Abstract

This article examines the Canada Line rapid rail transit project in Vancouver, British Columbia, a decade after its completion and the 2010 Winter Olympic Games for which it was accelerated. The case resides at the intersection of two project classes with well-documented patterns of underperformance: transit mega-projects and sporting mega-events. Beyond connecting a number of Vancouver 2010 venues, the Canada Line is notable for its use of a public-private partnership procurement (PPP) model, as well as the significant real estate development seen nearby. In particular, the article focuses on outcomes classified under three headings: procurement model, community impact, and land use impact. Prior to providing avenues for future research, this article finds that while the PPP model avoided substantial cost overrun risks, the lucrative operational concession was where the growth coalition pushing the project was able to make it sufficiently attractive for private partners, while externalizing cost on third-parties.

Introduction

Although mega-events such as the Olympics are perhaps viewed popularly as sporting endeavors, in financial terms they may be better thought of as infrastructure programs that can shape regional development and impact fiscal health in the longer term. Indeed accompanying related infrastructure costs can frequently exceed the official cost of a mega-event several times over (see Agha et al., 2012; Baade & Matheson, 2016). Even within a larger suite of infrastructure mega-projects that the literature has documented as substantially underperforming projections on cost, completion, and operation, the Olympics may top the podium.

While urban growth coalitions and proponent governments may argue that the mega-event is merely speeding up infrastructure investments that would otherwise be made, the hard event deadline can alter and move ahead projects in ways that make sense for the event, but may not be ideal for long term regional needs. One frequent element of Olympics-related mega-infrastructure is rapid rail transit lines. Despite being clearly contemplated as part of the Olympics, rail infrastructure projects are viewed by the IOC as “indirect capital costs” and thus often left out of reported Games expenditures (Flyvbjerg et al., 2016).

This article evaluates one such rapid rail transit investment linked to the Vancouver 2010 Olympics, the Canada Line. While work on the Canada Line and other Olympics-related rapid rail projects typically concentrates on the time leading up to the Games period, this study has the benefit of a decade since both the Canada Line’s opening and the 2010 Olympics. The longer horizon provides a more complete frame for assessing the project under three primary headings: procurement model, community impact, and land use impact. After a review of mega-events and urban growth coalitions, rapid rail projects and the Olympics, as well as the literature on rail transit project evaluation, the article discusses outcomes under the three identified lines of inquiry before offering lessons for future similar projects.

Mega-Events, Infrastructure, and Urban Growth Coalitions

Regime theory argues that the complexities of local politics impact policy through brokering, coalition building, and resource sharing between public (elected and bureaucratic) and private centers of political and economic influence (Basolo, 2000). This extends to competition between different jurisdictions to pursue economic development agendas, manifesting in variations of the “growth machine” concept through which coalitions of elite local organizations implement self-beneficial urban policies while selling these policies as benevolent (Logan & Molotch, 1987).

In the mega-event context, growth coalitions can be driven by national politicians and elites aiming to demonstrate their brand on the world stage, while consolidating support for a domestic agenda. Sometimes the objective will be to showcase a lesser known city in a country, a modern side of an existing hub, increase a tourism profile, or more broadly make gains in “soft power” and influence (see Grix & Lee, 2013). Domestically, the mega-events can be a political impetus to speed up infrastructure investments that will have legacies beyond the event period (Muller, 2017), or as ploys by local and sub-federal governments to direct central government investment to particular regions.

A relatively vibrant literature exists on infrastructure investments and legacies in a mega-event context. Some focus on directly on infrastructure and cost overruns (Flyvbjerg et al., 2016; Matheson, 2012), while others discuss event impacts (e.g., Andranovich & Burbank, 2011; Fourie & Santana-Gallego, 2011; Maennig & Zimbalist, 2012; Preuss, 2015), economics (Baade & Matheson, 2016), or argue that mega-events using existing infrastructure can have significant dividends (Gratton et al., 2006).

The 2010 Vancouver Olympics were something of a mega-event bookend to Expo ’86. With both events, a growth coalition of center-right politicians, business leaders, and media pushed the events as agents of economic and infrastructure growth that would help sell Vancouver as a global city (see Ginnell, 2013; Sant & Mason, 2015; Surborg et al., 2008; Sussmann, 2006; Whitson, 2004). The Canada Line is an expansion of the SkyTrain system that originated for the 1986 World’s Fair (the original line is the “Expo Line”).

With Vancouver 2010, previous works have addressed Games-related infrastructure projects in a legacy context (Kaplanidou & Karadakis, 2010; Kidd, 2011; Sant & Mason, 2015) as well as the Canada Line subway as a private-public partnership (PPP) (Siemiatycki, 2006). Sant and Mason (2015) in particular discussed major capital projects as one of three frames (along with economic and human impact) used to sell the bid and the Games by politicians and Games proponents. However, little has been written on the Canada Line in the decade since its opening.

Rapid Rail Infrastructure and the Olympic Games

Olympics-related rapid rail infrastructure can come in the form of light rail, heavy rail, and conventional rail: the first being tram-like vehicles within a city but without a completely separated right of way, the second typically elevated or underground (often electrified “third rail”) trains within a city on their own right of way, and the last category representing train connections between cities with more limited stops. Light rail was seen in Games such as Calgary, and Salt Lake, while subways or metro projects were found in Munich, Montreal, Barcelona, Atlanta, Athens, Torino, Beijing, Vancouver, and Rio. Intercity or traditional rail projects accompanied the Olympics in Albertville, Nagano, Sydney, London, Sochi, and Pyeongchang.

Games-related intra-city rail connections are most frequently made to connect central cities to their airports, or to major sporting clusters. This need to make Games-related transportation more feasible does not necessarily correspond to the greatest rail transportation need in a region, or how transportation dollars would be invested in the absence of the Olympics. Thus the value in Olympics-related rail infrastructure is reliant upon prudent planning to ensure that largely temporary Games uses can dovetail with existing and longer term transport needs.

In Calgary and Torino, Games-related rail infrastructure has aligned with longer term transit priorities. In Rio, Munich, and Vancouver, rail construction has skipped other projects that were previously deemed to be a greater priority. Some hosts have seen the Games serve as a transformational agent for transit systems. For instance the substantial metro expansion associated with Tokyo 1964 (International Paralympic Committee, 2014) was eclipsed by Beijing, with four metro lines attributable to accelerated construction and planning schedules following its successful bid for the 2008 Olympics (Fallows, 2011).

Evaluating Rapid Rail Transit Projects

The literature highlights a range of means for evaluating prospective rapid transit projects. These include traditional cost-benefit analysis, cost-effectiveness analysis, multi-criteria analysis, regional economic impact studies, and environmental impact assessment (De Brucker et al., 2011). The two most relevant and common are likely cost-benefit analysis (CBA) and multi-criteria analysis (MCA). The former compares relative marginal costs and benefits and can focus on attributes such as value for money, ridership, and travel times in different potential alignments. Regarding land use impacts, some CBA studies have questioned transport policy merits (Hatzopoulou & Miller, 2009; Loo & Cheng, 2010) and noted that a CBA may not be appropriate for some projects (Beuthe et al., 2000; Ustaoglu et al., 2016).

In part a response to CBA limitations, MCA can be viewed as a wider aggregation of cost-benefit analyses concerning both different variables and stakeholders as pertaining to a broader range of quantitative and qualitative criteria (De Brucker et al., 2011). This method has been critiqued primarily on qualitative weighting and subjectivity, as well as data mixing (Ustaoglu et al., 2016). Despite framing pitfalls, De Brucker et al. (2011) argue that MCA can be beneficially used through a stakeholder-centered or institutionalist approach to examining transit projects.

A number of works have evaluated relationships between the urban built environment and public transit with established projects. Many studies can be seen as understanding these relationships through measures focused on some combination of density, diversity of land use, design (such as street network), as well as destination accessibility, distance to transit, and destination management (Cervero & Kockelman, 1997; Ewing & Cervero, 2010). In particular, the comprehensive meta-analysis of Ewing and Cervero (2010) found that transit use was most strongly related to proximity and street network design, with land use a secondary influence.

Some project specific case studies are also useful. Pan et al. (2014) found that in cities as divergent as Shanghai and Houston, rapid rail lines have significant positive impacts on nearby residential real estate prices. This is supported by works showing that rapid rail stations are likewise positive indicators of property values (Chen et al., 1998; Debrezion et al., 2007; Hess & Almeida, 2007). However Zhong and Li (2016) argue that there is a premium for multi-family property values relative to single-family, as well as for heavy rail over light rail. Kilpatrick et al. (2007) highlight that without direct access, proximity to a transit corridor can actually have negative effects on adjacent property values.

The literature on evaluating projects through cost-benefit has also highlighted the trend toward using PPPs in the pursuit of value for money as well as managing the risks of cost and time overruns (Flyvbjerg et al., 2003, 2009). Flyvbjerg (2007) found that some 90% of transit projects failed to meet ridership projections. Although PPPs may bring higher baseline costs than public finance, these are potentially made up for through the lifecycle and the transfer of underperformance risk to private partners (Siemiatycki & Friedman, 2012). Still, the effectiveness of the theory may depend on the parameters of a particular project (Hodge et al., 2018). Indeed, the impact of any transit line is linked to other parts of the network that may be outside of the private partner’s control and lead to tension between partners (Siemiatycki, 2011).

There is less written directly on community impacts of rapid rail transit. Instead these considerations are often addressed in MCAs. Of note though, is an analysis of 14 American metro areas by Baker and Lee (2019) that did not find that light rail stations lead to localized gentrification. Additionally, in an analysis of light rail in Hamilton, Ontario, Topalovic et al. (2012) argued that the project should be considered a “catalyst for social change; improving the health, environment, sustainability and connectivity of the community.” Even if community impact of rapid transit is not the central focus of many academic works, this is a frequent frame for government analyses (e.g. Lichfield, 2005; Topalovic et al., 2012).

Flyvbjerg’s work on mega-project underperformance is a particularly useful lens for this study. The overarching theory from several articles centers on over-optimism and strategic misrepresentation by key actors as explaining underperformance in terms of cost and completion overruns, as well as failure to meet operating projections (Flyvbjerg et al., 2009). The phenomena is highlighted as being especially strong in the rail transit and mega-event realms (Flyvbjerg, 2007; Flyvbjerg et al., 2016). However Flyvbjerg’s work is focused on more traditional measures of cost-benefit, such as financial cost, operating revenue and usage, as well as completion timeline, leaving something of a gap where considering performance variables such as land use and community impact.

Method and Materials

The primary research issue is evaluating the outcomes of the Canada Line 10 years after its opening and the 2010 Olympic Games. From here, the objective is to contribute to broader literature on performance of rapid rail projects built to accompany mega-events. Centered on a retrospective, single case study method, there are three primary lines of inquiry: procurement model, community impact, and land use impact.

Documents were collected from government, media, industry, legal, and academic sources using a snowball technique from a combination of search engine terms, government websites, and databases until over 30 search term combinations pertaining to the Canada Line and the three headings of inquiry (procurement model, community impact, and land use impact) were exhausted. The collected documents were then initially reviewed for their prospective relevance as (1) independent sources and (2) as holding reference to other potentially relevant sources. The sources harvested from the second step were then examined through the same two-step process, repeated until no new documents were found. The initial review included examining abstracts, introductions, conclusions, and bibliographies, as well as searching for key terms within the text. Subsequently, the full body of relevant documents remaining after the two-step initial review were analyzed and synthesized across source headings as appropriate.

Government documents included feasibility and impact reports, annual and quarterly financial reports, contracts, regional council proceedings, property assessments, bylaws, planning, and development materials, as well as other documents from the Ministry of Transportation and relevant local governments. Where appropriate, documents were requested through the British Columbia Freedom of Information and Personal Privacy Act. The media review included articles from local, regional, and national newspapers, magazines, business reporters, and television stations. Secondary interviews or quotes from key actors were especially of interest. Legal sources centered on statute, case law, and law firm materials. Industry documents included real estate and construction trade publications. Unless otherwise specified, Canadian dollars are used.

Canada Line Overview

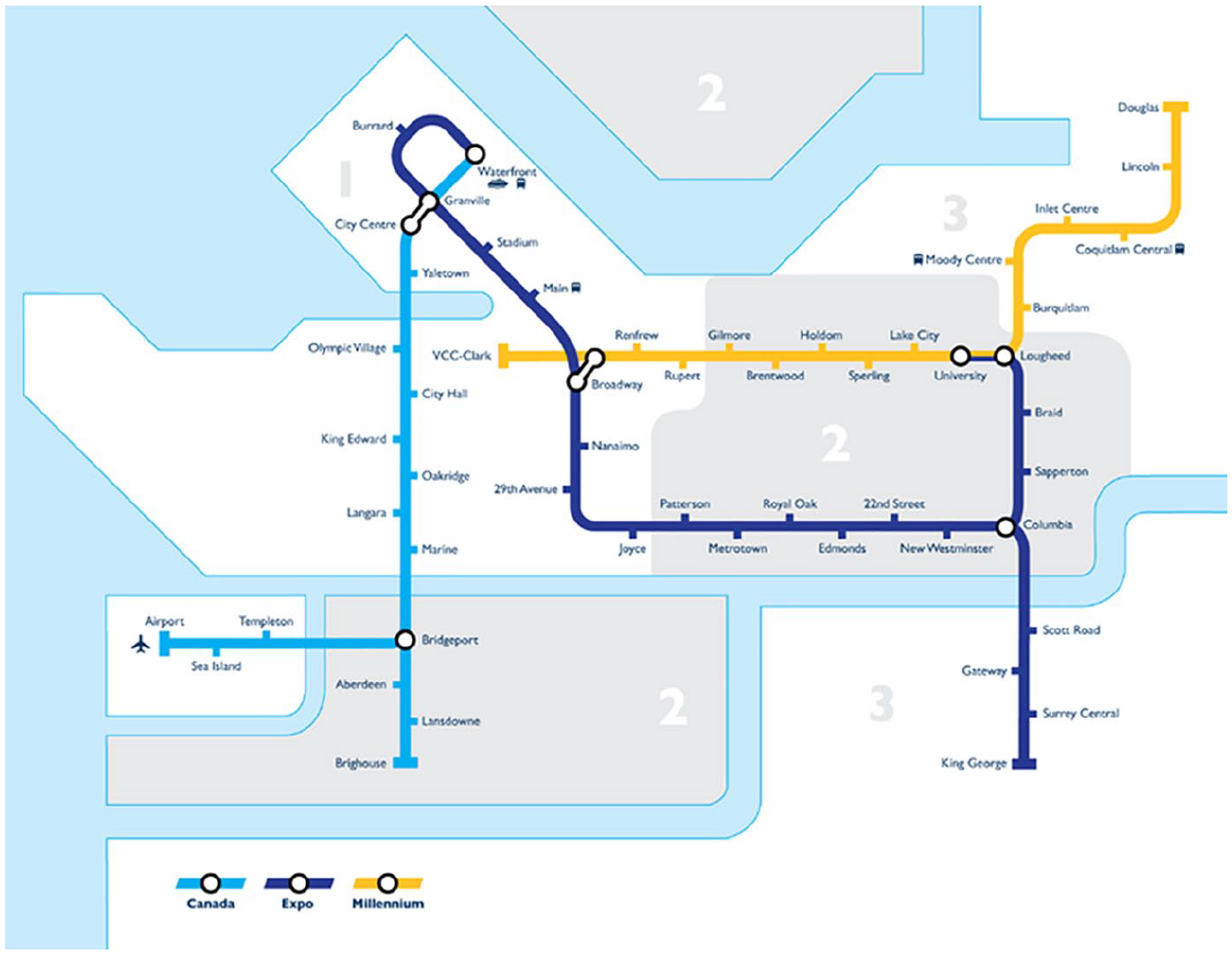

The Canada Line is a 19 km, 16 station heavy rapid rail line connecting downtown Vancouver to the suburb of Richmond, with a 4 km spur to the airport. Prompted by the provincial government’s desire to connect the airport and downtown prior to the Olympics as well as over $400 million of federal funding contingent on that objective, the then RAV (Richmond-Airport-Vancouver) line jumped the regional transit priority queue over a SkyTrain expansion to the northeast. Indeed the line ended up being a crucial Games transport spine linking three competition venues, the primary stadium for ceremonies, athletes’ village, and international broadcast center, with the province insisting on an “Olympic Village” station. However, there were serious questions as to whether this was the appropriate regional transit priority in the medium and longer term.

The initially $1.6 billion RAV line was intended as a PPP to be jointly funded by the federal and provincial governments, the regional transit authority (TransLink), and the Vancouver Airport Authority, with costs above $1.4 billion covered by a private partner. The private component came through the then provincial government’s interest in the PPP model for infrastructure mega-projects and the need to create a majority on the TransLink board. The board, with votes from several regional mayors, twice voted against the RAV line, but the third attempt was successful based upon the premise of capped public costs that would not further deplete funding for the northeastern Millennium Line expansion (Chan, 2014) (Figure 1).

Canada Line and the SkyTrain system.

Four consortiums bid on the Canada Line, with the winner led by Quebec construction/engineering firm SNC Lavalin. SNC was chosen over Bombardier, the manufacturer of Vancouver’s then two existing SkyTrain rapid transit lines. This saw the Canada Line use a different rail technology and lose the benefits of interoperability and a shared maintenance facility. Unlike with the original Expo Line, the federal government did not make its funding contingent on using Bombardier technology (Figure 2).

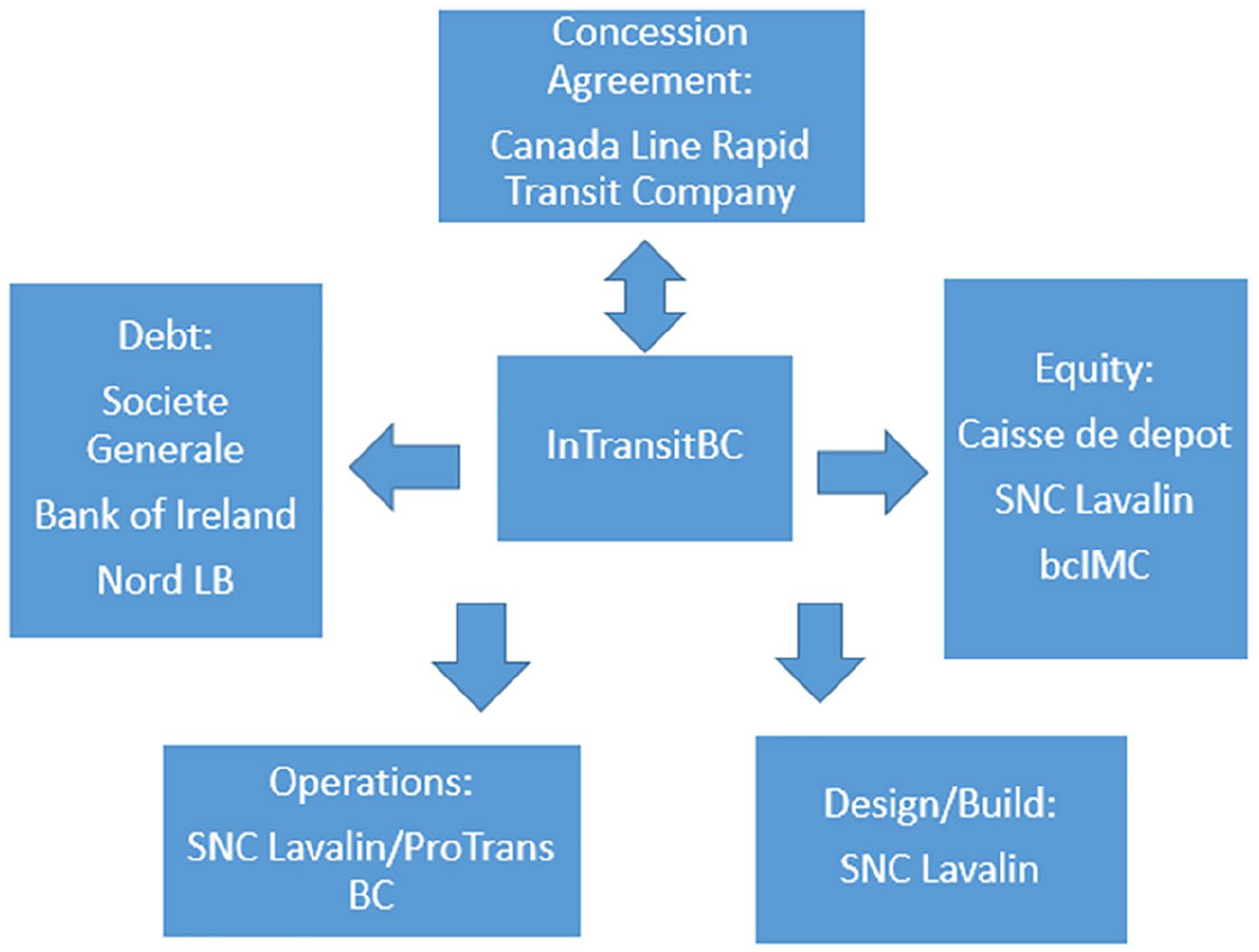

Canada Line deal structure.

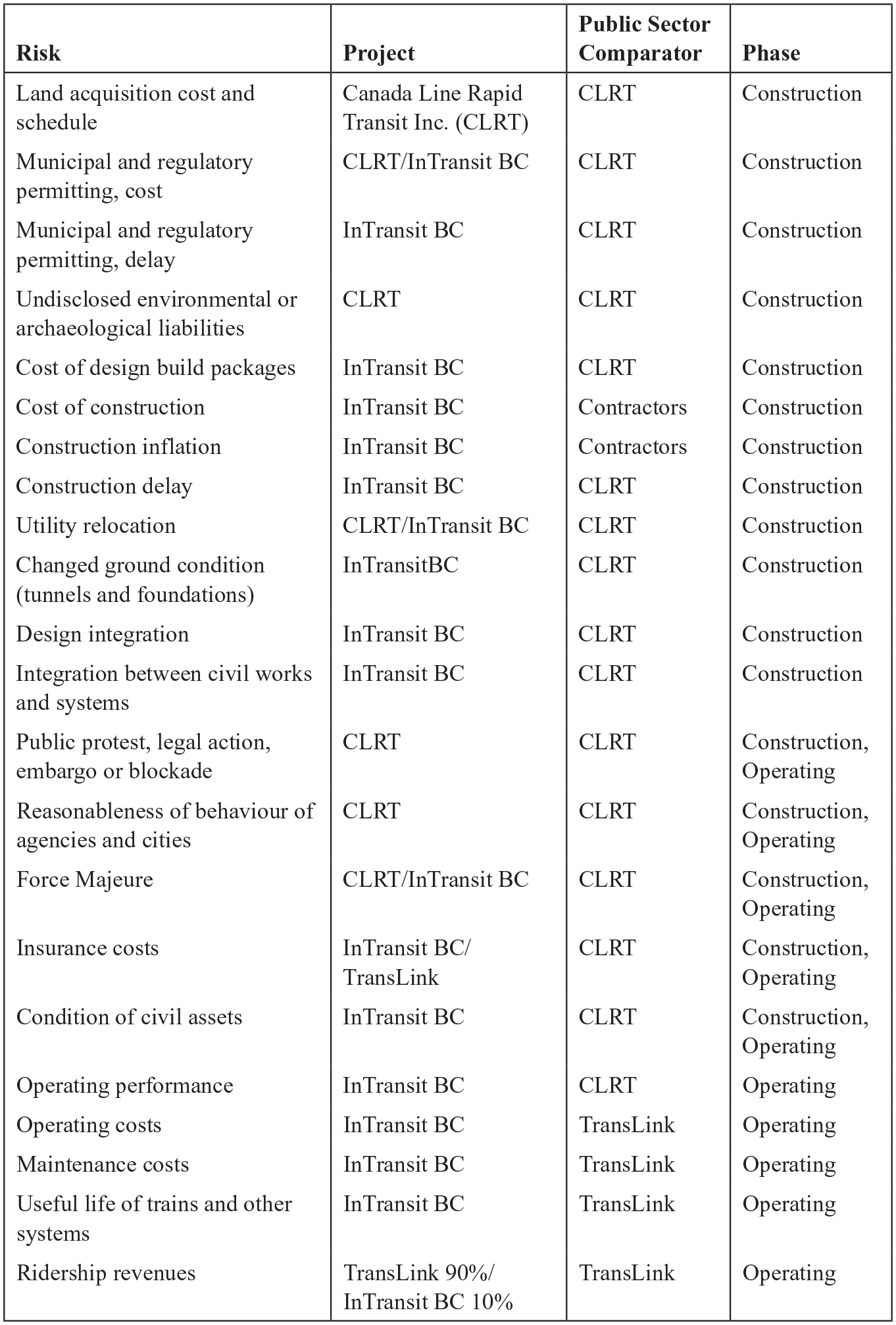

The concession agreement attempted to allocate risks to the partners best equipped to manage a particular risk (Canada Line Rapid Transit Inc., 2006). The design-build-finance-operate-maintain PPP saw a 35 year concession provided to the consortium-owned InTransit BC. The consortium exclusively took on the risks of construction costs, inflation, delay, municipal permitting, tunneling, civil works integration, systems performance, maintenance, and operating cost, and performance (2006). A wholly owned subsidiary of SNC Lavalin, ProTrans BC, receives the operational subcontract from InTransit. The publicly owned Canada Line Rapid Transit Corporation (a joint venture between the province and TransLink) retained risks for right of way and land acquisition, contaminated soils, archaeological discoveries, and public protests. Permitting costs, utility relocation, and force majeure were risks shared between InTransit and the public corporation, while insurance costs and ridership revenue risks were shared between InTransit and TransLink. With ridership revenues, TransLink retained 90% of the performance risk, reflecting that in an integrated transit system, TransLink was better situated to modify fares, bus routes and service to direct and maximize Canada Line ridership. Yearly concession payments to InTransit are based 70% on service availability (trains per hour), 20% on service quality, and 10% on volume (Figure 3).

Canada Line risk allocation.

PPP Outcomes

The PPP model delivered significant protection from cost overrun. InTransit paid $720 million of the $2.05 billion in capital costs, framed as “capital at-risk” against future underperformance. This is substantially offset by the significant yearly payments InTransit is entitled to from TransLink under the concession for operation and maintenance, as well as performance metrics and inflation. InTransit’s $720 million at risk is intended to be repaid over concession’s life through meeting performance targets. The payments ranged on a generally upward trend between $90 million and $107 million between 2010 and 2014, and were projected to run between $120 million and $132 million in the 2020 to 2024 period (TransLink, 2014, 2020). A $90 million yearly payment starting in 2010 adjusted for 3% inflation over 30 years equates to a future value of $4.28 billion, or a 2010 present value of $1.76 billion. Even if the true operational and maintenance costs for InTransit are estimated at up to 50%, the concessionaire is still recovering a significant profit on their capital.

Compared to maintenance and operational costs for the three publicly run SkyTrain lines using Bombardier technology, the concession payment is over twice as expensive on a per track kilometer or per boarding basis (Chan, 2017b), and three times as expensive on an operating cost per capacity kilometer basis (Translink, 2018a). Much of this can be accounted for by the return on capital provided to the private partner (Canada Line Rapid Transit Inc., 2006). Beyond capital return, there are likely scale economies with the 60 km of Bombardier technology SkyTrain, consistent with findings in the rail transit literature (see Savage, 1997). Indeed the failed Bombardier bid for the Canada Line was partially premised on efficiencies gained from a common maintenance facility and rolling stock, but these advantages were not allowed to be used in the award criteria (Chan, 2016).

The procurement included extensive outside expert analyses comparing the two options. While the traditional procurement model had a lower gross cost, once a risk premium was added, the 50th percentile outcome saw the PPP model return a savings of C$92 million in 2003 dollars at a 6% discount rate (Canada Line Rapid Transit Inc., 2006). The PPP model significantly narrowed the band between projected 5th and 95th percentile construction costs and ridership risks relative to the public sector alternative.

Risk shifting has been accompanied by the Canada Line consistently receiving higher customer survey ratings on safety, cleanliness, and service frequency measures (TransLink, 2017, 2018a). Likewise, the Canada Line opened 2 months ahead of schedule in September 2009. The line was estimated to need in the range of 100,000 daily riders to break even and there was skepticism that it would meet its targets. However the line almost met its 2013 projections within its first year of operation in 2010, and has since seen over 145,000 daily riders (TransLink, 2018b).

Instead of falling short of ridership projects like the previous SkyTrain expansion, the Canada Line is already seen as underbuilt and lacking capacity to deal with future demand. Again this is reflective of the financially driven incentives of the design-build specifications—the Canada Line was built with platforms half the length of the other SkyTrain lines in the region to cut capital costs. For the life of the concession, the realistic option will be to increase the number of trains, although this is seen as only sufficient for the next 15 years of growth (Chan, 2017b). If the public had retained operations, the government may have seen the cost of lengthened platforms as a worthy long term investment years before the asset is returned to full public control.

Community Impact

The Canada Line saw major community impact issues, which may both be somewhat associated with the scope of geography touched by the project, as well as the private sector incentives the PPP model brought. Most notably, although the original public discussion focused on bored tunneling along Cambie Street in Vancouver, outside of downtown, the tunnelling became almost exclusively cut and cover. Whereas with a bored tunnel, a tunneling machine will descend from a small footprint and excavate without disturbing the surface outside of its initial footprint, cut and cover closes a block of roadway at a time: a trench is created, tunnel laid, and the trench is covered back up.

This highly disruptive method became most controversial along a 12 block commercial strip known as the Cambie Village. Here the cut and cover excavation destroyed the walkable character of the shopping district, causing some businesses to close and many others to sustain significant losses. The provincial finance minister at the time, who happened to represent the local constituency, testified in a later lawsuit that “the construction was far more disruptive than anyone had anticipated, not only because it was done with a cut and cover method as opposed to the promised bored tunnel but also because pledges to only disrupt individual businesses for a maximum of 3 months were never kept” (Wintonyk, 2012). In reality some businesses experienced 18 months of cut and cover.

While the district has fully recovered its vibrancy and appeal in the decade since the Canada Line’s opening, the benefits have been experienced by landowners and new businesses replacing those who could not survive the years of construction in the area. The impact from shifting tunneling methods has been the subject of several lawsuits, including an initially successful class action that was sent back for a new trials by the BC Court of Appeal (Britten, 2020). Interestingly, TransLink’s management wanted to settle with Cambie merchants for $5 million, but the board overrode this decision and has forced years of litigation still ongoing. Even if TransLink is ultimately successful in court, the hard dealings with small business owners who have suffered significant loss as a result of the project has not improved TransLink’s image. Vancouver’s mayor between 2008 and 2018 categorized the handling of construction as “an injustice” (Wintonyk, 2012).

Another community impact as a consequence of geography is the further densification and development of the Richmond suburb. The city core served by the Canada Line is set to triple in population from 40,000 in 2014 to 120,000 by 2031. While transit-oriented urbanism is typically desirable, Richmond is a silt island sitting 1 m above sea level, protected from flooding by a series of dikes. As Vancouver is a high-risk earthquake zone, the island may partially liquefy in the event of an earthquake, or may be threatened more gradually by climate change. For these reasons the policy wisdom of encouraging population growth in this area has been questioned (Chan, 2014). In response, Richmond has built and refined an extensive flood management plan which includes flood construction levels and strategic land raising, alongside investments in dikes and pump stations (City of Richmond, 2019).

Finally, controversy surrounded the working conditions of 40 Latin American laborers brought in by SNC for downtown tunnel boring under the federal Temporary Foreign Workers Program. The BC Human Rights Tribunal ruled that these workers were illegally discriminated against in wages, housing, and benefits relative to their European coworkers. The initial tribunal award of $2.5 million was replaced by an undisclosed settlement to preclude further litigation (CBC News, 2014). Had the construction phase been more closely managed by the public sector, this situation may have been less likely or the use of temporary foreign workers avoided altogether.

Land Use Impact

The economic impact of a rapid transit line can be in significant part seen through unlocking land value through easing access for people and firms. With the Canada Line, there has been significant positive impact on nearby real estate values. South of the Cambie Village retail corridor, the boulevard and adjacent neighborhoods were dominated by single-family homes, with a 1970s era shopping mall and a scattering of towers at 41st Avenue.

The Canada Line has driven real estate appreciation in two phases. First, during construction, an academic study estimated that single-family homes within 500 m of certain stations saw 50% greater appreciation from before the construction phase to 2012 (Harlos, 2018). Even more significant movement was seen after the city up-zoned the corridor to encourage density. Since this rezoning in 2011, almost the entirety of single-family home stock has been sold and assembled for multi-family residential construction. The first phase of assembly saw 10 single-family homes sell for $3.4 million each in 2011. Speculation has continued since, with a former gas station going for $15 million in 2015 (O’Brien, 2015), and single-family home lots of 10,000 square feet selling in the $12 million range as of 2017 and 2018 (Lee-Young, 2017; Wright & DeCotiis, 2018).

While Vancouver may need to densify in order to provide affordability within reasonable commutes to job clusters, the land speculation frenzy has necessitated luxury construction for developers to profit. Out of the 6,600 hundred new units approved in the Cambie Corridor as of 2015, 630 were rentals, while 480 were social housing (City of Vancouver, 2015). A further $256 million in community amenity contributions were made from developers to the city (2015). However social housing and amenity requirements further pushed up price points, seeing much of the remaining supply sold to Chinese investors (Lee-Young, 2015) at price points beyond the mortgage stress test threshold for even upper middle class incomes in the city. The land frenzy has prompted the city to tell developers that it will not allow similar luxury dominated outcomes as it contemplates the east-west Broadway SkyTrain extension (Fumano, 2019).

In terms of incremental assessed value generated by the Canada Line, it is difficult to both collect assessment records specific to the Cambie Corridor and Richmond city center, and isolate Canada Line driven growth from the significant real estate appreciation seen in the region in the years following the Canada Line’s opening. For illustration, the City of Vancouver alone saw roughly $300 billion in incremental assessed value created between the Canada Line’s 2009 opening and 2018. Roughly 1/8th of the city’s geography can be considered within a kilometer of the line. Although land values are obviously not constant throughout the city, the corridor accounting for 1/8th of assessments is conservative. If this roughly $40 billion in incremental value is 20% allocated to the Canada Line and 80% to other market factors, then $8 billion of Canada Line specific increment has been created in a decade. In terms of Vancouver tax mills (City of Vancouver, 2019), this $8 billion would equate to C$99 million in additional revenues per year. This is in addition to the community amenity contributions that may have been otherwise able to be directed toward Canada Line construction as they clearly did not impede development feasibility.

Although the booming property market likely means that much of the Canada Line proximate activity would have likely occurred elsewhere in the city absent the line, meaning that the Canada Line specific revenue gain is probably much smaller than C$99 million per year, it does raise a value capture proposition. Namely that instead of grants from governments or finance from a private partner, a substantial share of the cost could have been covered through value capture or tax increment revenue bonds, with government grants serving as a backstop against underperformance. While BC does not have a tax increment financing (TIF) statute and there are significant limits on local government debt issues, the Vancouver Charter makes Vancouver the only local jurisdiction in the province that can issue its own bonds. In theory, these bonds could by bylaw be backed by incremental revenues of a transit value capture zone, but would require elector approval (Vancouver Charter, 1953, s. 242).

The City of Richmond however has used a form of value capture to fund a new station at Capstan Way. Instead of relying upon incremental property taxes, Richmond has collected $8,500 per unit in a development area around the station. With construction on 16 towers and over 2,000 residential units exceeding timelines foreseen when the station agreement was closed in 2012, the new station reached full funding in 2018, 9 years ahead of schedule, triggering a 30 month window for construction (Chan, 2017a). More generally, the experience of up-zoning and appreciation with the Canada Line, combined with significant regional penetration of transit-oriented development and housing demand, demonstrate major potential for closing funding gaps for future rapid rail lines through value capture.

Discussion

Beyond the lost chance to leverage value capture finance, alternatives can be evaluated in two primary ways with the Canada Line project: the use of a private partner versus a traditional procurement model, and the allocation of funding priority for a northeastern line instead of the north-south line to the airport.

With the former, once a final contract price was reached after major cost increases, the project was managed by the private sector without further price escalations for government. The downside however is the operational costs to return the private investment being far more expensive than publicly operated lines that were traditionally procured. Had the private partner been able to keep to the bid budget, it would have profited significantly. From the government’s perspective, a primary factor in limiting cost reflected at the bid stage was the shift in tunneling method. Effectively this somewhat reduced the private partner’s overrun risk and allowed the public to lock in a cheaper bid, while externalizing the cost on Cambie Street retailers who would not necessarily benefit from increased property values associated with the finished product.

As for the issue of project investment, Canada Line ridership has exceeded expectations to the extent that early qualms have been silenced. Although the land speculation induced by the Canada Line has resulted in housing weighted toward luxury product for those who do not earn their income locally, this is a planning problem at the city level. The Canada Line project itself allowed for significant densification in much closer proximity to job clusters than the northeastern line, which was more premised on shifting centers of employment to less valuable geography. With the northeastern Evergreen Line having entered operation in 2016, the early results have seen both inferior ridership (34,000 per day on a line roughly half as long; TransLink, 2018b) and lacking demand for office space components in transit-oriented developments.

Whereas many transit projects succumb to over-budget and late delivery with ridership failing to meet projections, the Canada Line only experienced one of these issues. Even when the project went over-budget, the private partner was responsible for almost $700 million in cost overruns. The PPP model with protections against cost-overruns was a necessity for the provincial government and Games boosters to surmount opposition from the regional council wanting to fund previously agreed rapid transit priorities that had no Games utility. However, while skeptics on the regional council were won over due to legitimate concerns on initial capital overruns, they may not have fully considered the long term cost of the inflated yearly payments under the concession agreement relative to the cost of publicly run maintenance and operations already demonstrated on existing SkyTrain lines.

Further, the upside of the lucrative operational concession was obtained on the premise that capital cost risk could be shifted through to the private partner. To attract bids within the approved regional funding amount, private partners were allowed to use a cheaper tunneling method outside of downtown, which effectively externalized the cost to retail leaseholders on the construction route. Additionally, the private partner was able to access a cheap foreign labour pool that would likely not be politically possible in a traditional public procurement.

The Canada Line was also a strong beneficiary of political will and financial capital made available by the Olympics. While in other host cities such political will to optimize a place for a 2 week Games period has had wasteful, or sub-optimal results, the Canada Line has in some ways proven its critics wrong, albeit with missed opportunities. Although the Canada Line has spurred transformational transit-oriented development and accompanying assessment gains for the cities in which it resides, the local government planning failure to ensure the densification adequately addressed the regional housing affordability crisis is a shortcoming to be learned from. Likewise, the line missed a window to leverage incremental property values to pay for the project that in part made the gains possible. However the incremental property value generated along with community amenity contributions from development, have instead created revenue windfall for the cities of Vancouver and Richmond.

Conclusion

Rapid rail transit projects are a frequent accompaniment to mega sporting events such as the Olympic Games. This class of projects is susceptible to the well-documented underperformance associated with both rapid rail transit and mega-events. The Canada Line is one such project that provides an opportunity to add to each literature with more than 10 years of outcomes since the line’s opening and the Vancouver 2010 Olympics. This article finds that while the PPP protected against capital cost overruns that are commonplace in mega-event mega-projects, there was significant additional cost to the public entrenched in the operational phase of the concession relative to the public option. Additionally, much of the initial cost certainty was obtained through changing to a more disruptive tunneling method that externalized a large part of the cost to commercial tenants along the line. Further, the significant gains in land value along the Canada Line corridor were a missed opportunity to leverage value capture and better tie the revenue benefit to the project cost. Still, despite shortcomings and lost opportunities, the Canada Line showed that sometimes the most desirable rapid transit project for Games use is also the best for medium and long term regional needs absent mega-event considerations.

Out of this paper, there are three particularly compelling avenues for future research. Most directly stemming from the Canada Line, the use of value capture from private ancillary real estate development to build future stations on existing lines is a concept that may be applicable to many cities. Similarly, the Canada Line highlights attributes that indicate potential for rezoning and densification to unlock land value which can finance a significant portion of the underlying rapid transit project. Can instances from other cities refine a model for the development of entire lines primarily or substantially from value capture? If so, what does the finance structure look like? Likewise, for mega-events that frequently include major real estate developments for athletes’ villages connected by new rapid transit lines, is there potential for the infrastructure to be in significant part self-financing? With governments and mega-events similarly concerned with fiscal and financial sustainability, future work on these threads may be of great value.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.