Abstract

Out-of-pocket payment is one of the indicators measuring the achievement of Universal Health Coverage. According to the World Health Organization, for countries from the Asia Pacific Region, out-of-pocket payments should not exceed 30%-40% of total health expenditure. This study aimed to identify factors influencing out-of-pocket payment for the near-poor for outpatient healthcare services as well as across health facilities at different levels. The data of 1143 individuals using outpatient care were used for analysis. Healthcare payments were analyzed for those who sought outpatient care in the past 6 months. The Heckman selection model was used to control any bias resulting from self-selection of the insurance scheme. The finding revealed that health insurance reduces average out-of-pocket payments by about 21% (P < .001). Using private health facilities incurred more out-of-pocket payments than public health facilities (P < .001). The study suggested that health insurance for the near-poor should be modified to promote universal health coverage in Vietnam.

Introduction

Globally, the drive to support the objectives of Universal Health Coverage (UHC) is growing. Vietnam is one of the countries recognized as having fully adopted UHC as a national strategy and as having made strong progress toward its goal of affordable access to needed and quality health services. One of the indicators measuring UHC is that people are financially protected. 1 Out-of-pocket payment (OOP) plays an important role in achieving the UHC enabling people to receive the health services they need without facing any financial difficulty, including issues of households’ OOP spending.2,3 Household spending for health is defined as the total household’s payment on health-related needs such as preventive, promotional and curative care. Household health payments can include prepayment before illness, such as the cost of health insurance and direct OOP health spending such as payment for hospital fees. For these countries in the Asia Pacific Region, OOP should not exceed 30%-40% of total health spending. 4

In Vietnam, the household OOP payment for healthcare services is quite high, accounting for 60%-70% of total payment.5,6 Without health insurance, OOP costs for an individual can rapidly increase up to 75% of the monthly nonfood per capita payment of a household. In 2012, the master plan of UHC was released, which identified the objectives of reaching 70% of social health insurance coverage by 2015 and 80% of social health insurance coverage by 2020. As a result, the OOP expenditures would be less than 40% by 2015. 1

To help people avoid financial risks and burdens caused by health issues, the Vietnamese government introduced the Health Insurance Law in 1992. According to this, insurance requires compulsory participation for all employees working in the public sector, retired people etc. Users of private medical services will have to pay their own costs. Results of the study in 1998 showed that 12.5% of the population had health insurance, with the insurance coverage accounting for 11% of the health spending.7,8 In 2008, the Law on Health Insurance was issued in the 12th National Assembly, marking an important development in the legal system on health insurance. This law made the highest legal basis for health insurance. Accordingly, children under 6 and the poor/near poor are required to participate in health insurance. As a result, the coverage of health insurance increased significantly, reaching nearly 70% after 5 years of implementation and health coverage covered vulnerable groups and the poor. 9 In 2014, to ensure universal health insurance and achieve the goal of developing an efficient and equal health care system contributing to progress, economic development and ensure social safety policies; the National Assembly amended and supplemented a number of articles regarding the Law on Health Insurance. This law has many innovative contents that clearly show the advantages of health insurance, that is, to expand the beneficiaries of health insurance, to expand the scope of health insurance benefits and the level of health insurance benefits, to open the route of medical examination and treatment with health insurance, to specify the management and use of the Health Insurance Fund and to regulate the responsibilities of relevant agencies and organizations. The law stipulates compulsory participation in health insurance for all people, demonstrates political determination to promote the implementation of universal health insurance goals and enhances the legitimacy to align the responsibilities of all people participating in health insurance, ensuring the principle of sharing of people participating in health insurance. 10

Health insurance, in the case of appropriate implementation, will support costs for the people, even helping to reduce 200% of the household’s OOP spending. 11 Total health payment for the poor is also significantly reduced by the coverage of health insurance that supports this population. 12 The same conclusion was made about the substantial reduction of the poor’s OOP spending for health. 13 This finding was recently reported in the studies conducted in countries such as Vietnam, India and Thailand14-17 where significantly lower OOP expenditures occurred among insured individuals more than the uninsured for outpatient healthcare services used. Also, most of the literature in these studied above mentioned that the type of out-patient visits at private or public health facilities was a determinant of financial burden on house-holds expenditure. Yet these studies showed that the health status or expenses on diagnostics were as a contribute factor in high OOP spending and frequent result from out-patient care.14-16 This study aimed to describe the OOP payments concerning outpatient healthcare services of the near-poor and to identify the impact of public health insurance on the private spending of this target group in Cao Lanh District, Dong Thap Province, Vietnam.

Methods

Study design

The study employed a cross-sectional design to describe the OOP health payments for outpatient healthcare services and explore the impact of public health insurance on OOP health expenditures of the near-poor.

Study sites

This study was conducted in Cao Lanh District, Dong Thap Province, Vietnam. Dong Thap is located in the Mekong River Delta area and consists of 12 districts. Cao Lanh is a district located in the southern part of the province including 17 communes and the district’s population is 194 000. Cao Lanh District was purposely selected as the health insurance scheme for the near-poor that has been much better implemented than those in other districts.

Study subjects and sampling

The sample size for this study was 2000 near-poor individuals who could have potentially used outpatient healthcare services in the past 6 months. In Cao Lanh District and other areas, the near-poor households have been identified as average income households’ within the levels stipulated by the Prime Minister. 18 A commune consists of, on average, 3 to 5 hamlets and in each hamlet, about 10 to 12 ‘Community Self-Management People’s Units’ were built by the district Vietnamese Fatherland Front. Each Unit was responsible to manage 30 households and also to identify a list of near-poor households. This list was then submitted to the Commune People’s Committee (CPC). In each commune, a review board has been established, consisting of several representatives from the CPC such as the head of the CPC, the head of the Division of Labor, Invalids and Social Affairs, the heads of hamlets in each commune etc. This board will make a final decision of who is eligible for near-poor status.

The study focused exclusively on outpatient care for two main reasons. First, those who reported using inpatient care account for a low rate, less than 20% as compared with those using outpatient care. Second, inpatient care is mostly provided by public health facilities with private health providers accounting for only 1%, similar to the reason reported by another study. 8 The sample size was based on a combination of an estimation of the power of the study to detect important differences and the practical limitations of the cost of recruitment. Of these, 1143 people accessed outpatient healthcare services at public and private health facilities. The sampling method is presented in Figure 1.

Flowchart of sampling approach.

Study instruments and data collection

A structured questionnaire was developed and undertaken with reference to the Vietnam Household Living Standard Survey (VHLSS) questionnaire to collect data about health insurance coverage, OOP payment for health services and other potential explanatory factors. The interviews were conducted by those who had been working as health workers in a community and had been trained for interviewers’ skills.

Measurement and variables

OOP expenditures for outpatient healthcare services between the insured and the uninsured would be compared in the model controlling for several factors such as age, sex, educational level, health status etc.. OOP is calculated using the total payment of hospital expenses such as medicine, transportation, diagnosis etc. The identification of the poor and near-poor is based on monthly household income. 19

Data management and analysis

Data was coded, cleaned and entered in the computer using Epi-data Software and analysed using SPSS 18.0. In this study, ordinary least square (OLS) analysis was first used to estimate the impact of near-poor health insurance on private OOP payments on health, controlling for observable factors in a linear regression model at P-value < .05. However, it would be possible that self-selection in the voluntary health insurance program was affected by unobservable variables, which in turn would impact the magnitude of health payments. When the effect of these unobservable variables is uncontrolled, the estimators of the coefficients will be biased and inconsistent. Thus, we also showed a model which controls for such bias by allowing unobserved variables influencing the decision to purchase health insurance to be related to unobserved variables that would also influence health payments. Expectations of health care needs and health seeking behaviours are examples to explain this affect.11,15 We estimated a dummy variable model to test and correct sample selection bias using the statistical technique of the Heckman Selection Model.

Ethics clearance

The study was approved by the Ethics Review Committee of Hanoi University of Public Health (Decision No 123/2012/YTCC-HD3). All the answers and information of the participants were kept confidential and used for the study purpose only. The studied individuals signed the informed consent form.

Results

Descriptive analysis

Table 1 shows the average OOP payments per outpatient visit at a health facility after excluding the health insurance premium and average number of outpatient visits by the insured and uninsured samples for 1143 respondents. Of the 1143 respondents in the household survey, 980 (85.7%) reported health facilities that were accessed for outpatient care.

Average OOP payment per outpatient contact and average number of outpatient contacts by health facility and insurance status (‘000 VND).

Two important features were identified of health payments for outpatient care and the number of visits. First, the average OOP payments per outpatient visit significantly differed among health facilities (F test = 27.2, P < .01). An outpatient visit at higher level public hospitals cost the uninsured about twice that compared with a visit at a commune health centre (328 000 VND and 164 000 VND, respectively). Second, the insured patients spent about 24% less on average than those with uninsured. Health insurance tended to reduce the OOP payment more for those accessing health services at lower level public health facilities, such as commune health centres (60%) and district hospitals (55%), than those who accessing health services at higher level public hospitals (6%). However, on average, insured patients spent 27% more per outpatient visits at private health facilities than those without insurance.

The result also showed the average OOP payments per outpatient visit. Under this costing scenario, the insured patients spent about 2% less on average than the uninsured. Health insurance still tended to reduce the OOP payments for those accessing health services at lower level health facilities, particularly commune health stations (34%) and district hospitals (39%), but increased the OOP payment for those who accessed health services at higher level health facilities, that is, hospitals (9%). At private health facilities, the insured patients spent on average 53% more per outpatient visit than those of the uninsured patients.

Econometric results

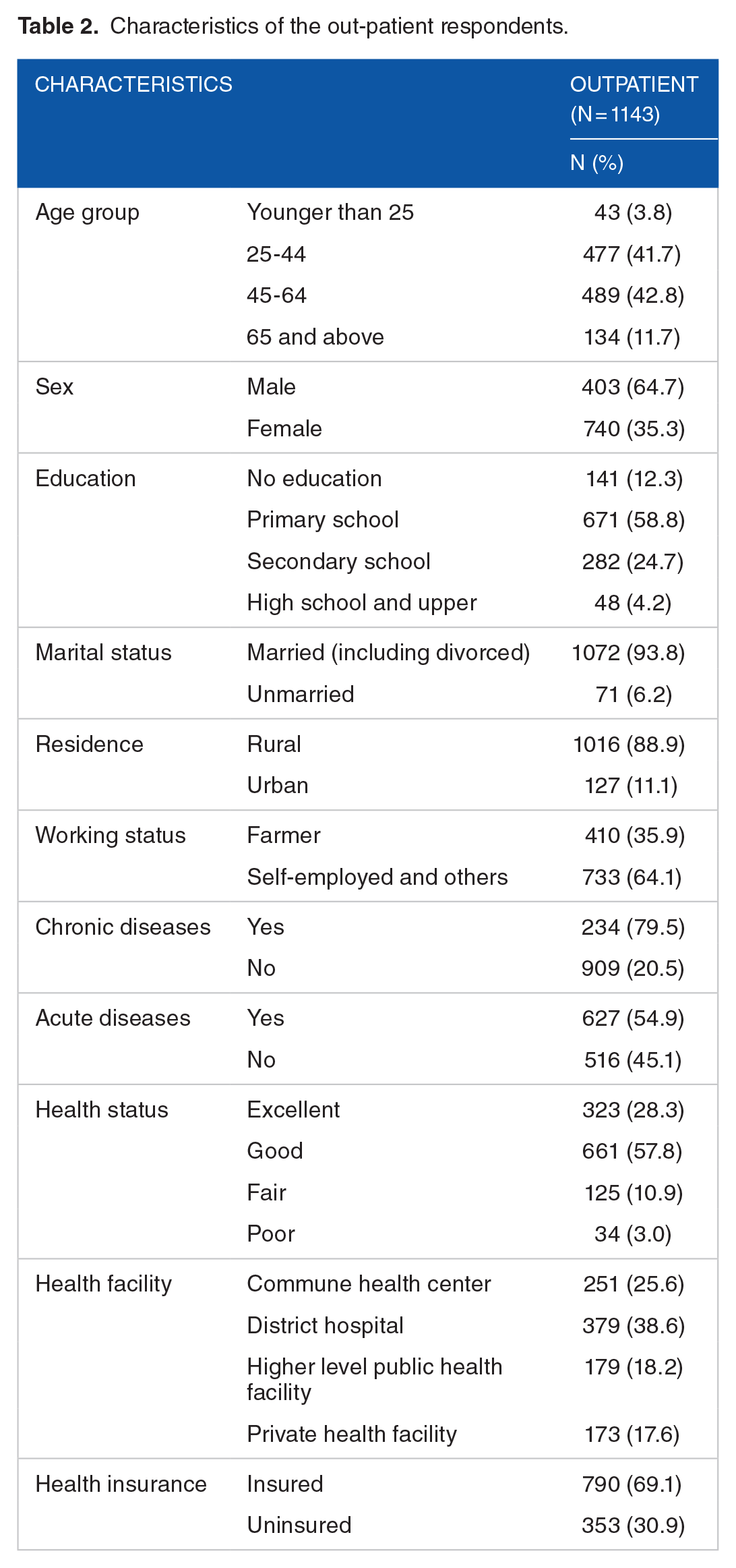

Several independent variables were found to be significantly associated with OOP payments including insurance status, residence, health status, health conditions and health facility use. Table 2 provides characteristics for the variables used in this study.

Characteristics of the out-patient respondents.

The dependent variable was the natural logarithm of real total OOP payments (in 2015 price) concerning outpatient treatments, including consultation, diagnosis, medication, travel and accommodation expenses at health facilities for 6 months. In this study, no individuals reported zero payments. The econometric findings from ordinary least squares and Heckman selection model are reported in Table 3.

Factors associated with private OOP payment for outpatient care.

significance at p<0.05

In the OLS model, the coefficient representing the insurance status indicated that on average the insured spent 13% less than the uninsured (P < .001). Those residing in urban areas spent 21% less than those residing in rural areas. It could be seen that those with excellent health spent 8% less than those with other health statuses. Poor health respondents spent 24% more than those with better health. Participants with conditions categorized as chronic diseases spent 19% more than those with other health conditions. Those who used provincial/center health facilities had to spend 22% more than those using other health facilities. Other independent variables were not significantly associated with OOP payments for outpatient treatments (P > .05). The model passed the Ramsey RESET test of model specification or omitted variables (P = .21), and returns with an R2 value of 0.26.

To create the Heckman’s selection model, we included one more variable using the number of visiting health facilities for seeking healthcare services in the selection equation assuming that this treatment seeking behavior would correlate to the decision of purchasing insurance, but not correlate with health expenditures. The model also was tested and corrected for selection using the Inverse Mills Ratio (IMR). The t-test of the null hypothesis revealing that the coefficient concerning this variable was zero, indicated that a correlation exists between health insurance status and health payments. The IMR was signif icant (P = .028), indicating that nonrandom self-selection in the health insurance scheme existed. Thus, this model generated a more consistent estimator of the effect of health insurance status on positive health spending. The finding showed that insured individuals spent on average 23% less than those without insurance, indicating a relatively high increase concerning the 13% lower average estimated by the OLS model.

Coefficients of most of the other variables had changed. Urban individuals spent on average 31% less than rural individuals, increased from 21% of the lower average estimated by the OLS model.

Those younger than 25 were found to have on average 76% lower health payments than other age groups (P < .01). Those working as farmers spent on average 45% more than those with other occupations (P < .01). Those using private health facilities spent 42% more than those using other health facilities (P < .05). Participants with chronic and acute diseases spent 48% and 30% less, respectively, than those with other health conditions (P < .05). The model passed the Ramsey RESET test of model specification or omitted variables (P = .20), and returned an R2 value of 0.25.

Discussion

The financial protection of health insurance as shown in many research, focused on the impact of insurance on household OOP payments for all kinds of healthcare.11,20,21 This study used 2 types of model to analyze the impact of health insurance on healthcare expenditures by using household survey data in Cao Lanh District, Dong Thap Province, Vietnam.

The average OOP payments per outpatient visit differed among health facilities at all healthcare level. An outpatient visit at higher level public health facilities cost more than at lower level public health facilities. The uninsured had to pay higher total OOP payments and pay at all levels of public health facilities except for private clinics/hospitals than the insured. These findings were consistent with related studies.8,21 In general, at all healthcare levels, the average number of outpatient visits of the uninsured was lower than those of the insured. While the uninsured were more likely to seek healthcare services at higher level health facilities than lower level ones, the insured were to the opposite. These results were also indicated in other studies.5,22 That outpatients were more likely to suffer from health conditions and their needs of medical care were high was widely understood. However, these needs were often not met due to the high medical expenses that could be reduced when those people were involved in health insurance schemes. The uninsured were more likely to use health care services at higher level health facilities because they might think that they had to access health services at health facilities at a higher technical quality after paying the full fees. Higher level public health facilities were considered to have better quality of care than lower level health facilities. 23

An OLS model assumed the impact of insurance status on health payment was independent of unobservable variables determining payments. However, unobservable factors influencing the purchase of health insurance might also affect health spending, leading to bias in the estimates. Thus, the Heckman model used in the analysis allowed the possibility of random self-selection in the scheme.

Several factors were found to be significantly associated with OOP payments. The insured spent 13% less on average than the uninsured. The Heckman model generated a consistent estimate of the effect of insurance on healthcare spending. This finding was consistent with other studies.8,14,21,24

The Heckman model also indicated that those residing in urban areas had lower health care payments than those residing in rural areas. This finding was similarly to other studies reporting no significant association between urban residence and private health payments.8,21 This difference might have been due to the study data indicating a difference in the knowledge level of health insurance schemes between the 2 groups and that the proportion of urban respondents enrolling in health insurance was higher than that of rural respondents. Thus, urban individuals might have used insurance benefits to reduce OOP payments more than rural individuals.

Those with poor health spent more than those with other health statuses in the OLS model, and still supported in the Heckman model although the association was insignificant. This finding was consistent with a related study11,14 suggesting that individuals reporting poor health condition were indeed more likely to experience diseases than those with other health status. As a result, they incurred more OOP spending when using healthcare services, while individuals with conditions categorized as chronic diseases incurred higher OOP payments. This result was also found in a related study. 20 However, this finding was not supported by the Heckman model where those with chronic and acute diseases spent lower health payments. These might be explained by the impact of health insurance to financially protect those with insurance experiencing diseases.

Using higher level public and private health facilities involved higher OOP payments than using lower level public health facilities.8,21 Patients were likely to access healthcare services at higher level health facilities due to limitations of care and perceived quality of care at lower level health facilities, especially for the insured. Thus, as well as paying for the direct cost of consultation, diagnosis and medication, they had to pay more for travel, accommodation and other indirect costs that would arise when using healthcare services in lower level health facilities. 5 Furthermore, those who accessed higher level health facilities would also have more complicated health needs that cost more to treat. It could be seen that insurance played no role on health payment for those who accessed higher level health facilities. This finding was consistent with a study conducted recently in Vietnam. 25 The reason might be that those who accessed outpatient care at higher level health facilities without a reference letter would be charged the full fee while service prices have increased.26,27

The government in Vietnam subsidized 100% of the health insurance premium for the poor, but only 70% of this premium for the near-poor. However, the income differential between the 2 groups was small. 28 Consequently, the near-poor incurred more payment when using healthcare services than the poor. The impact of health insurance scheme for the near-poor on reducing OOP payment on healthcare services might be higher if the government fully subsidized co-payments of premium and the co-payment of services fees was lower.

Conclusions

In summary, for the upcoming period, the health insurance program for the near-poor in Vietnam should be modified. In addition, it would be necessary to improve the quality of care provided, to increase health insurance enrolment and the likelihood of accessing insurance benefits and decreasing private OOP payments. The objectives of universal health coverage could then be secured.

The results also have several broader implications for universal health insurance. When the universal health insurance is to be funded through a universal income, it would be important that the community fully understands how insurance works and that this is communicated in forms that could be fully understood by people with low health literacy. Significant government attention needs to be paid to ensure that the quality of care provided to those who use their health insurance when seeking care are treated equally to those who pay directly. Finally, in terms of costs to the health system and to individuals, attention needs to be given to ensure that wherever appropriate, care is provided at the community health level and that this care is recognized as constituting high quality services.

The study was confined to a district in Dong Thap province that could not reflect the total Vietnamese population. Consequently, this could limit the generalizability of the results on health insurance coverage, utilization of insurance benefits, out-of-pocket expenditures and the associated factors to other locations. In this study, the analysis was based on insurance status, service utilization and OOP by the respondent himself or herself. The future research should be implemented on other household’s members because the information on health conditions, work and service utilization could also impact on income, OOP and the uptake of insurance and healthcare service use.

Footnotes

Acknowledgements

We would like to express our special thanks to the health workers and colleagues at the health communes in Cao Lanh District, Dong Thap Province, Vietnam for supporting and coordinating with us when conducting this research. Also, we would like to extend our appreciation to individuals and stakeholders at community level in Cao Lanh District for their active participation in this study.

Funding:

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests:

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Author Contributions

All authors contributed to the study conception and design. The first draft of the manuscript was written by NDT and BTMA. PTH, CHX, PQA checked and commented on previous versions of the manuscript. NDT and BTMA revised the final manuscript. All authors read and approved the final manuscript.