Abstract

In their efforts to combat climate change, some firms choose to develop environmental innovations. Given that environmental innovation strategies fall into the politically sensitive area of climate change protection, we theorize that CEO political ideological divergence can substantially impact the chosen strategy. Drawing on threat response theory, we find that CEO ideological divergence from a Republican president negatively affects environmental innovation intensity, while ideological divergence from a Democratic president positively affects it. Moreover, increased communication of sustainability orientation weakens this studied impact. We utilized a longitudinal data set of S&P 500 CEOs (2010–2018) with 916 firm-year observations and 188 unique firms, to present theoretical and managerial implications for environmental innovation, CEO political ideology, and threat response theory.

Keywords

Introduction

Growing industrialization and rising pollution levels have made climate change a major global concern. Following a deeper understanding of their ecological footprint (Takalo et al., 2021), firms have shifted focus from constantly seeking to increase profit margins to contributing to environmental improvements (Hizarci-Payne et al., 2021; Tsai & Liao, 2017). One major strategy is environmental innovation (Marchi et al., 2022; Takalo et al., 2021; Ullah et al., 2022). Firms can, through “new or modified processes, techniques, practices, systems, and products, avoid or reduce environmental damage” (Kunapatarawong & Martínez-Ros, 2016, p. 1219). Environmental innovation has become a priority for a broad range of stakeholders and shareholders (Garvare & Johansson, 2010; Meixell & Luoma, 2015; Yu & Zhao, 2015), who have some influence on their companies’ leadership regarding these issues (Raghupathi et al., 2020; Yang et al., 2018). A recent research call by Takalo et al. (2021) addressed these influences by acknowledging the need for more research on senior management antecedents of environmental innovation.

Responding to this call, our study is taking a promising new route by looking at the threat of government action a CEO might perceive as an influence factor of environmental innovation. In the growing ideological divide between the Republican and the Democratic party in the United States, environmental issues are one of the key differences—with Democrats pushing for climate protection, while Republicans tend to prefer investments in other areas (Fitz, 2023; Fowler, 2022; Kelso, 2017). Following this, CEOs might see a need to react to changes in the government by adjusting their firms’ environmental innovation strategies. We measure the perceived threat of government action felt by a CEO by looking at how much the political ideology of a given CEO diverges from the national political climate (Semadeni et al., 2022). While there are many potential influences on the governmental political environment, for example, the legislature and the judiciary, the role of the president is best suited to represent the national climate, as the president is selected by a federal election, and is the most visible government official (Mayer, 1999; Semadeni et al., 2022). We are examining CEOs as they tend to have strong influence on firm decisions (Hambrick, 2007b). Indeed, it has been found that CEO characteristics as wide ranging as tenure, general CEO power, cognitive style, passion and narcissism, all impact firm innovation outcomes (Cai et al., 2021; Cucculelli, 2018; de Visser & Faems, 2015; Pucheta-Martínez & Gallego-Álvarez, 2024; Wang et al., 2023).

Our study extends the literature on threat response theory (Staw et al., 1981) which posits that individuals and organizations have specific, mostly externally directed reactions in response to perceived threats (Connelly & Shi, 2022). However, specific managerial reactions in times of perceived threat remain unclear. Connelly and Shi (2022) call for researchers to “consider how the relationships under investigation [. . .] can help create generalized knowledge about the evolving and imminent threats that organizations face” (p. 1378). Applying this theoretical perspective of threat response theory, we hypothesize that CEOs experience stress and anxiety if the national political climate opposes their ideological beliefs. This stress response can affect the environmental innovativeness of their firms (Jackson & Dutton, 1988).

In the United States, political polarization has reached a new height, and executives are no exception to partisanship (Fos et al., 2022). This makes the country the ideal study ground to understand how divergence from the national political climate influences CEOs and firm behavior. Indeed, previous studies have shown that divergence from the national political climate has high relevance to CEOs’ decision-making (Arikan et al., 2023; Semadeni et al., 2022). In this vein, Nalick et al. (2023) found that CEO political ideological divergence reduces lobby expenditure. Similarly, Semadeni et al. (2022) claimed that the more that CEOs diverge from the prevailing governmental political climate, the more organizations retain their earnings and the less they invest in R&D. CEO political liberalism is positively associated with firms’ corporate social responsibility advancement (Chin et al., 2013) and previous studies have shown the impact of the regulatory policies, driven by the political party in power, on firms’ environmental innovation (e.g., Fabrizi et al., 2018). Our study will investigate the interplay of these two influence factors on environmental innovation. Specifically, understanding the effects of how CEOs’ political ideology diverges from the external political climate is crucial for understanding what propels or hinders the environmental innovativeness of large firms. That is, we hypothesize that liberal-leaning CEOs, when they diverge from the national political climate, will pursue less environmental innovation. Conversely, we hypothesize that conservative-leaning CEOs, when they diverge from the national political climate, will pursue more environmental innovation. The hypothesized relationships underline the need to look at political ideological divergence rather than political ideology or national political climate in an isolated way. The assumed impact directions oppose what we would normally expect from liberal- and conservative-leaning CEOs. At the same time, there is no change in behavior in times of no divergence.

To better understand how CEO political divergence affects firms’ environmental innovations, we examine how the relationship alters as a response to two moderating effects: firms’ communicated sustainability orientation and CEO duality. These two moderators were chosen as they directly moderate the threat perception of the CEO. The first essentially serves as an opposing threat, while the latter strengthens the reaction to a perceived threat due to increased CEO power. First, we chose a firm’s communicated sustainability orientation to account for a second threat to the CEO. A strongly communicated sustainability orientation, which has been publicized through letters to the shareholders, allows the CEO less leeway to move when the national political climate diverges from the CEO’s personal political convictions. This lack of leeway might be perceived as a second threat by the CEO, which overrules the perceived threat of divergence from the national political climate (Connelly & Shi, 2022) and consequently weakens the relationship of CEO ideological divergence to environmental innovation. Second, we chose CEO duality as a CEO-level moderator to moderate for the differing levels of power of a CEO. Specifically, we argue that ideological divergence is only a perceived threat, and the strength of the reaction of the firm will depend on the relative power of its CEO (Brewer, 1999; Semadeni et al., 2022). In choosing CEO duality as a proxy for CEO power, we follow multiple previous studies that have proven such an impact (Adams et al., 2005; Lee & Ko, 2022). We hypothesize (1) a negative (positive) impact of high CEO political divergence from a Republican (Democratic) president on environmental innovation; that this relationship is (2) weakened by firms’ communicated sustainability orientation; and (3) strengthened by CEO duality. To test these, we run a generalized estimating equation (GEE) model of CEO political ideological divergence on environmental innovation, adding firms’ communicated sustainability orientation and CEO duality as moderators. The estimation confirmed our Hypotheses 1 and 2. We also implemented robustness checks and discussed the theoretical and practical implications of our results.

Our research extends environmental innovation literature by introducing CEO political ideological divergence as a novel antecedent. This reveals a double-edged impact of government action, as political ideological divergence from a Republican president might have a negative impact on environmental innovation. Our study also contributes to CEO political ideology literature (e.g., Chin et al., 2013; Nalick et al., 2023; Semadeni et al., 2022) by examining the influence of CEO political ideology on environmental innovation within the national political climate. Thus, we offer a nuanced understanding beyond isolated political ideology studies and traditional firm outcomes. Finally, we contribute to threat response literature (e.g., Staw et al., 1981) by highlighting the divergence of CEO political ideology from the national political climate as a perceived threat in the CEO’s mind, causing a risk-averse threat response. This finding not only extends previous domain research, but brings threat response theory to bear on the globally relevant issue of the political divisions in the United States (Fos et al., 2022).

Theoretical Analysis and Hypothesis Development

Theoretical Background

In recent years, political polarization in American society has steadily increased (Fos et al., 2022). Top managers have started to engage in political discussions and are increasingly using their power to advocate their political views publicly. Researchers on CEO activism have observed that CEOs have become increasingly assertive about their opinions and beliefs (i.e., their political orientation; Larcker et al., 2018). Society can observe how executives, and CEOs in particular, deal with a government they support or do not. Following Hambrick (2007b), CEOs tend to have strong influence on firm decisions. Therefore, we conclude that one must study CEO decision-making based on personal political beliefs and the external environment. Researchers posit that political ideology is a “system of causal explanations and expectations, with implications changing depending on the environment” (Semadeni et al., 2022, p. 516). We follow Semadeni et al. (2022), interpreting the environment as the governmental political environment. Hence, the question arises about whether or not CEOs change their decision-making behaviors when their ideology converges or diverges from the prevailing political climate (Semadeni et al., 2022). Consequently, Semadeni et al. (2022) address this notion in a recent study and extend the liberalism-conservatism index (Chin et al., 2013) to the national political climate. The authors find that if the CEO’s political ideology diverges from the national political climate, they increase retained earnings and reduce R&D spending. This relationship is strengthened by CEO-vested stock options and attenuated by industry regulation. Following this research, Nalick et al. (2023) use organizational fit theories to prove that CEO political ideological divergence decreases lobbying investment activities. In our study, we continue to advance this emerging research area by introducing CEO political ideological divergence as a novel antecedent to environmental innovation as an environmental outcome for a firm.

Following Semadeni et al. (2022), the most appropriate theory to discuss the specific reaction of CEOs in times of political divergence is threat response theory (Staw et al., 1981). This is because threat response theory explains how individuals and firms behave in the presence of external threats, such as a diverging political environment. In their work, Staw et al. (1981) examine how adversity affects the adaptability of organizations and individuals. They claim that threats lead to restrictions on information handling and constrictions in an increasingly centralized control. The threat rigidity hypothesis states that, because of these changes, a “system’s behavior is predicted to become less varied or flexible” (Staw et al., 1981, p. 502). A threat usually causes individuals to experience psychological stress and anxiety. In our study, CEOs feel stressed and anxious about a national political climate that opposes their ideological beliefs. This leads to CEOs perceiving unfamiliar stimuli in terms of previously held “internal hypotheses,” that is, their own political ideology. Accordingly, CEOs perceive threats motivated by divergence rather than their own personal political ideology when faced with an opposing national political climate. Following Semadeni et al. (2022), our research pertains to “perceived” threats. Hence, the CEOs perceive a threat because they believe divergence will generate uncomfortable conditions. According to threat response theory, when an individual perceives a threat, their focus narrows, and they become more resistant to change or new information (March, 1991; Staw et al. 1981). Researchers see this inflexibility as a coping mechanism that helps the individual deal with the perceived threat by focusing their attention and resources on addressing it. Threat rigidity can have negative consequences, such as impeding decision-making and problem-solving, both at the individual and organizational levels. It can also lead to conflicts with others and decreased team performance.

Hypothesis Development

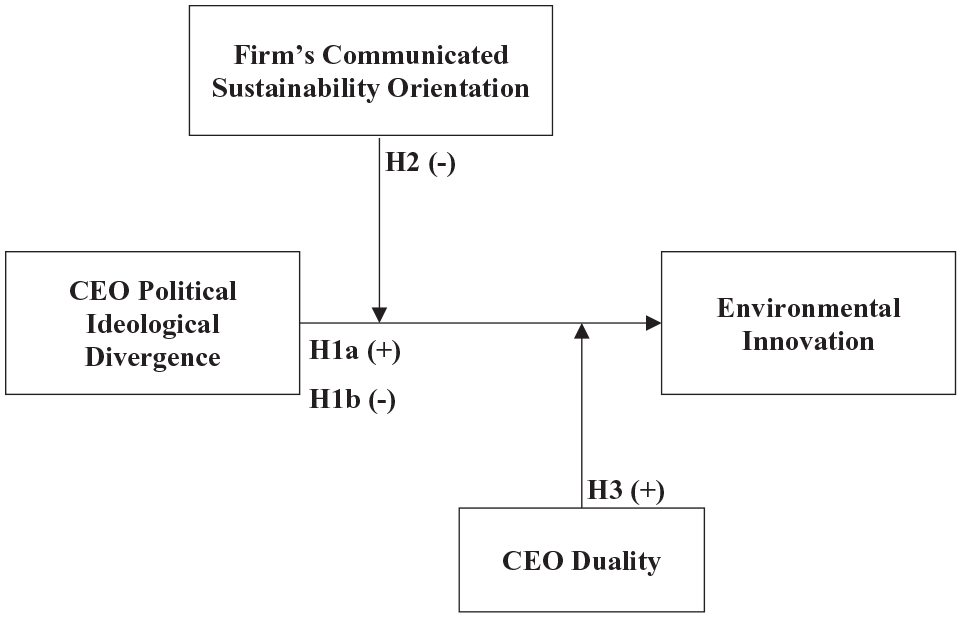

We hypothesize that CEO political ideological divergence from a Republican (Democratic) president is negatively (positively) associated with environmental innovation and that firms’ communicated sustainability orientation attenuates this relationship, whereas CEO duality strengthens it. Figure 1 summarizes our research model.

Illustration of the Research Model.

CEO Political Ideological Divergence and Environmental Innovation

We propose that CEO political ideological divergence leads American CEOs to react to the political ideology of the president in power, such that their environmental policymaking converges with the assumed views of the president. First, following threat response theory, the divergence of the CEO’s political ideology from the national political climate creates a perceived threat in the CEO’s mind (Brewer, 1999; Semadeni et al., 2022). This leads to a threat response that causes the CEO to adjust their decision-making regarding environmental innovation to the assumed views of the president. The perceived threat stems from the fear of outgroup hate (Brewer, 1999), according to which individuals often have negative attitudes and feelings toward members of groups that are perceived as different or outside of their own group (ingroup). In this case, it is toward the president and political party in power. This negativity may be based on a variety of factors, including past experiences, cultural and societal norms, and individual personality traits. Hence, a CEO with a diverging political ideology from the national political climate may view those who hold the dominant political beliefs as part of an outgroup and may fear negative consequences from this outgroup (Tajfel, 1974). The CEOs might be worried about being disadvantaged by this outgroup and may avoid potential negative consequences or conflict by adjusting their decision-making regarding environmental innovation toward the assumed views of the outgroup. Consequently, this perceived threat forces a close-minded threat response (Staw et al., 1981; Thórisdóttir & Jost, 2011). In other words, this response can be defined as an environmental innovation policy that no longer aligns with the CEOs’ strategic (and ideological) beliefs, but converges toward the beliefs of the outgroup, that is, the president in power.

Second, as the environmental policy making of Republican and Democratic presidents differs significantly, the threat response will differ based on the party of the president in power. While Democratic presidents generally place high importance on environmental protection, using a range of policy and decision instruments to encourage more climate protection (Fitz, 2023; Kelso, 2017), Republican presidents generally favor conserving existing programs rather than investing in new policies to address emerging environmental problems (Fowler, 2022). The response to these threats is notably different from other findings in the field, because we are not looking at an isolated threat response with significant short-term effects on firm finances, such as a decrease in R&D spending or an increase in retained earnings (Semadeni et al., 2022). Instead, an immediate change in environmental innovation policy will not strongly affect firm finances (Berrone et al., 2013). However, it will signal convergence with the political party of the president in power. The importance of this signal is reinforced by the fact that environmental protection can be seen as the site of a major ideological difference between Democratic and Republican presidents (Freemuth & Smith, 2007). CEOs who are trying to adjust their behavior in response to perceived threats from a president with opposing views will likely focus on such signals as they are of strong ideological importance. Other adjustments such as changes in the general innovation investments will have less signaling power.

Following the aforementioned, the responses of CEOs differ based on their personal political beliefs and the current party in power. Liberal CEOs generally tend to be intrinsically motivated to care about the environment (Gupta et al., 2021; L. Xu et al., 2022). Thus, their response to a Republican president can be described as a close-minded threat response that involves deprioritizing environmental innovation investments to avoid being seen as part of an outgroup by Republican policymakers (Tajfel, 1974). In contrast, a conservative CEO under a Democratic president might increase investment in environmental innovation. Specifically, the conservative CEO’s closed-minded threat response would involve prioritizing environmental innovation to signal the Democratic president that the firm is taking progressive steps toward climate change prevention, and thus avoid negative consequences from the outgroup of Democratic policymakers (Tajfel, 1974). Finally, we argue that CEOs who do not perceive any threat from the outside environment, having no political divergence from the governing president, will not change their behavior. This is an important differentiation in our argumentation as we are specifically focusing on perceived threats that are only experienced by CEOs with diverging political views. In contrast to realized threats, such perceived threats will only lead to a change in behavior for a subgroup of CEOs, who are diverging in their views from the political climate (Jackson & Dutton, 1988). Thus, our hypotheses capture the threat response of conservative CEOs to Democratic presidents, as well as that of liberal CEOs to Republican presidents:

The Moderating Role of Communicated Sustainability Orientation

We argue that firms with lower (higher) communicated sustainability orientation weaken the positive (negative) effect of CEO political ideological divergence from a Democratic (Republican) president on environmental innovation. We consider communicated sustainability orientation through the organization’s social and environmental value orientation (Moss et al., 2018). We chose a firm’s communicated sustainability orientation to account for the perceived threat of a CEO’s divergence from the firm’s communicated strategic agenda (Connelly & Shi, 2022). A communicated low or high sustainability orientation allows the CEO less leeway to move when the national political climate diverges from the CEO’s personal political convictions because strong divergence from the sustainability intention might lead to adverse market reactions (Kiattikulwattana, 2019). CEOs who put their firm’s communicated sustainability orientation in writing feel obligated to keep their word. If they change their sustainability strategies in response to changing political climate, they will lose integrity among shareholders (Hong et al., 2019).

Second, firms with higher communicated sustainability orientation are more likely to engage in costly environmental innovation initiatives that take years to redeem their value (Bansal & DesJardine, 2014). Reducing those initiatives, however, as a response to a political shift does not make sense because the involved cost and effort will eventually bear fruit. Similarly, firms with lower communicated sustainability orientation might decide not to significantly increase their investment, as the impact is likely to be felt only in the long term. On the contrary, if the short-term investment differs from the story told to shareholders, it might lead to adverse market reactions in times of anti-ESG (environmental, social, and governance) funds’ growing influence (Crews, 2023). To sum up, we hypothesize the following:

The Moderating Role of CEO Duality

Scholars have found that CEOs with role duality have a stronger influence on their organizations’ strategies than CEOs without such duality (Adams et al., 2005; Lee & Ko, 2022). We propose that CEO duality has an impact on the effect of CEO political ideological divergence on the firms’ environmental innovation, for the following three reasons. First, we argue that CEO duality affects decision-making dynamics as well as the CEO’s confidence when championing their decisions (See et al., 2011). That is, if CEOs perceive a threat coming from their divergence from the national political climate, the fact that they enjoy increased power from their role duality will help them make faster decisions about their threat responses. CEOs with role duality will essentially consult their peers less as they are more confident in their decision-making processes. This is particularly important given that we are arguing that ideological divergence is only a perceived threat that might not be felt in a similar way by their colleagues. The strength of the response of a firm to such perceived threats will fundamentally depend on the relative power a CEO has (Brewer, 1999; Semadeni et al., 2022).

Second, CEOs with role duality have better access to firm resources than less powerful CEOs, which increases their decision-making power and exposes them to fewer corporate control mechanisms (Berger et al., 1997). If CEOs have control over the company’s resources, they may be able to increase or reduce resource allocation toward environmental innovation when they feel threatened by the national political climate.

Third, CEOs with role duality may be able to use their influence to secure resources and support from other stakeholders, such as investors, customers, and suppliers, to tackle challenging tasks and build support for their vision and goals. Hence, if CEOs with role duality feel threatened because their beliefs diverge from the national political climate, they can use their resource control to make faster decisions about environmental innovation. To sum up, we hypothesize the following:

Method

Sample and Data Collection

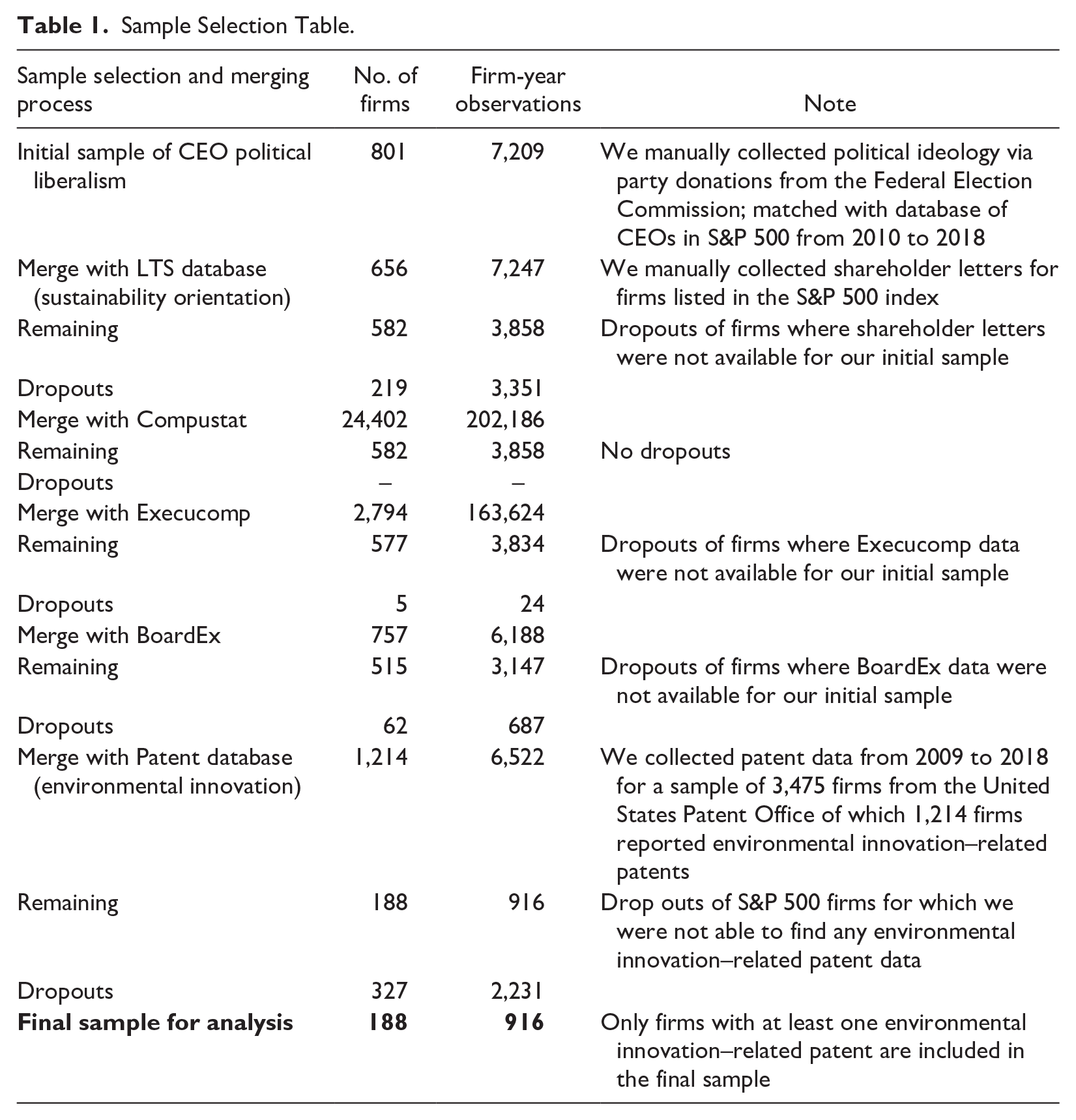

Our unique, hand-collected data set comprises members of the S&P 500 from 2010 to 2018 and builds the base for our longitudinal study. We chose to focus our study on the United States as the existing two-party system and the growing political polarization provide a solid foundation for our analysis. Furthermore, focusing on the United States allows us to use publicly available donation data to identify CEO ideology. We chose the S&P 500 index as it is one of the most reputable representations of the largest publicly listed firms in the United States, and S&P 500 companies account for approximately 80% of the total U.S. market capitalization (S&P Dow Jones Indices, 2023). Starting from the initial sample of CEOs with measurable political liberalism for 801 firms, we further extended our data set by merging it with our hand-collected data on letters to the shareholders from annual reports of 656 firms. After merging with S&P’s Compustat, S&P’s Capital IQ Execucomp and BoardEx databases and calculating all variables, we finally added our sample of patent data from 2010 to 2018 and only included data on firms that had registered at least one patent related to environmental innovation. The data on patent registrations were made publicly available from the U.S. patent office (United States Patent and Trademark Office [USPTO], 2023). Our final sample comprised 916 firm-year observations and 188 unique firms. As patent activities are different across industries, there could be some bias in our sample selection. For example, manufacturing firms are particularly active in patenting, while trade and financial services firms are less active. Our approach to measuring environmental innovation will, therefore, only include firms that innovate through patents (Morikawa, 2014). Process innovations at retailers or innovative insurance policies for insurance companies are not included. Table 1 shows our sample selection and merging process.

Sample Selection Table.

Measurement

Dependent Variable

We measured environmental innovation based on the count of green patents as “patent counts not only serve as a measure of innovative output but are indicative of the level of the innovative activity itself” (Popp, 2019, p. 269). We collected publicly available patent data from the U.S. patent office (USPTO). We analyzed patent classifications and used the official cooperative patent classification (CPC) “Y02.” The “Y02” scheme has been developed for patents filed for technologies to mitigate the effects of climate change (Angelucci et al., 2018). Haščič and Migotto (2015) further support the use of this scheme by arguing that the “Y02 scheme allows selected climate change mitigation technologies to be identified even by non-specialists” (p. 19). Although this approach to identifying environmental innovation may underestimate the total number of patents, it can still be considered as a good proxy for identifying trends in firms’ environmental innovation activities, as it can be expected that firms’ environmental innovations will behave similarly in all categories (Haščič & Migotto, 2015). We aggregated the numbers of patent applications in the “Y02” scheme to firms and firm years to derive environmental innovation (Fabrizi et al., 2018). We included patent data from 2010 to 2018 to avoid truncation bias (Dass et al., 2017). Firms that have submitted no patent applications under the “Y02” scheme in the respective years are not included in our sample. Thus, our sample includes data on firms that have filed patents from 2010 to 2018.

Independent Variable

We used two steps to build the measure of CEO political ideological divergence. We, first, measured CEO political liberalism and, second, deducted a binary score for the national political climate. We followed Chin et al. (2013) and used political donations to indicate CEO political liberalism. Political contributions are hand-collected from the U.S. Federal Election Commission (FEC). We calculated CEO political liberalism based on four indicators: “(1) the number of donations to Democrats divided by the number of donations to recipients of both parties (to handle zero values, we added .1 to all numerators and .2 to all denominators), (2) the dollar amount of donations to Democrats divided by the amount of donations to both parties, (3) the number of years the executive made donations to Democrats divided by the number of years the executive made donations to either party, and (4) the number of distinct Democratic recipients to which the executive made donations divided by the total number of distinct recipients of both parties.” (Chin et al. 2013, p. 208)

We then calculated the CEO political liberalism score as the simple average of the four indicators with a range from zero to one. Values above .50 indicate degrees of liberalism, whereas values below .50 indicate degrees of conservatism (Chin et al., 2013). While we are aware that this method of calculating CEO political liberalism includes various factors that are at different levels of measuring time and breath of donations, we follow an established literature stream that uses this approach to make sure to get a best-possible approximation of CEO liberalism (Briscoe et al., 2014; Chin et al., 2013; Gupta et al., 2018, 2021; Jeong et al., 2021; Nalick et al., 2023). Thereby, we include as many data points as possible in our calculation to avoid an under- or overestimation of political liberalism in years of no political donations of the CEOs.

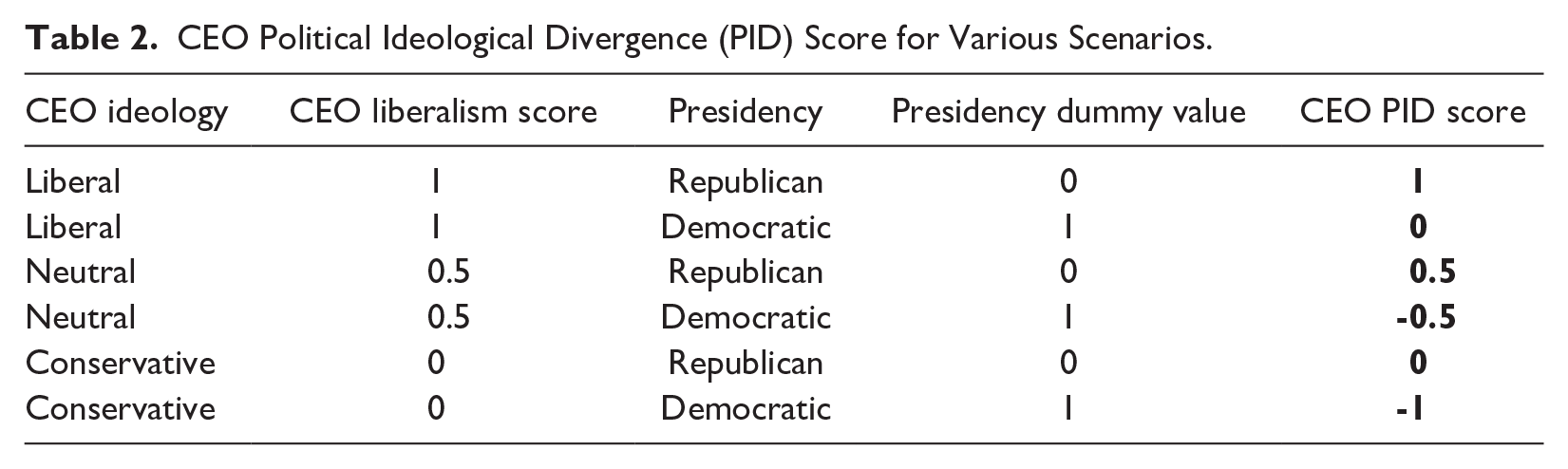

Subsequently, we assessed the national political climate and gathered data on either Democratic or Republican majorities in the U.S. government from 2010 until 2018. Due to the aforementioned importance of the role of the president, we subtracted “1” from the CEO political liberalism score if the president was a Democrat or “0” if the president was a Republican, yielding either a high or low divergence from the national political climate. We show the calculated CEO political ideological divergence (PID) scores for selected cases of government and CEO political ideology in Table 2. Finally, we lag CEO political ideological divergence by 1 year.

CEO Political Ideological Divergence (PID) Score for Various Scenarios.

Moderating Variables

Communicated Sustainability Orientation

We measured firms’ communicated sustainability orientation through the organization’s social and environmental value orientation (Moss et al., 2018), displayed by CEOs’ letters to shareholders (LTS) in annual reports (Vaupel et al., 2023). We followed Vaupel et al. (2023) in their argumentation that “shareholder letters are the most-read section of annual reports (Short et al., 2010) and represent a suitable source for sustainability orientation for three reasons. First, LTS typically represent the management team’s views on past and present developments and future priorities (Gamache et al., 2020; McKenny et al., 2018). Second, LTS are directed at the broad audience of annual report readers, so they reflect what a firm wants stakeholders to expect and associate it with (Short et al., 2010). Third, by their low degree of structural and linguistic standardization, LTS allow the management team to emphasize specific topics in their own style (McKenny et al., 2018).” (Vaupel et al. 2023, p. 407)

Similar arguments are given by McKenny et al. (2018). Social and environmental value orientation was measured based on a dictionary by Vaupel et al. (2023) and with the use of applied computer-aided text analysis (CATA). We applied the dictionary using the publicly available CAT-scanner tool (McKenny et al., 2013). As a basis for the CATA analysis, we hand-collected letters to shareholders from S&P 500 firms via annual reports. We counted the number of matched words per LTS per firm year and divided that sum by the total number of words to yield a result between 0 and 1 (Short et al., 2010). To enable an easier interpretation of the resulting scores, we normalized per thousand words for each letter (e.g., 0.006735 multiplied with 1,000 results in a score of 6.735).

CEO Duality

We measured CEO duality as a binary score based on the roles a CEO has according to S&P’s Capital IQ Execucomp database. A score of “1” means that a CEO simultaneously is chairman of the board of directors, and a score of “0” means he or she is not (Finkelstein, 1992; Graham et al., 2020).

Control Variables

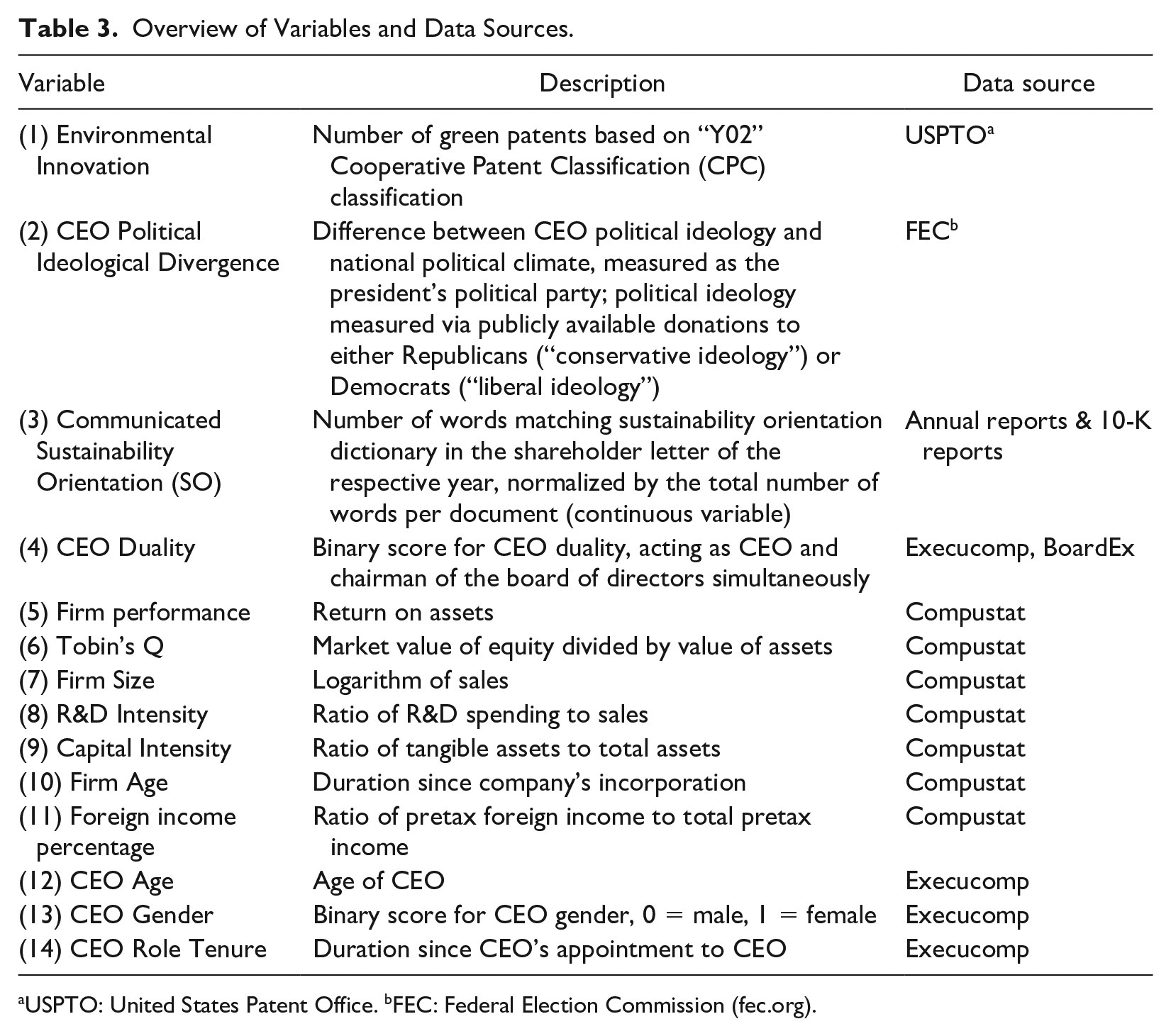

We based the selection of our control variables on research from the field of CEO political ideology (e.g., Chin & Semadeni, 2017; Christensen et al., 2015; Kashmiri & Mahajan, 2017; Semadeni et al., 2022). We also included industry- and year-specific dummy variables to enhance the robustness of our estimation model and to control for unobserved fixed effects accordingly (Wooldridge, 2014). We used S&P’s Compustat and S&P’s Capital IQ Execucomp databases for all our control variables. First, on a firm level, we controlled for firm performance, measured as return on assets, as innovation activity is influenced by present and past firm performance (Christensen et al., 2015). Next, we included Tobin’s Q, to control for firms’ valuation on the markets and their corresponding ability to invest in innovation (Mithas et al., 2013). We used firm size, measured as logged sales (Shalit & Sankar, 1977), as the size of the firm likely influences mechanisms of the firm’s management and governance as well as underlying motivations to innovate (Andries & Stephan, 2019). In addition, following a Schumpeterian perspective, the potential returns from innovation are higher for larger firms. This increases the likelihood that the firm will invest in innovation (F. M. Fisher & Temin, 1973). We included R&D intensity, measured as the ratio of R&D spending to sales (Dittmar & Thakor, 2007). Prior researchers have proven the relevance of R&D expenditures to a firm’s innovation activities. Their studies show that a higher investment in R&D indicates a greater willingness to invest in innovation (Banker et al., 2011). Moreover, we included capital intensity, measured as the ratio of tangible assets to total assets. Capital intensity has been shown to be a relevant moderator of innovation decisions based on a CEO’s market sentiment, given that entry barriers grow for more capital-intensive firms (Lartey et al., 2020). We included firm age, measured as the number of years after the firm’s founding, to control for possible bias toward younger firms investing more in environmental innovation (Balasubramanian & Lee, 2008). Finally, we have argued that environmental innovation is influenced by the perceived threat experienced by CEOs due to changes in the political landscape. This perceived threat may vary based on the specific circumstances of the CEOs and their firms. Given that it is not directly measurable, we introduced an additional control variable to account for a factor that could particularly impact the perceived threat intensity. Specifically, we included international exposure of the company, measured as the percentage of foreign pre-tax income relative to total pre-tax income. This measure allows us to control for the firm’s reliance on the national market and, consequently, the extent to which the CEO might feel threatened by domestic political changes (Christensen et al., 2015).

Second, on a CEO level, we employed CEO age as older CEOs might be more inclined not to invest in environmental innovation activities. We included CEO gender as gender affects corporate environmental strategy (Saeed et al., 2022). Finally, we included CEO role tenure as executives with longer tenure are more risk-averse (Finkelstein & Hambrick, 1990) and might therefore influence decisions regarding environmental innovation.

To improve the explanatory power of our model, we lagged all explanatory variables by 1 year and winsorized them at the 1% level. Table 3 provides an overview of our variables, including their definitions and sources.

Overview of Variables and Data Sources.

USPTO: United States Patent Office. bFEC: Federal Election Commission (fec.org).

Empirical Analysis and Results

Following leading researchers in the field (Chin et al., 2013; Gupta et al., 2017; Semadeni et al., 2022), we conducted our statistical analysis with GEEs that allow us to deal with multiple observations for our dependent variable. GEE is particularly useful when using cross-sectional time series data. It derives maximum likelihood estimates, and accommodates nonindependent observations (Chin & Semadeni, 2017). Due to our dependent variable of environmentally related patents taking count values, we chose a Poisson distribution for our GEE model with a logarithmic link function and independent correlation structure (Nelder, 1974). We clustered the analysis by firms and used year-fixed and industry-fixed effects for all regressions in our models.

Descriptive Results

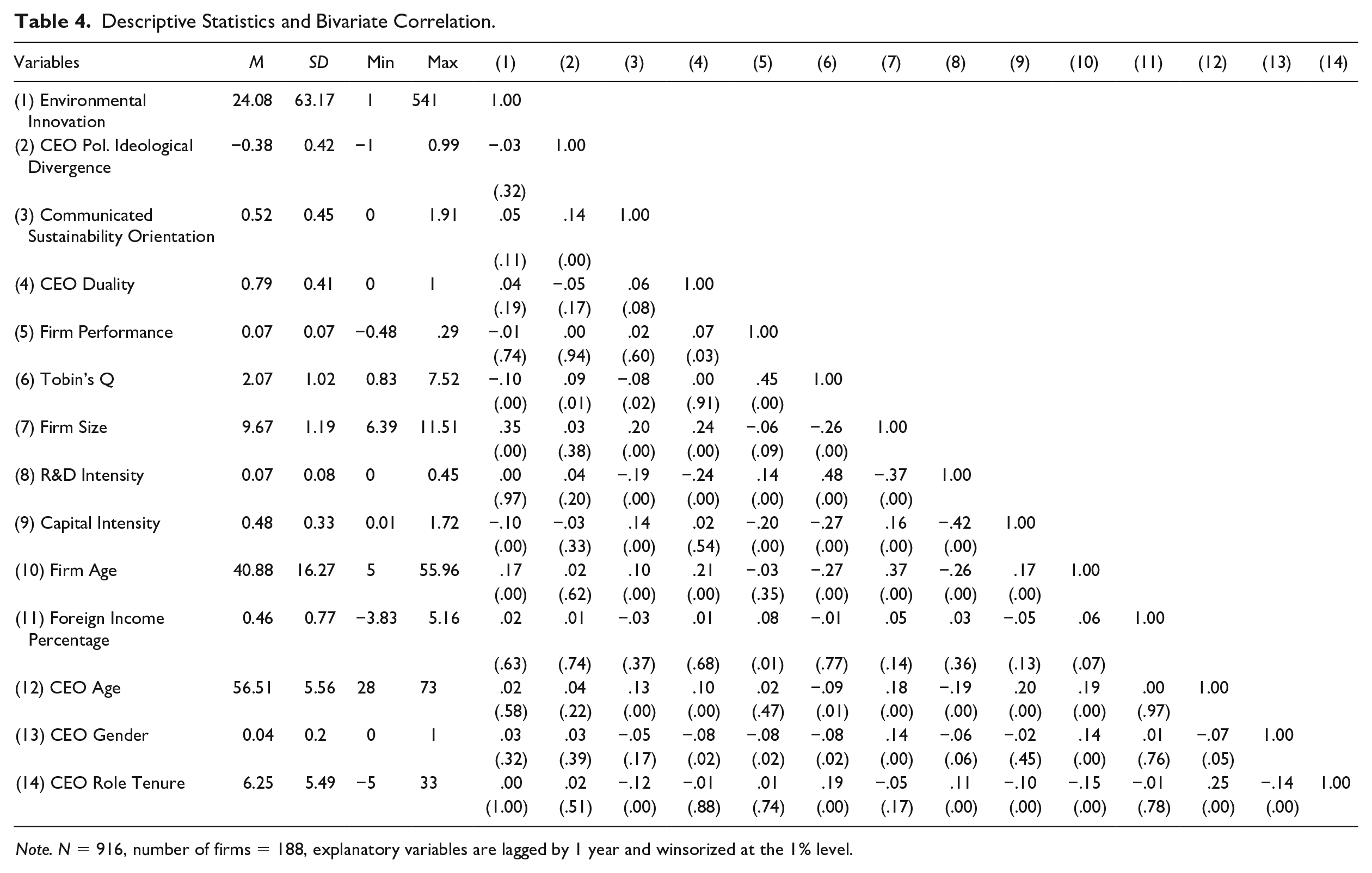

Table 4 presents the descriptive statistics and bivariate correlation coefficients. We examined potential multicollinearity problems between our explanatory variables in detail and found isolated Pearson correlation coefficients were higher than|0.3.| Therefore, we calculated the variance inflation factors (VIFs) associated with our predictor variables. Our mean VIF score is 2.18, below the cutoff of 5 (Cohen, 2013). Accordingly, we conclude that we do not have any multicollinearity problems.

Descriptive Statistics and Bivariate Correlation.

Note. N = 916, number of firms = 188, explanatory variables are lagged by 1 year and winsorized at the 1% level.

Regression Results

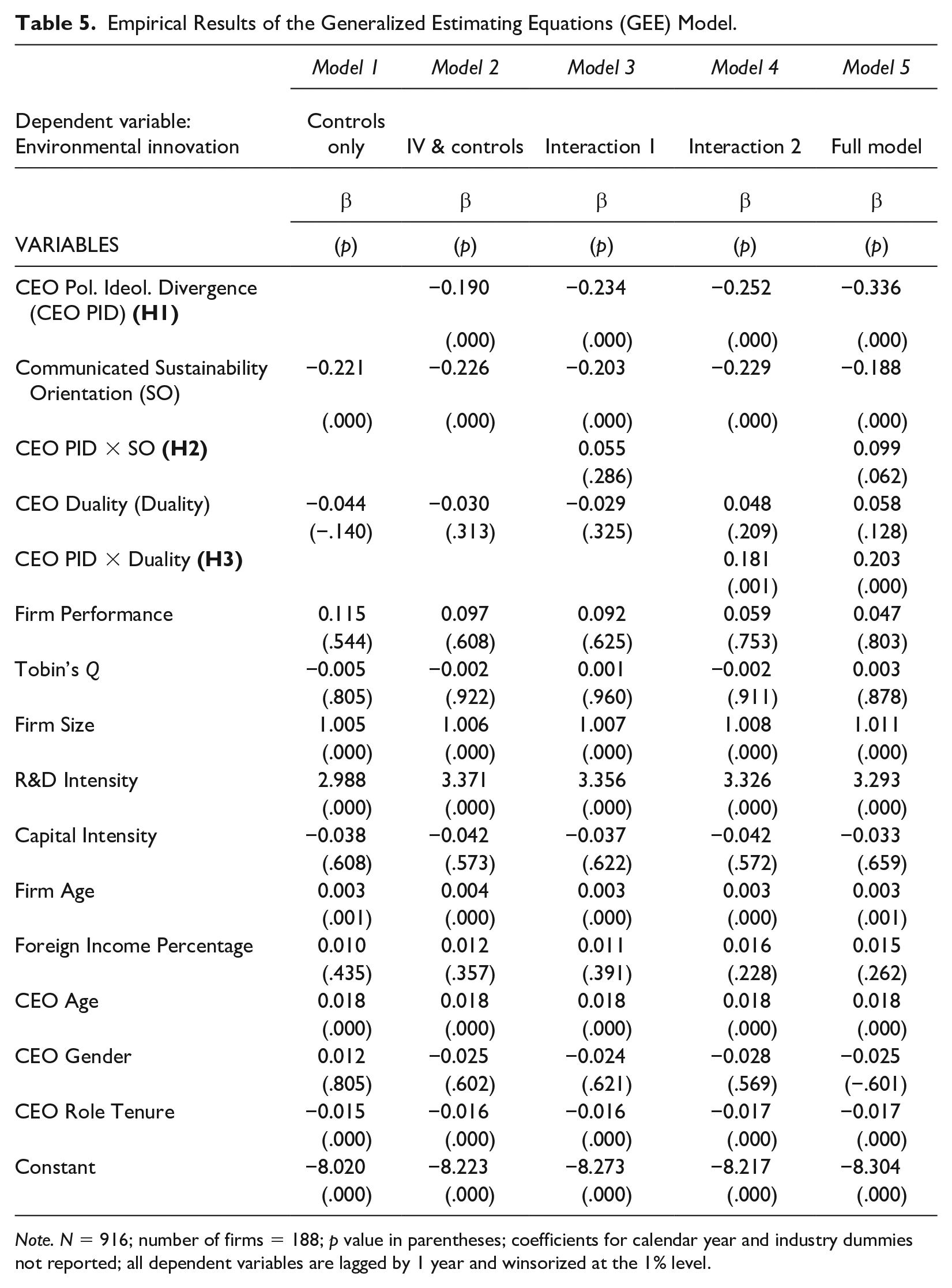

Table 5 presents the empirical results for our regression models. First, we ran our model only with control variables and fixed year- and industry effects (Model 1). Second, we included CEO political ideological divergence as our independent variable (Model 2). Subsequently, we introduced the interaction effects on firm communicated sustainability orientation (Model 3) and CEO duality (Model 4) to test our moderation hypotheses. Finally, we combined all variables and interaction effects in a full model (Model 5).

Empirical Results of the Generalized Estimating Equations (GEE) Model.

Note. N = 916; number of firms = 188; p value in parentheses; coefficients for calendar year and industry dummies not reported; all dependent variables are lagged by 1 year and winsorized at the 1% level.

We found evidence to confirm our Hypotheses 1 and 2. First, across all models, we find consistent evidence for our main hypotheses (Hypothesis 1a and 1b), stating that CEO political ideological divergence from a Democratic (Republican) president is positively (negatively) associated with environmental innovation. We find a negative and significant relationship, proving that CEO political ideological divergence leads to a reaction that conforms to the political party in power (β = −0.336, p = .000; Table 5, Model 5). Exponentiating the coefficient for easier interpretation reveals a value of 0.714 which corresponds to a negative change of 28.6% for a change of 1 in political ideological divergence. Specifically, we find that a strong divergence (PID =|1|) from a Democratic (Republican) president leads to an increase (decrease) of 28.6% environmentally relevant patents per year for firms that are filing patents in the field as compared with the case of no divergence.

Second, our model supports the idea that both of our chosen moderators have a significant effect on environmental innovation. The moderating effect of firms’ communicated sustainability orientation on the association of CEO political ideological divergence with environmental innovation has a positive beta coefficient and is marginally significant (β = 0.099, p = .062, Table 5, Model 5). This result does not hit the usually accepted boundary condition of 5% significance. Nonetheless, the significance of 6.2% indicates that a relationship is likely to exist and, consistent with other business research, we chose to report these results as marginally significant (e.g., D. Xu et al., 2014). Indeed, reporting marginally significant results has become more accepted over the last decade following a Fisherian interpretation of significance which sees the hard cutoffs for p-values as mostly arbitrary (R. A. Fisher, 1992; Pritschet et al., 2016). Furthermore, the moderation of CEO duality on CEO political ideological divergence and environmental innovation also has a positive beta coefficient and is significant (β = 0.203, p = .000, Table 5, Model 5).

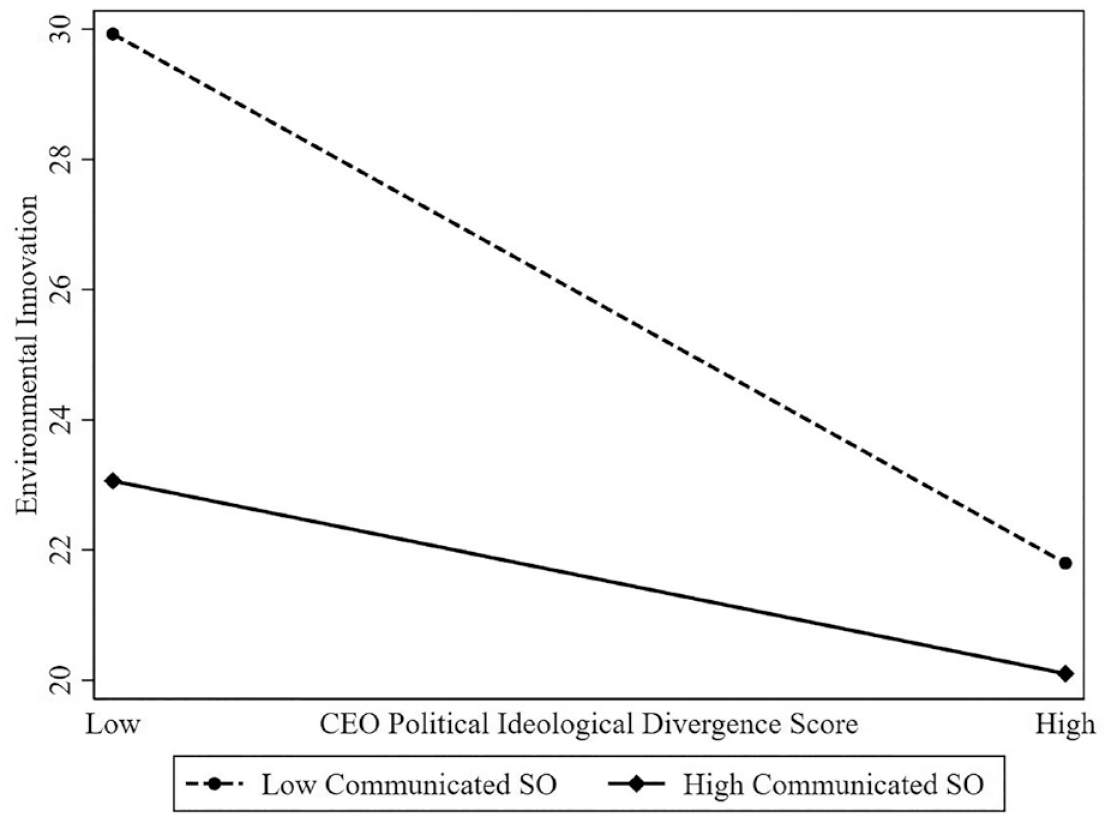

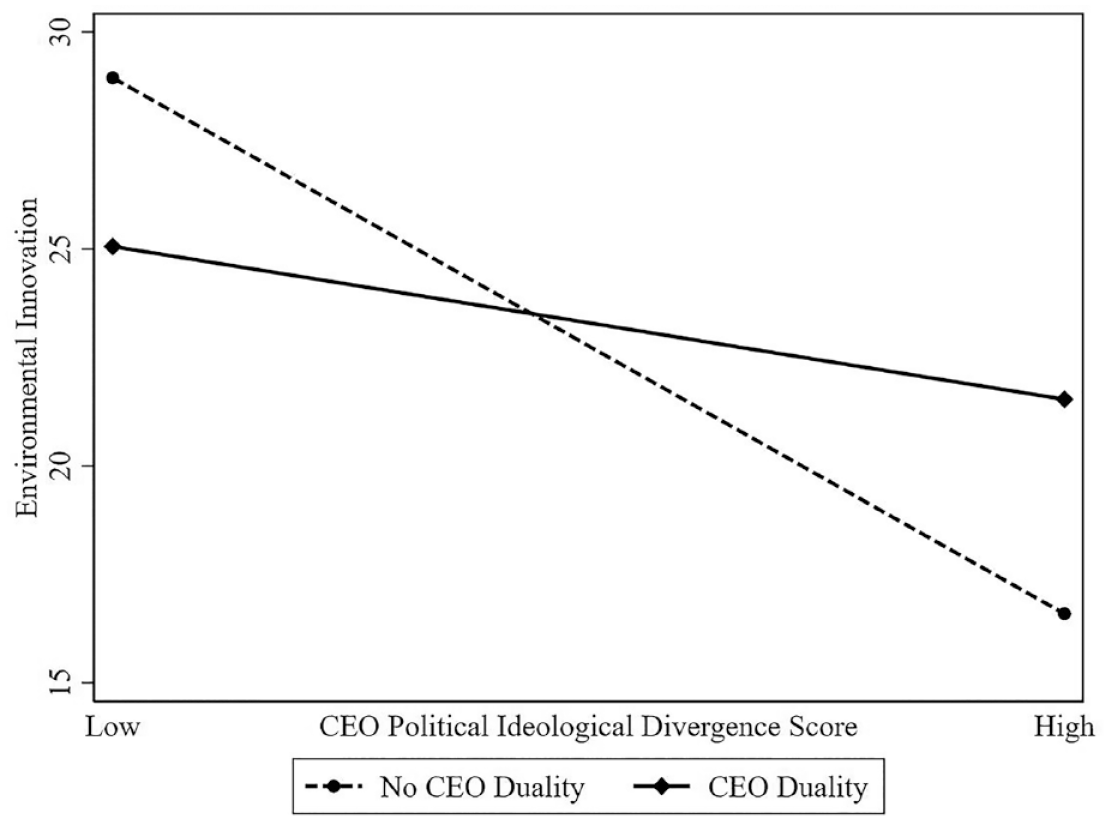

Third, following Busenbark et al. (2022), we analyzed the marginal effects of both moderators to derive their specific impact on environmental innovation and assess whether the predictions of our hypotheses hold. In Figures 2 and 3, we plot the relationship of CEO political ideological divergence on environmental innovation. A low CEO political ideological divergence score corresponds to a value of “–1” and can be interpreted as strong political ideological divergence from a Democratic president. On the contrary, a high score of “+1” corresponds to strong political ideological divergence from a Republican president. Figure 2 shows the Marginal Effect of Communicated Sustainability Orientation (SO) on the association between CEO Political Ideological Divergence and Environmental Innovation. Figure 3 shows the Marginal Effect of CEO Duality on the association between CEO Political Ideological Divergence and Environmental Innovation.

Marginal Effect of Communicated Sustainability Orientation (SO) on the Association Between CEO Political Ideological Divergence and Environmental Innovation.

Marginal Effect of CEO Duality on the Association Between CEO Political Ideological Divergence and Environmental Innovation.

In Figure 2, we plot the relationship at two levels of communicated sustainability orientation (high communicated sustainability orientation = mean + standard deviation = 0.97, low communicated sustainability orientation = mean – standard deviation = 0.06). The figure shows that communicated sustainability orientation weakens our hypothesized effect of political ideological divergence on environmental innovation. Indeed, the difference in environmental innovation between low CEO political ideological divergence scores (i.e., a conservative CEO under a Democratic president) and high CEO political ideological divergence score (i.e., a liberal CEO under a Republican president) is very low for highly communicated sustainability orientation at around two patents. For low communicated sustainability orientation, this difference is at around three patents. This confirms our Hypothesis 2 that argued that a highly communicated sustainability orientation weakens the effect of political ideological divergence on environmental innovation. Interestingly, firms with low communicated sustainability orientation tend to have a higher level of environmental innovation. This could be the case as all firms in our sample generally invest in environmental innovation and the firms that really have a substantial number of patents might see less importance in communicating about their achievements. Still, our Hypothesis 2 is confirmed and communicated sustainability orientation does indeed weaken the hypothesized effect of political ideological divergence on environmental innovation.

In Figure 3, we plot the relationship of CEO political ideological divergence with environmental innovation at two different levels of CEO duality (CEO duality = 1, no CEO duality = 0). Figure 3 shows that our Hypothesis 3 is not confirmed. Indeed, CEO duality seems to weaken the impact of CEO political ideological divergence. As such, firms with a CEO without role duality will react more strongly to CEO political ideological divergence. In the case of a low CEO political divergence score (a conservative CEO under a Democratic president), this means that a CEO without role duality will correspond to, on average, 29 patents. In contrast, in the presence of a high CEO political divergence score (a liberal CEO under a Republican president), a CEO without dual roles will correspond to significantly less environmental innovation as the number of registered patents decreases to around 16 parents, a difference of 13 patents. On the contrary, this difference is much less strong for CEOs with role duality as the number of patents only decreases from around 25 to around 23. This contradicts our hypothesis that firms with CEOs with role duality will react more strongly to CEO political ideological divergence. It might be the case that CEOs with such role duality do, indeed, feel more secure about their role and standing and are less impacted by external threats such as political ideological divergence from the president (Krause et al., 2014; Li & Tang, 2010).

Complementary Analysis

To validate our findings, we conducted several complementary robustness analyses. Overall, these robustness checks provide strong evidence for the validity of our findings and support the conclusion that CEO political ideological divergence from a Democratic (Republican) president positively (negatively) affects environmental innovation. First, we tested the robustness of our results using another independent variable. We calculated CEO political ideological divergence in an alternative way, as proposed by Semadeni et al. (2022). Instead of using the president’s political orientation, we calculated an average of the House of Representatives, the Senate, and the president’s political orientations. The results of the main effect align with our expectations (β = −0.336, p = .000). This allowed us to confirm that the negative relationship between CEO political ideological divergence and environmental innovation holds, even when using a different independent variable.

Second, we also tested the robustness of our results using another dependent variable. Instead of the green patent application count, we used the count of green patent citations. Previous research has shown that citation count is positively related to patent count and quality (Harhoff et al., 1999). We find that the main relationship remains unchanged (β = −1.490, p = .000) as do the moderation relationships. The results confirm our hypothesis and provide further evidence for the validity of our findings.

Third, as CEO donation patterns are mostly constant with a few fluctuations over the period considered, we also, instead of yearly data, control for 4-year averages of CEO political ideological divergence based on the time-limited political terms mandated in the United States. For our main relationship, we find a slightly stronger effect size at similar significance (β = −0.244, p = .000), while effect sizes for Hypotheses 2 and 3 are also of similar direction though less significant.

Finally, we excluded the finance industry from our regression, as finance firms operate in an entirely different regulatory environment than the other firms and are also unlikely to benefit in a similar way from environmental innovation as, for example, manufacturing firms. As in the models before, our main hypothesis also has a similar effect direction and size with high significance (β = −0.336, p = .000) and our Hypotheses 2 and 3 are similarly confirmed.

In addition to our robustness analysis, we also tested for endogeneity issues. Specifically, we followed (Hambrick, 2007a) and lagged all of our explanatory variables by one and two additional years. Lagging our variables means that we used data from the 2 and 3 years prior as our explanatory variables rather than using data from only 1 year prior. This allows us to account for any potential reverse causality or omitted variable bias, as our explanatory variables are not influenced by the values of our dependent variable. The effect sizes for our main hypothesis remain the same for the 2-year lag (β = −0.344, p = .000), as well as the 3-year lag model (β = −0.252, p = .000). We surprisingly found a significant strengthening—rather than the anticipated weakening—impact of communicated sustainability orientation (Hypothesis 2) on the relationship between CEO political ideological divergence and environmental innovation for 2- and 3-year lags (Hypothesis 2). This may occur because letters to the shareholders always need to be examined in light of the current situation of a firm. They usually are used to create a positive image of the company and to address potential concerns of stakeholders (Che et al., 2020). Therefore, the sustainability orientation communicated in previous years might lose significance in light of a new political environment and changing stakeholder demands. In light of a diverging political environment, the emphasis placed on sustainability orientation in earlier years could thus serve as an indicator of a CEO’s political leaning rather than as a guardrail for a company’s actions. CEOs who previously emphasized sustainability more strongly may react more intensely to potential threats of government action as the communication indicates their personal convictions, believing that investors are less likely to scrutinize shareholder communications from 2 or 3 years ago. The results for Hypothesis 3 are insignificant for the 2- and 3-year lags, which further shows that Hypothesis 3 could not be confirmed with our research.

Second, we included an instrument for CEO political ideological divergence to react to an assumed correlation of the error term with our dependent variable environmental innovation which occurs in case of omitted variables. Such correlation occurs when any variables that explain fluctuations in the dependent variable are excluded from the model. We ensured that our instrument fulfills the strength thresholds as defined by Stock and Yogo (2002) and the Hansen J test for overidentification. First, we applied a linear two-stage least square (2SLS) approach (Angrist & Pischke, 2009), using the “ivreg2” STATA command (Baum, 2006). Following Germann et al. (2015), we used as an instrument the industry average (on an SIC-2 code basis) of our independent variable CEO political ideological divergence. The first-stage regressions show that our instrument is marginally significant (β = 1.46, p = .144). We conclude that we are likely not facing endogeneity issues as the endogeneity test is insignificant (β = 2.174, p = .1404). Besides, we yield comparable, though less significant, results of our main regression effect when rerunning our analysis with our instrument and conclude that the model is not disproportionately affected by omitted variable bias.

Discussion and Conclusion

This study examines how CEO political ideological divergence helps or hinders the advancement of environmental innovation in an organization. We draw on threat response theory (Staw et al., 1981) to explain how CEO political ideological divergence is associated with environmental innovation. Relying on a sample of S&P-500 firms from 2010 to 2018, we find proof for our baseline hypotheses that the impact of political ideological divergence depends on the president in power. We further find that firms’ communicated sustainability orientation weakens the effect of CEO political ideological divergence. In other words, if the company communicated a sustainability orientation that aligns with the values of the CEO, the perceived threats of diverging from the communicated strategy outweigh the perceived threats of political ideological divergence, meaning that the firms stick with their communicated strategy. This reduces the impact of political ideological divergence of the CEO. Contrary to our initial hypothesis, our research also indicates that CEO duality weakens the influence of CEO ideological divergence on environmental innovation.

Theoretical Implications

The motivation for our research was to make a contribution by synthesizing two evolving literature streams, namely, environmental innovation and CEO political ideology. By doing so, we contribute to the literature in several ways. First, we extend environmental innovation literature by introducing CEO political ideological divergence as a novel and influential antecedent to environmental innovation. A variety of studies have examined the impact of government actions such as regulation policies on environmental innovation (e.g., Barnett et al., 2018; Chen et al., 2022; Du et al., 2021). Concerning CEO-level antecedents of environmental innovation, only CEO hubris (Arena et al., 2018) and CEO power (Zhang et al., 2022) have been examined. We bring in an antecedent that combines the emerging literature stream of political ideology, as a CEO personality characteristic, with external governmental influence. The combination of these two influences allows us to highlight an important nuance regarding the effect of (anticipated) government action. Namely, as we are arguing that a president with opposing political ideas might be perceived as a threat, we find that such ideological divergence might be negatively related to environmental innovation if a liberal CEO is politically diverging from a Republican president. That means, while government action might be indispensable to achieve viable actions against climate change, the impact is a double-edged sword. We argue that a liberal CEO might perceive a Republican president as a threat, leading to a reduction in those specific actions.

Second, our research adds to the growing body of CEO political ideology literature (e.g., Chin et al., 2013; Gupta et al., 2021; Hutton et al., 2015; Kashmiri & Mahajan, 2017; Semadeni et al., 2022) by examining a novel firm outcome—environmental innovation—and considering the impact of the national political climate on CEO political ideology, following Semadeni et al. (2022). This contribution is important, as previous research has focused on the relationship between CEO political ideology and traditional, broader firm outcomes such as financial policies (Hutton et al., 2014), tax avoidance (Christensen et al., 2015), even-handedness in capital allocation (Gupta et al., 2018), and broader corporate social responsibility activities (Chin et al., 2013; Di Giuli & Kostovetsky, 2014). Yet, by examining the relationship between CEO political ideological divergence and environmental innovation, we can provide a more nuanced understanding of the ways in which political ideology may influence CEO decision-making related to sustainability. As corporations are subject to regulation policies, CEOs, as the primary decision-makers of corporations, must operate within regulatory frameworks. The national political climate can serve as a key reference point for CEOs as they make decisions about how to position their company and respond to the expectations and preferences of stakeholders. When faced with opposing political views, CEOs can either affirm their beliefs through action or forsake them through inaction. We argue that when CEOs diverge from the national political climate, they perceive a threat, ultimately leading them to respond to this threat. Our study, along with previous research on CEO political ideological divergence (namely, Nalick et al., 2023; Semadeni et al. 2022), is important to raise the awareness of these influences and, more importantly, to guide other researchers to no longer examine CEO political ideology in isolation.

Third, these results are of interest with regard to the findings of Nalick et al. (2023) who show that CEO political ideological divergence correlates with lower lobbying expenditures. They argue that “a lack of value congruence and strategic complementarity with the governing party would taper the CEO’s desire to lobby (and vice versa for convergence), as they may interpret their power to influence the government has ebbed and the value of lobbying is therefore reduced.” (Nalick et al. 2023, p. 7)

Our article shows that CEOs might react in another way to the views of the president in power and, instead, choose to adjust their strategy in fields that are of particular focus in the bipartisan divide, such as environmental innovation (Fitz, 2023; Fowler, 2022; Kelso, 2017). Thus, we argue that instead of trying to influence the government, CEOs adjust their strategies to align more closely with the views of the president.

Fourth, our study contributes to the existing literature on threat response theory (Staw et al., 1981) by demonstrating that CEO political ideological divergence seems to affect environmental innovation intensity. Our findings, following threat response theory, indicate that a CEO’s political ideological divergence from the national political climate can be perceived as a threat. To react to the views of the political party in power, the CEO must react in a way opposite to their personal beliefs. This is particularly important to understand, as environmental innovation is positively related to firm performance (Andries & Stephan, 2019; Hizarci-Payne et al., 2021; Horbach, 2008). Our findings, therefore, support the idea that perceived threats can influence the decision-making of CEOs and lead them to make choices that go against their belief systems. Importantly, we are using threat response theory that emerged from the question of how adversity affects firm and individual behaviors and outcomes (Staw et al., 1981), to the much more timely issue of political polarization in the United States. As we have argued above, this issue is rising in importance, and giving firm stakeholders a potential guide to understand firm and CEO decisions in the context of diverging political climates, provides an important extension to the theoretical predictions of threat response theory.

Practitioner Implications

We also provide managerial implications. First, various stakeholders of an organization must be aware that changing political climates could affect a firm’s environmental innovation outcomes. That is, when a new president with an opposing political ideology is inaugurated, stakeholders must note whether CEOs change their strategic choices. A clear communication of a specific sustainability strategy seems to significantly weaken the impact of such CEO responses to perceived threats from opposing political views. Stakeholders could try to make sure that important strategic initiatives, such as sustainability strategies, are included in letters to shareholders, to mitigate the impact of an opposing political climate on CEO decisions.

We also provide contributions regarding executives’ self-awareness of threat response behavior. Understanding threat rigidity can be important for top managers because it can have an impact on their decision-making. When individuals become rigid in response to a perceived threat, they may decide to react opposing to their own personal believes and might no longer decide in a way that is potentially best for the company they run (Staw et al., 1981).

Limitations and Future Research

The limitations of our study provide directions for further research. First, our research focuses on some of the largest companies in the United States (S&P 500). Being the CEO of one of these firms brings significant power and national (political) attention. This attention could also explain why the CEOs seem to react so strongly to the impacts of diverging from the national political climate. Future research into the applicability of our results for smaller and medium-sized firms, with significantly less national political attention, might therefore be particularly interesting. In addition, CEOs might not be the sole decision-makers in such firms and it might very well be possible that boards are strategically hiring ideologically diverse top management team members to ensure more resilience against changes in administrations. Therefore, future research could look into the impact of political ideological divergence in top management teams or on the board level.

Second, when analyzing the outcomes of our study, it is important to acknowledge certain boundary conditions inherent to our research methodology. Specifically, our data set, comprising firms that have registered at least one environmental innovation–related patent within the research period, exhibits a pronounced emphasis on manufacturing firms compared with the broader composition of the S&P 500 index. Conversely, sectors such as wholesale and retail trade, finance, insurance, and real estate are underrepresented. This discrepancy stems from our methodological decision to measure environmental innovation through patent registrations—a metric that inherently applies more strongly to the manufacturing sectors than service-oriented industries like trade, finance, and insurance. Representation from other industries aligns more closely with their prevalence within the S&P 500 index. Future research may benefit from employing alternative measures of environmental innovation to include a wider array of firms, particularly those omitted from our current scope. In addition, our investigation centers exclusively on the intensity of environmental innovation within firms. That is, our analysis includes only those firms that have filed for at least one environmental innovation–related patent during the studied timeframe. With this focus, selection bias might be present as the data set very specifically only includes firms that invest in environmental innovation. This also means that we did not account for a potential two-step decision-making of firms. Such a two-step procedure would mean to first decide on whether to innovate and then to further evaluate whether the innovation is in the environmental field. Consequently, our findings only shed light on variations within firms actively engaged in environmental innovation, rather than contrasting these entities against firms that do not engage in such activities.

Third, we have consciously chosen moderating variables that are directly related to our main argument of threat response theory. Specifically, we are arguing that a communicated sustainability orientation restricts the CEO in their decision-making and, therefore, acts as a second and opposing threat. A CEO does not want to diverge from the communicated sustainability strategy and therefore has less leeway to move when the national political climate is diverging from her or his own views. Similarly, a CEO with dual roles will be able to make decisions more independently. As an ideological divergence is a perceived threat that is only experienced by the CEO but not necessarily anyone else in the top management team or the board, the reaction to such a perceived threat was hypothesized to be stronger with higher CEO power due to duality. However, there are multiple other influence factors on a CEO’s innovation decision-making that could also be included in further analyses. Researchers that are interested in this area could investigate other variables with potential impact on environmental innovation strategy.

Fourth, as our study focuses solely on the United States, our results might differ for other countries. This is because the United States has a two-party system that is easier to analyze compared with, for example, Japan, Germany, or France. Furthermore, the political polarization that has emerged in the United States over the past years might be different and not as intense in other countries. Hence, future researchers could investigate how political ideological divergences in different countries affect executive decision-making.

In addition, our study has the typical disadvantages associated with patents as we count applications for green patents to measure environmental innovation. Yet, the application of patents does not imply that the patents have been granted because multiple criteria must be met. Moreover, the fact that a patent has been granted does not mean that the organization has adopted the underlying technology. Some patents have little commercial value, indicating that most patented inventions are not broadly used (Lanjouw & Mody, 1996; Popp, 2019). Similarly, Haščič and Migotto (2015) explain that our approach to identifying environmental innovation might underestimate the total number of patents. While they argue that it nonetheless can be seen as a good proxy for identifying trends in environmental innovation activities of firms, future research could look into alternative ways to identify environmental innovativeness such as text-based measures (see, for example, Zimmermann et al., 2023).

Finally, reactive approach motivation theory (McGregor et al., 2010) comes out of psychology research and argues that a person’s reaction in case of uncertainty and anxiety would tend toward extremes (McGregor et al., 2009). Similarly, the executive job demand perspective argues that executives are more likely to resort to their cognitive traits and characteristics when facing uncertain or challenging job environments (Hambrick et al., 2005). Both these theories provide potentially worthwhile avenues for further research in events-based studies. It would be particularly interesting to more broadly understand the neuroscientific reactions that occur when a new president is elected, and how these would affect a variety of CEO decisions. Another intriguing avenue could be how job demands change in reaction to such an event, and how such changes could affect CEO strategy-setting and decision-making.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.