Abstract

It has become a common practice for restaurant firms to spend amounts exceeding their earnings on share buybacks by depleting their cash reserves or even by borrowing money. Given restaurant firms’ limited ability to generate internal cash and the high cost of debt financing, using these means to finance share buybacks could jeopardize restaurant firms’ long-term success. However, little is known about the factors influencing restaurant firms’ tendency toward this seemingly aggressive buyback behavior. This study revealed that the more restaurant firms’ earnings reduce, the greater their tendency is to conduct such aggressive share buybacks. This result could provide some evidence that managerial self-serving behavior plays a role in aggressive share buybacks in the restaurant industry. The study also demonstrated that the positive impact of reduced earnings on aggressive buybacks becomes stronger as a firm’s degree of franchising increases.

Introduction

Firms have two main ways of distributing their earnings to shareholders: the most traditional dividend payouts and the relatively new share buybacks. A share buyback occurs when a publicly traded firm decides to repurchase some of its own shares, thereby reducing the number of its outstanding shares (Pettit, 2001). Reducing the total number of outstanding shares gives each shareholder a bigger percentage of the firm’s ownership. Therefore, share buyback is viewed as another, albeit indirect, approach to distributing a firm’s earnings to shareholders besides dividends (Weigand and Baker, 2009). Moreover, increasing each shareholder’s ownership by repurchasing shares makes a firm’s shares more attractive to investors, thereby enhancing the firm’s stock price (Liu and Swanson, 2016).

However, critics of share buybacks have long expressed their concern that firms are distributing alarmingly high proportions of their earnings to shareholders through share buybacks (JonesJun, 2021; Lazonick, 2014; Teitelbaum, 2019). For example, in the past two decades, more than 80% of S&P 500 profits went toward share buybacks (DB Asset allocation, 2019). Critics have argued that companies using exceedingly large proportions of their earnings for stock buybacks would be diverting cash from other important investments, such as pursuing growth opportunities, paying higher employee wages, creating more jobs, and fostering innovation (Anwar, 2020; Wohner, 2021). The restaurant industry is no exception to this trend. Publicly traded U.S. restaurant firms were reported to have spent more on buybacks than they earned in net profits from 2015 to 2017 (Tung, 2018). In other words, restaurant firms had to drain their cash reserves or even use borrowed money to conduct share buybacks.

Spending more than what a firm earns on share buybacks could be especially problematic for restaurant firms. Restaurant firms are characterized by low profitability (Mun and Jang, 2018). Therefore, restaurant firms’ short-term ability to generate sufficient cash through business activities is limited, making their cash reserves and unused debt capacity potentially crucial for financing unexpected or unplanned future expenses. Especially given the high capital-intensive nature of restaurant firms (e.g., high fixed assets) (Lee, 2010; Lyssimachou and Bilinski, 2022), a significant amount of cash spending is required for restaurant firms to purchase, maintain, update and renovate fixed assets. In addition, since the restaurant industry is highly susceptible to economic conditions (Koh et al., 2018; Lee and Ha, 2012), as evidenced by the fact that one of the first expenses people reduce during a recession is non-essential dining out and travel expenses, restaurant firms may have a great need to secure their cash reserves and debt capacity in preparation for economic downturns.

However, financing share buybacks by depleting cash reserves and debt capacity inevitably limits the ability to use those funds for such future expenses (Anwar, 2020; Lazonick et al., 2020; Wohner, 2021). Unsurprisingly, the market is expressing great concern about this aggressive share repurchase behavior in the restaurant industry. For example, in 2016, Moody’s and Standard & Poor’s (S&P), the two largest credit rating agencies, downgraded McDonald’s credit rating from A to BBB (Sharma, 2018). This downgrade occurred soon after McDonald’s announced that it was issuing more debt to finance its share buyback program (Fitch Ratings, 2019). As mentioned, the credit market’s concern may be due to a perception that restaurant firms’ aggressive share buybacks are having a detrimental impact on firms’ long-term success and debt fulfillment ability.

Despite the anticipated negative impact of share buybacks exceeding earnings on restaurant firms’ long-term success and the market’s great concern about it, limited effort has been made in the restaurant industry to understand the determinants of this phenomenon. As previously mentioned, share buybacks are considered an alternative to dividends as a way of distributing earnings to shareholders (De Vries et al., 2012; Zhou et al., 2013). However, in the restaurant industry, firms could conduct more aggressive share buybacks when they experience a greater reduction in earnings. Specifically, due to the great vulnerability of restaurant demand to external factors, such as seasonality and economic conditions (Koh et al., 2018; Lee and Ha, 2012), and the high capital intensity of the industry (Lee, 2010), restaurant firms’ earnings could be highly volatile. Consequently, restaurant firms may have an innate difficulty in managing their earnings per share (EPS) figures, to which firm managers’ compensation is closely tied (Young and Yang, 2011). In this case, frequent reductions in EPS due to highly volatile earnings can be artificially remedied by reducing the number of outstanding shares through share repurchases. Therefore, restaurant managers could be encouraged to employ share buybacks to overcome their innate difficulty in managing EPS, thereby securing their compensation. Although not in the context of share buybacks, the close linkage between managers’ desire to pursue private benefits and their short-sighted behaviors was proposed by the bonus plan hypothesis regarding earnings management (Setyorini and Ishak, 2012; Yanti et al., 2019) and the empire-building hypothesis regarding overinvestment (Frattaroli, 2020; Leung et al., 2019), which posit that the reason why firm managers manipulate reported earnings and pursue aggressive mergers and acquisitions is associated with their private gains.

Moreover, the degree to which reduced earnings affect aggressive share repurchase behavior could vary depending on a firm’s degree of franchising, since restaurant firms that have many of their outlets run by franchisees and their less franchised peers could present different magnitudes of precautionary need to reserve cash for future purposes. Specifically, highly franchised restaurant firms could be less pressured to build cash reserves than their counterparts for the following reasons: first, as resource scarcity theory posits, franchisees use their own financial resources to open, operate, and maintain their outlets (Combs et al., 2004; Tracey and Jarvis, 2007); second, highly franchised firms enjoy a more stable stream of income owing to the franchise income (Weik, 2012); and lastly, the debt market shows a more favorable attitude toward highly franchised restaurant firms (Sun et al., 2019). Moreover, highly franchised restaurant firms and their counterparts could present different magnitudes of incentives to manage EPS figures. Franchisees are known to refer to the brand image of franchise firms when they choose the right franchise business for them (Erlinda et al., 2016). Given that a firm’s stock price is known to reflect its brand value (Hsu et al., 2013), firms that adopt franchising could be more encouraged to manage EPS, which determines the stock price of a firm (Manoppo, 2016; Talamati and Pangemanan, 2015), than their counterparts.

To the best of the author’s knowledge, an industry-wide phenomenon of aggressive share buybacks during periods of subpar earnings has not been empirically demonstrated and reported, nor has a possible difference in its impact depending on a firm’s degree of franchising. The findings of this study will encourage stakeholders, not only in the restaurant industry but also in other industries with similar characteristics to the restaurant industry, to examine the factors specified in this study to better understand firms’ aggressive share repurchase behavior.

Related literature and hypotheses

Share buyback and its related theories

In response to the growing popularity of share buybacks over the years, researchers have relied on some classical theories to explain firms’ motives for repurchasing shares. Signaling theory provides the most popular explanation (Andriosopoulos and Hoque, 2013; Gupta, 2017). This theory is closely associated with the concept of asymmetric information between sellers and buyers in economic transactions (Mavlanova et al., 2012). When a buyer has limited information about a seller—that is, when information asymmetry exists between a buyer and a seller—the result is often an unwillingness on the part of the buyer to pay for the seller’s product or service. In this situation, signaling theory posits that the seller can circumvent the problem of asymmetric information by credibly signaling positive information about themselves to the buyer. The buyer would then interpret the signal and adjust their purchasing behavior accordingly, usually by offering a higher price than if they had not received the signal. Signaling theory can also apply to share buyback (Baker et al., 2003). Since investors’ knowledge of a firm is limited to publicly available information, the firm’s prevailing share price may not reflect its true value. In this case, a share buyback can act as a corrective signal of the firm’s value, since massive spending on a buyback can signal a manager’s confidence in the firm’s future earnings and cash flows.

Another explanation for the motive behind share buybacks comes from agency theory. Agency theory focuses on resolving conflicts of interest in the principal–agent relationship (Van Puyvelde et al., 2012). In this relationship, one entity (principal) legally appoints another entity (agent) to act on its behalf and conflicts of interest that arise from this relationship are referred to as agency problems. In the field of finance, agency problems usually represent a conflict of interest between a firm’s shareholders (principal) and its management (agent) (Bebchuk and Fried, 2003). The manager, acting as an agent for the shareholders, is supposed to make decisions that maximize shareholder wealth. However, according to agency theory, when firms generate surplus cash, managers can easily be tempted to use this cash to serve their own interests. One way to mitigate excess cash is to disburse it in the form of a share buyback (Wang et al., 2009).

Despite the contributions of signaling and agency theories to clarifying the basic motives for share buybacks, these two classical theories do not seem to fully explain spending more than what a firm earns on share buybacks. Given the high opportunity cost of conducting share buybacks since money spent on buybacks is money that would otherwise be spent on pursuing growth opportunities and fostering innovation, the benefit from signaling activities and reduced agency problems through share buybacks cannot easily justify spending an excessive amount of earnings on share buybacks. However, many recent share buybacks have been financed through spending more than what firms earn, either by draining the firms’ cash reserves or using borrowed money.

Reductions in earnings and share buybacks in the restaurant industry

As previously mentioned, share repurchases, along with dividends, are how a firm distributes its earnings to shareholders (De Vries et al., 2012; Zhou et al., 2013). In particular, ever since share repurchases were legalized by the U.S. Securities and Exchange Commission (SEC) in 1982, they have exceeded dividends as a mode of distribution to shareholders, as evidenced by the considerable share repurchases conducted by S&P 500 amounting to $519.69 billion in 2020, compared to dividends amounting to $483.18 billion in the same year (Maurer, 2021). One of the primary reasons why share repurchases have become the most common way of distributing earnings to shareholders is because they provide firm managers with more flexibility than dividends (Jagannathan et al., 2000). Specifically, in the case of dividends, investors tend to interpret cuts or omissions as a signal of management’s incompetence or the firm’s future failure (Fracassi, 2008). Therefore, managers tend to maintain the previous level of dividends (Jeong, 2013).

In contrast, it has been demonstrated that share buybacks, by their very nature, offer an element of flexibility (Jagannathan et al., 2000). The key characteristic differentiating dividends from share buyback has been well documented in previous studies. For example, Iyer and Rao (2017) demonstrated that the proportion of repurchasing firms that reduced buyback payouts was greater than that of dividend payers that reduced their dividends during the financial crisis period. Moreover, Brav et al.’s (2005) survey results revealed agreement among most managers that reducing dividends will draw a negative abnormal market reaction, while only a small proportion of financial executives considered reducing buybacks as having such an adverse consequence.

Although this thinking is conventional, restaurant managers might counter intuitively have a strong incentive to conduct aggressive share buybacks during periods of reduced earnings. The possible reasons for this are as follows. Firms’ earnings per share (EPS) figures, which represents how much earnings a firm has generated for each share of stock, is one of the most important variables in determining the firm’s stock price (Manoppo, 2016; Talamati and Pangemanan, 2015). More importantly, due to the significance of EPS in determining a firm’s stock price, it is one of the most commonly used indexes to determine executive compensation (Young and Yang, 2011). However, restaurant firms may have some innate difficulty in managing EPS figures due to their irregular earnings.

Specifically, the restaurant industry is among the industries most affected by seasonality and economic conditions (Dewally et al., 2017; Koh et al., 2018; Lee and Ha, 2012). Accordingly, restaurant firms’ revenues and consequent earnings are highly volatile (Koh et al., 2018). Worse still, the high capital intensity (i.e., fixed assets) of the restaurant industry (Lee, 2010; Mun and Jang, 2022; Poretti and Heo, 2021) makes it even more difficult for restaurant firms to manage their earnings. A restaurant needs physical buildings, equipment, fixtures, and furniture at the launch of its business. With significant costs tied up in fixed assets, restaurant firms cannot easily cut expenses in response to reduced sales, since fixed costs do not vary in relation to sales (Alaghi, 2012). Therefore, restaurant firms’ limited ability to adjust expenses in the event of reduced sales makes it much more challenging for them to manage their earnings. Moreover, food costs, which comprise a significant portion of restaurant firms’ gross sales (e.g., about 33% of the total restaurant sector revenue) are known to be highly volatile (Park and Kim, 2021; Tang, 2015; Uddin et al., 2020), which certainly undermines restaurant firms’ earnings stability.

This means that even if a restaurant firm’s number of outstanding shares, which determines the denominator of EPS, remains the same, frequent fluctuations in earnings (i.e., the numerator of EPS) could still make it challenging for restaurant managers to manage their overall EPS figures. In this situation, one of the surest ways to minimize the negative impact of reduced earnings on EPS is to counteract a decrease in earnings (i.e., the numerator of EPS) by reducing the number of outstanding shares (i.e., the denominator of EPS), which can be effectively achieved through repurchasing shares. Consequently, managers in the restaurant industry could be encouraged to conduct more aggressive share buybacks during periods of reduced earnings as a way of resolving their difficulty in managing EPS figures.

Indeed, the above argument of this study is in line with that of the bonus plan hypothesis regarding earnings management and the empire-building hypothesis regarding overinvestment, both of which attempt to link managers’ short-sighted behaviors with their desire to pursue private benefits. Specifically, the bonus plan hypothesis, whose main argument is based on Healy (1985)’s seminal study, posits that managers’ tendency to shift future earnings to the current period is because of the managers’ motive to improve their compensation (Rath and Sun, 2008; Setyorini and Ishak, 2012; Yanti et al., 2019). In addition, the empire-building hypothesis, which originates from Jensen (1986)’s seminal study, argues that since an increase in the size of a firm can lead to a manager’s greater authority and wealth, managers could have a strong incentive to increase the firm size through aggressive mergers and acquisitions even if they could hurt the firm’s long-term profitability (Frattaroli, 2020; Leung et al., 2019).

Taken all together, based on a series of evidence that the current study provided above for the positive relationship between restaurant firms’ reduced earnings and their aggressive share buybacks, this study intends to investigate whether restaurant firms truly conduct more aggressive share buybacks during periods of reduced earnings by examining the following two hypotheses:

The moderating role of franchising in the relationship between reduced earnings and share buyback

As discussed, this study proposed that there could exist a positive relationship between restaurant firms’ reduced earnings and their aggressive share repurchase behavior. However, the positive impact of reduced earnings on aggressive share buybacks could further vary in magnitude depending on a firm’s degree of franchising. The possible reasons for this are as follows.

According to precautionary motive theory, which was introduced by Keynes (1937) in the context of personal spending behavior and was later adopted in the context of corporate finance (Kim et al., 2011; Magerakis and Habib, 2021), a firm has a precautionary motive to reserve some of its earnings to avoid costly external financing for unexpected future expenses. This is because as the pecking order theory states, when a firm finances business activities, the cost of using its retained earnings is cheaper than that of external financing (Sheikh et al., 2012). If external financing is required, debt is preferred over equity, since the cost of debt financing, which is interest payment, is considered to be cheaper than that of equity financing, which inevitably involves giving up a percentage of a firm’s ownership to investors (Rehayem, 2019).

However, when comparing restaurant firms that have many of their outlets operated by franchisees and their less franchised peers, the need to set aside some of their earnings for future purposes could be smaller for the former than the latter. The explanation for this is twofold. First, as posited by resource scarcity theory, firms adopt the franchise model mainly because franchisees use their own funds to open, operate, and maintain their outlets (Combs et al., 2004; Choi et al., 2018; Seo, 2016; Seo et al., 2018; Tracey and Jarvis, 2007). Hence, any unexpected expenses incurred for operating franchised outlets are borne by the franchisees. Moreover, unless the franchise contract expires, franchise firms receive consistent franchise income from franchisees (Franchise Business, 2022; Park and Jang, 2018; Weik, 2012). Therefore, highly franchised restaurant firms enjoy a more stable stream of income and thus could be less vulnerable to sudden needs for cash for future expenses than their counterparts.

Second, the debt market, which is the second most preferred financing option in financing hierarchy, is known to provide more favorable bond ratings to highly franchised restaurant firms than to their less franchised peers (Sun et al., 2019). The debt market deems highly franchised restaurant firms less risky borrowers than their less franchised peers due to the former’s lower business risk and thus lower default risk (Sun et al., 2019). Therefore, given highly franchised restaurant firms’ easier access to debt financing than their less franchised peers, the need to reserve earnings for future use could be less prominent for the former than the latter. Consequently, in the event of reduced earnings, highly franchised restaurant firms could be less constrained than their less franchised peers to spend their earnings on share buybacks.

Moreover, there could also exist a stronger incentive for highly franchised restaurant firms to stabilize EPS figures using share buybacks than their less franchised peers. When franchisees select a franchise business, not only do they consider the franchisors’ past accounting performance but they also examine the franchisors’ brand value and reputation recognized by the public (Erlinda et al., 2016). However, under the generally accepted accounting principle (GAAP) adopted by publicly traded U.S. firms, intangible assets, such as brand value and reputation, are not sufficiently reflected in a firm’s accounting performance (Gelb and Siegel, 2000; Høegh-Krohn and Knivsflå, 2000). Rather, a firm’s superior brand value and reputation are manifested in its high and stable stock price (Hsu et al., 2013). Therefore, given that a firm’s EPS figure heavily influences the firm’s stock price (Manoppo, 2016; Talamati and Pangemanan, 2015), in the event of reduced earnings, which could destabilize and decrease a firm’s EPS, firms that actively adopt franchising could be more encouraged than their counterparts to use a share buyback to artificially manage EPS.

In sum, due to highly franchised restaurant managers’ better position to use earnings during periods of reduced earnings and their additional incentive to artificially manage EPS figures, they could more actively engage in aggressive share buybacks during periods of reduced earnings than their less franchised peers. This reasoning leads to the development of the following two hypotheses.

Methodology

Samples and data

All the data used to calculate the variables of this study, except for the data pertaining to a firm’s degree of franchising, were collected from the Compustat database of Wharton Research Data Services (SIC code 5812) spanning 1995–2020. Compustat is a comprehensive database of fundamental financial and market information. In addition, 10-K reports were examined to identify the degree of franchising. Firms that do not have their own brand (e.g., pure franchisee firms) were excluded from the study sample. The year 1995 was selected as the beginning year because the Compustat database prior to 1995 contains too much incomplete and missing data to calculate some of the key variables of this study. This data collection process resulted in 1,322 observations. Since the purpose of this study was to examine whether greater reductions in restaurant firms’ earnings are associated with more aggressive share repurchase behavior, the observations were narrowed down to the ones presenting a reduction in earnings. This process yielded 441 observations for analysis.

Variables

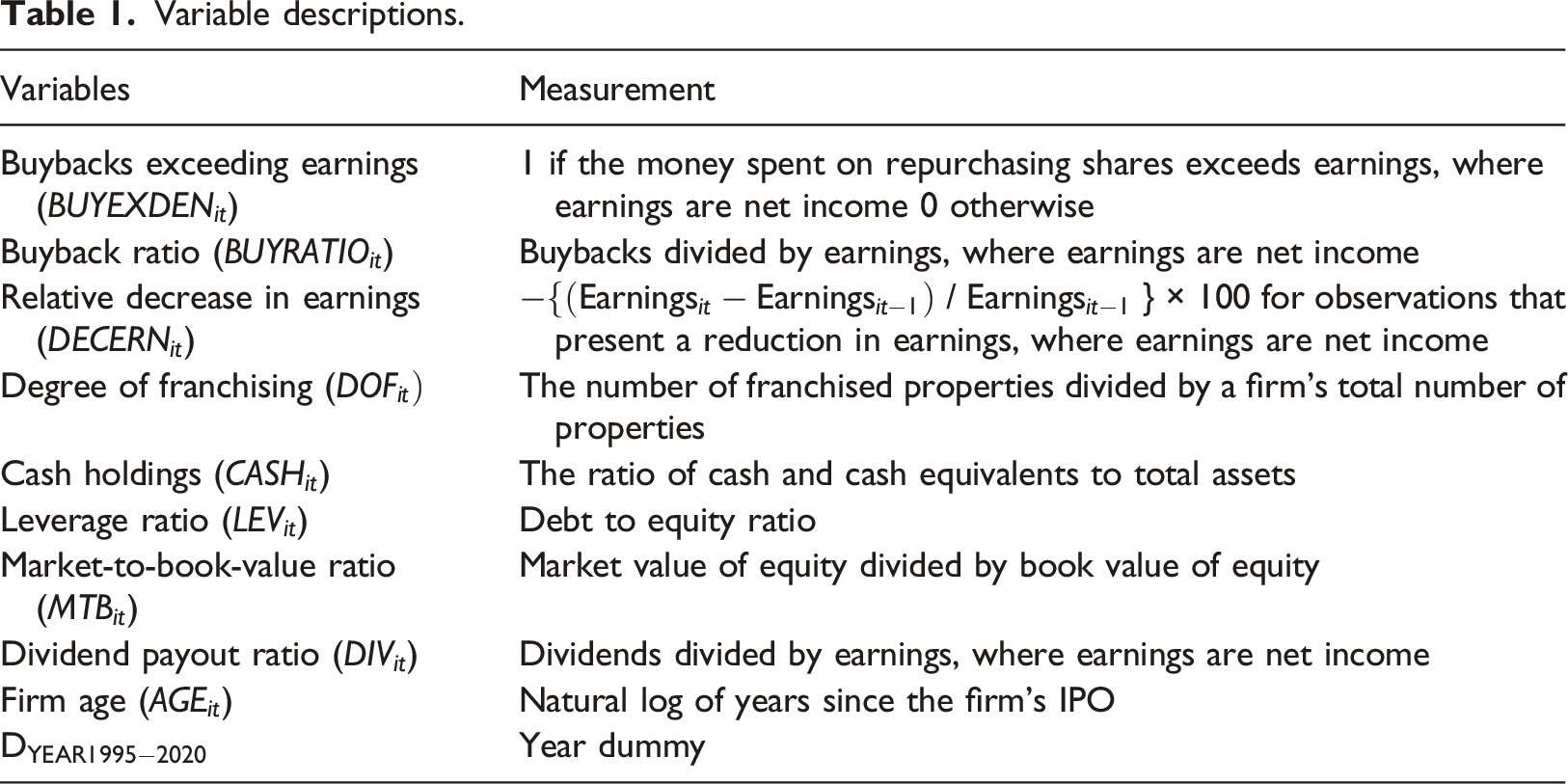

This study included the following two dependent variables: buybacks exceeding earnings (

Variable descriptions.

Model development

This study specified the following equations to test the impact of a relative decrease in earnings (

In addition, to test the moderating role of a firm’s degree of franchising

Reflecting the binary nature of the dependent variable used in models 1a and 2a (i.e.,

In addition, in models 2a and 2b, with a full regression equation including interaction terms, high multicollinearity was expected between first-order variables and the interaction terms. To prevent this, the variables associated with the interaction terms in models 2a and 2b (i.e.,

Results

Descriptive statistics

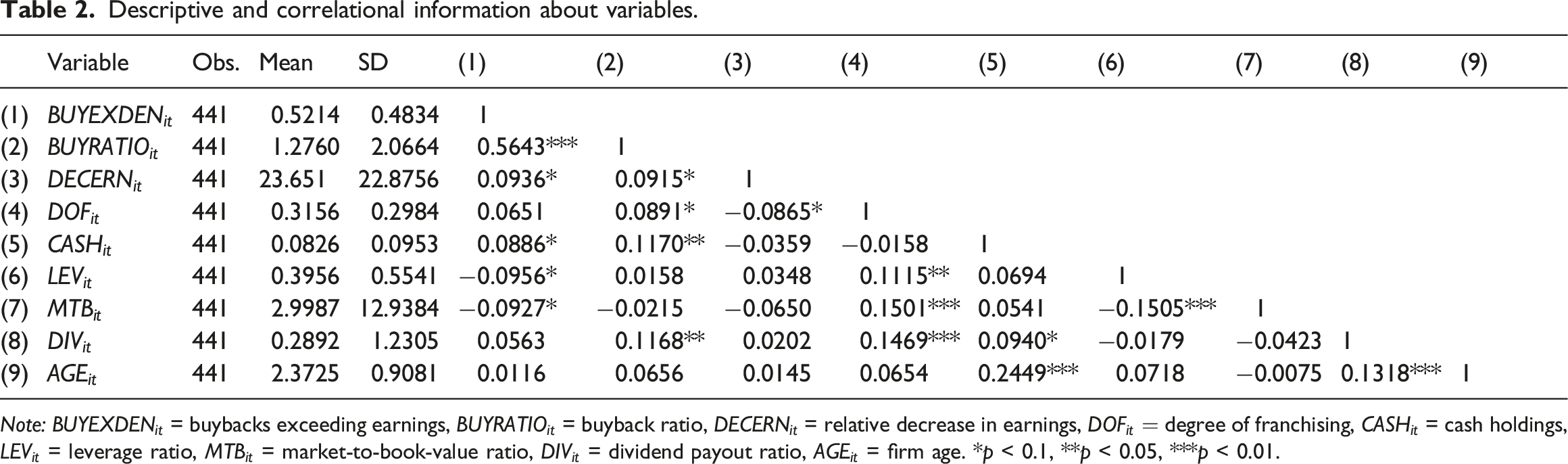

Descriptive and correlational information about variables.

Note:

According to the correlation matrix, buybacks exceeding earnings

Share repurchase behaviors of restaurant firms

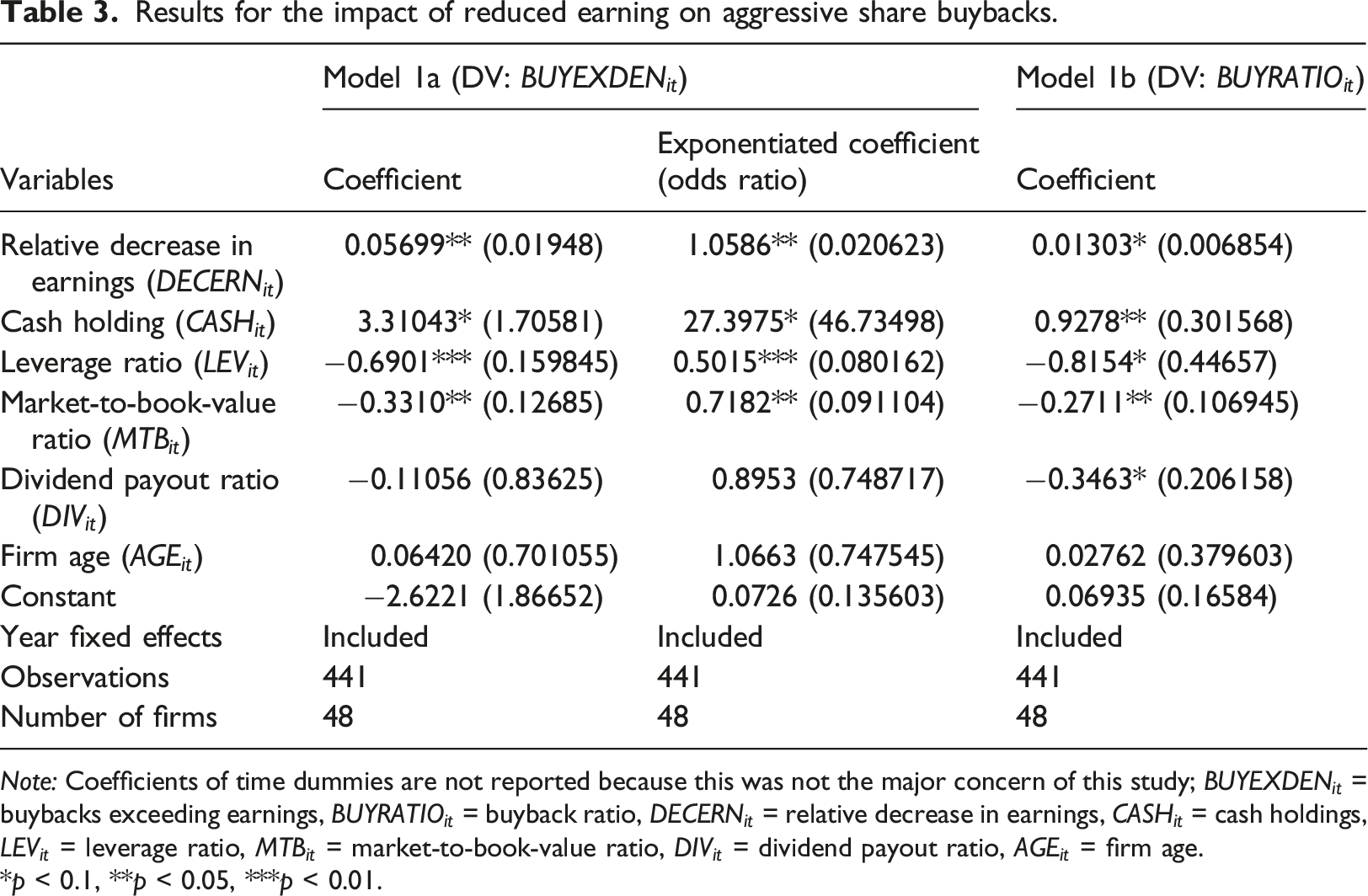

Results for the impact of reduced earning on aggressive share buybacks.

Note: Coefficients of time dummies are not reported because this was not the major concern of this study;

*p < 0.1, **p < 0.05, ***p < 0.01.

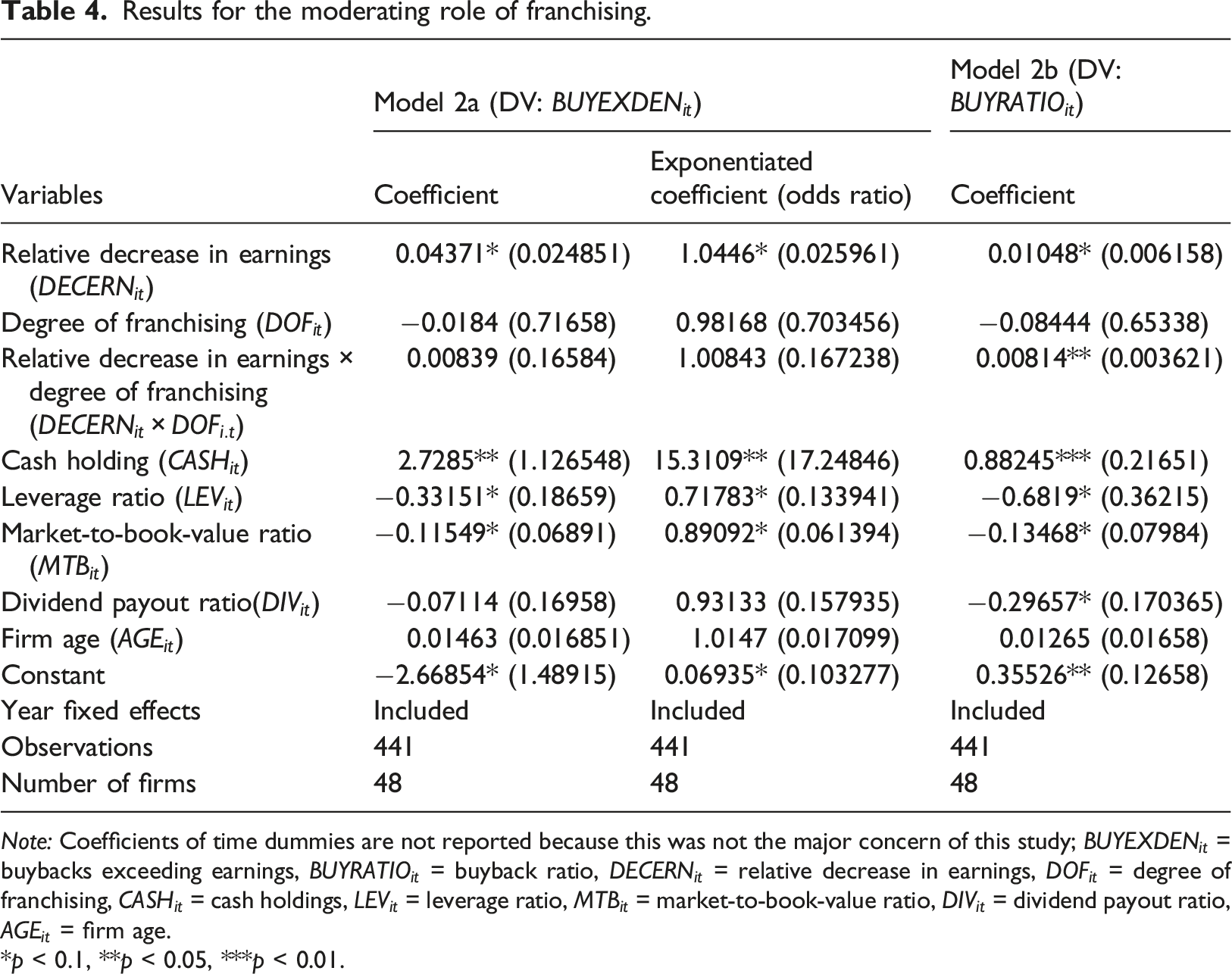

Results for the moderating role of franchising.

Note: Coefficients of time dummies are not reported because this was not the major concern of this study;

*p < 0.1, **p < 0.05, ***p < 0.01.

In Table 3, models 1a and 1b tested whether a greater reduction in earnings is associated with a greater tendency to conduct buybacks exceeding earnings (H1a) and a greater portion of earnings spent on share buybacks (H1b). First, in model 1a, with buybacks exceeding earnings (

Furthermore, models 2a and 2b in Table 4 tested the moderating effect of a firm’s degree of franchising (

Lastly, regarding the control variables of this study, leverage ratio (

Conclusion

General discussions

This study is the first to demonstrate an industry-wide phenomenon of aggressive share buyback behavior in the event of reduced earnings. Specifically, the study demonstrates that both restaurant firms’ tendency to conduct share buybacks exceeding earnings and the proportion of their earnings spent on share buybacks increased during periods of reduced earnings. However, the effectiveness of reduced earnings in explaining restaurant firms’ aggressive share repurchase behavior differed depending on a firm’s degree of franchising. Specifically, the positive impact of reduced earnings on the portion of earnings spent on share buybacks became stronger as a firm’s degree of franchising increased. However, the divergence in aggressive share buyback behavior between highly franchised restaurant firms and their less franchised peers during periods of reduced earnings did not seem to extend to the divergence in a tendency to conduct share buybacks exceeding earnings. This result may suggest that highly franchised restaurant firms’ less precautionary need to reserve cash could encourage managers at highly franchised restaurant firms to spend an even greater portion of earnings on share buybacks during periods of reduced earnings than their counterparts, which suggests that the former engages in more aggressive share buybacks than the latter during periods of reduced earnings. However, it should be noted that the more aggressive buyback behavior of highly franchised restaurant firms than their counterparts does not extend to the point of the former presenting a greater tendency to spend above earnings on share buybacks than the latter.

Practical implications

This study also has some practical implications. With the recent proliferation of share buybacks, critics of share buybacks have argued that firms have been using such programs merely to inflate stock prices to reap short-term benefits. This growing concern even prompted lawmakers to introduce a bill that could impose a limit on the number of shares a firm can repurchase (Smith, 2019). However, this bill has faced strong backlash from many corporations and economic liberals (Egan, 2018). The results of this study might suggest that some share buybacks are conducted to attain short-sighted managerial goals, supporting the critics’ argument for imposing restrictive measures on share buybacks. In addition, the critics of aggressive share buyback often accuse firms of spending hefty amounts of money on repurchasing shares instead of raising worker benefits and wages, which could eventually lead to the firms’ long-term profitability (Lowrey, 2018). This accusation bears even more importance in the restaurant industry, which employs millions of U.S. workers, many in low-wage, economically insecure jobs (Shierholz, 2014). According to Roosevelt (2018), the restaurant industry could pay the median worker an average of 25% more annually if the money spent on share buybacks was redirected to workers’ compensation. Furthermore, since aggressive share buybacks boost firms’ short-term stock prices at the expense of their long-term success, those share buybacks are most likely to benefit short-term, speculative traders at the cost of long-term genuine investors. The results of this study inform genuine investors how some factors in the restaurant industry influence managers’ tendency to conduct aggressive share buybacks, thereby helping to protect their wealth when they make investment decisions.

In particular, this study has identified the restaurant industry-specific determinant of aggressive share buybacks—that is, a firm’s degree of franchising. Given that franchising is a very common business format in the restaurant industry (Koh et al., 2009), previous studies made valuable attempts to investigate the role of franchising in explaining various diverging characteristics of restaurant firms. The previous studies on franchising mostly informed market participants in the restaurant industry of the positive aspects of franchising, such as the role of franchising in reducing geographically diversified firms’ risk (Song et al., 2019), decreasing vulnerability to economic conditions (Koh et al., 2018), and enhancing risk evaluations in the bond market (Sun et al., 2019). On the contrary, the results of this study demonstrate that market participants should be more vigilant about restaurant firms’ aggressive share buyback behavior as a firm’s degree of franchising increases, as evidenced by a greater portion of earnings spent on share buybacks during periods of reduced earnings as a firm’s degree of franchising increases.

Theoretical implications

Theoretically, the results of this study showed that some share buybacks cannot be sufficiently explained by the classical theories. Specifically, restaurant firms’ increased tendency to conduct aggressive share buybacks during periods of reduced earnings might be due to the managerial goal of adjusting a firm’s short-term EPS figures rather than their effort to signal their optimism about the firm’s prospects (Baker et al., 2003) or to mitigate agency costs associated with surplus cash (Wang et al., 2009). Moreover, the results of this study suggest that the main argument behind the bonus plan hypothesis regarding earnings management and the empire-building hypothesis regarding overinvestment—that managers’ short-sighted behaviors can originate from their incentive to pursue private gains—could also apply to the aggressive share buyback behavior of restaurant firms.

In addition, this study demonstrates that the main argument of the precautionary motive theory—firms’ precautionary need to reserve cash in preparation for unexpected future expenses (Kim et al., 2011; Magerakis and Habib, 2021)—might not apply uniformly throughout the restaurant industry. By demonstrating that highly franchised restaurant firms spent greater portions of their earnings on share buybacks than their less franchised peers during periods of reduced earnings, this study shows that the precautionary need to reserve cash might apply less strongly to the former than to the latter. In addition, highly franchised restaurant firms spending greater portions of earnings on share buybacks than their counterparts during periods of reduced earnings could support the validity of resource scarcity theory, which posits that highly franchised restaurant firms are less financially constrained than their counterparts since franchisees invest their own financial resources to operate their outlets (Combs et al., 2004; Tracey and Jarvis, 2007).

Limitations and future studies

Despite its contribution to the literature, this study is not free from limitations. First, this study created one of the two dependent variables, buybacks exceeding earnings (

Footnotes

Author contributions

JG: Conceptualization, methodology, data curation, writing-original draft, and writing-review and editing. SJ: Validation and writing-review & editing.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.