Abstract

Financial sanctions have become a major component of American foreign policy. Since 2015, the number of blacklisted actors has nearly tripled, coinciding with US financial campaigns against Iran, North Korea, and Russia. This paper centers an under-examined paradox of this proliferation: the complexity of lifting financial sanctions. Indeed, successful sanctions regimes necessitate both sticks (punitive sanctions) and carrots (economic incentives). Yet financial sanctions often limit the economic benefits promised to target states, as banks and other financial institutions risk hefty material and reputational costs if they are to cooperate with previously sanctioned actors. Thus, while financial sanctions are effective at producing negative market reactions against a target, they can be hugely damaging if market actors do not cooperate with the lifting of sanctions. To capture this dynamic, this paper leverages process-tracing to observe financial market reactions to sanctions relief in three key cases—Iran (2010–2015), North Korea (2002–2007), and Libya (1996–2008). It finds that in each case, the presence or absence of US Treasury blacklisting corresponds to the post-sanction willingness of financial actors to extend sanctions relief to targeted states. In doing so, this study identifies “reputational risk” as the primary causal mechanism limiting a target’s reintegration into the global economy.

Keywords

Introduction

Why do global financial actors sometimes choose to reintegrate previously sanctioned states to the global economy, though at other times choose not to? Sanctioned states may reasonably anticipate that when sanctions are removed, they should receive some form of relief, meaning that global financial actors—from banks to multinational corporations—should return to status quo capital flows and foreign direct investment. However, there are marked inconsistencies in the ways that previously sanctioned states experience such relief. In many cases, global financial actors have been so reticent to reinvest in previously sanctioned economies that the sanctioning states (or senders) have had to engage in lobbying efforts designed to assuage financial actors, and generate investment (Lakshmanan, 2016; Schwartz and Patrick, 2016).

Within the wider context of sanctions literature, little is yet known about the conditions in which target states succeed or fail in their economic recoveries, or the factors affecting their ability to attract global investment after sanctions have been removed. Rather, sanctions literature has, historically, focused on key issues related to sanctions effectiveness, the threat of sanctions, whether such measures are applied multilaterally or unilaterally, and compliance and enforcement problems, among others. Despite these important scholarly contributions, few empirical studies have explored the dynamics of the post-sanction environment. This is a significant gap in sanctions literature, which this study seeks to address.

In this study, I argue that the extent to which financial actors reintegrate previously sanctioned states depends on the type of sanctions program initially deployed by the sender, that is, primary or secondary sanctions, a distinction that requires brief explication. First and foremost, sanctions are intended to alter a target state’s malign behavior. In doing so, however, sender states must use sanctions to interrupt the business practices of multinational corporations. These corporations typically have business interests in the target state, and act as the intermediaries between target states and the global economy. Primary and secondary sanctions, however, target multinational corporations in different ways.

Primary sanctions are economic restrictions that require compliance from multinational corporations and individuals domiciled in the sender state. In the United States, for example, the Office of Foreign Assets Control (OFAC) may issue a variety of sanctions—such as asset freezes and economic embargoes—directly against firms and institutions in the target state. US persons and multinational corporations must then screen their customers against the OFAC list of sanctioned actors to ensure that they are not doing business with a sanctioned entity. Primary measures, however, do not impact non-US firms (i.e. third parties), who would thus retain access to sanctioned economies without recourse from the US government.

Secondary sanctions, on the other hand, are intended to affect third-party multinational corporations and individuals—that is, actors not domiciled in the sender state. Secondary measures do so by threatening to impose penalties on third parties for conducting business with their counterparts in the target state, such as firms domiciled in the target state or government institutions representing a target government (e.g. the Iranian Central Bank). Such penalties might include preventing offending third parties from accessing US financial markets, and being listed on the Specially Designated Nationals and Blocked Persons (SDN) list. Inclusion on OFAC’s SDN list is referred to as “blacklisting,” which often results in heavy reputational damage for affected firms (Eggenberger, 2018).

In instances of secondary sanctions, I expect third-party financial actors to assign reputational risks to a target state’s firms and financial institutions. Due to the higher reputational risks associated with their domestic firms and financial institutions, target states will thus struggle to reintegrate into the global economy. By contrast, I expect that states targeted by primary sanctions—in which third parties are not threatened with blacklisting—will experience more rapid reintegration into the global economy. To test the plausibility of the reputational risk hypothesis, this study utilizes process-tracing to analyze three key episodes involving the United States and their imposition and removal of financial sanctions: Iran (2010–2017), North Korea (2002–2007), and Libya (1996–2008). Here, I observe two positive cases (Iran and North Korea), each emphasizing reputational risk and its hypothesized negative effects on sanctions relief. In the third, Libya, I examine a negative case in which negative reputational effects, and their impact on sanctions relief, are expected but do not materialize.

This research makes several key contributions. First, it lays the groundwork for wider discussion about the implications of contemporary sanctions policies and their externalities. By understanding the conditions in which successful sanctions programs lead to failed sanctions relief, scholars might gain insight into the paradox at the heart of US financial sanctions. Indeed, while such tools are highly effective at producing negative market reactions against a target, they are simultaneously tools whose effects, once unleashed, are challenging to undo, directly limiting the effectiveness of sanctions relief itself. Furthermore, by offering one of the first systematic examinations of sanctions relief, this study appropriately centers post-sanction dynamics that remain under-examined in sanctions literature. In doing so, it aims to broaden how scholars think about the processes and causal mechanisms that lie at the heart of contemporary sanctions measures.

The article proceeds in the following manner. Section “The problem of sanctions relief” situates this study within the wider literature on economic sanctions, and makes a case for the importance of studying sanctions relief. Section “Theoretical argument” then provides my theoretical argument and hypothesis, delves into the dynamics of reputational risk more acutely, and discusses a potential counterfactual. Section “Methodology” lays out the study’s methodology, including case selection, process-tracing, and limitations. Sections “Failure of sanctions relief in the case of Iran,” “Failure of sanctions relief in the case of North Korea,” and “Successful sanctions relief in the case of Libya” provide empirical evidence, leveraging the three cases discussed above. Finally, Section “Conclusion” provides concluding remarks, and potential avenues for further study.

The problem of sanctions relief

Sanctions relief generally escapes significant scrutiny, particularly within the wider context of existing literature on sanctions. Historically, this literature has dealt overwhelmingly with questions of sanctions effectiveness (Allen, 2005; Drezner, 2000; Hufbauer et al., 1990; Lektzian and Souva, 2003; Pape, 1997). Here, sanctions literature has explored the links between sanctions success and factors like the cost of sanctions to the sender and/or target state, the regime type of targets, the matching of issue salience with the magnitude of sanctions measures, and whether or not sanctions measures are unilateral or multilateral. More recent scholarship in this realm, such as Kavakli et al. (2020), has delved deeply into these dynamics. Here the authors find that sanctions are more likely to succeed when senders hold a comparative advantage in goods exported to the target, though are more likely to fail in the event a target’s export portfolio is diverse or if the target has a comparative advantage in exports. Others, such as Jeong and Peksen (2019), have worked to disaggregate causal variables like “regime type,” assessing instead the institutional veto players that may influence leaders’ decisions to acquiesce to a sender’s demands, finding that such domestic institutions have enormous influence over such decisions. Dai et al (2021) also reveal that the duration of trade sanctions produces increasingly negative effects over time, raising the prospect of capitulation by the target.

However, much like the imposition of sanctions, sanctions relief requires significant coordination between public and private sector actors. Typically, the cumulative resources of private sector actors dwarf those of national governments, and thus, for sanctions relief to be effective and efficient, the interests of sender governments must align with those of private sector actors. Here, the role of private actors in the post-sanction environment is particularly important, as their ability and willingness to reintegrate target states into the global economy ultimately determine how much economic benefit a target state is likely to receive, how such benefits are distributed domestically, and how such outcomes shape the behavior of targeted states going forward.

The importance of this coordination is paramount, as significant problems can arise from the failure of sender states to coordinate relief for their targets. As Nephew explains, target states may reason that if they are willing to accommodate the conditions set by their persecutors, they will be able to resume business as usual. However, if target states perceive that there is nothing they can do to reattract global capital after sanctions are implemented, then their behavioral responses to sanctions become less predictable and less beneficial for the sender state. Sanctions are therefore a psychological tool as much as an economic one, and their power lies in the sender state’s ability to turn sanctions “on” and “off” as they see fit (Nephew, 2018: 1).

The implications of this research gap are striking, as without understanding the internal dynamics of sanctions relief, the implementation of defective policy measures may continue to the detriment of sender and target states alike.

Theoretical argument

Reputational risk

If sanctions relief requires coordination between state and private actors, the reputational risk associated with reintegrating target states is a significant barrier to coordination. Reputational risk is the “risk arising from negative perception on the part of customers, counterparties, shareholders, investors . . . or regulators that can adversely affect a bank’s ability to maintain existing, or establish new business relationships and continued access to sources of funding” (Bank for International Settlements, 2017: 4). Such reputational effects are often measured in terms of lost revenue, increased operating, capital or regulatory costs, or destruction of shareholder value (Feaver and Lorber, 2010).

Reputational risk is, indeed, a significant concern influencing financial actor decision-making. A reputational risk survey of firms, conducted by Deloitte in 2015, found that 87 percent of firm executives rated reputational risk as their “top strategic business risk,” finding that firms are particularly concerned with reputational damage in relation to key stakeholders, such as federal regulators, customers, and potential investors (Deloitte, 2015). In instances of reputational damage, firms were particularly concerned with significant losses of revenue, a reduced customer base, and increased regulatory scrutiny by federal regulators (Sheldon and Velan, 2020). Moreover, reputation assumes special importance in banking and financial sectors, because asymmetric information about other financial actors’ conduct can create systemic risk in which trusting relationships between financial actors begin to break down (Allen and Santomero, 1997, 2001).

At the firm level, firm reputation is often guarded by compliance officials, who are subject to a regulatory obligation to systematically comb through their client and transaction databases to detect potential partnerships or assets that violate sanctions. Any deal with sanctioned entities, or any payments facilitation with such entities, may be punished as a violation (De Leon Sotelo, 2018). Moreover, when establishing new correspondent banking relationships, banks are required to perform normal customer due diligence on respondent banks, and are required to gather sufficient information to understand the respondent bank’s business, reputation, and the quality of its supervision, including whether it has been subject to a money laundering or terrorist financing investigation or regulatory action (Financial Action Task Force (FATF), 2016).

Corporate compliance in these instances is vital from a reputational standpoint, as compliance or non-compliance at T0 sets an expectation of compliance or non-compliance at T1, T2, T3, . . . Tn, and so on. Corporate reputation is therefore based upon the historical precedence of an actor, and their behavioral tendencies over time. Brutger and Kertzer (2018: 696) suggest that an actor’s reputation is “informed by behavior in the past, and used to predict behavior in the future,” and thus, firms believe they must protect their reputations as lawful actors that eschew threats to their long-term financial wellbeing. Armed with this knowledge, actors can adapt their actions in advance in order to influence observers’ impressions (Ma and Parks, 2012), which may involve avoiding business relations with the reintegration of a previously sanctioned state.

Secondary sanctions introduce the threat of this long-term perception regarding a given firm or state’s suitability as a business partner; failure on the part of such firms to adhere to sanctions places their partners at risk of regulatory action, particularly blacklisting. As a result, if an actor finds themselves blacklisted for illicit behavior, the reputational costs of doing so would make it difficult for such actors to form business relationships once sanctions on them have been removed (Eggenberger, 2018).

While existing studies on reputational risk address the impact of sanctions implementation on individual firms’ share prices, there appear to be few studies addressing the persistence of these reputational effects following sanctions removal. Armour et al. (2017) show that the initial enforcement of financial sanctions by UK regulatory authorities has negative impacts on the market price of penalized firms, yet the authors simply address the initial announcement of misconduct and its effect on share price, rather than the corresponding changes in share price when punitive measures are lifted. Eggenberger (2018) shows that Organisation for Economic Co-operation and Development’s (OECD) blacklistings of Liechtenstein and Nauru triggered adverse market reactions that proved effective at altering these states’ behavior to become compliant with global money laundering regulations. Interestingly, Eggenberger briefly mentions the difficulty these states had in attracting foreign investment years after their initial infractions and changes in their behavior, yet does not engage with this long-term reputational effect.

Based on the preceding conditions, I posit the following hypothesis:

H1. Financial actors will be less likely to reintegrate former secondary sanctions targets into the global economy, though more likely to reintegrate targets of primary financial sanctions.

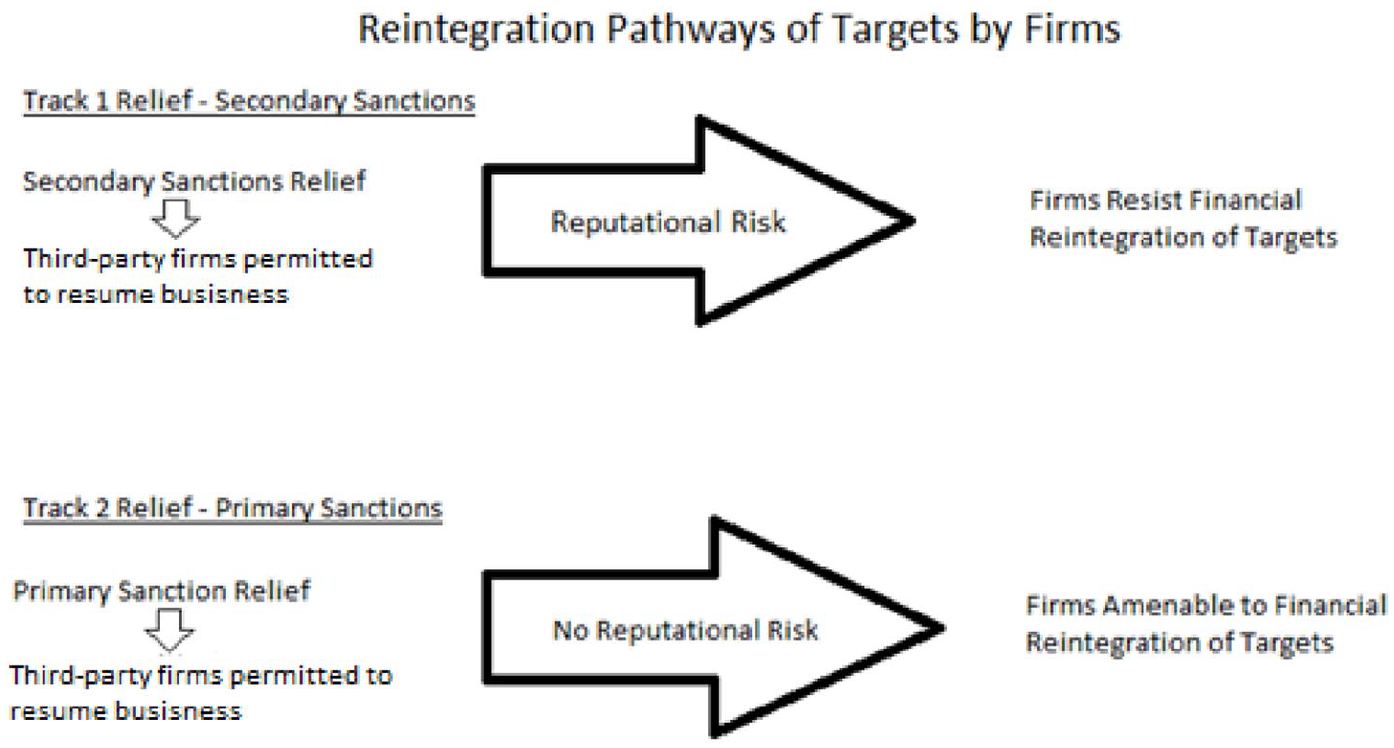

Figure 1 specifies the theoretical argument. As seen in Track 1, I expect that in cases of secondary sanctions, financial actors will deem firms and financial institutions in target states as sources of reputational risk. Third-party firms therefore choose not to financially reintegrate such actors. However, as seen in Track 2, cases where states have experienced primary sanctions should lead to the opposite phenomenon. Specifically, third-party financial actors should view firms and financial institutions in these states as low-risk and subsequently financially reintegrate them into the global economy.

Reintegration pathways of targets.

Counterfactual: Domestic market protectionism

If reputational risk is not responsible for the post-sanction reintegration dynamics we see in these cases, what may be causing them? First, one might consider the domestic interests and actors within the target state, and their willingness to open their domestic markets to global financial actors once sanctions are removed. Pond (2017) describes domestic pressures by firms within recently sanctioned states to raise tariff rates, seeking market protections by their governments from fresh influxes of international competition, thus allowing them to retain monopolistic positions within their home markets. Indeed, just as sender states must coordinate with market actors to ensure effective sanctions relief, there are likely mirrored processes within the target state, that is, coordinating state interests for sanctions relief with the interests of domestic economic actors, who may or may not ascribe to such outcomes. While this study does not address trade sanctions, one possible post-sanction market protection sought by domestic financial actors in financial sanction episodes is capital controls.

Indeed, there may be pressure from domestic financial actors for their governments to implement protective capital controls, particularly for disruptive short-term capital inflows. Morck et al. (2000) and Zingales and Rajan (2003) both argue that capital controls tend to favor entrenched firms and that such firms then lobby for the preservation of such policies, particularly when faced with economic re-openings, as suggested by Pond.

Such dynamics raise interesting implications surrounding the agency of target states, and whether or not they can affect meaningful change in the state’s post-sanction period. Existing scholarship, however, suggests that governments overseeing recovering economies have significant incentives not to impose capital controls, particularly when seeking to facilitate foreign direct investment (FDI) inflows, which are seen as long-term, stable forms of investment (Desai et al., 2006). Furthermore, Chwieroth (2010) shows that shifts toward liberalization of capital controls are made possible by severe economic crises, which force reconsideration among policymakers about the viability of the status quo. The uncertainty among domestic financial actors, generated by crises, in turn fosters a desire (and an opportunity) among government policymakers to experiment with policies that typically run counter to domestic actor preferences for protection (Chwieroth, 2010: 523). Consequently, were domestic lobbying for protections to take place, states still retain the policy tools, incentives, and agency to withstand calls for capital control protections when seeking sanctions removal.

Domestic protection-seeking behavior during economic re-opening is thus a compelling counterfactual explanation for the observed variation in post-sanction reintegration, although importantly this does not necessarily limit the independence of the state. This counterfactual is assessed within each case below.

Methodology

To illustrate the dynamics linking reputational risk and sanctions relief, this study employs a process-tracing approach to analyze three key episodes involving the United States and the imposition and relief of secondary financial sanctions: Iran (2010–2017), North Korea (2002–2007), and Libya (1996–2008). The data required for this analysis include flows of foreign direct investment, as well as news-media, business reporting, and primary source materials such as public statements and press releases by firms. These data were chosen as they reflect the reputational risk considerations of private sector actors involved in the implementation and relief of US financial sanctions, and how such considerations impact market behavior.

Case selection

In a study reliant upon a small sample of cases, it is important to acknowledge the possibility of selection bias, as small-N studies place very real restrictions on randomly selecting cases out of a larger universe of cases. Collier and Mahoney (1996) explain that, within the realms of International Relations and comparative politics, scholars may often select extreme cases on the dependent variable, leading to biased estimates of the impact of a given independent variable over the generalized population of cases. However, this study seeks to leverage three “substantively important” cases, defined by Mahoney and Goertz (2006) as cases possessing “special normative interest,” and that play a “current or major role in domestic or international politics.”

These three cases were selected as all three share vital components. In all three cases the source of financial sanctions remains constant, emanating from the United States, and thus we can assume that global financial actors are reacting to a similar set of financial regulations and seeking to retain access to the same financial market. Second, all three cases were designed as “financial embargoes,” meaning severe restrictions on almost all capital inflows and outflows from a target state, a condition which allows us to control for variation in the magnitude of different sanctions programs. Third, as all three cases involve US financial sanctions targeting the nuclear programs of other states, we are also able to control for variation in issue salience between cases. Fourth, as non-democracies, these cases allow us to control for regime type. The variation under observation, therefore, is the variation in reputational risk accompanying different types of sanctions implemented between these various cases and the downstream macro-economic impacts on financial actor behavior. The selection of these cases thus allows us to more keenly observe how the causal mechanism itself varies with different mediating conditions (Gerring, 2007; Seawright and Gerring, 2008).

Process-tracing

This study utilizes a process-tracing approach to observe four critical phases: (1) sanctions implementation, (2) initial market reaction to sanctions, (3) sanctions removal, and (4) market reaction to removal. In addressing these phases specifically, this study allows us to observe the initial variation in sanctions measures applied to US targets (either secondary or primary measures), followed by the impacts of such measures on targeted economies, and the subsequent economic effects accompanying their removal.

For the purposes of this study, applying process-tracing to a small-N sample offers a more informative analysis than that of a statistical, large-N approach. This study’s primary purpose is to isolate and assess the impact of reputational risk, and the ways in which it alters financial actors’ decision-making, a purpose for which a statistical approach would seem ill-suited. Indeed, while quantitative methods allow us to observe the effect of one or more independent variables on a given dependent variable, statistical outputs still require the explanatory power of largely unobservable causal mechanisms to assess causation, something for which process-tracing is more well-suited. Moreover, given the current lack of appropriate theorization about the reputational causal mechanism in sanctions and International Political Economy (IPE) literature, a more incisive qualitative approach assessing its impact is certainly appropriate from both an empirical and theory-building perspective.

Limitations

This study contains certain limitations in the availability of data, particularly in the North Korean case regarding firms’ reticence to publicly comment on the reasons behind their decisions, or to discuss their relations to North Korea in any institutional forward guidance. Such data, as a result, have been supplemented by secondary and anecdotal evidence.

Failure of sanctions relief in the case of Iran

Iranian sanctions and their impacts

In 2010, the United States introduced the Comprehensive Iran Sanctions, Accountability and Divestment Act (CISADA), a series of secondary financial sanctions prohibiting US- and foreign-based financial institutions from dealing with sanctioned Iranian actors and institutions. Under this sanctions program, virtually all Iranian financial institutions, including the Iranian Central Bank, found themselves cut off from Society for Worldwide Interbank Financial Telecommunications (SWIFT)—the global financial messaging system designed to send and receive money transfers. To that end, US financial sanctions sought to prevent global financial institutions from “handling any transactions with foreign banks that [in turn handled] transactions on behalf of an Iranian bank” (Katzman, 2013: i).

These secondary sanctions thus extended US financial restrictions from Iranian actors to any global financial institution found to be non-compliant with US sanctions measures. In return, non-compliant actors would ultimately be barred “from conducting deals in the United States or with the US dollar” (Laub, 2015). The coinciding reputational risks for global financial actors were so potent that even in cases where the Treasury extended oil import waivers for cooperative states, their “banks [were] no longer prepared to take the reputational risk of handling the payments. The result [was] that some banks cut their links with Iran even if legally they [did] not need to” (Blas, 2012).

The accumulation of reputational and material risks began a cascade of financial divestments from Iran’s oil sector beginning in July 2010. By September of that year, the US State Department announced that numerous European energy giants, including Glencore, Trafigura, Total, BP, Royal Dutch Shell, LUKOIL and ENI, had collectively pulled between US$50 billion and US$60 billion of upstream energy investments in Iranian oil production. US financial sanctions also triggered a general wave of capital flight, as “foreign direct investment tumbled from US$4 billion in 2010 to ‘a complete halt’ in 2012.” (Mufson, 2015).

During this period, US regulators reinforced these sanctions by levying major fines against global banks for processing transactions to and from Iran in violation of US financial sanctions. This included the likes of BNP Paribas, HSBC, and ING, while firms such as JP Morgan, Wachovia, and Citigroup were cited for inadvertent lapses in anti-money laundering standards that led to Iranian sanctions evasion (Viswanatha and Wolf, 2012). The impact of these fines stimulated an increasingly robust effort on behalf of large global banks to improve their anti-money laundering standards and invest heavily in compliance officers to screen payments and transactions that could come to be troublesome for their downstream performance (Sun, 2019).

Although the short-term impacts of reputational risk produced a strong, negative market reaction toward Iranian targets, the long-term consequences of this reputational effect would prove highly damaging, as the threat of reputational damage associated with non-compliance with US sanctions quietly filtrated throughout the global financial system, creating a condition in which the removal of sanctions had an observably muted impact on Iran’s financial reintegration into the global economy.

Sanctions removal: global financial actors’ response to the JCPOA

The formal removal of sanctions in 2015 came in the form of the Joint Comprehensive Plan of Action (JCPOA), which afforded Iran several key inducements. First and most important of which was the easing of secondary sanctions, which removed “(1) sanctions that limited Iran’s exportation of oil and sanction foreign sales to Iran of gasoline and energy sector equipment, and which limit foreign investment in Iran’s energy sector; (2) financial sector sanctions” (Katzman, 2013: 44). The ultimate expectation of these conditions was that “with the Central Bank no longer in the vise-like grip of the US Treasury, and with SWIFT messages flowing, Iran’s financial sector [would] soon be operating at pre-sanctions levels” (Nephew, 2016: 11).

The expected effects of unwinding US financial sanctions were therefore predicted to be significant. According to the World Bank, foreign direct investment was expected to “climb to as much as $3.5 billion in a couple years” (Mufson, 2015), while others, such as the Foundation For the Defense of Democracies, asserted that the effect of the JCPOA would provide an economic boost “from capital inflows that facilitate investment and employment,” though noting that “global companies are still reticent to invest in Iran” and that there was “no evidence of new investment yet” (Domjan et al., 2014: 13, 8).

The removal of financial sanctions brought with it a number of key sanctions relief outcomes. Foremost among these, Iran’s access to the SWIFT electronic payments system was restored in early 2016, which enabled Iran to re-establish capital mobility between it and the global financial system. However, despite this restoration of Iranian capital mobility, the US Congressional Research Service noted that global banks were reticent to reenter the Iranian market after the 2016 easing of sanctions, largely due to “lingering concerns over past financial penalties for processing Iran-related transactions in the U.S. financial system” (Nephew, 2016: 65). Regarding the dearth of global investment after sanctions removal, Reuters reported that despite the fact “international financial sanctions on Iran were officially lifted in January [of 2016] . . ., [Iran] has secured banking ties with only a limited number of smaller foreign institutions,” adding that “banks appear to be increasingly reluctant to do business now with Iran . . . [due to] extreme nervousness about that whole issue from a reputational risk perspective” (Saul and Hafezi, 2016).

This sanctions relief period witnessed the emergence of an “over-compliance” trend in global finance that rendered most large banks reluctant to underwrite deals with Iran (Rezaei, 2017). So strong was this trend for over-compliance that a senior European banker, speaking to the Guardian in January 2016, stated, “I am yet to find one tier-one European investment bank that wants to go back into Iran,” a level of caution that is consistent with most banks stating that “there was no change in their existing policy” after the removal of sanctions (Kamali Dehghan, 2016). Iran’s reintegration with international banking was “sufficiently slow and vexing [to] the Supreme Leader of Iran” who used his annual Nowruz speech in 2016 to criticize the United States for the lack of sanctions relief having reached Iran after sanctions had been removed (Nephew, 2016: 11).

The P5+1 pro-investment initiative

During the process, the United States expressed a strong desire to improve Iran’s global reintegration, in order to facilitate and incentivize its compliance with the non-proliferation conditions of US sanctions. During this post-JCPOA relief period, the US Department of State conducted a series of meetings with the heads of several of the world’s largest banking institutions, signaling to market actors not simply that it was safe to once again do business with and invest in Iran, but also US preferences for Iran’s reintegration into the global financial system.

In May 2016, US Secretary of State John Kerry chaired a joint meeting of nine executives from Europe’s largest banks, along with officials from the US Treasury, British Foreign Secretary Philip Hammond, Britain’s Secretary of State for Business Sajid Javid, and Norman Lamont, Britain’s trade envoy to Iran (Brunnstrom, 2016). Among the banking delegation was Deutsche Bank’s CEO John Cryan, HSBC UK head Antonio Simoes, Credit Suisse’s CFO David Mathers, as well as representatives from Standard Chartered, BNP Paribas, Santander, Royal Bank of Scotland, Lloyds, and Barclays. During this meeting, Reuters reported that Kerry “told Europe’s top banks they have nothing to fear from resuming business with Iran as long as they make proper checks on trade partners and pursue ‘legitimate business’” (Brunnstrom, 2016). Kerry stated soon afterward that the United States “[wanted] to make it clear that legitimate business, which is clear under the definition of the agreement, is available to banks” (Brunnstrom, 2016), and further signaled that “[the Iranians] have an expectation that the sanctions that are supposed to be lifted are in fact lifted” (Schwartz and Patrick, 2016). Despite this public, state-driven initiative, Iran’s annual foreign direct investment declined between 2016 and 2017, dropping from US$3.02 billion in 2016 to US$2.35 billion in 2017, 1 all despite a sharp rise in crude oil prices from US$36.77 per barrel in January 2016 to US$66.87 per barrel by December of 2017, 2 a spike of more than 45 percent.

The removal of secondary financial sanctions thus did not precipitate the level of sanctions relief and financial reintegration that was expected. The United States and its P5+1 partners hoped and needed global financial institutions to reintegrate targeted Iranian entities as a matter of long-term non-proliferation goals. Yet, reputational risk extended beyond the removal of financial sanctions, complicating Iran’s reintegration into the global economy. Indeed, “stigmatizing all business with Iran [had become] the new sanction,” and that sanction was privately enforced against the wishes of world powers (Lakshmanan, 2016).

Counterfactual

If reputational risk were not producing the observed outcome in Iran’s post-sanction reintegration, might such outcomes be explained by domestic protectionist interests? Here, we might expect Iran’s domestic financial actors to have lobbied for capital control protections in order to protect their domestic market positions from international competitors, thus corresponding to the observed difficulties in Iran’s ability to attract foreign capital. Here, we appear to find little evidence that domestic interest groups sought significant protections, or had particularly benefited from sanctions in a way that incentivized the establishment of a sanctions-like financial environment. Indeed, as a result of financial sanctions, Iranian banks’ profitability had sharply declined relative to their pre-sanction levels (Schwartz et al., 2017). Moreover, cost-push inflation and a need to keep banks capitalized led to higher interest rates, and consequently a higher rate of non-performing loans and over-leveraged institutions (Schwartz et al., 2017). Consequently, observers noted the likelihood of an “intense lobbying effort by Iran’s business community in support of the agreement” (Habibi, 2015). Formal meetings between the business community and government officials about ways to reach out to prospective investors in the global marketplace as reopening loomed to reinforce this point (Ramin et al., 2014). Hasan Rouhani’s government had subsequently begun pro-market reforms to prepare the economy for a post-sanction environment. One such move was a dismantling of Iran’s dual-exchange rate system, which would allow “commercial lenders to buy foreign currencies using rial rates set by the market rather than those dictated by the central bank” (Nasseri, 2016); indeed, the regime saw this as barrier to foreign direct investment (Mostaghim et al., 2014).

Summarily, it appears that Iran’s observed lack of economic reintegration had little connection with domestic economic constituencies’ protectionist motives. Not only were domestic actors supportive of economic opening, but the Iranian regime had simultaneously begun market-friendly reforms designed to attract global capital. Based on these dynamics, we might discredit the causal effect of domestic resistance to global capital and its relation to Iran’s stunted experience with reintegration.

Failure of sanctions relief in the case of North Korea

North Korean financial sanctions

North Korea, like Iran, has a long and complex history of nuclear-related sanctions. In November 2002, the withdrawal of North Korea from the Non-Proliferation Treaty (NPT) triggered a prolonged nuclear scramble, for which The Six-Party Talks became the primary diplomatic venue. Seeking to improve its bargaining position, the United States implemented financial sanctions targeting global banks responsible for facilitating illicit regime activity and sanctions evasion.

A significant aspect of the regime’s nuclear activities during this period derived from North Korea’s ability to access the global financial system through a sophisticated illicit network of financial institutions. Included within this network was a North Korean domestic bank, Tanchong Commercial Bank, the North Korean Mining and Development Corporation (KOMID), as well as Daedong Credit Bank, at the time the only international bank doing business in North Korea itself (Zarate, 2013: 225). The regime also retained a complex web of bank accounts spanning from Austria to Macau, Russia, Vietnam, Singapore, and China.

Beginning in 2002, the United States began a regulatory campaign known as the “Bad Bank Initiative,” targeting North Korea’s illicit financial ties (Zarate, 2013: 232). Here, the US Treasury sought to engineer a severe market reaction, targeting North Korean funds, and blacklisting complicit financial actors found to be harboring North Korean funds. We will first discuss the case of Banco Delta Asia—a Macau-based bank—and the wider market and reputational implications that accompanied its blacklisting by the US Treasury.

Banco Delta Asia and reputational risk

One of North Korea’s major points of entry into the global financial system was the Macau-based Banco Delta Asia (BDA), which US regulators found to be laundering North Korean funds through approximately 50 North Korean–held accounts (Zarate, 2013: 225). In September 2005, the US Treasury made BDA the focal point of its Bad Bank initiative and financial constriction campaign, publishing a “Section 311” regulatory advisement instructing US banks to end any and all relationships with what it described as “a primary money-laundering concern” facilitating North Korean nuclear proliferation (Zarate, 2013: 226).

As Zarate (2013) explains, “in a single stroke the bank was converted into a financial pariah in the US and international financial system” (pp. 240). Beginning soon after this regulatory action was “a chain of market-driven rejections of North Korean accounts and transactions” (Zarate, 2013: 240), including a run on approximately US$133 million of private BDA deposits—which accounted for some 33 percent of the bank’s total deposits (Greenless and Lague, 2007). Globally, “other financial institutions began severing their ties with North Korea, not wanting to risk entanglement in North Korean illicit activities and possible expulsion from US financial markets” (Lague and Greenless, 2007). The compliance officers and general councils of international banks with North Korean clients soon realized the reputational risks they faced and “started to shun business with North Korea, creating an informal financial embargo of the country” (Greenless and Lague, 2007). In short order, three South Korean Banks—Korea Exchange Bank, NFFC, and Shinhan Bank—had all terminated correspondent bank relations with BDA, and were joined by two major Japanese banks, Bank of Tokyo Mitsubishi UFJ and Mizuho Corporate Bank (Lee, 2006).

Importantly, Chinese state-owned banks, who had been among the most permissive financial institutions facilitating North Korean access to global financial markets, reacted to the BDA regulation just like other banks. Indeed, major Chinese financial institutions—such as The Bank of China, Chinese Citic Bank, the Chinese Construction bank, and Shanghai Pudong Development Bank—began freezing a number of accounts containing several million dollars (Firfield and Kirchgaessner, 2006) and blocking financial transactions between Chinese and North Korean companies and individuals (Fairclough, 2006).

Sanctions relief: failed attempts to financially reintegrate North Korea

The cumulative impact of this US-led market reaction included important diplomatic concessions in November 2006, when North Korea agreed to return to Six-Party Talks “on the premise that the issue of lifting financial sanctions [would] be discussed and settled” (Zarate, 2013: 253). The principal action in unwinding such financial sanctions centered around the “unfreezing” of US$25 million of North Korean assets held by Banco Delta Asia and the repatriation of such funds to Pyongyang.

Interestingly, “American senior officials would often ask if the briefers were misstating ‘million’ instead of ‘billion,” due to the fact that “twenty-five million dollars seemed a small price to pay to bring the North Koreans back to the Six-Party Talks” (Zarate, 2013: 255). However, as anecdotal evidence from Zarate (2013) explains, “the amount of money wasn’t the issue—they wanted the frozen assets returned so as to remove the scarlet letter from their reputation . . . [as] the first step in restoring their ability to do business with banks” (pp. 255–256). Securing the return of these assets via a recognized and “legitimate” international financial institution thus represented an opportunity for North Korea to demonstrate that “their assets were no longer toxic and could be touched again without fear of subsequent [sanctions]” (Zarate, 2013: 257).

However, removing secondary financial sanctions on BDA proved to be an intensely difficult exercise, for doing so required the US Treasury to find a reputable financial institution willing to receive tainted North Korean assets and divert them to Pyongyang. In the course of doing so, the Treasury found that “no bank . . . would even touch such a transaction,” due to fears that they would “be subject to some form of sanction or additional attention in the future” (Zarate, 2013: 258).

Market failure: US intervention in North Korea’s financial reintegration

In seeking to reintegrate North Korea into the global financial system, the United States actively sought the cooperation of Chinese financial officials with intent of transferring toxic North Korean assets through the Chinese financial system. Yet, despite being explicitly reassured that compliance with US sanctions relief measures was safe, Chinese financial actors actively resisted financially reintegrating North Korea into their financial system due to concerns “about the taint of North Korean accounts and the reputational impact [it] could have” on their access to global capital markets (Zarate, 2013: 256). Chinese financial officials “saw this as a moment to insulate the Chinese banking system from North Korea’s illicit financial activity,” and by refusing to expose Chinese banks to toxic North Korean assets and their corresponding reputational risks, Chinese finance officials had refused to comply with the US sanctions relief initiative (Zarate, 2013: 262).

Further US government efforts to mobilize global financial actors in the transfer of North Korean assets proved extremely difficult. Assistant Secretary of State for East Asian and Pacific Affairs, Chris Hill “spent weeks trying to find a bank that would help in the transfer of the assets” (Zarate, 2013: 263). In 2007, the BBC (2007a, 2007b) reported that “banks around the world have refused to touch the money” and that “banks in China and Vietnam [had] been approached and [had] refused to get involved.” As a result, US officials increasingly sought assistance from US banks in assisting with the transfer of North Korean funds, none of which were ultimately willing to expose themselves to such funds. One such bank—Wachovia—was approached by the US State Department, but “refused to carry out the transaction” (Weissman, 2007). The bank resisted complying with the US sanctions relief initiative out of concern that handling North Korean funds would make them vulnerable to “future sanctions or regulatory actions” and sought “assurances that it [would not be] in breach of section 311 [of the Patriot Act]” before ultimately declining any and all assistance to the US Treasury (BBC, 2007b).

Due to market wariness of toxic North Korean assets, the United States was forced to channel illicit North Korean funds through the Federal Reserve Bank of New York (n.d.) and the Russian Central Bank (Yukhananov and Strobel, 2014), who then transferred North Korean assets through the Far Eastern Bank in Vladivostok—where North Korea kept a long-unused account. From there, Far Eastern transferred the funds to the North Korean Foreign Trade Bank (Zarate, 2013: 264), and on 25 June 2007, a North Korean Foreign Ministry spokesman finally confirmed the receipt of its BDA funds (Davenport, 2019).

As reflected above, the reticence of global financial actors to comply with US sanctions relief initiatives was a direct consequence of reputational dynamics linked to the US Treasury’s secondary financial sanctions. Reputational effects in these preceding cases have shown a certain degree of “stickiness,” that is, that once reputational risks have been applied to certain “illicit actors,” such reputations are not easily undone, even in cases where sender states explicitly attempt to undo their own sanctions measures for their own national security purposes.

In these phases, we see clearly the impact of reputational risk on financial actor reintegration behavior. Here, financial actors that had previously comprised North Korea’s financial network refused to cooperate with its reintegration to the global financial system, a behavior that was mirrored by financial actors who had no previous involvement with North Korean capital or accounts.

Counterfactual

As shown, the removal of financial sanctions in the North Korean episode, accompanied by direct US efforts to intervene with financial actor decision-making, sought to assuage financial actors of any concerns related to the future reintegration of North Korean targets. Were reputational risk concerns not affecting financial actors’ decision-making in this case, might we expect a lack of reintegration into the global economy to be a function of opposition from North Korea’s domestic military-financial interests? Indeed, we might expect protectionist behavior in the form of North Korea sanctions-proofing its economy further to avoid future instances of financial leverage being brought against them. Unquestionably, North Korea’s domestic financial interests were subjugated to and facilitators of the state’s military interests. The introduction of market-based actors and reforms was still considered by Kim Jong-Il to be a significant threat to his hold on power (Solingen, 2007), and thus one would expect that domestic pressure to shun global financial relations would come from the state’s own institutions in a bid to ensure regime survival.

While a lack of systematic information regarding the inner workings of North Korea’s political economy makes definitive conclusions difficult, the domestic interests within North Korea clearly favored the development and maintenance of global financial relations as a means of funding the state’s nuclear program (Solingen, 2007; Zarate, 2013). The regime’s need to circumvent long-standing trade embargoes had resulted in dependence upon maintaining its integration into global financial networks, through which illicit activities could take place. Cumulatively, we might thus discredit the causal effect of domestic resistance to reintegration and its relation to North Korea’s stunted experience with reintegration into the global financial system.

Successful sanctions relief in the case of Libya

Unlike the reputational dynamics illustrated in the Iran and North Korean episodes—that is, strong market-driven rejections of previously sanctioned states—the Libyan episode reveals the inverse phenomenon, the removal of financial sanctions followed by a swift and positive response by global financial actors. Libya thus represents an intriguing test case, illustrating not only how financial sanctions might be more effectively implemented, but also the conditions under which the removal of such financial measures might lead to more successful relief overall.

As with the previous two cases, US sanctions removal in Libya became heavily linked to the nuclear weapons program of the target state. In July 1995, International Atomic Energy Agency’s (IAEA) reports asserted that Libya had made a “strategic decision to reinvigorate its nuclear activities, including gas centrifuge uranium enrichment,” a technology that could be used to enrich uranium for use in nuclear reactors (Davenport, 2019). The US policy response—in August 1996—was the passage of the Iran and Libya Sanctions Act (ILSA), authorizing the Executive branch to impose financial sanctions against foreign companies investing more than US$40 million into the Libyan oil sector, a figure that was lowered further to US$20 million in 2002 (Davenport, 2019). These measures “threatened US market access to any foreign company” engaging with or investing in this most vital of Libyan sectors (Nephew, 2018).

Over the coming months and years, Libya became increasingly cooperative on issues relating to its nuclear program and its wider non-proliferation efforts. Indeed, “Libya wanted to be largely normalized and was prepared to pay a price to achieve this end,” but in exchange, Libya “also wanted to receive the benefits of this normalization” (Nephew, 2018: 6). Libya’s improved compliance behavior was, in fact, tied directly to the quality of sanctions relief and financial reintegration it experienced following the removal of financial sanctions, as the regime “had gained concrete benefits from sanctions being lifted in the form of improved access to international markets and sources of capital” (Nephew, 2018: 20). In 2003, the year prior to sanctions removal, Libya’s FDI inflows stood at just US$143 million, a figure that would suddenly skyrocket to US$1.03 billion in 2005, the year following removal (IndexMundi—Libya FDI Inflows). 3 FDI inflows would continue to grow steadily in the post-sanction period, to US$2.06 billion in 2006, US$4.6 billion in 2007, and US$4.1 billion in 2008 (IndexMundi, 2016). This is a significant market response, given that between the implementation of the Iran and Libya Sanctions act in 1996, and the removal of these financial sanctions in 2004, the highest net inflow of FDI stood at just US$145 million, occurring in 2002 (IndexMundi, 2016). By understanding the nature of the measures implemented during this episode, and their coinciding reputational risk dynamics, it will be possible for us to more effectively understand the nature of financial sanctions more broadly, and the conditions for successful relief of these measures more specifically.

The Iran and Libya Sanctions Act: primary financial sanctions at work

Why did Libya experience such strong financial reintegration into the global financial system following the removal of US financial sanctions, while Iran and North Korea did not? Such curious variation can be explained by examining the ILSA itself, reflecting reputational risk dynamics that appear to be muted.

The ILSA in effect “blacklisted foreign firms for their activities in Libya” (Schwartz, 2007: 564), and was designed “to deter investment by non-US companies in [Libya’s] oil production sectors” (Meyer, 2008: 929). The violation of US secondary financial sanctions could result in the denial of access to US capital and any import–export financing or support for non-US firms and financial actors (Meyer, 2008: 929). The terms of these provisions, that is, the denial of access to US capital to non-compliant global actors, were secondary sanctions measures intended to “influence the activities of foreign firms operating [in Libya]” (Meyer, 2008: 930). However, the unilateral implementation of these secondary measures by the United States proved politically problematic, particularly with the European Union (EU), who began to implement their own “retaliatory laws to block or offset any damage to their companies’ business interests” (Meyer, 2008: 929).

In the face of this strong political backlash, “the United States ultimately relented by means of presidential waiver of application of the disputed secondary sanctions provisions” (Meyer, 2008: 929–930). In 1998, the EU received important concessions that the United States would not seek or propose, and [would] resist, the passage of new economic sanctions legislation based on foreign policy grounds which is designed to make economic operations of the other behave in a manner similar to that required of its own economic operators. (Smis and Van der Borght, 1999: 231)

The Clinton Administration, in response, extended waivers to EU member states, thus “exempt[ing] . . . EU companies from the most controversial aspects of the [ILSA],” effectively removing secondary financial sanctions and the threat of blacklisting for foreign financial actors (Smis and Van der Borght, 1999: 232).

With secondary measures removed, so too was the threat of US Treasury blacklisting and the corresponding reputational effects threatening exclusion from US financial markets for interacting with an actor under US sanctions. European financial actors could now operate in a regulatory environment that did not preclude them from conducting business with Libya, freeing them from the threat of blacklisting. As will be shown, financial sanctions removal preempted an immense and sustained inflow of foreign direct investment, as Libya experienced strong reintegration into the global financial system.

Sanctions relief: a positive market response

The global market response to the removal of financial restrictions on Libya was very different to that of previous cases this study has discussed because financial actors perceived sanctions as primary and thus low-risk regarding exclusion from US markets. According to Nephew (2018), “for those measures most directly linked to external participation, Libya benefited greatly from sanctions removal” (pp. 17). During the period in which the Iran and Libya Sanctions Act had been implemented (1996–2004), inflows of foreign direct investment averaged only US$24,155,456 per year (IndexMundi).

Following the removal of the secondary sanctions statute in 1998, global financial actors did not immediately reinvest in Libya, as UN Security Council members, France and Great Britain retained an embargo on oil-related investments and technology transfers, and, moreover, US financial sanctions still applied to US firms, particularly US oil production firms. In practice, this meant that Libya could not access vital technologies required to modernize their production facilities and extraction methods, all of which ultimately contributed to a lack foreign oil and gas investments (Bruce St. John, 2008: 83). Indeed, it soon became clear that the American oil companies would have to participate to generate the desired level of investment. Libya needed leading-edge exploration and development technology as well as the enhanced oil recovery techniques necessary to soften the natural decline in maturing fields. (Bruce St. John, 2008: 83)

However, the official removal of US sanctions triggered an enormous market reaction. Between the official removal of sanctions in 2004 and the onset of the global financial crisis in 2008, average inflows of FDI to Libya shot up to US$2.45 billion, reaching as much as US$4.68 billion in 2007 and a further US$4.1 billion in 2008 (IndexMundi). Libya’s financial reintegration into the global financial system was aided by a series of Exploration and Production Sharing Agreements (EPSAs), competitive bidding processes designed to stimulate investment in oil and gas exploration, all of which had previously been subject to sanction. The demand was immediate and substantial. In response to an offer of 15 onshore and offshore exploration areas in 2005, Libya “received applications from more than 120 oil companies. Libyan authorities later narrowed the field of potential bidders to 63, including several large US oil groups” who were now free from the constraints of US financial sanctions (Bruce St. John, 2008: 85). Among the entrants were US firms ChevronTexaco, and Occidental Petroleum, as well as Petrobras of Brazil, Indian Oil from India, Medco Energy International of Indonesia, Oil Search of Australia, and Verenex Energy of Canada (Bruce St. John, 2008: 85). Additional second, third, and fourth rounds of Exploration and Production Sharing Agreement (EPSA) offerings occurred throughout the course of 2005, 2006, and 2007, generating an additional 119 exploration and extraction applications (Bruce St. John, 2008: 86).

In conjunction with Libya’s EPSAs, the regime developed a bilateral engagement model encouraging foreign direct investment into the petroleum sector, a move that yielded further financial reintegration after the removal of financial sanctions. Included within this bilateral model were a series of successful negotiations with Occidental Petroleum in 2005, and Royal Dutch/Shell in 2004–2005 (Bruce St. John, 2008: 86). Moreover, on a state visit to Libya in 2007, Prime Minister Tony Blair announced a 7-year bilateral contract between Libya and British Petroleum worth US$900 million, designed to develop natural gas processing, transportation, and liquefaction for export (Bruce St. John, 2008: 86). As shown by Nephew (2018), in regard to inflows of foreign direct investment “Libya did well after 2004 and until 2008–2009, [prior to] the onset of the Great Recession,” an event that, in conjunction with the onset of civil war in 2011, brought to a premature halt Libya’s long-term economic recovery (pp. 17).

This rapid, enthusiastic market response to sanctions removal is curious when placed alongside the reticence of global financial actors in the Iranian and North Korean episodes. While all three cases share the same sender-state, program magnitude, issue salience, and regime-type, such cases also revealed key variation in the reputational dynamics built into their respective legal frameworks, dynamics which appear to account for the variation of financial reintegration experienced by US targets.

In the Iranian and North Korean episodes, the fact that global financial actors had been exposed to the threat of Treasury blacklisting, and thus internalized strong compliance behavior in response to its corresponding reputational risks, greatly clarifies the post-sanction market reaction in which financial reintegration was not extended to US targets. Yet, such actors had not faced such acute reputational risks during the period in which financial sanctions were in place in Libya. In this case, threats of US Treasury blacklisting and market exclusion for non-US financial actors had been removed via the use of Presidential waiver, in turn restricting investment into Libya by US firms exclusively, and removing the stigma of conducting business with Libya for non-US firms. As Nephew (2018) explains, considering the fact that countries outside the United States had been more or less free to invest in Libya, it is unlikely to be entirely coincidental that the end of US sanctions in 2004 paced a massive infusion of new investment into Libya. (Nephew, 2018: 18)

The reputational dynamic governing relations between target states, and the private market actors responsible for reintegrating them, is thus a crucial piece of variation explaining the divergence in market responses to the removal of financial sanctions in these instances. Consequently, this variation also reflects the reputational “stickiness” of blacklisting after the removal of secondary financial sanctions, and the downstream impact of reputational damage on the reintegration of previously targeted actors themselves.

In a methodological context, this case is different in the sense that the absence of a specific condition—reputational risk—determines the success of the hypothesis. Given the absence of observable variables, this case appears to provide strong smoking-gun evidence in which US Treasury blacklisting of third-party financial actors does not occur, and thus explains, in theoretically consistent manner, the more enthusiastic market responses to sanctions removal in the Libyan episode.

Counterfactual

If a lack of reputational risk were not responsible for Libya’s successful reintegration into the global economy, is it possible that Libya’s domestic actors and government sought little to no protectionist measures for the domestic economy? Here, Libya’s record was mixed. As shown above, the Libyan government was keen to attract FDI in the energy sector, as Libya’s state-owned National Oil Corporation (NOC) required leading-edge exploration and development technology, and enhanced oil recovery techniques to develop effectively. However, at the time, the NOC accounted for approximately 90 percent of Libya’s revenues and 95 percent of its export earnings (Bruce St. John, 2008: 82), and a 2006 report by the National Democratic Institute for International Affairs (NDI, 2006) noted that the political system remained based on a state-run economy, suggesting that domestic financial actor interests and government interests were largely one and the same.

In non-hydrocarbon sectors, however, Libya’s domestic financial actors actively resisted economic opening. Public criticism of liberalization policies increased after May 2005 when Libya imposed a 30% hike in fuel prices and doubled the price of electricity for consumers of more than 500 kilowatts a month. A related decision to lift customs duties on more than 3,500 imported commodities raised job security concerns in local factories poorly equipped to meet foreign competition. (Bruce St. John, 2008: 82)

Domestic resistance to non-hydrocarbon liberalization policies thus stalled economic reforms designed to open the economy more broadly. Cumulatively, this suggests that Libya’s successful reintegration experience was partially a result of lowering barriers to investment in a single competitive sector, although the overall economic climate remained hostile to liberalization and retained protectionist, rent-seeking inclinations. Here, there is some support offered to counterfactual expectations, although, overall, the inconsistency with which counterfactual expectations explain financial reintegration in each case suggests it has little generalizable impact.

Conclusion

The increased use of financial sanctions in global affairs has arisen, in part, because of these tools’ effectiveness in financially isolating illicit actors from the global financial system. Previous studies have shown that the effectiveness of implementing such tools is largely a result of reputational risk calculations tied to the blacklisting of firms by the US Treasury for non-compliance with US sanctions measures. This study shows that the same dynamics that are so effective at generating compliance from private market actors are the very same dynamics that make removing such financial measures particularly challenging.

As shown in the Iran and North Korean episodes, global financial actors complied strongly with US secondary financial sanctions during their implementation period, yet, once such measures were lifted, these actors also showed a strong aversion to assisting the United States in reintegrating targeted actors into the global financial system. In the Libyan episode, however, the removal of secondary statutes in the financial sanctions of the Iran and Libya Sanctions Act removed the threat of blacklisting by the US Treasury for non-US firms, and, importantly, any reputational effects associated with being blacklisted, that is, exclusion from US capital markets. Indeed, the absence of reputational risk embedded in US sanctions measures does well in explaining the swift and positive market response to the removal of financial restrictions on Libya.

The implications of this research suggest a strong paradox in the tools of US economic statecraft, one that ultimately threatens to render US financial tools wholly ineffective in the long term. While US financial sanctions certainly benefit from the reputational effects associated with the US Treasury blacklist, the same dynamics may ultimately prevent the United States from being able to credibly offer positive inducements to its targets in exchange for more compliant state behavior. In highlighting these peculiar dynamics, this study sought to illuminate the apparent “stickiness” of reputational risk as a long-term condition, rather than a short-term reaction. The ease of implementation and the magnitude of their effects will undoubtedly be attractive to policymakers with limited tenure and short-termist agendas. However, the pyrrhic nature of secondary sanctions suggests that their implementation will ultimately limit future policy options for the sender, calling into question their long-term viability as tools of economic statecraft.

There are additional implications that offer intriguing avenues of future research. First, the pyrrhic dynamics of secondary sanctions raise questions about the extent to which the threat of such sanctions may be effective in future episodes. For example, if potential target states recognize that sanctions, once imposed, effectively remain permanent, they may be forced to acquiesce to sender demands well before the onset of sanctions. It is also possible that the threats made by sender states may trigger the advent of significant numbers of alternative payment systems, which target states might use to evade the effects of secondary sanctions. Were this to occur, the global financial system may dissolve into financial spheres of influence. In addition, such dynamics raise questions over whether or not the mere threat of secondary sanctions is enough to produce reputational damage, such that, even if sanctions are not ultimately imposed on potential targets, they might observe a permanent adverse market reactions to their illicit behavior. While this study does not address sanctions threats explicitly, this will undoubtedly be an important avenue of study in future research.

A final implication for future study involves the heterogeneity of financial agents themselves. Indeed, financial agents may harbor different appetites for reputational risk, and thus certain firms may be more willing to re-engage with previously sanctioned states than others. Sectoral differences may offer one possible source of variation; however, an alternative source of variation may be the form of capital firms typically deploy, that is, patient or impatient capital, which often are rooted in the corporate governance structure of their home country (Hall and Soskice, 2001). Here, firms operating in liberal market economies (LMEs) or coordinated market economies (CMEs) have varied time and stakeholder pressures on their investments. Firms in CMEs, for example, are more reliant on patient capital, that is, capital that does not entirely depend on short-term returns on investment. LMEs, however, are typically more reliant on “impatient capital,” public information about firm finances and short-term capital, in which returns on investment are paramount. Based on such variation, one might reasonably expect firms deploying patient or impatient capital to approach post-sanction economies differently. A detailed study of the impacts of firm heterogeneity on post-sanction reinvestment would, indeed, be an illuminating avenue for scholars to pursue.

Footnotes

Acknowledgements

I would like to thank the editors at the European Journal of International Relations and the two anonymous reviewers, whose rigorous feedback greatly strengthened the paper and its contributions. I am hugely grateful to Heidi Hardt, Erin Lockwood, Samantha Vortherms, Daniel McDowell, and Spencer Wolfe for their valuable comments on earlier versions of the manuscript. Earlier versions of this manuscript were presented at ISA 2020 and ISA West 2021, and I am grateful to the participants in these fora for their comments and suggestions.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.