Abstract

In the aftermath of recent crisis, national governments across the global south increasingly see state ownership and control of finance as a vital public policy tool. What explains variation in state control of finance in the wake of crisis? Interventionist policies can elicit disinvestment or exit threats from private financial actors if they limit profitability. When disinvestment threats are credible, policymakers may rule out reform for fear of devastating economic consequences. I argue that the credibility of disinvestment threats is conditioned by two key variables, the resilience of the national economy to capital flight, which affects the level of damage capital flight will inflict, and global financial liquidity, which can be used to undercut domestic disinvestment threats. These arguments are developed through comparative case studies of cross-national and over-time variation in the scale and scope of public development banking in Brazil and South Africa in the wake of the 2008 crisis.

Keywords

Introduction

During the post-war period, governments across the developing world tended to ‘repress’ or exercise control over their financial sectors. State-owned banks, established either under public ownership or through nationalization of private banks, featured prominently. Since the onset of financial globalization in the 1980s, state ownership and control of the domestic financial sector steadily declined across the world. Financial globalization pressures have long been thought to encourage a convergence of national financial systems towards the liberalized Anglo-Saxon model. Furthermore, as capital account mobility increased financial actors’ capacity for exit over policies they disliked, reversal of financial liberalization reforms was thought to be all but impossible.

During the 2000s, this trend was disrupted, and unorthodox financial policies including public banking took on renewed importance in some emerging market (EM) countries (Bertay et al., 2012). Despite common shocks associated with the 2008 crisis, developing countries exhibited striking variation in their use of state-owned banking to manage the aftermath (Cull et al., 2018). Some governments scaled back, while others not only directed public development banks to mount strong countercyclical responses, but also play a continued role in resource allocation well after the end of the crisis period (Luna-Martinez et al., 2018). External globalization pressures alone cannot explain this variation. These recent trends indicate that financial globalization may limit national autonomy to a lesser extent than previously thought, and that financial actors are not always all-powerful. However, little is known about the conditions under which policymakers are able to exert autonomy and financial actors’ preferences are undermined.

In countries where domestic pressures to increase national control over finance are weak, it is unsurprising that governments will shore up market-based methods of resource allocation. Where such pressures are strong, often from domestic labour and industry groups concerned with job creation and access to investment credit, policymakers are likely to attempt to use crisis as an opportunity to increase public control of financial resource allocation. Out of the subset of EM countries where pressures are strong, why were some governments able to increase state control of the financial sector, through scaling up public development banks, while others were unable to push through significant financial reform?

I argue that this variation in policy outcomes depends on the credibility of the disinvestment or exit threats from the domestic private financial sector, which is likely to be opposed to public control. Because public development banks usually have access to subsidized funding sources, which enable them to make cheap loans, private banks perceive them as competitive threats, which can limit profits. Significant public development bank expansion may also increase government indebtedness and result in sovereign ratings downgrades, which trigger foreign portfolio outflows. This has negative knock-on effects for domestic banks and institutional investors, such as decreasing the value of their assets and increasing their borrowing costs.

Through its ownership and control of vital capital, the private financial sector has enormous potential structural power over policymakers. If domestic capital flees or foreign investors exit, this can inflict enormous economic damage. But this potential structural power becomes decisive only when policymakers perceive disinvestment threats to be credible. I argue that credibility is conditioned by two key variables: the resilience of the national economy to capital flight and the global financial cycle, which affects the availability of external replacement capital. When policymakers perceive national financial resilience to be strong, and replacement capital is readily available during global financial booms, they are likely to ignore disinvestment threats and aggressively increase state control of finance, and vice versa.

This could explain the rise of unorthodox financial policies among the major EMs with stronger external balances, including China, Brazil, India, Russia and Argentina, in the post-crisis high liquidity period (Ban and Blyth, 2013; Chen, 2020). In countries with extensive capital controls that never seriously liberalized in the first place, such as India and China, external market pressures should be even more muted, though not absent due to dollar requirements and illegal capital flight. Major oil exporters such as Venezuela and Kazakhstan should have the policy autonomy for interventionism due to an abundance of foreign exchange during commodity booms (Jepson, 2020). On the other hand, more limited deviations from orthodoxy or further liberalization in EMs such as South Africa, Mexico, Colombia, Turkey, Romania and the Philippines could be due to either policymakers’ perceptions of weak financial resilience or a lack of demand from domestic interest groups.

Policymakers have historically used a variety of tools to control financial resource allocation. The scale and scope of national development banks are the main focus of this paper because they are the most direct form of state control. They can be mandated to channel funds according to strategic government priorities, 1 and are the main tool of financial control used in my country cases. More indirect tools include interest rate controls, credit quotas to direct private bank lending, banking entry restrictions and loan guarantees among others. While the tools may vary, the purpose is similar: to direct financial resources to priority sectors in volumes or at prices they would not receive privately, often against market signals, and with the aim of structurally transforming the economy, usually as part of an industrial policy. State control implies that the financial sectors, or parts of it, no longer function according to a purely profit-making logic, but are free to pursue a broader range of objectives, for better or worse.

Relying on 113 interviews conducted during extensive fieldwork, I utilize in-depth comparisons of the scale and scope of public development banking in Brazil and South Africa to examine my claims. Despite the common shock of the 2008 crisis and global liquidity boom that followed, public banking responses diverged sharply. This was despite strong pro-intervention pressures from a coalition of labour and industry, and centre-left governments in power in both countries. After the 2008 crisis, Brazil’s public banking sector became one of the largest and most interventionist in the world, while South Africa’s remained small and passive.

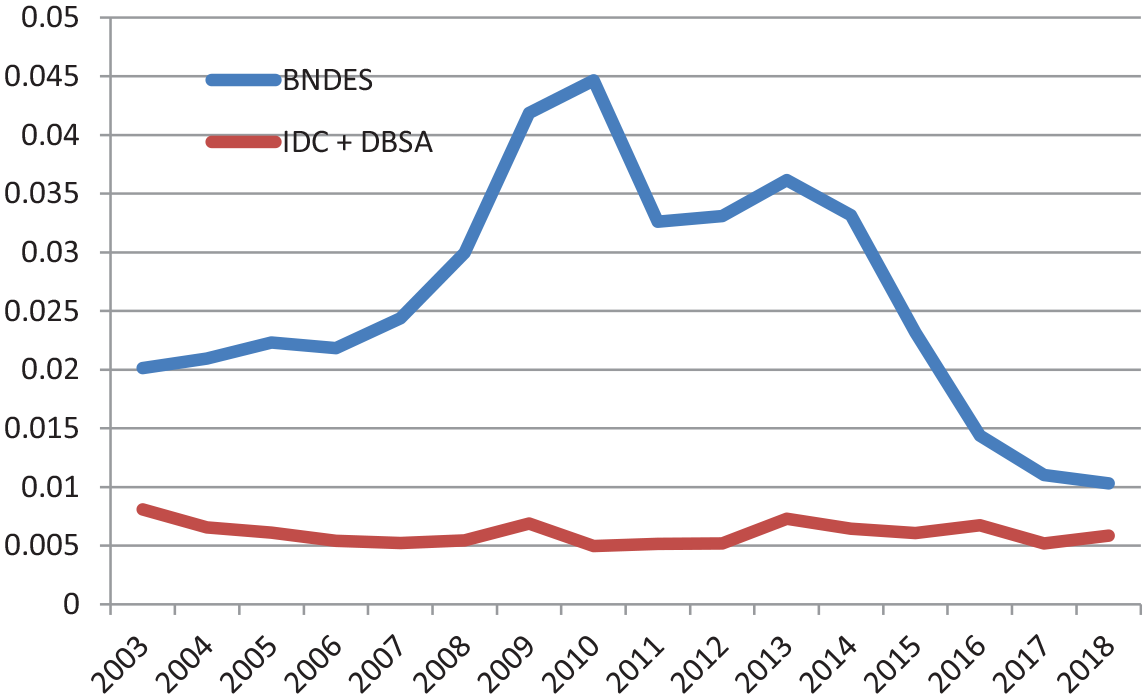

Between 2006 and 2014, Brazil’s main national development bank, the National Bank for Economic and Social Development (BNDES), was scaled up dramatically in comparison with South Africa’s main development banks, Industrial Development Corporation (IDC) and the Development Bank of Southern Africa (DBSA), after which BNDES was dramatically scaled down once again (Figure 1). While scale is a useful proxy for state control, and enables rough cross-national comparison, more important is the scope: the extent to which public banks play a market-defying role through lending to developmentally important sectors that might be more risky, or less profitable, and the amount of state support they receive to enable this. BNDES was aggressively expanded through direct fiscal transfers, which insulated it from market pressures. This allowed it to take on a market-defying role by financing priority sectors at favourable terms and exerting strategic influence over their investment decisions through the use of conditionalities. The IDC and DBSA on the other hand were denied significant additional budgetary resources, leaving them not only small in scale, but more importantly, limited in scope and unable to engage in developmental activities. Because IDC had to appease its private funders, it was unable to make risky long-term investments, instead supporting mainly sectors that were already established and profitable, but not necessarily beneficial for development, based on commercial considerations.

Development bank activity (loan disbursements % GNI).

This article makes a number of contributions to the literatures on globalization and policy autonomy and business power. I show how international financial market pressures on policymakers are often indirect, conditional on enforcement by domestic financial actors. By considering EM cases, I account for how a state’s location in the international economic hierarchy conditions the capacities of domestic actors exercising structural power. Furthermore, I shed light on the conditions under which domestic financial actors prevail in political struggles over the control of resource allocation, and those under which they lose. In doing so, I highlight how domestic financial actors’ structural power, and policymakers’ autonomy, varies over time with global liquidity and cross-nationally with perceived vulnerability to capital flight. More broadly, the analysis reveals that developing country policymakers exercise agency in some aspects of their engagement with international finance, while others remain outside their control.

Competing explanations for state interventionism

Partisan approaches (Huber and Stephens, 2012; Murillo, 2009) link variation in policy outcomes to variation in the preferences of the dominant party. Governments composed of left-leaning parties are more likely to be responsive to pressures for financial control to satisfy the distributional preferences of their support base, or due to ideological pre-dispositions. However, this alone is not sufficient: left governments frequently renege on anti-business campaign promises following elections under business pressure (Campello, 2014). Empirically, the timing of interventionist financial policies does not follow the election of left governments in my cases.

Historical institutionalists emphasize how past experience and long-standing policy differences continue to influence current policy outcomes (Lieberman, 2003). However, the historical record shows that the BNDES and IDC played a comparably central role in industrial policy during the import substitution industrialization era by providing subsidized funds for risky new ventures (Fine and Rustomjee, 2018; Von Mettenheim, 2015). Both banks were corporatized but not privatized over the 1980s and 1990s. While path dependency may explain the renewed focus on these long-standing institutions as the key tool of financial control, it cannot explain why the scale and scope of these institutions changed so dramatically over time, and why they differed so much between cases.

Constructivist political economy points to the ideological orientation of key actors to explain interventionism (Sikkink, 1991; Thurbon, 2016). Developmentalist ideas that finance should be directed towards productive sectors through state control may be traced back to historic formative experiences of policy elites (Thurbon, 2016) or domestic international policy from peer countries (Ban, 2016; Dobbin et al., 2007). Developmentalist ideas about finance had a deep-rooted history and were prominent at high levels of government in South Africa as well as Brazil (Habib and Padayachee, 2000), and both countries were part of similar international networks. Policy norms and diffusion certainly focused societal demands for financial intervention on development banking and fed into policymakers’ motivations, but cannot explain varying outcomes.

The Ministry of Finance (MoF), which controlled budgetary allocations to development banks, was dominated by developmentalist policymakers in Brazil between 2006 and 2015, but liberal policymakers in South Africa. However, this difference is itself explained by structural power. Leaders worried about disinvestment threats may appoint liberal rather than developmentalist policymakers to key positions to signal their commitment to pro-market policies. As evidenced in later empirical sections, in Brazil, developmentalists were only appointed to influential ministries after disinvestment threats became less credible, while in South Africa they were appointed only to ministries of secondary importance as disinvestment threats endured.

Others point to the preferences of sectoral or other interest group coalitions and how they are aggregated (Bunte, 2019; Pepinsky, 2008). In both Brazil and South Africa, pro-intervention labour and manufacturing groups influenced policymakers at developmentalist ministries and left leaning political parties formally through lobbying by their representative associations, and informally through personal connections, yet policy outcomes diverged sharply. While interventionist labour or manufacturing group preferences are likely to be a necessary condition, because without these demands policymakers would not face sustained pressure to implement such contentious policies, this explanation remains incomplete without an account of variation in the power of these groups. Structural power explanations offer such an account.

Structural power explanations

Because economic elites control the investible resources on which the economy depends for growth and employment, credible threats of disinvestment or capital flight may force policymakers to rule out or backtrack on certain reforms (Fairfield, 2015; Winters, 1996). Due to its unique ability to extend credit to firms and government, the domestic financial sector is considered to have a privileged position in the economy (Culpepper, 2015; Roos, 2019). Similarly, external creditors such as the International Monetary Fund (IMF) and World Bank are able to impose financial liberalization conditionalities on borrowing governments because they can cut off access to vital hard currencies (Roos, 2019). For upper-middle-income countries, private foreign investors were the most important source of low-conditionality source of external finance during the period under study (Cormier, 2022; World Bank Group, n.d.).

Despite attaching no formal conditionalities to their lending, foreign portfolio investors are thought to impose market discipline on interventionist governments through their capacity for exit over policies they dislike (Mosley, 2003). Developing countries whose assets are seen as risky by foreign investors are especially vulnerable to capital flight; its consequences are also likely to be more severe due to the sheer size of foreign institutional investors’ balance sheets relative to small domestic markets (Akyüz, 2017).

Recent studies show that market discipline is weakened during high liquidity periods because international investors become risk tolerant, while policymakers face less pressure to attract foreign capital (Ballard-Rosa et al., 2021; Campello, 2015; Zeitz, 2021). Foreign portfolio investors are more responsive to global financial cycles, driven by US interest rates, than to recipient country-specific economic policy. When US interest rates are low, investors move into EM assets in search of higher yield, resulting in a virtuous circle of inflows and ratings upgrades. The opposite occurs during high interest rate periods (Akyüz, 2017; Bauerle Danzman et al., 2017; Rey, 2015). Furthermore, while substantial evidence exists that international financial markets react directly to key macroeconomic outcomes such as debt, growth and inflation, Mosley et al. (2020) show that the same does not hold for microeconomic supply-side policies. Despite being scapegoated by governments as a key impetus for supply-side reforms such as financial, labour market or tax policies, foreign investors do not actually react to these systematically (Mosley et al., 2020).

While these studies highlight how market discipline is contingent on global liquidity, less is known about why governments respond so differently to similar external market pressures when it comes to making policy choices. Similarly, little is known about the relationship between market discipline and specific supply-side policies such as public banking and other forms of financial interventionism.

My paper fills this gap by tracing out the causal mechanisms by which these international market conditions are connected to specific domestic policy choices. I show that not only do the disciplining effects of international financial markets vary over the course of the global financial cycle, but also that they are largely conditional on enforcement by domestic financial actors, who have more at stake than foreign investors when it comes to interventionist financial policy.

National financial resilience, global liquidity and the credibility of disinvestment threats

Disinvestment threats by domestic actors can take different forms, including a reduction in domestic lending by private banks, a reduction in demand for government bonds by domestic banks or institutional investors or a capital flight out of local and hard currency assets by domestic and foreign banks and institutional investors. 2

Domestic financial actors have to take strategic action to convince interventionist policymakers that interventionism will increase debt or reduce private bank lending, will cause disinvestment and exit and will damage the economy. For threats to be credible, policymakers need to perceive that the dangers are both real and consequential enough to produce a cascade of damaging economic effects.

This is not just an automatic reaction by policymakers to market realities. Extreme uncertainty exists about the effects of interventionist policies, whether or not these effects will cause disinvestment or exit, and if disinvestment or exit occurs, how damaging this will be to the economy. As a result, policymakers form perceptions about the credibility of disinvestment threats in constant dialogue with domestic and international financial actors, either directly through conversations between Ministries of Finance or central banks and business associations or firm representatives or indirectly through monitoring the financial press or market movements. Policymakers often actively seek the help of domestic financial actors when trying to predict policy effects due to their perceived expertise in the subject. It is also possible that interventionist policymakers misjudge and then backtrack, or miss opportunities for reform by being too cautious.

Although foreign financial actors and rating agencies frequently state they will react negatively to interventionist financial policies, their actions do not always reflect their rhetoric. Foreign investors are likely to flee if expansion of public bank funding and lending increases debt or risk to the extent of triggering downgrades or even sovereign debt or domestic banking crisis. Outside of these extreme scenarios, there is a large grey area where the effects of interventionism are uncertain and may not be considered serious enough to act upon by foreign investors. This is particularly likely when core country interest rates are low and foreign investors have strong incentives to increase investments in high-yielding emerging markets regardless of host country fundamentals.

Because exit by foreign institutional investors is so much more damaging than what domestic financial actors could achieve on their own, domestic actors have an incentive to exploit this uncertainty over the effects of interventionism, to convince policymakers of the likelihood of foreign exit. Financial actors are not the only ones who act strategically. Liberal factions within government might also use financial actors’ disinvestment threats tactically to achieve their own ideological or partisan objectives, or might genuinely believe interventionist policies will be economically damaging.

Domestic financial actors and their allies frequently make domestic disinvestment, resident flight and foreign exit threats in response to policies they dislike, but these are not always effective. Policymakers’ perceptions of two key factors, a state’s financial resilience to capital outflows and global liquidity, influence the leverage of private financial actors by making policymakers more or less likely to find disinvestment threats credible.

Capital flight can have a harmful effect on external balances due to causing sharp currency depreciation, exponential increases in borrowing costs and debt and, in extreme cases, balance of payments crisis (Akyüz, 2017; IMF, 2019). It can also affect domestic financial stability, by increasing domestic borrowing costs for governments, SOEs and banks, causing assets held by domestic financial actors to deteriorate in value, causing imported inflation and, in extreme cases, domestic banking crisis (Brunnermeier et al., 2012).

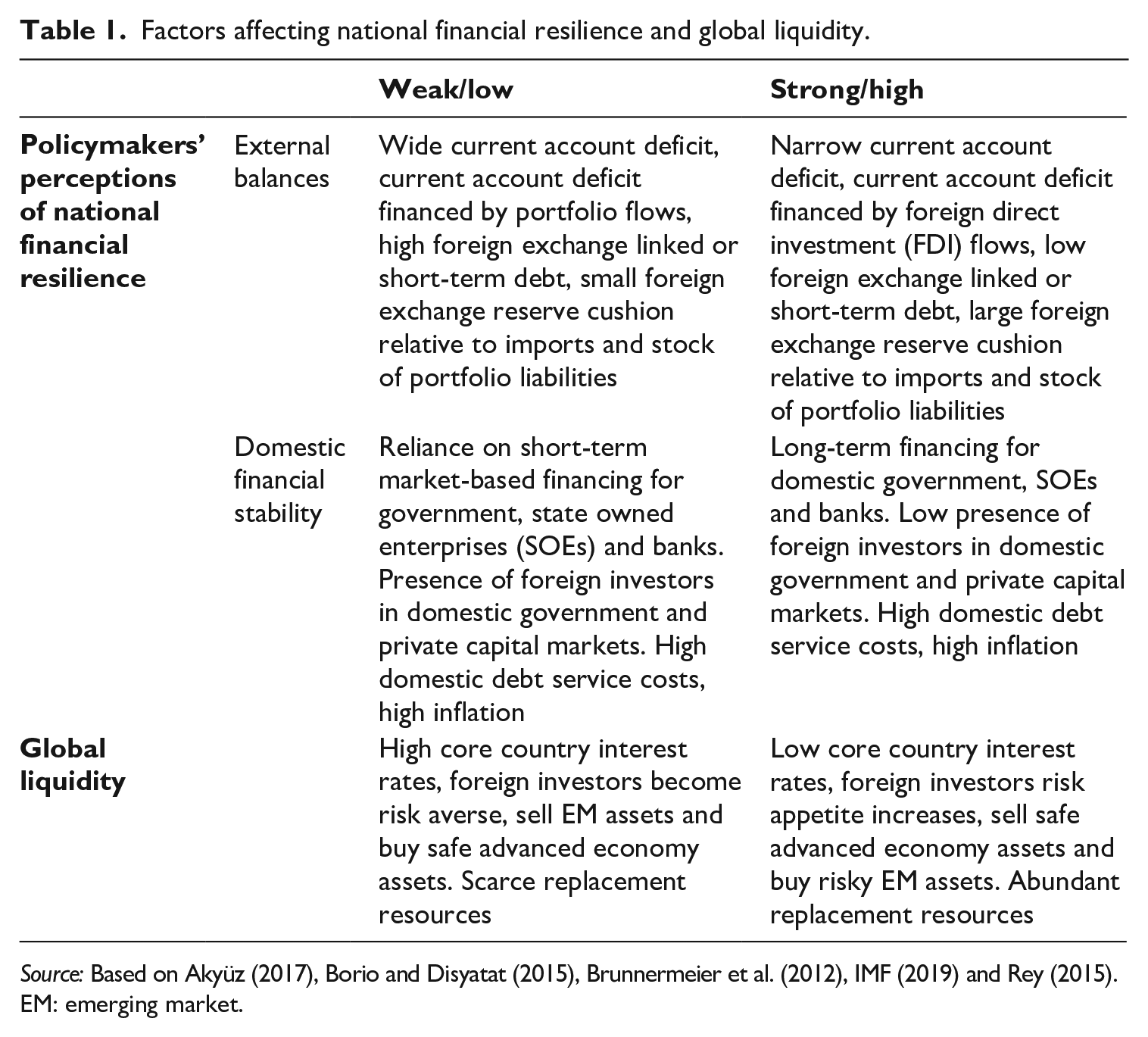

Policymakers’ perceptions of how resilient the economy may be to this kind of damage are likely to be shaped by a variety of national characteristics (Table 1). These include the size and composition of the current account deficit and national debt, which influence external financing needs, whether these needs are financed by volatile portfolio flows or more stable direct investment, and the extent of foreign exchange reserve cushions which can be used to defend against capital outflows and adverse currency movements. Reliance of governments and banks on market-based financing also influences the extent to which capital outflows may result in domestic financial instability. Policymakers may perceive financial resilience to be weak if even one of these characteristics is seen as an Achilles heel or these indicators are strong but exhibiting a weakening trend. Different aspects of financial resilience may become more or less salient over time, depending on what policymakers perceive to be important.

Factors affecting national financial resilience and global liquidity.

Source: Based on Akyüz (2017), Borio and Disyatat (2015), Brunnermeier et al. (2012), IMF (2019) and Rey (2015).

EM: emerging market.

The more serious policymakers perceive the consequences of capital flight to be for external balances and domestic financial stability, the more likely they are to be sensitive to disinvestment threats. On the other hand, when financial resilience is perceived to be strong, policymakers are more likely to ignore these threats.

Policymakers are also more likely to be sensitive to exit threats by domestic financial actors during periods of low global liquidity, when capital outflow by foreign investors is more likely and the state lacks easy access to external borrowing with which to undercut the disinvestment threats of domestic finance. Low global liquidity may also weaken policymakers’ perceptions of financial resilience, and vice versa, because national financial resilience is not completely independent of external factors. For instance, low liquidity decreases reserves via dollar outflows, increases debt service costs via putting pressure on central banks to increase interest rates and increases inflation via currency depreciation, and vice versa. Periods of high global liquidity, or access to any other form of low-conditionality external finance, on the other hand result in easy access to replacement resources, which policymakers can use to fund expansion in public banks, and undercut exit threats of domestic finance (Table 1).

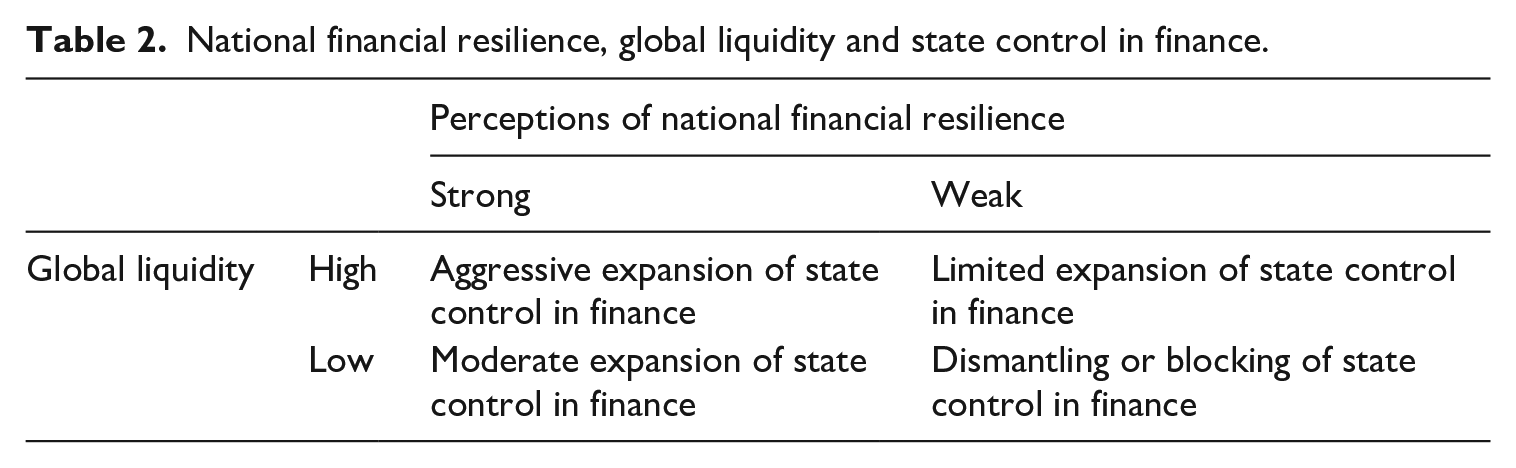

Policymakers are likely to be most sensitive to disinvestment threats when national financial resilience is perceived to be low and global liquidity is low (Table 2, lower right quadrant). Under these conditions, blocking of demands for or scaling back of state control in finance is likely. On the other hand, when financial resilience is perceived to be strong and international markets are flush with liquidity, policymakers are most likely to ignore disinvestment threats, and aggressively expand state control (Table 2, upper left quadrant).

National financial resilience, global liquidity and state control in finance.

If policymakers perceive financial resilience to be strong during conditions of unfavourable global liquidity, they may conduct interventionist policies, but the scale is likely to be limited due to difficulty in finding resources (Table 2, lower left quadrant). On the other hand, if policymakers perceive vulnerability to lesser capital movements or ratings downgrades, access to replacement capital might not be sufficient to undercut the structural power of domestic investors, and expansion of state control in finance may still be blocked, or limited (Table 2, upper right quadrant).

The vagaries of the global financial cycle are outside the control of policymakers. While it is hard for policymakers to improve financial resilience when external conditions are unfavourable, favourable external conditions by themselves are not sufficient to generate lasting improvements. Policymakers also need to utilize deliberate strategies to undermine the structural power of finance, such as eschewing consumption to build sizable reserve cushions and influencing external debt composition to reduce foreign currency debt. While financial resilience is not completely independent from external factors, in contrast to global liquidity, policymakers can exert at least some influence over it.

Methods

This paper combines cross-national and over-time case comparisons in Brazil and South Africa. Comparing two countries across four time periods yields eight cases, featuring all four combinations of the two independent variables, financial resilience and global liquidity. This allows me to make inferences about the mechanism by which variation in the independent variables leads to changes in the scale and scope of public banking policies.

The country case selection follows a most similar logic. To explore the argument that variation in policymakers’ perceptions of national financial resilience influences financial interventionism, I compare countries that vary on this score, but are otherwise as similar as possible with regard to other variables of interest (Gourevitch, 1986; Lieberman, 2003). Brazil and South Africa share a number of similarities that help rule out alternative explanations. Both are middle-income countries with similar industrial structures where industrial and labour groups hold a similar position in the domestic economy and have a similar intensity of preferences for financial interventionism. Both have largely open capital accounts and occupy a similar position in the international monetary hierarchy and so are subject to similar movements in global liquidity. Both countries had left-leaning governments in power, similar institutional and state capacities, similar prevalence of developmentalist ideologies among policymakers and within political parties and similar historical experiences with financial interventionism followed by liberalization.

The four-period over-time comparison, divided according to common global financial conditions, allows me to explore how variation in global liquidity impacts policy within each country. In period 1 (2003–2007), a financial and commodity boom began in 2003, following a period of low global liquidity. Period 2 (September 2008–2009) began when the collapse of Lehman brothers triggered a sudden stop in capital flows to EMs. The situation reversed in period 3 (late 2009–May 2013) after core economies responded to the crisis by lowering interest rates and launching quantitative easing programmes, flooding international markets with liquidity. The boom ended in period 4 (2013–2017), when the Fed’s May 2013 announcement that it would begin scaling back quantitative easing (QE) triggered the ‘taper tantrum’, a global investor panic (Akyüz, 2017). The analysis ends in 2017 when expansion of state control in finance ceased to be a serious policy option in both countries.

Evidence for within case analysis draws heavily on 113 in-depth interviews with key informants conducted during extensive fieldwork in Brazil (Sao Paulo, Rio de Janeiro and Brasilia) and South Africa (Johannesburg, Pretoria and Cape Town), between March 2017 and June 2018, as well as national statistics, public and private documents and newspaper articles. Interviewees include high-level policymakers, development bankers, private sector representatives from peak and sectoral business associations and umbrella and sectoral labour unions, targeted through snowballing until saturation point was reached. A full list of anonymized interviewees is given in Appendix 1.

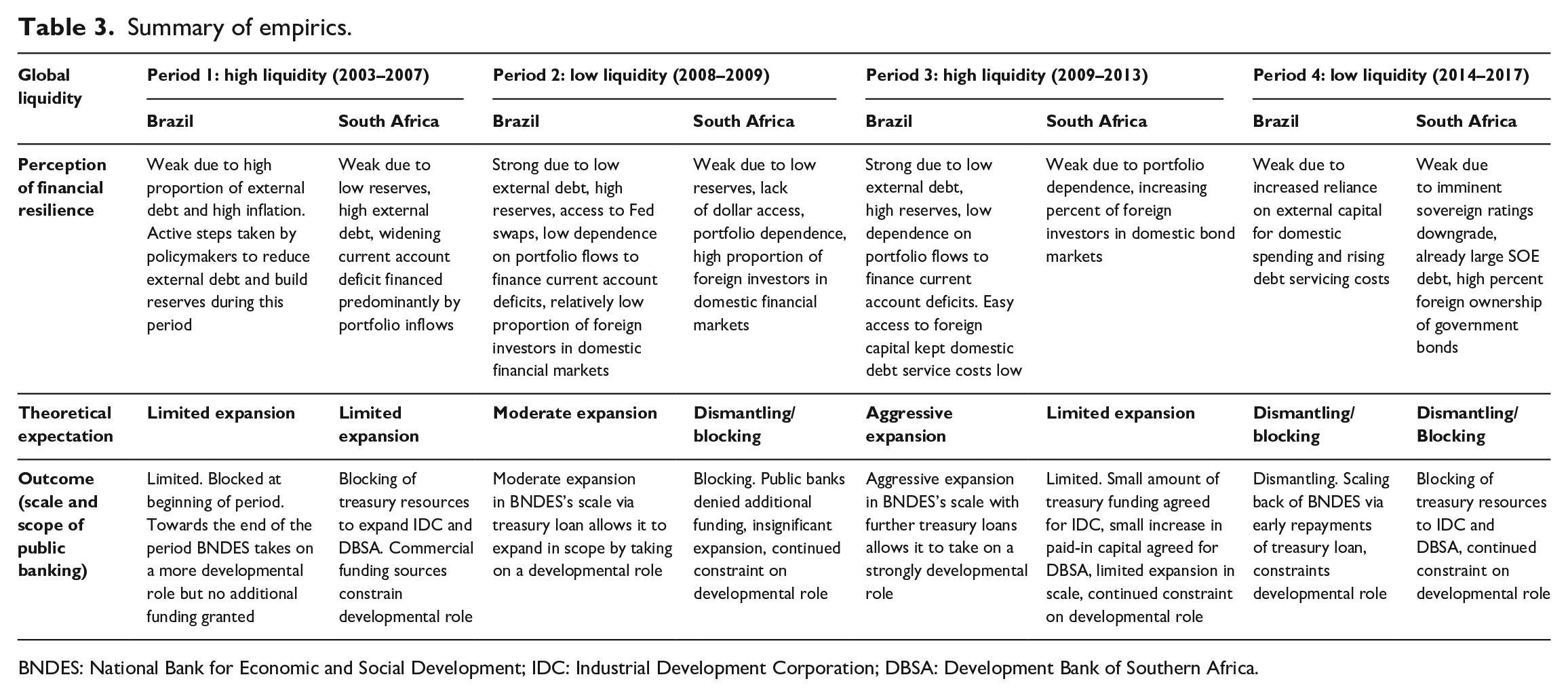

In the following sections, I examine how international financial conditions first enabled and then worked against increased financial interventionism in Brazil. I then show how similar international conditions did not produce a parallel escape from structural constraints in South Africa, as domestic financial actors’ disinvestment threats remained credible due to continued weak financial resilience. The empirics are summarized in Table 3.

Summary of empirics.

BNDES: National Bank for Economic and Social Development; IDC: Industrial Development Corporation; DBSA: Development Bank of Southern Africa.

Brazil

Period 1: high global liquidity (2003–2007)

In period 1, weak financial resilience and high global liquidity resulted in only a limited expansion of public banking in Brazil. In October 2002, the leftist PT (Workers’ Party), that had historically advocated for radical financial policies, including bank nationalization, won a historic victory under the leadership of Luiz Inacio Lula de Silva. Its support coalition included unionized workers and sections of the traditional manufacturing elite, which had suffered from expensive credit and severe import competition after financial and trade liberalization (Saad-Filho and Morais, 2018). The manufacturing sector required subsidized credit for investment, 3 while industrial labour unions supported access to credit for their sectors and viewed high interest payments to banks as resources that could be put more productively towards job creation and social programmes. 4

These demands were successfully blocked by the opposition of domestic investors, which had punished the PT with capital flight and currency crisis during the electoral campaign (Campello, 2015). In addition to assuming power at a time of low global liquidity, policymakers perceived national financial resilience to be weak. Two-thirds of the public debt was directly linked to exchange rates or short-term interest rates, increasing the likelihood that capital flight and resulting currency depreciation would result in a balance of payments crisis (Orair and Gobetti, 2017). Inflation was already high due to the prior currency depreciation (Barbosa-Filho, 2008), so the leadership was wary of increasing funding to public banks in case it further triggered inflationary expectations. 5

Not only was the PT’s historically leftist agenda, which included outright bank nationalization, completely off the table, but the first Lula administration kept Brazil’s IMF loan and associated conditionalities in place, and made liberal appointments to important portfolios to signal commitment to orthodox economic policies (Barbosa-Filho, 2008; Campello, 2015). These policymakers rejected demands for increased public spending to fund BNDES, arguing that this would result in an unsustainable debt burden, lead to devaluation of the Real and increase inflation. 6

Although the financial and commodity boom began in 2003, soon after the first Lula administration took power, it was not until policymakers took deliberate steps to improve financial resilience, to reduce vulnerability to exit threats that leftward shifts were made in domestic financial policy.

Policymakers at the MoF took advantage of strong dollar inflows, which reduced hard currency borrowing needs. The Treasury conducted active debt management policies and used hard currency resources to repurchase existing private foreign exchange linked and short-term external debt, so that debt would not spiral out of control in the event of currency depreciation (Caputo Silva et al., 2010: 69). By late 2005, Brazil had enough dollars to repay remaining IMF and Paris Club debt ahead of schedule to be free of policy conditionalities. The central bank began building up foreign exchange reserves as a form of self-insurance, to shield against capital flight and adverse currency movements.

It was only by the end of the first period, once global liquidity was high and financial resilience had improved that the Lula administration began to shift policy leftward, appointing developmentalists to key positions. Guido Mantega, associated with the left of the PT and disliked by private banks, 7 was appointed finance minister in March 2006. Following a second victory for the Lula administration in the October 2006 presidential election, Luciano Coutinho, a developmentalist economist seen as a natural ally of the industrial manufacturing sector, 8 was appointed president of BNDES in April 2007. These appointments, made in the midst of a financial boom, did not trigger investor exit. However, Henrique Meirelles, who came from a private financial sector background, was kept on as president of an independent central bank with an inflation-targeting mandate (Saad-Filho and Morais, 2018).

President Lula authorized Coutinho to take on a more strategic industrial policy role and scale up operations moderately, but without providing an additional funding source. The result was a moderate increase in scale, and a temporary funding gap of 15bn Real which had to be filled through expensive short-term market borrowing which would have proved unsustainable in the long run. 9

Period 2: the post-crisis reform window (2008–2009)

In period 2, strong financial resilience and low global liquidity resulted in a moderate expansion of public banking. When the 2008 crisis hits, capital flows to Brazil reversed, causing a severe foreign exchange shortage (Stone et al., 2009). Despite low global liquidity, capital outflows and ratings downgrades, MoF policymakers were not overly concerned, due to strong financial resilience In Brazil people don’t care if you are not investment grade. The government has very little external debt. Because of our strong external account . . . being investment grade or not is not so dramatic. Most of our current account deficit is financed by FDI, which also means it is much less volatile. Our stock market is not that big. Our companies borrow abroad but not too much.

10

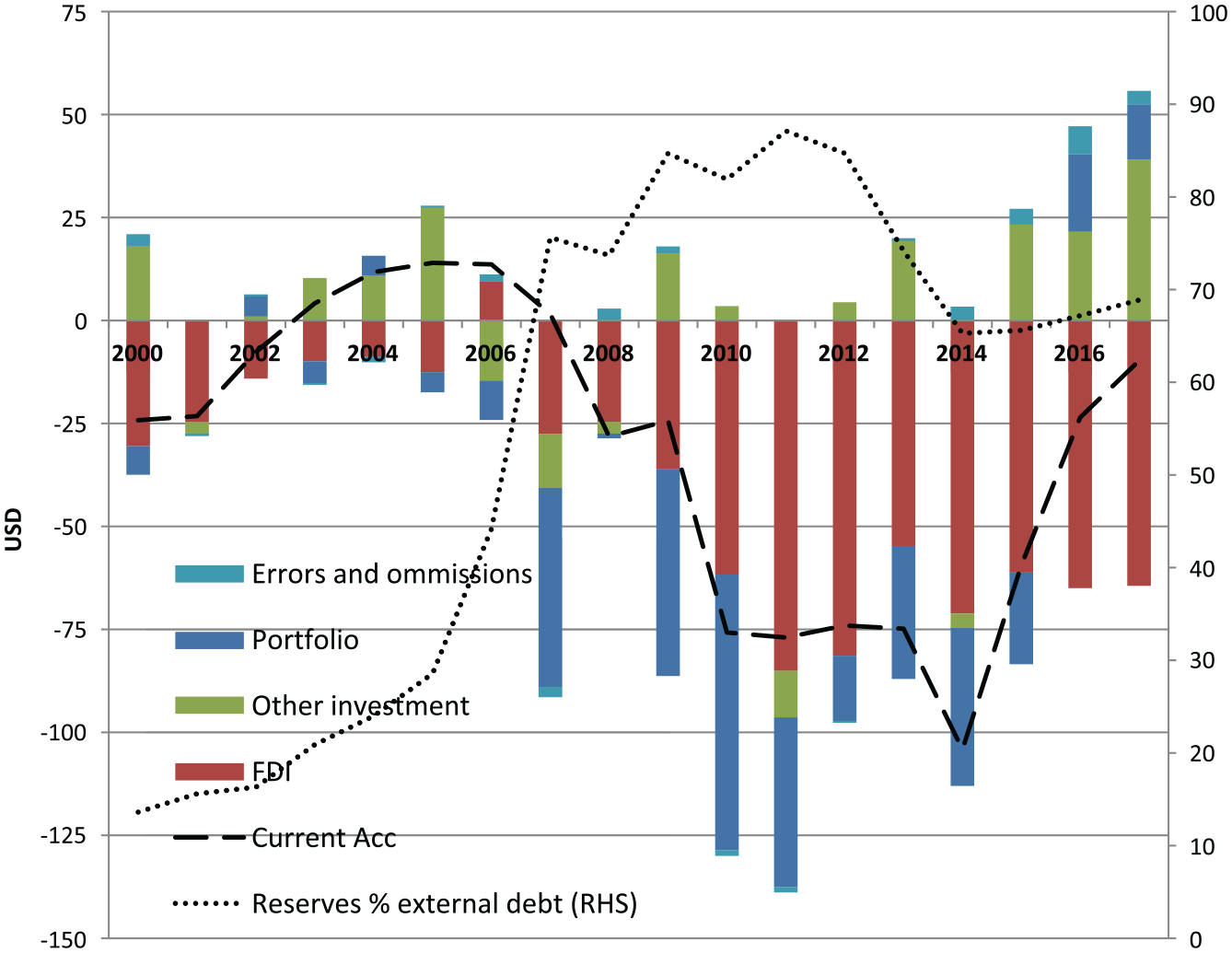

Due to policymakers’ actions in the previous period, Brazil was relatively well cushioned. Foreign exchange-linked debt was low, the central bank had a strong reserve position and the relatively narrow current account deficit was financed mainly by FDI (Figure 3). Furthermore, the bilateral swap offered by the Federal Reserve gave the state direct control over an important source of dollars, which allowed the central bank to use its own reserves to defend the currency. This in turn enabled it to keep interest rates low, allowing for fiscal expansion.

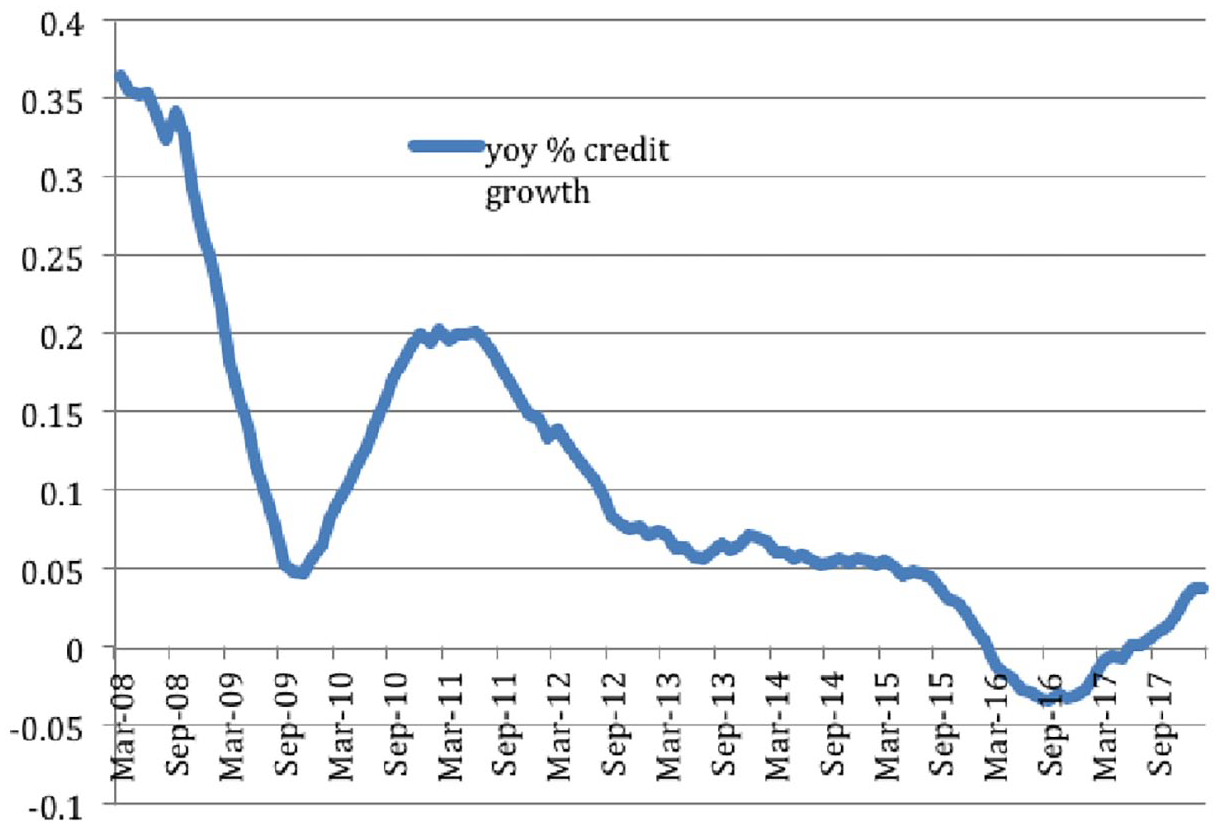

In the immediate aftermath of the crisis, Brazilian private banks became risk averse and scaled back their domestic lending (Figure 2). This created a reform window between approximately September 2008 and September 2010. Focused on retrenchment, private banks did not see BNDES and public commercial banks Banco do Brazil and Caixha Economica Federale as a competitive threat to their profits, and were not opposed to them stepping in to ease the domestic and foreign exchange credit crunch. 11 According to a private bank representative, ‘initially a lot of us thought it [scaling up of public banks] was ok . . . a few were suspicious, but there was no huge fear it could become permanent’. 12

Brazilian private bank lending.

Brazil current account position and financing.

Because private lending had already dropped sharply, policymakers were not worried that scaling up public banking would induce further private disinvestment. Instead policymakers took measures to co-opt private banks by sharing some of the profit. About half of BNDES’s activities were conducted through on-lending arrangements. BNDES offered cheap loans to private banks, which would assume the credit risk and on-lend at higher interest rates of their choosing: ‘this was the way we envisaged to have private banks aligned with BNDES and not always orchestrating campaigns against’. 13 Private banks were also allowed privileged access to the lucrative consumer finance market, as well as allowing them to charge high interest rates on corporate lending and investment in government bonds. 14

In response to intensified demands for countercyclical credit from its support coalition of labour and industry, PT policymakers launched a stimulus package centred on the expansion of activities by public banks and SOEs (Saad-Filho and Morais, 2018). The PT leadership overcame its initial reluctance and increased BNDES’s budgetary funding through a series of subsidized long-term loans and capital injections directly from the Treasury, supported by a developmentalist finance minister. 15 These budgetary funds allowed BNDES to increase its disbursements by over 50 percent between 2008 and 2009 alone (BNDES, 2009). Public commercial banks Banco do Brasil and Caixa were also instructed scaling up their consumer and corporate working capital lending as part of the countercyclical measures. 16

Period 3: high global liquidity (2009–May 2013)

In period 3, strong financial resilience and high global liquidity resulted in an aggressive expansion of public banking. After late 2009, high global liquidity gave policymakers access to vast replacement resources. Foreign inflows into the Real-denominated government bond market allowed the MoF to make local currency loans to the BNDES cheaply, without relying on borrowing from domestic private banks. 17

The PT administration won the October 2010 election under Dilma Rousseff. Rousseff maintained the Lula administration’s core economic team, but replaced central bank President Meirelles with Alexandre Tombini, a technocrat seen as more closely aligned with her political priorities (Brandimarte, 2013).

Industrialists became increasingly reliant on BNDES, viewing subsidized loans as compensation for rising labour and tax costs under the PT government. 18 Moreover, as the economy boomed, industrialists looked to increase investment, but found credit was still too expensive despite BNDES subsidies, 19 while industrial labour unions continued to decry high interest costs. 20 In October 2011, manufacturing associations Federation of Industries of the State of Sao Paulo and Brazilian Association of the Machinery and Equipment Industry formally allied with major industrial labour unions to launch the ‘campaign for a Brazil with lower interest rates, more jobs and greater production’, which lobbied the government and the central bank to lower interest rates (ANDIF, 2011; Severo and Gamon, 2011).

The Rousseff administration responded to these pressures by pressuring BNDES to lower its average long-term lending rates, which made it harder to on-lend through private banks. 21 Banco do Brasil and Caixa were also instructed to lower their own interest rates to force private banks to follow suit through competitive pressures. In addition, the central bank began lowering the policy rate (SELIC) from 12.4 percent in August 2011 to 7.25 percent by April 2013, its lowest value since 1986 (Singer, 2015).

After 2012, when the Rousseff administration began reducing interest rates, private banks turned decisively against the government’s interventionist financial policies, complaining about unfair competition from banks with state-subsidized funding sources. 22 Private bank profits were squeezed from all sides. Since they could no longer easily profit from investment in government bonds due to a lower SELIC, they were forced to turn to real economy lending, but found that BNDES had captured their market share in the commercial working capital and SME loans markets, and Banco do Brasil and Caixa in personal loan, credit card, automobile and mortgage finance markets.

Private banks argued that since they were forced to lower interest rates due to ‘political rather than market forces’, this would crowd out private sector lending, lower profitability, lead to higher levels of default and reduce lending and investment down the line. 23 Private banks and institutional investors also threatened to disinvest from government bonds, arguing that treasury financing of BNDES presented an unsustainable fiscal burden leading to ratings downgrades and potential default, and that public bank lending was inflationary. 24

International organizations, including the IMF, World Bank, and The Organisation for Economic Co-operation and Development (OECD), joined private banks in arguing that the scale of public banking would reduce investment and decrease creditworthiness (IMF, 2012; OECD, 2013). This was ignored by policymakers who were no longer reliant on them for borrowing. 25 Ratings agencies criticized financial interventionism due to increased public bank risk exposure and associated fiscal burdens. 26 However, the actual direction of flows ran counter to these warnings, and capital inflows triggered ratings upgrades for both the sovereign and the public banks (Moody’s, 2012).

In April 2012, the president of FEBREBAN met with Nelson Barbosa, Executive Secretary at the MoF to present private banks’ views. Strong financial resilience and high global liquidity meant that policymakers could not be credibly threatened with ratings downgrades and capital flight.

27

Domestic disinvestment threats were not effective either, as long as easy access to external replacement resources provided an outside option to reliance on domestic banks and investors. Any reduction in domestic private lending could be replaced through further expansion of public bank lending, funded by the Treasury via foreign borrowing. Domestic private divestment from government bonds could also be replaced by foreign borrowing. According to a former Minister of Finance: the huge level of international liquidity meant there was a lot of foreign investors that would buy long-term treasury paper in Real. This allowed Treasury to finance BNDES with long-term liability without currency mismatches . . . if it was done just locally through borrowing from the [private] banks then it would be more expensive.

28

As a result, private banks calculated that if they did not reduce their spreads, they would simply lose even more market share to public banks. 29 Later that April, the president of the Brazilian Federation of Banks acquiesced to the demands of the MoF and private banks began reducing spreads, causing their profitability to decline (Singer, 2015).

National financial resilience began weakening during the latter part of the boom due to rising domestic debt service costs. In April 2013, the independent central bank began hiking interest rates and imposing credit restrictions to control inflation (BCB, 2013). Higher interest rates in the context of vast fiscal expansion and growing deficits reduced financial resilience by increasing the cost of domestic borrowing. The government became increasingly reliant on continued capital inflows to keep the borrowing costs of funding public banks under control. 30

Period 4: end of the financial boom (May 2013–2017)

In period 4, weak financial resilience and low global liquidity resulted in a scaling back of public banking. Lower global liquidity forced the central bank to continue increasing interest rates in an attempt to prevent capital flight and currency depreciation, causing policymakers to fear that domestic debt-servicing costs would spiral out of control. 31 In June 2013, Standard and Poor’s (S&P) changed its sovereign rating outlook from BBB (two notches above investment grade) stable to negative, citing slow growth and continued treasury borrowing to support public banks. 32 As access to external replacement resources for the financing of public banks dried up, and ratings downgrades became imminent, the government became increasingly reliant on domestic financial actors for its borrowing. Policymakers began to take domestic banks’ threats to disinvest from government bonds and reduce their lending seriously. 33

Following a left-leaning campaign, Rousseff won the October 2014 elections by a narrow margin. The option favoured by labour and the PT left was to combat recession via a public banking stimulus as had been done in 2008. Public bank expansion could be funded either through a default on domestic debt to reduce the debt service costs or through higher taxes. 34 Once in power the second Rousseff administration ruled out default because it would result in banking crisis due to banks’ large holdings of government bonds, require further bailouts and ultimately increase public debt further. Increasing public investment through higher taxes would not only destroy support from PT’s industrial sector allies, but was also seen to be far from sufficient to cover expenditure. The option to implement fiscal austerity and scale back developmentalist policies was instead chosen for having the greatest chance of holding the PT’s support coalition together by appeasing industry (Saad-Filho and Morais, 2018).

As part of fiscal consolidation measures, known fiscal hawk Joachim Levy was appointed Minister of Finance, and the National Treasury’s loan policy to the BNDES was ended, removing an important funding source. As a result, BNDES disbursements fell by 28 percent in 2015 (National Bank for Economic and Social Development (BNDES), 2015), marking the beginning of a period of gradual scaling back of the role of public banking in the Brazilian economy.

In the context of already low global liquidity and weakened financial resilience, the economically liberal Temer administration was successful in further dismantling the BNDES and other public banks, reducing both their size and their strategic policy roles, citing concerns that public bank expansion would crowd out private investment and lead to further downgrades (Dwyer, 2018). The Lava Jato corruption scandals, which involved some of BNDES’s key clients, eroded public support for development banking, further increasing the costs for policymakers who wished to maintain state control of finance. 35

South Africa

Period 1: high global liquidity (2003–2007)

In period 1, although my theory predicts weak financial resilience and high global liquidity should result in a limited expansion of public banking, we observe expansion being blocked altogether. This deviation from theoretical expectations is because the liberal Mbeki faction of the African National Congress (ANC) government, which was not responsive to interventionist labour and industry preferences, was in power during this period.

South African labour movement, represented by umbrella union Congress of South African Trade Unions (COSATU), the left faction of the ruling ANC party and the South Africa Communist Party (SACP), became increasingly mobilized in favour of interventionist reform in the early 2000s (Habib, 2013: 28). At the 2002 Alliance Summit, COSATU advocated a more assertive strategy to direct investment from public sources, including through the expansion of publicly owned development and post office banks, and tools such as differentiated interest rates, prescribed asset requirements and capital controls, to ‘discipline and regulate [private] capital’ to direct investment to labour-intensive manufacturing sectors (COSATU, 2002: 25). From 2005, the pro-intervention demands escalated and gained traction within the ANC party. A turning point in favour of the left faction was the ANC’s December 2007 Polokwane party conference where Zuma was elected ANC party leader. The conference resolution affirmed ANC’s commitment to statist economic planning in which public banks were to play a key role (African National Congress (ANC), 2007).

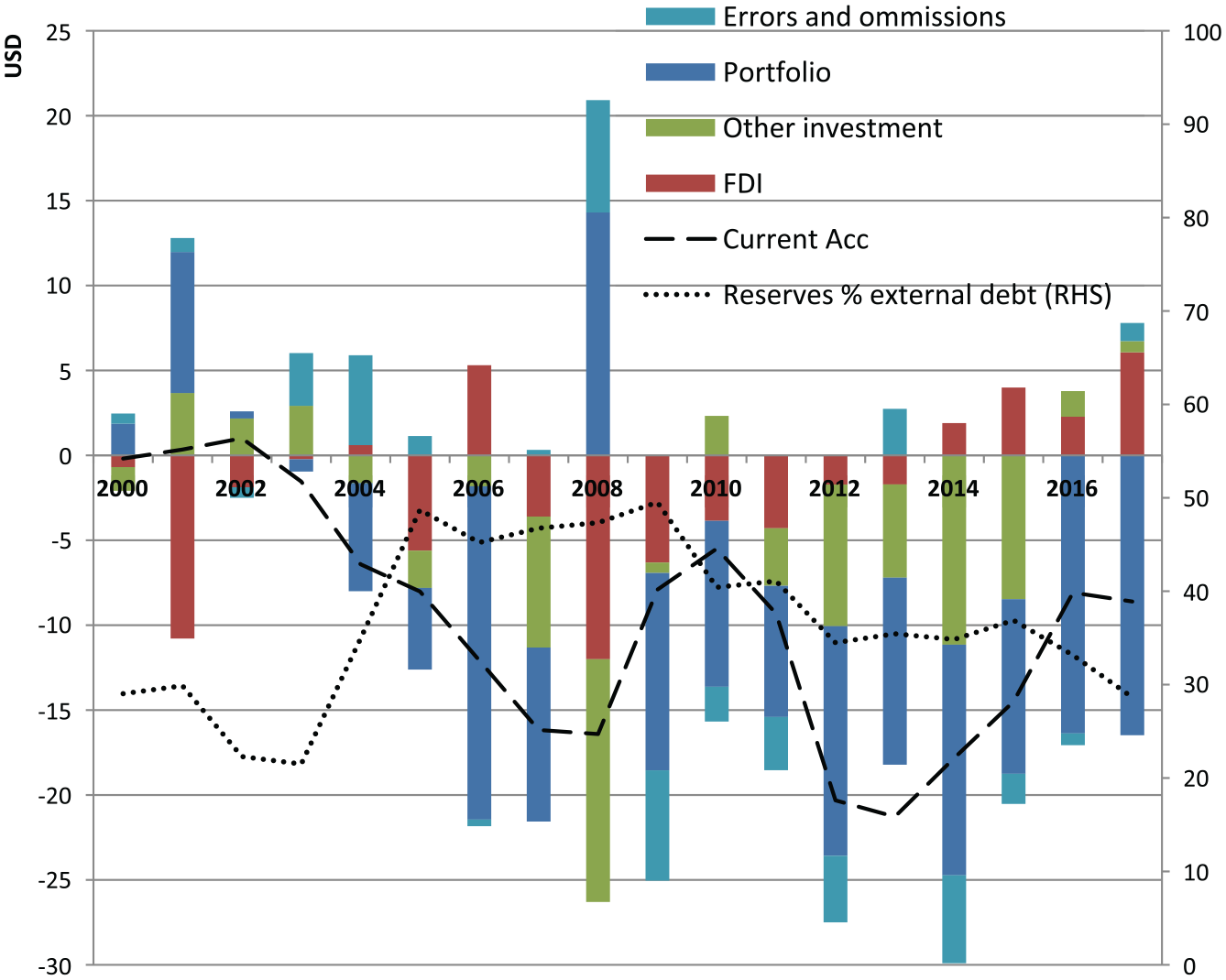

Financial resilience during this period was weak: reserves remained low, short-term external debt remained high and the current account deficit continued widening and was predominantly financed by portfolio inflows (Figure 5). Foreign ownership in the stock and bond markets continued increasing, and banks relied on short-term wholesale funding sources (SARB online database). Nonetheless, using Brazil in period 1 as a counterfactual, high global liquidity should have allowed for at least a limited expansion in public banking.

During this period, the right faction of the ANC party led by President Mbeki dominated government. The ANC right faction represented the financial sector, large conglomerates mainly in the mining and metals sectors and smaller black-owned business, and wanted to continue liberalizing, deregulating and privatizing the financial sector (Habib, 2013).

Although interventionist demands from the labour movement were escalating, the Mbeki administration was not responsive to their preferences. Even though the Mbeki administration increasingly used interventionist rhetoric in response to demands for public banking, this did not translate to the policy level and public banks were denied additional budgetary resources. Nor did policymakers take advantage of the 2003–2007 financial boom to strengthen national financial resilience as Brazil had done under the first Lula administration. Liberal appointments were made to key positions, including former pro-liberalization Trade Minister Trevor Manuel as Minister of Finance and Tito Mboweni from the right wing of the ANC as central bank Governor.

Period 2: the post-crisis reform window (2008–2009)

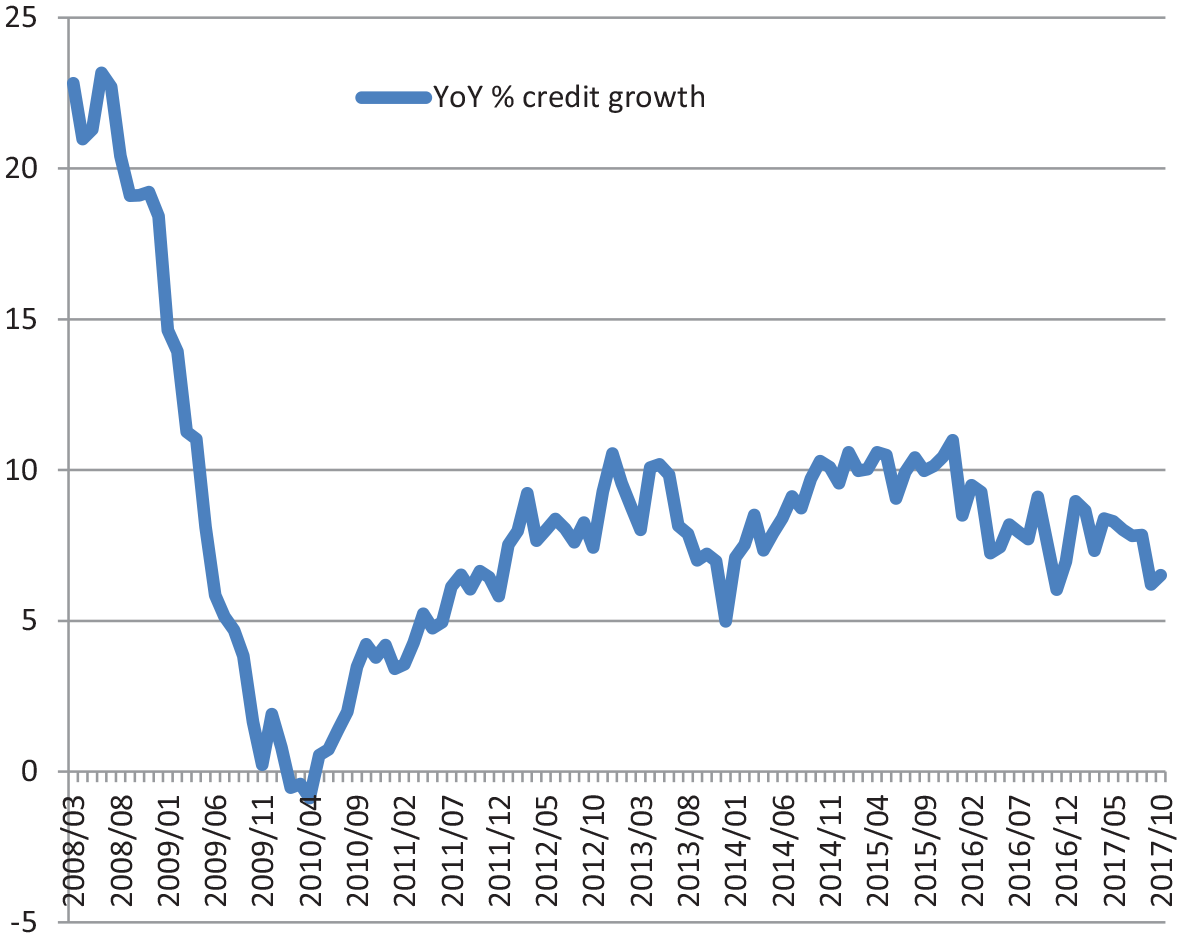

In period 2, despite a left government representing labour coming to power, weak financial resilience and low global liquidity led to demands for expansion of public banking being blocked.

Like in Brazil, the 2008 crisis resulted in risk aversion and retrenchment in South African domestic private banks, creating a reform window of approximately the same length (Figure 4). The ANC’s support base demanded a strong countercyclical public banking response to the crisis. The labour movement saw the financial crisis as an opportunity to break with the policy path chosen by ANC in 1996, and instal an interventionist developmental state (COSATU, 2012: 44). Labour was of the view that public banking to promote domestic manufacturing was necessary to combat the unemployment crisis and improve the quality of jobs. The drive to recapitalize public banks was spearheaded by industrial labour unions National Union of Metalworkers of South Africa (NUMSA) (metal workers) and South African Clothing and Textile Workers Union (SACTWU) (textiles), and supported by COSATU, SACP and the ANC left. According to NUMSA: In the early 2000s there were debates about [public bank] recapitalisation but we were on the defensive fighting against retrenchments . . . after Polokwane and the 2008 crisis, we went on the offensive. We need recapitalisation and we need the BNDES model.

36

South African private bank lending.

South Africa current account position and financing.

Labour unions were joined in their calls for financial reform by sections of the private manufacturing sector that had been hit hard by limited availability of finance and import competition led by the Manufacturing Circle, which was set up by the Department of Trade and Industry (DTI) in 2008 to give a unified voice to industry needs. 37

Following Mbeki’s forced resignation in September 2008, Zuma won the national elections and became president in May 2009. This was widely seen as a victory for the left factions of the Tripartite Alliance and brought expectations for a more interventionist approach to economic management in general, and finance in particular (Habib, 2013).

Despite strong demands from its support base, once in power the Zuma administration did not take advantage of the reform window created by the weakening of domestic banks and continued to pursue liberal financial policies. Weak financial resilience at a time of low global liquidity made the leadership fearful that dramatic leftward policy shifts could result in real economic damage. According to a senior ANC advisor: It [lack of radical policy shifts] is because they were thinking about pleasing markets, both foreign and domestic because they are highly integrated, but in South Africa when you’re talking about pleasing the markets, you are essentially talking about the CEOs of big banks.

38

In comparison to Brazil, a wider current account deficit in 2008 made South Africa more dependent on attracting external finance to avoid balance of payments crisis. While Brazil’s external deficit was financed primarily by FDI, South Africa was far more reliant on volatile portfolio inflows due to persistently low levels of FDI (Figures 3 and 5). Reserves remained at just under 3 months of import cover, in comparison to Brazil’s 8.5, and well below the IMF’s recommendation of 12 months, as well as insufficient to mitigate damage caused by portfolio outflows, at only about 50 percent of the stock of portfolio debt liabilities compared to Brazil’s 85 (IMF BOP Statistics). Unlike Brazil, South Africa did not receive a bilateral swap line from the US Fed. 39 Combined with low reserves, this meant the South African government did not have control over an important source of dollars it could use to defend its currency or cover import needs at this crucial moment.

Capital flight was also perceived as more likely to cause instabilities in the South African domestic financial system due to greater foreign investor presence in the domestic government bond market where central government, SOEs and public banks funded themselves, 24 percent compared to 12 percent in Brazil (Arslanalp and Tsuda, 2014). Domestic financial actors and ratings agencies argued that if foreigners exited this market, the SOEs and public banks would lose funding. The government would have to bail them out while itself facing increased borrowing costs in domestic markets, while being shut out of international markets. Policymakers feared this would have knock on effects for the stability of the domestic financial system. Because of their exposure to government and SOE debt, bank’s asset quality would fall, and institutional investors could stop funding the banks, potentially necessitating further government bailouts. 40 As stock markets also had a high percentage of foreign ownership, in the event of capital flight, equities prices would fall, having knock on effects on the balance sheets of stock holders, including banks and institutional investors. 41 South African domestic banks were, in contrast to Brazilian private banks, also more dependent on short-term market-based funding which would dry up in the event of a financial panic or ratings downgrade. 42

The first Zuma administration instead opted to pursue a cautious path of pro-market continuity, and made liberal appointments to key economic ministries. While Trevor Manuel was removed from the key post of Finance Minister under pressure from COSATU and SACP, who saw him as the main architect of neoliberal reform, he was kept on as head of the newly created and powerful Planning Commission. Pravin Gordhan, an equally staunch proponent of liberalization policies, was appointed finance minister to signal pro-market policy continuity (Bell, 2009). Liberal appointments were also made to the independent central bank and the IDC and DBSA themselves.

To appease COSATU and SACP, which had been instrumental to Zuma’s electoral victory, the leadership made developmentalist appointments to secondary economic ministries. Rob Davies from the SACP, a prominent proponent of activist industrial policies, was appointed to the DTI. A new Economic Development Department (EDD) was established with the idea of creating a pilot agency to lead the developmental state and control the public banks, headed by Ibrahim Patel of COSATU.

Despite a sharp increase in demand for public credit due to the inability of private banks to serve their clients, the MoF under Gordhan denied IDC additional resources. The result was an almost insignificant countercyclical response, with public banks re-prioritizing within their portfolios to cross-subsidize a few developmental projects within the limits set by their market-based funding model through IDC (2009).

Period 3: high global liquidity (2009–May 2013)

In period 3, weak financial resilience and high global liquidity led to a limited expansion in public development banking. As South Africa went into recession and unemployment crisis mounted, demands for the government to use public banks to boost labour-intensive manufacturing gained further momentum. In May 2010, labour and manufacturing industry entered an official alliance in a joint ‘Declaration on Industrial and Economic Policy interventions needed to create decent jobs’. 43 The declaration was described as a ‘historic intervention by employers and workers to act jointly against deindustrialisation of our economy, and create decent jobs on a large scale’, and re-iterated the call for concessional finance for productive investment, and demanded that public banks should be required to actively promote the DTI’s industrial policy agenda (Manufacturing Circle, 2010).

By the time these demands gained traction in policymaking circles in 2010 private banks were already well on their way to recovery (Figure 4), and opposed public bank expansion, rather than initially accepting them like the Brazilian private banks. The South African banking and institutional investors associations Banking Association South Africa (BASA) and Association for Savings and Investment argued that not only were the IDC and DBSA already unfairly competing with private banks, but also that they presented an unsustainable fiscal burden that would impact negatively on external balances. 44

A battle over economic policy ensued within the state. Labour unions and the manufacturing sector’s demands were represented by the DTI and EDD, while the financial sectors’ position was represented at the MoF, Planning Commission and central bank. The financial sector had close professional connections with these governmental bodies through their financial sector associations, as well as personal connections through high-level individual meetings and revolving doors, facilitated by liberal ministerial appointments. 45

Pressures to scale up public banking continued gaining momentum within the ANC party, and among policymakers at the DTI and EDD between 2010 and 2013. At the NUMSA initiative, and supported by COSATU and manufacturing business associations, the ANC launched a task team on SOEs and public banks. 46 The team produced a report, approved at the ANC’s July 2012 policy conference, which advocated a more strategic industrial policy role for public banks, and noted that to allow them to play this role, access to subsidized government funding was necessary. The report recommended a separate budgetary line from the Treasury and privileged access to tax-based funding, along the lines of the BNDES model (ANC, 2012). Within government, the DTI’s Industrial Policy Action Plans of 2011 and 2012 and the EDD’s development plan and the New Growth Path of 2010 outlined a key industrial policy role for IDC and DBSA and echoed ANC recommendations on increasing their funding.

Despite intense preferences for financial interventionism from the ruling coalitions’ support base, and support at allied ministries, without support at the MoF, which remained allied to the financial sector, these demands were repeatedly blocked. According to an ANC advisor: the problem is that . . . we [ANC party] don’t have power, its Treasury [MoF] who controls the funding model. We can’t tell them the final detail on how to manage their relationship with public banks. Treasury largely determines economic policy because they determine what has been allocated to you . . . The left was appointed within the DTI and they do industrial policy, but somebody has to fund it.

47

During negotiations with labour and industry representatives at the National Economic Development and Labour Council, MoF officials used the precarious state of the current account as a pretext for blocking funding for public banks they [Treasury] said they . . . are sympathetic to our demands, which they were not, but cannot go to parliament and ask for the direct appropriation to IDC. They said this will further weaken the already weak current account position and will invite the wrath of the international markets and will further lead to our downgrade to junk status.

48

Using the lack of adverse international market reactions to the Brazilian expansion of BNDES during the financial boom as a counterfactual, it is likely that if the Zuma administration had made developmentalist appointments at the MoF and scaled up public banking during the high liquidity period, its capital flight fears would not have materialized. Yet abundant replacement resources were seen as inadequate to compensate for weak national financial resilience, especially as South Africa’s current account deficit had widened, and dependence on foreign portfolio flows further increased between 2010 and 2013 (Figure 5). Policymakers remained sensitive to disinvestment and exit threats; Pravin Gordhan was kept on as Minister of Finance, and expansion of state control in finance was extremely limited. Apart from a very small amount of additional funding agreed in mid-2011, the IDC did not receive fiscal resources (Zalk, 2014), while DBSA was provided with only modest support (DBSA, 2012). Without a significant subsidized non-market source of funding, South African public banks were unable to play a developmental role despite the DTI and EDD’s detailed plans. 49

Period 4: end of the financial boom (May 2013–2017)

In period 4, weak financial resilience and low global liquidity led to blocking of demands for further public bank expansion. Weak financial resilience to capital flight, which had worsened over the course of the boom period, triggered a panic in the domestic financial sector after the global liquidity environment turned unfavourable following the taper tantrum of May 2013. Disinvestment threats became even more decisive after June 2014 when S&P downgraded South Africa’s foreign currency long-term sovereign credit rating from BBB to BBB−, just one notch above sub-investment grade status, with Fitch following suit in December 2015 (Hanusch et al., 2015: 1). The Ratings agencies as well as private banks and institutional investors were particularly worried about the high percentage of foreign investors in government bond markets, which had further increased to 36 percent by Q1 of 2014 (Arslanalp and Tsuda, 2014). Contingent liabilities of SOEs and public banks were considered to be ‘the big South African subprime systemic risk’ and if foreign investors exited government bond markets then they would lose their funding, triggering a government debt and domestic banking crisis. 50

Rating agencies explicitly warned the MoF against increasing budgetary resources for public banks to avoid further downgrades: To come up with adventurous ideas around what DFIs [public banks] can do in the current situation, we say there just not the fiscal flexibility for them at the moment. It would be alarming for us from a ratings perspective if we saw a policy to shift DFIs as quasi budgets to fulfil policy purposes, or to take on new risks, like what happened in Brazil. That’s a red flag anywhere.

51

Any shift to more developmentally oriented activity would also result in downgrades of the public banks themselves ‘if their mandate changed we would ask, what will that do to your balance sheet? . . . if too politically driven, they might take on unsustainable risk’. 52

The very real threat of further ratings downgrades combined with weak financial resilience vastly improved the bargaining position of the MoF, private banks and institutional investors already opposed to putting more resources into the IDC. In this environment, despite strong criticism of the ratings agencies for being anti-developmental, the ANC, labour unions, manufacturing sector and the DTI began to accept that public bank expansion could be dangerous: ‘Everyone was made to fear the rating agencies. There a belief even on the left that those are people you don’t want to mess with’. 53 The MoF was able to use the threat of downgrades to block the ANC party, DTI and EDD’s proposals to scale up public banks using budgetary resources, and remove public banking reform as a serious item on the reform agenda. 54 Low global liquidity and weak financial resilience made the leadership sensitive to disinvestment threats and the MoF assured domestic and foreign investors that the Treasury would stay the course of fiscal consolidation (Basson and du Toit, 2018).

Corruption scandals that became more prevalent after 2017 further discredited the statist left among the public. Although no evidence was found directly implicating public banks, they became tainted by scandals at the SOEs. As the full extent of graft was revealed, this was the final nail in the coffin for financial interventionism, and scaling up public banks was no longer considered a serious policy option.

Conclusion

This paper argues that differences in financial interventionism in Brazil and South Africa can be explained by variation in global liquidity and national financial resilience, which influenced policymakers’ sensitivity to disinvestment threats, and should have broader implications for other financially integrated emerging countries. Future research could systematically investigate whether state control in finance varies with these two factors for a broader range of countries, and consider how the credibility of financial disinvestment or exist threats varies according to a countries’ position in the global economic hierarchy. The following paragraphs provide a brief sketch.

In lower income countries that cannot easily borrow on private markets, the availability of low-conditionality sources of official and bilateral external finance, such as Chinese loans, and commodity revenues should be more important for increasing access to replacement resources and reducing IMF liberalization conditionalities than global financial market liquidity (Bunte, 2019; Jepson, 2020). On the other hand, the prevalence of dollarization in these economies may weaken financial resilience to capital flight, and decrease the likelihood of interventionism (Naqvi, 2021).

For core economies at the top of the currency hierarchy, it should be possible to borrow on international markets at low cost, even during crisis periods (Cohen, 2018; Winecoff, 2020). As such, global financial cycles should have less of an impact on policymakers’ sensitivity to disinvestment threats. This exorbitant privilege means that should they wish to, policymakers in core countries have greater scope to borrow internationally to shore up public banking and counter private disinvestment threats.

A broader implication is that policymakers from countries lower in the global economic hierarchy are more externally constrained than those at the top. The availability of external financing and global liquidity is determined exogenously, outside of their control. Yet these policymakers are not merely passive victims tossed about by the gale forces of global liquidity cycles and domestic disinvestment, but can proactively shore up the position from which they confront these structural forces through building up national financial resilience.

Supplemental Material

sj-xlsx-1-ejt-10.1177_13540661221114370 – Supplemental material for Economic crisis, global financial cycles and state control of finance: public development banking in Brazil and South Africa

Supplemental material, sj-xlsx-1-ejt-10.1177_13540661221114370 for Economic crisis, global financial cycles and state control of finance: public development banking in Brazil and South Africa by Natalya Naqvi in European Journal of International Relations

Footnotes

Appendix

| Number | Date | Interviewee | Place |

|---|---|---|---|

| 1 | 27 March 2017 | Former BNDES leadership | Sao Paolo, Brazil |

| 2 | 27 March 2017 | Brazilian Association of the Machinery and Equipment Industry (ABIMAQ), Capital goods and machinery firm | Sao Paolo, Brazil |

| 3 | 27 March 2017 | Capital goods and machinery firm | Sao Paolo, Brazil |

| 4 | 28 March 2017 | Investe Sao Paolo | Sao Paolo, Brazil |

| 5 | 28 March 2017 | Investe Sao Paolo | Sao Paolo, Brazil |

| 6 | 29 March 2017 | Brazilian Association of the Machinery and Equipment Industry (ABIMAQ) | Sao Paolo, Brazil |

| 7 | 30 March 2017 | Ministry of Science and Technology (MDIC) | Brasilia, Brazil |

| 8 | 30 March 2017 | Ministry of Industry, Foreign Trade and Services (MCTIC) | Brasilia, Brazil |

| 9 | 30 March 2017 | APEX Brazil Trade Promotion Agency | Brasilia, Brazil |

| 10 | 03 April 2017 | Brazilian Industrial Development Agency (ABDI) | Brasilia, Brazil |

| 11 | 03 April 2017 | UK FCO in Brazil | Brasilia, Brazil |

| 12 | 04 April 2017 | Brazilian National Confederation of Industry (CNI) | Brasilia, Brazil |

| 13 | 05 April 2017 | Brazilian National Confederation of Industry (CNI), Entrepreneurial Mobilization for Innovation (MEI) | Brasilia, Brazil |

| 14 | 06 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 15 | 07 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 16 | 07 April 2017 | Brazilian Financial and Capital Markets Association (ANBIMA) | Rio de Janeiro, Brazil |

| 17 | 07 April 2017 | Brazilian Financial and Capital Markets Association (ANBIMA) | Rio de Janeiro, Brazil |

| 18 | 10 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 19 | 10 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 20 | 10 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 21 | 10 April 2017 | Former Brazilian Financial and Capital Markets Association (ANBIMA) | Rio de Janeiro, Brazil |

| 22 | 10 April 2017 | Former BNDES official | Rio de Janeiro, Brazil |

| 23 | 11 April 2017 | Former BNDES leadership | Rio de Janeiro, Brazil |

| 24 | 11 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 25 | 11 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 26 | 11 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 27 | 11 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 28 | 11 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 29 | 12 April 2017 | Casa das Garcas think tank | Rio de Janeiro, Brazil |

| 30 | 12 April 2017 | BNDES advisor | Rio de Janeiro, Brazil |

| 31 | 12 April 2017 | BNDES official | Rio de Janeiro, Brazil |

| 32 | 18 April 2017 | Brazilian Federation of Banks (FEBRABAN) | Sao Paolo, Brazil |

| 33 | 18 April 2017 | Federation of Industries of the State of Sao Paulo (FIESP) | Sao Paolo, Brazil |

| 34 | 18 April 2017 | Federation of Industries of the State of Sao Paulo (FIESP) | Sao Paolo, Brazil |

| 35 | 18 April 2017 | Federation of Industries of the State of Sao Paulo (FIESP) | Sao Paolo, Brazil |

| 36 | 18 April 2017 | Federation of Industries of the State of Sao Paulo (FIESP) | Sao Paolo, Brazil |

| 37 | 18 April 2017 | Former Brazilian Innovation Agency (FINEP) | Sao Paolo, Brazil |

| 38 | 19 April 2017 | Sao Paolo Research Foundation (FAPESP) | Sao Paolo, Brazil |

| 39 | 19 April 2017 | Brazilian Association of the Infrastructure and Capital Goods Industries (ABDIB) | Sao Paolo, Brazil |

| 40 | 19 April 2017 | Brazilian Electrical and Electronics Industry Association (ABINEE) | Sao Paolo, Brazil |

| 41 | 19 April 2017 | Domestic private bank | Sao Paolo, Brazil |

| 42 | 19 April 2017 | Domestic private bank | Sao Paolo, Brazil |

| 43 | 19 April 2017 | Domestic private bank | Sao Paolo, Brazil |

| 44 | 20 April 2017 | Brazilian Textile and Apparel Industry Association (ABIT) | Sao Paolo, Brazil |

| 45 | 20 April 2017 | Brazilian Textile and Apparel Industry Association (ABIT) | Sao Paolo, Brazil |

| 46 | 20 April 2017 | Foreign private bank | Sao Paolo, Brazil |

| 47 | 20 April 2017 | Inter-Union Department of Statistics and Socio-Economic Studies (DIEESE) | Sao Paolo, Brazil |

| 48 | 27 May 2018 | Former Competition Commission | Johannesburg, South Africa |

| 49 | 27 May 2018 | Former Department of Trade and Industry and Presidency | Johannesburg, South Africa |

| 50 | 27 May 2018 | Former Industrial Development Corporation | Johannesburg, South Africa |

| 51 | 27 May 2018 | Centre for Competition, Regulation and Economic Development (CCRED) | Johannesburg, South Africa |

| 52 | 27 May 2018 | CCRED | Johannesburg, South Africa |

| 53 | 27 May 2018 | CCRED | Johannesburg, South Africa |

| 54 | 27 May 2018 | CCRED | Johannesburg, South Africa |

| 55 | 28 May 2018 | Private bank | Johannesburg, South Africa |

| 56 | 28 May 2018 | Private bank | Johannesburg, South Africa |

| 57 | 28 May 2018 | Private bank | Johannesburg, South Africa |

| 58 | 28 May 2018 | Private bank | Johannesburg, South Africa |

| 59 | 29 May 2018 | National Treasury, Ministry of Finance | Johannesburg, South Africa |

| 60 | 29 May 2018 | South African Chamber of Commerce and Industry, former Landbank | Johannesburg, South Africa |

| 61 | 29 May 2018 | Centre for Development and Enterprise think tank | Johannesburg, South Africa |

| 62 | 29 May 2018 | Banking Association South Africa, former Ministry of Finance | Johannesburg, South Africa |

| 63 | 29 May 2018 | Banking Association South Africa | Johannesburg, South Africa |

| 64 | 30 May 2018 | Department of Trade and Industry (DTI) | Pretoria, South Africa |

| 65 | 30 May 2018 | Department of Trade and Industry (DTI) | Pretoria, South Africa |

| 66 | 30 May 2018 | Department of Trade and Industry (DTI) | Pretoria, South Africa |

| 67 | 30 May 2018 | Department of Trade and Industry (DTI) | Pretoria, South Africa |

| 68 | 30 May 2018 | South Africa Reserve Bank (SARB) | Pretoria, South Africa |

| 69 | 30 May 2018 | South Africa Reserve Bank (SARB) | Pretoria, South Africa |

| 70 | 30 May 2018 | South Africa Reserve Bank (SARB) | Pretoria, South Africa |

| 71 | 30 May 2018 | South Africa Reserve Bank (SARB) | Pretoria, South Africa |

| 72 | 30 May 2018 | South Africa Reserve Bank (SARB) | Pretoria, South Africa |

| 73 | 30 May 2018 | South Africa Reserve Bank (SARB) | Pretoria, South Africa |

| 74 | 30 May 2018 | South Africa Reserve Bank (SARB) | Pretoria, South Africa |

| 75 | 31 May 2018 | Business Leadership South Africa | Johannesburg, South Africa |

| 76 | 31 May 2018 | Business Unity South Africa | Johannesburg, South Africa |

| 77 | 31 May 2018 | Business Unity South Africa | Johannesburg, South Africa |

| 78 | 31 May 2018 | Manufacturing Circle | Johannesburg, South Africa |

| 79 | 31 May 2018 | Industrial Development Corporation | Johannesburg, South Africa |

| 80 | 01 June 2018 | Former Department of Trade and Industry (DTI) | Cape Town, South Africa |

| 81 | 01 June 2018 | Parliamentary Budget Office | Cape Town, South Africa |

| 82 | 01 June 2018 | Association for Savings and Investment (ASISA), NEDLAC task team on SOEs and DFIs | Cape Town, South Africa |

| 83 | 01 June 2018 | Association for Savings and Investment | Cape Town, South Africa |

| 84 | 04 June 2018 | Parliamentary Budget Office | Cape Town, South Africa |

| 85 | 04 June 2018 | Former Department of Trade and Industry | Cape Town, South Africa |

| 86 | 04 June 2018 | Former COSATU | Cape Town, South Africa |

| 87 | 04 June 2018 | COSATU | Cape Town, South Africa |

| 88 | 05 June 2018 | ANC National Executive Committee | Johannesburg, South Africa |

| 89 | 05 June 2018 | ANC Economic Transformation Committee | Johannesburg, South Africa |

| 90 | 07 June 2018 | Former Economic Development Department (EDD) | Johannesburg, South Africa |

| 91 | 07 June 2018 | Public Investment Corporation | Johannesburg, South Africa |

| 92 | 07 June 2018 | Department of Trade and Industry (DTI) | Johannesburg, South Africa |

| 93 | 07 June 2018 | Researcher | Johannesburg, South Africa |

| 94 | 08 June 2018 | South Africa Reserve Bank (SARB) | Johannesburg, South Africa |

| 95 | 08 June 2018 | Department of Trade and Industry (DTI) | Johannesburg, South Africa |

| 96 | 08 June 2018 | South African Insurance Association | Johannesburg, South Africa |

| 97 | 08 June 2018 | Development Bank of South Africa | Johannesburg, South Africa |

| 98 | 08 June 2018 | Development Bank of South Africa | Johannesburg, South Africa |

| 99 | 08 June 2018 | Development Bank of South Africa | Johannesburg, South Africa |

| 100 | 11 June 2018 | Land Bank | Johannesburg, South Africa |

| 101 | 11 June 2018 | South Africa Capital Equipment Export Council | Johannesburg, South Africa |

| 102 | 12 June 2018 | National Association of Automotive Component and Allied Manufacturers (NACAAM) | Johannesburg, South Africa |

| 103 | 12 June 2018 | Private bank, former National Treasury | Johannesburg, South Africa |

| 104 | 13 June 2018 | International ratings agency | Johannesburg, South Africa |

| 105 | 13 June 2018 | SBP (SME research agency) | Johannesburg, South Africa |

| 106 | 13 June 2018 | Domestic private bank | Johannesburg, South Africa |