-led entertainment’ (BBC, 2015), the proportion of the channel’s output (in minutes) devoted to comedy actually fell post-switch, from 41% to 33%. This is likely a consequence of the decision to strip the channel of its ‘US animation imports’ (Woods, 2017: 142), which included Family Guy and American Dad!, American animated sitcoms that BBC Three had broadcast, on average, more than four times a day. Although comedy made up a lower proportion of the minutes of programming available on BBC Three after its linear TV channel closed, the genre accounted for a higher proportion of viewing minutes after the switch (see Figures 5 and 6).

Changes in the availability of BBC Three programmes of different genres before and after the channel closed its broadcast platform. The data represent the proportions of the channel’s total minutes of (1) linear broadcast output in the 12 months before its linear TV channel was closed and (2) programming available on iPlayer during a 12-month non-consecutive period (November 2018 to October 2019) after the closure. TV: television. Source: BARB and the BBC.

Changes in the consumption of BBC Three programmes of different genres before and after the channel closed its broadcast platform. The data represent the proportions of the total viewing minutes the channel received (1) on linear TV in the 12 months before its linear TV channel was closed and (2) via non-linear TV, PCs, tablets and smartphones in a 12-month non-consecutive period (November 2018 to October 2019) after the closure. TV: television. Source: BARB and the BBC.

The other editorial pillar of the newly online-focussed BBC Three was ‘Make Me Think’, intended to ‘cover drama, flagship factual, authored documentaries, news and current affairs’ (Ramsey, 2018: 159). The proportions of the channel’s output (in minutes) devoted to drama and factual did, indeed, both increase. However, although factual makes up a higher proportion of the minutes of programming available on BBC Three since it closed its broadcast platform, the genre accounts for a lower proportion of viewing minutes after the switch. This is not the case for drama, where there were increases in both the proportional availability of the genre and in its proportional consumption (see Figures 5 and 6).

The minutes of news, sport, music and children’s programming transmitted by BBC Three on linear TV in the year before that platform closed were negligible. These genres have, for all practical purposes, become unavailable since BBC Three was reinvented online. It is no surprise then that, given the unavailability of news, sport and children’s programmes, those genres are no longer consumed, and although there is still some consumption of music programming, it represents just 0.01% of total viewing minutes (see Figures 5 and 6).

Discussion

Audience size

This study has shown that the size of BBC Three’s audience fell by between 60% and 70% in the year after it closed its broadcast platform. Given that the channel was experiencing falls in audience before the switch, it is important to ask how much of the post-broadcast fall was attributable to its reinvention online. Figures 1 and 2 make it clear that the rates of decline were higher (by between about three and five times) in the year after the closure of its linear TV channel than they were in the years before, but it is possible to be sure that this is not in line with what analysts have called a wider ‘relentless decline’ in TV viewing that ‘began in 2011’ (Aquilina and Thomson, 2019)?

To check, Touchpoints data for six of BBC Three’s competitor TV channels, who continued to broadcast, were analysed. The data show that the average audience of these other channels did decline between 2015 and 2017, but to a lesser degree – by between 7% and 15% (see Figures 7 and 8). It is safe to conclude, therefore, that BBC Three’s online reinvention was responsible for at least three-quarters of its fall in audience size.

Average number of British monthly viewers of six UK TV channels (BBC1, BBC2, ITV, ITV2, Channel 4 and E4) that have continued linear broadcasting, 2013–2019. TV: television. Source: IPA Touchpoints Hub Survey.

Average number of British weekly viewers of six UK TV channels (BBC1, BBC2, ITV, ITV2, Channel 4 and E4) that have continued linear broadcasting, 2013–2019. TV: television. Source: IPA Touchpoints Hub Survey.

The large falls in audience size suffered by BBC Three after the closure of its linear TV channel contrast with the changes in net readership that previous studies (Thurman and Fletcher, 2018, 2019) have found for a newspaper – The Independent – and a magazine – the NME – that went online-only. It is necessary, however, to proceed carefully when comparing the changes in net readership that took place at these print publications with the change in net viewers found at BBC Three because of the differences in the frequency with which some of their content platforms are distributed. While they all have a – more-or-less – continuously updated online presence, the NME and The Independent, before they moved online-only, had, respectively, weekly and daily print publications, and BBC Three was a TV channel that broadcast daily. As Thurman and Fletcher (2019) have shown, the big differences that can exist in the frequency with which consumers visit media brands’ on- and offline platforms can interact with the periodicity of their publication intervals and the time period over which readership is calculated to make it impossible to compare changes in readership (1) between media outlets with platforms that issue content with different frequencies and (2) using different calculation periods.

Therefore, no comparison of changes in audience size should be made between the NME and BBC Three. However, a comparison between changes in audience size at The Independent and BBC Three is legitimate if it is made using data calculated over identical time periods. The only data available on post-print changes in readership at The Independent that includes mobile readers are calculated on a monthly basis. Given the importance of mobile devices to newspapers’ readership, it is that data that should use in any comparison with BBC Three. Making this comparison shows that The Independent increased its net monthly readership – by 7.7% – after it went online-only in 2016 (Thurman and Fletcher, 2018), while, as this study has shown, BBC Three’s monthly audience shrank by 63% when it closed its linear TV channel the same year. Why might BBC Three have suffered such a large fall in its monthly audience after it closed its offline platform when The Independent did not?

The primary reason is likely to do with the relative proportions of the outlets’ audiences that consumed them exclusively offline before the outlets closed their offline platforms. At the point it ditched print, The Independent’s monthly online audience dwarfed its monthly print-only audience: in the 12 months up to its move online-only, The Independent’s monthly print-only readership was 1,361,000, just 7.6% of its net monthly readership (Thurman and Fletcher, 2018). By contrast, the BBC reported that, in 2015, only 20% of BBC Three’s weekly viewers also accessed BBC iPlayer in that week (Communications Chambers, 2015: 26).

Because large proportions of The Independent’s net monthly readership were already reached by the brand’s online editions before it went online-only, the impact of losing print-only readers who did not transition to the newspaper’s online editions was negligible. However, because at the point at which BBC Three closed its offline platform, the vast majority of its audience only watched it via linear TV, the impact of losing viewers who only watched the channel on linear TV and did not follow the channel online was substantial.

A second reason for the difference observed between BBC Three and The Independent in how the size of their audiences changed after they closed their offline platforms is likely due to how the size of BBC Three’s audience (see Figures 1 and 2) was already on a downward trajectory when it shuttered its broadcast platform. By contrast, The Independent’s net monthly print and PC readership actually increased between 2013 and 2015, by 7% (National Readership Survey (NRS), 2014, 2015).

Viewing intensity

This study analysed changes in the intensity with which BBC Three was watched after it closed its broadcast platform, using two metrics collected using different methodologies. The first metric, GHCs, is self-report e-diary data. The second metric, minutes of viewing, is passively collected tracking data. Both metrics show that the attention that BBC Three attracted from its audience was hugely reduced after its linear TV channel was closed. It is well understood that different ways of measuring media audiences can give different results, in part because people can both over- (see, e.g. Prior, 2009) and underestimate (see, e.g. Pellegrini et al., 2015) their media consumption. It is reassuring, then, to see two different data sources telling similar stories about the change in intensity with which BBC Three was watched after it reinvented itself online.

Given the size of the fall in GHCs for BBC Three, it seems highly likely that BBC Three’s online reinvention is the primary cause. Looking at Touchpoints data for six of BBC Three’s competitor TV channels that continued linear broadcasting adds weight to this hypothesis, showing that the total GHCs for all these other channels actually increased between 2015 and 2017, by 5.6% (see Figure 9).

Total weekly GHCs for six UK TV channels (BBC1, BBC2, ITV, ITV2, Channel 4 and E4) that have continued linear broadcasting among 16- to 34-year-olds and those aged 35+, 2015–2019. One GHC is registered when one viewer claims to have watched a channel for at least part of a designated half hour period. GHC: gross half hour claim; TV: television. Source: IPA Touchpoints Hub Survey (e-diary).

The similarity of the falls in time spent with BBC Three (−89% if viewing of BBC Three-commissioned/acquired content on other BBC TV channels is excluded, around −72% if it is included), The Independent (−81%) and the NME (−72%) suggest that the negative effects on time spent with media brands caused by the closure of their offline platforms may be similar in degree for both TV stations and print publications.

This study’s results show how over three-quarters of the minutes of online viewing of BBC Three after the channel closed its broadcast platform was via TV sets, and less than a quarter was via PCs, smartphones and tablets. This appears to confirm other research (e.g. Simons, 2009) that suggests the TV set remains the preferred device for consuming televisual content, even for a channel that has reinvented itself online. The reasons for this are likely to do with the social context in which televisual content may be viewed and audiences’ habitual viewing routines (see, e.g. Lee and Lee, 1995).

Content availability and consumption

The results show that the mix of BBC Three programming consumed on linear TV before the channel reinvented itself online differs from the mix consumed after (see Figure 6). This may be due, in part, to how availability of programmes of different genres has changed (see Figure 5). For example, news, sports and children’s programming are no longer available and, therefore, no longer consumed. However, the higher proportional consumption of comedy cannot be explained solely with reference to this genre’s proportional availability, which declined after BBC Three closed its linear TV channel. Similarly, the lower proportional consumption of entertainment and factual programming cannot be explained solely with reference to these genres’ proportional availability, which increased.

As mentioned earlier, multiple factors may have contributed to these changes, including scheduling effects, and changes to the demographics of BBC Three’s audience. The article’s main variable of interest – the change in BBC Three’s distribution mechanism – may have had an effect too. Although it was out of the scope of this study to analyse whether this was the case, theoretically it could have been. For example, based on a survey of 257 American students, Youn (1994) claimed that, in the context of TV, an increase in programme choice enables viewers to choose content that better matches their preferences. Via its linear broadcast, BBC Three was relatively ‘low choice’. Viewers could watch the particular programme that was being transmitted at the time they tuned in – or a slightly wider selection via catch-up viewing. By contrast, its on-demand streaming service is relatively ‘high choice’, offering hundreds of individual episodes simultaneously. It may be, then, that a reason for the higher proportional consumption of comedy on BBC Three after the channel closed its broadcast platform (despite the genre being less available) is because viewers with a preference for the genre were able to choose it at will, freed from the limitations of the TV schedule.

Data limitations

The Touchpoints survey data used to answer RQ1 relies on respondents’ imperfect memories (see, e.g. Prior, 2009). Media diaries can suffer from compliance problems, although e-diaries with built-in reminders – the source of this study’s data on GHCs 5 – can help ameliorate this issue (see, e.g. Lev-On and Lowenstein-Barkai, 2019). Any methodological biases in the Touchpoints data due to recall or compliance issues should be consistent over time, meaning it is possible to be confident about the validity of the trends observed.

Data from BARB were used to estimate the change in minutes BBC Three was watched before and after its broadcast channel was closed and how that viewing was distributed across platforms and programmes. There are a number of limitations in respect of BARB’s data, relating to whether the consumption of BBC Three programmes at particular times and via particular devices and platforms is recorded. A full description of these limitations is included in the Supplemental Material.

Conclusion

Many – including the BBC itself – expected BBC Three’s online reinvention to have negative consequences for how many viewers the channel attracted and for how long. As this study has shown, this was, indeed, the case. The number of monthly viewers fell even further than a BBC-commissioned survey of viewers (Communications Chambers, 2014: 4) suggested it might, with the channel shedding almost two-thirds of its monthly viewers – and a little more than two-thirds of its weekly ones (see Figures 1 and 2). These losses are undeniably a result of its reinvention online, being greater than the more modest falls BBC Three had been experiencing beforehand and the falls experienced by its competitors who continued to broadcast. Also undeniable is the effect of BBC Three’s online reinvention on the intensity with which BBC Three is watched, with GHCs down by 86% and annual viewing minutes after the switch 89% less than the channel achieved on linear TV before (around 72% less if viewing of BBC Three-commissioned/acquired content on other BBC TV channels is included). More surprising, perhaps, is that the size of BBC Three’s 16- to 34-year-old target audience has reduced to a greater extent than the size of its 35+ audience, raising doubts about whether, in the context of BBC Three, young audiences were, as the BBC’s director general suggested, ‘most ready to move to an online world’ (Plunkett and Sweney, 2014). It is perhaps no surprise then that, by May 2020, the BBC’s official position was that ‘there is potentially a strong case for restoring BBC Three as a linear channel’ (BBC 2020), with a final decision due to be made in ‘the autumn’ (BBC News 2020).

Given that the present study is the first to analyse the audience effects on a TV channel of ceasing linear broadcasting, there is a clear need for further research to establish whether the falls in audience size and viewing intensity experienced by BBC Three are typical. The Danish Broadcasting Corporation’s channels DR3 and DR Ultra, which went online-only in January 2020, are obvious case study candidates.

Studies on the substitutability of BVOD services and TV have showed that – at least up to 2012 – the former did not substitute for the latter (Cha, 2013; Taneja et al., 2012) or only did so partially (Jang and Park, 2016). This study has, for the first time, examined such substitutability in the context of the broadcast TV and online platforms of a single media brand, showing that, even by 2018/2019, the online platform – albeit offering fewer and different programmes – was, for most viewers, not a suitable substitute.

More widely, this study develops the nascent ‘theory of media platform cessation’ (Thurman and Fletcher, 2019) by making two original contributions. Firstly, by analysing the audience effects on a TV station as opposed to a periodical, and secondly, by analysing how the availability and consumption of an outlet’s content – rather than the consumption of an outlet in its entirety – changed.

The results suggest that the size of a media outlet’s exclusively offline audience may influence changes in the size of a media outlet’s audience after it closes its offline platform. By comparing BBC Three and The Independent using these variables, this study has provided evidence that lends credibility to this reasonable, but previously untested, hypothesis.

This study also suggests that the sudden and substantial falls in time spent with media brands caused by the closure of their offline platforms may be similar in degree for periodicals and TV stations. In light of the important democratic functions newspapers and public service media (PSM) – like BBC Three, DR3 and DR Ultra – perform, it will be important to monitor how these functions are affected as more periodicals – and perhaps more PSMs – close their offline platforms.

BBC Three’s reinvention online was intended to make its audience ‘laugh’ and ‘think’ and, as has been shown, the proportional availability of some programme genres did change in line with this ethos. Of wider interest, perhaps, is the possibility, suggested by our results, that the change in distribution mechanism altered what viewers chose to watch. To establish whether this was actually the case, however, further research using multivariate analysis would be required that accounted for other influences such as linear scheduling, promotion and availability of episodes on the iPlayer, audience demographics and the levels of marketing, advertising and critical and popular acclaim programmes receive.

Supplemental Material

Supplemental Material, Copy_of_Supplemental_Material_5 - When a TV channel reinvents itself online: Post-broadcast consumption and content change at BBC Three

Supplemental Material, Copy_of_Supplemental_Material_5 for When a TV channel reinvents itself online: Post-broadcast consumption and content change at BBC Three by Neil Thurman in Convergence: The International Journal of Research into New Media Technologies

Footnotes

Acknowledgements

Research assistance was provided by Velina Chekelova, Iuliia Khobotova, Antonia Klatt, Cosima Kopfinger, Iuliia Kozlovskaia, Maire Palias, Kseniia Tikhomirova, Lisa Tratner, Sarah Will, Chaoying Yuan and Tianrun Zhao. The author would also like to thank Simon Bolus, Lindsay Carroll, Daniel Flynn, Tony Forester, John Hobart, Kevin Johnson, Sarah Mowbray, Matt Ross, Doug Whelpdale and Jacob Wieland for their help and support. The Enders Analysis team, in particular Julian Aquilina and Gill Hind, provided additional data and analysis, which helped improve this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was supported by a research grant from the Volkswagen Foundation (A110823/88171).

Notes

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.