Abstract

This policy insights paper explores the development of public-private partnerships (PPPs) in the Gulf Cooperation Council (GCC) region over the past three decades and argues that although GCC states did not embark on a full-fledged experience with PPPs, unstable oil and gas prices are changing this approach. PPPs are increasingly gaining strong political support, and GCC states have made numerous reforms to the existing regulatory and institutional systems to enable a more extensive uptake of PPPs that encompasses a broader spectrum of social and economic infrastructure services. This article offers an overview of the historical development of PPPs in the GCC region since the 1990s, illustrating policy discussions and motivations for adopting PPPs, the meaning and types of PPP projects that have been implemented or planned in the region, and the most recent developments in the regulatory and institutional frameworks underpinning PPPs.

Keywords

Introduction

Public-private partnerships (PPPs) are “agreements where public sector bodies enter into long term-contractual agreements with private sector entities for the construction or management of public sector infrastructure facilities or the provision of services” (Grimsey & Lewis, 2000, p. 108). The PPP research has primarily centered either on the experiences of countries that seek the promised efficiency of the private sector in delivering infrastructure projects (Koppenjan, 2005), or the experiences of developing countries where the World Bank and other developmental agencies recommended PPPs as part of a broader package of structural reforms to address budgetary deficits (OECD, 2013; Osei, 2004; Pessoa, 2007; World Bank, 2019). While this literature has broadened our knowledge about the successes and failures of PPPs in different geographical settings where financial or efficiency gains are the main drivers for embracing PPPs, we know much less about the experiences of rich, oil-exporting countries where the financial or efficiency gains from PPPs might not be as significant.

Specifically, what remains heavily unexplored in existing PPP scholarly debates is the experiences of oil-exporting countries of the Gulf Cooperation Council (GCC) region, which encompasses the countries of Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates (UAE) that have had limited experience with the PPP phenomenon over the past few decades (Biygautane, 2017). This article aims to address this gap in the literature and investigate how PPP has evolved within the GCC states to form a better understanding of how PPPs emerge and perform beyond the geographic contexts of North America, Europe, or developing countries, all of which are well documented in the PPP literature. Furthermore, the GCC region is undergoing critical and transformative reforms with the aim of increasing the role of the private sector in the economy. GCC governments consider PPPs as an essential pillar of this transformative journey (Middle East Economy, 2023).

This article explores the development of PPPs in the GCC region over the past three decades and finds that PPPs have been used in technology-intensive sectors, particularly Independent Water Power Plants (IWPPs) and Independent Power Plants (IPPs), which GCC governments could not deliver on their own. The central argument of this policy insights paper is that while GCC states were selective in their choice of which PPPs to adopt, not initially embarking on a full-fledged experience with PPPs due to abundant financial resources from oil revenues, the declining prices of oil and gas are changing this approach. There is a robust political drive from GCC governments to strengthen the role of the private sector in the economy and diversify their economies, which offers a strong motivation for adopting PPPs at a much larger and broader scale.

The authors provide an overview of the historical development of PPPs in the GCC region since the 1990s, illustrating policy discussions and motivations for adopting PPPs, the meaning and types of PPP projects that have been implemented or planned in the region, and the most recent developments in the regulatory and institutional frameworks underpinning PPPs in the GCC. The article highlights the serious strategic intent of GCC governments to institutionalize PPPs as a preferred form of project delivery, one that has translated into numerous institutional and regulatory reforms already underway.

Policy Discussions and Interest in Public-Private Partnerships Within the Gulf Cooperation Council Region

The traditional motivations for adopting PPPs, such as financing public projects through private funds and seeking the capability and know-how of the private sector to deliver services with higher levels of efficiency and value for money, did not find receptive ground in the GCC region over the past few decades. The reasons were an excess of good fortune bestowed by nature. The GCC region is home to 34% of the global proven oil reserves (International Energy Agency, 2023) and the revenue from this abundant source of income meant that GCC governments could directly fund their infrastructure projects, irrespective of the levels of efficiency.

Elsewhere in the world, PPPs were seen as a central part of the neo-liberal policy agenda (Liu et al., 2022, 2023). Debates and policy discussions around PPPs flourished in many countries less well-endowed by nature. It was in the second half of 2014, that GCC governments started seriously considering PPPs as an appropriate policy alternative for the provision of infrastructure services. Nature’s bounty was diminishing in value. This year witnessed one of the sharpest recent falls in global oil prices. The price plunged from $105 per barrel in 2013 to less than $50 in 2015 and continued to fall to a record low of $40 in 2016, as shown in Figure 1. Although oil prices have witnessed considerable increases since the Russian invasion of Ukraine in 2022, soaring to an average record high of $102, the capacity of GCC governments to fully finance infrastructure projects was seriously challenged by budget deficits occurring during the previous ten years of low oil prices (International Monetary Fund, 2020). Fluctuation of global oil prices ($US/bbl) between 2013 and 2022. Source: MEED (2023)

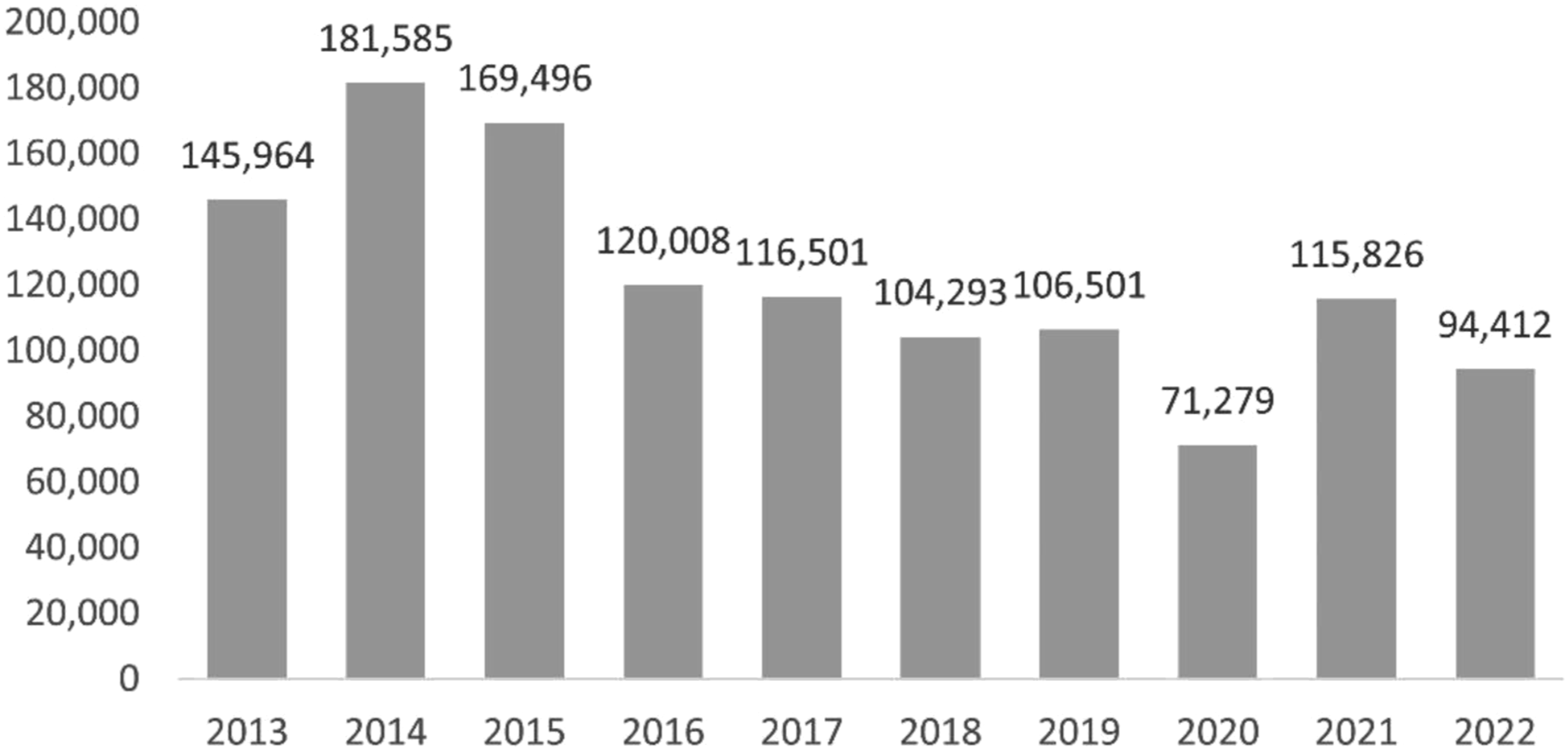

Due to lower global oil prices, which resulted in budget deficits, the value of infrastructure contracts awarded by GCC governments between 2013 and 2022 constantly declined. Figure 2 demonstrates that while in 2014 the infrastructure projects awarded amounted to more than $181 billion, their value gradually decreased to a record low of $71 billion by 2020. Lower investment in infrastructure projects was a direct consequence of lower oil prices as well as the repercussions of the COVID-19 pandemic. Despite the GCC countries’ lifting all restrictions imposed on travel and work in 2022, these GCC governments maintained a relatively conservative approach their public spending (MEED, 2023: see Figure 2). Value of GCC contracts awarded 2012–2023 ($ million). Source: MEED (2023)

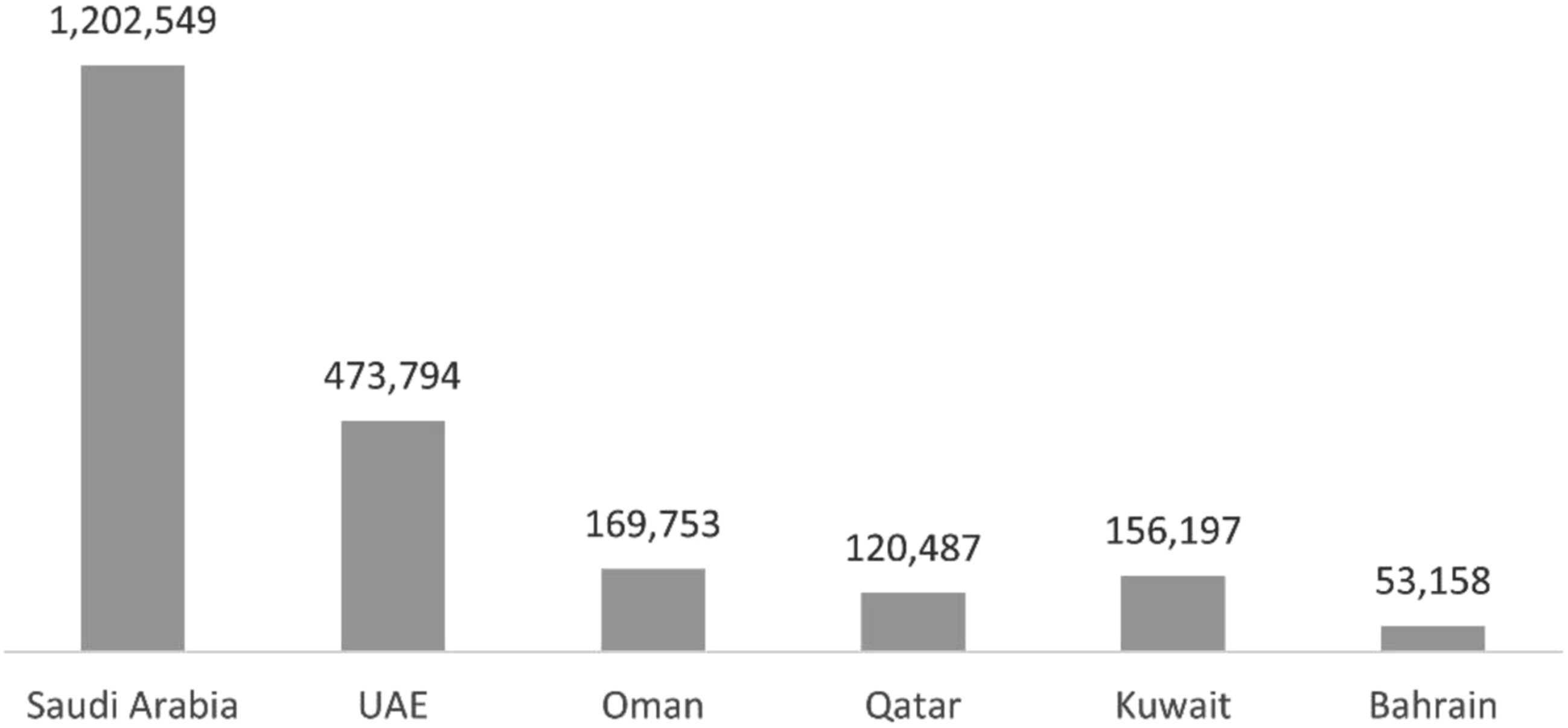

The decline in government spending and the value of contracts awarded particularly affected the construction sector. While, since 2019, investments in gas and power projects—which form the bedrock for government revenues—have increased significantly from $11 billion in 2019 to $30 billion in 2021 and from $5 billion to $13 billion, respectively (MEED, 2023), government spending on infrastructure dropped from $41 billion in 2019 to $23 billion, and from $16 billion to $8 billion in the transportation sector in 2021 (MEED, 2023). Importantly, direct government spending on infrastructure projects declined during a period when the need for social and economic infrastructure projects was increasing drastically. The result was significant spending deficits on infrastructure projects (MEED, 2023). As Figure 3 shows, there is a shortfall of more than $2 trillion in known, planned, but unawarded projects in the GCC region, particularly in Saudi Arabia, in which there is $1.2 trillion in unawarded projects, followed by the UAE, with unawarded projects worth more than $47 billion (Middle East Economy, 2023). Value of known, planned, and un-awarded projects in the GCC region in 2022 ($ million). Source: MEED (2023)

The GCC states’ strategic vision collectively aims to achieve ambitious economic development plans that consist mainly of diversifying their economies and building the necessary infrastructure for tourism and industrialization to develop further. Given the decade-long volatile and unpredictable trajectory of oil prices and the resultant negative repercussions on government balance sheets, it is increasingly evident that the decades of purely government-funded infrastructure projects are ending (Middle East Economy, 2023). It would seem to be inevitable that GCC governments will engage local and foreign investors and commercial banks in the financing, construction, and operation of mega-infrastructure projects. PPPs offer a viable tool for this purpose. Transitioning out of oil and gas dependence and diversifying economies will have to be driven mainly by the private sector.

The Meaning and Types of Public-Private Partnership Projects in the Gulf Cooperation Council

The idea of partnerships between the public and private sectors is not entirely new to GCC states. Before the discovery of natural resources in the region, the rulers relied heavily on the traditional merchant families who, for centuries, had financed and operated critical projects, such as roads, seaports, and the provision of other essential social infrastructure (Kamrava, 2012). However, since the 1950s the discovery and exploitation of oil and gas resources in commercial quantities saw the transformation of GCC states from relatively poor tribal states to wealthy modern societies. This transformative era was supported by accelerated government spending to develop state-of-the-art infrastructure facilities. An economic model developed in this period that relied on a culture of patron-client relationships in which the local private sector relied entirely on government spending and contracts to deliver infrastructure services (Kamrava, 2009). It would be appropriate to regard the relations that ensued between government agencies and selected private sector firms as akin to those of a government as a patron and the contactors as clients. The ever-present risk in such arrangement is that of ‘crony capitalism’ as Diwan and Haidar (2019) argue. PPPs, in principle, by combining government funding with private sector initiative and competitive tendering, offer a reforming route from any ‘cronyism’ that past practices might have produced, offering the prospect of improved value for money (Biygautane, 2023).

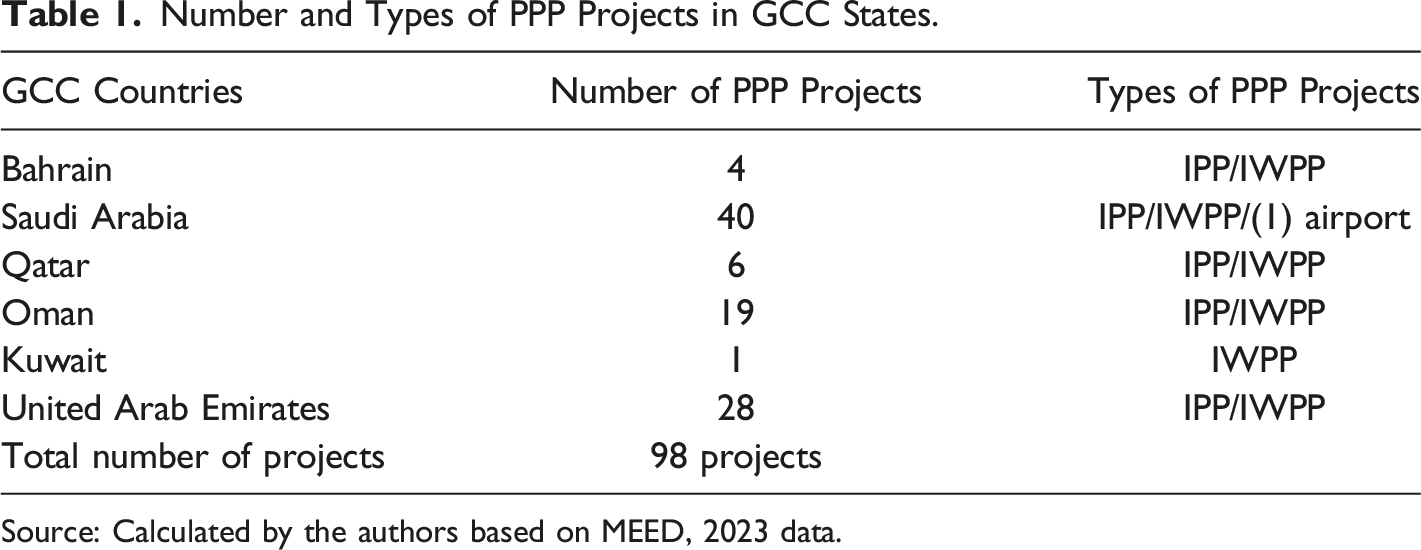

Number and Types of PPP Projects in GCC States.

Source: Calculated by the authors based on MEED, 2023 data.

GCC states have not yet extended their use of PPPs to other social and economic sectors for several reasons. First, these projects could be financed by government without the need to go through a complex bidding process involving numerous local and foreign private actors. Recourse to open competitive tendering would have delayed the delivery of essential infrastructure projects that were important to meet the economic and social needs of these countries. Second, PPPs require a complete restructuring of legal and institutional systems underpinning the procurement of public infrastructure projects. GCC states have historically financed infrastructure projects directly with the private sector in charge of delivering on a traditional Engineering, Procurement and Construction (EPC) basis. Consequently, the existing institutional and legal arrangements were only suitable for this construction model and not for PPPs (Biygautane, 2022). Third, those countries elsewhere that rely heavily on PPPs have a long history of private sector engagement in economic development and delivery of services. In part this was because these countries embraced the ethos of New Public Management (NPM), one of whose aims was to reduce the role of government in the economy. In the GCC, NPM has been of far less consequence because the role of government remains critically important in the provision of all social and economic services. Government drives economic growth and development, primarily supported by oil and gas revenues (Kamrava, 2009). Fourth, investment laws restricted foreign direct investment, in most GCC states, stipulating that local businesses had to own more than 51% of any project. Although business ownership rules have now changed in some GCC states, these regulations were the legal bottleneck that restricted the use of PPPs in the GCC, making it difficult to finance projects.

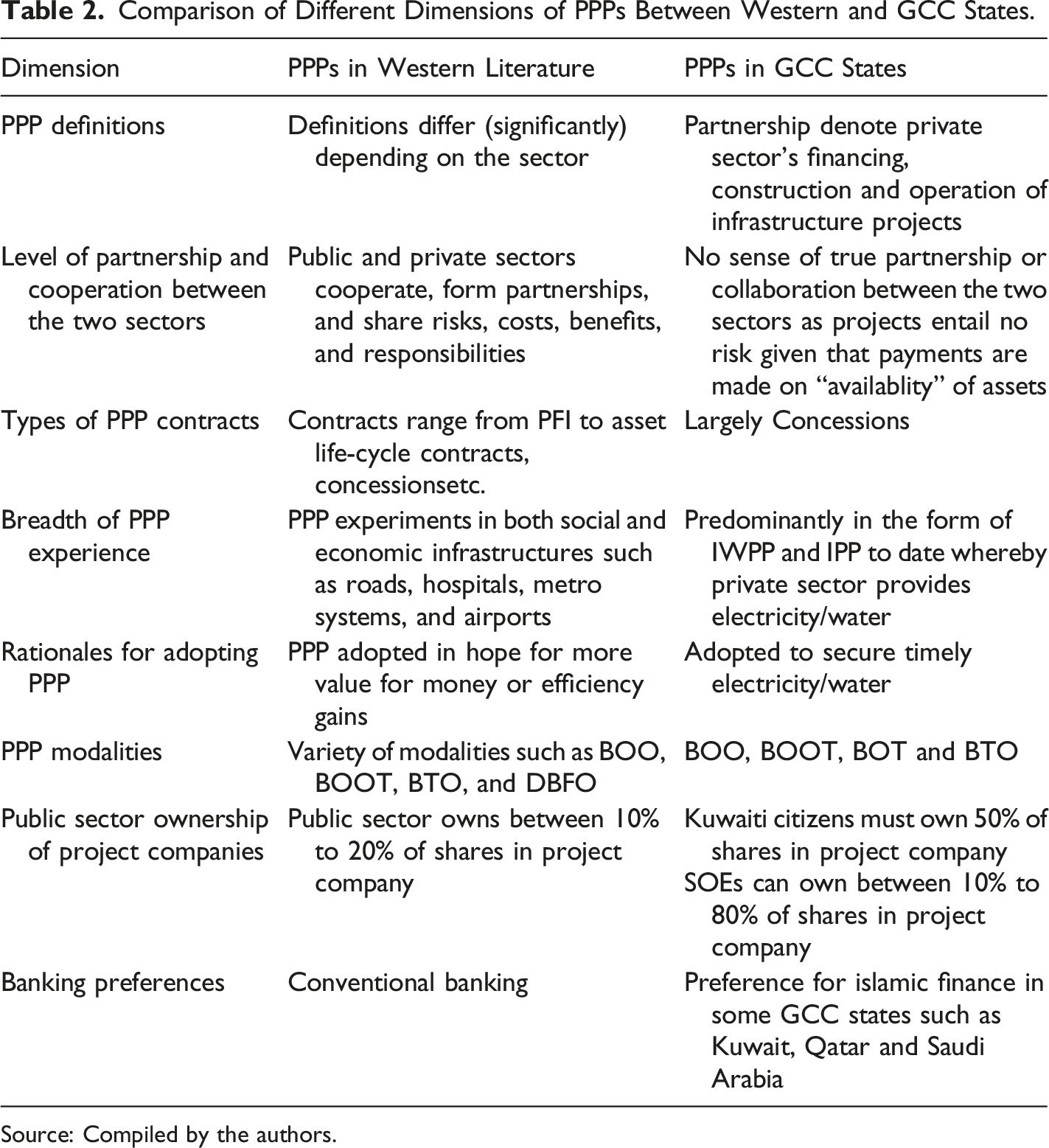

Comparison of Different Dimensions of PPPs Between Western and GCC States.

Source: Compiled by the authors.

Recent Developments in the Regulatory and Institutional Frameworks Underpinning Public-Private Partnerships in the Gulf Cooperation Council

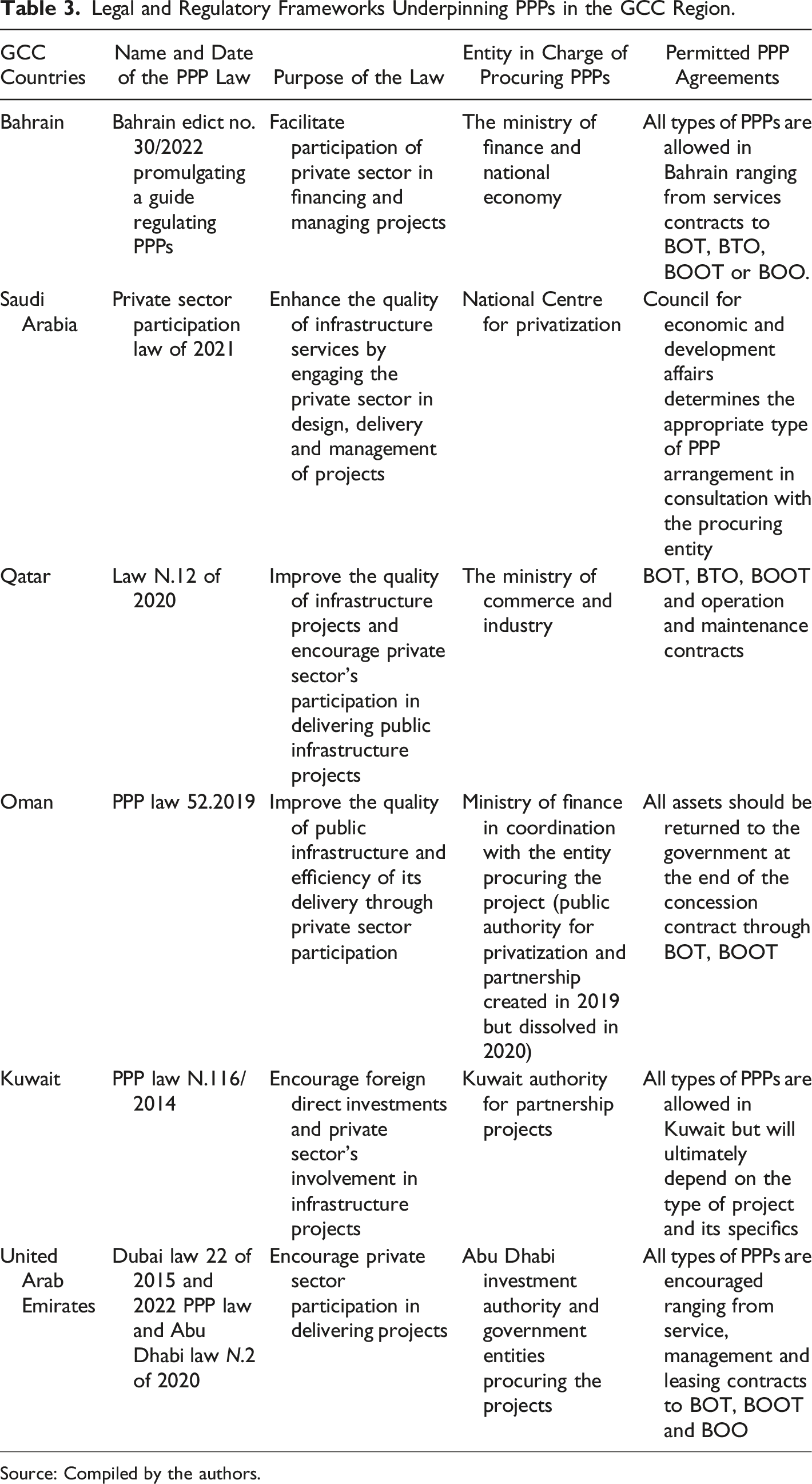

Legal and Regulatory Frameworks Underpinning PPPs in the GCC Region.

Source: Compiled by the authors.

A bigger critical juncture occurred during the advent of COVID-19 which resulted in a further decline in government spending on infrastructure and an increased supply of social benefits to citizens and support to local businesses (Gulf Business, 2021). The other GCC states accelerated the promulgation of PPP laws, with Qatar and Abu Dhabi issuing their PPP laws in 2020, Saudi Arabia following suit in 2021, Bahrain in 2022, with Dubai issuing a newer PPP law in 2022 that simplified the process of initiating and governing PPPs. COVID-19 was a strong driving force for embracing PPPs. Its consequences, with restricted movement and investment, demonstrated the fragility of the economies of the GCC state’s extensive reliance on oil and gas resources that tend to fluctuate drastically in response to external shocks. GCC states are now demonstrating strong political support for opening their economies to international investors, with several states, such as the UAE and Saudi Arabia, unprecedentedly simplifying their investment laws to allow 100% foreign ownership.

These recent PPP laws offer a long-awaited regulatory and institutional framework suitable for administering PPP projects. As shown in Table 3, the laws offer a clear purpose that generally aims to facilitate the partnership of the private sector in financing and managing infrastructure projects, thus enhancing the quality of projects and their efficiency gains. Kuwait’s PPP law directly encourages foreign direct investments as one of the key targets of adopting PPPs for infrastructure services. Furthermore, clear institutional frameworks were also designed to deliver PPP projects that were to be embedded within the ministries of finance, as in Bahrain and Oman, or within the ministry of commerce and industry, as in Qatar. At the same time, other countries such as Saudi Arabia, Kuwait, and the UAE created dedicated and specialized PPP units to procure projects on behalf of public entities. In addition, these entities showcase existing projects to foreign investors, locally and internationally, inviting the provision of know-how and other forms of support required to facilitate fruitful partnerships between the public sector and local and foreign private actors.

Discussion and Lessons From the Gulf Cooperation Council Experience

The findings of this policy insights paper offer valuable theoretical and practical insights to expand our knowledge and understanding of the phenomenon of PPPs beyond the Western context that dominates the PPP literature. The paper presented the experience of GCC states’ encounters with PPPs and described the unique form of PPP exclusively focused on IWPPs and IPPs. GCC experience demonstrates a motivation for and approach to delivering PPPs that is driven by a lack of capacity to deliver critical infrastructure projects in the domain of utilities that are technology and capital-intensive. These forms of PPP do not capture the essence and spirit of PPPs embedded in the UK’s PFI model, the seed for so many global PPPs. The existing PPP literature argues that PPPs are used to provide social and economic infrastructure that is delivered through raising private finance to fund projects within budget and time constraints (Osei, 2004). Advocates of PPPs argue that they ultimately enhance the efficiency of projects and services (OECD, 2013; Pessoa, 2007). The wider applications of the public private partnership model have not emerged as of now in the Gulf states.

In large part, the paper shows how dependence on oil revenues to finance public projects created a culture and tradition of dependence on state funding, that limited the internationalization of private sector participation in delivering infrastructure services. PPPs have flourished in institutional contexts that have a history of active participation of the private sector in delivering services through outsourcing or privatization of government entities. For GCC states to benefit fully from the assumed efficiency gains that PPPs can offer, they would need a drastic shift from regarding the public sector as the sponsor of projects and the private sector as the delivery mechanism. The binarism implicit to this model would need to be subsumed by an institutional and organizational context in which the public and private sectors work together, respecting each other’s perspectives, sharing risks and responsibilities of delivering projects, learning in partnership. The paper illustrates the GCC region going through a transformational phase, shifting from using PPPs to import technological know-how for building, running, and maintaining utilities-related projects, into PPPs as capital-raising ventures. Interest in PPPs has tended to fluctuate in the GCC region, largely in response to exogenous shocks, particularly financial crises, which saw interest in PPPs rise with the fall of oil prices only to see interest decline once oil prices recovered again.

The GCC region demonstrates an unprecedented political will to use PPPs as a vehicle for transition from a state-led economic development model that relies heavily on oil and gas resources into a mature economy driven by the private sector (Middle East Economy, 2023). All GCC states have now adopted robust regulatory and institutional frameworks that would convince international investors that the GCC region is a safe environment for investment in large-scale mega-infrastructure projects. In 2022, PPPs were awarded for numerous projects in social housing, hospitals, schools, and other projects across the GCC region. The uptake in PPPs across a broader spectrum indicates the region’s willingness to innovate beyond the utility sector, creating numerous opportunities for further evolution within the Gulf context. Given the emergence of PPPs as a specific object of interdisciplinary research (Liu et al., 2022, 2023), the opportunities for further empirical research on their effectiveness in practice could bot enrich the Gulf context and be enriched by it.

Conclusion

The recent policy developments in PPPs within the GCC region demonstrate that although PPPs received little attention from GCC states in the past three decades, there is a clear policy shift towards embracing them for future infrastructure development. Lower oil prices have functioned as a critical driver toward adopting PPPs, and all GCC states have now put regulatory and institutional frameworks in place that could potentially enable a bigger uptake of PPP projects in the region. As the transition globally from fossil to sustainable sources of energy quickens, hastened in Europe by the need to be less dependent on unstable sources of supply, such as Russia (Clegg, 2023), together with the rapid rise of electrification of the automobile sector, led by China (People’s Daily Online, 2023) the longer-term prospects for the fossil fuel industry as a sustaining economic foundation recede, making PPPs ever-more attractive as a way of financing future infrastructure provision.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.