Abstract

This paper focuses on asymmetric tax treaties and investigates from an empirical perspective the impact of OECD member states’ double tax relief method and of treaty tax-sparing provisions on investments in developing countries, while considering network effects. Our results suggest that having a treaty between the OECD member state and the developing country, which improves the investor's conditions in terms of tax burden, by changing the unilateral tax relief method, increases FDI to the developing country. The positive effect prevails when investigated within investments made through the direct route from residence to source. Results suggest that OECD member states offer tax-sparing provisions mostly to less-developed economies, which already receive very low FDI. Finally, we extend the investigation to an analysis of the impact of residence countries’ tax relief methods on source countries’ domestic tax policy. Our results suggest that developing countries set higher CIT rates when the OECD member state relieves double taxation through the exemption method, as compared to when it offers a foreign tax credit.

Keywords

Introduction

Today's global treaty network shows a tendency toward residence taxation, which implies that, if following their national law, source states can levy taxes without any limitations, the tax treaty shifts the taxing rights to the residence state because in many instances tax treaties limit the source state's taxing rights (Daurer 2014: 696). 1 The revenue cost of source tax limitations imposed by tax treaties will largely depend on the capital flows between the countries. While the revenue disparity is probably insignificant between two developed countries, 2 on the contrary, in the case of tax treaties between countries with asymmetric investment flows, a distributional conflict between net capital importers and exporters arises as the lowering of withholding tax rates, limiting the extent of source taxation, involves a revenue transfer from the net capital importer to the net capital exporter. Consequently, the reason why developing countries sign tax treaties with developed economies becomes questionable. For capital importers, encouraging inbound investment might be the focus, with policy makers wishing to attract foreign direct investment (FDI) (Braun and Zagler 2014).

A dramatic increase in FDI during the 1990s led to a boom in economic research studying the forces affecting FDI, in particular the effect of double taxation treaties on FDI. Whereas studies using aggregate country and country-pair-level data tend to find negative or no effect of DTTs on FDI (e.g., Blonigen and Davies 2004; 2005; Davies 2003; Egger et al. 2006), there is a tendency for studies based on micro-data to find some positive effects of DTTs (e.g., Davies, Norbäck, and Tekin-Koru 2009; Egger and Merlo 2011; Blonigen, Oldenski, and Sly 2014; Marques and Pinho 2014). Except for Petkova, Stasio, and Zagler (2020), previous research does not consider aspects of residence, conduit, and source tax systems, that is, treating the DTTs as a dummy variable. Previous research considers even less the complexity of DTTs, their domestic and international interactions, and the heterogeneity of the treaty content. In this paper, we aim to fill this gap by looking at the heterogeneity of the treaty content. We look at the treaty heterogeneity content, and aim to understand whether the change of the relief method in the OECD country due to the treaty with a developing country, and the inclusion of tax-sparing provisions in the treaty between the two, has a positive impact on FDI stocks in developing countries.

While countries can typically adopt a specific relief method in their domestic law, a double tax treaty can alter the applied relief method for a specific partner country. As MNEs care about their combined tax liability in both the source and the residence country, we expect that the source country's aim to attract more FDI will thus be frustrated, especially when the residence country imposes worldwide taxation. Whereas the credit method imposes the foreign CIT rate, the exemption method permits developing economies to implement a tax policy on their own. Consequently, we consider that the residence country's tax relief should reflect an additional gain that the investor gets when the treaty switches the relief method, and thus be a determinant which might incentivise foreign direct investments to the developing country. Second, in the hope of attracting FDI and given the sensitivity of FDI to taxes, developing countries make wide use of tax incentives for MNEs. For tax incentive measures not to be canceled out by the domestic tax policies of the other signatory state, developing countries can negotiate tax-sparing credits in bilateral tax treaties. In treaties with countries that use the credit method or that make exemption of foreign income conditional on a certain level of taxation in the source country, the inclusion of tax-sparing provisions under a tax treaty can ensure that the benefit of tax incentives of the source country is maintained. In the roots of the legal analysis, we investigate empirically the determinacy of tax-sparing agreements on FDI in developing countries while considering network effects.

Using a sample of tax treaties between 37 OECD member states and 71 low-and middle-income countries over the period 2005–2016, and bilateral FDI stock data from UNCTAD for the same observation period, our paper investigates the following research questions: (i) Does the relief method in the residence country (OECD member state) matter for the foreign direct investments in the source country (developing)?; (ii) Do the tax-sparing provisions affect foreign direct investment to developing countries? 3 We investigate both the impact of the tax relief method and of tax-sparing provisions on FDI in developing countries, while distinguishing between investments from developed countries to developing countries going through a direct route, and investment made through conduit countries, hence through an indirect route. This adds a further value to the contribution and novelty of our paper in the related area of research. On the grounds of the theory in Petkova, Stasio, and Zagler 2020, we investigate each of the research questions empirically, using a Poisson-pseudo-maximum-likelihood (PPML) estimator for the analysis of research questions (i) and (ii). We use as a dependent variable the bilateral FDI stocks in millions of dollars from the OECD member state to the developing country between 2005 and 2016 to investigate both research questions.

Our results suggest that the double tax relief method in the OECD member state is a determinant for the FDI in developing countries. Having a treaty between the OECD member state and the developing country, which improves the investor's conditions in terms of tax burden by changing the unilateral (domestic) tax relief method that the OECD member state would otherwise apply, results in an additional gain for the investor, and increases foreign direct investment to the developing treaty partner country. The positive effects prevail when investigated within investments made through the direct route from the OECD member state to the developing country, rather than through an eventual indirect route through conduit countries. In addition, we can only capture a negative between effect of the tax-sparing agreements included in the asymmetric tax treaty, on FDI stocks in developing economies, which suggests that OECD member states offer tax-sparing provisions mostly to less-developed economies, which already receive very low, if any, foreign direct investment.

The paper extends to a second part, where in addition we focus the analysis to an empirical investigation of a dogma which, as to our best knowledge, is questioned so far only from a legal perspective. As explained in Paolini et al. (2016), the relief method in the residence country of the multinational, may restrain the possibility of the source country to reduce taxes in order to attract foreign capital investments (p. 384). For instance, when taxes levied in the developing country are lower than those applicable in the developed country, the developed country will in fact levy its own taxes on income produced within the territory of the developing country. As a consequence, developing countries would refrain from compensating their more favorable domestic tax regimes by raising tax rates to the level of developed countries. In the paper, we investigate this from an empirical perspective, questioning (iii) whether the residence country's tax relief method restrains the source country's domestic tax policy. Our results suggest that developing countries set higher corporate income tax rates when the OECD member state treaty partner relieves double taxation through the exemption method, as compared to when it offers a foreign tax credit. This result would suggest that OECD member states offer the exemption method to developing countries, which impose high corporate income tax rates, while they offer nothing but a foreign tax credit to repatriated profits sourced in developing countries with low corporate income tax rates.

Results of the paper lead to two lessons to be learned for policymakers. First, developed countries are willing to concede tax sparing, but currently seem to offer it only to very poor countries with very limited FDI inflows. Developing countries may want to stretch the margin and try to be included into that category and negotiate tax sparing. Second, the paper clearly shows that countries that offer more generous relief methods will benefit from FDI inflows, pointing to tax competition and a potential race to the bottom. So far, we have not seen much tax competition going on, but this may change, unless countries coordinate their treaty policies, at least on a regional level.

The remainder of the paper is organized as follows. The second section reviews the literature. Third section 3 presents the research questions (i) and (ii). Fourth section focuses on the investigation of research question (i) and (ii), where the subsection represents the data; shows the theoretical basis for the main variables’ construction; discloses the empirical methodology; discusses the results of the analysis; while in the next subsection. several robustness checks are explained and discussed. The fifth section is dedicated to the investigation of research question (iii). The sixth section concludes.

Review of Previous Literature

A dramatic increase of FDI during the 1990s led to a boom in economic research studying the forces that affect it. A part of this literature looks at the relation of government policies and FDI. Blonigen and Davies (2004) were the first to explore the effects of tax treaties on foreign direct investment, using data over the period 1966–1992 on U.S. inbound and outbound FDI, and concluding that tax treaties have a strong positive impact on FDI. Davies (2003) examines the impact of treaty renegotiations over the period 1966–2000 on both inbound and outbound U.S. FDI, suggesting that treaties have either zero or even a negative effect on FDI. 4 Similar to Davies (2003), Blonigen and Davies (2004), focusing on U.S. inward and outward investment stocks, find that DTTs have no positive effect on inward or outward FDI. Using inbound and outbound FDI stock and flow data for OECD countries between 1982 and 1992, Blonigen and Davies (2005) show that the treaty age makes a difference, that is, old treaties have a positive and significant effect on FDI, while the opposite states for new treaties. Egger et al. (2006) estimates the effect of tax treaties on bilateral outward FDI from OECD countries over the period 1985–2000 and find a negative average treatment effect of DTTs on FDI. Di Giovanni (2005) examines the impact of various macroeconomic and financial variables on cross-border M&A activities as a component of FDI, suggesting that a DTT is accompanied by increased cross-border acquisition activities. Coupé, Orlova, and Skiba (2009), using fixed and random effects, as well as an instrumental variable (IV) strategy to estimate a gravity model, do not find any evidence of the impact of DTTs on FDI flows for a sample of OECD source countries to transitioning economies between 1990 and 2001. Instead, Barthel, Busse, and Neumayer (2010) show that DTTs are indeed positively associated with foreign investment in the source country, while their results hold for different specifications of the econometric model. Lejour (2014) concludes that new tax treaties increase bilateral FDI by 21% if the tax treaties are instrumented with geographic variables, although this effect tempers out after ten years. In addition, the author finds that treaty shopping exists, but does not attempt to quantify how much it contributes to the increase in FDI stocks.

Whereas studies using aggregate country and country-pair-level data tend to find negative or statistically insignificant results, there is a tendency for studies based on micro-data to find some positive effects of DTTs (Petkova, Stasio, and Zagler 2020: 3). Davies, Norbäck, and Tekin-Koru (2009) and Egger and Merlo (2011) analyze the extent at which bilateral tax treaties affect foreign investment decisions at the extensive margin (i.e., location decisions) and intensive margin (i.e., level of investment). Both studies find that the existence of a tax treaty with the parent country, respectively with Sweden and Germany, increases the probability of a multinational having a subsidiary in each treaty partner country. Blonigen, Oldenski, and Sly (2014), using U.S. firm-level data for the period 1987–2007 from the Bureau of Economic Analysis (BEA), find a positive effect of DTTs on foreign direct investment, which is larger for firms that use differentiated inputs. Marques and Pinho (2014) analyze the extent to which tax treaties influence the number of new foreign subsidiaries incorporated by European multinationals between 2000 and 2009. They provide evidence that tax treaties induced a positive and significant impact on the number of foreign subsidiaries incorporated in the last decade. In contrast to Marques and Pinho (2014), Petkova, Stasio, and Zagler (2020)—building on previous literature, which focuses on the relationship between tax treaties and FDI by initiating the use of network analysis in the international tax field (e.g., Mintz and Weichenrieder 2010; Dreßler 2012; Weyzig 2013) 5 —consider the possibility of treaty shopping and measure the impact of tax treaties relative to domestic law. The authors treat the international tax system as a network and subsequently account for treaty shopping potential when estimating the effects of DTTs on FDI. Differentiating between relevant and neutral DTTs—that is, tax treaties that offer investors a financial advantage—and irrelevant DTTs, the authors find that only relevant and neutral tax treaties increase bilateral FDI, whereas irrelevant DTTs do not.

The sample of most existing studies on the impact of DTTs on FDI flows includes both developed and developing countries as potential source countries. The grouping of both types of countries in an empirical analysis, that is, the simultaneous presence of both OECD and developing countries in the sample, can be problematic because the investment location decisions in developed and developing countries are likely to be determined by very different factors (Blonigen and Wang 2004; Neumayer 2007). Exceptions are Neumayer (2007), Baker (2014) and Braun and Fuentes (2016).

Neumayer (2007) investigates whether DTTs with the United States attract more FDI to developing countries. This study suggests that developing countries that sign a DTT with the United States benefit from a higher FDI stock and share of FDI stock originating from U.S. investors. However, once the sample of developing countries is split into low-income and middle-income countries, the positive effect is only found for the latter group. Baker (2014), using a dataset between 1991 and 2006, shows that DTTs do not have any effect on FDI, explaining this with a further qualitative analysis of the domestic tax legislation of developed countries. Finally, Braun and Fuentes (2016) analyze the Austrian DTT network with developing countries, looking at the effects of DTTs on Austrian outward foreign direct investment (OFDI). Their analysis suggests that middle-income countries signing a DTT with Austria may expect an increased number of foreign direct investment projects from Austrian companies. 6

Our paper adds to these studies and overcomes the limitations of grouping both developed and developing countries in an empirical analysis. Accordingly, we restrict the analysis to double taxation treaties signed between countries with asymmetric investment flows, where developed countries are considered as residence countries of the MNEs, and the developing countries are considered as the source countries of the MNEs.

Research Questions

From a tax policy perspective, offering a tax credit for the foreign taxation by the country of residence, reduces the possibilities for developing countries to attract foreign capital through tax policy, because a reduction of such tax by the country of source turns into a lower credit against taxes due in the country of residence. Consequently, the tax relief method in the residence country is a major and probably the most determinant for the FDI to developing economies (Paolini et al. 2016: 384). Based on this rationale, in this study, we investigate empirically (i) whether the relief method in the residence country (OECD member state) matters for the foreign direct investments in the source country (developing)?

There are roughly five different relief methods available to avoid double taxation: exemption, indirect credit, direct credit, deduction, and no relief (Petkova, Stasio, and Zagler 2020). Countries can typically adopt a specific relief method in their domestic law, but a double tax treaty can alter the applied relief method for a specific partner country. DTTs contain a provision on the method of double tax avoidance, specifying that, where exclusive tax jurisdiction over certain income is allocated to the country of source, the initial responsibility for preventing double taxation is on residence countries by granting their residents exemption or a foreign tax credit. Whereas the credit method imposes the foreign corporate income tax rate, the exemption method permits developing economies to implement a tax policy on their own (Paolini et al. 2016). The exemption method entails a residence country altogether excluding foreign income from its tax base, with the source country being given the exclusive right to tax. Exemption in the residence state can therefore lower the overall tax burden of the investor if tax concessions are granted by the source country. On the other hand, the credit method entails the resident remaining liable in the country of residence on its global income. However, a credit for tax paid in the source country is given by the residence state against its domestic tax, as if the foreign (source) tax were paid to the country of residence itself. Hence, the credit method leads to a stable tax rate, as any lowering of tax rates in the source state is calculated against the resident state's tax rate. While the exemption method puts investors in a more favorable condition in terms of tax burden as compared to the foreign tax credit, both methods are more advantageous than a simple deduction, or than the refusal to grant a tax relief in the country of residence. Accordingly, as multinationals care about their combined tax liability in both the source and the residence country, the source country's aim to attract more FDI will thus be frustrated, especially when the residence country imposes worldwide taxation (Azémar and Dharmapala 2019). We expect the outward FDI stocks from the OECD member state to the developing economy to react to the change in the OECD member country's relief method once a treaty between the two countries is signed. This, because changes in the residence country's tax relief should reflect an additional gain that the investor gets when the treaty switches the relief method, that is, when the relief method applied under the treaty differs from the unilateral (domestic) relief method.

(ii) Do the tax-sparing provisions affect foreign direct investment in developing countries? In order to promote FDI and consequently boost local economic growth, developing countries are frequently willing to offer substantial fiscal incentives to international investors. Tax holidays and preferential tax rates remain by far the most widely used incentive instruments in developing countries (Andersen, Kett, and von Uexkull 2018). However, the tax system in the country where the parent company is headquartered, that is, where the MNE is based, makes a significant difference in how effective these measures are. Residence countries with worldwide tax systems impose tax on the active foreign business income of resident. Residence countries with territorial (or exemption) systems exempt the active foreign income of their MNEs from residence country taxation. However, both worldwide and territorial residence countries typically tax the passive foreign income earned by their resident MNEs. For instance, when a source country initiates a tax holiday for an MNE based in a worldwide residence country, the tax holiday's benefits to the MNE may be entirely or partially offset by higher taxes owing to the residence country. This is because, when a local affiliate sends a dividend to the parent, the reduced tax paid to the source nation reduces both the parent's tax burden and the tax credit available to the parent in its residence jurisdiction (Azémar and Dharmapala 2019: 89–90).

For tax incentive measures not to be canceled out by the domestic tax policies of the other signatory state, developing countries can negotiate tax-sparing credits in bilateral tax treaties. Tax sparing is the practice by which capital-exporting countries amend their taxation of foreign source income to allow firms to retain the advantages of tax reductions provided by source countries. Specifically, tax sparing often takes the form of allowing firms to claim foreign tax credits against residence-country tax liabilities for taxes that would have been paid to foreign governments, in the absence of special abatements, on income from investments in certain developing countries (Hines 2001). In treaties with countries that use the credit method or that make exemption of foreign income conditional on a certain level of taxation in the source country, the inclusion of tax-sparing provisions under a tax treaty can ensure that the benefit of tax incentives of the source country is maintained.

Legal analysis predominantly suggests that the tax-sparing provisions are regarded as tools of economic development that foster the flow of FDI to developing countries since they can ensure that the benefit of the source country's tax incentives is maintained (e.g., Dagan 2000; Pickering 2013). 7 Empirical literature on the effects of tax-sparing agreements on investments is quite limited, and there exist just a few studies suggesting that tax sparing is an important determinant of FDI (Hines 2001; Azémar, Desbordes, and Mucchielli 2007; Azémar and Dharmapala 2019).

We replicate prior literature investigation looking at the impact of tax-sparing agreements on FDI by analyzing it in a panel data of asymmetric double tax treaties between 37 OECD members states and 71 developing economies. In addition, the novelty of our paper consists on the estimation of tax-sparing provisions’ effect on FDI, while considering network effects. We distinguish between a direct route and an indirect route through conduit countries for investments from OECD countries to developing countries. We expect the positive impact of tax-sparing provisions on FDI in developing countries to be greater when investors choose the direct route to invest from residence (OECD members) to source (developing countries), since it offers the shortest tax distance.

Treaty Heterogeneity Content and FDI in Developing Countries

Data

This paper uses a dataset of double taxation treaties between 37 OECD member states, considered as developed (capital-exporting) countries, and 71 developing (capital-importing) countries. We follow prior literature, which uses OECD members as proxy for developed countries and non-OECD members as proxy for developing. We consider as developing countries those classified as low income, lower-middle income, and upper-middle income economies in the World Bank classification 8 at the initial period of the analysis, that is, 2005. The time dimension considered for the investigation of the research questions is between 2005 and 2016. Accordingly, our dataset is a dyadic panel data set that consists of country-pairs with a developing country on the one hand and an OECD member state on the other hand, which have an effective tax treaty either for some or for all the years between 2005 and 2016.

Data for the existence of a double tax treaty between each of the OECD member states and developing countries is taken from the most comprehensive available dataset of bilateral tax treaties, that is, IBFD Tax Research platform, as well as from the tax treaties database from Petkova, Stasio, and Zagler (2020). 9 Information taken includes the treaty's year of signature, year of effectiveness, termination of the treaty, re-signature, as well as years of amendments by protocols. Overall, we consult 946 tax treaties that became effective before 2016, to hand-collect the relevant withholding tax rates and method of double tax relief from the respective DTTs and applicable protocols. We use the IBFD Global Corporate Tax Handbooks (2005–2016) to collect information on the domestic tax system and on taxation of foreign income, including the methods of double taxation, as well as domestic corporate and withholding tax rates from the respective yearbook. For data not available in the IBFD handbooks, we rely on EY Corporate Tax Guides (2005–2016), PwC Worldwide Tax Summaries (2005–2016), Deloitte, and most importantly, various national websites. Furthermore, the treaty network might be subject to changes, that is, new treaties becoming effective; treaties being terminated at a later point in time; the conditions of the treaties being changed through protocols in the following years; the conditions of the treaties being altered through amendments in domestic law (Petkova, Stasio, and Zagler 2020: 582). We take all these changes into consideration when manually collecting data on international tax networks.

Another relevant variable of the empirical investigation is the inclusion of the tax-sparing provisions in each of the treaties of the country-pairs. We code tax-sparing agreements by searching the text of each bilateral tax treaty between any of the OECD members and any of the developing countries for language specifying a tax-sparing provision. Following Azémar and Dharmapala (2019), we searched in particular for the “shall be deemed to include” language, and for language that is similar in function.

Data on bilateral inward FDI stocks (in millions of dollars) between 2005 and 2016 is obtained under special request from UNCTAD's database. We invert it to measure the investment from the residence to the source country. Note that our analysis is unidirectional, therefore in our data set we only have information on investments from the OECD member country (residence) to the developing country (source). Since the available data reports only the immediate residence to source country FDI stocks, we estimate the impact of the relief method and of tax-sparing provisions on these immediate residence to source country FDI stocks. The dataset is identified at the country-pair-year level—that is, each observation represents the FDI stock held by investors from residence country o in source country d in year t. In principle, the same country could appear as both a residence and a source country, and FDI from residence country o in source country d in year t would represent a separate observation from FDI from residence country o in source country d in year t. However, this does not occur in our data, because residence countries are restricted to be developed (OECD member states) and source countries to be developing.

Following prior literature on the impact of tax treaties on FDI, as control variable, we include the bilateral investment treaties (BITs) signed between the OECD member states and developing countries. Information on BITs is taken from the Investment Policy Hub of UNCTAD, as well as from the International Centre for Settlement of Investment Disputes (ICSID) World Bank Group database.

Theory basis

We rely on the theoretical background of Petkova, Stasio, and Zagler (2020) to calculate the tax distance between the two countries, where authors define the tax distance as “the cost of channelling corporate income from one to another in terms of taxes to be paid” (p. 579). In line with that study, in our analysis the tax cost of a multinational enterprise (MNE) consists of corporate income taxes and non-resident withholding taxes on the income of the subsidiary. Depending on the relief method applied in the resident country o on income from source country d,

10

the combined effective tax rate tdo (relief method) for the multinational company can be defined as: a) tdo (no relief) = 1 − (1 − td) (1 − wd) + to − tdto b) tdo (deduction) = 1 − (1 − td) (1 − wd) (1 − to) c) tdo (direct credit) = max {1 − (1 − td) (1 − wd), 1 − (1 − td) (1 − to)} d) tdo (indirect credit) = max {1 − (1 − td) (1 − wd), to} e) tdo (exemption) = 1 − (1 − td) (1 − wo)

We make use of the above formulas to calculate two types of tax burdens included in the main analysis, that is, the After-treaty-tax-burden and the Absent-treaty-tax-burden.

The After-treaty-tax-burden is the combined effective tax rate (tax cost) for the multinational enterprise which consists of corporate income taxes to be paid in the country of residence of the parent, corporate income taxes to be paid in the country of source, and withholding taxes on the income of the subsidiary to be paid in the source country, calculated according to the tax relief method in the resident country applied under the effective treaty between the OECD member country and the developing country, that is, taking into consideration the change in the residence's tax relief method due to the treaty.

The Absent-treaty-tax-burden is the combined effective tax rate (tax cost) for the multinational enterprise, which consists of corporate income taxes to be paid in the country of residence of the parent, corporate income taxes to be paid in the country of source, and withholding taxes on the income of the subsidiary to be paid in the source country, as if the double tax treaty between the OECD member country and the developing country had not unilaterally changed the tax relief method in the OECD country: that is, as if the residence country had continued to apply the unilateral relief method despite the effective treaty with the source country. Thus, in calculating the tax burden, tdo, we consider the corporate income taxes to be paid in the country of residence of the parent, corporate income taxes to be paid in the country of source, and withholding taxes on the income of the subsidiary to be paid in the source country as negotiated under the treaty, while the relief method at residence equals the one that would have been applied in the absence of the treaty. 11 In this way, the difference between the Absent-treaty-tax-burden and After-treaty-tax-burden is only due to the relief method in the resident country. Differently from the calculation of After-treaty-tax-burden, in the calculation of the Absent-treaty-tax-burden, each of the taxes is equal to the rates under the double tax treaty, while the tax relief method is equal to the relief method under the domestic law, and thus to the relief method as if there were not an effective double tax treaty between the country-pair, even when actually there is an effective double tax treaty which has changed the unilateral residence's tax relief. It is relevant to underline that Absent-treaty-tax-burden differs from After-treaty-tax-burden only for country-pairs for which the tax treaty relief method differs from the unilateral (domestic) tax relief method.

While the analysis of treaty shopping and the identification of conduit countries is not the main purpose of this paper, we do understand that both the residence country's tax relief method and the inclusion of the tax-sparing provisions in the treaty between the OECD member state and the developing country matter for investments from the former to the latter, if investors choose the direct route to invest in the developing country, instead of an indirect route through conduit countries. Therefore, the analysis extends to a distinction between treaties, which make the direct investment from residence to source more convenient in terms of tax distance than investing through an indirect route.

We add a dummy variable, which equals one if the direct route exhibits a shorter tax distance than an indirect route, namely the variable Direct_cheap. In order to encode this dummy variable, we make use of two variables as constructed and taken from Petkova, Stasio, and Zagler (2020), that is, DirectTaxDistance and distance_minimum. 12 While the DirectTaxDistance is the tax distance, that is, the effective tax rate on overseas profits, taking into account a possible tax treaty between the two countries, the distance_minimum is the minimum indirect cost between any two countries, that is, the lowest tax distance, considering intermediate countries (up to a maximum of two conduit countries). Accordingly, if the DirectTaxDistance equals the distance_minimum, investing directly from residence to source is the cheapest route in terms of tax distance. Otherwise, if the DirectTaxDistance is bigger than the distance_minimum, then there is a cheaper route, which goes through one or two conduit countries and it is the minimum distance, that is, the cheapest route through the network. Comparing the DirectTaxDistance with the distance_minimum, if they are equal, investors do not use a conduit, while if the distance_minimum is lower than the DirectTaxDistance, apparently, they use a conduit, which makes it cheaper. Our dummy variable Direct_cheap equals one in the first case (DirectTaxDistance = distance_minimum) and zero otherwise (DirectTaxDistance > distance_minimum).

As can be observed in Table A1 in Online Appendix 1, the sample includes 753 asymmetric tax treaties in 2005, that is, in the initial year of the observation period, and 939 asymmetric tax treaties in 2016, that is, in the last year of the observation period. In 2005, the OECD member countries relieve double taxation on cross-border dividends through a foreign tax credit (direct and indirect) in 78.74 percent of the effective tax treaties, and through the exemption method in 21.24 percent of them. In 2016, the OECD member countries relieve double taxation through a foreign tax credit (direct and indirect) in 79.65 percent of the effective tax treaties, and through the exemption method in 20.34 percent of them.

After constructing the dummy variable containing qualitative information on whether the direct route is the cheapest route to invest from the OECD member country to the developing country, we count that in 2005 (2016), in 52.72 percent (44.51 percent) of the cases (country-pair-year obs.), the direct route exhibits a shorter tax distance than the indirect route, that is, investing through conduit countries.

The two graphs in Figure 1 in Online Appendix 1, show the percentage of treaties for which the residence country's double tax relief method, once the treaty becomes effective, remains equal to the residence country's unilateral double tax relief method (see bar “Equal”), and the percentage of treaties for which the residence country's double tax relief method, once the treaty becomes effective, differs from the residence country's unilateral double tax relief method (see bar “Different”). This is represented respectively for 2005 and 2016. In 2005 (2016), in 64.70 percent 13 (73.0 percent) 14 of the effective tax treaties in place between OECD member states and developing economies, the bilateral tax relief method at residence differs from the unilateral tax relief method, which would otherwise apply (i.e., in the absence of the treaty).

Table A2 in Online Appendix 1 provides summary statistics for variables used in the empirical analysis for the estimation sample.

Empirical Methodology

We investigate first whether the residence country's double tax relief method has an impact on the foreign direct investments from OECD member countries to low- and middle-income countries, which have an effective tax treaty for the elimination of the double taxation in force. Second, we extend the analysis to the tax-sparing provisions, and investigate whether the inclusion of tax-sparing provisions in asymmetric tax treaties has an impact on the investments from the developed treaty partner country to the developing treaty partner country. In analyzing both questions, we consider the possibility for treaty shopping that might give multinational companies benefits, such as lower or no withholding taxes. Following Petkova, Stasio, and Zagler (2020), we evaluate whether the direct tax distance investing from the OECD country (residence) to the developing country (source) is lower than the indirect tax distance, that is, investing from residence to source through conduit countries, and allow for a differential effect of the residence country's relief method and of tax-sparing provisions on FDI.

We exploit our panel data to investigate each of the questions estimating an empirical model, which looks like the following:

The first two variables of interest are Absent-treaty-tax-burdeno−d,t and After-treaty-tax-burdeno-d,t. Since these two variables enter the regression simultaneously, we find it relevant first to make sure that they do not have a high correlation between the two. 20 Second, the dummy variable, namely Direct_cheapo−d,t, indicates whether the direct route of investing from country o (OECD member country, residence) to country d (developing country, source) exhibits a shorter tax distance than a possible/eventual indirect route through conduit countries. Thus, it equals one if investing directly from the OECD member country to the developing country exhibits a shorter tax distance than investing through an indirect route, that is, using conduit countries, and zero otherwise. In order to investigate for the effect of the Absent-treaty-tax-burden and After-treaty-tax-burden within investments going from residence to source through an indirect route, the Direct_cheapo−d,t enters interacted with both Absent-treaty-tax-burdeno−d,t and After-treaty-tax-burdeno−d,t; Xo−d,t is a vector of control variables, which in our case is only a dummy variable controlling for a BIT within the two countries (OECD member country and developing country) in year t; finally, ηd,t denotes time-varying source country fixed effects, θo,t denotes time-varying residence-country fixed effects, and γod denotes country-pair fixed effects; εd,t is the Poisson error term. Time-varying source country and residence-country fixed effects absorb any between country variation over time, while country-pair fixed effects control for physical distance between the source and the residence country (see Wooldridge 2010; Baier and Bergstrand 2007). 21 Thus, we restrict the analysis to the within-country-pair variation over time. The ppml-panel_sg STATA command by default clusters standard errors at country-pair level.

Since our dependent variable FDIo−d,t is in level form, the coefficient can be interpreted analogous to a log-linear estimation, where a unit increase in the regressor will lead to a 100(eβ −1) percentage increase in the dependent variable. Because the PPML estimator does not allow for negative values of FDI stocks, we replace the negative FDI stocks with zero in our main analysis. 22 We extend the analysis and re-estimate equation (1) adding a dummy variable, namely Tax sparingo−d,t, which contains qualitative information on whether the tax treaty between the OECD member state and the developing country in year t includes tax-sparing agreements, which enforce the residence country to allow firms to claim foreign tax credits against residence-country tax liabilities for taxes that would have been paid to foreign governments, in the absence of special abatements, on income from investments in the developing treaty partner country. We investigate the impact of tax-sparing provisions on investment from OECD member states to the developing countries, while controlling for the relief method effect, as well as allowing for a differential effect between treaties which make the direct route cheaper than an indirect route through conduit countries, that is, introducing an interaction term between tax sparing dummy, Tax sparingo−d,t and Direct_cheapo−d,t.

Results

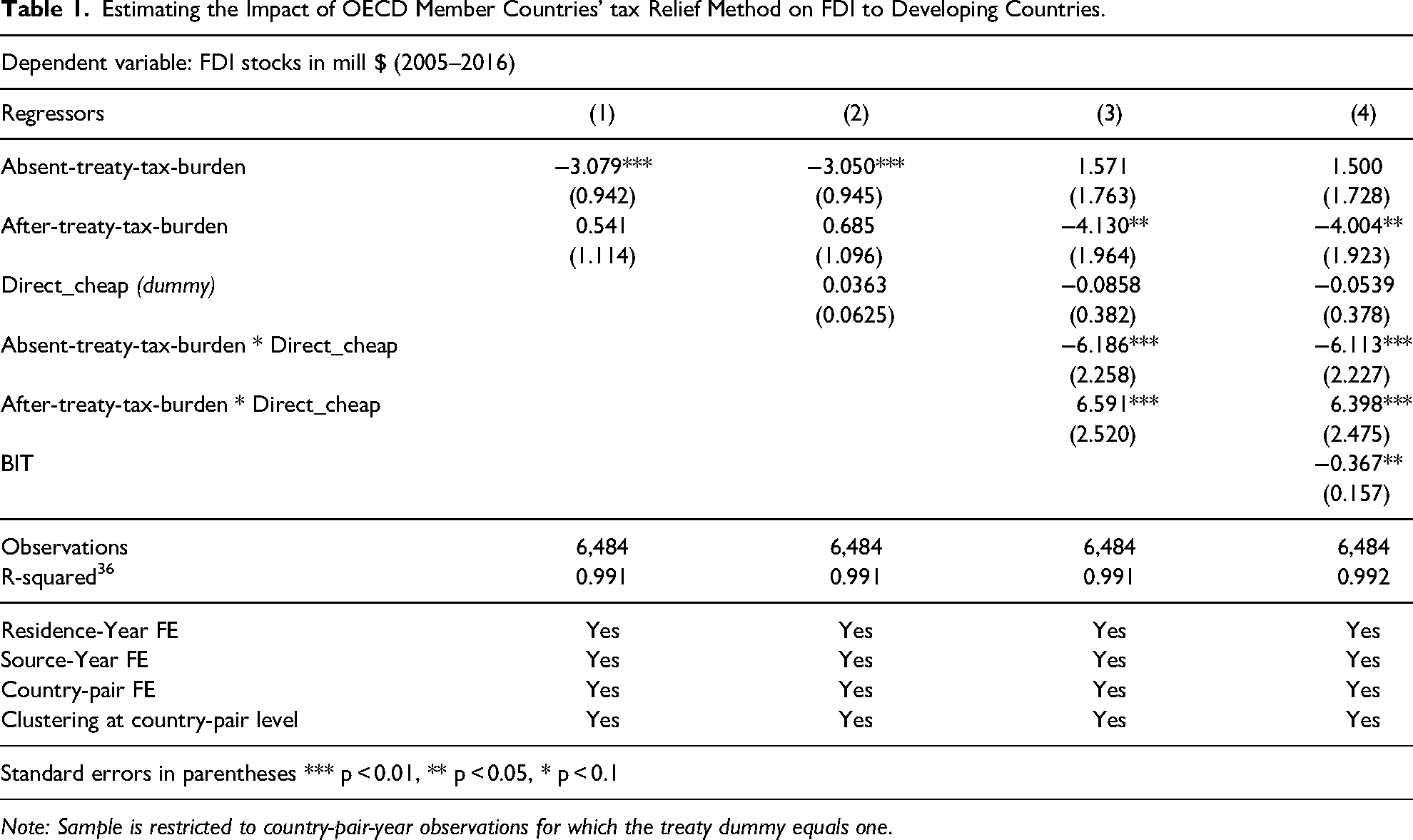

Results of the estimation of equation (1) are represented in Table 1. All the specifications (columns 1–4) include residence-year, source-year and country-pair fixed effects. Standard errors are clustered at country-pair level.

Estimating the Impact of OECD Member Countries’ tax Relief Method on FDI to Developing Countries.

Note: Sample is restricted to country-pair-year observations for which the treaty dummy equals one.

First, in column 1, we introduce only the two types of tax burden, that is, After-treaty-tax-burden, which is the tax burden that the investor investing in the developing country actually bears due to the tax treaty in place within the country-pair; and Absent-treaty-tax-burden, which is the tax burden that the investor investing in the developing country would bear, if the OECD member state (residence) had continued to apply the unilateral tax relief method, hence, if the treaty between the OECD member state and the developing country had not changed the residence country's unilateral (domestic) tax relief method. Both tax burdens enter the regression in decimals.

We obtain a strongly statistically significant negative effect of the Absent-treaty-tax-burden on FDI stocks in developing countries, where increasing by 10 percentage points the Absent-treaty-tax-burden decreases FDI stocks by almost 9.5 percent. 23 Accordingly, while the tax treaty is expected to improve the investor's tax burden, either through lower withholding tax rates at source, or through a more advantageous tax relief method, then a treaty, which although it lowers the withholding tax rates does not improve the relief method, can actually deteriorate investments to developing countries.

On the other hand, the coefficient on the After-treaty-tax-burden is positive, although statistically insignificant. Unfortunately, at this point we can only make use of the positive sign of the coefficient on the After-treaty-tax-burden, to interpret it as the additional gain that the investor gets 24 when the residence country imposes a different relief method from the unilateral (domestic) one, hence when the treaty between the partners improves the tax relief method. 25 Although the effect is only insignificantly positive, the sign of the coefficient is due to the switching to a more favorable relief method (i.e., from credit method to exemption, or from no relief to credit). Although part of it may be due to cases where the opposite happens (e.g., switching from exemption to credit method), these cases do not matter, since the more favorable domestic relief method prevails (e.g., exemption).

In column 2, we distinguish between tax treaties that make the direct route the cheapest route in terms of tax distance to invest in the developing country, as compared to an eventual indirect route through conduit countries, introducing Direct_cheap, which equals one if the direct route exhibits the shortest tax distance, and zero otherwise. While the coefficient on the dummy variable is positive, we cannot say that the level of FDI stocks in developing countries is statistically significantly higher when the direct route exhibits the shortest tax distance as compared to when an indirect route is cheaper.

Particularly relevant for our analysis are the estimation results in columns 3 and 4, where each of the tax burdens enters interacted with the Direct_cheap(dummy), that is, Absent-treaty-tax-burden*Direct_cheap and After-treaty-tax-burden*Direct_cheap, allowing us to look at the impact of respectively Absent-treaty-tax-burden and of After-treaty-tax-burden on our dependent variable, when investors choose the direct route to invest from the OECD member state to developing country. The coefficients on both interaction terms result statistically strongly significant, suggesting that the impact of the Absent-treaty-tax-burden and of the After-treaty-tax-burden on FDI stocks to developing countries differs between investments through the direct and indirect route.

Results suggest that for country-pair-years for which the direct route is the cheapest and FDI investments go directly from the OECD member country to the developing country, an increase in the Absent-treaty-tax-burden by 10 percentage points decreases FDI stocks by almost 9.9 percent, 26 the effect being statistically significant at the 1 percent significance level. Accordingly, once the investors are investing through the direct route, increases in the tax burden that they would bear due to a tax treaty, which however does not change the residence country's tax relief method, discourage FDI. On the other hand, we find a very large positive effect of the After-treaty-tax-burden on FDI stocks in the cheapest direct route, that is, an increase by 10 percentage points in the After-treaty-tax-burden increases FDI stocks by more than 10 percent, 27 which reflects the advantage gained when the relief method switches following the treaty's year of effectiveness. Finally, the different effect of the Absent-treaty-tax-burden and of After-treaty-tax-burden on the FDI stocks is strongly statistically significant. An increase in the difference between the Absent-treaty-tax-burden and After-treaty-tax-burden by 10 percentage points, decreases FDI stocks that go through the direct route by almost 9.9%. 28

Note that the coefficients on the single terms Absent-treaty-tax-burden and After-treaty-tax-burden, respectively 1.571 and −4.130, capture now the impact of each of the tax burdens on FDI stocks in country-pair-year observations for which the indirect route exhibits the shortest tax distance (hence for which Direct_cheap(dummy) equals zero). While the Absent-treaty-tax-burden has no effect on FDI stocks within the indirect route, the After-treaty-tax-burden has a negative effect on them, which is statistically significant at the 5 percent significance level. Thus, if the direct route does not exhibit the shortest tax distance, and investments go from residence to source through conduit countries, increases in the After-treaty-tax-burden significantly reduce FDI, which might be explainable by countries not using the indirect route, that is, sometimes the advantage gained is so small that firms simply do not build conduit structures and choose the direct route, nevertheless.

In column 4, we control for the bilateral investment treaty within the country-pair, which has a negative effect on FDI stocks of almost 30.7 percent. 29 While the negative effect of the Absent-treaty-tax-burden on FDI stocks in the direct route being the cheapest remains strongly statistically significant, the positive effect of the After-treaty-tax-burden becomes marginally significant.

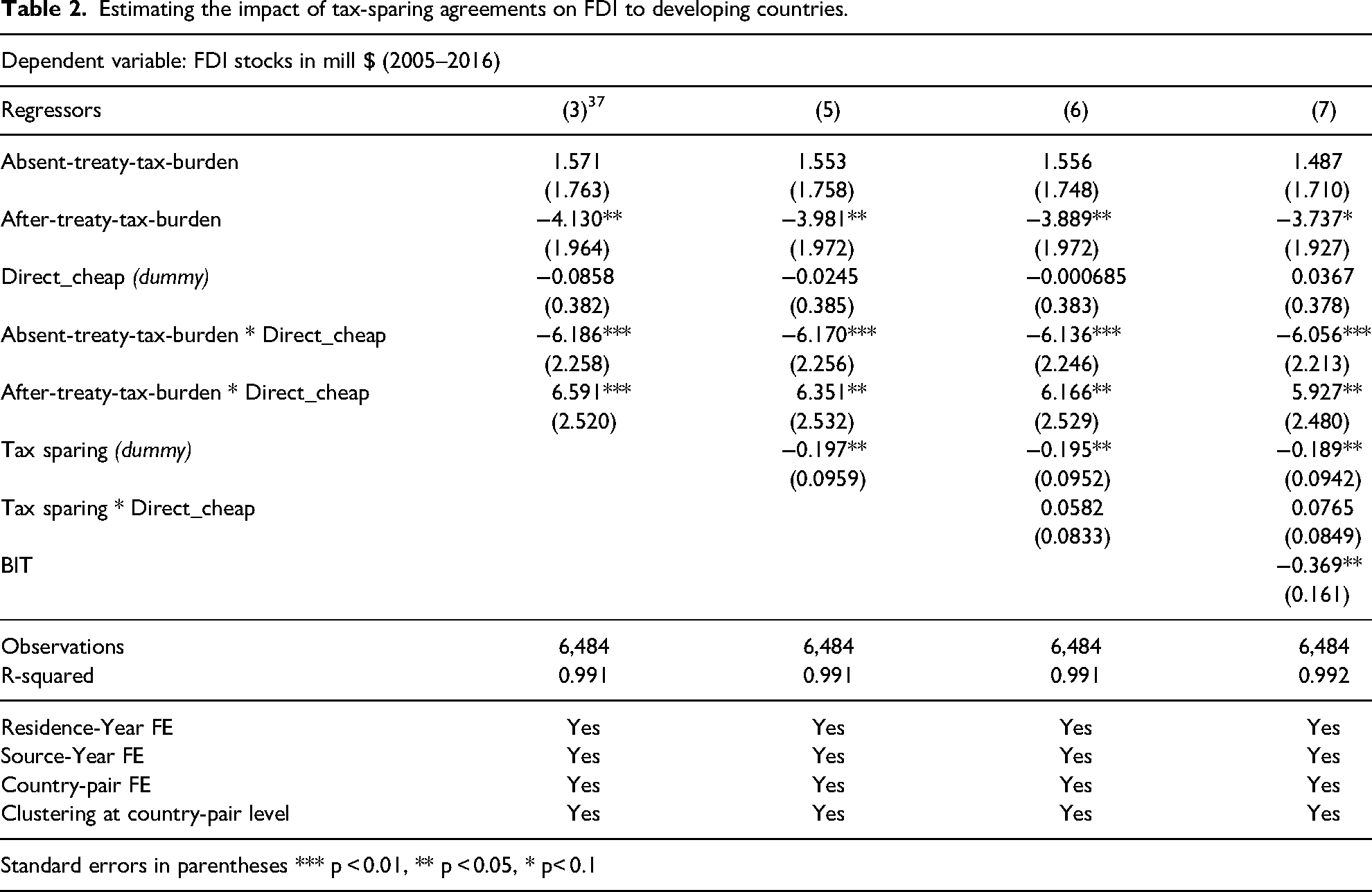

Table 2 is a continuation of Table 1. It retakes Table 1 from the regression reported in column 3, and adds to that estimation regressions for the additional analysis on the impact of tax-sparing agreements included in the tax treaty between the OECD member states and developing countries on FDI stocks in the developing country. We introduce the Tax_sparing(dummy) in specification 5. The main findings remain as in Table 1, that is, the Absent-treaty-tax-burden exhibits a strongly statistically significant negative effect on FDI stocks through the direct route, 30 while the After-treaty-tax-burden exhibits a positive effect on FDI stocks through the direct route, 31 which is only marginally statistically significant.

Estimating the impact of tax-sparing agreements on FDI to developing countries.

The coefficient on the Tax_sparing(dummy) suggests a negative effect of the tax-sparing agreements on the FDI stocks to developing economies of almost 17.88 percent, 32 and is statistically significant at the 5 percent significance level. In specification 6, we look for the effect of tax-sparing agreements on investments going through the direct route, it being the cheapest in terms of tax distance over the treaty network. However, we fail to find an interaction effect between the Direct_cheap (dummy) and the Tax_sparing(dummy); in specification 7, we control for the BIT as well. While we did expect a positive effect of the inclusion of tax-sparing provisions in asymmetric tax treaties on FDI to developing economies, our results show the opposite. Our expectation was based on the intuition that giving a credit for taxes that “shall have been paid” would attract more FDI to the developing countries, which would be free to use various tax incentives without bearing the risk of the tax incentives being canceled by the residence country's tax relief method. Nevertheless, the negative effect of the tax-sparing agreements on investments to developing economies might be attributed to reverse causality. While many developing countries have signed one or more tax-sparing provisions with OECD countries, most tax-sparing agreements entered into force before the initial year of our observations period. Furthermore, while tax-sparing provisions signed in the same year when the tax treaty was signed would have been another source of longitudinal variation for our analysis, note that we restrict the analysis to country-pair-year observations for which the treaty dummy variable equals one. We identify only 14 instances 33 in which tax-sparing agreements were terminated over the period 2005–2016 and no instances in which new tax-sparing agreements were signed.

Potential explanation for the negative coefficient on the effect of the tax-sparing agreements on FDI stocks to developing economies, might be that that OECD member states tend to offer tax-sparing provisions mostly to less-developed economies, which already receive very low, if any foreign direct investment, nevertheless. Therefore, the costs arising by providing tax-sparing agreements to these economies are close to being irrelevant, since these countries do not however receive FDI.

Robustness

The results obtained are robust to several robustness checks, as reported in the online appendix. While the coefficients can be easily observed from Table A3(a) to Table A7, linear combinations of the coefficients and their significance level are available upon request.

Following Azémar and Dharmapala (2019), we use a subset of 23 OECD member states, excluding those OECD member states that are themselves developing or transition economies, and restricting the analysis to tax treaties between developed and developing countries, instead of between OECD members and developing economies. The results remain robust. In Table A3(a), which is a replication of Table 3, in specifications 3 and 4, we obtain significant coefficients on both interaction terms, which in line with the main results, suggest that the impact of the Absent-treaty-tax-burden and of the After-treaty-tax-burden on FDI stocks to developing countries differs between investments through the direct and indirect route. Table A3(b), is a continuation of Table A3(a), representing results of the additional analysis on the impact of tax-sparing agreements included in the asymmetric tax treaties. The coefficient on the Tax_sparing(dummy) suggests a negative effect of the tax-sparing agreements on the FDI stocks to developing economies of almost 17.40 percent and is statistically significant at the 10 percent significance level. In specification 6, we look for the effect of tax-sparing agreements on investments going through the direct route, it being the cheapest in terms of tax distance over the treaty network. However, same as in the main analysis, we fail to find an interaction effect between the Direct_cheap (dummy) and the Tax_sparing(dummy).

Estimating the impact of relief method and tax sparing on corporate income tax in source (developing) countries.

In this paper, following previous literature, we used OECD member states as a proxy for developed countries and low- and middle-income countries as a proxy for developing economies. Accordingly, while investigating the impact of the tax relief method and of tax-sparing provisions on FDI stocks, we considered developed economies as net capital exporters and developing economies as net capital importers. Although we conducted a robustness check restricting the sample to 23 OECD member countries, by excluding those countries which are both OECD member states and developing economies, it is relevant to classify the developing countries as source and all the OECD members as residence countries for all the years of the observation period, based on a comparison of bilateral FDI data. Following Chisik and Davies (2004), we compared the relative FDI activity of the two countries of each country-pair for each year that bilateral FDI stock data was available to make sure that the OECD member state had higher activity in all the years between 2005 and 2016. We conduct a robustness test estimating the impact of the tax relief method and of the tax-sparing provision on the FDI stocks to developing economies, while excluding China from the estimation sample: although classified as a developing country, its outward FDI stocks to OECD member countries are larger than the inward FDI stocks from OECD countries for most country-pair-year observations. In addition, we exclude all the country-pairs for which in at least one year during the observation period the inward FDI stocks reported in the developing country from the OECD member country were lower than the inward FDI stocks reported in the OECD member state from the developing country. The results of this robustness check can be observed in Table A3(c). We still find that the impact of the Absent-treaty-tax-burden and of the After-treaty-tax-burden on FDI stocks to developing countries differs between investments through the direct and indirect route. However, we do not obtain a statistically significant effect of tax-sparing provisions, neither an interaction effect between with the Direct_cheap (dummy) and the Tax_sparing(dummy).

In our baseline estimations, we follow the standard practice in the empirical literature on the effects of DTTs and use FDI stocks as the dependent variable (Blonigen and Davies 2004; Egger et al. 2006; Azémar and Dharmapala 2019; Petkova, Stasio, and Zagler 2020). Petkova, Stasio, and Zagler (2020: 602) suggest using FDI flows in cases where there could have been a lot of inertia in FDI and changes in the treaty network might only affect new FDI; following this, we include one-year lagged FDI as an independent variable in Tables A4(a) and A4(b), which results statistically insignificant. The rest of the results remain robust.

Braun and Weichenrieder (2015) suggest that firms invest in tax havens for non-tax reasons, such as secrecy, beyond lower tax rates. While our set of time-varying source and residence country fixed effects should capture any unobservable reasons to invest in tax haven jurisdictions, following Petkova, Stasio, and Zagler (2020), to confirm that our results are not biased by the presence of tax havens, we conduct a separate analysis and exclude all of them. We consider as tax havens countries defined as such in Dyreng and Lindsey (2009) and Dyreng et al. (2015), thus excluding from the sample Aruba, Botswana, Lebanon, Mauritius, Panama, Seychelles, and Uruguay. As can be observed in Tables A4(a) and A4(b), our results are robust to the presence of tax havens.

As mentioned previously in the paper, we identify only 14 instances in which tax-sparing agreements were terminated over the period 2005–2016, and no instances in which new tax-sparing agreements were signed. These instances are mostly identified between India and OECD countries, as well as between China and OECD countries. To make sure that our findings on the impact of tax-sparing clauses on investments to developing countries are not driven by larger economies with more treaties, we estimate the impact of tax-sparing agreements on investment flows in developing countries excluding China, and then excluding India. The results of this robustness test are reported in Table A5.

Because the PPML estimator does not allow for negative values of FDI stocks, we replace these observations with zero. However, we conduct a robustness check, reported in Table A6, considering them as missing values, since while negative FDI flows are economically meaningful and represent disinvestments in the source economy, negative FDI stocks are generally the consequence of accounting methods (Petkova, Stasio, and Zagler 2020). Different to the main results, the After-treaty-tax-burden effect on FDI stocks remains positive, although insignificant.

In Tables A7(a) and A7(b), we use an alternative strategy to investigate the effect of the change in the residence countries’ tax relief method on FDI stocks. First, we take the difference between the Absent-treaty-tax-burden and the After-treaty-tax-burden, and then enter simultaneously in the regression the difference between the two calculated tax burdens and the Absent-treaty-tax-burden, that is, Difference btw. tax burdens. In this way, we keep in the regression elements of both domestic law and the treaty. While Absent-treaty-tax-burden captures the effect of tax treaties that do not change the relief method as compared to the domestic law of the residence country, the difference between Absent-treaty-tax-burden and After-treaty-tax-burden captures the effect of tax treaties changing the domestic relief method. In the first two columns of Table A7(a), we obtain a strongly statistically negative effect of the Absent-treaty-tax-burden on FDI stocks, while the coefficient on the difference between the two-tax burdens is statistically insignificant. However, once we distinguish between investments going through the direct and indirect route, the results are optimistic and in line with our main results in Table 3. We obtain a strongly statistically significant negative effect of the Absent-treaty-tax-burden on FDI stocks going through the direct route from the OECD members to developing countries, where an increase of the Absent-treaty-tax-burden by 10 percentage points would decrease FDI stocks by almost 8.8 percent. Of interest for us, is the negative effect of the difference between the two calculated tax burdens on FDI stocks going through the direct route. We find that when the difference between Absent-treaty-tax-burden and After-treaty-tax-burden increases by 10 percentage points, FDI stocks decrease by almost 9.1 percent. Accordingly, greater is the difference between the tax burden that investors would pay under a tax treaty that does not change the residence country's tax relief method as compared to what they pay under a tax treaty which changes the residence country's tax relief method, lower are the direct FDI stocks from developed to developing countries. Results remain the same, in column 4, where BIT dummy control variable is added.

We continue the same alternative estimation strategy when extending the investigation to the impact of tax-sparing provisions on FDI stocks. Results are shown in Table A7(b). In line with Table 4, in column 2 of Table A7(b) we obtain a negative statistically significant negative effect of the tax-sparing provisions on FDI stocks, which does however disappear once we distinguish between direct and indirect route in column 3 and 4.

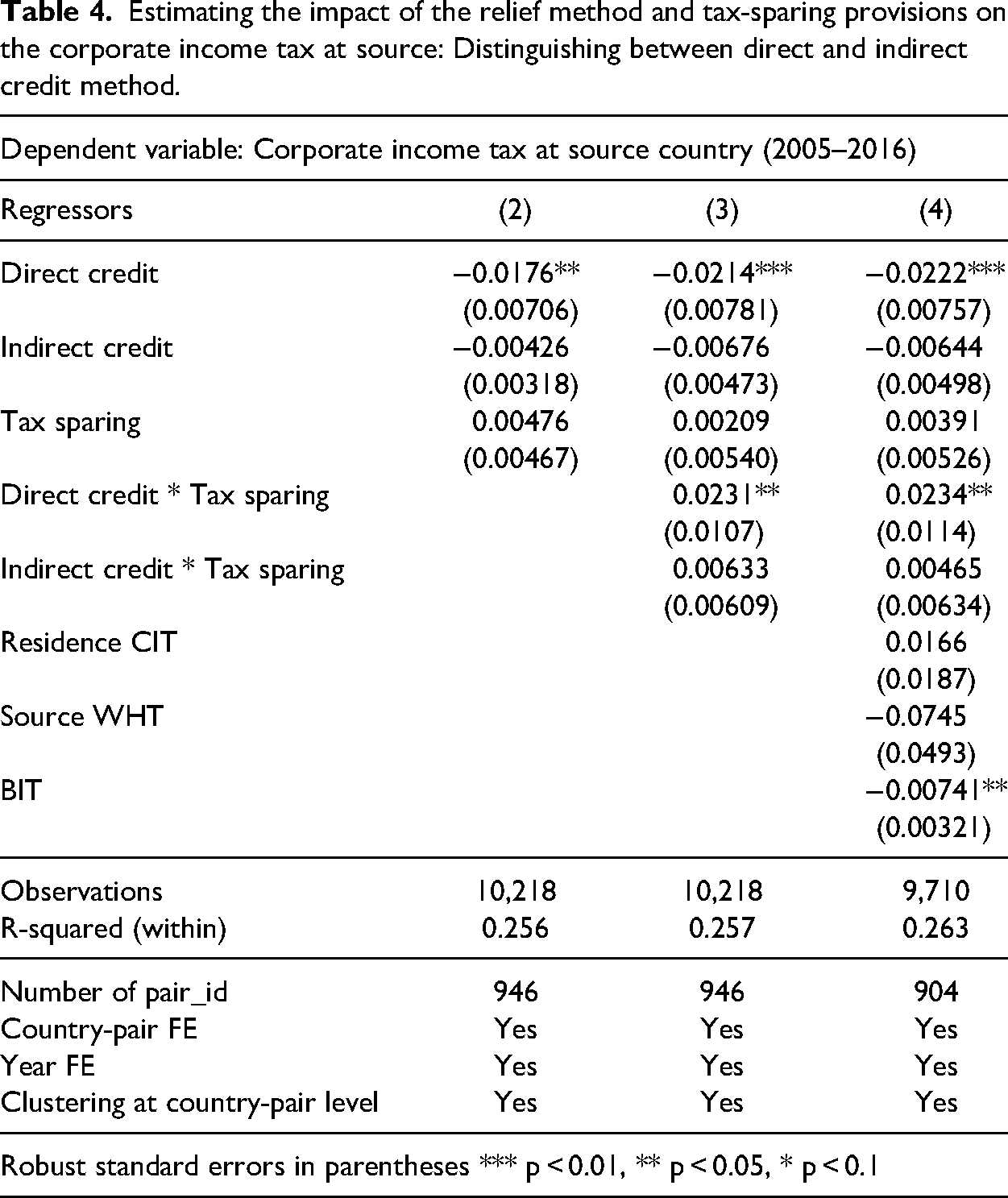

Estimating the impact of the relief method and tax-sparing provisions on the corporate income tax at source: Distinguishing between direct and indirect credit method.

Does the Residence's Relief Method Restrain the Source's Domestic Tax Policy?

One country's international tax policy affects the revenue and international tax policies of other countries, and this external impact is most pronounced when one country is developed, and the other is developing. Developing countries can have difficulties designing tax policies to attract investment when major foreign investors use the worldwide system of taxation. 34

We expand the analysis to an empirical investigation of a dogma questioned so far, as to our best knowledge, only from a legal perspective. As explained in Paolini et al. (2016), the relief method in the residence country of the multinational, may restrain the possibility of the source country to reduce taxes in order to attract foreign capital investments. For instance, “from a tax policy perspective, offering a tax credit for the foreign taxation by the country of residence, reduces the possibilities for developing countries to attract foreign capital through tax policy. A reduction of such tax by the country of source turns into a lower credit against taxes due in the country of residence” (Paolini et al. 2016: 384). This would restrain the possibility for countries to reduce taxes in order to attract foreign capital, that is, when taxes levied in the developing country are lower than those applicable in the developed country, which is usually the case, the developed country will in fact levy its own taxes on income produced within the territory of the developing country. As a consequence, developing countries would refrain from compensating their more favorable domestic tax regimes by raising tax rates to the levels of developed countries. In this section, we investigate this from an empirical perspective, questioning (iii) whether the residence country's tax relief method restrains the source country's domestic tax policy, in particular its corporate income tax rate. An empirical investigation of this argument constitutes, as to the best knowledge, a novelty to current research in the related area.

We build the intuition on the premises that under a foreign tax credit mechanism, the level of the corporate income tax rate in the source economy is frustrated, given that the credit method sets a bottom threshold for the CIT in capital-importing countries, beyond which any tax rate in the capital-importing country would result in a tax revenue shift to the capital-exporting country. Therefore, with the purpose of minimizing the tax wedge, the source (developing) country cannot set a corporate income tax rate which is lower than the one in the residence (developed) country. This highlights the role of the credit method in the capital-exporting countries in setting a lower bound for tax competition, as well as on restricting the capital-importing countries’ tax policy to attract investments. On the contrary, under the exemption mechanism, developing countries have the exclusive right to tax. Consequently, either they might be engaged in tax competition setting low levels of corporate income tax rates, or they might have a high CIT, subject thereafter to tax holidays and tax incentives to attract FDI, which in any case would not be canceled by a residence country's relief methods. Using the same dyadic panel of asymmetric tax treaties, we aim to provide empirical evidence on this dogma so far interpreted only from a legal perspective.

Furthermore, developed countries with worldwide tax may preserve the advantages created by the corporate tax policies in the developing country by allowing a credit for taxes that would have been paid in the absence of the tax incentive, adapting the tax-sparing provisions. Accordingly, the empirical analysis extends to the tax-sparing provisions, investigating whether their presence gives more discretion to the source developing country in deciding the CIT rate. In addition, we expect the effect of the tax-sparing provisions on the source country's CIT rate to alter the impact of the residence country's double tax relief method on the source country's CIT. While the inclusion of tax-sparing provisions is irrelevant if the residence country exempts foreign-sourced profits, it is expected to be crucial when the residence country provides a foreign tax credit which, according to tax-sparing rules, should be given for the taxes that would have been paid in the absence of tax incentives. Thus, the empirical analysis aims to provide evidence on an interaction effect between the tax relief method in the residence country and the tax-sparing provisions included in the treaty.

Empirical methodology

We use the same dyadic panel dataset of asymmetric tax treaties in order to analyze whether the double tax relief method on repatriated profits applied in the OECD member country (in the role of residence country) affects the corporate income tax under domestic law in the developing country (in the role of source country), when the two countries have an effective double tax treaty in force. In addition, we explore the impact of the inclusion of tax-sparing agreements on the source country's CIT, as well as whether they alter the impact of the relief method on the source country's domestic tax policy. As in the first part of the analysis, since we investigate the impact of the residence country's relief method on the source country's tax policy, while the two countries have an effective tax treaty in force, the sample is restricted to country-pair-year observations for which the dummy containing qualitative information on the effective tax treaty in year t equals one.

Using this sample of 10,218 observations, we estimate an empirical model, which looks like the following:

Our first main variable of interest is a dummy variable containing qualitative information on the relief method on dividends applied in the residence country o in year t. Under the tax treaty rules, the residence country can either exempt dividends sourced in the source country or can provide a foreign tax credit for taxes paid abroad. Therefore, we introduce the dummy variable Exemptiono,t, which takes the value one if the OECD member country relieves double taxation on dividends repatriated from the developing country through the exemption method, and zero if it provides a foreign tax credit (either direct or indirect credit).

Tax sparingo−d,t, is the second main variable of interest, which contains qualitative information on whether the tax treaty between the OECD member country and the developing country includes tax-sparing agreements, which enforce the residence country to allow firms to claim foreign tax credits against residence-country tax liabilities for taxes that would have been paid to foreign governments, in the absence of special abatements, on income from investments in the developing treaty partner country. This dummy is then interacted with the relief method dummy, Exemption*Tax_sparing, to investigate an eventual interaction effect between the relief method and the inclusion of tax-sparing agreements in the treaty between the country-pair, on the source country's corporate income tax rate.

Xo,d,t is a vector including three control variables, namely the residence country's statutory corporate income tax rate in year t (Residence CIT), the withholding tax (WHT) rate in the source country (Source WHT), and a dummy variable on whether a bilateral investment treaty is in force within the country-pair (BIT). The statutory corporate income tax rate in the residence country (OECD member) may have an impact on developing country tax policy, especially when the former relieves double taxation through the credit method, setting in this way a sort of bottom threshold for the overall tax that might be credited against the residence CIT. On the other hand, as for the source country withholding tax rate's impact on the source country's corporate income tax rate, while it may reflect general preferences toward taxation, it might also have a substitutive effect. The developing country may want to tax business profits moderately and in turn realize more revenue from the repatriations of foreign-owned firms through withholding taxes (Rixen and Schwarz 2009: 454). Finally, we expect that the signature of a BIT between the country-pair will incentivise a lower CIT rate in the source country, because of the missing negative impact on tax revenue due to an increase in foreign direct investment following the BIT signature.

Because our independent variables exhibit variability mainly across country-pairs, an incorporation of country-specific fixed effects—in addition to entailing a significant loss in degrees of freedom—would result in imprecise points estimates (Chisik and Davies 2004: 1131–1132; Rixen and Schwarz 2009: 455). While the Hausman test does suggest a fixed effects model over a random effects model, we introduce country-pair fixed effects to control for the physical distance between the source country and the residence country, and time-fixed effects to control for unobserved time effects. Standard errors are clustered at country-pair. Table A7 reports the results of the estimation of equation (2).

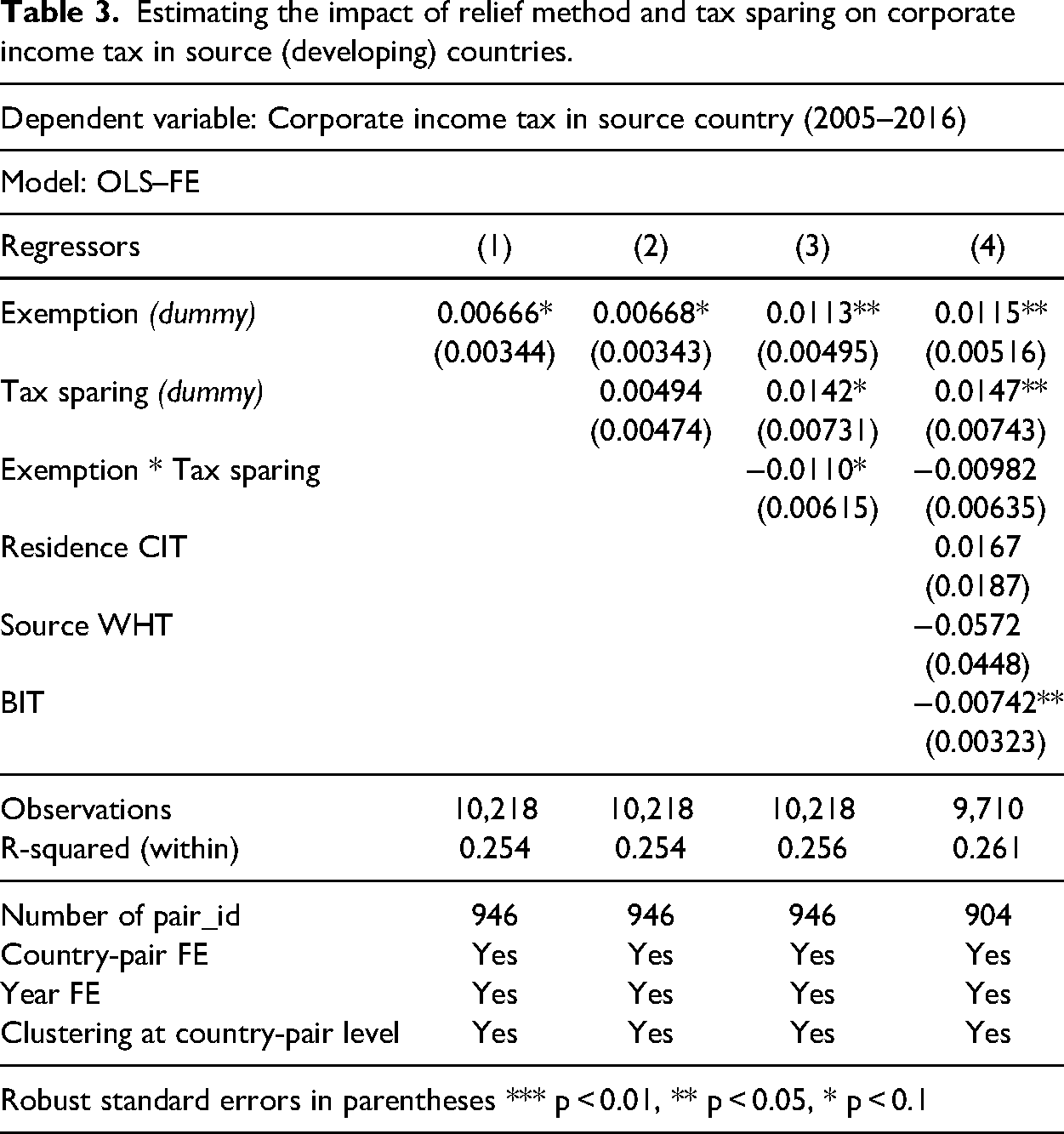

Results

We start here from the interpretation of columns 3 and 4 of Table A7, where all the main variables of interest (column 3) and control variables (column 4) are included. All the specifications include country-pair and year fixed effects, while the standard errors are clustered at country-pair level.

Results suggest a positive impact of the exemption method in the residence country on the corporate income tax rate in the source country. Source countries (developing economies) set corporate income tax rates which are between 0.011 and 0.012 percentage points higher when the residence country relieves double taxation through the exemption method, as compared to when it uses foreign tax credit as a tax relief method. The effect is statistically significant at the 5 percent significance level. The exemption method entails a residence country altogether excluding foreign income from its tax base, with the source country being given the exclusive right to tax. Since exemption in the residence state can therefore lower the overall tax burden of the investor if tax concessions are granted by the source country, developing countries should have then an incentive to engage in tax competition. The opposite would happen with the residence country applying the credit method on repatriated profits. In the latter case, if the residence country's corporate income tax rate is high, the source country reducing its corporate income tax rate does not give any benefit to the investors, since any lowering of tax rates in the source country is calculated against the residence state's tax rate, leading to one tax rate for the investor. Accordingly, we expected higher corporate income tax rates at source under the residence country's credit method, as compared to the residence country's exemption method. A reasonable explanation for the results obtained might be that OECD member states offer the exemption method to developing countries, which impose high corporate income tax rates, while they offer nothing but a foreign tax credit to repatriated profits sourced in developing countries with low corporate income tax rates.

In line with our expectation, we obtain a positive and statistically significant positive effect of tax-sparing provisions on the corporate income tax rate in the source country. Developing countries set corporate income tax rates between 0.013 and 0.15 percentage points higher when they have a double tax treaty with an OECD member state which includes tax-sparing agreements, that is, when the residence country offers a credit for taxes that “shall have been paid,” as compared to when it does not.

This is in line with the intuition that tax-sparing agreements might incentivise developing countries to set high corporate income tax rates, making the CIT thereafter subject to tax holidays and tax incentives, without bearing the risk of tax incentives being canceled by the residence country tax relief method, since the OECD member state would be forced to provide a credit for the rate that would have been paid at the source. In addition, the lack of statistical significance in column 4—where the full set of main and control variables is included—on the interaction term Exemption*Tax sparing, is in line with the expectation that tax-sparing provisions matter for the source country's tax policy, as long as the residence country offers a foreign tax credit for the taxes paid at source, while they become irrelevant when the residence country already exempts foreign repatriated profits. 35

While we do not obtain any significant effect of the residence country's corporate income tax rate (Residence CIT) and of the source country's withholding tax rate (Source WHT) on the source country's corporate income tax rate, a BIT between the OECD member state and the developing country lowers the corporate income tax rate in the developing country, and the effect is statistically significant at the 5 percent significance level.

As mentioned previously in the study, the credit method can either be direct or indirect. Under the indirect credit method, the parent company receives a tax credit which may be used against its tax liability, equal to the corporate income tax and withholding tax rates paid abroad. In the case of direct credit, the parent company only gains a credit in the non-resident withholding tax rate paid. Differently said, only under the indirect credit method would a home country credit the underlying CIT of the host country. Otherwise, only withholding taxes can be credited so that the host country can still determine the overall tax burden on the foreign investment via the CIT. In order to take care of this distinction, we estimate equation (2) using as baseline group country-pair-year observations in which the OECD member state (residence) exempts foreign-sources dividends and distinguishing in the regression between the indirect credit and direct credit methods. Table A8 reports results of this estimation.

In column 2, results suggest a negative effect of only of the direct credit method on the corporate income tax in the developing countries, of about 0.018 percentage points, statistically significant at the 5 percent significance level. Owing mostly to the small number of available observations because most of the OECD member countries in our sample when having a foreign tax credit as tax relief method, they limit it to the direct credit, we find no effect for the indirect credit on the corporate income tax rate. Accordingly, the source countries tend to set significantly lower corporate income tax rates when the residence countries offer a direct credit as compared to when they offer an exemption. Offering a direct credit at residence, rather than an exemption, has a negative effect on CIT at source. In addition, interacting the tax relief method with the tax-sparing provisions, we obtain statistically significant interaction effect between the direct credit method and the tax-sparing provisions (see column 2 and column3). The inclusion of tax-sparing agreements vanishes the negative effect of the direct credit on the source CIT, which might suggest that following an agreement on tax sparing, developing countries increase their corporate income tax rates, offering thereafter tax incentives and tax holidays, without bearing the risk of these incentives being canceled by the residence country's tax policy.

Opposite results in Tables A7 and A8 are in line with our intuition, that is, for high (er) CIT rates in developing countries, OECD members would likely provide exemption to the treaty partner country, which in this case excludes the need and the effectiveness of the tax-sparing provisions. On the contrary, for low(er) CIT rates developing partners, OECD member countries would rather offer a direct credit method to tax the “extra” profits. This is however softened by the allowance of the tax-sparing provisions, which are an effective shelter for the developing country's tax policy. Finally, Following Azémar and Dharmapala (2019), we use a subset of 23 OECD member states, excluding those OECD member states that are themselves developing or transition economies, and restricting the analysis to tax treaties between developed and developing countries, instead of between OECD members and developing economies. Using this subset, we re-estimate equation (2) and report results in Table A8. Although the coefficients’ sign for all the variables remains in line with the results obtained in Table A7, they are however statistically insignificant.

Conclusions

This paper has investigated the impact of the double tax relief method and of tax-sparing agreements on foreign direct investments in developing countries. It focuses on tax treaties between countries with asymmetric investment flows, that is, between 37 OECD member states, in the role of residence countries, and low- and middle-income countries, in the role of source countries, over the period 2005–2016.