Abstract

Public-Private Partnerships (PPPs) have been adopted globally to reduce funding gaps amidst an increasing need for public infrastructure. However, they are prone to several risks. Little attention has been paid to this crucial phenomenon in Uganda, despite the rising interest in the use of the PPP model. Through a questionnaire survey with PPP experts in Uganda, 34 principal risks were identified of which the top 10 are construction completion, government corruption, construction cost overrun, land acquisition, delay in project approval and permits, high financing cost, operation cost overrun, inadequate tender competition, procurement risk, and inability to service debt risk. Most of these were found to arise from inadequate experience in PPPs, the complexity of the PPP model, high levels of corruption and the immature domestic financial market. The knowledge of these risks can guide PPP contract negotiations and potential investors in their investment decisions, especially the objective assessment of PPP projects.

Introduction

Globally, about 800 million, 4.5 billion, and 2.2 billion people cannot access electricity, good sanitation, and safe drinking water, respectively, and most countries have congested and inadequate transport facilities (World Bank, 2019b). This is in conflict with the United Nations (UN) 2030 Agenda for sustainable development which foresees a world free of poverty, hunger, and disease, with quality education, health care, and infrastructure (United Nations, 2015). Many countries are currently witnessing widening infrastructure gaps and are financially constrained to provide much-needed infrastructure (Pratap & Chakrabarti, 2017). For example, it is estimated that countries need to invest 3.8% of the GDP, or around US$ 3.3 trillion, to achieve their estimated growth rates (Badasyan & Riemann, 2020). This situation has been worsened by the COVID-19 pandemic which has added to already existing development challenges, including high debt burdens and weak governance, thereby putting more livelihoods at risk (Public-Private Infrastructure Advisory Facility, 2020). Also, there is increasing pressure on governments to reduce public sector debt, amidst limited funds for public infrastructure expansion (Ahmad et al., 2017; Carbonara et al., 2015; Carbonara & Pellegrino, 2018; Gopalan, 2014). All these challenges are coupled with the poor performance of conventional public procurement which has been associated with high costs, delays, operational inefficiencies, and poor quality infrastructure and services (Demirag et al., 2012; Grimsey & Lewis, 2004; Hwang et al., 2013; Jin, 2010; Mustafa, 1999; Wang et al., 2018; Xu et al., 2010).

These pressures have led governments to enter into longer-term contracts with the private sector to develop, finance, construct, and operate public infrastructure (Dykes & Jones, 2016; Grimsey & Lewis, 2002; Jin, 2010; Kisitu, 2018; Liu et al., 2014). Furthermore, the COVID-19 pandemic has underscored the value of relationships between the public and private sectors (Rabie & Ndevu, 2021). The private sector is considered to possess better technical and managerial abilities which places it in a better position to deliver competitive, high quality, and less costly infrastructure projects than the public sector (Forrer et al., 2010, p. 475; Shrestha et al., 2019). Accordingly, governments are seeking increased participation of the private sector in the provision of public infrastructure through Public-Private Partnerships (PPPs). The use of PPPs is in line with the UN SDG17.17 which advocates for partnerships between governments, the private sector, and civil society to achieve the sustainable development agenda (Leitao et al., 2018; United Nations, 2015). PPPs are also in line with New Public Management theory that focuses on improving the effectiveness and efficiency of public service delivery by borrowing principles from the private sector (Diefenbach, 2009; Klijn & Koppenjan, 2012). Therefore, PPPs have emerged as an alternative approach for delivering public infrastructure as governments continue to review how to fund the increasing demand for infrastructure amidst the limited funds (Anderson, 2012; Carbonara et al., 2014; Grimsey & Lewis, 2002; Ibrahim et al., 2006; Wang et al., 2019). This study adopts the World Bank's (2017a) definition of a PPP which defines it as a long-term contract between a private party and a government entity, for the provision of a public asset or service, in which the private party bears significant risk and management responsibility and compensation are linked to performance.

Despite the successes, failed PPPs have also been reported mainly due to unanticipated and/or poorly managed risks (Ibrahim et al., 2006; Ke et al., 2011; Kwak et al., 2009; Wang et al., 2018). For example, projects, such as the Channel Tunnel Project (1987), Toll Road Project in Mexico (1989–1994), Philippine Power Supply Project (2002), the Singapore Sports hub (2010–2014) and the Bird’s Nest stadium project in Beijing, Lekki toll road concession in Nigeria have struggled, mainly due to risks (Kim & Kwa, 2020; Nwangwu, 2013; Wang et al., 2020). Some of the risks facing PPP projects are macro-economic; changes in legislation; political opposition; construction; operations; corruption; market environments; force majeure; economic viability; and government intervention risks (Appuhami & Perera, 2016; Chan et al., 2011; Chung et al., 2010; Xu et al., 2010). These risks result from complex organisational structures, documentation, sub-agreements, and financing arrangements associated with PPP projects. In addition, differing project characteristics, political opportunism, poor legal and regulatory frameworks, the long duration of contractual relationships, and the involvement of many stakeholders with different interests are risks facing PPP projects (Carbonara et al., 2014; Grimsey & Lewis, 2002; Mazher et al., 2017; Shrestha et al., 2019; Zayyanu & Johar, 2017; Kwak et al., 2009; Sanda et al., 2020). Such risks have accounted for the poor performance of most PPPs in many countries, and Uganda is no exception.

Little is known about the principal risks associated with PPP projects in the Uganda context, a gap that this article sought to fill. Therefore, the research question being addressed in this study is: What are the principal risks associated with PPP projects in Uganda and at what PPP phase are they most likely to occur?

The research described in this paper was therefore structured to identify the most likely and impactful risks that arise during the various phases of the PPP process in Uganda. In this way, appropriate risk management strategies can be developed that are targeted to these specific risks rather than broadly addressing the entire PPP process. This article is organised as follows: it starts with an introduction followed by a discussion on PPPs in Uganda. It then moves on to discuss the literature on risks associated with PPPs followed by the methodology employed in this study. Results and discussion then follow in which the principal risks and the PPP phases where they are most likely to occur are discussed. The article ends with the conclusion and implications of the study.

Public-Private Partnerships in Uganda

Uganda has recently renewed its interest in the use of PPPs mainly in an effort to implement its “Vision 2040”, which is to transform “Uganda from a predominantly agricultural and low-income country to a competitive upper-middle-income country by 2040” (National Planning Authority, 2020; World Bank, 2019a). To achieve this vision, the government has planned to implement numerous infrastructure projects, particularly in the energy, transport, water, education, agriculture, and health sectors (National Planning Authority, 2020; World Bank, 2017b, p. 39). However, Uganda lacks the required resources to enable it to deliver the necessary infrastructure to achieve its vision. For example, Uganda currently has an annual infrastructure development financing gap of nearly US$1.4 billion and loses approximately US$300 million annually because of inefficiencies in public procurement (World Bank, 2017b, p. 41). Also, by the financial year 2020/2021, public sector debt had increased to 50% of Uganda’s GDP coupled with increasing interest payments (The World Bank Group, 2021). This has forced Uganda to consider collaborating with the private sector through PPPs to address this financing gap (Alinaitwe, 2011; Mwesigwa et al., 2018; World Bank., 2017, World Bank, 2019, World Bank., 2019).

Uganda’s move towards the involvement of the private sector in public service delivery started in the 1990s. Although real interest developed around the 2000s when a policy was developed by the Ministry of Finance Planning and Economic Development to guide PPP transactions (Kyaligonza, 2021). Uganda adopted the use of PPPs because of the need to fast-track construction of infrastructure projects, continued budgetary constraints, the huge demand for infrastructure investment, and the inefficiencies associated with traditional public procurement (Kyaligonza, 2021; Mwesigwa et al., 2018). Uganda has now developed a comprehensive regulatory framework for PPP implementation.

PPPs in Uganda are regulated by the PPP policy framework of 2010 which informed the subsequent PPP Act of 2015, and the PPP Regulations and Guidelines of 2019. The PPP Act as the principal law seeks “to regulate the identification, preparation, procurement, implementation, maintenance, operation, management, monitoring and evaluation of PPP throughout the project cycle.” (World Bank, 2017b, p. 44). Regarding the institutional framework, PPPs in Uganda are managed by the PPP Committee whose membership includes the Attorney General, the Permanent Secretary, a representative of the Ministry of Finance, the Office of the Prime Minister, the Ministry responsible for Lands, the Ministry responsible for Local Governments, the Director of the PPP Unit, a representative of the National Planning Authority, the Private Sector Foundation, the Uganda Investment Authority, experts from academia, and a retired judge. The main function of the PPP Committee is to ensure that each PPP project is consistent with the provisions of the PPP Act and to formulate policies on PPPs (Section 7 of the PPP Act). The PPP Unit serves as the secretariat and technical arm of the PPP Committee and provides technical, legal, and financial expertise to the PPP Committee and the project team (Sections 10 & 11 of the PPP Act). The contracting authority is responsible for identifying, appraising, developing, procuring, and monitoring PPP projects (Section 12 of the PPP Act). The other parties involved in the management of PPPs include the accounting officer, project officer, project teams, transaction advisor, process auditor, evaluation committee, and the private party (Section 13-20 of the PPP Act) (PPP Unit, 2019b; Republic of Uganda, 2015).

Regarding the PPP lifecycle, the PPP project goes through six major phases: 1. The inception phase is where projects are selected for further development as a PPP through the preparation of a project concept note. This involves the identification of the project, a preliminary cost-benefit analysis, confirmation of the suitability of the project for a PPP arrangement, the appointment of a project officer and project team, and the registration of the project with the PPP Unit. 2. The feasibility phase involves a detailed assessment of the feasibility and desirability of undertaking the project as a PPP arrangement. This includes a financial, value for money, and project risk analysis. The project is thoroughly investigated, and all aspects of the feasibility are assessed: technical, economic, financial, fiscal, environmental, social and legal, amongst others. The contracting authority also appoints the transaction advisor who will undertake the feasibility study and manage the procurement and contracting process. 3. The procurement phase involves the selection of a private party for the implementation of the PPP project. Depending on the procurement method used, this may involve a confirmation of funds; the preparation of bidding documents, the pre-competitive promotion of the project, pre-qualification, the issue, receipt and opening of bids, bid evaluation, contract negotiations, the process auditor’s report, a solicitor’s general review, cabinet approval of the agreement, and award of a contract. 4. The construction phase mainly involves the purchase, installation, and/or construction of the project’s assets. 5. The operation phase involves the operation and maintenance of the project assets and the provision of project services to the users. 6. The transfer phase involves the return of the assets to the contracting authority at the end of the PPP agreement. An inspection of the state of the public assets is conducted by an independent expert and a determination of any maintenance requirements is made before the assets are handed back (PPP Unit, 2019b; Republic of Uganda, 2015).

A total of 30 PPP contracts worth US$1.9 billion were concluded between 1990 and 2020 in Uganda (Cytonn, 2022; World Bank, 2019a, 2020) some of which include: Umeme Power Distribution Concession, Rift Valley Railways (RVR) Concession, Kampala Serena Hotel Concession, Bujagali Hydro Power Project (HPP), Kalangala Infrastructure Services (KIS) Project and Eskom Power Generation Concession (Mugarura, 2019; Nduhura, 2019; Niwabiine, 2019; World Bank, 2017b, 2019a; Yescombe, 2017). Other projects in the pipeline include Kampala-Jinja Expressway, The Uganda Rural Water Development Project, Gulu Logistics Hub, Kampala Waste Management. and Entebbe Iconic ICT Park (PPP Unit, 2022).

Many of these PPP projects such as the Umeme concession, Bujagali HPP, RVR. and KIS project have not performed as expected (Ladu, 2019; Mugarura, 2019; Office of the Auditor General, 2019c; World Bank, 2019a). Some have been characterised by public officials bypassing the PPP processes enshrined in the PPP Act 2015, high costs, delays, non-transparent negotiations, many false promises and complex contracts (Ladu, 2019; Mbabazi, 2019). For example, in the Nakivubo War Memorial Stadium project, the PPP agreement was signed with the private developer without considering the proposed amendments by the Auditor General. Moreover, the tenure of the PPP agreement between Nakivubo War Memorial Stadium and the private investor was never specified (contrary to section 43 of the PPP Act of 2015). Additionally, project monitoring reports were not submitted as required and the private party (Ham Enterprises) neither submitted any annual reports nor audited financial statements to the contracting authority (contrary to section 28(2)) of the PPP Act of 2015) (Office of the Auditor General, 2019a, pp. 8–9). There has also been unbalanced risk allocation and a tendency to dump all the risks to one party without adequately assessing their capacity to manage them. For example, in the KIS project, Umeme concession, Bujagali HPP, and Lubowa International Hospital, the private party is allocated the biggest share of profits from the project while the government has to absorb most of the losses (Ladu, 2019). Also, the 25-year RVR concession that had been operating the railway between Kenya and Uganda since 2006 failed to meet specifications and was terminated in 2017 (World Bank, 2019b). Another case is the International Specialised Hospital of Uganda worth US$379.71 million, which started attracting complaints before it even kicked off. This project was characterised by land ownership conflicts, dissatisfaction that no apparent risk had been transferred to the investor, a lack of transparency, complaints that the arbitration of contractual disputes was to be done in the UK, and bypassing PPP tendering procedures (Namusobya, 2019). Other examples are the Umeme and ESKOM 20-year concessions and the Bujagali HPP whereby risks were inappropriately assessed and allocated in favour of the investors at the expense of the end-users (World Bank, 2017b).

This suboptimal risk identification, allocation and management has resulted in mixed reactions concerning the relevance of PPPs as an alternative model for infrastructure development and increased debates on whether they have delivered their promise (Angumya, 2013; Mugarura, 2019; Nduhura, 2019). This may explain why several PPP projects in Uganda have delayed starting and in others, private investors have failed to commit to these projects (Mugarura, 2019; World Bank, 2019a). All of this could be attributed to the government’s failure to fully assess and manage risks associated with PPPs due to the limited skills in identifying, assessing, valuing, and allocating risks in PPP projects. This situation, therefore, forms the rationale for this study because if nothing is done, the PPP model in Uganda will continue to perform poorly and the infrastructure gap will continue to widen thus leaving very many people without access to the services provided by the needed infrastructure. By highlighting the principal risks, appropriate risk management strategies can be developed.

The choice of Uganda as a research context was justified for the following four reasons: 1. A study of this developing country allowed us to assess whether the insights presented in the literature on PPPs in developed countries apply to developing countries and to compare other developing countries’ experiences of risks of PPP projects with those of Uganda. 2. As risk management in PPP projects has not been well researched, especially in a developing country context, the study was conceived to fill this gap by investigating the topic in the context of Uganda. 3. The challenges and negative publicity of PPP projects in Uganda such as considering them to be politically motivated, costly, and not suitable for the Ugandan context also needed to be investigated. 4. Using Uganda as a case study provided the opportunity to understand the risks associated with PPPs, which would later lead to the development of a risk management model.

Literature Review

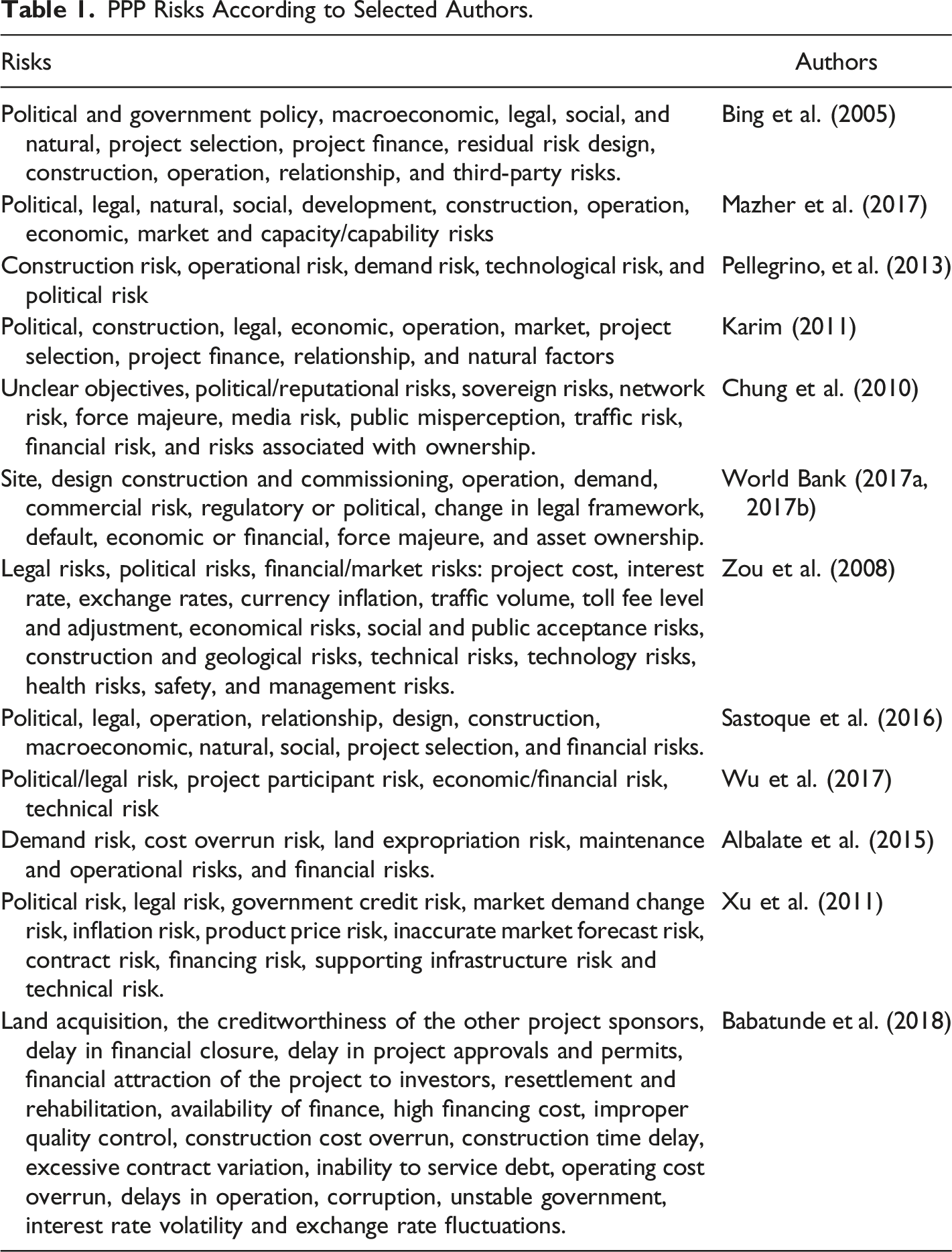

PPP Risks According to Selected Authors.

From these studies, we observed that the PPP model is associated with many risks and there is increasing research on PPPs in developing countries. This increased research interest is apparently due to the increased use of PPPs by governments in developing countries to address their funding challenges amidst increasing infrastructural needs (Gordon, 2012). However, the progress of the PPP model in developing countries has been slower than in developed economies (Appuhami et al., 2011; Wang et al., 2019) based on the number of PPP projects completed in developing countries when compared to those in developed countries. For example by 2020, in Africa, only 335 PPP projects worth US$ 59 billion had been completed, which include South Africa with 34 projects, Nigeria with 35, Uganda with 30 and Kenya with 22 (National Treasury, 2021; Nduhura, 2019; World Bank, 2019a). Developing countries not only have fewer PPP projects but also a higher number of failed ones (Osei-Kyei & Chan, 2016). Also, PPP markets in developing countries have not yet attracted a reasonable number of private investments (Osei-Kyei & Chan, 2017; Wang et al., 2019), Furthermore, of the studies that have been conducted on risk management in PPPs in developing countries (Ameyaw & Chan, 2013; Andon, 2012; Ma et al., 2019; Neto et al., 2016; Roumboutsos & Anagnostopoulos, 2008; Yakubu & A Anigbogu, 2016), none focused on Uganda.

There have been a few studies conducted regarding Ugandan PPPs, however. For example, a study regarding the governance of PPPs in Uganda Mugarura (2019) revealed that the adoption of PPPs in Uganda is hampered by limited understanding and awareness of PPPs, and low PPP readiness among other challenges. On the other hand, Settumba (2022), focused on the role of PPPs in the health sector and found that PPPs have helped the government fund many health programmes and infrastructural development. He also found out that political interference, bureaucracy in the process of implementing health projects, conflict of interest, poor communication and coordination, insufficient funding, and a poor sustainability plan as some of the challenges associated with PPPs in Uganda. Kyaligonza (2021) explored the barriers to private partner identification using the Uganda Police accommodation project as an example. He found that there were inception-related barriers to partner identification, weaknesses in the development of a business case, constraints to constituting a technical team to plan, coordinate, evaluate and report at each stage of the project, inadequate political oversight, and absence of pre-feasibility studies to inform PPP decision making. He also revealed significant tendering-related barriers, notably the absence of standardized PPP procurement documents and procedures and lack of established criteria for partner evaluation, lengthy procurement processes, high costs of bidding, changes in design and specifications and communication gaps. Nduhura (2019), in his study of the Bujagali hydropower project found that existing PPP models have enabled Uganda to improve availability, access, reliability, and quality of power, and reduced the cost of government in extending electricity to its people, although, tariffs and design issues remain key challenges. As a result, he proposed that the Build Own Operate and Transfer (BOOT) model be extended to Design Build Own Operate Transfer (DBOOT) alongside other interventions to improve competitiveness of the hydroelectricity sub-sector. Mwesigwa et al. (2019), revealed that the key antecedents of stakeholder management in Uganda include communication, engagement, commitment, and trust.

From the focus of these studies, we observe that risk management in PPP projects in the context of Uganda has hitherto not been well studied. Previous studies in their approach to the topic had centred on governance (Mugarura, 2019); the role of PPPs (Asasira & Ahimbisibwe, 2018; Settumba, 2022); challenges (Kisitu, 2018; Kyaligonza, 2021); success factors (Alinaitwe, 2011; Alinaitwe & Ayesiga, 2013; Nsasira et al., 2013); competitiveness and performance (Ndandiko, 2010; Nduhura, 2019; Niwabiine, 2019); and stakeholder management (Akampurira et al., 2017; Mwesigwa et al., 2019; Nuwagaba et al., 2022; Twinomuhwezi, 2018).

Methodology

A survey questionnaire was used to collect data from PPP practitioners in the public and private sectors and experts who had participated in PPP projects in different roles, namely bank or financial advisors, academics, researchers, and consultants. The population of the study could not readily be determined because there is no official list of PPP experts in Uganda because the PPP model is still in its infancy and the number of organisations involved in PPP projects is still evolving. Therefore, we used snowball and purposive sampling to identify 130 experts. This sample size is in line with Roscoe's (1975) rule of thumb where he indicated that sample sizes larger than 30 and less than 500 are appropriate for most research (Sekaran & Bougie, 2016). Similarly, Stutely (2014) recommend a minimum sample of 30 for statistical analyses (Saunders et al., 2019). Therefore, a sample of 130 respondents was above the recommended minimum sample size and because the PPP model is relatively new in Uganda and only a few experts could be considered for this study (Kisitu, 2018; Mugarura, 2019; Nduhura, 2019; Nuwagaba, 2019; Twinomuhwezi, 2018). Additionally, these respondents were involved or had experience in PPPs which meant that the validity of the data can be reasonably inferred which is in line with Patton's (2015) argument that the purposive samples should be judged based on the rationale of the study. Also, in parametric analysis, a minimum sample of 30 is required to fulfil the assumed normal distribution (Field, 2009; Salkind, 2017, p. 387). However, this study used nonparametric statistics, which are distribution-free. Similar sample size ranges were used by other scholars such as Ahmad et al.(2017), Ahmad et al. (2018), Babatunde et al. (2018), Hwang et al. (2013), Shrestha et al. (2017), Wu et al. (2017) and Jokar et al. (2021).

Because we used snowball and purposive sampling to identify the right respondents, we adapted selection criteria from Chan et al. (2001), wherein a qualified respondent had to satisfy at least one of the following criteria. • In-depth knowledge of the general practice of PPPs and had followed very closely the development of PPPs in Uganda. • Current/recent and direct involvement in risk management of PPPs in Uganda. • Sound knowledge and understanding of the concepts of PPP risks in Uganda. • Working experience (at least one project) and/or research experience in PPP project delivery in Uganda.

To ensure that the respondents met the defined criteria, we made initial contact with the suggested respondent to briefly assess their background information and experience before we sent them a questionnaire. We also contacted the PPP Unit and other agencies involved in PPP projects to identify possible respondents. We also requested the identified respondents to suggest colleagues who met the above criteria and were interested in participating in this study.

Risks and their Definitions.

We analysed data using Mean Score Ranking with the assistance of the Statistical Package for Social Sciences (SPSS) version 23. We computed mean scores for each risk regarding the probability of occurrence and impact. Frequencies were used for the background information of the respondents and the phase where risks were most likely to occur.

Results and Discussion

Response Rate

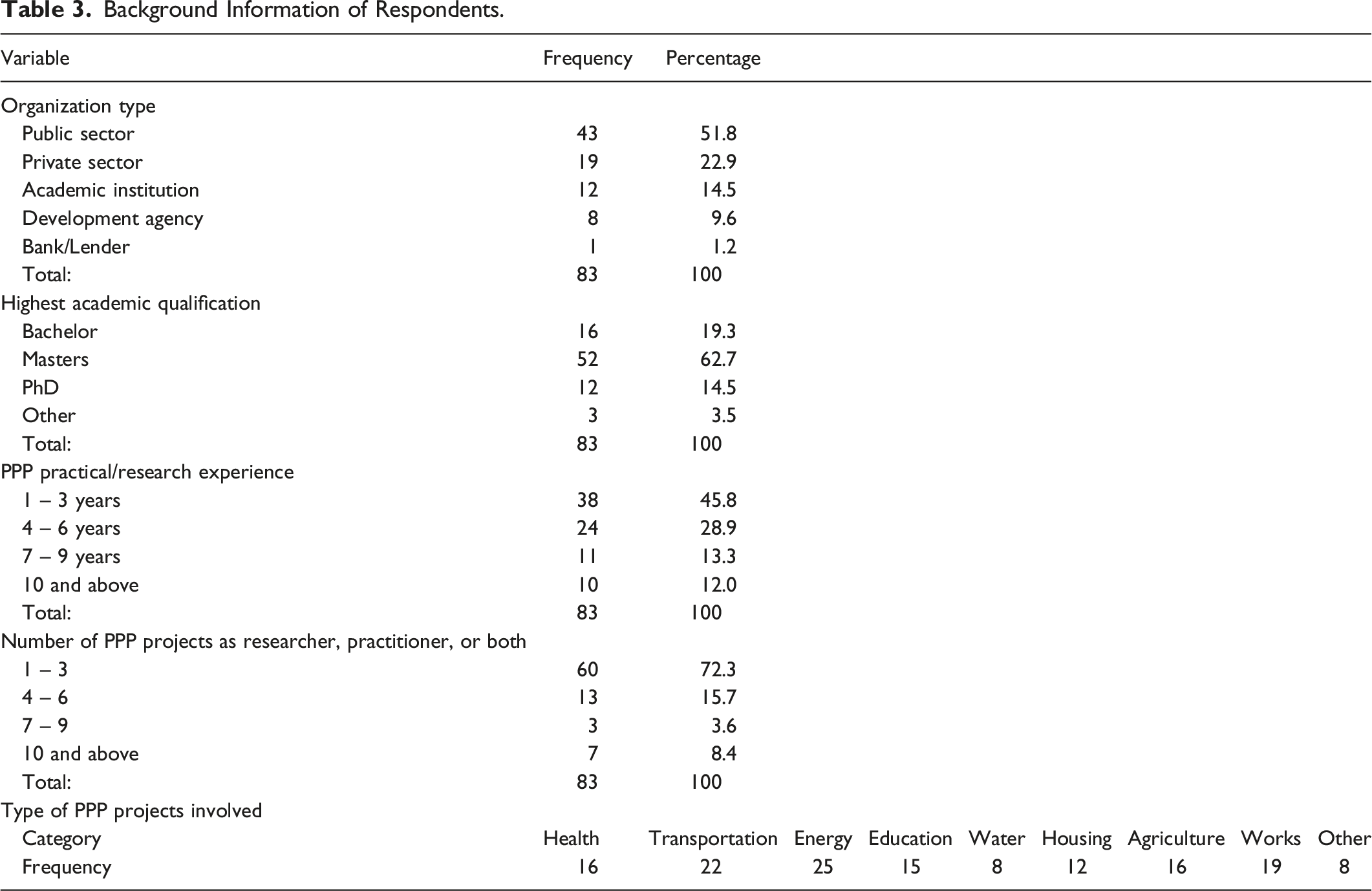

Of the 130 questionnaires issued, 94 responses were received, of which 83 were judged suitable for analysis (64% effective response rate). This was considered acceptable because it is well above the typical response rate in PPP research which averages around 30%. For example, Bing et al. (2005) received 61 responses (12% response rate), Frank-Jungbecker et al. (2009) received 53 responses (9% response rate), Chan et al. (2011) received 105 responses (18%), Shrestha et al. (2017) received 35 responses (30%) and Hwang et al. (2013) received 48 responses (40%). Because these were studies conducted in similar PPP projects, we considered them appropriate for comparison. Besides, considering the limited number of PPP experts in Uganda, 83 responses were considered acceptable for this analysis (Field, 2009; Roscoe, 1975; Stutely, 2014). Since an online questionnaire was used the 64% response rate is considered adequate as Sekaran and Bougie (2016, p. 143) state that “a 30% response rate is considered acceptable and in many cases even exceptional” in online surveys. Also, the sample size used in this study was comparatively larger than the ones used in previous studies.

Background Information of Respondents

Background Information of Respondents.

Overall Ranking of Risks Associated with PPP Projects in Uganda

The Overall Ranking of Risks Associated with PPP Projects in Uganda.

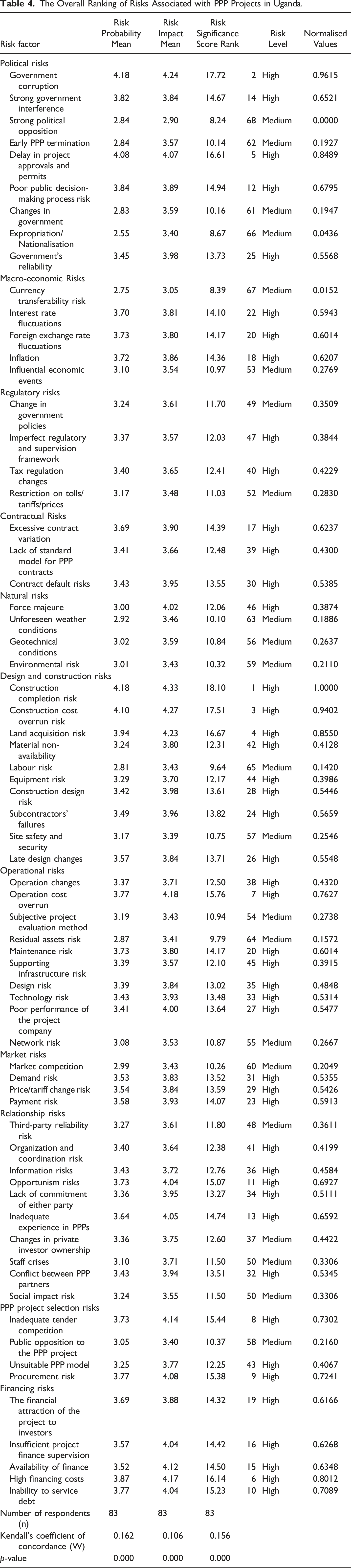

Kendall’s coefficient of concordance (W) was used to measure the degree of consensus among the respondents regarding the ranking of the 68 risks. The values of W for the rankings of risk probability, risk impact, and risk significance of the 68 risks were all statistically significant at a 5% significance level as shown in Table 4. This means that there is significant agreement among the PPP experts on the ratings of the risks associated with PPP projects in Uganda.

Principal Risks Associated with PPP Projects in Uganda

Because the purpose of this article was to evaluate the principal risks, we first determined the significance score of each risk using the following formula. Risk Significance = Risk Probability × Risk Impact. With this approach, risks with a higher significance score are considered more significant (more likely to affect the project) compared to those with lower significance scores and should be prioritised. This approach has been used by other scholars (see, Ameyaw & Chan, 2015a; Babatunde et al., 2018; Chan et al., 2011; Osei-Kyei & Chan, 2017; Shrestha et al., 2017; Xu et al., 2010). Because the study used a scale of 1 to 5 for both the probability and impact of the risk, it means that risk significance scores range from 1 to 25. Using the significance score of each risk, we categorised the 68 risks into three risk levels using the scale adopted from Ozorhona and Demirkesena (2015) that is: those with a significance score less than or equal to five were categorised as “low”, those between five and twelve as “medium” and those greater than twelve “high”.

As shown in Table 4, of the 68 risks, 46 (68%) fall into the high-risk category, while 22 (32%) are in the medium-risk category and no risk fell in the low-risk category. Most of the high-risk categories came from the design and construction, operational, relationship, political and financing risk groups. Therefore, based on these risk levels, we determined that PPP projects in the Ugandan context are perceived by the respondents as highly risky. This is in line with other studies that have considered PPP projects as being associated with many risks.

To determine the cut-off, point for the principal risks, we computed normalised values for all the risks by scaling between 0 and 1 for each risk using equation (1).

Only risks with normalised values ≥0.50 (Ameyaw & Chan, 2015b; Ameyaw, 2015; Fabi & Akinseinde, 2021; Rezaeenour et al., 2018; Wu et al., 2017; Xu et al., 2010) were deemed as principal risks and qualified for subsequent analysis. These studies have indicated ≥ 0.5 as a cut-off to consider a risk factor critical. This is because a value closer to 1 implies that the patterns of correlations are relatively compact and would yield distinct and reliable factors. Normalisation is important in ensuring compliance with factor analysis (Ameyaw, 2015; Xu et al., 2010). As shown in Table 4 under normalised values, 34 risks had normalisation values ≥0.50 and were considered the principal risks associated with PPP projects in Uganda. These risks are ranked from 1 to 34 and have been highlighted for easy visibility. Of these, five belong to political, three to macro-economic, two to contractual, six to design and construction, three to operational, three to market, five to relationship, two to PPP project selection, and five to financial risk groups. From these results, we observed that design and construction risks are the most common in Uganda, followed by political, financing and relationship risks. Similar findings have been reported by other scholars, for example, Ameyaw and Chan (2013, 2015a), Babatunde et al. (2018), Chan et al. (2011), Cheung and Chan (2012), Ke et al. (2011) and Osei-Kyei and Chan (2017). Therefore, the risks associated with PPP projects as reported in Uganda, do not differ so much from what has been reported in other developing countries. The only difference may lie in the ranking of these risks.

We now discuss the top 10 risks in-depth and highlight their possible causes in Uganda. This approach was taken because given the time and space constraints, it was not feasible to discuss all 34 principal risks in-depth. Additionally, from experience, investors and other practitioners normally give the first 10 risks priority (Nguyen, 2015). The idea of an in-depth discussion of the top 10 risks has also been used by Nguyen (2015). However, this is not to imply in any way that the remaining 24 risks are not as important as the ones discussed. Therefore, the top 10 risks are (in descending order), construction completion risk (18.10), corruption and bribery (17.72), construction cost overrun (17.51), land acquisition risk (16.67), delays in project approvals and permits (16.61), high financing costs (16.14), operation cost overrun (15.76), inadequate tender competition (15.44), procurement risk (15.38), and inability to service debt (15.23).

Construction Completion Risk

Construction completion risk was ranked the topmost risk associated with PPP projects in Uganda with a significance score of 18.10. Its probability and impact mean values were 4.18 and 4.33 respectively. One of the main causes of construction completion risk in Uganda is difficulty in securing PPP project land. For example, several PPP projects have been delayed owing to land compensation claims. Because of the magnitude of PPP projects, many people are displaced and must be compensated before construction starts. For example, the Bujagali HPP was delayed because of land compensation disputes (Nduhura, 2019; World Bank, 2007). The Kampala Entebbe Expressway project was also delayed because of the disagreement between the Uganda National Roads Authority (UNRA) and a property owner over the value of the property (World Bank, 2017b, p. 47). In addition, the road construction component of the KIS project was completed after 36 months instead of the planned 12 months partly owing to land acquisition challenges. These results agree with those of Osei-Kyei and Chan (2017), who cited compensation claims as key factors delaying the completion of PPP projects in developing countries. Kavishe (2018) maintains that construction completion delays are caused by land-related disputes.

The fact that Uganda is a landlocked country also contributes to delays in PPP project completion because of stalled delivery of construction materials, especially those being imported. The other causes of construction completion risk include a lack of coordination between contractors, delays in obtaining project approvals, a shortage of skilled labour and design variations (Budayan, 2019; Owolabi et al., 2020). Selecting a private party with inadequate capabilities is also a contributing factor (Shrestha et al., 2017). Therefore, if construction completion risks are not managed appropriately, PPP projects will likely experience cost escalations and a delayed maturity period, which affects loan repayments. Moreover, delays in PPP project construction may inhibit the provision of the intended public services, which would taint the image of the government and the PPP model.

Generally, these results agreed with studies carried out in other developing countries, which have highlighted construction completion delays as among the top risks associated with PPP projects (Ahmad et al., 2017; Ameyaw & Chan, 2015b, 2015c; Babatunde et al., 2018; Budayan, 2019; Hwang et al., 2013; Kavishe, 2018; Shrestha et al., 2017).

Government Corruption

Government corruption is the second most significant risk associated with PPPs in Uganda with probability and impact mean values of 4.18 and 4.24, respectively. Corruption manifests itself in the form of government officials asking for bribes from private investors to be awarded PPP contracts, bid shopping, side-stepping competition, and extortion (Ameyaw & Chan, 2015a). Key decision-makers may be bribed by the private partner to present the PPP model as the most desirable approach for a particular infrastructure project (Iossa & Martimort, 2013). PPP project characteristics, such as size, uniqueness, infrequency, many contractual links and complexity, make PPP projects more susceptible to corruption (Locatelli et al., 2017). Though a PPP project is structured to discourage corruption, it can still be manipulated (Arimoro, 2019). This view is shared with Fombad (2014) who indicated that despite the available PPP regulations, PPPs are susceptible to manipulation by companies and government officials, which is difficult for the public and anti-corruption agencies to spot. For example, public officials can select a project for the sake of illicit profit or to meet the interests of some politicians mainly those seeking re-election. Some may be bribed to present a project as PPP though it may not be suitable for that mode (Arimoro, 2019).

These results confirm the 2020 Corruption Perceptions Index, which ranks Uganda 142 out of 180 countries with a score of 27 out of 100, which is below the continent's average of 33 out of 100 (Transparency International, 2021). These results further confirm the allegations of corruption in some of the PPP projects implemented in Uganda. For example, at the initial stages of the Bujagali HPP, the U.S. power developer, Applied Energy Services (AES), pulled out of the project in 2003 owing to corruption allegations (Yescombe, 2017). Corruption tendencies have also been reported in the Universal Secondary Education project (Twinomuhwezi, 2018). This project involved the government partnering with private secondary schools to provide fee-free education at the secondary level. The government would provide grants to these schools in return for the provision of fee-free education. It was reported that there was a lack of accountability for the PPP grant by these schools which greatly frustrated the project (Twinomuhwezi, 2018). There are also allegations that private investors are compelled to bribe public officers to win contracts (Mugarura, 2019) and instances when PPP projects are proposed because of personal interests.

Uganda has been associated with poor legal and supervisory systems and political interference that create room for corruption (Mugarura, 2019; Twinomuhwezi, 2018). Corruption has also been identified by other studies as a key risk in PPP projects in developing countries, for example, Chan et al. (2011) and Cheung and Chan (2012) rank it as the second most significant PPP risk, while Xu et al. (2010) rank it third and other scholars rank it amongst the top ten (Ameyaw & Chan, 2015b; Babatunde et al., 2018; Ke et al., 2011; Osei-Kyei & Chan, 2017). Therefore, Uganda, like other developing countries, has been battling corruption in PPP projects.

Corruption in PPPs distorts competition, affects its operational efficiency, and increases the risk of contract abrogation. Because of corruption, an inefficient bidder can be awarded a contract resulting in additional costs for the public partner (Schomaker, 2020). Additionally, it affects the public’s perception and trust in the PPP arrangement, which may lead to public opposition to the project. Corruption also distorts government decision-making, increases market risks, and delays projects, thereby affecting private interests in such projects. Therefore, higher levels of corruption may increase the probability of PPP failure and may discourage genuine investors from participating in the Ugandan PPP market.

Construction Cost Overrun

The results indicated that construction cost overrun is the third most significant risk associated with PPPs in Uganda. Its probability and impact mean values were 4.10 and 4.27, respectively. Construction cost overrun is the result of an increase in the cost of construction materials and equipment and unexpected changes in design and site conditions. Construction costs may also increase owing to unpredictable inflationary trends and increased labour costs. Similarly, Chan et al. (2011) indicate that fluctuations in economic factors, such as interest rates and inflation, may generate cost overruns in a project.

Changes in design due to unexpected site conditions, which may require additional specialists and materials, also contribute to construction cost overruns (Ameyaw & Chan, 2015a). A delay in the completion of construction work is another contributing factor. In addition, at times, the costs associated with constructing a PPP facility are underestimated. For example, a survey of 58 rail PPP projects conducted by Flyvbjerg et al. (2005) found that costs were underestimated by an average of 45%.

The results are supported by evidence from projects implemented in Uganda that experienced cost overruns. For example, the World Bank (2018a, 2018b) and Yescombe (2017) revealed that the Bujagali HPP had over US$50 million in construction cost overruns, which Nduhura (2019) maintains resulted from a rock found below water, which was not detected during the design of the dam. Another example is the KIS project for which the government paid Ushs 40.85 billion in the form of road support payments instead of the estimated Ushs 40.16 billion (Office of the Auditor General, 2019c). These examples confirm that construction cost overrun is indeed a key risk associated with PPP projects in Uganda and is mainly due to their complexity, corruption, construction delays, inflation, and poor estimation of the construction costs.

Because PPP projects involve significant financial resources, any cost overrun would result in more expensive public services, which exacerbate public opposition and reduce profit margins for private investors. For example, there have been complaints about the cost of energy generated by the Bujagali HPP partly due to construction cost overruns. Construction cost overrun may result in allocative inefficiency of scarce resources, further delays, contractual disputes, claims and litigation, total project failure and abandonment (Gbahabo & Ajuwon, 2017).

Land Acquisition Risk

The results revealed that land acquisition is the fourth most significant risk associated with PPPs in Uganda. Its probability and impact mean scores were 3.94 and 4.23, respectively, with a significance score of 16.67. Land acquisition risk is common in PPP projects because they mostly require large areas of land, which often entails displacing people. These results agree with the World Bank (2017a, p. 143), which cited land acquisition as a key challenge in developing PPP projects because of the delayed compensation of project-affected people and the local land tenure system (Mugarura, 2019; Nduhura, 2019). In Uganda, the land tenure system allows the right to the ownership of land and demands negotiations with landowners, which end up being prolonged, cumbersome and associated with contested valuations (Mugarura, 2019; World Bank, 2017b). For example, the Bujagali HPP was delayed because of resettlement and compensation claims, as the project affected persons refused to vacate their land, even though they had already been compensated for it (Nsasira et al., 2013).

Another example is the project to redevelop the Nakawa-Naguru estate into a modern satellite city, which failed to start owing to land acquisition disputes. In this project, Opec Prime Properties, the private investor awarded the contract to redevelop the estate, could not make any progress because the government had allocated some of the land meant to be used for the development to other parties. This resulted in litigation and the private investor losing interest in the project (Mwesigwa et al., 2018). Similarly, the Kampala-Jinja Expressway has experienced delays related to land ownership and compensation of the project affected persons. For example, according to the Office of the Auditor General (2021, p. 20) by January 2022, 21% of the compensation amount had not yet been paid out, which was most likely to impede the timely handover of the project and commencement of works. Some of the reasons for the delays included a lack of proper ownership documents, ownership disputes, absenteeism, and rejection of compensation awards. This confirms Mugarura's (2019, p. 205) argument that there are always conflicts between landowners which delay the land acquisition process. Also, the Kampala-Entebbe Expressway project was delayed by a disagreement between UNRA and a property owner who demanded Ushs 48 billion, although UNRA valued it at Ushs 4 billion (World Bank, 2017b, p. 47).

Opportunistic behaviour has also been cited as contributing to land acquisition risks. For example, Mugarura (2019, p. 204) reveals that “crooked behaviour has cropped up where people rush to buy or develop land on corridors proposed for government projects, expecting higher pay from the government. Some landowners deliberately decide not to turn up for land valuation exercises and only emerge during road works to then demand exorbitant rates.” Others indicate that their land houses burial grounds and resist giving up the land (Nduhura, 2019).

The results of this study are supported by other studies that were carried out in India, Vietnam, Nigeria, China, Ghana and other developing countries that highlighted land acquisition as a key risk in PPP projects (Babatunde et al., 2017, 2018; Likhitruangsilp et al., 2017; Osei-Kyei and Chan, 2017; Le et al., 2019; Xu et al., 2010). Land acquisition risk is said to be very common in developing countries because of resettlement challenges, corruption, political interference, weak planning institutions, and extensive legal delays.

A delay in obtaining project land slows and hinders project progress, resulting in cancellations, blocking or even the nationalisation of PPP projects (Soomro & Zhang, 2016). Land acquisition risks may result in the delay of the entire project and cost overruns, which affect the financial viability and attractiveness of a PPP project.

Delay in Project Approvals and Permits

Delays in project approvals and permits is the fifth most significant risk associated with PPPs in Uganda. Its probability and impact mean values were 4.08 and 4.07, respectively. Delays could be explained by inefficient processes coupled with corruption that delays the PPP approval process in Uganda. Other reasons for delays are understaffing and an inexperienced PPP Unit, contracting authorities’ lack of experience, and inadequate coordination between the implementing agencies (Mugarura, 2019, p. 200). According to the World Bank (2018a, p. 9), the PPP Unit remains underfunded and understaffed, and the country lacks adequate capacity within line ministries and contracting agencies to develop and implement PPPs. Yet, the PPP Unit must review the projects earmarked as PPPs (feasibility reports) and consult with the contracting authorities.

The above reasons for delays in project approvals and permits are supported by various studies, such as that conducted by Zhang et al. (2019), who found delays were also due to the complicated permit process and governments’ lack of PPP experience. Moreover, Le et al. (2019, p. 11) state the following: “Incompetent and unprofessional government officials, complexities of approval procedures and frequent changes in laws and regulations were mainly responsible for the delays in project approvals and permits.”

Other than the PPP Unit, other government agencies may contribute to the delays in project approvals. For example, in Uganda, a PPP project must go through various agencies before it can be approved, such as the Contracting Authority, the PPP Unit, the PPP Committee and the Ministry of Finance (Republic of Uganda, 2015). This long procedure in PPP approvals has also been reported in other developing countries. For example, Zhang et al. (2019) mention China, where to get a PPP project approved, one must go through more than 30 agencies at the central, provincial and sometimes municipal levels. Likewise, Li and Song (2017) point out that the PPP project approval process involves numerous fragmented departments at both the national and local levels. Ng and Loosemore (2007) state that PPPs are associated with a lengthy and frustrating approval process because of their complexity. Similarly, Cheung and Chan (2011) maintain that most PPP project approvals experience delays due to political debates and public consultation.

The risk of delays in project approvals and permits has also been ranked highly in other countries. For example, it was ranked 2nd in Vietnam, 5th in India, 10th in Ghana and 14th in China (Likhitruangsilp et al., 2017; Nguyen, 2015; Osei-Kyei & Chan, 2017). A delay in PPP approval and permits has devastating effects on a project’s success, as it may increase total project costs, delay the start, and finish time of construction and subsequently affect the payback period. Eventually, these delays may frustrate private investors and lead to the cancellation of the project.

High Financing Costs

This is the sixth most significant risk associated with PPPs in Uganda. Its probability and impact mean values were 4.18 and 4.24, respectively. High financing costs are a key risk because of the high-interest rates associated with borrowing to finance PPP projects. PPP projects require a large investment that results in the private partner acquiring loans from banks, which implies that any change in interest rates increases the cost of financing. Uganda has been experiencing high-interest rates compared to its East African neighbours with an average of 21% since the 1990s (Mugume & Rubatsimbira, 2019). Additionally, interest rates were fluctuating between 17.1% and 20.9% between 2020 and 2021 (Bank of Uganda, 2021, 2022). The high-interest rates are mainly explained by the high operating costs faced by the banks, the small size of the banks, and the risks associated with the borrowers (Mugume & Rubatsimbira, 2019).

High financing costs were cited during the pre-construction phase of the Bujagali HPP, as there was a fear that the high financing costs could affect Bujagali Energy Limited's (private partner) ability to mobilise sufficient funds for the project (World Bank, 2007). For example, there was an increase of 19% in the Bujagali HPP financing fees (World Bank, 2018a, 2018b, p. 13). According to the World Bank (2018a, 2018b, p. 33), the interest rate during construction and financing fees amounted to US$111,695,000. The increase in financing fees was mainly because of the increase in interest rates. All these point to the high financing costs associated with the project.

Most of the PPP projects in Uganda are funded by loans from foreign banks, which are denominated in foreign currencies, which exposes the PPPs to foreign exchange risk that further increases the cost of financing. Project funders resort to foreign sources of funds because there is limited long-term financing and domestic private capital for investment in Uganda (Frisari & Micale, 2015; World Bank, 2017b). For example, the commercial banks and Uganda’s only development bank have not played an active role in providing long-term financing for Uganda’s development needs (World Bank, 2017b). Local commercial banks do not provide funds for PPP projects and even if they had the capacity, are typically not willing to offer long-term debt financing, although they might do so at high-interest rates and demand prohibitive collateral securities. Even the pension and insurance markets have not yet shown interest in PPPs in Uganda (Mugarura, 2019). The capital markets are also not yet sufficiently developed to offer long-term financing (World Bank, 2017b). The limited local long-term financing may be due to the uncertainties surrounding PPP implementation in Uganda, as the financing institutions may lack trust in PPP projects in general. Also, the limited experience of Uganda just like most African countries in PPPs increases the risk perception of commercial financial institutions which leads to an increase in the price of finance (AfDB, 2021).

The dearth of private investors and commercial lenders in Uganda makes it difficult and expensive to secure financing for any project. Because of this challenge, some projects could be abandoned, or investors might have to resort to expensive sources of funds, which would lead to high costs of services from these PPP projects. This discourages private investors from investing in PPP projects in Uganda.

Operational Cost Overrun

Operational cost overrun is the seventh most significant risk associated with PPPs in Uganda. It had a significance score of 15.76 with probability and impact mean values of 3.77 and 4.18, respectively. Operational cost overruns arise from low operation efficiency, force majeure, changes in technology, inadequate risk allocation and an increase in the cost of operational equipment and materials (Osei-Kyei & Chan, 2017). Many operational challenges, such as the unstable prices of materials, inflation, corruption, and foreign exchange fluctuations increase operational costs.

Similar challenges are mentioned by Ameyaw and Chan (2015a), who add that operational cost overruns in developing countries are mainly due to prevailing economic conditions, such as exchange rate fluctuations, inflation and increasing energy prices. Therefore, prevailing economic conditions in Uganda, such as foreign exchange fluctuations, inflationary tendencies and increasing fuel prices, are key contributing factors to high operational costs, which make the services from PPP projects costly and may affect the profit margins of the investors. In addition, high operational costs may affect the marketability of PPP projects, and this may explain why only a few private investors show interest in Ugandan PPP projects.

Inadequate Tender Competition

Inadequate tender competition was ranked as the eighth most significant risk associated with PPPs in Uganda. Its probability and impact mean values were 3.73 and 4.14, respectively. This risk is due to the complexity of PPPs, as it is costly to prepare bids, and few companies can submit tenders (Kyaligonza, 2021). Therefore, some PPP projects in Uganda have hardly attracted any bidders. For example, in the RVR concession, of the seven pre-qualified firms, only two managed to submit their bids (Yescombe, 2017). In the KIS project, the government received an unsolicited bid and could not subject the project to competition as the project was considered too risky (Office of the Auditor General, 2019c). This implied that there was no insufficient competition for this project and the government could not validate whether this private investor was the best for this project. According to international best practices, the government should have established a mechanism to increase competition such as allowing additional parties to submit competing proposals (the Swiss challenge) and allowing the initial party to match those proposals. In the case of the Uganda Police Force accommodation project, although five firms had expressed interest, only two submitted their proposals, and only one qualified to submit a technical and financial proposal. The Police Force decided to retender, but with no success (Kyaligonza, 2021). In the Gulu Logistics Hub PPP project, only one respondent, Unifreight Mitchell Cotts Consortium was pre-qualified for the next stage of the procurement process (Uganda Railways Corporation, 2022).

The low number of bids is also explained by the huge financial requirements needed to participate in PPP projects. For example, Nduhura (2019) posits that most Ugandan firms cannot commit the huge financial resources needed for PPP projects because the payback period may be more than 10 years. Additionally, Ugandan firms generally do not have the money to commit to PPP projects because of the weak capital market in Uganda. Because a large amount of capital is needed for a firm to bid for a PPP project, opportunities are left to a few firms that can raise the funds. This is in line with Hall’s (2015) report entitled Why PPPs don’t work, where he argues that entry barriers to the PPP markets are too high, resulting in an uncompetitive market. He adds the following: “The long, complex and costly procurement process limits the appetite for consortia to bid for projects and also means that only companies, who can afford to lose millions of pounds in failed bids, can be involved.” (Hall, 2015, p. 44).

There are also perceived risks associated with PPP projects in Uganda given its lack of PPP experience. This is in line with the African Development World Bank (2020) which states that African countries cannot identify, develop, structure, and bring bankable PPPs to the market. Also, some potential investors do not believe in what is being presented in the request for proposals as African countries have a weak pipeline of feasible projects (Infrastructure Consortium for Africa, 2018).

Inadequate tender competition limits appropriate opportunities for the government, as it brings about unfair negotiations resulting in ineffective risk allocation. In addition, the few capable bidders may also use their negotiating power to propose prohibitive demands. Non-competitive tendering may also result in protests by the public and facility users owing to high tolls/prices, poor service delivery, alleged corruption, and political favouritism.

Procurement Risk

The respondents ranked procurement risk with a significance score of 15.38 as the ninth most significant risk associated with PPPs in Uganda. Its probability and impact mean values were 3.77 and 4.08, respectively. This risk is associated with unethical practices in the procurement process, such as bribery, bid rigging, cronyism, breaches of confidentiality, and collusion. For example, specifications, bidding period or bidding documents may be modified in favour of particular bidders to exclude specific competitors (Arimoro, 2019; Iossa & Martimort, 2013). This is coupled with unrealistic and undervalued bids (Sanchez-Cazorla et al., 2016) due to opportunistic behaviour by the private parties. For example, Xiong et al. (2017) maintain that one of the most popular opportunistic behaviours is that the private partner wins the bid with a low price and then seeks renegotiations after the contract has been signed to gain a higher price. This risk emanates from immature procurement systems, which result in defective contract designs, legal disputes, and poor PPP project performance.

In the Ugandan context, procurement risk can be explained by Uganda’s inadequate experience in managing PPP projects, especially at the procurement stage, inadequate tender competition coupled with corruption as earlier mentioned. The PPP procurement process in Uganda is susceptible to corruption, a lack of transparency, and other unethical practices that could limit competition (Mugarura, 2019). For example, Kyaligonza (2021), in his study of the Uganda Police accommodation project, cited several challenges that would translate into procurement risks. Notable among these were the absence of standardized PPP procurement documents and procedures, the absence of established partner evaluation criteria, lengthy procurement processes, high costs of bidding, changes in design and specifications, and communication gaps.

These results are in line with those of Mugarura (2019), who found that procurement corruption such as bribery and bid rigging is due to bidders fighting to win tenders any way they can in Uganda. For example, in the Kampala-Jinja Expressway, there were allegations of firms trying to interfere with the procurement process (Parliament of Uganda, 2020, p. 28). Procurement corruption results in unfair competition in the procurement process. Additionally, there has been limited transparency in the procurement process of PPP projects, as the government alleges that the information is confidential. Limited transparency in the procurement process breeds biases, favouritism, and distorts effective competition in awarding contracts in PPP projects. For example, in Uganda, it is not uncommon to find that a decision to award a project to a given private company has been made before the bidding process. Moreover, at times, the credentials of the private company are not investigated in detail.

Procurement risk may lead to the selection of inexperienced bidders, who may end up underperforming, thus undermining the PPP model. Procurement risk may also discourage potential qualified investors from participating in PPP projects in Uganda. It may also increase the cost of the project, as the private investor must consider all the procurement-related costs in the total cost of the project.

Inability to Service Debt

The inability to service debt was ranked the tenth most significant risk associated with PPPs in Uganda. Its probability and impact mean values were 3.77 and 4.04, respectively. One of the key reasons why the private partner may fail to pay a debt could be related to the demand risk because it becomes difficult to finance a debt when the revenues are less than what was expected. This is especially true where the financial analysis during the feasibility study was not comprehensive as guided by the PPP guidelines (PPP Unit, 2019a). Furthermore, several PPP projects generate profits in the long term, which implies that in the short run, a private partner might struggle to meet its debt obligations, especially where its sources of project finance were not adequately assessed.

For example, in Uganda, some of the reasons that led to the termination of the RVR concession was the failure to pay its debts. RVR failed to pay the entry fees, staff salaries, concession fees, its fuel bills, and office rent. It had losses of the equivalent of US$131 million by 2016 (Yescombe, 2017, p. 108). By 2016, RVR had ceased to make principal repayments on its debt and was just paying interest (Yescombe, 2017, p. 111). This prompted lenders to withhold loans needed for more capital-intensive improvements (Ndonye et al., 2014). The failure to meet RVR’s debt obligations was due to the low revenue compared to what had been anticipated as it had reported losses of more than 10% of its revenue every single year since 2011 (World Bank, 2016).

Our results are in line with those of Sirtaine et al. (2005) who maintained that, on average, PPP projects became profitable only after about 10 years, and several projects do not have the potential to ever become profitable. An inability to service debt may also be due to an increase in operating costs, which leaves fewer funds available for servicing the debt. This risk may also be due to the high costs of financing. The inability to service debt may harm the relationship between lenders and borrowers, thus endangering the viability of the PPP project. It thus affects the reputation of private investors when it comes to future borrowings.

Principal Risks at Different Phases of the PPP Lifecycle

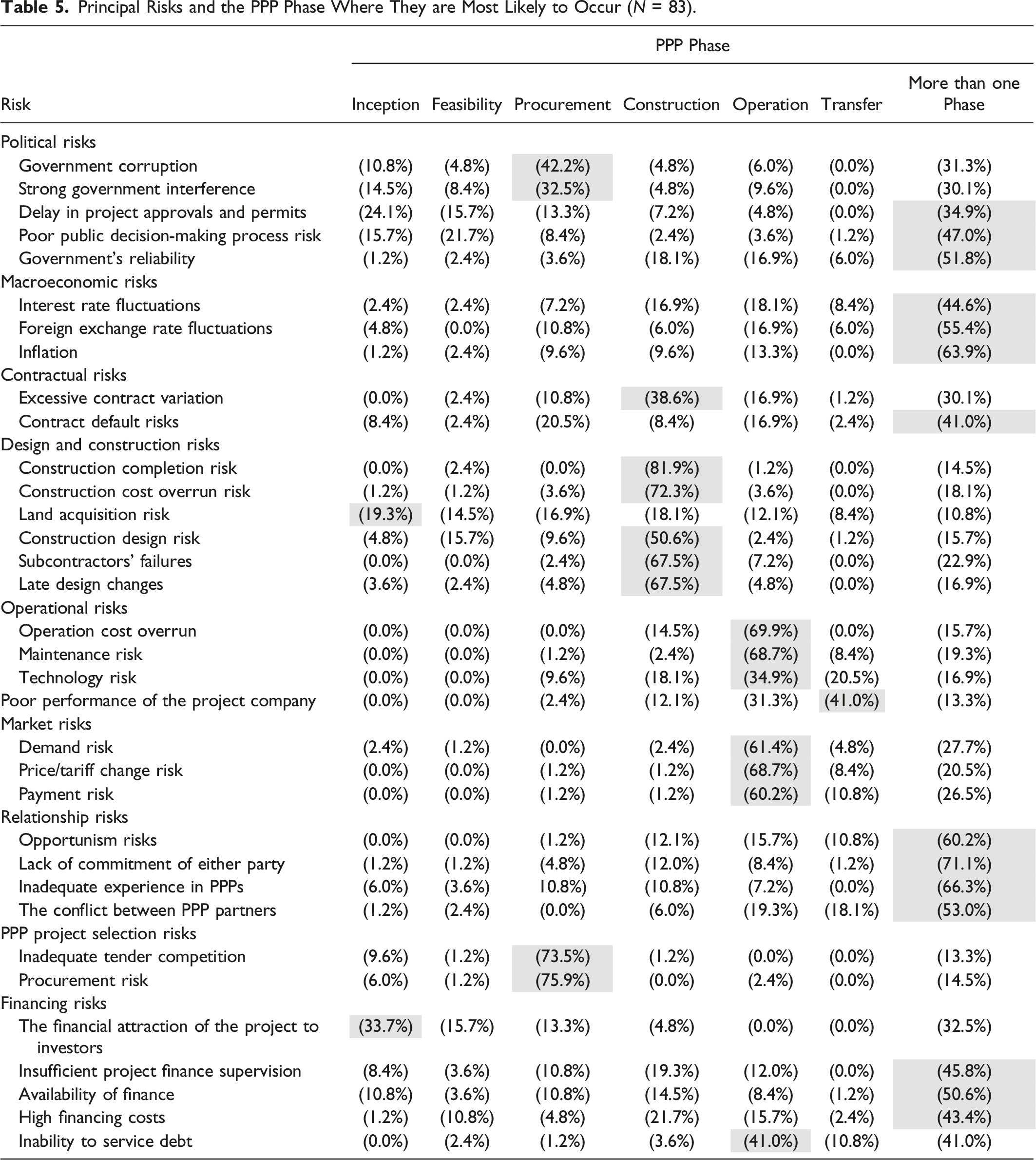

After identifying the principal risks, we sought to ascertain the phase of the PPP lifecycle where these risks are most likely to happen. We considered this important as it may guide PPP stakeholders in understanding the phase which is most vulnerable and must be given adequate attention. Besides, PPPs have a longer duration than projects procured under conventional procurement and the probability of risks occurring at the various phases may vary (Shrestha et al., 2017). Additionally, risks may change at the various phases of the PPP lifecycle demanding an appropriate response. We considered six phases of the PPP process, inception, feasibility, procurement, construction, operation, and transfer. Guided by the literature, we noted that not all the risks take place in one phase and some of the risks occur in more than one phase (Babatunde et al., 2018; Le et al., 2019). As such, we provided the respondents with the option of selecting more than one phase to accommodate such risks.

Principal Risks and the PPP Phase Where They are Most Likely to Occur (N = 83).

The two principal risks identified at the inception phase were land acquisition and the financial attraction of a project to investors. This is in line with Babatunde et al.'s (2017) study that identified land issues and the attraction of the project to investors as key risks in the initial phase of a PPP project. This could be because most contracting authorities are concerned about the bankability of the PPP project at this stage. If a project is considered not bankable from an investor perspective, it will not be able to attract enough investors and it will have to be procured using approaches other than a PPP unless there is a “viability” gap funding. In addition, the land needs to be secured before sourcing an investor. Therefore, land is considered a key issue at project inception because private investors will not be attracted to the project if they are not assured that the project land has been secured.

None of the risks was found to be most likely to occur at the feasibility stage because this stage mainly involves the contracting authority and the transaction advisor. At this stage, most of the activities are geared toward assessing the feasibility of the project. Besides, the private partner is not yet engaged. and there is still room to correct any issues that could arise. As such, the respondents did not find this phase to be risky. Also, it's at the feasibility stage that a decision will be made as to whether to implement the project using the PPP route.

Respondents indicated that the risks most likely to occur at the procurement phase as government corruption, inadequate tender competition, strong government interference, and procurement risks. Although corruption may take place in more than one PPP phase it is more common at the procurement phase mainly due to the limited experience of PPPs in developing countries (Appuhami & Perera, 2016; Cuadrado-Ballesteros & Peña-Miguel, 2021). Risks at this phase mainly arise from unethical practices and the costs associated with the PPP project procurement process. This phase is considered crucial because it is when the private partner is selected, and if a wrong partner (one without the capacity to implement the project) is selected, it will affect the other phases of the PPP project.

The principal risks identified at construction were construction completion, construction cost overrun, excessive contract variation, subcontractors’ failures, late design changes and construction design. These results agree with those of Babatunde et al.'s (2017) and Le et al.'s (2019) studies that found that the construction phase faces a considerable number of risks. Similarly, Perera et al. (2014) maintain that the construction phase is vulnerable to risks because it is more demanding for the private partner and is highly influenced by both natural and human factors. Shrestha et al. (2017) and Budayan (2019) also identify the construction phase as one of the riskiest stages of the PPP lifecycle. Zou and Zhang (2009) observe that although many risks might occur throughout the PPP lifecycle, the construction phase is risky, which indicates the need for the effective implementation of risk management strategies.

Even though risks were identified by the respondents in almost all phases of the PPP lifecycle, they considered the operation stage the most vulnerable, which is in line with the results of Shrestha et al.'s (2017) study. The operation phase is vulnerable to risk because it is the longest phase of the PPP lifecycle, thereby increasing its exposure to many risks. In addition, the operation phase affects the financial performance of the PPP project because the private party does not receive payment until the operation phase. Also, many stakeholders are involved at this stage, which further complicates it and creates more room for risks to occur. The principal risks identified at the operation phase were operation cost overrun, the inability to service debt, technology, maintenance, payment, price/tariff change and demand. These results agree with those of the studies conducted by Babatunde et al. (2018) and Gupta and Verma (2020), which revealed that project cost escalation, operation, maintenance, payment and market risks are the top risks in the operation phase of the PPP.

The poor performance of the project company was the only risk perceived to be most likely to occur at the transfer phase. Although no PPP project has reached the transfer stage in Uganda, the respondents believed that the performance of the operator greatly determines the state of the assets in this phase.

It should be noted that most of the principal risks were found to occur at more than one phase with the significant ones being delays in project approvals and permits, high financing costs, poor public decision-making, opportunism, contract default risk, and an inadequate experience of PPPs. These results concur with those of Le et al. (2019), who found that several risks may appear at any phase of the PPP lifecycle, especially those from the macro-environment that are difficult to control. Zou and Zhang (2009) claim that many risks associated with PPP projects can occur throughout the PPP lifecycle, such as funding, inadequate experience, and opportunism risks, which should be handled to ensure the success of PPP projects.

From these results, we note that each phase of the PPP lifecycle is associated with risks though some of these are most likely to occur at one phase than the other. These findings confirm that principal risks change across the PPP lifecycle, implying a need to assess and manage the risks at the different phases of the project. Risks may appear not to be significant at one stage, but if not mitigated, may affect subsequent phases of the PPP lifecycle. However, the operation and construction phases remain the riskiest phases.

Conclusion, Implications, and Limitations

Uganda’s need to achieve its “Vision 2040” and the required infrastructure to grow its economy has created an interest in developing infrastructure using the PPP model. This study revealed that the PPP model is prone to several risks which must be managed to achieve PPP project success. The study revealed 34 principal risks associated with PPP projects in Uganda with the majority falling into the design and construction category closely followed by risks in the political, financing, and relationship risks categories. All risks observed in this study can occur for any nature of the PPP project, not only in Uganda but also in other developing countries. These risks arise mainly from inadequate experience in PPP implementation, poor land tenure systems, weak regulatory systems, a weak domestic financial market, corruption, and opportunistic behaviours. The operation and design and construction phases are the most vulnerable to these risks. While examining the causes of these risks, we found out that some of these risks are interrelated. This implies that the existence of one risk leads to the occurrence of other risks. For example, corruption as a risk may lead to procurement risks, operational cost overruns, inadequate tender competition, and delay in project approvals and permits.

Knowledge of these risks could guide both the public and private sectors on aspects to consider in all stages of the PPP process, and in so doing contribute to PPP success in Uganda and other developing countries. Therefore, insights into these identified principal risks may encourage policymakers to design and adopt policies to guide PPP implementation. This article, therefore, provides policymakers with a comprehensive checklist that can aid them in developing PPP project risk management guidelines. The knowledge of these risks will also guide PPP contract negotiations, especially regarding how these risks should be allocated between the public and private sectors. This is because the principal risks herein were identified through a rigorous process utilizing PPP experts with experience and knowledge of a developing country. This article adds to the existing literature by introducing the Ugandan context regarding the risks associated with PPP projects. Although it focused on Uganda, the findings can be applied to other countries.

To those seeking to invest in PPP projects in countries such as Uganda, this study provides them with useful insights, enabling them to enhance their understanding of the more significant risks in this context. This article may guide their investment decisions, especially in determining which PPP projects to invest in and how much premium should be charged for the risks absorbed. Accordingly, appropriate precautions can be taken to avoid or mitigate the likelihood and impact of these risks.

We identify the principal risks, the phases where they are most likely to occur, their possible causes and how they affect the implementation of PPP projects. To ensure that no one is left behind, the government and the private sector partners must manage these risks to ensure successful public services and infrastructure delivery. Successfully managing these risks will enable the government and its partners to meet the infrastructure needs of their citizens.

We conclude that despite the numerous risks associated with the PPP model, it is still considered more advantageous because of the opportunity to transfer risk and access to the finances and expertise possessed by the private sector. PPPs play a vital role in addressing the public infrastructure funding gaps and reducing government monopoly over public service delivery because of the inefficiencies of many public agencies.

This study has limitations. Because the study was conducted in Uganda, this may serve as a limitation and could make generalization difficult due to the uniqueness of PPP country-wise. Also, the study was conducted without any specific reference to a particular PPP project and therefore the ranking of the risks was made regardless of the PPP project type. These can be addressed in future studies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the DAAD German Academic Exchange Service (91759052).