Abstract

When do political parties propose long-term investments? Electoral competitiveness should be a key variable explaining parties’ investment priorities: parties can be less responsive to voters’ short-term priorities and overcome time inconsistencies when they are more likely to win the next election. The article distinguishes the characteristics of three types of investments in education, environmental protection and technology and infrastructure, gathered from the Comparative Manifesto Project. It finds a linear positive relationship between parties’ probability of entering office and the proportion of manifestoes allocated to statements about technology and infrastructure. In contrast, statements about education are highest at high levels of electoral competitiveness, as parties propose more education to attract voters, while statements about the environment are affected by parties’ ideology on the left-right axis rather than by electoral competitiveness. Power-sharing institutions help parties to overcome time inconsistency problems, reducing the impact of electoral competition on investments.

Introduction

Fighting climate change, building the infrastructure for tomorrow’s economy or adapting public finances to the challenges of an aging society all involve making sacrifices in the present to build a more prosperous future. Short-sighted governments will generally refrain from imposing these costs on voters. Rather, they will deliver policies offering visible and immediate benefits, postponing long-term investments indefinitely (Jacobs, 2016). How can governments reverse this tendency and prioritize long-term investments?

This article studies two political impediments to the implementation of long-term investments: voters’ own preferences for policies benefiting themselves in the short term and a time inconsistency problem deriving from the fragility of governments’ long-term commitments. If a government invests in a policy whose benefits unfold only in the future, it risks losing office before the benefits of the investment materialize, reducing its incentives to implement it. Parties, voters and interest groups face a time inconsistency problem since they cannot know if the next government will deliver the specific investment or instead choose to reallocate it towards other purposes. Under such uncertainty, it is difficult for political parties to reorient public policies towards long-term investments.

This argument assumes that voters are myopic and prefer policies whose benefits unfold in the short term (Achen and Bartels, 2017). Political parties fearing for their survival in office should be more attentive to voters’ preferences than parties that are almost certain to win the next election (Hobolt and Klemmensen, 2008). Thus, electoral competitiveness should influence parties’ decisions to propose long-term investments. Political parties in safe electoral situations should be encouraged to invest in the future because they are less vulnerable to short-run voter dissatisfaction and more likely to stay in office to reap the benefits of a long-term investment (Jacobs, 2016).

Power-sharing institutions imposing constraints on executive power also influence parties’ incentives to propose long-term investments as they limit time inconsistency problems. In a power-sharing political structure, the government in power today is more likely to maintain a role in future governments or to remain a veto player which diminishes the likelihood of policy reversals. This reassures the party in power at time t and the groups it represents that they will get a share of the benefits of a future-oriented reform at time t+x. Hence, power-sharing institutions help to break political uncertainty about future investments by ‘locking in’ commitments (Jacobs, 2016; Lindvall, 2017). Thus, parties can solve the time inconsistency problem either when political institutions share power between multiple actors or when electoral competitiveness is low.

Relatively few studies analyse the effect of electoral competition on parties’ positions (Abou-Chadi and Orlowski, 2016). Using time series cross sectional analysis of panels of OECD countries, we study the effect of office probability (Cronert and Nyman, 2019), which is the likelihood that a specific party enters the cabinet at the next election, on political parties’ investment priorities. Policy positions about investments are calculated as a proportion of party manifestoes dedicated to investments in technology and infrastructure, education and the environment, the three most future-oriented categories in the comparative manifesto project (CMP). We contrast these long-term investments with propositions for additional short-term consumption that we operationalize as statements about welfare expansion.

Of these long-term investments, only statements about technology and infrastructure and their ratio relative to short-term consumption are linearly affected by office probability as they are facing clear intertemporal trade-offs without being a policy associated with left or right parties. In contrast, statements about education are highest when electoral competition is the most intense as parties of all ideological stripes propose to invest in education to attract voters since it is a particularly popular policy. Finally, statements about the environment are not influenced by office probability, but are rather associated with left-wing ideology as they necessitate a significant expansion of the state’s degree of intervention in the economy (Farstad, 2018; Schulze, 2021). Disentangling how the characteristics of different investments influence their relationship with electoral competition represents one of the main innovations of this study.

Another contribution of the article is to integrate electoral competitiveness to the study of power-sharing institutions, while most studies about the determinants of long-term investments focus on one or the other. We innovate by modelling an interaction showing that electoral competitiveness has no effect on investments in a political system characterized by a high degree of political constraints on the executive. These power-sharing institutions help to ‘lock in’ policy commitments, limiting parties’ time inconsistency problems regardless of the degree of electoral competitiveness they face. Our findings suggest that because they constrain the potentially detrimental effect of electoral competition on long-term investments, power-sharing institutions favour long-term-oriented governance more so than power-concentrating institutions.

The final contribution of this article concerns the theoretical foundations of the determinants of long-term investments. We do not find support for the myopia hypothesis, which proposes a U-shaped relationship between investments and electoral competition, supposing that investments should be lowest when electoral competition is the most intense and highest when a party is almost certain to win or lose the next election (Cronert and Nyman, 2020; Seiferling, 2019). The time inconsistency problem, rather than voters’ myopia, represents the main impediment to investments, as parties are much more likely to propose investments in technology and infrastructure when they have a strong probability to win the next election.

The article is divided in four sections. The first section discusses the concept of long-term investments and presents the theoretical perspective about the constraints against their implementation, while the second section considers measurement issues. The third section presents the regression results, while the fourth section discusses the consequences of the findings for the prospects of long-term investments in advanced democracies.

Theory

Conceptualizing investments

The notion of social investment is at the forefront of the ‘electoral turn’ in comparative political economy (Beramendi et al., 2015). This perspective is interested in the policy coverage of social risks faced by different constituencies. Social investment, which includes education, childcare and active labour market policies, tends to cover new social risks, prevalent among women, the youth and labour market outsiders, while social consumption covers old social risks, like aging, illness and income losses and is typically preferred by male production workers. In the ‘electoral turn’, preferences for investment and consumption are primarily driven by material interests and parties are mere agents of the policy preferences of the constituencies they represent and aim to attract. The notion of investments’ intertemporal trade-off is largely absent from this perspective.

In contrast, we rely on a temporal conception of investment which highlights the importance of intertemporal trade-offs: investments involve discounting the present in order to boost capital accumulation or improve social outcomes in the future, whereas consumption generate immediate gains for voters (Jacobs, 2016; Lindvall, 2017). This definition includes investments in education that enhance human capital, public investments in research and development and infrastructure that create the conditions for future growth and environmental protection policies adapting tomorrow’s economy to a changing climate.

Different types of investments are characterized by distinct degrees of intertemporal trade-offs. Social investments in education offer clear benefits to defined constituencies such as students, teachers and parents and are appealing to educated middle-class voters (Busemeyer et al., 2020). Investments technology and infrastructure offer fewer short-term benefits and their positive impact takes time to unfold. Even if infrastructure investments can be used during a recession to boost the economy, governments cannot quickly implement a large-scale infrastructure project, which reduces its short-term appeal. While infrastructure investments can reward geographically targeted constituents, they offer visible and short-term benefits mostly to constituencies living close to the physical investment project. Moreover, social investments resemble a private good with clear benefits for individuals, while investments in technology and infrastructure are similar to public goods with diffuse, long-term benefits. This is reflected in the relative popularity of education and infrastructure investments: retrenchment of infrastructure investments do not lower public support for the government, whereas cutbacks to education are impopular (Hübscher et al., 2020). Finally, environmental protection is also a long-term investment, but it involves an even clearer cost imposition in the short term than the two other types of investments (Finnegan, 2019b) and should thus be prioritized mostly by parties that are committed to the issue (Schulze, 2021).

In contrast to the ‘electoral turn’ in comparative political economy, we assume that parties aren’t simply office-seeking and directly responsive to voters; they are also policy-seeking and should have better information about policy consequences than voters (Wenzelburger and Zohlnhöfer, 2020). They are thus more likely than voters to prefer long-term investments benefiting society as a whole. Hence, the degree of electoral competitiveness should moderate how much parties can focus on policy rather than on vote-seeking objectives.

Intertemporal trade-offs and political uncertainty: the impediments to investments

Two factors make it particularly difficult to overcome intertemporal trade-offs for democratically elected policymakers: voters’ own preferences for policies offering immediate rewards and a time inconsistency problem deriving from the fragility of governments’ long-term commitments (Jacobs, 2016; Lindvall, 2017).

Voters’ short-termism and politicians’ willingness to respond to voters’ preferences are the first impediment to long-term investments. Citizens have poor information about policies, tend to be impatient and prefer immediate rewards to long-term gains (Achen and Bartels, 2017; Wang, 2018). Thus, long-term investments are not the average voter’s preferred policy since they involve the imposition of short-term costs (via higher taxes and/or lower spending in the present) to generate uncertain long-term gains (Wang, 2018). Unless institutions make policy promises credible, citizens generally do not support long-term investments (Jacobs and Matthews, 2017), although some cultural traits are associated with different temporal preferences (M. Wang et al., 2016). Voters are signaling their own short-sightedness to governments as they reward immediate relief after a catastrophe rather than investment in preparedness to future shocks (Healy and Malhotra, 2009). Reflecting what they perceive as voters’ short-termism, governments often engage in political budget cycles, lowering taxes and increasing visible public transfers before an election, to the detriment of long-term investments (Philips, 2016).

For a long time, political scientists have proposed that the degree of electoral competitiveness should moderate governments’ incentives to engage in political budget cycles or to prioritize the short term (Tufte, 1978). Governments facing hotly contested elections tend to implement vote-seeking strategies (Abou-Chadi and Immergut, 2019) and are more likely to prioritize short-term policies to please impatient voters (Franzese, 2013). Indeed, governments’ responsiveness to voters is higher in more competitive settings (Powell, 2000). Assuming that citizens are myopic, the more a government must be responsive to voters, the more it will prioritize policies beneficial in the short term. If governing parties enjoy a large lead in the polls, they are less likely to lose the next election and are less vulnerable to voter dissatisfaction. Hence, incumbent governments with a strong probability to stay in office should be more likely to invest in the future (Jacobs, 2016).

The relationship between office probability and investments can take three forms, depending on how parties are expected to perceive their own incentives: it can follow a U-shaped, an inverted U-shaped or a linear relationship. A theoretical perspective based on voters’ myopia implies a U-shaped relationship between electoral competitiveness and investments. Governments’ incentives to respond to myopic voters are highest when electoral competition is strongest. As such, investments should be higher when a government is very likely to win or to lose the next election, while they should be lower when the probability of victory of the incumbent government approaches 50%. Seiferling (2019) finds that governments facing very competitive elections tend to produce higher budget deficits, while deficits are lower for governments that are very likely to win or to lose the next election.

This U-shaped relationship between office probability and investments should hold if voters’ myopia is the only factor motivating parties to implement long-term investments. However, time inconsistency problems also impede investments: even if a government has the courage to extract resources from constituents to invest in a long-term policy, it might lose office and the next government could divert the investment to other purposes. Unless a government is convinced that it will reap the benefits of a long-term investment, it maintains a relatively short time horizon (Besley and Coate, 1998). Moreover, to implement a long-term investment, a government needs to credibly commit to voters and to interest groups: they must believe that the sacrifices they make in the present will be paid off by the returns of the investment (Jacobs, 2011).

When parties have a high probability stay or enter office, they can commit more easily to deliver long-term policies to voters, which should favour long-term investments. In contrast to the myopia hypothesis suggesting that parties propose more investments if they are very likely to win or lose elections, the lack of credible commitment involves that parties should propose fewer investments when they are likely to lose the next election. This perspective based on credible commitment mechanisms suggests a linear relationship between office probability and investments: the more a party is likely to win an election, the more it should propose investments. Hobolt and Klemmensen (2008) support this argument by finding an inverse linear relationship between governments’ popularity and their likelihood to seek to please voters. Finnegan (2019a) finds that gasoline taxation is higher when politicians are insulated from voter punishment.

Statements about technology and infrastructures are a quintessential long-term investment characterized by intertemporal trade-offs and commitment issues since they are public goods offering very few short-term benefits. We hypothesize that parties should propose more of these investments if they are more likely to win office:

H1a: There is a linear positive relationship between a party’s office probability and its statements about technology and infrastructure.

Statements about education are a different type of investment. Of the investments studied in this article, education is by far the most popular (Busemeyer et al., 2020; Hübscher et al., 2020) because it offers more clearly defined short-term benefits (notably for students, parents and teachers) and because they represent a form of social protection against skills obsolescence that most citizens demand in a knowledge economy (Busemeyer and Garritzmann, 2019). Investments in education appeal to middle-class voters that are at the center of both left and right parties’ vote-seeking strategies (Jensen, 2011). They can thus be used as a vote maximization strategy (Abou-Chadi and Immergut, 2019) in contrast to investments in technology and infrastructure, that are less visible and offer fewer short-term benefits. We thus hypothesize that parties will propose more investments in education when electoral competition is fierce.

H1b: There is an inverted U-shaped relationship between a party’s office probability and its statements about education.

The issue of the environment is more contentious than the two other types of investments that are closer to being a valence issue (Kraft, 2018). Climate change mitigation policies involve a direct imposition of costs on businesses and citizens and a significant increase in the state’s intervention in the economy (Finnegan, 2019b). Farstad (2018) finds that manifesto statements about climate change are driven by parties’ left-wing ideology and are not made salient by mainstream parties, suggesting that they do not represent valence issues. Only left-wing parties have electoral incentives to emphasize environmental protection, whereas right parties do not (Schulze, 2021). As such, statements about the environment should not be influenced by office probability but should rather be a function of parties left-wing ideology.

H1c: Statements about the environment are influenced by parties’ left-right ideology.

Electoral competition is not the only factor limiting time inconsistency problems. By reducing the likelihood of policy reversals, power-sharing institutions, such as institutional constraints on the executive, can also solve the time inconsistency problem. The government in power today is more likely to maintain a role in government in the future or to remain a veto player in a power-sharing political structure (Lijphart, 2012). This reassures the party in power today and the groups it represents that they are likely to get a share of the benefits of a future-oriented reform (Lindvall, 2017). The diffusion of power inherent to power-sharing institutions between multiple actors implicated in the policy process involves a more incremental pattern of policy making. It favours the implementation of new investments by breaking political uncertainty about future investments as it ‘locks in’ policy commitments (Lindvall, 2017). Finnegan (2019b) finds that power-sharing institutions structure the ability of governments to impose higher carbon prices.

This argument can be related to Lijphart’s (2012) consensus model of democracy: it forces parties to learn to negotiate and it enhances policy stability by increasing the likelihood of reaching enduring compromises (Lijphart, 2012). In contrast, in systems concentrating power, parties constantly change their policy platforms to attract voters, which creates a discontinuity between governments. Uncertainty concerning other parties’ behaviour if they win elections decreases governments’ incentives to pursue long-term strategies (Martin, 2015). This argument differs from a public choice perspective which would predict that long-term investments are more likely to be implemented by single-party governments in power-concentrating institutions that facilitate the imposition of short-term costs on recalcitrant actors (Franzese, 2013).

In brief, a party can ‘lock in’ commitments and solve the time inconsistency problem either by being likely to win the next election, or if the political system shares power between multiple actors. We should expect a conditional effect of power-sharing on investment proposals: power-sharing institutions should dampen the effect of electoral safety on investments because they offer an alternative way to solve the time inconsistency problem. Electoral safety should thus have a stronger effect on investments in power-concentrating institutions. While both electoral competition and power-sharing institutions are among the variables identified in theories of long-term governance (Jacobs, 2016), very few quantitative studies integrate them together in the same models.

H2: Power-sharing institutions dampen the effect of electoral competitiveness on long-term investments.

Measurement and modelling

This study analyses the propositions of long-term investments made by political parties in their manifestoes. There are several reasons for focusing on manifesto statements rather than policy choices. Manifestoes are well suited to analyse the impact of electoral competition on investments since both are measured at election periods. To our knowledge, no measure of electoral competition is available between elections. If we were analyzing how policy choices made between elections are affected by electoral competition, we would be forced to make arbitrary modelling decisions: should the degree of electoral competition of the previous election matter for a government’s policy decisions at mid-mandate or should we assume that governments can foresee the degree of electoral competition they will face at the next election 1 ? Moreover, analyzing policy choices at election time limits the number of cases, whereas with party manifestoes we can significantly increase the number of cases by comparing multiple parties competing at the same election with different probabilities of winning it.

Unlike policy trade-offs, manifestoes do not impose direct costs on voters. However, when producing a manifesto, parties still need to make trade-offs by deciding which issues will be the most salient to the detriment of others. In party systems in which issue competition rather the policy positioning becomes the central concern of political competition(Green-Pedersen, 2007), parties that focus on future-oriented policy issues may lose votes to parties offering more tangible propositions to voters. Still, we approximate a situation of parties discounting short-term benefits for implementing long-term investments by measuring the ratio of investment relative to consumption in a manifesto as one of our dependent variables. Moreover, this analysis relies on two assumptions: despite their myopia, voters will lend some credibility to promises made in party manifestoes and, ceteris paribus, voters will prefer a manifesto proposing more policies with immediate benefits than a manifesto proposing more uncertain long-term investments.

With these caveats in mind, this study uses parties’ investment priorities as a dependent variable, based on the Comparative Manifesto Project (CMP). The CMP codes parties’ manifesto statements during an election into ‘quasi sentences’ and assigns each of them to one of 56 categories. Parties are more likely to distinguish themselves on the salience they attribute to investments rather than on their position about them, since no party is against any of the investments we study. Thus, the dependent variable is constructed to take advantage of what the CMP does best: identifying the relative emphasis that parties put on different issues and providing a comparable measure of the salience of an issue (Gemenis, 2013). We analyse separately three categories of the CMP to measure investments as a percentage of the statements of each party manifesto. These three categories are: positive statements on technology and infrastructure (per 411), about environmental protection (per 501) and positive statements on education (per 506).

We also measure the ratio of each investment relative to short-term consumption. In the political economy literature, a large proportion of the welfare state is considered as consumption expenditures, whereas policies like education and infrastructure are considered as investments (Beramendi et al., 2015). We thus measure short-term consumption with the welfare state expansion category (per 504). This is the CMP category the most associated with policies that are clearly offering short-term benefits to voters. The ratio is measured as the log of each category of investment relative to welfare expansion (Lowe et al., 2011).

Traditionally, researchers have used vote shares at the previous election to gauge electoral competitiveness, but this measure cannot adequately compare between party systems with differing vote-seat elasticity and number of parties. To measure electoral competitiveness at the party level, we use the measure of the probability of entering office of each party in OECD countries developed by Cronert and Nyman (2019). While previous measures of electoral competition used only pre-electoral uncertainty (based on previous vote shares and on vote intention polls) (Kayser and Lindstädt, 2015), their measure also includes post-electoral uncertainty, which reflects the likelihood that a party succeeds in post-electoral bargaining, based on parties’ coalition and incumbency history. This measure has a superior predictive capacity than the alternative measures since it is better suited to multiparty parliamentary systems where coalition governments are the norm. Office probability ranges from 0 (no probability of victory) to 0.996 (certain to enter office).

Regarding the measurement of power-sharing institutions, we are interested in how institutions limit the likelihood of policy reversals and help to lock in policy commitments. The political constraint index developed by Witold Henisz measures how much a change in the preferences in one political actor can lead to a change in government policy. Henisz composes an index based on the number of independent branches of government with a veto power over policy changes, the presence of effective bicameralism, party alignments across government (whether or not the same party or coalition controls different branches) and the fractionalization of each branch of government. The data is available from the Quality of Government dataset.

We control for party-level and country-level variables that may influence both office probability and investment priorities. We calculate two measures of parties’ ideology, one on the state/market dimension and the other on social values dimensions. Following common practice (Lowe et al., 2011), we use the log of the ratio of the sum of right-wing categories on left-wing categories, positive values being more right-wing. Extreme values on both dimensions may influence office probability. We control for traditional state-market positions, as we would expect that interventionist parties propose more investments regardless of the degree of electoral competitiveness they face (Boix, 1998). The state/market dimension uses categories such as welfare state expansion (limitation), free enterprise, economic incentives, market regulations and views on labour groups. Note that we exclude welfare state expansion and limitations from the index when modelling the ratios of long-term investment relative to welfare state expansion as a dependent variable. We control for the social value dimension since parties attracting younger and more educated voters, who have more liberal social values, may propose more investments (Beramendi et al., 2015; Kraft, 2018). The social value dimension is based on categories such as support for political authority, a traditional way of life, multiculturalism, and law and order.

In models including environmental protection as a dependent variable, we also control for a dummy coded 1 when the manifesto is issued by a Green party, since Green parties own the issue and tend to have lower office probability. We control for the share of uncoded sentences to capture measurement errors in the coding of manifestos and for the length of the manifesto because it tends to influence the range of topics addressed (Gemenis, 2013). We also control for incumbency status, since incumbent governments may have higher office probability and propose more investments (Kraft, 2018).

At the country level, we control for economic conditions (GDP growth and unemployment rates) to capture business cycles, which may influence office probability and manifestoes’ content. Moreover, since demand for public investment increases as economies become more globalized and service-oriented (Busemeyer and Garritzmann, 2019), we control for deindustrialization (measured as the share of manufacturing employment in total civilian employment) and trade openness to capture the level of globalization. Research has shown that public investments are particularly constrained by fiscal pressures (Breunig and Busemeyer, 2012; Jacques, 2021a). Hence, we control for government debt and deficits as measures of fiscal pressures, which may also influence office probability. Finally, we control for electoral disproportionality: in majoritarian systems, parties have more incentives to provide geographically targeted investments in infrastructure (Breunig and Busemeyer, 2012) and their office probability is more volatile (Kayser and Lindstädt, 2015). Summary statistics and a detailed description of all the variables are reported in the Supplemental Appendix.

There are 28 OECD countries in the dataset. 2 The party-level time series differ considerably; some are ranging from 1951 to 2017 and others are only appearing in the 1990s. The dataset is thus unbalanced and has a relatively short time series since units are observed only at each election. T ranges from 1 to 20 (mean = 6.44, sd = 5.05), while N = 1688.

Theoretically, we expect a contemporaneous effect between the probability of winning an election and investment priorities. 3 We include a lagged dependent variable since parties take previous policy positions as a starting point for their manifestoes (Wenzelburger and Zohlnhöfer, 2020) and are thus characterized by serial correlations. We cluster the error term by parties to correct for heteroscedasticity and serial correlation. The unit of analysis in all the equations is party/election. Our main hypothesis assuming a linear relationship between office probability and investment statements is tested with equation (1):

where Y is a measure of investment priorities in a party manifesto, X is a measure of office probability observed at each election t for party

Equation (2) presents a quadratic equation to model the U-shaped or inverted U-shaped relationships proposed by the myopia argument:

Equation (3) presents the interaction model between office probability and power-sharing institutions, expecting that electoral competitiveness exerts a stronger effect when political constraints are lower:

where X is parties’ office probability and Z is power-sharing institutions at the country-level and

Results

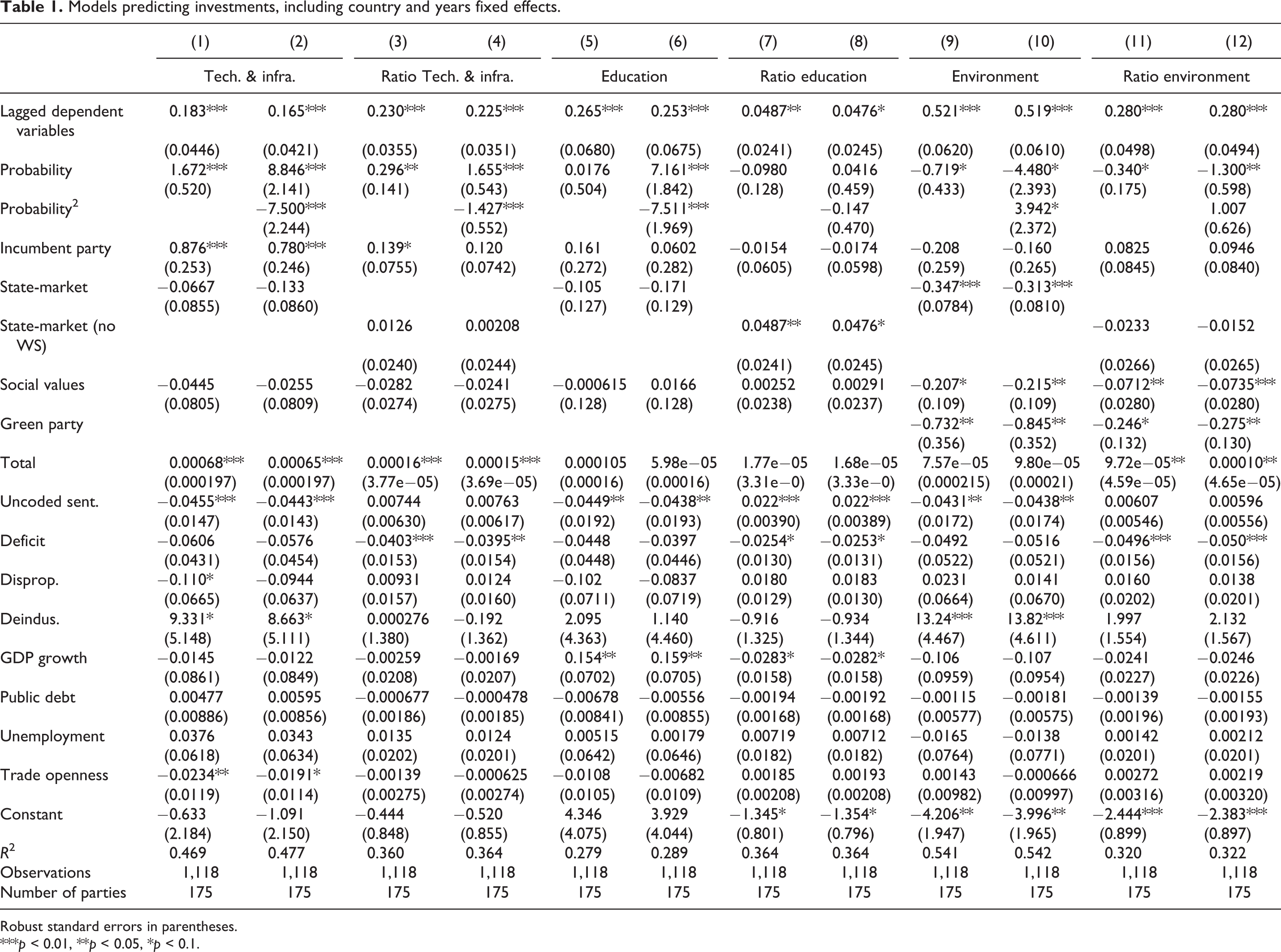

Table 1 presents the results of models predicting investment priorities. Models with odd numbers present linear effects of office probability based on equation (1), while even models present quadratic relationships with office probability and its square, based on equation (2). Office probability exerts a significant positive linear effect on statements about technology and infrastructure (model 1) and on the log ratio of technology and infrastructure relative to short-term consumption (model 3). 4

Models predicting investments, including country and years fixed effects.

Robust standard errors in parentheses.

***p < 0.01, **p < 0.05, *p < 0.1.

Models 9 and 11 show that office probability has a negative effect on statements about the environment and on their log ratio, but the effect is only significant at the p = 0.1 level. To explore this relationship, an interaction model presented in the Supplemental Appendix reveals that office probability decreases the proportion of investments only among non-right-wing parties, suggesting small that left-wing parties are those most likely to propose high proportions of statements about the environment, while non-right-wing parties propose fewer statements on the environment as they become more mainstream and have higher office probability. Left-wing parties tend to propose more statements about the environment, confirming Farstad (2018) findings. We can thus reject the null of hypothesis 1c.

Office probability does not produce a significant linear effect on education statements or on their ratio relative to short-term consumption, although model 6 reveals a quadratic effect that we discuss below. These results suggest that office probability has a linear and significant effect only on technology and infrastructure, as predicted by hypothesis 1a, and a quadratic effect on both education and technology and infrastructure.

We present several robustness checks in the Supplemental Appendix. The results are robust to removing country-level controls, which expands sample size. Models are also robust to the exclusion of extreme values on the dependent variable and to the use of a jackknife technique removing one country at a time. Since models using a lagged dependent variable and country fixed effects may produce a Nickell bias when T is small (Plümper et al., 2005), we also present models without lagged dependent variables in the Supplemental Appendix. We include party fixed effects as another robustness check presented in the Supplemental Appendix. This is a very conservative test of the hypothesis since few party-level series are long enough to detect within-party effects of office probability.

There are two potential concerns about causality. Firstly, we run a Granger reverse causality test to confirm that manifesto statements do not influence office probability. Secondly, to ensure that omitted variables do not bias the results, we run Oster’s (2019) bounds tests and add additional controls that could capture public opinion dynamics. The effect of office probability remains robust to these additional controls, while the bounds tests reveal that selection on unobservables would need to be particularly severe for the effect of office probability to be null. Although we cannot make any definitive statements about causality given our models based on observational data, the tests and their results discussed in greater length in the Supplemental Appendix allow us to partially rule out reverse causality and omitted variable biases.

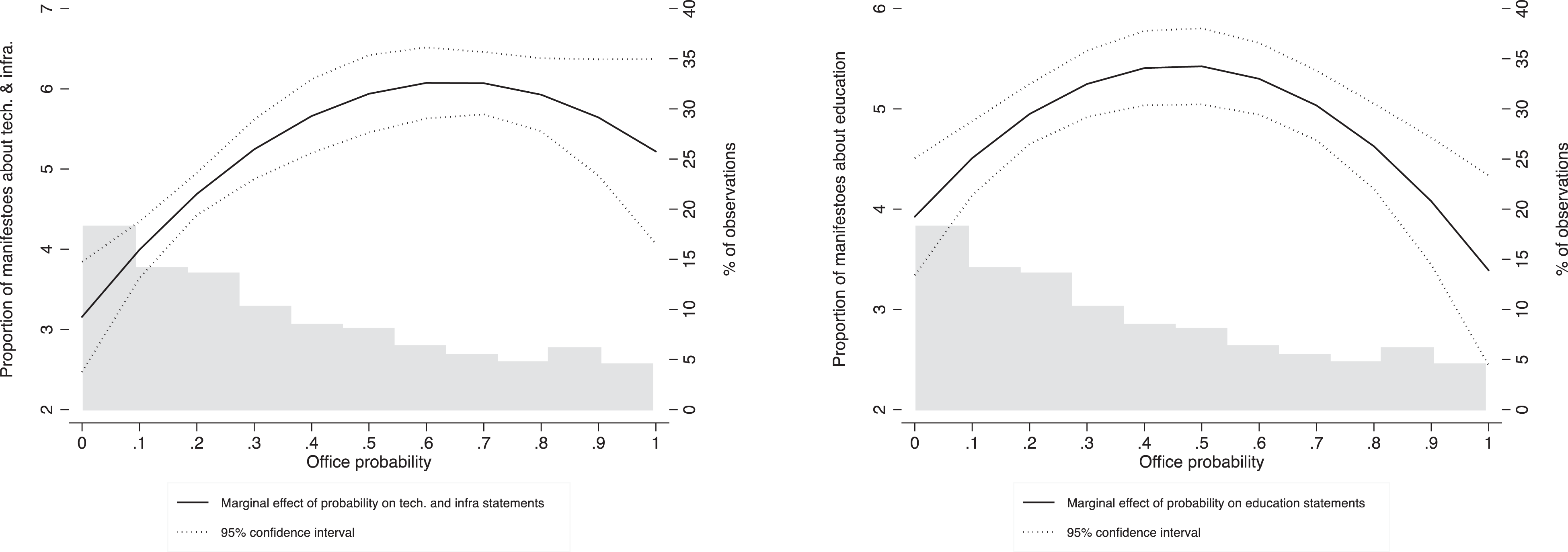

Figure 1 presents the quadratic relationships between office probability, technology and infrastructure (left plot, based on model 2) and education (right plot, based on model 6), while the quadratic effect is not significant for the environment. The right figure shows that statements about education are highest when parties are facing the most severe degree of electoral competitiveness and lowest at high and low electoral competitiveness. This supports the hypothesis 1b: statements about investments in education are useful vote-seeking strategies in situations of competitive elections. In contrast, the left figure shows that the relationship between office probability and technology and infrastructure statements is almost linear, confirming hypothesis 1a, with more statements about technology and infrastructure when office probability is high and fewer statements at low office probability, with the highest level being reached at about one standard deviation above the mean of office probability (0.65). The large confidence intervals at high office probability reflect the small number of cases as there are fewer than 10% of observations above 0.8. The different relationships between the two figures can possibly be explained because technology and infrastructure are policies characterized by stronger intertemporal trade-offs as they offer fewer benefits in the short term to key voters than education. Figure 1 goes against the argument based on voters’ myopia assuming that electoral competitiveness exerts a U-shaped effect on investments. In the Supplemental Appendix, we show that the functional form of the relationship is similar when using a higher order polynomial and when adding restricted cubic splines.

Quadratic regressions based on models 2 (left panel) and 6 (right panel) of Table 1.

Descriptive statistics presented in the Supplemental Appendix confirm that statements about technology and infrastructure increase linearly with office probability, while those about education are highest at mid-levels of electoral competition. Statements about the environment are highest at low levels of office probability, possibly because they are favoured by small left and Green parties.

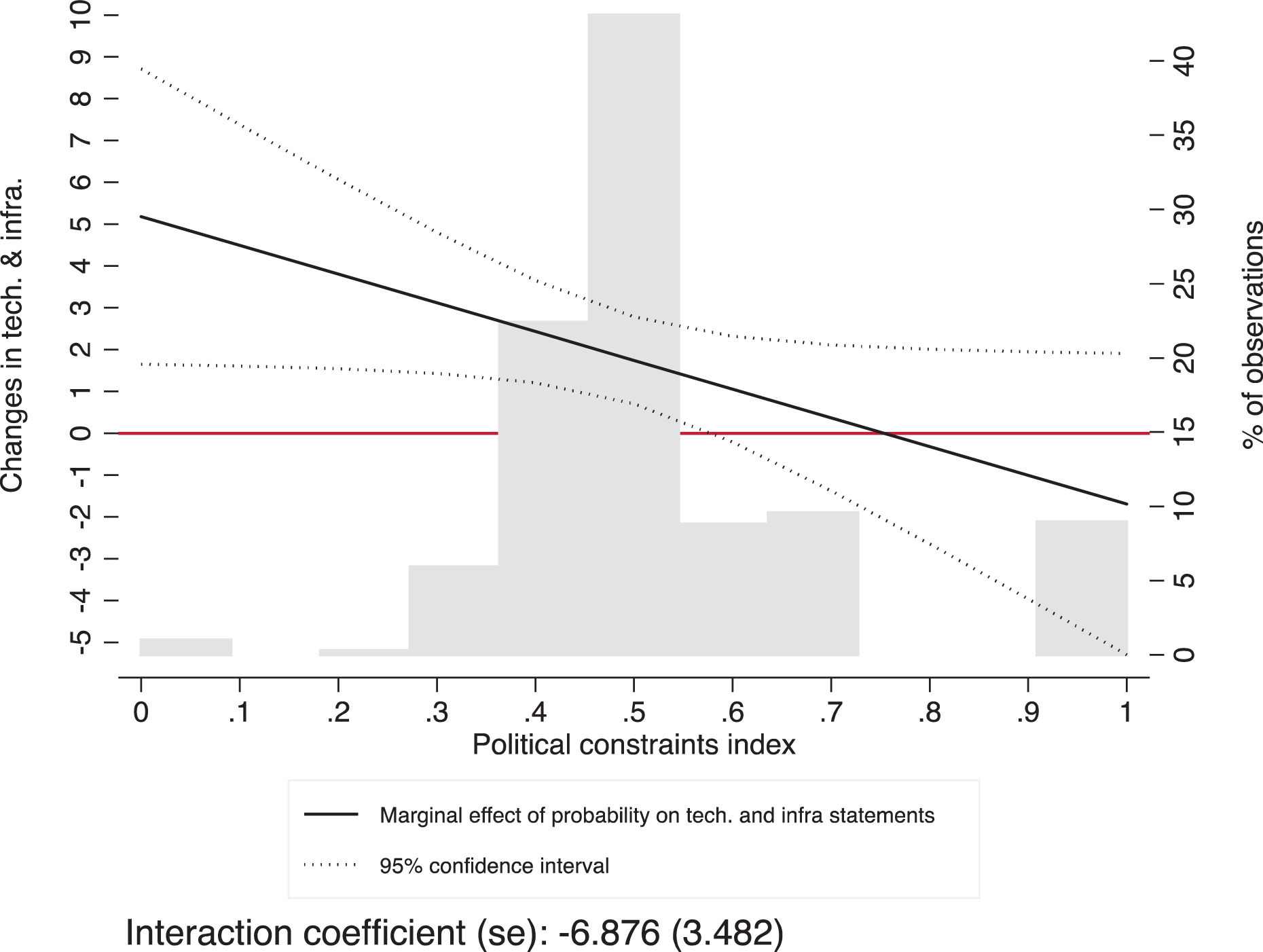

Based on equation (3), Figure 2 presents the effects of office probability on investments, conditional on power-sharing institutions. We restrict the analysis of conditional models to statements about technology and infrastructure since they are the only ones that are linearly predicted by office probability. The table of the interaction models, along with robustness checks of the interaction are presented in the Supplemental Appendix. The interaction shows that the positive effect of electoral competitiveness on technology and infrastructure statements decreases as political constraints on the executive increase. Electoral competitiveness has a significant positive effect on investments when political constraints are below 0.57, which is for about 75% of observations. The effect of electoral competitiveness is insignificant for the quarter of the sample with the highest degree of political constraints, since parties can use power-sharing institutions to limit the time inconsistency problem. The results reveal that office probability has a positive effect on investment only when political institutions are not putting strong enough constraints on the executive to limit parties’ time inconsistency problem.

Effect of office probability on technology and infrastructure statements, conditional on political constraints.

Discussion and conclusion

This study represents one of the first large N quantitative analyses of the effects of electoral competitiveness on parties’ capacity to prioritize future-oriented investments. It contributes to the literature on the politics of long-term investments (Jacobs, 2011, 2016; Lindvall, 2017). The distinction between different types of investment whose characteristics shape their relationship with office probability, as well as the modelling of a conditional effect between electoral competition and power-sharing institutions, are this article’s innovations relative to the innovative study of Kraft (2018) on the determinants of investments in party manifestoes.

We demonstrate that a party’s likelihood of entering office is one of the few significant predictors of the prioritization of investments in infrastructure and technology in its manifesto. The relationship between office probability and investment is linear, allowing us to reject the null of hypothesis 1a. However, this relationship is conditional on power-sharing institutions: political systems with strong political constraints on the executive limit parties’ time inconsistency problems regardless of the degree of electoral competitiveness they face. We thus contribute to the debate about which institutions favours long-term investments (Finnegan, 2019b; Jacobs, 2016; Lindvall, 2017) by suggesting that power-sharing institutions are more likely than power-concentrating institutions to allow parties to break the political uncertainty problem characterizing long-term investments.

Interestingly, investments in education and in environmental protection are not significantly affected by electoral competitiveness in linear models. Investments in education follow an inverted U-shaped relationship with electoral competitiveness: parties propose more education statements when elections are particularly competitive, confirming hypothesis 1b. This suggests that the politics of education is not dictated by inter-temporal trade-offs and voters’ myopia. In contrast, parties use education investments to attract voters, and are more encouraged to do so when elections are very competitive than when they already know their fate at the next election.

These results suggest that analysts must distinguish between different types of investments. In some cases, short-term electoral considerations may increase governments’ likelihood of proposing policies producing benefits in the long term. We might find such a different relationship between electoral competitiveness and types of investments because the intertemporal trade-offs of investments in education are less acute than those of investments in infrastructure and technology, since the former provide immediate benefits to influential constituencies such as parents and teachers. The effect of office probability is linear and significant when a policy is characterized by a strong degree of intertemporal trade-off and when it isn’t a particularly ideologically driven policy, like for infrastructure and technology investments.

Indeed, the effect of office probability on statements about the environment is insignificant, since they are determined by parties’ ideology on the state-market axis. Green parties’ ownership of the issue of environmental protection can help to explain why a party’s office probability does not affect the proportion of manifesto statements it allocates to the environment. Non-green parties cannot credibly commit to be the most likely party to deliver investments in environmental protection, even if they have a high probability of victory, further reducing their incentives to promise more investments in environmental protection. Moreover, mainstream parties tend to be slow to make the environment salient, leaving the issue to more peripheral parties (Farstad, 2018) and left-wing parties are the only ones benefiting electorally from making the environment salient (Schulze, 2021).

Our study suffers from three main limitations. Further research should analyse whether the conditional relationship we find for investment priorities expressed in manifestoes also influence policy choices, as manifesto pledges do not necessarily translate to policy choices (Jacques, 2021b; Mansergh and Thomson, 2007). Secondly, we cannot completely rule out reverse causality with the observational data at hand as it remains possible that parties become more successful because theypropose long-term investments. One solution would be to analyse in depth cases where parties’ office probability changes exogenously. Thirdly, our results also suggest that the log ratio of investment relative to short-term consumption is influenced by electoral probability. Using welfare state expansion as a measure of short-term consumption is inspired by the comparative political economy literature (Beramendi et al., 2015) which considers traditional cash benefits as consumption. However, a more fine-grained measure of short-term consumption would be necessary to confirm our results, since welfare state expansion includes some policies offering long-term benefits as well.

Still, this study provides a rare empirical test of the theory contending that electoral competition may influence parties’ capacity to propose long-term investments. While electoral competitiveness is crucial for a functioning democracy and can certainly lead to several positive outcomes, such as a greater responsiveness to voters’ preferences, this study suggests that some degree of electoral safety is beneficial for long-term investments. However, voters’ myopia doesn’t seem to be the main factor influencing investments, as none of our models display a U-shaped relationship between investments and electoral competition. Our results reveal that the politics of investments is more about credible commitments between parties and voters than about limiting governments’ responsiveness to voters’ myopic preferences. This suggests that the adoption of long-term investments may depend on a stable party system, within which political parties aim to maintain their reputation as competent long-term-oriented managers of the economy and can perceive themselves to be in office in the future. Hence, the destabilization of advanced democracies’ party systems might reduce parties’ incentives to propose long-term investments, as it diminishes the probability that a party will stay in office in the future.

Supplemental material

Supplemental Material, sj-pdf-1-ppq-10.1177_13540688211036382 - Electoral competition and the party politics of public investments

Supplemental Material, sj-pdf-1-ppq-10.1177_13540688211036382 for Electoral competition and the party politics of public investments by Olivier Jacques in Party Politics

Footnotes

Authors Note

The author Olivier Jacques is now affiliated with Université de Montréal, Canada.

Acknowledgments

Previous versions of the paper have benefited from comments by Axel Cronert, Dietlind Stolle, Silja Häusermann, Alan Jacobs, Catherine Moury, Julian Garritzman, Timo Seidl, Jared Finnegan, Per Andersson, Costin Ciobanu, Isadora Borges Monroy, Joan Ricart-Huguet, participants to the Midwest political science association conference 2021 and to the SASE conference 2021. The author wishes to thank the three anonymous reviewers of the journal for their insightful suggestions.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author wishes to acknowledge the postdoctoral scholarship from the Fonds de Recherche du Québec Société et Culture.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.