Abstract

This article uses a Bourdieuian notion of organizational field and social movement’s frame analysis to understand the successful legitimation project of the socially responsible (SR) mutual fund industry. We show how institutional entrepreneurs, as both insiders and outsiders of the dominant organizational field, compete with existing mutual fund logics and become a legitimate presence in the mutual fund industry. The SR mutual fund industry has grown exponentially since its introduction in the 1970s, even though the product it sells is ambiguous in nature (Wood, 2000). Thus, while the product could be perceived as subversive, as the SR industry is arguing that companies should act ‘responsible’ in their efforts to make money, the reality is that industry innovators do not disrupt the existing mutual fund logic of ‘fiduciary responsibility’ in order to legitimate themselves. Rather, SR institutional entrepreneurs use their social location in multiple organizational fields to argue that consumers can ‘make money while doing good’. Such a frame is not completely subversive nor completely compliant with the existing logic, yet it successfully appeals to both mutual fund insiders and social movement outsiders.

Keywords

Legitimacy of a new organizational form requires political mobilization and resources by institutional entrepreneurs. Innovators must carefully craft organizational language and patterns of behaviors to extract the values, beliefs and ideas that are currently fashionable (Suddaby and Greenwood, 2005). Indeed, Rao and Giorgi (2006) call institutional entrepreneurs ‘ideological activists’ because they are skilled social actors who can negotiate social reality and convince others to adopt the new institutional logic they are offering (Fligstein, 1997). An important assumption in the institutional literature is that successful innovation comes from institutional entrepreneurs who are either insiders or outsiders within an organizational field (Thornton and Ocasio, 2008). For example, Reay and Hinings (2009) argue that the dominant cultural logic within the medical field transformed when outsiders from the government forced new rules and regulations upon the health industry that insiders then had to negotiate. On the other hand, Creed et al. (2002) claim that insiders were able to transform gay and lesbian work policies when employees adopted and employed social justice frames into the workplace. Such arguments imply that insider and outsider positions are mutually exclusive. We argue, however, that successful innovators are likely to be mobile across organizational fields. Therefore, they are both insiders and outsiders to any given organizational field. Further, we argue that being both an insider and an outsider enhances one’s ability to innovate by providing one with alternative institutional logics from which to draw. We show this by examining the socially responsible mutual fund industry; an industry that cannot guarantee to its consumers that it is actually selling the ‘socially responsible’ investments that it claims to be selling (Entine, 2003, Markowitz, 2007).

Legitimacy is ‘a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions’ (Suchman, 1995: 574). The legitimation project that new forms undertake entails considerable framing work. Institutional entrepreneurs must diagnose an absence in existing goods and then convince the public that their new product provides the solution for this lacuna in the market (Campbell, 2004; Rao et al., 2000). The question is, from where do these new frames come? Do they emerge simply from the creative impulses of institutional entrepreneurs or do they reside outside them within the structural realm (Schneiberg and Lounsbury 2008)? We argue that the successful legitimation project of the socially responsible mutual fund industry brings forth an interesting revelation: institutional entrepreneurs, who are occupants of multiple institutional fields, draw on resources and imagery from their social locations to develop innovative frames. This is particularly interesting within the socially responsible mutual fund industry as the industry has little to offer consumers that differentiate it from existing products and competitors. We make our argument by applying a Bourdieuian concept of organizational fields within the neo-institutional literature (De Clercq and Voronov, 2009a, 2009b; Emirbayer and Johnson, 2008; Lounsbury and Ventresca, 2010) and by synthesizing them with concepts from social movement theories. Innovation, then, comes from creative entrepreneurs, but entrepreneurs who pay great attention to the social structures and contexts that influence and shape their innovation (see Lounsbury and Ventresca, 2010).

Institutional fields, logics and the insider/outsider dilemma

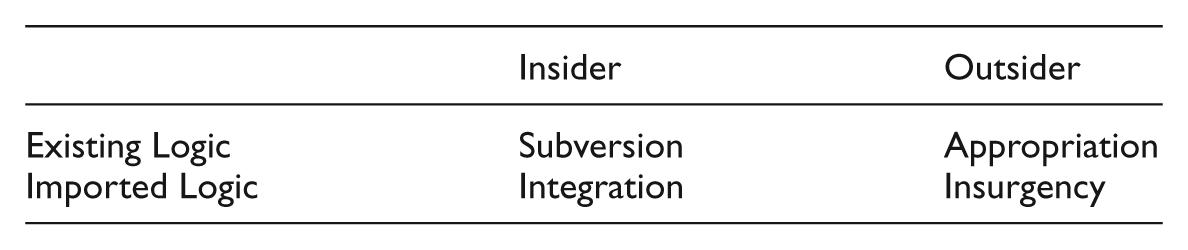

In trying to explain how new cultural logics emerge, Rao and Giorgi (2006) suggest that all current logics have contradictions that allow innovators to exploit fissures, a process they call ‘code breaking’, and introduce new organizational forms. They make the case that cfode-breakers are innovators who, as insiders to the dominant organization, morph existing logics or integrate new ones and, as outsiders to the organization, appropriate existing logics or import new ones. Rao and Giorgi (2006: 273) define insiders as, ‘one who started in a focal industry and is a member of the focal industry, and is perceived by industry critics to be part of the focal industry or domain’ while outsiders are the opposite. The code-breakers, as either outsiders or insiders, then create framing strategies around those new logics; successful frames legitimate the new codes and, hence, new organizational forms survive. Their matrix appears to offer four mutually exclusive categories to understand code-breaking and entrepreneurs’ legitimation practices. While they provide only ideal types, they do not offer any statement about the possibility of hybrid forms. Further, their use of exemplars for each quadrant, does not attend to the conceptual ambiguities that forms, such as socially responsible mutual funds, raise.

Their matrix appears as follows (see Rao and Giorgi, 2006: 273):

Our problem with the matrix developed by Rao and Giorgi is that it assumes institutional entrepreneurs act only as ‘insiders’ and must either subvert or integrate existing logics or as ‘outsiders’ and must either appropriate or act as insurgents. We contend the process may be far more muddled and dynamic, particularly for hybrid forms. Alternatively, Emirbayer and Johnson (2008) and DeClercq and Voronov (2009a, 2009b) draw on Bourdieu and provide analyses of how power relations and social interaction lead to mixed approaches, whereby entrepreneurs are members of multiple organizational fields and thus are both insiders and outsiders who use existing institutional logics from several fields to legitimate themselves as true innovators. Habitus alone may be insufficient for understanding these relationships, by adding an analysis of fields we can understand how these systems dynamically address needs, frameworks, and ideas (Bourdieu, 1990). Bourdieu’s work on habitus and organizational fields are particularly useful for examining legitimation in contemporary hybrid forms (1977, 1984).

The concept organizational field, as introduced by Bourdieu (1977, 1990), has been borrowed and expanded by many neo-institutional theorists (Reay and Hinings, 2009). Emirbayer and Johnson (2008) argue, however, that the fundamental meaning of the term has been lost through repeated usage. While Bourdieu (1990), for example, envisioned fields to be defined by their changing, organic nature, many scholars use the concept field to explain why organizations are isomorphic and loath to change. According to Emirbayer and Johnson (2008) an organizational field is characterized by both structure and interaction. It is ‘a terrain of contestation between occupants of positions differentially endowed with the resources necessary for gaining and safeguarding an ascendant position within that terrain’ (2008: 36). This constant vying for power is what provides fields with their fluid potential. The context for challenges to existing logics is potentially riddled with contradictions and competing logics within a heterogeneous field (Schneiberg and Lounsbury, 2008). Moreover, Bourdieu (1984) suggests decision-makers draw on multiple models of rationality in these dynamic environments.

It is indisputable that fields have logics that embody norms, values and practices which serve to reproduce the organization and provide meaning to occupants (Thorton and Ocasio, 2008). Institutional logics help define the field and maintain stability (Reay and Hinings, 2009). Indeed, as De Clercq and Voronov (2009a, 2009b) argue newcomers to a field must ‘fit in’ and respect the current institutional logic before they can legitimately initiate change. However, fields also have occupants who use a variety of resources (in the language of Bourdieu these resources are symbolic, cultural and economic capital) to ‘stand out’ and change their power relations within the field (De Clercq and Voronov, 2009a, 2009b; Emirbayer and Johnson, 2008).

Bourdieu’s work suggests that neo-institutional theorists should focus on the location of the resources that innovators use to generate change and recognize institutional entrepreneurs’ embeddedness. We know that successful innovation requires skilled social and political actors (Fligstein, 1997), but from where do they draw their resources? In the present project, we argue that change comes from the reality that all institutional members occupy multiple organizational fields (family, religion, social movements), each with their own institutional logic, some overlapping more and some overlapping less (De Clercq and Voronov, 2009a; Emirbayer and Johnson, 2009; Reay and Hinings, 2009; Thorton and Ocasio, 2008). As Thorton and Ocasio claim, ‘institutional entrepreneurs creatively manipulate social relationships by importing and exporting cultural symbols and practices from one institutional order to another’ (2008: 115).

If we conceptualize organizations as populated by individuals who exist in multiple organizational fields, then we view these individuals as accessing institutional logics from multiple fields. Except, perhaps, in the case of inmates under the all-encompassing control of total institutions such as asylums and prisons (Goffman, 1962), individuals are always both insiders and outsiders to any given organizational field. To greater or lesser degrees, then, the resources that occupants use to ‘stand out’ (De Clercq and Voronov, 2009a, 2009b) may be both subversive and integrative and/or appropriative and insurgent, depending on their positions within the multiple fields to which they belong. We believe using the model by Rao and Giorgi with more explicit recognition of the need for multiple contrasting strategies (De Clercq and Voronov, 2009a, 2009b; Emirbayer and Johnson, 2008) provides a more nuanced approach. In particular, we contend that entrepreneurs may consist of insiders and outsiders engaged in the same legitimation project. Likewise, legitimation projects may not fit neatly into one analytic category.

We will show below that successful SR mutual fund companies fit complexly in all four categories of the matrix developed by Rao and Giorgi (2006). More specifically, we claim that innovators appropriated/integrated the ‘rational-legal’ framing of traditional mutual funds, while also using the logic of insurgents to subvert this frame with the adoption of a ‘socially responsible investor’ identity frame. This ‘subversive’ identity frame connects the emergent organizational form with an identifiable outsider, the world of social activism. We argue that part of the explanation for the SR activist identity frame specifically lies in the uniqueness of the good it is offering; it is selling an ambiguous product. Unlike producers of automobiles and beer, SR mutual fund companies cannot guarantee to their consumers that the mutual funds they sell are ‘actually’ socially responsible. The ambiguity of the product forces us to understand the appeal to an activist identity in the legitimation project of the SR mutual fund industry. As a result, we must unpack how two seemingly distinct cultural logics successfully come together to generate a new frame, a new frame that helped a new organizational form emerge and survive.

Frame analysis

Recognizing the ambiguity of their product, SR entrepreneurs have turned their attention to the consumer and sought to attract market share by creating the ‘SR investor’ as a social identity. All organizations work with categorization systems and, as others have demonstrated, coding or categorizing mutual funds has been at ‘the heart of how mutual funds companies and consumers have made sense of the variety of funds’ (Lounsbury and Rao, 2004: 972). However, categorization is but one result and/or facet of entrepreneurs framing activities. SR entrepreneurs must engage in framing that not only legitimates the new product but also firmly entrenches the fund within the socially responsible category. Categories are identity markers and serve to distinguish the product while also ‘blending’ with others in the industry (Lounsbury and Rao, 2004). Thus, attempting to attract both activists and simply concerned citizens alike to take on this identity, SR entrepreneurs have applied framing strategies (Snow et al., 1986) designed to represent the purchase of shares of their particular funds as a socially responsible act.

While Snow and colleagues (1986) applied frame analysis to social movements, the original theory comes from Goffman (1974) and is a general one. Goffman viewed frames as ‘schemata of interpretation’ (1974: 21) which condition social action and interaction. Given adequate understanding of a given frame, one can communicate it in attempts to influence the action of others. To emphasize this point, Snow and Benford (1988, 1992) define frames in terms of beliefs that motivate and legitimate social action. Benford (1993) identifies diagnostic, prognostic, and motivational frames as a relevant typology. Diagnostic frames identify a perceived problem with the status quo, prognostic frames identify social action that may solve or minimize the affects of this problem, and motivational frames seek to encourage a constituent public to get involved.

Like social movement frames, the organizational frames we deal with here are constructed via competitive processes in which opposing factions contest relative legitimacy (McAdam et al., 1996). In such framing contests, social movement leaders and organizational innovators alike seek to distinguish their frames from the status quo through boundary framing (Hunt et al., 1994), the establishment of symbolic boundaries between themselves and opponents. Further, the strategic goals of innovators may involve frame extension (Snow et al., 1986), the insertion of an innovative frame into social territory occupied by others.

Underlying this logic is the recognition that frames exist within discourses and, therefore, in relation to interactional contexts. They are socially constructed via framing processes and responsive to these contexts. Organizational fields provide the context by generating cues, which Goffman referred to as ‘keys’ (1974: 45), which locate a frame’s meaning within the field’s institutional logic. As frames are communicated across organizational fields, the keying and rekeying of frames creates a layering effect that Goffman refers to as ‘lamination’ (1974: 82). Thus, when a frame is communicated from one organizational field to another, it arrives as a logical potential open to rekeying by cues provided in the new organizational field. When the rekeyed frame is communicated back to the original field, it arrives as a new logical potential which has been modified by keying from the second field. It is helpful, therefore, to think of frames that are communicated across organizational fields in terms of potential meaning rather than literal meaning.

We discussed above how legitimation is a political process in which institutional entrepreneurs uncover the normative values of society and capitalize on them. We further discussed how rationality and identity-building are two legitimating strategies in contemporary U.S. society. We contend that SR institutional entrepreneurs gain legitimacy for the ambiguous product they offer in three ways. First, they draw from the existing institutional logic by adopting the rational myths and ceremonies of conventional mutual fund companies. This fits with the Rao and Giorgi matrix in that some innovators were financial insiders who integrated the existing logic about mutual funds while others were outsiders to the field who appropriated this logic. Second, they use boundary framing to distinguish themselves from other mutual funds by integrating activist frames and emphasizing their own commitment to social responsibility. Finally, they use the framing strategies of social movements to motivate and mobilize a consumer base by extending a ‘Socially Responsible Investor’ identity frame. This corresponds with the Rao and Giorgi matrix in that social movement activists, or outsiders, acted as insurgents to challenge the entire notion of ‘investor’. This insurgency, in turn, allowed insiders to develop the subversive identity of ‘ethical consumer’ and extend it into the consumer base. What follows is a brief discussion of the emergence of the socially responsible mutual fund industry in the U.S. and its correspondent ambiguities.

Ambiguities: What is corporate social responsibility?

The US socially responsible mutual fund industry has historical roots reaching back a hundred years to the Quakers who wished to avoid investing in goods related to war (Domini, 2001). The current industrial growth in the industry began in the early 1970s, during the Vietnam era, with the introduction of two anti-war mutual funds. Yet, it did not begin to flower until the early nineties when there were sixty SR mutual funds that claimed, first, to avoid investments in such negative activities as weapons production and Apartheid and, second, to purchase stocks in such positive activities as companies with diversity policies and environmental stewardship records (Kinder et al., 1994). Today there are approximately 200 mutual funds in the US that call themselves socially responsible (Social Investment Forum, 2007).

Prior to the 1980s, the average citizen had little invested in the stock market (Friedberg and Owyang, 2002). Workers attained their wealth primarily from wages and retirement packages provided by their employers. In response to global competition, however, many businesses found it beneficial to give workers responsibility over their own retirement. Thus, defined-contribution plans soon became the norm at the expense of defined-benefit ones. Indeed, the number of workers with a 401(k) increased more than five-fold from 1983 to 1993 (Hawley and Williams, 2000: 23). Since the 1980s, then, the average citizen has had no choice but to become firmly planted in the investment world (Krumsiek, 1997). SR institutional entrepreneurs took advantage of the increase in new investors by introducing socially responsible mutual funds. Their only dilemma was how to convince workers to invest their money ‘socially’ rather than conventionally.

The broader SR industry has grown along with the swell in the mutual fund industry. In 1994, Kinder et al. reported that the industry of socially responsible investors, financial institutions, advisors and planners comprised a 625 billion dollar industry. By 1999, it was estimated to stand at more than two trillion dollars (socialfunds.com/news/article.cgi/74.html). Indeed, Amy Domini reported in 2001 that one in every nine dollars invested with professional managers was invested in the name of socially responsibility (Domini, 2001). Many SR experts, like ‘craftsmen brewers’, attend conferences, join associations and have other social networking opportunities. Further, conventional businesses have now joined the SR bandwagon. Many have directors of social responsibility sites on their webpages dedicated to publically explicating their socially responsible acts and/or are members of associations dedicated to issues of social responsibility (Wood, 2000). Clearly, the extensive time and money spent on the issue of social responsibility conveys the legitimacy of the concept. Yet, what is ‘social responsibility’ and can it really be bought and sold?

Attempts to define, theorize and measure corporate social responsibility (CSR) in the academic literature abound, yet the concept stills remains elusive (Dejean et al., 2004; Griffin, 2000; Mitnick, 2000; Rowley and Berman, 2000; Woods and Jones, 1995). Indeed, one author claims:

A fundamental problem in the field of business and society has been that there are no definitions of corporate social performance (CSP), corporate social responsibility (CSR1), or corporate social responsiveness (CSR2) that provide a framework or model for the systematic collection, organization, and analysis of corporate data relating to these important concepts. No theory has yet been developed that can provide such a framework or model, nor is there any general agreement about the meaning of these terms from an operational or a managerial viewpoint. (Clarkson, 1995: 363)

The difficulty in defining social responsibility stems from a variety of factors. At the foundation of these lies the unavoidable subjectivity of the term itself. Do actions alone evidence a sufficient condition for SR, or must ‘appropriate’ motivation back them up? For example, if a company offers donations to a non-profit organization, but does so only to reduce its tax burden, is that CSR? What if a company is the only in its industry to follow environmental standards set out by law? Moreover, which better constitutes social responsibility—a generalist approach to social justice or more idiosyncratic and issue-specific responses? Is there a difference between ‘cause-related marketing’ and CSR? Must a company’s structure and product be organized around CSR, or can responsible acts be an incidental by-product? The issue of intent versus outcome is a serious definitional problem that is still hotly contested within the CSR literature (Griffin, 2000; Wood, 2000).

Some academics intend to solve the above debate by developing a theory of CSR. Neo-classical economists argue that CSR cannot exist except through ‘enlightened self-interest’. If businesses engage in SR it is only because their financial values increase if they do. To act responsible for any other reason questions the entire existence of capitalism (Friedman, 1970). The stakeholder theory approach, however, argues that corporations are part of broad set of complex, social webs that require them to consider the effect of their actions on various groups involved, including workers, communities and the environment (Wood and Jones, 1995). The stakeholder approach, with its emphasis on multiple stakeholders, allows us to consider that corporations are not uniform in their approach to CSR. While they may, for example, address environmental hazards in one area, they may ignore them in another. Yet, the complexity afforded to us with the stakeholder approach still does not quell debate about accepted definitions and measurements.

Interestingly, much of the literature on CSR does not bother with defining the abstract construct, CSR; its existence is accepted as real. Instead, researchers have been more concerned with neo-classical economic questions about the relationship between profit and socially responsible behavior. While it seems such a question would be difficult to answer without valid or reliable measurements of the independent variable, researchers are undaunted. They use such measurements as managers’ perceptions of CSR, single events illustrating CSR, managerial intent to engage in CSR and other single and multi-dimensional approaches that are often then tied to economic performance outcomes (see Wood and Jones, 1995). Given the multiple methods used to define and measure CSR, it should not be surprising that results showing a relationship between CSR and financial performance are mixed (Mitnick, 2000).

The problem researchers have in defining, theorizing and measuring CSR affects more than the ‘ivory tower’ of academia. It is a practitioner’s problem as well. How can one claim to sell socially responsible mutual funds if there is little agreement about what actions reveal corporate social responsibility or which companies engage in it? The issue of CSR definition and measurement prompted Paul Hawken to research exactly in which companies most SR mutual funds invest. He gathered the investment holdings of the 602 world-wide mutual funds calling themselves socially responsible. He found that, ‘the cumulative investment portfolio of the combined SRI mutual funds is virtually no different than the combined portfolio of conventional mutual funds’ (2004: 15). A list of the 30 most common stocks in SR funds showed that two-thirds of the stocks were also reflected in the Dow Jones Industrial Average. Another study that only looked at the top ten holdings for SR mutual funds and a sample of traditional funds corroborated Hawkens’ results (Markowitz, 2007). Markowitz (2007) found that 70% of the holdings from SR and conventional funds were the same. Further, Hawken finds that the majority (over 90%) of SR mutual fund holdings come from the Fortune 500. Hawken argues that sloppy definitions and measurements of CSR among SR mutual fund companies have created a product that is no different from conventional mutual funds.

The above calls into question the validity and reliability of definitions of CSR and the empirical distinctions in product between SR and conventional funds. Unlike Hawken, however, we are not making a moral argument that the above information means the SR mutual fund industry is a sham and requires dramatic overhaul. Rather, what interests us about the information is how, in spite of ambiguities with the product, the SR mutual fund industry has managed to legitimate itself.

Methods

We offer a case study of the socially responsible mutual fund industry in an attempt to elaborate existing understandings of the ways in which institutional entrepreneurs enact successful legitimation projects. We believe analysis of this industry provides an opportunity to build on the work already established by DeClercq and Voronov (2009a, 2009b), Emirbayer and Johnson (2008) and Rao and Giorgi (2006). This case study design then provides in-depth analysis of seven leading socially responsible mutual funds companies that define themselves exclusively as selling only socially responsible products to consumers. Like Barnett and Salomon (2003), this effort does not focus on the moral questions regarding the relative profitability of the SR mutual fund industry.

In 2005, the Social Investment Forum provided the top ten socially responsible mutual funds in terms of assets. The companies that offered the funds were: Calvert, Citizens, 1 Domini, Dreyfus, Grantham Mayo, MMA Praxis, New Covenant, Parnassus, and Pax World, Smith Barney. Of the top ten, seven funds came from companies that defined themselves as exclusively socially responsible (all funds excluding Dreyfus, Grantham Mayo, Smith Barney). 2

We use these seven socially responsible mutual funds companies as exemplars of the field. Their status as specialists in social responsibility suggests expertise as well as ideological commitment. These companies are widely regarded as leaders in the socially responsible mutual fund industry. Moreover, these companies’ holdings include some of the largest mutual funds in terms of holdings under management. For example, Calvert and Domini are often regarded as two of the largest socially responsible mutual funds. Additionally, these mutual fund companies control billions of dollars in assets. Our logic suggests that the size of a fund’s holdings indicates that fund’s successful integration into an industrial field. It also may indicate the fund’s attractiveness to consumers and, arguably, the potential of the fund to influence corporate behavior and produce social change.

According to Social Investment Forum, there are approximately 12 social screens, These screens fit within four major arenas: environment, social, governance and products. These screens may restrict or prohibit investments in companies that pollute, violate human rights or deal with alcohol, tobacco, gambling, weapons, animal testing, etc. Barnett and Salomon (2003) have demonstrated that there is a relationship between the mutual fund company’s number and type of social screens and financial performance. Among the funds listed above, there is variation in their screening approaches. Calvert funds, for example, tend to allow ‘positive’ investments in eight categories and ‘restrict’ investments in six. There is still variation even among Calvert funds with more restrict policies among some. Calvert funds do not appear to ‘exclude’ investment options in any category. In contrast, Domini funds often have explicit restriction of investment in four categories. Similarly, Parnassus excludes investments in some arenas because of screening protocols while Pax World does not appear to do so. Although our research is not intended to offer a systematic comparison by type of screens, it is important to consider the potential influence that rigor of screening may have on the patterns evident here. In general, we offer this information to suggest that these funds are not entirely homogenous and that they are, in fact, selective in their screening, albeit to varying degrees.

A case study design is particularly useful for this line of research given our interest in elaborating existing understandings of the ways in which entrepreneurs were successful at legitimating a new form. Additionally, by focusing on a new organizational form that offers an ambiguous product with a fuzzy distinction between itself and the dominant alternative, we are able to provide a detailed and theoretically informed description of a frame that has been legitimated as a new organizational form against considerable odds. We focus on the socially responsible funds because the funds that are part of conventional fund families do not face the same pressures to legitimate themselves or their product. Their conventional status is already socially accepted, the socially responsible mutual fund is then just another option among many investment options.

We draw on multiple data sources in our analyses of these seven SR mutual fund companies with the largest funds. A primary technique within this case study design is content analysis of the websites of these seven funds focusing on discursive framing processes (see Johnston, 1995). This allows us to use comparative analysis at the level of the fund to generate descriptive analysis at the level of the industry (Walton, 1973). As we do not address questions concerning competition among funds, our focus on only the most successful fund companies is warranted. We have focused on survivors intentionally because we want to understand the details of a successful legitimation project for an industry—not a systematic comparison of the ways in which varied socially responsible mutual funds use framing as part of their legitimation efforts.

We accessed websites at calvert.com, citizensfunds.com, domini.com, praxis.com, newcovenantfunds.com, parnassus.com and paxworld.com. All information from these websites was retrieved between November 2006 and Janurary 2007, primarily, with follow-up in 2009 and 2010. In order to enhance the study’s reliability, each author independently reviewed websites, coded them, and contributed to the analysis. Content analysis of websites is particularly useful because it allows us to consider the rhetoric and presentation of themes in a static and finite setting. Given the heavy reliance of web interfaces among investors, the ways in which organizational leaders choose to present information about their funds is vital to understanding the image they seek to present and their efforts to steer the discourse to areas that provide social acceptance (Goffman, 1973). In so doing, we pay close attention to institutional vocabularies (Suddaby and Greenwood, 2005). For our purposes, institutional vocabularies include the words, imagery, and texts commonly associated with ‘distinct conceptions’ of the socially responsible mutual fund industry (Suddaby and Greenwood, 2005: 43). We also use archival data, particularly media interviews with institutional entrepreneurs and critics and other news stories published about the rise of socially responsible mutual funds.

Furthermore, we consider the extent to which there is commonality in presentation among these mutual funds as well as possible similarities and differences relative to conventional mutual funds. As we analysed data, we considered the claims on each website to represent the kinds of language, imagery and organization that institutional entrepreneurs used to create the appearance of social acceptance and comprehensibility to their primary constituencies (their peers, institutional investors, and individual investors).

While our approach provides depth of knowledge regarding these seven leading mutual fund companies, we recognize that these exemplars cannot be assumed to be representative of the population of all such companies. Smaller socially responsible mutual fund companies might frame their purpose and relevance differently than larger ones. Given the success of these mutual funds, we would anticipate convergence and similarity in framing strategies among other mutual funds as they seek to emulate their practices. We are, however, cognizant of the variation within the SR Mutual Fund arena based on types of screens and differing characteristics of institutional entrepreneurs. Regardless, however, our focus on these seven mutual fund companies provides a relevant view of the field and our case study may provide valid industry-level measures. We turn now to a discussion of our evidence regarding how the socially responsible investment industry legitimated its existence and its product. We supplement this discussion with detailed description of the recently legitimated organizational form as framed by the websites.

Findings

In a highly rationalized society, institutional entrepreneurs must convince consumers that the new product they are offering is the logical choice. Most institutional entrepreneurs do so by distancing themselves from already established companies (Rao et al., 2000). Micro-brewers distanced themselves from large, corporate brewers by challenging the brewing process used by the corporate brewers. Yet entrepreneurs must delicately balance their roles as conformists and innovators (DeClercq and Voronov, 2009a, 2009b).

SR mutual funds do not vilify conventional companies, nor do they wish to distance themselves too far (Zimmerman and Zeitz, 2002). They are at once subversive/insurgent and integrative/appropriative. As both insider/outsider, they offer new opportunities to create identities, however they also co-opt the frames of conventional companies by using similar myths of rationality to establish their legitimacy. Zimmerman and Zeitz argue that myths of rationality involve establishing legitimacy such that it:

[H]elps motivate the investor by signaling that the organization is properly constituted; committed to the proper scripts, rules, norms, values, and models; able to use appropriate means: and pursuing acceptable ends-all of which signal that it is appropriate to invest in the new venture, despite actual uncertainty about the future financial performance of the organization. (2002: 416)

In other words, even if socially responsible mutual funds are the funky friends with tattoos, they must dress themselves up in designer clothes to be accepted into the elite Country Club. We argue that SR mutual fund companies establish the following myths of rationality not only to fit in with the ‘ritzy’ crowd, but also to avoid discussions about the ambiguities of socially responsible investing. They must integrate themselves and appropriate the logic of the conventional mutual fund industry while framing themselves and their product as subversive/insurgent (DeClercq and Voronov, 2009a, 2009b).

Existing logic: Insiders/outsiders appropriate and integrate

Innovators who generated the SR mutual fund industry have attempted to legitimate themselves in the existing industry in three primary ways: (1) they conform to practices of conventional funds, (2) they advertise their acceptance by conventional sources and (3) they act primarily like investment firms, not activists.

Conforming to practices of conventional funds

‘Socio-political normative legitimacy’ is indicated when new organizational forms integrate/appropriate the norms already established in an industry (Zimmerman and Zeitz, 2002). We argue that socially responsible mutual funds demonstrate such legitimacy by conforming to conventional funds through (a) presenting consumers with financial experts; (b) following their fiduciary responsibility; and (c) presenting information about funds in the same way that conventional funds do.

First, SR mutual fund managers integrate the idea that good mutual fund companies are led by ‘insider’ financial experts. Even though SR mutual fund leadership implies expertise in two areas, finance and social responsibility, most SR institutional entrepreneurs are insiders to the mutual fund industry who have a history of experience only in finance. Of the seven companies, five (not Parnassus and Domini) have fund managers whose experience derives solely from conventional investing and all managers have business degrees specializing in finance. Thus, the central (and successful) entrepreneurs are largely insiders, with a few potential outsiders. For example, the Pax World fund manager worked at New York Stock Exchange brokerage firm, was Vice-President of a full-house investment company, and graduated from Boston University with a Management degree, specializing in finance. Further, while New Covenant did not have its own managers, it had subsidiary investment firms that controlled the money for each of its funds. None of the investment firms specialized in socially responsible investing. Indeed, each was a conventional company.

At both Parnassus and Domini, the financial leaders have both conventional financial experience (insiders) and experience in socially responsible activism (outsiders). The CEO of Parnassus worked at a conventional savings and loan and helped start Working Assets. Further, he was active in several non-profit organizations including Haight Ashbury Free Medical Clinics, Project Open Hand, the Social Investment Forum and the San Francisco Museum and Historical Society. Thus, referring back to the Rao and Giorgi model, it is difficult to place these institutional entrepreneurs solidly as either insiders or outsiders.

Regardless of their roots, however, all seven companies found reason to appropriate/integrate the presentation of their leaders as financial experts with little or no attention to justifying their executives’ commitment or experience as social change agents. As Calvert boasts, ‘Our highly regarded portfolio managers have been engaged in their professions for, on average, more than 20 years. They offer you expertise honed through widely varied market and economic conditions’ (http://www.calvert.com/about.html).

A second way SR mutual funds appropriate/integrate conventional funds ideals is by presenting themselves as upholding their fiduciary responsibility to consumers. Legally, all mutual funds managers have a fiduciary responsibility to their investors. Socially responsible mutual funds are not different. They are held to the same legal standard as conventional funds. This legal requirement, however, does more than guide SR mutual fund directors in their actions. Adhering to this law and highlighting conformity also provide legitimacy for SR mutual fund companies. If SR mutual funds can show that they take their financial responsibilities just as seriously as conventional companies, investors may trust them more and not see them as risky outsiders.

Arguably, because conformity to the law is necessary and expected, what is important is the centrality and persistence of their highlighting of these tasks. All seven of the SR mutual fund managers considered here do this by publically discussing on their websites the objective process they use to determine which holdings to include. Calvert talks about their four-tier process, called ‘FourSight’, which emphasizes its responsibility to manage duration, monitor the yield curve, optimize sector allocation and analyse credit quality (http://www.calvert.com/nrc/literature/documents/5853.pdf?litID=5853).

Each of these steps are financial strategies for choosing holdings, not socially responsible ones. Pax World provides the investment objective for each of its funds. About its balance fund, it states, ‘The Fund uses a blend of carefully chosen stocks, bonds, and government securities to seek income, preservation of capital, and moderate growth; long-term capital growth is secondary’ (http://www.paxworld.com/funds/balanced-fund/). Parnassus discusses its ‘5-step Process’ (fundamentals, financials, management, catalysts and security selection) that results in the selection of holdings with ‘favorable risk-reward ratio’ (http://www.parnassus.com/how-we-invest/default.aspx). Although it is not surprising that socially responsible mutual fund managers highlight these issues, one might anticipate more complex discussion about both financial and ‘social’ returns.

Another example of how SR mutual fund managers publically integrate/appropriate the fiduciary responsibility theme comes from an interesting debate held by Amy Domini, manager of the largest SR mutual fund and considered the pioneer of SR investing by many in the industry, and Paul Hawken, a supporter of corporate social responsibility. In a letter to the editor of the Green Money Journal (2003), Hawken publically criticizes the Domini Invest Fund for owning stock in what he considers to be socially irresponsible companies. He identifies McDonalds as one of Domini’s largest holdings and argues that McDonalds is problematic because it encourages obesity and poor health and contributes to problematic conditions in the cattle industry.

Amy Domini, who we describe above as both an insider and an outsider, responds to these attacks in the same journal by invoking her fiduciary duty as a mutual fund manager. She invokes the language of financial managers rather than activists by emphasizing investors’ desires:

[W]e try to invest in a manner that reflects what most socially responsible investors want. Despite the health concerns concerning fast food that Mr. Hawken highlights, including obesity and the increase in Type 2 diabetes, mainstream social investors have not yet decided that they will refuse to invest in companies that sell fast food or that make use of factory farming (http://www.organicconsumers.org/organic/hawken032403.cfm).

Domini does not defend McDonald’s right to produce ‘fast food’ or the manner in which it does so. Rather, she defends her position as a manager of a mutual fund. She expresses her job as that of someone who listens and responds to the desires of her consumers. By publically justifying the financial process for choosing holdings, SR mutual fund managers purposefully align themselves with conventional funds to show their investors that SR investing is neither risky nor irrational.

SR mutual fund companies also integrate/appropriate the message of conventional fund companies in the way they present financial information. Conventional fund companies provide investors with a variety of financial information on their websites. For example, potential investors can find out the net assets, risk factors, composition and average annual returns of all funds being offered. The information is presented in graph and tabular forms with written descriptions. SR mutual fund companies present their information in a similar format with the same kinds of information. For example, Smith Barney presents a pie chart of its portfolio composition. New Covenant Fund does the same. Smith Barney has a graph of its funds growth on a $10,000 investment. New Covenant Fund does the same. Smith Barney reports its annual total returns in chart form. New Covenant does the same.

One noticeable difference between conventional and SR fund companies is the location and prominence of their investment disclaimers. It is required by law that investment businesses place disclaimers on their literature to warn potential consumers that their money is not guaranteed to grow or, even, remain stable. Conventional companies tend not to place this disclaimer prominently. SR mutual fund companies do, thereby framing a boundary distinguishing themselves from the conventionals that once again tries to appropriate the idea they are financially stable and hence even more rational than traditional insiders. They place the disclaimers not only on the investment page (as do conventional companies) but also on the first page investors see when they visit the website. For example, at the bottom of Domini’s home page it says, ‘You should consider the Domini Funds’ investment objectives, risks, charges and expenses carefully before investing. View or Order a copy of the Funds’ current prospectus for more complete information on these and other topics. Please read the prospectus carefully before investing or sending money’ (http://www.domini.com).

Advertising their acceptance

Legitimation is a social process that requires acceptance, recognition, and validation by external constituencies (DeClercq and Voronov, 2009a, 2009b; Rao and Giorgi, 2006). As such, socially responsible mutual funds seek ‘socio-political regulatory legitimacy’, the approval from external sources outside the industry that are already deemed trustworthy (Zimmerman and Zeitz, 2002). Such external sources might include credentialing associations, professional organizations or any other powerful group that has an already established sense of legitimacy. We found that all seven socially responsible mutual fund companies advertise their acceptance by external sources on their webpages. Such external validation serves to, once again, show consumers that the mutual fund is not merely filled with outsiders who apply different goals than traditional mutual fund companies.

Prominently displayed under the company name on the Citizens site is a link to a Forbes article that ranks Citizens high among ‘no-load, responsible mutual funds’ (November 2, 2006). Domini has a ‘News’ link that displays their honors, like how Time Magazine deems Amy Domini as one of the ‘100 most influential people’ (http://www.domini.com/about-domini/News/Press_Release_Archive/archive-050411.doc_cvt.htm). In their ‘News’ section, Pax World has a list of quotes from respected newspapers, such as the Wall Street Journal, The Washington Post and The Financial Times, that advertise that the Pax World Balanced fund is a strong performer.

These funds each use mainstream media claims to bolster their own bids as socially acceptable alternatives to traditional investment options. Since the central criticism from dominant investing paradigms has consistently been that, as outsiders with non-traditional goals, socially responsible investments would underperform, any evidence that suggests strong performance by SR mutual funds is important to the legitimation project as it shows that such funds are led by mutual fund insiders.

Act like an investment firm

Institutional entrepreneurs demonstrate ‘cognitive legitimacy’ when they use language and actions that display their acceptance of ‘widely held beliefs’ in the broader, institutional field’ (Zimmerman and Zeitz, 2002). Some people have likened socially responsible investing to a social movement (Sparkes, 2002). Indeed, Russell Sparkes calls socially responsible investing, ‘a global revolution’ (2002). Institutional entrepreneurs in the field use the language of social activists to build identity among potential consumers—a point we discuss below. However, socially responsible mutual fund entrepreneurs act more like ‘insiders’ rather than social movement ‘outsiders’ in how they challenge corporations.

Social protests are used by social movement leaders to challenge multinational corporate control. For example, non-governmental organizations (NGOs) call for boycotts of Nike, Mcdonalds, and Nestle (Lubbers, 2002). However, none of the socially responsible mutual fund companies in our sample identify social protest as a way to change corporate behavior. Indeed, none of the socially responsible mutual fund companies in this study singles out any corporation for egregious behavior. Rather, when social activism is proposed, these SR mutual fund companies integrate/appropriate the less challenging actions used by conventional mutual fund companies, filing shareholder resolutions or company dialogue, over the more radical protest strategies of activists.

Not only do most SR mutual fund companies refrain from radical types of activism, most also distance themselves from more moderate strategies, like divesting. SR mutual fund leaders have argued that the radical transformation of the Apartheid regime in South Africa occurred because activist investors divested their money from the country. Indeed, the Social Investment Forum touts the divestment from South Africa as leading to the growth of the SR mutual fund industry (http://www.socialinvest.org/pdf/research/Trends/1995 Trends Report – After South Africa.pdf).

Yet, many SR mutual fund companies have distanced themselves from divesting. For example, MMA praxis justifies investing in Wal-Mart, ‘the retail behemoth’ whose ‘single-minded dedication to lowering prices has promoted great innovations and also generated substantial concerns’ (praxis.com December 11, 2006). The company claims that filing shareholder resolutions and corporate dialogue are more strategic for changing corporate behavior than divesting. Pax World provides the same rationale. Recognizing that others might want it to be more activist, Pax World argues that ‘Sometimes, therefore, we may maintain an investment (if it still meets our guidelines) in order to urge a company to improve its performance in an area we find questionable’ (paxworld.com December 11, 2006). Domini avoids divesting from companies with poor human rights, labor and environmental standards with this disclaimer: ‘The situation is further complicated by the fact that virtually no company has been notably effective in improving these conditions’ (domini.com December 11, 2006). Parnassus justifies its strategy by arguing that divestment leads to short-termism and pressures companies to make money quickly. ‘By being thoughtful, long-term investors, we give management the flexibility they need to make the right decisions’ (Parnassus.com December 11, 2006).

To summarize, our analyses support Meyer and Rowan’s (1977) contention that new organizational forms gain legitimacy by reproducing myths and rituals associated with bureaucratic rationality. As insider/outsiders, the SR mutual fund companies in our sample legitimate themselves, in large part, by appropriating/integrating normative industry standards, by affirmatively recognizing the authority structure, and by expressing agreement with widely held institutional beliefs. Because innovators were both insiders and outsiders, extending traditional frames cannot be isolated as either solely integrative or appropriative. As we discussed above, each of the companies, regardless of the background of their key players, pays obvious attention to industry-wide standards in the mutual fund industry. As we discuss below, however, we also find that by including activist frames in their discourse these companies set themselves apart from conventional ones by linking progressive social change to their own and their clients’ financial success.

Importing logics: Insiders/outsiders subvert using insurgent logic

Saul Alinsky (1971) envisioned that ‘proxy tactics’ would revolutionize corporations. Social activists would purchase stocks in a corporation prior to its annual meeting and then attend the meeting with the purpose of disrupting it. Ralph Nader furthered this strategy by submitting radical shareholder resolutions. The purpose was not to invest for the sake of monetary benefit but, rather, for protest. These activists demonstrated their priorities by divesting after the period of the given corporation’s annual meeting. While neither Alinsky nor Nader are considered pioneers in the SR mutual fund industry, their insurgent framing of the idea that companies can and should be places of social responsibility set the stage for SR mutual company insider/outsiders to challenge the existing logic that a company’s only goal is to make a profit.

We find that the language and images used by the SR fund companies are best understood as a lamination of the preceding activist frame designed as an exercise in boundary framing (Hunt et al. 1994) and frame extension (Snow et al., 1986). By drawing a political line between themselves and conventional funds, SR fund companies create a clear choice of distinct alternatives through diagnostic framing. Using prognostic frames, they inform potential consumers that socially responsible investing can produce positive social change. By presenting motivational frames that emotionally connect investments with political values, they extend an identity frame into the consumer base that is constructed via lamination as the original frame is passed back and forth across organizational fields.

Consistently, the socially responsible mutual fund companies in question discuss the connection between investor values and SR mutual funds. Although not always the most prominent message among all, these messages are overt and encourage investors to balance their desire to invest with their potential to help change the world. As the following texts illustrate, socially responsible mutual funds show the positives of connecting social values with financial investments.

Pax World enables investors to align their financial goals with their personal values through a selection of professionally managed mutual funds. By screening companies not only by their investment potential but also by standards of social responsibility, Pax World challenges companies to reach for a higher ‘bottom line’ and offers investors the opportunity to do good while doing well. (paxworld.com January 7, 2007) SRI is catching on with many individual and institutional investors who seek to align their investment portfolio with their personal values by avoiding companies that do not meet certain standards. (calvert.com January 7, 2007)

Thus, SR mutual fund companies emphasize their outsider status by linking emotionally provocative statements and images with creating an SR identity among investors. SR mutual funds practice boundary framing when they present themselves as political alternatives to conventional funds; they advertise ‘screening’ processes that weed out companies that fall short of ‘standards’. This frame suggests that the market is populated by two kinds of companies, socially responsible ones and socially irresponsible ones. The problem is diagnosed as the ability of socially irresponsible companies to hide, to avoid detection and continue attracting investors, even socially responsible ones. Thus, social responsible mutual fund entrepreneurs act like outside insurgents when they present themselves as holding knowledge of screening processes. However, they are also inside subversives as they claim that enforcing socially responsible screens is a political act that links social justice to individual wealth as joint consequences. We want to emphasize here that while many traditional fund companies (like Merrill Lynch and Vanguard) now offer SR funds to their clients, such companies do not use the language of values as SR fund companies and do not mention screening for any standards but economic ones. They work from a position of established legitimacy as the dominant form within the mutual fund marketplace and their socially responsible mutual funds represent just more ‘acceptable’ offerings from established companies (see Markowitz, 2007). As insurgent outsiders, socially responsible mutual fund companies attempt to convince consumers that when they invest with their values, they are being social activists. A social activist is someone who tries to change an injustice. All seven SR mutual funds extend the social activist frame to mutual fund investing; they argue that the simple act of investing creates social change. One of the most prominent specialty funds, Domini, sets the tone and establishes this practice clearly.

The Way You Invest Matters—Be Part of the Solution: As a shareholder in the Domini Funds, you make a difference in the world. Engaging companies on global warming, sweatshop labor, and product safety. Revitalizing distressed communities. Bringing new voices to the table. Redefining corporate America’s bottom line. (domini.com January 13, 2007)

Likewise, the website emphasizes ‘the emblematic starfish story expressed so often by Amy Domini and posted prominently in its publications’.

Thousands of starfish washed ashore. A little girl began throwing them in the water so they wouldn’t die. ‘Don’t bother, dear’, her mother said, ‘it won’t make a difference. The girl stopped for a moment and looked at the starfish in her hand. ‘It will make a difference to this one. (domini.com Jan 14, 2007)

In an interview with the Baltimore Sun, Domini said, ‘Simple messages work … People want to believe that some of what they invest is working toward a world of universal human dignity and environmental sustainability’ (Smitherman, 2005).

Similarly, at New Covenant, their social orientation is prominently featured on the front page of the website.

In addition to the specific investment objective of each of the funds, New Covenant Funds makes investment decisions consistent with the social-witness principles adopted by the General Assembly of the Presbyterian Church (USA). These policies flow from our faith and stewardship of God’s resources entrusted to the Church. (New Covenant January 15, 2007)

These messages are further evidenced on the websites of other funds.

Socially concerned, active shareholders are an increasingly important voice in supporting the development of business practices that provide both social and financial benefits (MMA Praxis January 17, 2007). The adviser also takes an active role in promoting other socially responsible practices involving the environment, social and racial equality, shareholder action and community support by voting shares within their portfolios (New Covenant January 17, 2007).

These quotes from the SR mutual fund companies display the fuzzy distinction between outside insurgents and inside subversives as the messages attempt to promote an activist investor identity balanced with a theme of profit motivation. Consider the simplistic messages of Calvert and Parnassus. ‘At Calvert, investment success isn’t measured by numbers alone. In our view, a successful investment not only earns competitive returns, it helps build a sustainable future’ (calvert.com December 11, 2006). Pax World offers an explicitly integrative message that justifies the logic of socially responsible investing within the paradigm of financial acumen and progressive politics.

By challenging companies to meet ethical standards, by monitoring corporate behavior, and by using shareholder voting rights to influence business practices in a positive fashion, socially responsible mutual funds give investors a collective voice in corporate decision making (pax.com December 11, 2007). Towards that end, we have developed a process that combines thorough financial analysis with another, critically important set of factors that most investment managers ignore—environmental, social and governance (ESG) criteria. This integration of rigorous financial analysis with equally rigorous ESG analysis provides an increased level of scrutiny that helps us identify companies with the following attributes: They are forward-thinking and acting. They are leaders in their respective industries. They meet positive standards of corporate and environmental responsibility. They are focused on the long term. We believe these companies are better managed, more innovative and better positioned to deliver long-term performance than their less enlightened competitors. By investing in them, we intend for our shareholders to benefit from their vision and success. (Pax World December 17, 2006).

Finally, Parnassus reiterates this same message in a parsimonious way: ‘Do well by doing good’ (Parnassus.com December 17th, 2006). SR mutual funds apply prognostic frames by representing the act of investing as a mechanism of social change. The vehicle to social change is the mutual fund itself. Like traditional social movements, they argue that only through the collective muscle of their participants (harnessed through the mutual fund), can peoples’ voices be heard (Snow and Benford, 1992, 1988). Yet SR mutual funds craftily blend the insurgent/subversive social activist message with the integrative/appropriative one of financial returns.

Critics of socially responsible investing have focused on two primary arguments, that the investments are not necessarily socially responsible or meaningful for social change and that using screens of social responsibility is antithetical to maximizing profit by enhancing performance. Given the growth of socially responsible investing, it appears that institutional entrepreneurs’ identity claims and promotion of ‘values investing’ have gained wide acceptance, wide enough to legitimate a new organizational form. Nonetheless, they have had to face nagging criticisms and predictions of low performance. In response, they sometimes link social responsibility to an investment logic that justifies screening as a way to achieve even higher returns than those provided by conventional funds. Consider ‘Domini’s Story’:

They didn’t know what the results would be. It seemed logical that companies with better social and environmental records would perform at least as well as polluters and firms with poor employee relations—probably better—but there was simply no evidence one way or the other. Wall Street analysts told them it would never work: Including social and environmental considerations into investment decisions would limit the investment universe, and therefore limit returns. They didn’t acknowledge that traditional money managers are paid large sums of money to do just that—limit their investment universe to a profitable portfolio of stocks. Analysis of the long-term record of the Domini 400 Social Index* has shown that social and environmental standards have led to strong individual stock selection and potentially higher returns (domini.com January 5, 2007).

This point reinforces our previous discussion of the tendency of socially responsible mutual companies to conform to the insider rhetoric and presentation of traditional mutual funds. Domini additionally argues, however, that social responsibility need not involve decreased financial expectations. Individual profit and social progress are presented as linked rather than mutually exclusive. Hence, the entrepreneurs act as both inside subversives and outside insurgents. Doing so carefully avoids any questions about whether the concept of ‘socially responsible investing’ is real.

Generally, these socially responsible mutual fund companies argue that investing for good does more than allow investors to put their money where their mouth is. It also allows investors to make more money. As Parnassus boasts, ‘We were among the first firms that implemented the idea that an investment firm could generate solid investment returns by taking a disciplined approach to investing while also having a positive impact on society’ (http://www.parnassus.com/downloads/FundsBrochure.pdf). All seven of the socially responsible mutual fund companies stir up positive emotions and link purchasing SR mutual funds both to making money and to doing good.

In sum, the message that socially responsible mutual fund companies are trying to construct for their consumers is that investing in a market economy is not necessarily morally problematic. According the their messages, participating in the market through socially responsible investing is a form of social activism that helps investors uphold their values and create social change, all while making money. The purpose of this message is to legitimate a new organizational type—socially responsible mutual funds. Through conforming to conventional funds in form, socially responsible mutual funds show the public that they are not radical or risky. Yet, socially responsible fund companies must also subvert and challenge existing codes by invoking a new identity around their funds to differentiate themselves from the traditional product they are mimicking. They do so by generating emotional language and images around social responsibility. Such emotions help socially responsible investors understand that they are not investing solely for individual gain, but for the social benefit of all and helps steer any questions away from the ambiguities of the concept ‘social responsibility’.

Discussion and conclusion

We discussed above how legitimation is a socio-political process imbued with power with institutional entrepreneurs uncovering the normative values of society and capitalizing on them. While we find Rao and Giorgi’s (2006) model useful and informative, we contend that hybrid forms, such as socially responsible mutual fund companies, may not fit neatly into the formulation. As such, the perspective of DeClercq and Voronov (2009a, 2009b) offers a useful framework upon which to build.

Nevertheless, we believe that our case illuminates conceptual overlap not fully captured or elaborated in these works. Drawing on Bourdieu’s (1984) tradition and Schneiberg and Lounsbury (2008), we contend that these hybrids provide fertile ground for expanding scholarly understandings of the complex nature of legitimation projects within dynamic organizational fields that integrate insider and outsider logics. Minimally, our data suggest that code-breaking may involve insiders and outsiders who use multiple strategies that conform to and/or challenge existing institutional logics. The overlap we depict is illustrative of the strategies the socially responsible mutual fund industry used in its successful legitimation project. The overlap of institutional legitimation and innovation strategies is not entirely surprising given DeClercq and Voronov’s (2009a, 2009b) work.

We argue that by fusing the messages from the two distinct organizational fields from which institutional entrepreneurs belong, socially responsible mutual funds leaders have appealed to traditional marketplace demands of institutional investors and captured the interests of individuals attracted to an SR consumer identity. This fusion helped establish the industry as institutionally legitimate. More specifically, socially responsible institutional entrepreneurs gain legitimacy for the ambiguous product they are offering by adopting the rational myths and ceremonies of conventional mutual fund companies while using the language of social activists to sew a socially responsible identity among their consumers.

When socially responsible mutual funds conform to traditional funds, they legitimate themselves as neither radical nor risky. Yet, by adopting a social activist identity, socially responsible funds convey to their consumers that investing can be more than a rational act, it can also be an impassioned act made by compassionate people. In combining the rational with the emotional, socially responsible mutual funds avoid difficult questions about the product itself. Further, while most studies find that institutional entrepreneurs discuss the traditional forms from which they are breaking negatively, we find that socially responsible funds do not vilify conventional mutual funds. In fact, quite the opposite is true. They try to mimic conventional funds in form and financial presentation.

Yet, this identity-making process cannot conflict with the profit imperative of investing. Snow and colleagues (1986) recognized that the successful recruitment of individual participants to social movements required that movements specifically align themselves with the individual interests of potential participants. Because the potential participants involved here are investors, adequate frame alignment involves linking investment both to social change and to individual profit.

It is widely held that institutional entrepreneurs must identify openings within their organizational field and identify opportunities within existing organizing and operating processes in order to carve out a niche for their innovation (Fligstein, 1997). How they identify such contradictions and then use ‘symbolic resources’ to stake their claims as a socially acceptable alternative even when there is no corroborating evidence remains an important question within organizational sociology (Suddaby and Greenwood, 2005). Our data suggest that as both insiders and outsiders, institutional entrepreneurs were able to combine the message of their dominant counterpart and carve out new space for themselves by exploiting consumers’ growing unease with corporate malfeasance and social irresponsibility. The new organizational form acquired legitimacy within the established institutional logic by carefully framing a perception of difference within a contention of overall similarity (Aldrich and Fiol, 1994; Suddaby and Greenwood, 2005) SRI institutional entrepreneurs did not need to dismantle the dominant institutional logic; they needed only to bridge the worlds of social movements and traditional investing by aligning claims of social responsibility with acts of fiscal responsibility. In spite of variation in screening types among our sample, we find significant consistencies in their efforts to attend to insider/outsider logics. Nevertheless, our small number of cases did not allow for thorough comparison on the basis of types of screens employed, and there may be further opportunity to elaborate these relationships by considering variation within the industry.