Abstract

In this study, we investigate why companies intend to use nonownership services by conducting qualitative interviews with 10 experts to develop our hypotheses, then using a survey to test them. Our findings show that, as hypothesized, firms’ intentions to use nonownership services are affected by both financial (i.e., tax efficiency and cash and liquid asset management) and nonfinancial (i.e., control over assets and access to the latest technology and tools) factors, with access to the latest technology and tools being the most important driver. Furthermore, we show that the effect that the desire to gain access to the latest technology and tools has on intentions to use nonownership services is enhanced (i.e., moderated) when firms wish to reduce the risk of obsolescence. The hypothesized moderation effect of firm size on the importance of cash and liquid asset management is marginally significant. These findings are an important contribution to the literature, as previous studies have almost exclusively focused on the financial drivers of nonownership service use.

Keywords

Introduction

Fierce competition and high market complexity have forced traditional product manufacturers to gradually shift their focus from tangible products to intangibles, such as skills and knowledge, and to extend their service offerings (Vargo and Lusch 2004; Wirtz and Ehret 2013). Consistent with this development, scholars increasingly question the traditional goods-dominant marketing logic (e.g., Lovelock and Gummesson 2004; Vargo and Lusch 2004). Adopting a service-dominant logic may help firms to restructure their business model away from selling goods and towards offering access to goods (Vargo and Lusch 2004). Lovelock and Gummesson (2004) even criticize the existing distinction between services and goods, which is based on intangibility. They propose a new lens for services marketing—nonownership or rental/access. Lovelock and Gummesson differentiate services from goods by characterizing services as market exchanges that convey benefits through temporary access rather than ownership, such as car leasing or hiring consultants to gain access to their knowledge and expertise.

Business-to-business (B2B) services are an important force driving the growth of the service sector (Wirtz and Ehret 2009). Important subsectors of B2B services that are also examples of nonownership services include rental, outsourcing, and leasing. Leasing is one of the most widely used nonownership B2B services (Dasgupta, Siddarth, and Silva-Risso 2007) and the focus of this study. Leased equipment accounted for approximately one third of the capital equipment in the United States in 2010 (Chemmanur, Jiao, and Yan 2010), and for 28% of the same in Europe in 2008 (Leaseurope 2009). Given the popularity of the nonownership option in the B2B services sector, it is puzzling that much of marketing theory still assumes that transactions involve the transfer of ownership (Lovelock and Gummesson 2004).

Only a few academic studies have adopted the rental/access paradigm proposed by Lovelock and Gummesson (2004), focusing predominantly on nonownership models in a business-to-consumer (B2C) rather than a B2B context (e.g., Dasgupta, Siddarth, and Silva-Risso 2007; Moeller and Wittkowski 2010). Further research is needed to better understand the growing demand for corporate nonownership services.

This study contributes to the current state of knowledge in five ways. First, it extends the services marketing literature by developing the rental/access paradigm. Second, it contributes to a widely applicable definition of nonownership service by empirically analyzing and transferring the theoretical construct of nonownership into a practical context. Third, by investigating the financial and nonfinancial determinants of intentions to use nonownership services, our study integrates findings from the finance and marketing literature. In this, we follow the example of Dasgupta, Siddarth, and Silva-Risso (2007), who adopt a similar approach to examine consumer nonownership decision making. Fourth, this study adds to the B2B literature by empirically demonstrating that both financial and nonfinancial factors influence nonownership services use intentions. Fifth, this study helps managers to develop and market nonownership services by identifying the most important purchase motives.

Literature Review, Qualitative Study, and Hypotheses

Literature Review

Conceptual definition of intentions to use nonownership services

The term nonownership is related to Lovelock and Gummesson’s (2004) definition of services. Services can be classified as transactions through which the customer gains the right to use tangible or intangible resources. Lovelock and Gummesson identify the following nonownership service categories: (1) rented goods services—the customer rents a good for a defined period of time for a fee (e.g., renting a machine); (2) place and space rentals—the customer purchases access to a specified space or place in a location (e.g., renting a space in a factory building); (3) labor and expertise rentals—the customer rents the labor or expertise of another person (e.g., hiring a lawyer); (4) physical facility access and usage—the customer buys access to a facility and the exhibits therein (e.g., renting admission to a conference site); and (5) network access and usage—the customer temporarily possesses the right to participate in a network (e.g., telecommunications).

Lovelock and Gummesson’s framework illustrates the range of transactions that can be defined as nonownership services. Our study focuses on their first category, rented goods services, which gives a company access to an asset. An asset is defined as a tangible, movable, nonfinancial economic resource that can be consumed or used for production.

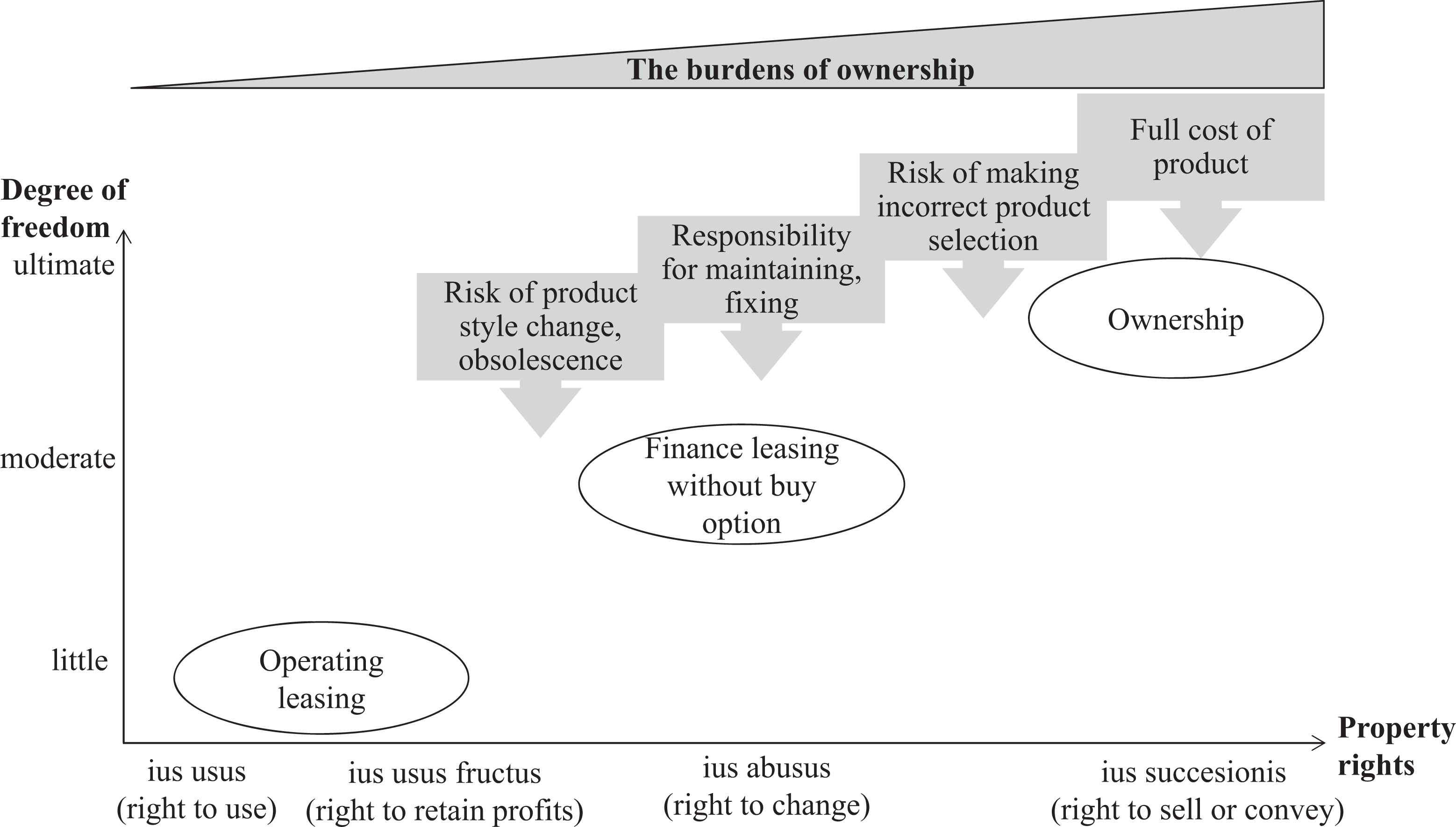

Previous research has suggested (e.g., Moeller and Wittkowski 2010; Wirtz and Ehret 2009) that a property rights theoretical framework can enhance our understanding of the nonownership construct. Property rights play an important role in transactions involving both movable and immovable assets (Kleinaltenkamp and Jacob 2002). According to property rights theory, ownership is represented by a set of distinct rights: (1) the right to use the good (ius usus); (2) the right to retain profits obtained through use of the good (ius usus fructus); (3) the right to change the property (ius abusus); and (4) the right to sell the property or convey some of the rights to others (ius succesionis; Furubotn and Pejovich 1972). In nonownership, these four rights do not rest with a single party, but are shared among multiple parties (Ehret 2008; Haase and Kleinaltenkamp 2011; Moeller and Wittkowski 2010).

Assets have different attributes to which distinct property rights are attached. As such, property rights are separable (Barzel 1997), which allows for the separation of ownership from authority in the form of legitimate power (Besley and Ghatak 2010). Parties holding property rights to an asset gain value from it by exercising specific rights (Ely 1995). Reich (1964) states “property draws a circle around the activities of each private individual or organization. Within that circle the owner has a greater degree of freedom than without” (p. 771). Thus, the more property rights an individual or institution owns for a particular asset, the greater the freedom to use that asset. We define freedom as the right to determine action without constraints, as long as these actions do not violate the rights of others.

However, property rights can also turn into duties (Kleinaltenkamp and Jacob 2002), as owners are responsible for and bear all of the costs for maintenance, storage, use, and disposal of the property. This is why Berry and Maricle (1973, p. 44) coined the term “burdens of ownership,” which is defined as (1) “the risk concerning product style change and obsolescence,” (2) “the risk concerning making an incorrect product selection,” (3) “responsibility for maintaining, fixing, and moving the product,” and (4) “the full cost of products [ … ] for which the consumer may have only intermittent, infrequent use.” With non-ownership, the allocation of property rights changes and the customer gains access to the good, yet most of these burdens of ownership remain with the owner (Ehret 2008; Moeller and Wittkowski 2010).

Against this theoretical background, we define nonownership service as service in which customers acquire some property rights to an asset and are offered a certain degree of freedom in using this asset for a specified period while the burdens of ownership remain with the owner. Intentions to use nonownership services are defined as a firm’s definite plan to acquire access to an asset through nonownership.

Figure 1 presents an overview of distinct nonownership and ownership options. It shows the interplay between the degree of freedom customers acquire with each option and the associated burdens. With increasing freedom, customers gain access to a growing number of property rights, but also assume more ownership duties. Leases are classified into two categories: finance and operating. We subsequently describe both categories as examples of nonownership options to further clarify Figure 1.

Burdens of ownership and property rights associated with forms of nonownership and ownership.

Finance leases are usually long-term or intermediate-term, noncancellable contracts that are fully amortized over their basic term. The equipment is treated as an asset of the lessee, who assumes all of the liabilities connected with its use and has the option to buy the asset at the end of the leasing contract (Gao 1995). If the lessee executes this option, he obtains full ownership of the asset. Finance leasing offers a moderate degree of freedom because the lessees can negotiate the product specifications and gain access to three property rights: the right to use the asset, the right to retain the profits obtained from this use, and the right to change the asset within specified limits. The lessees also bear several burdens, for example, the maintenance and repair of the asset. If they decide not to purchase the asset (see Figure 1: Finance leasing without buy option), at the end of the leasing period all property rights, risks, and burdens are returned to the lessor.

In contrast, operating leases are typically short-term, cancellable contracts that usually do not include a purchase option. The lessor remains the owner of the asset and depreciates it, while the lessee receives the right to use the equipment (Anderson and Lazer 1978). Operating leases come with the right to use the asset and retain the profits resulting from this use with few ownership burdens.

Determinants of intentions to use nonownership services

Judd (1964) and Rathmell (1966) are the first to point out that services do not involve a transfer of ownership from buyer to seller. Lovelock and Gummesson (2004) develop these ideas in their rental/access paradigm. However, apart from some leading marketing textbooks, such as Kotler and Keller (2006) and Lovelock and Wirtz (2011), the rental/access paradigm remains largely unexplored. Nonownership services use is particularly underresearched.

The vast majority of studies examining nonownership in B2B markets are in finance and accounting, and hence concentrate on the financial benefits of nonownership services (e.g., Braund 1989; Myers, Dill, and Bautista 1976). Thus, although some studies suggest that firms’ use of leases goes beyond financial benefits (e.g., Gavazza 2011), much of the discussion appears to be on tax- (e.g., Drury and Braund 1990; Graham, Lemmon, and Schallheim 1998) and financial liquidity-related motives (e.g., Sharpe and Nguyen 1995).

Anderson and Bird (1980), Schallheim (2009), and Wirtz and Ehret (2009) belong to a small group of scholars who explore the determinants and motivations for firms’ use of nonownership services from a wider perspective. Anderson and Bird (1980) identify 40 potential advantages of leasing and show, in a descriptive study, that nontax and noncash flow rationales do exist for companies’ use of nonownership services. Schallheim’s (2009) theoretical study examines the benefits that leasing promises to deliver and concludes that, in addition to financial factors, various nonfinancial factors determine firms’ use of nonownership services. Specifically, firms choose nonownership because it supports a unique structuring of contracts and serves companies’ individual needs (Schallheim 2009). In their conceptual paper, Wirtz and Ehret (2009) relate property rights theory, the resource-based view, and the entrepreneurial theory of the firm to the nonownership concept and to business services. According to Wirtz and Ehret, service providers can generate the following fundamental value propositions by offering non-ownership services: (1) reduction of the costs of asset-ownership (property rights theory), (2) freeing scarce management capacity to focus on high value-creation opportunities (resource-based view), and (3) enhancing entrepreneurial agility and leverage (entrepreneurial theory of the firm).

Together, these descriptive and conceptual studies suggest that intentions to use nonownership services are driven by a range of variables beyond those related to tax and liquidity. Furthermore, given that leasing as a form of nonownership can be characterized as an alternative to purchasing (Nevitt and Fabozzi 2000), one might argue that the determinants for firms’ usage intentions of nonownership services are as complex as those affecting purchasing decisions. Therefore, we believe that firms choose nonownership services not only for financial, but nonfinancial reasons as well.

Qualitative Study

Our hypotheses were generated from an extensive literature review and 10 in-depth, personal interviews with experts using semistructured interview guides. To capture a complete view and explore the determinants of firms’ intentions to use nonownership services from several perspectives, we used a triangulation strategy (Jick 1979) and interviewed an industry expert and decision makers from both lessee and lessor companies. We used a key-informant approach and interviewed organizational members with specific knowledge of the subject matter (Heide and Weiss 1995). Specifically, the industry expert is a publicist from the Federal Association of German Leasing Companies and the remaining nine interviewees represent the following industries: tax advisory, legal, and financial and leasing services. Five interviews were conducted in person, three over the phone, and the remaining two via e-mail. We digitally recorded and transcribed the interviews conducted in person and via telephone. We then sent the transcripts to the respective interviewees to verify their accuracy and allow them to add information. The returned transcripts were analyzed to identify the main determinants of firms’ intentions to use nonownership services.

The interviews began with a brief explanation of the study. Respondents were then asked to identify and describe the main determinants of companies’ intentions to use nonownership services, and to list the advantages and disadvantages of each determinant. The interviewees were also asked to give the reasons for their firms’ choices. The interviewer used the laddering technique to further investigate the topics (e.g., Reynolds and Gutman 1988).

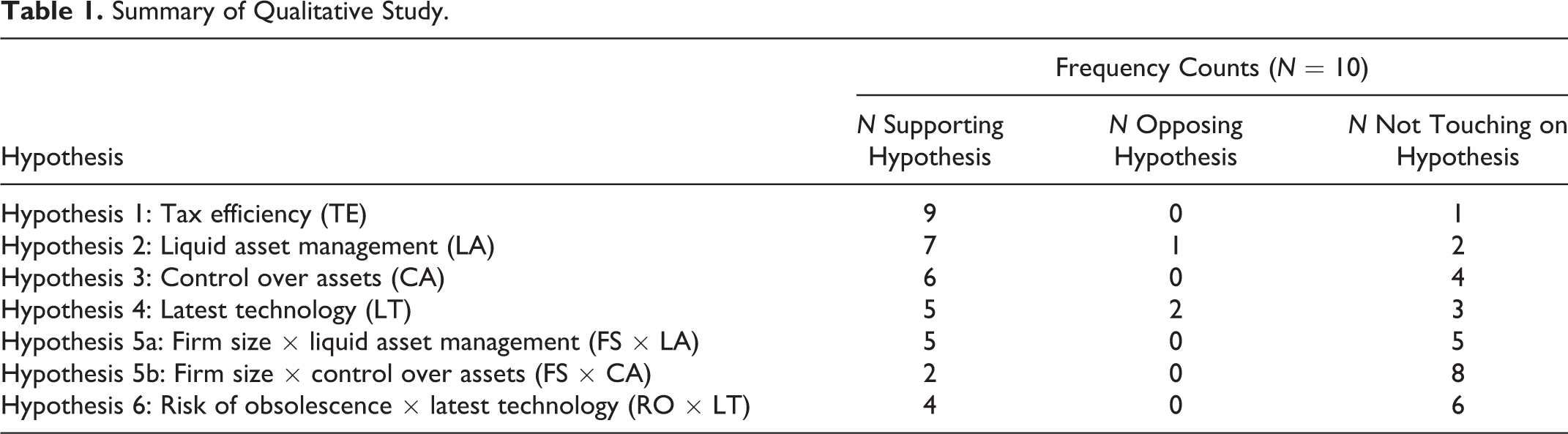

Overall, the comments from the lessee- and lessor-side respondents and those of the industry expert converge. Firms’ intentions to use nonownership services are driven by financial (i.e., the importance attached to tax efficiency and cash and liquid asset management), and nonfinancial factors (i.e., the extent to which firms aim for control over assets and the desire to obtain access to the latest technology and tools). Our findings are summarized in Table 1 and are integrated into the hypotheses development section below.

Summary of Qualitative Study.

Hypotheses Development

Tax efficiency

Operating leasing is a tax-efficient way to gain access to assets (Graham 2003). It is tax efficient because leasing expenses can be fully charged to a firm’s profit and loss statement, whereas the purchase price of an owned asset can only be depreciated over several years (Graham 2003).

Taxes are an essential component of transaction decisions (Myers, Dill, and Bautista 1976). Smith and Wakeman (1985) show that among other factors, taxes are a rationale for firms’ nonownership service use. This is supported by the results of our qualitative study; nine of the ten interviewees mentioned tax efficiency as a determinant for companies’ intentions to use nonownership services (see Table 1). For example, the chief executive officer (CEO) of an IT leasing firm noted: Tax optimization is the most important driver. Let us assume the following: management anticipates high profits for the next two years. Leasing allows us to reduce these profits and thus has a positive effect on the tax situation.

We therefore predict that tax considerations determine firms’ usage intentions of nonownership services.

Hypothesis 1: The level of importance attached to tax efficiency has a positive effect on firms’ intentions to use nonownership services.

Cash and liquid asset management

Firms need liquidity to meet the transaction needs of daily business activities and for unforeseen contingencies (Dittmar, Mahrt-Smith, and Servaes 2003). Leasing preserves liquidity because it requires lower initial payments than full purchase price upon acquisition (Zimmerer 1972). Our qualitative study shows that many firms that are struggling to raise funds and/or do not have sufficient collateral for loans will opt for nonownership to preserve liquidity. According to seven of the ten interviewees, non-ownership provides a viable alternative form of financing and liquidity. This is illustrated in the following two quotes: Liquidity retention definitely plays an important role in the leasing decision. This aspect becomes especially important in times of tight monetary and economic conditions when banks only grant a limited number of loans. (CEO of a small tax advisory firm) It makes a huge difference whether a firm pays £350 [as leasing fee for a year] or £600 [the purchase price] for the asset. This is what counts for a CFO”. (CEO of a leasing firm for IT software, equipment, and cars)

Thus, we suggest that an interest in improved liquidity is a determinant of companies’ intentions to use nonownership services.

Hypothesis 2: The level of importance attached to cash and liquid assets has a positive effect on firms’ intentions to use nonownership services.

Control over assets

The use of nonownership services affects firms’ strategic orientation, such as their maintenance strategy (Richardson 2004). Thus, we conjecture that firms choosing nonownership services not only take financial issues into account but also consider whether leasing will support other strategic objectives.

Wirtz and Ehret (2009) propose the resource-based view (Penrose 1959; Wernerfeldt 1984) as a theoretical lens through which to perceive companies’ use of nonownership services. According to the resource-based view, a firm consists of bundles of resources and each firm is different from its competitors because it has a unique set of resources that result in a competitive advantage (Ghosh and John 1999).

The theory of core competence is a subtheory of the resource-based view. Amit and Shoemaker (1993) describe a core competence as a firm’s ability to combine or bundle resources in a unique way. In line with Leonard-Barton (1992), we define core competencies as a set of knowledge that is employed when using an asset that provides a firm with a distinct competitive advantage. Strategy research on core competencies supports the idea that firms should focus on those capabilities that create or could create unique value, and should transfer the remaining functions to other organizations (e.g., Mayer and Salomon 2006). In practice, nonownership allows firms to follow this proposition, as shown by the following quotation: The additional services offered with leasing become increasingly important [ … ] Firms use these services in order to be able to concentrate on their core business. (publicist from the Federal Association of German Leasing Companies)

The expertise needed for the additional services provided with the core nonownership services, such as maintenance or installation, often represent core competencies for the lessor, but auxiliary functions for the lessee. For example, many firms are uncertain about the use of IT and often require assistance with these noncore activities. Echoing this sentiment, a CEO from an IT leasing company made the following declaration: The additional services we offer become increasingly popular. A large number of these firms associate a great risk with the use of IT. They do not know which system suits their business model best. [ … ] These firms often require a lot of assistance.

Ownership can be described as the degree of control over an asset (see Figure 1). A party can only obtain more control over an asset by diminishing the rights of another party (Grossman and Hart 1986). With nonownership, control over an asset is shared between parties. Commenting on the importance of retaining full control over assets in certain contexts, the CEO of a leasing corporation for IT explained: Let us, for example, look at the big audit firms—they own all of their IT, they do not use leasing. And that is mainly because of the data that the firms store on their PCs. With leasing—usually at the end of the leasing period all data should be erased from the devices. However, sometimes the lessor fails to remove the information and the highly sensitive data is involuntarily disclosed to the next user of the device.

Furthermore, sharing control over an asset can have severe consequences for a firm’s core competencies and competitive position. For example, some providers offer critical expertise, activities, and assets to competitors of the buyer firm and/or later enter their clients’ markets and compete with them (Quinn and Hilmer 1994). Therefore, some firms are reluctant to share control over their assets with service providers, as they fear losing control over core activities. Firms that prefer to have full control over their assets and that draw strong external boundaries will have lower usage intentions of nonownership services.

In sum, we propose that the relative importance of control over assets, whether it be for strategic or other reasons, will determine a firm’s intentions to use nonownership services.

Hypothesis 3: The level of importance attached to maintaining control over assets has a negative effect on firms’ intentions to use nonownership services.

Latest technology and tools

The theory of management fashion examines the diffusion of popular management techniques and describes the behavior of firms under conditions of uncertainty. Principles of fashion theory are not merely applicable to management’s mindset but also to management actions in “marketing, finance, accounting, operations, as well as almost every area of technical endeavor” (Abrahamson 1996, p. 25).

Abrahamson (1996) claims that both exogenous (e.g., changes in the economic and political environment) and endogenous (e.g., a company’s desire to differentiate itself from competitors and the search for novelty) forces can lead to performance gaps. Fashion-setting organizations identify gaps between expected and achieved performance, and then promote certain management fashions by claiming that these concepts will improve efficiency. We argue that the rapid development of technology leads to a cycle of gaps that continue to widen once a new technology has been implemented. Managers seeking to fill these gaps adopt suggestions and innovations promoted by fashion setters (Abrahamson 1996).

We believe that to close these gaps, firms adopt new technologies that put them at the forefront of their industries. The new technologies lead to new management techniques that lead to new performance gaps, creating a constant cycle of replacement and renewal. Here, we propose that nonownership is especially attractive to firms striving to obtain access to the latest technology and tools. Furthermore, firms are more likely to use nonownership services if the expected period of use is shorter than the useful life of an asset (Smith and Wakeman 1985). The short leasing periods allow firms to access assets for a limited time and replace them with the latest developments.

Half of the respondents from the qualitative study state that companies interested in using the latest assets use nonownership services. Nonownership seems especially attractive to firms using assets that are constantly replaced by new developments and quickly go out of fashion, as is shown in the following quotation: The possibility to use the latest tools is definitely one of the main drivers for nonownership usage. Let us talk, for example, about an engineer working in the automotive industry. While the number of software packages is increasing, the hardware becomes slower. He does not want to have to sit in front of the computer and wait because the hardware is not capable of dealing with all the software. (key account manager of a leasing firm for IT soft- and hardware, and cars)

In sum, we propose that firms that use the latest technology and tools have high intentions to use nonownership services.

Hypothesis 4: The desire to access the latest technology and tools has a positive effect on firms’ intentions to use nonownership services.

The moderating role of firm size

Lasfer and Levis (1998) show that firm size shapes firms’ nonownership services use. Specifically, small firms are more focused (or often must focus) on the liquidity-related aspects of non-ownership than larger firms are. For many smaller firms, nonownership services are a substitute for high cost financing and necessary for either survival or growth (Lasfer and Levis 1998). Thus, firm size, liquid asset management, and nonownership are linked. We conjecture that the size of the company moderates the relationship between the extent to which firms value liquidity and their intentions to use nonownership services.

Hypothesis 5a: Firm size moderates the positive effect of cash and liquid asset management on firms’ intentions to use nonownership services, such that the effect is greater for smaller firms than it is for larger firms.

Smaller companies are often owner-managed, which is usually associated with more centralized decision making. At the same time, smaller firms often have to substitute leasing for financing due to their less optimal financing situation, and these owners are often hesitant to share property rights. This reluctance to lease equipment related to the core competence is also high for very specialized companies, which most small companies are (Smith and Wakeman 1985). Consistent with this argument, two of the interviewees mentioned the moderating role of firm size: For the some of the small, owner-managed companies ownership is still important. (publicist from the Federal Association of German Leasing Companies) They do not want to share the ownership rights with a third party. (CEO of an IT leasing corporation)

Thus, having full asset control seems to be more important to small firms. Therefore, we propose that firm size moderates the relationship between degree of control over assets and firms’ usage intentions of nonownership services.

Hypothesis 5b: Firm size moderates the negative effect of control over assets on firms’ intentions to use nonownership services, such that the effect is greater for smaller firms than it is for larger firms.

The moderating role of risk of obsolescence

Firms’ asset replacement decisions are driven by either the poor performance of the current asset (performance obsolescence) or the availability of a newer, improved version of the asset (technological obsolescence; Hartman 2001). Firms interested in using the latest technology and tools continuously face the risk of asset obsolescence because the introduction of a new version may create the sense that the current asset is outmoded. Nonownership allows firms to transfer this risk to the service provider (Drury and Braund 1990). Thus, the desire to transfer the risk of obsolescence is one motivation for using nonownership services (Mukherjee 1991). In particular, firms that desire continuous access to the latest technology will use nonownership services to reduce the risk of obsolescence as is shown in the following quotation: Reducing the risk of obsolescence is one of the main motivations why companies use leasing. Especially for those that tend to continuously use the latest technology. (CEO of an IT-leasing company)

Therefore, we contend that the degree of importance attached to reducing the obsolescence risk of assets moderates the relationship between the desire to access the latest technology and tools, and a firm’s intent to use nonownership options.

Hypothesis 6: The desire to reduce risk of obsolescence moderates the positive effect of the desire for the latest technology/tools on firms’ intentions to use nonownership services, such that the effect is greater for firms with a higher desire to reduce the risk of obsolescence.

Method

Measures

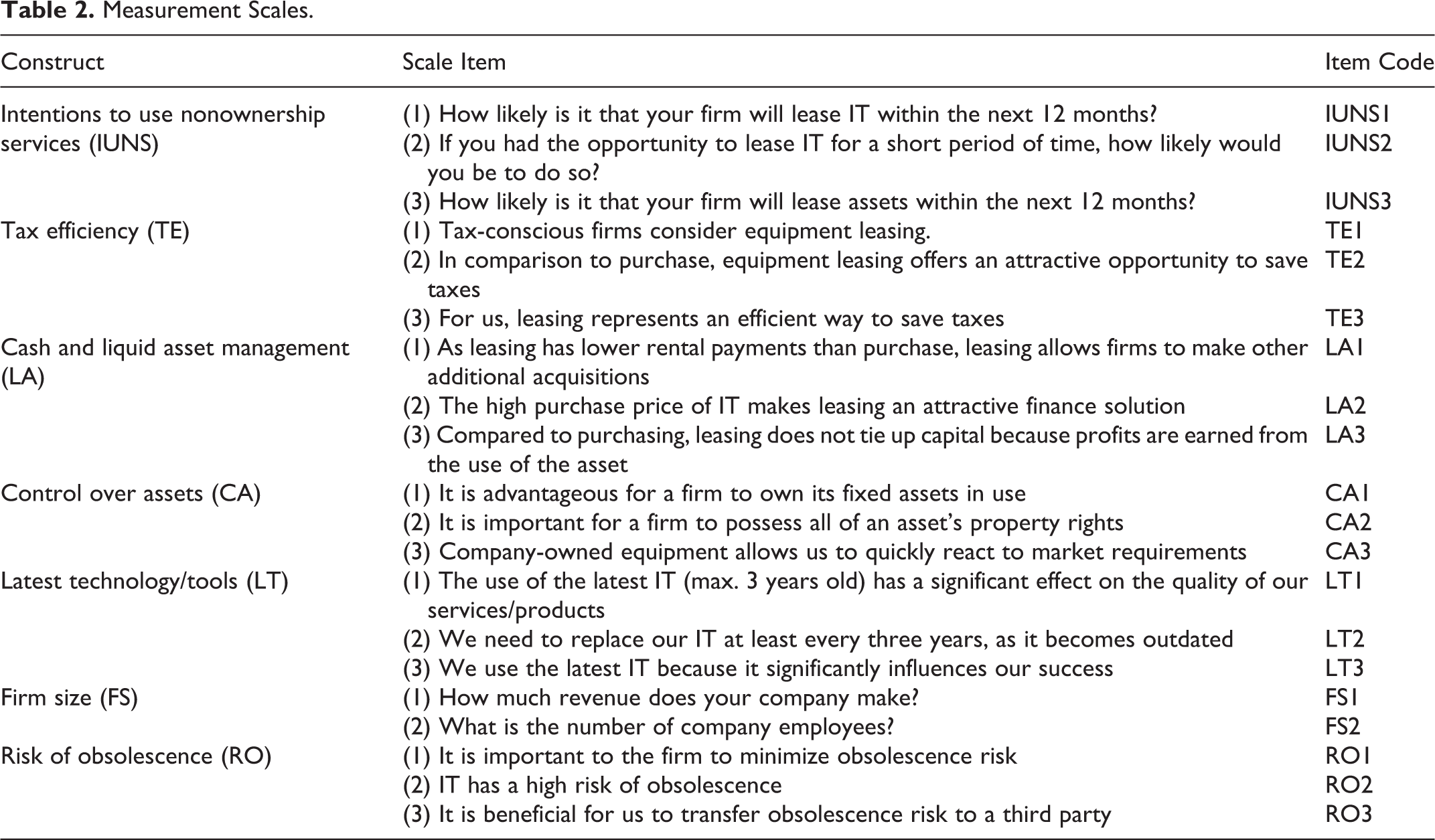

An extensive literature review was conducted to develop the measurement instruments (see Table 2), based on the above conceptual definitions. However, the literature did not provide measures for all of the scales, so some of the instruments were self-developed. We designed the items to measure cash and liquid asset management (LA), tax efficiency (TE), and risk of obsolescence (RO) according to Anderson and Bird’s (1980) measures. We chose a 5-point, Likert-type rating scale.

Measurement Scales.

Intentions are good predictors of future behavior related to high involvement and routine purchase decisions (cf. Armstrong, Morwitz, and Kumar 2000). Thus, we captured respondents’ intentions to use nonownership services by assessing their actual use. We collected data on IT hardware as representative of nonownership services. To enhance the validity of the responses, we made the questions as directly relevant to IT services as possible. Specifically, our dependent variable “intentions to use non-ownership services” consists of 3 items measured on 5-point Likert-type scales (1 = very unlikely; 5 = very likely).

A pretest assessment of the validity of the measures was performed using an item-sorting task (Anderson and Gerbing 1991) conducted with a sample of 16 participants drawn from the sample population. All of the indicators appear to be valid measures of the theoretical constructs, as the results of the pretest provide values for the proportion of substantive agreement above 0.70 and all of the substantive-validity coefficients were above 0.5 (Dunn, Seaker, and Waller 1994). The questionnaire was then pre-tested to minimize response errors. Based on these steps, minor adjustments were made to the questionnaire (Dunn, Seaker, and Waller 1994).

Setting and Data Collection

We focused on the IT-leasing decisions of small and medium-sized firms (SMEs) for a number of reasons. First, to ensure a significant response rate, we selected an asset, nonownership IT services, that is widely used across industries. Second, SMEs represent a large proportion of companies in every economy, and are therefore an attractive existing or potential customer base for nonownership service providers. Third, in SMEs, the recruiting and retaining of qualified internal information system experts is difficult due to limited career options. Therefore, SMEs are more dependent on external expertise and services for IT than larger firms. Finally, the lack of resources and the low level of in-house information systems expertise make the adoption of IT a greater risk for small companies than for large companies. Thus, external support and assistance provided by nonownership services might be particularly attractive to SMEs.

Our data were collected using computer-assisted-telephone-interviewing (CATI). For our original sample, we randomly chose 5,000 CEOs from German SMEs with a maximum of 300 employees from a company directory. To increase the response rate we used prenotification e-mails and follow-up phone calls. In our research design, nonrespondents were sent a follow-up e-mail 3 weeks after the first call, at which point they were called again during normal business hours. After five unsuccessful callbacks, a firm was categorized as a nonresponder. The final sample consisted of 314 respondents, giving a response rate of 7%. In seven cases, the chief information officers of the firms were interviewed because the CEOs did not feel knowledgeable enough regarding the firm’s leasing decision making.

To minimize common method bias in terms of common rater effects, we protected respondents’ anonymity and the confidentiality of the study, and urged respondents to answer questions as honestly as possible and to remember that there were no right or wrong answers. Moreover, we used a simple and concrete design for our scale items.

We tested for potential nonresponse biases by comparing the firm size and leasing behavior of the first 42 respondents with the behavior of 50 firms that answered after receiving the second notification (Armstrong and Overton 1977). There is no statistically significant difference between the groups. These findings are consistent with Krosnick’s (1999) prediction that low response rates do not necessarily indicate nonresponse error. Although telephone interviews offer numerous advantages, they also suffer from shortcomings. We minimized the potential acquiescence interviewer biases by ensuring respondents that their answers were anonymous and by training interviewers and monitoring them during the interviews.

In Germany, the vast majority of SMEs adhere to national and noninternational accounting standards. We focus on operating leasing because German regulations define leasing as operating, rather than finance leasing (where assets are treated as purchased and financed).

The sample consisted mainly of industrial firms (52%), followed by service providers (26%), and retailers (11%), with industrial medicine, real estate, traffic and transfer, and hotels and restaurants collectively accounting for the remaining 11%. The corporations are located in major cities across Germany. Forty-three percent of the firms in the sample have revenues of less than €5 million and less than 100 employees, whereas 11% have sales exceeding €50 million and more than 250 employees. One-third of the firms lease IT-equipment (i.e., IT hardware, printers, projectors, copier machines, and/or telecommunication devices) and/or software. We tested for differences between companies with and without previous leasing experience and did not find significant differences, which allowed us to analyze the groups together.

Analysis and Findings

Measurement Models

We employ a two-stage approach to structural equation modeling (SEM). In the first step, the measurement models are analyzed. In the second step, the relationships between the latent constructs (i.e., the structural model) are investigated.

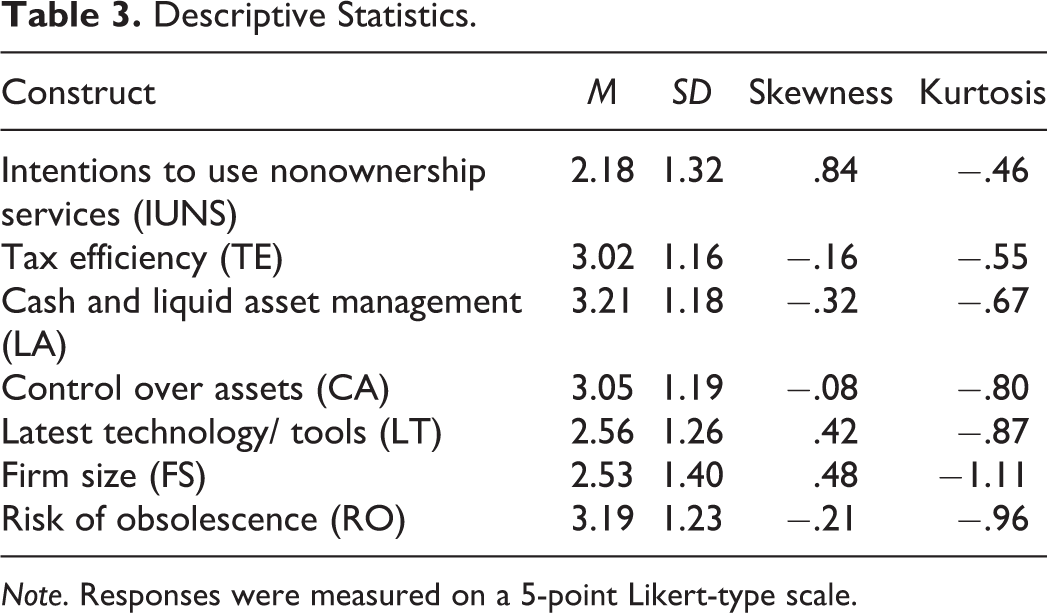

The descriptive statistics of the constructs are shown in Table 3. Except for intentions to use nonownership services (IUNS), the means of all of our 5-point Likert-type scales are above the midpoint of 2.5. All of the values for skewness and kurtosis indicate univariate normality. The data also have a multivariate normal distribution as shown by the Mardia’s normalized multivariate kurtosis coefficient of 86.3, which is smaller than the upper limit of 441 (based on the formula p(p + 2), where p is the number of observed variables in the model (Raykov and Marcoulides 2008)). This initial analysis suggests that our data are suitable for SEM.

Descriptive Statistics.

Note. Responses were measured on a 5-point Likert-type scale.

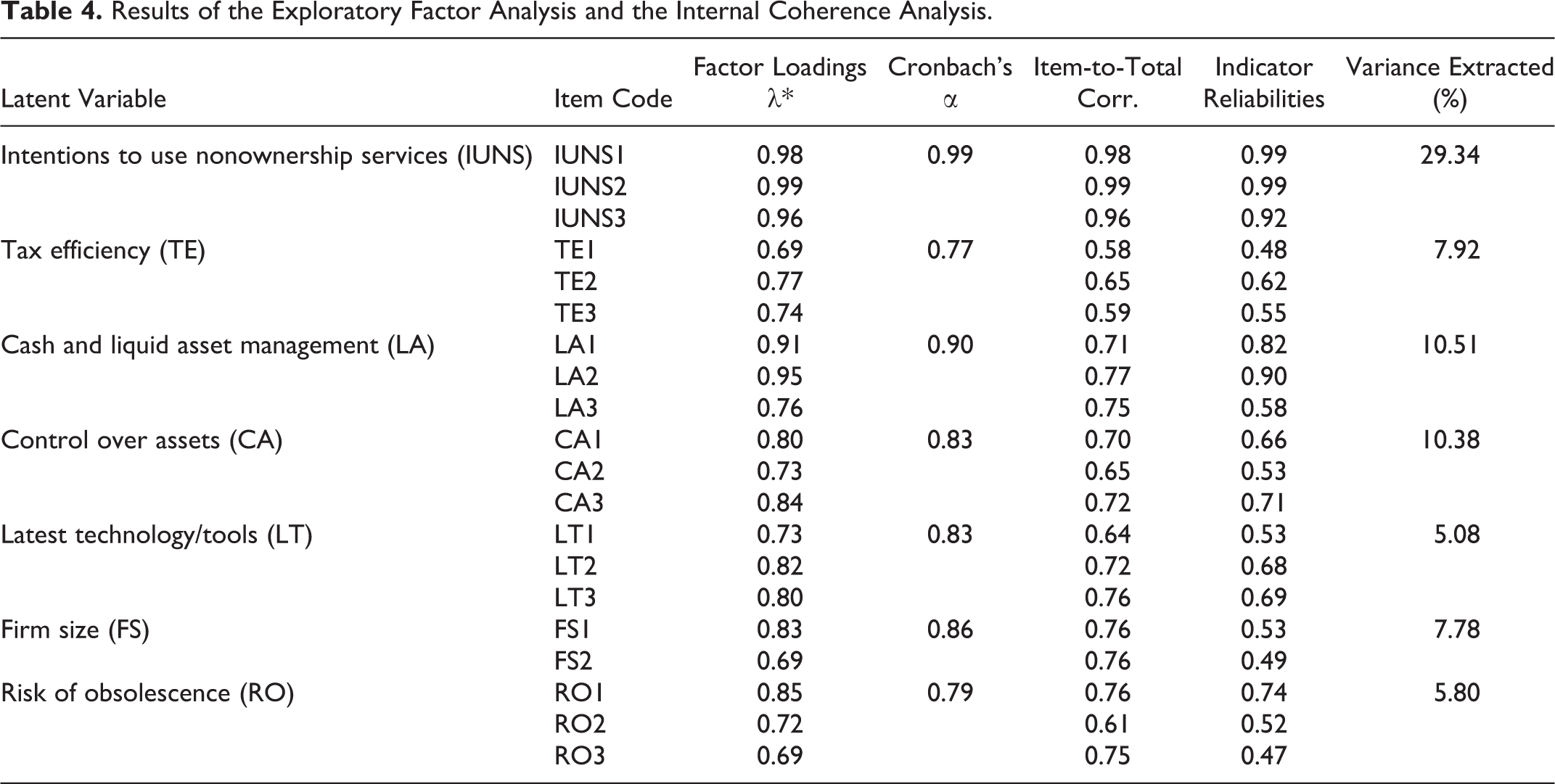

The initial exploratory factor analysis, using principal component analysis with Varimax rotation, extracts seven factors (Table 4). All of the indicators load on our proposed dimensions. All of the Cronbach’s α values exceed .70, suggesting good scale reliability.

Results of the Exploratory Factor Analysis and the Internal Coherence Analysis.

Method bias may have a negative effect on the validity of studies (King et al. 2007). To assess the common method bias, we use Harman’s single factor test (Podsakoff et al. 2003). We load all of the items used to measure independent and dependent variables into a single exploratory factor analysis. The seven factors together account for 81% of the variance, whereas the first factor explains 29%; that is, it does not explain the majority of the variables. This suggests that the common method bias is unlikely to be a concern in our study (Podsakoff and Organ 1986). However, it should be acknowledged that because this is an individual study, method bias cannot be fully excluded (Burton-Jones 2009).

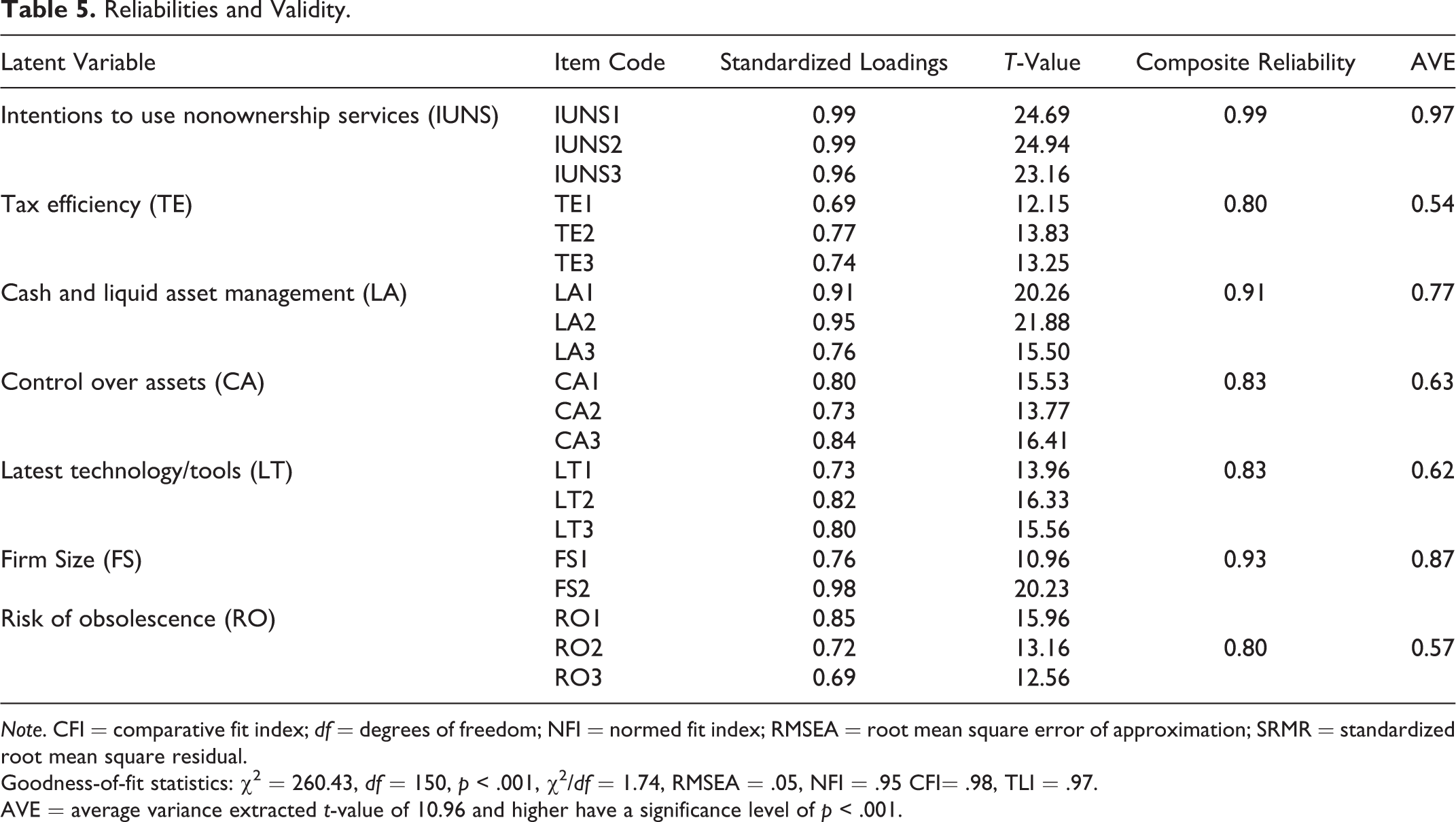

To investigate the quality of the measurement models we conduct a confirmatory factor analysis using AMOS 19. To ensure item reliability, factor loadings of 0.70 and t-values of 1.645 are used as cutoff values (Hulland 1999). As shown in Table 5, all of the items are above these values and indicate good item reliability. Also, we assess convergent validity by looking at the composite reliabilities and the average variance extracted (AVE). All of the values exceed the threshold values of 0.70 and 0.50, respectively. Thus, all of the measures show satisfactory reliability and convergent validity.

Reliabilities and Validity.

Note. CFI = comparative fit index; df = degrees of freedom; NFI = normed fit index; RMSEA = root mean square error of approximation; SRMR = standardized root mean square residual.

Goodness-of-fit statistics: χ2 = 260.43, df = 150, p < .001, χ2/df = 1.74, RMSEA = .05, NFI = .95 CFI= .98, TLI = .97.

AVE = average variance extracted t-value of 10.96 and higher have a significance level of p < .001.

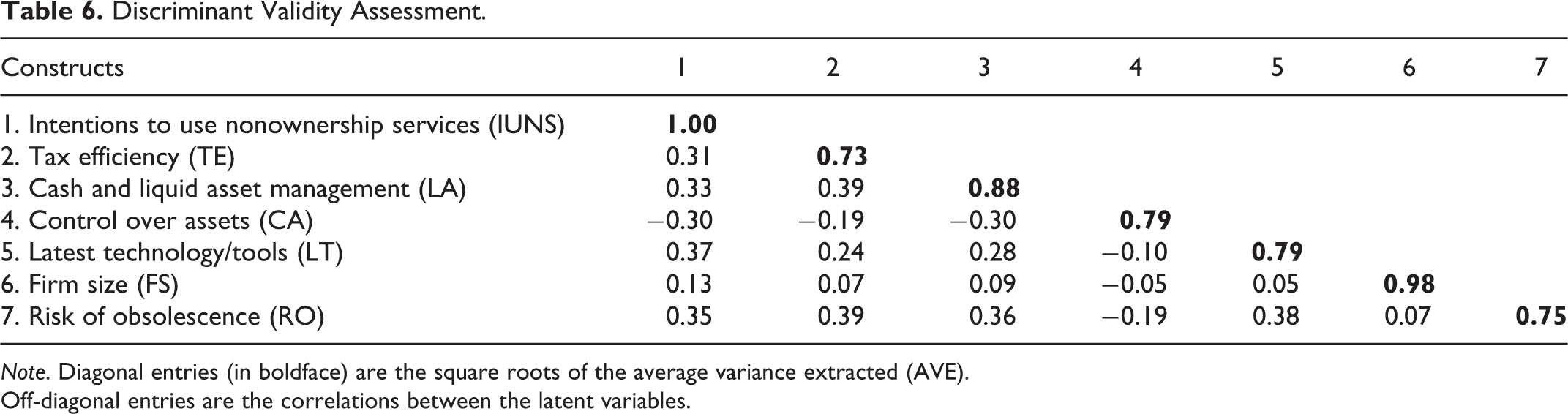

AVE and the Fornell-Larcker criterion are used to evaluate discriminant validity (Fornell and Larcker 1981). Again, all of the values are greater than the critical value of 0.50 for AVE. As shown in Table 6, all of the square roots of the AVEs of the constructs are greater than the correlations among the constructs, suggesting discriminant validity.

Discriminant Validity Assessment.

Note. Diagonal entries (in boldface) are the square roots of the average variance extracted (AVE).

Off-diagonal entries are the correlations between the latent variables.

Test for Interaction Effects

The interaction effect terms are constructed following the recommendations of Little, Bovaird, and Widaman (2006). We use residual centering to ensure orthogonality between the product term and its first-order constituents. We regress the product terms onto their first-order constituents constructs and save the residuals as indicators of the latent interactions.

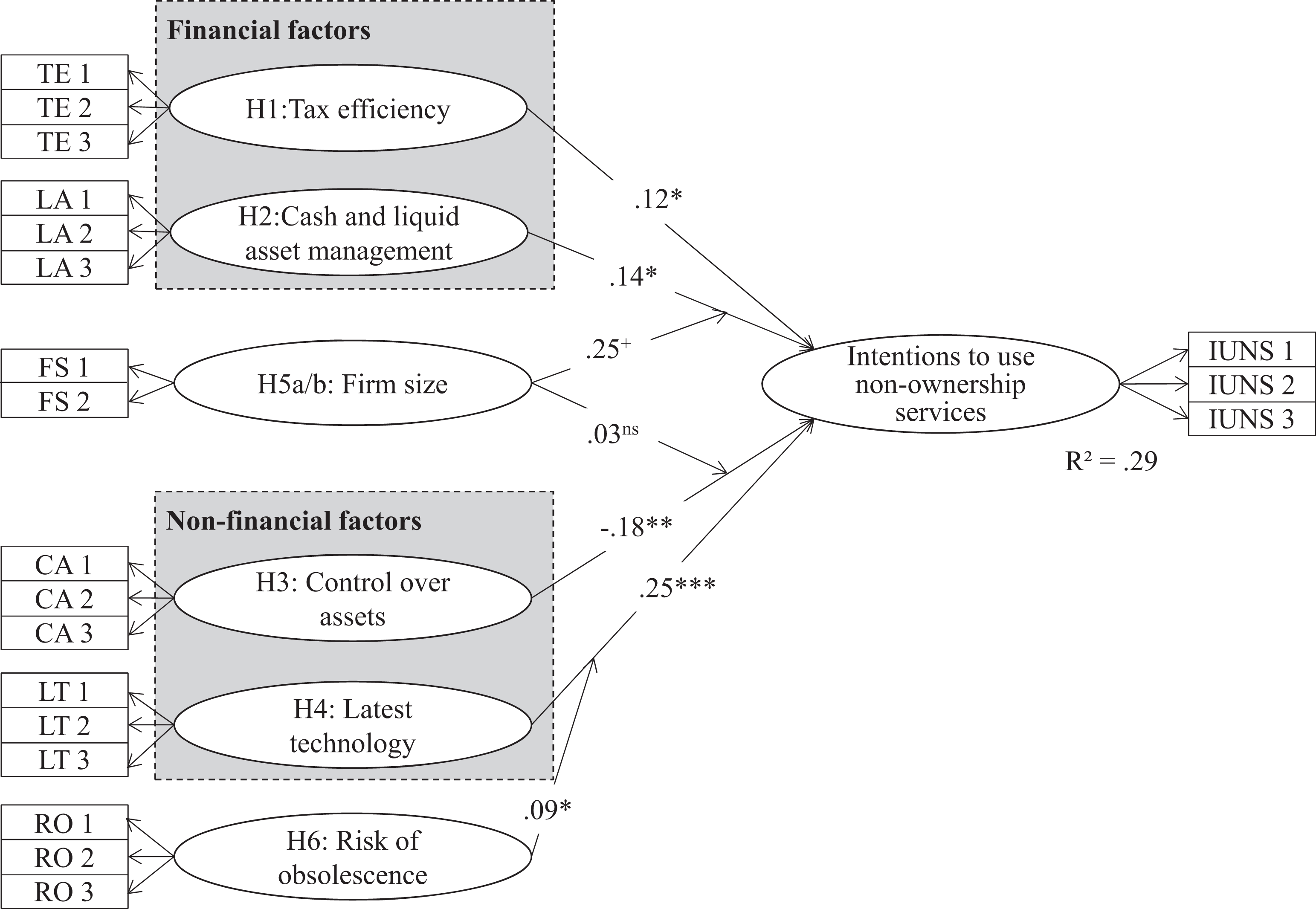

Structural Model

We first include the products of firm size and cash and liquid asset management (FS × LA), of firm size and control over assets (FS × CA), and of risk of obsolescence and latest technology and tools (RO × LT) into the main model and assess the structural model. To determine the significance of the hypothesized moderating effects, we compare the model without interaction effects to one that includes the interaction effects FS × CA, FS × LA, and RO × LT. Because the model fit improves significantly, the null hypothesis that there is no moderation is rejected.

The final model demonstrates good model fit, χ2 = 825.62, degrees of freedom (df) = 694, p < .001, χ2/df = 1.19, root mean square error of approximation (RMSEA) = 0.03, normed fit index (NFI) = 0.91, comparative fit index (CFI) = 0.98, Tucker-Lewis Index (TLI) = 0.98, and standardized root mean square residual (SRMR) = 0.05. Furthermore, the total variance of intentions to use nonownership services is satisfactory with an R 2 of 29%. Figure 2 provides an overview of the final model.

Results of the final structural model. Note: ns = coefficient is not significant at p > .10; + p < .10; *p < .05; **p < .01;***p < .001.

Hypotheses Testing

Hypothesis 1 suggests that firms striving for tax efficient ways to conduct business have higher intentions to use nonownership services. Our findings confirm Hypothesis 1 (b TE-IUNS = 0.12, p < .05) and are consistent with findings from other studies (e.g., Graham, Lemmon, and Schallheim 1998). We hypothesize in Hypothesis 2 that firms aiming for improved cash and liquid assets intend to use nonownership services. The results confirm Hypothesis 2 (b LA-IUNS = 0.14, p < .05) and support the findings of Sharpe and Nguyen (1995).

We suggest in Hypothesis 3 that firms desiring full control over their assets are less likely to have intentions of using nonownership services. Our results support Hypothesis 3 and display a significant negative path coefficient (b CA-IUNS = −0.18; p < .01). Therefore, the closer firms draw their external boundaries, the less inclined they are to use nonownership services.

The final model also provides support for Hypothesis 4, as latest technology and tools has a significant positive effect (b LT-IUNS = 0.25, p < .001) on firms’ usage intentions of nonownership services. Companies that intend to use the latest technology and tools are more inclined to use nonownership services. These firms may find that the short rental periods associated with nonownership suit their needs.

Hypothesis 5a suggests that firm size moderates the relationship between a firm’s liquid asset management and its nonownership service use intentions. The coefficient is in the hypothesized direction and marginally significant (b FS × LA-IUNS = 0.25, p = .07). As the qualitative study also provides good support for Hypothesis 5a (see Table 1), we interpret the combined findings as confirming Hypothesis 5a. Thus, the smaller the firm, the stronger the effect of the importance attached to retaining cash and liquid assets on nonownership use intentions.

Hypothesis 5b, that firm size moderates the relationship between control over assets and firms’ intentions to use nonownership services, is not supported (b FS × CA-IUNS = 0.03, p > .10). This finding is not surprising given that, of all of the hypotheses, Hypothesis 5b receives the lowest support in our qualitative interviews (see Table 1).

Hypothesis 6, which proposes the moderating effect of risk of obsolescence and the desire to use the latest technology on a firm’s usage intent of nonownership services, is supported. The path coefficient from the interaction term is significant at p < .05 (b RO × LT- IUNS = 0.09). This finding suggests that the more a firm feels that it is important to minimize obsolescence risk, the stronger the effect of the firm’s desire to use the latest technology is on their intentions to use nonownership services.

Implications, Limitations, and Future Research

This study investigates the determinants of corporate nonownership services use intentions. We empirically demonstrate that both financial (i.e., tax efficiency and liquid asset management) and nonfinancial (i.e., the desire to use the latest technology and tools, and the importance of asset control) factors are part of the organizational decision to obtain access to an asset through nonownership.

Implications for Theory

This study contributes to our understanding of nonownership services in a B2B context, and of the determinants of companies’ decisions to use such services. Our results extend the existing literature in several ways. First, our study contributes to the services marketing literature by following Lovelock and Gummesson’s (2004) call for further research on the rental/access paradigm. They criticize the literature for only considering leasing as an opportunity to market manufactured goods, and not as a type of nonownership and hence, as a service. Moreover, our study adds to conceptual nonownership research by providing a general definition of nonownership services. Lovelock and Gummesson focus on the different forms nonownership can take. Our research takes the next step and helps to clarify the nonownership framework by transferring a theoretically developed concept into practice. Previous studies have been concerned with the conceptual development of nonownership, whereas this study is one of the first to empirically analyze the theoretically formulated, nonownership construct.

Second, findings from this study yield insights into leasing behavior in both the finance and marketing fields. Our results demonstrate that nonfinancial factors have a stronger effect on companies’ usage intentions of nonownership services than financial considerations. Thus, the generally accepted assumption in the finance literature that tax and liquidity efficiency are the main (and perhaps only) drivers of firms’ intentions to use nonownership services seems questionable. Similarly, our findings contribute to the B2B marketing literature, where the determinants of corporate nonownership services use intentions have received scant scholarly attention (e.g., Anderson and Bird 1980). For both the finance and B2B marketing literature to be able to provide valuable recommendations for practice, research must empirically identify the determinants of leasing behavior (Tomkins, Lowe, and Morgan 1979). This study is one of the few studies to empirically investigate firms’ motivations for using nonownership services, and hence extends the practice-oriented literature on leasing.

Third, by defining leasing as a form of nonownership, this study considers leasing a service and brings the theoretical concept of nonownership to the B2B marketing literature. Our findings can provide managers with more focused recommendations on how to respond to the growing demand for nonownership services and how to better address the needs of these customers.

Fourth, our study demonstrates that a holistic model is needed to analyze the determinants of companies’ intentions to use nonownership services. In addressing the financial and the nonfinancial determinants of nonownership services use intentions, we combine insights from the finance literature with research from the field of marketing, allowing us to apply a broader perspective and consolidate knowledge from different disciplines.

Managerial Implications

Our research has implications for both client firms and providers of nonownership services. From a buyer perspective, it is important for management to evaluate which ownership or nonownership method best fits their overall business model and aligns with their strategic, operational, and financial goals. Selecting the right nonownership service may be crucial, as these business services can open new avenues for growth by releasing financial resources and management capacity (Ehret and Wirtz 2010). Furthermore, although previous research has suggested that firms primarily need to assess the financial benefits of nonownership and ownership options (Braund 1989), our findings show that additional factors play a role in the nonownership decision, with the most important being the desire to use the latest technology and tools. Following this finding, managers deciding whether to use nonownership services should consider both financial and nonfinancial factors.

Our results also show that nonownership services may be especially attractive to small firms seeking to preserve liquidity. They can negotiate contractual agreements with nonownership service providers to tailor the lease payments according to their cash flow generation pattern.

Overall, the flexibility of leasing contracts allows the design of customized solutions that maximize the buyer firm’s benefits. For example, companies interested in using the latest technology and tools, that do not want to bear the risk of equipment obsolescence, should choose short-term nonownership contracts such as operating leasing. Whether it is access to the latest technology or preserving liquidity, managers should clearly communicate the benefits they anticipate from nonownership services before they sign a contract, and should cooperate closely with their providers to maximize the value received.

There are also a number of implications for providers of nonownership services. Our quantitative study of the factors that determine firms’ choice of nonownership service providers provides some additional data. The data show that for more than two thirds of the respondents, the degree of adaptability of contracts is a decisive factor. This indicates that service providers may want to offer buyers the opportunity to renew the nonownership contract by replacing assets with newer versions. In particular, this helps to address the desires of customer firms whose goal is to remain current with the latest technology and tools and to transfer the risk of obsolescence. This approach has the potential to help service providers build an enduring relationship with their customers. Moreover, approximately two thirds of the respondents claim that communication over the phone or in-person are their preferred methods for gathering information regarding offered services. This finding underlines the critical role of sales in nonownership services. Due to their close involvement with decision makers and employees from customer firms, sales representatives from nonownership service firms require specific networking skills. Thus, they should be carefully selected and trained to understand the decision criteria used by potential customers when considering nonownership services.

In sum, most firms are still centered on the selling and marketing of goods rather than services, and do not focus on the benefits of services for the customer (Vargo and Lusch 2004). The perception of value during the initial service process (value in transformation) and, thereafter, the value in use, rests with the buyer (Moeller 2008). Given that customers do not initially buy a service, but rather a value proposition, offering customers the “right” value propositions is critical for providers of nonownership services, who should combine both financial and nonfinancial benefits into a compelling value proposition.

Limitations and Further Research

There are certain limitations in the context and method of this study. First, as our study focuses on the IT-leasing practices of SEMs in Germany, our findings might not be generalizable to large firms. Nevertheless, Anderson and Bird’s (1980) results show that large corporations also use nonownership services for nontax and noncash flow reasons. This suggests that the determinants of the nonownership services use intentions of large companies are similar to those of SMEs. Future research should examine the related intentions of large firms and compare the findings with our results.

Previous studies on nonownership (outsourcing and leasing) have concentrated on the use of nonownership services in American and British firms (e.g., Myers, Dill, and Bautista 1976). Our study focuses on the nonownership services use intentions of German firms and therefore offers insights from a different cultural context. Further research could extend our findings and investigate the use of nonownership services among firms in different global markets. As German companies generally tend to downplay the financial evaluation of projects compared to strategic factors when making investment decisions (Carr, Kolehmainen, and Mitchell 2010), further research may reveal that the nonfinancial determinants of nonownership services use intentions play a less important role in other countries.

Another potential limitation is that we investigate the determinants of only one type of nonownership service, namely leasing. Further research could add to our definition of nonownership service by empirically investigating the determinants of firms’ intentions to use other types of nonownership services, such as business process outsourcing. Dìaz-Mora (2008) suggests that companies not only outsource for financial reasons, but also for strategic reasons. Therefore, the determinants for corporate nonownership services use intentions may be similar among different types of nonownership services. Nevertheless, different types of contracts with varied property rights may result in diverse decision criteria.

Further research could also compare the use intentions of firms that have never used nonownership services with experienced nonownership service users. Additionally, to confirm our findings, we encourage researchers to assess firms’ nonownership services use over time, perhaps using their financial statements to assess the generalizability of our findings.

Previous research has suggested that to understand exchange relationships between firms it is necessary to analyze the dyadic between the industrial buyer and seller, and the network in which this relationship is embedded (e.g., Anderson, Håkansson, and Johanson 1994). An interesting avenue for further research would be to examine nonownership transactions from a vendor’s viewpoint.

Several studies have highlighted the importance of contracts in the efficient management of economic exchanges (e.g., Gavazza 2011; Kashyap, Antia, and Frazier 2012; Weber, Mayer, and Macher 2011). In nonownership transactions, the sharing of property rights to an asset incurs unique risks for both actors (Haase and Kleinaltenkamp 2011). As contracts clearly define the obligations and benefits of the parties involved, they are intended to reduce such risks (Lui and Ngo 2004). Therefore, firms offering nonownership services would benefit from guidelines on contract design to manage these risks. Previous studies have evaluated firms’ governance decisions and the contracts determining the efficiency of these transactions, using transaction cost logic (e.g., Ghosh and John 1999; Mayer and Salomon 2006) or agency theory (e.g., Kashyap, Antia, and Frazier 2012). To provide recommendations for practitioners on how to successfully design and manage nonownership transactions, further research could draw on transaction cost economics and agency theory.

According to the property rights literature in law and economics, the main benefit of ownership is that the owner can make changes to and derive values from the assets (e.g., through selling or leasing). When a firm leases assets, its legal rights over their use should be specified in the leasing contract. However, the contract may not fully specify rights for the lessee regarding certain aspects of the asset and/or under certain (previously unspecified) conditions. Contracts in dynamic market environments will necessarily be incomplete and unable to cover all contingencies. Future research could investigate governance mechanisms that help mitigate risks, addressing how contracts can be designed to deal with uncertainty.

Footnotes

Acknowledgments

The authors would like to thank the Editor and the three anonymous reviewers for their constructive comments that have significantly improved the manuscript. They also thank the participants of the 2011 Winter AMA conference for their valuable feedback.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors gratefully acknowledge support from a German leasing corporation.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.