Abstract

In the European Economic and Monetary Union, the fiscal background must ensure the sustainability of the public debt, but fiscal policies must also keep enough flexibility to stabilize global economic activity in case of large shocks, as the common monetary policy becomes less efficient. In the prospect of a reform of the Fiscal Compact after the standby of European fiscal rules with the COVID-19 health crisis, and in conformity with theoretical studies underlying the advantages of such rules, the current paper suggests a rule related to nominal public expenditure excluding interest rates, with a debt feedback mechanism to ensure the sustainability of the public debt path. According to this rule, it appears that six Economic and Monetary Union member countries are particularly highly indebted and should probably control and reduce their public expenditure in order to make their public debt sustainable: France, Spain, Italy, Belgium, Portugal, and Greece.

Introduction

An appropriate fiscal framework is necessary to the conduct of economic policy in any country; but it is all the more necessary for the member countries of a monetary union as the European Economic and Monetary Union (EMU). Indeed, this fiscal framework must be enough constraining to allow debt sustainability in the long run; it must avoid a “deficit bias” due to the fact that it is politically easier to increase public expenditure, that an excessive public debt accumulation and negative fiscal externalities must particularly be avoided in the context of a monetary union. So, public debt sustainability is the first and main goal of any government. Sound public finances are necessary in order to let the fiscal policy enough room for maneuver to play an efficient role in macroeconomic stabilization, in particular in case of a large health and economic crisis as the COVID-19 crisis. Without being “sane” in normal times, fiscal policy risks to be pro-cyclical. But fiscal policy has a second goal which is as important: it must have enough flexibility, in particular in the context of a monetary union. Indeed, with a common monetary policy, fiscal policy is a fundamental economic stabilization tool, the only one which really remains country-specific and independent; so, it must keep its shock-absorbing role. This is particularly true in case of asymmetric shocks. After a crisis as the COVID-19 crisis, provided the public debt is sustainable, the fiscal space must be sufficient to stabilize and to absorb large shocks; it must be compatible with the stabilization function of fiscal policy, and with demand management. Blanchard, Leandro, and Zettelmeyer (2021) underline the influence of fiscal policy on global economic growth, in a framework where monetary policy is constrained and of prices and wages rigidities. So, beyond a pure fiscal approach, it is necessary to consider a global economic framework.

Furthermore, the complexity of the European fiscal framework is due to the successive historical phases of its completion and deepening. In 1997, the Stability and Growth Pact (SGP) assumed that the budget deficit of the EU member States should not exceed 3% of their Gross Domestic Product (GDP), and that their public debt levels should not exceed 60% of their GDP. Indeed, fiscal externalities were supposed to increase with the creation of the EMU. It was then considered necessary to constrain with fiscal rules the fiscal policies of the member countries, in order to avoid a too lax fiscal policy in one country harmful to its partners. However, the potential sanctions considered in the Pact were never effectively used and applied. Besides, in March 2020, given the gravity of the recession implied by the COVID-19 health crisis, the conditions of the Pact were suspended in the context of exceptional severe economic difficulties. Today, the large dissatisfaction with the operation of the SGP is obvious, in an environment of missed inflation targets, low growth, and high public debt levels. Therefore, in 2021, the European Commission began to contemplate a revision of the Pact, as it was clear that existing rules would lead to an excessive fiscal contraction. As mentioned by Blanchard, Leandro, and Zettelmeyer (2021), the SGP must be reformed. However, “given the complexity of the answer, it is an illusion to think that EU fiscal rules can be simple. But it is an illusion to think that they can ever be complex enough to accommodate most relevant contingencies.”

In February 2020, the European Commission launched a review of the SGP; however, it was soon put on hold as, in March 2020, the fiscal rules were suspended due to the COVID-19 crisis. As the Pact could be suspended in case of “severe economic downturn,” the Commission activated the General Escape Clause in response to this unprecedented health crisis. The review restarted in October 2021; but in the post-Covid world, it was necessary to reform rules which became unrealistic and which could not be complied with, in the context of such a large crisis. Martin, Pisani-Ferry, and Ragot (2021) underline the unprecedented increase of public debt levels in the EMU with the financial crisis of 2007 and afterward mainly with the COVID-19 crisis, well above the Maastricht reference value of 60% of GDP. However, this increase was heterogeneous among EMU member countries, and therefore, the fiscal framework should take into account this heterogeneity.

In January 2024, the General Escape Clause will expire, and the reform should then be considered. In this context, the current paper studies the usefulness and potential implications of a reform of the European fiscal framework based on the following rule: a target for nominal public expenditure excluding interest rates, with a debt feedback mechanism to ensure the sustainability of the public debt path. Such a rule could accurately make public expenditure and the allowed budget deficit depend on the public debt of a given country. So, the contribution of the current paper is to use the feedback effect from the debt level to the interest rate, and to the desired fiscal balance, in the determination of an operational public expenditure target for each specific country. In this way, for each country, we could examine whether its past and anticipated share of public expenditure in GDP is likely or not to ensure its debt sustainability.

The second section provides a review of literature on propositions of potential reforms of the current European framework, of the SGP and of the Fiscal compact. The third section underlines the advantages of a rule related to nominal public expenditure excluding interest rates with a debt feedback mechanism. The fourth section analyzes the teachings of our theoretical model for the 19 member countries of the EMU. The fifth section concludes the paper.

Review of Economic Literature

For fiscal authorities, the main concern is the sustainability of fiscal policy and of the public debt. Fiscal flexibility and fiscal space should be left to EU member countries, as long as the public debt remains sustainable, which is the only condition that should be controlled and scrutinized. Indeed, without sustainability, one day, a government would have to default, to restructure its public debt (pressure for bail-out), or to cause an excessive inflation (monetization), all events which should be avoided. Nevertheless, the problem is then to define this sustainability, in a context of uncertainty, as we cannot know all future and anticipated values of budget deficits, growth rates, and interest rates over an infinite horizon. So, because it is forward-looking and anticipated, the sustainability of the public debt is very difficult to transform into an operational empirical budget rule. Besides, as mentioned by Debrun et al. (2019), the ability of a government to repay its public debt is fundamentally different from its willingness to pay, which is a political and strategical choice. Martin, Pisani-Ferry, and Ragot (2021) mention that the European fiscal framework should mainly be concerned with debt sustainability, whereas the appropriate fiscal trajectory is fundamentally heterogeneous among member countries.

After the sovereign debt crisis, Schuknecht et al. (2011) proposed to strengthen fiscal policy governance and the enforcement provisions of the SGP, essential for effective policy coordination and sound public finance in the future. In this direction, the “Fiscal Compact” entered into force on 1st January 2013. The 3% of GDP limit for budget deficits, the medium-term objective of budget positions in balance, and the constraint for countries running a structural deficit to cut it by at least 0.5% of GDP per year were maintained. Regarding the preventive arm of the SGP, a Medium-Term Budgetary Objective (MTO) is fixed for the structural balance (adjusted for cyclical economic conditions, and net of one-off and other temporary measures, including interest payments) of each Member State, according to its debt level and to macroeconomic conditions (the potential output defines the cyclical component of the deficit). A net expenditure rule also intends to constrain the growth of an aggregate for government expenditure relative to the economy's potential growth rate, net of discretionary revenue measures, net of interest payments, spending on EU programs paid for by EU funds and cyclical elements of unemployment benefits (European Commission, 2019). An adjusted measure of real government expenditure cannot grow faster than the medium-term potential economic growth if the country's structural balance is at its MTO or higher. However, if the structural balance has not yet reached its MTO, expenditure growth must be lower than potential growth.

Furthermore, the corrective part of the SGP was also strongly reinforced. Countries should submit each year a Stability and Convergence Program (SCP) and reduce their budget deficits according to a schedule proposed by the Commission. Besides, countries whose indebtedness levels exceed 60% of GDP are supposed to take commitments to make it converge toward a defined target. Specifically, a debt-to-GDP ratio above 60% is to be considered “sufficiently diminishing” and approaching the reference value “at a satisfactory pace,” if its distance with respect to this reference value has reduced over the previous three years at a rate of the order of one twentieth per year. The Six Pack Reform aimed at strengthening debt sustainability criteria, whereas at the same time reinforcing the flexibility to stabilize economic activity in case of crisis, and to avoid the harmful pro-cyclicality of fiscal rules. However, it increased the complexity of the European fiscal framework (European Fiscal Board, 2019, 16).

Indeed, in the context of the COVID-19 crisis, it was impossible to verify such strict rules. As mentioned by De Angelis and Mollet (2021), the governments called for simpler and more transparent EU fiscal rules. Instead of quantitative rules, Blanchard, Leandro, and Zettelmeyer (2021) propose enforceable fiscal standards, qualitative prescriptions, statements of general goals that leave room for judgment, together with a process to decide whether the standards are met. However, Martin, Pisani-Ferry, and Ragot (2021) assess that fiscal rules must be preserved, in order to impose sanctions on a member State breaking its obligations of debt sustainability. The ECFIN services of the European Commission (2014) use a very accurate and enhanced Debt Sustainability Analysis for the member countries of the European Union. Fiscal criteria regarding the debt-to-GDP ratio and its evolution are considered but also an indicator of short-term fiscal stress risk. The ECB (see Bouabdallah et al., 2017) also provides a Debt Sustainability Analysis for European countries, considering debt dynamics and the feasibility to achieve given primary balance surpluses, taking into account relevant indicators capturing liquidity and solvency risks, the ability to maintain market access in the short term. However, these analyses do not study the question of the most operational and efficient fiscal rules, in order to secure public debt sustainability in each EU member country.

Darvas and Anderson (2020) underline that the current EU framework is too complex and relies on unobserved variables: potential output, medium-term potential growth rate, output gap, and structural balance. Indeed, a rule in terms of structural balance implies drawbacks. The European Commission uses a Cobb–Douglas production function to estimate the potential output, but the estimation method is then complex; this indicator is pro-cyclical by construction and ambiguous regarding the size of the necessary fiscal effort. More precisely, Heimberger (2020) underlines that a strong crisis like the COVID-19 crisis empirically implies large downward revisions in potential output forecasts for all future periods. This translates into higher “structural” part of budget deficits and fiscal consolidation pressures to overcome the crisis, when fiscal policies sustaining growth would still be necessary (negative pro-cyclical effect). Heinemann (2018) also underlines that the structural balance has the drawback to be unobservable. A structural balance rule necessitates to estimate the potential output gap, and it is therefore difficult to monitor and to communicate to the public.

Besides, in the current European fiscal framework, too much attention is given to annual rather than to longer-term performance indicators. Ayuso i Casals (2012) mentions that a multi-annual rule is always superior to a rule setting a target for only one year. Indeed, a rule for several years avoids the possibility to postpone expenditure or structural adjustments (or to delay important investment expenditure) to the future to circumvent the rule. A fiscal strategy embedded in a multi-term framework can better adapt to economic and country-specific circumstances, while making stabilization and consolidation objectives more compatible. Structural and long-lasting deviations from the budgetary target must be corrected, while short-term adaptations can be accommodated. Therefore, Claeys, Darvas, and Leandro (2016) propose to replace the structural balance rule with a public expenditure rule with debt-correction feedback, embodied in a multi-annual framework, which would also support the central bank's inflation target.

The operational rule to ensure debt sustainability could thus be an expenditure-based rule. Indeed, except for unemployment expenditure (largely pro-cyclical) or interest rates expenditure on public debt, government expenditure is more independent from the business cycle and controllable by the government than a structural balance. Besides, an expenditure rule retains stabilization properties, by allowing automatic stabilizers to operate fully on the revenue side (revenues are allowed to fluctuate with the business cycle). According to Eyraud et al. (2018), the budget is more likely to remain in balance over the macro-economic cycle with a spending rule, which is deficit neutral on average. Indeed, if economic conditions are better than expected, no additional fiscal resources would be available for greater spending or tax cuts, the budgetary bonus is supposed to be saved. On the contrary, in case of recession, a spending rule would tolerate a budget deficit through its automatic stabilizers, but would not allow any discretionary supplementary expenditure. A spending rule also allows more stable anticipations of budgetary trajectories and of funding of budget lines in a multi-year framework.

According to Ayuso i Casals (2012), expenditure rules have many advantages. They target the main source of deficit bias, that is, frequently spending overruns compared to initial targets. They target the part of the budget the most controllable by the governments; they are transparent and easy to communicate to the public opinion 1 . Empirically, successful fiscal consolidations over the 1970s and 1980s were mainly expenditure based, with a particular emphasis on primary current expenditure (mainly public wages and transfers). Institutional reforms and the introduction of such rules have been effective to promote a healthy fiscal situation in some Nordic European countries (Netherlands, Sweden, Denmark, and Finland). On the contrary, the difficulty to avoid an un-constrained increase of public expenditure largely explains the fiscal difficulties of other Southern European countries before 2007. For 29 countries with expenditure rules between 1985 and 2013, Cordes et al. (2015) also find that these rules are associated with spending control, counter-cyclical fiscal policy, and improved fiscal discipline (higher compliance).

So, the European Fiscal Board (2019) proposes a reform of the European fiscal framework organized around a medium-term debt anchor, and a ceiling on the growth rate of net primary expenditure, but only for countries with public debt in excess of 60% of GDP, as the main policy instrument. On the contrary, Darvas and Anderson (2020) favor an expenditure target for all countries, whatever their initial public debt level. They recommend, as operational target, a multi-year ahead expenditure rule anchored in an appropriate public debt target (five-year ahead or seven-year ahead debt ratio change objective), augmented with an asymmetric golden rule that provides extra fiscal space only in times of recession. The ceiling of net expenditure growth would be set for a period of three years, and a “compensation account” would serve to accumulate or de-cumulate deviations from planned net primary expenditure growth. The gross public debt target would be country-specific and should be reached after a seven-year period horizon.

Heinemann (2018) also underlines that a debt anchor is necessary as long-term solvability criteria. However, it is not directly observable and controllable by governments. The rule must reflect the current fiscal effort in terms of flow; targeting a debt-to-GDP ratio is not directly operational without a rule in terms of current fiscal policy. Therefore, Andrle et al. (2015) argue for moving to a two-pillar approach with a single fiscal anchor (the public debt-to-GDP ratio) and a single operational target (an expenditure growth rule, possibly with an explicit debt-correction mechanism) linked to the anchor. In the same way, Eyraud et al. (2018) underline that a debt anchor establishing a medium-term objective, combined with a small number of operational rules, could be established and effective.

In conclusion, for the European Union fiscal framework, theoretical studies could favor the adoption of a target for nominal public expenditure excluding interest rates, with a debt feedback mechanism to ensure the sustainability of the public debt path. “Theoretical Proposal of a Rule Targeting Public Expenditure” section now aims at proposing such a rule, in conformity with these recommendations of the economic literature, which could be operational, before confronting it with empirical data in “Empirical Results” section.

Theoretical Proposal of a Rule Targeting Public Expenditure

According to the theoretical background mentioned in “Review of Economic Literature” section, our goal is to define a fiscal rule for the EMU member countries in terms of nominal public expenditure, in order to avoid the difficulty to estimate the inflation rate, which is not under the control of governments. We make the conventional hypothesis that public debt consists of one-period bonds. The public debt in a given period (t) corresponds to the public debt inherited from the former period (t-1) increased by interest rates, and to the current budget deficit, the difference between public expenditure and tax resources. The variation of the public debt is then:

Obviously, public indebtedness is more legitimate if it concerns public investments which are more beneficial for the future: green investment, infrastructure, digital economy, etc. However, a “Golden rule” excluding public investment useful for the future and some government expenditure from the budgetary target to comply with implies a problem of estimation of the profitability of various public investments. It strongly reduces the simplicity of the calculation of the budget rule, as well as its enforceability. Therefore, we consider that the implementation of a global budget rule is easier, even if it is less desirable.

Necessity of a Debt Feedback Mechanism

According to equation (3), the variation of the public debt to GDP ratio is as follows: If (r > y), the maximal long-term public debt level which is sustainable would increase with and would be limited by the maximal budget surplus that a country can generate. Sustainability is then insured only if primary surpluses necessary to the financing of the debt never exceed a limit threshold considered as practicable

2

. Blanchard, Leandro, and Zettelmeyer (2021) assumed that interest rates could remain low and below growth rates. So, if (r < y), the public debt automatically decreases and converges toward a positive and finite value increasing with the maximal conceivable budget deficit. Maintaining a constant positive debt ratio is then consistent with running primary deficits forever. Nevertheless, this ideal situation seems undermined today, with the restart of interest rate increases in the United States as well as in Europe.

However, we can complicate the previous equations. Indeed, beyond the cyclical component of the budget balance depending on the output gap because of automatic stabilizers (β∼1), the primary balance seems empirically to react to the public debt level (α>0). So, we can write the budget deficit to GDP ratio as follows:

The European Commission (2019, 17) mentions that in the European Union, fiscal revenues move approximatively as GDP, as long as non-tax revenues are relatively low (

By combining equations (4) and (6), we obtain: The public debt decreases ( On the contrary, if the budget balance is weakly sensitive to the public debt level

The public debt then converges toward a level which verifies:

Therefore, a feedback mechanism constraining the level of the budget deficit allowed in case of an excessive public debt level (α sufficiently high) appears as useful, and even as fully necessary to the long-term sustainability of the public debt level.

Besides, we can also consider that a high public debt level is a bad signal for financial markets, which can increase the interest rate on government bonds of a given country, and which modifies the previous equations. So, if the interest rate increases with the public debt [ If ( If ( If (

Therefore, (

Proposition of a Rule Limiting Public Expenditure

In the spirit of the Swiss “debt brake” and of the mechanism proposed by Debrun, Epstein, and Symansky (2008) for Israel, the European Union could adopt a public expenditure rule in combination with a debt feedback mechanism, an error correction mechanism preserving consistency with a debt stabilization objective. Such a rule would avoid excessive pro-cyclicality and would encourage medium-term expenditure planning, with better smoothing properties, which imply counter-cyclical benefits. In this framework, a (n) years (n is to define, a horizon of 5–10 years) ceiling on nominal public expenditure excluding interests as medium-term target is the implementation component to reach a given public debt path.

We make the hypothesis that the goal is to reach a targeted public debt level (

Therefore, with constant total tax revenues to GDP ratio (tax), if the equilibrium public debt level (

Sensitivity Analysis

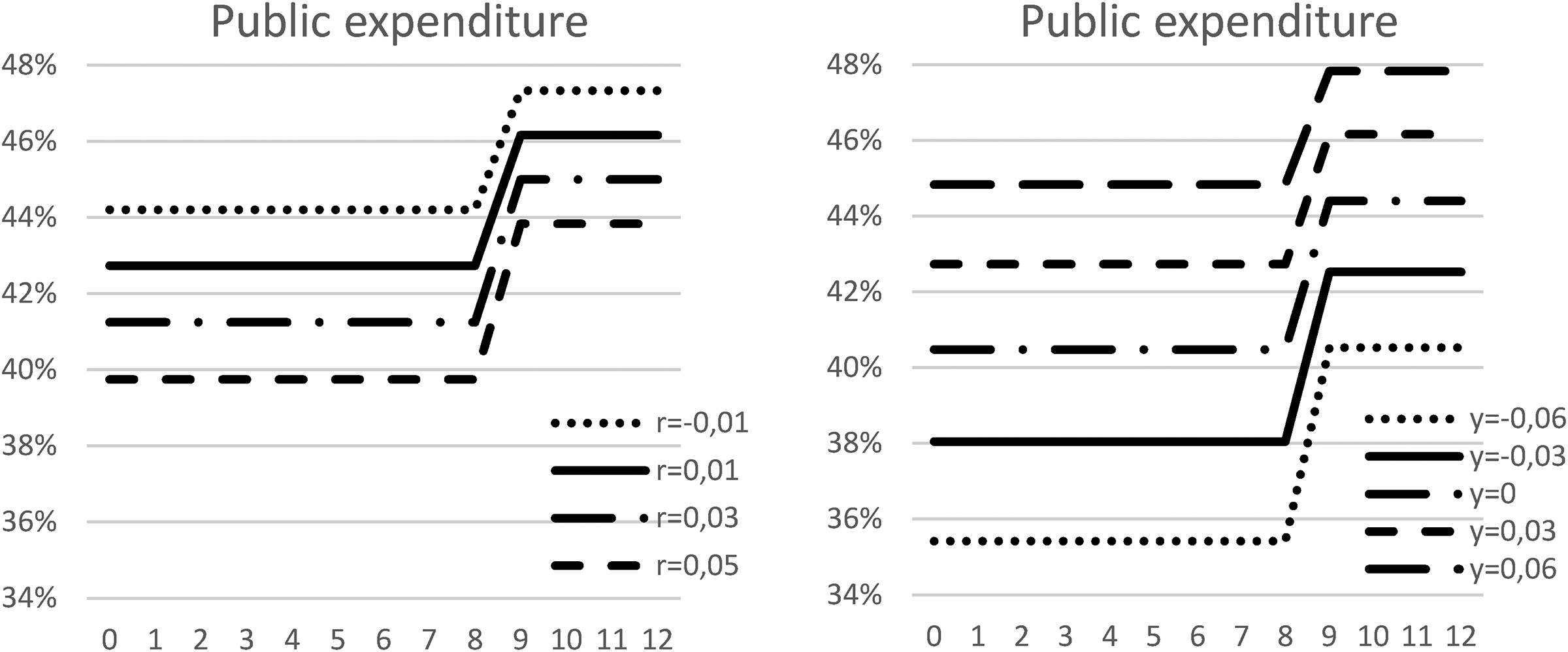

A first way to increase allowed budget expenditure would be to increase fiscal revenues; indeed, both increase proportionally in equation (12). Regarding the crucial role of revenue generation, it is possible to increase the ratio of fiscal revenue to GDP (tax) and the level of compulsory contributions (taxation rates). Revenue generation is then very heterogeneous among European countries; in 2022, tax-to-GDP ratios ranged from about 22.3 in Ireland to 52.9 in France. Policy priorities regarding the desired level of compulsory contributions, and of institutional intervention of the state in the economy, obviously affect the proposed rule. However, taxation rates on labor, consumption, and capital are already quite high in most European countries, and increasing their weight would be difficult to sustain for households and firms. Therefore, generating more fiscal revenues mainly go through increasing economic growth, as both are exactly proportional in the framework of our model (see Figure 1 and the discussion about the variation of the nominal growth rate).

Stabilization path for public expenditure, according to the nominal interest rate or to the nominal growth rate.

If the targeted public debt level is (

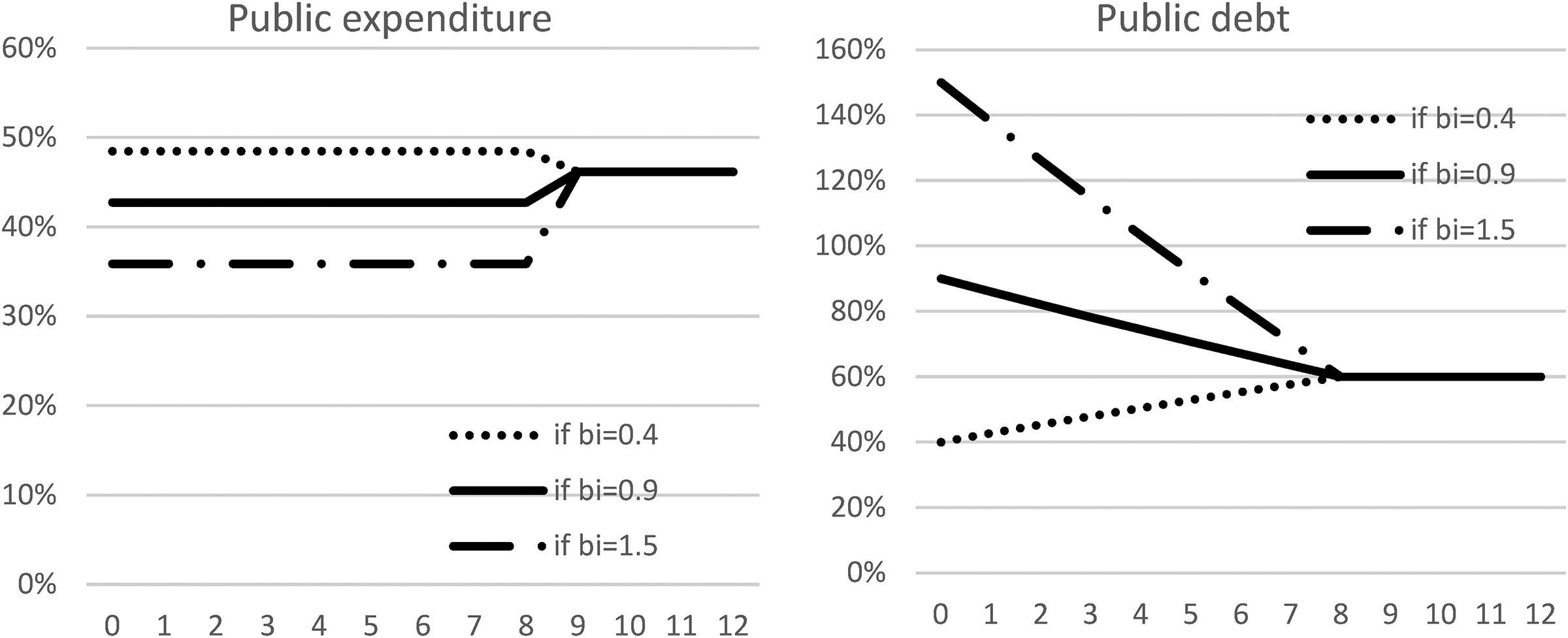

Stabilization path for public expenditure and the public debt, according to the initial public debt level.

Besides, the delay granted before the public debt target is reached (n) increases public expenditure which is allowed at the beginning of the period, if the initial public debt level is above the target (

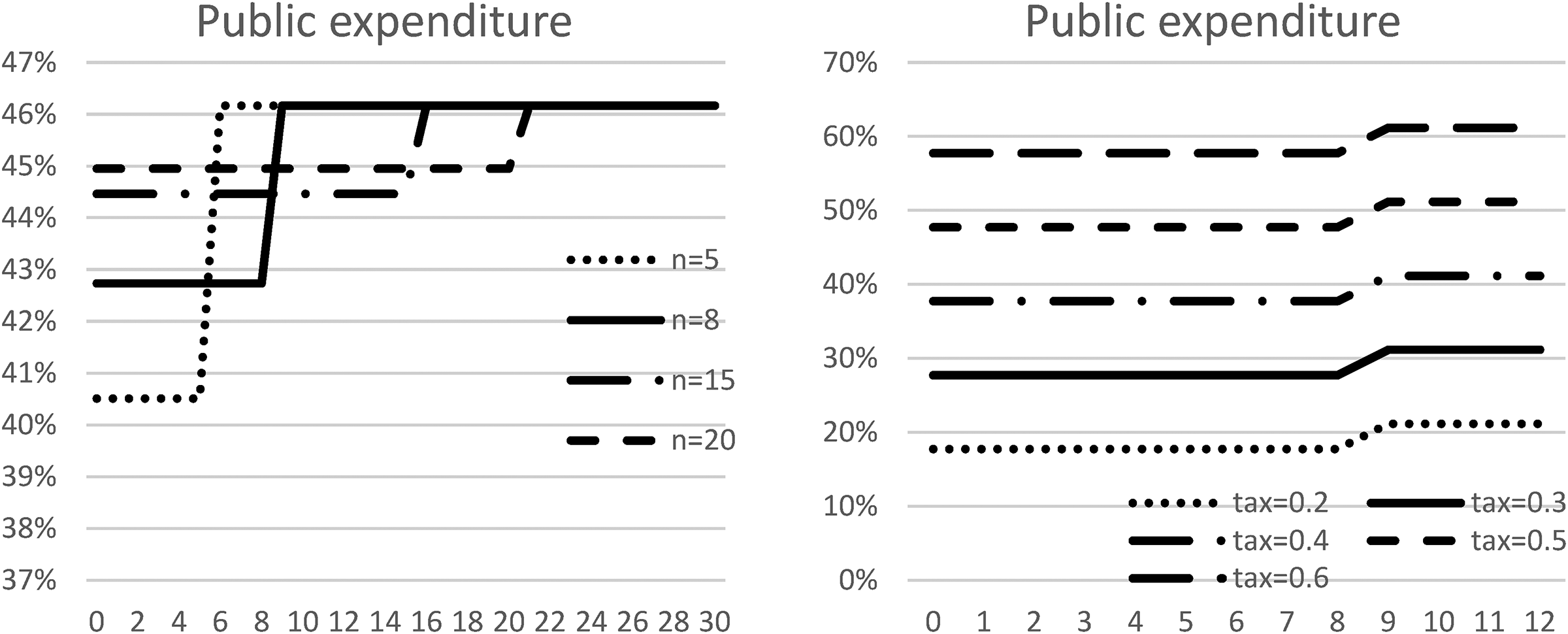

Stabilization path for public expenditure, according to the horizon of stabilization and to the tax to Gross Domestic Product (GDP) ratio.

A higher interest rate also reduces public expenditure which is allowed at the beginning of the period as well as once the debt target has been reached. Indeed, if the initial public debt level is (

Finally, a smaller economic activity reduces public expenditure which is allowed at the beginning of the period as well as once the debt target has been reached. Indeed, if the initial public debt level is (

Empirical Results

We can now derive empirical results for EMU member countries, in light of the theoretical model of the previous “Theoretical Proposal of a Rule Targeting Public Expenditure” section. Data come from the AMECO Database (extracted: 15/05/2023), for the period 1995–2022. We use data for total government expenditure excluding interest (

The AMECO Database provides data for total government revenue in percentage of GDP at market prices (

Weakly Indebted Countries

First, we can mention the situation of seven EMU member countries for which there seems to be no problem with the sustainability of the public debt. The public debt in Estonia was only 18.40% of GDP in 2022. A budget expenditure excluding interests representing 40.20% of GDP would then allow to stabilize the public debt at this very low level according to equation (12), whereas it represented only 39.4% of GDP in 2022. The public debt in Luxembourg was only 24.60% of GDP in 2022. A budget expenditure excluding interests representing 46.16% of GDP would then allow to stabilize the public debt at this very low level according to equation (12), whereas it is supposed to reach only 44.5% of GDP in 2023 according to the current forecasts. The public debt in the Netherlands was only 51% of GDP in 2022, and long-term nominal interest rates are particularly low (even negative) in this country. A budget expenditure excluding interests representing 44.73% of GDP would then allow to stabilize the public debt at this low level according to equation (12), which is fully in line with the current forecasts for 2023. The public debt in Malta was only 53.40% of GDP in 2022. A budget expenditure excluding interests representing 38.95% of GDP would then allow to stabilize the public debt at this low level according to equation (12), whereas it represented only 34.8% of GDP in 2019 before the COVID-19 crisis.

The public debt in Latvia was only 40.80% of GDP in 2022. A budget expenditure excluding interests representing 38.20% of GDP would then allow to stabilize the public debt at this low level according to equation (12), whereas it represented only 37.5% of GDP in 2019 before the COVID-19 crisis. Public expenditure is expected to remain at 39.5% of GDP in 2023 but to fall back to 38.5% of GDP in 2024. The public debt in Lithuania was only 38.40% of GDP in 2022. A budget expenditure excluding interests representing 36.12% of GDP would then allow to stabilize the public debt at this low level according to equation (12), whereas it represented 35.8% of GDP in 2019 before the COVID-19 crisis. Public expenditure is expected to reach 37.1% of GDP in 2023 but to fall back to 36.5% of GDP in 2024. Therefore, in 2022, the European Council recommended to Latvia and Lithuania to control the growth of nationally financed current expenditure (European Parliament, 2022). But both countries should be on the way to realize this correction in 2024.

In Ireland, public expenditure has known a huge increase until reaching 44.90% of GDP in 2009, with also a huge increase in the public indebtedness until 120% of GDP in 2013. Nevertheless, the public debt decreased afterward and was brought back to 44.70% of GDP in 2022. Therefore, with a long-term nominal interest rate (

In 2022, general government budget deficits represented 4.4% of GDP in Latvia and 5.8% of GDP in Malta. These values were excessive according to the Fiscal Compact and to fiscal rules prevailing in the European Union before 2020. Nevertheless, public debts were low in both countries, and therefore, the public expenditure rule proposed in our paper would consider that the fiscal situation of these countries was not dangerous.

Countries with an Intermediate Public Debt

Besides, there are six EMU member States with an intermediate public debt level. In Germany, the public debt reached 66.30% of GDP in 2022, a value which is slightly above the Maastricht reference value, but which remains sustainable. Indeed, long-term nominal interest rates on the German public debt have been negative and particularly low before the COVID-19 crisis (

In Austria, the public debt reached 78.40% of GDP in 2022, a value which is above the Maastricht reference value. However, long-term nominal interest rates on the Austrian public debt have been sufficiently low before the COVID-19 crisis (

In Finland, the public debt reached 73% of GDP in 2022, a value which is above the Maastricht reference value but which remains sustainable. Indeed, long-term nominal interest rates on the Finnish public debt have been sufficiently low before the COVID-19 crisis (

In Slovenia, the public debt was only 21.80% of GDP in 2008, but it reached 69.90% of GDP in 2022, a value which is now above the Maastricht reference value. A long-term share of government revenue in GDP (

In Slovakia, the public debt reached 57.80% of GDP in 2022, which corresponds to the Maastricht reference value and which is sustainable. A long-term share of government revenue in GDP (

In Cyprus, the public debt was only 45.50% of GDP in 2008, but it reached 113.8% of GDP in 2020, a value which can be considered as excessively high. A long-term share of government revenue in GDP (

High-Debt Member Countries

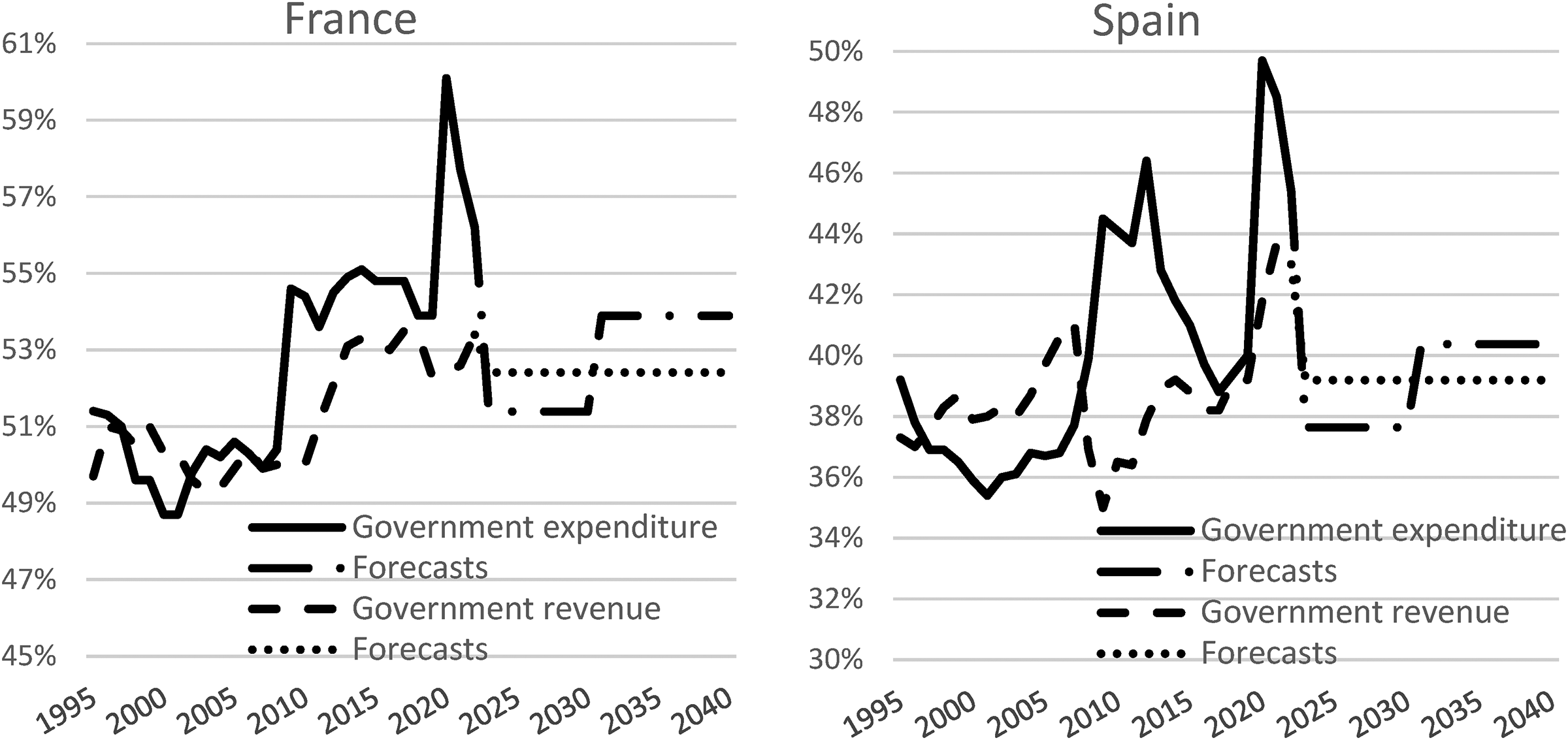

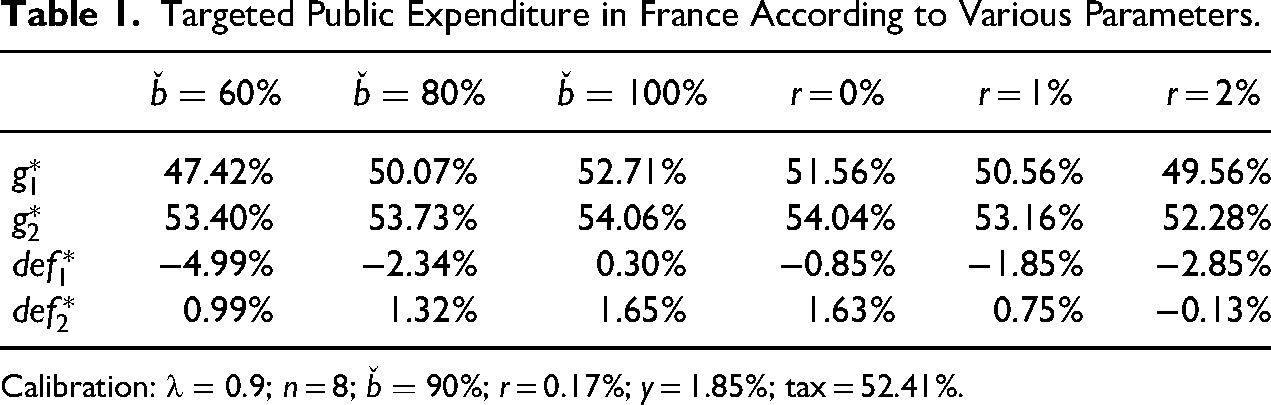

There are six EMU member States with a high level of public debt. In France, in 2022, the public debt reached 111.6% of GDP, and the government budget deficit 4.7% of GDP, values which are well above the Maastricht reference values. Besides, the trend of this public debt is dangerous. Indeed, a long-term share of government revenue in GDP (

Government expenditure and revenue in France and Spain.

Current French public expenditure is excessive even to stabilize the public indebtedness level at the targeted value: (

Targeted Public Expenditure in France According to Various Parameters.

Calibration: λ = 0.9; n = 8;

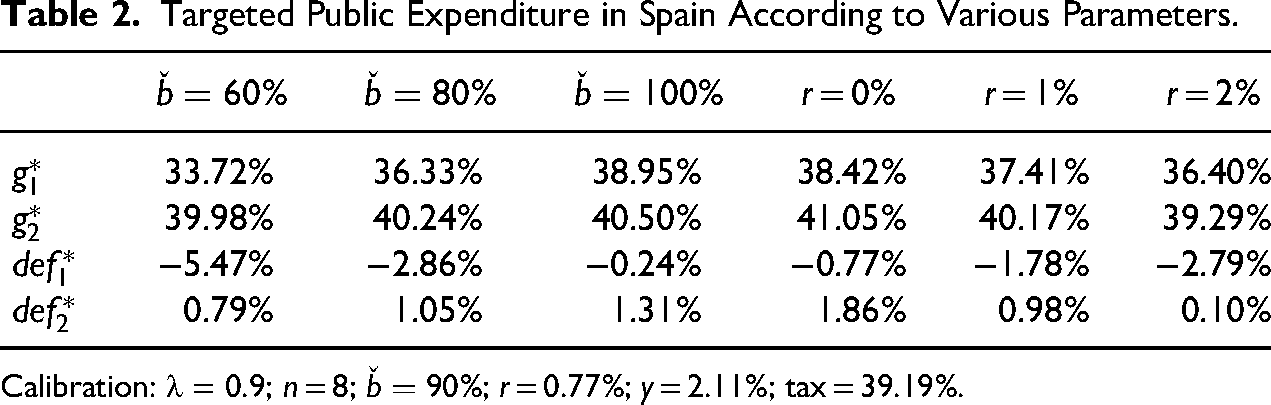

In Spain, in 2022, the public debt reached 113.2% of GDP, and the government budget deficit 4.8% of GDP, values which are well above the Maastricht reference values. Besides, the trend of this public debt is dangerous. Indeed, a long-term share of government revenue in GDP (

Current Spanish public expenditure is excessive even to stabilize the public indebtedness level at the targeted value: (

Targeted Public Expenditure in Spain According to Various Parameters.

Calibration: λ = 0.9; n = 8;

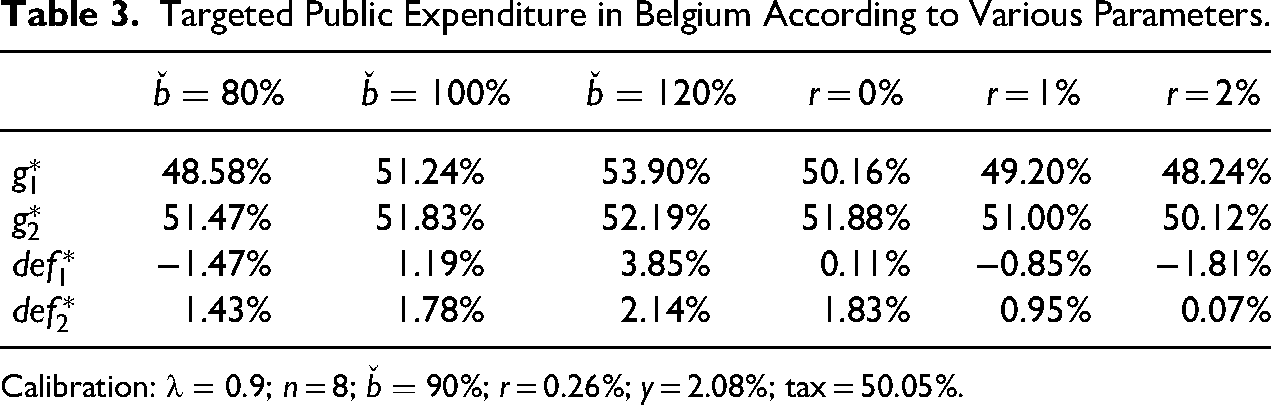

In Belgium, in 2022, the public debt reached 105.1% of GDP, and the government budget deficit 3.9% of GDP, values which are well above the Maastricht reference values. Besides, the trend of this public debt is dangerous. Indeed, a long-term share of government revenue in GDP (

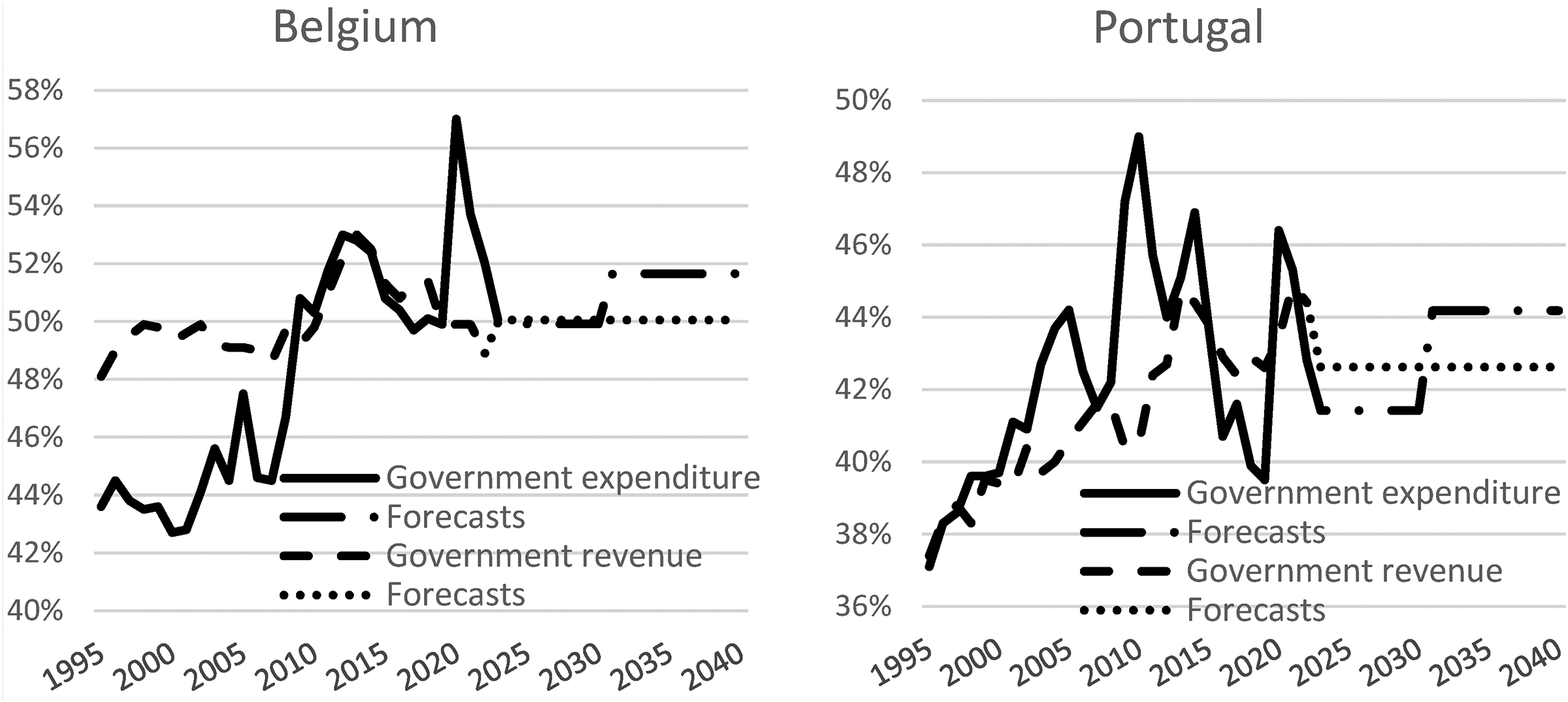

Government expenditure and revenue in Belgium and Portugal.

Current Belgian public expenditure could only stabilize the public indebtedness at a targeted level around (

Targeted Public Expenditure in Belgium According to Various Parameters.

Calibration: λ = 0.9; n = 8;

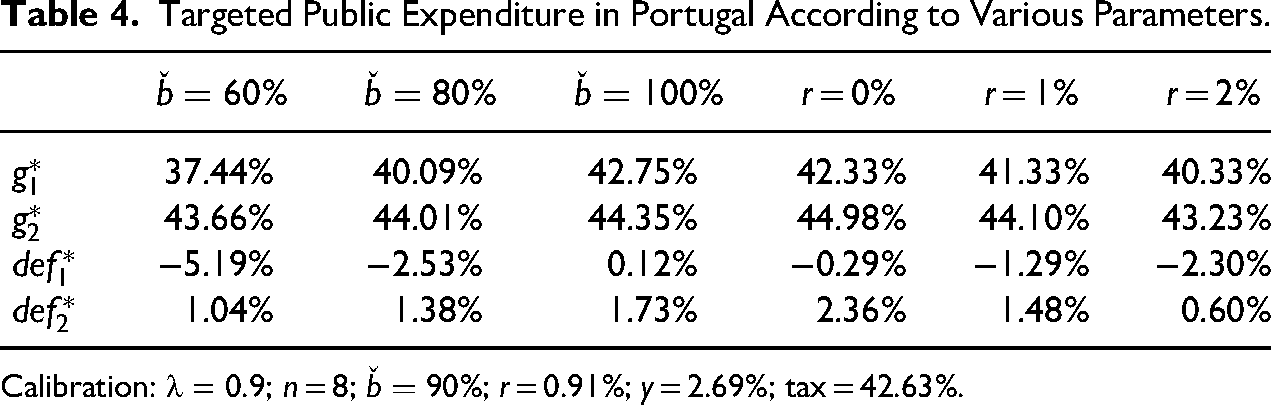

In Portugal, in 2022, the public debt reached 113.9% of GDP; however, the government budget deficit was only 0.4% of GDP, a value which remained well below the Maastricht reference value, and compatible with a healthy fiscal situation. A long-term share of government revenue in GDP (

Current Portuguese public expenditure could only stabilize the public indebtedness level at the targeted value: (

Targeted Public Expenditure in Portugal According to Various Parameters.

Calibration: λ = 0.9; n = 8;

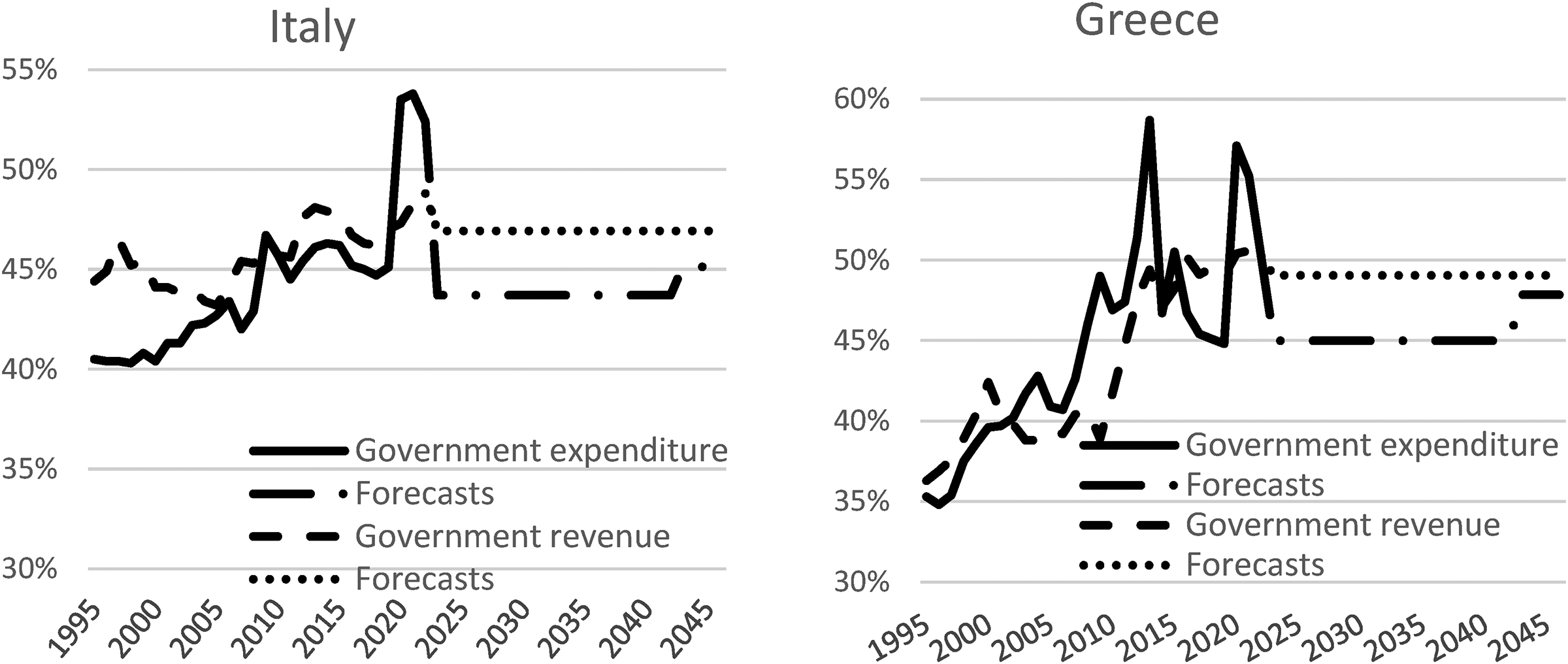

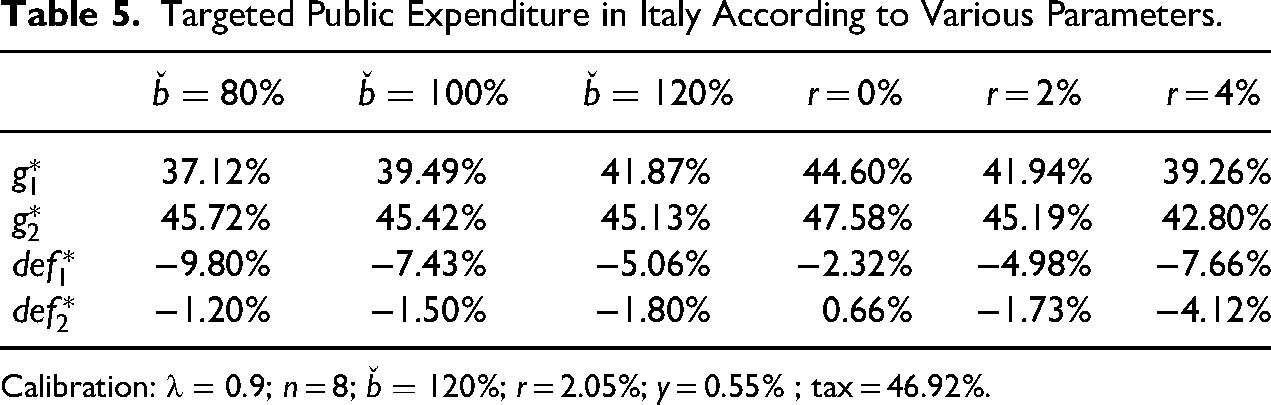

In Italy, in 2022, the public debt reached 144.4% of GDP, and the government budget deficit 8% of GDP, values which are largely above the Maastricht reference values. Besides, the trend of this public debt is dangerous. Indeed, a long-term share of government revenue in GDP (

Government expenditure and revenue in Italy and Greece.

Current Italian public expenditure could not even stabilize the public indebtedness at the level (

Targeted Public Expenditure in Italy According to Various Parameters.

Calibration: λ = 0.9; n = 8;

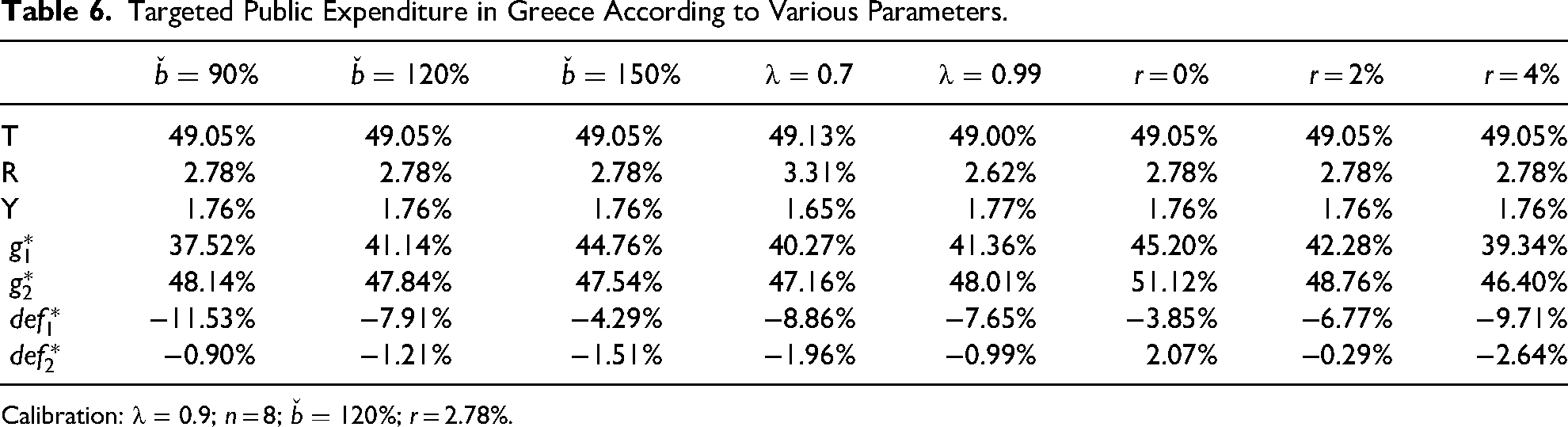

In 2017, the plan of the Eurogroup for Greece contemplated primary budget surpluses of 3.5% of GDP between 2017 and 2022, and afterward steady-state budget surpluses close to 2% of GDP between 2023 and 2060. Such projections represented an excessive weight for future generations and did not seem politically feasible. So, Eichengreen et al. (2018) underlined that under plausible projections for growth, interest rates, and fiscal performance, the Greek government's debt was unsustainable. Therefore, they assumed that more official debt relief was unavoidable, in the form of interest rate concessions and maturity extensions. Indeed, in 2022, the Greek public debt reached 171.30% of GDP, an excessively high value, even if the budget deficit was only 2.3% of GDP and below the Maastricht reference value. What are then the teachings of our model regarding the Greek situation?

A long-term share of government revenue in GDP (

Current Greek public expenditure would be excessive to stabilize the public indebtedness even at the targeted level (

Targeted Public Expenditure in Greece According to Various Parameters.

Calibration: λ = 0.9; n = 8;

Conclusion

Sustainability of the public debt should obviously be the fundamental goal of any fiscal framework. However, in the European EMU, in a background where monetary policy of the European Central Bank can only manage an average situation in the whole Union, economic stabilization cannot be left to monetary policy alone, and the global fiscal policy must take part to this macro-economic stabilization. Beyond fiscal rules for the solvency of the public debt, it is then important to consider also the stabilization function of the global fiscal stance in the monetary union. A rule in terms of nominal primary public expenditure, including a debt feedback mechanism, could then be enforced in the EMU.

The budget rule in terms of public expenditure proposed in the current paper could easily be enforced by countries with low public debt levels. On the contrary, such a rule would require an important adjustment of public expenditure for high-debt countries, which are therefore in a more difficult and problematic situation. Six EMU member countries are then particularly highly indebted and should probably control and reduce their public expenditure in order to make their public debt sustainable: France, Spain, Italy, Belgium, Portugal, and Greece.

Nevertheless, global fiscal policy and fiscal coordination between the fiscal authorities are as important as fiscal rules. This coordination would imply the reduction of the excessive public indebtedness of some countries but in correlation with higher public expenditure and higher public investment in high-growth sectors for weakly indebted countries. It also means a fiscal capacity of the European budget, in order to promote public investment with a high profitability for the future, for example regarding green investment, public infrastructure, and the digital economy. In this context, the EU recovery plan Next Generation EU is granted with €750 billion, and it is based on Community-level borrowing to finance priority investments in member States. Finally, the question of the most appropriate institutional framework to really enforce an effective fiscal rule is very important, but beyond the scope of the current paper.

Footnotes

Acknowledgments

The author deeply thanks the two referees of Public Finance Review for their very interesting and helpful comments, which helped me to improve the first version of the paper.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.