Abstract

Some business leaders, just like some artists and politicians, acquire celebrity status and become more visible as star CEOs through increased media attention. However, to date, little has been known about how such celebrity status affects the individual and their organizations. Based on identity control theory and celebrity role constraints logic in the context of upper echelons perspective, this study provides initial empirical evidence on how restaurant CEOs’ celebrity affects managerial risk-taking actions and how CEO-specific and firm-specific factors moderate this relationship. The results indicate that the main effect of CEO celebrity on risk-taking is insignificant. Yet, the dynamic is swayed positively by a CEO’s background, especially when CEOs are outsiders; these celebrity CEOs demonstrate a propensity for bolder strategies. Moreover, as a restaurant firm’s franchising quotient escalates, a star CEO exhibits amplified risk tendencies. The results provide theoretical and practical implications for restaurant corporate governance and shareholders.

Introduction

CEOs have always had influence in various contexts, but their radius of action tended to be mostly limited to their organizational or business setting in the past. Recently, however, more and more CEOs have become public figures by achieving celebrity status, and scholars and practitioners started recognizing the importance of such celebrity status for CEOs themselves, businesses, and society (Gerdeman, 2021). To add value to the discussion, this study attempts to uncover how CEO celebrity affects CEO actions. While CEO celebrity could serve as a benefit and/or burden to firms with celebrity CEOs, we still have a limited understanding of the implications that celebrity has for organizations. Therefore, this study aims to address this gap by providing the first empirical evidence on whether and under which conditions celebrity status affects CEOs’ managerial risk-taking decisions.

Specifically, CEOs in the realm of hospitality and restaurants exert a more pronounced influence compared to their counterparts in other industries (Finkelstein et al., 2009). The restaurant industry is inherently risky, characterized by high volatility, making the decision-making, particularly in risk-taking, a critical focus (De Noble and Olsen, 1986; Parsa et al., 2005; Slattery and Olsen 1984). Moreover, celebrity status augments the discretion granted to restaurant CEOs, as both the CEOs and surrounding stakeholders acknowledge and assimilate their celebrity (Hayward et al., 2004; Sinha et al., 2012). As such, celebrity status awards restaurant CEOs with even greater managerial discretion, which in turn, affects their actions and strategic choices. While star CEOs, or celebrity CEOs, can signal to investors and the public that their firms are socially prestigious and safe, quality businesses that can attract capital and resources, the enhanced visibility that celebrities have could also invite a greater level of social scrutiny, potentially increasing the pressures on the firm (Liu et al., 2022). Given these implications, it is crucial to understand what implications CEO celebrity has on organizations so that stockholders and corporate boards can make informed decisions and govern accordingly.

Although there has been a growing interest in the topic of CEO celebrity, its eventual impact on host organizations’ behaviors or outcomes remains under-explored. One notable gap in the literature pertains to the implications of CEO celebrity on managerial risk-taking behaviors, defined as “the degree to which potential outcomes associated with a decision are consequential, vary widely and include the possibility of extreme loss” (Sanders and Hambrick, 2007:1057). Apart from Cho et al. (2016), few have investigated how a CEO’s celebrity status may influence their propensity for risk. Celebrity CEOs often make strategic decisions that are consistent with their cultivated celebrity identity, revealing a tendency to take risks in preserving this identity (Cho et al., 2016).

Given the emphasis placed on organizations’ risk-taking behaviors within the broader strategic management (SM) literature, it is crucial and timely to delve deeper into the effects of CEO celebrity on such behaviors.. Moreover, this study explores two boundary conditions (CEO origin as a CEO-specific characteristic and franchising as a firm-specific characteristic) to provide a more nuanced interpretation of the main relationship.

To encapsulate, the insights from our study serve to enhance the literature on CEO celebrity by incorporating perspectives from identity control theory and extending upper echelons theory. Moreover, we provide practical implications for the industry, elucidating how celebrity CEOs might shape their firms’ risk-taking behaviors, and emphasizing the potential moderating roles of CEO and firm characteristics.

Literature review and hypotheses development

CEO celebrity

CEOs have historically held pivotal roles within companies, often emerging as the public face of their businesses. This visibility extends beyond corporate circles to the general public. Prominent examples include Steve Jobs, Elon Musk, and Jeff Bezos. In the restaurant industry, CEOs like Howard Schultz (Starbucks), Steve Ells (Chipotle), and David Novak (Yum! Brands) have achieved celebrity, sometimes through avenues other than their culinary expertise (Friedman, 2019; Tan, 2013).

Such celebrity CEOs, while adept at traditional business management, frequently leverage their charisma to draw public attention (Tedlow, 2021). This popularity and celebrity status may influence their managerial decisions (e.g., Malmendier and Tate, 2009; Sinha et al., 2012; Zhou et al., 2023). This leads us to question how CEO celebrity impacts organizational choices, particularly from an upper echelons perspective. In this study, CEO celebrity is defined as “the extent to which a CEO elicits positive emotional responses from a broad public audience” according to Lovelace et al. (2018:421).

The emerging trend of CEO celebrity and its business and social implications have spurred academic inquiry. Initial studies posited that celebrity CEOs likely become overconfident about their abilities when they internalize their celebrity (Hayward et al., 2004). Later, Sinha et al. (2012) further elaborated CEOs’ inclination towards maintaining commitment to failing strategies, implying that celebrity CEOs are rigid in their strategy development and implementation. Furthermore, the compensation benefits enjoyed by celebrity CEOs and their executive teams exceeded those of non-celebrity counterparts (Graffin et al., 2008; Malmendier and Tate, 2009).

While Treadway et al. (2009) theorized positive implications of CEO celebrity, in the form of enhanced organizational reputation and performance, empirical evidence has not been consistent. Some studies indicate diminishing company performance post-celebration of CEO of the Year Award by Financial World (Malmendier and Tate, 2009; Wade et al., 2006). Clearly, the implications of CEO celebrity remain nuanced and warrant deeper exploration, especially concerning organizational risk-taking.

CEO celebrity and risk-taking behavior

CEO celebrity and its implications

Up until now, the primary attention of CEO celebrity research has been on outcomes specific to the CEO, such as enhanced compensation, a greater propensity for attaining external board roles, and amplified protection against termination (Malmendier and Tate, 2009; Wade et al., 2006). It has been observed that senior executives in the same organization as a celebrated CEO also see heightened prospects of ascending to CEO roles in different companies (Graffin et al., 2008). Nevertheless, comprehensive studies focusing on the behavioral outcomes of CEOs, which can be translated to organizational-level consequences, are still limited, and their findings are often ambiguous (Lovelace et al., 2018). This research aims to bridge this gap by exploring the influence of CEO celebrity on their strategic decisions.

The emphasis of this research is on the risk-taking behaviors stemming from CEO celebrity status. A common theme in celebrity CEO research highlights the connection between media-induced CEO celebrity and resulting overconfidence (Hayward et al., 2004; Wade et al., 2008). Though several works delve into the association between CEO overconfidence and risk behavior in management (e.g., Hayward and Hambrick, 1997; Seo and Sharma, 2018), there’s a dearth of empirical data linking CEO celebrity directly with risk-taking. A notable exception is Cho et al. (2016), which tied star CEOs to acquisition premiums, viewing these premiums as a risk metric.

However, Cho et al. (2016) indicated that celebrity CEOs may adopt risks, not necessarily out of overconfidence but to safeguard their cultivated celebrity identity. Yet, many previous studies including that of Cho et al. (2016) operationalized celebrity CEOs with a CEO certificate by Financial World. This approach may not accurately measure CEO celebrity, as these recognitions seem more antecedents than reflections of celebrity, thus raising questions about its construct validity (Pollock et al., 2019).

CEO celebrity and its influence on risk-taking

Understanding the impact of CEO celebrity on risk-taking is essential, given shareholder expectations about CEO risk behaviors (Arrfelt et al., 2018). The diverging viewpoints on risk-taking between shareholders and managers have been pivotal in both theoretical explorations and practical research in strategic management. To illustrate, shareholders, with presumably diversified individual-level investment portfolios, often desire managers of firms to pursue strategies that offer high returns, even if these entail elevated risk-taking. Conversely, managers, due to the large stakes of their professional and financial futures tied to their firm’s performance, tend to lean towards risk aversion given the firm-specific risks they bear (Arrfelt et al., 2018).

CEO celebrity often arises from distinct, noticeable behaviors. To sustain their celebrity status, CEOs may exhibit an amplified tendency towards these hallmark behaviors, such as innovation, strategic shift, or bold, unconventional actions, inherently tied to risk-taking (Lovelace et al., 2018). Media attention on these actions reinforces both stakeholders’ and CEOs' alignment with them (Lee et al., 2020).

Drawing from identity control theory (Burke, 2007), identities are molded via social interactions, with individuals constantly gauging societal feedback to ensure alignment with their self-identities (Burke, 1991). Hence, CEOs embracing their celebrity tend to align their actions with societal expectations. As these CEOs internalize media commendations, largely for their risk-taking actions, they might deliberately uphold or intensify such behaviors to nurture their star identity. Specifically, if these CEOs are praised for risk-taking behaviors, they will consciously sustain or even intensify such behaviors to perpetuate their celebrity. Existing studies indicate that CEOs may adhere more firmly to these perceived formulas for success as they accumulate achievements (Hambrick and Fukutomi, 1991). Thus, celebrity CEOs may emphasize actions that spotlight them, aiming to bolster their social recognition (Adler and Adler, 1989).

Celebrity also subjects CEOs to amplified performance expectations. Intense media scrutiny and high societal expectations can compound the pressure on celebrity CEOs (Cho et al., 2016). To address these escalating benchmarks, CEOs might be inclined to adopt a more risk-oriented approach to elevate their chances of success. Not meeting these standards might jeopardize their celebrity standing and its related benefits, and could harm their self-esteem, pushing them towards greater risk-taking.

Furthermore, their celebrity status, with the accompanying empowerment, might also sway them to risk. Key decision-makers, such as senior executives or boards, could be more accommodating towards celebrity CEOs, observing the societal esteem and respect attached to their celebrity status (Khurana, 2002; Sinha et al., 2012). This could afford the celebrity CEO an increased latitude of action, thereby creating more room for risk-taking (Finkelstein and Hambrick, 1990).

Lastly, considering the central role of positive emotional responses in the conceptualization of celebrity and based on the rationale of Johnson and Tversky (1983) suggesting that positive emotional reactions spur risk-seeking decisions and behaviors, a CEO celebrity may likely lead to an increase in risk-taking behaviors. Hence, this research introduces the subsequent hypothesis:

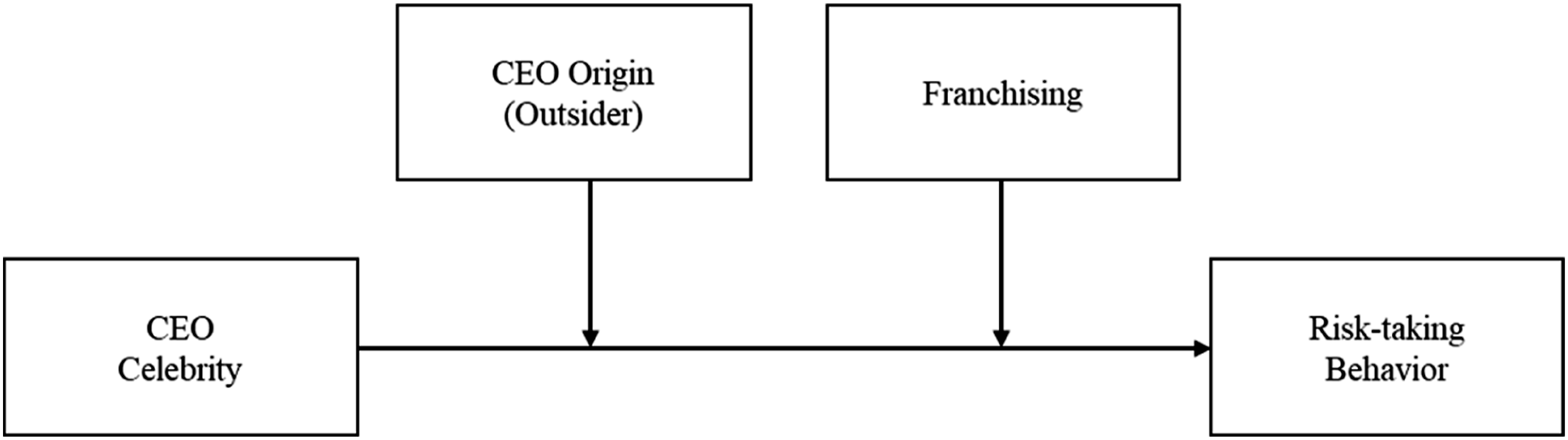

CEO celebrity will be positively associated with risk-taking behaviors.

Moderating role of CEO origin

The origin of a CEO, whether they are an external hire or a promotion from within the organization, significantly affects their strategic decisions (Hambrick and Mason, 1984). Traditionally, CEO appointments have favored insiders, making up the majority of succession decisions. However, in recent times, there has been a discernible shift towards 4/-hiring outsider CEOs as part of deliberate succession planning. By 2018, 27% of new CEOs in S&P 500 companies were external hires (Stuart, 2018), a rise from the 1970s’ 8% (Schloetzer et al., 2017).

CEOs brought in from outside an organization (henceforth referred to as outsider CEOs) might not have the depth of understanding about the firm’s internal culture, knowledge base, and relationships that come from years spent within the organization (Agrawal et al., 2006; Legg et al., 2022). However, when a company opts for an external hire over an insider, it often reflects a value assessment where the perceived benefits of the outsider surpass the intrinsic advantages of an internal hire. Their recruitment might involve significant compensation (Tichy, 2015), signaling heightened performance expectations, and possible increased risk inclination.

Celebrity CEOs, already prone to risk, might further amplify this tendency when they are outsiders. Management literature suggests that when outsider CEOs are appointed, there’s an underlying expectation that they can act as a savior (Khurana, 2002) to invoke significant shirts or revitalize performance (Cannella and Lubatkin, 1993; Lovelace et al., 2018). Highlighting this trend, 58% of CEO hires after high-pressure resignations in 2018 were external (Stuart, 2018). Thus, while internally developed CEOs might preserve the status quo and prioritize consistency over transformative shifts, outsider CEOs, especially celebrities, often show increased risk tendencies (Yunlu and Murphy, 2012).

Outsider CEOs often employ strategies to navigate their ‘outsider' status, potentially augmenting their perceived roles (Powell and Baker, 2014). Their identity, shaped by societal role perceptions (Burke and Tully, 1977), can influence their behaviors. Celebrity outsider CEOs, aligning with such perceptions, might naturally lean into risk.

Given their celebrity status, CEO actions and decisions might face limited criticism from the top management team and stakeholders, encouraging them to replicate their bold strategies that once earned them acclaim. This can prompt outsider CEOs to emphasize risk-taking tendencies that initially boosted their status (Powell and Baker, 2014).

In conclusion, given the expectations placed on outsider CEOs to adopt, often radical, strategies to enhance firm performance, CEO origin potentially influences the interplay between CEO celebrity and risk-taking. The outsider nature of a CEO can amplify the positive impact of their celebrity on risk inclination.

Outside CEO background will positively moderate the relationship between CEO celebrity and risk-taking behaviors.

Moderating role of franchising

Franchising is a defining characteristic in the restaurant sector, accounting for 30% of the total U.S. franchise establishments and almost 60% of the total U.S. franchise employment (Bailey, 2023). The extensive presence of franchising in this sector highlights its critical role.

For individual firms within this landscape, it’s essential to measure the extent to which they embrace the franchising model. In this study, we utilize the “degree of franchising” as our measure. Contrary to a binary understanding, the “degree of franchising” doesn’t simply indicate whether a firm franchises or not. It quantifies the extent of a firm’s reliance on franchising, calculated as the ratio of franchised outlets to the total number of outlets a firm has in a given year (Combs and Castrogiovanni, 1993; Kim et al., 2018). Such a measure provides a granular insight into the strategic choices of individual firms.

Given the restaurant industry’s inherent risks and volatility (De Noble and Olsen, 1986; Parsa et al., 2005; Slattery and Olsen, 1984), franchising serves as a well-established growth strategy (Roh, 2002). One of the main reasons for its widespread adoption is its ability to facilitate efficient scaling of business while concurrently distributing risks with franchisees (Combs and Castrogiovanni, 1993; Lafontaine and Bhattacharyya, 1995). This makes franchising a risk-mitigating strategy in hospitality (Choi et al., 2018; Seo and Sharma, 2018; Sun and Lee, 2016).

Considering the current restaurant market’s saturation (IBIS Report, 2023), franchising provides celebrity CEOs a safeguard against variable investment risks, allowing for more ventures associated with higher risk (Lafontaine and Bhattacharyya, 1995). Predictable income streams from branding such as loyalty fees enable firms to mitigate anticipated risks within this fluctuating market (Seo, 2016; Spinelli et al., 2004

Consequently, we posit that in the restaurant industry, the degree of franchising amplifies the association between CEO celebrity and risk-taking, offering added scope for celebrity CEOs to embrace their distinctive approaches and pursue risk, while simultaneously growing their business and mitigating investment risks through the franchise model.

The degree of franchising will positively moderate the relationship between CEO celebrity and risk-taking behaviors. Taken together, the conceptual model of the study is illustrated in Figure 1.

Conceptual model.

Methodology

Sample and data

This study scrutinizes U.S.-based publicly traded restaurant companies. We source essential financial and franchising information from the Compustat database, supplementing it with annual reports and proxy statements that are relevant to each year under consideration. To gather comprehensive CEO-specific data such as their outsider status, age, and tenure, we turn to a variety of authoritative sources. These sources comprise the Execucomp database, Bloomberg’s Executive Profile and Biography sections, relevant press releases, and the annual reports of the respective companies. In assessing the public visibility and recognition of these CEOs, a key component of our study to measure CEO Celebrity, we utilize the FACTIVA database to examine media coverage. Specifically, we focus on articles that mention both the CEO and the organization’s name at least twice during the CEO-year for analysis.

Our analysis incorporates a broad spectrum of 51 unique publicly traded restaurant companies and 108 distinct CEOs. The timeframe for our study spans from 1992 to 2019. This period is chosen deliberately: 1992 represents the earliest year for which comprehensive data is available in our dataset, ensuring a wide-ranging historical analysis. The endpoint of 2019 is selected to preclude the distorting impact of the COVID-19 pandemic on the industry, thus maintaining the integrity of the study’s focus on long-term trends and patterns. Depending on the analytical model applied, the total number of observations ranges from 651 to 678.

Variables

Dependent variable

Aligning with seminal works in the strategic management field (Sanders and Hambrick, 2007) and extending into hospitality and tourism research (Lee and Moon, 2016; Seo and Sharma, 2018), this study operationalizes risk-taking based on the magnitude of expenditures in three domains that are traditionally associated with high-risk and forward-looking longer-term investment activities (Beckman and Haunschild, 2002). Specifically, these expenditures include capital investment, research and development (R&D), and acquisitions. Due to a noticeable number of low or zero R&D expenditure cases in our restaurant dataset, we have adjusted the expenditure figure by adding a constant of one before applying a logarithmic transformation. This step helps manage the data’s skewness. We then combined the adjusted figures by summing the logarithmically-transformed values of R&D, acquisition, and capital expenditure investments, thereby providing a holistic measure of an entity’s propensity for engaging in high-stake, long-term financial commitments.

Main variables

We measure the independent variable, CEO celebrity, adopting the recent measure of Lovelace et al. (2022) with two dimensions: (1) the amount of media attention a CEO receives and (2) the degree to which such media coverage entails positive emotional responses towards a given CEO. Most existing literature used the CEO of the Year award by Financial World in operationalizing CEO celebrity; however, the recent literature that differentiates the construct of status from celebrity suggests that such award and certification are rather the reflection of status than celebrity and they are at best precedent or a contributing factor to CEO celebrity rather than the reflection of their celebrity, hence lacking the construct validity (Pollock et al., 2019).

To measure media attention, we created a multi-item index from media content including news, magazine articles, and broadcast transcripts, including only instances where a CEO was mentioned by name at least twice. If a CEO appears on the cover page or in feature/special articles or lead stories or is mentioned by name in the title, more weight has been given as these instances signal heightened visibility. Once the analysis across the three media elements was complete, we standardized each value by fiscal year, forming a comparably indexed social attention score. We subsequently combined these components to form a holistic annual measure of social attention.

Next, we evaluated the emotional responses expressed in media coverage, the second crucial aspect of celebrity. We downloaded all the articles and broadcast transcripts from the Factiva database and conducted content analysis utilizing Linguistic Inquiry Word Count (LIWC). We evaluated the valence of each piece, either positive or negative, using LIWC. The ratio of content evoking a positive emotional response to total affective content was then calculated for all qualifying articles or transcripts. Each CEO was then assigned an annual standardized composite score summarizing the proportion of positive emotional responses which is the sum of the standardized average proportion of positive emotional responses to total affective contents for each source (news articles, business magazine articles, and broadcast transcripts) by year. Finally, our measure of celebrity was derived by combining these two essential elements. We calculated the celebrity score by multiplying the composite of the summarized social attention and the aggregate positive emotional responses for each CEO per year (i.e., celebrity score = the consolidated measure of overall social attention received x the combined ratio of positive emotional responses garnered by each CEO annually).

CEO outsider status is coded as one when a CEO is appointed from outside the company within 3 years of taking over the role (Quigley et al., 2019; Zhang and Rajagopalan, 2010), and 0 in all other instances. To assess the impact of a CEO’s external origin, only those who have served in the firm for over a year are evaluated. The franchising degree is gauged by the proportional count of franchised establishments relative to the company’s overall property (Combs and Castrogiovanni, 1993; Kim et al., 2018). Thus, the franchising degree equals the number of franchised locations divided by the firm’s total count of restaurant locations.

Control variables

Several control variables were included to account for possible confounding effects. Firm size, measured by the natural log of firm sales, is controlled as it affects the slack resources available for investment spending (Daniel et al., 2004; Sanders and Hambrick, 2007) as well as the amount of media attention that firms with different sizes could receive, which can affect corporate risk-taking and CEO celebrity, respectively. Past firm performance at t-1 is included due to its generally positive association with risk-taking propensity (Bromiley, 1991; Song et al., 2024). At the CEO level, CEO tenure, measured by the number of years in office in a given firm, and CEO age are included because they could affect one’s risk preference and behaviors (Park et al., 2018; Serfling, 2014).

Econometrics estimation

Given that this study hypothesizes a relationship between celebrity and strategic risk-taking behavior, moderated by a time-invariant variable (CEO outsider origin), a fixed-effects model would be unsuitable for exploring this relationship. Consequently, adhering to the methodologies of preceding research (Wade et al., 2006) and acknowledging the benefits of Generalized Estimating Equations (GEE), this study employs GEE for hypothesis testing. GEE is a favored method in upper echelons research due to its computational simplicity compared to maximum likelihood estimator alternatives and its flexibility in distributional assumptions. For instance, while Wade et al. (2006) utilized a fixed-effects model as their primary method to study the influence of CEO celebrity on a company’s abnormal returns, they also applied GEE for supplementary robustness checks. Subsequently, Cho et al. (2016) applied GEE to study the correlation between CEO celebrity and risk-taking, addressing static crucial variables in line with our research.

Results

Descriptive statistics

Drawing from the Standard Industry Classification code 5812 (referring to eating establishments), the preliminary panel data earmarked for analysis encompassed 2913 firm-year observations. After listwise deletion of missing values and excluding outliers with studentized residual values exceeding the absolute value of 4, the conclusive sample size for our main analyses ranges from 651 to 678.

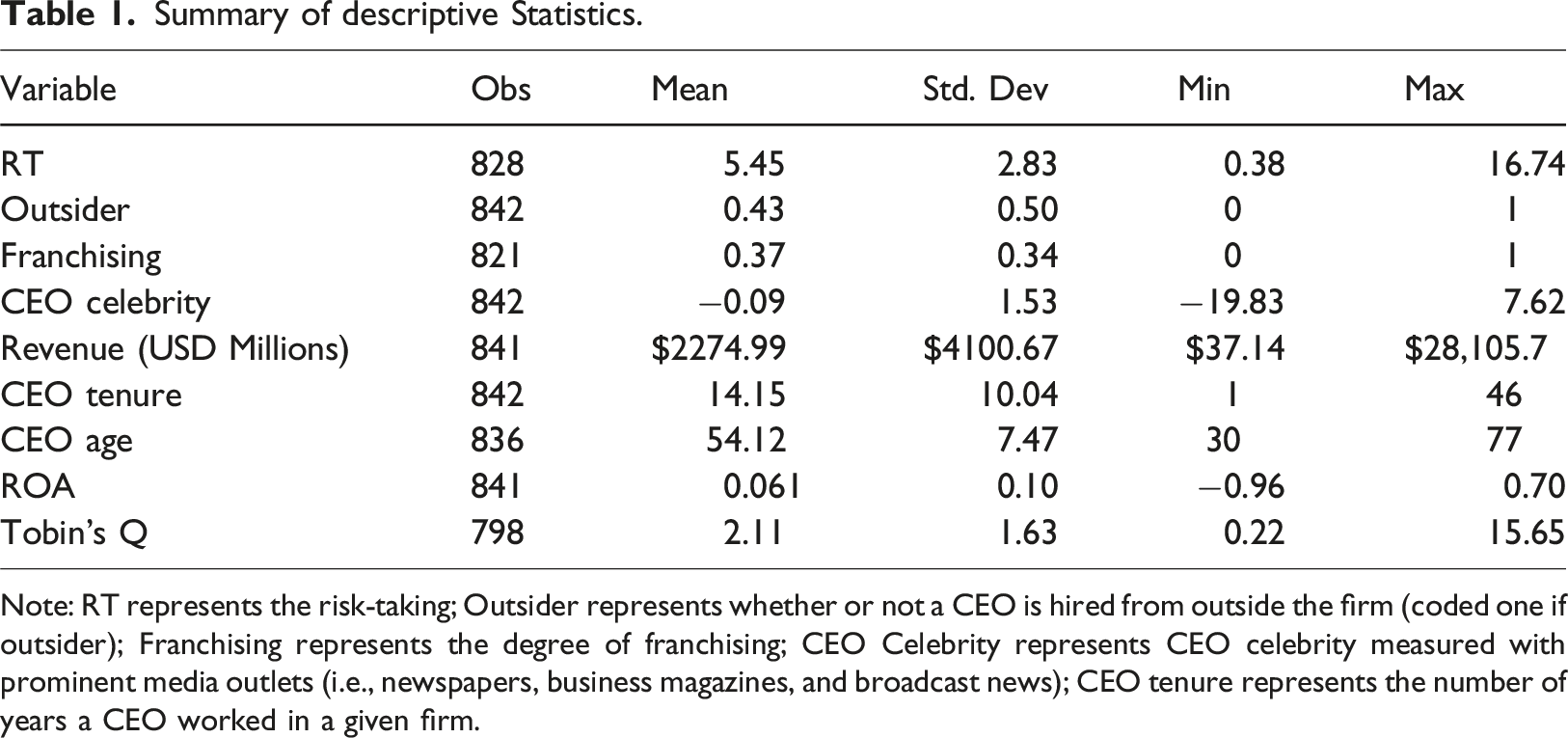

Summary of descriptive Statistics.

Note: RT represents the risk-taking; Outsider represents whether or not a CEO is hired from outside the firm (coded one if outsider); Franchising represents the degree of franchising; CEO Celebrity represents CEO celebrity measured with prominent media outlets (i.e., newspapers, business magazines, and broadcast news); CEO tenure represents the number of years a CEO worked in a given firm.

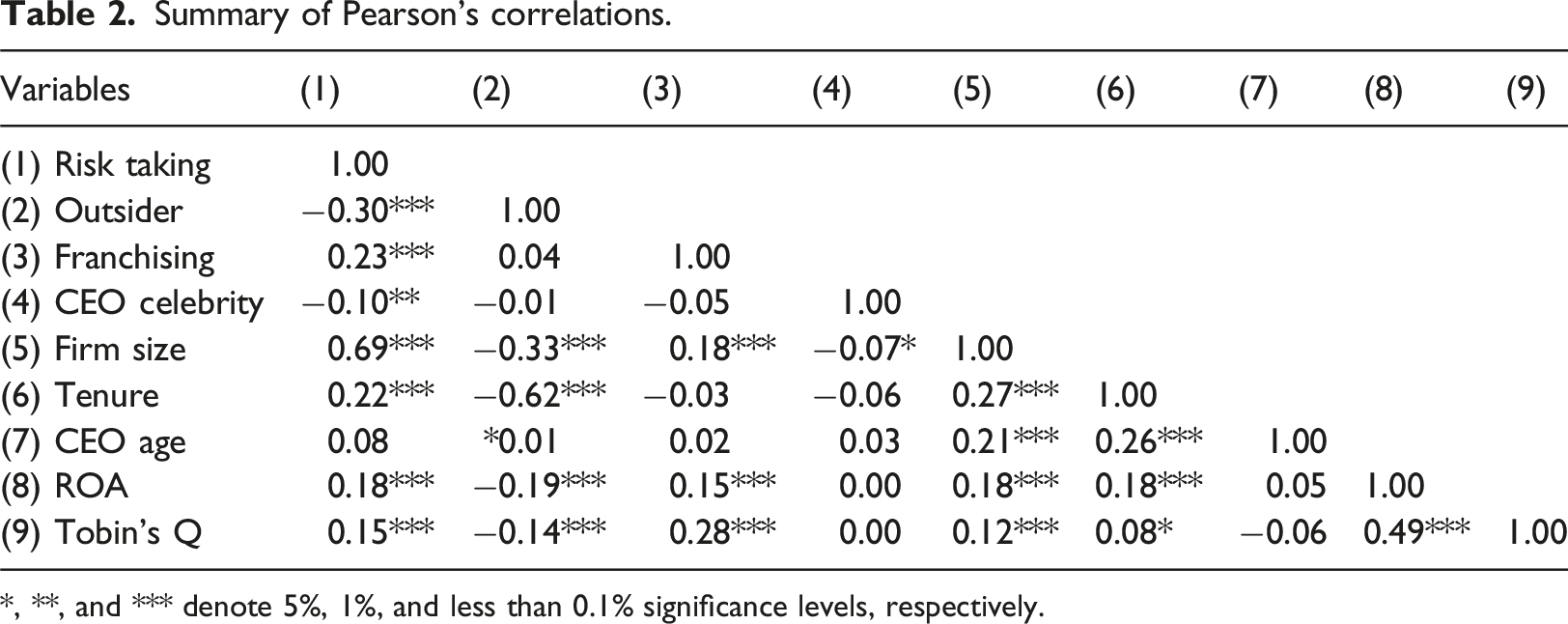

Summary of Pearson’s correlations.

*, **, and *** denote 5%, 1%, and less than 0.1% significance levels, respectively.

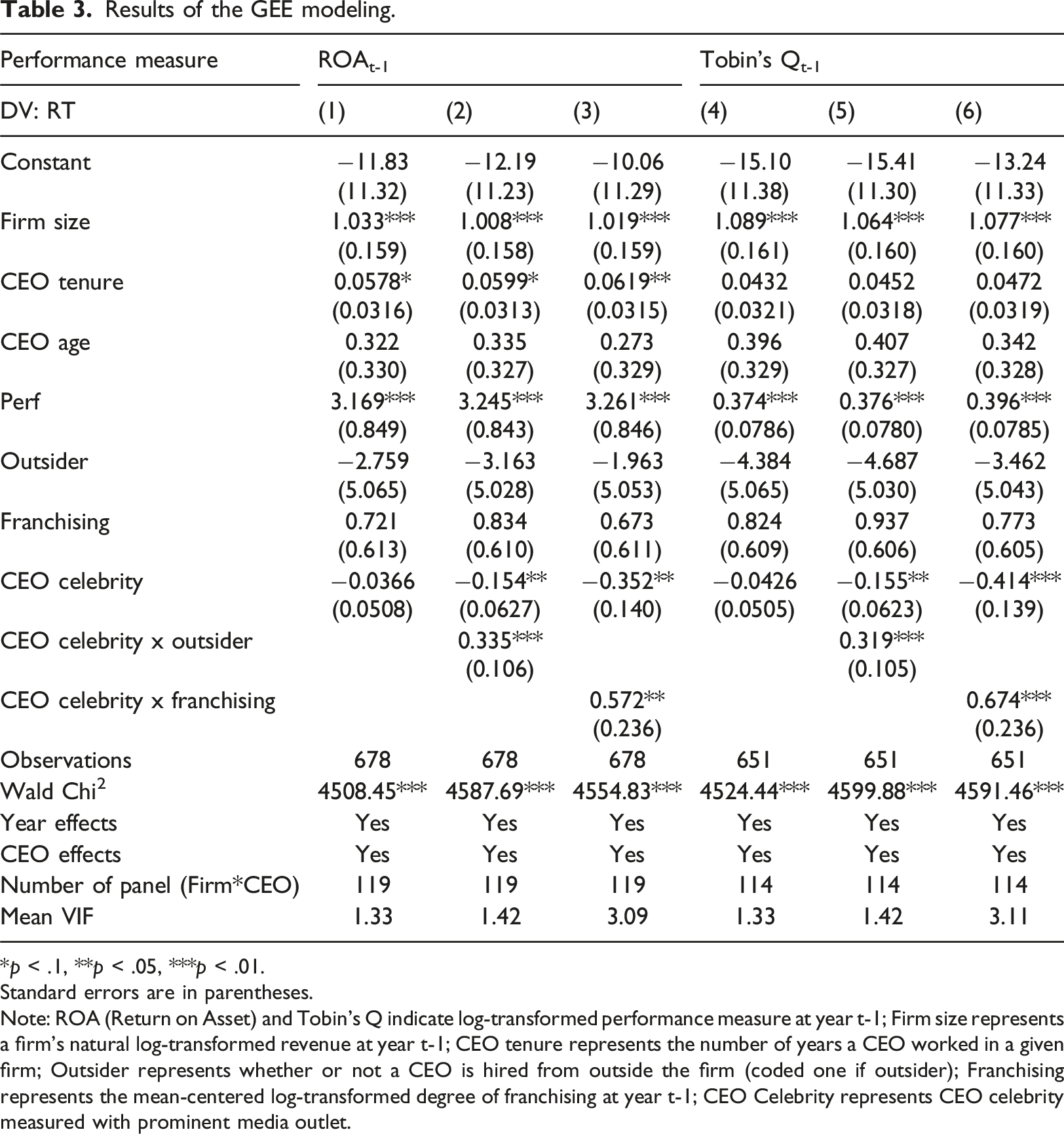

Results of the GEE modeling.

*p < .1, **p < .05, ***p < .01.

Standard errors are in parentheses.

Note: ROA (Return on Asset) and Tobin’s Q indicate log-transformed performance measure at year t-1; Firm size represents a firm’s natural log-transformed revenue at year t-1; CEO tenure represents the number of years a CEO worked in a given firm; Outsider represents whether or not a CEO is hired from outside the firm (coded one if outsider); Franchising represents the mean-centered log-transformed degree of franchising at year t-1; CEO Celebrity represents CEO celebrity measured with prominent media outlet.

Main analyses

Table 3 provides the results of the GEE modeling of the main analysis using RT as a dependent variable, incorporating R&D spending, capital investment, and acquisition investment. Models (1) and (4) in Table 3 portray the fundamental impacts of CEO celebrity on risk-taking behaviors. With control variables kept constant, the coefficients for CEO celebrity remain consistently negative and statistically insignificant across models for CEO risk-taking behaviors (i.e., b = −0.0366, p = .471 in Model (1); b = −0.0426, p = .399 in Model (4)). Hence, Hypothesis 1, proposing a positive, significant linkage between CEO celebrity and risk-taking, does not find support.

Subsequently, Models (2) and (5) from Table 3, reveal the moderating role of CEO origin in delineating the link between CEO celebrity and CEO risk-taking behaviors. Keeping the control variables constant, these models consistently indicate the positive moderating impact of outsider CEO on the links between CEO celebrity and risk-taking actions models (i.e., b = 0.335, p = .002 in Model (2); b = 0.319, p = .002 in Model (5)) at a significance level of 0.1%. Thus, strong evidence supports Hypothesis 2.

Meanwhile, the moderating role of franchising in determining the relationship between CEO celebrity and CEO risk-taking behaviors is presented in Models (3) and (6) in Table 3. While maintaining constant control variables, a consistently positive and significant moderating impact of franchising on the relationships between CEO celebrity and risk-taking behaviors is observed across these models (i.e., b = 0.572, p = .016 in Model (3); b = 0.674, p = .004 in Model (6)) at a 5% significance level. Therefore, Hypothesis three is strongly supported.

Sensitivity analysis

To alleviate any potential endogeneity issue, the Gaussian copula approach was conducted as a sensitivity analysis. It is an instrument-free method that can directly model the correlations between the endogenous regressor and the error term by using a copula (Park and Gupta, 2012). In summary, the analysis including the copula term alone without lagging reveals that the copula term itself is statistically insignificant and the results for the interaction term remain largely unchanged. Next, the analysis with the lagged copula term showed that the copula term becomes statistically significant, but it still did not alter the significance of the main results for the interaction term. These results underscore the robustness of our main results.

Discussion and conclusion

This research aimed to uncover how the celebrity of restaurant CEOs affects their managerial actions and to examine conditions moderating this relationship. Specifically, we investigated the link between CEO celebrity and risk-taking actions, considering the CEO origin and the firm’s franchising degree. Through GEE modeling, we identified a significant and positive moderation effect for both CEO origin and franchising, but a nonsignificant main effect of CEO celebrity on risk-taking behaviors.

First, the finding of the nonsignificant main effect of CEO celebrity may suggest that celebrity CEOs in the restaurant industry are triggered to more aggressively engage in risk-taking behaviors only under certain conditions (e.g., being outsider CEOs and/or when employing a higher degree of franchising as revealed in the current study). This may imply that celebrity CEOs in the industry tend to be significantly influenced by their conditions and environments which signifies the importance of potential boundary conditions for a better understanding of the effect of their celebrity status. This can be a meaningful avenue to be explored further in the future.

Second, the origin of the CEO, meaning whether they are recruited externally or promoted internally, significantly impacts the strategic decisions made by CEOs (Hambrick and Mason, 1984). As posited in this research, findings indicate that CEOs brought in from outside the company, particularly those with celebrity status, are prone to adopt riskier strategies. Companies often recruit outsider CEOs, particularly those with celebrity status, to adopt riskier strategies with hopes of revitalizing the firm (Cannella and Lubatkin, 1993; Lovelace et al., 2018). Consequently, such outsider CEOs often employ a range of strategies to navigate their new environments, including adopting riskier approaches, a tendency that is accentuated when the CEO has celebrity status and recognition.

Third, this study additionally evaluates the role of franchising as a moderator, a pivotal strategic approach at the firm level within the restaurant industry. As expected, increased franchising strengthens the relationship between CEO celebrity and risk-taking. The results manifest that through franchising, restaurant companies can hedge risks whilst extending their business with diminished investment risks, thereby providing celebrity CEOs in the restaurant sector with expanded latitude for risk-taking.

Additionally, the results concerning the moderating roles of CEO origin and franchising remain significant and uniform, incorporating both market and accounting-based performance indicators as control variables (i.e., previous year firm performance based on ROA and Tobin’s Q). These results may suggest that implications of CEO celebrity for their risk-taking behaviors within the restaurant sector may be affected by ROA and Tobin’s Q in a similar manner and scope.

This research enriches both the fields of celebrity and hospitality literature by offering initial empirical insights into the influence of the celebrity status of restaurant CEOs on managerial risk-taking decisions. Despite the relatively high degree of managerial leeway restaurant celebrity CEOs could have, the implication of CEO celebrity for the restaurant firm in various contexts and especially CEO behavioral outcomes such as risk-taking behavior in this study have been rarely explored. Thus, this research addresses an existing gap in hospitality studies, presenting the first evidence on the consequences of celebrity status amongst restaurant CEOs, intertwined with crucial moderating elements pertaining to CEO and organizational factors.

Moreover, the findings of this study enhance the understanding of both the risk-taking and upper echelons domains, underscoring the significant role of CEO characteristics within an organization. Specifically, this research elucidates the moderating impact of CEO origin, indicating that the outsider status of CEOs propels those with celebrity to embrace more risks—a factor seen as favorable by investors given the generally risk-avoiding tendency of many CEOs and managers (Sanders and Hambrick, 2007). Additionally, by unveiling the positive moderating influence of franchising, the insights obtained from this study shed light on a crucial contingent element that fosters risk-taking tendencies in CEOs, especially those with celebrity status.

Practically, this research yields valuable insights into the restaurant sector. Boards of directors (BOD) and CEO hiring committees may consult the findings to understand that CEO celebrity per se does not automatically increase firm-level strategic risk-taking. However, it should be noted that outsider CEOs and the degree of franchising increase the risk-taking actions of celebrity CEOs. Therefore, BOD and shareholders might consider external CEO appointments to increase the chance of securing a risk-prone manager, aligning with shareholder preferences. Investors aiming for high-risk, high-reward portfolios may also find the results beneficial. Particularly, celebrity CEOs, especially those appointed externally, exhibit a higher propensity for risks compared to their less renowned counterparts. Furthermore, celebrity CEOs leading firms with extensive franchising are more prone to risks compared to those in firms with limited franchising, enabling investors to tailor their investment portfolios aligned with their risk preferences.

Limitations and future research

This study, while making significant contributions, is not without its constraints. The initial sample size is restricted, mainly due to data availability across multiple sources and media coverage. We based our measurements on corporate reports, newspapers, business magazines, and broadcast news. If any components from these sources were missing, a reliable dataset could not be composed. Therefore, the corresponding measure was not observed. Nevertheless, our analyzed data is the best available at the time, and the significant findings regarding the two moderating effects, despite the sample size, are encouraging.

Next, although the current celebrity measure used in this study is the most up-to-date measure, it does not integrate a social media component, which is increasingly molding public opinions. Social media conversations significantly influence perceptions about CEOs, and people may be more influenced by their social media circle’s views than by mainstream media. However, using social media as a primary metric for CEO celebrity can be misleading. The content might not mirror public interest, might be biased due to CEO preferences or specific follower groups, or could be managed by PR teams, leading to potential biases.

In today’s digital age, audiences choose their information sources more selectively (Schrøder, 2014). This shift demands rethinking of traditional celebrity measures, especially for public figures like CEOs. Future studies could delve into how this selective engagement on social media impacts CEO attention perception and valence. Additionally, a comparative study on the influence of social media interactions versus traditional media on the volume and valence of attention a CEO receives could be enlightening.

Building on our findings about the CEO’s celebrity and its impact on risk-taking and boundary conditions that moderate this relationship, future studies can explore the underlying mechanism of these quantitative results. For example, investigating how stakeholders such as internal managers and top management teams perceive and interact with celebrity CEOs and how CEO celebrity impacts the company’s decision-making culture and performance could be a fruitful avenue. For a comprehensive understanding, qualitative methods might also be a valuable investigative tool.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Author biographies

Bora Kim is a senior lecturer in the School of Hospitality and Tourism Management at the University of Surrey. She examines managerially relevant questions in the tourism and hospitality industry from the perspective of strategic and financial management. Her research interests include corporate social responsibility, sustainability, and strategic leadership.

Seoki Lee is a professor in the School of Hospitality Management at the Pennsylvania State University in the U.S. His research mainly focuses on hospitality and tourism issues in strategic and financial management including the following topics: corporate social responsibility, ESG, sustainability, internationalization, franchising, diversification, and top management team.