Abstract

There are numerous accounts of the financial crisis that shocked the Western world in 2008. Almost all the commentaries are steeped in the same cognitive paradigm of linear thinking and assumptions of economic self-interest that could be seen to have created the crisis. While acknowledging the multiplicity of reasons for the crisis and how it should be managed, this article offers an alternative in presenting a gendered perspective that could complement but also challenge some of the conventional wisdom. It suggests a link between managing masculinity and mismanaging the corporation leading to government bailouts for the banks and a near collapse of Western economies. Although new governance and regulation are clearly important responses to the crisis, they do not necessarily get to the root of the problem. A more sociological form of analysis could help us to understand how individual material and symbolic self-interest deriving partly from misrecognition of the self as autonomous but reinforced by masculine fragilities was a major condition of the excesses leading to the crisis. This article explores how this self-interest is not just a reflection of the neo-liberal economic consensus but also of masculine discourses within the business class elite that make the pursuit of ever spiralling remuneration almost obligatory.

Keywords

This article is stimulated by our reflections on the global financial crisis of 2008 and the exposure of earlier financial and other scandals and crises in corporate capitalism. 1 While there arenumerous accounts across a spectrum that extends from focusing on individual scapegoats to concentrating on systemic failures and risks, few 2 offer a gendered analysis of these events. We seek to fill this lacuna in the literature not as a way of displacing other forms of analysis but as a complement to them. Gender research from the late 1980s onwards was confronted with a reaction to, or a backlash against, feminism epitomized by books such as Iron John (Bly, 1990) and a proliferation of hand-wringing books about the crisis of masculinity (Clare, 2000; Cohen, 1990; Eldredge, 2001; Rutherford, 1988; Seidler, 1989, 2005). As Gill (n.d.) argues, ‘little of this “crisis talk” was based on sound empirical research’ and she doubts the very existence of a crisis. Her view is that we just need more ‘feminist-inspired, critical men’s studies’ that seek to problematize rather than just commiserate or celebrate masculinity. This is the perspective from which we seek to develop our analysis of managing masculinity and mismanaging the corporation especially, though not exclusively throughout the period leading up to the financial crisis of 2008. We could have applied this kind of analysis to any one of the crises that are historically fairly routine events but we focus on the 2008 global financial crisis because of its ferocity, continued topicality and potential negative impact on society in general and gender equity in particular.

The financial sector is particularly important because ‘it exerts more and more influence over more and more people’s everyday life’ (Blomberg, 2009: 204). Partly this may be attributed to the financialization of global economies under neo-liberal political regimes since the 1980s (Epstein, 2006; Froud et al., 2006; Krippner, 2011; Martin, 2002)—a situation where social relationships are reduced to financial transactions (Dembinksi, 2009) that are deprived of any non-economically instrumental content. The neo-liberal belief that ‘free’ markets have largely positive effects because they are efficient in allocating resources and are productive of economic growth was the prevailing consensus prior to, but also once again since, the global financial crash. What is taken for granted in this consensus is that the market is fuelled by individual economic self-interest, the consequences of which in the form of the ‘invisible hand’ are wholly positive for everyone. While commonsense regards self-interest as an unavoidable aspect of human nature, sociologists invariably understand it as socially produced and reproduced. Callon (1998) and others have revisited this recently to argue that a great deal of effort and energy is involved in the production of the self and self-interest. Self-interest relies on a process of calculation that is ‘dependent upon the complex temporal framing of the relationships in which a person is engaged’ (Roberts and Jones, 2009: 857). This temporary framing is the set of market relations through which such self-interests are realized as the self becomes ‘disentangled’ from them. For Callon (1998) then, the market as a network of relations is less an outcome of economic individual self-interest than the means through which it is produced. Similarly we would argue that within the business elite, economic self-interest is produced or at least substantially reinforced by another kind of framing—the homosocial bonding that surrounds discourses of masculinity. Having said that, subjects do not enter a market or homosocial relations innocent of already pre-formed senses of economic self-interest that have their genesis in previous networks. Consequently, it may be more appropriate to argue that economic self-interest is both a condition and consequence of the complex temporal framings of network relations that revolve around markets and discourses of masculinity.

The financial crisis in 2008 hit everybody by surprise and not least the bankers that had sanctioned a system of excessive rewards and expansion regardless of adequate risk assessment. This article examines the crisis in Sweden, the UK, and the US largely through media documents but in the case of Sweden also attendance at over 40 corporate Annual General Meetings in banks, investment trusts and big export companies. Three of the observations were made during the peak of the crisis. 3 It is difficult to avoid attributing blame to one or other of the participants in this series of events and especially to senior executive managers. For they have sanctioned reckless expansion, overexposed borrowing, traded in untested securitized loan instruments, advanced a culture of short term targets supported by stratospheric bonuses, and have been determined to reward themselves excessively even when their companies are facing siege conditions and have received government assistance. We are of the view that many of the commentaries that have sought to understand the financial crisis are steeped in the same cognitive paradigm of linear rational thinking and economic self-interest that could be said to have created the problems in the first place. Moreover, the way of thinking and the accounts they give rise to is not unrelated to the masculine discourses that are our focus. So, for example, the neo-liberal faith in free markets can be seen as grounded in the self-same ontology of autonomy, rationality and individual self-interest out of which the psychological and economic accounts are constructed. But these assumptions are not discrete from discourses of masculinity since they are also very much an outcome of autonomy, rationality and individual self-interest. Consequently to attribute a crisis of these proportions to a single set of explanations would be folly. Nonetheless, there is a tendency in the media to seek explanations for the crisis that are either psychological in the sense of finding individual ‘greedy’ scapegoats or political in identifying a systemic failure of regulation and governance/management control.

We focus neither on scapegoating individual managers for being greedy or selfish nor on the identification of different governance and regulatory solutions to the failure. These have been well documented in the media and some academic publications (see Ephemera, 2010). Given the seriousness of the crisis in having forced upon us a global recession and massive public indebtedness, it is vital that governance procedures and regulatory controls are improved to restrain any future collective kamikaze in the finance sector. Although new governance and regulations may be necessary to prevent are-occurrence of these financial events, ‘there still remains a space in which critical social science can engage and explore more deeply the roots of the crisis, the impact it is making on organizations and the role of different actors in these processes’ (Morgan et al., 2005). We seek to complement but also challenge conventional accounts by developing a sociological analysis that seeks to understand the crisis as reflecting and reproducing a class and gendered pursuit of material and symbolic advantage.

We begin the article by focussing on discourses of masculinity and in particular that which is hegemonic in contemporary management and perhaps manifests some of its worst excesses within the financial sector. Our theoretical position is grounded in constructionist perspectives on the production and reproduction of social identities (Butler, 1990). Butler’s work is distinctive in having denied any essential content in gender or sexuality, arguing that both have to be performed in order to exist. More particularly, we have focused on identities of masculinity within management (Brittan, 1989; Kerfoot and Knights, 1993) even though these are often made to appear invisible, as for example in concealing the body behind uniformity of dress. Quoting from a chapter on male ballet dancers, it is suggested that ‘Since in the early 19th century masculinity was figured to be a kind of violent blundering, the invisibility of masculinity could be said to appertain particularly to the middle classes; this process continues apace today’ (Saglia, 2010, quoted in Emig and Rowland, 2010: 1). However, we argue that in contemporary corporations, remuneration and hierarchical position are important visible yet symbolic elements of the social construction of masculinity, especially to that kind of masculinity, which we connect to the white business class elite. Within this discussion we examine the insecurity in both management and masculinity as a condition and consequence of the pursuit of material and symbolic wealth as evidenced by the preoccupation with high salaries and bonuses of the business class elite.

This provides us with a different kind of analytical purchase on the global financial crisis than is available elsewhere. We provide an outline and typical accounts of the crisis first in relation to the US/UK where it had its genesis but then through examining some media scandals concerning the crisis and the behaviour of some well-known Swedish senior executives in the finance sector. In particular, we are concerned to focus on financial bonuses and managerial attachments to them as a proxy for, or indirect evidence of, competitive masculinity. Our argument is that while the diverse explanations of the financial crisis are plausible and perhaps indispensable, they are far from exhaustive and largely leave out of account questions of gender and, in particular, masculinity. In the third section we present some secondary data from Sweden and the US that helps to illustrate the arguments about bonuses and their connection to masculine identities. The choice of Sweden is biographically driven but one of the authors conducted empirical research on boards of directors where discourses of homosocial masculinity were extremely dominant. This provided us with some material regarding the excessive concern with achieving high pay and bonuses that serves as a good proxy for dominant masculine discourses among the bankers and other senior managers. Finally we provide a summary and conclusion about the relationship between the financial crisis and the management of masculinity.

Masculinity at work

The strong link between management and masculinity has for some time been discussed and analysed from different perspectives. At first the focus was on the obvious majority in numbers of men among managers, how that affected power relations and the consequences for a minority of women (Collinson and Hearn, 1996; Kerfoot and Knights, 1996; Knights and Kerfoot, 2004; Moss Kanter, 1977; Wahl, 1996). Although she was aware of the majority/minority problems, Moss Kanter also predicted that over the course of time, the allocation of power in corporations would change to reflect more gender equality. We now realize that her optimism was a little misguided. The movement to a more equal allocation has been slower than expected and white men continue to dominate senior management positions in most Western corporations. Moreover, although the numbers of women managers have increased to some extent, management discourses are still predominantly masculine. The conservative, consensual and individualistic character of assumptions about gender mask the domination and discrimination in social relations, including those along lines of class, race, ethnicity, sexual orientation, age, mental and physical ability, region, religion, as well as gender (Brod, 1995).

Our analysis is based on a view of gender as continually constructed and sustained through different performative acts. Gender is not there, to be played out as a set of role expectations; it has to be performed and working life is an important arena for this process of doing gender (Butler, 1990; West and Zimmerman, 1987) and in particular of doing masculinity. Other scholars developed this perspective further and have shown how the allocation of labour, of wages and power positions contribute to the social construction of gender (Acker, 1992; Gherardi, 1994; Wahl, 1996). Following Butler (1993/1997, 2004) we eschew any sense of an essential gender identity that lies behind the performance; gender is all drag, a stylized repetition of acts. The gender binary has to be continually repeated and reproduced and its effect is to sustain the dominance of heterosexuality but the performance is not simply ‘within the grasp or control of the individual as it is social and cultural’ (Butler 1997 quoted in Emig and Rowland, 2010: 7). Nor is it the subject that performs; it is the performance that constitutes the subject (Butler, 1993/1997). The concepts of performance and performativity relate to the perspective of understanding social life in terms of theatrical metaphors (Schechner, 2002). This enables us to identify certain behaviours and attributes as well as bodily and personality characteristics, as instrumental in the production of ‘the right kind of man (or woman)’ according to the prevalent script. Relevant examples of these performative elements in producing and sustaining masculinity in business are: acquiring a managerial status; complying with deeply felt heterosexual norms that sustain male bonding; displaying authoritative expertise; thinking smart; taking risks and not least, securing ever increasingly high levels of remuneration. However, within business life we find several different discourses where one element may be more important than another in the act of performing masculinity. We also recognize connections between different accounts. So, for example, the neo-liberal faith in free markets can be seen as grounded in the self-same ontology of autonomy, rationality and individual self-interest out of which the psychological and economic accounts are constructed. But these assumptions are not discrete from discourses of masculinity since they are also very much an outcome of autonomy, rationality and individual self-interest. Nonetheless the same capitalist values and economic self-interest are taken for granted as a central driving force.

In an ethnographic study of finance culture in The City of London, McDowell (1997) discusses several different types of male financial operators, for example, the patriarchs from the boardrooms and the macho dealers from the floor. While they are all part of the same business, they are clearly differentiated in dress codes, behaviour and bodily acts. Nonetheless, they share similar performances that come to constitute their masculine identities.

This perspective facilitates a scrutiny not only of how gender is constructed and which elements are performative in this process but also the impact it may have on society and, as in this article more specifically, on values, attitudes and behaviour in the context of the financial sector. Although not subscribing to an identical ontology, Connell (1995) and Butler (1993) both emphasize the normative aspects of gender. Not only should you appear as a man or a woman physically—your desires must also reflect the heterosexual script. 4 Western societies in general and business life in particular are organized according to the principles of hegemonic masculinity and the heterosexual norms. By reading the TV comedy The Office as a cultural text and as a parody of gender performativity, Tyler and Cohen (2008) demonstrate ‘the desire for recognition that underpins the organizational performance and management of gender in accordance with the terms of the heterosexual matrix’. Thus homophobia becomes a powerful means to keep discipline and to sustain male bonding in ways that help to secure a stable masculine identity. In homosocial networks (Wharton and Bird, 1996) such as the ones that shape top level management, there are many strong emotions and a real interest in constantly confirming your masculinity—that you are a man of material and symbolic substance. This is one reason for developing and holding on to strong group norms that emphasize masculine values (Collinson and Hearn, 1996). However, it is not only gender but also hierarchical positions in the class structure that drives behaviour and leads to closing ranks when threatened, as for example, in the challenging of bankers bonuses by public outrage after the financial crisis. Of course, within the hierarchy the minority of women also have to comply with the norms of masculinity if they are to maintain their positions (Pullen and Knights, 2007; Wajcman, 1998).

The heterosexual matrix establishes ‘gender categories that support gender hierarchy and compulsory heterosexuality’ (Butler, 2004) but we don’t argue that sexism is the exclusive preserve of the white business elite as it is widely endorsed by men throughout the class structure. Indeed, it may be argued that white and black working class men adopt an even more explicit aggressive version of masculine superiority (bell hooks, 2004; Knights and Collinson, 1987).

Insecurity in masculinity and management

It has to be recognized that insecurity is not the prerogative of masculine subjects for Lacan’s (2008) account of how in the mirror image stage of ego development, a misrecognition occurs wherein the self identifies with a solid image of itself (the imaginary) as if this were solid, separate, discrete and independent of others. Insofar as everyday reality routinely contradicts this identification of self as autonomous, an intense insecurity is generated that forever has to be denied, ‘fixed’ or managed. So while all identities are insecure because of identifying with the image of an autonomous self, masculine identities suffer additional fragility because of social expectations of what it is to be a man—tough, independent, a winner if not a breadwinner, impregnable, and indestructible. Filling these social expectations takes a variety of forms, for example dangerous sports, gang warfare, body abuse, self mutilation, sexual conquest, aggressive competition, excessive drinking and drug taking and, risk taking (Dolan, 2011; Walsh, 2010). While this behaviour can result in some pretty dreadful social consequences, only within the finance sector of business corporations is it catastrophic. This is because executive managers in finance exercise disproportionate power and are able to take enormous risks with other people’s money. In addition they are able to vote one another excessive remuneration packages that alongside other conditions we discuss later, resulted in a financial bubble that inevitably had to burst to leave us all in chaos.

The discourse of masculinity that involves hierarchical claims to superior wealth and status is closely connected with management. To be a senior manager involves conquest, competition and control as performative elements in the process of doing masculinity in business life (Kerfoot and Knights, 1993). In the past, hierarchical managerial authority was more stable due partly to a less dynamic class structure. Once in a position of authority you could probably count on remaining there as long as you wanted. This is not the case today. Claims to knowledge about management and leadership have proliferated. The number of books, seminars, training programs and consultancy on management is steadily increasing. So also the money spent on the process of recruitment increases to ensure the selection of the most competent managers. As a consequence, today managers and leaders have a comparatively high public profile. In addition, the average number of years that corporate CEOs remain in post currently is only three to four years. A common message from the Chairs of Boards is ‘that he has done a very good job but now the company needs another kind of competence’. Obviously a senior management position in contemporary business life is socially risky if not always personally economically so 5 , and thus the masculinity associated with it is quite fragile. The spoils of conquest can readily be lost in a highly competitive environment. We argue that the development of strong (heterosexual) group norms, a standard dress code verging on what might be seen as a uniform (Mörck and Tullberg, 2005) and the homosocial male bonding (Roper, 1996) increase the material and symbolic security and mutually confirm the business class elite in their respectable middle class masculinity. 6

Drawing on MacIntyre (1984/2003: 88), we argue that the very possibility of management knowledge is open to question. This is because it fails to equate with the natural science capability to predict events through the application of abstract and generalized laws. A lack of knowledge combined with the unpredictability of human behaviour leaves management in a constant struggle to be in control even if this could never be wholly accomplished. It is this comparative absence of what might reasonably be described as knowledge that renders managers particularly uncertain and insecure. This is so especially when management feel the need to live up to an image of masculine power that is almost equally as elusive. Not surprisingly then, management tends to manage its insecurity by over-compensation in terms of an unadulterated aggressive masculine assertiveness (Knights, 2006). This conceals its weaknesses at least until the unanticipated consequences of such behaviour return to haunt the organization, as has happened in the financial sector of late. It also helps to explain why managers are attached to securing ever-spiraling increases in salaries and bonuses. First of all, high levels of remuneration are a sign of market value, which is self-assuring and provides them with a sense of self-importance and independence from society. Secondly, as a retired senior public official remarked recently at a conference ‘managers with such high incomes believe it cannot go on for ever so they grab all they can before the Armageddon’ (Bristol Business School, 2010).

The lack of knowledge also helps to account for management’s fascination with gurus that appear to offer panaceas to fill the vacuum (Knights and Richards, 2003). The development of a proliferation of new financial instruments in the form of derivatives, securitized mortgages, collateralized debt obligations (CDOs), and other structured asset backed securities is a form of management innovation albeit one facilitated by mathematical expertise. It provides a seemingly magical process that converts subprime debt into high quality investment securities that can be distributed to other investors almost ad infinitum (Roberts and Jones, 2009: 857). Senior managers sanction these instruments without necessarily understanding them largely because they are shown to offer new channels for profit making and, by implication, bigger bonuses for themselves. Hence the continuous turnover of new management techniques and solutions in the form of organizational or product innovation, the latter of which contain a diverse range of bundled debts and have been adopted by senior financial sector executives even when, on their own admission, they have not always understood them.

While agreeing with McIntyre regarding the absence of any scientific certainty surrounding management knowledge, this is no less true of a whole range of knowledge not just in the social sciences but also within some of the natural sciences, especially those such as theoretical physics that are at the forefront of new knowledge. Also, although intimated, McIntyre does not acknowledge fully how knowledge is drawn upon in the exercise of power and how power stimulates the very production of knowledge (Foucault, 1980). So while management may not possess knowledge that can guarantee to generate predictable outcomes, its deployment in exercises of power often produces self-fulfilling effects that give it the appearance of certainty and predictability. This is because management exercises hierarchical and gendered power over subordinates, which in turn, often secures employee compliance, given the unequal control of resources in hierarchical organizations. Not that resistance is precluded by managerial and masculine power for indeed, compliance when combined with indifference and distancing behaviour may be seen as a form of resistance (Collinson, 1994).

Of course, practicing managers are rarely naive enough to believe that their knowledge has the status that is claimed for it in the pursuit of managerial legitimacy. They are also aware that what works at one point may not at another, and in order to legitimize their privileges they must forever be seeking new and exclusive knowledge. But the continuous necessity to be searching for, and applying, new knowledge is in itself anxiety provoking and generative of insecurity (Watson, 1994). There is then a double sense in which managers are insecure: first, they are aware that management knowledge does not have the certainty and stability of science even though managerial legitimacy is based upon a specialist ‘expertise’ that is dependent precisely on such uncertain knowledge. Second, these conditions make it necessary for managers continually to seek new knowledge that is capable of giving the appearance of an exclusive expertise and masculine security. This, it may be argued, is one of the main reasons why those offering plausible prescriptions can very soon claim a guru status. From Scientific Management to Business Process Re-engineering, the history of management is littered with prescriptive knowledge that provides the most convincing response to the demand for solutions to uncertainty. But these innovative solutions themselves promote continuous change that are threatening of routinized securities, especially given that the solutions often take the form of a fashion to be abandoned almost as speedily as adopted once a new solution emerges. In combination, these insecurities exacerbate the anxieties that we have already identified to be a feature of management and masculinity. While most innovations are comparatively harmless even though rarely delivering what they promise, the innovative financial instruments that contributed significantly to the financial crisis of 2008 clearly delivered what they promised but at an unanticipated very heavy cost to Western economies.

The financial crisis

Banks have never been the most popular of institutions but in 2008 they exceeded themselves in offending almost everyone through high risk lending policies. In addition, the accumulation of securitized and re-securitized debts in the form of Collateralized Debt Obligations (CDOs) and their insurance through Credit Default Swaps (CDS) eventually resulted in many banks becoming financially vulnerable as these toxic assets became untradeable. No one could imagine that institutions traditionally seen as following the conservative standards of probity, risk aversion and stability could find themselves in such a financial crisis as to become dependent on financial aid from their nation states.

The crisis had its genesis in the rise of defaults in subprime mortgages in a falling housing market in the US, which exposed the loans that had been bundled into securitized packages traded worldwide and fuelling an enormous growth of credit. It may be added that subprime lending originally was stimulated by the ‘affirmative action’ elements of Carter’s Community Reinvestment Act (1977) and Clinton’s reinforcement of these in the 1980s as part of good intentions to improve race relations and community disorder through social and economic policy. 7 While banks have traditionally lent around ten times their assets, this debt/asset ratio has multiplied massively as a result of institutions selling their debts as securitized products in a global market. When subprime mortgage holders began to default, the provision of credit through money markets dried up. This had a domino effect in starving certain banks of the funds that they had become reliant on in financing their mortgage portfolios. As a result, large numbers of banks throughout Western economies came close to bankruptcy and had to rely on state funds to remain solvent. Once a default on subprime debts occurred and the securitized packages that had fuelled the economic boom became unmarketable, the money markets dried up as a source of funds and it was clear that the banks were under-capitalized and in need of a massive bail-out through the taxpayer. The US government brought the crisis to a head when in September 2008 it allowed the investment bank Lehman Brothers to go into administration and almost immediately afterwards was forced to bail out several large financial institutions such as the largest mortgage lenders Freddie Mac and Fannie Mae who were taken into public ownership in. Later the government had to support, to the tune of $20bn, Bank of America’s $50bn acquisition of Merrill Lynch and then had to purchase the insurer AIG at a cost of $85bn, and provide financial support for many of the retail banks. In total the financial crisis has absorbed $9.7 trillion of taxpayers funds in the US (Lee, 2009).

While the default of subprime mortgages was not a major issue in the UK, levels of personal debt had reached unsustainable proportions of over £1 trillion and UK banks had participated in reckless lending partly fuelled by trading packaged securitized mortgages both as sellers and buyers. Some of the banks had relied on the money markets rather than personal deposits as a source of finance and when these dried up in the early days of the credit crunch, they had insufficient funds to trade and first Northern Rock had to be taken into public ownership and later Bradford and Bingley, Royal Bank of Scotland (RBS), Halifax Bank of Scotland (HBOS) and LloydsTSB hadto turn to the government for finance at a total cost to the taxpayer approaching £1 trillion (Boden et al., 2009).

Whether or not the law was broken, 8 there is little question that the behaviour of many managers and ‘experts’ in 21st century financial services was of dubious moral propriety. Of the major institutions surrounding the crisis only Lehman Brothers falsified their accounts (as did Enron in 1990) in order to make their corporation seem more financially stable. As to whether the bankers are solely to blame or merely victims of conditions created by the neo-liberal cultural fascination with the ‘free’ market, government pressure on the sector not to discriminate against blacks and Hispanics in the US combined with a failure of regulation is open to question. Regulators could have refused to surrender to pressures from the financial sector for ‘light touch’ regulation and we believe that the neo-liberal political consensus played a significant part in sustaining a faith in financialization 9 as the key to economic growth in post-colonial Western economies.

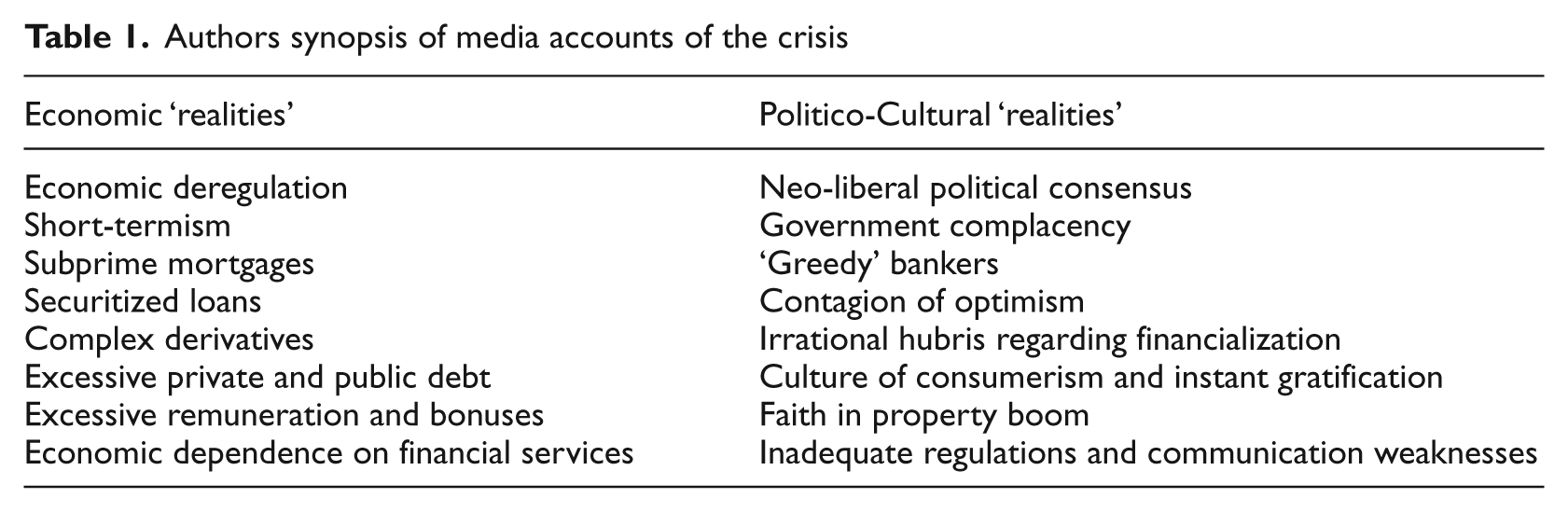

There are numerous explanations for the financial crisis that has wreaked havoc in global economies in the late noughties and these could be classified in different ways but here we simply divide them between what may be seen as ‘realities’ belonging to the economic sphere contrasted with those relating to political or cultural life (see Table 1). These are a synopsis of various accounts that the authors have discerned from extensive readings in the media. There were, at the time of the crisis, certain feminists who sought to attribute the crisis to the comparative absence of women in senior management (Economist, 2009) and while we are sympathetic to the demand for greater gender equality, we are not convinced that more women per se would have averted the crisis since they have not tended to erode the dominant masculine discourse. The Economist found ‘no empirical link in any direction between sex equality and susceptibility to the financial crisis’ (Economist, 2009).

Authors synopsis of media accounts of the crisis

While these are drawn largely from media accounts or political pundits and should not therefore be seen as providing sound academic explanations for the crisis, they are indicative of a continuing consensus that regulation to eradicate or diminish significantly these conditions will resolve any future crisis tendencies. An academic interview survey of practitioners in the sector tends to replicate much of what is being said in the media (Ashby, 2010). Despite numerous possible causes of the crisis, he concludes that there were three central problems in the views of his respondents: human/cultural, communication and regulatory/supervisory weaknesses. Ashby argues that by correcting these weaknesses future crises can be prevented but one is bound to ask how such lessons were not learned from previous crises. One of the features that is acknowledged but not explored in much detail in accounts of the crisis is the neo-liberal political philosophy of an extreme faith in ‘free’ and ‘efficient’ markets that was both a condition and consequence of economic deregulation in the 1980s. This was a more or less universal trend that spread throughout all Western and many Asian and Eastern economies stimulated by New Right politics and economics that became known as Reaganomics and Thatcherism. Perhaps a good reason for this comparative absence of a critical discourse on neo-liberalism is that with the collapse of the Soviet Union and the adoption of market principles in China, there is no publicly available, alternative discourse. While neo-liberal faith in the free market should not be ignored neither should the alternatives suggested here that revolve around diversity, gender, feminist and postcolonial theory and, in particular discourses of masculinity.

There have been a limited number of feminist based journalistic accounts that have attributed the crisis to the asymmetrical predominance of men in senior management (Observer, 2009). As we shall indicate shortly, the mere presence of women even at the very top as CEOs is no guarantee of the demise of masculine discourses partly because in climbing the greasy pole women need to subscribe to them. It could be that if women had an equal representation to men in senior management here this would change but we can only speculate.

All of these features of the financial system can be seen to have contributed to this 20th/21st century boom and bust nightmare but what is completely ignored is any sense that discourses and practices of masculinity may have played a significant part. We believe that one of the ways in which masculine discourses have contributed to the crisis is in its relationship to the preoccupation with excessively high salaries and bonuses. We turn to some general data on chief executive salaries to illustrate our thesis here. There is little question that in a materialistic Western capitalist society, everyone is somewhat preoccupied with wealth and income. This is simply part of fixing the autonomy of the self against the reality of its continual erosion. We are all engaged in this attempt to secure the image we have of ourselves through elevating it above others whether in the form of power, status or wealth. However, our point is that high levels of pay and bonuses (certainly a contributing factor in the crisis) is a particular concern of managers whose masculine superiority is increasingly threatened on a number of fronts—managerial visibility, dearth of predictive knowledge, and feminist challenges. The visibility of managers and a more sceptical and discerning media and society persistently places management (particularly the most senior) in the firing line of public scrutiny and criticism. At the same time, as discussed earlier, management knowledge has not kept pace with these changes such that it is not any more reliable or predictable than in the past. The challenge from feminism has not just resulted in more women competing for managerial positions but has threatened masculine discourses in more subtle ways in questioning managerial prerogative and patriarchal authority. As a result masculine identities have become even more fragile than hitherto and one response is for managers to seek other signs of superiority—large salaries and bonuses being one such possibility.

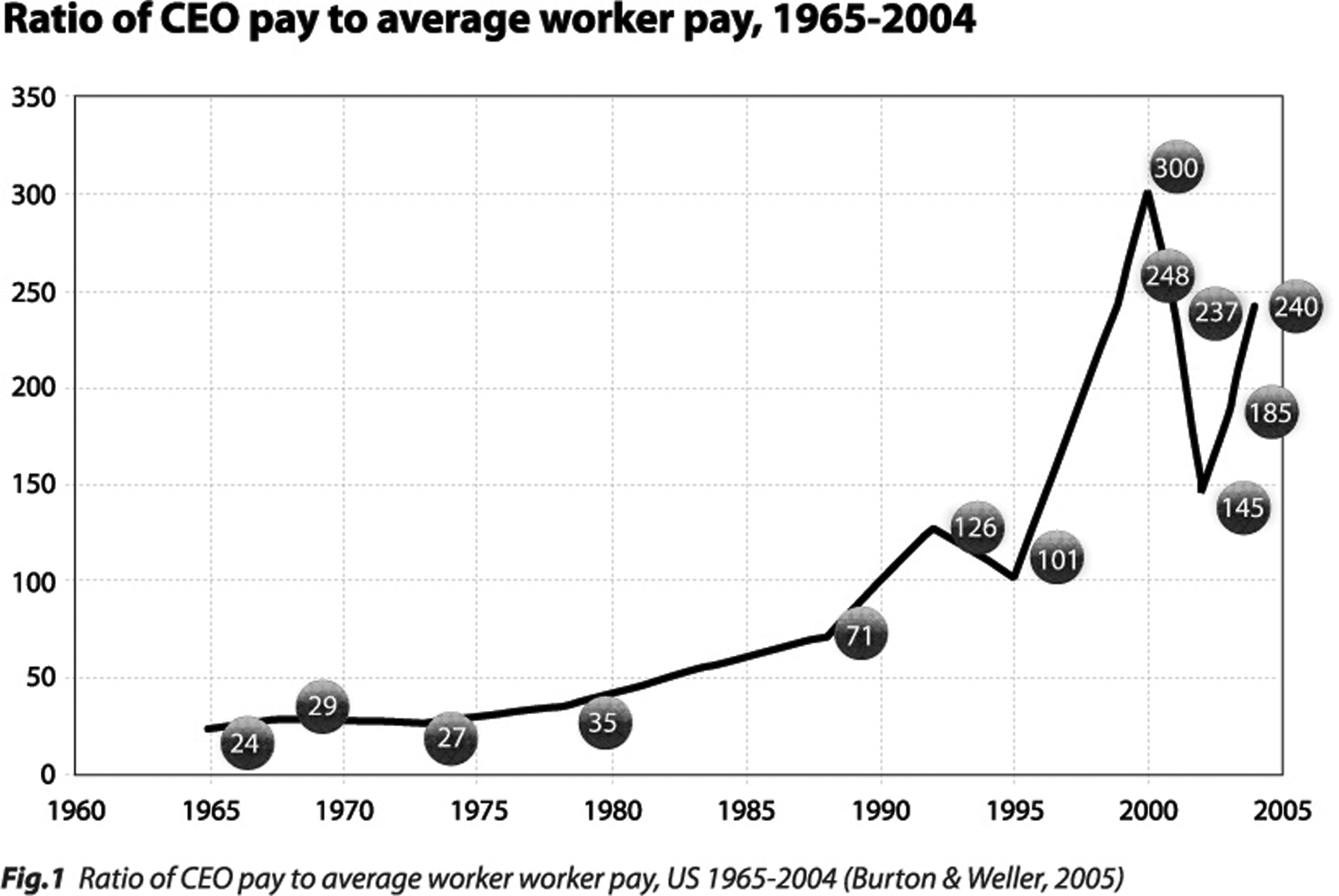

It is true that in the financial sector it is not just managers but also traders who are captured in the demand for excessive pay. We have two things to say about this. First, it has been demonstrated that traders feel intellectually inferior to analysts (Blomberg, 2009). This would contribute to their insecurity and may help to explain their preoccupation with high levels of remuneration. Secondly, when traders get big bonuses this benefits managers since their pay is usually linked to the profits from trades. What is significant for our thesis is that the income of senior executives increased dramatically during this period for as ‘adjusted for inflation, CEO pay skyrocketed 480% between 1980 and 2003’ (Burton and Weller, 2005) but increased dramatically in the mid 1990s (see Figure 1).

Ratio of US CEO pay to average worker pay, 1965–2004 (Burton and Weller, 2005)

Figure 1 shows that in the United States the average pay of CEOs compared to that of an average worker began to rise at a faster rate in the mid-1980s and much more dramatically after 1995. After the dip due to the recession in 2000 the rate of change in the gap again resumed the same proportions as prior to the recession. We realize that this data is only vaguely connected with our focus on the financial crisis but the steep rise in CEO pay coincides precisely with the period of an intensification of the financialization of Western economies and the proliferation of new financial instruments such as Collateralized Debt Obligations and their insurance through Credit Default Swaps that eventually were to implode. It was also a period when governments (especially in the UK) were convinced that the growth of financial services could stimulate the economy sufficiently to render the economic cycle of booms and slumps a thing of the past.

After the crisis, the British Prime Minister, Gordon Brown, became a late subscriber to the view that markets are not the self-regulating and efficient mechanisms that the New Right consensus and he had previously presupposed. He argued that ‘a new economic philosophy would replace the “unbridled free market dogma”, which had been discredited by the financial crisis’ (Boden et al., 2009). Yet that same support for the ‘free market’ fuels the policies of all major Western governments as they engage in massive public borrowing to restore the ‘free’ market that all but collapsed because there was too much freedom. So the cure for ‘casino capitalism’ (Strange, 1997) would appear to be more of the same. Throw public money at banks that failed to take ‘good’ care with our money in the first place and create more rules and regulations to constrain their foolish behaviour. There is even the same mentality of individual material self-interest or what is generally understood as greed that fuelled the bonanza of bankers’ bonuses creeping into the solutions for increasing the performance of regulators. 10

In the context of the failure of these highly paid bankers, it is surprising that a part of the establishment wants to emulate the same excessive remuneration packages in the public sector rather than challenge the presumed link between pay and performance. Prescribing for the public sector precisely the same reward system that has played a significant part in wreaking havoc in global economies is beyond belief. Apart from attributing to advocates of such policies some kind of mental aberration, we believe the only explanation is to be found in discourses that drive these men and indeed some women to be obsessive about financial rewards partly as a means of resisting threats to their masculinity and authority as managers. For it is our view that high earnings have less to do with performance and productivity than with managing the insecurity of managerial and masculine identities through seeking to be at the top of the material and symbolic hierarchies that constitute our patriarchal class system.

For the public sector it is unlikely that the high earnings of the private sector could be matched but even if they were, the evidence suggests that there would be no guarantee of securing the kind of expertise claimed to be necessary for regulators to be one step ahead of, or able to stand up to, the bankers. For expertise has traditionally been perpetrated simply to legitimize material and symbolic managerial and masculine privileges. As discussed earlier in the article, such managerial expertise is a myth since there is no secure knowledge upon which it could be based (MacIntyre, 1984/2003:88). While new regulations may be necessary, however, they are unlikely to be sufficient to prevent crises in the financial sector from re-occurring.

Swedish scandals

In this section we draw on some vignettes from Sweden, which we consider reflect some of the excesses of masculine discourses and practices as well as the inability of managers in the financial sector to be sensitive to the public anger, which has followed because of the damaging consequences of their actions. Part of this insensitivity is their narcissistic sense of being distinctive and special, deserving of huge economic rewards because of the risks they take, but only subconsciously are they aware of the necessity of the big salaries and bonuses as evidence of their superiority. Early in 2009 the economic crisis was the main item on the agenda within the media—there was a global storm, which nobody seemed to be able to control, fully explain or understand. The Swedish state finances were in better condition than in most European countries but the finance sector was vulnerable. The Swedish banks and pension funds were affected by the problems in the US, the UK and Iceland although not because of any direct investments there or involvement with the subprime mortgage market. The main problem for Swedish banks was their development of excessively risky loans to the Baltic countries that began to default at the time of the global crisis. Also, the export industry suffered seriously from the declining markets in the US and Europe, the stock market dropped, the pension funds were drawing back earlier returns and for the first time the pay out from the state pension was reduced. The headlines were of two kinds, either about another bankruptcy, rising unemployment figures, reduced finance for schools, or they were about certain individuals aggrieved about having to take smaller or no bonuses on top of their very high salaries or how to secure large additions to their pension funds. Every now and then a new scandal among senior business managers is exposed, but due to the financial crisis a more focused examination of senior executives has revealed a culture in which the business class elite mutually reward each other on a level that seems to be just plain fantasy. Within the business elite in Sweden interlocking directorships but more importantly the fact that everybody knows everybody else means that awarding others high pay can eventually benefit oneself through informal norms of reciprocity. But what caused a real shock among the employed, the shareholders and media journalists was the obvious incapacity among top management to connect their own behaviour and situation to what was going on in the society, acting as if they lived in a completely different world. For when large swathes of employees were and are losing their jobs, many pensioners were and are having their income cut dramatically because of depleted investments and reduced income from savings, and others suffering the possibility of property repossession due to redundancy, it seems hardly credible that the richest section of society were and are awarding themselves large increases in remuneration.

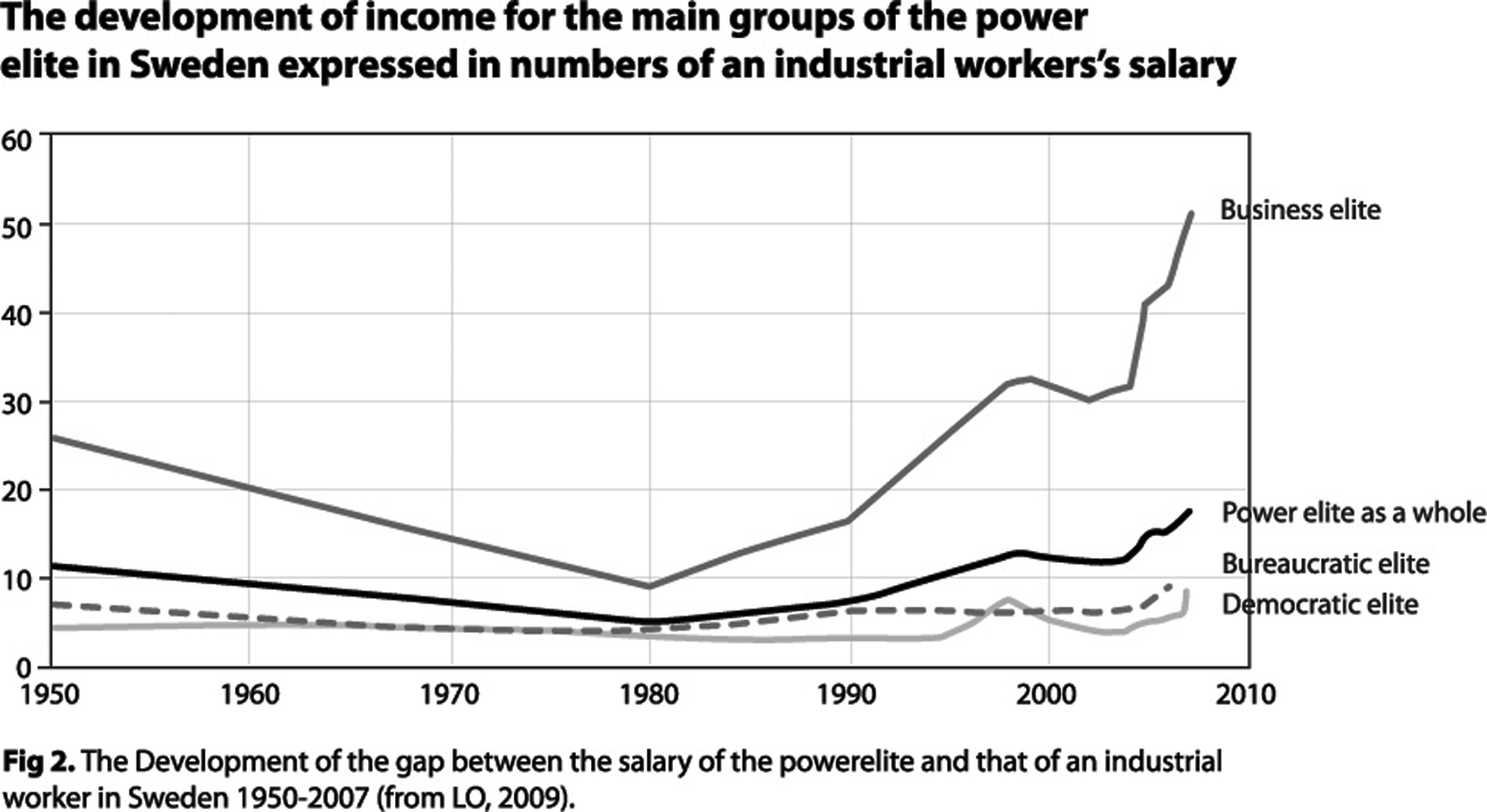

Information regarding the high levels of income among senior management is nothing new but the income gap has been steadily widening whilst the proportion of pay deducted in tax by the wealthy has been falling. The latest statistics demonstrate that CEOs in 2007 earned on average 51 times a worker’s wage, compared with 1950 when the ratio was about 25 to 1 (LO, 2009). However, a manager in the financial sector working for private equity or investment companies might have a multiple of several hundred’s of an average employee’s salary. The pension benefits are not included in these statistics, nor are the significantly reduced tax rate on high incomes that has evolved over recent decades. The gap is becoming wider at an ever-increasing speed.

The graph from the LO-report (2009) (Figure 2) illustrates the development of the income gap between the elites and the shop floor industrial workers. The upper curve represents the business elite, the lowest one the democratic elite (government, parliament) and the dotted one, the bureaucratic elite (the senior management in the civil service). The second curve from the top shows the average of the entire elite. The figure demonstrates the development towards more income equality from 1950 to the beginning of the 1980s and then it goes into reverse, due largely to the neo-liberal economic consensus, the development on the stock exchange and a turn in Sweden from a Continental-European attitude to a more Anglo-American one. In international comparisons Sweden and Britain are among the countries with the most marked change, for only the Netherlands have increased the gap more rapidly (LO, 2009).

LO Report 2009

In late February 2009 an individual and personalized ‘bonus case’ hit the headlines. The government had offered a guarantee system for the banks where one of the conditions of joining the system was to cancel all kinds of managerial bonuses. Only one of four banks joined the system, the others refused on the declared basis that the EU had set too high a price. The media, speaking on behalf of what it felt was public opinion, claimed that the real reason for refusing the government guarantees was a disinclination to cancel all bonuses—an explanation of course heavily denied by senior bank executives.

Pretty soon the situation became more difficult for the banks due to the prospect of large losses in the Baltic area as Eastern Europe began to feel the ‘cold wind’ of the recession in the West and therefore the state guarantees became more attractive if not essential. New issues of shares were planned since capital ratios needed to be raised to cope with recession-led defaults. At the beginning of March, just before the Annual General Meeting, the CEO for the bank SEB (one of the main banks in Sweden) gave a press conference and informed the public about her decision to deny herself a bonus. ‘I want the focus to be on the bank, not on my remuneration’, she said.

At the Annual General Meeting this message was repeated, but still the Chair of the Board as well as the CEO wanted to convince shareholders of the bank’s impressive performance during the year, despite the upcoming financial crisis— ‘We have a performance culture’, the CEO said. The new issue of shares was just a move to get extra security but was claimed to be the reason forthe withdrawal of dividends in that year. Tax wise the shareholders would be better off this way, the Chair emphasized. It was important now to be careful with the resources, to keep the money and to work even harder with the cost structure. In addition it was important because the bank now wanted to be able to co-operate with the government now that the conditions from the EU were less onerous. The CEO underlined that she was very happy that the bonus program had been cancelled, because now the focus was on the bank again.

Later news broke that completely contradicted her rationalizations. A daily newspaper announced that at the same time as the bonuses were temporarily suspended, the senior management had secured a wage increase for 2009 up 25% on 2008 rates of pay. At first there was little reaction from the bank representatives. The Chairman just declared that these figures would become public in the next annual report in 2010. This response soon became untenable as the media informed the public that the CEO would now have a fixed wage of about 9 millions instead of 7 million Swedish Kronas (SKr). The public reaction was disbelief and even the Prime Minister and the Minister for Finance condemned the decision to raise salaries at a time of economic crisis. The latter talked about ‘the obvious greediness in human nature’ and that it now was out of the question to let the bank join the guarantee system. This behaviour was against the rules. The Chair of the Board, from a well-known family of finance and a patriarch according to McDowell’s (1997) categories, tried to explain and defend the decision about higher wages to the media. From his point of view the new salaries were in fact a decrease and part of an entirely new system of rewards, ‘but if the government has another opinion we of course have to discuss with them’. The tone was humble, but not humble enough. The scandal grew and finally the CEO herself had to agree to give an interview on television, early on the Saturday morning (TV4, 14 March 2009). She regretted the development and said that ‘we have made a mistake, we have failed to communicate … ’, as if it were merely a failure of communication. ‘We have failed to explain so people can understand … ’. This was, of course, to underestimate people at best and seen as wholly condescending at worst. People, many of them customers in the bank, understood very well, as did the government and some days later the Board had to back off, finally realizing that they had to respond to the critics. Wages were then frozen for the year 2009.

Parallel in time with the bank case there were several other decisions unmasked about bonus and/or pension benefits and which strongly demonstrated that among the business class elite there were no plans for taking any personal responsibility for the severe situation in the financial markets and the wider economy.

One was the case of AMF Pension and where the Vice CEO (the former CEO) and the Chairman were the main actors. AMF Pension (‘Labour Market Pension Insurances’) is an institution for investing the pension capital of employees across the nation and is managed jointly by the unions and the employers’ federation. AMF Pension administers the largest part of the occupational pension investments in Sweden and much of the capital is placed there automatically due to employee inertia or limited understanding of financial markets. Like most investment companies, this institution had a very bad year in 2008 due to the financial crisis. So bad, that they had to draw back about 8% of the pension capital.

In early spring 2009 it become clear that some months before this decision was taken and the pension holders were informed about it, the vice CEO had transferred his own pension capital of 33 million SKr out of the institution to what he considered to be a safer place, to another kind of account. He refused to give an account of this action arguing that this was his private savings and seemed quite annoyed at the demands for explanations or comments. He claimed that the legal advisors had said it was OK and that he hadn’t done anything wrong. When journalists began investigating his affairs more closely it also became evident that he had received large extra pension benefits over the last few years, as he was very close to retirement. On a wage of 4–5 million SKr plus bonuses he had a pension investment of more than 9 million during the year 2008. Very soon the main issue turned to the question of how these figures could be possible in an institution where the Chair of LO (The Swedish Trade Union Federation) was a member of the board. LO had for several years been criticizing excessively high wages, bonuses and redundancy payments for managers but was that only lip service? The media turned to questioning the Chair of LO, a woman. She become very upset and defended herself saying that she didn’t recognize the figures, that she hadn’t got that information and that she didn’t know that all this money was for such a short period of time. The focus in the media turned from the high remuneration and the unethical behaviour of the vice CEO and instead the woman Chair of LO was made a scapegoat, accused of being not competent enough, too caught up in the power of the establishment and too busy in too many other boards to represent her own organization properly.

Later on it was revealed that the very generous contract with the Vice CEO was constructed outside the board in the remuneration committee and then presented in a very superficial way to the board. The Chair of LO seemed to have the right to be upset. Moreover, the other representative from LO in the AMF Pension board, a man, was a member of the remuneration committee but the media didn’t question him and the story died. Less than one year later another woman board member told her version of the AMF Pension story in a book (Lindsö, 2010) in which the vice CEO and the Chair of AMF Pension also are accused of an ‘old boy network’ collusion. Up to now (December 2010) no public denial of this has been reported.

These vignettes not only demonstrate the ‘grab as much as you can mentality’, but also the obvious incapability of understanding and even less of predicting people’s reactions. The response of senior management seems to be pure surprise that their mere compliance with the letter of the law is not sufficient to assuage the public. Is it perhaps some narcissistic sense of being special, of being better than ordinary mortals as evidenced by their levels of remuneration that leaves them oblivious to public anger about the high salaries and bonuses that are continuing even after their companies have been bailed out by the taxpayer? There is certainly no show of remorse or commitment to public expectations of higher ethical standards from the economic elite. The vignettes also show how women have to subordinate themselves to the values of hegemonic masculine discourses but also that they are not protected by the homosocial male network where, at least in the AMF Pension case, gender prove to be more important than class.

Summary and conclusion

In this article we have sought to examine the various accounts that have arisen to make sense of the global financial crisis of 2008. A multiplicity of accounts has been documented in the article and it is clear that none of them can be entirely ignored. However, we have focused on two accounts—one that has been acknowledged but the other that has not. The first is the neo-liberal consensus and its support for so-called free markets grounded in individual or institutional economic self-interest. This has been recognized as a problem but solutions to the crisis have rarely challenged its hegemony in all things economic. Also identification of the problem has been fairly superficial in the sense of merely questioning whether markets are always efficient but failing to explore deep seated flaws in their construction. One of these is the presumption that individual economic self-interest is socially valuable because of the ‘hidden hand’ or what may now be described as the unintended beneficial aggregated consequences of individual action. Even Adam Smith (1793/1976) who coined the term ‘hidden hand’ was fully aware that market relations depended on behaviour meeting high moral and ethical standards. These ethical standards are conditioned by and a consequence of individuals recognizing their social interdependence rather than treating interestsas ‘internal to the self’ (Roberts and Jones, 2009: 858). Generally those trading in securitized products such as collateralized debt obligations (CDOs), Credit Default Swaps (CDS) and the numerous other sophisticated financial instruments seemed to have lost sight of the sense in which the self is a social not an individual formation and that interests cannot be separated off from and treated as independent of the network of social relations in which they are embedded (Roberts and Jones, 2009). As we have sought to demonstrate, this self-interest does extend beyond theindividual to the group that can sustain class, gender and racial privileges.

The second account but one entirely neglected in conventional interpretations relates to gender and more specifically, discourses of masculinity. An analysis of masculine discourses and identities indicates how they have affected management and traders in such a way as to exacerbate their risk drenched self-interested behaviour. We have argued that one of the pervasive characteristics of masculine and managerial identities is the degree to which they exhibit high levels of insecurity largely because both are dependent on a social recognition and confirmation of success in strongly competitive conquests as well as skill in controlling events. Due to the limited knowledge and unpredictability of business life, masculine and managerial identities are extremely fragile and precarious. We have suggested that this fragility has resulted in men and some women pursuing an ever-increasing spiral of material rewards since high salaries and bonuses can serve as a proxy for the social recognition that is so elusive and precarious. As we have suggested, there is a sense in which managers in the financial sector see the high salaries and bonuses as their entitlement for the risks they take with other people’s money but then the level of remuneration becomes in its turn evidence of their distinctive and special status. It also helps to sustain if not fully secure their masculine identities. Without it they would revert to being ordinary mortals indistinguishable from the mass of the population; hence the determination to preserve their bonuses despite having wreaked havoc on society and being subject to widespread public criticism.

We have been drawing on gender theories of masculinity and in particular gender as a performative act. Yet if gender is an act, a play, it is an act not just on a theatre stage but has consequences for the practices of everyday life. One of these consequences, we argue, is a management preoccupation with outward signifiers or symbols of success and superiority. This preoccupation manifests itself in the excessive salaries and bonuses exposed by and partly responsible for the financial crisis. The bonus scandals that we have referred to are examples of male bonding, manifesting insularity from the rest of the society that they had severely damaged. Strong group norms and class solidarity effectively prevent anybody in the group breaking rank and acknowledging that the levels of remuneration are obscene.

Insofar as masculine identities are a product of performance, they are necessarily precarious since there is no ‘inevitability, universality or constancy in ‘what it means to be a man’’ (Kerfoot and Knights, 1996: 85). Consequently managers are perpetually and competitively driven to achieve higher and higher salaries and bonuses to secure their status as men. In these contexts, masculinity can be threatened by the mere awareness that others are paid more. Paradoxically one of the reforms designed to arrest this inflationary spiral of managerial remuneration has the exact opposite effect. Transparency of senior executive remuneration may give shareholders some ammunition to constrain their executives but it only serves to increase the importance of reward levels for managers since they know explicitly where they sit in the hierarchy of remuneration. Thus the battle for who is on top is conducted not just in the bedroom but also in every Boardroom and Board meeting where wildly excessive executive bonuses and salaries are negotiated and approved.

In conclusion, by focusing on insecure masculine identities surrounding management and trading in the financial services, we have offered a different though complementary account of the crisis that hit financial markets in 2008. So far, however, we have provided an implicit critique of masculine discourses while actually subscribing to precisely the same kind of discourse ourselves, representing the other as if we were not at one and the same time representing ourselves. In this sense, we can be seen as giving centrality to our own consciousness as possessing ‘greater or better knowledge that is gradually revealed to the reader’ (Pullen, 2006: 278). To a very limited degree, we have acknowledged our own and society’s anger in response to the damage that global bankers have inflicted on large numbers of people not least some of their own redundant staff but also because of government bailouts, on current and future generations of global citizens especially those connected with the public sector, including students. However, we are not so much in the text as gendered and embodied beings whose bodily and emotional experience (Knights and Thanem, 2005) has shaped the content and structure of our thesis. In this sense, we have been fairly authoritative and less than completely open regarding our own position in writing this narrative. In writing critically on an issue that is explicitly gendered, we have remained agendered. Thus in seeking to generate a critique of masculine discourses we may have inadvertently reproduced as much as represented them.

Although not necessarily offering new visions in this analysis of masculinity and management, as a feminist woman and a pro-feminist man we have sought ‘re-sitings and re-sightings’ (Pullen, 2006: 294) of managing masculinity. The crisis provided us with material to locate masculine discourses in different sites of the financial sector and within diverse practices such as the bonus culture, homosocial bonding to protect privileges and the pursuit of ever increasing salaries among the business elite. This gave us new in-sights into how corporations were mismanaged to the point of near collapse despite a past history of prudential solidity and cautious stability. We have also sought to avoid the conventional masculine practice of displacing all other accounts with our own as a means of securing our identities in the representations that we impose on others. In this sense we supported a multiplicity of different accounts of the financial crisis and offered our own gendered interpretation as complementary rather than as an alternative authoritative account. Deconstructing hegemonic masculinities is implicitly what we are concerned to do but the hegemony is beyond the power of one article to do more than chip away at the edges.